Samsonite International: The Story of the World's Largest Luggage Company

I. Introduction & Episode Roadmap

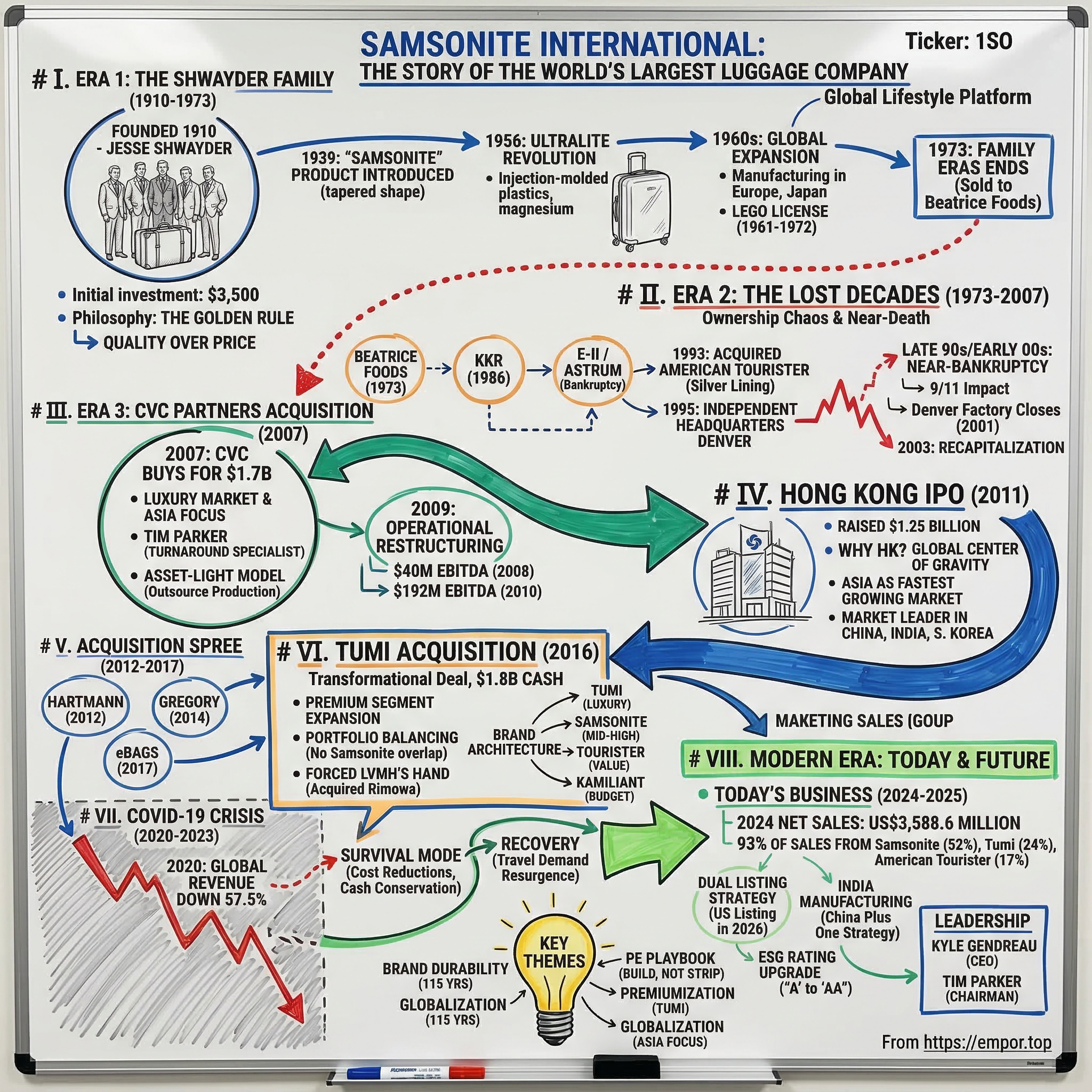

Picture an airport baggage carousel, anywhere in the world. Watch the suitcases emerge, tumbling down the conveyor. Perhaps one in five bears a name you've heard since childhood: Samsonite. Or its sleeker sibling Tumi. Or the colorful American Tourister your parents packed for family vacations. All three belong to the same company—a company that has outlasted world wars, the Great Depression, a half-dozen private equity owners, near-bankruptcy, and a global pandemic that brought air travel to a standstill.

Samsonite Group S.A., the world's best-known and largest travel luggage company, represents something rare in the consumer goods universe: a brand with 115 years of heritage that still dominates its category. For the year ended December 31, 2024, consolidated net sales were US$3,588.6 million.

The central question for this deep dive is deceptively simple: How did a trunk-making company founded by a religious salesman in Denver become a global lifestyle brand listed in Hong Kong, now preparing for a dual listing in the United States, after surviving five different owners in 21 years?

The answer spans three major transformations. First, the family business era: from 1910 to 1973, the Shwayder family built Samsonite from a $3,500 investment into the world's leading luggage manufacturer, establishing manufacturing innovations that defined the industry. Second, the lost decades: from 1973 to 2007, Samsonite passed through the hands of Beatrice Foods, KKR, Fortune Brands, and various restructurings—a cautionary tale of what happens when private equity treats a consumer brand as a financial asset rather than a living business. Third, the modern renaissance: from 2007 to present, private equity firm CVC Capital Partners acquired a troubled company, installed turnaround specialist Tim Parker, took it public in Hong Kong, and transformed Samsonite into a multi-brand global platform through strategic acquisitions.

Key themes will emerge throughout this narrative. Brand durability: why consumers still trust a name from 1910. The PE playbook: how CVC's approach differed from prior financial owners. Premiumization: the strategic logic behind the $1.8 billion Tumi acquisition. And globalization: the pivot to Asia that defined the company's modern era.

"In January 2025, following a vote of the Company's shareholders, the Company changed its name from Samsonite International S.A. to Samsonite Group S.A.," reflecting "an important evolution in the Company since its IPO in Hong Kong in 2011. Then, our business largely comprised a single brand, Samsonite. Since 2011, we have added the TUMI, Gregory, Lipault and other complementary brands to our portfolio, and we have also significantly grown our American Tourister brand. Today, we are truly a multi-brand business."

That transformation from single-brand to multi-brand, from manufacturing company to asset-light platform, from American heritage brand to Asia-focused global enterprise—this is the story of Samsonite.

II. Founding & The Shwayder Family Era (1910-1973)

The Origin Story

Samsonite owes its start to Colorado native Jesse Shwayder. After growing up in the American West during the late 1800s, Shwayder was working in New York as a salesman for the Seward Trunk and Bag Company by his mid-20s. He was making a lot of money, but he missed Colorado and longed to pursue his dream of starting his own business. Thus, Shwayder quit his job when he was 28 and moved back to Denver. Shortly thereafter, on March 10, 1910, he founded the Shwayder Trunk Manufacturing Company with his life's savings of $3,500.

In 1910, Jesse Shwayder opened a small luggage factory in Denver with his father, Isaac, and brothers, Mark, Maurice, Benjamin, and Solomon. This was very much a family affair—five brothers and their father, all working together to build something from nothing in the American West.

With a work force of ten men, Shwayder began manufacturing what were known as "suitcases" in a 50 x 125 foot room that he had rented in downtown Denver. The management philosophy he adopted to guide the firm from day one, according to company annals, was the Golden Rule (do unto others...), to which Shwayder adhered tenaciously.

This wasn't mere corporate platitude. Jesse Shwayder's official corporate philosophy was the Golden Rule: "Do unto others as you would have others do to you." All company officers and salesmen carried a Golden Marble, which they were told to take out and look at whenever they had to make an important business decision.

Strategy from Day One: Compete on Quality, Not Price

The Shwayders' success was no accident. Indeed, Jesse drew from his work experience in New York to develop a strategy that he would pursue from the start. He realized that he was facing stiff competition from deep-pocketed luggage manufacturers. So, rather than trying to compete with other luggage companies on price, he would differentiate his products by quality and charge as high a price as the market would bear.

To reflect the quality and durability of their luggage, the Shwayders named their first products "Samson" after the powerful Biblical character. Indeed, the chief advantage of the cases was that they could take a lot of punishment and were extremely durable. In 1916, in fact, the Shwayders took a picture that would become an advertising coup. The four brothers and their father, Isaac, stood on a plank positioned atop one of their suitcases above the caption, "Strong enough to stand on."

This marketing image—five portly Shwayder men weighing over 1,000 pounds combined, standing on a single suitcase—became the company's defining advertisement for decades. It captured something essential about the brand promise: this luggage could handle anything you threw at it.

Building the Family Business

All the Shwayder brothers held executive positions in the company in the 1920s. Jesse was the company's president, Mark Shwayder directed sales, Maurice and Ben Shwayder oversaw manufacturing, and Solomon Shwayder served as the company's lawyer.

By 1918, the brothers were able to nationally market one of their quality suitcases for the first time. For the next eleven years, they experienced substantial business success as revenue grew. However, the stock market crash of 1929 and the subsequent Great Depression delivered setbacks—truck shipments dropped by fifty percent in just a couple of years.

By the 1930s, in fact, the Denver luggage plant was the most modern of its type in the world. From that plant came innovative Samson luggage with exclusive features such as wood-frame construction, super-strong handles, rayon linings, fiber finishes, and secure locks. Specialty fibre finishes were developed by Shwayder Trunk specifically as a covering for Samson suitcases. In 1939 the company introduced a unique suitcase that Jesse dubbed "Samsonite." The suitcase, which was the predecessor to the popular Samsonite Streamlite line, was covered with sturdy vulcanized fiber that was used with a leather binding. The case's tapered shape was destined to become a classic within the industry.

A religious man, Shwayder named one of his initial cases Samson, after the Biblical strongman, and began using the trademark Samsonite in 1941 for its tapered vulcanized fiber suitcase, introduced in 1939.

Innovation Leadership: The Ultralite Revolution

Importantly, the company introduced the Ultralite luggage line in 1956. That luggage was the first to abandon wood-frame construction in favor of magnesium and injection-molded plastics. This was a milestone in the luggage industry—arguably the most significant innovation in suitcase design since the suitcase itself.

Think about what this meant. For decades, luggage was essentially a miniature trunk: wood frame, leather covering, brass fittings. The Ultralite changed the fundamental materials science of the industry, enabling lighter, more durable, more affordable products. Modern luggage manufacturing still builds on principles established by this 1956 breakthrough.

Global Expansion Under King Shwayder

In 1961, Jesse Shwayder's son, King D. Shwayder, became president of the company, and in 1965 the Shwayder Brothers, Inc., changed its name to Samsonite Corporation. Under King's leadership, Samsonite managed to firmly establish itself as the world's leading manufacturer of molded luggage and attaché cases by the early 1970s. The company added manufacturing operations and sales offices throughout Europe and Japan during the 1960s and enjoyed substantial sales increases in those regions.

Also in 1956, Shwayder Brothers expanded out of the United States with a separate Canadian subsidiary and an export sales department focused on Europe. Meanwhile, the flourishing furniture division was consolidated and relocated to a giant production facility in Tennessee. During the 1960s, the company introduced a number of new products under the increasingly popular Samsonite brand name.

The LEGO Interlude

Here's a footnote in Samsonite history that few people know: Beginning in 1961, Samsonite manufactured and distributed Lego building toys for the North American market under license from the Lego Group.

The snap-together plastic building blocks for children enjoyed immediate acceptance in the North American marketplace and eventually became one of the most popular toys of all time. The stellar success of LEGO prompted Shwayder Brothers to launch more than 50 new toy items before the early 1970s. Lagging performance of the toy division, however, caused the company to jettison the operation in 1972 and focus on furniture and luggage.

A licensing dispute ended the arrangement in the U.S. in 1972, but Samsonite remained the distributor in Canada until 1986.

The LEGO episode illustrates both the Shwayders' entrepreneurial ambition and the discipline to exit when diversification didn't work. The family recognized that luggage was their core competency. What they couldn't have anticipated was that within a year, they would no longer control the company at all.

The Shwayders sold the Samsonite Corporation in 1973. After 63 years of family ownership, an era ended. The Golden Rule marble would be inherited by new owners who viewed the company very differently.

III. The Lost Decades: Ownership Chaos (1973-2005)

The Beatrice Acquisition & KKR Era

The Shwayder family sold the company to Beatrice Foods in 1973. This was an era when conglomerates were in fashion—Beatrice Foods was acquiring everything from dairy products to industrial equipment. Luggage fit somewhere in between.

Samsonite operated with relative independence within Beatrice until 1986, when Samsonite was sold to Kohlberg Kravis Roberts. Subsequently, in the 1980s and into the 1990s, Samsonite went through multiple ownership changes. Forbes Magazine states that "the company spent most of the 1980s and 1990s in turmoil amidst multiple handoffs."

This was the PE playbook of the 1980s: leverage, extract, flip. KKR didn't buy Samsonite to build a luggage empire. They bought it because they could use the company's stable cash flows to service acquisition debt. The problem with this approach for consumer brands is that it starves the business of the reinvestment needed to maintain brand equity and market position.

The E-II Bankruptcy & Astrum

First, Samsonite was spun off from KKR as part of E-II, which came under the control of Fortune Brands. E-II went through bankruptcy and was renamed Astrum International. In 1993, Astrum purchased American Tourister luggage, complementing Samsonite. In 1995, Astrum split, and an independent Samsonite (now including American Tourister) was once again headquartered in Denver.

The American Tourister acquisition was the silver lining in this chaotic period. Founded in 1933, American Tourister was the #2 luggage brand in America, positioned at a lower price point than Samsonite. The combination created the portfolio approach that would later define the company's strategy—multiple brands at different price points serving different customer segments.

By 1994, the combined operations were generating sales of approximately $600 million annually. Samsonite posted record sales in 1994 of $634 million, about $72 million of which was profit. For a moment, stability seemed possible.

Near-Death Experience & 9/11 Impact

Then came the dark years. The company survived four straight years of losses totaling $285.3 million in the late 1990s and early 2000s. It was close to a major refinancing deal in 2001, but the deal fell through after the September 11, 2001, terrorist attacks because lenders feared a major decline in the travel industry.

The company struggled over the next two years—Its shares were traded on the Nasdaq Smallcap Market from 1994 until 2002, when it had to drop off the exchange because its market capitalization fell below the minimum threshold. Only a 2003 recapitalization that shareholders approved pulled Samsonite back from the brink of bankruptcy.

The Denver factory, which employed 4,000 people at its peak, closed in May 2001. This was the factory the Shwayder brothers had built, the most modern luggage plant in the world in its day. Its closure marked the end of Samsonite as an American manufacturing company.

The Bottoli Turnaround Attempt (2004-2007)

In 2005, the company was acquired by Marcello Bottoli, former CEO of Louis Vuitton, to pull it out of a long slump. Bottoli left the company in 2009.

Bottoli's appointment was fascinating—here was someone with luxury brand credentials trying to reposition a mass-market luggage maker. He introduced the Samsonite Black Label line, attempting to bring premium positioning to the brand. The strategy had merit: if Louis Vuitton could charge thousands for luggage, why couldn't Samsonite capture some of that premium?

The answer, as it turned out, was brand architecture. Consumers who saw "Samsonite Black Label" still saw "Samsonite"—a reliable, quality brand, but not a luxury one. The premium line struggled to justify its prices, while the simultaneous introduction of a Blue Label economy line confused consumers and cheapened the brand's reputation.

After a change of ownership in May 2005, Samsonite's headquarters moved from Denver to Mansfield, Massachusetts. Effective September 1, 2005, Samsonite then moved its U.S. marketing and sales offices from Warren, Rhode Island, to Mansfield, Massachusetts.

The company had survived, but it was a shadow of its former self—overleveraged, unfocused, and without a clear strategic direction. What it needed was an owner with the patience and capital to rebuild properly.

IV. KEY INFLECTION POINT #1: The CVC Capital Partners Acquisition (2007)

The Deal

In July 2007, private equity firm CVC Capital Partners took over Samsonite for $1.7 billion. CVC Capital Partners Ltd. became Samsonite's fifth owner in 21 years.

European private equity firm CVC Capital Partners agreed to buy US-based Samsonite Corporation, a designer and manufacturer of luggage. The deal was part of a drive to increase CVC's US presence. CVC acquired all of Samsonite's outstanding stock for $1.49 per share in cash. The capital structure of the deal was one-third equity and two-thirds debt.

On October 1, 2007, private equity firm CVC Capital Partners acquired consumer products company Samsonite International from Ontario Teachers Pension Plan and Ares Private Equity Group for 1.7B USD.

Why would CVC want a company that had been passed around like an unwanted hand-me-down for three decades? The answer lay in what CVC saw that others had missed.

The CVC Vision

CVC said in a statement that it expected to orient the brand more towards the luxury market and Asia. Managing partner Luigi Lanari of CVC said in the statement that "China and India present particularly interesting opportunities for growth." If the business grows as planned, Samsonite will be "highly suitable for an initial public offering at some later date." Additionally, Samsonite would make "selective acquisitions" to step-change its growth profile in certain key markets.

This was a fundamentally different playbook from prior PE owners. CVC wasn't buying Samsonite to strip it—they were buying it to build. The strategy had three pillars: operational turnaround, geographic expansion to Asia, and eventual IPO as an exit mechanism.

The PE Playbook: Restructuring & Transformation

The first step was bringing in the right leadership. Private-equity group CVC Capital Partners bought the company in 2007, then put it through financial restructuring. The CEO at the time left and corporate-turnaround specialist Tim Parker came in 2008 as chairman (and later as CEO).

Timothy Charles Parker (born 19 June 1955) is a British executive. He has been chairman of the National Trust, Post Office Ltd and Her Majesty's Courts and Tribunals Service (HMCTS). From 1986 to 2014 he was CEO of a number of companies, including successively Kenwood, Clarks Shoes, Kwik-Fit, the AA and Samsonite.

Parker's track record was remarkable. In 1996, Parker became CEO of Clarks Shoes. He substantially reorganised the company, closed 20 factories, moved manufacturing overseas, and revived the Clarks brand with more up-to-date shoe styles. Within six years, the company's profitability increased by 150%, and by the time he left, in 2002, it had revenues approaching £1 billion a year.

He brought the same approach to Samsonite.

In November 2008, he was appointed non-executive chairman of Samsonite, and was made CEO in January 2009. CVC Capital Partners acquired Samsonite in July 2007. The 2008 financial crisis affected the luggage company due to the declines in international air travel and consumer spending; 2008 earnings before interest, tax, depreciation, and amortisation collapsed from $120 million to $40 million. Parker was brought in to turn the company around. He restructured the company, replaced its management, cut jobs, closed stores, and invested funds in new suitcase designs and marketing. In 2010, earnings before interest, tax, depreciation, and amortisation revived to $192 million.

That's a staggering improvement: from $40 million EBITDA in 2008 to $192 million in 2010—nearly a 5x increase in just two years. Parker achieved this through a combination of cost rationalization and strategic focus.

The Asset-Light Manufacturing Model

One of the most significant strategic shifts was the move to asset-light manufacturing. Samsonite started out manufacturing luggage at its own factories, but after stumbles over the past decade, it now outsources production. Almost all of its manufacturing is done in Asia, with Chinese factories supplying 84 percent of its suitcases.

This wasn't just about cost reduction—it was about focus. Samsonite's competitive advantage wasn't in manufacturing; it was in brand, design, and distribution. By outsourcing production to specialized suppliers in China and elsewhere, the company could focus its capital and management attention on activities that drove differentiation.

Setting Up for the Future

On September 2, 2009, Samsonite Company Store LLC (U.S. retail division), formally known as Samsonite Company Stores Inc., filed for Chapter 11 bankruptcy. It planned to close up to 50% of its stores and discontinue the "Black Label" brand in the United States. In June 2011, Samsonite raised $1.25 billion in an initial public offering in Hong Kong.

From the depths of near-bankruptcy in 2001-2003, through chaotic ownership changes, through the 2008 financial crisis, Samsonite had finally found an owner willing to invest in the business rather than strip it. The stage was set for the next chapter.

V. KEY INFLECTION POINT #2: The Hong Kong IPO (2011)

Why Hong Kong?

Italy-based Prada decided Hong Kong was a better market for its IPO earlier this year than the Borsa Italiana or the London Stock Exchange; Samsonite, the American luggage maker founded in 1910, has chosen Hong Kong for its IPO. When asked why he chose Hong Kong, Samsonite's CEO, Tim Parker, told The New York Times, "We want to orient the company to where the world's center of gravity is going to be in the future."

"We need to orient the company to where the center of gravity will be in the future, which I think is going to be in China and Hong Kong," Chairman Tim Parker said.

This was a bold call in 2011. American companies overwhelmingly listed in New York. European companies listed in London or Frankfurt. An American brand with European PE ownership choosing Hong Kong for its primary listing was newsworthy.

China and India are Samsonite's second- and third-biggest markets. Only the United States is bigger. The company predicts Asia will be the world's fastest growing luggage market over the next four years, powered by a surge in Chinese and Indian travelers.

The IPO Execution

The company was listed on the Hong Kong Stock Exchange in June 2011, raising $1.25 billion in the IPO.

Private equity firm CVC Capital Partners owns about 54.3 percent of Samsonite while Royal Bank of Scotland owns 30 percent. Parker said CVC and RBS would sell off a large chunk of their shares but will "still be left with an appreciable stake in the business."

Samsonite sold shares comprising an international offering and a Hong Kong public offering. Of the Offer Shares, 121,100,005 were new shares and 550,135,595 were secondary shares to be sold by Selling Shareholders, consisting of certain funds managed and advised by CVC Capital Partners.

The world's biggest luggage maker, Samsonite International, dropped 11% in its Hong Kong trading debut on Thursday, June 16. Samsonite's fall underscored tepid investor appetite for initial public offerings as global markets struggled. The U.S.-based firm's slump was the latest in a string of weak Asian IPO performances from companies including MGM China and commodities trader Glencore.

The weak debut didn't faze management. However, Chief Executive Officer Timothy Parker remained upbeat about Samsonite's performance in the markets. "Well I think in a way it wasn't quite at the bottom of the price range and that was actually not a bad place to be considering, as I said, where markets are at the moment, which I think you'll agree is in a pretty tough place."

Market Dominance Position

The IPO documents laid out Samsonite's competitive position. The company had a 9.6 percent share of the global luggage market last year, according to research by Frost & Sullivan cited by Samsonite. Second-place VF Group, maker of Jansport, Eastpak and North Face bags, had 3.1 percent.

With an annual retail sales value approximately six times larger than its nearest direct competitor, Samsonite International was well positioned to expand its share in the growing US$24.7 billion global luggage market. The emerging high-growth Asian market, where the Company's net sales grew at a CAGR of approximately 23% between 2001 and 2010, included three of its top five markets by net sales (China, India and South Korea) in 2010, in each of which the Company was the luggage market leader. Samsonite International was growing fastest in some of its highest margin markets. Its net sales in Asia, which accounted for 33.3% of its total net sales in 2010, increased by 45.1% over 2009. Asia was the Company's most profitable region in 2010, with an Adjusted EBITDA margin of 19.8%, and accounted for 41.7% of its Adjusted EBITDA.

This market position—three times the share of the nearest competitor—was the foundation for everything that followed. When you're the dominant player in a fragmented industry, you have options that smaller competitors don't.

Delivering on IPO Promises

Samsonite reported that its full-year revenue increased 29 percent to $1.59 billion for the year. That was due largely to a gain of nearly 43 percent in revenue from Asia and a 28 percent improvement in North America. Latin America showed a 22 percent gain in sales and Europe nearly 18 percent. "The global traffic market is very strong, despite the ups and downs, particularly in the European economies, last year," Samsonite chief executive Tim Parker told investors.

"This year is just a confirmation of our strategy," Parker said.

The Hong Kong listing marked a new era for Samsonite. It was no longer a PE portfolio company to be eventually flipped—it was a public company with accountability to shareholders and a clear growth mandate in Asia.

VI. The Acquisition Spree: Building a Portfolio (2012-2017)

Post-IPO M&A Strategy

Before 2012, the Company's business was primarily centered on the Samsonite brand, focused largely on travel luggage, and distributed principally through the wholesale channel. Management recognized that to achieve the next level of growth, they needed to expand the portfolio.

The acquisition of the premium luggage brand Tumi came as part of Samsonite's continued global acquisition strategy. In fact, since 2012 Samsonite has announced nine acquisitions, aiming to double its annual sales to c.$5bn in the six years ending 2020, as it expands into distributing and selling other travel and non-travel bag brands.

Key Acquisitions

Hartmann (2012): In August 2012, Samsonite paid $35 million in cash to buy the high-end luggage brand Hartmann, which was founded in 1877. Hartmann represented Samsonite's first foray into the premium segment—a heritage brand even older than Samsonite itself, with positioning above the core Samsonite line.

Gregory Mountain Products (2014): In June 2014, Samsonite agreed to buy technical outdoor backpack brand Gregory Mountain Products from Black Diamond, Inc., for $85 million in cash. This acquisition expanded Samsonite's reach beyond travel luggage into outdoor and casual bags—a category with different growth dynamics and customer segments.

eBags (2017): In April 2017, Samsonite agreed to acquire eBags.com for $105 million in cash. eBags represented a digital distribution play—one of the largest online luggage retailers in the United States, with customer data and e-commerce capabilities that complemented Samsonite's wholesale-heavy model.

"Samsonite has announced nine acquisitions since 2012 and says its strategy to grow through acquisitions is working."

These bolt-on acquisitions served multiple purposes: filling gaps in the product portfolio, expanding into new categories, adding distribution capabilities, and—critically—developing the organizational muscle for integrating acquired businesses. Each deal was relatively small and manageable, allowing the team to build the playbook they would need for something much larger.

VII. KEY INFLECTION POINT #3: The Tumi Acquisition (2016)

The Transformational Deal

Samsonite International S.A. and Tumi Holdings, Inc. announced that they had entered into a definitive agreement whereby Samsonite would acquire Tumi for US$26.75 per share in an all cash transaction, valuing Tumi at an equity value of US$1.8 billion. "This is a transformational acquisition for Samsonite. It will meaningfully expand our presence in the highly attractive premium segment of the global business bags, travel luggage and accessories market," said Ramesh Tainwala, Chief Executive Officer of Samsonite. "Tumi is a perfect strategic fit for our business. The brand is beloved by millions of loyal customers for its high quality and durable premium business and luggage products."

This represented a 13.6x multiple of enterprise value to Tumi's Adjusted EBITDA for the last twelve months ended December 31, 2015 and a premium of approximately 38% to Tumi's volume weighted average price. Samsonite intended to fund the transaction through committed bank financing. In connection with the transaction, Morgan Stanley, HSBC, SunTrust and MUFJ arranged the committed financing.

Samsonite has zipped up a deal to acquire luxury rival Tumi for around $1.8 billion, in what was the largest acquisition for Samsonite since its initial public offer in 2011. The deal was expected to close in the second half of 2016 subject to shareholder approval.

Strategic Rationale

Ideal and complementary fit with Samsonite. With approximately 2,000 points of distribution across 75 countries, Tumi's leading market position in the premium business and luggage segment was a perfect complement to Samsonite's strong and diverse portfolio of brands and products, with limited overlap in market positioning, price point and distribution. The addition of Tumi built on Samsonite's proven track record of successful acquisitions across multiple product categories and price points to broaden its portfolio. It enabled Samsonite to strategically expand into the highly attractive premium segment of the global business bags, travel luggage and accessories market with a business and travel brand that was recognized worldwide as being "best-in-class" in the premium segment.

A core-brand as Samsonite is very widely distributed and as a result does not have the attraction a premium brand would need to have. Therefore, the acquisition of a high-end brand Tumi should help the company rebalance its portfolio of baggage brands. The deal seemed to have upside potential for both companies. On the one hand, Samsonite would gain from diversification of its product portfolio, expanding its presence in the highly attractive premium segment of the global business bags, travel luggage and accessories market. On the other hand, the New Jersey-based Tumi with two thirds of its net sales in the US market would benefit from Samsonite's growing global infrastructure when expanding further into key markets such as Asia, Europe, and South America.

The Premium Positioning Problem Solved

Remember the failed Samsonite Black Label experiment? The lesson was that consumers wouldn't pay premium prices for a luggage line with "Samsonite" in the name, no matter how many "Black Label" modifiers you added.

"Samsonite Black Label stayed in our imagination and our internal communications -- but whenever the customer was seeing 'Samsonite Black Label,' he was seeing 'Samsonite,'" Tainwala recalled. It turns out that the tiered structure simply confused consumers, with few willing to pony up extra cash for a high-end bag. Meanwhile, the Samsonite Blue label cheapened the company's reputation, encouraging consumers to shift down from the $300 "regular" bag to a $100 option. It also caused buyers of the regular bags to question whether they were really getting the same old quality in their trusty Samsonite.

So instead of sticking with its own high-end line, Samsonite made the largest acquisition in its history in August 2016 when it paid $1.8 billion for luxury luggage-maker Tumi Holdings. Samsonite is now using that buy to help segment its business by brand: The company sells luxury bags under the Tumi label, often with leather finishing. These are "aspirational" pieces of luggage, with Tumi's black ballistic business case serving as a best seller. Tumi also offers an increasing number of pieces with fashion-influenced flair for female travelers. Samsonite remains the company's flagship brand, offering mid- to high-end luggage that typically comes with a hard-metallic case. American Tourister, which Samsonite bought in 1993, serves as a "family brand" of more-affordably priced luggage. Kamiliant is a budget brand aimed at backpackers and first-time travelers.

Industry Impact: Forcing LVMH's Hand

"This acquisition follows the acquisition of Tumi by Samsonite, removing the only other meaningful high-end luggage brand from the market. Luggage should be favored by the continuing development of tourism," said Exane BNP Paribas analyst Luca Solca. Samsonite agreed to buy New Jersey-based Tumi in a $1.8 billion deal earlier this year.

With Samsonite's acquisition of Tumi earlier in 2016, LVMH's move with Rimowa is set to partially counter-balance Samsonite's dominance in luggage.

"Rimowa is the only high-end brand remaining in the market, after the acquisition of Tumi by Samsonite. The multiple paid by LVMH makes sense, as it is in line with that paid by Samsonite for Tumi."

Within months of the Tumi acquisition, LVMH announced it would acquire 80% of Rimowa for €640 million ($716 million). If all went according to plan, Samsonite and LVMH, the parent of Louis Vuitton, would control roughly 25% of the world's luggage market, based on data from market-research firm Euromonitor International. Even before the acquisition of Tumi, Samsonite's market share dwarfed that of LVMH, its closest rival, which had a 5% share last year.

The Tumi acquisition didn't just add a premium brand to Samsonite's portfolio—it reshaped the competitive landscape of the entire luggage industry, triggering a consolidation wave at the premium end of the market.

VIII. KEY INFLECTION POINT #4: The COVID-19 Crisis & Recovery (2020-2023)

The Pandemic Impact

If you wanted to design a crisis that would devastate a luggage company, you couldn't do better than COVID-19. Borders closed. Airlines grounded fleets. Business travel collapsed. Leisure travel vanished. Nobody needed a new suitcase.

For the year ended December 31, 2020, Samsonite's net sales decreased by US$2,102.1 million, or 57.5%, to US$1,536.7 million.

The year-on-year decline in net sales widened to 77.9% during the second quarter of 2020 when most of the Group's markets were subject to government-mandated lockdowns. As governments loosened social-distancing restrictions and markets around the world began to reopen, the year-on-year decline in the Group's net sales moderated to 64.7% during the third quarter of 2020, and further improved to a year-on-year decrease of 58.1% during the fourth quarter of 2020.

From a market cap of approximately $6 billion pre-pandemic, Samsonite dropped to $1.5 billion at the trough—a 75% decline in shareholder value.

Survival Mode

Samsonite announced it had completed the syndication and allocation of a new term loan borrowing and amended its credit agreement to provide financial covenant relief. These actions enhanced Samsonite's strong liquidity position and increased its financial flexibility as the Company addressed the ongoing impact of the COVID-19 pandemic. On April 30, 2020, Samsonite completed syndication and allocation of a senior secured incremental term loan B facility in the aggregate principal amount of US$600.0 million.

"While Samsonite addresses the ongoing impact of the COVID-19 pandemic, the health and safety of our employees and their families, as well as our customers and business partners, has been and will continue to be our top priority. Samsonite also is focused on maintaining a strong balance sheet, liquidity position and financial flexibility."

As a result of our comprehensive program to reduce costs and conserve cash, we identified total estimated annualized run-rate fixed cost savings of approximately US$200 million (including savings from actions to be executed in 2021).

The Turnaround Within the Crisis

"The COVID-19 pandemic brought its challenges as the world suddenly stopped traveling. Yet, through bold actions and careful management, we navigated the business through that period and emerged stronger. Most importantly, our teams and business remained intact. It was truly a giant effort by all, especially companies in the travel industry."

The company's response was swift and comprehensive. Approximately US$116 million in annual advertising & promotion savings vs. prior year; US$125 million of cash savings from suspending annual cash distribution to shareholders; Approximately US$103 million in capital expenditure and software purchase savings.

The Recovery

The recovery, when it came, was dramatic. In 2022, Samsonite reported revenue of $3.2 billion, showcasing a strong recovery from the pandemic's impact, with net income rising to $396 million. The company attributed this growth to increased consumer demand and the resurgence of international travel. In 2023, total global revenue reached approximately $3.7 billion.

"The strong increase in Adjusted EBITDA, along with our ongoing attention on cash flow management, enabled Samsonite to generate total cash of US$175.6 million during the fourth quarter of 2021, an increase of US$59.5 million from the US$116.1 million generated in the third quarter of 2021, and a considerable improvement from total cash burn of (US$27.3) million in the second quarter and (US$64.6) million in the first quarter of 2021. Overall, Samsonite generated total cash of US$199.8 million for the year ended December 31, 2021, an improvement of US$559.9 million compared to total cash burn of (US$360.1) million in 2020."

The crisis tested whether the multi-brand, asset-light model Samsonite had built was resilient. The answer was a definitive yes.

IX. Modern Era: Today's Business & Future Strategy (2024-2025)

Current Performance

For the year ended December 31, 2024: Consolidated net sales were US$3,588.6 million, a decrease of 2.5%, but approximately flat on a constant currency basis, versus a strong net sales base in 2023. Expanded gross profit margin by 70 basis points year-over-year to 60.0%. Achieved adjusted EBITDA margin of 19.0%. Increased adjusted free cash flow by US$26.5 million year-over-year to US$311.0 million. Returned US$307.6 million to shareholders through US$157.6 million in share buybacks and a US$150.0 million cash distribution. Maintained substantial liquidity of US$1.4 billion.

Achieved Q4 adjusted EBITDA of US$195 million, representing a record Q4 adjusted EBITDA margin of 20.7%, up 160 basis points vs. Q4 2023 mainly due to lowered advertising spend as a percentage of net sales and higher gross profit margin. Maintained overall discipline on expenses with combined Q4 2024 distribution and G&A expenses of US$332 million, a US$2 million decrease compared to Q4 2023, despite adding 67 net new stores over the past year.

Brand Portfolio Today

Samsonite Group S.A. engages in the design, manufacture, sourcing, and distribution of luggage, business and computer bags, outdoor and casual bags, and travel accessories in Asia, North America, Europe, and Latin America. The company sells its products under the Samsonite, Tumi, American Tourister, Gregory, High Sierra, Lipault, and Hartmann brands, as well as other owned and licensed brand names. It distributes its products through wholesale distribution channels, as well as through company-operated retail stores and e-commerce. The company was formerly known as Samsonite International S.A. and changed its name to Samsonite Group S.A. in January 2025.

When Samsonite IPO-ed in 2011, it was seen as a single-brand business, with the Samsonite brand contributing over three-quarters of revenue. But over the years, the company has deliberately diversified and built out its brand portfolio. It expanded American Tourister and acquired Tumi in 2016, which brought in a new customer base and price point (read luxury). Today, these three brands make up 93% of group sales—Samsonite at 52%, Tumi at 24%, and American Tourister at 17%. The rest comes from smaller brands like High Sierra, Hartmann, Lipault, Gregory, Kamiliant, and eBags. This brand architecture allows Samsonite to serve different price points, regions, and retail channels without cannibalizing itself—something many consumer companies struggle to balance.

About 40% of Samsonite's revenue comes from its direct-to-consumer channel—which includes e-commerce and over 1,100 self-operated stores. The remaining 60% is wholesale. This omni-channel approach is essential to control margins, gather consumer insights, and mitigate reliance on external retail partners. It also provides more pricing power and resilience during economic cycles.

Recent Performance by Brand

Samsonite continues to grow steadily, with 3.3% YoY sales growth, driven by strong branding and functional product upgrades. Tumi saw a 0.8% decline, largely because luxury and premium segments are feeling the pinch of slower discretionary spending. American Tourister took the biggest hit, down 6.1%, due to increased price competition in India and weaker demand from North American wholesalers.

The good news? Momentum started to return in Q4 2024. Samsonite and Tumi both posted net sales growth of 4.6% and 4.4% respectively. The fourth quarter often reflects peak travel periods, so a strong showing there suggests the brand strength remains intact.

2025 Update: Latest Results

Q3 2025 represented a sequential improvement compared to the 4.9% period-over-period net sales decline in the second quarter of 2025. The sequential improvement in period-over-period net sales growth during the third quarter of 2025 was driven largely by improvement in Asia (-4.3% in the third quarter of 2025 from -9.0% in the second quarter of 2025), coupled with positive growth in Europe (+1.3%) and Latin America (+8.0%). During the third quarter of 2025, the TUMI brand reported net sales of US$204.3 million, an increase of 5.0% compared to the third quarter of 2024.

"Though we are closely monitoring the global economic backdrop and trading conditions, we are encouraged by the recent improvement in trends in our business. Our Board of Directors and management firmly believe a dual listing of the Company's securities in the United States will enhance shareholder value creation over time, and assuming a constructive environment, we intend to complete our dual listing in 2026."

The Dual Listing Strategy

Samsonite announced that its board of directors has authorized the Company's management to pursue listing the Company's shares on a second leading stock exchange in addition to the Hong Kong Stock Exchange. The Company recently announced outstanding results for the year ended December 31, 2023, including strong double-digit net sales growth year-on-year and record gross profit margin and Adjusted EBITDA margin. An additional listing would increase liquidity of the Company's shares and create an opportunity to reach investors in markets that are an important part of the Company's global footprint and growth drivers for its business.

Luggage maker Samsonite International has decided to pursue a second stock listing in the United States, its single-biggest market by sales, to reach more investors and boost liquidity of the firm's shares. Samsonite, which has been listed in Hong Kong since 2011, revealed that initiative in its interim results, ending months of speculation after initially mentioning the dual-listing plan in March. "The company believes this dual listing will build on its strong investor support on the Hong Kong stock exchange and help the company continue to deliver on its value-creation goals."

Samsonite is said to be working with JPMorgan Chase & Co. and Morgan Stanley toward a dual listing in the US.

Sustainability & ESG Recognition

"In recognition of our progress and achievements, MSCI upgraded its environmental, social and governance rating on Samsonite Group from 'A' to 'AA', and TIME ranked Samsonite Group at number 40 out of 500 in its list of the 'World's Best Companies in Sustainable Growth 2025' and 2nd in the Retail, Wholesale & Consumer Goods category. We are passionate about the sustainability initiatives Samsonite Group is pursuing, and we are tremendously honored to be recognized for our ongoing commitment to leverage our scale to create a path towards a more sustainable future for the bags and luggage industry."

India: The Manufacturing Powerhouse

The Nashik plant, with 8 lakh units of monthly capacity, is the group's largest manufacturing unit and is also under a Rs 100-crore expansion which should be completed by early next year. The main Nashik plant, set up 13 years ago, manufactures products under Samsonite, American Tourister and Kamiliant brands.

Samsonite's product portfolio encompasses both hard and soft luggage, with the latter designed in-house and manufactured by third-party suppliers. The Nashik plant takes pride in being the world's first and only facility employing patented pressure molding technology for crafting hard luggage bodies and casings.

According to Jai Krishnan, CEO of Samsonite South Asia, the company expects the Indian unit to meet the company's global luggage requirements as it works on its 'China Plus One' strategy to deal with supply chain disruptions. "The unit at Nashik will be Samsonite's biggest manufacturing base in this year itself."

X. Leadership: The People Behind the Transformation

Kyle Gendreau: From CFO to CEO

Mr. Kyle Francis Gendreau has served as an Executive Director of the Company since its incorporation in March 2011 and as an executive director of the consolidated group since January 2009. He has served as the Chief Executive Officer of the Company since May 31, 2018 and is responsible for the Company's overall strategic planning and for managing the Group's operations. Prior to his appointment as Chief Executive Officer, Mr. Gendreau served as the Company's Chief Financial Officer from January 2009 until May 2018 and was actively involved in the development of the Group's business and in implementing the Company's strategic plan, in addition to managing all aspects of the Group's finance and treasury matters. He continued to serve as Interim Chief Financial Officer from May 2018 to November 2018. Mr. Gendreau joined the Group in June 2007 as Vice President of Corporate Finance and as Assistant Treasurer.

Prior to joining the Group, he held various positions including vice president of finance and chief financial officer at Zoots Corporation, a venture capital-backed start-up company (2000 to 2007), assistant vice president of finance and director of SEC reporting at Specialty Catalog Corporation, a listed catalog retailer (1997 to 2000) and a manager at Coopers & Lybrand in Boston (1991 to 1996). Mr. Gendreau holds a BS in Business Administration from Stonehill College, Easton, Massachusetts, USA (1991) and is a Certified Public Accountant in Massachusetts.

Gendreau's career trajectory is notable: he joined as a finance executive just as CVC acquired the company, was promoted to CFO during the turnaround, led the finance function through the Hong Kong IPO, oversaw the debt financing for the Tumi acquisition, and was elevated to CEO in 2018. He has been with Samsonite for 18 years.

"My journey at Samsonite Group has been, and continues to be, amazing. We are an industry leader with brands like Samsonite, Tumi and American Tourister, which touch every part of the globe. I served as CFO for 10 years and have now begun my eighth year as CEO. We listed the company on the Hong Kong Stock Exchange in 2011 while I was CFO, and since then, we've acquired several companies, including Tumi in 2016. Over my 18 years here, the business has experienced tremendous growth."

"In every role, I made it a point to get involved beyond my defined responsibilities and always focused on building strong relationships, staying true to core values and supporting people and teams. One of the most important leadership lessons I've learned is to treat everyone the same—whether they're on the factory floor, in a retail store, part of the office team or sitting in the boardroom. Everyone has a role to play, and we're all working toward the same goals. I see myself as just another member of the team, which keeps me grounded and connected to the people I lead."

Tim Parker: The Turnaround Specialist

Mr. Timothy Charles Parker has been the Chairman of the company since 2011. He served as the Chief Executive Officer at the company from 2009 to August 2014, the Non Executive Chairman from 2008 to 2009. Previously, he served as the Chief Executive Officer at The Automobile Association from 2004 to 2007, Kwik-Fit from 2002 to 2004, Clarks from 1997 to 2002, and Kenwood Appliances from 1989 to 1995.

Parker's track record as a turnaround specialist at Clarks Shoes, Kwik-Fit, and the AA made him the ideal choice for Samsonite's post-CVC transformation. His approach—restructure, refocus, reinvest—proved the template that restored Samsonite to profitability and positioned it for the Hong Kong IPO.

XI. Competitive Landscape & Strategic Analysis

Market Position

Samsonite is the largest luggage company in the world, with a dominant 20% global market share and US$3.6 billion in annual revenue. That might not sound massive, but keep in mind—the luggage industry is highly fragmented. The next biggest player? Rimowa, owned by LVMH, and even then, Rimowa's estimated sales come in at just around US$1 billion. There's a huge gap between number one and everyone else.

Samsonite led the market with a 6% share, underscoring its prominent position as a major player in the luggage industry. Rimowa followed with a 4% market share and is known for its high-quality aluminum and polycarbonate suitcases. Tumi held a 3% share, appealing to luxury and business travelers with its premium products. American Tourister and Eastpak each captured 2% of the market, targeting budget-conscious and younger demographics, respectively. However, the majority of the market, comprising 79%, was occupied by a diverse array of other manufacturers, which suggests a highly fragmented market where no single company holds overwhelming dominance.

Note that Samsonite owns both the Samsonite brand (#1) and Tumi (#3), giving it a combined share that's roughly 3x that of its nearest independent competitor.

The DTC Disruption: Away and New Entrants

"We're all fighting to steal market share from Samsonite, which owns 25% of the market, and LVMH, which owns another 10%."

A decade ago, most tourists were wheeling around suitcases from luggage giants Samsonite, Delsey, American Tourister, Tumi, and Rimowa. But these days, while these brands still dominate roughly half the market, there's a flock of new brands shaking up the $174 billion global luggage sector. The trend began with Away, the startup founded in 2015, known for its wheeled cases with signature grooves, affordably priced at $275 for a carry-on. Fueled by $156 million in venture capital funding, it grew quickly in its early years, selling millions of cases.

Away, a New York-based direct-to-consumer travel start-up that was valued at $1.4 billion in May 2019, presents the biggest challenge to Rimowa. Away's hardside bags—which now include aluminium—cost roughly a third of Rimowa's products. (A large aluminium carry-on from Away is $495, while Rimowa's comparable Original Cabin Plus bag is $1,250).

The direct-to-consumer luggage brands represent real competition, particularly among younger consumers who grew up buying online. However, Samsonite's scale advantages in manufacturing, distribution, and brand recognition remain formidable barriers.

The LVMH Response

After quadrupling sales in five years following LVMH's acquisition, the German luggage maker Rimowa is seeing continued momentum during rocky times for high-end shopping, including in China. Despite that lingering sluggishness, Rimowa "has returned to our pre-Covid growth track." The brand's sales have nearly quadrupled in five years, and are growing by double-digits this year, even as most luxury brands report falling revenues. While owner LVMH does not report sales for individual units, Rimowa was one of only three brands called out for "confirming their solid momentum" along with Loro Piana and Loewe. CEO Bonnet-Masimbert said the brand is even still growing in China, the key market that's caused many luxury firms to teeter.

Porter's Five Forces Analysis

Threat of New Entrants: MODERATE The luggage industry has relatively low barriers to entry for basic products—any manufacturer can make a suitcase. However, building brand recognition, distribution networks, and manufacturing scale creates significant barriers at the premium end. DTC brands like Away have demonstrated that digital-native approaches can work, but sustaining growth remains challenging.

Bargaining Power of Suppliers: LOW Samsonite's asset-light model means it works with numerous contract manufacturers, primarily in Asia. With 84% of production sourced from China, the company has leverage over individual suppliers. The "China Plus One" strategy to expand manufacturing in India further reduces supplier concentration risk.

Bargaining Power of Buyers: MODERATE The wholesale channel (60% of revenue) includes powerful retailers like department stores and airport retailers who can negotiate on price. However, Samsonite's brand recognition and product breadth give it leverage. The growing DTC channel (40% of revenue) reduces buyer power.

Threat of Substitutes: LOW TO MODERATE There's no direct substitute for luggage when traveling—you need something to carry your belongings. However, changing travel patterns (e.g., more carry-on only travel) and multi-function bags can shift demand within the category.

Competitive Rivalry: MODERATE TO HIGH The market is fragmented with many players, but Samsonite's scale creates significant advantages. Competition intensifies at different price points—fierce at the value end, more differentiated at the premium end.

Hamilton Helmer's 7 Powers Framework

Scale Economies: STRONG Samsonite's manufacturing scale, global distribution network, and marketing spend create meaningful cost advantages versus smaller competitors. The company can amortize fixed costs across a much larger revenue base.

Network Effects: WEAK There are no direct network effects in luggage—one person's purchase doesn't make the product more valuable to others.

Counter-Positioning: MODERATE Samsonite's multi-brand, omni-channel strategy is difficult for single-brand competitors to replicate without cannibalizing their own positioning. DTC-only brands like Away face challenges expanding into wholesale without building infrastructure Samsonite already has.

Switching Costs: LOW Consumers face no switching costs between luggage brands. However, brand loyalty based on product quality and familiarity creates some retention.

Branding: STRONG This is Samsonite's primary moat. The Samsonite brand has 115 years of heritage, global recognition, and associations with quality and durability. Tumi has premium positioning in business travel. American Tourister has family-friendly value positioning. These brand assets would take decades and billions to replicate.

Cornered Resource: MODERATE The Tumi brand, in particular, represents a cornered resource—it's the only premium business luggage brand with global scale that Samsonite could acquire. "Rimowa is the only high-end brand remaining in the market, after the acquisition of Tumi by Samsonite."

Process Power: MODERATE Samsonite's manufacturing partnerships, particularly the patented pressure molding technology at the Nashik plant, represent proprietary processes. The company's integration playbook for acquisitions also represents embedded knowledge.

XII. Bull & Bear Cases

The Bull Case

Travel recovery has legs. Global travel continues to grow, driven by rising middle classes in Asia and increased leisure travel among millennials and Gen Z who prioritize experiences over possessions.

Brand moat is deep. Samsonite's three core brands—Samsonite, Tumi, and American Tourister—command positions across the price spectrum that would be nearly impossible to replicate. The company is three times larger than its nearest competitor.

China and India upside. Management believes China revenue could double over the next five years if outbound travel fully recovers. India is already Samsonite's largest manufacturing base and a fast-growing market.

"Management remains cautiously optimistic. They're betting on continued recovery in global travel—especially in China and India. They believe China alone could see revenue double over the next five years. That's a bold statement, but not impossible if outbound travel fully recovers and middle-class consumption rebounds. Tumi is also expanding beyond its traditional luggage focus."

Asset-light model generates cash. With 60% gross margins and an asset-light manufacturing model, Samsonite generates significant free cash flow—US$311.0 million in adjusted free cash flow for 2024. This cash can fund shareholder returns, debt reduction, and growth investments.

Dual listing catalyst. "Assuming a constructive environment, we intend to complete our dual listing in 2026." A US listing could unlock valuation upside by making shares accessible to American investors and improving liquidity.

The Bear Case

Consumer discretionary headwinds. Luggage is a deferrable purchase. In economic downturns, consumers repair existing suitcases or delay purchases. 2024's flat revenue (on constant currency) demonstrates this sensitivity.

DTC competition at the lower end. Brands like Away, Monos, and July continue to capture younger consumers with sleek designs and digital-native marketing. While Samsonite has scale advantages, brand preference among Gen Z is less certain.

China exposure is a double-edged sword. The company is heavily exposed to Chinese consumer spending, which remains sluggish. Geopolitical tensions between the US and China could affect both supply chains and demand.

Tariff and trade policy risk. "These ties are also expected to worsen under a Donald Trump administration, with Trump having recently imposed a 20% trade tariff on China." With 84% of manufacturing in China, tariff exposure is significant.

Commodity luggage pricing pressure. At the value end of the market, price competition from unbranded and private-label products is intense. American Tourister's 6.1% sales decline in 2024 reflects this pressure.

Myth vs. Reality

| Myth | Reality |

|---|---|

| "Samsonite is just a luggage company" | It's a multi-brand lifestyle platform spanning luggage, business bags, outdoor gear, and accessories across 8 major brands |

| "DTC brands like Away are disrupting Samsonite" | Away raised $156M in VC but still captures a tiny fraction of the $174B market; Samsonite's scale and distribution moat remain formidable |

| "The Hong Kong listing was a mistake" | Asia generates higher EBITDA margins than any other region; the listing provided access to capital markets aligned with growth strategy |

| "Premium luggage is recession-proof" | Tumi saw a 0.8% decline in 2024 as premium discretionary spending slowed; no segment is immune to economic cycles |

XIII. Key Performance Indicators (KPIs) to Watch

For investors tracking Samsonite's ongoing performance, two metrics stand out as particularly revealing:

1. Constant Currency Net Sales Growth

The most important metric for assessing Samsonite's underlying business health is constant currency net sales growth. Currency fluctuations can mask or amplify reported performance—the company operates in 40+ currencies. Constant currency growth isolates the actual business momentum from foreign exchange noise.

In 2024, reported net sales declined 2.5% but were "approximately flat on a constant currency basis." This distinction matters: flat constant currency growth against a strong 2023 base, during a year of consumer caution, suggests the franchise is stable even if not growing.

2. Adjusted EBITDA Margin

Adjusted EBITDA margin reveals operational efficiency and pricing power. Samsonite achieved 19.0% adjusted EBITDA margin in 2024, with Q4 reaching a record 20.7%. These margins are high for a consumer goods company and reflect the asset-light model, brand pricing power, and cost discipline.

Margin expansion during a flat-revenue year demonstrates management's ability to protect profitability even in challenging conditions. Margin compression, conversely, would signal competitive pressure or cost inflation that the company can't pass through to consumers.

XIV. Material Risks & Regulatory Considerations

Trade Policy: With 84% of manufacturing sourced from China, Samsonite faces material tariff exposure. The company is pursuing a "China Plus One" strategy, expanding production in India, but significant supply chain shifts take years to complete.

Hong Kong Listing Dynamics: Samsonite was among the foreign luxury and leisure brands to have flocked to Hong Kong for initial public offerings around 2011, lured by rapid growth in China's economy and private consumption back then. But recent years of slowdown in the world's second largest economy—with few if any signs of a turnaround soon—coupled with Hong Kong's sagging stock market have encouraged them to contemplate options elsewhere. The dual listing strategy addresses this, but execution risk remains.

Debt Position: As of December 31, 2024, the Company had US$676.3 million in cash and cash equivalents and outstanding financial debt of US$1,778.9 million, resulting in a net debt position of US$1,102.5 million. While manageable relative to cash flows, this debt load constrains flexibility and creates refinancing risk.

Consumer Discretionary Cyclicality: Luggage purchases are deferrable. In recessions, the luggage industry typically contracts faster than GDP. The COVID-19 experience—57.5% revenue decline in 2020—demonstrates extreme downside scenarios, though the recovery also demonstrated resilience.

XV. Conclusion: The Enduring Journey

Samsonite's story spans three centuries: founded in the early 1900s, turbulent through the late 1900s, reborn in the 2000s. The company that Jesse Shwayder started with $3,500 and the Golden Rule is now a $3.6 billion global enterprise.

What makes Samsonite's story remarkable isn't just survival—plenty of companies survive. It's the ability to reinvent while preserving what matters. The core brand promise Jesse Shwayder established in 1910—durable, quality luggage you can trust—remains the foundation of the business. But everything else has changed: manufacturing, distribution, geography, portfolio, ownership.

The transformation under CVC and subsequent public ownership demonstrates what's possible when private equity approaches a consumer brand as a business to build rather than assets to strip. Tim Parker's turnaround, the Hong Kong IPO, the acquisition spree culminating in Tumi, the COVID survival, and now the dual listing strategy—each chapter built on the one before.

"Even after 18 years, I'm still excited about this business and its potential. It's a company I love, with hard-working teams around the world, iconic brands and an industry tied to such a fun part of our lives—travel!"

The Company continues to follow its time-honored guiding principle: "Do unto others as you would have them do unto you."

Jesse Shwayder would recognize that Golden Rule. And he might be surprised to see his Denver trunk company, 115 years later, as the world's largest luggage maker, trading on the Hong Kong Stock Exchange, preparing for a US listing, manufacturing in India, and selling to travelers on every continent.

The journey continues.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube