ACEA SpA: Rome's 115-Year-Old Municipal Utility Becomes Italy's Water Champion

I. Introduction: The Eternal City's Essential Company

Picture the Roman Forum at twilight. The Colosseum glowing against the darkening sky. A fountain splashing in the Piazza Navona. Few tourists pausing to take photographs realize that the electricity illuminating these ancient monuments and the water feeding those baroque fountains flow through infrastructure managed by a single company—one whose history stretches back over a century, intertwined with Rome itself.

ACEA SpA is a multiutility operative in the management and development of networks and services in the water, energy and environmental sectors. Originally the city of Rome's provider, the ACEA group is the main national operator in the water sector with a catchment area of about 10 million people.

The central question driving this analysis: How did a municipal power company created to light Rome's streets become Italy's leading water operator and a multi-billion euro infrastructure champion?

The answer involves a fascinating journey through Italian political economy, European utility privatization, and the peculiar dynamics of natural monopolies in essential services. Today, ACEA commands a market capitalization of approximately $4.86 billion with trailing twelve-month revenue of $3.81 billion. The company employs 8,506 people across its operations.

But raw numbers only tell part of the story. ACEA represents something rare in European capital markets: a partially privatized municipal utility that retained its public service DNA while achieving meaningful commercial scale. ACEA remains listed on the Mercato Telematico Azionario organized and managed by Borsa Italiana, with Roma Capitale as its majority shareholder holding a 51% equity interest.

The episode themes that emerge from ACEA's history include municipal privatization, natural monopolies, Italian regulatory evolution, and infrastructure as essential service. Understanding ACEA requires understanding how Italy has attempted—with mixed success—to modernize a water sector characterized by fragmentation, underinvestment, and political complexity.

For long-term infrastructure investors, ACEA presents a distinctive profile: regulated revenue streams, infrastructure critical to millions, and exposure to a consolidating Italian water market where the company holds the pole position.

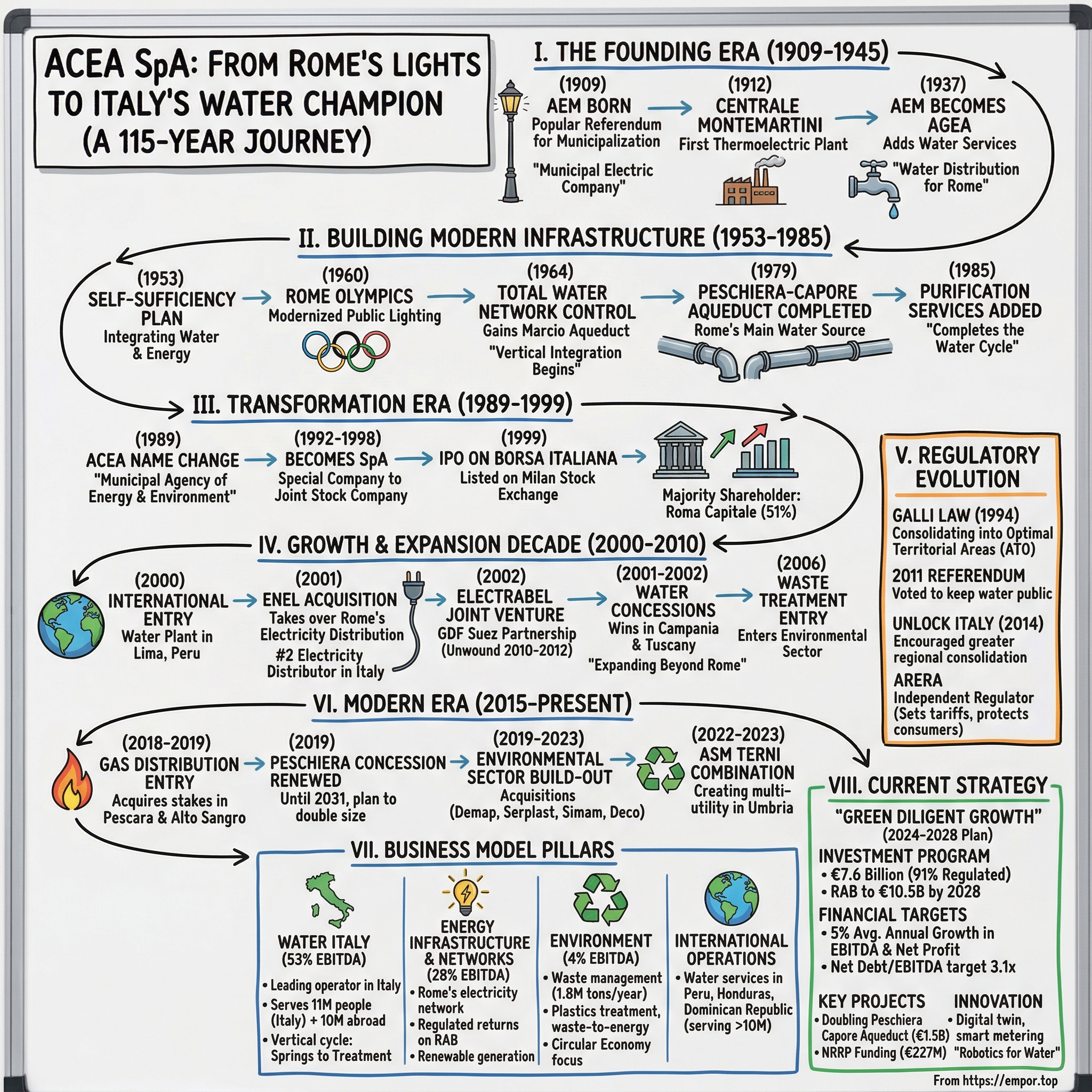

II. The Founding Era: Lighting the Eternal City (1909-1945)

The story begins not with water but with electricity—and with a popular referendum that would shape Rome's infrastructure for the next century.

The construction of a public power plant had been set in motion following the results of the September 20, 1909 Popular Referendum, in which citizens had given their assent to the municipalization of Rome's public utilities. The result of the Referendum also led to the birth of AEM, the Azienda Elettrica Municipale.

Rome's Municipal Electric company, better known by its Italian acronym AEM, was founded in 1909 to provide public and private street lighting. In 1912, AEM opened the Centrale Montemartini, its first thermoelectric power plant through which AEM started selling electricity in Rome.

The Centrale Montemartini deserves attention as more than a footnote. The area chosen for the construction of the power plant stands on land located between the Via Ostiense and the bank of the Tiber, thus suitable for a continuous supply of water necessary for the operation of the machines. It was easily accessible by rail and road and was located outside the daziale belt and was therefore not subject to fuel taxes.

In 1913 the plant was named in memory of Giovanni Montemartini, Councillor for Technology in the Nathan Junta, who died during a City Council meeting. The choice of naming reflected the progressive political movement that had championed municipalization—a belief that essential services should serve citizens rather than private profit.

By 1926, AEM was renamed Azienda Elettrica del Governatorato di Roma, or AEG (Electricity Company for the Governorship of Rome) as the company expanded its operations. By this time, street lighting in Rome had surged to nearly 18,000 lamps.

The Fascist Era: Water Enters the Picture

The transformative moment came in 1937, under Mussolini's regime. In 1937, the governor of Rome entrusted the company with building and managing of aqueducts as well as the water distribution network for the city. This seemingly bureaucratic decision created the dual identity that would define ACEA for decades to come.

With the newfound responsibilities, AEM changed its name to AGEA (an acronym for "Azienda Governatoriale Elettricità e Acque", Italian for "Government Electricity and Water Company") before changing it again to its current name Acea in 1945.

The addition of water services wasn't just operational expansion—it was the beginning of ACEA's journey toward becoming an integrated utility managing the essential flows that make urban life possible.

Surviving the War

World War II tested every assumption about infrastructure resilience. Allied bombing campaigns devastated Rome's industrial capacity. Yet ACEA's founding power plant survived. At the end of World War II, the Centrale Montemartini was the only available power plant still operational because it coincidentally escaped the bombings.

The power plant never ceased to operate even under the bombings and after the war provided the city with the energy required for its recovery.

This wartime survival embedded something important in ACEA's organizational DNA: the identity as keeper of essential services that must continue regardless of circumstances. The company emerged from the war not merely intact but with its purpose clarified—Rome's lights would stay on, its water would flow, because ACEA would ensure it.

The municipal DNA and essential service mission established in these decades still defines ACEA today. Every strategic decision the company makes—from acquisitions to technology investments—must be understood through the lens of this founding identity: a utility that exists to serve Rome and its citizens.

III. Building Rome's Modern Infrastructure (1953-1985)

The postwar decades transformed Rome from a historical relic into a living, growing capital. ACEA grew alongside it, layering infrastructure investments that would prove foundational for decades to come.

In 1953, the Municipal Council of Rome approved Acea's plan for self-sufficiency in electricity with the aim of improving the city's water system. This integrated approach—viewing energy and water as interconnected systems—would become a defining characteristic of European multiutilities, though ACEA embraced it before the term existed.

The 1960 Rome Olympics

The 1960 Summer Olympics presented both challenge and opportunity. The world would watch Rome, and Rome needed to look modern. For the Rome Olympics in 1960, Acea also took responsibility for the city's public lighting systems.

In preparation for the 1960 Rome Olympics, Acea modernised the city's public lighting network. This wasn't merely installing more bulbs—it required coordinating energy supply, network capacity, and aesthetic considerations across Rome's unique landscape of ancient monuments and modern venues.

The Olympic expansion cemented ACEA's role as Rome's comprehensive infrastructure provider. When dignitaries arrived for the games, they experienced a city that functioned smoothly because ACEA had invested ahead of demand.

Water Network Consolidation

In 1964, Acea gained control of Rome's entire water network on the expiry of the concession to Acqua Pia Antica Marcia for the management of the Marcio Aqueduct.

The Marcio Aqueduct reference reveals something remarkable: ACEA was absorbing infrastructure with roots in Roman antiquity. The original Aqua Marcia, built in 144 BC, had supplied Rome for millennia. ACEA's assumption of this responsibility connected the modern utility to an unbroken tradition of bringing water to Rome's citizens.

In 1976, Acea's plan for hydro-sanitary and street lighting refurbishment was approved within the framework of the redevelopment policy of Rome's suburbs launched by the Rome Municipality. The company's mandate expanded from serving central Rome to ensuring suburban residents received equivalent service quality.

The Peschiera-Capore Aqueduct: Engineering for Centuries

The most significant infrastructure achievement came in 1979. In 1979, the Peschiera-Capore aqueduct system was completed, which continues to be Rome's main water source.

Understanding the Peschiera-Capore system requires appreciating its scale and significance. The pipeline runs parallel to the existing one, completed in 1938. The original system represented decades of planning and construction. The project focuses on the construction of a new aqueduct infrastructure that supports and integrates the existing aqueduct, about 27,450 metres long, which ensures the water supply of the city of Rome and the Rieti territory, the Lower Sabina and the northern coast of Lazio, from Fiumicino to Civitavecchia.

The guarantee for residents of having drinking water which is pure and uncontaminated is a result of the specificity of the Peschiera-Capore pipeline: starting from its sources, this water stays underground for 15-20 years before being collected in the Aqueduct. After it has been extracted and distributed in the pipelines, the water is constantly checked to make sure that its quality remains unaltered, from the source to the household tap.

This infrastructure—built to last generations—represents exactly the kind of long-lived asset that creates durable value for patient capital. The Peschiera-Capore system would later become the centerpiece of ACEA's largest capital project.

Completing the Water Cycle

It was in 1985 that the company completed the management of the water cycle by taking on purification services.

This final piece created true vertical integration in water: from springs to homes to treatment and return. ACEA now controlled the complete water cycle for Rome—a position of infrastructure dominance that few utilities globally can match.

For investors considering ACEA today, this history matters. The infrastructure investments of the 1950s-1980s created assets still generating returns decades later. The company's competitive position rests on physical infrastructure that cannot be replicated and would take decades to build from scratch.

IV. Transformation Era: From Municipal Agency to SpA (1989-1999)

The late 1980s brought ideological shifts that would reshape European utilities. Privatization was ascendant. Margaret Thatcher had sold off British utilities. Continental Europe debated how to introduce market discipline while preserving public service missions. ACEA would navigate this transition while maintaining its unique character.

In 1989, Acea changed its name from "Azienda Comunale Elettricità" (Municipal Electricity and Water Agency) to "Azienda Comunale dell'Energia e dell'Ambiente" (Municipal Agency of Energy and the Environment).

The name change signaled strategic evolution—from a pure utility to an environmental services company. ACEA was positioning itself for a world where sustainability and circular economy thinking would reshape the utility sector.

Infrastructure Modernization

In the nineteen eighties and nineties, the Tor di Valle cogeneration plant began operation (in 1984, converted later to combined cycle from 1996) and the EUR water centre was inaugurated (1993).

The combined cycle conversion exemplified the efficiency improvements possible with modern technology. Converting existing thermal capacity to combined cycle operation increased output while reducing fuel consumption per kilowatt-hour generated.

The IPO: Bringing ACEA to Public Markets

The transformation culminated in what remains ACEA's most significant corporate milestone: the 1999 initial public offering.

In 1991, the Municipality transformed Acea into a special Company and, on 1 January 1998, the SpA was incorporated. From 19 July 1999, Acea SpA was admitted to listing on the Italian Stock Exchange and began an intense spin-off process.

In 1992, Acea became a Special Agency and, from the first of January, 1998, a Joint Stock Company (Acea S.p.A.) which, with Chief Executive Officer Paolo Cuccia at the helm, made its entrance on the Milan Stock Exchange on the 16th of July the following year.

As chief executive, he got ACEA, the City of Rome's water and energy utility company, listed on the stock exchange.

The IPO structure proved crucial. Rome retained majority control at 51%, ensuring the public service mission remained paramount. But minority shareholders gained access to a portfolio of essential infrastructure assets.

Since 1999, when Acea was floated on the stock market, the share capital of €1,098,898,884.00, represented by 212,964,900 ordinary shares each with a nominal value of €5.16 and carrying equal rights, has not changed.

Context: Italy's Privatization Ambiguity

ACEA's partial privatization reflected broader Italian ambivalence about utility reform. The Italian government embarked on a bold reform process of the Italian water sector by passing the Galli Law in 1993. The law aimed at consolidating municipal service providers into regional utilities, separating service provision from regulation, achieving cost recovery from tariffs.

In 2001, it introduced norms that forced municipalities to award concessions to private companies, abolishing the direct award of concessions to public companies. However, faced with opposition, the norms were revised to allow direct "in-house" awards if it could be demonstrated that in-house provision was more efficient than a concession.

In the meantime, the foreign private companies that had entered the Italian water market in the late 1990s faced difficulties: "Foreign players including Thames Water and Saur attempted to enter the Italian market only to become embroiled in never-ending political, regulatory and legal wrangles".

ACEA's mixed ownership structure—majority municipal, minority private—proved more durable than either pure public or pure private models. The company could access capital markets while retaining political legitimacy as a public service provider.

This structure created the template ACEA would use for the next quarter century: growth through acquisition, financed partially through capital markets, but anchored by Rome's controlling stake and the essential service mission.

V. The Growth Decade: Expansion & Partnerships (2000-2010)

The new millennium brought aggressive expansion. ACEA leveraged its newly public status to pursue acquisitions, partnerships, and international ventures that transformed the company from a Roman municipal utility into a national and international player.

International Expansion: Testing Waters Abroad

The year 2000 saw Acea's entry into the overseas market, with the construction and concession of a water plant in Lima.

The Lima venture signaled ambition beyond Italy's borders. ACEA would eventually build a meaningful Latin American presence: The Group also operates in Latin America, managing water operations in Honduras, the Dominican Republic and Peru, where it serves about 10 million inhabitants.

The Enel Acquisition: Becoming Rome's Power Distributor

In 2001 Acea took over the Enel electricity distribution network in Rome. This acquisition reshaped ACEA's energy profile fundamentally.

In 2001, Acea acquired the Enel branch responsible for electricity distribution in the metropolitan area of Rome. The deal made ACEA Italy's second-largest electricity distributor—a position it retains today.

The largest municipal utility in Italy, it is also Italy's #1 water utility and a top electricity distributor. ACEA provides water to about 9 million people and distributes power to more than 2.7 million homes and businesses in Rome and surrounding areas including Tuscany, Umbria, and Campania.

The Enel acquisition demonstrated how partial privatization enabled growth. A purely municipal entity would have struggled to finance such a transaction. ACEA's access to capital markets—while maintaining Rome's controlling interest—provided the financial flexibility to pursue transformational deals.

The Electrabel Joint Venture: European Partnership

In 2002, ACEA formed what would become one of its most significant partnerships. In the same year, together with the partner GdF Suez, it created the joint venture AceaElectrabel operative in the energy area.

ACEA has a controlling stake of 59.41% in AceaElectrabel and Electrabel Italia a stake of 40.59%. The agreements on the constitution of the joint venture provided that ACEA was to transfer to AEP two thermoelectric production installations and five hydroelectric power plants, while Electrabel was to provide a number of projects for the construction of installations.

The former monopoly has also built on Enel's Roman distribution assets, and through a joint venture with Electrabel, it has expanded into power generation, energy marketing, and natural gas distribution.

The Electrabel partnership brought European expertise and capital to ACEA's energy operations. Though the joint venture would eventually be unwound, In 2010-2012 together with the partner GdF Suez, it establishes the winding-up of the joint venture AceaElectrabel, active in the energy sector, thereby becoming entirely independent in this sphere. With a view to this, in 2011 Acea adopted a corporate structure for the production and sale of electricity which it fully owns and runs (Acea Produzione and Acea Energia).

Water Sector Consolidation

While energy partnerships grabbed headlines, the more strategically significant moves came in water. In 2001, as business consortium leader, Acea was awarded the management of the integrated water service in Campania for Ato ("Optimal Territorial Area") 3 Sarnese-Vesuviano and in Tuscany for Ato 2 (Pisa) and Ato 6 (Grosseto-Siena). In 2002, the company won the tender for Ato 3 (Florence), as well as for the management of Ato 5 Southern Lazio - Frosinone.

These concession wins expanded ACEA's water footprint far beyond Rome. The ATO (Optimal Territorial Area) system created regional water authorities that ACEA could win through competitive tenders—using its operational expertise and financial resources to outcompete smaller local operators.

Entry into Waste/Environment

In 2006 Acea entered the waste treatment and valorisation sector.

This diversification would prove prescient. The circular economy movement and European environmental regulations created growth opportunities in waste management that ACEA had positioned itself to capture.

The 2000-2010 decade established the strategic template ACEA follows today: dominant in Roman essential services, expanding nationally through concession wins and acquisitions, building selective international presence, and diversifying into environmental services.

VI. The Regulatory Evolution & Italian Water Market Dynamics

Understanding ACEA's competitive position requires understanding the peculiar dynamics of Italy's water sector—a market characterized by fragmentation, underinvestment, and ongoing reform efforts that create both challenges and opportunities.

The Infrastructure Gap

In Italy, 60% of the water network is more than 30 years old and 25% is more than 50 years old: a factor linked to the high level of network losses.

About one third of the water withdrawn for municipal supply is not billed to the customers because of leakage, malfunctioning...

This infrastructure deficit represents both a problem and an opportunity. For ACEA, aging networks require capital investment—but also create opportunities to deploy technology and expertise to reduce losses and improve service quality.

The Fragmentation Problem

Before 1994, the Italian water and sanitation sector was highly fragmented with about 13,000 local water and sanitation service providers, often providing water and sewer services separately in the same locality.

Italy currently hosts over 100 regional water utilities.

This fragmentation creates inefficiency but also acquisition opportunity. As smaller operators struggle with capital requirements and regulatory complexity, ACEA can offer partnership or acquisition as an alternative to continued independence.

The Galli Law and ATO System

The reform, introduced in 1994 with the Galli Law, provides for the organisation of water supply and sewerage through the aggregation of municipal utilities into Optimal Territorial Areas.

Firstly, it consecrated the recognition of water as 'a public good and as a resource which must be protected and utilised according to criteria of solidarity'. Secondly, the main goals of this reform were to reduce the fragmentation of the organisational framework by charging the operator with both drinking water production and distribution.

The ATO system created the framework through which ACEA expanded beyond Rome. By winning management contracts for regional water authorities, ACEA could grow without acquiring the underlying municipal infrastructure.

The 2010 Referendum and Its Aftermath

Italy's 2011 referendum on water privatization added complexity. Citizens voted to keep water services public—but the practical meaning of "public" remained contested. ACEA's mixed ownership structure positioned it awkwardly: majority public, but with private shareholders expecting returns.

In the Italian policy debate, public ownership has been raised as a possible solution to the sector's difficulties. This appears to be in line with a European political and cultural climate that is moving towards an enhanced role for municipalities in organisational and ownership structures.

The Unlock Italy Decree (2014)

On 11 November 2014 the Italian government enacted its 'Unlock Italy' set of economic reforms. This decree facilitates the reduction of municipal multi-utility holdings in the water sector to reduce debt. It also builds on the 2012 Development Decree that laid out tendering terms for awarding public water concessions to private operators, which includes longer term tariff visibility and less risk for ownership transfers.

As part of 2015 budget negotiations, the government envisions greater regional consolidation to create fewer, more efficient water utilities led by potential national champions such as Acea SpA, Gruppo Hera, Iren Group, and A2A.

This regulatory evolution positions ACEA as a potential national champion—one of a handful of operators capable of driving the consolidation Italy needs to modernize its water infrastructure.

ARERA: The Regulatory Framework

The Italian Regulatory Authority for Energy, Networks and the Environment (Autorità di Regolazione per Energia Reti e Ambiente, ARERA) is an independent body created under Italian Law No. 481 of 14 November 1995 for the purposes of protecting consumer interests and promoting the competition, efficiency and distribution of services with adequate levels of quality, through regulatory and control activities.

In December 2011, the Italian Authority for Electricity and Gas was assigned regulatory and control functions over water regulation in Italy. Since then, the presence of the regulator has promoted decision-making among stakeholders and contributed to the development of the sector by increasing transparency, facilitating industry aggregation and promoting investments.

ARERA's role in setting tariffs and investment incentives directly impacts ACEA's returns. Understanding this regulatory framework is essential for investors evaluating the company.

VII. Modern Era: Strategic Acquisitions & Diversification (2015-Present)

The past decade has seen ACEA pursue a disciplined acquisition strategy focused on three themes: consolidating water leadership, building environmental services capacity, and entering gas distribution. Each initiative extends the company's infrastructure footprint while maintaining the regulated revenue streams that provide earnings stability.

Gas Distribution Entry (2018-2019)

In October 2018, we entered this sector via the acquisition, completed in March 2019, of a 51% stake in Pescara Distribuzione Gas, the company that manages the entire gas distribution network for the municipality of Pescara.

In 2020, we also acquired a 51% stake in Alto Sangro Distribuzione Gas, which operates in twenty-four municipalities in the province of L'Aquila, enhancing our presence in the sector as regards the region of Abruzzo.

Gas distribution represents natural adjacency for ACEA. The skills required—network management, metering, customer service, regulatory compliance—transfer directly from water and electricity distribution.

The Peschiera Concession Renewal

On 10 July 2019, Acea, the Rome Municipality and the Lazio Region signed the renewal of the concession until 2031 for the management of the Peschiera aqueduct, an agreement made in light of the plan to double its size.

The renewal of the concession for the Peschiera-Le Capore springs, the lifeblood of the aqueduct, has been a crucial step. This agreement made it possible to start construction of the second line of the infrastructure in 2020.

This concession renewal—extending through 2031—provides visibility into ACEA's most critical infrastructure asset. The doubling project represents the company's largest capital commitment.

Environmental Sector Build-Out (2019-2023)

ACEA's environmental services expansion involved numerous acquisitions:

Acquisition of a 90% stake in Demap, a company specialised in the treatment of plastics and owner of a plant in Beinasco, in the province of Turin. Consolidation in the plastic recycling sector via the acquisition of a 70% stake in Serplast and a 60% stake in Meg, which own facilities located respectively in the Abruzzo and Veneto regions.

Growth in the engineering and construction of environmental and water treatment plants via the acquisition of a 70% stake in Simam, a leading company in the engineering, construction and management of water and waste treatment facilities, and in environmental interventions and remediation, with high-tech integrated solutions. In April 2023 Acea has finalised its acquisition of the remaining 30% stake in Simam.

Acquisition of Deco SpA and, through the latter, of a 100% stake in Ecologica Sangro SpA. Deco operates in the waste management sector in Abruzzo, designing, building and operating facilities used in the treatment, disposal and recovery of solid urban waste and in the recovery of energy from renewable sources.

The economic value of the Simam transaction, in terms of enterprise value for 100% of the company, is equal to 30 million. Acea had acquired 70% of the company's capital in May 2020.

ASM Terni Business Combination (2022-2023)

The ASM Terni deal exemplifies ACEA's approach to regional expansion:

In December 2022, we completed the closing for the first phase of the business combination transaction with ASM Terni, aimed at creating a multi-utility active in the Umbria region in the integrated water cycle, distribution and sale of electricity and gas and waste management sectors.

In April 2023 the second closing completing the combination transaction between Acea, ASM Terni and the Terni Municipality has been finalised.

Following the completion of this agreement, Acea's stake in the share capital of Asm rises to 45% and the Umbrian utility acquires 20% of the capital of Orvieto Ambiente, the spinoff company of Acea Ambiente. Thus, the first integrated multi-utility in Umbria is strengthened, an industrial reality active in the water sector, in waste management, in the production of electricity and in the distribution and sale of electricity and gas.

The ASM Terni structure—where ACEA takes a significant minority stake and industrial partnership role rather than full control—represents a template for expansion into regions where outright acquisition faces political resistance.

Open Fiber Partnership

On 12 January 2018, Acea and Open Fiber stipulated an agreement for the development of an ultra-wide band communication network in Rome.

The Open Fiber partnership leveraged ACEA's network access and civil engineering capabilities for fiber deployment—an example of infrastructure adjacency driving new revenue opportunities.

VIII. Business Model Deep Dive: The Four Pillars

ACEA's business model rests on four pillars, each with distinct characteristics, growth profiles, and competitive dynamics.

1. Water Segment: The Core Business

The contribution of the various areas to consolidated EBITDA is as follows: Water Italy 53%.

Water dominates ACEA's economics. The Italian Water Utility industry is a €7.8B market according to the 2022 Blue Book. ACEA with €1.2B in revenue in 2021 is the largest player with 15% market share.

Acea, the leading water operator in Italy and the second largest in Europe, serving 11 million people in Italy and 10 million abroad.

With over 56,000 km of drinking water networks, 23,000 km of sewerage network, and 1,365 wastewater treatment plants, Acea focuses on innovation and on improving the efficiency of infrastructure and networks.

The water segment benefits from regulated revenues, long-term concessions, and essential service demand that persists regardless of economic cycles. ACEA manages the complete water cycle—from springs to treatment—providing vertical integration that smaller operators cannot match.

WATER Italy - EBITDA for the sector, amounting to 823.8 million Euro, shows an increase of 10.7% with respect to 2023 mainly as a result of organic growth driven by the investments carried out and the implementation of the tariff update as per the new regulation MTI-4.

2. Energy Infrastructure & Networks Segment

Grids and Public Lighting 28%.

Beyond water, Acea manages Rome's electricity network, the most extensive urban network in Europe, with investments of 2.3 billion euros in energy efficiency and flexibility through 2030.

It supplies 9 TWh of electricity to Rome and the surrounding municipalities, managing its public and artistic lighting.

ACEA's electricity distribution network serves as Rome's primary power infrastructure. The segment benefits from regulated returns on the Regulatory Asset Base (RAB)—a framework that rewards capital investment with predictable returns.

Acea is one of the leading Italian players in the energy generation from renewable sources, with 750 GWh of energy produced. It is particularly present in the photovoltaic sector with a power of 101 MW, in the thermoelectric sector with 110,7 MW and in the hydroelectric one with 119,3 MW.

3. Environment Segment

Environment 4%.

The Acea Group is responsible for waste management with 1.8 million tons of waste managed every year. With an eye on a circular economy, it manages composting plants like the one in Aprilia, the largest in Lazio, and the anaerobic digestion plant of Monterotondo Marittimo in Tuscany.

In 2019, Acea entered the plastics treatment sector. It also manages waste-to-energy plants in San Vittore and Terni.

The environment segment represents ACEA's bet on the circular economy. While smaller than water or networks, environmental services offer growth potential as Italian waste management evolves toward higher value-added treatment and recovery.

4. International Operations

Beyond Italy, the industrial Group also has an international presence, particularly in Latin America, with consolidated operations in Peru, Honduras, and the Dominican Republic, where integrated water services serve over 10 million people. In Peru, it carries out operational management activities including water abstraction system, treatment, and the supply of drinking water, as well as the maintenance of the water and sewerage network in Lima. In the Dominican Republic, the Group manages the technical-commercial aspects of the water service, while in Honduras, it operates the water service in San Pedro Sula under concession.

International operations provide diversification but remain a minority contributor to group economics. The Latin American presence demonstrates ACEA's water management capabilities can translate across geographies.

IX. Current Strategy: Green Diligent Growth (2024-2028)

In March 2024, ACEA unveiled its five-year business plan under the banner "Green Diligent Growth"—a strategy that doubles down on regulated infrastructure while emphasizing sustainability and operational efficiency.

The Plan, which we have called "Green Diligent Growth", envisages significant growth and focus on three regulated businesses aimed at making our infrastructure more and more sustainable and resilient, with investments totalling 7.6 billion Euro to sustain the country's development.

Investment Program

The business plan calls for investments in the period 2024-2028 of EUR7.6 billion, where 91 percent of capex will be allocated to regulated activities.

Overall investments will amount to €7.6 billion, with average annual capex corresponding to €1.5 billion, compared with around €1 billion during the period 2020-2023.

Consolidated RAB (Regulatory Asset Base) will reach €10.5 billion by 2028, up by 42% compared with 2023, indicating a CAGR of over 7% during the plan period.

The RAB growth trajectory matters enormously for investors. Regulated utilities earn returns on their RAB—so growing the RAB translates directly to growing earnings power.

Financial Targets

Italian utility operator ACEA said that it expects earnings before interest, taxes, depreciation and amortisation (EBITDA) and net profit to grow by 5% each year on average, as it unveiled its 2024-2028 business plan.

Under its "Green Diligent Growth" plan, the company projected EBITDA of 1.80 billion euros in 2028, compared with 1.39 billion euros last year, mainly driven by "organic growth and operating efficiency". It also expects net profit to reach 350 million euros in 2026 and 375 million in 2028, up from 294 million euros in 2023.

Management also flagged that the group's net financial position-to-EBITDA ratio could decline to 3.1 times in 2028 from 3.5 times in 2023.

The Peschiera Doubling Project

Among the Group's flagship projects is the doubling of the Peschiera Capore Aqueduct: the main water infrastructure project in Italy, with an investment of 1.5 billion euros to ensure the capital's water supply.

The first and most important phase of the project consists in completing the second section of the pipeline: a new gallery which is about 27 km, starting from the sources of the river Peschiera and reaching the intersection with the Salisano aqueduct.

The Peschiera-Capore System, built in the 1930s, has operated continuously for over 80 years and needs updating to ensure continuity of service in the water supply. Reduce the risk of outages in the current system, which could have serious impacts on the water supply.

The Peschiera doubling represents exactly the kind of long-lived infrastructure investment that creates durable value. Once completed, the new pipeline will serve Rome for decades—potentially a century or more.

NRRP Funding

We've received €227 million in funding for 2021-2026. This money will be used for key water sector projects.

The NRRP has provided a historic boost in accelerating interventions on networks and plants.

European recovery funding—channeled through Italy's National Recovery and Resilience Plan—provides ACEA with access to subsidized capital for infrastructure improvement. This external financing enhances returns on equity for investments that would be made regardless.

Dividend Policy

ACEA said it is targeting a 4% annual growth rate for its dividend per share, which stood at 0.88 euros in 2023, with a total return to shareholders of more than 1 billion euros throughout the plan.

The 2024-2028 Business Plan provides for the distribution of over €1 billion (accrual-based) during the plan period, with an annual DPS (Dividend per Share) growth of 4% compared with 2023.

The dividend commitment signals management's confidence in cash generation. For income-oriented investors, ACEA offers a combination of current yield and growth that few European utilities can match.

Technology & Innovation

We employ advanced technologies such as digital twin, robotics, predictive maintenance, and smart metering to optimize the network, reduce losses, and ensure the safety of our technicians. With the Robotics for Water project, we are among the first companies in Europe to introduce intelligent underwater robots to inspect water pipelines in operation, without service disruption.

Technology investment supports both operational efficiency and service quality. In a regulated environment where returns are tied to performance metrics, technology that reduces losses and improves service translates to better regulatory outcomes.

X. Competitive Analysis: Porter's Five Forces & Strategic Position

1. Threat of New Entrants: LOW

The barriers to entry in water distribution are nearly insurmountable. Consider what a new entrant would need:

- Physical infrastructure: Tens of billions of euros to replicate pipeline networks built over decades

- Concessions: Long-term agreements with municipalities that lock in existing operators

- Technical expertise: Water system management requires specialized knowledge accumulated over generations

- Regulatory relationships: The ATO system and ARERA oversight create complexity that favors established players

On 10 July 2019, Acea, the Rome Municipality and the Lazio Region signed the renewal of the concession until 2031 for the management of the Peschiera aqueduct. Concessions like this create regulatory moats that persist for years or decades.

2. Bargaining Power of Suppliers: LOW-MODERATE

Water is a natural resource—ACEA doesn't purchase its primary input from suppliers who can demand higher prices. The company sources from springs (Peschiera-Capore) and manages the entire supply chain.

Equipment and construction suppliers hold moderate power, but ACEA's scale provides negotiating leverage. The €7.6 billion investment program makes ACEA one of Italy's largest infrastructure customers.

3. Bargaining Power of Customers: LOW

Customers cannot easily switch water providers—there's typically one pipeline to each property. Demand is highly inelastic; people need water regardless of price.

Regulatory oversight limits pricing power, but also protects against customer defection. The tariff framework ensures reasonable returns while keeping prices affordable.

4. Threat of Substitutes: VERY LOW

There are no substitutes for municipal water supply at scale. Bottled water serves specific use cases but cannot replace piped water for household needs. Rainwater collection and wells serve rural areas but not urban Rome.

5. Competitive Rivalry: MODERATE-LOW

In water, ACEA faces limited competition within its service territories. Concession structures create local monopolies. Competition exists primarily in bidding for new concessions—where ACEA's scale, expertise, and financial resources provide advantages.

As part of 2015 budget negotiations, the government envisions greater regional consolidation to create fewer, more efficient water utilities led by potential national champions such as Acea SpA, Gruppo Hera, Iren Group, and A2A.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: ACEA benefits from scale in water operations, spreading fixed costs across millions of customers. Network operations involve significant fixed costs for monitoring, maintenance planning, and regulatory compliance that don't scale linearly with customer count.

Network Effects: Limited direct network effects, though ACEA's infrastructure becomes more valuable as Rome grows and more connections join the network.

Counter-Positioning: ACEA's mixed public-private ownership creates a positioning that pure private operators cannot easily copy. The combination of public service mission and commercial efficiency serves both political and financial stakeholders.

Switching Costs: Extremely high. Changing water suppliers would require rebuilding physical infrastructure—effectively impossible for residential customers.

Cornered Resource: ACEA controls access to the Peschiera-Capore springs through its concession—a literal cornered resource that competitors cannot access.

Branding: Limited relevance in regulated utility services where choice is absent.

Process Power: ACEA has accumulated operational expertise over 115 years. The company's ability to manage complex water systems efficiently represents institutional knowledge that cannot be quickly replicated.

XI. The Bull and Bear Case

The Bull Case

1. Essential Infrastructure with Regulated Returns

ACEA owns and operates infrastructure essential to daily life. Among the Italian multiutility companies, we are the industrial entity with the highest percentage of regulated business: 87% of our 2024 EBITDA came from regulated sectors (Water Italy, Grids & Public Lighting and Environment).

Regulated returns provide visibility and stability that few business models can match. The RAB-based regulatory framework rewards capital investment with predictable returns.

2. Consolidation Opportunity

Italy's fragmented water sector provides acquisition opportunities. A significant reduction in the number of operators in the Italian water industry was observed in 2017 compared with 2012, from around 2,900 (most of which were small) to 2,100.

As the largest operator, ACEA can participate in consolidation from a position of strength—acquiring smaller operators and bringing operational efficiency.

3. Infrastructure Investment Tailwinds

European and Italian policy supports infrastructure investment. NRRP funding, EU sustainability directives, and Italian regulatory reform all favor investment in modernizing water and energy infrastructure.

4. Undervaluation Relative to Peers

ACEA(Ticker:ACE) trades at a 9PE and 6% dividend yield vs a peer average of 32PE and 3% dividend yield.

Italian utilities trade at significant discounts to US and UK peers. If this discount narrows, shareholders benefit from multiple expansion alongside operational growth.

5. Execution Track Record

The 2024 results demonstrated management's ability to execute: Results reach all-time high in terms of EBITDA and net profit, in excess of guidance, confirming the stability and strength of the group's industrial model. EBITDA: €1,557m, +12% versus 2023 (recurring EBITDA €1,515m, +11%, approximately 87% from regulated sectors).

Consolidated revenue €4,270 million, EBITDA €1,557 million +12% vs 2023, Group net profit €332 million +18% vs 2023.

The Bear Case

1. Political Risk from Municipal Control

Rome's 51% stake means political priorities can override commercial logic. Changes in city government could affect strategic direction, dividend policy, or management selection.

According to Consob data, as at 31 December 2024 the other direct or indirect significant shareholdings are owned by Suez SA (23.33%) and Francesco Gaetano Caltagirone (5.45%).

The shareholder structure creates complexity. Suez, as a strategic shareholder with its own global water ambitions, may not always align with other minority shareholders.

2. Italian Regulatory Uncertainty

Italy's water sector reform has proceeded slowly and inconsistently. The Italian political scientist Andrea Lippi argues that "most of the essential prerequisites (for the Galli reforms to succeed) were missing". According to him, the Galli law had "offered Italian politicians a solution to escape away from a persistent legitimacy problem" by "adopting an innovative and fashionable legal framework" that was ultimately unable to fulfill the strong expectations for improvement that it had created.

Regulatory uncertainty creates risk around tariff structures, concession renewals, and investment returns.

3. Infrastructure Execution Risk

The €7.6 billion investment program requires executing major projects including the Peschiera doubling. The doubling of the aqueduct shows similarities with cases followed in the last two years by the Citizens' Observatory for Green Deal Financing. In fact, Peschiera–Le Capore is one of several high-impact projects included in the recovery plan that have been accelerated under the new EIA procedure adopted by the Italian government.

Environmental opposition and permitting challenges could delay critical projects, affecting returns on invested capital.

4. Rising Interest Rates Impact

Net financial costs are up by 8.0 million Euro to 144.5 million Euro, essentially due to the rise in interest rates and the increase in average debt.

While ACEA has managed interest rate exposure well (91% fixed rate debt), higher rates increase the cost of new financing for growth investments.

5. Environmental/Climate Risks

According to the Tiber River Basin Authority, its ecological outflow, the volume of water necessary for an aquatic ecosystem to continue to thrive and provide essential services, is 1,600 litres per second.

Water scarcity, climate change, and environmental pressures could affect both source availability and regulatory requirements. Balancing extraction rights with environmental needs creates ongoing tension.

XII. Key Performance Indicators for Monitoring

For investors tracking ACEA's ongoing performance, three metrics deserve particular attention:

1. Regulatory Asset Base (RAB) Growth

RAB growth directly drives earnings power in regulated utilities. Consolidated RAB will reach €10.5 billion by 2028, up by 42% compared with 2023, indicating a CAGR of over 7% during the plan period.

Monitoring actual RAB growth versus plan provides early indication of execution success. RAB growth below plan would suggest capital deployment challenges; growth above plan could indicate acceleration opportunities.

2. Water Segment EBITDA Growth

As the largest contributor to group economics, water segment performance drives overall results. EBITDA of the Water Italy regulated business is expected to show a steady increase (CAGR 2023-2028 +7%), driven by organic growth.

Quarterly water EBITDA versus year-ago periods provides the clearest signal of operational health. Deviations from expected growth rates warrant investigation into tariff realization, volume trends, or cost pressures.

3. Net Debt / EBITDA Ratio

At 31 December 2024, the Net Debt/EBITDA ratio stands at 3.18x, with a notable improvement compared to both 31 December 2023 (3.49x) and guidance (~3.4x).

This ratio balances growth ambitions against financial prudence. The business plan targets 3.1x by 2028. Deterioration above 3.5x would signal leverage concerns; improvement below 3.0x might indicate investment underspend or acquisition capacity.

XIII. Conclusion: The Eternal City's Essential Partner

ACEA's 115-year history offers lessons about infrastructure investing that transcend any single company. Essential services create durable businesses. Municipal roots provide both constraints and opportunities. Patience—measured in decades, not quarters—rewards those who maintain long-term perspective.

The first electric lights to illuminate the streets of Rome were switched on from here at the Montemartini power plant. Having opened in 1912, the Montemartini power plant accompanied the expansion of Rome and increased its productive capacity precisely in order to meet the energy needs of a constantly evolving city. Its over one hundred-year history is indissolubly linked to that of the capital.

Today, that original power plant houses a museum—ancient Roman sculptures displayed among industrial machinery from Rome's early electrification. In the late 1980s, Acea decided to undertake a complete renovation of the historic plant: the Engine Room and the new Boiler Room, with its underlying rooms, were transformed into an Art Center and multimedia center.

The juxtaposition captures something essential about ACEA: an organization that bridges Rome's ancient heritage and modern needs, managing infrastructure that connects past and future.

For investors, ACEA presents a distinctive opportunity: exposure to essential infrastructure serving millions, regulated returns that provide stability, and growth potential from Italian market consolidation and infrastructure investment. The risks are real—political complexity, regulatory uncertainty, execution challenges—but the underlying asset base represents physical infrastructure that will serve Rome for generations to come.

The central question posed at the outset—how a municipal power company became Italy's water champion—has an answer rooted in consistent execution over more than a century. ACEA built the infrastructure that made Rome's modern life possible, then expanded that capability across Italy and internationally.

CEO Fabrizio Palermo stated: "The strong discipline on costs and investments is a key aspect of our strategy to support cash generation combined with optimisation of our financial structure and capital allocation".

The next chapter will be written over the coming decades. The Peschiera doubling, when complete, will serve Rome for a century or more. The environmental services build-out positions ACEA for the circular economy transition. The continued consolidation of Italian water creates opportunities for national champions willing to invest.

For patient capital seeking essential infrastructure exposure with regulated returns, ACEA merits serious consideration. The company that lit Rome's first electric streetlights continues its mission: ensuring the eternal city has the water, power, and environmental services its citizens need.

Material Regulatory and Legal Considerations:

Investors should note ACEA's exposure to regulatory decisions by ARERA that directly impact tariff structures and investment returns. The company's majority ownership by Roma Capitale creates governance dynamics different from fully private companies. Concession renewal risks exist for various operating territories, though the Peschiera concession extends through 2031. Environmental permitting for the Peschiera doubling project faces ongoing review and potential opposition.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube