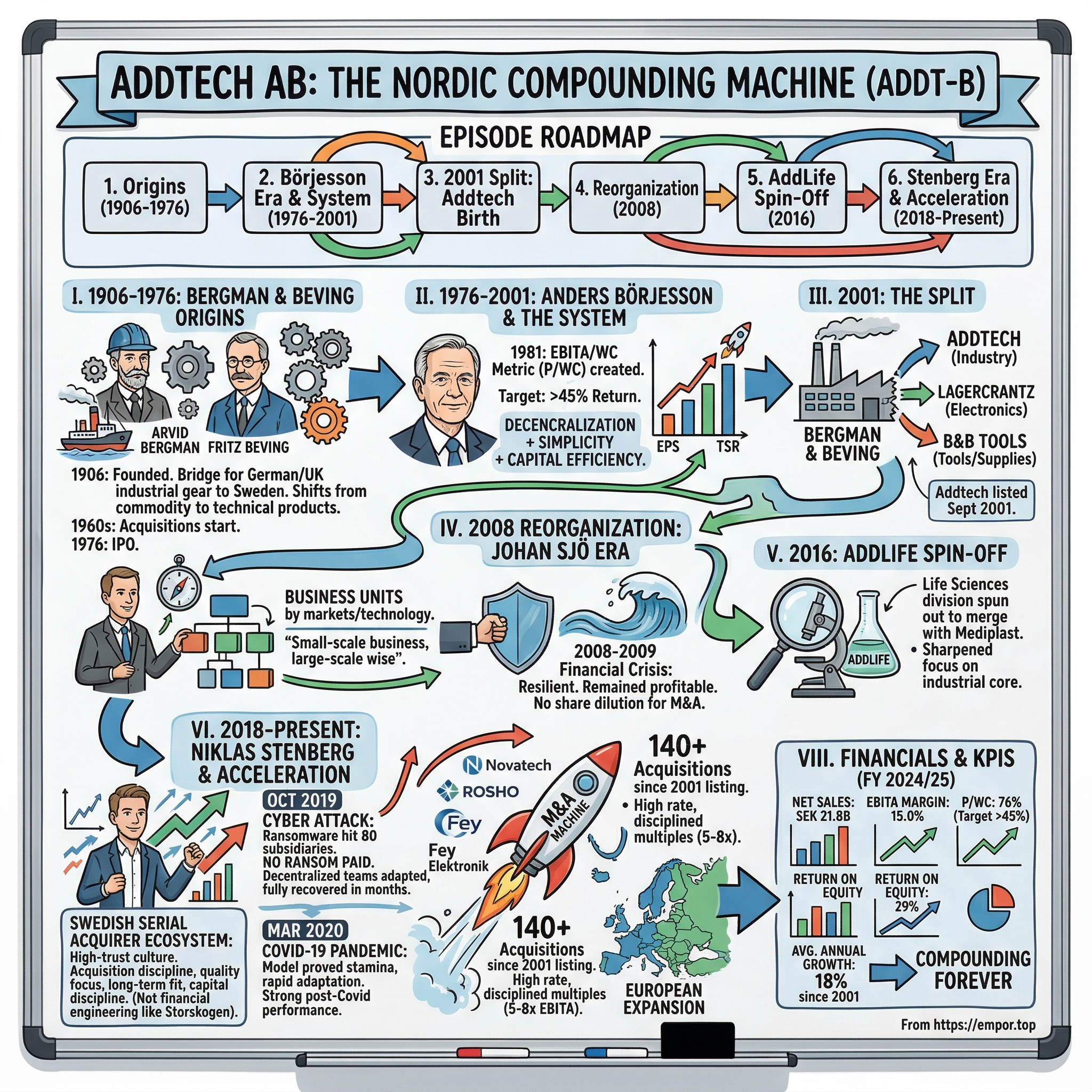

Addtech AB: The Nordic Compounding Machine

I. Introduction & Episode Roadmap

In the labyrinthine world of industrial distribution, where middlemen are often derided as value-extractors rather than value-creators, one Swedish company has quietly built something extraordinary. Addtech AB doesn't manufacture jet engines, develop pharmaceuticals, or write software. Instead, it does something far more elegant: it compounds capital at rates that would make most tech investors jealous while operating in markets so boring that most analysts refuse to cover them.

Consider this: Since its listing in September 2001, Addtech's average share price increase has been 17 percent annually. Over the corresponding period, the Stockholm exchange's OMX Stockholm index changed by an average of 5 percent. That's not a typo. While the broader Swedish market merely tripled over two decades, Addtech shareholders watched their wealth multiply more than 20-fold, not including dividends.

For the fiscal year ending March 2025, the company posted SEK 21.8 billion in net sales, generated EBITA margin of 15.0%, and achieved a return on working capital of 76%. The company now operates more than 150 subsidiaries with about 4,000 employees, generating annual sales exceeding SEK 20 billion.

But Addtech's story isn't primarily about numbers. It's about a philosophy—a nearly religious devotion to decentralization, an obsession with a single metric that governs all capital allocation decisions, and a Swedish cultural backdrop that makes certain types of trust-based business models possible in ways they simply aren't elsewhere.

Fundamentally, Addtech has had the same business concept for more than 100 years. In 1906, engineers Arvid Bergman and Fritz Beving founded Bergman & Beving, with the business concept of importing technical products from Germany and selling them on to the rapidly expanding Swedish industries.

What makes this story worthy of a deep dive isn't just the returns—though those alone would justify attention. It's the system. Addtech represents one of the purest expressions of what some call the "Berkshire model" applied to industrial distribution: buy good businesses, leave the operators alone, measure obsessively but simply, and compound forever. The twist is that Addtech operates at a scale and pace of acquisition that Berkshire never did—completing over 140 acquisitions since its 2001 listing while maintaining disciplined multiples and profit growth.

The Nordic serial acquirer ecosystem that Addtech inhabits has produced some of the best-performing stocks in European market history. In Sweden, there are a number of what investors call "serial acquirers." But there are many others including Addtech, Indutrade, Lagercrantz and more. Understanding why Sweden became the breeding ground for these compounding machines is essential to understanding whether the model can continue or whether it's reaching its natural limits.

This is the story of a company that traces its lineage to the industrial revolution, survived two world wars, adapted to the digital age, weathered a massive cyberattack, and continues to grow profits at 18% annually without issuing shares to fund acquisitions. Let's begin.

II. The Bergman & Beving Origins (1906-1976)

The story begins not in a garage or a university lab, but in the shipyards and factories of turn-of-the-century Germany and England. During the 1890s, Arvid Bergman and Fritz Beving were working in Germany and England in the midst of the industrial revolution. This experience led them to foresee further rapid industrialisation in Sweden. But there was one problem: industrial suppliers didn't have the local knowledge to sell into the Nordics.

The insight was deceptively simple: Swedish factories needed German industrial equipment—precision tools, measuring instruments, specialized components—but German manufacturers had neither the linguistic skills nor the market knowledge to sell directly into Scandinavia. Bergman and Beving saw themselves as the bridge.

In 1906, the two founders created Bergman and Beving (B&B) as the first importer and agent for foreign manufacturers to sell industrial products to Sweden. Over 100 years later, this heritage has created four listed companies that manage hundreds of operating subsidiaries with over $10bn in enterprise value.

What made B&B different from the start was its focus on technical products rather than commodities. In the 1920s, the company slowly began to shift strategy. Bergman & Beving moved on from standard products to instead invest in more advanced products with better margins. Quartz lamps and later also microscopes, spectrographs, carbon brushes and vacuum pumps became important contributions to improved profitability.

This early strategic pivot—from commodity distribution to value-added technical trading—established the DNA that would drive the company for the next century. The logic was elegant: if you're selling something complicated, customers need you. They need your engineers to explain how the equipment works, your technicians to install it, your support staff to troubleshoot problems. Standard products commoditize; technical products create relationships.

After World War 2, B&B signed a deal to sell the electronic measuring instruments of Danish firm Radiometer. This was the first move into 'value-added distribution'. B&B would now not only sell the products but also provide technical services and training to the end users.

The post-war boom accelerated B&B's growth as Swedish industry modernized. But the truly transformative strategic shift came in the 1960s. In the mid-1960s, an era of corporate acquisitions commenced with the objective of complementing existing operations with companies in adjacent market segments. Acquisitions have since been part of the day-to-day operations, bringing new business opportunities and skilled employees.

Bergman & Beving (B&B), founded in 1906, has a rich history of decentralization and simplicity, starting their acquisition journey already in the 1960s. This was decades before the concept of "serial acquirer" became fashionable in investment circles. B&B discovered early that acquiring small, owner-operated technical trading companies was far more efficient than building capabilities internally. The entrepreneurs who built these businesses knew their customers and products intimately; B&B could provide capital, shared services, and a long-term home.

Bergman & Beving was listed on the stock exchange in November 1976. The IPO marked the beginning of a new era—one that would see the formalization of the acquisition-driven business model and the emergence of the man who would codify the entire system.

III. The Anders Börjesson Era & The Creation of a System (1976-2001)

Every great institution has its architect, the figure who takes raw materials and shapes them into something coherent and replicable. For Addtech and its entire family of spinoffs, that figure is Anders Börjesson.

Anders Börjesson is Addtech's largest shareholder. He started his B&B journey as an external auditing consultant and gained fame by spotting a tax declaration error that saved the firm millions. And this was around 1976, the year of B&B's IPO, when the revenues and EBT of B&B were SEK 167m and 8m, respectively.

The story of Börjesson's arrival reads like corporate legend. A young accounting consultant, brought in for routine work, notices something others missed—an error that saves the company substantial money. But what transforms this from interesting anecdote to foundational myth is what Börjesson had been thinking about for years before he walked through B&B's doors.

Six years earlier, at his student dorm, he had read the book "The new millionaires, ten new super entrepreneurs in the Swedish Middle Way ('Folkhemmet')." Five of the profiled entrepreneurs, including Ingvar Kamprad (IKEA) and Erling Persson (H&M), had almost been forced to become asset-light, as net assets of privately held firms were subject to a wealth tax.

This insight—that Swedish tax policy had inadvertently created a class of entrepreneurs obsessed with capital efficiency—would become the intellectual foundation for everything that followed. In a world where accumulating assets on the balance sheet triggered punitive taxation, the survivors were those who found ways to generate profits while keeping capital invested to a minimum. Kamprad famously doesn't own IKEA stores (franchisees do). Börjesson would apply similar logic to industrial distribution.

He entered B&B's group management in 1979, launched the EBITA/WC metric together with his mentor Torsten Fardell in 1981, became CEO in 1990, and stayed on until 2001. In his last year, he split the group into three by separately listing Addtech and Lagercrantz.

The EBITA/WC metric—known internally as P/WC or "Profit over Working Capital"—deserves special attention because it governs virtually every capital allocation decision at Addtech to this day. The target is deceptively simple: each subsidiary should generate operating profit equal to at least 45% of its working capital.

Think about what this means in practice. If a subsidiary has SEK 10 million tied up in inventory and receivables (net of payables), it needs to generate at least SEK 4.5 million in operating profit to meet the hurdle. Companies that achieve this are rewarded with autonomy and capital for growth. Companies that consistently miss it face tough questions.

The beauty of P/WC is its flexibility. A high-margin business with modest asset turns can hit the target. So can a lower-margin business that runs extremely lean on inventory and collects receivables quickly. Management doesn't dictate how subsidiaries should operate—just that they need to hit a return threshold. The path is up to them.

Bergman & Beving has always been a growth company. Our goal is long-term earnings growth of 15 percent per year. To promote stronger growth in the future, we will acquire companies to complement our existing businesses. Over the years, we have acquired more than 160 companies, and more than 85 percent of these acquisitions have proven to be successful in the sense that they have contributed to increased earnings per share.

The 85% success rate is remarkable in a world where academic studies consistently show that most acquisitions destroy value. The secret appears to lie in the combination of extreme discipline on price, careful cultural matching, and the decentralized post-acquisition approach that lets acquired entrepreneurs continue running their businesses.

B&B's EPS grew by 18% annually from 1976 to 2001, and the annual total shareholder return (TSR) was 25%. Lagercrantz has boasted a 20% TSR CAGR from 2001 to today, while Addtech has performed even better.

By the late 1990s, however, B&B had grown to a size where its three main business areas—technology trading, electronics distribution, and tools/industrial supplies—had begun to diverge strategically. The company that had pioneered Swedish serial acquisition was about to pioneer something else: the strategic spinoff.

IV. The 2001 Split: Birth of Addtech

In 2001, Anders Börjesson made perhaps his most consequential decision as CEO: he would split Bergman & Beving into three independent, publicly traded companies. The move was radical for its time. While conglomerates elsewhere were still trying to prove synergies existed, Börjesson concluded that his businesses would create more value if shareholders could invest in each one separately.

In the early 2000s, Bergman & Beving divided its operations into three independent subsidiaries, each of which was listed on the Stockholm Stock Exchange. Addtech was built on Bergman & Beving's Industry business area, which had sales of slightly less than SEK 2.5 billion and approximately 1,100 employees.

The strategic rationale was characteristically Börjesson: different businesses attract different acquisition targets, and trying to house life science distributors alongside industrial component traders only confused potential sellers about what kind of home they were joining. Separately listed entities could sharpen their focus and accelerate their individual acquisition programs.

In 2001, B&B spun out Addtech and Lagercrantz separately. Addtech later spun out Addlife, its medical sciences division. After the 2001 spins, B&B renamed itself B&B Tools to focus on tools and supplies for the manufacturing and construction sectors.

Addtech, led initially by CEO Roger Bergqvist, emerged from the spinoff as a focused technology trading company serving industrial customers. But its first years as an independent entity would prove far more challenging than anyone anticipated.

The telecom crisis hit Addtech hard, but also served as a valuable lesson.

The early 2000s telecom bust devastated companies with exposure to the technology and telecommunications sectors. Addtech, with significant business in electronic components serving telecom customers, wasn't spared. Revenues fell, profits dropped, and the newly public company had to demonstrate whether its decentralized model could handle crisis.

The experience shaped Addtech's subsequent evolution in important ways. First, it reinforced the importance of diversification—not just across products, but across customer segments and geographies. A company too concentrated in any single end market was vulnerable to sector-specific downturns. Second, it proved the resilience of the decentralized model: subsidiary managers, empowered to make decisions quickly, could cut costs and adapt to changing conditions faster than centralized competitors.

Anders Börjesson remained Chairman of the Board since 2001. He was also a Board member at Bergman & Beving and at a number of companies within Tisenhult-gruppen. Professional experience: President and CEO of Bergman & Beving.

Börjesson's continued presence on the board ensured continuity of philosophy even as operational leadership passed to a new generation. The 2001 spinoff had created three laboratories for the Bergman & Beving model. Each would evolve somewhat differently, but all would maintain the core principles: decentralization, the P/WC metric, disciplined acquisitions, and long-term orientation.

V. Key Inflection Point #1: The 2008 Reorganization

Seven years after its listing, Addtech underwent its first major organizational transformation. The Board of Directors of Addtech AB has appointed Johan Sjö to serve as new President and Chief Executive Officer of the Company effective as of 1 January 2008. The current President, Roger Bergqvist, will remain in his position until then. Thereafter Roger Bergqvist will be active in the Addtech Group in development and strategy issues.

Johan Sjö brought a unique perspective to the CEO role. Johan Sjö has been a member of group management at B&B TOOLS since 2003, where he was President of B&B Development and a driving force in the group's expansionary phase, which included the acquisition of some 40 companies. During the years 1994-2002 Johan Sjö was active at Alfred Berg, in areas such as analysis and corporate finance.

Sjö's combination of investment banking background and operational experience in the B&B ecosystem made him ideally suited to scale Addtech's acquisition program. His first major initiative was structural: reorganizing the company around business units rather than pure geographic or product-based divisions.

In 2008, a new business-oriented organisation was introduced with the subsidiaries being grouped into business units linked to overarching markets or areas of technology.

The logic was straightforward but powerful. By clustering subsidiaries that served similar markets or shared technological expertise, Addtech could create centers of gravity for both organic growth and acquisitions. Business unit managers could identify gaps in their portfolios, build relationships with potential targets in their niches, and oversee integration more effectively than a purely centralized corporate team.

The 2008-2009 financial crisis struck just as Sjö was implementing these changes. It was a brutal test of the model's resilience. Global trade collapsed, industrial customers slashed spending, and acquisition financing dried up across markets.

Addtech's strategy is to acquire and develop in successful, well-managed and market-leading niche companies with the potential to generate long-term profitable growth. Despite various crises, recessions, cyber attacks and pandemics, we have continuously delivered shareholder value, with an average annual growth of 18 percent since the start in 2001.

The key point: Addtech didn't lose money during the financial crisis. Profits declined—as they did across most industrial companies—but the company remained solidly profitable and quickly recovered when conditions normalized. This resilience stemmed directly from the decentralized structure. Each subsidiary, responsible for its own P&L, could make the necessary adjustments independently. The corporate center didn't need to micromanage cost cuts across 130 entities; each entrepreneur knew their business and took appropriate action.

"Our concept has been successful for more than 100 years, which shows that, despite industrial development and fluctuations in the economy, a link between manufacturers and users is required – as long as it adds value." - Johan Sjö, Former CEO of Addtech

Sjö also articulated why value-added distribution remained attractive in the Nordics despite globalization and digital disruption: "You therefore have 26 to 28 million people. You have different languages so for companies coming from outside, if they are going to be able to establish themselves in a region like that, I think it's very complex. You need to have a critical mass; you need to have the countries if you are going to be successful, because you also need to translate, for example, the manuals and so on. In some cases, you need to answer in the local languages. It is quite complicated to establish that business if you do not already have a Nordic setup or a Nordic organization."

The argument was compelling: the fragmented Nordic market—four major countries with different languages, regulations, and business cultures—created natural barriers for foreign manufacturers trying to serve customers directly. A skilled intermediary who understood all four markets could add genuine value that justified its margins.

VI. Key Inflection Point #2: AddLife Spin-Off & Sharpening Focus (2016)

By 2015, Addtech had grown to include a substantial life science division that traced its origins to a 2005 acquisition. Addtech acquired the operations in AddLife in 2005. Since then it has performed very well and now has estimated annual sales of approximately SEK 1.7 billion with good profitability. AddLife currently has strong market positions in several Life Science niche areas in the Nordic region.

But life science distribution—selling to hospitals and research labs primarily through public procurement processes—operated quite differently from Addtech's core industrial business. The spin-off will benefit both AddLife and Addtech, allowing each company to focus on its respective core market. AddLife sells primarily to Nordic healthcare providers, largely through public procurement. This type of sales has limited connection to the rest of Addtech's business, which focuses on industrial markets. Separating the businesses will increase the opportunity for long-term profitable growth for both companies.

In March 2016, Addtech distributed its shares in AddLife to shareholders, and AddLife began trading on Nasdaq Stockholm as an independent company. On March 16, 2016, AddLife shares were listed on Nasdaq Stockholm. AddLife was formed in June 2015 and represents the incorporation of the former Life Science business area within the Addtech Group.

Established as a spin-off of Addtech's life science business unit, AddLife is an independent player in the Nordic life science market. "It's our opening-day on the stock exchange but AddLife has a hundred year old history as a spin-off from Bergman & Beving and Addtech. We'll now be able to fully focus on continuous profitable growth, both organically and through acquisitions."

The spinoff followed the playbook Börjesson had established in 2001: create focused entities that can attract the right acquisition targets and allow shareholders to invest precisely in the exposures they want. AddLife went on to become a tremendous success, benefiting from healthcare spending growth and eventually from COVID-19-related demand for diagnostics and protective equipment.

In 2016, Addtech spun out the Life Sciences division to merge with Mediplast and list in Stockholm. Today, Addlife is worth 30bn SEK and Addtech ~40bn SEK.

For Addtech, the spinoff sharpened focus on its core industrial markets and freed up management bandwidth to pursue acquisitions in its remaining business areas. It also demonstrated something important about the Bergman & Beving model: spinning off successful divisions wasn't failure—it was a feature. When a business grew large enough and different enough to benefit from independence, the parent would let it go, creating value for shareholders in the process.

VII. Key Inflection Point #3: Niklas Stenberg Era & Acceleration (2018-Present)

In March 2018, Addtech announced its third CEO since listing. Current CEO Johan Sjö has at his own request, decided to leave his operational role in Addtech to focus more on his external board assignments. The Board of Directors has appointed Niklas Stenberg as new President and CEO of Addtech AB. Niklas Stenberg will take over in connection with the Annual General Meeting 30 August 2018.

Stenberg represented a new generation of Addtech leadership. Niklas Stenberg has solid experience from the Group and has been Business Area Manager of Power Solutions and part of Group Management since 2015. Between 2010 and 2015 Niklas has held various senior positions within Addtech, such as Business Unit Manager and Managing Director of subsidiaries. In 2005-2010, Niklas was employed in various positions within Bergman & Beving/B&B Tools and before that as a lawyer at Advokatfirman Delphi. Niklas Stenberg is 44 years old and holds a law degree from Uppsala University.

The new CEO wasted no time making changes. The new Automation business area is established in 2019, meaning that Addtech now has five business areas.

Then came the crisis that would define early months of Stenberg's tenure.

The Cyber Attack Test

When Addtech were victims of a massive ransomware attack in October 2019, nearly all activity was halted. 80 of the 130 subsidiaries were affected, which meant that almost 1700 of the 2900 employees of the group were impacted.

The ransomware attack struck Addtech's IT systems just over a month ago, on October 30, 2019. The ransomware attack struck Addtech's IT systems on October 30, 2019.

For a company that prided itself on decentralization, the attack was particularly ironic: the shared IT infrastructure that connected all subsidiaries had become a vulnerability. The response, however, was characteristically Addtech.

In October, Addtech is hit by a cyber-attack affecting 80 of the 130 companies. The attackers encrypt the central IT environment and then demand a ransom to reinstate it. For Addtech, not paying is the obvious course of action, and the company opts instead to explain openly what has occurred.

For Addtech, submitting to the attackers' ransom demands was never under consideration. The crime was reported to the police, and databases and files with encrypted information were able to be saved anyway.

The decision not to pay was both principled and pragmatic. Paying ransoms encourages future attacks and provides no guarantee of data recovery. But it required confidence that the company could rebuild—and transparency with stakeholders about what was happening.

In October 2019, 80 of Addtech's subsidiaries were affected by a ransomware attack estimated to have impacted net sales by approximately SEK 130 million and EBITA by approximately SEK 100 million for the financial year.

Now it feels good that we are in a position where we can again put all the focus on business and get back to normal, says Niklas Stenberg, president and CEO of Addtech. As previously announced, the attack was a so-called ransomware attack in which 80 of the group's 130 companies were hit, equivalent to about half of the group's turnover. Following the attack, a brand new IT environment with significantly more security layers has been built together with some of Europe's foremost cybersecurity experts.

After a couple of weeks of nonstop intense work, parts of the business started to regain functioning systems. After roughly two months, each of Addtech's systems were back in production.

The recovery demonstrated the paradoxical strength of decentralization: even as central IT systems went down, individual subsidiaries adapted. Many reverted to offline operations, processing orders manually while the crisis was resolved. The entrepreneurial culture that Addtech cultivated meant employees at the subsidiary level didn't wait for headquarters to solve their problems—they found workarounds and kept serving customers.

COVID-19: The Decentralized Model Proves Itself

The pandemic followed just months after the cyber attack recovery was complete. In March 2020, the World Health Organisation (WHO) announced that the spread of the corona virus had been classified as a pandemic. Some of Addtech's segments were hit hard, while the business situation remained far more positive in other areas of the operations. During the pandemic, the business model and corporate culture demonstrate once more their stamina and capacity in rapidly adapting the operations to external changes.

The numbers speak for themselves: sales rose by 16 percent, divided equally between organic growth and contributions from acquisitions, operating profit increased by 28 percent and the EBITA margin reached a record high of 11.6 percent. On the other hand, we encountered the toughest possible circumstances in the second half of the financial year – initially in the form of a large-scale cyberattack and later in the form of the COVID-19 pandemic that has shaken up the entire global economy.

The years following COVID would prove to be among Addtech's strongest. Despite the uncertainty in the general business environment, the year has been characterised by a high level of activity, resulting in a sales increase of 9 percent, with organic growth in all quarters, earnings growth of 14 percent and a strengthened EBITA margin of 15.0 percent (14.3). With a high rate of acquisitions combined with the strength of our well-diversified business of entrepreneurial niche companies in strong positions, we have once again managed the challenges, while capturing the potential of the market in a highly satisfactory manner.

The acquisition pace accelerated under Stenberg's leadership. Significant acquisitions during the 2024-2025 period include Novatech (April 2025), ROSHO (February 2025), COEL (January 2025), Nanosystec (November 2024), and GoDrive (April 2024 for $75 million).

During the financial year, completed acquisitions resulted in an increase of the number of employees by 325. The average number of employees in the latest twelve month period was 4,341.

VIII. The Addtech Business Model Deep Dive

Understanding Addtech requires understanding what "technical solutions" actually means in practice. Addtech offers high-tech products and solutions for companies in the manufacturing and infrastructure sectors. We add both technical and financial value by being a skilled and professional partner. This means that we shall add value by helping customers produce their goods more efficiently, helping make their products more competitive in the development towards a sustainable tomorrow.

The company organizes its operations into five business areas: The company's segments include Automation, Electrification, Energy, Industrial Solutions, and Process Technology. It generates maximum revenue from the Energy segment. Energy produces and sells products for electricity transmission, electrical installation, and safety products in transport.

The Decentralization Philosophy

The operating philosophy can be summarized in a phrase Addtech uses constantly: "small-scale business—large-scale wise."

That means decisions about the companies' operations are taken close to the market. Addtech combines the flexibility, personality and efficiency of a small company with the resources, networks and long-term approach of a large business.

Addtech provides clear instructions to operating companies: 'do what you should, how and when you want - but keep the deadline and explain all deviations'. Accountability is pushed as close as possible to the front line to empower employees to act as owners.

The decentralized model serves multiple purposes. First, it preserves the entrepreneurial energy that made acquired companies successful in the first place. Second, it creates accountability—each managing director owns their P&L and can't hide behind corporate bureaucracy. Third, it enables speed—decisions don't require approval chains that extend to Stockholm.

What the parent company provides is equally important. Our strategy of continuous profitable growth, both organically and through acquisitions, has been proven to be effective. Our principal task as owners is to make life easier for our companies, so that they can focus on continuing their successful development, benefiting from Addtech's network and our resources in the form of skills and expertise, experience and financing.

Addtech supports subsidiaries with financing for growth, foreign exchange management, shared accounting resources, logistics coordination, ERP systems, framework agreements with major suppliers, and legal expertise. These are functions where scale creates value without impinging on operational autonomy.

The Acquisition Machine

Addtech's strategy is to acquire and develop in successful, well-managed and market-leading niche companies with the potential to generate long-term profitable growth.

Addtech prefers targets with a high knowledge & technology content in their existing niches, that possess strong supplier relationships, and that are profitable with growth potential. Börjesson developed the following checklist for evaluating businesses, where it is best to have marks on the left, and it is still in use today.

The acquisition criteria have remained remarkably consistent for decades. Addtech seeks companies that: - Operate in technical niches with meaningful barriers to entry - Have strong relationships with quality suppliers - Generate sustainable profits (not turnarounds) - Are run by entrepreneurs willing to stay post-acquisition - Can be acquired at reasonable multiples

Addtech makes sure that key individuals (often owners, but sometimes the marketing or technical managers) are motivated and enjoy running their businesses under the Addtech umbrella after selling. Business owners frequently sell to Addtech as they continuously encounter Addtech's commonsensical approach within their niches.

The multiples paid remain disciplined. Based on available data, Addtech typically pays 5-8x EBITA on initial purchase consideration, with earnout structures that can increase total consideration based on future performance. This is far lower than the multiples private equity typically pays for quality businesses.

Long-term Relationship Building

The consistency of their approach not only helps serial acquirers avoid poor acquisitions, but it also helps establish their reputation as an attractive home for private companies. Serial acquirers often nurture relationships with potential targets for longer than, say, private equity competitors. Trust takes time to build. It involves frequent conversations and, in Sweden, many rounds of coffee.

For instance, Addtech took a decade to finally acquire Fey Elektronik, a leading German player in industrial battery solutions, in 2021. After a decade of trusting relationship building, the owners were finally ready to sell their life's work to Addtech.

The Fey Elektronik example illustrates the long-term orientation. Addtech Electrification a business area in the Addtech Group, has today signed an agreement to acquire 90% of the shares outstanding in Fey Elektronik GmbH. Fey serves European OEM customers with development, design and manufacture of customized battery solutions. Fey has 160 employees and annual sales of around 55 MEUR.

"We have known Fey and Michael Witte for many years and we are very happy to be able to acquire the leading German battery company when it comes to high quality battery systems for a number of industry segments. Fey is a very well-run company and we are proud to welcome Fey to the family", says Niklas Stenberg, CEO Addtech.

This patient approach creates competitive advantage. Many business owners, particularly older entrepreneurs considering succession, want to sell to a buyer who will preserve their legacy—not strip-mine the business for quick returns. Addtech's reputation as a long-term owner who leaves management in place makes them the preferred buyer for many targets, even at somewhat lower prices than private equity might offer.

The best serial acquirers have often been in talks or had relationships with the seller for years before a deal even is on the table. This is very different than a structured process where brokers and advisors run auctions, with a limited due diligence period and often seeking the highest price possible. This gives experienced serial acquirers two distinct advantages, adverse selection and a deep insight into the people running the business.

IX. The Swedish Serial Acquirer Ecosystem

One question I liked to ask is "Why Sweden?" Why are there so many of these structures in Sweden? You don't find them in other European markets. There are some. The UK has several good ones. But it's not the same as you find in Sweden. Two common answers I got when canvassing different people: One is a matter of history and culture. Swedish society works with a high level of trust.

Sweden's high-trust culture enables the decentralized model to work. When headquarters empowers subsidiary managers to make major decisions independently, there must be confidence that those managers will act in the company's interest. Swedish business culture, with its emphasis on consensus, transparency, and long-term relationships, creates this foundation.

The second explanation is institutional: But that model has proven so attractive that suitable M&A opportunities in the Nordic region's biggest economy are becoming something of a crowded trade. "The Swedish market has faced higher competition because there are several who have taken inspiration from those on the stock exchange who have succeeded and now want to do it themselves," said Jon Hyltner, a portfolio manager at Enter Fonder AB. Hyltner says there's now more difficulty in unearthing targets at attractive multiples in Sweden, which is why the likes of Indutrade have been actively buying in the U.K. and Germany.

The success of Bergman & Beving and its spinoffs created a template that others have followed. The Stockholm Stock Exchange now hosts dozens of companies using variations of the serial acquirer model. Some focus on software (Constellation Software's Swedish competitors), others on dental equipment (Lifco), others on industrial components (Indutrade, Lagercrantz).

But not all serial acquirers succeed. The Swedish market also provides cautionary tales.

It's not so easy to build a successful serial acquirer. It's not just buying a bunch of companies and trying to play a financial arbitrage game. Things can go horribly wrong. And a case study on this would be Storskogen, an aggressive gobbler of companies.

The manager believes that Storskogen, despite a lower quality level than for example Addtech and Lagercrantz, is now attractively valued. Storskogen is not considered to be of the same quality, but according to the manager it has improved considerably after the share price fall of recent years. The company has completed eleven divestments, representing around six percent of sales, since the new CEO took over in February last year, which has strengthened the operating margin, improved the organic growth profile and strengthened cash flow. The manager believes that Storskogen, despite a lower quality level than for example Addtech and Lagercrantz, is now attractively valued with a debt-adjusted operating profit multiple of around 10x, compared to around 30x for the most established serial acquirers.

What separates successful serial acquirers from failures? The evidence suggests several factors: acquisition discipline (not overpaying in competitive situations), quality focus (buying profitable businesses rather than turnarounds), cultural fit (ensuring acquired entrepreneurs will thrive post-sale), and capital discipline (funding acquisitions from operating cash flow rather than excessive leverage or share issuance).

Serial acquirers that issue lots of shares are a red flag, in my opinion. Issuing shares could be opportunistic, which is fine, but it should definitely not be a habit. Serial acquirers that acquire companies with their organic cash flow significantly reduce the risk of blow-ups.

Addtech has been remarkably disciplined about shareholder dilution. Addtech has increased EBITA by 18% annually since its listing in 2001 (without diluting shareholders).

X. Financials & By-The-Numbers

As of August 2025, Addtech is a public entity with a market cap of approximately $8.87 billion USD and 270 million shares outstanding. The company employs about 4,585 people across over 150 subsidiaries, achieving annual sales of around SEK 22 billion by July 2025. Its operations are segmented into Automation, Electrification, Energy, Industrial Solutions, and Process Technology, with the Energy sector being the highest revenue generator.

The financial transformation since listing is remarkable:

| Metric | 2001 | FY 2024/25 |

|---|---|---|

| Net Sales | ~SEK 2.5B | SEK 21.8B |

| Employees | ~1,100 | ~4,500 |

| Subsidiaries | ~40 | 150+ |

| EBITA Margin | ~8% | 15.0% |

Earnings growth 14%. Return on working capital (P/WC) 76%.

The P/WC of 76% means Addtech generates operating profit equal to 76% of its working capital investment—far above the 45% minimum threshold. This reflects both operational excellence at subsidiaries and the high-margin nature of value-added distribution.

As of March 31, 2025, Addtech reported a return on equity of 29 percent and an equity ratio of 38 percent.

The 29% return on equity is exceptional for any industrial company, let alone one in a supposedly "boring" sector like distribution. It reflects the asset-light model, disciplined capital allocation, and consistent profit growth.

From the outset in September 2001, the Addtech share has achieved an average price increase of 20 percent annually.

For perspective on what 20% annual returns mean: an investor who put SEK 100,000 into Addtech at its 2001 listing would, before dividends, have seen that investment grow to over SEK 2 million by 2025. Including dividends, the total return would be even higher.

The Track Record vs. Targets

Despite various crises, recessions, cyber attacks and pandemics, we have continuously delivered shareholder value, with an average annual growth of 18 percent since the start in 2001.

Addtech's stated target is 15% annual profit growth. Achieving 18% over more than two decades—through the telecom bust, the financial crisis, the euro crisis, a ransomware attack, and COVID—suggests the target is conservative. But management insists the 15% target remains appropriate, reflecting both the difficulty of sustaining high growth rates and the company's conservative culture.

XI. Strategic Analysis & Key KPIs

Myth vs. Reality

Myth: Value-added distribution is a dying business model being disintermediated by the internet.

Reality: For technical products requiring customization, installation, training, and support, the middleman adds genuine value. Addtech's margins have expanded, not contracted, over the past two decades. Digital tools have enhanced rather than replaced the customer relationship.

Myth: Serial acquirers are just financial engineering—buying cheap, marking up, and playing multiple arbitrage.

Reality: The best serial acquirers like Addtech genuinely develop their acquisitions. Organic growth rates have been positive in most years. The P/WC improvements at acquired companies suggest operational value creation, not just financial alchemy.

Myth: The Swedish serial acquirer model can't travel.

Reality: Addtech generates substantial revenue outside Sweden and has successfully acquired companies across Europe. Geographically, the company derives maximum revenue from Sweden, and the rest from Denmark, Finland, Germany, Norway, the United Kingdom, the Rest of Europe, and other countries. The model appears transportable as long as management maintains discipline.

Porter's Five Forces Analysis

Supplier Power: Moderate. Addtech represents meaningful volume for many suppliers, but switches to alternative suppliers exist. The company's value-add reduces dependence on any single supplier.

Buyer Power: Low to Moderate. Customers are typically industrial companies with complex technical needs. Switching costs include relationships, installed bases, and training. Price sensitivity exists but is balanced by service requirements.

Threat of New Entrants: Low in individual niches, moderate overall. Each subsidiary operates in a niche with meaningful barriers (technical expertise, supplier relationships, installed base). New competitors could enter, but replicating the full network would be extremely difficult.

Threat of Substitutes: Low. The fundamental need for intermediaries who can customize, install, and support complex industrial products is persistent. Digital platforms can complement but rarely fully replace this role.

Competitive Rivalry: Moderate. Competition exists at the subsidiary level from other distributors and from manufacturers' direct sales efforts. The fragmented market structure limits intense price competition.

Helmer's 7 Powers Analysis

Scale Economies: Moderate. The holding company benefits from scale in financing, shared services, and management expertise. Individual subsidiaries are often too small for meaningful scale advantages, but the aggregate portfolio generates scale benefits.

Network Effects: Moderate. The network of 150+ subsidiaries creates knowledge-sharing benefits. Subsidiaries can share leads, best practices, and technical expertise. This internal network grows more valuable as more companies join.

Counter-Positioning: Strong. Addtech's decentralized model is difficult for traditional competitors to copy without cannibalizing existing structures. Large manufacturers who might try to forward-integrate would struggle to replicate the local knowledge and entrepreneurial culture.

Switching Costs: Moderate to Strong at the subsidiary level. Customers who have integrated a subsidiary's products into their manufacturing processes face meaningful switching costs.

Branding: Weak at holding company level, variable at subsidiary level. Individual subsidiaries may have strong brand recognition in their niches. The Addtech name itself carries limited customer-facing brand value.

Cornered Resource: Moderate. The pool of experienced managers who understand the B&B heritage represents a cornered resource. Similarly, long-standing relationships with potential acquisition targets are difficult to replicate.

Process Power: Strong. The institutionalized acquisition process—developed over decades and applied to 140+ transactions—represents genuine process power. Newcomers cannot easily replicate this accumulated expertise.

Key Performance Indicators to Track

For investors monitoring Addtech, three KPIs matter most:

-

P/WC (Return on Working Capital): The core metric that governs capital allocation across the entire organization. Declining P/WC would signal deteriorating operational quality at subsidiaries. The 2024/25 result of 76% significantly exceeds the 45% hurdle.

-

Organic Growth Rate: While acquisitions drive much of the growth, organic growth validates that existing businesses remain healthy. Negative organic growth would raise questions about market positioning. Consistent positive organic growth alongside acquisitions is the ideal.

-

Acquisition Multiples and Integration Success: Though not directly disclosed, investors should monitor acquisition announcements for deal sizes relative to revenues and compare performance of recently acquired businesses to determine if integration is succeeding.

XII. Bull and Bear Cases

The Bull Case

Addtech possesses a rare combination: a proven business model, excellent capital allocation, strong management continuity, and large addressable markets for continued acquisition growth.

The macro environment supports continued expansion. The energy transition requires exactly the kinds of technical products and solutions Addtech provides—batteries, power electronics, automation equipment, sustainable technology. Each major industrial trend (electrification, automation, infrastructure modernization) creates acquisition opportunities.

Geographic expansion has barely begun. While Sweden is becoming crowded with serial acquirers, continental Europe remains fragmented with thousands of family-owned technical distributors seeking succession solutions. As Hyltner says there's now more difficulty in unearthing targets at attractive multiples in Sweden, which is why the likes of Indutrade have been actively buying in the U.K. and Germany. Addtech has substantial runway for continued acquisitions.

Management stability provides continuity. With Börjesson still active on the board, Johan Sjö serving as chairman, and Niklas Stenberg executing the playbook, there's minimal risk of strategic drift. The culture is deeply embedded and reinforced constantly.

Valuation, while not cheap at ~30x earnings, reflects quality. Companies that compound earnings at 18% annually deserve premium valuations. The question is whether such growth can continue, and the evidence suggests it can.

The Bear Case

Addtech trades at multiples that assume continued high performance. Any stumble—slowing acquisition pace, integration challenges, margin compression—would likely result in significant multiple contraction alongside earnings pressure.

The competitive landscape is intensifying. More players are chasing the same pool of acquisition targets, potentially driving up multiples. If Addtech cannot maintain its 5-8x EBITA acquisition discipline, returns on capital will decline.

End-market cyclicality is real. Industrial production cycles affect all of Addtech's customer segments. A deep recession would pressure revenues and earnings across the portfolio, as occurred (moderately) in 2008-2009.

The decentralized model has limits. With 150+ subsidiaries, management attention becomes stretched. The 7-7-7 structure (approximately 7 business areas, each with approximately 7 business units, each with approximately 7 subsidiaries) can only scale so far before coordination costs become prohibitive.

Currency exposure creates volatility. With substantial operations outside Sweden but SEK-denominated reporting, currency movements can create earnings volatility independent of underlying business performance.

The company's performance is intrinsically linked to the broader economic climate. Downturns in manufacturing investment or weakened capital markets can directly impact demand for Addtech's offerings, as seen with challenges in the construction market and subdued order intake in the sawmill sector during Q4 2024/2025.

XIII. Conclusion: The Compounding Machine

The Addtech story offers several lessons for investors and business strategists alike.

First, simplicity scales. The P/WC metric, established in 1981, still governs capital allocation today. The decentralized operating model, developed under Börjesson, remains unchanged. Great business systems don't require constant reinvention—they require consistent application.

Second, culture matters more than strategy. Addtech's strategy could fit on an index card: buy good companies, leave them alone, measure rigorously, compound forever. What's harder to replicate is the trust-based culture that makes decentralization work, the long-term relationships that yield quality acquisition opportunities, and the managerial bench that has developed over decades.

Third, the best holding companies add value by getting out of the way. Addtech doesn't integrate acquisitions in the traditional sense—no rationalization of workforces, no consolidation of facilities, no imposed "best practices." Instead, it provides capital, removes bureaucratic friction, and lets entrepreneurs do what they do best. This humility about what the center can contribute is itself a competitive advantage.

Fourth, succession planning works. The seamless transitions from Börjesson to Bergqvist to Sjö to Stenberg demonstrate that founder-dependent cultures can institutionalize successfully. Each leader has maintained the core philosophy while making appropriate adaptations to changing conditions.

"Addtech has an ambitious target to grow the operating profit by 15 percent annually. With an average outcome of over 20 percent since the listing in 2001 and a clear focus on entrepreneurship and decentralized responsibility, we have built strong positions over time in technical niches with good growth opportunities, both in the Nordic region and internationally."

For investors, the question is whether Addtech can continue compounding at historical rates. The bull case rests on substantial remaining acquisition opportunities, favorable secular trends in the company's key markets, and a management team that has demonstrated remarkable consistency. The bear case emphasizes competitive intensity, valuation, and inevitable cyclicality.

What seems clear is that Addtech represents something valuable: a business model refined over more than a century, applied with discipline and patience, and delivered to shareholders without dilution or drama. In a world obsessed with disruption, the company offers a reminder that some of the best investments come from applying timeless principles—buy quality, allocate capital wisely, and let compound interest work—in industries boring enough that most investors don't bother to look.

Note: This analysis is based on publicly available information and should not be construed as investment advice. Past performance does not guarantee future results.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube