Accenture: From Andersen's Ashes to AI's Apex

I. Introduction & Opening Hook

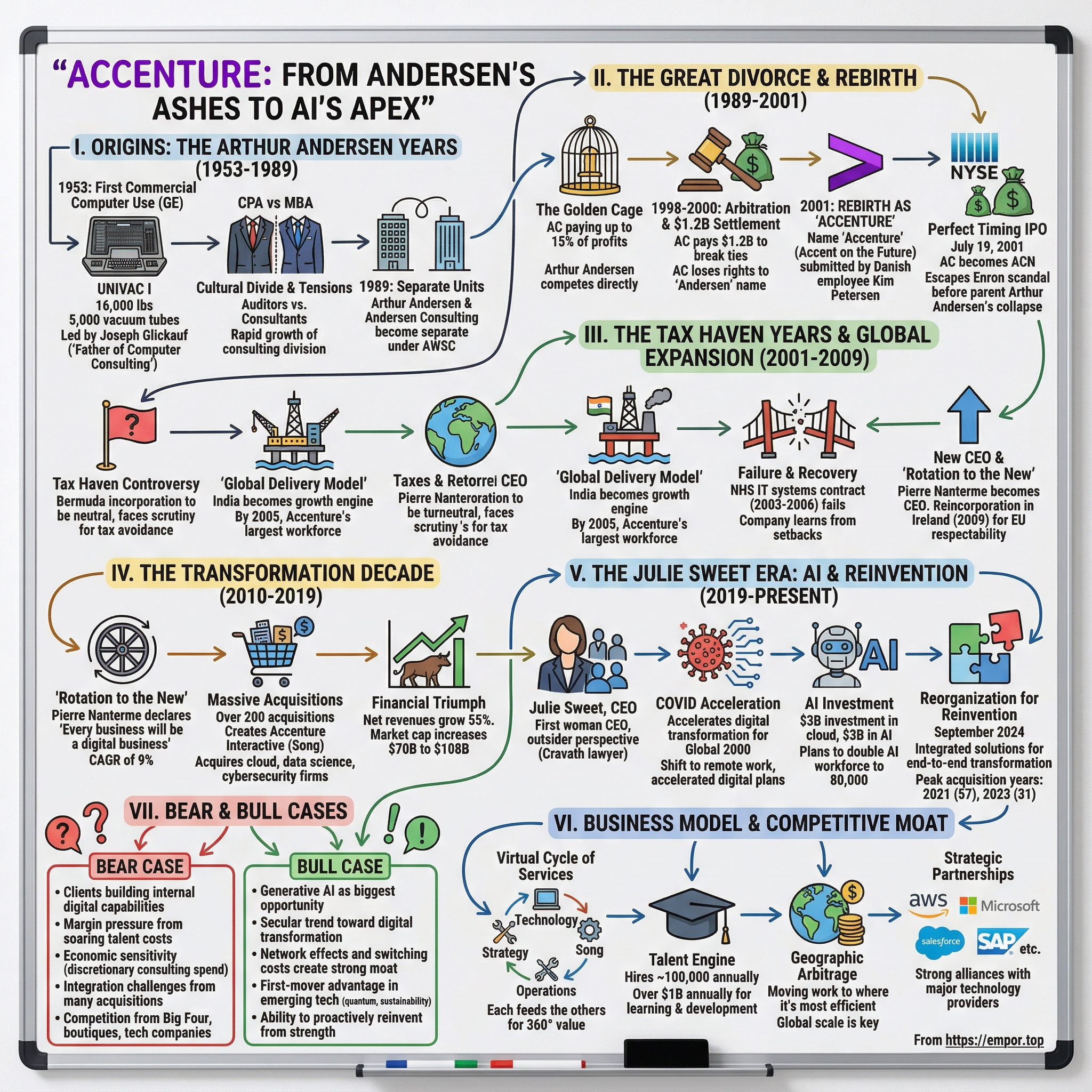

Picture this: July 19, 2001. The New York Stock Exchange buzzes with anticipation as a company with a strange, meaningless name—Accenture—begins trading. The shares open at $14.50, a respectable debut for the former Andersen Consulting. In the wings, Arthur Andersen executives watch with what must have been envy. Their former consulting division, which they'd fought tooth and nail to keep, had just escaped to freedom with perfect timing.

Ten months. That's all that separated Accenture's independence from catastrophe. By June 16, 2002, the U.S. Securities and Exchange Commission would prosecute Arthur Andersen for obstructing justice and accounting fraud around the Enron scandal. The parent company that had demanded $1.2 billion just to let its consulting arm go would soon collapse into rubble, taking 28,000 jobs with it.

Fast forward to today: Accenture reported revenues of $64.9 billion in 2024 with approximately 774,000 employees—a workforce larger than the population of San Francisco. The company generated total returns of approximately 370% between 2015 and 2024, outperforming the S&P 500 and Goldman Sachs. This isn't just a survival story. It's a masterclass in strategic timing, relentless reinvention, and the art of being boring in all the right ways.

The central question isn't how a consulting spinoff survived—it's how it became indispensable. How did a company that couldn't even keep the Andersen name transform into the world's largest professional services firm? And more importantly, what can the methodical rise of Accenture teach us about building enduring value in an era of constant disruption?

II. Origins: The Arthur Andersen Years (1953-1989)

The seeds of what would become Accenture were planted in 1953, in the most unlikely of places: a General Electric appliance factory in Louisville, Kentucky. Arthur Andersen conducted a feasibility study for General Electric to automate payroll processing and manufacturing at their Appliance Park facility, which led to GE's installation of a UNIVAC I computer and printer. This wasn't just any computer installation—it was believed to be the first commercial use of a computer in the United States.

The UNIVAC I was a beast of a machine. It weighed 16,000 pounds, used 5,000 vacuum tubes, and could perform about 1,000 calculations per second. GE became the first commercial buyer of the UNIVAC I in 1954, and Arthur Andersen's consulting division was there to shepherd this technological revolution. The consulting team helped design systems that could handle everything from payroll to inventory control—tasks that seem mundane today but were revolutionary in an era of punch cards and manual ledgers.

GE bought the UNIVAC I to automate payroll, budget analysis, inventory control and other tasks at its appliance division, but underestimated the complexity of integrating the system, and reports of GE's problems gave other potential customers the jitters. Yet Arthur Andersen's consultants persevered, learning from each setback. This early struggle with technology integration would become the foundation of a consulting practice that understood not just the promise of technology, but its pitfalls.

Joseph Glickauf, who led the GE project, would later be recognized as the father of computer consulting. Under his guidance, Arthur Andersen's technology consulting practice grew from a small team of accountants who understood computers into a formidable division. By the 1960s and 1970s, they were helping Fortune 500 companies navigate the transition from mainframes to minicomputers, from batch processing to real-time systems.

But success bred tension. The consulting division was growing faster than the audit practice, generating higher margins, and attracting a different breed of professional—MBAs and computer scientists rather than CPAs. The cultural divide was palpable. Auditors in conservative suits viewed their consulting colleagues with suspicion, while consultants chafed at being controlled by what they saw as a hidebound accounting culture.

In 1989, Arthur Andersen and Andersen Consulting became separate units of Andersen Worldwide Société Coopérative (AWSC), a Swiss coordinating entity. This wasn't a divorce—not yet. It was more like separate bedrooms in an unhappy marriage. Throughout the 1990s, tensions grew between the two units, with Andersen Consulting paying Arthur Andersen up to 15% of its profits each year while Arthur Andersen competed directly through its own newly established business consulting service.

The irony was rich: the consulting division had to pay tribute to its parent while that same parent was setting up a rival consulting practice. It was a recipe for war, and war is exactly what they got.

III. The Great Divorce & Rebirth (1989-2001)

The 1990s began with Andersen Consulting trapped in a golden cage. Business was booming—revenues were growing at over 20% annually through the mid-1990s—but the division was hemorrhaging talent and cash to its parent company. The dispute came to a head in 1998, when Andersen Consulting put the 15% transfer payment into escrow and issued a claim for breach of contract, leading to arbitration that concluded in 2000 with Andersen Consulting paying $1.2 billion to Arthur Andersen to break all contractual ties.

The arbitration was brutal. Both sides hired armies of lawyers and presented thousands of pages of evidence. At stake wasn't just money, but the future of both organizations. In 2000, an arbitrator granted Andersen Consulting complete independence from Arthur Andersen, but the consulting unit paid a $1.2 billion settlement and crucially lost the rights to the Andersen name.

Losing the name was supposed to be a catastrophe. Andersen Consulting had spent decades building brand recognition. Now they needed a new identity, fast. The company launched a global brainstorming exercise, receiving 2,677 suggestions from employees worldwide. The winner came from an unlikely source: Kim Petersen, a Danish employee from the company's Oslo, Norway office, submitted "Accenture," derived from "Accent on the future".

Petersen hoped that the name would not be offensive in any country in which Accenture operates, because the word itself was meaningless. It was a blank slate—no baggage, no history, no associations. Critics mocked it as corporate gibberish, but that meaninglessness would prove to be its greatest strength.

On January 1, 2001, Andersen Consulting adopted the name "Accenture". Six months later came the IPO. The company issued an estimated pricing of $13 to $15 a share, with the offering including 132.2 million shares, making it worth about $1.8 billion and one of the biggest IPOs of the year.

The timing couldn't have been more fortunate—or more narrow. Just months after Accenture's IPO, the Enron scandal exploded into public view. Arthur Andersen collapsed by mid-2002, as details of its questionable accounting practices for Enron were revealed, with the firm found to have fraudulently reported $100 billion in revenue through systematic accounting fraud.

Accenture's new meaningless name suddenly looked like genius. There was no "Andersen" to connect them to the scandal. While Arthur Andersen's 28,000 employees lost their jobs and the Big Five became the Big Four, Accenture sailed on, unscathed. They had paid $1.2 billion for their freedom. In retrospect, it was the bargain of the century.

IV. The Tax Haven Years & Global Expansion (2001-2009)

Accenture was incorporated in Bermuda in 2001, a decision that would shadow the company through its first decade of independence. In October 2002, the Congressional General Accounting Office identified Accenture as one of four publicly traded federal contractors incorporated in a tax haven, though unlike the other three, Accenture had not been incorporated in the United States before moving offshore, leading critics like Lou Dobbs to accuse the company of tax avoidance.

The Bermuda incorporation wasn't just about taxes—it was about neutrality. Accenture served clients in over 100 countries. Being nominally based in Bermuda meant they weren't an "American" company competing in Europe or a "European" company competing in Asia. They were deliberately placeless, a global entity without a homeland.

But this strategy had costs. Government contracts came under scrutiny. Politicians grandstanded about "Benedict Arnold corporations." The company found itself defending its structure repeatedly, arguing that it had never been a U.S. company to begin with—it had emerged from a Swiss entity and chose Bermuda as a neutral ground.

Meanwhile, the real transformation was happening on the ground. Accenture was building what it called the "global delivery model"—a euphemism for moving work to wherever it could be done most efficiently. India became the engine of growth. By 2005, Accenture employed more people in India than in any other country, though this wouldn't be publicly acknowledged for years.

The company also stumbled into one of the great IT disasters of the decade. In 2003, Accenture won a contract to modernize the UK's National Health Service IT systems. By 2006, they were forced to withdraw, walking away from a contract amid delays and cost overruns. It was a humbling reminder that even the world's largest consulting firm could fail spectacularly when ambition exceeded capability.

Yet the company learned from its failures. William D. Green became CEO in September 2004 and was replaced by Pierre Nanterme in January 2011. Under Green's leadership, Accenture doubled down on what worked: large-scale outsourcing, systems integration, and the emerging cloud opportunity. They weren't trying to be innovative; they were trying to be indispensable.

On May 26, 2009, Accenture announced that its board unanimously approved changing the company's place of incorporation from Bermuda to Ireland. The move was partly about escaping the "tax haven" label, but mostly about positioning for the future. Ireland offered EU membership, a skilled workforce, and yes, favorable tax rates—but now wrapped in the respectability of being based in a "real" country.

V. The Transformation Decade (2010-2019)

Pierre Nanterme became chief executive officer in January 2011 and assumed the additional position of chairman of the board in February 2013. The French executive brought a different energy to Accenture—less American corporate, more European intellectual. He spoke in frameworks and mental models, constantly talking about "rotating to the new."

Nanterme inherited a solid but uninspiring business. Accenture was good at what it did—implementing SAP systems, running call centers, managing IT infrastructure—but none of it was particularly exciting. The company was like a utility: essential but invisible. Nanterme saw that the world was changing and Accenture needed to change with it.

The pivotal moment came in 2013. Nanterme declared that "every business would be a digital business." It sounds obvious now, but in 2013, many CEOs still thought of digital as a channel or a department, not a complete transformation of their business model. From 2013 to 2019, Accenture grew at a compound annual growth rate of 9%, driven by this digital-first strategy.

Since 2013, Accenture has acquired over 200 companies. But these weren't random shopping sprees. Each acquisition fit into a broader strategy of building new capabilities. The company bought design agencies to create Accenture Interactive (later renamed Accenture Song), making it one of the world's largest digital agencies. They acquired cloud specialists, data scientists, and cybersecurity firms.

Nanterme transformed Accenture and was instrumental in rotating its business to high-growth areas in digital, cloud and security-related services, which together came to account for more than 60 percent of Accenture's total revenues. This wasn't just adding new services; it was fundamentally changing what Accenture was. The company that had started by installing mainframes was now designing mobile apps and customer experiences.

The financial results were staggering. Accenture's net revenues grew 55 percent from $25.5 billion in fiscal 2011 to $39.6 billion in fiscal 2018, while the market cap increased approximately $70 billion to $108 billion, with a total return to shareholders of 309 percent.

But Nanterme's transformation came at a personal cost. Diagnosed with colorectal cancer in 2016, he died in Paris on January 31, 2019, at age 59, just twenty days after stepping down as CEO. His death marked the end of an era, but his vision of Accenture as a digital powerhouse would endure.

VI. The Julie Sweet Era: AI & Reinvention (2019-Present)

Accenture named Julie Sweet its CEO effective September 2019, the first woman to hold that position, replacing interim CEO David Rowland, and at the time of her appointment, she was one of 27 women leading companies in the S&P 500. Sweet's background was unconventional for a consulting CEO. She was an attorney at Cravath, Swaine & Moore for 17 years, working as partner for 10 years and becoming the ninth woman ever to make partner at the firm.

Since becoming CEO in September 2019, she's been the first woman to lead Accenture and the first CEO in the company's history who didn't start there straight out of college. This outsider perspective would prove crucial. Sweet didn't think like a consultant; she thought like a lawyer—systematically, strategically, always three moves ahead.

Her timing was either terrible or perfect, depending on your perspective. She became CEO in 2019, and put in place in March 2020 the next growth model, which was all about scaling digital transformation for the next decade. Then COVID hit. Suddenly, every company on Earth needed to transform digitally, not in five years but in five weeks.

Accenture's 774,000 employees shifted to remote work almost overnight. But instead of retreating, Sweet accelerated. She announced a $3 billion investment in cloud capabilities. The company hired aggressively while competitors froze. Under her leadership, Accenture launched a $3 billion AI investment plan to double its data and AI workforce to 80,000 specialists.

Under her leadership, the company's revenue has grown more than 50%. But the real transformation has been in what Accenture does. The company is no longer just implementing technology; it's reimagining entire businesses. When a bank needs to create a digital-only subsidiary, when a retailer needs to build a metaverse presence, when a manufacturer needs to embed AI into its production line—they call Accenture.

The acquisition pace has been breathtaking. Peak acquisition years included 2021 with 57 acquisitions and 2023 with 31. Each deal adds a specific capability: quantum computing experts, sustainability consultants, creative agencies. Sweet isn't building a consulting firm; she's assembling a transformation machine.

In September 2024, Sweet announced another reorganization, bringing together previously separate units to create integrated solutions. The old model of selling discrete services—a cloud migration here, a digital marketing campaign there—was dead. Clients wanted end-to-end transformation, and Accenture reorganized to deliver it.

The numbers tell the story: From the $14.50 IPO price in 2001 to a market capitalization approaching $200 billion today. From 75,000 employees to 774,000. From an IT services firm to what Sweet calls "the reinvention partner" for the Global 2000. It's a transformation that would make even Pierre Nanterme proud.

VII. The Business Model & Competitive Moat

Accenture's business model looks simple on paper but is nearly impossible to replicate. The company combines services across Strategy & Consulting, Technology, Operations, Industry X and Song, with a culture of shared success and commitment to creating 360° value. Each segment feeds the others in a virtuous cycle: strategy work leads to implementation, implementation requires operations support, operations generate data that inform new strategies.

The real moat isn't any single service—it's the combination at scale. When Walmart needs to compete with Amazon, they don't just need cloud migration or a mobile app or supply chain optimization. They need all of it, coordinated globally, delivered by teams that understand retail. Accenture can put 10,000 people on a client project, across 20 countries, combining expertise in everything from AI to warehouse automation.

The talent engine is equally formidable. Accenture hires roughly 100,000 people annually—more than most companies employ in total. They're not just hiring; they're training. The company invests over $1 billion annually in learning and development. Every employee averages 40 hours of training per year. It's a university disguised as a consulting firm.

Geographic arbitrage remains central to the model, though the company rarely discusses it explicitly. A consultant in New York might cost $500 per hour; the same work done by an equally skilled professional in Manila or Bangalore might cost $50. Accenture captures the difference while maintaining quality through rigorous processes and training.

Strategic partnerships provide a significant competitive advantage, with Accenture being a key partner of technology providers including Adobe, Amazon Web Services, Google, Microsoft, Oracle, Salesforce, SAP, ServiceNow and many others. These aren't just vendor relationships; they're deep partnerships where Accenture often has more certified professionals than the technology companies themselves.

The pyramid economics still work, but they've evolved. Instead of just leveraging junior consultants, Accenture now leverages automation, AI, and offshore delivery. A partner might oversee work that's 20% done by consultants, 30% by offshore teams, and 50% by automated tools. The margins expand even as prices fall.

Why hasn't consulting been killed by AI? Because someone needs to implement the AI, integrate it with existing systems, train the workforce, and transform the business processes. Every new technology that threatens consultants actually creates more consulting work. Accenture doesn't fight disruption; it sells disruption.

VIII. Power Dynamics & Strategic Lessons

The power dynamics in professional services are counterintuitive. Unlike software, where winner-takes-all dynamics prevail, consulting rewards breadth over depth. Accenture's power comes not from being the best at any one thing, but from being very good at everything.

Network effects operate differently here. Each new client makes Accenture more valuable to other clients. When Accenture implements a supply chain system for Procter & Gamble, they learn lessons they can apply at Unilever—without violating confidentiality. The knowledge accumulates, compounds, and creates a widening moat.

The platform shift has been subtle but profound. Accenture no longer just provides services; it provides a platform for transformation. This includes proprietary tools, methodologies, and increasingly, pre-built solutions that can be customized for each client. They're selling products disguised as services.

Capital allocation under Sweet has been aggressive but disciplined. The company returns cash to shareholders through dividends and buybacks while spending billions on acquisitions. The M&A strategy isn't about buying revenue; it's about buying capabilities that would take years to build organically. When AI became critical, Accenture didn't try to train thousands of AI experts from scratch—it bought companies that already had them.

The "leapfrog" strategy—moving into technologies before clients need them—requires patience and capital. Accenture invested in cloud capabilities years before most enterprises were ready for cloud migration. When COVID accelerated digital transformation by five years, Accenture was ready. They weren't predicting the future; they were preparing for multiple futures.

Building trust at the C-suite level is perhaps the most underappreciated aspect of Accenture's model. CEOs don't hire Accenture because they have the best technology or the lowest prices. They hire them because when a transformation goes wrong—and they often do—the CEO can tell the board they hired the industry leader. Nobody gets fired for hiring Accenture.

IX. Bear & Bull Cases

Bear Case:

The existential threat isn't AI replacing consultants—it's clients getting smart enough not to need consultants. As enterprises build internal digital capabilities, the need for external transformation partners could diminish. Why pay Accenture millions when you can hire your own digital talent?

Margin pressure is real and growing. Talent costs are soaring, especially for specialists in AI, cloud, and cybersecurity. Accenture is competing against tech companies that can offer stock options worth millions. The company's relatively staid compensation structure—good salaries but no lottery tickets—makes it harder to attract the best technical talent.

Economic sensitivity remains a vulnerability. Consulting spend is discretionary; when revenues fall, it's often the first budget cut. A global recession could see enterprises pulling back on transformation projects, no matter how strategic they claim to be.

Integration challenges multiply with each acquisition. Accenture has bought over 200 companies since 2013. Each brings different cultures, technologies, and ways of working. At some point, the integration machine could break down, leaving Accenture with an unwieldy collection of loosely connected businesses.

Competition is intensifying from every direction. The Big Four accounting firms are building consulting practices. Boutique firms are winning specialized work. Tech companies like Salesforce and Microsoft are building their own consulting arms. Even clients are building internal consulting capabilities. Accenture is fighting a multi-front war.

Bull Case:

Generative AI isn't a threat—it's the biggest opportunity in Accenture's history. Enterprises need help understanding, implementing, and scaling AI. Accenture has already generated billions in AI-related bookings. The company that helped enterprises navigate mainframes, PCs, the internet, mobile, and cloud is perfectly positioned for the AI transformation.

The secular trend toward digital transformation is unstoppable. Every company needs to become a technology company. Most lack the capabilities to transform themselves. They need a partner with scale, expertise, and global reach. Accenture is often the only realistic option.

Network effects and switching costs create a powerful moat. Once Accenture is embedded in an enterprise—running their SAP systems, managing their cloud infrastructure, handling their customer service—it's incredibly difficult to switch. The cost and risk of changing providers often exceeds any potential savings.

First-mover advantage in emerging technologies keeps compounding. Accenture's investments in quantum computing, metaverse capabilities, and sustainable technology position it for the next waves of enterprise transformation. They're not betting on which technology will win; they're betting that enterprises will need help with whatever wins.

The ability to reinvent from a position of strength is perhaps Accenture's greatest asset. The company transformed itself from mainframe installer to digital powerhouse without ever having a near-death experience. This proactive evolution, rather than reactive survival, suggests a management culture that can navigate whatever comes next.

X. Lessons & Takeaways

The power of strategic timing cannot be overstated. Accenture's history is a series of perfectly timed moves: splitting from Arthur Andersen just before Enron, going public just before the scandal, moving to Ireland before tax inversions became politically toxic, investing in digital before it was obvious, and pivoting to AI before the ChatGPT explosion.

Cultural transformation while maintaining core values is possible but difficult. Accenture changed almost everything about itself—its name, headquarters, services, even its fundamental business model—while maintaining the consulting culture of client service, analytical rigor, and professional development. The company Pierre Nanterme led looked nothing like the one he joined, yet it was recognizably the same organization.

The acquisition integration playbook is now a core competency. Most companies struggle to integrate one or two acquisitions annually. Accenture integrated 57 in 2021 alone. They've industrialized the process: standard integration templates, dedicated integration teams, and clear metrics for success. They don't buy companies; they absorb capabilities.

Building a learning organization at scale requires massive investment but pays massive dividends. Accenture's training budget exceeds the revenue of many mid-sized consulting firms. But this investment creates a workforce that can adapt to whatever technology or business model emerges next.

Being "boring" can be beautiful in business. Accenture doesn't make headlines like Tesla or Amazon. It doesn't have a celebrity CEO or a cult following. It just steadily, methodically helps large organizations transform themselves. The stock chart may not have moonshot moments, but it has something better: consistent, compounding returns.

The importance of reinventing from a position of strength is perhaps the most important lesson. Most companies transform only when facing existential threats. Accenture transformed while growing, while profitable, while winning. This proactive reinvention—what Nanterme called "rotating to the new"—is what separates enduring companies from those that merely survive.

In the end, Accenture's story isn't about consulting or technology or even transformation. It's about the power of patient capital, strategic thinking, and the courage to change before you have to. It's about building a business so essential that clients can't imagine operating without you. And it's about recognizing that in business, as in life, the most powerful position is often the one that appears the least powerful—the trusted advisor, the reliable partner, the boring company that makes everything else work.

From a contentious divorce worth $1.2 billion to a market capitalization approaching $200 billion, from 75,000 employees to 774,000, from mainframe installations to AI transformations—Accenture's journey proves that sometimes the best strategy is simply to be indispensable. The company that emerged from Arthur Andersen's ashes didn't just survive; it became the phoenix that helps other companies learn to fly.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube