Anglo American: The Ultimate Metamorphosis

I. Introduction & The $39 Billion Siege

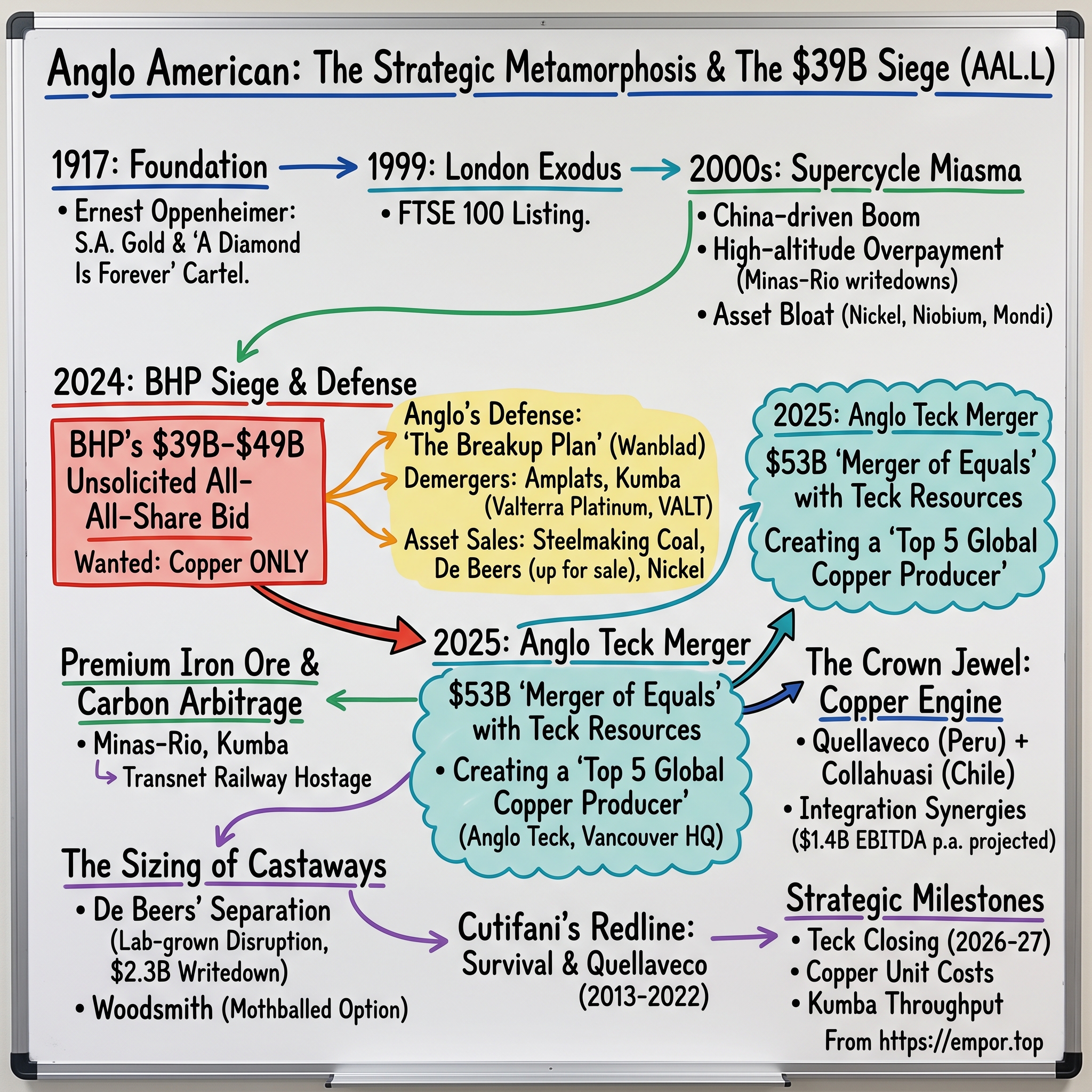

On the morning of April 25, 2024, the boardroom at 17 Charterhouse Street in London had the atmosphere of a house that had just discovered an intruder already inside. Anglo American plc — a 107-year-old institution born in the gold reefs of the Witwatersrand — had received an unsolicited, all-share approach from BHP Group, the largest mining company on Earth. The board rejected it the next day, calling it "opportunistic" and a structure that "significantly undervalues Anglo American."1 The first proposal valued the company at roughly £31 billion.2 Within a month it would climb to £38.6 billion — about $49.2 billion — and become the most consequential takeover drama in the history of the global mining industry.4

Here was the twist that made the siege so revealing: BHP did not actually want all of Anglo American. It wanted the copper. Anglo's crown jewels — tier-one copper mines in Peru and Chile — were, in BHP's reading, buried under a pile of assets that a disciplined Australian miner had no appetite to own: a politically radioactive South African platinum business, an iron-ore operation hostage to a collapsing state railway, and a diamond empire sliding into irrelevance. So BHP structured its bid as a kind of financial surgery. Before BHP would take Anglo, Anglo's own shareholders had to first swallow two separate demergers — spinning out Anglo American Platinum and Kumba Iron Ore — leaving BHP to walk away with a clean copper-and-iron-ore portfolio and none of the mess.13

It was, in effect, an invitation to Anglo to dismember itself for a predator's convenience. The genius — and the audacity — of the Anglo defense was to accept the logic of dismemberment while denying BHP the prize. If the market was applying a "conglomerate discount" to Anglo, punishing it for owning too many unrelated things, then CEO Duncan Wanblad would tear the conglomerate apart faster and more radically than any acquirer could, and hand the value to Anglo's own shareholders rather than BHP's. On May 14, 2024, in the middle of the bid battle, Wanblad unveiled what he called "the most radical changes to Anglo American in decades."7 Call it defense-by-implosion: blow up your own house so the burglar has nothing left to steal.

The strategy worked in the narrow sense — BHP walked away on May 29, 2024, unable to make a firm offer before the UK Takeover Panel's deadline, and was barred from re-approaching for six months.45 But the more astonishing outcome came sixteen months later. On September 9, 2025, the streamlined Anglo announced a "merger of equals" with Canada's Teck Resources to create Anglo Teck, a roughly $53 billion critical-minerals champion and a top-five global copper producer, headquartered in Vancouver and primary-listed in London.910 The company that BHP had tried to carve up had instead reassembled itself, on its own terms, as exactly the kind of focused copper business the market had been begging for.

There is a deeper reason the siege matters beyond the drama of a single takeover fight. Anglo American is one of the purest case studies in business history of a specific pathology: the diversified resource conglomerate that owns genuinely great assets and is nonetheless chronically undervalued because the market cannot see them through the clutter. For two decades, sophisticated investors had looked at Anglo and performed a mental sum-of-the-parts, concluding that the copper alone was worth more than the whole company's market capitalization — which meant the market was assigning the platinum, diamonds, coal, nickel, and iron ore a negative value in aggregate. When an asset is worth less inside a company than outside it, you have, by definition, a structure that destroys value simply by existing. BHP's bid was the moment that latent arbitrage became explicit, and it forced a question every conglomerate eventually faces: break yourself up, or let someone else do it to you.

This is the story of how Anglo answered that question. It runs through the diamond and gold cartels of Sir Ernest Oppenheimer's South Africa; the 1999 exodus to London; the value-destroying acquisition fever of the China supercycle; a near-death experience in 2015 and the turnaround that followed; the BHP siege and the fire-sale of legacy assets; and finally the copper engine that made Anglo worth fighting over in the first place. Along the way we will test the bull and bear cases on the newly minted Anglo Teck, and ask the question that matters for any long-term owner: is this a genuinely durable business, or simply a well-executed escape?

II. The Oppenheimer Empire: South African Gold, Diamond Cartels, and the London Exodus (1917–1999)

Ernest Oppenheimer arrived in Kimberley in 1902 as an eighteen-year-old diamond buyer, a German-Jewish émigré who would spend the next half-century building the most powerful private enterprise the African continent had ever seen. On September 25, 1917 — with Europe still tearing itself apart in the Great War — he incorporated the Anglo American Corporation of South Africa with roughly £1 million of capital.1112 The name was a marketing flourish as much as a description: the money came from both sides of the Atlantic, with British investors on one side and American financiers, including J.P. Morgan & Co. and the Newmont Mining Corporation, on the other.1113 The purpose was blunt and specific — to raise the enormous sums needed to mine the deep-level gold of the East Rand, where the richest ore lay thousands of feet underground and beyond the reach of any single small operator.

Gold built the company, but diamonds made it legendary. Oppenheimer understood something Cecil Rhodes had grasped a generation earlier when he founded De Beers Consolidated Mines in 1888: a diamond has no intrinsic industrial value to speak of, so its price depends entirely on the control of supply and the manufacture of desire.14 Oppenheimer joined the De Beers board in 1926 and became its chairman in 1929, seizing the levers of the global diamond trade at the precise moment the Great Depression threatened to collapse it.1113 His answer was the Central Selling Organisation — a single channel through which the world's rough diamonds would flow, with De Beers stockpiling stones in downturns and releasing them in booms to hold prices firm.1315 At its peak the cartel controlled the overwhelming majority of the world's rough supply. Two decades later the machine acquired its immortal tagline when copywriter Frances Gerety of the N.W. Ayer agency wrote "A Diamond Is Forever" in 1947; the line first ran in 1948 and has anchored De Beers marketing ever since, single-handedly inventing the modern engagement ring as an obligation.15

What the diamond cartel demonstrated — and what matters for understanding Anglo's entire subsequent history — is that the company's foundational skill was never really geology. It was the engineering of scarcity and the management of political relationships. Under Ernest's son Harry Oppenheimer, who chaired Anglo American from 1957 to 1982, the corporation became something close to a parallel state.16 By the 1980s Anglo and its affiliates were estimated to account for around a quarter of South Africa's GDP and a majority of the value on the Johannesburg Stock Exchange, with tentacles in coal, steel (Scaw Metals), paper and packaging (Mondi, founded 1967), gold, and beyond.1617 Harry Oppenheimer publicly criticized apartheid while his company profited handsomely from the cheap, controlled Black labor that the system produced — a contradiction that liberal Anglo never resolved and that its critics never forgot.

It is worth pausing on how the diamond cartel actually worked, because it is the clearest early example of the kind of engineered advantage Anglo would spend the rest of its life chasing. De Beers did not sell diamonds the way a normal company sells a product. It aggregated the world's rough production — its own mines plus stones bought in from rivals and, later, from the Soviet Union and others — into a single stockpile, then sold pre-assorted, pre-priced parcels called "sights" to a hand-picked list of "sightholders" who were not permitted to negotiate. Take the box at the stated price, or lose your seat at the table. By controlling how much rough reached the market and when, De Beers could hold prices firm through recessions that would have crushed any freely traded commodity. It was a cartel in the textbook sense, and for the better part of a century it worked, because there was no meaningful substitute for a natural diamond and no rival with the balance sheet to hoard inventory at De Beers' scale. Remember that mechanism — supply control plus manufactured demand — because its eventual collapse, when a genuine substitute finally arrived, is one of the most important threads in the modern part of this story.

By the early 1990s, with apartheid ending and a democratic South Africa arriving in 1994, Anglo faced a strategic cage. Its capital was trapped behind South African exchange controls, its valuation was hostage to emerging-market risk premiums, and it could not compete for global assets against the likes of a newly merging BHP Billiton or Rio Tinto. The escape came in May 1999, when Anglo American Corporation combined with its offshore vehicle Minorco to form Anglo American plc, moved its headquarters to London, and began trading on the London Stock Exchange on May 24, 1999 with a market capitalization of roughly £6.1 billion — instantly large enough for the FTSE 100.1718 The official rationale was access to global capital markets; the practical effect was liberation from the rand and from South African political risk. It was a bet that Anglo could shed its identity as a national champion and become a genuinely global, diversified, tier-one miner.

That bet set up the central tension of the next quarter-century. Anglo went to London to be treated as a peer of BHP and Rio Tinto. Instead, the market would spend the 2000s and 2010s deciding that it was something worse — a sprawling, indisciplined conglomerate that happened to own some world-class assets. How Anglo earned that reputation is the story of the supercycle.

III. The Supercycle Miasma: High-Altitude Overpayment and Asset Bloat (2000–2012)

If you want to understand how a great company loses its way, watch what it does at the top of a cycle. The 2000s handed the mining industry the single greatest demand shock in its modern history: China's industrialization, which turned the country into a bottomless furnace for iron ore, copper, coal, and steel. Prices went vertical. Iron ore, which had traded in single-digit-per-tonne obscurity for decades, peaked near $187 a tonne in early 2011; copper touched roughly $10,000 a tonne in the same window.17 For a diversified miner, it felt like the laws of gravity had been repealed. And when management teams believe gravity has been repealed, they overpay.

In 2007, Anglo appointed Cynthia Carroll as chief executive — the first non-South African, the first woman, and the first outsider ever to run the company.19 An American with a geology background who had run Alcan's aluminum smelters, Carroll arrived with a mandate to modernize a clubby, insular institution. What she also brought was a conviction that Anglo needed a transformational growth asset of its own. She found it in Brazil, in a project owned by the flamboyant Brazilian billionaire Eike Batista, whose MMX Mineração was developing the Minas-Rio iron-ore deposit in Minas Gerais.

The Minas-Rio acquisition became a case study taught in business schools as a warning. In January 2008, at the very crest of the cycle, Anglo agreed to pay around $5.5 billion for a vehicle holding Batista's Minas-Rio and Amapá interests — a price struck when iron ore seemed destined only to rise.20 Then reality arrived. The project needed a 529-kilometer slurry pipeline to carry iron-ore concentrate from the mountains to the coast, and it ran headlong into Brazil's labyrinthine environmental licensing, land disputes, and construction overruns. First ore did not ship until October 2014 — years late — and the total development bill swelled to roughly $8.8 billion, on top of the purchase price.22 When the iron-ore price then collapsed, Anglo wrote down billions against the asset, taking a charge of around $3.5 billion on Minas-Rio within a broader impairment in its 2014 results.23 A peak-cycle purchase had become one of the most value-destructive acquisitions in the history of mining.

Minas-Rio was the most spectacular wound, but the deeper problem was structural. By the end of Carroll's tenure Anglo was a genuine conglomerate — nickel, niobium, phosphates, paper, coal, diamonds, platinum, copper, iron ore — with 68 separate mining operations and no coherent identity.24 Contrast that with the ruthless focus emerging at BHP and Rio Tinto, which were concentrating capital in a handful of enormous, low-cost, long-life assets and returning cash to shareholders. Investors rewarded focus and punished sprawl, and Anglo traded at a persistent discount to its diversified peers — the so-called conglomerate discount that would still be dragging on the shares when BHP came knocking twelve years later.

It is tempting, with hindsight, to make Carroll the villain of this chapter, but that would be lazy history. She was doing what the entire industry was doing, and what her own board and shareholders were demanding: growing into a supercycle that everyone believed had years left to run. The deeper failure was institutional. Anglo lacked the capital-allocation discipline — the willingness to say no at the top of a cycle, the honest project engineering, the ruthless post-mortems — that separates the miners who compound wealth from the miners who merely dig. A company that could engineer a diamond cartel to the last carat somehow could not build a pipeline in Brazil on budget. The gap between Anglo's commercial sophistication and its operational execution is a recurring character in this story, and it would not be truly addressed for another decade.

Carroll's leadership frayed under the strain. The South African platinum business, Anglo American Platinum, was wracked by labor conflict; in October 2012, in the tense aftermath of the wildcat strikes sweeping the platinum belt, Amplats dismissed around 12,000 workers, a decision that inflamed both unions and the government.21 (The infamous Marikana massacre that August, in which police killed 34 miners, occurred at a rival, Lonmin — but the entire sector, Anglo included, was engulfed in the fallout.) Carroll announced her departure in January 2013.19 Anglo had spent the supercycle proving it could grow. What it had not proven was that it could allocate capital. That job fell to a blunt-spoken Australian who arrived believing the company was, in his own estimation, close to broken.

IV. Cutifani's Redline: Survival, Quellaveco, and the Sirius/Woodsmith Gamble (2013–2022)

Mark Cutifani took over as Anglo American's chief executive on April 3, 2013, and he did not sugarcoat what he inherited.19 A miner's miner — he had started underground in Australian coal and gold pits before running AngloGold Ashanti — Cutifani looked at Anglo's portfolio and saw a company that was, operationally and financially, dangerously overextended. His timing was cruel: within two years the supercycle finally broke. Chinese demand growth slowed, commodity prices cratered across the board, and by late 2015 Anglo was staring at an existential crisis.

The numbers told the story of a near-death experience. In December 2015 Cutifani suspended the dividend and announced a restructuring so severe it amounted to reconstructive surgery: the workforce would be cut from around 135,000 toward 50,000, the number of business units collapsed, and dozens of assets sold, with a target of driving net debt below $10 billion.24 The share price, which had traded above 1,500 pence in headier days, collapsed to roughly 215 pence in January 2016 — a level that implied the market was pricing in the possibility that Anglo would not survive as an independent company.24 It is difficult to overstate how close the institution came to the edge.

Cutifani's response defined his legacy. Over the following years he shrank the empire from 68 operations to around 37, ruthlessly high-grading the portfolio toward assets that could survive at the bottom of the cycle.24 He layered on a technology and sustainability program branded "FutureSmart Mining," an attempt to reimagine mining around automation, digital control, and lower water and energy intensity.25 Some of this was genuine operational improvement and some was corporate theater, but the direction was right: a smaller, higher-quality, more disciplined Anglo. The balance sheet healed, the dividend returned, and the company that had been left for dead in 2016 was, by the end of the decade, once again generating serious cash.

Cutifani's signal achievement was Quellaveco — a giant copper project in the Moquegua region of southern Peru, 60% owned by Anglo and 40% by Japan's Mitsubishi. Where Minas-Rio had been a monument to peak-cycle overreach, Quellaveco was delivered with unusual discipline. Anglo poured its FutureSmart ambitions into it, building one of the most digitally advanced mines in the world, run from a remote operations center with a fleet of autonomous haul trucks. First production came in July 2022, at a capital cost of around $5.5 billion, and the mine settled into the first quartile of the global cost curve — the cheapest and most defensible position a miner can occupy.35 Quellaveco is the reason Anglo became a copper story, and the reason BHP came calling. We will return to it.

Not every Cutifani-era bet aged as well. In March 2020, days before COVID shut down the world, Anglo completed the acquisition of Sirius Minerals, a British company that had run out of money trying to build the Woodsmith mine beneath the North York Moors — a project to extract polyhalite, a naturally occurring multi-nutrient fertilizer that Anglo would market as POLY4.2829 Sirius had already invested more than $1 billion and had spectacularly failed to raise a roughly $500 million bond in September 2019 after the UK government declined to backstop it, leaving retail shareholders — many of them local Yorkshire investors — facing wipeout.3031 Anglo swooped in with a rescue offer of 5.5 pence per share, valuing Sirius at about £405 million, a fraction of the money that had poured into it.28 Cutifani framed Woodsmith as a multi-generational bet on low-carbon crop nutrients — real optionality, but at a scale and technical difficulty that would soon collide with a leaner Anglo's tolerance for capital risk. That collision is a later chapter.

What did the Cutifani years actually prove, and what did they leave unfinished? They proved that Anglo could be operationally excellent when it had to be — that it could deliver a first-quartile copper mine in Peru on discipline rather than hope, and that it could cut itself down to a survivable core when the alternative was insolvency. But they left the fundamental strategic problem untouched. Even after all the cutting, Anglo entered the 2020s still owning platinum, diamonds, coal, nickel, iron ore, and a speculative British fertilizer project alongside its copper. It was a better-run conglomerate, but it was still a conglomerate — and the market still applied its discount accordingly. Cutifani had performed triage; he had not performed the amputation the market ultimately wanted. That decision, and the crisis that would force it, belonged to his successor.

Cutifani retired in April 2022, handing a repaired but still sprawling company to a South African lifer named Duncan Wanblad. Within two years, Wanblad would be fighting for the company's independence.

V. The Game of Thrones (2024): BHP's Predatory Bid, South African Politics, and the Demerger Defense

Duncan Wanblad is, in almost every respect, the anti-Carroll. Where she was an outsider parachuted in to modernize, he is an engineer from the University of the Witwatersrand who spent more than three decades inside Anglo American, beginning his career underground as a junior engineer before working his way up through the business.2627 He became chief executive on April 19, 2022, and for his first two years he was largely a continuity candidate, executing a modest simplification of the portfolio. Then, in the spring of 2024, BHP's Mike Henry forced him into the fight of his life.

BHP's calculus was cold and, on its own terms, rational. Henry looked at Anglo and saw a copper business trapped inside a South African holding company. BHP wanted the copper; it did not want to become the reluctant owner of Anglo American Platinum or of Kumba Iron Ore, with all the South African labor, community, and political obligations those entailed. So the proposal was conditional: Anglo would have to demerge both Amplats and Kumba to its own shareholders before the deal closed, delivering to BHP a portfolio stripped down to the assets it actually coveted.1 The final, third proposal valued Anglo at £29.34 per share, or £38.6 billion in total, structured as an all-share exchange in which Anglo holders would end up owning a minority of the combined group.34

The Anglo board's public objection was partly about price and partly about something subtler and more damning: execution risk. Wanblad's team argued that forcing two simultaneous, complex demergers in South Africa as a precondition to a takeover created what they called "material completion risk," a process that could drag on for eighteen months or more with no certainty of success, all while Anglo shareholders bore the danger of the deal collapsing midway.3 In plain terms, BHP was asking Anglo to do the hard, risky, value-destroying part — the South African disentanglement — and then hand over the reward. The board rejected the proposals unanimously across late April and May 2024.

The politics were combustible. South Africa's Minister of Mineral Resources and Energy, Gwede Mantashe, made his hostility personal and public, saying he would not support the deal and pointing to BHP's history in the country — its 2015 spinout of unwanted assets into South32, which Mantashe characterized as having left South Africa worse off. "Our experience with BHP has not been positive," he said, warning of capital flight.6 For a foreign giant proposing to restructure two of South Africa's most important employers, that political wall was as formidable as any financial obstacle. On May 29, 2024, BHP declined to make a firm offer before the Takeover Panel's deadline and walked away, locked out by UK rules from re-approaching for six months.45

But Wanblad had already seized the strategic initiative. On May 14, 2024, in the middle of the bid, he announced a sweeping portfolio simplification with a clarifying message: Anglo would refocus on copper, premium iron ore, and crop-nutrients optionality, and shed almost everything else — targeting around $800 million in annual pre-tax cost savings in the process.7 The execution, over the following two years, was relentless:

- Platinum. Anglo demerged Anglo American Platinum, which was renamed Valterra Platinum. The demerger became effective on May 31, 2025, with Valterra admitted to the London Stock Exchange under the ticker VALT alongside its Johannesburg primary listing; Anglo retained a residual holding of just under 20% to sell down over time.8

- Nickel. In February 2025, Anglo agreed to sell its Brazilian nickel business to MMG — a subsidiary of China's state-controlled 中国五矿集团 China Minmetals — for up to $500 million, comprising $350 million upfront plus price-linked and contingent payments.60

- Diamonds. Anglo put De Beers up for sale or demerger, a process complicated by a collapsing diamond market and, ultimately, a $2.3 billion impairment booked in early 2026.59 (More on that in Section IX.)

- Steelmaking coal. This became the saga within the saga. Anglo first agreed to sell its Australian metallurgical-coal portfolio to Peabody Energy for up to about $3.8 billion. Then, in March 2025, an ignition event at the Moranbah North mine forced a suspension of longwall production, and in August 2025 Peabody terminated the deal, invoking a material-adverse-change clause — a termination Anglo disputed and moved to challenge.61 Only in May 2026 did Anglo find a new buyer, agreeing to sell the coal business to Dhilmar Limited for up to $3.875 billion, structured as $2.3 billion upfront plus an earnout of up to $1.575 billion tied to future coal prices.62

Step back and consider the sheer nerve of what Wanblad attempted here, because it is easy to lose in the list of transactions. A conventional takeover defense argues that the bidder is offering too little and the target is worth more as it stands. Wanblad's defense conceded the opposite: he agreed the company as constituted was worth less than the sum of its parts, and then argued that Anglo's own management could unlock that value faster and more cleanly than BHP could — capturing it for Anglo shareholders instead of surrendering it to the acquirer. It was, in a sense, an admission of decades of strategic failure repackaged as a rescue plan. The risk was obvious: having publicly committed to dismantling itself, Anglo now had to execute, in weak markets, under a spotlight, with every slipped deadline becoming ammunition for the next predator or the next activist. A defense-by-implosion only works if you can actually control the implosion.

The coal episode is worth dwelling on because it punctures any tidy narrative of a smooth, masterful restructuring. Divesting legacy assets into weak or volatile markets, with operational accidents and hostile counterparties, is slow, expensive, and uncertain. Anglo executed the strategy under duress and largely delivered it — but the transaction friction was real, the timelines slipped, and the proceeds came in below the headline hopes of 2024. For all the talk of nimbleness, the machinery of dismemberment ground slowly. What made the whole exercise worthwhile was the quality of the assets left standing at the center of it. Chief among them: copper.

VI. The Crown Jewel Deep-Dive: The Copper Engine (Quellaveco, Collahuasi, Los Bronces)

To understand why anyone would fight a two-year corporate war over Anglo American, you have to understand copper — and specifically, why the world is running short of it. Copper is the physical substrate of electrification. It is in the windings of every electric motor, the cabling of every power grid, the charging infrastructure of every electric vehicle, and, increasingly, in the power-hungry guts of AI data centers. It has few economic substitutes at scale; aluminum can replace it in some transmission applications, but for most electrical uses copper's conductivity is irreplaceable. And the problem is supply. In January 2026, S&P Global projected that copper demand would reach around 42 million tonnes by 2040 — roughly 50% above current levels — while mine supply was set to peak around 2030 and then decline, opening a structural shortfall it estimated at close to 10 million tonnes and described as a "systemic risk" to the energy transition.39 New tier-one copper discoveries have become vanishingly rare, permitting takes a decade or more, and grades at existing mines are falling. In that world, a portfolio of long-life, low-cost copper mines is close to irreplaceable — which is exactly what Anglo owns.

Quellaveco in Peru is the modern showpiece, and its story we have already told: 60% Anglo, 40% Mitsubishi, first production in 2022, first-quartile costs, and a level of automation — a remote operations center directing a fleet of autonomous trucks — that makes it one of the most digitally sophisticated mines on the planet.3536 It was designed to produce on the order of 300,000 tonnes of copper a year in its first decade. Crucially, it is a young mine with decades of reserves ahead of it, in a country where Anglo has managed the community and water relationships that so often sink Andean copper projects.

Collahuasi in northern Chile is the quiet giant of the portfolio, and arguably the most valuable single asset Anglo owns. It is jointly held — 44% Anglo, 44% Glencore, and 12% Japan's Mitsui — and it sits atop one of the largest and highest-grade copper deposits in the world, with a reserve grade of nearly 1% copper that dwarfs most of its Chilean peers. Anglo's attributable share of production runs in the region of 245,000 tonnes a year.38 Collahuasi's value is not just its scale but its longevity: this is a multi-decade orebody, the kind of cornerstone asset that cannot be replicated by any amount of exploration spending. Its challenges are the classic Chilean ones — declining head grades over time and the perennial scarcity of water in the Atacama, the driest desert on Earth — but these are problems of management, not of resource quality.

Los Bronces, also in Chile and 50.1% Anglo-owned, is the portfolio's problem child and its most honest lesson. It is an older, higher-cost mine that has been battered by exactly the twin pressures the sector fears most: a multi-year Chilean drought that starved it of water, and a long grade decline that meant digging more rock for less metal. Anglo's response was telling. Rather than chase volume, management placed the smaller and less efficient of the site's two processing plants on care and maintenance around mid-2024, adopting an explicit "value over volume" posture — accepting lower output in exchange for better margins — while pinning its hopes on a desalination supply coming online in 2026 and a higher-grade underground development phase expected to lift production from around 2027.3738 Los Bronces is a reminder that not all tier-one assets are created equal, and that even a great copper franchise contains mines fighting the slow entropy of depletion.

A word on water, because it is the single most underappreciated variable in Andean copper and it runs through all three assets. Copper processing is thirsty — grinding ore into slurry and floating out the metal consumes enormous volumes of water — and the great copper deposits of Chile and Peru sit in some of the driest terrain on the planet. For years, miners drew on scarce Andean aquifers and glacial melt, pitting them against farmers and communities in fights they increasingly lose. The industry's answer is desalination: build a plant on the coast, and pump treated seawater hundreds of kilometers uphill to the mine, often climbing thousands of meters in elevation. It works, but it is staggeringly capital-intensive and energy-hungry, effectively adding a second megaproject alongside every mine. This is why "who has secured desalinated water" is quietly becoming as important as "who has the best orebody" in Chilean copper — and why, as we will see, water infrastructure sits at the heart of the logic for combining Anglo and Teck's neighboring Chilean mines. A miner without a water solution is a miner on borrowed time.

Across the group, Anglo produced 773,000 tonnes of copper in 2024, dipping to 695,000 tonnes in 2025 as grades softened, with guidance of roughly 700,000–760,000 tonnes for 2026.38 How does that stack up against the majors? BHP's Escondida in Chile — the largest copper mine on Earth — alone produces on the order of 1.28 million tonnes a year.40 Freeport-McMoRan's Grasberg complex in Indonesia is another giant, and Antofagasta's clustered Chilean mines produce roughly 670,000–710,000 tonnes.4142 Anglo, in other words, was a serious but sub-scale copper player — big enough to be a prize, not big enough to be a leader. That gap between "prize" and "leader" is precisely what the Teck merger was designed to close.

VII. The Anglo Teck Masterstroke: Inside the 2025/2026 Consolidation of Global Metals

Corporate history rarely offers a plot twist this clean. Fifteen months after fending off a predator that wanted its copper, Anglo American announced that it would combine with another company's copper — voluntarily, as equals, on its own terms. On September 9, 2025, Anglo and Canada's Teck Resources unveiled a "merger of equals" to create Anglo Teck, described by both boards as a "global critical minerals champion."910 The structure was elegant: an all-share, nil-premium merger under a Canadian plan of arrangement, in which Anglo would issue 1.3301 of its shares for each Teck share, leaving Anglo shareholders owning about 62.4% of the combined company and Teck holders about 37.6%.9 The whole thing was valued at roughly $53 billion.44

To appreciate why this was a coup rather than a capitulation, you need Teck's backstory, which rhymes uncannily with Anglo's own. Teck is a Canadian mining institution controlled for decades by the Keevil family through a dual-class share structure — Class A shares carrying 100 votes each against Class B shares carrying one — with patriarch Norman Keevil holding sway over a majority of the Class A stock.47 Like Anglo, Teck had been stalked: in April 2023, Glencore made an unsolicited roughly $23 billion approach for Teck, which the Keevils rejected as strategically wrong for Canada.47 And like Anglo, Teck had already begun purifying itself into a copper company, agreeing in November 2023 to sell its steelmaking-coal business, Elk Valley Resources, in a deal valuing it at $9 billion, with Glencore taking 77% for $6.9 billion and Nippon Steel and POSCO taking the rest.48 Teck's prize was Quebrada Blanca (QB), a newly ramped-up copper mine in northern Chile.

And here is the strategic hinge on which the entire merger turns. Teck's Quebrada Blanca sits right next to Anglo's Collahuasi. They are neighbors in the same Chilean copper belt. The two companies estimate around $800 million in annual pre-tax synergies from the overall combination, but the headline prize is separate and larger: an additional roughly $1.4 billion of potential annual EBITDA (on a 100% basis, over 2030–2049) from physically integrating Collahuasi and QB — sharing processing plants, desalinated water infrastructure, and logistics between two adjacent orebodies that were, absurdly, being developed as if the other did not exist.910 Independent analysts at CRU have described the integration as a "billion-dollar gift," modeling the trucking or conveying of high-grade Collahuasi ore into QB's underused mill capacity — a textbook case of value that exists only when two owners become one.43 This is scale economics in its purest form: not bigger for the sake of bigger, but the elimination of duplicated fixed infrastructure in one of the hardest places on Earth to build it.

The combined entity is designed to be a pure critical-minerals play: a top-five global copper producer with combined output of around 1.2 million tonnes a year, rising toward 1.35 million tonnes by 2027, and offering investors more than 70% exposure to copper.9 The corporate architecture reflects a careful balancing of nations and egos. Global headquarters will sit in Vancouver — a significant symbolic concession, planting the flag in Canada — with the primary share listing remaining in London and secondary listings in Johannesburg, Toronto, and New York.910 Duncan Wanblad will be CEO; Teck's Jonathan Price becomes deputy CEO; John Heasley is CFO; and Sheila Murray chairs the board.9 As part of the deal, Anglo declared a $4.5 billion special dividend to its own shareholders — about $4.19 per share — payable before completion, a sweetener that also helps balance the value exchange between the two shareholder bases.9

There is a governance subtlety here that a careful investor should not miss. Teck was controlled, for decades, by the Keevil family's supervoting Class A shares — the very structure that let Norman Keevil swat away Glencore's advances regardless of what ordinary shareholders wanted. A merger of equals with a widely held London company like Anglo necessarily requires collapsing or neutralizing that control, and the deal terms reflect painstaking negotiation over the dilution of family influence, board composition, and the symbolic geography of headquarters. Planting the head office in Vancouver, keeping a Canadian deputy CEO and chair, and preserving a Toronto listing are not accidents; they are the price of persuading a proud Canadian institution and its controlling family to fold into a company still viewed, in some quarters, as fundamentally South African and British. The special dividend, too, is more than a sweetener — it rebalances value between two shareholder bases whose assets and net debt differ, ensuring neither side feels it overpaid at a nil-premium "at-market" exchange. Mergers of equals are notoriously the hardest deals to make work precisely because there is no premium to paper over the inevitable clashes of culture and ego; the ones that succeed are the ones where the strategic logic is overwhelming enough to survive them. Here, the logic — two neighboring orebodies, one shared set of infrastructure — is about as overwhelming as mining gets.

Whether the masterstroke actually lands depends on closing, and closing depends on politics. The merger requires approval under Canada's Investment Canada Act plus competition clearances across multiple jurisdictions and shareholder votes on both sides. Canada granted its Investment Canada Act approval in December 2025 — a critical hurdle cleared — and Anglo has said it expects the final approvals to fall between September 2026 and March 2027.4546 Wanblad has publicly insisted the integration is "moving at pace," with remaining clearances the gating item rather than any dispute between the two sides.64 Until those clearances arrive, Anglo Teck is a plan, not a company. But the strategic logic is hard to dispute: two stalked copper businesses, each having spent years shedding legacy baggage, combining to become too large and too Canadian to be easily swallowed. The best defense against the next predator is to become the consolidator yourself.

VIII. Premium Iron Ore & The Direct Reduction Carbon Arbitrage (Minas-Rio & Kumba)

There is a common misconception that iron ore is a commodity — a single, fungible red dirt priced off one benchmark. It isn't, and the difference is where Anglo's iron-ore story gets genuinely interesting. The great decarbonization challenge for steel is that the traditional blast furnace runs on coking coal and belches carbon dioxide. The cleaner alternative — direct reduction paired with an electric arc furnace, potentially using green hydrogen — is chemically fussy: it demands very high-grade iron feedstock, generally above 65% iron content, to work efficiently. High-grade ore, in other words, is becoming a decarbonization input, and it commands a premium that low-grade ore does not. Anglo owns two sources of exactly this premium product.

Minas-Rio in Brazil — the asset that nearly broke Anglo in Cynthia Carroll's era — has, in one of the quieter ironies of this story, matured into a genuinely valuable business. It produces premium pellet feed of roughly 67–68% iron content, precisely the grade prized for low-carbon direct-reduction steelmaking; Anglo has signed supply agreements aimed at that market, including with Bahrain Steel.51 In 2024 the mine delivered a record 25 million tonnes.53 The asset that was once a monument to overpayment is now a first-and-second-quartile cash generator, and Anglo has been quietly enlarging it. In two transactions across 2024, Anglo brought Vale in as a 15% partner in an enlarged Minas-Rio, folding in Vale's adjacent Serra da Serpentina orebody — a multi-billion-tonne resource that Anglo says creates the scope to roughly double its premium pellet-feed production over time.4950 The lesson is worth pausing on: a catastrophic acquisition, given fifteen years, a rebuilt pipeline, and a decarbonizing steel market, can eventually become a keeper. It did not vindicate the price Anglo paid in 2008; it simply outlived the mistake.

That said, Minas-Rio's history is a cautionary tale about operational fragility. In March 2018, two leaks on its 529-kilometer slurry pipeline forced Anglo to suspend the entire operation for a full inspection lasting roughly 90 days — a reminder that a single point of infrastructure failure can idle a whole mine.52 Premium ore is worth a premium precisely because it is hard to produce and deliver reliably.

Why does the grade premium matter so much, in plain terms? A blast furnace, the traditional way to make steel, can tolerate lower-grade iron ore because it burns coking coal to strip out the impurities — but that combustion is exactly what makes steelmaking one of the largest industrial sources of carbon dioxide on the planet. The cleaner route, direct reduction, uses natural gas or hydrogen instead of coal to convert iron ore into metallic iron at lower temperatures, and it can slash emissions dramatically. The catch is that direct reduction is chemically intolerant of impurities: feed it mediocre ore and the resulting product is riddled with slag-forming waste that clogs the downstream electric furnace. It demands the good stuff — high iron content, low silica and alumina. So as the world's steelmakers face pressure to decarbonize, the small slice of global iron ore that meets direct-reduction specifications is poised to command a widening premium over the ocean of ordinary ore. That is the "carbon arbitrage" in this section's title: owning the scarce feedstock that a decarbonizing industry will increasingly be forced to pay up for. It is a real thesis, though an unproven one — green-steel adoption has been slower than the optimists promised, and the premium only materializes if and when direct reduction scales.

Kumba Iron Ore in South Africa, 69.7% owned by Anglo and separately listed in Johannesburg, is the other half of the premium story — and the more troubled half.5455 Kumba's Sishen and Kolomela mines produce high-grade lump and fine ores that earn a premium over the benchmark; in 2024 the company realized an average FOB export price of about $92 per wet metric tonne, some 3% above the 62% iron benchmark.54 The ore is excellent. The problem sits between the mine and the sea. Kumba is a hostage to Transnet, South Africa's state-owned rail and port operator, whose freight network has deteriorated into one of the country's most visible infrastructure failures — derailments, locomotive shortages, cable theft, and chronic underinvestment. Rail volumes to port have fallen sharply since 2019, forcing Kumba to shelve expansion plans, stockpile unsold ore at the mine gate, and cut production to match what Transnet can actually move.56 Kumba produced 35.7 million tonnes in 2024 and guided 2026 output down to 31–33 million tonnes, a reduction driven not by geology but by the state of a railway.54

This is the cruelest kind of value destruction: a world-class orebody throttled by infrastructure the company does not control. It also explains a great deal about Anglo's broader strategic logic. An asset whose output is capped by a dysfunctional state monopoly, in a jurisdiction with elevated political risk, is precisely the sort of thing that dragged on Anglo's valuation and made BHP want to leave Kumba behind. Anglo intends to keep its premium iron ore in the Anglo Teck portfolio — the grade advantage is real and the decarbonization thesis is credible — but Kumba's fate will be written less in the ore body than in the Transnet control room. For investors, that makes rail throughput one of the few genuinely load-bearing numbers to watch.

IX. Sizing the Castaways: De Beers' Separation, Woodsmith's Crop Nutrients, and Divestment Realities

Every restructuring produces castaways — assets sized not to the ambitions once attached to them but to their true, diminished economic weight. Anglo has two that deserve honest accounting precisely because their symbolism vastly exceeds their current worth: the diamond empire that was once the family's crown, and the fertilizer mega-project buried beneath the Yorkshire moors.

De Beers is the more poignant story, because it is the story of a moat that dissolved. For most of a century, De Beers controlled diamonds by controlling supply and manufacturing desire — the Central Selling Organisation and "A Diamond Is Forever" were two sides of the same engineered scarcity. Two forces have now broken that machine. The first is lab-grown diamonds, which are physically and optically identical to mined stones, cost a fraction as much, and have collapsed the consumer's willingness to pay a premium for the natural version — a textbook substitution shock against a product whose entire value was psychological. The second is a broad luxury slowdown, particularly in China, that has left the rough-diamond market awash in unsold inventory. The financial results are brutal. De Beers swung to an underlying EBITDA loss of $25 million in 2024, from a small profit the year before, and the bleeding worsened to a $189 million loss in the first half of 2025 as realized rough prices kept falling.57 In early 2026, reporting its full-year 2025 results, Anglo took a $2.3 billion impairment against De Beers, cutting its carrying value from about $4.1 billion to roughly $2.3 billion — the third consecutive annual writedown of the business — and posted a group net loss of $3.7 billion largely on the back of it.5859

The lab-grown threat deserves to be understood precisely, because it is a textbook disruption and a cautionary tale about the fragility of brand-based moats. A lab-grown diamond is not a fake or a simulant like cubic zirconia; it is chemically, physically, and optically an actual diamond, grown in a reactor in weeks rather than a billion years in the mantle, and indistinguishable to the naked eye or even to most gemological equipment. When the substitute is genuinely identical and costs a fraction as much, the incumbent's only defense is the story — the idea that a natural diamond carries meaning a manufactured one cannot. De Beers spent a century and untold marketing billions building exactly that story, and for a while it held. But stories are the weakest form of moat, because they depend entirely on the customer continuing to believe them, and younger consumers have proven far more willing to buy the cheaper identical stone and pocket the difference. Wholesale lab-grown prices have collapsed as production scaled, dragging perceptions of diamond value down with them, and the natural-diamond premium has compressed accordingly. This is the mirror image of the cartel's founding logic: De Beers once manufactured scarcity: technology has now manufactured abundance, and no marketing budget can outlaw a chemistry set.

Wanblad has said the sale of De Beers is "at an advanced stage," with a deal targeted in 2026, and the process involves the Government of Botswana, which holds 15% of De Beers and supplies the majority of its rough diamonds.59 But the honest read is that Anglo is trying to sell a declining asset into a falling market, with a strategically essential but financially constrained partner beside it. The moat that Ernest Oppenheimer spent a lifetime building has become a liability to be exited at whatever price the market will bear. There is no clearer illustration in this entire story of how a durable competitive advantage — control of supply plus manufactured demand — can be undone by a genuine substitute the incumbent cannot outlaw.

Woodsmith, the polyhalite project in North Yorkshire that Anglo rescued from Sirius Minerals in 2020, is the opposite kind of castaway: not a faded moat but an unproven, capital-devouring bet on a fertilizer market that may or may not materialize at the scale required. The thesis is genuinely attractive in the abstract — POLY4 is a natural, low-carbon, multi-nutrient fertilizer, and the world needs more sustainable crop inputs. The problem is the price of admission. Building a mine more than a kilometer beneath a national park, with a 37-kilometer underground tunnel to the coast, is one of the most technically demanding construction projects in Britain, and the costs kept climbing. Anglo booked a $1.7 billion impairment against Woodsmith in its 2022 results and a further $1.6 billion in mid-2024, when — under the pressure of the BHP defense and its own balance-sheet discipline — it decided to dramatically slow development, cutting planned capital to around $200 million in 2025 and to nil in 2026 while it completed technical studies and searched for a joint-venture partner to share the multi-billion-dollar burden of finishing the mine.323334

The Woodsmith decision is a useful window into Anglo's revealed priorities. Faced with a war for survival, management chose to protect copper and the balance sheet and to defer the speculative fertilizer dream, effectively mothballing a project into which billions had already gone. That is disciplined capital allocation under duress — but it is also an admission that Woodsmith, in its current form, was a bet the company could not afford to keep funding alone. For a long-term investor, Woodsmith is best understood as a cheap, deep, out-of-the-money option: potentially valuable if a partner and a strong crop-nutrient market appear, close to worthless if they don't, and correctly sized by management to almost nothing on the balance sheet today. The danger in options is paying too much to keep them alive; Anglo, for now, has stopped paying.

X. Playbook: Business Lessons, 7 Powers Analysis, and the Bull-vs.-Bear Investment Spine

Strip away the century of history and the two years of corporate warfare, and what is left is a specific question for a long-term owner: does the business that emerges from this metamorphosis actually possess a durable competitive advantage, or has Anglo simply traded a bad portfolio for a good one at a favorable moment in the copper cycle? Let's run it through the frameworks and test it honestly.

The Cornered Resource. In Hamilton Helmer's 7 Powers, the most relevant power to a miner is the Cornered Resource — preferential access to a coveted asset that others cannot replicate. This is where Anglo Teck's case is strongest. Tier-one copper orebodies like Collahuasi and Quellaveco are, in a real sense, irreplaceable: greenfield discoveries of comparable quality have essentially stopped, permitting horizons stretch beyond a decade, and grades industry-wide are falling.39 You cannot build a new Collahuasi; you can only own the one that exists. That scarcity, combined with a structural demand shortfall driven by electrification, grids, and AI data centers, is the spine of the bull case. It is also the one advantage in this story that looks genuinely durable rather than cyclical.

Scale Economies. The Teck merger's central rationale — the physical integration of the adjacent Collahuasi and Quebrada Blanca operations — is a clean example of scale economics: sharing processing capacity, desalination, and logistics to spread fixed costs that neither owner could optimize alone.43 But note the honest caveat: this power is prospective, not proven. The $1.4 billion of integration EBITDA is a projection stretching to 2049, contingent on merger completion, capital spending, and execution in a brutally difficult desert environment.9 Believe in it, but discount it for the ten-year path between promise and delivery.

Porter's Five Forces, applied to the copper business, are mostly favorable. Barriers to entry are enormous — the capital, permitting, water, and time required to build a new mine are prohibitive, which protects incumbents. The threat of substitutes for copper in its core electrical uses is low. But two forces cut against the miner. Supplier power is real and rising: water, electricity, and specialized labor in Chile and Peru are scarce and increasingly expensive, and the desalination plants that solve the water problem are themselves enormous capital commitments. And the industry remains a price-taker on a globally traded commodity — no individual miner, however large, sets the copper price. That is the permanent ceiling on any mining "moat": you can own the lowest-cost, longest-life assets in the world and still see your earnings swing violently with a price you do not control.

The activist stress test. A skeptical investor would press several points. First, execution risk is stacked high: Anglo is simultaneously trying to close a $53 billion cross-border merger, complete the sale of De Beers into a falling market, finalize a twice-troubled coal disposal, and sell down residual stakes — a lot of moving parts for one management team, any of which could slip.5962 Second, the Kumba/Transnet problem is not something Anglo can fix; it is a bet on the recovery of a South African state enterprise with a poor track record.56 Third, the copper portfolio is still sub-scale and cyclically exposed, and much of the bull case rests on a supply-shortfall forecast that, like all commodity forecasts, could be wrong.39 Fourth, there is Woodsmith — billions spent, now mothballed, with no proven path to positive returns.33

Management credibility. Wanblad's scorecard is genuinely mixed, and worth reading behaviorally rather than taking at face value. On the positive side, he set out a radical simplification plan in May 2024 and, over two years, largely delivered it against real resistance — that is execution against a stated promise, the gold standard for judging a management team.7 Against him: the coal-sale timeline slipped badly, the proceeds came in below early hopes, and De Beers has been a serial disappointment written down three years running. Most tellingly, in December 2025 Anglo proposed that a majority of executives' share bonuses should automatically vest if the Teck merger completed — a plan the proxy adviser ISS opposed as poor UK governance practice, and which Anglo withdrew on December 8, 2025, the day before the merger shareholder vote.63 Backing down under pressure was the right outcome, but the fact that the board tried it at all is exactly the kind of self-serving capital-allocation instinct an owner should file away. Wanblad is aligned on paper — bound by a shareholding guideline of four times salary — but the bonus episode is a reminder that alignment on paper and alignment in practice are not the same thing.26

Myth versus reality. Three consensus narratives deserve puncturing. The first myth is that Wanblad brilliantly out-maneuvered BHP — that the restructuring was a masterstroke conceived to defeat the bid. The reality is more prosaic and more interesting: the simplification plan was a strategic necessity the company had been circling for years, and BHP simply forced Anglo to do quickly and publicly what it should have done slowly and privately. The bid was the catalyst, not the reason. The second myth is that Anglo Teck is a "done deal." It is not; as of mid-2026 it remains an announced merger awaiting several regulatory clearances, and until those arrive the combined company exists only on paper.45 The third myth is that shedding South Africa makes Anglo a clean copper play. In reality, the group will keep its 69.7%-owned South African iron-ore business, which means it retains direct exposure to Transnet, to South African political risk, and to the rand — the "escape from South Africa" is partial, not total.54 Good analysis separates the transformation that actually happened from the tidier one the headlines describe.

Why it wins, why it may not. The bull case is clean: pure-play exposure to structurally scarce copper and premium decarbonization iron ore; a genuine, once-in-a-generation synergy in the Chilean copper belt; and a simplified balance sheet with the platinum, diamond, and nickel distractions removed. The bear case is equally coherent: the whole thesis is a leveraged bet on the copper price and on flawless execution of a merger that has not yet closed, sitting atop a South African iron-ore business hostage to a broken railway and a diamond business being sold at a loss. Both cases are true at once. That is the nature of a company mid-metamorphosis — the caterpillar is gone, and the butterfly has not yet dried its wings.

XI. Epilogue & Strategic Milestones to Watch

Stand back from the whole saga and the shape of it is almost novelistic. A company founded to mine apartheid-era gold, that built the world's most famous cartel, that fled to London to become a global major, that nearly destroyed itself buying at the top of a cycle and nearly died at the bottom of the next one — that company was cornered by the largest miner on Earth and responded not by surrendering but by turning itself inside out. The conglomerate that BHP found too messy to own was disassembled, and its cleanest, scarcest parts were recombined with a like-minded Canadian survivor into something the market had wanted all along: a focused copper business.

Whether it works is not yet knowable, and no honest observer should pretend otherwise. The transformation is real; the vindication is pending. For investors tracking whether the butterfly actually flies, three numbers carry most of the weight:

-

Copper unit costs and grades at Quellaveco and Collahuasi. The entire bull case rests on these assets holding their first-and-second-quartile cost position as grades naturally decline. Watch whether Anglo Teck can keep costs contained and whether the Collahuasi–Quebrada Blanca integration begins converting projected synergies into actual production and cash.3843

-

The Anglo Teck closing timeline and the De Beers sale. The merger's regulatory approvals are expected between September 2026 and March 2027; the De Beers sale is targeted for 2026. Both are binary events. Delay or failure in either would materially change the story, and the diamond sale in particular is a live test of whether management can exit a declining asset without further value leakage.4559

-

Transnet throughput at Kumba. Premium iron ore is only worth its premium if it reaches a ship. Kumba's volumes are a direct read on the health of South African rail infrastructure — a variable Anglo cannot control but cannot escape.56

The final reflection is this. Anglo American spent a century proving it could find and control scarce things — diamonds, gold, then copper. What it repeatedly failed to prove, from Minas-Rio to Woodsmith, was that it could allocate capital with discipline. The BHP siege forced the issue, stripping away everything that was not scarce, low-cost, and long-lived, and leaving management with almost nowhere to hide. If Anglo Teck succeeds, it will not be because a strategy was clever on a slide; it will be because, for once, a great mining company was disciplined enough to keep only what it should have owned all along. That is the test now. The metamorphosis is complete; the flight has not yet begun.

References

-

Anglo American rejects BHP's third bid, extends deadline — Mining.com, 2024-05-22 ↩

-

Anglo American rejects further BHP proposal and extends PUSU deadline to 29 May 2024 — Anglo American, 2024-05-22 ↩↩↩

-

BHP walks away from proposed $49bn takeover of Anglo American — Mining.com, 2024-05-29 ↩↩↩↩

-

Anglo American response to BHP announcement and rejection of request for PUSU extension — Anglo American, 2024-05-29 ↩↩

-

Gwede Mantashe vents his displeasure over BHP's unsolicited mega merger offer to Anglo — Daily Maverick, 2024-04-25 ↩

-

Anglo American accelerates delivery of strategy to unlock significant value — Anglo American, 2024-05-14 ↩↩↩

-

Anglo American completes demerger of Valterra Platinum (formerly Anglo American Platinum) — Anglo American, 2025-06-02 ↩

-

Teck and Anglo American to Combine Through Merger of Equals to Form a Global Critical Minerals Champion — Teck Resources, 2025-09-09 ↩↩↩↩↩↩↩↩↩

-

Anglo American and Teck to combine through a merger of equals — Anglo American, 2025-09-09 ↩↩↩↩

-

Sir Ernest Oppenheimer — The Brenthurst Library (from Optima, Sept 1967) ↩↩↩

-

Sir Ernest Oppenheimer — South African History Online, updated 2020-11-10 ↩↩↩

-

Harry Oppenheimer biography shows the South African mining magnate's hand in economic policies — The Conversation, 2023-06-01 ↩↩

-

Anglo American PLC — Encyclopedia.com (International Directory of Company Histories) ↩↩↩

-

Anglo American announces switching main listing to London — South African History Online ↩

-

Anglo American appoints Mark Cutifani as Chief Executive — Anglo American, 2013-01-08 ↩↩↩

-

Anglo American Platinum fires 12,000 workers — Mining.com, 2012-10-05 ↩

-

Mark Cutifani leaves Anglo American a better company — The Globe and Mail ↩↩↩↩

-

Anglo American appoints Duncan Wanblad as Chief Executive — Anglo American, 2021-11-03 ↩↩

-

Recommended cash offer for Sirius Minerals — Anglo American, 2020-01-20 ↩↩

-

Anglo American completes acquisition of Sirius Minerals — Anglo American, 2020-03-17 ↩

-

An overview of Anglo American's deal to take over Sirius Minerals — NS Energy ↩

-

Sirius's shareholders approve takeover by Anglo American — Mining.com ↩

-

Anglo American Takes $1.7 Billion Hit on Giant U.K. Mine — Industrial Info, 2023-03-13 ↩

-

Anglo American Interim Results 2024 — Anglo American, 2024-07-25 ↩↩

-

Increased investment for the Woodsmith Project — Anglo American, 2023-02-23 ↩

-

Anglo American announces first copper production from Quellaveco project in Peru — Anglo American, 2022-07-12 ↩↩

-

Los Bronces in transition phase while Anglo American focuses on value — Fastmarkets (Hotter Commodities), 2024-04-18 ↩

-

'Substantial Shortfall' in Copper Supply Widens as the Race for AI and Growing Defense Spending Add to Accelerating Demand — S&P Global, 2026-01-08 ↩↩↩

-

Quarterly Production Report – Q3 2024 — Antofagasta plc, 2024-10-16 ↩

-

A billion-dollar gift that keeps on giving: Collahuasi–Quebrada Blanca Integration — CRU Group, 2025 ↩↩↩

-

Anglo-Teck merger would create a 'global minerals family' HQ'd in Vancouver — Mining.com ↩

-

Anglo American expects final approval for Teck merger around Q3 — Mining.com ↩↩↩

-

Teck and Anglo American receive Government of Canada approval for merger of equals under Investment Canada Act — Teck Resources, 2025-12-15 ↩

-

Glencore–Teck Saga: Analysis — Bocconi Students Investment Club ↩↩

-

Teck Announces Full Sale of Steelmaking Coal Business — Teck Resources, 2023-11-13 ↩

-

Anglo American completes transaction to add multi-billion tonne Serpentina premium iron ore resource at Minas-Rio — Anglo American, 2024-12-03 ↩

-

Anglo American secures additional multi-billion tonne high quality iron ore resource at Minas-Rio — Anglo American, 2024-02-22 ↩

-

Partnering with Bahrain Steel to drive a more sustainable steelmaking industry — Anglo American ↩

-

Anglo American suspends Minas-Rio iron ore operation for pipeline checks — Anglo American, 2018-04-03 ↩

-

Kumba Iron Ore Q4/FY2024 Production and Sales Report — Kumba Iron Ore, 2025-02-06 ↩↩↩↩

-

Kumba guidance threatened by Transnet as mine stocks grow — Miningmx, 2024-07-18 ↩↩↩

-

Preliminary Financial Results for 2024 — De Beers Group, 2025-02 ↩

-

Anglo American Slashes De Beers' Value in Half — Rapaport, 2026-02-22 ↩

-

Anglo American hit by De Beers writedown, posts $3.7-billion loss — The Globe and Mail, 2026-02-20 ↩↩↩↩↩

-

Anglo American agreement to sell its nickel business in Brazil, valued at up to US$500 million — IBRAM, 2025-02-18 ↩

-

Peabody Energy terminates acquisition agreements with Anglo American — Mining Technology, 2025-08-20 ↩

-

Anglo American agrees sale of steelmaking coal business for up to US$3.875 billion in cash — Anglo American, 2026-05-18 ↩↩

-

Anglo American scraps controversial bonus plan on eve of shareholder vote — The Globe and Mail, 2025-12-08 ↩

-

Duncan Wanblad says Anglo Teck merger moving at pace — Business Day, 2026-04-30 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube