The Ultimate Conglomerate Split: The Story of Associated British Foods & Primark

I. Introduction & The Grand Split

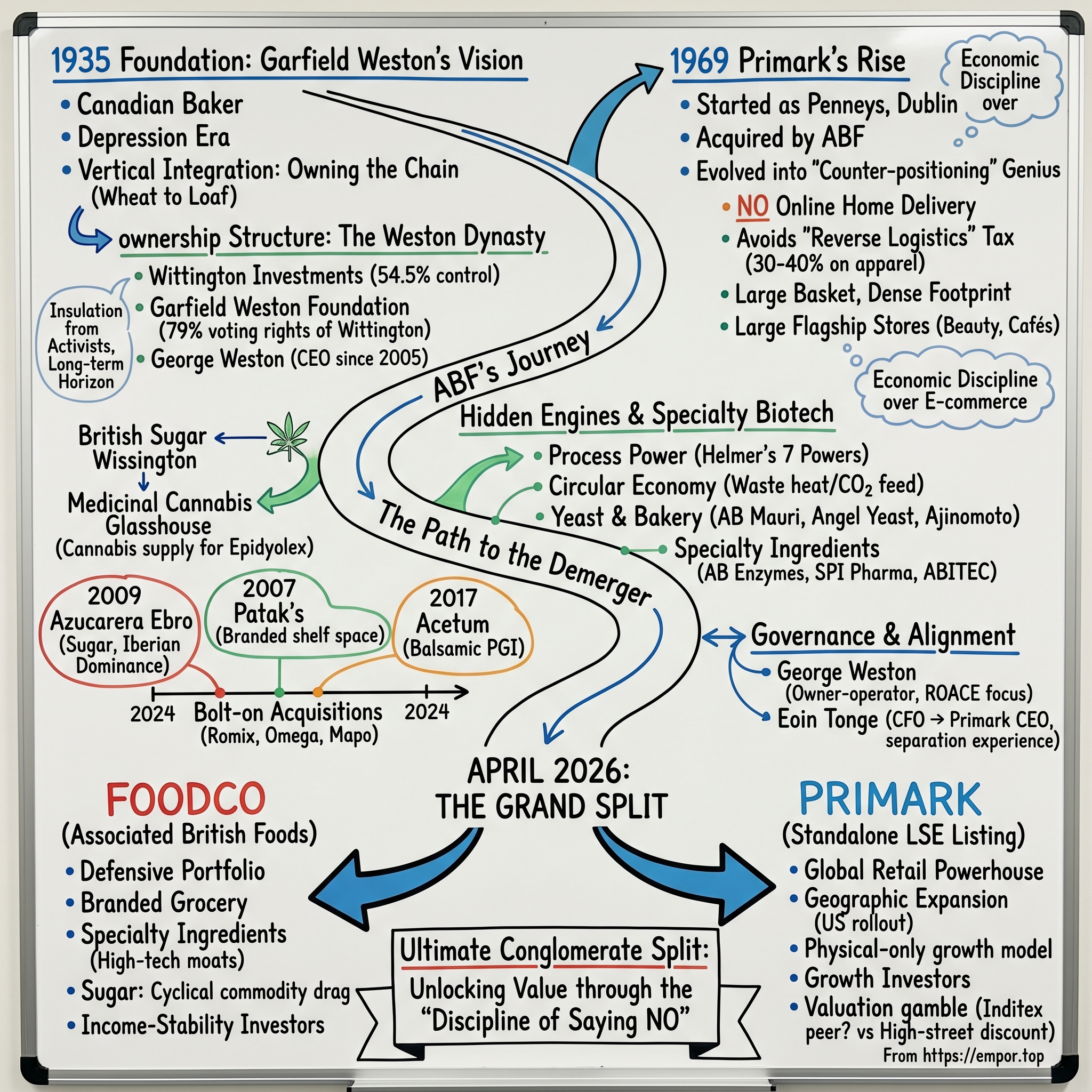

On the morning of April 21, 2026, the Regulatory News Service of the London Stock Exchange carried an announcement that, on first reading, sounded almost impossible. Associated British Foods plc — a company most British shoppers had never knowingly bought a single product from, yet whose goods sat in nearly every kitchen cupboard, sugar bowl, and high-street wardrobe in the country — was proposing to tear itself in half.1

The plan was audacious in its simplicity. ABF would demerge Primark, the cult fast-fashion retailer beloved by teenagers and budget-conscious families across Europe and North America, into a separate, standalone company listed on the London Stock Exchange. What had been a single sprawling conglomerate worth roughly £13 billion would become two distinct FTSE 100 constituents: a standalone Primark valued by analysts at around £9 billion, and a residual food, ingredients, and agriculture business — quickly nicknamed "FoodCo" in the City — worth something closer to £4 billion.1[^7]

To understand why this was so striking, you have to sit with the central paradox of the company. Associated British Foods was founded in the depths of the Great Depression by a Canadian baker. Its DNA is flour, yeast, and sugar beet — the unglamorous, slow-compounding world of industrial food processing, where a good year means margins tick up by half a percentage point and a bad year means a European sugar price crash wipes out an entire division's profit. And yet, bolted onto this nineteenth-century-feeling food empire was one of the most disruptive retail phenomena of the twenty-first century: a fashion chain that grew to billions in revenue while flatly, almost defiantly, refusing to sell clothes online for home delivery in an era when every consultant, every analyst, and every competitor insisted that e-commerce was the only future.

How does a post-Depression baking company become the parent of a global fast-fashion giant that rejects the internet? And why, after decades of holding these wildly mismatched businesses together under one roof, would the family that controls it decide in 2026 that the time had finally come to let them go their separate ways?

This is a story about a family — the Westons — whose multi-generational control structure is itself one of the most remarkable corporate moats in the world. It is a story about Primark's almost heretical "physical-only" business model, and the counter-positioning genius that let it thrive precisely because it refused to do what everyone else did. It is a story about hidden engines most investors have never heard of: a Norfolk glasshouse growing medicinal cannabis heated by waste steam from a sugar factory; a specialty enzymes and pharmaceutical-excipients business quietly compounding double-digit margins. And it is, ultimately, a story about the strategic playbook of saying no — and how that discipline created billions in value that the 2026 demerger is now designed to unlock.

Let us begin where the whole thing started: with a baker, a depression, and an obsession with controlling everything that went into the loaf.

II. The Weston Dynasty: Trust, Sugar, and Longevity

The year was 1935, the world was still climbing out of the Great Depression, and a Canadian entrepreneur named Garfield Weston was buying up British bakeries with a conviction that bordered on zealotry.[^2] Weston had inherited a biscuit business from his father in Toronto and crossed the Atlantic with a simple, radical idea: that the path to durable profit in food was not in any single clever product, but in owning the entire chain — the wheat, the milling, the baking, the distribution, all of it knitted together so that no middleman could clip a margin he could capture himself. In 1935 he incorporated Allied Bakeries, the entity that would, over the following decades, swell and rename itself into Associated British Foods.[^2]

It is worth pausing on how unusual Garfield Weston's instinct was for its time. Most food businesses of the era thought in terms of a single craft — you were a baker, or a miller, or a sugar refiner. Weston thought in terms of systems. If you controlled the supply chain end to end, you smoothed out the violent price swings of agricultural commodities and you compounded small efficiencies at every link. That obsession with vertical integration is the genetic code that runs through everything ABF later became — including, improbably, a fast-fashion retailer that insisted on controlling its own stores rather than renting space on someone else's website.

But the truly decisive legacy Garfield Weston left was not a baking technique. It was an ownership structure.

At the centre of ABF sits a holding company called Wittington Investments Limited, which controls roughly 54.5% of Associated British Foods.[^7] And Wittington itself is not controlled by a person seeking to maximise their own quarterly net worth — 79% of its voting rights are held by the Garfield Weston Foundation, one of the largest charitable grant-makers in the United Kingdom.[^7] Read that structure again slowly, because it is the single most important fact in this entire story. The controlling shareholder of a £13 billion public company is, in effect, a charity, working in concert with a family that has run the business for nearly a century.

Why does this matter so much? Because it inverts the incentives that govern almost every other listed company. A typical FTSE 100 chief executive lives and dies by the next set of half-year results, hostage to activist investors who can accumulate a stake and demand a buyback, a spin-off, or a margin-juicing pivot within eighteen months. The Weston structure is the ultimate corporate shield. No activist can storm the gates when a family-and-foundation bloc holds a controlling 54.5%. No hedge fund can force management to chase a fashionable strategy against its judgment. This is what the strategist Hamilton Helmer would call a cornered resource — an asset competitors and agitators simply cannot replicate — and we will return to it, because it is the quiet enabler of nearly every contrarian decision ABF ever made.

The most famous of those contrarian decisions was the refusal, for years, to build Primark an online home-delivery business. Every rival was pouring capital into e-commerce warehouses and free-returns logistics. ABF, insulated by its ownership, could simply decline. It could deploy capital on a ten- and twenty-year horizon while others optimised for the next earnings call. That patience is not a personality trait; it is a structural feature engineered into the company's bones.

Steering this for more than two decades has been George Weston, Garfield's grandson, who became chief executive of ABF in 2005.[^2] George Weston's leadership style is, by the standards of modern public-company chief executives, almost startlingly understated. He is not a creature of the earnings-call theatre, not given to grand visions of synthetic transformation or buzzword-laden strategy decks. His preoccupation, by every account, is the unglamorous discipline of steady cash compounding — generating cash from the food and sugar engines, redeploying it into defensible assets, and letting time and reinvestment do the heavy lifting. It is a philosophy that would feel entirely familiar to his grandfather.

That philosophy explains how a baking company could afford to nurture, for decades, a retail business that broke every modern rule. To understand that, we have to go back to 1969, and a small clothing shop in Dublin.

III. Primark's Rise: Retail Anachronism or Genius?

The first store opened in Dublin in 1969 under a name that meant nothing to anyone: Penneys. It was a small Irish clothing shop, and when ABF acquired it that year and later expanded into Britain, the name "Penneys" was already taken by an American chain, so in the UK and beyond it was rebranded Primark.[^2] For decades it remained a curiosity — a value clothing chain tucked inside a food conglomerate, the sort of asset analysts struggled to categorise. How exactly did a discount fashion retailer end up as a sibling of sugar refineries and yeast plants?

The answer, for most of the late twentieth century, was almost accidental: it generated cash, it fit the family's instinct for businesses that served ordinary households, and nobody had a compelling reason to sell it. But somewhere along the way, Primark stopped being a curiosity and became the crown jewel — the highest-growth, most valuable single asset in the entire ABF portfolio. The way it got there is one of the great counterintuitive stories in modern retail.

To appreciate Primark's genius, you have to understand the economics of online fashion — and specifically, the thing that quietly destroys it. When you buy clothes on the internet, you cannot try them on. So you order three sizes, keep one, and send two back. Across the industry, return rates on online apparel run somewhere between 30% and 40%, and every one of those returns has to be shipped back, inspected, repackaged, restocked, or written off. The industry has a grim term for this hidden cost: reverse logistics. It is a tax — a brutal, margin-eroding tax — and for a value retailer selling a T-shirt for a few pounds, it is fatal. There is simply no room in the price of a £4 top to absorb the cost of shipping it out, having it returned, and processing it back into inventory.

Primark looked at this math and drew a conclusion that horrified the consultants: it would not sell clothes online for home delivery at all. Full stop. While H&M, ASOS, and a hundred digital-native brands raced to build e-commerce empires, Primark planted its flag in the physical world and refused to move. This was not technological backwardness. It was a deliberate, ruthless reading of unit economics. By staying out of home delivery, Primark dodged the reverse-logistics tax entirely, and that is precisely what let it hold prices low enough that no online competitor could follow it down without bleeding to death.

The model that replaced e-commerce was what we might call "large basket, dense footprint." Primark does not run a thousand small shops; it runs enormous, theatrical flagship stores — destinations in their own right, with beauty halls, cafés, and constantly refreshed ranges designed to pull in foot traffic and keep shoppers wandering. The strategy is to get a customer through the door, surround them with cheap, tempting, fast-changing product, and let the basket size do the work. High footfall, large baskets, and ferociously fast inventory turns combine to make each square foot of selling space extraordinarily productive. The store is not a cost centre that an online business is trying to escape; the store is the entire machine.

It is worth war-gaming Primark against its rivals to see how strange and strong its position is. The Spanish giant Inditex, parent of Zara, built its empire on speed — a vertically integrated supply chain that can move a design from sketch to shop floor in weeks, supporting premium-ish prices and a celebrated omnichannel operation. Sweden's H&M went heavy on e-commerce and global scale, and has spent years wrestling with exactly the online-margin problems Primark sidestepped. Then there is the new breed of ultra-fast-fashion disruptors, above all 希音 Shein, the China-founded behemoth that ships absurd volumes of micro-trend product directly to consumers' doors at rock-bottom prices, weaponising the very e-commerce model Primark rejected. And in Japan, 株式会社ファーストリテイリング Fast Retailing — the parent of Uniqlo — built a different kind of compounding machine, prioritising durable basics and physical-retail excellence over disposable trends.

Set against that field, Primark is the deliberate anachronism: no home delivery, no global webstore arms race, just relentless price leadership executed through physical stores. For years the consensus held that this was a fatal weakness, a business living on borrowed time, destined to be swept away by the digital tide. The consensus would shortly get a real-world stress test — and so would the human cost buried inside the supply chain that made those low prices possible.

IV. The Crisis Points: Rana Plaza & Supply Chain ESG

On the morning of April 24, 2013, on the outskirts of Dhaka, Bangladesh, an eight-storey building called Rana Plaza collapsed. Inside were garment factories supplying brands from across the Western world. More than 1,100 people died and thousands more were injured in what became the deadliest disaster in the history of the garment industry. The day before, cracks had been spotted in the building; workers had been ordered back inside regardless. Primark was one of the brands with a supplier operating in that building.

For Primark, and for the entire fast-fashion industry, Rana Plaza was a watershed — the moment the abstract phrase "low-cost manufacturing" acquired an unbearable human face. The business model that delivered £4 tops to British high streets rested, ultimately, on garment workers in some of the poorest countries on earth, and the disaster forced a public reckoning with what that supply chain actually was and who bore its risks.

What is notable, in hindsight, is the nature of Primark's response. Rather than treating the tragedy as a one-off public-relations wound to be bandaged and forgotten, the company moved quickly to establish long-term compensation funds for the victims and their families, paying out to workers from its supplier in the building, and it committed to a far more rigorous regime of structural and fire-safety auditing across its sourcing base. Over the following years it also developed the Primark Sustainable Cotton Programme, working directly with cotton farmers — initially in India — to train them in more sustainable growing methods, an attempt to push transparency and standards all the way back to the raw fibre.

The deeper strategic shift was structural. Before Rana Plaza, much low-cost garment sourcing across the industry was fundamentally transactional: a brand placed an order, a factory filled it, and the layers of subcontracting in between were often opaque even to the buyer. After Rana Plaza, Primark moved decisively toward audited, long-term, structured partnerships with a more controlled base of suppliers, with visibility into the buildings its clothes were actually made in. This was costly and operationally demanding — but it quietly transformed what had been a liability into something closer to a moat.

Here is the underappreciated point for investors. Building a deeply audited, structurally safe, long-term supplier network is expensive and takes years. It is exactly the kind of capability a new ultra-fast-fashion entrant, optimising purely for speed and price, struggles to replicate. ESG compliance, done seriously rather than cosmetically, becomes an operational asset: it lowers the risk of catastrophic supply-chain failure, it satisfies increasingly demanding Western regulators and consumers, and it raises the bar for anyone trying to compete at Primark's price point without cutting the same corners. The tragedy in Dhaka, in other words, permanently changed how Primark sourced its products — and in doing so, hardened the very model that critics kept predicting would collapse.

That prediction of collapse would get its most literal test not from a competitor or a scandal, but from a virus that shut Primark's stores entirely.

V. The Digital Defiance: Click & Collect Trial

In the spring of 2020, the unthinkable happened to a business that had staked everything on physical stores: the stores closed. As COVID-19 lockdowns swept across Europe, Primark's shops — every single one of them — went dark. And because Primark had no online home-delivery business to fall back on, its retail revenue did not merely decline. For stretches of the pandemic, it went to essentially zero. Zero sales, while rent and other fixed costs kept ticking.

This was the moment the bears had been waiting for. For years, sceptics had pointed to Primark's lack of e-commerce as a glaring structural vulnerability, and now reality had delivered the cruellest possible demonstration. A purely physical retailer, in a world where people could not physically shop, had no Plan B. Every digital-first competitor kept selling through lockdown; Primark could only watch its empty stores haemorrhage cash. It was, on paper, the perfect refutation of the whole "physical-only" thesis.

And yet the company's response revealed the discipline beneath the strategy. Primark did not panic into building the very home-delivery operation it had spent years rejecting. It understood that the pandemic was a temporary, if brutal, shock — and that capitulating to full e-commerce would mean permanently importing the reverse-logistics tax it had so carefully avoided. Instead, it waited, weathered the storm on the strength of its parent's balance sheet, and then pivoted on its own terms.

That pivot arrived in the form of a Click & Collect trial, which Primark began rolling out from late 2022 into 2023. Crucially, this was not home delivery. Customers ordered online and then came to a store to pick up their purchases. The initial trials focused on a deliberately narrow slice of the range — children's wear and nursery items, categories where parents particularly value being able to reserve specific sizes and products in advance — before the offering was progressively expanded to more stores and a broader assortment.

The strategic elegance of Click & Collect, for Primark specifically, is worth dwelling on, because it threads a needle that looked impossible. Consider what it requires and what it avoids. It leverages space the company already has — the back rooms and floor space of stores it already operates — rather than demanding a brand-new national network of fulfilment warehouses. It involves no fleet of delivery vans, no last-mile logistics, no doorstep returns. And here is the genius part: to collect an online order, the customer has to physically walk into a Primark store. Which means they walk past the beauty hall, past the new-season range, past the £3 impulse buys stacked by the tills. The collection point is, in effect, a machine for generating incremental, high-margin footfall. The online order becomes not a replacement for the store visit but a reason for one.

In one move, Primark answered the bears' central critique — yes, it now has a digital channel — without surrendering an inch of the economic logic that made it special. It got the marketing reach of an online presence and the convenience customers increasingly demanded, while keeping the dreaded returns tax firmly outside its walls. It was counter-positioning refined: not a rejection of digital, but a refusal to do digital on anyone else's terms.

If Primark represents the art of saying no to conventional wisdom in retail, the rest of ABF represents something quieter and equally deliberate: the patient deployment of all that retail cash into defensive, high-moat food assets. To see that strategy at work, we need to follow the money into beet sugar and balsamic vinegar.

VI. Capital Allocation & Strategic M&A: Beet Sugar & Balsamic Vinegar

Here is the financial heart of the old conglomerate, and the logic that justified holding such mismatched businesses together for so long. Primark threw off cash. The food side of ABF, run with George Weston's compounder's mindset, took that cash and bought assets with deep, defensible moats — businesses that would never grow explosively but would generate stable, resilient profit for decades. To understand ABF's capital allocation philosophy, you study what it chose to buy, and how it thought about price.

Start with sugar. In 2009, ABF acquired Azucarera Ebro, the dominant sugar business of Spain, from the food group Ebro Puleva for a total of around €526 million — comprising roughly €385 million of enterprise value plus about €141 million tied to restructuring assets.[^11] The strategic prize was straightforward: the deal handed ABF effective dominance over the entire Iberian sugar market. The way to think about the price is through the lens of operating profit — ABF paid in the region of 8.7 times the operating profit it was buying.

What does a multiple like that actually mean? It means ABF paid roughly nine years' worth of current profits up front for the asset. For a fast-growing tech company that would be cheap; for a no-growth industrial commodity business it is a real price, and it only makes sense if you believe the cash flows will keep coming for far longer than nine years. ABF believed exactly that — and was largely vindicated. Even when the European Union reformed its sugar quota regime in 2017, ending the production caps that had long shaped the industry and unleashing a wave of price volatility, the Spanish business kept generating cash. Decades of stable regional cash flow have, in effect, fully paid back the purchase price several times over. The point is not that sugar is a great growth business — it manifestly is not — but that a dominant position in a regional commodity market, bought at a sensible multiple and held for the very long term, is a cash machine that funds everything else.

Now contrast that with a very different kind of acquisition: Patak's, the Indian-food brand, acquired by ABF in 2007. Where the figures are publicly estimated, the price was somewhere in the range of £100 million to £200 million against roughly £66 million of revenue — meaning ABF paid a premium of perhaps two to three times sales.[^2] Paying two-to-three times revenue for a food brand is not cheap on the face of it. But the logic was defensive, not opportunistic. Folded into ABF's "world foods" strategy alongside the Blue Dragon brand, Patak's gave ABF something close to monopoly shelf space in the Indian and pan-Asian food aisles of British supermarkets. And shelf space, in grocery, is destiny. Once you own the dominant brand in a category that shoppers reach for habitually, you command resilient, double-digit operating margins that are extraordinarily hard for a challenger to dislodge. You are not paying for growth; you are paying for an almost unassailable position in a defensible niche.

The third acquisition completes the picture and reveals ABF's taste for assets protected by something even stronger than brand: geography and regulation. In 2017, ABF acquired Acetum, the world's leading producer of Balsamic Vinegar of Modena, for £284 million (about €300 million) against roughly €103 million of net sales — a multiple of around 2.9 times sales.[^12] Again, a premium price. But consider what Acetum actually owns. Balsamic Vinegar of Modena carries a Protected Geographical Indication, or PGI — a legal designation under European law that means the product can only be made in a specific region of Italy, under specific rules. You cannot simply build a balsamic-vinegar factory in Birmingham and compete. The supply is constrained by law and geography, the brand is the global leader, and the product sits at the premium, culinary end of the market. ABF paid up for the undisputed champion of a category that is structurally protected from new entrants, and then invested behind it, expanding aging capacity toward nearly 20 million litres and compounding its margins in a global premium-food niche.

Step back and the pattern across all three deals is unmistakable. ABF does not chase growth multiples or fashionable categories. It buys dominant positions in defensible markets — protected by scale, by shelf space, or by regulation and geography — at prices that look full in the moment but are vindicated by decades of stable cash flow. It is the Weston philosophy expressed in M&A: patience, defensibility, and the long compound.

But the most extraordinary asset in the ABF portfolio is not sugar, or vinegar, or Indian cooking sauces. It is a glasshouse in Norfolk growing a drug — and it is powered by waste.

VII. The Hidden Engines: Cannabis Glasshouses & Specialty Biotech

If you drove through the flat Norfolk countryside near the village of Wissington, you would pass what looks like an ordinary, if enormous, agricultural glasshouse. For years it grew tomatoes — millions of them, heated cheaply by a neighbour most growers would envy: an adjacent British Sugar factory churning through sugar beet. Then, in 2017, the tomatoes were phased out, and the glasshouse began growing something far more valuable and far more surprising. Behind the glass, on roughly 18 hectares, British Sugar now cultivates low-THC, high-CBD medicinal cannabis.

This is not a recreational-drug story; it is a pharmaceutical one. The cannabis grown at Wissington is cultivated under contract to supply the active botanical ingredient for Epidyolex, a medicine developed by GW Pharmaceuticals — since acquired by Jazz Pharmaceuticals — that treats severe, treatment-resistant forms of childhood epilepsy. For families whose children suffer dozens of seizures a day, it can be life-changing. And it is being grown, of all places, on the grounds of a British sugar operation.

The reason it sits there, rather than anywhere else, is the most beautiful expression of Garfield Weston's original obsession with integrated systems. The glasshouse is powered almost entirely by the by-products of the sugar factory next door. Processing sugar beet generates enormous quantities of surplus heat and waste carbon dioxide. Plants, famously, crave warmth and CO2. So British Sugar pipes the factory's waste heat and waste CO2 straight into the glasshouse, feeding the cannabis plants with what would otherwise be emissions vented to the sky. The result is a near-zero-carbon, remarkably low-cost production system for a high-value pharmaceutical ingredient — a genuine circular economy in which one business's waste is another's essential input. It is process power in the Helmer sense: an embedded, hard-won operational capability that a standalone competitor could not easily copy, because it depends on physically co-locating a drug glasshouse next to a sugar factory and engineering the two to feed each other.

This circular-economy mindset runs throughout ABF's food and ingredients operations, and it points to the part of the company that most investors overlook entirely: the specialty biotech and ingredients businesses. To frame their importance, consider the segment-level shape of the food empire in its recent 2024–2025 performance. The Grocery division generated around £4.125 billion of revenue at roughly £478 million of operating profit — an operating margin near 11.5%.[^2] The Ingredients division, smaller but higher quality, produced about £2.041 billion of revenue at roughly £257 million of operating profit, an even fatter margin of around 12.6%.[^2] And Sugar — the volatile commodity engine — generated about £2.054 billion of revenue but slipped to a roughly £2 million operating loss, dragged down by a sharp European sugar-pricing downturn in 2025.[^2] That contrast tells the whole investment story of FoodCo in three lines: stable, branded grocery; high-margin specialty ingredients; and cyclical, sometimes painful, commodity sugar.

It is the Ingredients segment — branded internally as ABF Ingredients, or ABFI — that deserves far more attention than it gets. This is a collection of genuinely high-tech, high-margin businesses: AB Enzymes, which makes specialty industrial enzymes; SPI Pharma, which produces pharmaceutical excipients — the inactive but critical ingredients that make a pill bind, dissolve, and deliver its active drug correctly; and ABITEC, which makes specialty lipids used in pharmaceuticals and nutrition. These are not commodity food businesses; they are science-led suppliers selling into demanding, regulated, sticky end-markets where reformulating away from a qualified supplier is slow and expensive.

Alongside them sits AB Mauri, ABF's global yeast and bakery-ingredients business — one of the largest yeast producers in the world. Yeast may sound humble, but it is a fermentation-science business with real scale economics and a global competitive map. AB Mauri's principal rivals include 安琪酵母 Angel Yeast, the formidable Chinese yeast and fermentation champion that has expanded aggressively across global markets, and, in the broader world of fermentation and amino-acid biotechnology, the Japanese giant 味の素株式会社 Ajinomoto, whose mastery of industrial fermentation set the standard for the field. Competing in yeast and fermentation is, in essence, competing in applied biology at industrial scale — and it rewards exactly the kind of patient, capital-intensive process expertise that ABF has cultivated for a century.

What is striking is how the company has kept quietly bolting on capability. Through 2024, ABFI and its sister businesses made a series of small but strategically pointed acquisitions: Romix Foods, which strengthened AB Mauri's gluten-free and clean-label bakery capabilities; Omega Yeast Labs, a specialist in liquid yeast for craft breweries, picked up by AB Biotek to deepen its craft-fermentation reach; and Mapo, an Italian specialist, broadening the ingredients portfolio further.[^14]2 None of these deals were large enough to move the headline numbers, and that is precisely the point. They reflect a deliberate strategy of compounding high-margin, "clean label" and craft-fermentation capabilities one bolt-on at a time — the same patient, defensibility-first M&A philosophy seen in sugar and vinegar, now applied to specialty biotechnology.

This is the hidden FoodCo that the demerger will finally expose to daylight: not a sleepy bakery business, but a portfolio of branded grocery, regulated specialty ingredients, and genuinely novel circular-economy assets. The question of who will lead these two newly separated companies — and how their leaders are paid to think — brings us to governance.

VIII. Governance & Leadership: The Weston-Tonge Era

To understand how ABF will be run after the split, you have to understand how its leaders are incentivised before it — and few public companies align management with owners as tightly as this one.

Consider George Weston, the chief executive who has steered ABF since 2005. His base salary sits at £1.28 million, and his total 2024 remuneration package came to roughly £6.05 million.2 By the inflated standards of FTSE 100 pay, that is substantial but hardly extravagant. The number that matters, though, is not what he is paid — it is what he owns. George Weston directly holds about 0.56% of ABF's shares, a stake worth well over £100 million.2 To put that in perspective, the company asks its executives to hold shares worth 300% of their base salary, a typical alignment requirement; George Weston's personal holding exceeds that threshold many times over. This is not a hired manager renting the corner office for a few years. This is an owner-operator whose personal fortune rises and falls with the long-term value of the enterprise — which is exactly why he can afford to think in decades rather than quarters.

The incentive design reinforces that horizon. Rather than loading executive pay onto short-term earnings targets that invite the gaming of quarterly numbers, ABF weights its long-term incentives toward a Restricted Share Plan tied to measures such as dividends, governance standards, and — critically — keeping Return on Average Capital Employed, or ROACE, safely above the company's cost of capital. In plain terms, management is paid to ensure that every pound of capital the business deploys earns more than it costs to fund. That single discipline, applied consistently, is the mathematical engine of long-run compounding, and it is the metric the whole edifice is built to protect.

If George Weston represents continuity, the other defining figure of this era represents the bridge to the new structure: Eoin Tonge. Tonge had served as ABF's Group Chief Financial Officer, and before that had been a senior finance executive at Marks & Spencer — a pedigree steeped in exactly the disciplines a major listed retailer demands. His path to the top of Primark was anything but smooth. In early 2025, Primark's long-serving chief executive, Paul Marchant, departed suddenly, leaving a leadership vacuum at the group's most valuable business at a delicate moment. Tonge stepped in, and on March 5, 2026, he was confirmed as the permanent Chief Executive of Primark.[^9]

The logic of putting a former Group CFO and M&S veteran in charge of Primark becomes obvious once you know what was coming six weeks later. Spinning a business out of a conglomerate and standing it up as an independent FTSE 100 company is, above all, a feat of financial engineering and investor relations — designing the capital structure, setting dividend policy, building the relationships with a brand-new shareholder base, and telling the equity story to a market seeing the business on a standalone basis for the first time. There are few backgrounds better suited to that task than a seasoned group finance chief who also understands large-scale retail from the inside. Tonge was, in effect, appointed to run Primark precisely because he could run its separation.

And so the demerger leadership blueprint announced in April 2026 falls neatly into place. Under the split, George Weston will lead the legacy food, ingredients, and agriculture business — FoodCo, the continuing Associated British Foods — as its chief executive, returning the family's steward to the assets his grandfather built. Eoin Tonge will lead the standalone Primark as a separately listed company on the London Stock Exchange. Two businesses, two dedicated leadership teams, two distinct equity stories — each finally able to be run, and valued, on its own terms.

Why this should create value, and where the risks lie, is best understood through the strategic frameworks that explain what each business actually is.

IX. Strategic Frameworks: Porter's 5 Forces & Hamilton's 7 Powers

Strip away the narrative and ask the analyst's question: what, precisely, protects these businesses from competition? The honest answer is that ABF's two halves are defended by different powers, and naming them clearly is the best way to see what the demerger is really separating.

Begin with Hamilton Helmer's 7 Powers, the framework that asks which durable advantages allow a business to sustain returns above its cost of capital. Primark possesses scale economies of a particular kind. Its enormous purchasing volumes and dense network of high-traffic stores give it buying power and cost absorption that smaller rivals cannot match at its price points. When you are sourcing clothing at Primark's volumes, you negotiate input costs and spread fixed overheads across a base that a boutique competitor simply cannot rival — and at the bottom of the price market, where every penny of cost shows up in the shelf price, that scale advantage is decisive.

But Primark's most interesting and most durable power is counter-positioning — and this is the concept worth sitting with, because it is the strategic core of the entire Primark thesis. Counter-positioning describes a situation where an incumbent cannot copy a challenger's model without damaging its own existing business. Primark's refusal to offer e-commerce home delivery is the textbook case. Its rivals — H&M, ASOS, and the digital-native fashion brands — are structurally committed to online delivery and free returns. Those channels carry the reverse-logistics costs described earlier, and the rivals' whole cost structure and customer promise are built around them. Now imagine one of those competitors tried to match Primark's rock-bottom in-store prices. They could not — not without abandoning the online model their business depends on, and not without bleeding margin until they collapsed. Primark's prices are, in effect, a position the incumbents cannot occupy without burning down their own house. That is counter-positioning, and it is why the "Primark is doomed without e-commerce" thesis had it exactly backwards: the absence of e-commerce was the moat.

The third power belongs not to a business but to the ownership structure itself: the Weston family's controlling 54.5% stake via Wittington Investments is a cornered resource. No competitor, and no activist, can acquire control of ABF on the open market. This single structural fact immunises the company from the short-term pressures — hostile takeovers, activist-forced digital pivots, margin-destroying buyback demands — that have pushed so many peers into value-destroying decisions. The freedom to say no to e-commerce, to hold sugar through a downturn, to invest behind a cannabis glasshouse, all ultimately traces back to this one cornered resource.

And the fourth power lives in the food and ingredients businesses: process power, the deeply embedded operational know-how of ABF's circular-economy systems — the Wissington heat-and-CO2 exchange, the integration of sugar by-products into bioethanol and animal feed, the fermentation expertise of AB Mauri. These are not advantages you can buy off the shelf; they are accreted over years of operating physically integrated assets, and they let ABF extract more value from each tonne of agricultural input than a less integrated rival could.

Now run the same businesses through Porter's Five Forces, which asks where the structural profitability of an industry comes from. The threat of new entrants is low in both of ABF's core domains. To compete in industrial sugar refining you need vast capital expenditure, regulatory permits, and agricultural supply relationships that take years to build; to compete with Primark at scale you need a global low-cost sourcing network and the capital to roll out enormous stores. Neither is something a start-up conjures overnight. Competitive rivalry, by contrast, is genuinely fierce in fast fashion — Inditex, H&M, Shein, and a hundred others are all fighting for the same wallet — but Primark mitigates that rivalry through its extreme price leadership and its distinct, physical-only positioning, which keeps it from competing head-to-head on the same terms as everyone else. Buyer power is diffuse (millions of individual shoppers, none of whom can dictate terms), while supplier power varies — concentrated in branded inputs but weak in the commodity garment and agricultural supply base where ABF's scale dominates.

The frameworks converge on a clean conclusion: these are two fundamentally different businesses, protected by fundamentally different powers, that happened to share a parent. Which is exactly why the market may value them very differently apart than together — the question at the heart of the bull and bear case.

X. The Bear vs. Bull Case & Standalone Valuation

The entire intellectual justification for the demerger rests on a single idea familiar to anyone who has studied conglomerates: the conglomerate discount. When a fast-growing global retailer and a slow-compounding food-and-commodity business sit inside the same share, neither set of investors gets quite what they want. Growth investors are diluted by the cyclical sugar drag; income-and-stability investors are unsettled by retail's capital intensity. Separate them, the theory goes, and each can attract its natural shareholder base and be valued on its own merits. So what does each standalone business actually look like through the eyes of a fundamental investor?

Take FoodCo first — the continuing Associated British Foods. The bull case is that of a highly defensive, deeply cash-generative portfolio: branded grocery throwing off stable double-digit margins, a high-margin specialty ingredients arm with real technological moats, and genuinely differentiated assets like the Wissington pharmaceutical glasshouse, all freed from the heavy, ongoing capital demands of Primark's store-expansion programme. Liberated from funding retail growth, FoodCo can return more cash to shareholders and lean into its highest-return ingredients and grocery niches. It is, in essence, a quality compounder for patient income investors.

The bear case on FoodCo is written in that single line from the recent segment data: a sugar division that swung to an operating loss in 2025.[^2] FoodCo remains structurally exposed to commodity price volatility, and European beet sugar is the prime offender — when EU sugar prices roll over, as they did in 2025, an entire division's profit can evaporate, dragging group results with it. Layer on the low-growth, fiercely competitive UK bakery market, where ABF's Allied Bakeries and its Kingsmill brand grind against tough supermarket buyers and thin margins, and you have a business whose stability is real but whose growth ceiling is modest and whose cyclical floor can be uncomfortably low. The single most important number to watch here is the European sugar price and its feed-through to the Sugar division's operating result — it is the swing factor that will make or break FoodCo's earnings in any given year.

Now Primark. The bull case is a pure-play global retail powerhouse with a long runway. After decades of European expansion, Primark's largest unexploited opportunity is geographic: a still-early store roll-out across the United States and a deepening presence in Southern Europe, executed by a dedicated board and management team no longer competing for capital and attention inside a food conglomerate. If the model — proven across the UK, Ireland, and continental Europe — travels successfully to America at scale, the growth runway is long and the unit economics are among the most attractive in value retail.

The bear case on Primark is the world outside its control. As an importer of physical goods moving from Asian factories to Western stores, it is exposed to global shipping disruptions, freight-cost spikes, and raw-material inflation in cotton and synthetics — the kind of input shocks that squeeze a low-price retailer hardest, precisely because it has the least room to pass costs on. And while counter-positioning protects it against the traditional online players, the rise of ultra-fast digital-only disruptors like 希音 Shein represents a genuine competitive pressure on the value-fashion consumer, particularly the younger shopper comfortable buying micro-trend product direct from a phone. The two KPIs that matter most for standalone Primark are like-for-like (same-store) sales growth, which reveals whether the existing estate is still pulling shoppers and baskets, and the pace and productivity of new store roll-out, especially in the United States — together they tell you whether the physical-only growth engine is still running.

Which brings us to the valuation question the whole demerger ultimately turns on: what is a standalone Primark worth? The bullish framing points to Inditex, the gold standard of listed fashion retail, which has historically commanded a premium earnings multiple — north of twenty times earnings — befitting a high-quality global compounder.[^10] If the market comes to see Primark as a business in that class — disciplined, defensible, with a genuine international growth runway — it could attract a similarly premium rating, which is precisely the re-rating the demerger is designed to capture. The bearish framing warns that the market may instead anchor Primark closer to the deflated multiples of traditional, structurally challenged high-street and department-store retail, treating its lack of a full e-commerce business not as a moat but as a liability. The gap between those two outcomes — premium global compounder versus discounted high-street retailer — is, in essence, the prize the 2026 split is gambling on. Which way the market lands is, of course, not yet known.

XI. Epilogue

Return, finally, to where this began — to Garfield Weston in 1935, buying bakeries in a depression with a conviction that owning the whole chain, and holding it patiently, was the surest path to durable wealth. Nearly a century later, his great experiment culminated in a £13 billion enterprise that the family chose, in April 2026, to deliberately split in two — not out of weakness, but to crystallise the value that decades of patient, contrarian compounding had quietly built.1

The throughline from that 1935 bakery to the 2026 demerger is the discipline of saying no. No to the middleman, in Garfield Weston's day. No to the activists and the short-term pressures, courtesy of the cornered resource of family control. No, most famously, to the e-commerce orthodoxy that every consultant insisted was Primark's only future — a refusal that turned out to be the very source of its strength. The deepest lesson of Associated British Foods is that conventional wisdom, in business as in markets, is most dangerous precisely when it is most universal, and that the patient capital to defy it is itself a rare and valuable asset. What happens next — whether two FTSE 100 companies prove worth more apart than the conglomerate was together — is the open question the market will spend the coming years answering.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube