Türkiye Sigorta: The Consolidation of a Nation's Risk

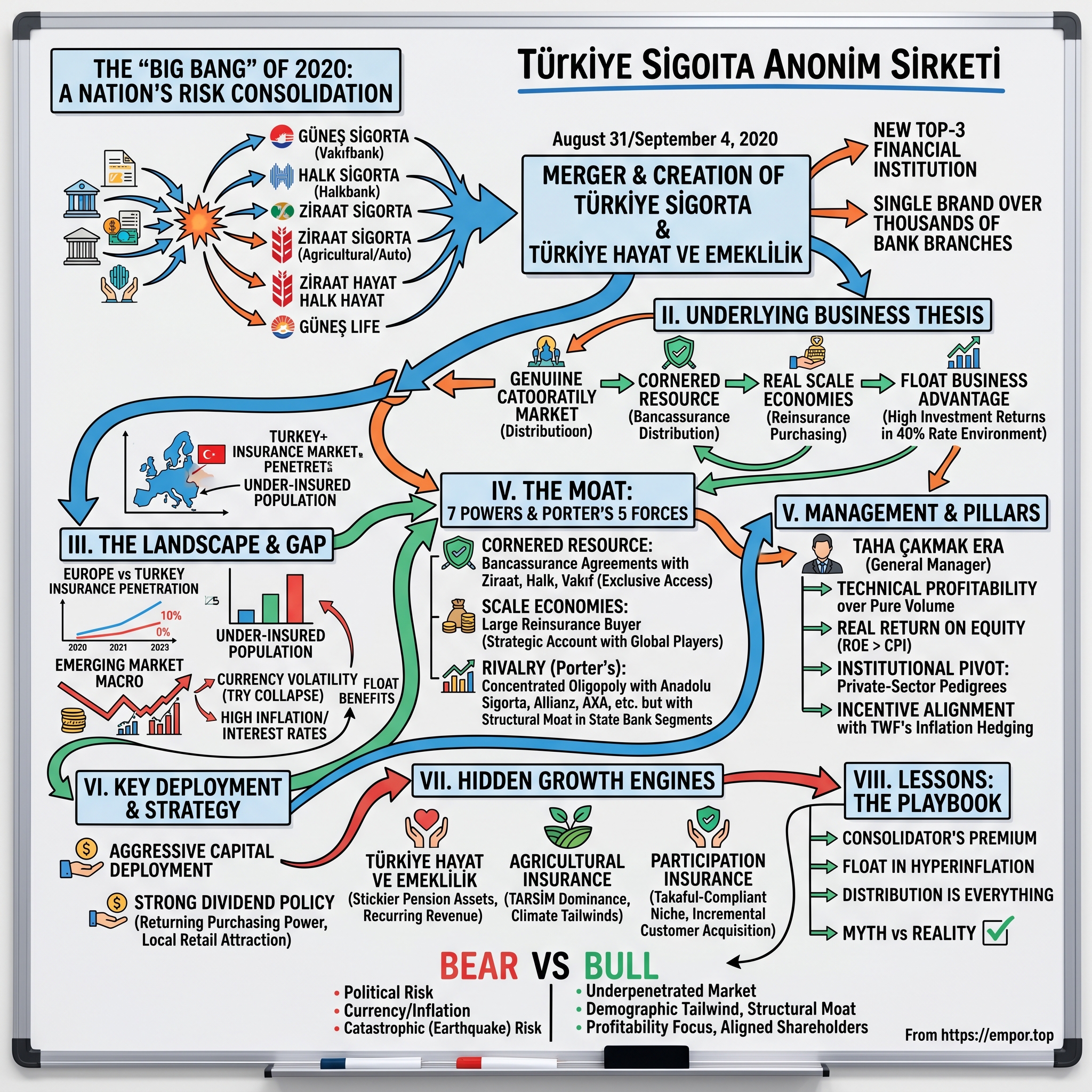

I. Introduction: The "Big Bang" of 2020

Picture Ankara in late August 2020. The city is half-empty, flags snap in the dry Anatolian wind, and most of the world is still arguing about masks and lockdowns. Inside the offices of the Türkiye Wealth Fund—the sovereign holding vehicle the Erdoğan government had quietly been loading with prize state assets since 2016—a handful of bureaucrats, lawyers, and Istanbul-trained insurance actuaries are preparing to do something that, in any Western economy, would have taken a decade and a small army of investment bankers.

They are preparing to switch off six companies on a Friday and switch on one on a Monday.

The six were not obscure outfits. Güneş Sigorta, the former insurance arm of Vakıfbank. Halk Sigorta, the property-and-casualty wing of Halkbank. Ziraat Sigorta, the agricultural and auto arm bolted onto Turkey's oldest state-owned lender. And three life-and-pension companies—Ziraat Hayat ve Emeklilik, Halk Hayat ve Emeklilik, and Güneş's own life entity—which had spent years chasing overlapping customers through the same branch networks they all, ultimately, belonged to. On August 31, 2020, the three non-life companies were merged into Türkiye Sigorta. On September 4, 2020, the three life companies were merged into Türkiye Hayat ve Emeklilik. By the following Monday morning, a single brand was hanging over thousands of bank branches from Diyarbakır to Edirne, and a new top-three financial institution had been born with a stroke of a regulator's pen.

The thesis of this episode is simple but under-appreciated. On the surface, Türkiye Sigorta looks like the sort of state-assembled utility that Western investors reflexively discount—a bloated champion stitched together for political reasons, exposed to a currency that has, in the last five years, done things to purchasing power that most insurance textbooks do not contemplate. But underneath the noise sits something much more interesting: a company with a genuine Hamilton Helmer-style Cornered Resource in bancassurance distribution, real Scale Economies in reinsurance purchasing, a float business that behaves very differently in a 40% policy-rate environment than it does in a 2% one, and a capital-return policy that, denominated in hard currency, has quietly transferred enormous value to shareholders while the lira has collapsed around it.

To understand how all of that came to be, the story has to start not in 2020, but with the conditions that made the "Big Bang" necessary. It starts with a country that was chronically under-insured, a banking system whose distribution rails were state-owned, and a sovereign wealth fund that had decided, quite explicitly, that six small swords were less useful than one massive shield.

II. The Landscape: Insurance in an Emerging Market

To feel the commercial logic of Türkiye Sigorta, you first have to feel the gap. In Germany, insurance premiums run in the neighborhood of seven percent of GDP. In France, a little higher. In the United Kingdom, higher still. In Turkey, for most of the 2010s, the number hovered somewhere between one and a half and two percent, and even that headline figure flattered reality because so much of it was compulsory third-party motor coverage that consumers resented rather than valued. Life insurance penetration was, by European standards, almost a rounding error. Private pension assets, despite a decade of government prodding, were a fraction of what a country of eighty-five million people with a median age in the early thirties should have produced.

There is a standard emerging-markets explanation for this, and it is half right. Cultural factors matter. Extended families self-insure. A strong social safety net in healthcare removes one of the largest Western insurance categories from the private sector almost entirely. Mortgage penetration is low, so the home-insurance flywheel that drives so much Western premium growth never got to spin properly. And there is the uncomfortable fact that Turkish consumers have spent most of the last twenty years watching the lira lose value faster than almost any insurance product could promise to replace.

But the other half of the explanation is distribution. In a country where trust in financial institutions has historically tracked closely to trust in the state, and where the state-owned banks are still, unambiguously, the banks that most of the population uses for their first account, their first mortgage, and their first tractor loan, the natural point of sale for insurance is the bank branch. And until 2020, that point of sale was fragmented, fought over, and weirdly inefficient. A farmer walking into a Ziraat Bank branch to refinance equipment might be cross-sold a Ziraat Sigorta policy. A civil servant walking into a Halkbank branch the same afternoon would be offered Halk Sigorta. A small-business owner at Vakıfbank would be funneled toward Güneş. Three state-backed insurers, competing for the same ultimate shareholder's customers, burning duplicate customer-acquisition cost on the same captive base.

Layered on top of all that was the macro backdrop that every emerging-market investor now knows by heart. The lira, which had traded around three to the dollar in 2016, crossed seven in 2020, ten in 2021, nineteen by the end of 2022, and pushed well past thirty in the years that followed. Inflation, which the central bank officially admitted was in the mid-80s in late 2022, functionally ran in triple digits on many consumer goods. Interest rates swung violently—cut in defiance of orthodoxy under one governor, then raised in apology under another, with the policy rate climbing above forty percent in 2024 as the new economic team under Mehmet Şimşek attempted to re-anchor expectations.

For most businesses, that environment is an existential threat. For an insurance company with a large investment portfolio and short-tail liabilities, it can be a quiet bonanza. Insurance, famously, is a float business: premiums come in up front, claims pay out later, and the money sits on the balance sheet in the meantime earning whatever the risk-free rate will bear. When that risk-free rate is forty percent and the regulator forces most of the portfolio into lira-denominated government paper, the arithmetic of the investment return starts to swamp the arithmetic of the underwriting result. The underwriting becomes, in effect, a ticket to play the yield game. And the bigger the float, the bigger the ticket.

Which brings us to the Türkiye Wealth Fund, and the decision that triggered everything that follows. By 2019, the TWF—the sovereign holding company into which the government had deposited its stakes in Ziraat Bank, Halkbank, Turkish Airlines, BOTAŞ, and dozens of other crown jewels—had concluded that the fragmented state insurance footprint was leaking value. Margins were mediocre. Reinsurance was being purchased six different ways by six different treasuries. IT stacks were duplicated. Brands were stepping on each other. And none of the individual companies was large enough, on its own, to command the scale discounts that Allianz, AXA, and Generali took for granted in their home markets. The decision, when it came, was not subtle: roll them up, strip out the overlap, and put a single national champion on the field. The bigger-is-better mandate was not a hypothesis—it was a directive. And it was about to produce the most consequential corporate event in the history of Turkish insurance.

III. The Great Consolidation: Merging the Six

Spend enough time around veterans of the Turkish insurance market and a particular kind of story starts to repeat. It goes something like this. A mid-sized corporate client, let's say a logistics firm in Izmir with a fleet of two hundred trucks, would be bid on for its annual motor-fleet policy not by two or three insurers, but by half a dozen—and three of them would be state-backed competitors of each other, each represented by the relationship manager of a different state-owned bank, each undercutting the others on price to win the account, and each, at the end of the year, reporting a combined ratio that looked better in the pitch book than it did in the loss triangles. The same dynamic played out in agricultural insurance, in workplace accident coverage, in fire-and-allied-perils for small industrial sites. The state was, quite literally, the most aggressive price-cutter in the market against itself.

The pre-merger histories of the three non-life companies told the same story from different angles. Güneş Sigorta, founded in 1957, was the oldest and arguably the most commercially minded of the three, with a history of foreign ownership that had ended only when Vakıfbank and the state re-consolidated it. Halk Sigorta, repositioned into Halkbank's orbit after a series of ownership changes in the 2000s, had built a strong SME book on the back of Halkbank's tradesman-banking franchise. Ziraat Sigorta, the youngest of the three as a standalone entity, had leveraged Ziraat Bank's unmatched rural footprint—nearly every town of any size in Anatolia has a Ziraat branch—to dominate crop, livestock, and agricultural machinery coverage. Individually, each was a credible top-ten player. Collectively, if you added their books together, they were already the largest non-life insurer in the country before the merger even happened. They just weren't behaving like it.

The structural feat of the 2020 consolidation is worth lingering on, because it is the sort of thing that sounds simple in a press release and is, in practice, extraordinarily difficult. Three non-life companies with different IT systems, different actuarial reserving conventions, different claims-handling workflows, different agent networks, different product catalogs, and different cultures had to be merged into a single legal entity without disrupting the continuous coverage of millions of policyholders. Three life-and-pension companies had to be merged in parallel, with the added complication that pension assets carry a fiduciary tail that stretches out for decades and cannot tolerate a messy integration. All of this had to happen while the country was in the middle of a pandemic, while the insurance regulator was itself being restructured, and while the currency was entering what would become its most volatile period in a generation.

The integration playbook borrowed more from banking consolidation than from Western insurance M&A. The three non-life balance sheets were pooled, and Türkiye Sigorta emerged on day one as the number-one player in nearly every major line: motor third-party liability, motor own-damage, fire, engineering, agricultural, and workplace. The three life balance sheets were pooled into Türkiye Hayat ve Emeklilik, which immediately became one of the two largest pension providers in the country. Overlapping head-office functions were collapsed fast—actuarial, risk, finance, HR, and IT were merged within the first eighteen months. Duplicate regional offices were consolidated. Agency contracts were renegotiated. The reinsurance program, which had previously been purchased in six separate slices, was retendered as a single treaty, which is where the first hard synergy showed up: the combined entity was writing enough premium that global reinsurers had to treat it as a strategic account, and the pricing reflected that.

The synergy bet was, at heart, a very simple one. Take the combined revenue base, strip out the duplicate cost stack, use the larger balance sheet to negotiate better reinsurance terms, and let operating leverage do the rest. Management guidance at the time suggested the integration costs would be recovered within roughly two years. The actual outcome ran close to that projection, which in the context of Turkish corporate history was itself a minor miracle.

But the merger also produced something that was harder to measure in the early years and much more valuable in retrospect: a single institutional memory. Six loss-history databases became one. Six pricing models became one. Six fraud-detection systems became one. And sitting on top of all that data was, for the first time, a management team that could look at the entire state-bank customer base—tens of millions of retail customers, millions of SMEs, hundreds of thousands of farmers—as a single addressable market rather than three overlapping ones. That shift in perspective, more than any line-item cost synergy, is what set up the profitability story of the following five years. And it set the stage for a management team that would have to prove, in the teeth of a currency crisis, that a state-assembled champion could be run like a commercial one.

IV. Current Management and the Institutional Pivot

If the 2020 merger was the structural story, the 2021-2026 period has been the cultural one. And culture, in a state-assembled financial champion, is not a soft topic. It is the difference between a company that writes premium to hit volume targets set by politicians and a company that writes premium to generate returns on equity that keep pace with inflation. Türkiye Sigorta, remarkably, has mostly managed to become the second kind of company, and the turn has a great deal to do with the leadership that took the helm after the initial integration was stabilized.

The generational shift at the top is worth describing in some detail, because it is not a story Turkish insurance has told before. Historically, the CEOs of state-owned insurers were drawn from a pool of career civil servants and bank executives whose primary loyalty was to the ministry that had appointed them. Compensation was modest, tenure was tied to political cycles, and strategic ambition was generally capped at "do not embarrass the government this year." The post-merger Türkiye Sigorta broke that mold almost immediately. The board, working through the TWF, recruited executives with genuine private-sector pedigrees—people who had run underwriting at multinationals, who had built life-insurance franchises at Western-owned rivals, who understood the difference between accounting profit and economic profit in a high-inflation environment.

The Taha Çakmak era has been the most visible expression of that shift. Çakmak, who took over as General Manager and has become the public face of the company in investor forums, came out of a background that blended banking, insurance, and regulatory experience—the sort of portfolio that in Turkey tends to produce either policy wonks or operators, and in his case produced very much the latter. His public messaging, across earnings calls, investor days, and the company's annual reports, has consistently pushed the same drumbeat: profitability over pure volume, return on equity as the north-star metric, and a willingness to walk away from unprofitable business lines even when they came with political cover.

That last point matters more than it sounds. In a country where compulsory motor third-party liability pricing has periodically been capped by the government, where agricultural insurance is partially subsidized, and where the temptation to underwrite marginal risks to keep a state bank's cross-sell machine humming is constant, a management team that is willing to say no is a meaningful cultural break. The company's public commentary through 2023 and 2024 repeatedly emphasized technical profitability in motor lines, selective growth in fire and engineering, and a refusal to chase market share at the expense of combined ratio. That stance did not always make the company popular with politicians. It did, however, make it considerably more popular with foreign institutional investors, who by 2025 had built meaningful positions in the free float.

The incentive structure underpinning all of this is the quiet key to the whole story. The Turkey Wealth Fund owns roughly 81% of Türkiye Sigorta, with the remainder held by the state-owned banks that were the original sponsors and by public free float on the Borsa Istanbul. Unlike a typical Western shareholder, the TWF is not looking for quarterly EPS beats. It is looking for a portfolio company that can, over a cycle, generate returns on equity that meaningfully outpace Turkish CPI—because the TWF's own balance sheet is denominated in lira and eroded by inflation in exactly the same way a retail investor's savings account is. That alignment, strange as it sounds for a sovereign-owned entity, is actually cleaner than many Western shareholder structures. The majority owner needs the company to out-earn inflation, because if it doesn't, the owner itself gets poorer. Management compensation and KPIs have accordingly been structured around ROE targets that carry real teeth in an environment where the CPI benchmark is a moving target.

The free-float dynamics add a further layer. The roughly 19% of shares trading freely on the BIST have, for much of the post-merger period, been held by a mix of domestic retail investors drawn to the dividend yield, local pension funds obliged to hold large-cap financials, and a growing cohort of foreign emerging-markets funds who view Türkiye Sigorta as a more-liquid, less-politicized proxy for Turkish financial-services exposure than the state banks themselves. The stock has consequently traded with a volatility that reflects lira risk more than operational risk, which is both its curse and, for a long-term holder, its opportunity. And it is the distribution of returns to that free float—through a dividend policy that has become one of the most aggressive among large-cap Turkish financials—that sets up the next part of the story.

V. M&A and Capital Deployment

The question that always comes up, eventually, when Western investors study the 2020 merger, is whether the state overpaid. It is a sensible question, and it has a slightly unsatisfying answer: the concept of "paying" does not really apply in the way a Western M&A framework would assume. The six entities were already owned by the Turkish state through various bank subsidiaries and holding structures. Consolidating them into a single vehicle under the TWF was an internal reorganization, not an arm's-length acquisition. There was no premium paid to outside shareholders, because there were essentially no outside shareholders to pay a premium to. The "cost" of the merger was the friction cost—legal fees, integration spend, IT migration, redundancy payments—and that cost was modest relative to the size of the combined balance sheet.

Benchmarked against regional peers, the merger looks structurally attractive regardless of how one counts. Allianz Sigorta, the Turkish subsidiary of the German giant, has been a perennial top-three player and is a formidable underwriting franchise, but it lacks the captive bancassurance rail that Türkiye Sigorta enjoys. AXA Sigorta, similarly, has built its business through independent agencies and has had to fight for every point of market share. Anadolu Sigorta, the other great Turkish national-brand insurer, has the advantage of a long operating history and a tight link to İşbank—but İşbank, for all its reach, is one bank, not three. The implicit "multiple" the state paid for the consolidation, if one were to reverse-engineer it from the synergies realized, came in well below what an Allianz would have had to pay to buy a similar footprint in the open market. Because the merger was essentially an internal reshuffle, the entry cost was the integration friction, and that cost was recovered within about two years through the combined purchasing power in reinsurance and the elimination of duplicate overheads.

Since then, the company's capital deployment story has been less about M&A—there is, essentially, nothing left to roll up at scale in the state-owned insurance space—and more about the allocation of a growing pile of retained earnings in a high-inflation environment. The choices, roughly, are four: reinvest in the operating business, build up reserves, fund growth in the pension and life subsidiary, or return cash to shareholders. Türkiye Sigorta has done all four, in a mix that has shifted with the macro environment.

The dividend policy, in particular, has become a signature feature. Across the post-merger years, the company has paid out a meaningful share of distributable earnings, with dividend yields on the stock often reaching double digits in lira terms. That policy is not universally popular with prudential regulators, who would prefer to see more capital retained on the balance sheet, and it has to be balanced carefully against solvency ratios and the growing book of long-tail liabilities. But the logic, from the company's and the TWF's perspective, is sound. In a currency that loses twenty to forty percent of its value against hard currency every year, retained earnings sitting in lira reserves are being quietly confiscated by inflation. Paying out a chunk of those earnings to shareholders—including the majority shareholder, which then redeploys the cash across its broader portfolio—is, in purchasing-power terms, a more efficient use of capital than letting it erode in-house.

The counterbalance is the need to keep enough capital to support the underwriting book's growth. Gross written premiums have compounded at extraordinary nominal rates since the merger, driven partly by real volume growth and partly by inflation-indexed pricing on motor, fire, and engineering lines. Each lira of new premium requires its own small pile of supporting capital, and in a market growing at nominal rates of fifty to eighty percent, that capital consumption adds up quickly. The company has managed this tension through a combination of retained earnings, selective reinsurance to cede away capital-intensive risks, and periodic subordinated debt issuance when markets have been receptive. Solvency ratios have stayed comfortably above regulatory minimums, but the management team has been clear in public commentary that it monitors the balance carefully.

What makes the capital-deployment picture distinctive—and, for a long-term shareholder, more interesting than it first appears—is the combined effect of three things: aggressive premium growth, strong investment yields on the float, and meaningful dividends. The company has essentially been running as a high-velocity compounder, recycling float income into shareholder distributions while using retained earnings and reinsurance to finance volume growth. That model works spectacularly well in a high-rate, high-inflation environment, provided the underwriting stays disciplined. It works less well if rates collapse or if underwriting discipline slips. And it sets up a very specific question about where the real growth engines of the business actually sit, because the headline numbers obscure some of the most interesting sub-segments.

VI. The Hidden Businesses: The Engines of Growth

The name on the door is Türkiye Sigorta, but anyone who has read the annual report cover to cover will tell you that a lot of the most interesting growth is not happening in the flagship non-life company at all. It is happening in three quieter, structurally advantaged sub-businesses that rarely make the headlines but are, in aggregate, changing the shape of the group's earnings.

The first, and most important, is Türkiye Hayat ve Emeklilik—the life-and-pension sibling born from the same 2020 merger. To understand why this entity matters, it helps to understand the peculiar history of private pensions in Turkey. Starting in 2013, the government launched a voluntary private-pension system with matching state contributions, an attempt to build a second pillar of retirement savings beyond the public pay-as-you-go system. Uptake was modest. Then, in 2017, the government rolled out "Otomatik Katılım Sistemi"—OKS, the Automatic Enrollment System—which defaulted employees into workplace pension plans and required them to opt out rather than opt in. The opt-out rates were high in the early years, as employees found ways to leave the scheme. But the infrastructure was now in place, and it has grown. By the mid-2020s, OKS and its voluntary counterpart had become a substantial, sticky pool of long-duration assets under management, administered by a handful of large players, of which Türkiye Hayat ve Emeklilik has consistently been either the largest or a very close second.

The commercial characteristics of that pension book are extraordinary, and underappreciated in equity research. Unlike non-life insurance, where contracts reset every year and customers can shop around each renewal, pension assets accumulate month after month, year after year, and are unusually sticky because the frictions of switching providers are high and because the government contribution acts as a kind of loyalty glue. The fee income is modest in percentage terms but enormous in aggregate, and it compounds as the underlying asset base grows with new contributions, investment returns, and inflation-driven nominal wage increases. For a long-term investor looking for recurring-revenue characteristics in a Turkish financial company, this is as close as the market gets.

The second hidden business is agricultural insurance, and more specifically the company's dominant role in TARSİM—the Turkish agricultural insurance pool that combines private insurers with state reinsurance support. TARSİM is a structurally fascinating arrangement. Premiums are partially subsidized by the government, losses above a certain threshold are backstopped by a public reinsurance facility, and the participating insurers share in the pool's underwriting result according to their market-share contributions. Türkiye Sigorta, drawing on the combined Ziraat Sigorta legacy book and the reach of Ziraat Bank's rural branch network, is by a wide margin the largest participant in TARSİM. That position is almost impossible for a competitor to dislodge, because the distribution relies on the trust and foot traffic of a bank network that competitors simply do not have.

The macro tailwinds behind agricultural insurance in Turkey are also worth understanding. Climate volatility has been worsening across Anatolia, with more frequent droughts in the central plateau, hailstorms in the tobacco-growing regions, and frost events in the apricot and hazelnut belts. Each incident drives both claims payments and, more importantly, awareness. A farmer who lost an uninsured crop to a hailstorm in 2023 is a farmer who buys coverage in 2024. The government, for its part, has leaned harder into agricultural insurance as a tool of rural policy, both to manage fiscal exposure from ad-hoc disaster relief and to anchor food security in an era of global supply-chain anxiety. All of that translates into durable premium growth in a line of business where Türkiye Sigorta has an essentially unassailable position.

The third and perhaps most under-the-radar engine is participation insurance—the Takaful-compliant, sharia-based insurance products that cater to a segment of the Turkish population that has historically stayed out of conventional insurance for religious reasons. The participation-finance sector in Turkey has grown rapidly as state banks have launched participation subsidiaries and as the regulator has formalized the rules around Islamic-compliant financial products. Türkiye Sigorta's participation-insurance arm has been among the leading players in this niche, offering both non-life and life products structured around risk-sharing rather than risk-transfer principles. The economics of participation insurance are not dramatically different from conventional insurance once the accounting is understood, but the customer base is meaningfully different: it tends to be more rural, more conservative, and less likely to have engaged with financial products at all before. That makes every new customer an incremental addition to the total addressable market rather than a customer won from a competitor. In an industry where most growth is a zero-sum battle for market share, incremental customer acquisition is unusually valuable.

Stack those three engines together—the pension compounder, the agricultural monopoly, and the Takaful growth story—and the picture of Türkiye Sigorta changes. It is not simply a state-assembled motor-and-fire insurer coasting on a bancassurance rail. It is a diversified financial-services group with several structurally advantaged sub-franchises, each of which has its own growth dynamic and its own moat. Which is the perfect cue to frame the whole business through the analytical lens that has been hanging over this entire conversation.

VII. The 7 Powers and Porter's 5 Forces

Hamilton Helmer's 7 Powers framework is, at its heart, an answer to a single question: why does a business earn returns above its cost of capital, and why do those returns persist? For Türkiye Sigorta, the honest answer involves at least two of the seven powers and arguably a third.

The clearest is Cornered Resource, in the specific form of the bancassurance agreements with Ziraat Bank, Halkbank, and Vakıfbank. These are not casual referral arrangements. They are long-term, deeply embedded distribution contracts that give Türkiye Sigorta effectively exclusive access to the point-of-sale moment at some of the largest bank-branch networks in the country. When a customer walks into a Ziraat branch to take out a mortgage, the home-insurance policy attached to that mortgage is overwhelmingly a Türkiye Sigorta policy. When a small-business owner at Halkbank takes on a commercial-vehicle loan, the motor coverage is a Türkiye Sigorta product. When a farmer at Ziraat buys crop coverage, TARSİM routes the policy through Türkiye Sigorta's agricultural arm. The "cornered resource" is not a patent or a mine—it is the front-row seat at the branch window. Competitors can build great products, hire better actuaries, and run cheaper back offices, but they cannot buy their way into that seat. The state owns the seat, and the state has decided to give it to one insurer.

The second power is Scale Economies, most visible in reinsurance purchasing. Reinsurance, for those new to the plumbing, is the insurance that insurers buy to protect themselves against catastrophic losses. A company writing a large earthquake-exposed book in Istanbul, for instance, does not want to hold all of that risk on its own balance sheet; it cedes some portion of it to global reinsurers like Munich Re, Swiss Re, and Hannover Re in exchange for a premium. Those global reinsurers price the business based on size, diversification, data quality, and long-term relationship value. Türkiye Sigorta, as by far the largest single buyer of reinsurance in Turkey, negotiates terms that a smaller domestic insurer simply cannot access. Better terms translate into lower net cost of risk, which translates into better underwriting margins, which translates into more capital to reinvest or distribute. It is a virtuous loop, and it gets stronger as the company grows.

There is a plausible third power in Process Power—the accumulated operational know-how of running integrated bancassurance at scale—but it is harder to measure and easier to imitate over time, so it is safer to treat it as a supporting factor rather than a standalone moat.

Running the same business through Porter's Five Forces produces a picture that largely confirms the Helmer read but adds texture around competitive intensity. The bargaining power of buyers is low in many key lines, because motor third-party liability is legally compulsory, mortgage insurance is effectively compulsory as a condition of the loan, and agricultural insurance is increasingly a prerequisite for rural credit. Customers, especially retail customers, do not shop around much in Turkey; they buy what the bank offers. The bargaining power of suppliers—reinsurers, in this case—is real but mitigated by scale, as discussed above. The threat of new entrants is moderate at best, because the bancassurance rail is essentially closed; the only way to replicate Türkiye Sigorta's distribution would be to acquire or partner with a major bank, and the state-owned banks are spoken for. The threat of substitutes is modest in the short term, though the rise of digital-native insurers and price-comparison platforms could chip away at the private auto segment over time.

The intensity of rivalry is where the picture gets most interesting. Anadolu Sigorta, backed by İşbank and the Turkish Armed Forces Pension Fund (OYAK), is a genuinely formidable competitor—well-managed, historically strong in motor and corporate lines, and with a distribution rail of its own through İşbank's large branch network. Allianz, AXA, and a handful of other multinationals compete aggressively in corporate lines, broker-distributed segments, and certain specialty areas. The Turkish non-life market is not a monopoly; it is a concentrated oligopoly with a clear leader. What sets Türkiye Sigorta apart is not the absence of rivals but the depth of its distribution moat in the specific segments where the state-owned banks are dominant—retail mortgages, SME lending in certain regions, agricultural credit, and public-sector employee products. In those segments, rivalry is structurally muted. In broker-distributed corporate lines, it is intense. The mix across the book is the story.

Put the two frameworks together and the shape of the competitive advantage becomes clearer. Türkiye Sigorta is not universally dominant. It is structurally dominant in the segments that matter most for durable, low-cost premium growth, and it is competitive but not unchallenged in the segments that matter most for pricing discipline and product innovation. That is a healthier configuration than pure monopoly, because it keeps the management team honest, but it is a far better position than the merely-large state insurer that critics sometimes caricature it as. And it leads directly into the practical lessons that fall out of the entire story.

VIII. The Playbook: Business and Investing Lessons

Every great Acquired episode produces a handful of lessons that transcend the specific company, and Türkiye Sigorta is no exception. The lessons here are not exotic, but they are unusually concrete, because the company has essentially run a series of controlled experiments on each of them.

The first lesson is the Consolidator's Premium. In a fragmented market, the player who successfully rolls up the middle of the pack into a clear number one usually wins, and wins on margin more than on revenue. The mechanics are straightforward: duplicate overhead gets eliminated, purchasing power goes up, fixed-cost absorption improves, and the resulting scale becomes self-reinforcing because customers, regulators, and counterparties all prefer to deal with the largest player. What Türkiye Sigorta illustrates is that this logic works even when the consolidator is the state, and even when the rollup is mandated rather than negotiated. The accounting may look different—there is no goodwill line from an arm's-length acquisition, no premium paid to public shareholders—but the operational physics are identical. Fragmented markets with duplicate state-backed players are, in fact, unusually fertile ground for consolidation plays, because the friction costs of integration are lower when all the entities share an ultimate owner.

The second lesson is about float in a hyperinflationary environment. Float—the cash insurers hold between premium receipt and claim payment—is famously Warren Buffett's favorite asset. In a stable, low-inflation environment, float is valuable because it costs less than debt. In a hyperinflationary environment, float becomes something more interesting: it is a way to ride the yield curve at genuinely extraordinary nominal rates, provided the management team invests it prudently and matches duration to liabilities. Türkiye Sigorta's investment portfolio during the 2022-2025 rate-hike cycle earned nominal yields that, in local currency terms, dwarfed most of the company's underwriting income. The lesson is not that hyperinflation is good for insurers—it isn't, because claims inflation erodes reserves and underwriting volatility spikes. The lesson is that in the specific configuration where a regulator anchors reserves in short-duration local-currency instruments and where policy rates are pushed to punitive levels to fight inflation, the investment side of the business can temporarily carry the whole P&L. Smart management recognizes the windfall, locks in as much of it as possible, and resists the temptation to loosen underwriting standards on the back of easy investment income.

The third and most durable lesson is that in insurance, distribution is everything. Product innovation matters. Actuarial sophistication matters. Claims service matters. But the moat, the thing that compounds year after year and that competitors cannot easily replicate, is the distribution rail. Türkiye Sigorta's bancassurance position at three state-owned banks is not a clever marketing insight—it is a structural reality bolted into the state's ownership chart. Companies that build equivalent distribution moats in other markets, whether through branch networks, captive broker relationships, or exclusive digital channels, tend to earn the kind of persistent returns that attract long-term capital. Companies that try to compete on product alone, without a distribution edge, tend to find themselves stuck fighting for share in the most competitive, lowest-margin segments.

A brief aside on the myth-versus-reality read of the company, since the lessons above push against some common assumptions. The myth, especially among Western investors encountering Türkiye Sigorta for the first time, is that it is essentially a political asset masquerading as an insurer—exposed to state mandates, unable to price freely, and destined to be run for volume rather than profit. The reality is that the company has, since the merger, consistently prioritized underwriting profitability over volume, has walked away from unprofitable motor business when the numbers demanded it, and has built out genuinely commercial sub-franchises in pensions, agriculture, and participation insurance. The myth is that the bancassurance rail is a gift that could be withdrawn at any time by political whim. The reality is that the state's incentive to preserve the arrangement is strong, because the TWF owns the insurer, and weakening its distribution would weaken the TWF's own balance sheet. The myth is that the lira will consume any investor return. The reality is that hard-currency investors have had a volatile ride, but the company's dividend policy has returned substantial purchasing power even when currency-translated book value has looked ugly.

A handful of secondary diligence points sit around the edges of the story and deserve brief mention. Accounting in a hyperinflationary environment is genuinely complex: Turkish companies have had to apply inflation accounting under IAS 29 for reporting periods starting 2023, which restates non-monetary items and changes the shape of reported earnings meaningfully. Comparisons across reporting periods require care, and investors who are used to reading Turkish financials in nominal lira from pre-2023 periods need to adjust. Regulatory overhangs are real but manageable: periodic caps on motor third-party liability pricing have squeezed margins in that line at various points, and the insurance and pension regulator (SEDDK, now operating as SDK) has been active in pushing for higher reserving standards. Climate exposure is rising, particularly in earthquake-prone zones where the February 2023 Kahramanmaraş earthquake sequence was a grim reminder of the tail risk; the state-backed DASK pool absorbs most of the residential earthquake exposure, but commercial and engineering lines still carry meaningful seismic risk. Key-personnel risk is manageable but not zero in a management-dependent turnaround story. These are the kinds of things a careful holder wants to monitor rather than lose sleep over.

And the KPIs that matter. Strip away the noise and there are really only three numbers that tell the story of this company's ongoing performance. The first is the combined ratio—the ratio of claims plus expenses to earned premiums. A combined ratio below 100 means the underwriting book is profitable on its own; above 100 means the company is relying on investment income to carry the day. The second is return on equity, measured against CPI rather than against a nominal benchmark, because in a hyperinflationary economy a nominal ROE figure is almost meaningless. Real ROE—ROE minus inflation—is what actually tells you whether shareholder capital is compounding or eroding. The third is gross written premium growth in the strategic lines, particularly pension assets under management and agricultural premiums, because those are the segments where the moat is deepest and where durable value is being created. Track those three, and a reader will always know whether the flywheel is spinning faster or slower. Chase quarterly nominal earnings, and a reader will be perpetually confused.

IX. Bear vs Bull

Start with the bear case, because it is the one that most foreign investors encounter first and that the company has to defend against most often.

The bear case begins with political risk, and it is not frivolous. Türkiye Sigorta is 81% owned by a sovereign wealth fund that answers to the President's office. In a country where the political cycle has, at various points, produced unorthodox monetary policy, informal pressure on pricing in regulated industries, and periodic "lira-ization" initiatives designed to encourage local-currency savings over foreign-currency holdings, the prospect of a future government reaching into the insurance sector for fiscal or political reasons cannot be dismissed. Compulsory motor third-party liability pricing has already been capped at various points; agricultural insurance premiums are already partially subsidized; health insurance lines could, in principle, be further regulated. None of these risks are catastrophic in isolation, but they cumulatively cap the upside that a purely commercial insurer might enjoy.

The second bear pillar is currency and inflation. The lira's decline against the dollar has been, over the last decade, one of the most dramatic among major emerging-market currencies. Hard-currency investors have had to earn extraordinary local-currency returns just to stand still in dollar terms. While the company's dividend policy has mitigated this meaningfully, the structural reality is that an investor holding Türkiye Sigorta in a hard-currency portfolio is taking on significant foreign-exchange risk that has, historically, tilted against them. The current economic team under Mehmet Şimşek has re-anchored orthodox policy and brought inflation down from its peak, but the path back to single-digit inflation is long and political support for it is not guaranteed across election cycles.

The third bear pillar is catastrophic risk. Turkey sits on major fault lines, and the country has suffered multiple significant earthquakes in recent decades. While the DASK pool absorbs most residential earthquake exposure, commercial fire and engineering lines remain exposed, and a major seismic event in Istanbul—which most serious geoscientists consider a question of when rather than if—would test the reserving and reinsurance adequacy of every Turkish insurer, including this one.

The bull case is structurally the inverse of the bear case, but with a different temperament. Turkey is a country of eighty-five million people with a median age of roughly thirty-three, which is to say it has one of the youngest large populations in the wider European neighborhood. Insurance penetration is a fraction of what demographic gravity would suggest it should eventually become. Financial-services formalization is still working through segments of the economy that have historically operated on cash and trust. Every year, a meaningful cohort of new consumers moves from unbanked to banked, from uninsured to insured, from unpensioned to auto-enrolled. Türkiye Sigorta, sitting at the front row of three state-bank distribution networks, captures a disproportionate share of that new formation.

Layer onto that demographic tailwind the structural moat analyzed through the 7 Powers and 5 Forces lenses, and the bull case is essentially this: a company with genuine Cornered Resource and Scale Economies advantages, operating in an underpenetrated market with strong demographic tailwinds, run by a management team that has repeatedly chosen profitability over volume, with a majority shareholder whose incentives are aligned with long-term compounding, paying out a meaningful share of earnings as dividends while still growing premiums faster than the broader economy. In purchasing-power terms, that is a recipe for a compounder. The trick, as always, is to hold through the volatility, and the volatility will not be subtle.

Benchmarked against regional peers, the bull case also holds up. Anadolu Sigorta is a fine business but lacks the three-bank rail. Allianz and AXA are fine businesses but lack the state relationship. Aksigorta and Mapfre Sigorta are credible mid-tier players without either advantage. The combination Türkiye Sigorta enjoys is, quite literally, not available elsewhere in the market. That does not make it invulnerable, but it does make it structurally distinctive. And in a market where distinctiveness is hard to earn and easy to lose, that distinctiveness is the asset that long-term investors are ultimately paying for.

X. Epilogue

The narrative arc of Türkiye Sigorta, in the end, is the arc of a national-champion experiment. Six state-owned companies, competing against each other on the same distribution rails, consolidated in a single weekend into a unified champion, then handed to a sovereign wealth fund whose incentives pushed toward commercial discipline rather than political softness. The experiment has, so far, worked better than skeptics expected and perhaps better than its architects dared to hope. The company has compounded premiums, grown the strategic sub-franchises, maintained underwriting discipline through a currency crisis, and returned meaningful capital to shareholders along the way.

For the investor trying to understand this company from first principles, the primary sources are the annual reports filed with the Public Disclosure Platform (KAP), the company's investor-relations website at turkiyesigorta.com.tr, the quarterly earnings presentations that accompany each set of financials, and the investor-day materials that the company publishes each spring. The Turkish Insurance Association and the insurance regulator publish market-wide data that is essential for benchmarking. Anadolu Sigorta's filings are the natural comparison point for anyone wanting to calibrate the competitive landscape. And the TWF's own annual reporting, while less detailed than a Western sovereign wealth fund's would be, provides the overarching context for how the majority shareholder thinks about this and its other portfolio companies.

The picture of Türkiye Sigorta that emerges from all of that material is of a business that sits at the intersection of demographic tailwinds, institutional consolidation, and macroeconomic turbulence—and whose long-term fate will be decided as much by the macro path of the country as by the day-to-day decisions of its management. Six small swords became one massive shield. Whether that shield holds, grows, and compounds in the decades ahead is the question that every long-term holder of the stock is ultimately asking. And it is, even after everything above, a question that the next decade of operating results—not the last—will answer.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube