Xero: The Cloud Accounting Challenger from New Zealand

I. Introduction: A Small Country's Big Bet on Cloud Accounting

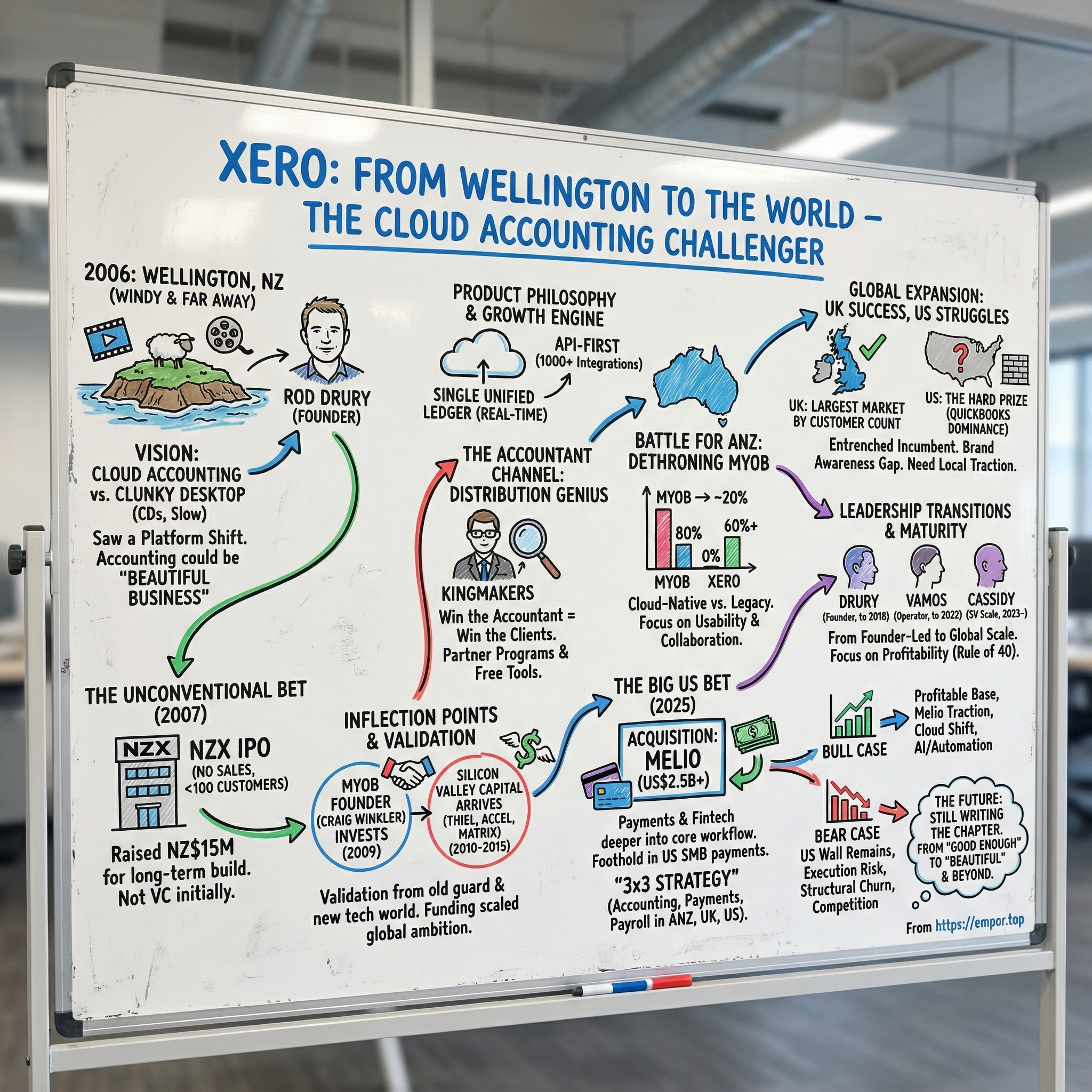

In 2006, a serial entrepreneur on the far edge of the South Pacific made a bet that looked, to most people, completely unreasonable.

Rod Drury was in Wellington, New Zealand—a city better known for its wind and film than for minting global software giants. He looked at the desktop accounting programs small businesses were stuck with—slow, clunky, installed from CDs, and allergic to change—and he didn’t just see a boring category. He saw a once-in-a-generation platform shift.

That year, Drury and Hamish Edwards co-founded Xero in Wellington. And then Drury did something that almost no startup founder would do, especially not with Silicon Valley as the default dream destination: he took the company public in 2007 on the New Zealand Stock Exchange.

Here’s what made it wild. Xero had fewer than 100 customers. It had no sales.

In an era when the startup playbook was all about pitching venture capital firms and chasing a US-style exit, Drury went to public-market investors on a small exchange in a small country. Not because it was flashy—but because he needed real money to build a real product, and New Zealand’s venture market simply wasn’t big enough.

What he did have was conviction: that cloud computing would fundamentally change how small businesses ran their books, and that the first company to build a great cloud accounting platform could ride that wave across the world.

Nearly two decades later, the size of that bet is hard to ignore. By December 2025, Xero’s market cap sat at A$20.01 billion, making it the world’s 1571st most valuable company by market data. From a modest base in Wellington, it grew into a global cloud accounting platform used by millions of small businesses and the accountants who advise them, across more than 180 countries.

At its core, Xero is accounting software for small to medium-sized businesses, freelancers, and accounting practices—built to automate the painful parts of finance and make the rest feel less like punishment. It started as an antidote to traditional accounting systems, and it turned into a category leader in places like Australia, New Zealand, and the United Kingdom.

But this isn’t just a story about being early to the cloud. It’s a story about turning a disadvantage—being far from the world’s tech capitals—into a different kind of edge. It’s a story about distribution, about product philosophy, and about how you compete with incumbents who already sit on almost every desk.

Because while Xero has won big in several markets, the largest prize is still the hardest: North America, where entrenched players remain stubbornly dominant.

So the real questions behind Xero’s rise are the ones every challenger eventually faces. How do you build software people actually want to use in a category most people dread? How do you win when the buyer and the user aren’t always the same person? And when a founder eventually steps aside, can a company keep its identity—and its momentum?

To answer those, we start where we should: with the founder who decided accounting could be different.

II. The Founder: Rod Drury's Origin Story

Picture Hawke’s Bay, New Zealand, in the early 1980s. The personal computer revolution is kicking off half a world away in California. But here on the North Island’s east coast, life still revolves around sheep, orchards, and vineyards—not silicon and software.

Rod Drury grew up in that world: the son of a tradesman and an executive assistant, raised in Taradale, near Napier. He is reported to have Māori heritage, with his father tracing lineage to Ngāi Tahu. He attended Napier Boys’ High School, where, by his own account, he first fell into computer programming—then went on to study commerce and administration at Victoria University of Wellington.

What’s striking is the pairing. In high school, Drury didn’t just get hooked on coding. He also learned accounting. Programming and double-entry bookkeeping—two subjects most teenagers would run from—became his favorite things. And they didn’t feel like separate interests. They felt like a combined superpower: software that could make money move.

But before Drury could become a founder known for selling a vision—of products, of the future, of what “cloud” could mean—he had to beat something far more personal.

In his early 20s, he stuttered so severely that speaking on the phone was a struggle. Around age 27, he took a smooth speech course and overcame it. Drury has said that getting past the stutter was crucial to starting Xero.

That detail matters because so much of what comes later—raising money, recruiting talent, convincing accountants, standing on stages and pitching a brand-new way to do the most dreaded task in small business—requires a founder who can communicate. Xero wasn’t built by a quiet technical genius shipping code in the corner. It was built by someone who would eventually have to lead out loud.

Drury later described the early shape of his career like this:

"I got into computer programming at school, and I think coming from a small set of rocks in the South Pacific, being able to build something with your brain, and that would sell while you're sleeping, always really appealed to me. My first job was at Arthur Young, before the merger with Ernst & Young, which is now EY, so I did auditing for my first year, then talked my way into the IT consulting group. I really came up on the Microsoft side of the fence."

That first job—Arthur Young, pre-EY—turned out to be perfect training for what he’d build later. Drury started in auditing, then moved himself into IT consulting. In the early 1990s, that meant living inside financial systems: how the numbers flow, where controls break, how messy reality looks compared to a clean ledger. He got a front-row seat to how big organizations ran finance—and just how little the tooling and thinking worked for everyone else.

Then he did what founders do: he left.

In 1995, Drury established Glazier Systems, a New Zealand software development and consulting company. In 1999, it was acquired by Advantage Group for approximately $7.5 million. That early exit gave him two things every future entrepreneur needs: credibility and the confidence that he could build something real, then sell it.

He kept going. Drury subsequently co-founded Context Connect, and then founded AfterMail, serving as CEO. AfterMail—an email archiving company—was acquired by Quest Software. The sale, reported at US$45 million in 2006, was a major milestone in his run as a serial entrepreneur.

AfterMail also gave Drury something else: the freedom to choose his next problem. He didn’t have to start Xero. He got to.

By the time Xero was forming, Drury was already being recognized at home. He won Hi-Tech New Zealand’s “Entrepreneur of the Year” award in 2006 and 2007. In 2008, he was named an Honorary Fellow of the New Zealand Computer Society—only the 21st person to receive the title in the Society’s 48-year history at that time. Later honors followed: NZ Herald Business Leader of the Year in 2012, and Ernst & Young Entrepreneur of the Year the next year. In 2025, he was inducted into the New Zealand Business Hall of Fame.

The awards tell you he was successful. But they don’t tell you why Xero happened.

The real setup is simpler: a founder with deep exposure to financial systems, a lifelong obsession with both accounting and software, and the hard-won ability to persuade people—looking at a category everyone hated, right as cloud computing was about to change the rules.

III. The Genesis: Why Accounting Software?

To understand why Rod Drury bet his next act on accounting software—one of the least glamorous categories in tech—you have to start with what he’d spent his career staring at: how money actually moves through a business, and how painfully the tools lagged behind reality.

Back at Arthur Young, before it became EY, Drury lived in financial systems first as an auditor, then as an IT consultant implementing them. He learned the mechanics: ledgers, controls, integrations, the whole plumbing. But he also learned the uncomfortable truth: the systems were built for large organizations with finance teams, not for the vast majority of businesses that were just trying to survive.

For small businesses, bookkeeping wasn’t “process.” It was dread. And the software didn’t help. It was designed by accountants for accountants, stuffed with jargon, and optimized for correctness over comprehension. If you were a florist, a plumber, or a freelance designer, you weren’t looking for a lecture on debits and credits. You wanted to know what you owed, who owed you, and whether you were actually making any money.

Then cloud computing started to feel real—not as a buzzword, but as a new default. And Drury saw an opening that incumbents either didn’t believe in or didn’t want to chase: accounting delivered as a service, always on, always current, accessible from anywhere. No CDs. No manual upgrades. No “send me your backup file.” Just live data.

He captured the ambition in a blunt line: "SMBs are the biggest monetization opportunity on the web." In other words, this wasn’t a niche. Small businesses were everywhere, and they all had the same recurring need: track income and expenses, invoice customers, pay bills, reconcile bank transactions, and eventually hand everything to an accountant or the tax office. The demand was massive. The product experience, in 2006, was almost universally miserable.

And the incumbents looked entrenched. MYOB owned Australia and New Zealand with desktop software that had become the default. Sage dominated much of the UK with similarly dated tools. In the US, Intuit’s QuickBooks was the standard—less because people loved it, more because it was what everyone used.

But Drury’s key insight wasn’t just “put the same software in a browser.” The cloud changed the job the software could do. Desktop accounting meant installs, patches, backups, and being tied to one machine. Cloud accounting meant the books could be shared in real time between business owner and accountant. It meant automatic updates. It meant always-on access. And most importantly, it made “live” possible—like bank feeds that could pull transactions directly into the ledger instead of forcing someone to retype them line by line.

That’s the moment Xero starts to make sense: not as accounting software with a fresh coat of paint, but as an attempt to rebuild the category around what the internet made possible.

And then Drury layered on the thing almost no one in that industry took seriously: design. He believed accounting software didn’t have to look like it was built in the mid-90s. It didn’t have to speak like an exam prep book. It could be intuitive. It could be approachable. It could even be, in his framing, beautiful.

That belief—cloud plus usability—became the foundation of Xero’s identity. And it set up the next, far more unconventional move: how he decided to fund it.

IV. Founding Xero: The Unconventional Launch

In 2006, Rod Drury and Hamish Edwards founded Xero in Wellington—where Xero Limited’s headquarters still sit today. At first, it didn’t even have the name we know. The working title was Accounting 2.0.

That label was a perfect artifact of the era: peak Web 2.0, when startups signaled “the future” by slapping “2.0” on the front door. The name didn’t last—Xero was shorter, sharper, and implied a clean break from the old world—but the intent was obvious. This wasn’t going to be a slightly better version of desktop bookkeeping. Drury wanted a reset.

What really separated Xero from the usual startup story wasn’t the logo. It was the financing.

Instead of doing the standard early-stage venture capital round, Drury decided to take Xero public—almost immediately.

The logic was bluntly practical. New Zealand’s venture market in 2006 was small. The biggest rounds were typically only a couple million dollars. But Drury’s plan required far more than a scrappy team and a few laptops. Building a serious accounting platform meant hiring engineers, testers, designers, sales, and support. He estimated a team of around 50 people would cost roughly half a million dollars a month. Raising NZ$2–3 million at a time wouldn’t build a product like this; it would just buy a little time.

So, in June 2007—despite having fewer than 100 customers and no sales—Xero listed on the New Zealand Stock Exchange. The IPO raised NZ$15 million. The stock jumped about 15% on its first day, but the bigger story was what that public-market structure gave Drury: room to think long-term. Without the typical venture timeline and exit pressure, he could keep building, keep iterating, and keep investing in the product before the market fully caught up.

And while the funding move grabbed headlines, Xero’s early technical decisions mattered just as much. During development, Drury made the expensive call to rebuild the platform on Microsoft’s .NET framework to ensure it could scale. It wasn’t a minor refactor—it meant throwing away work and starting over. But the bet was straightforward: if Xero was going to win, it couldn’t just be cloud-based. It had to be built for millions of businesses, not thousands.

Back home, the move changed more than Xero’s prospects. It helped legitimize SaaS itself inside New Zealand’s tech scene. Grant Ryan of Ngāi Tahu put it plainly: “We don't have to explain software-as-service to the New Zealand market because of Xero. Rod has helped educate the market, and that has enabled us to get some resource to have a good hard go at it.” Drury, for his part, framed the IPO as a personal milestone as much as a strategic one: “When I was in my 20s I used to read all the Silicon Valley books and one of the things that got drummed into me was that as a business person, especially in the technology space, the ultimate was always to take a company public and do an IPO. It's been incredibly satisfying, and I don't think I would ever have been fulfilled if I hadn't done it."

As Xero grew beyond its home market, its listing followed. It added a listing on the Australian Securities Exchange on November 8, 2012—accessing a deeper pool of capital and a larger investor base. And in 2018, it made the shift official: Xero transitioned to a sole ASX listing on February 5, 2018, delisting from the NZX days earlier.

That arc—NZX first, then ASX, then ASX only—mirrored the company’s trajectory: from a Wellington startup with an audacious idea, to an Australia–New Zealand contender, and eventually to a business with global ambitions that needed global-scale funding to match.

V. Inflection Point #1: The MYOB Founder Invests

In 2009, Xero hit an inflection point that mattered for reasons far bigger than the number on the check.

That year, Xero received NZ$23 million of funding led by Craig Winkler—the founder of MYOB.

It’s hard to overstate how unusual that was. MYOB was the incumbent giant in Australia and New Zealand. Winkler had built it into the default choice for businesses and accountants across the region. If anyone had both the incentive and the insight to keep backing the old world, it was him.

Instead, he backed the upstart.

This wasn’t just “smart money.” It was the ultimate form of category validation: the person who understood ANZ accounting software better than almost anyone was effectively saying the cloud transition was real, and Xero was the team most likely to capitalize on it.

For the market, it landed like a quiet but decisive signal. If the founder of the champion believed the challenger had the momentum, it forced everyone else—investors, accountants, partners—to look again at what was happening.

And the capital had real impact. The funding gave Xero more runway to push the product forward and invest in the ecosystem it would need to win. Just as valuable, it brought proximity to someone with deep knowledge of how accountants influenced purchasing decisions and where the incumbent’s weak spots were.

Xero still had a long way to go. But after 2009, it no longer looked like a clever Wellington startup with a contrarian idea. It looked like a company the old guard was taking seriously—even, in this case, financing.

VI. Inflection Point #2: Peter Thiel & Silicon Valley Capital Arrives

If Craig Winkler’s check was validation from the heart of the accounting industry, the next wave of capital was validation from somewhere else entirely: Silicon Valley.

In 2010, Peter Thiel’s Valar Ventures invested an additional NZ$4 million into Xero. Two years later, Valar followed on with another US$16.6 million in February 2012. Then, in November 2012, Xero raised $49 million in a round led by the same cast of characters, with major participation from Thiel and Matrix Capital.

Thiel isn’t just famous. He’s famous for being early, and for being willing to look “off-map.” As PayPal’s co-founder and Facebook’s first outside investor, he had already built a reputation for betting on category shifts before they became consensus.

And Xero fit that pattern. It was a company from New Zealand—essentially the farthest possible distance from Sand Hill Road—building in a category most venture investors considered boring. But Valar and its co-investors saw the upside hiding in plain sight: small-business accounting was massive, fragmented, and overdue for a platform transition. If cloud was the reset, then the winner wouldn’t just build a product. They’d inherit an industry.

By May 2013, Xero had raised more than $100 million at a valuation of approximately $1.4 billion on the NZE. And it wasn’t done. In October 2013, it raised an additional NZ$180 million from Thiel and Matrix, pushing total funding to more than $230 million.

Zoom out and that’s the remarkable part: a Wellington-based company reaching a unicorn valuation at a time when “unicorn” still actually meant something—before the mid-2010s boom made billion-dollar price tags feel routine.

The capital kept stacking. On 25 February 2015, Xero raised another $100 million from Accel, plus $10.8 million from Matrix Capital.

This wasn’t just about having a bigger war chest. These names brought a different kind of leverage: credibility outside ANZ, relationships in the US, and the kind of investor network that can accelerate partnerships and hiring when you’re trying to go global.

Then, in October 2018, Xero announced a settlement of US$300 million in convertible notes—more than had previously been raised by a New Zealand or Australian company not listed in the United States.

Put it all together and the funding story tracks the company’s ambition. Xero started with a small-country IPO because it had to. Then it won an endorsement from the founder of its biggest regional rival. And now it had the backing of Thiel, Accel, and Matrix—capital sources that don’t show up unless the opportunity is big enough to matter on a world scale.

Xero’s trajectory also became a proof point in its home region: it was founded in 2006 and scaled globally through competitive differentiation and private investment, rather than depending on core government grants. By 2023, that approach had helped it expand to over 4 million subscribers across 180 countries.

VII. The Product Philosophy: "Beautiful Business"

Walk into a small business that runs on Xero and you’ll often notice something that used to be unthinkable in this category: people don’t actively resent their accounting software. For decades, “necessary evil” was basically the product strategy. Xero decided to try something else.

Under the hood, the core idea is straightforward but powerful. Xero runs on a single unified ledger, so everyone—business owners, bookkeepers, accountants—works from the same set of books, from anywhere, on any operating system. On top of that, it delivers the everyday mechanics a small business actually needs: automatic bank feeds, invoicing, accounts payable, expense claims, fixed asset depreciation, purchase orders, and bank reconciliations.

Today, those sound like table stakes. In 2007, in the world of desktop software and emailed backup files, they felt like a different era. A shared ledger meant a business owner in Sydney could log in and see what their bookkeeper entered that morning. Bank feeds cut out the soul-crushing routine of typing every transaction by hand. And automated reconciliation—using machine learning to suggest matches between bank transactions and the ledger—pushed the product toward something closer to “assistive” software than a digital spreadsheet.

But the feature list was never the whole point. The real differentiator was the philosophy: make accounting software that feels modern, approachable, and even pleasant to use.

That’s what Xero meant by its tagline, “Beautiful business.” The interface leaned into clean design and intuitive navigation, deliberately avoiding the clutter and intimidation factor that defined legacy accounting tools.

And then there was the language. Xero made a conscious choice to speak human instead of speaking accountant. Traditional products were full of terms like debits, credits, journals, and general ledgers—perfectly clear if you’re a CPA, and completely alien if you run a café. Xero reframed those concepts into plain-English prompts like “invoices owed” and “bills you need to pay.”

That might sound cosmetic. It wasn’t. It was a strategic decision about who the software was for. By reducing the intimidation, Xero made it plausible for business owners to use the product directly, not just hand everything to their accountant and hope for the best.

The other foundational choice was even more forward-looking: from launch in 2007, Xero built the platform around its API. At the time, that was a radical posture—more like a platform company than a packaged software vendor. But it laid the groundwork for what became one of Xero’s biggest long-term advantages: a huge ecosystem of third-party apps, where Xero competes with Intuit’s QuickBooks for the largest footprint.

That API-first architecture turned Xero into the financial hub for a business’s other tools. It’s a big reason Xero has been especially popular in industries like retail, hospitality, eCommerce, consulting, and professional services—places where point-of-sale systems, inventory tools, payroll providers, and expense apps all need to talk to the books.

By 2025, Xero integrated with over 1,000 third-party business applications, spanning everything from payments and POS to inventory management and payroll.

And once you have that, you get the compounding effect. More integrations make Xero more valuable, which attracts more customers, which attracts more developers, which creates even more integrations. It’s a flywheel that doesn’t just improve the product—it makes the platform harder and harder to displace.

VIII. The Accountant Channel: Distribution Genius

If there’s one insight that explains Xero’s rise better than any feature, it’s this: small businesses might use accounting software, but accountants and bookkeepers decide what gets used.

Most owners don’t run a full bake-off. They don’t spend weekends comparing ledgers and bank reconciliation workflows. They ask a trusted advisor, “What should I be on?” And then they follow the recommendation—because the accountant is the one who has to live with the books at year-end.

That makes accountants the kingmakers. Win the accountant, and you don’t just win one customer. You win an entire book of clients.

By 2025, that preference showed up clearly in Australia: Xero captured 55.14% of accountant click share, versus 17.15% for MYOB and 8.03% for QuickBooks. That isn’t just share. It’s default behavior. And default behavior is what turns a product into a category standard.

Xero earned that position by treating accountants as a first-class customer, not an afterthought. It built partner programs, practice-specific tools, and incentives that made it easy—and economically rational—for accountants to standardize on Xero and bring clients along.

The partner toolkit was designed to make a practice run smoother. Xero HQ centralized client data and dashboards. Xero Practice Manager handled workflows, time tracking, and billing. Xero Workpapers streamlined the busywork of preparing financial statements and tax returns.

Then came the kicker: partner accountants received free subscriptions to Xero’s premium plan. That removed the friction of “try it later.” If you’re an accountant, you can live in Xero every day inside your own practice. And once you’re fluent, your recommendations tend to follow.

The flywheel is powerful and self-reinforcing. Each accountant who adopts Xero can bring along dozens—or hundreds—of small business clients. Those clients, in turn, prefer working with accountants who already know Xero. Which nudges more firms to learn it. Which brings in more clients. And around it goes.

It also solves a brutal go-to-market problem. Selling directly to millions of small businesses is expensive and noisy. Selling to a smaller number of influential accountants—who then effectively distribute the product for you—turns growth into a channel strategy. And for Xero, it became one of the most defensible advantages in the entire business.

IX. The Battle for ANZ: Dethroning MYOB

Australia and New Zealand were Xero’s first true proving ground. And the company it had to beat wasn’t some sleepy niche vendor—it was the default choice for an entire region.

For decades, that default was MYOB. Founded in 1991, MYOB (Mind Your Own Business) built a franchise on desktop software tailored to the realities of Australian and New Zealand accounting: GST, BAS statements, superannuation, and all the local complexity that generic software tends to get wrong. For a long time, if you ran a business in ANZ and you needed accounting software, the answer was basically pre-selected.

A decade ago, MYOB reportedly held more than 80% market share. It looked untouchable.

Fast forward to 2025, and the map has flipped. Xero holds over 60% market share in Australia’s online accounting market, while MYOB sits around 20–25%. That’s not a gradual shift. That’s a dethroning.

So what changed?

First, the platform shift that Drury bet on actually arrived—and MYOB got caught in the classic innovator’s dilemma. Its desktop products weren’t just successful; they were the business. Moving customers to the cloud risked cannibalizing lucrative legacy revenue. But staying put meant letting a cloud-native competitor define the future. Xero, by contrast, didn’t have to manage that tradeoff. It was born in the cloud, and it could push forward without worrying about protecting an installed base.

Second, focus mattered. MYOB had to serve multiple segments with a portfolio of products. Xero concentrated on one thing: cloud accounting for small businesses, built to feel modern and easy. That clarity showed up in iteration speed, in product cohesion, and especially in the accountant channel. When the books live online, collaboration between accountant and client becomes the core workflow—exactly where Xero wanted to win.

By 2025, the preference signal was hard to ignore. Xero captured 55.14% of accountant click share in Australia, versus 17.15% for MYOB (and 8.03% for QuickBooks). That’s what it looks like when the profession starts standardizing.

MYOB didn’t disappear, and it still fit certain needs—particularly for businesses with more complex requirements or teams that preferred more traditional approaches. But for the center of the market, Xero’s combination of usability, cloud-first collaboration, and ecosystem depth became the new default.

And that ANZ victory mattered beyond bragging rights. It gave Xero something every global challenger needs: a strong home base. Dominance in a developed market creates a more predictable foundation—one that can help fund expansion without betting the entire company on the next beachhead.

It also raised the bar for anyone else trying to enter. With accountants trained on Xero, integrations built around Xero, and millions of businesses already on the platform, switching stopped being a simple feature comparison. The market started to lock in.

Which set up Xero’s next chapter: taking what worked in ANZ and seeing whether it could travel—first to the UK, and then to the most difficult market of all.

X. Global Expansion: UK Success, US Struggles

With ANZ largely won, Xero went looking for bigger ponds. The next phase of the story is where you see both sides of the Xero playbook: how powerful it is when the conditions are right, and how stubborn markets can be when they’re not.

The United Kingdom was the obvious next stop. It looked a lot like Australia and New Zealand: a fragmented market, plenty of businesses still running on older desktop systems, and an accounting community open to better ways of working. On top of that, regulatory initiatives like Making Tax Digital created a real tailwind for moving bookkeeping online.

The results followed. By 2017, Xero had more than one million customers globally. The following year, it passed one million subscribers in Australia and New Zealand alone.

And in the UK, it didn’t just show up—it broke through. By customer count, the UK became Xero’s largest market, even surpassing Australia. For a company founded in Wellington, that’s a remarkable outcome: walking into a market with established players like Sage and local QuickBooks offerings, and still carving out the lead.

By the mid-2020s, Xero’s scale started showing up in the financials too. In the year ending 31 March 2025, Xero reported revenue up 23% to NZ$2.1 billion, alongside a 22% increase in adjusted EBITDA to NZ$640.6 million. Free cash flow rose 48% to NZ$506.7 million, lifting free cash flow margin to 24.1% from 20% the prior year. In other words: it wasn’t just growing. It was starting to look like a mature, cash-generating platform.

Then there’s the United States, where the story flips.

In North America, Xero has struggled to build meaningful mindshare. It’s not for lack of effort, and it’s not because the category is small—it’s because the market is effectively owned. Intuit’s QuickBooks is the default, deeply embedded in how American small businesses and accountants operate.

The numbers reflect that reality: QuickBooks holds more than 62% of the SMB accounting software market, while Xero sits under 9%. And QuickBooks’ user base is overwhelmingly concentrated in the US, which is why Intuit pours so much product energy into American payroll, tax, and compliance workflows. For US SMBs, QuickBooks doesn’t feel like “a choice.” It feels like the standard.

That’s the real problem Xero is up against. In ANZ, Xero built the network effects: accountants trained on Xero, firms standardized on Xero, and small businesses followed their advisors. In the US, those same dynamics exist—just pointed at QuickBooks. Accountants know it, clients expect it, and the ecosystem around payroll, tax, compliance, and support is built around it.

So breaking in means doing the hard, unglamorous work: localize the product, deepen accountant relationships, expand integrations, and spend to overcome a brand-awareness gap that compounds over time.

Xero has been grinding on that foundation. Over the past two years, it expanded direct US bank feeds from 20 to more than 700—a big move in a market with over 4,000 financial institutions, each with their own quirks and technical constraints. Improving bank-feed coverage and reliability is essential, because if getting transactions into the ledger is painful, nothing else matters.

But even that kind of infrastructure investment has a ceiling. You can match features. You can close product gaps. What’s harder is matching an incumbent’s installed base and default status without doing something bigger.

Which brings us to Xero’s most significant strategic move in years.

XI. Leadership Transitions: From Founder to Scale

In April 2018, Xero made the transition every founder-led company eventually faces. Steve Vamos was appointed CEO, replacing Rod Drury, who stayed on the board as a non-executive director until 2023.

For Drury, stepping aside was more than a title change. He’d spent 12 years running Xero—taking it from a Wellington idea to a global, multi-billion-dollar public company. Now he was handing the day-to-day over to someone whose job wasn’t to invent the next chapter, but to industrialize it.

A few months before the handoff, in November 2017, Drury sold $95 million worth of Xero shares, leaving him with a 13% holding. He said the sale would help fund “future plans to pursue a range of philanthropic and social endeavours.” In March 2018, he officially stepped down as CEO, remaining involved through the board.

Vamos brought a different profile to the role. With experience at Apple, Microsoft, and ninemsn, he was a professional operator rather than a founder-entrepreneur. His mandate was clear: scale the organization, professionalize how it ran, and keep pushing the global expansion that Drury had set in motion.

Under Vamos, Xero kept growing—but the company also matured. The early startup intensity gave way to tighter processes and governance, the kind you need when you’re running a large public company with global ambitions.

Then, in November 2022, Xero named its next CEO. Sukhinder Singh Cassidy joined and began transitioning into the role, officially commencing as CEO in February 2023. Around that same period, Xero brought in Diya Jolly as Chief Product Officer in 2023, and in April 2024 announced her promotion to Chief Product and Technology Officer.

Cassidy’s arrival marked a new phase for Xero. Where Vamos brought operating discipline from the Australian and broader tech world, Cassidy brought deep Silicon Valley experience—exactly the kind of background that matters if the next big challenge is the US.

Sukhinder Singh Cassidy (born 1970) is a technology executive and entrepreneur. She is the CEO of Xero and the former president of StubHub. Over her career, she has worked across Google, Amazon and Sky UK, Yodlee, and Polyvore.

She was born in Dar es Salaam, Tanzania, to parents of Indian Punjabi Sikh descent. Her family moved to St. Catharines, Ontario, Canada, when she was two, and she grew up in the Niagara Region. She graduated from the University of Western Ontario and earned an honours degree in business administration from the Ivey School of Business in 1992.

In 2003, Singh Cassidy joined Google as the first general manager for Google Local and Maps, and head of content acquisition for Books, Scholar, Shopping and Video. There, she launched Google Local and Maps with product manager Bret Taylor and a team of engineers. In 2004, she became head of Google’s international operations in Asia Pacific and Latin America, became a VP in 2005, and then president of those markets in 2008. She is credited with helping build Google’s presence across 103 countries in Asia Pacific and Latin America.

From 2018 to 2020, as President of StubHub, she oversaw more than US$5 billion in total GMV and its US$4 billion sale in 2020. Before StubHub, she spent seven years in e-commerce, founding video commerce pioneer Joyus and premium talent marketplace theBoardlist. Earlier, she served as the business founder at fintech pioneer Yodlee from 1999 to 2003.

On paper, it was a résumé built for Xero’s moment: global scaling from Google, marketplace dynamics from StubHub, fintech instincts from Yodlee—and, critically, far more direct exposure to the US market than Xero’s prior leadership had.

As Cassidy took the reins, Drury completed his long transition out. In July 2023, he announced he would retire from Xero’s board, ending a 17-year tenure from founding through global scale. The company framed it as the natural next step in a more mature Xero: refreshed oversight, with the founder no longer formally in governance.

And the business didn’t wobble. In the period ended September 30, 2023, Xero’s adjusted EBITDA rose 44% year-over-year, and the share price lifted by a corresponding 44%—a strong signal that the market viewed the leadership change, and the underlying momentum, as real.

Xero also rounded out its executive bench for the next push. Ashley Hansen Grech joined in 2023, after stints at Recharge and Square, and now serves as Chief Revenue Officer, leading global go-to-market functions including sales operations, regional leadership, customer experience, partnerships, and revenue operations. Michael Strickman joined in October 2023 as Chief Marketing Officer. Together, the team has been focused on accelerating innovation and raising Xero’s profile—especially in the US, where brand awareness and distribution have been the hardest parts of the fight.

XII. The 2023 Restructuring: A Pivot to Profitability

When Sukhinder Singh Cassidy took the reins, she ran into the question that eventually confronts every growth-stage SaaS company: how long can you optimize for growth before you have to prove you can generate durable profit?

Xero’s answer came fast.

In March 2023, Cassidy announced the removal of 700–800 roles—about 15% of the company. At the time, Xero reportedly had more than 3.5 million subscribers and roughly 4,500 employees spread across New Zealand, Australia, North America, the UK, and Southeast Asia. The company said it finished the cuts by November 2023, taking headcount down to 4,242.

It was a painful move, but it wasn’t random. Like a lot of tech companies that scaled quickly in the low-interest-rate years, Xero’s cost base had expanded faster than its revenue trajectory could comfortably support. The restructuring forced a reset: fewer bets, more focus, clearer prioritization.

Cassidy framed that focus around three “super jobs”: core accounting, payments, and payroll—concentrated in Xero’s biggest markets: Australia, the UK, and the US. That shift came with more than layoffs. It also meant exiting work that didn’t fit the new center of gravity: divesting from the finance platform Waddle and the project management tool WorkflowMax, and discontinuing Xero Go. As Cassidy put it, “We were over-invested as a company, so we pared back in order to give ourselves room.” And, “The things we're exiting are just trying to bring focus… If we don't buckle down, and at least deliver the core, we risk losing focus.”

That philosophy hardened into what Xero calls its “3x3 strategy”: three core product areas—accounting, payroll, payments—across three priority markets—Australia, the UK, and the US.

The payoff, at least by the metrics public-market SaaS investors like to see, showed up quickly. In May 2024, Xero reported a Rule of 40 outcome of 41.0%, followed by 43.9% in November 2024. Rule of 40 is the shorthand benchmark that adds a SaaS company’s revenue growth rate to its free cash flow margin; crossing 40% is generally seen as a signal you’re balancing growth with profitability instead of choosing one at the expense of the other.

By FY25, Xero reported a Rule of 40 outcome of 44.3%. Cassidy summed it up: “Our FY25 results demonstrate Xero's macro-resilient growth and effective execution of our strategy. Our focus on balanced profitable growth has enabled us to again deliver strong EBITDA growth and a greater than Rule of 40 outcome.”

With that momentum, Xero reaffirmed the aspiration it had outlined in February 2024: to double the size of the business over time while maintaining Rule of 40 or better performance.

It’s a bold target. But it captures exactly what this chapter of Xero is about: staying ambitious—especially on the US opportunity—without losing the financial discipline that public markets now demand.

XIII. Acquisition Strategy: Building vs. Buying

Throughout its history, Xero followed a simple playbook for expanding what the platform could do: build what it must, partner where it makes sense, and buy when speed or control matters.

The “buy” part started early. In July 2011, Xero acquired the Australian online payroll provider Paycycle for a mix of cash and shares totaling NZ$1.9 million, bringing payroll capability closer to the core product. A year later, in July 2012, it acquired Spotlight Workpapers for a mix of cash and shares totaling $800,000—leaning into the accountant workflow that had become one of Xero’s biggest distribution advantages.

As the platform scaled, the acquisitions became more strategic. In August 2018, Xero acquired Hubdoc, a data capture application. Later that year, in November 2018, it acquired Instafile, a cloud-based accounts preparation and tax filing application, for £5.25 million. In August 2020, it acquired Waddle, an Australian invoice financing startup, for A$80 million.

Hubdoc, in particular, was an important tell. Data capture—pulling the right details out of bills, receipts, and invoices without a human retyping them—is the raw material of accounting automation. By bringing Hubdoc in-house, Xero wasn’t just adding a feature. It was tightening the loop between “a business spends money” and “the books reflect reality,” while keeping more of that value inside the Xero product instead of letting it leak out to third-party tools.

Then, in September 2024, Xero announced the acquisition of Syft Analytics, a cloud-based reporting, insights, and analytics platform, for up to US$70 million. Syft extended Xero’s reporting depth—less about getting transactions into the ledger, more about turning that ledger into answers. As businesses get used to real-time books, they start asking for real-time insight.

But the acquisition that truly signaled where Xero wanted to go next came in 2025.

In June 2025, Xero announced an agreement to acquire Melio, a New York-based payments provider, for US$2.5 billion in cash and stock, plus up to US$500 million in additional payments over three years. Melio co-founder and CEO Matan Bar was set to lead US operations of the combined business. Xero completed the acquisition on October 15, 2025.

Melio is an SMB bill pay platform that integrates accounting and payments. It focuses on accounts payable workflows for SMBs, accountants, and bookkeepers, offering multiple payment methods and more visibility and control over cash flow. Founded in 2018, Melio had grown to serve 80,000 customers. In FY25 (31 March year end), it processed over US$30 billion in payments, generated US$153 million in revenue, and reported March 2025 annualised revenue of US$187 million.

For Xero, this was a very different kind of bet. At US$2.5 billion, plus potential earnouts, it was vastly larger than anything Xero had done before. And it made the strategic message hard to miss: Xero wasn’t just building “better accounting software.” It was trying to pull payments and fintech deeper into the core workflow.

The logic comes down to what Xero has been missing in the US.

First, a real foothold. Melio’s customer base and payment volume gave Xero meaningful presence in American SMB payments—something that’s hard to build from scratch when an incumbent already owns the default accounting relationship.

Second, embedded payments. If accounting is the system of record, payments are the system of action. Owning bill pay lets Xero weave payments directly into the workflow, rather than relying on integrations that can feel bolted-on.

Third, distribution. Melio partners with institutions like Capital One and Shopify, and with distribution partners like Fiserv, enabling embedded accounts payable products through its syndication model.

And fourth, economics. Payments can generate more revenue per customer than subscription software, which matters in a market where Xero has historically struggled to reach escape velocity.

Xero said the Melio deal was expected to double its 2025 US revenue figures by 2028. It also pointed to the size of the opportunity, noting that accounting and payments are critical needs for American SMBs, and describing the U.S. SMB payment total addressable market as a $29 billion opportunity supported by digitization of accounts payable and rising demand for software that saves time and improves cash-flow management.

Of course, the risk is the part you can’t spreadsheet away. Integrating a US$2.5 billion acquisition while keeping the core product strong is hard. Doing it while trying to crack a US market where QuickBooks remains deeply entrenched is harder.

Still, Cassidy framed it as part of a broader push: “Xero's momentum—particularly in the U.S.—is being driven by strong core fundamentals and strategic investment in our technology. As small businesses face increased external pressures and uncertainty, adoption of cloud accounting and workflow automation for SMBs continues to accelerate,” she said.

XIV. Bull Case vs. Bear Case: Analyzing Xero's Position

After following Xero from a windy corner of Wellington to a global public company—and watching it place its biggest bet yet in the U.S.—it’s worth stepping back and asking the simple question investors always ask: what, exactly, does Xero have going for it now, and what could still go wrong?

One way to pressure-test that is with two classic lenses: Porter’s Five Forces and Hamilton Helmer’s 7 Powers. They’re not perfect, but they force the right kind of clarity.

Porter's Five Forces Analysis

Threat of New Entrants: Low to Moderate. Accounting software looks easy until you try to ship it. A credible platform takes years to build, and every new market adds compliance, payroll, tax rules, and endless edge cases. Then there’s distribution: once accountants standardize, the market gets sticky. That said, a well-funded entrant with a genuinely different approach could still break in.

Bargaining Power of Buyers: Moderate. A single small business doesn’t have much leverage. But collectively, SMBs can and do churn if the software is painful or the price feels unjustified. The accountant channel concentrates power further: one firm’s preference can steer hundreds of clients.

Bargaining Power of Suppliers: Low. Xero’s key “suppliers” are cloud infrastructure (like AWS) and engineering talent. Cloud compute is a competitive market; there are options. Talent is expensive, but it’s broadly available.

Threat of Substitutes: Moderate. For the smallest businesses, spreadsheets are still “good enough.” Over time, AI-driven workflows could reduce the need for traditional accounting interfaces, though that’s still more theory than reality. And some vertical platforms—like e-commerce stacks—can swallow pieces of the accounting workflow even if they don’t replace the general ledger.

Competitive Rivalry: High. This is a knife fight. In the U.S., Intuit’s QuickBooks is the default. In ANZ, MYOB is smaller than it used to be but still present. In the UK, Sage and others keep pressure on pricing, features, and accountant partnerships. The competition isn’t just product—it’s ecosystem, distribution, and mindshare.

Hamilton Helmer's 7 Powers Analysis

Network Effects: Strong in ANZ, Moderate Elsewhere. Xero’s biggest structural advantage comes from accountants: as more businesses use Xero, more accountants learn it; as more accountants learn it, more businesses get recommended onto it. That loop is strongest where Xero already leads (ANZ, UK), and weakest where the loop points at someone else (the U.S.).

Switching Costs: Moderate to High. Nobody “casually” changes their general ledger. Switching means migrating data, retraining staff, redoing workflows, and risking mistakes. That helps retention—but it also makes new customer wins harder and slower.

Scale Economies: Present but Not Decisive. Software benefits from scale, but Intuit has scale too, and often more of it—especially in the U.S. Scale matters, but it’s not an automatic win condition here.

Counter-Positioning: Diminished. Early on, Xero’s cloud-native stance was a real weapon against desktop incumbents. Now nearly everyone has a cloud offering, which blunts that advantage.

Cornered Resource: Limited. Xero doesn’t appear to have a truly exclusive resource—like unique distribution rights, proprietary data no one else can access, or a one-of-one technical moat.

Process Power: Moderate. Xero’s product sensibility and pace of iteration have been real differentiators historically. The challenge is that competitors can copy many product patterns over time.

Brand: Strong in ANZ, Emerging Elsewhere. Xero’s “Beautiful business” positioning has earned genuine affection in its home markets. Replicating that level of brand pull globally—especially in the U.S.—is still unfinished work.

The Bull Case

-

A profitable, defensible base. With dominant share in Australia and a leading position in the UK, Xero has a stable foundation that can fund expansion rather than gamble the company on it.

-

Melio changes the U.S. equation. The acquisition brings payments capability, U.S. customers, and distribution—exactly the ingredients Xero has historically lacked in North America.

-

The cloud shift isn’t over. Even now, a lot of SMBs are still in partial digitization—some cloud tools, some legacy processes. Continued movement toward cloud accounting, plus regulatory pushes toward digital record-keeping, keeps expanding the pie.

-

Evidence of pricing power. Xero has been able to raise prices with limited churn, suggesting customers see enough value to tolerate higher spend.

-

AI and automation as the next step-change. Cassidy has said the company will keep a disciplined approach to capital allocation, with a focus on product development—and specifically further investment in AI built into the software to deliver more capability and flexibility for customers.

The Bear Case

-

The U.S. could remain a brick wall. QuickBooks’ entrenchment is cultural as much as technical. Even with Melio, Xero may struggle to win meaningful market share—and a large acquisition can become a distraction from the core product.

-

Price increases can create fragile growth. Xero’s churn remained low—around 1% monthly when excluding removed idle subscriptions—but price sensitivity in SMB is real. If churn ticks up, growth gets harder quickly.

-

SMB churn is structural. Small businesses fail at higher rates than enterprises, and that baseline churn forces constant investment in marketing and sales just to stay even.

-

Competition keeps getting better funded. Intuit continues to invest heavily in QuickBooks Online. Other large players could push down-market, and the broader category remains crowded and aggressive.

-

Little room for execution mistakes. At current prices, the market is effectively underwriting continued growth and improving margins. If Xero stumbles—on integration, on U.S. traction, or on profitability—public markets can re-rate the story fast.

XV. Key Metrics for Investors

If you’re watching Xero as a long-term story, there are three numbers that tend to tell you what’s really happening beneath the headlines.

1. Average Revenue Per User (ARPU)

Average revenue per user (ARPU) rose 15% to NZ$45.08 (US$26.50). Xero attributed the lift to a better product mix, pricing changes, and continued payments growth.

ARPU is where pricing power and platform expansion show up. When customers adopt more of Xero—payroll, payments, analytics—ARPU climbs. When Xero raises prices and customers stay, ARPU climbs. Over time, steady ARPU growth is one of the cleanest signals that the product is delivering enough value to charge more for it.

2. Net Subscriber Additions (adjusted for idle account removals)

Subscriber growth needs a small asterisk this year. Xero removed 160,000 “long idle subscriptions” in the first half of the financial year, which reduced the headline subscriber count. Excluding that clean-up, the company would have added 414,000 subscribers, or 10% growth.

This metric matters because it’s the engine of everything else. SMBs churn for reasons that have nothing to do with software—businesses close, owners retire, side hustles end—so Xero has to keep winning new customers just to stand still, and then win more to grow. Watching net adds, especially in the UK and the U.S., is one of the best ways to gauge whether the go-to-market motion is actually working.

3. Operating Expense Ratio (Operating Expenses as % of Revenue)

Profitability in SaaS is a story of operating leverage: can the company grow revenue faster than it grows its cost base?

For FY26, Xero expected total operating expenses as a percentage of revenue to be approximately 71.5%, with the ratio higher in the first half than the second. After including Melio, Xero said the outlook improved slightly, and it now expected operating expenses to be around 70.5% of revenue in FY26—driven mostly by efficiencies, with a small benefit from Melio.

The direction here is the point. As Xero scales, this ratio should fall, opening the door to higher margins. If it doesn’t—if operating expenses start taking a bigger bite of revenue—that’s often a sign that competition is forcing more spend, integration is creating drag, or execution is slipping.

XVI. Conclusion: The Road Ahead

Nearly two decades after Rod Drury decided to build “the world’s best accounting engine” from an office in Wellington, Xero stood at another inflection point.

Drury didn’t just found a product. He built a global small-business accounting platform into one of the ASX100’s standout technology stories, a company worth more than A$10 billion at points along the way, employing over 4,000 people across 25-plus locations. Even after stepping back from formal governance, he remained Xero’s largest shareholder.

Along the way, Xero did a few things that are genuinely rare. It dethroned an incumbent in its home market. It made a category people tolerate—barely—feel modern, even enjoyable. It drew backing from some of the most sophisticated technology investors in the world. And it navigated leadership transitions without losing the thread of what made it work in the first place.

In FY25, that thread was captured in the company’s “Win the 3x3” strategy: go deeper in accounting, payroll, and payments, across its three priority markets. As CEO Sukhinder Singh Cassidy put it, “We have achieved this while maintaining strong momentum across our strategic pillars and, importantly, have increased our product velocity to bring more value to customers through our focused 3x3 strategy.”

Still, the hardest part of the map hasn’t changed. The United States—millions of small businesses, a massive opportunity in SMB payments, and an entrenched incumbent—remains both the biggest prize and the stiffest test.

That’s what made Melio so consequential. Cassidy framed it like this: “We’re thrilled to announce we’re acquiring Melio, a leading US B2B payments platform that strongly aligns with our 3x3 strategy and US growth ambitions. Adding Melio’s world-class team, technology platform, and innovative A/P solutions to Xero enables a step change in our North America scale and the potential to help millions of US SMBs and their accountants better manage their cash flow and accounting on one platform.”

It’s an audacious move—one that echoes the original Xero playbook: make the bet before the world agrees it’s safe. It could finally change Xero’s U.S. trajectory. Or it could become an expensive distraction. The next few years will decide which.

Through it all, the idea that launched Xero hasn’t aged: small businesses deserve software that’s clear, intuitive, and actually helps. In an industry that spent decades treating mediocrity as normal, Xero insisted that “good enough” wasn’t good enough.

Drury has always described entrepreneurship less like a single heroic swing and more like accumulation. “Think of entrepreneurship as a series of baby steps,” he said. “You always hear the stories of the person that smacked it out of the park in their 20s, but actually, a far more repeatable process is doing a number of smaller deals, and with each thing, you get more experience, more of your own money, so you can have more of it, and you usually get better ideas, as you gain more experience.”

From a small set of rocks in the South Pacific, Xero helped change how millions of businesses manage their money. And after everything it’s already pulled off, the most important chapter may still be the one it’s writing now.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube