Crédit Agricole S.A.: From French Farmers' Bank to Global Financial Giant

I. Introduction & Episode Roadmap

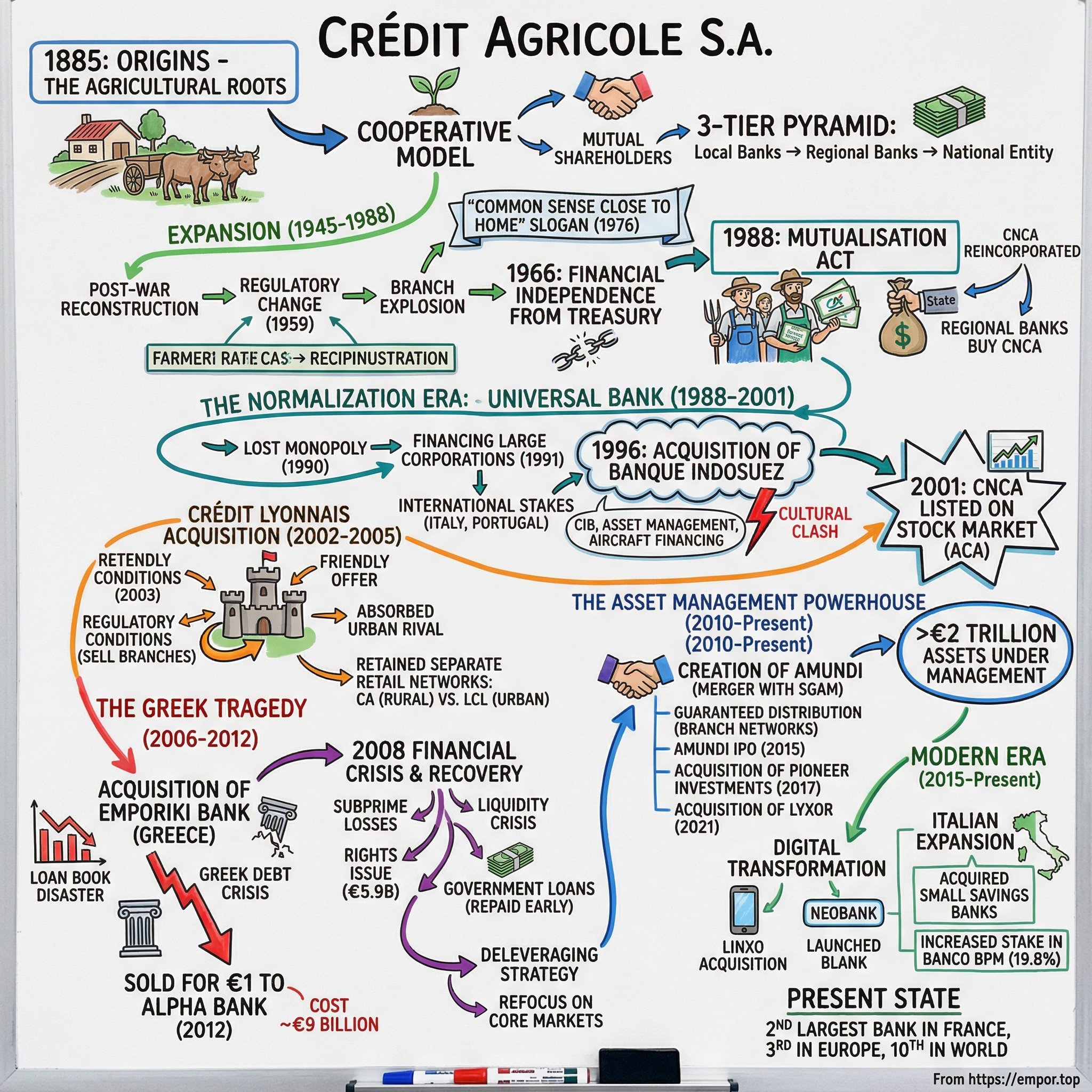

Picture this: It's 1885 in the rolling hills of the Jura region in eastern France. The phylloxera plague has devastated vineyards, agricultural prices have collapsed, and French farmers are living through what historians would later call "the great depression of European agriculture." In this unlikely moment of crisis, two visionaries—a local entrepreneur and a Parisian legal scholar—meet in the small town of Salins-les-Bains to create what seems like a modest experiment in rural finance.

Alfred Bouvet (1820-1900), a local entrepreneur, and Louis Milcent (1846-1918), a landowner and former legal assistant at France's Conseil d'Etat, gather 72 farmers to establish something revolutionary: a bank owned by its customers, where farmers could borrow from each other at reasonable rates. They call it the Caisse de crédit mutuel agricole de l'arrondissement de Poligny.

Fast forward 140 years. That small farmers' cooperative has morphed into Crédit Agricole S.A., the second largest bank in France, after BNP Paribas, as well as the third largest in Europe and tenth largest in the world. With total assets of 2.19 trillion euros in 2023, it's a universal banking colossus operating across retail banking, corporate and investment banking, asset management, and insurance. The transformation is so complete that today, agriculture represents just a tiny fraction of its business.

How did a bank created to help farmers buy oxen become a global financial powerhouse managing more wealth than the GDP of most countries? How did it survive two world wars, navigate France's complex political landscape from monarchy to republic to Vichy to modern democracy, and emerge from the 2008 financial crisis stronger than many of its peers? And perhaps most intriguingly, how has it maintained its cooperative structure—where local farmers still technically own the bank—while competing with the world's most sophisticated financial institutions?

This is a story of paradoxes. It's about a mutual bank that went public, a farmers' cooperative that became an investment banking powerhouse, and a French institution that tried to conquer Europe—sometimes with spectacular success, sometimes with equally spectacular failure. We'll explore the genius moves, like the 2010 creation of Amundi, now Europe's largest asset manager. And we'll dissect the disasters, like the Greek tragedy of Emporiki Bank that cost the bank over €5 billion.

But at its core, this is a story about navigating the fundamental tension in modern finance: Can you serve both local communities and global capital markets? Can you be both a cooperative and a corporation? Can you maintain a social mission while maximizing shareholder returns?

The answer, as we'll see, is complicated. And that complexity makes Crédit Agricole one of the most fascinating case studies in modern finance.

II. Origins: The Agricultural Roots (1885–1945)

The France of 1884 was a nation in agricultural crisis. The phylloxera destroyed the vignes, production agricole fell, prices collapsed, and the petiteness of exploitations didn't favor profitable cultures. The farming world was living through a great depression. Banks viewed farmers as unbankable—too poor, too risky, lacking collateral. When farmers did manage to secure loans, if the farmer went to the notary or banker, they lent at an interest rate too high for him to manage.

Enter Louis Milcent, a fascinating character who embodied the contradictions that would define Crédit Agricole. A "grand bourgeois established on his property and attentive to its management," a confirmed jurist (auditor at the Conseil d'Etat) and excellent orator, Milcent wasn't your typical rural reformer. He was a Parisian intellectual who married into landed wealth, yet he understood viscerally the struggles of small farmers.

At a meeting on November 17, 1884, establishing the Agricultural Union of Poligny, Milcent delivered a speech that would change French banking history. He painted a vision not just of credit, but of solidarity—farmers pooling their meager resources to lend to each other, cutting out the predatory middlemen. Mutualism is a socio-economic model that consists of bringing together people who share the same goal. Mutual shareholders pool money in a "fund" and can lend money to members of society according to their needs.

Three months later, on February 25, 1885, the "Caisse de crédit mutuel agricole de l'arrondissement de Poligny" was created. The first headquarters? A house situated opposite the fairground of Barbarine in Salins-les-Bains—symbolically placed where farmers gathered to trade livestock.

The early loans were almost touchingly modest. Borrowers - "honest and hard-working farmers" - could obtain loans of up to 600 francs, the price of two draught oxen. These weren't loans for speculation or expansion—they were survival capital, allowing farmers to buy seed for next season or replace a dead animal.

What made this model revolutionary wasn't the amounts but the structure. This was a three-tier pyramid that would become Crédit Agricole's defining characteristic: local banks owned by farmer-members, regional banks owned by the local banks, and eventually a national entity coordinating it all. Each level maintained independence while benefiting from the collective strength. It was federalism applied to finance.

The French government, desperate to modernize agriculture and stem rural exodus, took notice. The 1894 Act, championed by Agriculture Minister Jules Méline, authorized the creation of similar local banks nationwide. But crucially, the government provided no funding—these banks had to bootstrap themselves through member contributions. The 1894 Act conferred no particular financial advantages on Local Banks, which quickly found themselves running out of capital. In 1897, the government ordered the Banque de France to provide Crédit Agricole with funding in the form of an endowment of 40 million gold francs.

The structure grew with remarkable speed. By the time of the First World War, every département had at least one Regional Bank. But growth brought challenges. The local banks were run by farmers with little financial expertise. Fraud was common. Some regional banks collapsed. The model needed professionalization.

World War I paradoxically strengthened Crédit Agricole. The bank was called upon to finance the redevelopment of derelict land and restore farms located close to the front line. It was also called upon to extend preferential loans to disabled ex-servicemen and civilian casualties. The crisis had revealed the strategic importance of agricultural finance to national security.

In response, the government created a central coordinating body in 1920. The Act of 5 August 1920 established the Office National du Crédit Agricole, giving greater autonomy to what had previously been no more than a department of the Ministry of Agriculture and creating a central clearing organisation for the Regional Banks. In 1926, this central clearing organisation was renamed Caisse Nationale de Crédit Agricole (CNCA). This public sector institution sits atop Crédit Agricole's institutional "pyramid".

The interwar period saw Crédit Agricole gradually expand beyond pure agricultural lending. In the 1920s, Crédit Agricole expanded its geographical footprint and made its first forays into new areas of business, extending loans to small rural tradesmen, financing rural electrification in 1923, granting the first home loans to farmers of limited means in 1928. This mission creep would become a defining pattern—each crisis or opportunity pushing the bank further from its agricultural roots while maintaining the fiction of its original purpose.

The 1930s brought the Great Depression and another test of the model. The Local and Regional Banks did not emerge unscathed from the 1930s crisis. The most exposed were supported by CNCA, which stepped up its supervisory activities. A joint deposit guarantee fund was set up in 1935. The mutualist structure proved its worth—stronger regions supporting weaker ones, the collective absorbing shocks that would have destroyed individual banks.

Then came Vichy and Nazi occupation. The Vichy regime strengthened state control over Crédit Agricole, though this was only a temporary state of affairs. However, the institution underwent a major financial transformation during the period: Crédit Agricole issued its first five-year notes, funnelling rural savings to the Treasury. The bank had learned to survive by making itself useful to whatever regime held power—a skill that would serve it well in the decades to come.

III. Post-War Expansion & Independence (1945–1988)

If the first sixty years of Crédit Agricole were about survival and slow growth, the post-war era was about explosive expansion and the gradual transformation from agricultural lender to universal bank. This period would see the bank throw off government control, expand internationally, and lay the groundwork for becoming a financial superpower.

The immediate post-war years were about reconstruction. France's agricultural sector had been devastated, and Crédit Agricole became the government's primary tool for modernization. The bank's branch network exploded: The regional banks opened many offices, with the total increasing from 1,000 in 1947 to 2,259 by 1967. Every small town in France soon had its green-signed Crédit Agricole branch, becoming as much a part of the rural landscape as the church steeple.

But the real transformation began in 1959 with a seemingly minor regulatory change. In 1959, Crédit Agricole was authorised by decree to finance property loans for primary residences in rural areas, irrespective of the status of the owner (even non-farmers). This was the thin end of the wedge. Once you could lend to non-farmers for houses, why not for cars? Why not for consumer goods? The mission creep accelerated.

The 1960s brought modernization under Paul Driant, the first Chairman of CNCA to come from a farming background. He remained in this position for 14 years. Despite his agricultural roots, Driant understood that Crédit Agricole's future lay beyond farming. Under his leadership came the pivotal moment of 1966.

In 1966, Caisse Nationale de Crédit Agricole became financially independent, with deposit inflows no longer passing through the Treasury. This wasn't just an accounting change—it was liberation. For the first time since 1920, Crédit Agricole controlled its own money. The government could no longer raid its coffers to fund other priorities. The bank could now think strategically about its future.

The 1970s saw the arrival of what would become Crédit Agricole's most famous slogan: "Le bon sens près de chez vous" ("Common sense close to home"), launched in 1976. The genius of this tagline was how it positioned the bank—not as sophisticated or international (which it increasingly was), but as local, practical, and trustworthy. You might bank with BNP for prestige, but you banked with Crédit Agricole because they understood you.

The late 1970s and early 1980s marked the beginning of international expansion. The bank opened its first foreign branch in Chicago in 1979, a bold move for an institution that most Americans couldn't even pronounce. But the real action was happening at home, where Socialist President François Mitterrand had just nationalized the banking sector—except for Crédit Agricole, which was already technically owned by the state through CNCA.

This anomalous position—neither fully private nor fully nationalized—created an opportunity. While competitors were paralyzed by government bureaucracy, Crédit Agricole could maneuver. The bank used this period to consolidate its domestic position and prepare for what its leaders saw as inevitable: privatization.

That moment came in 1988, though "privatization" isn't quite the right word for what happened. On 18 January 1988, the CNCA Mutualisation Act came into force. CNCA was reincorporated into a public limited company, with a 90% stake sold to the regional banks and 10% to staff. Crédit Agricole became fully independent of the government, putting an end to the latter's practice of skimming off surplus funds.

This was a uniquely French solution—a mutual organization buying itself from the government. The farmers who owned the local banks, which owned the regional banks, now owned the national entity. The law of "mutualization" authorized this very special privatization that allowed the regional banks and employees of the group to buy back from the State the CNCA, previously transformed into a corporation, for the "modest" sum of seven billion francs.

The price was controversial. Critics argued the government had given away a valuable asset for a fraction of its worth. Supporters countered that Crédit Agricole had built its value despite, not because of, government ownership. The debate would rage for years, but the die was cast. Crédit Agricole was now master of its own destiny.

IV. The Normalization Era: Becoming a Universal Bank (1988–2001)

The newly independent Crédit Agricole faced an existential question: What exactly was it? A farmers' bank that happened to do other things? A retail bank with agricultural heritage? Or something else entirely? The answer would come through a series of transformative acquisitions and regulatory changes that would fundamentally alter the bank's DNA.

The transformation began almost immediately after mutualization. In 1990, Crédit Agricole lost the monopoly on granting low-interest loans to farmers and one year later, in 1991, the "normalisation" process was completed as it was allowed to begin financing large corporations. These two changes were seismic. The first removed Crédit Agricole's protected market; the second gave it access to the entire economy.

International expansion accelerated. International expansion continued with the acquisition of stakes in Banco Ambrosiano Veneto in Italy in 1989 and Banco Espírito Santo in Portugal in 1991. These weren't just investments—they were learning experiences. Crédit Agricole was studying how to operate in foreign markets, building capabilities it would need for larger ambitions.

Meanwhile, consolidation began at home. Consolidation among the regional banks began officially in 1990, with the aim of reducing costs. The aim was to halve the number of regional banks, and that objective had been surpassed by the turn of the 21st century. This wasn't popular with local stakeholders who saw their regional identities subsumed, but it was necessary. The cozy world of local agricultural lending was giving way to the brutal efficiency demands of global finance.

The real game-changer came in 1996 with a single acquisition that would transform Crédit Agricole's identity: In 1996, the group bought Banque Indosuez and then created Indocam, an asset management subsidiary (renamed Crédit Agricole Asset Management in 1999), and Crédit Agricole Indosuez for corporate and investment banking.

Banque Indosuez wasn't just any bank. Banque Indosuez was a French bank, the product of the 1975 merger of Banque de l'Indochine and Banque de Suez et de l'Union des mines. It was purchased by Crédit Agricole in 1996, and formed the core of what is now Crédit Agricole Corporate and Investment Bank. This was old French banking aristocracy—the bank that had financed French colonial ventures, that had relationships with every major French corporation.

The acquisition was controversial within Crédit Agricole. Old-timers worried about cultural clash—how could farmers' representatives oversee sophisticated investment bankers? The Indosuez bankers, for their part, were horrified at being bought by what they saw as provincial peasants. The cultural integration would take years, and scars remain to this day.

But strategically, it was brilliant. Crédit Agricole's business was greatly boosted by the acquisition of Indosuez in 1996. It meant the Group was operating in corporate and investment banking, commercial banking, asset management (Indocam) and aircraft financing. Overnight, Crédit Agricole had capabilities that had taken competitors decades to build.

The late 1990s saw further diversification. In 1999, diversification continued as the group took a stake in the newly privatised Crédit Lyonnais, and acquired leading consumer finance company Sofinco. Each acquisition pushed Crédit Agricole further from its roots while paradoxically making it stronger.

The culmination of this transformation came in 2001. CNCA was listed on the stock market in 2001 under the name Crédit Agricole S.A. This gave the regional banks a listed vehicle through which to carry out major acquisitions. The group's acquisitions enabled it to strengthen its leadership in French retail banking, expand its position in corporate and investment banking and build up its international network of branches and subsidiaries.

The IPO was structured in typical Crédit Agricole fashion—Byzantine complexity masking brilliant strategy. The regional banks retained majority control through a holding company, ensuring the cooperative structure remained intact. Public shareholders got economic exposure but limited control. It was the best of both worlds: access to capital markets while maintaining mutual principles.

By 2001, the numbers spoke for themselves. By now, the group was the number-one bank in France with 28% of the domestic market, the global number-two by revenues and number-ten by profits, according to Fortune magazine, and number-15 worldwide according to Forbes rankings. The farmers' bank had become a global giant.

V. The Crédit Lyonnais Acquisition: A Defining Moment (2002–2005)

December 15, 2002. Jean Peyrelevade, the aristocratic CEO of Crédit Lyonnais, sits across from Jean Laurent, chairman of Crédit Agricole, in a Parisian meeting room. The atmosphere is tense. For over a century, these two banks had represented opposite poles of French banking—Crédit Lyonnais, the urban sophisticate founded in 1863, and Crédit Agricole, the rural upstart. Now, in a twist that would have seemed impossible just years earlier, the farmer was about to swallow the city slicker.

The story of how Crédit Agricole acquired Crédit Lyonnais is really three stories: the spectacular rise and fall of Crédit Lyonnais itself, the political theater of French bank privatization, and the strategic brilliance of Crédit Agricole's management team.

The Crédit Lyonnais was a major French bank, created in 1863 and absorbed by former rival Crédit Agricole in 2003. Its head office was initially in Lyon but moved to Paris in 1882. In the early years of the 20th century, it was the world's largest bank by total assets. This wasn't just any bank—this was French banking royalty, the institution that had financed France's industrial revolution.

But by the 1990s, Crédit Lyonnais had become a cautionary tale of banking excess. Under the leadership of Jean-Yves Haberer from 1988 to 1993, the bank had gone on an acquisition spree that would make even the most aggressive private equity firm blush. The strategy was simple: buy everything, everywhere, at any price. The execution was disastrous. By 1993, Crédit Lyonnais had racked up losses that threatened not just the bank but the entire French financial system.

The French government, which owned Crédit Lyonnais, spent the next decade cleaning up the mess. Multiple bailouts, bad bank structures, European Union negotiations—the saga dragged on. By 2002, the government was desperate to get Crédit Lyonnais off its books. They announced an auction.

The opening moves played out like a carefully choreographed dance. In November 2002, the government conducted an auction for its residual ten-percent stake, which was won by BNP Paribas. BNP Paribas, Crédit Agricole's arch-rival, seemed to have won. But Crédit Agricole had been preparing for this moment for years.

What followed was a masterclass in French financial maneuvering. On December 16, 2002, Crédit Agricole S.A. and Sacam Développement presented jointly a friendly public mixed offer on the capital of Crédit Lyonnais. The offer, closed in May 2003, was a success and ended with a public offer of withdrawal in July 2003.

The "friendly" nature of the takeover was crucial. Crédit Agricole didn't want to be seen as a raider. They positioned themselves as saviors, preserving French banking independence against potential foreign buyers. Crédit Agricole's management made every effort to reassure the staff of both companies and said that there would be no redundancy plan. It forecast that the creation of the new entity would result in 4,600 job losses over a three-year period, but stated that 'natural wastage' in both banks combined was already running at 4,500 employees per year.

The regulatory approval process revealed the sheer scale of what Crédit Agricole was attempting. The Banking and Investment Committee gave the green light for the two banks to merge on 13 March 2003, on the condition that the new entity: sells off 85 branches in 18 départements of France during the current year; and places a moratorium on opening new agencies in 32 départements for a period of two years. Even with these restrictions, the combined entity would dominate French banking.

Integration was where the real work began. Crédit Agricole merged its own investment banking arm, Banque Indosuez, with Crédit Lyonnais's and renamed the merged entity Calyon (for Crédit Agricole Lyonnais) in 2004. The name Calyon was widely mocked—it sounded like a synthetic fabric, not a major investment bank. But the substance was serious: Crédit Agricole now had investment banking capabilities to rival any European bank.

The retail network presented different challenges. Its former French retail network survives as LCL S.A., a fully owned subsidiary of Crédit Agricole, under the brand LCL adopted in 2005 with reference to "Le Crédit Lyonnais". The LCL rebrand was brilliant in its simplicity—keeping brand recognition while signaling renewal.

But the masterstroke was keeping the two retail networks separate. Crédit Agricole's rural/suburban network and LCL's urban network barely overlapped. Instead of forced integration and branch closures, Crédit Agricole maintained both, allowing them to compete. Internal competition drove innovation while avoiding the cultural warfare that had doomed many bank mergers.

The numbers validated the strategy. The acquisition cost roughly €16 billion all-in, but it transformed Crédit Agricole into France's undisputed banking champion. Market share in French retail banking approached 30%. The combined investment banking operations could compete for any mandate. The enlarged balance sheet provided the firepower for international expansion.

Yet the Crédit Lyonnais acquisition also marked a turning point in Crédit Agricole's identity. The farmer's bank that had grown by serving rural communities now controlled one of France's most urban, sophisticated financial institutions. The contradictions inherent in this combination would shape every strategic decision that followed.

VI. The Greek Tragedy: Emporiki Bank (2006–2012)

Georges Pauget was not a man who lacked confidence. Appointed CEO of Crédit Agricole in September 2005, the former economics professor had grand visions of European expansion. At a December meeting with the Financial Times at Paris's Plaza Athénée hotel, he laid out his philosophy: "We are not just in France. That is not a real view of our position," Pauget told the reporter, and he was "ready to forget the cautious lessons about banking deals" that he once taught as an economics professor.

Six months later, Pauget would make good on that promise with a deal that would haunt Crédit Agricole for years: the acquisition of Greece's Emporiki Bank.

In June 2006, Pauget pounced on Emporiki Bank of Greece, offering €3.1 billion in cash to take it over. On paper, it looked brilliant. Greece was booming, the Olympics had just showcased a modernizing nation, and euro membership had brought interest rates to historic lows. Emporiki appeared to have potential as the fourth largest residential mortgage provider and the fifth largest consumer credit provider with about 10 percent of the Greek market share. "People in Greece have an average of 2.5 banking products per person, so there is a lot of opportunity," the French bank said in a press release at the time. "In France the average is seven to nine products per person".

But Pauget saw something even bigger. "One can no more understand the vigor and the potential of the Greek economy simply in terms of its 10 million citizens; instead, one must look at it as being inseparable from the broader region's economies," he was quoted saying in 2006. Emporiki wasn't just about Greece—it was Crédit Agricole's gateway to the Balkans, to Turkey, to the entire Eastern Mediterranean.

The warning signs were there from the start. The bank was nationalized in 1975 amid political and economic changes in Greece. In 2006, it was privatized and acquired by the French banking group Crédit Agricole. Emporiki was the Greek government's last major privatization asset, and they were eager to sell. Perhaps too eager.

Greece's biggest foreign investment, the Emporiki sale sparked a strike among Greek employees worried that the new owners would fire many of them. The cultural clash was immediate. French managers arrived in Athens expecting to find a Mediterranean version of Crédit Lyonnais. Instead, they found a bank that operated more like a government ministry—overstaffed, politically connected, with lending decisions often based on relationships rather than risk assessment.

Crédit Agricole threw money at the problem. They invested in new IT systems, brought in French executives, launched new products. By 2008, they had increased their stake to over 90% and invested billions in capital. The transformation seemed to be working—loan growth was strong, market share was increasing.

Then came September 2008 and the global financial crisis. But it was what came next that turned Emporiki from a disappointing investment into an existential crisis for Crédit Agricole.

The onset of the Greek financial crisis severely impacted Emporiki Bank's performance in its home market. The bank faced significant financial difficulties and mounting losses, which strained Crédit Agricole's willingness to maintain its Greek operations.

The Greek sovereign debt crisis that erupted in 2010 revealed the true horror of what Crédit Agricole had bought. Emporiki's loan book was a disaster. Mortgages that would never be repaid, corporate loans to businesses that existed only on paper, consumer credit extended without basic documentation. As Greece's economy collapsed—GDP falling by 25%, unemployment soaring above 25%—Emporiki's losses exploded.

The numbers were staggering. In 2006 the French bank Crédit Agricole bought the Greek Emporiki bank, for €2.8 billion, at the peak of a bull market for bank takeovers. Six years, a major financial crisis, and €5.2 billion of losses later, in a context of great uncertainty in the European banking sector, what decision should Crédit Agricole take regarding Emporiki?

By 2012, Crédit Agricole faced an impossible choice. Continue pouring money into Emporiki, risking the parent company's stability? Or admit defeat and exit, crystallizing massive losses? The French government, worried about Crédit Agricole's exposure to Greece potentially triggering a broader European banking crisis, was applying pressure for a solution.

The end came with shocking swiftness. Crédit Agricole decided to sell Emporiki's Greek business to Alpha Bank in October 2012. The sale was made for the nominal sum of €1, reflecting the distressed condition of the bank. One euro. For a bank they had paid €2.8 billion for six years earlier, plus billions more in capital injections.

The Greek branch Emporiki was separated from its profitable wealthy parts in Albania, Bulgaria and Romania which were integrated into the Crédit Agricole group. The whole investment into Emporiki cost around €9 billion. The remaining Greek part was sold off to Alpha Bank for €1.

The post-mortem was brutal. The aim of this paper is to see how NOT to manage an acquisition through the case study of one of the worst M&As in recent years: Emporiki Bank's by Crédit Agricole. Although the role of the banks is to manage risk, the acquisition of Emporiki by Crédit Agricole shows how easy it is, when ill prepared, to make one mistake after another and get trapped without a way out. It can even cause to take such desperate decisions as in this case sell an entire bank for one single euro.

What went wrong? Everything. Due diligence was rushed. Cultural integration was botched. Risk management was absent. But the fundamental error was strategic: Crédit Agricole had confused being in the European Union with being in Europe. They assumed that European monetary union meant European economic convergence. They learned, at enormous cost, that Greece was not France with better weather.

The Emporiki disaster had profound consequences. It ended Crédit Agricole's international expansion ambitions for years. It contributed to the resignation of CEO Jean-Paul Chifflet in 2015. Most importantly, it reinforced a cultural tendency toward caution that persists to this day. When Crédit Agricole executives consider acquisitions now, someone always asks: "Is this another Emporiki?"

VII. The 2008 Financial Crisis & Recovery (2008–2014)

While Crédit Agricole was wrestling with Emporiki in Athens, a different crisis was brewing in New York. The collapse of Lehman Brothers in September 2008 triggered a global financial catastrophe that would test every assumption about modern banking. For Crédit Agricole, the crisis would prove to be both a near-death experience and, ultimately, a catalyst for transformation.

The first signs of trouble came early. On 18 April 2008, Credit Agricole revealed that it would post $1.2 billion in losses related to subprime mortgage securities. This was before Lehman, before the full crisis. Crédit Agricole's investment banking arm, like many European banks, had gorged on AAA-rated American mortgage securities that were now toxic waste.

As credit markets froze, Crédit Agricole faced a liquidity crisis. The bank's funding model—borrowing short-term to lend long-term—suddenly looked terrifyingly fragile. Although less negatively impacted than some rivals by the 2008 financial crisis, when the interbank lending market seized up, Crédit Agricole was forced in January 2008 to sell its long-standing stake in Suez for €1.3 billion and then in May 2008 to organise a €5.9 billion rights issue to which all the regional banks subscribed to meet Basel II regulatory requirements.

The rights issue was particularly painful. In May 2008 Credit Agricole sought to raise €5.9 billion in equity capital from its shareholders. The shares controversially sold off from €19 to €6 over the successive period as the 2008 financial crisis escalated. Shareholders who participated saw their investment immediately decimated. Those who didn't were massively diluted.

Asset sales accelerated. In May 2008 Credit Agricole identified €5 billion of asset disposals including the bank's 5.6 percent stake in Italian bank Intesa Sanpaolo, which was worth an estimated €3 billion. These weren't strategic disposals—this was a fire sale, selling whatever could find a buyer to raise cash.

Then came the government bailouts. At the end of 2008, the government decided to loan France's six largest banks €21 billion in two tranches, at an interest rate of 8%, to enable them to continue to play their role in the economy. Crédit Agricole did not take part in the second tranche and repaid the government in October 2009. Crédit Agricole's crisis exit strategy was well received by the markets, with the share price gaining more than 40% over 2009.

The fact that Crédit Agricole could repay the government loan early was significant. Unlike American banks that were forced to take TARP money whether they needed it or not, French banks had more flexibility. Crédit Agricole's early repayment signaled strength, distinguishing it from weaker peers.

But the real crisis management happened at the operational level. Jean-Paul Chifflet, who became CEO in 2010, implemented a radical deleveraging strategy. Investment banking assets were slashed. Proprietary trading was eliminated. Complex derivatives were unwound. The transformation was painful—thousands of highly paid investment bankers were let go—but necessary.

The 2008 crisis also revealed an unexpected strength in Crédit Agricole's unusual structure. The regional banks, still owned by their farmer-members, provided ballast during the storm. They continued lending to local businesses and farmers even as capital markets seized up. The boring, old-fashioned retail banking that investment bankers had sneered at became the group's lifeline.

The amount of its provisions to deal with unpaid loans by its clients increased to 3.2 billion euros in 2008 compared to the previous year. The increase involves all the group's units, except its activities in France: international retail banking (880 million euros), consumer credit (627 million euros) and investment banking (1.3 billion euros). The geographic pattern was telling—France held up while international adventures collapsed.

Recovery strategy crystallized around three principles: simplify, refocus, and strengthen. Simplify meant unwinding the complex web of subsidiaries and cross-holdings that had accumulated over decades. Refocus meant returning to core French and European markets. Strengthen meant building capital buffers that would make Crédit Agricole fortress-like in its solidity.

By 2012, the strategy seemed to be working. In 2012, Crédit Agricole continued to report negative results, posting a loss of around €3 billion in the third quarter, but this was largely due to one-time charges for goodwill writedowns and the Emporiki disposal. The underlying business was recovering.

The crisis had changed Crédit Agricole fundamentally. The swashbuckling expansion of the Pauget era was over. In its place was a more cautious, more French, more retail-focused institution. Some saw this as retreat. Others saw it as returning to the bank's true identity. The debate continues to this day.

VIII. The Asset Management Powerhouse: Amundi's Rise (2010–Present)

In the depths of the 2009 financial crisis, with banks failing globally and regulators demanding higher capital ratios, two fierce French rivals made an unexpected decision: they would cooperate. Crédit Agricole and Société Générale, who had competed for over a century, agreed to merge their asset management arms. The result would become one of European finance's great success stories.

Founded on 1 January 2010, the company is the result of the merger between the asset management activities of Crédit Agricole (Crédit Agricole Asset Management, CAAM) and Société Générale (Société Générale Asset Management, SGAM). With €670 billion of assets under management on the eve of its creation, Amundi emerged as the third largest European asset management company, behind Axa and Allianz, and became one of the top 10 biggest asset managers worldwide.

The creation of Amundi was born from crisis but designed for growth. Both parent banks needed capital and saw asset management as non-core. But Yves Perrier, appointed CEO of the new entity, saw opportunity where others saw a distressed merger. Perrier, a Crédit Agricole lifer with the demeanor of a philosophy professor and the instincts of a private equity shark, would transform Amundi into a European champion.

The structure was clever: Crédit Agricole owned 75%, Société Générale 25%, but both banks committed to distribute Amundi products through their branch networks. Amundi's funds are primarily distributed through the banking networks of its majority shareholders: Crédit Agricole, LCL (a subsidiary of Crédit Agricole), Société Générale and Crédit du Nord (a subsidiary of Société Générale), which collectively comprised more than 70% of Amundi's net inflows at inception. This guaranteed distribution was Amundi's secret weapon—while competitors fought for shelf space, Amundi had privileged access to millions of French savers.

The first years were about integration and efficiency. The merger of the two teams took place progressively over the course of 2010 and led to 260 jobs being cut globally, and the creation of about 60 new positions in risk management and commercial distribution. Perrier ran Amundi like a factory—standardized products, industrial-scale processes, razor-thin margins compensated by massive volume.

But Perrier had bigger ambitions. He wanted Amundi to be independent, to prove it could succeed beyond its parent banks' distribution networks. The path to independence would be through an IPO.

On 17 June 2015, Crédit Agricole and Société Générale announced their intention to list Amundi on the stock market before the end of the year. The IPO enabled Société Générale to sell its 20% stake in the company and Crédit Agricole to sell 5%, remaining the majority shareholder with 75% of Amundi's overall share capital. Amundi Group was listed on the Euronext stock exchange on 12 November 2015 with a market capitalisation of 7.5 billion euros. The group's shares were priced at 45 euros per share and ended their first session at just above 47 euros.

The IPO was a triumph, especially given the challenging market conditions. The press contrasted the success of the IPO with those of Deezer and Oberthur Technologies, both of which had to be cancelled prior to Amundi's flotation in the context of a difficult trading environment due to market turbulence in summer 2015. At €7.5 billion, it was the largest French IPO in a decade.

But the real coup came a year later. In December 2016, Amundi announced the 100% acquisition of Pioneer Investments, the asset management subsidiary of Italian bank UniCredit. Pioneer brought €220 billion in assets and, crucially, strong positions in America and emerging markets where Amundi was weak. The price—€3.5 billion—seemed steep, but Perrier promised €180 million in annual cost synergies.

The integration of Pioneer showcased Amundi's operational excellence. Within 18 months, the synergies were achieved. Duplicate products were merged, back offices consolidated, investment teams rationalized. What had taken other firms years, Amundi did in quarters.

In 2017, the Amundi group acquired Pioneer Investments, the asset management subsidiary of Unicredit, and in 2021 acquired Lyxor Asset Management, a subsidiary of Société Générale. The Lyxor acquisition was particularly sweet—Société Générale, having exited Amundi at the IPO, was now selling its remaining asset management business to its former subsidiary. The student had become the master.

By 2023, the transformation was complete. A subsidiary of the Crédit Agricole group and listed on the stock exchange, Amundi currently manages more than €2 trillion of assets. From a crisis merger to Europe's largest asset manager in just 13 years—it was a stunning achievement.

The success of Amundi holds important lessons. First, in financial services, distribution is king. Amundi's guaranteed access to retail networks gave it an unassailable competitive advantage. Second, in asset management, scale matters enormously. Every basis point of cost savings drops straight to the bottom line. Third, cultural integration can work if there's a clear leader—Crédit Agricole's dominance meant no paralysis from equal partnerships.

For Crédit Agricole, Amundi represents redemption after Emporiki. It proves the bank can execute complex acquisitions, can build world-class businesses, can compete globally. For the full year 2023, the Asset Gathering division contributed 38% of the underlying net income Group share of Crédit Agricole S.A.'s core businesses. What started as a defensive merger during a crisis has become one of the group's most valuable assets.

IX. Modern Era: Digital Transformation & Italian Expansion (2015–Present)

Philippe Brassac doesn't look like a revolutionary. The Crédit Agricole CEO, who took the helm in 2015, has the measured demeanor of a career banker who rose through the ranks. But under his leadership, Crédit Agricole has undertaken two transformations that would have seemed impossible to his predecessors: becoming a digital innovator and doubling down on Italy when everyone else was retreating.

The digital transformation began with an admission of weakness. By 2015, Crédit Agricole's technology was embarrassingly outdated. Core banking systems dated from the 1980s. Mobile apps were afterthoughts. Young French customers were fleeing to neobanks like Revolut and N26. Something had to change.

On January 28, 2020, Crédit Agricole announced an 85% stake acquisition in the fintech Linxo for its budget management app. In 2021, the Crédit Agricole group entered the neobank market by launching Blank, a mobile app tailored for self-employed workers, offering them a professional account and an ecosystem of management tools.

The acquisition of Linxo was small—just €24 million—but symbolically important. This was Crédit Agricole saying: we won't build everything ourselves, we'll buy innovation. Blank was even more radical: a neobank created by a 140-year-old institution, targeting millennials and gig workers who would never walk into a traditional branch.

The group continued expanding in the sector in 2022, announcing the launch of two new professional accounts: Propulse by CA and LCL Essentiel Pro through its subsidiary LCL. Both offerings were developed in partnership with Blank via the startup studio La Fabrique by CA. La Fabrique, Crédit Agricole's startup studio, represented a new model—not just investing in fintechs but incubating them, giving them access to 51 million customers as a testing ground.

But technology was just one front in Brassac's transformation war. The other was geographic expansion, specifically in Italy. This seemed counterintuitive—hadn't Emporiki taught them to avoid Southern Europe? But Brassac saw Italy differently. This wasn't Greece 2006; this was a mature, sophisticated market where Crédit Agricole already had presence and could build scale through consolidation.

The Italian strategy unfolded methodically. In 2017, the group bought three small Italian independent saving banks (Banca Carim, Cassa di Risparmio di Cesena and Cassa di Risparmio di San Miniato), in addition to Banca Leonardo through Indosuez Wealth Management. These weren't trophy acquisitions but tactical moves, adding branches in wealthy Northern Italian regions.

Then came the boldest move. In December 2024, Crédit Agricole increased through derivatives its stake in Banco BPM up to 19.8%, the increase was authorized by the ECB in April 2025. Banco BPM is Italy's third-largest bank, and Crédit Agricole's stake makes it the largest shareholder. This isn't a controlling position—Italian regulations and politics make that impossible—but it's enough to influence strategy and potentially engineer a merger with Crédit Agricole's existing Italian operations.

The Italian expansion reflects a broader strategy: European consolidation. Brassac believes that European banking remains too fragmented, with over 6,000 banks compared to fewer than 5,000 in the much larger United States. As the weakest banks fail or seek buyers, Crédit Agricole wants to be a consolidator, not consolidated.

The COVID-19 pandemic tested both strategies. Digital adoption accelerated dramatically—customers who had never used mobile banking were suddenly dependent on it. Crédit Agricole's investments in digital infrastructure paid off. The bank processed record volumes without major outages, while some competitors struggled.

Meanwhile, in Italy, Crédit Agricole played a crucial role in distributing government-guaranteed loans to businesses. The bank's local presence and relationships meant it could assess credit quickly when speed mattered for survival. This built enormous goodwill—and market share.

In August 2023, Crédit Agricole announced its intent to purchase a majority stake in Belgian private bank Degroof Petercam via its subsidiary Indosuez Wealth Management, the acquisition was finalised in 2024 with Crédit Agricole owning a 65% stake in Degroof Petercam. The Degroof Petercam acquisition showed another dimension of the strategy—wealth management for Europe's rich. As European wealth consolidates in fewer hands, Crédit Agricole wants to manage it.

The modern era strategy is working, at least financially. For the entirety of 2023, the group reported over €8 billion in net profit for the third consecutive year. Its insurance division alone grew by 12.6% compared to the previous year, achieving a net result of €1.65 billion. The stock price has more than doubled since Brassac became CEO.

But challenges remain. Digital transformation is expensive and never-ending. Italian expansion is politically sensitive—France buying Italian banks triggers nationalist reactions. And the fundamental question persists: Can a cooperative structure compete in digital banking where winner-takes-all dynamics favor pure technology players?

X. Playbook: Business & Strategy Lessons

After 140 years of evolution, what can we learn from Crédit Agricole's journey? The lessons aren't always what you'd expect from a traditional banking case study. This is an institution that has thrived not despite its contradictions, but because of them.

Lesson 1: The Cooperative Advantage Is Real

It consists of a network of Crédit Agricole local banks, 39 Agricole regional banks and a central institute, the Crédit Agricole S.A.. It is listed through Crédit Agricole S.A., as an intermediate holding company, on Euronext Paris' first market and is part of the CAC 40 stock market index.

The three-tier mutual structure that seems archaic is actually a competitive advantage. The local banks provide stability and customer acquisition at virtually zero cost. The regional banks offer scale and risk diversification. The listed holding company provides access to capital markets. It's a structure that combines the best of mutual and shareholder-owned models.

During crises, this structure provides remarkable resilience. Farmer-members don't panic and withdraw deposits like institutional investors dump stocks. The regional banks can support each other through local economic shocks. The patient capital allows for long-term strategic thinking impossible in quarterly-earnings-obsessed public companies.

Lesson 2: Universal Banking Still Works (If You Do It Right)

Crédit Agricole operates across retail banking, corporate and investment banking, insurance, and asset management. In an era when many banks are specializing, Crédit Agricole remains stubbornly universal. And it works.

The key is genuine synergies, not PowerPoint synergies. Retail branches distribute asset management products and insurance. Corporate banking relationships lead to investment banking mandates. Private banking serves the wealthy clients identified through retail banking. The businesses genuinely reinforce each other rather than just sharing overhead costs.

Lesson 3: M&A Is About Timing and Integration, Not Just Price

Crédit Agricole's M&A track record is mixed—brilliant successes (Crédit Lyonnais, Amundi) and spectacular failures (Emporiki). The difference isn't price paid but timing and integration.

Crédit Lyonnais was bought when the French government was desperate to sell and competitors were distracted. Integration preserved both cultures rather than forcing assimilation. Emporiki was bought at the peak of a bubble with no understanding of local culture and forced integration that destroyed value.

The lesson: In banking M&A, cultural fit matters more than financial models. A 20% lower price doesn't compensate for a failed integration. And timing—buying during crisis, not euphoria—is everything.

Lesson 4: Build Ecosystems, Not Just Products

In 2019, Crédit Agricole drew on its history, its universal banking model and its role as the leading financer of the French economy to formulate its raison d'être: "Working every day in the interest of our customers and society".

Crédit Agricole doesn't just offer banking products; it offers ecosystems. Farmers get not just loans but insurance, investment advice, and succession planning. Corporations get not just credit but cash management, foreign exchange, and capital markets access. The ecosystem creates switching costs and deepens relationships beyond what any single product could achieve.

Lesson 5: Geography Matters More Than You Think

Crédit Agricole's international adventures teach a crucial lesson: banking is still a local business. Success in France didn't translate to Greece. What works in Paris doesn't work in Athens. Cultural understanding, regulatory relationships, and local presence matter more than financial engineering or global brand names.

The corollary: When expanding internationally, buy local franchises with deep roots rather than building from scratch. And stay close to home—Crédit Agricole succeeds in Belgium and Italy, struggles in Greece and Eastern Europe. Geographic proximity correlates with success.

Lesson 6: Patience Is a Competitive Advantage

The cooperative structure gives Crédit Agricole unusual patience. Amundi took five years from merger to IPO. The Italian expansion is playing out over decades. Digital transformation is a rolling multi-year program, not a big-bang implementation.

This patience allows for strategies unavailable to banks facing quarterly earnings pressure. Crédit Agricole can accept lower returns initially to build market position. It can invest through cycles rather than cutting at the first sign of trouble. In finance, where most players are impatient, patience becomes a sustainable competitive advantage.

XI. Analysis & Bear vs. Bull Case

Where does Crédit Agricole stand today? The numbers tell one story: total assets of 2.19 trillion euros in 2023, making it one of Europe's banking giants. But numbers alone don't capture the strategic position of this unique institution.

The Bear Case: Structural Headwinds

The pessimistic view starts with European banking's structural challenges. Europe has too many banks chasing too little growth. Interest rates, while rising, remain historically low. Regulatory costs keep increasing—Basel IV, ESG reporting, digital operational resilience requirements. The regulatory burden falls disproportionately on universal banks like Crédit Agricole that must comply with rules across multiple business lines.

Competition is intensifying from unexpected directions. Big Tech companies are cherry-picking profitable banking products. Neobanks are stealing young customers. American investment banks are dominating capital markets. Crédit Agricole, with its complex structure and legacy systems, seems ill-equipped for this new world.

The cooperative structure, while providing stability, also constrains strategic flexibility. Major strategic shifts require approval from thousands of local board members, many of them farmers with limited financial sophistication. The ownership structure makes transformative M&A nearly impossible—any dilution of the regional banks' control would face fierce resistance.

Italy exposure is particularly concerning. Crédit Agricole is doubling down on Italian banking just as Italy's debt dynamics look increasingly unsustainable. The Banco BPM stake could become another Emporiki if Italy faces a sovereign debt crisis. The bank seems to be repeating its pattern of buying into Southern Europe at the wrong time.

Digital disruption poses an existential threat. Crédit Agricole's digital initiatives, while impressive for a legacy bank, pale compared to native digital players. Young customers don't care about 140 years of history or local presence. They want seamless digital experiences, which Crédit Agricole struggles to provide.

ESG commitments could backfire. Crédit Agricole has actively pursued a sustainable finance strategy, pledging to reduce its carbon footprint and finance the energy transition. But these commitments could constrain profitable lending to carbon-intensive industries while competitors without such scruples gain share.

The Bull Case: Hidden Strengths

The optimistic view sees Crédit Agricole's apparent weaknesses as hidden strengths. Start with the cooperative structure. Yes, it's complex, but it provides unmatched funding stability. The regional banks will never face a bank run. The local presence creates customer acquisition costs that neobanks can only dream of. The patient capital allows for long-term value creation impossible at quarterly-earnings-driven competitors.

For 2023, Crédit Agricole reported €8.3 billion in net profit, demonstrating remarkable earnings power. The diversified business model provides resilience—when investment banking struggles, insurance compensates; when France slows, Italy might accelerate. This diversification is real, not theoretical.

The asset management success with Amundi proves Crédit Agricole can build world-class businesses. Amundi currently manages more than €2 trillion of assets, generating steady, high-margin fees. This isn't a declining traditional bank but a diversified financial services group with growing fee-based revenues.

Scale advantages are increasing, not decreasing. Banking is becoming more technology-intensive, requiring massive investments in cybersecurity, data analytics, and digital infrastructure. Only the largest banks can afford these investments. Crédit Agricole's €2+ trillion balance sheet provides the scale to compete.

European banking consolidation is inevitable, and Crédit Agricole is positioned as a consolidator, not a target. The cooperative structure makes it essentially takeover-proof while allowing it to acquire others. As weaker European banks fail or seek buyers, Crédit Agricole can cherry-pick the best assets.

The Italian strategy could pay off handsomely. Italy isn't Greece—it's the EU's third-largest economy with world-class companies and wealthy individuals. If Crédit Agricole becomes a leading player in Italian banking through consolidation, the returns could be enormous. The Banco BPM stake provides optionality without full acquisition risk.

The Verdict: Resilient but Uninspiring

The truth lies between these extremes. Crédit Agricole is neither doomed nor destined for greatness. It's a resilient, profitable institution that will likely continue muddling through—generating decent returns for shareholders, serving customers adequately, adapting slowly to digital disruption.

The bank's competitive position is solid but not spectacular. In France, it will remain one of three dominant players (with BNP Paribas and Société Générale). In Europe, it will be a second-tier player—large but not leading. Globally, it's a regional champion with limited reach.

For investors, Crédit Agricole offers a classic value proposition: a stable dividend yield, trading at book value, with limited downside but also limited upside. It's a widow-and-orphan stock, not a growth story. For those seeking excitement, look elsewhere. For those seeking 4-5% annual returns with minimal drama, Crédit Agricole fits perfectly.

XII. Epilogue & "If We Were CEOs"

As we close this examination of Crédit Agricole, it's worth stepping back to appreciate the sheer improbability of this institution's journey. A farmers' cooperative bank, founded when horses were the primary form of transportation, has survived and thrived into the age of artificial intelligence and blockchain. Through two world wars, multiple financial crises, and complete transformation of the global economy, Crédit Agricole has not just endured but prospered.

What Would We Do Differently?

If we were running Crédit Agricole today, we'd focus on three strategic imperatives:

First, embrace the paradox rather than resolve it. Crédit Agricole keeps trying to be either a cooperative or a modern bank. Instead, lean into being both. Create a "dual-brand" strategy where the Crédit Agricole brand represents stability, mutualism, and local presence, while building or acquiring pure digital brands for younger, urban customers. Don't try to make the farmer-owned bank cool; create something new that is.

Second, double down on European wealth management. Europe is aging rapidly, wealth is concentrating, and inheritance flows over the next decade will be massive. Crédit Agricole, through Indosuez and recent acquisitions, has strong positions but lacks scale. We'd engineer a transformative merger—perhaps with a Swiss private bank—to create Europe's undisputed wealth management leader. The fee income would reduce dependence on interest margins and create a more valuable multiple for shareholders.

Third, fix Italy or exit. The current strategy of gradual stake building in Banco BPM feels like Emporiki redux—a slow-motion disaster where Crédit Agricole gains exposure without control. Either engineer a full takeover and integration (accepting the political backlash) or sell everything and redeploy capital elsewhere. Half-measures in banking M&A almost always fail.

The Banco BPM Endgame

The ongoing Banco BPM saga deserves special attention. Crédit Agricole increased through derivatives its stake in Banco BPM up to 19.8%, making it the largest shareholder but without control. This limbo can't continue indefinitely.

The endgame likely involves one of three scenarios: (1) Crédit Agricole launches a full takeover bid, probably requiring Italian government blessing and potentially a local partner; (2) Another player, possibly UniCredit, bids for Banco BPM, forcing Crédit Agricole to either counter-bid or cash out; (3) The status quo persists, with Crédit Agricole as a passive investor earning dividends but unable to drive strategy.

Our bet: Within two years, European banking consolidation pressures will force action. Crédit Agricole will either own Banco BPM outright or exit entirely. The current position is unstable and value-destructive for all parties.

Digital Reality Check

The digital transformation efforts, while admirable, feel insufficient. Crédit Agricole is fighting the last war—building better mobile apps when the battlefield has shifted to embedded finance, open banking, and AI-driven services. The bank needs a more radical digital strategy.

We'd propose creating an autonomous digital bank, separately capitalized and managed, with freedom to cannibalize the parent. Give it €5 billion in capital, hire talent from technology companies not banks, and set it loose. Yes, it would compete with traditional Crédit Agricole branches. That's the point. Better to disrupt yourself than be disrupted.

The ESG Opportunity

Crédit Agricole's agricultural heritage provides unique positioning for the sustainability transition. No bank better understands the intersection of finance and food systems. As climate change reshapes agriculture, Crédit Agricole could become the global leader in sustainable food finance.

This means going beyond current ESG commitments to build new businesses: carbon credit trading for farmers, regenerative agriculture financing, alternative protein ventures, vertical farming infrastructure. The opportunity is to own the future of food finance, not just comply with regulations.

Final Reflections

Crédit Agricole's story is ultimately about institutional resilience. Not the flashy resilience of constant reinvention, but the quiet resilience of gradual adaptation. The bank has survived not by predicting the future but by maintaining enough flexibility to respond as the future unfolds.

The three-tier cooperative structure that seems like an anachronism is actually a sophisticated mechanism for balancing stability and change. The local banks provide continuity and customer relationships. The regional banks enable scale and risk-sharing. The listed holding company offers strategic flexibility and capital access. It's a structure that has evolved through trial and error into something uniquely suited to its purpose.

Looking forward, Crédit Agricole faces the same challenges as all European banks: low growth, intense competition, digital disruption, regulatory burden. But it also has unique advantages: patient capital, loyal customers, diversified revenues, and a proven ability to survive crises.

Will Crédit Agricole exist in another 140 years? Almost certainly, though in what form is impossible to predict. The farmers' bank has proven remarkably adaptable, transforming from agricultural lender to universal bank to digital financial services provider. Whatever comes next—blockchain, quantum computing, financial services in the metaverse—Crédit Agricole will probably adapt, slowly and pragmatically, as it always has.

The greatest risk isn't disruption or competition but complacency. Crédit Agricole has become so successful, so established, that it might forget the entrepreneurial spirit that created it. When Louis Milcent and Alfred Bouvet met in Salins-les-Bains in 1885, they weren't trying to build a global banking giant. They were trying to solve a real problem for real people. That spirit—practical, local, mutual—remains Crédit Agricole's greatest asset. If it loses that, it loses everything.

As we close, it's worth returning to that rainy day in 1885 when this all began. The founders couldn't have imagined smartphones or derivatives or €2 trillion balance sheets. But they understood something fundamental: finance is about trust, and trust is built through relationships, not algorithms. In a world of increasing digitalization and automation, that insight might be more valuable than ever.

Crédit Agricole's next chapter will be written by leaders we haven't met, facing challenges we can't imagine, using technologies that don't exist. But if history is any guide, they'll face those challenges with the same combination of pragmatism and patience that has defined the institution since the beginning. The farmers' bank will endure, transformed but recognizable, a testament to the power of cooperative capitalism and the enduring importance of "common sense close to home."

XIII. Recent News

The latest developments at Crédit Agricole reflect both continuity and change. In Q4 2023, the bank demonstrated remarkable resilience despite challenging conditions. The insurance division faced significant weather-related claims from European storms, yet still delivered strong profits. This highlights both the diversification benefits of the universal banking model and the increasing impact of climate change on financial institutions.

The Banco BPM saga continues to evolve. Italian political dynamics and European regulatory scrutiny make any major move complex. The situation resembles a chess match where all players can see several moves ahead but no one wants to make the first move. Market speculation suggests resolution by end-2025, but Italian banking consolidation has consistently taken longer than expected.

Management changes reflect generational transition. The senior leadership team now includes more women and younger executives with technology backgrounds. This isn't window dressing—it reflects recognition that Crédit Agricole's future leaders need different skills than their predecessors.

Digital initiatives are accelerating. The partnership with Worldline (where Crédit Agricole acquired a 7% stake in January 2024) signals serious commitment to payments innovation. The bank is also experimenting with blockchain for trade finance and digital identity solutions for know-your-customer requirements.

Regulatory developments continue to shape strategy. The implementation of Basel IV will require additional capital, though Crédit Agricole's strong ratios provide cushion. More interesting are emerging regulations around sustainable finance, where Crédit Agricole's agricultural heritage provides competitive advantage in understanding and pricing climate risks.

XIV. Links & Resources

For those seeking to dive deeper into Crédit Agricole's history and operations, the primary sources remain the annual reports and investor presentations available on the company's investor relations website. The Universal Registration Documents provide comprehensive financial and strategic information, though they require patience to navigate.

Academic studies of cooperative banking offer valuable context. The works of Professor Hans Groeneveld at Tilburg University provide rigorous analysis of cooperative banking models. The European Association of Co-operative Banks publishes regular studies comparing different cooperative banking systems.

For historical perspective, André Gueslin's histories of French agricultural credit remain definitive, though primarily available in French. The Crédit Agricole corporate archives in Paris contain fascinating primary documents, though access requires special permission.

On the Emporiki disaster, Harvard Business School's case study "Persephone's Pomegranate: Crédit Agricole and Emporiki" (2012) provides detailed analysis. The academic paper "Crédit Agricole and Emporiki: Buying a Greek bank in 2006. What could go wrong?" offers a brutal post-mortem.

For ongoing coverage, the French financial press—particularly Les Echos and La Tribune—provides superior insight compared to English-language sources. The Financial Times and Bloomberg cover major developments but often miss nuances important to understanding this complex institution.

Analyst reports from French banks and brokerages offer the most detailed financial analysis, though accessing them typically requires institutional relationships. BNP Paribas Exane and Société Générale's equity research are particularly thorough, despite the competitive dynamics.

The story of Crédit Agricole continues to evolve, shaped by forces both ancient and modern. From its origins serving farmers who couldn't afford a pair of oxen to its current position managing trillions in assets, it remains a unique institution—neither fully mutual nor fully capitalist, neither purely local nor truly global, neither traditional nor modern. In these contradictions lies both its challenge and its opportunity. The farmers' bank has come a long way from Salins-les-Bains, but in some fundamental sense, it has never left.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube