Admiral Group: The Data Insurgent

I. Introduction and The Cardiff Miracle

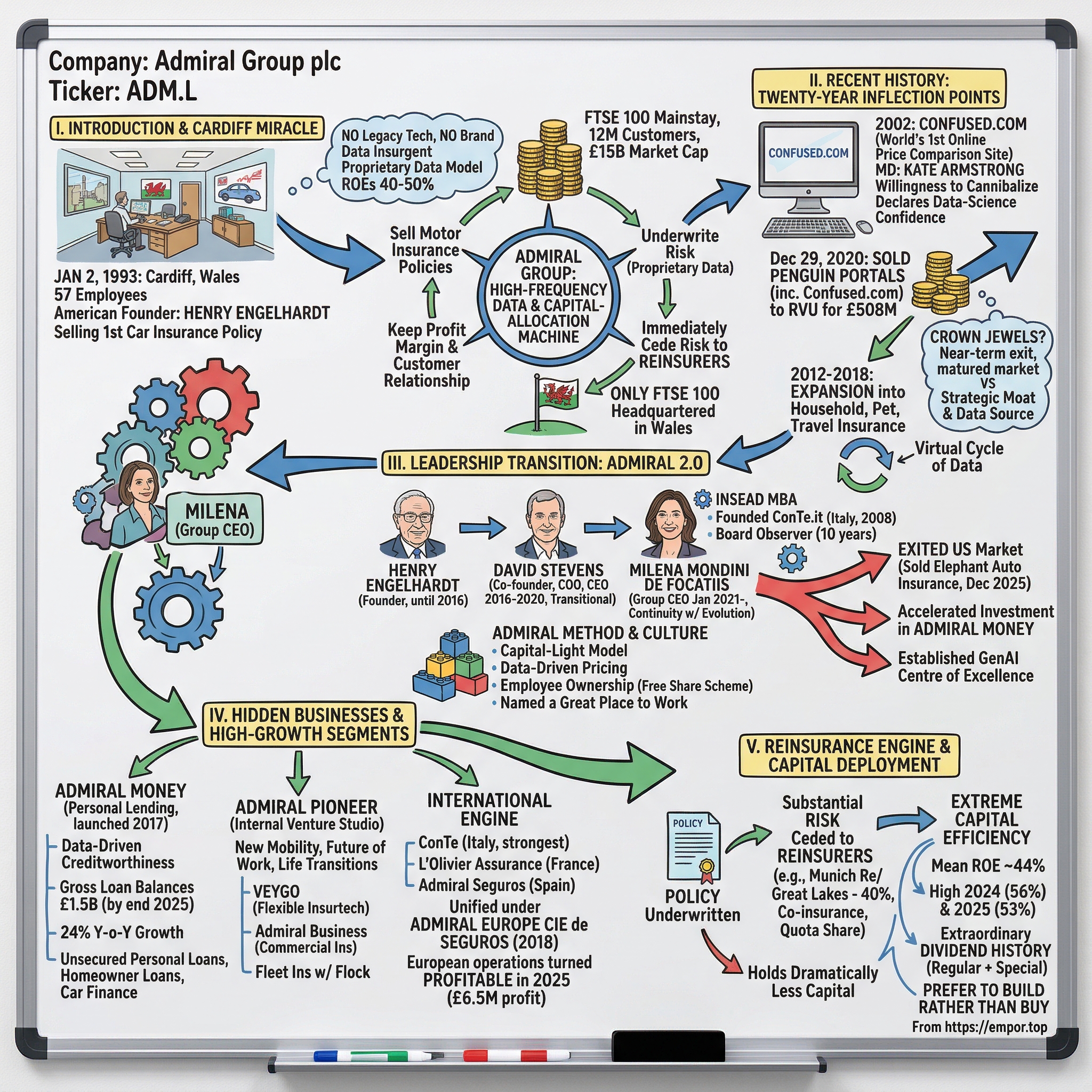

Picture this: January 2, 1993, a small office in Cardiff, Wales. Fifty-seven employees sit at their desks, nervous, caffeinated, and about to sell their very first car insurance policy at 9:10 in the morning. The company has no legacy technology, no brand recognition, and no London pedigree. Its founder is a fast-talking American from Chicago who studied journalism at Michigan, traded futures on the Chicago Mercantile Exchange, and somehow wound up in South Wales after his wife convinced him to get an MBA at INSEAD in France. His name is Henry Engelhardt, and the company he just launched will become one of the most consistently profitable financial services businesses in European history.

The thesis of Admiral Group is deceptively simple, and yet almost no one has replicated it in three decades. Admiral is not really an insurance company. It is a high-frequency data and capital-allocation machine that happens to sell motor insurance policies. While legacy insurers in London and Zurich spent the 1990s and 2000s managing sprawling balance sheets, Admiral built something radically different: a business model where the company underwrites risk using proprietary data, then immediately offloads a huge chunk of that risk to reinsurers, keeping only the profit margin and the customer relationship. The result is a company that consistently generates returns on equity north of forty percent, sometimes touching fifty or even higher, in an industry where most players struggle to clear ten.

To understand what makes this so remarkable, consider the context. Motor insurance in the United Kingdom is a brutally competitive, commoditized market. Every driver is legally required to carry it. There are dozens of providers competing on price. Customers are fickle, switching providers for savings of twenty or thirty pounds a year. And yet Admiral, from its Cardiff headquarters, has grown from that tiny office to a FTSE 100 mainstay with nearly twelve million customers globally, a market capitalisation that has at times exceeded fifteen billion pounds, and a culture so distinctive that it has been named a Great Place to Work for twenty-six consecutive years. The only FTSE 100 company headquartered in Wales, Admiral has become something of a national institution, a Cardiff miracle in an industry not known for producing miracles of any kind.

How did they do it? The answer involves a price comparison website that changed an entire industry, a reinsurance structure that turned conventional wisdom on its head, and a lending business that might just be the most underappreciated fintech in Europe. But it starts, as all the best stories do, with a misfit who saw what everyone else missed.

II. Recent History and The Twenty-Year Inflection Points

The year was 2002, and the internet was still in its awkward adolescence. Dial-up connections hummed in living rooms across Britain, and the idea of buying something as complex as car insurance online seemed, to most industry executives, somewhere between impractical and absurd. Customers still picked up the phone, called a broker, and accepted whatever quote they were given. Comparison shopping meant physically ringing multiple insurers, one by one, which almost nobody bothered to do. The friction in the system was enormous, and it protected the incumbents beautifully.

Henry Engelhardt and his team looked at this landscape and asked a question that would reshape the entire UK financial services industry: what if we built a website where customers could see every insurer's price, side by side, in seconds? The result was Confused.com, widely credited as the world's first online insurance price comparison website. Its founding Managing Director was Kate Armstrong, an IT consultant originally from Sydney, who built the platform from scratch. The name itself became a cultural phenomenon. A 2002 study found that "Confused.com" was the third most used phrase of the year in the UK, a remarkable feat for what was essentially a tech startup inside an insurance company.

The strategic brilliance of Confused.com was not the technology itself. It was the willingness to cannibalize. By building a platform that let consumers compare Admiral's prices against every competitor's, Admiral was effectively telling the world: we are confident we will win on price. This was a bet on their own data-science capabilities, a declaration that their actuarial models were better than everyone else's. And for years, that bet paid off spectacularly. Confused.com drove enormous traffic, Admiral captured a disproportionate share of customers who comparison-shopped, and the company grew at a pace that stunned the industry.

But comparison sites also changed the game in ways Admiral could not fully control. By the late 2000s, competitors had figured out the model. GoCompare launched with memorable advertising, and Compare the Market unleashed its "meerkat" campaign, one of the most successful marketing efforts in British advertising history. Confused.com's market share came under sustained pressure from 2009 onward. The aggregator business was becoming a marketing arms race, and the economics of running a price comparison platform were diverging from the economics of running an insurance company.

Meanwhile, Admiral was proving that its core methodology, the relentless application of data science to risk pricing, was portable far beyond motor insurance. Between 2012 and 2018, the company expanded into household, pet, and travel insurance, applying the same low-cost, high-data approach that had worked so well in motor. The "Admiral Method" turned out to be a transferable skill, not a product-specific trick. Each new vertical added another data stream, which in turn made the risk models more sophisticated, creating a virtuous cycle that compounded over time.

Then came the great divestment. On December 29, 2020, Admiral announced it was selling the entire Penguin Portals Group, which included Confused.com, the Spanish comparison site Rastreator.com, the French site LeLynx.fr, and Admiral Technologies, along with its fifty percent share of Preminen Price Comparison Holdings. The buyer was RVU, a subsidiary of ZPG, which was backed by Silver Lake, the technology-focused private equity giant. The price: five hundred and eight million pounds, with net proceeds to Admiral of approximately four hundred and sixty million after minority interests and transaction costs. The deal closed on April 30, 2021.

The question every analyst asked was whether Admiral had sold the crown jewels. The answer depends on the timeframe. In the near term, the sale looked brilliantly timed. The comparison website market was mature, intensely competitive, and capital-hungry. Admiral was exiting a business whose best growth days were behind it, at a valuation that reflected peak optimism about fintech businesses. The proceeds went straight to the balance sheet, funding the next phase of growth. But the bears argued that Confused.com had been more than a business: it was a customer acquisition engine, a data source, and a strategic moat. Selling it meant Admiral would now be competing for customers through the very comparison sites it no longer controlled, paying for traffic it once owned.

Benchmarking the valuation tells its own story. GoCompare was acquired for around four hundred and sixty million pounds in 2017, and Moneysupermarket Group traded at significantly higher multiples during the fintech boom. Admiral's five hundred and eight million pounds looked like a fair price, perhaps even generous, for a business that was no longer the market leader. The sale was not a fire sale. It was a calculated exit from a business that was consuming management attention and capital that could be better deployed elsewhere. Whether that redeployment succeeds is the central question of Admiral's next chapter.

III. The Leadership Transition: Admiral 2.0

Every great company faces the same existential test: what happens when the founder leaves? For Admiral, that test came in stages. Henry Engelhardt, the charismatic American who had built the company from nothing, stepped down as CEO in the spring of 2016. He handed the reins to David Stevens, who had been there from the very beginning as co-founder and Chief Operating Officer since 1999. Stevens was the insider's insider, the operational mind behind Engelhardt's entrepreneurial vision. His tenure as Group CEO from 2016 to 2020 was competent and steady, but it was always understood as a transitional period. The real question was who would lead Admiral into its next era.

The answer arrived in January 2021, when Milena Mondini de Focatiis became Group CEO, the first person to hold that title who was neither a founder nor a co-founder. Her path to the top was unusual and revealing. Born in Italy, she holds a telecommunications engineering degree from the Universita degli Studi di Napoli Federico II and, like Engelhardt, an MBA from INSEAD, a connection that says something about the kind of intellectual culture Admiral values. Before joining Admiral in 2007, she worked as a management consultant at Accenture, giving her a grounding in operational efficiency that would prove essential.

Her defining moment at Admiral came in 2008, when she founded ConTe.it, the company's Italian direct motor insurance brand. Building an insurance company from scratch in Italy, a market dominated by agents and face-to-face sales, was a formidable challenge. Italian consumers were deeply skeptical of buying insurance online, and the regulatory environment was complex. Mondini de Focatiis navigated all of it, growing ConTe into a profitable business and earning her seat at the leadership table. She had been attending Admiral board meetings as an observer since 2011, a decade-long apprenticeship that ensured there would be no surprises when she took over.

Her leadership style represents what she has called "continuity with evolution." She has not torn up the Admiral playbook. The capital-light model remains intact. The culture of employee ownership remains sacrosanct. The obsession with data-driven pricing continues unabated. But she has made subtle, important shifts. Under her watch, Admiral exited the US market by selling Elephant Auto Insurance to J.C. Flowers in a deal that completed on December 31, 2025, acknowledging that the American market was a capital drain that showed no realistic path to the returns Admiral expects from its businesses. She has accelerated investment in Admiral Money, the lending arm. And she has pushed the company to establish a GenAI Centre of Excellence, recognising that artificial intelligence will fundamentally change how insurance is priced, sold, and serviced.

The management incentive structure at Admiral deserves particular attention because it is genuinely unusual. The company operates a "Free Share" scheme that is available to every single employee, regardless of role or seniority. After twelve months of service, every Admiral employee qualifies for a free share allocation worth up to three thousand six hundred pounds per year. This is not a senior executive perk. It applies to call centre staff, claims handlers, and IT developers alike. The philosophy behind it is captured in Admiral's motto: "People who like what they do, do it better." If everyone is an owner, the argument goes, everyone thinks like an owner, which means lower turnover, better customer service, and a culture that self-reinforces.

Mondini de Focatiis's own share ownership aligns her incentives with long-term performance. The compensation structure at Admiral is deliberately tied not just to volume growth but to loss ratio performance, the single most important metric in insurance. A company that grows by writing underpriced policies will eventually face a reckoning when claims come in higher than expected. Admiral's incentive system is designed to prevent that trap by rewarding profitability, not just top-line expansion.

The Cardiff culture itself is a competitive advantage that is easy to underestimate. Admiral's headquarters at Ty Admiral on David Street is not a gleaming London tower. It is a building in a Welsh city where the cost of living is reasonable, talent is loyal, and the company is genuinely the biggest game in town. Admiral has over ten thousand employees globally, with additional offices in Swansea and Peterborough, but Cardiff remains the beating heart. The company's four culture pillars, Communication, Equality, Reward and Recognition, and Fun, sound like corporate platitudes until you realise that Admiral has been named to The Times' Best Companies list for over two decades running. This is not a company that talks about culture. It is a company that has built its business model around it.

The question for investors is whether this culture can scale globally as Admiral pushes further into continental Europe and new product lines. Mondini de Focatiis, as someone who successfully exported the Admiral culture to Italy, may be uniquely qualified to answer it.

IV. Hidden Businesses and High-Growth Segments

In the summer of 2017, Admiral quietly launched something that had nothing to do with car insurance. Admiral Money, an unsecured personal loans business, opened for applications with minimal fanfare. Most analysts barely noticed. Admiral was an insurance company, after all, and personal lending was a different world with different risks, different regulations, and different competitive dynamics. But inside Admiral's Cardiff headquarters, the logic was crystal clear: the company was sitting on decades of data about millions of UK consumers, data about their driving behaviour, their claims history, their payment patterns, their demographics. That data, properly modelled, could predict creditworthiness with remarkable accuracy, potentially better than the traditional credit scoring models used by incumbent lenders.

The results have been quietly extraordinary. By the end of 2025, Admiral Money had gross loan balances of one and a half billion pounds, growing at twenty-four percent year-on-year. Profit nearly doubled to twenty-six million pounds. The division has expanded from unsecured personal loans into homeowner loans and car finance, with a point-of-sale motor finance product in development. Perhaps most tellingly, Admiral Money's data-driven approach has allowed it to approve eighteen percent more loan applicants than traditional models would suggest, while simultaneously maintaining strong repayment rates and catching more fraud. The underwriting time has been halved from thirty minutes to fifteen minutes per application.

This is the business that could re-rate Admiral from a traditional insurer to something closer to a fintech. Personal lending in the UK is a massive market, and Admiral's data advantage is genuine and difficult to replicate. A new entrant would need decades of proprietary customer data to build comparable models. The lending business is still small relative to insurance, contributing just twenty-six million in profit against the group's nine hundred and fifty-eight million total. But at a thirty-plus percent compound annual growth rate in balances, Admiral Money is on a trajectory that demands attention.

Then there is Admiral Pioneer, the company's internal venture studio. Based at Capital Tower in Cardiff, Pioneer operates as something between a startup incubator and a corporate R&D lab. Its mandate is to identify unmet customer needs and build new businesses to serve them, with a focus on three domains: new mobility, the future of work, and life transitions. The most mature Pioneer venture is Veygo, launched in 2016, which offers flexible pay-as-you-go and monthly subscription insurance products aimed at learner drivers, new drivers, and experienced drivers who do not want traditional annual policies. Admiral Business provides flexible commercial insurance, and a partnership with Flock delivers fleet insurance using real-time risk management technology.

Pioneer matters because it represents Admiral's attempt to stay ahead of structural shifts in how people use transportation. Pay-per-mile insurance, car-sharing coverage, and gig-economy products are not mainstream yet, but the trends are unmistakable. Having an internal studio experimenting with these models gives Admiral optionality that does not appear on the balance sheet.

The international engine is the third hidden asset, though "hidden" may be generous given the losses it has generated over the years. Admiral operates across continental Europe through ConTe in Italy, L'Olivier Assurance in France, and Admiral Seguros in Spain, which runs multiple brands including Qualitas Auto and Balumba. These businesses serve around 1.9 million customers and are unified under Admiral Europe Compania de Seguros, the single insurance entity created in 2018 to consolidate the European operations.

For years, the international businesses were a source of frustration, burning cash while management insisted that profitability was just around the corner. In 2024, the European insurance operations posted a loss of nearly twenty million pounds. But 2025 marked a genuine turning point: the European businesses swung to a profit of six and a half million pounds, the first time the combined continental operation has been in the black in recent memory. Italy, where Mondini de Focatiis built ConTe from scratch, has been the strongest performer, while Spain and France are earlier in their maturation curves.

The elephant in the room, quite literally, was the US business. Elephant Auto Insurance launched in 2009 in Richmond, Virginia, and gradually expanded to eight states including Maryland, Texas, Illinois, and Georgia. The US market was supposed to be the ultimate prize: a massive, fragmented motor insurance market where Admiral's data science could theoretically create the same advantages it enjoyed in the UK. In reality, the US proved to be the "Final Boss" that Admiral could not defeat. American driving patterns, litigation environments, and regulatory structures are fundamentally different from the UK. Each state is essentially its own market with its own rules. Elephant posted persistent losses, including a staggering forty-nine million pound loss in 2022 alone. By the time Admiral sold Elephant to J.C. Flowers with the deal completing at the end of 2025, the decision felt less like a strategic retreat and more like a mercy killing.

The sale of Elephant was arguably the most important strategic decision of the Mondini de Focatiis era. It freed up management bandwidth and capital that can now be deployed into businesses with proven economics: Admiral Money, the recovering European operations, and the core UK franchise. Sometimes the best capital allocation decision is knowing when to stop.

V. M&A, Capital Deployment, and The Reinsurance Engine

To understand why Admiral's financial returns are so unusual, you need to understand an arrangement that most investors completely overlook. It starts with a simple question: what happens to the risk after Admiral sells you a car insurance policy? In a traditional insurance company, the answer is straightforward. The insurer collects your premium, puts it on the balance sheet, sets aside reserves to pay future claims, and holds regulatory capital against the possibility that claims come in worse than expected. This is capital-intensive, which is why most insurers generate single-digit returns on equity and trade at or below book value.

Admiral does something fundamentally different. When it underwrites a policy, it immediately cedes a substantial portion of the risk to reinsurance partners through proportional risk-sharing agreements. The most important partner is Munich Re, specifically its subsidiary Great Lakes, which currently underwrites forty percent of Admiral's UK car insurance business. Twenty percent goes on a co-insurance basis, with that arrangement extended through 2029, and another twenty percent on a quota share reinsurance basis extended through 2026. Additional reinsurance capacity comes from Gen Re and Axis, who have increased their participation over time.

Think of it like a restaurant that does not own the building, does not employ the chef, and does not buy the ingredients, but keeps a large share of the profit on every plate served because it knows exactly which dishes to put on the menu and how to price them. Admiral's genius is in the selection and pricing of risk. The actual bearing of that risk is substantially outsourced. The arrangements operate on a "funds-withheld basis," meaning Admiral retains the ceded premium, nets out the reinsurer's margin, and uses the retained funds to pay claims and expenses. The profit commission terms ensure that Admiral keeps a significant portion of the profit generated on the ceded book.

The result is a company that needs to hold dramatically less capital than its peers. And because return on equity is profit divided by equity, less equity with the same profit means a much higher ROE. Admiral's mean return on equity over the past decade is approximately forty-four percent. In 2024, it hit fifty-six percent. In 2025, it was fifty-three percent. These are not just good numbers for an insurer. These are extraordinary numbers for any financial services company, anywhere. GEICO, the gold standard of US auto insurance owned by Berkshire Hathaway, does not consistently generate returns this high. Progressive, the other great US auto insurer, runs in the high teens to mid-twenties in good years. Admiral is in a different league.

This capital efficiency also explains Admiral's extraordinary dividend history. Because the company does not need to retain earnings to support an ever-growing balance sheet, it can return enormous amounts of capital to shareholders. Admiral has a long tradition of paying special dividends on top of regular dividends. In 2025, total dividends per share reached two hundred and five pence, including a substantial special dividend. In 2024, shareholders received one hundred and twenty-one pence, including a special dividend of nearly thirty pence. The solvency ratio, a measure of how much capital the company holds above regulatory minimums, stood at one hundred and ninety-three percent at the end of 2025, well above the comfort zone, meaning there is room for further capital returns.

Admiral's acquisition discipline is the natural corollary of this model. If your business generates fifty-percent-plus returns on equity organically, the bar for acquisitions is astronomically high. Almost no target can offer returns that justify diluting the existing franchise. This is why Admiral has historically preferred to build rather than buy. The sale of Penguin Portals to RVU was the major exception that proved the rule, and even that was a divestiture, not an acquisition. Admiral's M&A history is notable mainly for its absence. When the company has expanded internationally, it has done so by building greenfield operations, ConTe in Italy, L'Olivier in France, Balumba in Spain, rather than acquiring existing businesses. The organic approach is slower but preserves the culture and the operating model.

The risk in the reinsurance model is concentration and dependency. If Munich Re were to withdraw or significantly reprice its capacity, Admiral's economics would change overnight. The extension of the co-insurance arrangement to 2029 provides medium-term visibility, but it is a relationship that must be continuously maintained. The fact that Gen Re and Axis have increased their participation suggests that reinsurers find the Admiral book attractive, which is itself a validation of the company's underwriting quality. Reinsurers are sophisticated evaluators of risk. They do not increase exposure to books that are poorly priced.

VI. Strategy Framework: Seven Powers and Five Forces

Admiral's competitive position becomes clearest when examined through the lenses that sophisticated investors use to evaluate durable business advantages. Start with Hamilton Helmer's Seven Powers framework, which identifies the sources of persistent differential returns.

The most powerful of Admiral's advantages is its cornered resource: a thirty-year proprietary dataset of UK driving behaviour and claims outcomes. Every policy Admiral has ever written, every claim it has ever processed, every customer interaction it has ever recorded feeds into pricing models of extraordinary granularity. This is not a dataset you can buy. It was built one policy at a time, over three decades, and it compounds in value with each passing year. A new entrant starting today, even one with brilliant data scientists and unlimited capital, would need decades to build anything comparable. The dataset is not just large; it is longitudinal, capturing how risk profiles evolve over time, across economic cycles, through regulatory changes, and in response to shifting driving patterns. This is the single most important reason why Admiral can consistently price risk more accurately than competitors.

The second power is counter-positioning. When Admiral created Confused.com, it was doing something that the incumbent insurers could not rationally copy. The big brokers and direct insurers of the 1990s had spent decades building distribution networks, agent relationships, and brand loyalty. A price comparison website that stripped away all of that and reduced insurance to a pure price competition was an existential threat to their business model. They could not embrace it without destroying their own economics. Admiral, starting with a blank sheet, had no legacy distribution to protect. It could build the comparison site because it had nothing to lose and everything to gain. Even after selling Confused.com, the counter-positioning advantage persists: Admiral's entire operating model is built for a world of radical price transparency, while many competitors are still struggling to adapt.

Scale economies provide the third pillar. Admiral's UK customer base of over nine million generates massive purchasing power in claims handling, driving down the cost per claim through volume discounts with repair shops, parts suppliers, and medical providers. Marketing spend can be amortised across a larger base. Technology investments in pricing algorithms, fraud detection, and customer service platforms have near-zero marginal cost per additional policy. These scale effects create a cost advantage that compounds over time and makes it progressively harder for smaller competitors to match Admiral's prices while remaining profitable.

Turning to Porter's Five Forces reveals the competitive pressures Admiral navigates. The threat of new entrants is superficially high because the barriers to starting a managing general agent in UK motor insurance are relatively low. You need a license, some capital, and a reinsurance partner. But the threat of a new entrant achieving scale is an entirely different matter. Without the proprietary data that Admiral has accumulated over three decades, a new player is essentially flying blind on risk pricing. They can write policies, but they cannot price them with the same precision, which means they will either overpay claims or underprice risk, neither of which is sustainable. The data moat functions as an invisible barrier that is far more effective than regulatory hurdles.

The bargaining power of buyers is the force that most constrains Admiral. Price comparison websites have made UK motor insurance one of the most transparent, price-sensitive markets in the world. Customers can switch providers in minutes for savings of a few pounds. This relentless price pressure forces Admiral to be the lowest-cost operator in the market, which it has achieved through the capital-light model and operational efficiency. But it also means that pricing power is essentially zero. Admiral cannot charge a premium for its brand in motor insurance. Its only defence is to be more accurate in pricing risk, so that it can offer the lowest price to good risks while avoiding the bad risks that competitors misprice.

Supplier power, in Admiral's case, manifests primarily through the reinsurance relationships. Munich Re, Gen Re, and Axis are sophisticated counterparties with significant leverage. If they decide to reduce capacity or increase pricing, Admiral's economics change materially. The mitigation is that Admiral's underwriting track record makes it an attractive partner, creating mutual dependency. Reinsurers want access to well-priced books of business just as much as Admiral wants their capital.

The threat of substitutes is evolving. Traditional motor insurance could be disrupted by pay-per-mile models, embedded insurance from car manufacturers, or autonomous vehicles that shift liability from drivers to manufacturers. Admiral Pioneer's work on new mobility products is a direct response to this threat, an attempt to be the disruptor rather than the disrupted.

Rivalry among existing competitors is intense. In the UK, Admiral faces Progressive-like competitors including Direct Line, Aviva, and dozens of smaller players. The market is mature, growth comes primarily from market share gains, and the pricing cycle swings between hard markets where rates rise and profitability improves and soft markets where competition drives margins to razor-thin levels. Admiral's response to this rivalry has been to focus on underwriting discipline, cutting prices when the data supports it to gain share and raising prices aggressively when claims inflation threatens profitability. In 2022, when claims costs surged due to parts and labour inflation, Admiral raised rates by over twenty percent, sacrificing volume for profitability. In 2024, when the data showed that claims trends were improving, Admiral cut prices earlier than the market, winning 1.4 million additional customers while competitors were still running scared. This counter-cyclical pricing discipline, enabled by superior data, is the practical expression of Admiral's competitive advantages.

VII. The Playbook: Lessons for Founders and Investors

There is a particular kind of business genius in choosing to compete in a market that nobody else wants. Motor insurance is not glamorous. It does not attract the best students at elite business schools, who dream of technology startups and private equity. It does not generate breathless coverage in the financial press. It is, by almost every measure, a boring, commoditized, hyper-competitive market where margins are thin, customers are disloyal, and regulatory burdens are heavy. And that is precisely why Admiral has been able to compound at extraordinary rates for three decades.

The lesson for founders is about marginal gains in data. When you compete in a commodity market, the winner is not the company with the best brand or the flashiest product. It is the company that is one percent better at the thing that matters most. In insurance, the thing that matters most is pricing risk accurately. If you can price a twenty-three-year-old male driver in Birmingham who commutes sixteen miles to work and parks on the street at night with fractionally more precision than your competitor, you win that customer at a profitable price while your competitor either loses the bid or wins it at a loss. Multiply that one percent advantage across millions of policies and you get Admiral's economics. It sounds unsexy because it is. But the compounding of small data advantages over long periods creates advantages that are nearly impossible to replicate.

The employee equity model contains a second lesson that extends far beyond insurance. Admiral's Free Share scheme, which gives every employee up to three thousand six hundred pounds in shares annually after twelve months of service, creates alignment that no amount of management oversight can achieve. When the call centre agent handling your claim is also a shareholder, they care about the outcome. When the data scientist building the pricing model knows that their work directly affects their own net worth, they pay attention to the details. Admiral has consistently lower staff turnover than its competitors, and its customer satisfaction scores reflect the difference. The lesson is not that every company should give away shares. It is that alignment of incentives, genuinely felt at every level of the organisation, is a competitive weapon that is cheap to implement and nearly impossible for competitors to copy.

The capital efficiency lesson is perhaps the most transferable. Admiral's entire model is built on the principle of not using your own balance sheet when someone else's will do. The reinsurance structure means that Munich Re, Gen Re, and Axis are effectively lending their balance sheets to Admiral, which keeps the profit margin and the customer relationship. This is not unlike an asset-light platform business in technology, where the platform owner captures the economics without owning the underlying assets. For founders in capital-intensive industries, the question Admiral poses is: which parts of your value chain absolutely require your own capital, and which can be sourced from partners who are willing to bear the risk in exchange for a predictable return?

The bear case for Admiral deserves honest examination. Inflationary pressure on claims costs remains the most immediate threat. The cost of car parts, repair labour, and medical treatment has risen sharply in recent years, and there is no guarantee that these pressures will fully abate. If claims inflation proves structural rather than cyclical, Admiral's combined ratios will remain elevated, and its pricing advantage may narrow as all insurers are forced to raise rates. The "Amazon-ification" of insurance, the possibility that a large technology platform could enter the market and use its consumer data and distribution power to disintermediate traditional insurers, is a longer-term but potentially existential risk. Amazon, Apple, or Google all have deeper consumer data than Admiral and could, in theory, price risk just as accurately if they chose to enter the market.

The regulatory environment is also worth watching. The UK's Financial Conduct Authority has been increasingly active in insurance regulation, with recent interventions around pricing practices and consumer protection. Any further regulatory tightening could disproportionately affect companies like Admiral that rely on granular data-driven pricing, if regulators decide that certain pricing variables are discriminatory or unfair. The FCA's general insurance pricing reforms, which banned the practice of charging existing customers more than new customers, already reshaped the competitive landscape and forced Admiral to adjust its retention strategies.

On the other side of the ledger, the bull case is compelling. Admiral Money is the most obvious catalyst. If the lending business continues to grow at its current rate, it could become a material profit contributor within three to five years, diversifying Admiral's earnings away from the cyclicality of motor insurance. The market is unlikely to value an insurer growing its lending book at twenty-four percent a year in the same way it values a pure play on motor underwriting. A re-rating toward fintech multiples, even partially, would have significant implications for the share price.

The international businesses represent a second source of upside. With Elephant sold and the European operations finally reaching profitability, Admiral's international portfolio is cleaner and more focused than it has been in years. Italy and Spain are large motor insurance markets with lower levels of online penetration than the UK, meaning there is more structural growth available for a direct, data-driven insurer willing to invest over a long time horizon.

For investors tracking Admiral's ongoing performance, three key performance indicators matter above all others. First is the combined ratio, the percentage of premium income consumed by claims and operating expenses. A combined ratio below one hundred means the company is making an underwriting profit. Admiral's 2024 combined ratio of seventy-seven percent and 2025 figure of eighty percent are exceptional by industry standards, but they also benefited from reserve releases and favourable claims trends. Watching whether the combined ratio can stay in the low eighties or better will tell investors whether Admiral's data advantage is holding. Second is the loss ratio specifically, which strips out operating costs and measures only claims against premiums. This is the purest measure of Admiral's pricing accuracy and the metric most directly tied to the management incentive structure. Third is Admiral Money's loan book growth and impairment rate, which together will reveal whether the lending business can scale without sacrificing credit quality. These three numbers, tracked consistently over time, tell the story of whether Admiral's engine is still running as designed.

VIII. Outro

Admiral Group is, in many ways, the Progressive of Europe. Like Progressive in the United States, Admiral built its franchise on superior data science applied to a commodity product, paired with a willingness to experiment with distribution that competitors found threatening. Like Progressive, it has compounded at rates that seem implausible for an insurance company. And like Progressive, it has created a culture that attracts and retains talent in an industry not known for doing either.

But Admiral is also something uniquely its own. The Cardiff origins, the American founder with the journalism degree, the employee share scheme that turns call centre workers into shareholders, the reinsurance model that turns a capital-heavy business into a capital-light one, the price comparison website that changed an entire industry before being sold at what now looks like a smart price, all of these elements combine into a business that has no precise analogue anywhere in the world.

The Milena Mondini de Focatiis era is still young, but the early decisions have been sound. Exiting the US was painful but necessary. Investing in Admiral Money shows strategic vision. Turning the European operations profitable demonstrates operational competence. And maintaining the culture through a leadership transition is perhaps the hardest thing any company can do.

Henry Engelhardt wrote a book called "Be a Better Boss," and its central argument is that great businesses are built by treating people well, a philosophy that sounds naive until you see it compound over three decades. Admiral's annual reports, particularly the sections on culture and employee engagement, are worth reading not just for what they reveal about the company but for what they suggest about how exceptional businesses are built.

The Cardiff miracle continues. Whether it becomes something even larger, a diversified European financial services platform with lending, insurance, and new mobility products, depends on whether the data advantage holds, whether the culture scales, and whether the next generation of leaders can be as shrewdly unconventional as the American in Cardiff who started it all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube