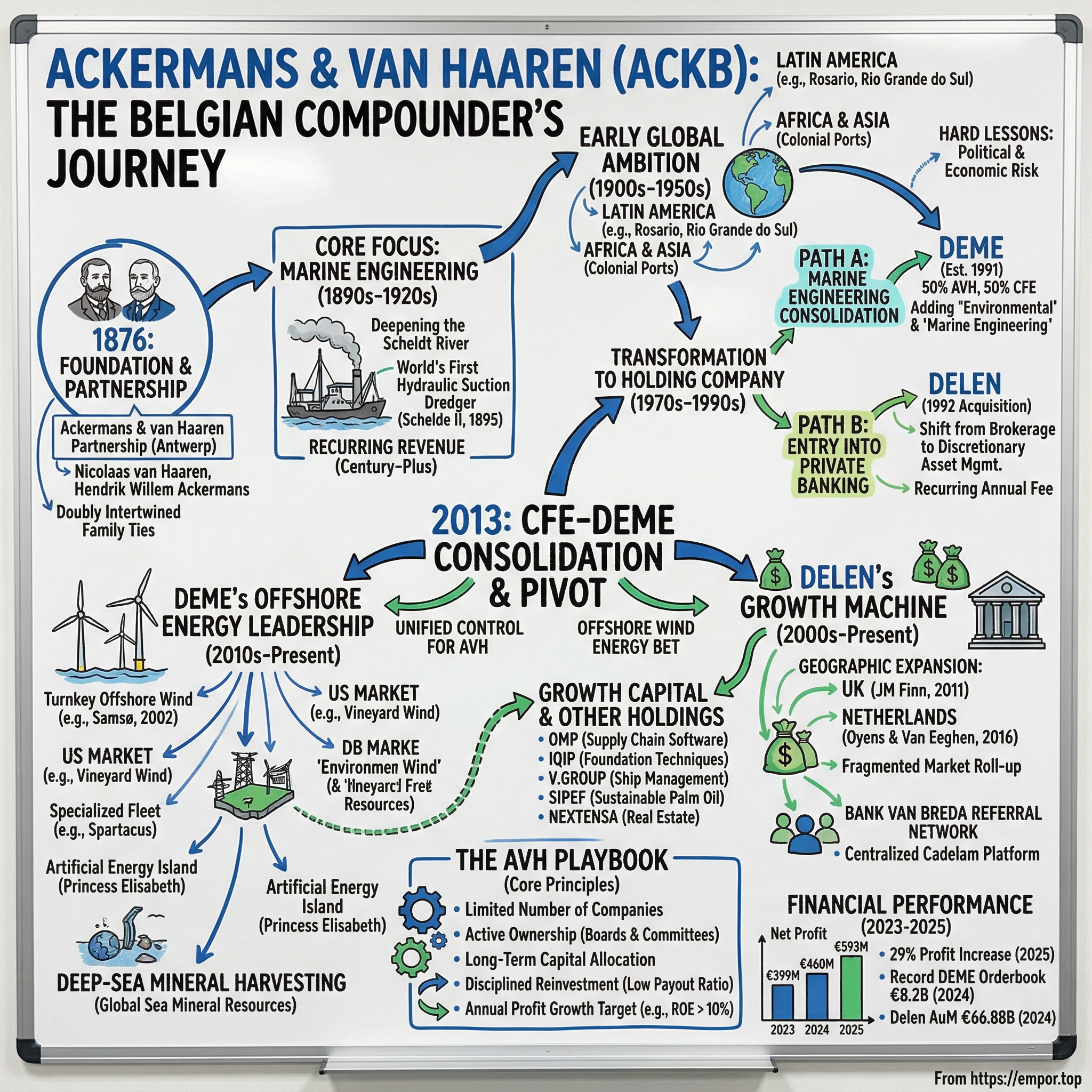

Ackermans & van Haaren: The Belgian Compounder Building Market Leaders

Forty-five kilometres off the coast of Ostend, in the grey-green swells of the Belgian North Sea, something extraordinary is taking shape. Massive concrete caissons, each weighing 22,000 tonnes — heavier than a fully loaded aircraft carrier — are being lowered onto the seabed to form the Princess Elisabeth Island, the world's first artificial energy island. The island will serve as an offshore electricity hub, bundling power cables from a vast new wind zone and transmitting 3.5 gigawatts of renewable energy to shore. The company building it has been working these same waters for more than a century. Back then, the task was dredging sand from the Western Scheldt so that coal-burning steamships could reach the Port of Antwerp. Today, the task is constructing the physical infrastructure of the energy transition. The company's name is DEME, and its majority owner is a 150-year-old Belgian holding company that most investors outside of Europe have never heard of.

In the annals of European business, a handful of holding companies have earned the rare distinction of compounding shareholder value across centuries, not merely decades. Berkshire Hathaway gets the headlines. Investor AB in Sweden has its admirers. But tucked away on Euronext Brussels, largely invisible to American investors, sits Ackermans & van Haaren — a diversified group that has quietly built one of Europe's most impressive track records of long-term wealth creation.

The numbers speak for themselves. In 2025, AvH posted a net profit of nearly €593 million, a 29 percent increase over the prior year. Its equity base reached €5.7 billion, delivering a return on equity above 10 percent — the group's own long-standing growth target. On a look-through basis, its portfolio companies generated €7.7 billion in annual turnover and employed nearly 25,000 people across 103 countries. The stock is a constituent of both the BEL20 index and the pan-European Stoxx 600, with a market capitalization hovering near €6.5 billion. And yet, outside of Belgium and a small circle of European value investors, almost nobody talks about it.

How did a 19th-century Dutch dredging partnership become Belgium's premier conglomerate, quietly compounding through marine engineering, private banking, and the energy transition? The answer is a story about patient capital, strategic reinvention, and an almost obsessive focus on owning a limited number of businesses with the potential to become market leaders. It is a story that touches on the strategic importance of the Scheldt estuary, the explosive growth of offshore wind energy, the art of private wealth management, and the surprisingly difficult question of how to run a holding company without destroying value.

The journey runs from dredging the Western Scheldt to installing turbines off the coast of Massachusetts, from a one-man brokerage in wartime Antwerp to managing nearly €67 billion in client assets, from colonial-era port construction in Africa to deep-sea mineral harvesting four and a half kilometres below the Pacific Ocean. Along the way, AvH has made a series of pivotal strategic decisions — some obvious only in retrospect — that transformed a family contracting business into a diversified industrial group with two world-class franchises: DEME, one of the largest dredging and offshore energy companies on the planet, and Delen Private Bank, one of Belgium's dominant independent wealth managers.

This is the story of how they did it — from the muddy banks of the Scheldt to the windswept waters of the North Atlantic, from a one-room brokerage in wartime Antwerp to the boardrooms of Europe's wealthiest families, and from a simple partnership between two Dutch families to a €6.5 billion holding company that has outlasted empires, survived two world wars, and reinvented itself for each new era.

From Dutch Contractors to Marine Engineers (1850–1920)

Picture the Dutch countryside in the 1860s. The province of Gelderland, flat and green, laced with rivers. In the small town of Kerkdriel, about eight kilometres north of 's-Hertogenbosch, a civil contractor named Nicolaas van Haaren was building a reputation that would echo across continents. Born in 1835, van Haaren was a man of bridges — literally. His defining early achievement was serving as lead contractor on the Culemborg railway bridge over the Lek River, completed in 1868. At 150 metres, it was the longest railway bridge in Europe at the time, notable as one of the first major structures built with what would later be defined as steel rather than wrought iron. The semi-parabolic arch design was ahead of its era. Van Haaren was not merely a builder; he was an engineer who understood that infrastructure at the frontier of technology commanded premium margins and created enduring reputations.

Twenty years younger and also from Kerkdriel, Hendrik Willem Ackermans was a different kind of figure. Born in 1855, he would live to the remarkable age of 89 or 90, his life spanning the entire arc from horse-drawn canal boats to powered suction dredgers. Later scholars would describe him as an "industrial pioneer," and his personal diaries — published posthumously under that title — reveal a restless, detail-oriented mind with an appetite for faraway places and large-scale projects. He was the kind of man who would, at age 48, board a ship to Argentina to personally supervise dredging operations in Rosario.

On January 1, 1876, these two men formalized their partnership in Antwerp. Van Haaren was forty, experienced and established. Ackermans was just twenty or twenty-one — astonishingly young for a business co-founder, but connected to van Haaren through something deeper than commerce.

The family ties were intricate: van Haaren's second wife was Elisabeth Maria Ackermans, Hendrik Willem's sister. And Hendrik Willem Ackermans himself married Elisabeth van Haaren, a daughter of Nicolaas from his first marriage. The two families were doubly intertwined by marriage, a common pattern in 19th-century Dutch business dynasties where trust was measured in bloodlines as much as balance sheets. This interweaving of family and business would prove remarkably durable — the partnership would survive both founders and endure across generations, a testament to the depth of the personal bonds that underpinned the commercial relationship.

Why Antwerp? The answer lies in one of the great geographic advantages of European commerce.

Antwerp sits roughly fifty to eighty kilometres inland from the North Sea on the right bank of the River Scheldt, at the crossing point of Europe's most important maritime route and its densest network of rivers, canals, and railroads. For centuries, it had been one of Europe's great trading cities — home to the first stock exchange in the modern sense, a centre of diamond trade, and a gateway between the Atlantic world and the European interior.

The port had suffered centuries of political misfortune — blocked by the Spanish in 1585, causing economic collapse and mass emigration — but the 1863 abolition of Dutch tolls on Scheldt navigation unlocked its modern potential. Belgium was the first continental European country to industrialize, and by 1876, Antwerp was the critical gateway for raw materials flowing in and manufactured goods flowing out. Larger steamships demanded deeper channels. The commercial logic was irresistible: whoever could deepen and maintain the Scheldt would control access to one of Europe's most important ports.

Between 1894 and 1911, Ackermans & van Haaren undertook what would become their signature project: deepening the Belgian and Dutch stretches of the Western Scheldt, removing approximately 25 million cubic metres of sediment. To put that in perspective, imagine excavating a canal ten metres deep, one hundred metres wide, and twenty-five kilometres long. The scale was enormous for the era, and the technology was evolving in real time. In 1895, the firm designed and built the Schelde II, the world's first hydraulic suction dredger capable of self-unloading. This was not a marginal improvement — it was a paradigm shift in dredging efficiency. Rather than relying on mechanical bucket chains and separate barges to haul away material, the new vessel could suck sediment from the riverbed and deposit it elsewhere under its own power. It was faster, cheaper, and more versatile than anything competitors could field.

The Scheldt deepening campaign coincided with the Port of Antwerp's massive expansion: quays straightened, five new docks added in the 1880s, eight docks completed by 1908. Ackermans & van Haaren was not merely a contractor executing someone else's vision. The firm was becoming a marine engineering company — designing vessels, innovating hydraulic techniques, and building the institutional knowledge that would compound across generations. Nicolaas van Haaren died in 1904, having seen his partnership grow from a small civil contracting operation into a maritime enterprise with international ambitions. Ackermans would carry on for another four decades, but the pattern was set: invest in proprietary technology, win projects that demand scale and expertise, and use each engagement to build capabilities for the next one.

There is something deeply revealing about the Scheldt deepening campaign that goes beyond the raw numbers. Consider the client relationship: the Belgian and Dutch governments needed the Scheldt kept navigable as ships grew larger with each passing decade. This was not a one-time project but an ongoing commitment — capital dredging followed by maintenance dredging, year after year, decade after decade. AvH signed up for the long game, and the Scheldt paid them back with a century-plus of recurring revenue. More than 130 years after Ackermans & van Haaren first dredged the Scheldt approaches, DEME companies remained the primary contractors for maintenance and capital dredging of the same waterway. In an era when businesses chase quarterly growth, there is something almost meditative about a revenue stream that spans three centuries.

The implications for long-term investors are fundamental. AvH's competitive moat traces directly back to these early decades. The dredging industry, then and now, rewards accumulated expertise and specialized assets. You cannot Google how to dredge a shipping channel through rock substrate at thirty metres depth. You cannot rent a cutter suction dredger on short notice. The knowledge is embodied in people, vessels, and institutional memory — exactly the kind of intangible assets that compound over time and resist competitive entry. The self-unloading suction dredger that AvH pioneered in 1895 was not merely an invention — it was the first move in a technology arms race that would continue for 130 years and culminate in machines like the Spartacus. Each generation of vessels was larger, more powerful, and more capable than the last, and each generation raised the barriers to entry for anyone trying to compete without that accumulated engineering heritage.

AvH's roots in 1876 planted the seeds for DEME's dominance 150 years later.

Early Expansion: Latin America, Africa, and Learning Hard Lessons (1900–1950)

The turn of the century brought ambition on a global scale. In 1903, Ackermans & van Haaren secured its first international contract: dredging operations to enlarge the port of Rosario in Argentina's Santa Fé province. Hendrik Willem Ackermans, then 48, did not delegate. He sailed to South America and spent from May through July 1904 personally supervising the work, staying with Jacobus van Haaren — family, as always, at the heart of the enterprise.

The Rosario project was no brief engagement. The company worked there for ten years, eventually handling 9.5 million cubic metres of dredging and 5.7 million cubic metres of land reclamation. From this foothold, AvH expanded across the Argentine coast: La Plata, Bahía Blanca, Puerto Belgrano, San Nicolas, and beyond. They built the port of Montevideo in Uruguay. Between 1908 and 1916, they dredged 8.5 million cubic metres in the Brazilian port of Rio Grande do Sul.

These were heady years. European contractors in Latin America operated in a world of enormous demand — growing nations needed port infrastructure to export agricultural commodities like beef, grain, and coffee — and limited local competition. The margins were attractive, the projects were massive, and the work kept coming.

But the experience was not without its hard lessons. Economic booms turned to busts with devastating speed. Argentina's prosperity in the early 1900s — it was one of the ten wealthiest countries in the world at the time — gave way to financial crises and political instability. The impact of World War I disrupted shipping lanes, supply chains, and the ability to move equipment and personnel across the Atlantic. Internal management difficulties multiplied across vast distances, in an era when a letter from Buenos Aires to Antwerp took weeks and decisions had to be delegated to local managers whose judgment could not always be verified. Currency fluctuations could wipe out profits earned in local pesos when converted back to Belgian francs.

Academic studies of AvH's Latin American period describe it as "a hard lesson learnt, crowned with success" — a characterization that suggests the success was real but came at a cost. The lesson was not that international expansion was wrong. It was that managing operations across oceans required a fundamentally different set of skills than managing them at home, and that political and economic risk in emerging markets could overwhelm even the best-executed engineering project.

Africa presented a different set of challenges. AvH executed port construction projects across the colonial territories: Algeria (dredging two million cubic metres at Béjaïa in 1927-28, plus work at Oran), Morocco (Casablanca, Tangier, Rabat), Tunisia (Bizerte), Cameroon (Douala), Guinea (Conakry), and Congo-Brazzaville. The firm often worked as a subcontractor to major French construction companies on these North and West African projects. In Asia, the company dredged the Mekong River at Phnom Penh and worked on the Persian port of Now-Chahr in Iran. Even in the Baltic, AvH built military harbours in Saint Petersburg and naval docks at Sveaborg near Helsinki. By the 1930s, the flagship dredger Antwerpen III was being dispatched to the far corners of the globe.

What mattered most about this half-century of international expansion was not the revenue or the cubic metres. It was the institutional education. AvH learned to operate across different legal systems, political regimes, and physical environments. They learned that political risk could wipe out years of profit in a single nationalization or revolution. They learned the importance of maintaining strong ties to the home market while venturing abroad. And most critically, they learned the philosophy that would define the company's later incarnation as a holding company: the value of "active ownership" — staying close to operations, deploying experienced people on the ground, and maintaining strategic control rather than simply writing checks from a distance.

The Latin American experience also revealed a strategic truth that would shape AvH for the next century: the difference between building things and building companies. In Argentina and Brazil, AvH was fundamentally a contractor — executing projects, collecting fees, and moving on to the next job. The value creation was linear: one project, one payment. But the relationships built, the organizational capabilities developed, and the institutional knowledge accumulated — these were assets that compounded. The question for AvH's future leaders would be: how do you capture that compounding value in a corporate structure? The answer, decades later, would be the holding company model.

Meanwhile, the African and Asian projects expanded AvH's geographic footprint across the colonial world. In North Africa, the firm dredged harbours in Algeria, Morocco, and Tunisia, often working as a subcontractor to major French construction companies. In West and Central Africa, AvH built port infrastructure in Cameroon, Guinea, and Congo-Brazzaville. In Asia, the flagship dredger Antwerpen III worked the Mekong River at Phnom Penh and the Persian port of Now-Chahr. Even in the Baltic, the company constructed military harbours in Saint Petersburg and naval docks near Helsinki. At Gdynia in Poland, AvH dredged 36 million cubic metres — a project that dwarfed even the Scheldt deepening campaign.

The sheer geographic breadth of these operations is important context. By the mid-20th century, AvH had executed projects on five continents. The institutional knowledge this created — how to mobilize equipment across oceans, how to manage polyglot workforces, how to navigate foreign legal systems and corrupt colonial bureaucracies — was a strategic asset that no competitor could replicate quickly. It was also deeply personal: Hendrik Willem Ackermans, who had crossed the Atlantic himself at age 48 to supervise the Rosario project, died in 1945 at the remarkable age of 89 or 90, having lived through both world wars and seen his family's small Dutch contracting firm grow into a multinational marine engineering enterprise.

The formal incorporation of the company as Ackermans & van Haaren NV on December 30, 1924, marked the transition from family partnership to modern corporate structure. But the DNA — engineering expertise, international ambition, family governance, and a willingness to learn from failure — was already deeply encoded. When the next generation would transform AvH from an operating company into an investment holding, they drew on exactly these lessons.

Transformation into a Holding Company (1970s–1990s)

Every great conglomerate has a pivotal strategic moment when it stops being one kind of company and starts being another.

For Ackermans & van Haaren, that transformation unfolded gradually over two decades, from the 1970s through the early 1990s, as the group evolved from a pure operating company focused on dredging into a diversified investment holding. Two parallel developments defined this era: the consolidation of the marine engineering business into what would become DEME, and the entry into private banking through the acquisition of Delen.

The marine engineering consolidation came first. By the 1970s, the global dredging industry was entering a phase of consolidation. Larger projects — mega-ports in the Middle East, land reclamation in Singapore and Hong Kong, channel deepening for supertankers — demanded fleets and expertise that no single small contractor could provide. The era of the boutique dredger was ending.

In September 1974, AvH merged its dredging operations with Société Générale de Dragage — a firm incorporated in 1930 — to form Dredging International. This was a recognition that scale mattered. The merged entity was stronger, with a larger fleet and broader geographic reach, but it was still one piece of a puzzle.

The decisive corporate restructuring came in 1991, when DEME — Dredging, Environmental and Marine Engineering — was established as a holding company combining Dredging International with Baggerwerken Decloedt & Zoon, another Belgian dredging contractor active along the Belgian coast since 1875. Ownership was split equally: 50 percent AvH, 50 percent CFE (Compagnie d'Entreprises CFE, a Belgian construction group). The name DEME was itself a statement of ambition — adding "Environmental" and "Marine Engineering" to what had been purely a dredging business signalled an intention to diversify into higher-value activities. The environmental remediation market was growing as European governments tightened regulations on contaminated soil and sediment, and DEME saw an opportunity to leverage its dredging expertise into a new business line.

But the truly transformative acquisition happened in the world of finance, not engineering. In 1936, a 32-year-old Antwerp man named André Delen had established a brokerage firm called "Delen & C" — armed, as the company's own lore describes it, with nothing more than a pen, a notebook, and the newspaper. André Delen placed orders on the stock market and practiced what he called "responsible wealth management." It was modest in scale but serious in philosophy.

The generational transition at Delen proved decisive. In 1975, André stepped back and handed management to his sons. Jacques Delen, the youngest, became CEO.

For fifteen years, Jacques quietly ran the brokerage, building relationships and refining the firm's approach to client service. He was a listener, not a showman — the kind of banker who remembered clients' children's names and understood that trust in financial services is built in small increments over years, not through aggressive sales pitches.

Then, in 1990, Paul De Winter joined the firm, and together they orchestrated a strategic pivot that would define Delen for the next three decades: the shift from traditional brokerage to discretionary asset management.

The distinction matters enormously, and it is worth dwelling on because it explains the economics that make Delen so valuable today. In a brokerage model, the client makes the decisions and the firm executes trades, earning a commission on each transaction. Revenue is inherently unpredictable — it depends on how often clients trade, which depends on market conditions and individual whim. In a discretionary model, the client entrusts full portfolio authority to professional managers, and the firm charges a recurring annual fee based on assets under management. Whether the client calls once a year or once a day, the fee is the same. Whether markets are volatile or calm, the fee keeps flowing. The revenue becomes predictable, recurring, and directly tied to the total pool of assets — which, in the long run, tends to grow both through market appreciation and net new client deposits.

More importantly, the discretionary model aligns the manager's incentive with long-term performance rather than trading volume. A brokerage earns more when clients trade more, which can create a perverse incentive to encourage activity. A discretionary manager earns more when client portfolios grow, which aligns incentives with patient, long-term compounding. Jacques Delen and Paul De Winter understood that wealthy Belgian families wanted trustworthy stewardship, not stock tips. It was a bet on relationships and compounding, not speculation.

In 1992, the Antwerp stockbroking company Delen became part of Ackermans & van Haaren. This was the marriage that would define AvH's future.

The strategic logic was compelling. AvH's existing business — marine engineering — was inherently capital-intensive and cyclical. Vessels cost hundreds of millions. Maintenance docks cost tens of millions. And revenue depended on the timing of large infrastructure projects that could be delayed by government budget decisions, environmental approvals, or economic downturns. Private banking, by contrast, required almost no physical capital. There were no vessels to maintain, no weather delays, and margins expanded rather than contracted with scale. What followed was a series of acquisitions that built Delen from a regional brokerage into a national banking franchise: Bank O. de Schaetzen in 1994 (critically important because it gave Delen formal banking status), stockbroking firm De Ferm in 1996, Brussels-based Havaux in 2000, and Capital & Finance in 2007, which brought with it Cadelam, the dedicated in-house fund management company that would eventually oversee more than €47 billion in client assets.

The other transformative event of the 1990s was the privatization of the Société Nationale d'Investissement in 1994, when the Belgian State sold its participation in the SNI to AvH. This single transaction created two entirely new business pillars: Sofinim, which became AvH's private equity and growth capital vehicle, and Leasinvest, which became the group's real estate investment arm (later merged with Extensa to create Nextensa). In one stroke, AvH went from a company with two legs — marine engineering and private banking — to one with four: marine engineering, private banking, real estate, and growth capital. The architecture of the modern holding company was complete.

The man who oversaw much of this transformation was Luc Bertrand, who joined AvH as financial director in 1986, became Chairman of the Executive Committee in 1990, and would remain the dominant strategic figure for the next three decades. Bertrand had begun his career at Bankers Trust in New York as Vice-President and Regional Sales Manager for Northern Europe — a background that gave him both financial sophistication and an international perspective unusual for a Belgian family business. A founding member of Guberna, the Belgian institute for good governance, Bertrand brought a rigour to capital allocation and board governance that elevated AvH from a well-run family company to a professionally managed investment group.

To understand Bertrand's impact, consider the discipline he imposed. Under his leadership, AvH adopted a set of principles that sound simple but are remarkably hard to execute consistently: each participation must be responsible for its own balance sheet, each must target annual profit growth, and the group should focus on a "limited number" of strategic holdings rather than sprawling across dozens of positions. Bertrand understood something that many conglomerate managers miss — that adding more holdings does not diversify risk if you lack the bandwidth to govern them actively. Better to own five businesses brilliantly than fifteen businesses adequately. This philosophy meant saying no far more often than saying yes, turning down attractive deals because they would dilute management attention, and periodically selling mature investments to recycle capital into higher-growth opportunities. Bertrand's tenure is inseparable from the AvH story.

The architecture that emerged from this period had an elegance to it. Marine Engineering (DEME) was capital-intensive, cyclical, and tied to global infrastructure spending — a business that generated enormous cash flows in good years but required continuous fleet investment. Private Banking (Delen) was capital-light, recurring, and tied to financial markets — a business that generated steady fees regardless of whether ships were sailing or sitting in port. Real Estate (eventually Nextensa) provided inflation protection and development optionality. Growth Capital (eventually the successor to Sofinim) provided exposure to emerging themes and entrepreneurial ventures. The four pillars did not merely coexist — they actively balanced each other, diversifying the group's earnings across economic cycles and market environments.

There was also a philosophical consistency across all four. In each case, AvH sought to own businesses where long-term relationships mattered more than short-term transactions, where accumulated expertise created barriers to entry, and where patient capital could generate returns that impatient capital could not. Dredging the Scheldt. Managing a family's wealth across generations. Developing a city quarter over decades. Backing a software company through its scaling phase. Different industries, same principle.

For investors, the 1970s-1990s transformation established the core principle that still drives AvH: own a limited number of strategic participations where you can exercise active influence, ensure each one is responsible for its own financial performance, and compound the portfolio's value through a combination of organic growth and disciplined capital recycling. It sounds simple. Very few companies execute it this well.

The CFE-DEME Consolidation (2013)

If the 1990s were about assembling the pieces, the 2010s were about arranging them correctly. And the first arrangement that needed fixing was DEME's ownership.

By 2013, DEME had grown into one of the world's largest dredging and marine engineering companies. But its corporate structure was a mess. Ownership was shared between AvH and CFE, a Belgian construction group in which French industrial conglomerate VINCI held a 46.84 percent stake. AvH and CFE exercised joint control over DEME — an arrangement that worked operationally but created strategic friction. Joint ventures between shareholders with different time horizons and strategic priorities are inherently unstable, and the offshore energy market was beginning to demand the kind of decisive capital allocation that joint control structures struggle to deliver.

The resolution required careful negotiation between two very different corporate cultures. AvH, the long-term Belgian holding company with family roots. VINCI, the French infrastructure giant with a €30 billion market cap and a portfolio of global concessions. In September 2013, they reached an agreement that was elegant in its architecture. AvH would contribute its 50 percent shareholding in DEME to CFE in exchange for newly issued CFE shares at €45 per share. Simultaneously, VINCI would sell half of its CFE stake to AvH at the same price. The result, upon closing in December 2013: CFE became the sole 100 percent shareholder of DEME, and AvH became the majority shareholder of CFE with a 60.39 percent stake. VINCI retained a minority 12.1 percent position in CFE and stepped back from governance.

The genius of the deal was that it accomplished three things at once.

First, it gave DEME a single, clear owner through CFE, eliminating the governance friction of joint control. Second, it gave AvH effective control over the combined entity, consolidating strategic authority. And third, it allowed VINCI — which had its own strategic priorities in concessions and infrastructure — to exit gracefully while maintaining a residual financial interest. All three parties got what they needed. No one felt shortchanged. It was the kind of deal that only works when all sides understand both their own strategic priorities and those of their counterparties.

Why did this matter so much? Because DEME was on the cusp of a transformation that would require billions in capital investment and years of patient execution: the pivot to offshore wind energy. The dredging industry's traditional markets — port expansion, land reclamation, channel maintenance — were mature and cyclical. Offshore wind was nascent, capital-intensive, and growing exponentially. To commit the fleet investments and take the project risks required for offshore wind leadership, DEME needed a shareholder willing to think in decades, not quarterly earnings cycles. AvH, with its philosophy of long-term active ownership, was the ideal parent. VINCI, for all its excellence as an infrastructure operator, was oriented toward different strategic priorities.

Consider the counterfactual. Without the 2013 consolidation, DEME would have remained a 50/50 joint venture between AvH and a CFE that was itself partially controlled by VINCI. Every major capital expenditure decision — ordering a new installation vessel, bidding on the Vineyard Wind contract, investing in deep-sea mining technology — would have required consensus between shareholders with fundamentally different strategic horizons. VINCI, as a global infrastructure concessions operator, might have prioritized cash returns over long-term fleet investment. The offshore wind pivot, which required billions in speculative capital deployment before the market proved itself, might never have happened — or happened too slowly to capture the leadership position that DEME now holds.

The 2013 consolidation was, in retrospect, the inflection point that enabled everything that followed: the offshore wind buildout, the fleet expansion, the Vineyard Wind contract, the separate listing, and the extraordinary financial performance of the 2020s. Without unified control, none of it would have happened at the same pace or with the same conviction. It was the kind of structural corporate move that creates no immediate headlines but generates compounding value for years afterward — exactly the sort of thing AvH does better than almost any European holding company.

DEME's Offshore Wind Energy Pivot (2010s–Present)

Stand on the deck of DEME's installation vessel Orion in the North Atlantic, watching a 3,500-tonne offshore substation being lowered into position off the coast of Massachusetts, and you are witnessing something historically unprecedented. Not just the physical feat — though lifting structures heavier than most buildings onto platforms in open ocean is spectacular enough — but the broader industrial transformation of a 150-year-old dredging company into one of the world's leading offshore energy contractors.

DEME's entry into offshore wind dates to the year 2000, but the real breakthrough came in 2002 with the Samsø project in Denmark — the company's first turnkey offshore wind installation contract. It was small by today's standards, but it proved the concept: a dredging company's expertise in marine logistics, heavy lifting, and working in hostile sea conditions translated directly into the ability to install wind turbines and their foundations offshore.

The logic was hiding in plain sight. Dredging companies already owned and operated heavy marine vessels. They already employed crews with decades of experience working in open water. They already understood the logistics of mobilizing equipment to remote marine locations, managing weather risk, and executing complex operations on tight schedules. Installing a wind turbine foundation in 30 metres of water required essentially the same set of capabilities as dredging a shipping channel — just applied to a different task. DEME saw this overlap earlier and more clearly than most of its competitors, and moved to capitalize on it with conviction. Over the next two decades, it would ride this insight to dominance.

The diversification was deliberate and systematic. Beyond traditional dredging, DEME expanded into soil remediation, silt recycling, offshore services for oil and gas, aggregate extraction, wind farm installation (both nearshore and far offshore), marine salvage, wreck removal, and heavy lifting.

In 2019, the company formalized its offshore capabilities by merging three predecessor units — GeoSea, Tideway, and A2Sea — into a unified DEME Offshore division. The combination created a one-stop-shop for every aspect of offshore wind construction: foundations, turbines, inter-array cables, export cables, and substations. Where competitors might handle one piece of the puzzle, DEME could offer clients a complete, integrated solution — reducing interface risk, simplifying project management, and capturing a larger share of each project's total value.

The results have been staggering. In 2023 alone, DEME installed over 700 megawatts of wind turbines and 1,212 megawatts of foundations. Offshore Energy achieved 57 percent growth in turnover that year, reflecting execution of installation projects spanning Europe, Taiwan, and the United States. The company has now completed over 350 offshore wind projects and installed more than 5,000 kilometres of subsea cables across wind farms in Europe and the US.

For those unfamiliar with the offshore wind installation process, it is worth pausing to explain why this business is so difficult to enter. Installing an offshore wind turbine is nothing like putting up a wind turbine on land. First, you need to drive a monopile foundation — a hollow steel cylinder weighing up to 3,000 tonnes and stretching over 100 metres in length — into the seabed, often through layers of clay, sand, and rock. This requires a specialized jack-up vessel that can position itself on the ocean floor, lift the monopile off a transport barge, and hammer it into place with a hydraulic impact hammer while compensating for wave motion, tidal currents, and wind. Then you install a transition piece on top of the monopile. Then you erect the turbine tower, the nacelle (the housing for the generator and gearbox), and the blades — each of which can exceed 100 metres in length on modern turbines. All of this happens at sea, often tens of kilometres offshore, in weather windows that may close with only hours of warning. The precision required is extraordinary. The capital at risk — each turbine can cost tens of millions of euros — is enormous. And the vessels needed to execute this work cost hundreds of millions to build and years to deliver from the shipyard.

The geographic expansion was equally striking. In Taiwan, DEME played a central role in building the island nation's offshore wind industry from scratch. The Taiwanese government, facing energy security concerns after the Fukushima nuclear disaster prompted a decision to phase out nuclear power, committed to building 5.7 gigawatts of offshore wind capacity by 2025, with ambitions extending to 20 gigawatts by 2035. DEME was among the first international contractors to enter the market, installing foundations and turbines for projects like Changfang & Xidao and Greater Changhua. The work required adapting to typhoon-prone waters, local content requirements, and the logistical complexity of operating 9,000 kilometres from home base. It was exactly the kind of challenge that rewarded DEME's deep institutional experience in working hostile marine environments across the globe.

The American market proved even more significant. DEME Offshore US was selected for Vineyard Wind 1, the first large-scale offshore wind project in the United States, located approximately 24 kilometres south of Martha's Vineyard, Massachusetts. The scope was massive: transportation and installation of monopile foundations, transition pieces, the offshore substation, scour protection, and wind turbines for the 800-megawatt, 62-turbine project. When DEME's vessel Orion set the 3,500-tonne substation in place — the single heaviest lift of the entire campaign — it marked the first offshore wind substation installation in US history. Pioneering a new market on this scale, working with Jones Act-compliant feeder vessels, was exactly the kind of project that separates DEME from competitors lacking the fleet, the expertise, or the risk appetite.

The fleet itself is a competitive weapon. DEME operates more than 100 specialized vessels, and the jewel in the crown is the Spartacus — the world's most powerful self-propelled cutter suction dredger. Delivered in August 2021 by Royal IHC in the Netherlands, Spartacus is a 164-metre-long, 34-metre-wide behemoth with a total installed power of 44,180 kilowatts. To put that in human terms: it has the power of roughly 600 mid-size cars, concentrated into a single dredging machine. Its production capacity and ability to cut through hard rock substrate are unmatched anywhere in the industry. It can dredge to depths of 45 metres, with 72-metre-long spud anchors and 14 interchangeable cutterheads designed for everything from fine sand to solid rock. It is also the first cutter suction dredger of its class capable of running on liquefied natural gas, reflecting DEME's commitment to reducing its own carbon footprint even as it builds the renewable energy infrastructure for others.

Beyond wind turbines, DEME is advancing two frontier technologies that could define the next decade. The first is the Princess Elisabeth Island, the world's first artificial energy island, being constructed 45 kilometres off the coast of Ostend in the Belgian North Sea. This artificial island will serve as an electricity hub, bundling cables from Belgium's second offshore wind zone and transmitting power to shore via both high-voltage direct current and alternating current infrastructure, with a total capacity of 3.5 gigawatts. DEME is building it in a joint venture with Jan De Nul (the "TM EDISON" consortium) for Belgian grid operator Elia. Construction began in 2024, with completion expected by 2028. The concept — an entirely man-made island engineered specifically as a renewable energy nexus — sounds like science fiction, but it is under construction today, with massive 22,000-tonne concrete caissons being placed in the North Sea.

The second frontier is deep-sea mineral harvesting. Through its subsidiary Global Sea Mineral Resources, DEME holds exclusive exploration rights across 75,000 square kilometres of the Clarion-Clipperton Zone in the Pacific Ocean — a deep-sea area where potato-sized polymetallic nodules rich in nickel, cobalt, copper, and manganese rest on the seabed at 4,500 metres depth. These are exactly the metals critical for battery production and the energy transition. In 2021, GSR's pre-prototype collector robot Patania II successfully harvested nodules at full ocean depth, observed by scientists from 29 European research institutes. Transocean, the global offshore drilling giant, has made a non-controlling investment in GSR. Whether commercial deep-sea mining ultimately proceeds depends on regulatory frameworks still being debated at the International Seabed Authority, but if it does, DEME is positioned at the frontier.

The financial results speak volumes. DEME's 2024 turnover grew 25 percent to exceed the €4 billion threshold for the first time, driven by market demand, expanded fleet capacity, high utilization rates, and effective project execution. The EBITDA of €764 million represented a 28 percent increase, with the margin ticking up to 18.6 percent — indicating not just revenue growth but improving profitability per project. Net profit reached €288.2 million — a 77 percent jump over the prior year.

But the most remarkable number is the balance sheet transformation. DEME generated €729 million in free cash flow — a staggering figure for a company of its size — enabling it to completely deleverage, ending 2024 with a net cash position of €91 million after carrying net debt of €512 million just twelve months earlier. To swing from half a billion in net debt to net cash in a single year, while simultaneously investing in fleet expansion and new technology, is a testament to the operating leverage embedded in DEME's business model when utilization rates are high and the project mix is favourable. The orderbook stood at €8.2 billion, a record, providing multi-year revenue visibility.

In 2025, DEME completed the acquisition of Havfram, adding two state-of-the-art wind turbine installation vessels — Norse Wind and Norse Energi — to its fleet. These are next-generation vessels designed to handle the largest turbines in development, with rotor diameters exceeding 300 metres and monopile weights up to 3,000 tonnes, in water depths up to 70 metres. The acquisition was a strategic move to secure installation capacity ahead of the enormous pipeline of European and American offshore wind projects expected through the 2030s.

For a company that started by dredging the Scheldt with bucket chains in the 1890s, the transformation into a global leader in offshore energy installation — with frontier plays in artificial islands and deep-sea mining — is nothing short of extraordinary.

And it was only possible because AvH's 2013 consolidation gave DEME the unified ownership and long-term capital commitment needed to make these bets. No short-term shareholder would have approved the capital expenditures. No quarterly-focused board would have sanctioned the risk. The offshore wind pivot is the ultimate vindication of patient, long-term ownership — and the most powerful argument for the holding company model that AvH represents.

The CFE-DEME De-merger (2022)

If the 2013 consolidation unified DEME and CFE under AvH's control, the 2022 de-merger was the logical next step: separating two fundamentally different businesses so each could be valued and managed on its own terms.

In December 2021, CFE's board announced its intention to transfer its 100 percent stake in DEME to a new company by means of a partial demerger. The rationale was straightforward: DEME and CFE operated in different markets, different geographic segments, and with fundamentally different strategic priorities. DEME was a global marine engineering and offshore energy company with a €4.5 billion offshore wind orderbook. CFE was a Belgian, Luxembourgish, and Polish construction and real estate development business. Bundling them under one listed entity created a conglomerate discount and prevented the market from fully assessing the value potential of either one.

The board's statement captured it precisely: "As DEME and CFE operate in different markets and geographic segments, each with distinct strategic priorities, the board believes that it is in the interest of all its stakeholders to take the next step and to split the group into two."

The timing of the announcement was notable. DEME's offshore wind orderbook had swelled to approximately €4.5 billion in contracts, the global offshore wind pipeline was accelerating dramatically, and governments from the United States to Taiwan were committing hundreds of billions to offshore energy development. A separate listing would allow the market to value DEME's offshore wind franchise directly, without the dilution of being bundled with a Belgian construction company.

The separate listing of DEME on Euronext Brussels took place on June 30, 2022, at an admission price of €96 per share, giving the company an initial market capitalization of approximately €2.43 billion.

AvH retained majority ownership of both independently listed companies, holding approximately 62 percent of each. The structural benefit was immediate.

For DEME, the separate listing meant pure-play visibility. Investors who wanted exposure to the offshore energy transition could now buy DEME directly, without also taking a position in Belgian construction. Institutional funds with ESG mandates, infrastructure-focused investors, and European equity managers could all access the DEME story in a clean, transparent wrapper.

For DEME's management, the benefit was even more profound. Capital allocation, strategy communication, and employee compensation could all be structured purely around the marine engineering and offshore energy mission, without the complexity of a parent entity pursuing different objectives.

The timing proved fortunate. DEME listed just as the global offshore wind market was accelerating dramatically, with European and American governments committing hundreds of billions to offshore wind development. As a pure-play listed entity, DEME attracted new institutional investors who had previously found the CFE conglomerate structure unattractive. The subsequent financial performance — 25 percent revenue growth and near-doubling of profit in 2024 — validated the strategic logic of separation.

The de-merger also unlocked a subtler benefit: management focus. When DEME was a subsidiary of CFE, its leadership had to operate within the corporate governance framework of a construction conglomerate. Capital allocation requests competed with CFE's contracting and real estate development businesses. Management incentive structures were diluted by the parent company's diverse portfolio. After the de-merger, DEME's management team — led by CEO Luc Vandenbulcke — could set strategy, allocate capital, and structure compensation purely around the marine engineering and offshore energy mission. The stock price became a direct measure of their execution, creating powerful alignment between management and shareholders.

For investors, the CFE-DEME de-merger highlighted an important aspect of AvH's holding company approach. Unlike conglomerates that resist breaking up because empire-building incentives override shareholder value creation, AvH demonstrated a willingness to create structures when they serve strategic purposes (the 2013 consolidation) and dismantle them when they no longer do (the 2022 de-merger). This flexibility — the ability to act as both assembler and dis-assembler of corporate structures — is rare and valuable. It requires a governance culture where the holding company's identity is tied to value creation, not to the perpetuation of any particular organizational form.

For AvH, the de-merger was a masterclass in value creation through corporate structure. No new assets were acquired. No new capabilities were developed. The same people ran the same businesses with the same clients. But by changing the wrapper — separating two distinct businesses into two distinct listed entities — AvH unlocked significant value for all shareholders. It is a reminder that in the world of holding companies, how you own things can matter as much as what you own.

Private Banking Dominance: Delen's Growth Machine (2000s–Present)

If DEME is the physical engine of AvH — steel vessels and concrete caissons, salt spray and diesel exhaust — then Delen Private Bank is the financial engine: lighter, quieter, housed in tasteful offices rather than on rolling decks, and compounding with a relentlessness that would make any capital allocator envious.

By the time the 2000s arrived, Delen had already established its core model: discretionary asset management for wealthy Belgian families, delivered through long-term relationships built on trust rather than transaction volume. The 1990s acquisitions — Bank O. de Schaetzen, De Ferm, Havaux, Capital & Finance — had assembled the pieces. What followed in the 2000s and 2010s was the methodical expansion of this model into new geographies.

The United Kingdom came first. In 2011, AvH and Delen jointly acquired approximately 70 percent of JM Finn & Co for roughly €67 million. JM Finn, established as a partnership in 1945 and headquartered in the City of London, managed wealth for British families with a strong emphasis on discretionary mandates. Luc Bertrand articulated the strategic logic explicitly: "Over the years, Delen has built a position as one of the top two independent wealth managers in Belgium, and has for some time been seeking to acquire a presence in another European market beyond Luxembourg and Switzerland." JM Finn was the vehicle. Over the subsequent decade, Delen progressively increased its stake to 95.1 percent. By year-end 2024, JM Finn managed approximately €13.1 billion in total client assets and contributed €13.8 million to Delen's net profit.

The Netherlands proved to be the bigger growth opportunity, and the story of Delen's Dutch expansion is a case study in disciplined market entry. Delen entered the Dutch market in 2016 with the acquisition of Oyens & Van Eeghen, one of the oldest private banks in the Netherlands, founded in 1797. The choice was deliberate: Oyens & Van Eeghen provided not just a client base but a venerable Dutch brand, local regulatory licenses, and an operational platform that could serve as the foundation for further expansion.

Unlike Belgium, where the private banking market had largely consolidated around a few major players, the Netherlands remained remarkably fragmented. Dozens of independent wealth managers operated across the country, each with loyal local client bases, often founded by a single entrepreneur or family, and typically managing a few hundred million to a few billion in assets. This was precisely the kind of landscape where Delen's roll-up playbook could work: acquire firms whose cultural emphasis on discretionary management aligned with Delen's own philosophy, integrate them onto a common technology and fund management platform, and leverage Cadelam's centralized investment engine to deliver institutional-quality portfolio management to what had been boutique operations.

Nobel Vermogensbeheer followed in 2019, Groenstate Vermogensbeheer in 2023, and Puur Beleggen in early 2024. Each acquisition was small individually, but the cumulative effect was significant. Then came the real step-change: in October 2024, Delen acquired Box Consultants, a wealth management firm founded in 1976 in the Eindhoven region. This single deal doubled Delen's Dutch assets under management, catapulting the Netherlands from an outpost to what Delen now describes as a "second home market." The Dutch pipeline remains rich, and given the fragmented landscape, further acquisitions appear likely.

Back in Belgium, the acquisition machine continued. In July 2024, Delen announced an agreement to acquire 100 percent of Dierickx Leys Private Bank, an Antwerp-based institution with approximately €3 billion in client assets, 73 employees, and five branches. Founded in 1928, Dierickx Leys was one of Belgium's oldest independent private banks, known for its conservative, value-oriented investment philosophy — a cultural match for Delen's own approach. The deal closed in the first quarter of 2025, financed entirely from Delen's own resources, requiring no external capital or debt.

The strategic pattern across all these acquisitions is remarkably consistent: identify well-run private banks whose cultural emphasis on discretionary management aligns with Delen's own philosophy, acquire them at reasonable valuations, retain their client-facing teams and local relationships, and integrate them onto a single technology platform with centralized fund management through Cadelam. The Cadelam integration is the key to the economics — once a newly acquired firm's assets are migrated onto Cadelam's fund platform, the marginal cost of managing those assets is negligible while the fee revenue is immediate.

The results of this strategy are extraordinary. By year-end 2024, the consolidated assets under management of the Delen Private Bank group reached €66.88 billion, a 22 percent increase from €54.76 billion a year earlier — an absolute increase of more than €12 billion in a single year. The combined net profit of Delen Private Bank and Bank Van Breda reached €327.7 million, a 24 percent increase over an already strong 2023. Bank Van Breda, the sister institution focused exclusively on entrepreneurs and liberal professionals, crossed the €100 million net profit threshold for the first time in its history.

The symbiosis between Bank Van Breda and Delen is one of AvH's most underappreciated competitive advantages. Bank Van Breda serves as a specialized advisory bank for self-employed professionals — doctors, lawyers, architects, accountants — providing lending, insurance, and financial planning services tailored to their practice economics. When these clients accumulate investable wealth, they are referred to Delen for discretionary management. By year-end 2024, €16.9 billion of Delen's assets under management — representing 31 percent of total Continental European AuM — came from clients introduced by Bank Van Breda. It is a textbook example of a network effect within a financial services group: each bank makes the other more valuable.

The investment approach that underpins these results is deliberately conservative. Delen allocates primarily through Cadelam, its centralized fund manager, with €47.6 billion invested through Cadelam funds at year-end 2024. The philosophy emphasizes equities as the primary long-term return driver, a buy-and-hold orientation, and a willingness to stay invested through market volatility rather than attempting to time cycles. In 2024, the portfolio benefited particularly from strategic overweights in US equities and technology companies. Client satisfaction metrics are striking: 92 percent of clients rated the bank eight out of ten or higher, and 88 percent expressed high satisfaction with discretionary management.

What makes Delen's growth trajectory even more impressive is the discipline of the model. Ninety-one percent of group assets under management are managed under discretionary mandates — meaning Delen's investment professionals have full authority over portfolio decisions. This is not a brokerage house where clients call to place trades. The centralization through Cadelam creates extraordinary operating leverage: each incremental billion in AuM flows into the same fund structures, managed by the same investment team, on the same technology platform. The marginal cost of managing the next billion is negligible; the marginal revenue is substantial. It is a business model that becomes more profitable as it grows, with essentially no diseconomies of scale until the fund sizes themselves become market-moving.

The leadership transition at Delen has been smooth. After Jacques Delen moved to Chairman, Paul De Winter served as CEO from 2014 to 2019, followed by René Havaux until November 2022, and then Michel Buysschaert — a veteran Belgian banker recruited from Van Lanschot — who took the helm in December 2022. The continuity of philosophy across leadership changes reflects the strength of the institutional culture rather than dependence on any individual. The Delen family retains 21.25 percent of the bank through the vehicle Promofi NV, with AvH holding 78.75 percent through its subsidiary FinAx — a stable ownership structure that provides the long-term alignment critical for a trust-based business.

For investors evaluating AvH, the private banking segment is the ultimate compounding business. It grows organically through market appreciation and net new money flows, inorganically through acquisitions funded from its own cash generation, and structurally through the Bank Van Breda referral network. The business requires minimal capital investment relative to its earnings, produces high and increasing returns on equity, and benefits from client relationships that can last generations. It is, in many ways, the perfect complement to DEME — one business that is capital-intensive and cyclical, and another that is capital-light and recurring.

The AvH Playbook: Active Ownership and Capital Allocation

Ackermans & van Haaren defines itself as "an independent and diversified group aiming at creating shareholder value through long-term investments in a limited number of companies with growth potential on an international level." Every word in that sentence is deliberate. "Limited number" — not a sprawling empire. "Growth potential" — not turnaround stories or deep-value plays. "International level" — businesses that can become market leaders beyond Belgium. And "long-term" — the defining characteristic that separates AvH from private equity funds with five-year exit horizons.

The active ownership philosophy means AvH does not simply hold stakes and collect dividends. The group takes direct responsibility at the boards of directors and advisory committees of its portfolio companies. Each participation sets its own strategy and manages its own balance sheet, but within a framework of clear objectives agreed upon with AvH. The expectation is straightforward: annual growth in profit, both at the individual company level and for the group as a whole. The long-term perspective does not mean patience with mediocrity; it means patience with the natural rhythms of business building while maintaining accountability for results.

The leadership transition in May 2022 — from Jan Suykens, who had served AvH for 32 years, to the co-CEO team of Piet Dejonghe and John-Eric Bertrand — crystallized the company's generational ambition. Suykens described himself as "a transitional figure between the two Bertrands," referring to chairman Luc Bertrand and his son John-Eric. Dejonghe, a former Boston Consulting Group consultant with a law degree from KU Leuven and an MBA from INSEAD, brings analytical rigour and external perspective. John-Eric Bertrand, who studied commercial engineering at UCLouvain and earned an MBA from INSEAD after stints at Roland Berger and Deloitte, brings the continuity of family commitment. The dual CEO structure is unusual and carries execution risk, but it reflects AvH's instinct for balance: insider knowledge paired with outside expertise, family continuity paired with professional management.

The recent Growth Capital investments illustrate AvH's strategic thinking. In November 2020, the group acquired a 20 percent stake in OMP, one of the leading supply chain planning cloud companies worldwide. Jan Suykens commented at the time: "We believe SCP cloud solutions are a structural growth theme, and OMP is ideally positioned to further strengthen its global market position." It was a classic AvH bet — a market leader in a growing niche, privately held, capital-hungry, and seeking a patient partner rather than a private equity firm looking to flip the business.

In August 2023, AvH acquired a 40 percent stake in IQIP Holding for €100 million, alongside co-investors HAL Investments and MerweOord (the family holding of the Van Oord dynasty). IQIP, based in Sliedrecht in the Netherlands, specializes in foundation techniques for offshore wind turbines — designing and assembling hydraulic hammers, noise mitigation systems, and precision tools for lifting, upending, gripping, and guiding monopile foundations. Think of IQIP as the company that makes the specialized tools DEME uses on the job site. The investment connects directly to DEME's offshore wind business, creating a strategic relationship across the value chain without formal vertical integration. As the offshore wind market scales up and monopile sizes grow from 1,500 to 3,000 tonnes and beyond, IQIP's equipment becomes indispensable — and the company has been investing heavily in its equipment fleet to prepare for the anticipated double-digit market growth.

In September 2024, AvH acquired approximately one-third of V.Group, the world's largest ship management company, for roughly $150 million as part of a consortium led by STAR Capital. V.Group, headquartered in London, manages approximately 900 vessels from 50 offices in 30 countries, with a network of over 44,000 seafarers and some 2,900 shore-based employees. The company provides technical management, crewing, procurement, and compliance services to vessel owners who increasingly prefer to outsource these complex functions. The maritime services industry — driven by growing regulatory complexity, technological advancement, and decarbonization mandates — is exactly the sort of structural growth market that AvH seeks. Regulatory compliance alone is becoming so complex that many vessel owners find it more economical to hand operations to a professional manager like V.Group than to build the capability in-house.

The group also maintains significant positions in SIPEF, a listed agro-industrial group managing nearly 87,000 hectares of sustainable palm oil production in Southeast Asia, and Nextensa, a real estate investor and developer with a portfolio of approximately €1.1 billion anchored by the Tour & Taxis development in Brussels and the Cloche d'Or project in Luxembourg. Smaller Growth Capital investments include MRM Health (microbiome-based biotherapeutics), Biotalys (crop bioprotection), and VKC Nuts.

The portfolio also includes frontier bets that reveal AvH's appetite for the unconventional. Through SIPEF and Verdant Bioscience (in which AvH holds approximately 42 percent), the group is investing in advanced non-GMO breeding techniques for oil palms that promise significant yield increases per hectare without additional deforestation. Through MRM Health, AvH has backed a clinical-stage biopharmaceutical company developing microbiome-based therapeutics for ulcerative colitis. Through Biotalys, it is supporting next-generation crop bioprotection. These are small positions relative to the portfolio, but they reflect an intellectual curiosity and willingness to venture beyond the group's traditional competencies that keeps the investment pipeline fresh.

The capital allocation discipline shows in the dividend policy. AvH has paid a dividend continuously for 25 years without a single cut in at least the last twelve. The proposed dividend for 2025 of €4.60 per share represents a 21 percent increase over the prior year, yet the payout ratio remains around 21 percent of earnings — remarkably low, leaving the vast majority of cash generation available for reinvestment. The message is clear: AvH returns some capital to shareholders each year, but the real shareholder value creation comes from compounding retained earnings at high rates of return within the portfolio.

Consider what that 21 percent payout ratio means in practice. For every euro AvH earns, roughly 79 cents stays inside the group to be reinvested. If those retained earnings are deployed at the company's 10 percent return-on-equity target, the intrinsic value of the business compounds at roughly 8 percent annually from reinvestment alone — before accounting for any upside from growth capital investments hitting their stride or DEME's orderbook converting to profit at expanding margins. The math of patient compounding is not glamorous, but over decades, it is relentless.

Porter's Five Forces and Hamilton's Seven Powers Analysis

Strategy frameworks are only as useful as the businesses they analyze. But applied to AvH's two anchor businesses, Porter's Five Forces and Hamilton Helmer's Seven Powers reveal a holding company with remarkably durable competitive advantages on both sides of its portfolio.

DEME: Marine Engineering and Offshore Wind

In Michael Porter's framework, the threat of new entrants to DEME's business is remarkably low. More than 140 years of accumulated operational expertise, a fleet of over 100 specialized vessels including irreplaceable assets like the Spartacus, and deep relationships with government clients and offshore wind developers create formidable barriers. You cannot enter the global dredging or offshore wind installation market with a venture capital check and a good idea. The minimum ante is billions in vessel investment, decades of project experience, and an institutional safety record that clients trust with their most complex and high-stakes projects. The "Big Four" — DEME, Jan De Nul, Van Oord, and Boskalis — dominate the industry, and the barriers to joining that club grow higher with each generation of larger, more specialized vessels.

Buyer power is moderate. DEME's clients include sovereign governments (for port infrastructure and channel maintenance) and large energy developers (for offshore wind). Governments tend to award contracts on technical capability and track record rather than pure price competition, which insulates DEME from margin pressure. In offshore wind, the clients are major utilities and energy companies with deep pockets and long-term contracts, but the scarcity of qualified installation contractors shifts bargaining power toward DEME. Supplier power is similarly moderate — DEME relies on specialized shipbuilders like Royal IHC for its vessels, but these are long-term strategic relationships rather than spot market transactions.

The threat of substitutes is effectively zero. There is no alternative to dredging for keeping shipping channels navigable, no alternative to heavy-lift vessels for installing offshore wind turbines, and no alternative to specialized cable-laying ships for connecting wind farms to the grid. The competitive rivalry among the Big Four is real and ongoing, with each company investing aggressively in fleet expansion and technology, but the market is growing faster than capacity — particularly in offshore wind — which means rivalry plays out more as a competition for orderbook share than a destructive price war.

Delen Private Bank

The competitive dynamics are different in private banking. The threat of new entrants is moderate — regulatory barriers are significant, but fintech disruption and new digital wealth management platforms create ongoing competitive pressure. Buyer power is moderate as well — high-net-worth clients have abundant options, but the relationship-driven nature of discretionary wealth management creates significant switching costs once a client has entrusted their portfolio. The estate planning documents have been prepared, the multi-generational structures are in place, and the personal relationships with advisors run deep. These switching costs are among the most durable in financial services.

The threat of substitutes deserves particular attention. Robo-advisors and low-cost index funds have disrupted parts of the wealth management industry, particularly for clients with smaller portfolios who are primarily seeking market exposure. But Delen's core client base — high-net-worth families with complex estate planning needs, multi-generational wealth transfer requirements, and a preference for human relationships — has proven relatively resistant to digital disruption. These clients do not merely want a portfolio; they want a trusted advisor who understands their family dynamics, their tax structures, and their long-term goals. That is a fundamentally different value proposition from what a robo-advisor delivers, and it carries correspondingly higher margins.

Competitive rivalry is high. Belgium's private banking market includes strong players like KBC, BNP Paribas Fortis, and ING. In the UK, JM Finn competes against St. James's Place, Brewin Dolphin (now part of RBC), Rathbones, and other established wealth managers. In the Netherlands, the market is fragmented but competitive. Delen's edge is not that it faces no competition; it is that its model — centralized discretionary management through Cadelam, the Bank Van Breda referral network, and a culture of conservative long-term stewardship — generates superior client retention and organic growth that compounds faster than rivals can match.

Through the lens of Hamilton Helmer's Seven Powers, AvH's competitive advantages come into even sharper focus.

Scale Economies. DEME's fleet and global infrastructure enable it to bid on mega-projects that smaller competitors simply cannot execute. Consider the Princess Elisabeth Island: the project requires the design and placement of massive concrete caissons, the installation of complex electrical infrastructure, and years of marine engineering work in the open North Sea. Only a handful of companies on earth possess the fleet, the expertise, and the financial strength to bid on such a project. The cost of maintaining a fleet of 100-plus specialized vessels is enormous, but it is spread across a multi-billion-euro revenue base that generates operating leverage. Each incremental project contributes disproportionately to profit because the fixed cost base is already covered. At Delen, scale economies manifest differently: the centralized Cadelam fund management platform means that each additional billion in AuM is managed at essentially zero marginal cost, driving relentless margin expansion as the asset base grows.

Network Effects. The Bank Van Breda referral network is a genuine network effect within AvH's private banking segment. Each new entrepreneur client at Bank Van Breda is a potential future Delen wealth management client, and the more clients in the system, the more referrals flow. With €16.9 billion — 31 percent of Continental European AuM — sourced through this channel, the referral network is not a nice-to-have; it is a core pillar of the business model.

Counter-Positioning. This is perhaps AvH's most powerful competitive advantage at the holding company level. AvH positions itself as the long-term partner of choice for family businesses and management teams, explicitly contrasting itself with private equity firms that impose five- to seven-year exit timelines and aggressive leverage.

This counter-positioning is genuine: AvH held Delen for over 30 years and counting, DEME for 150 years and counting. Founders and management teams who want to build for the long term — and who are alienated by the PE model of leveraged buyout, cost-cutting, and exit — preferentially seek AvH as a partner. This gives AvH access to deal flow that PE firms cannot access. When a Belgian family business founder is considering who to partner with for the next chapter of growth, AvH's 150-year track record of patient ownership is a powerful differentiator that no amount of PE marketing can replicate.

Switching Costs. Deeply embedded in both businesses. DEME's clients return project after project because the cost of qualifying a new contractor, building trust on complex offshore installations, and accepting execution risk with an unproven partner is prohibitive. Delen's clients stay because their wealth management relationship is intertwined with estate planning, tax structures, and multi-generational family governance that would be enormously disruptive to reorganize.

Branding. "Ackermans & van Haaren stands for 150 years of entrepreneurship." In a world of rapidly built and rapidly destroyed corporate reputations, that sentence carries extraordinary weight. The brand is not flashy — there are no celebrity endorsements or Super Bowl ads. But in Belgium's tight-knit business community, among the family business owners and entrepreneurs who are AvH's natural partners, the name carries tremendous authority. Trust built over a century and a half is not something competitors can replicate with a marketing campaign.

Cornered Resources. DEME's specialized vessel fleet is a cornered resource in the most literal sense. The Spartacus, the Orion, the newly acquired Norse Wind — these are assets that take years to design and build, cost hundreds of millions each, and cannot be replicated quickly even by well-funded competitors. The company's unrivalled track record in the transport and installation of foundations, turbines, cables, and substations for offshore wind farms is an intangible cornered resource built over decades.

Process Power. DEME's 140-plus years of accumulated operational know-how in complex marine engineering, and Delen's advanced IT infrastructure for seamless client onboarding, represent process power — the ability to execute complex operations with consistently lower cost and higher quality than competitors, derived from institutional learning curves that cannot be compressed.

Comparing DEME to its Big Four peers illuminates these advantages in practice.

Jan De Nul (Belgian, family-owned, €2.9 billion turnover in 2023) is the closest competitor in both dredging and offshore wind. The two companies even collaborate on the Princess Elisabeth Island project while competing fiercely for other contracts — a dynamic that reflects the concentrated, oligopolistic nature of the industry.

Van Oord (Dutch, family-owned, roughly €1.7 billion revenue) is strong in dredging and increasingly active in offshore wind but smaller in scale. Boskalis (Dutch, approximately €4.5 billion revenue, taken private by HAL Investments in 2022) is the largest by revenue but more diversified across towage and salvage activities.

DEME's advantage lies in its combination of scale, offshore wind specialization, technological leadership in vessels like Spartacus, and the financial backing of a patient long-term owner in AvH. Among the Big Four, only DEME is backed by a publicly listed holding company with an explicit 150-year investment horizon.

Financial Performance and Current State (2023–2025)

Numbers tell stories too, when you know how to read them.

The three years from 2023 through 2025 represent a golden period for Ackermans & van Haaren — the harvest of decades of strategic positioning.

In 2023, the group posted a net profit of approximately €399 million, with record contributions from both DEME and the private banks. On a look-through basis, the portfolio companies generated turnover of approximately €6.5 billion and employed nearly 22,000 people. It was a strong year, but what followed was even stronger.

The 2024 results stepped up substantially. Group net profit grew 15 percent to €460 million, in line with AvH's long-standing target of 10 percent annual growth in total equity return. Every major segment delivered. DEME's turnover exceeded €4 billion for the first time, a milestone that underscored the scale of the offshore wind buildout. Delen and Bank Van Breda combined for a net profit of €327.7 million — the private banking segment alone was generating more profit than many standalone Belgian listed companies. Marine Engineering and Contracting, including Deep C Holding, CFE, and Green Offshore, contributed €201.8 million to AvH's group result. Total look-through turnover reached €7.6 billion across more than 23,000 employees.

The balance sheet story was equally compelling. DEME ended 2024 with a record orderbook of €8.2 billion and had completely delevered — moving from over half a billion euros in net debt to a net cash position in a single year. At the Delen level, the updated shareholder arrangements announced in November 2024 between AvH and the Delen family confirmed the long-term partnership structure, with provisions for enhanced governance rights and increased dividend distributions. The signal was clear: both AvH and the Delen family viewed the private banking franchise as a multi-generational asset, not a financial position to be optimized for short-term return.

The 2025 results, announced on February 27, 2026, were the best in AvH's history. Net profit surged 29 percent to €592.5 million. Equity reached €5.7 billion, and return on equity came in at 10.3 percent — precisely on target. Annual look-through turnover was €7.7 billion, with nearly 25,000 employees across 103 countries. The proposed dividend of €4.60 per share, a 21 percent increase, reflected the board's confidence in the sustainability of the earnings trajectory.

The first half of 2025 had already set the tone. H1 net profit reached a record €273.2 million, up 36 percent year-over-year, prompting management to raise full-year guidance to at least 15 percent growth. DEME's H1 turnover reached €2.12 billion with EBITDA surging 35 percent to €464 million and an orderbook of €7.5 billion. When the full-year numbers confirmed a 29 percent profit increase, the market recognized that AvH was not merely meeting its targets — it was exceeding them.

The acceleration from €399 million to €460 million to €593 million in three consecutive years — growth of 15 percent followed by 29 percent — demonstrates what happens when a holding company's core businesses simultaneously hit their stride.