A2A: Italy's Multi-Utility Giant and the Energy Transition

I. Introduction: From Municipal Roots to National Champion

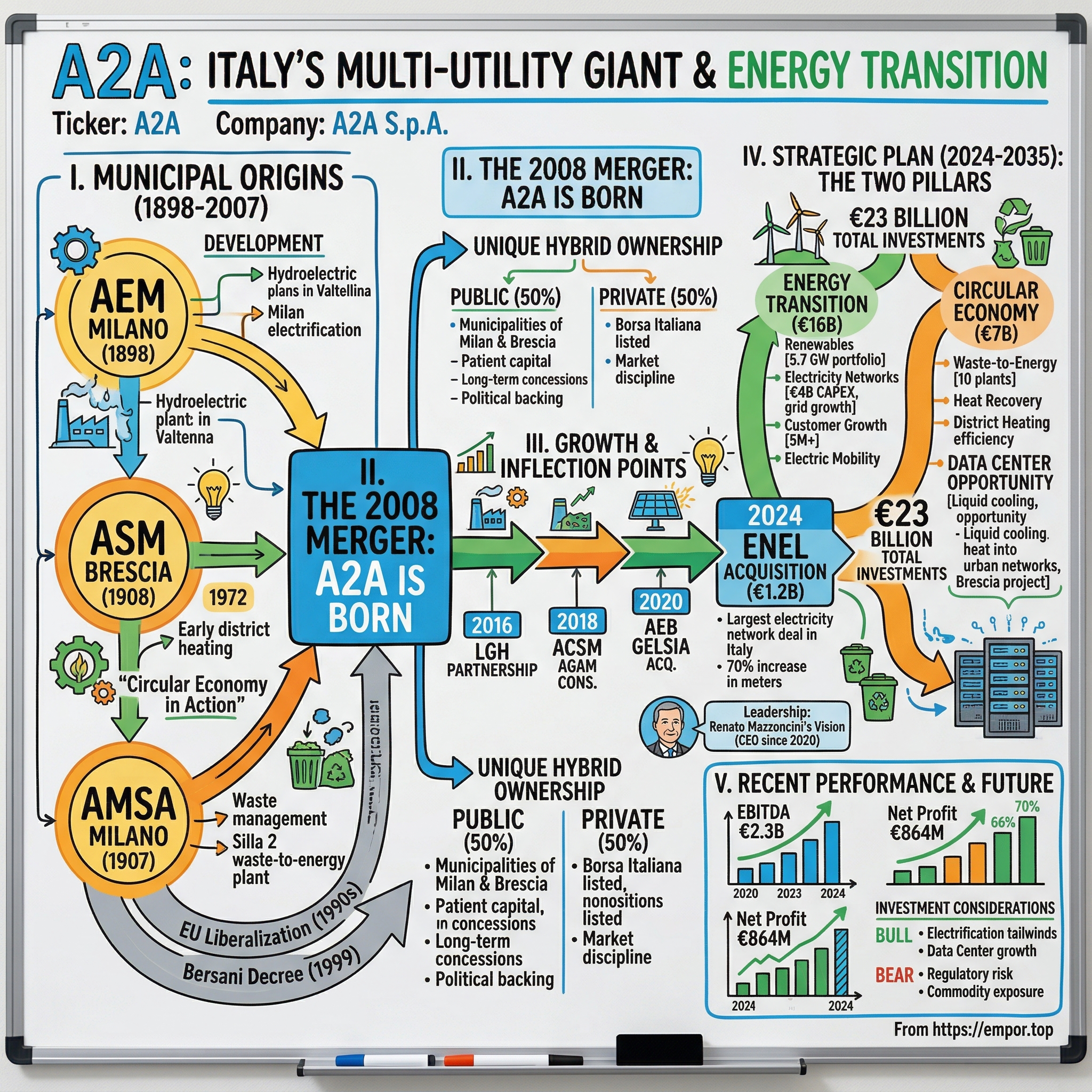

Picture Milan in 1898: Italy's industrial capital pulsing with ambition, its factories hungry for power, its streets awaiting illumination. When the Milan Municipal Council convened that year to address the "electricity issue," they faced a crossroads. The Edison Committee—named after the American inventor whose technology had transformed the world—was demanding terms that local officials considered exorbitant. Rather than capitulate, Milan chose a different path: it would generate power itself, for its own citizens.

The decision taken in 1898 by the Milan Municipal Council to deal with the "electricity issue" and to begin producing the new energy in its own right following the requests, considered exaggerated at the time, from what was then known as the "Edison Committee", laid the foundations for the birth of AEM (Azienda Elettrica Municipale di Milano - the Milan Municipal Electricity Company).

That fateful decision—to reject private monopoly in favor of public ownership—would ripple through more than a century of Italian infrastructure history, ultimately producing A2A: Italy's largest multi-utility. The Group is the second energy operator in the country in terms of installed capacity and distributed electricity, and the leading national player in the environmental sector.

A2A S.p.A. is an Italian company, organised as a società per azioni, that generates, distributes, and markets renewable energy, electricity, gas, integrated water supply, and waste management services. A2A is listed on the Borsa Italiana and is a member of the FTSE MIB index.

In 2024, it reported revenues of €12.64 billion and net profit of €864 million. But the numbers alone don't capture what makes A2A remarkable: this is a company where municipal ownership functions not as a handicap but as a competitive moat—where vertical integration across energy, waste, water, and digital services creates synergies that purely private competitors struggle to replicate.

The central question for investors analyzing A2A is deceptively simple: How did three municipal utilities from Milan and Brescia merge to become Italy's multi-utility champion? And more importantly: can the model that worked in Lombardy scale across Italy and into Europe?

The answer lies in understanding five interconnected themes:

-

Municipal ownership as strategic advantage: Far from bureaucratic deadweight, A2A's 50% municipal ownership (split between Milan and Brescia) provides long-term territorial concessions, political backing for major projects, and patient capital orientation.

-

Vertical integration across the value chain: A2A doesn't just generate power—it distributes it, sells it, and manages the waste that creates it. Each link in the chain reinforces the others.

-

Infrastructure as destiny: The company's €23 billion investment plan through 2035 positions it at the intersection of Europe's two great transformation waves: energy transition and digital infrastructure.

-

Decarbonization as growth driver: Unlike utilities that treat environmental mandates as costs to be minimized, A2A has built its strategy around the premise that circular economy and energy transition investments generate superior returns.

-

Lombardy as laboratory: Italy's wealthiest region serves as both proving ground and profit center, with the company's district heating networks, waste-to-energy plants, and electricity grids creating an integrated ecosystem difficult to replicate elsewhere.

II. The Municipal Origins: AEM, ASM & AMSA (1898–2007)

A. AEM Milano: Electrifying the Industrial Capital

The story of A2A begins in the Alpine valleys of Valtellina, where the glacial rivers tumbling from the peaks of northern Italy held the promise of industrial transformation. In 1910, the municipal electrical company (AEM) was founded to participate in and promote development in Milan. From 1920 to 1950, the company expanded and consolidated its existing plants in Valtellina and also built new hydro-electric power plants there.

AEM, founded in 1910 following a public referendum with strong citizen support, had been instrumental in Milan's electrification, acquiring hydraulic sites in Valtellina for its first hydroelectric plant in 1907 (13,500 kW capacity).

This wasn't merely an engineering exercise—it was civic nation-building. Browse through the archives of the Corriere della Sera from that era and you'll find articles celebrating electricity as a public good, "for the common benefit of everyone." In 1909, AEM introduced favorable rates for council house lighting and studied special tariffs for small businesses—social policy embedded in utility operations.

Amongst its most outstanding achievements in that period were the illumination of Milan's principal architectural monuments, such as the Castle, and construction of splendid illuminated fountains. The serious damage caused during the last war was overcome during the fifties, thanks to the injection of major investment, dedicated above all to the construction of hydro-electric plants in Alta Valtellina, which effectively doubled production capacity in 1963 compared with the pre-war period.

This meant that AEM was able to supply the energy required for the "economic boom" of the sixties, during which period the consumption of electricity increased by 7.5% annually.

The hydroelectric heritage matters today for two reasons. First, it provides A2A with approximately 1.9 GW of low-cost, zero-carbon baseload generation—a valuable asset in an era of volatile gas prices. Second, it established the template for A2A's approach: build infrastructure that serves the community, optimize it relentlessly, and expand from a position of strength.

In 1959, AEM, in collaboration with ASM in Brescia, began construction of the thermo-electric plant in Cassano d'Adda, which was subsequently extended in 1984. This collaboration between Milan and Brescia—two cities that would later merge their utilities—demonstrated the strategic logic of regional consolidation decades before it actually occurred.

B. ASM Brescia: Pioneer in District Heating

Brescia, forty kilometers east of Milan, took a different but complementary path. Shortly afterwards, ASM (Azienda dei Servizi Municipalizzati - the Municipal Services Company) also came into being (1908) from a resolution by the Municipality of Brescia, and was entrusted with managing the tram service and the ice factory.

But Brescia's true innovation came in the 1970s. While the oil crises sent shockwaves through global energy markets, Brescia, with ASM, was the first in Italy to make this infrastructure available to its citizens—referring to district heating, a technology that would prove transformative.

Ahead of its time in 1972, district heating in Brescia today serves 70% of city buildings, both residential and tertiary, thanks mainly to the heat production facility that uses as fuel the waste of the WtE site in Via Lamarmora, just south of the city centre.

During 1972, Brescia Due, being a neighborhood under construction, was involved in the experimentation of ASM district heating. The service was launched in September of the same year and was then extended to the rest of the city in the following decade.

The genius of Brescia's model was integration. The city didn't just burn waste—it captured the heat and piped it into homes. The heat produced by waste to energy covers over 40% of the heating requirements of district-heated constructions. The integrated system Waste to energy - District heating has permitted the city of Brescia to reach, greatly in advance of the fixed date (2010), the objectives of reducing emissions of carbon dioxide, as proposed by the international Community.

Today, Brescia's district heating network represents what A2A calls "circular economy in action"—a system where nothing is wasted, where one process's output becomes another's input. Thanks to these solutions, which have helped reduce the use of gas, 83% of the heat distributed in Brescia in 2024 will come from non-fossil sources.

C. AMSA: Milan's Waste Management Champion

The third pillar of A2A's foundation came from Milan's waste management system. With the municipalisation of the Milan street cleaning service and the hiring of six hundred or so street sweepers who were then active, the same period saw the constitution of AMSA (1907), a company that over the ensuing decades absorbed SPAI (Servizi Pubblici Anonima Italia), which was established in 1929 providing the waste collection services for Milan.

Amsa (then SPAI - Servizi Pubblici Anonima Italiana) built the first waste incinerator in Milan in via Zama, in 1968, distinguishing itself as the first company in Italy to adopt waste-to-energy to produce energy from waste.

The Silla 2 waste-to-energy plant, which came into operation in 2001, represents AMSA's modern legacy. Silla 2 is the waste-to-energy plant in Milan and is located in the north-west area, near the Figino district. Waste-to-energy is a process which, through the combustion of residual waste from separate collection not subject to recycling, is capable of producing electricity and hot water for heating buildings. The Silla 2 waste thermoelectric power plant supplies heat for district heating to the western area of Milan (Gallaratese district), to the Rho-Pero exhibition center and to those users connected to the district heating network in the Municipalities of Pero and Rho.

At full capacity, Silla 2 is able to provide heating to approximately 30,000 families and to generate electricity for the benefit of approximately 147,000 families. In 2016, the plant's full operation made it possible to save around 87,000 TOE (tonnes of oil equivalent) and avoided the emission of around 305,000 tonnes of carbon dioxide.

D. The Pre-Merger Context: EU Liberalization

By the 1990s, the comfortable world of Italian municipal utilities was transforming. This picture has been partly altered by the process of privatisation and liberalisation of the markets in the 1990s as Italy's energy sector underwent structural adjustments. The reform radically transformed both segments of the market—gas and electricity—which are very different from an economic, institutional and ownership point of view.

The so-called Bersani Decree for the reorganisation of the electricity system was passed in 1999 with the aim of liberalising the electricity sector and enhancing competition.

The merger was driven by the deregulation of Italy's energy sector in the 1990s, which introduced reforms to local public services and progressive liberalization of electricity and natural gas markets, encouraging municipal operators to merge for scale and competitiveness.

The 1990s were the years of the liberalization of the electricity market in Europe. The monopoly on electricity production ended, and Enel was asked to drop below 50% of production capacity to leave room for competition with other operators.

AEM responded by seeking scale and strategic partnerships. In 1998, it floated on the Milan Stock Exchange and 49% of the company share capital was floated on the market. In 1999, following the adoption of the energy markets ordinance, the company was restructured as an industrial group with operative companies in each sector of activity to become a multi-service company.

The stage was set for the merger that would create A2A.

III. The 2008 Merger: Creating A2A

A. The Strategic Logic

By 2007, the three municipal utilities—AEM, ASM, and AMSA—had operated in adjacent territories for nearly a century, occasionally collaborating (as with the Cassano d'Adda power plant) but never truly integrating. The logic of combination had become irresistible: scale to compete against Enel, synergies across adjacent businesses, and financial strength to fund the infrastructure investments that Italy's energy transition would require.

The merger process moved with characteristic Italian complexity. On September 21, 2007, court-appointed experts determined the share exchange ratio: one ASM share would convert to 1.6 AEM shares. On October 22, 2007, extraordinary shareholder meetings of both ASM and AEM gave final approval to the merger project.

On December 19, 2007, the Antitrust Authority approved the transaction. On December 24, 2007—Christmas Eve—the split agreement and merger documents were signed.

B. Birth of A2A

A2A was formed on 1 January 2008 by the merging of three Northern Italian municipality-owned utilities. They include Azienda Elettrica Municipale (AEM, est. 1880) and Azienda Milanese Servizi Ambientali (AMSA, est. 1907), both of Milan, and Azienda dei Servizi Municipalizzati (ASM, est. 1908) of Brescia.

The choice of name—A2A—carried symbolic weight: the alphanumeric formula evoked both a mathematical equation and the tagline "energia in comune" (energy in common). Technically, AEM incorporated both ASM and AMSA, but the merger was structured as a combination of equals, with governance balanced between the two founding municipalities.

A2A S.p.A. was born out of the merger between of the three Italian companies AEM, ASM and Amsa at the end of 2007. It is the third largest company in Italy in the production and distribution of electricity.

C. The Unique Ownership Structure

What makes A2A structurally distinctive is its hybrid public-private model. As of December 2024, it remains partially owned by the Municipalities of Milan and Brescia (25% ownership each). The municipalities are responsible for appointing 12 out of its 15 directors.

This ownership structure is often dismissed by investors as a governance liability—the dead hand of municipal bureaucracy constraining commercial dynamism. But that analysis misses the strategic value that municipal ownership creates:

Territorial concessions: District heating networks, waste collection contracts, and electricity distribution require long-term agreements with local governments. When your shareholders are the local government, contract renewal becomes considerably simpler.

Patient capital: Municipal owners aren't activists demanding quarterly buybacks. They want stable dividends, reliable employment, and infrastructure that serves their citizens. This orientation enables long-term investment horizons that pure private capital often cannot support.

Political backing: Major infrastructure projects—waste-to-energy plants, grid expansions, renewable installations—require regulatory approvals and community acceptance. Municipal ownership provides legitimacy and advocacy that purely private developers often lack.

Long-term orientation: The municipalities have owned these utilities for over a century. They think in generational timescales, not quarterly reporting cycles.

The remaining 50% of shares trade freely on the Borsa Italiana, providing liquidity, market discipline, and access to capital markets. This balance—half anchored, half floating—gives A2A the stability of public ownership with the efficiency incentives of market capitalism.

IV. First Decade: Building Scale (2008–2018)

A. Early Acquisitions & Consolidation

From its first day of operation, A2A pursued an aggressive consolidation strategy. Following its formation in 2008, A2A pursued a growth strategy centered on mergers and acquisitions to achieve vertical integration across the utilities sector, particularly in energy distribution, while consolidating its presence in northern Italy. This approach involved over 10 transactions documented in the company's press releases since 2008.

A pivotal early acquisition occurred on June 16, 2008, when A2A signed an agreement to acquire certain generation assets from Endesa Italia in northern Italy, in exchange for its 20% equity stake in Endesa Italia. This deal strengthened A2A's generation capabilities in the region.

The acquisition strategy was disciplined: target assets in or adjacent to existing territories, focus on infrastructure that creates natural monopolies or long-term contracts, and integrate rapidly to capture synergies.

B. Market Position

By the end of its first decade, A2A had established dominant positions across multiple business lines. The company ranked as Italy's number one in district heating, demonstrating the enduring value of Brescia's 1970s innovation. In electricity, it held the number two position in terms of installed capacity and sales volumes.

At present, A2A is: one of the main players in the environmental sector in Italy with approximately 3 million tons of waste treated; in 1st place between the former Italian public utilities companies in terms of clients and turnover; in 1st place in Italy in the district heating sector; in 2nd place in Italy in terms of installed electric capacity and volumes of sales.

The hydroelectric heritage proved especially valuable. Renewable energies—principally hydroelectric generation—accounted for a high percentage of output, approximately 28%, significantly above Italian utility averages. This renewable base would prove prescient as carbon pricing and environmental mandates reshaped European energy economics.

C. Surviving the European Energy Crisis of 2014

The middle years of A2A's first decade brought severe challenges. Lower prices of electricity in the market were caused by the expiration of the favorable convention named "Comitato Interministeriali Prezzi" in which those producing energy through renewable sources may sell them at a higher price in the market.

Moreover, from a macro point of view, the tensions between Ukraine and Russia affected negatively the energy sector as a whole, but in particular, given the fact that A2A has no take-or-pay contracts with its suppliers, mainly gas ones, rendered the situation unstable which forced the company to search for other sources of raw materials such as Algeria.

The revenue picture told the story: total revenues sharply decreased from about 5.6 billion euros in 2013 to about 4.9 billion euros in 2016. In 2017, the value increased to roughly 5.8 billion euros and reached 6.5 billion euros as of December 2018.

A2A navigated this period through cost discipline, portfolio optimization, and strategic patience. The multi-utility model proved its value: when commodity prices crushed generation margins, waste management and distribution businesses provided stable cash flows. This diversification—deliberately constructed since the 2008 merger—demonstrated its worth during the industry's darkest hours.

D. Strategic Regional Consolidation

The first decade culminated with major consolidations that expanded A2A's Lombardy footprint. A2A fully consolidated Linea Group Holding in August 2016 and ACSM AGAM in July 2018. The AEB Gelsia acquisition followed in November 2020.

Each transaction followed the same template: acquire adjacent municipal utilities, integrate operations to capture synergies, expand geographic coverage while deepening territorial density. The result was a regional champion with sufficient scale to compete nationally while maintaining the local relationships that municipal heritage provides.

V. Key Inflection Point #1: The LGH Merger (2021)

The completion of A2A's consolidation of Linea Group Holding (LGH) in 2021 marked the culmination of a five-year integration process that exemplified the company's disciplined M&A approach.

With reference to the merger between A2A S.p.A. and Linea Group Holding S.p.A., a company 51% controlled by A2A, it is hereby announced that the respective Boards of Directors approved the merger project by incorporation of LGH into A2A.

In 2021, A2A advanced its consolidation in the energy sector through a merger to acquire the remaining 49% stake in Linea Group Holding (LGH). The proposal was formalized in April 2021, with board approvals in June and October, culminating in the merger deed signing on December 15, 2021, and statutory effects effective from December 31, 2021. This transaction incorporated LGH's energy production and distribution assets, primarily in Lombardy and Emilia-Romagna, enabling A2A to streamline operations and expand its multi-utility portfolio.

The merger by incorporation of LGH into A2A is in line with the process of rationalising the companies of the A2A Group and completes the path of evolution of the partnership between A2A and the minority shareholders of LGH (Azienda Energetica Municipale S.p.A. at 15.15%, Cogeme S.p.A at 15.15%, A.S.M. Pavia S.p.A at 7.79%, Astem S.p.A. at 6.48% and Società Cremasca Servizi S.r.l. at 4.43%), as outlined and described in the partnership agreements signed on 4 March 2016 and subsequently integrated.

The merger is the culmination of a process of integration between the two companies which has evolved over the years and, as already announced, at the end of the transaction LGH's minority shareholders (who currently hold a total of 49% of LGH's share capital) will hold 2.75% of A2A's share capital. The merger, in addition to rationalising the group companies, will enable economic synergies to be generated over time thanks to the integrated management of processes and systems.

The LGH merger demonstrates a key element of A2A's playbook: patient partnership preceding full integration. The 2016 partnership agreements established the framework; five years of operational collaboration proved the synergies; full merger followed only when both parties had validated the value creation thesis.

For investors, the LGH transaction illustrated A2A's ability to execute complex multi-stakeholder transactions—essential for a company whose growth depends on consolidating Italy's fragmented utility landscape.

VI. Key Inflection Point #2: The €1.2B Enel Acquisition (2024)

A. The Deal

On March 9, 2024, A2A announced the largest acquisition in its history—and the largest in Italy's electricity distribution sector. A2A and e-distribuzione, an Enel Group company active in the electricity distribution sector, have signed an agreement for the sale and purchase of e-distribuzione's business relating to the electricity network in a number of areas of Lombardy, in the provinces of Milan and Brescia. The agreement will allow the A2A Group to exploit territorial synergies and accelerate the investments required for the energy transition. Specifically, the transaction provides for the acquisition by A2A of 90% of a newly incorporated company to which e-distribuzione will contribute its electricity distribution assets in the province of Milan (excluding certain municipalities in the northern belt) and in Valtrompia (in the Brescia area), totalling approximately 800,000 PODs, approximately 5,000 km of medium voltage cables, over 12,000 km of low voltage cables, approximately 9,500 secondary substations and 60 primary substations.

The agreement provides for A2A to pay a consideration of approximately 1.2 billion euros, based on an enterprise value (for 100% of the company) of around 1.35 billion euros.

B. Closing & Impact

A2A S.p.A. entered into an agreement to acquire Enel's electricity distribution in the provinces of Milan and Brescia from Enel SpA on December 30, 2024. A2A S.p.A. completed the acquisition of Enel's electricity distribution in the provinces of Milan and Brescia from Enel SpA on December 31, 2024.

With the completion of this acquisition, the largest in the sector in Italy, the Group increases the managed electricity meters by 70% - with a network that grows by 17,000 km in the provinces of Milan and Brescia.

CEO Renato Mazzoncini highlighted plans for over €4 billion in additional investments in distribution by 2035, with the Group's regulatory asset base projected to reach €3.4 billion by then.

C. Strategic Rationale

We have taken a very important step for the Group's growth in the management of strategic infrastructure to support the electrification process of consumption. – commented Renato Mazzoncini, CEO of A2A – With this transaction, we are acquiring significant assets, confirming our objective of accelerating investments in electricity networks, promoting the decarbonisation of the country and creating value for communities, in line with our business plan.

The Enel transaction represented more than a simple asset purchase—it was a strategic statement about A2A's future direction. The company was betting heavily on electrification: as heat pumps replace gas boilers, as electric vehicles displace internal combustion, as data centers proliferate, electricity demand will surge. Distribution infrastructure becomes the critical bottleneck—and the investment opportunity.

The transaction will also make it possible for A2A to carry out and remunerate greater investments in the electricity distribution network of approximately EUR 1.4 billion by 2035, in support of the energy transition and in line with A2A's strategic plan and decarbonisation objectives.

He also noted the importance of scaling infrastructure to support electrification and AI development, citing expected European investments in electricity networks of €580 billion ($600.9 billion) by 2030, with €60 billion ($62.2 billion) dedicated to Italy.

VII. The Two Pillars Strategy: Energy Transition & Circular Economy

A. The 2024-2035 Strategic Plan

A2A's strategic plan through 2035 represents one of the most ambitious investment programs in European utilities. A2A raises total investments for 2024–2035 to €23 billion (US $27 billion), with €16 billion for the energy transition and €7 billion for the circular economy. The plan forecasts EBITDA of €3.6 billion and net income above €1.1 billion by 2035, maintaining debt below 2.8 times EBITDA.

22 billion euros investments planned over 2024-35 period, of which: 6 for Circular economy, 16 for Energy transition. CAPEX eligible for European Taxonomy: ~75% average over the Plan period. The Board of Directors of A2A, chaired by Roberto Tasca, has examined and approved the 2024-2035 Strategic Plan Update which confirms the Group's long-term industrial growth objectives announced in March 2024 Plan. The strategy rests on the two pillars of Circular economy and Energy transition, while combining decarbonisation and competitiveness.

The 22 billion in investments to be made by 2035 and which "we have targeted in the Strategic Plan, are very important. It is important to say that these 22 billion euros come from our cash flows. That is, it is the money that A2A is able to generate with its own cash flows, there is not a single euro of public financing" highlighted CEO Mazzoncini.

B. Energy Transition Pillar

The €16 billion allocated to energy transition encompasses four major investment themes:

Electricity Networks: This acquisition is part of A2A's overall electricity network development strategy with 4 billion euros in planned CAPEX during the Plan period, which will enable A2A to generate 500 million euros in EBITDA by 2035 and consolidate its position as Italy's second-largest operator and among the top 20 in Europe for distributed electricity. The new perimeter outlined and the significant associated investments will allow RAB to increase from 1 billion euros in 2023 to 3.4 billion in 2035.

Renewable Generation: The Group's contribution to the country's Energy transition and decarbonisation will also be achieved with 4.6 billion euros in CAPEX dedicated to the development of a 5.7 GW RES portfolio by 2035, up by 3.1 GW compared to 2023, thanks to which more than 10 TWh of green energy will be produced by 2035. To achieve the planned growth, A2A can count on a wind and solar plant pipeline of over 1.8 GW, 83% of which are internally developed projects.

Its renewable-generation strategy targets 3.7 gigawatts of installed wind and solar capacity by 2035, complemented by modernised, high-efficiency thermal assets to balance intermittency and demand.

Customer Growth: With the perspective of supporting people and businesses along the path of Energy transition, the Group intends to increase its customer base from 3.5 million in 2023 to over 5 million in 2035, with an offer increasingly focused on the electrification of consumption. To support the growth of its customer base, A2A can count on the success of past acquisition campaigns, a multi-channel strategy, a consolidated reputation and customer satisfaction, elements that will enable it to achieve a market share increasing from 6% in 2023 to over 9% in 2035.

Electric Mobility: The Group is also committed to the decarbonisation of transport, with around 0.5 billion euros invested in the development of electric mobility: the recharging network will grow from 2,000 points in 2023 to 34,000 in 2035. The group also plans to install 16,000 public charging points for electric vehicles by 2035, advancing Italy's mobility electrification.

C. Circular Economy Pillar

The circular economy pillar—€7 billion through 2035—represents the modern evolution of Brescia's 1970s district heating innovation.

We have 10 waste-to-energy plants, 5 of which include high-efficiency cogeneration plants serving the urban district heating grids of Bergamo, Brescia, and Milan. Our investment plan involves increasing our waste treatment and recovery capacity by consolidating our leading position in the Waste-to-Energy sector.

Central to waste treatment is A2A's network of waste-to-energy (WtE) facilities, where five high-efficiency cogeneration plants—serving district heating in Bergamo, Brescia, and Milan—process non-recyclable waste to generate electricity and heat, linking to broader energy production efforts. Collectively, A2A's WtE operations handle around 1 million tons of waste annually, producing approximately 821 GWh of electricity exported to the grid.

Recent investments demonstrate the strategic commitment. A2A has invested 110 million euros to make the Brescia waste-to-energy plant, Italy's largest, even more efficient and sustainable, including 45 million euros earmarked for equipment that allows for an additional 40 percent cut in emissions.

The new technology puts energy into circulation so that nothing is wasted, recovering any waste heat that can contribute to the decarbonization of the city's district heating. And, thanks to this technology, it will be possible to generate extra thermal energy for 12,500 households in Brescia for the same amount of waste treated, thus reducing the use of gas to feed the district heating network and bringing the plant's efficiency close to 100 percent (from 84 percent to 98 percent).

D. The Data Center Opportunity

Perhaps the most intriguing element of A2A's strategy is its positioning at the intersection of energy infrastructure and digital economy. Within this pillar, A2A is introducing a data-center business to capture opportunities from rising digital-infrastructure demand. About €1.6 billion will fund new data-center development and management, leveraging its energy networks and heat-recovery systems. Lombardy, home to both Milan and Brescia, is emerging as Italy's primary hub for digital infrastructure, giving A2A a strategic foothold in thermal and electrical integration for hyperscale clients.

In Lombardy (northern Italy), data-centre capacity is expected to rise tenfold over the next five years. Data centres consume very large amounts of power. A2A sees a business opportunity in supplying and managing that power.

The innovation lies in connecting data center heat output to district heating networks. At the same time, they also offer an extraordinary opportunity for cities equipped with district heating networks: to recover waste heat from servers and convert it into usable thermal energy," explained Renato Mazzoncini. "In Milan alone, based on the projects in the pipeline, an estimated 150,000 apartments could be heated simply by capturing that residual heat.

In June 2025, A2A inaugurated a breakthrough project: A2A has inaugurated a new data center in Brescia, designed by French company Qarnot, which utilizes a liquid cooling system to recover heat from servers and feed it directly into the city's district heating network. The project—presented at the Lamarmora thermoelectric power plant in Brescia, fifty years after the Lombard city became the first in Italy to adopt a district heating network—marks one of the country's first applications of heat recovery from data centers and is the first to employ liquid cooling technology in an urban network. Once fully operational, the facility will be able to meet the thermal needs of over 1,350 apartments, preventing the emission of around 3,500 tons of CO2 per year.

VIII. Recent Performance & 2024 Results

A2A's 2024 results validated the strategic direction established over the preceding decade. "The excellent economic and financial performance achieved in the first nine months of 2024 has allowed us to proceed more quickly with the investments envisaged in our Plan. The results of this third quarter further confirm the consistency of our strategy: we have achieved an unprecedented net profit of over 700 million euro, exceeding what was recorded in the whole of 2023," comments Renato Mazzoncini, CEO of A2A. "With these results, we have been able to revise upwards the guidance for 2024, with an expected EBITDA between 2.28 and 2.32 billion euro and a Group net ordinary profit between 0.80 and 0.82 billion euro."

EBITDA at 1,804 million euro: +33% compared to the first nine months of 2023 (1,357 million euro). Net profit at 713 million euro: +68% compared to the same period of 2023 (425 million euro). Revenues of 9,097 million euro: -17% compared to the first nine months of 2023 mainly due to the contraction in energy commodity prices. Capex of 898 million euro, +13% compared to the first nine months of the previous year, devoted to the development of photovoltaic plants, the upgrading and efficiency of networks to support decarbonisation.

The full-year results confirmed the trajectory. In 2024, we invested almost 3 billion euro, an all-time record for our Group. In the last year, generation from renewable sources accounted for about 50% of our total production, up compared to 2023: we have therefore been able to offer more green energy to the market. The activities we have carried out have allowed us to achieve an EBITDA of more than 2.3 billion and a net profit of more than 800 million. This allows us to propose a dividend of 0.10 euro per share to the next Shareholders' meeting, up 4.4%.

The A2A Group's 2024 results confirm a growth in operating margins, driven by the increase in energy production from renewable sources as a result of high hydraulicity and the positive contribution of the energy retail sector. It should also be noted that the financial ratios remained solid, with a NFP/EBITDA ratio of 2.5x, a slight increase compared to the previous year (equal to 2.4x), despite the significant acquisition of the electricity distribution network from e-distribuzione, without the contribution of the related share of EBITDA for 2024.

The capacity market provided additional validation. In the capacity market auction called by Terna for the 2026 delivery year, the A2A Group's existing capacity portfolio was awarded for a total of approximately 4.4 GW, with a technological mix that includes gas and renewable source plants, to support the energy transition. The Group was also awarded annual contracts for 520 MW of foreign capacity. The outcome of this auction is in line with what was assumed in the update of the 2024-2035 Strategic Plan.

IX. Leadership: Renato Mazzoncini's Vision

Understanding A2A requires understanding the man who has led its transformation since 2020. Born in Brescia on 13 January 1968, Mazzoncini has held executive positions in private, public and semi-public companies in the public services and utilities sector since 1997. CEO and Managing Director of the Ferrovie dello Stato Group until 2018.

In 1992, he graduated with a Master of Science in Electrical Engineering from the Polytechnic University of Milan. He is married and has three children.

Renato Mazzoncini has been Managing Director and Chief Executive of A2A since May 2020. Electronic engineer and professor at the Politecnico di Milano scientific-technical university, where he teaches the Mobility - Infrastructures and Services course and is also a member of the Advisory Board.

Mazzoncini's path to A2A was anything but linear. In 2012, Ferrovie dello Stato Italiane S.p.A introduced a new company called Busitalia, which aimed to expand the group's role in the public road transport sector. Mauro Moretti, at the time CEO of the group, asked Mazzoncini to head this new holding. He accepted, at the condition that he would be CEO and Director-general of every new company held by Busitalia. The first acquisition he made while at Busitalia was Azienda Trasporti Area Fiorentina, the public transport network operator in Florence.

While restructuring ATAF, he met Matteo Renzi, who at the time was mayor of Florence and would go on to become Prime Minister. Their partnership reportedly started with a quarrel: a raise in the prices of bus tickets prompted a very heated reaction from an infuriated Renzi, who phoned Mazzoncini while he was skiing in Northern Italy. After meeting in person, the two reportedly got along much better.

This anecdote captures something essential about Mazzoncini: he is an infrastructure executive who doesn't shy from conflict, who builds relationships through direct engagement rather than bureaucratic caution.

He started working at Ansaldo, then led private, public, and mixed companies in local public services until he joined the Ferrovie dello Stato Group in 2012 as CEO of the subsidiary Busitalia. He reached the top of the FS Group as CEO and General Manager, from 2015 until 2018. During that time, among other things, Anas was integrated into the FS Group.

On 25 July 2018, Renato Mazzoncini stepped down from his roles in Ferrovie dello Stato Italiane S.p.A, accusing the government of operating a "spoils system" after the new Transport Minister, Danilo Toninelli, dismissed the entire board of the company.

An expert on climate change, the environment, the green economy, energy transitions and mobility, Mazzoncini has co-authored books and articles on energy transformation, smart and green cities, and environmental strategies for a zero-emission future.

Passionate and knowledgeable about environmental issues, green economy, and climate change, he participated in the drafting, along with other global experts, of the "Roadmap to 2050 A Manual for Nations to Decarbonize by Mid-Century" presented at COP 25.

Under Mazzoncini's leadership, A2A has accelerated its transformation from a traditional utility into an infrastructure platform for the energy transition. The strategic plan through 2035, the Enel distribution acquisition, and the data center initiative all bear his fingerprints—ambitious scale, long investment horizons, and integration across traditional business boundaries.

X. Competitive Landscape and Investment Considerations

The Italian Utility Hierarchy

A2A operates in a competitive landscape dominated by one giant and several regional champions. A2A's main competitors include Edison, Iren, Eni and Enel Group. A2A's competitors and similar companies include Edison, Iren, Eni and Enel Group.

Italy represents the third largest market for energy service in Europe. Italy's main energy supplier is ENEL S.p.A, holding a 45% market share; that is to say, the remaining side of the supply is left for all the other competitors.

Enel SpA has 60,950 employees and $80.0B revenue. Hera SpA has 10,441 employees and $13.9B revenue. IREN SpA has 11,862 employees and $6.4B revenue. Acea SpA has 8,928 employees and $4.5B revenue.

The competitive dynamics are shifting in A2A's favor. Analysts at Equita argue that "the abolition of the protected market is a slightly positive element for utilities A2A, Iren, Hera, Acea". Similarly, Intermonte believes that liberalization "should represent an opportunity to increase the customer base for local utilities like A2A, Hera and Iren".

Competitive Analysis: Porter's Five Forces

Threat of New Entrants (Low): The utility sector requires massive capital investment, long-term territorial concessions, and regulatory relationships built over decades. A2A's municipal ownership provides insurmountable advantages in securing and renewing these concessions. New entrants cannot replicate a century of territorial relationships.

Bargaining Power of Suppliers (Moderate): A2A's integrated model—generating its own power through hydroelectric and renewable sources—reduces dependence on external fuel suppliers. However, gas procurement remains a vulnerability, as the 2014 Ukraine crisis demonstrated. The shift toward renewables progressively reduces this exposure.

Bargaining Power of Customers (Low to Moderate): For regulated services (distribution, waste collection), customers have no choice. For competitive services (retail energy), switching costs are low, but A2A's territorial density and service bundling create retention advantages.

Threat of Substitutes (Low for Distribution, Moderate for Generation): Distribution networks have no substitutes—every electron and gas molecule must flow through the pipes and wires. Generation faces substitution from distributed solar and batteries, but A2A's own renewable investments position it on both sides of this transition.

Competitive Rivalry (High in Retail, Low in Infrastructure): Retail energy markets feature intense price competition, particularly as Italy completes liberalization. Infrastructure businesses—distribution, waste management, district heating—face limited competition due to natural monopoly characteristics and long-term concessions.

Hamilton Helmer's Seven Powers Analysis

Scale Economies: A2A benefits from scale in procurement, IT systems, and corporate overhead. The LGH and Enel acquisitions specifically target scale advantages in distribution operations.

Network Effects: Limited direct network effects, but A2A's territorial density creates ecosystem effects—customers using multiple services (electricity, gas, waste, water) have higher switching costs.

Counter-Positioning: A2A's circular economy model—integrating waste, heat, and power—represents counter-positioning against pure-play utilities that cannot easily replicate the integrated approach.

Switching Costs: High for business relationships (long-term contracts), moderate for residential customers, very high for municipal concessions.

Branding: Limited power in commodity energy markets, but A2A's territorial presence and municipal heritage create trust advantages in local markets.

Cornered Resource: A2A's hydroelectric concessions in Valtellina and long-term waste management contracts represent cornered resources that competitors cannot easily acquire.

Process Power: The integration of district heating with waste-to-energy, and now data center heat recovery, represents process innovations that create sustainable competitive advantage.

Bull Case

-

Electrification Tailwinds: As Italy electrifies transport, heating, and industry, A2A's distribution network becomes increasingly valuable. The Enel acquisition positions the company perfectly for this structural shift.

-

Data Center Opportunity: Lombardy's emergence as Italy's data center hub creates a multi-billion-euro opportunity for A2A to supply power, manage heat recovery, and potentially develop its own data center capacity.

-

Municipal Ownership as Moat: Far from a liability, the 50% municipal ownership ensures preferential access to territorial concessions, patient capital for long-term investments, and political support for major projects.

-

Circular Economy Leadership: A2A's integrated waste-to-energy-to-heat model becomes increasingly valuable as European regulation tightens on landfills and carbon emissions.

-

Consolidation Runway: Italy's fragmented utility landscape offers continued acquisition opportunities, with A2A's proven integration capabilities and balance sheet capacity enabling further value-creating deals.

Bear Case

-

Regulatory Risk: Italy's regulatory environment for utilities has historically been volatile. Tariff changes, new environmental mandates, or shifts in concession frameworks could compress returns.

-

Municipal Governance: The same ownership structure that provides advantages also creates governance complexities. Municipal shareholders may prioritize employment or political considerations over shareholder returns.

-

Commodity Exposure: Despite diversification, A2A remains exposed to energy commodity volatility. Prolonged periods of low prices compress generation margins, while high prices create political pressure for intervention.

-

Execution Risk: The €23 billion investment plan through 2035 requires flawless execution across multiple business lines. Any major project failures or cost overruns could damage returns and credibility.

-

Competition from Enel: Italy's dominant utility has superior scale, brand recognition, and financial resources. A2A's regional advantages could erode if Enel prioritizes Lombardy market share.

Key Metrics to Watch

EBITDA Margin: A2A's ability to expand margins through operational efficiency and business mix optimization. The 2024 result of €2.3 billion provides a strong baseline.

Regulated Asset Base (RAB) Growth: For distribution networks, RAB determines the allowed return. Track the trajectory toward the 2035 target of €3.4 billion.

Renewable Capacity Additions: Progress toward the 5.7 GW renewable portfolio by 2035. Execution on the 1.8 GW pipeline indicates strategic momentum.

Customer Growth: Net customer additions in the competitive retail market, particularly following Italy's full liberalization.

Debt/EBITDA Ratio: Financial discipline despite the aggressive investment program. Management commitment to remaining below 2.8x through the plan period.

XI. Conclusion: Infrastructure as Strategy

A2A's journey from three municipal utilities to Italy's largest multi-utility offers lessons that extend beyond the energy sector. The company demonstrates that public ownership, properly structured, can create rather than destroy value—that long-term territorial relationships, patiently cultivated, generate sustainable competitive advantages—and that integration across adjacent businesses creates synergies that pure-play competitors cannot replicate.

The €23 billion investment program through 2035 represents a wager on three interconnected convictions:

First, that electrification will transform energy markets more profoundly than any shift since the original electrification of the late 19th century—and that owning distribution infrastructure positions A2A to capture value from this transformation.

Second, that circular economy principles—turning waste into resources, capturing heat that would otherwise be lost, closing loops that linear business models leave open—will increasingly define competitive advantage in infrastructure businesses.

Third, that digital infrastructure—the data centers powering AI, cloud computing, and the digital economy—will become as essential as the energy infrastructure that A2A's predecessor companies built a century ago, and that utilities with the right capabilities can capture a share of this emerging market.

A2A's strategy reflects a broader European pattern: utilities are evolving from energy suppliers into integrated infrastructure developers. The plan's dual focus on decarbonisation and digital infrastructure places A2A among the few continental utilities aligning circular-economy goals with the data-driven economy's energy needs. For investors and policy leaders, the company's roadmap offers a model for coupling long-term emissions reduction with new-market expansion.

The Brescia district heating network that began in 1972 was, in its way, an early experiment in circular economy thinking—capturing waste heat that would otherwise be lost, integrating systems that had previously operated in isolation. Fifty years later, A2A is applying the same integrative logic to data centers: the servers that power artificial intelligence become, through heat recovery, the furnaces that warm Italian homes.

Whether this vision will fully materialize depends on execution across thousands of individual decisions over the next decade. But the strategic logic is coherent, the financial resources are substantial, and the organizational capabilities—proven through more than a century of municipal utility operations—appear well-suited to the challenge.

In an era when infrastructure investment has become a strategic imperative for nations and a compelling opportunity for investors, A2A offers a distinctive model: patient capital, territorial depth, integrated operations, and a willingness to think in generational timescales. The municipal utilities of Milan and Brescia that came together in 2008 have built something that neither could have achieved alone—and that neither Enel's scale nor private equity's financial engineering can easily replicate.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube