Axactor: The Janitors of European Capitalism

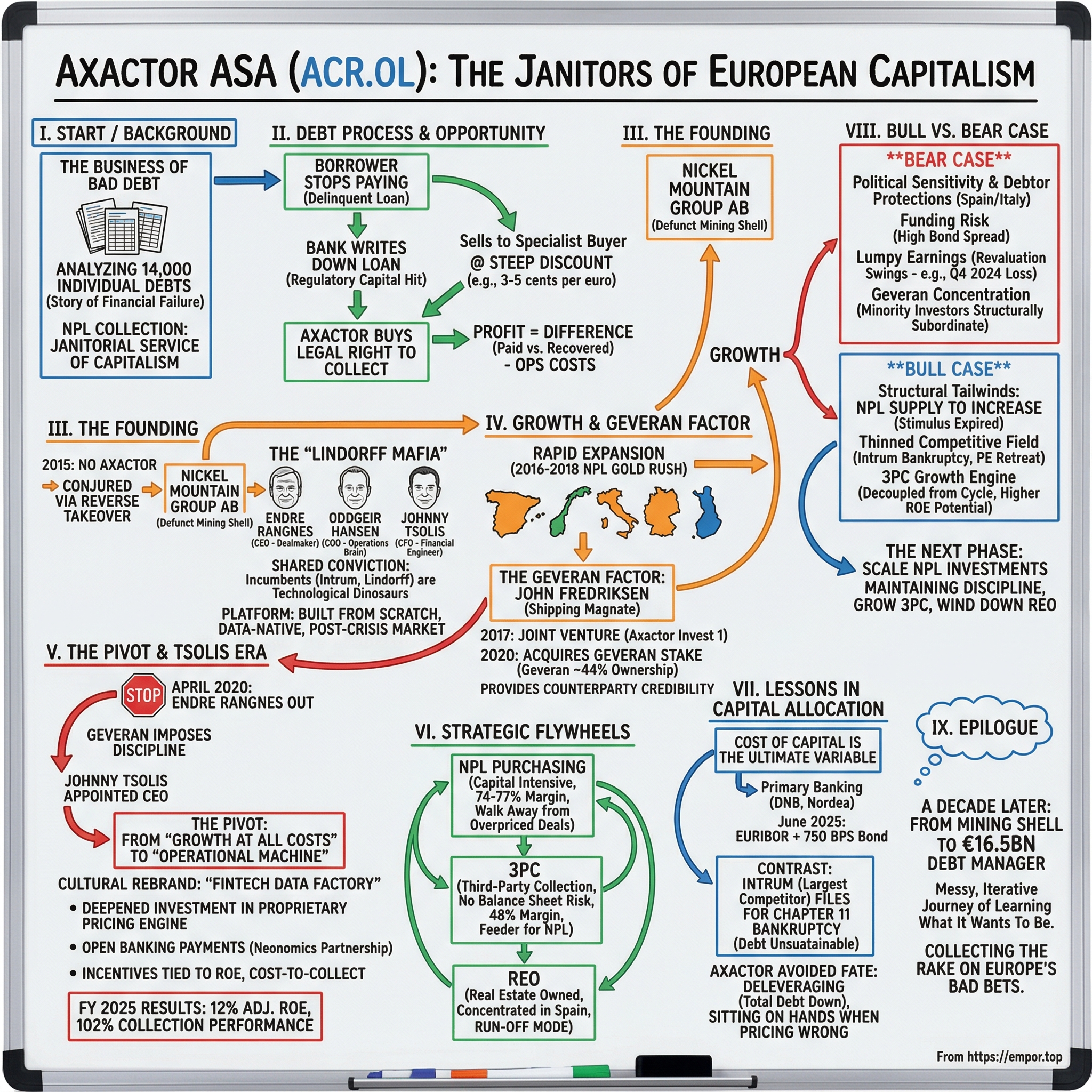

I. Introduction: The Business of Bad Debt

Somewhere in a nondescript office park outside Madrid, a twenty-six-year-old data analyst is staring at her screen. She is not trading stocks. She is not building an app. She is looking at a spreadsheet of 14,000 individual debts — each one a human story of financial failure — and her job is to figure out which of these people will eventually pay something back, how much, and when. The algorithm she feeds will determine whether her employer bids €4.2 million or €3.8 million for the entire portfolio. Get it wrong by half a cent on the euro, and tens of millions in expected profit evaporate. Get it right, and the company earns a quiet, unglamorous return that most investors never bother to understand.

This is the business of non-performing loan collection. It is, in the most literal sense, the janitorial service of European capitalism. When a borrower stops paying a bank — when the mortgage goes delinquent, when the small business loan curdles, when the credit card balance becomes a permanent fixture of someone's shame — the bank eventually needs to move on. It writes down the loan, takes the regulatory capital hit, and sells the mess to a specialist buyer at a steep discount, sometimes for as little as three to five cents per euro of face value. The buyer then owns the legal right to collect whatever it can. The difference between what was paid and what gets recovered, minus operating costs, is the profit.

The company doing that work in the Madrid office park is Axactor ASA, listed on the Oslo Stock Exchange under the ticker ACR.OL. It is a company that did not exist before 2015. It was conjured into being through a reverse takeover of a defunct Swedish mining shell, built by a trio of Norwegian executives who had spent their careers inside the debt collection industry's old guard, and bankrolled by the investment vehicle of John Fredriksen, Norway's wealthiest person. In the decade since, Axactor has assembled a portfolio spanning roughly 16.5 billion euros in face value debt across nearly a million individual claims, operating in six European markets from Norway to Italy.

The story of Axactor is not a rocketship growth narrative. It is something rarer and, for a certain kind of investor, more interesting: a story about capital allocation discipline in one of the most cyclical, misunderstood, and structurally important corners of European finance. It is a story about what happens when a startup enters a market dominated by century-old incumbents, grows aggressively, nearly overextends, gets disciplined by a demanding cornerstone shareholder, pivots from "growth at all costs" to "operational machine," and then watches its largest competitor stumble into bankruptcy court while it stands ready with dry powder and a freshly refinanced balance sheet.

To understand why Axactor exists and why it matters, you first have to understand the mess it was created to clean up.

II. The Backdrop: The Great European Deleveraging

In the spring of 2012, the president of the European Central Bank, Mario Draghi, had not yet uttered his famous "whatever it takes" line. European sovereign bond spreads were blowing out. Greek banks were hemorrhaging deposits. Italian and Spanish banks were staring at balance sheets stuffed with loans that borrowers had stopped servicing — mortgages on apartments in coastal towns where prices had halved, construction loans for housing developments that sat unfinished, consumer credit extended to workers who had since lost their jobs.

The numbers were staggering. By mid-decade, European banks held more than one trillion euros in non-performing loans. In Italy, the NPL ratio at some institutions exceeded 15 percent. In Greece, nearly half of all outstanding loans were classified as non-performing. Spain, Ireland, and Portugal were not far behind. The entire European banking system was, to use an unglamorous but accurate metaphor, constipated.

Here is why that matters beyond the banking sector. A bank's balance sheet works like a water pipe. Deposits and wholesale funding flow in one end, get transformed into loans, and flow out the other end as credit to businesses and households. When loans go bad, they clog the pipe. Each non-performing loan forces the bank to set aside regulatory capital — money that cannot be lent to someone else. Multiply that clogging effect by hundreds of billions of euros, and you get an economy where creditworthy borrowers cannot get loans, businesses cannot invest, and growth stalls. That is what was happening across Southern Europe.

The regulatory response was decisive. Basel III, the international banking accord phased in during this period, imposed stricter capital requirements that made holding bad loans punishingly expensive. The European Central Bank published supervisory guidance pressuring banks to reduce NPL ratios or face consequences. Then in 2019, the EU backstop regulation went further still, requiring banks to provision against non-performing exposures on a strict calendar — essentially an ultimatum: sell this garbage or we will force you to write it down to zero.

This created the largest forced-selling opportunity in European financial history. Banks that had been reluctant to crystallize losses by dumping bad loans at a discount were now being compelled to do so by their regulators. An entire industry of specialized debt purchasers and servicers emerged to absorb the flood.

The established giants of this world were Scandinavian. Intrum, founded in Stockholm in 1923, was the continent's largest player. Lindorff, a Norwegian firm with roots stretching back over a century, was another heavyweight. These companies had deep relationships with European banks, large balance sheets, and decades of operational experience. But they also carried the baggage of their age: legacy IT systems built in the 1990s, bloated cost structures, and organizational cultures that prioritized portfolio size over return on capital.

A small group of executives who had spent years inside these legacy firms watched the post-crisis NPL wave build and reached a shared conclusion: the incumbents were not built for this moment. The technology was outdated, the decision-making was slow, and the cost structures were too heavy for an industry where the difference between a profitable portfolio and a money-losing one often came down to a fraction of a cent per euro of face value.

They believed a new platform — built from scratch, data-native, designed for the post-crisis market — could do what the old guard could not. They just needed a vehicle, capital, and the audacity to compete against firms fifty times their size. What they found was a mining company in Sweden that had never successfully mined anything at all.

III. The Founding: The "Lindorff Mafia" and Nickel Mountain

In late 2014, three men began meeting regularly in Oslo to sketch out something ambitious. Endre Rangnes was the most prominent. His career trajectory read like a Nordic corporate who's-who: he had been country general manager for IBM Norway, then CEO of EDB Business Partner (one of Scandinavia's largest IT services firms) from 2003 to 2010, and then CEO of the Lindorff Group from 2010 to 2014, where he ran one of Europe's biggest debt collection operations. Rangnes was a builder, a dealmaker, a CEO who moved fast and thought in terms of platforms and scale.

Oddgeir Hansen had followed a parallel track — IBM, then COO of EDB Business Partner, then COO of Lindorff under Rangnes. He was the operations brain, the person who knew how to make collection systems actually work across borders and legal jurisdictions.

The third member was Johnny Tsolis, and his profile was different. Tsolis held a Sivilokonom degree (the Norwegian equivalent of an MSc in economics) from BI Norwegian Business School and had built his career in investment banking and corporate advisory — first at Handelsbanken Capital Markets, then at Cardo Partners, then at DHT Corporate Services. He was the financial engineer, the person who understood deal structures, capital markets, and the mathematics of buying distressed debt at the right price.

What bound the trio was their time at or around Lindorff and a shared conviction that the industry's legacy players were technological dinosaurs. At Lindorff, Rangnes and Hansen had seen firsthand how inflexible the old IT systems were — systems that could not easily adapt to new jurisdictions, that required manual intervention for tasks that should have been automated, and that made it nearly impossible to run the kind of sophisticated, data-driven collection strategies the market demanded. Tsolis had modeled the economics and knew that a modern platform could collect more per euro spent.

Their solution was characteristically pragmatic. Rather than spend two years pursuing a traditional IPO process, they identified a classic shortcut: the reverse takeover. Their target was Nickel Mountain Group AB, a company incorporated in Sweden in 1982 and listed on Nasdaq Stockholm. Nickel Mountain's business was supposed to be nickel mining, specifically a project called Ronnbacken in northern Sweden. By 2015, the project had gone nowhere. The company was a shell — a listed entity with a stock exchange listing, a corporate structure, and nothing else of value.

In December 2015, the founders executed a precise sequence of transactions. Nickel Mountain acquired ALD Abogados, a Madrid-based debt recovery law firm with roughly ninety employees, injecting the first real operating asset into the shell. Simultaneously, the Ronnbacken mining project was divested to Archelon AB, stripping out anything related to minerals. On December 23, 2015, an extraordinary shareholders' meeting voted to rename the company Axactor AB. The name change took effect on January 11, 2016. A failed mining company had been transmuted into a European debt platform in a matter of weeks.

Spain was chosen as the first market for good reason: Spanish banks were among the most aggressive NPL sellers in Europe, the legal infrastructure for debt recovery was well developed, and the sheer volume of distressed debt available made it an ideal laboratory for testing the new platform.

The pace of what followed was breathtaking. In February 2016, Axactor purchased its first major NPL portfolio in Spain, roughly €500 million in face value. In March, they acquired IKAS Norge, a Norwegian collection company with about seventy employees, for NOK 291 million. In May came Geslico, a Spanish firm with three hundred employees across eight cities, providing national coverage. In June, they entered Italy through CS Union, a firm managing over a billion euros in debt, in partnership with Banca Sistema. By September, they had expanded into Germany by acquiring Altor Group in Heidelberg, and later added Finland through the purchase of SPT Group in 2018.

Within eighteen months, the mining shell had morphed into a multi-country operation with over nine hundred staff and billions in managed portfolios. The speed was exhilarating. It was also dangerous. The 2016-2018 period was the "NPL Gold Rush" in Europe — capital was cheap, competition for portfolios was fierce, and the temptation to overpay was enormous. The question of whether Axactor maintained pricing discipline during this frenzy, or got swept up in the same exuberance that would later cripple some competitors, would only become clear in hindsight.

What was clear immediately was that the founding team needed more firepower. The kind of serious, patient, whale-sized capital that could transform a promising regional startup into a genuine continental challenger. That capital arrived from an unexpected direction: the world of oil tankers.

IV. The Geveran Factor: Shipping Magnates and Debt

John Fredriksen does not make polite investments. The Norwegian-born, Cypriot-domiciled shipping magnate — consistently ranked as Norway's wealthiest individual — has built his fortune through a playbook that is elegant in its simplicity and brutal in its execution: find capital-intensive, cyclical industries; invest aggressively when assets are cheap and others are panicking; use leverage to amplify returns; operate at the lowest possible cost; and hold through the cycle until values recover. He has applied this formula to oil tankers (Frontline), offshore drilling (Seadrill), dry bulk shipping (Golden Ocean), fish farming (Mowi), and real estate. In 2017, he turned his gaze toward European distressed debt.

Geveran Trading Co. Limited — the investment vehicle controlled by trusts established for the benefit of Fredriksen's immediate family — made its first significant move in August 2017. The structure of the initial deal revealed exactly how Fredriksen thinks about capital deployment. Rather than simply buying shares on the open market, Geveran and Axactor established a jointly owned portfolio investment company, Axactor Invest 1, domiciled in Luxembourg. Each side contributed €30 million in equity. Geveran then layered on a €120 million subordinated debt facility at 650 basis points over EURIBOR with a five-year maturity. Combined with €120 million in bank financing, the vehicle had roughly €300 million in total investment capacity. Axactor would provide exclusive collection services at a 5 percent markup over cost, and Geveran received 130 million warrants exercisable at NOK 3.25.

This was vintage Fredriksen: debt-funded, structurally creative, with multiple ways to win. He was earning a healthy coupon on the subordinated debt, gaining equity upside through warrants, and outsourcing the operational grunt work to a team he believed could execute. The arrangement gave Axactor something it desperately needed — the ability to bid on portfolios large enough to matter, backed by a name that European banks recognized and trusted as a counterparty.

Through late 2017, Geveran acquired over 173 million Axactor shares at roughly NOK 2.65 each, reaching an 11.5 percent ownership stake. By May 2018, further purchases brought the position to 186 million shares and just over 12 percent. But the relationship deepened dramatically in December 2020, when Axactor acquired Geveran's 50 percent stake in the Axactor Invest 1 vehicle in exchange for 50 million newly issued shares. The book value of Geveran's equity interest in the vehicle was approximately €55 million, but the transaction's purpose was structural simplification — bringing all portfolio assets under one roof. The share issuance catapulted Geveran's ownership from roughly 33 percent to 44.3 percent, triggering the mandatory offer threshold under Norwegian securities law.

In January 2021, Geveran launched the required mandatory bid at NOK 8.00 per share. Few shareholders tendered. The price offered no premium to the prevailing market, and Geveran showed no inclination to sweeten it. The message to the market was unambiguous: this was a legal formality, not a hostile takeover. Fredriksen was in for the long haul.

The Geveran factor matters beyond the capital itself. When Axactor negotiates portfolio purchases with major European banks, the implicit backing of Fredriksen's empire provides a counterparty credibility that smaller competitors cannot replicate. Banks selling hundreds of millions in NPLs need assurance that the buyer can close and has the staying power to manage a multi-year collection cycle. A 44 percent shareholder with a personal fortune measured in the tens of billions provides that assurance — not as a formal guarantee, but as a powerful signal.

The relationship also carries governance implications that not all minority shareholders love. Four of six Axactor board seats have historically been associated with the Geveran shareholder bloc. When strategic direction shifts, it shifts because Fredriksen's representatives want it to — a dynamic that became dramatically visible in the spring of 2020, when the founding CEO discovered that Fredriksen's patience had limits.

V. Management and The Pivot: The Johnny Tsolis Era

On April 2, 2020, three weeks into the COVID-19 lockdowns that were shutting courts and freezing collection activity across Europe, Endre Rangnes was released as CEO of Axactor with immediate effect. The timing seemed absurd. The world was in freefall. But the decision had been building for months.

Rangnes later told Dagens Naeringsliv, Norway's premier business daily, that the move was orchestrated by Fredriksen's board representatives, noting that "four of six board members were elected by one shareholder" and that the decision was made within 24 hours. The grounds were disputed, but the direction was not. Chairman Glen Ole Rodland — closely associated with the Geveran bloc — framed the transition with clinical precision: "The company has historically been focusing on growth. We are now entering a new phase where return on capital, profitable growth, and returning cash to shareholders will be key priorities."

Johnny Tsolis, who had been serving as EVP of Strategy and Projects and had earlier held the CFO role, was appointed acting CEO the same day. He was confirmed as permanent CEO on June 26, 2020. His first public statement set the new tone: "Profitability, return on capital, and value creation for all stakeholders will be my top priority for the years to come."

If Rangnes was the dealmaker — charismatic, externally focused, instinctively aggressive — Tsolis was the accountant's accountant. Quiet, analytical, more comfortable dissecting a discounted cash flow model than giving a keynote. His background was in investment banking and corporate finance, not in operations or sales. This was precisely what Axactor needed at that moment. The company had built the platform. It had entered the markets. It had assembled the portfolio. What it had not done was prove that the economics actually worked at scale.

Tsolis rebuilt the management team, bringing in Nina Mortensen as CFO, Arnt Andre Dullum as COO, Karl Mamelund as CIO, and Kyrre Svae as Deputy CEO and Chief Strategy Officer. More importantly, he rewired the incentive structure. Under the founding team, compensation had leaned heavily on stock options — instruments that rewarded share price appreciation regardless of underlying profitability. Tsolis shifted the framework to targets anchored in return on equity and cost-to-collect ratios. The difference in philosophy was stark: options reward optimism, ROE targets reward efficiency.

The cultural rebranding was equally deliberate. Tsolis stopped calling Axactor a "collection agency" and started calling it a "FinTech data factory." This was not mere corporate wordsmithing. It reflected a genuine shift in how the company operated. Under Tsolis, Axactor deepened its investment in its proprietary pricing engine — the data model that segments every individual debtor by likelihood to pay, optimal contact channel, and most effective payment plan structure. Think of it as a recommendation engine, like the ones Netflix uses to suggest movies, except instead of predicting whether you will watch a thriller, it predicts whether a plumber in Milan will repay €500 over the next three years, and what sequence of text messages, phone calls, and payment plan offers will maximize the probability of that happening.

The company also partnered with Neonomics, a Norwegian open banking platform, to become the first European debt collector to offer account-to-account payments via open banking. In practice, this means a debtor can receive a digital invoice, view their balance, and make a same-day payment or schedule installments through their phone — no call center interaction required. It sounds incremental, but in an industry where every percentage point of collection efficiency drops straight to the bottom line, these digital touchpoints compound into significant economic advantages.

The results showed up in the numbers. Fiscal year 2025 delivered revenue of approximately €260 million, net income of €36 million, and an all-time-high adjusted return on equity of 12 percent, with the fourth quarter annualizing at 14 percent. Collection performance on the NPL portfolio hit 102 percent of forecast for the full year, reaching 106 percent in the fourth quarter — meaning the company collected more than its models had predicted. For a business where the models are everything, this is the most powerful proof of operational capability.

The contrast with the Rangnes era is instructive for anyone thinking about the lifecycle of founder-led companies. Rangnes built the vehicle. Tsolis made it fuel-efficient. The open question is whether Tsolis can now step on the accelerator without losing the discipline that defined his first five years — a question that the next European credit cycle will answer.

VI. Segment Deep Dive: The Hidden Flywheels

Understanding how Axactor actually makes money requires grasping three business segments that operate on fundamentally different economic logic. The interplay between them is where the strategic insight lies.

The first and largest segment is NPL, or Non-Performing Loan purchasing. Imagine you are a Spanish bank holding a bundle of 10,000 consumer loans where the borrowers stopped paying more than 90 days ago. You cannot make new loans because regulators force you to hold capital against the bad ones. You want them gone. Axactor shows up and offers to buy the entire bundle for, say, five cents per euro of face value — meaning a portfolio with €100 million in outstanding balances might sell for €5 million. Axactor now owns the legal right to collect whatever it can from those 10,000 individuals. If it ultimately recovers €9 million over five years while spending €3 million on collection costs, the profit is €1 million on the original €5 million investment — a decent return, but one that requires patience, precision, and significant upfront capital.

The art lies entirely in pricing. Axactor's proprietary model analyzes each loan using dozens of variables — debtor income, employment status, payment history, geographic location, type of debt, legal jurisdiction — to predict total expected collections and their timing. If the model says "this portfolio will generate €9 million over five years" and the seller is asking €5 million, the deal works. If the seller asks €7.5 million, it does not. The discipline to walk away from overpriced portfolios is what separates the survivors from the casualties in this industry.

As of early 2026, Axactor manages approximately €16.5 billion in total face value debt across 964,000 individual claims, with estimated remaining collections of about €2.5 billion. The contribution margin on NPL runs between 74 and 77 percent, meaning for every euro collected, roughly three-quarters flows through after direct collection costs. However, this is inherently capital-intensive: every portfolio must be purchased upfront, funded through a combination of equity, bank credit facilities, and bonds.

The second segment — and the one that gets analysts most excited — is 3PC, or Third-Party Collection. In this business, Axactor does not buy the debt at all. Instead, it collects on behalf of the original creditor, who retains ownership, and earns a commission for every euro recovered. Think of the difference between buying a rental property (NPL) and managing one for someone else (3PC). The economics are entirely different: 3PC requires no balance sheet commitment, no funding cost, and no portfolio risk. It is pure fee income.

This segment grew 19 percent organically in fiscal year 2025, with Spain accounting for roughly 60 percent of revenue and double-digit growth also recorded in Norway and Germany. The contribution margin reached 48 percent in the fourth quarter, up from 44 percent in the prior year. While the percentage margin is lower than NPL's, the return on capital is theoretically infinite because the capital invested is zero. No debt is purchased. No funding is required. Every euro of 3PC profit is earned on someone else's balance sheet.

3PC also functions as a strategic feeder for the NPL business. When Axactor collects well on behalf of a bank's delinquent portfolio, it demonstrates operational capability with hard data. That demonstrated competence opens doors to NPL portfolio purchases down the line. The bank has seen, with real numbers, what Axactor can recover. It is the world's most boring and effective form of customer acquisition.

The third segment is REO, Real Estate Owned, concentrated almost entirely in Spain. When secured loans backed by real estate default and the collateral is seized through legal proceedings, someone has to manage, maintain, and eventually sell the physical properties. Axactor holds two significant REO portfolios: roughly 1,500 assets with an appraisal value around €102 million from a large Spanish financial group, and a 75 percent stake in two special purpose vehicles holding over 4,060 REO assets with combined appraisal values exceeding €228 million.

REO is the least loved part of Axactor's business, and for good reason. Selling repossessed Spanish apartments is slow, illiquid, and operationally messy. Properties need insurance, maintenance, marketing, and patient negotiation with bargain-hunting buyers. Management has placed this segment in run-off mode, meaning they are selling down existing inventory rather than adding new properties. In late 2024, the company completed an €83 million portfolio sale in Spain at a 2 percent premium to book value, demonstrating that the assets can be monetized at or above carrying values.

The trajectory of the segment mix tells the story of Axactor's strategic evolution. Under the founders, NPL purchasing consumed nearly all management attention and capital. Under Tsolis, the emphasis has shifted toward growing 3PC as a percentage of the overall business — because it generates returns without consuming capital — while winding down REO. The ideal Axactor of the future is one where 3PC provides a growing, predictable, high-margin base of fee income, and NPL investment is deployed selectively only when pricing meets strict hurdle rates.

VII. The Playbook: Lessons in Capital Allocation

In the debt purchasing industry, the single most important competitive variable is not collection technology or market access or team quality, though all of those matter. It is the cost of capital. When your raw material is money — you borrow money to buy debt to collect money — the price at which you borrow determines everything.

Consider the math. Axactor buys a portfolio for €80 million and expects to collect €120 million over five years. If funding costs are 4 percent, the spread between collection yield and funding expense is healthy. When European rates spiked in 2022 and 2023, funding costs for many industry players doubled or tripled. The same portfolio that was profitable at 4 percent funding became marginal or money-losing at 8 percent. This is the single biggest risk in the business, and it is the risk that destroyed Axactor's largest competitor.

Axactor's primary banking relationships are with DNB and Nordea, the two largest financial institutions in the Nordic region. The company's revolving credit facility — €545 million, refinanced in 2025 with a three-year maturity plus a two-year extension option — provides the backbone of its funding structure. In June 2025, Axactor placed a €125 million bond at EURIBOR plus 750 basis points, roughly three percentage points tighter than its previous bond issuance. That improvement in pricing reflected both operational improvement and the credit market's recognition that Geveran's 44 percent backing provides an implicit layer of support.

A boutique debt purchaser funding itself through private credit or junior high-yield bonds will pay meaningfully more for capital. That cost difference flows directly through to portfolio returns, and it compounds over time across dozens of portfolio purchases. It is the kind of structural advantage that Hamilton Helmer would recognize as a barrier to entry — not impossible to surmount, but expensive enough that it effectively limits the competitive field.

The most instructive contrast is with Intrum. The Swedish giant pursued aggressive growth through the late 2010s, deploying billions in portfolio purchases funded largely with debt. When rates rose sharply, Intrum's annual interest expenses ballooned from roughly $180 million to over $300 million. The debt load became unsustainable. In November 2024, Intrum filed for Chapter 11 bankruptcy protection in a Texas court to restructure between $4.5 and $5.3 billion in obligations. The plan was confirmed on December 31, 2024, and Intrum emerged in mid-2025, but with a severely weakened balance sheet and minimal capacity for new investment.

Axactor avoided this fate not through superior foresight about interest rates — nobody predicted the speed and magnitude of the 2022-2023 hiking cycle — but through a fundamentally different capital allocation philosophy after 2020. Under Tsolis, the company prioritized deleveraging. Total debt peaked at €953 million in 2022 and was reduced to €843 million by the end of 2025. NPL investment in 2025 was deliberately held to just €59 million, far below the company's capacity, because the pricing in the market did not meet Tsolis's return hurdles. The discipline to sit on your hands while competitors chase volume is the hardest skill in investing, and it proved to be the most valuable one.

A tool worth understanding in Axactor's arsenal is the forward flow agreement. Rather than competing in one-off portfolio auctions where aggressive bidders drive up prices, Axactor has locked in long-term contracts with banks like Monobank and Instabank, under which the bank commits to selling a steady stream of newly generated NPLs to Axactor at pre-negotiated terms. These agreements — covering estimated annual volumes of €15-25 million — provide earnings visibility, reduce acquisition costs, and deepen the banking relationships that are the bedrock of the entire business. Forward flows are the debt-purchasing equivalent of a subscription model: less exciting than a blockbuster deal, but far more predictable.

VIII. Analysis: 7 Powers and 5 Forces

Strip away the jargon about NPLs and collection curves, and the fundamental question about Axactor is the same question that applies to any business: does it have a durable competitive advantage, or is it simply riding a cyclical wave that any reasonably competent operator could exploit?

Start with Hamilton Helmer's 7 Powers framework, which identifies the sources of persistent competitive advantage.

The primary power Axactor possesses is scale economies. The fixed cost of building and maintaining the data platform, the legal and regulatory infrastructure across six jurisdictions, the jurisdiction-specific collection "recipes," and the relationships with major banks must be incurred whether the company manages €5 billion or €20 billion in face value debt. As the portfolio grows, these fixed costs are spread across a larger base, reducing the cost per euro collected. A boutique operator managing €500 million in debt must absorb similar platform costs with a fraction of the volume, making its unit economics structurally inferior. This is the classic fixed-cost-spreading mechanism that creates durable advantages in any industry with high upfront investment and low marginal costs.

The second relevant power is process power — what Helmer defines as organization-embedded capabilities developed through sustained experience that competitors cannot easily replicate. Axactor's collection "recipes" — the jurisdiction-specific sequences of digital contact, phone calls, negotiation tactics, payment plan structures, and legal actions — represent knowledge accumulated through years of trial and error across six different European legal systems. Collecting from a self-employed tradesman in Naples requires a different playbook than collecting from a salaried office worker in Oslo or a retired pensioner in Seville. The optimal contact timing, communication tone, payment structure, and legal remedy all vary by country, debtor type, and debt category. This knowledge is embedded in Axactor's data models and cannot be acquired by hiring a few data scientists.

Now layer on Porter's Five Forces for the broader industry picture.

Bargaining power of suppliers — meaning banks — is the most dynamic force in this market. Banks are the sellers of NPL portfolios, and their leverage depends on regulatory pressure, macroeconomic conditions, and the number of buyers competing at each auction. When regulatory pressure is high and many banks are forced to sell simultaneously, buyer power increases and portfolio prices decline. When pressure eases, banks can hold and wait, driving up prices. The EU NPL Directive, adopted in 2021 with a December 2023 transposition deadline, created a harmonized licensing and passporting framework for credit servicers across the EU. Over time, this directive is expected to expand cross-border NPL transactions, growing the addressable market for authorized pan-European servicers like Axactor. Forward flow agreements are the strategic response to supplier power — by locking in supply at negotiated terms, Axactor reduces its dependence on the volatile spot market.

Competitive rivalry has been dramatically reshaped by the interest rate cycle. During the low-rate era from 2015 to 2021, cheap funding attracted aggressive capital deployment from listed players and private equity alike, compressing returns industry-wide. The 2022-2024 rate shock reversed this dynamic violently. Intrum's Chapter 11 was the most spectacular casualty, but several PE funds — Cerberus, Blackstone, Fortress — also scaled back European NPL exposure as returns fell below hurdle rates. For survivors, reduced competition at auctions means better pricing, and distressed competitors selling assets create buying opportunities.

Threat of new entrants is moderate. Regulatory licensing under the EU NPL Directive creates barriers, but the true deterrent is the multi-year, multi-million-euro investment required to build operational capability and banking relationships across jurisdictions. Threat of substitutes is low: banks have limited alternatives to NPL sales, as internal restructuring is expensive, slow, and capital-intensive. Buyer power — the power of debtors — is limited by the legal framework: debts are legally owed, and the question is not whether they will be pursued but how effectively.

Among listed peers, KRUK of Poland stands out as the most formidable competitor, reporting roughly 21 percent return on equity in 2024 with strong Central and Eastern European positioning. Hoist Finance in Sweden benefits from a banking license that gives it access to cheaper deposit funding, reporting 17 percent ROE. B2 Impact, Axactor's closest Norwegian peer with similar Southern European exposure, is the most direct comparable but lacks the Fredriksen-backed funding advantage. Axactor's 12 percent adjusted ROE in 2025 is competitive but still trails the top performers, and closing that gap is the central challenge of the next strategic phase.

IX. The Bull vs. Bear Case

The bear case against Axactor begins where most bear cases in financial services begin: with regulation. Debt collection is politically sensitive in every European jurisdiction. Consumer protection rules have steadily tightened around how, when, and how aggressively collectors can pursue debtors. Spain has expanded debtor protections. Italian court backlogs create unpredictable recovery timelines. Any significant regulatory crackdown on digital collection methods — the automated text messages, the algorithmically optimized contact sequences that form the backbone of Axactor's efficiency advantage — could compress margins and reduce collection performance in ways that are hard to model in advance.

Funding risk remains genuine. Axactor's leverage ratio stood at 3.6 times at the end of 2025, slightly above management's self-imposed maximum of 3.5 times. The direction of travel is positive — down from 4.0 times at the start of 2024 — but the company remains dependent on continued access to bank credit and bond markets at reasonable terms. The 750-basis-point spread on the June 2025 bond means Axactor pays over 10 percent all-in when including the EURIBOR base rate, leaving limited margin for error if collection performance disappoints or rates rise further.

The accounting judgment issue deserves a footnote. The carrying value of NPL portfolios on Axactor's balance sheet is based on management's estimate of future cash collections — a projection that requires assumptions about debtor behavior, legal outcomes, and macroeconomic conditions stretching years into the future. When those estimates are revised downward, the impact on reported earnings is immediate and severe. This happened in the fourth quarter of 2024, when a €104 million downward revaluation of collection curves produced a full-year net loss of €79.5 million, erasing what had otherwise been a strong operational year (cash EBITDA was up 35 percent). These revaluation swings are inherent to the business model and make quarterly earnings inherently lumpy.

The REO overhang in Spain, while being actively managed, remains a source of balance sheet risk tied to the Spanish property market, which is beyond management's control.

Then there is the Geveran concentration itself. With one shareholder holding 44 percent, minority investors are structurally subordinate. The abrupt firing of the founding CEO in 2020 demonstrated that Geveran has both the willingness and the board control to intervene decisively. Geveran's interests — long-term, Fredriksen-style, focused on asset value rather than quarterly earnings — may not always align with those of shorter-duration public shareholders, particularly on questions of dividends (none are currently paid) and capital returns.

The bull case rests on three converging structural tailwinds.

First, NPL supply is expected to increase. The pandemic-era stimulus programs that kept European delinquencies artificially suppressed have expired. Stage 2 loans — the precursor category just above non-performing status that serves as a leading indicator of future defaults — were running at 9.5 percent of total European bank lending as of early 2025, an elevated level. As economic normalization continues and forbearance measures fade, banks will have more bad debt to sell. Axactor has spent two years building capacity and deleveraging specifically for this moment.

Second, the competitive field has thinned dramatically in Axactor's favor. Intrum's post-Chapter-11 balance sheet limits its capacity for new investment. Several private equity players have retreated from European NPLs. The number of well-capitalized, operationally ready buyers at portfolio auctions has contracted, which should translate into better pricing and more attractive return profiles on new investments.

Third, the 3PC segment provides a growth engine decoupled from the credit cycle and funding markets. As European banks increasingly outsource early-stage collection to specialized third parties, the addressable market for these services is expanding. Axactor's 19 percent organic growth in 2025, combined with margin expansion from 44 to 48 percent, suggests the company is gaining share in a growing market with no balance sheet risk.

The "hidden upside" is the potential for a re-rating of how the market values the business. As of early April 2026, Axactor trades at roughly NOK 2 billion in market capitalization — approximately €185 million — against book equity of €368 million. The market prices the shares at roughly half of book value, a valuation typical of a financial company with below-average returns and above-average risk. If Axactor can sustain mid-teens ROE and demonstrate that the 3PC platform is a scalable, recurring, data-driven business with SaaS-like characteristics, the market may begin to assign a higher multiple. The re-rating from "collection agency" to "data platform" is aspirational, but it requires multiple years of consistent execution to become credible.

For investors tracking Axactor's performance, two KPIs matter above all others. The first is return on equity, which captures the profitability of the entire business relative to the capital base and is management's own primary metric, with a stated minimum target of 12 percent. The trajectory of ROE over coming quarters will reveal whether the Tsolis pivot has built a durable earnings engine or merely optimized a single cycle. The second is collection performance versus forecast on the NPL portfolio — the ratio that measures actual cash collected against the model's predictions. This ratio is the operational heartbeat of the business. When it runs consistently above 100 percent, as it did at 102 percent for full-year 2025 and 106 percent in the fourth quarter, it means the data engine is working, the collection recipes are effective, and the portfolio was priced conservatively. When it dips below 100, something is breaking — in the models, the market, or the operational execution.

X. Epilogue

A decade ago, Axactor was a nickel mining shell with no employees, no revenue, and a project in northern Sweden that had produced nothing of value. Today, it manages €16.5 billion in face value debt across six European countries, employs over a thousand people, and has survived a pandemic, a rate shock, and the near-destruction of its largest competitor. It has been through a founding CEO's ouster, a dominant shareholder's intervention, a strategic pivot from growth to efficiency, and a fourth-quarter revaluation charge that wiped out a year of profits.

The narrative arc is not a smooth upward line. It is the messy, iterative, sometimes painful story of a company learning what it wants to be. The founding team built the platform and entered the markets. The dominant shareholder imposed discipline when the founders would not. The new CEO made the operation efficient. And the credit cycle, that merciless arbiter of financial services businesses, sorted the disciplined from the reckless.

Whether Axactor can now execute the next phase — scaling NPL investment back up to €100-200 million annually while maintaining operational discipline, growing 3PC to reduce capital intensity, and winding down the REO drag — will determine whether the company becomes a permanent fixture of the European financial landscape or another cautionary tale in an industry that has produced many.

In the casino of global finance, someone has to collect the rake on everyone's bad bets. Axactor has spent a decade learning how to be that someone.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube