Thai Life Insurance (TLI) – The Human Sovereign of Southeast Asia

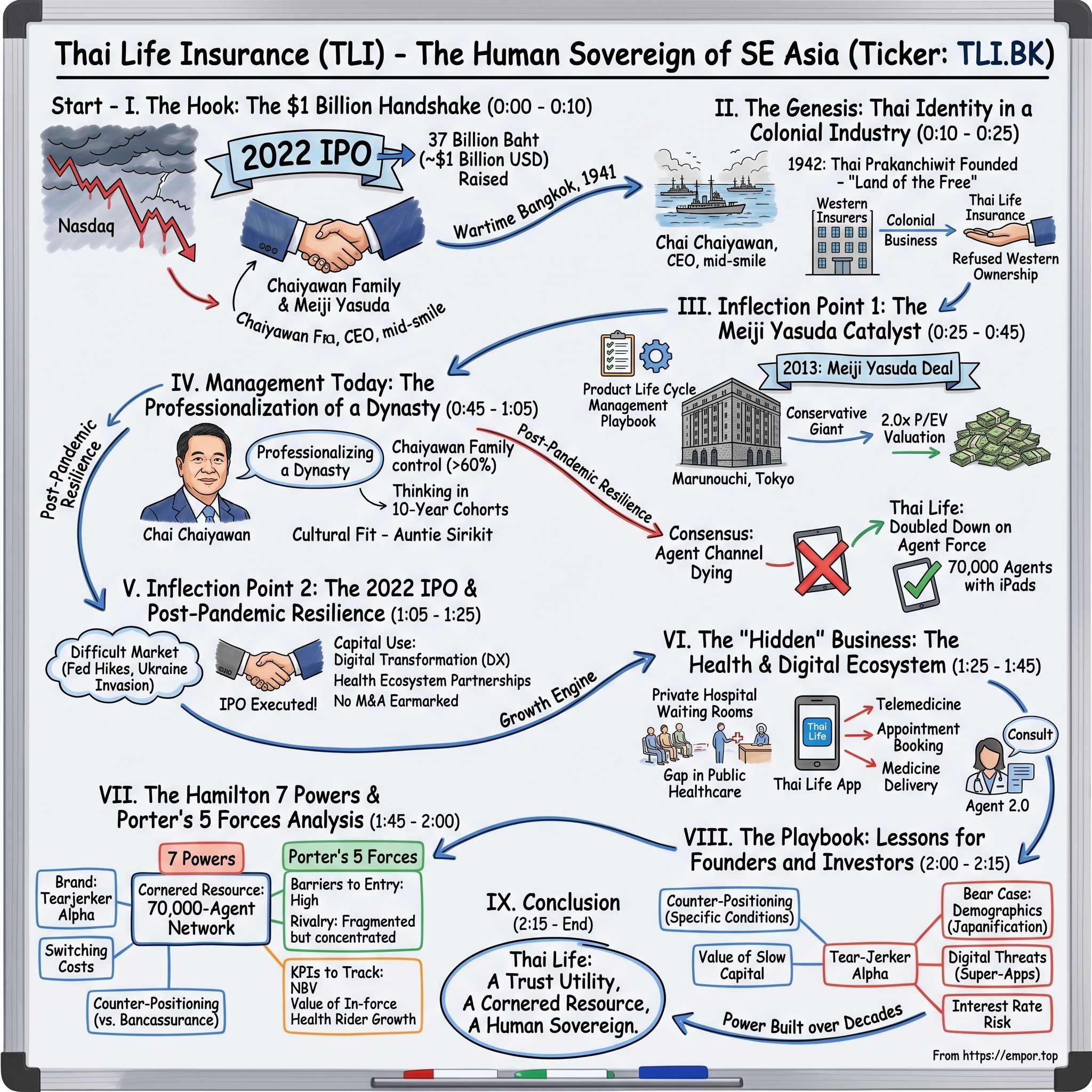

I. The Hook: The $1 Billion Handshake (0:00 – 0:10)

July 25, 2022. Bangkok. The trading floor of the Stock Exchange of Thailand opened under a sky that felt, even for those who don't read tea leaves, distinctly ominous. Six thousand miles away, the Nasdaq was bleeding. The Fed had just delivered its second consecutive 75-basis-point hike, crypto had imploded, Softbank had posted the largest quarterly loss in Japanese corporate history, and the phrase "tech winter" was being used so often it had already become a cliché. In venues from New York to Hong Kong, IPO calendars were being quietly shredded.

And yet, on that particular Monday morning in Bangkok, a company founded in 1942—the year the Japanese Imperial Army occupied large swathes of Southeast Asia, the year Casablanca premiered, the year the Manhattan Project was greenlit—walked onto the public markets with one of the largest IPOs in Thai history. Thai Life Insurance Public Company Limited, ticker TLI, raised roughly 37 billion Baht. Call it a billion US dollars, give or take. In a market where the median IPO that year raised under $50 million, this was a statement.

The Chaiyawan family, which had controlled the business for three generations, rang the bell alongside executives from Meiji Yasuda Life Insurance, the 140-year-old Japanese giant that had bought a strategic stake nearly a decade earlier. Chai Chaiyawan, the CEO, wore a dark suit; the photographers captured him mid-smile, mid-handshake, and that image ran in every Thai business paper the next morning. What the photograph did not capture was the quiet, almost defiant thesis behind the listing: in a world where every life insurer on earth was being told the future belonged to robo-advisors, bancassurance partnerships, and digital-first insurtech, Thai Life was going public on the strength of 70,000 human agents walking door-to-door through Thai villages and suburbs, carrying iPads.

That is the puzzle this episode is going to spend the next two hours unpacking. How does an 80-year-old family-controlled insurance company, operating in a middle-income emerging market, defend a moat built on human relationships in the age of algorithms? How did it convince one of Japan's most conservative financial institutions to write a roughly $700 million check for a minority stake back in 2013? Why did it choose the ugliest IPO window in a decade to go public? And most importantly for our long-term investor audience—what exactly is the durable, underappreciated asset hiding on the balance sheet of a company that most foreign investors could not name if you put a gun to their heads?

The thesis, stated plainly, is this. Thai Life is not primarily an insurance company. It is a trust utility. It is the institutional manifestation of the Thai family safety net, monetized over a 30-year contractual horizon, priced at a fraction of what an equivalent franchise trades at in Hong Kong or Singapore. The "Cornered Resource"—Hamilton Helmer's phrase, and we will come back to it—is not the investment portfolio, not the actuarial model, not the reinsurance treaties. It is the relationship between 70,000 agents and a customer base that does not trust banks, does not trust foreigners, and has not, historically, trusted insurance either—except for this one firm.

The roadmap for today is a story in four movements. We start in wartime Bangkok, with a small group of Thai businessmen refusing to let Western firms own their country's future. We move to 2013, when Meiji Yasuda's capital injection transformed a regional player into a professionalized giant. We walk through the 2022 IPO and its aftermath. And we finish with the bear case—aging demographics, Grab and Sea Group circling financial services, and the quiet question of whether the "Human-First" model is genius or nostalgia. By the end, you should understand not just what TLI does, but why it survives. Let's begin at the beginning.

II. The Genesis: Thai Identity in a Colonial Industry (0:10 – 0:25)

Picture Bangkok in 1941. The city was still officially the capital of a neutral kingdom, but neutrality in December of that year was a polite fiction. On December 8, Japanese troops landed on the southern coast and marched north, and within 36 hours Field Marshal Plaek Phibunsongkhram had signed an alliance with Tokyo. By the following year, Allied air raids were a regular feature of Bangkok nights, the Chao Phraya River was patrolled by Japanese gunboats, and British and American expatriates who had dominated Bangkok's commercial district were either in internment camps or had fled. Into this chaos, on January 22, 1942, a group of Thai entrepreneurs founded a new kind of company.

Insurance in Siam—only renamed Thailand four years earlier—had been, from its very beginnings in the 1870s, a colonial business. The great British insurers arrived with the rubber and teak concessions. The Dutch came down from Batavia. American firms followed after the First World War. By the 1930s, if a Thai merchant wanted to insure a warehouse, a shipment, or his own life, he had to walk into the Bangkok office of a firm headquartered in London, Amsterdam, or New York, sit across from a European underwriter, and argue his case through a translator. The policies were written in English. The premium schedules assumed Western mortality tables. The sales force, to the extent one existed, was drawn from the thin ranks of mission-school-educated Thai clerks.

Thai Life Insurance was founded to be the opposite of that. The founders—a coalition of Sino-Thai merchant families with roots in the rice and textile trades—made a decision that was half patriotism, half commercial opportunism. They would build an insurer run by Thais, staffed by Thais, using the Thai language, pricing risk against the realities of life in the kingdom's villages and paddy fields rather than the assumptions of a London reinsurer. The Japanese occupation made the timing commercially logical; Western competitors had mostly vanished. But the founding charter was written in a spirit that would outlast the war. The company's original Thai name, Thai Prakanchiwit, translates almost literally as "Thai Life Insurance"—but the word "Thai" there carries the same emotional weight it does in "Thailand," which itself means "Land of the Free."

For the first two decades after the war, the company was, frankly, a middling regional life insurer. It grew with the Thai economy, which in the 1950s and 1960s was transforming from an agricultural backwater into a light-manufacturing hub, but it was not yet a national champion. That transformation came with the arrival of the Chaiyawan family in the early 1970s. The Chaiyawans—Vanich Chaiyawan, the patriarch, and his sons—had built their fortune in banking, property, and beverages. They approached insurance not as number-crunchers but as social engineers. Vanich, in interviews later in life, repeatedly framed life insurance as a civilizational institution: in a country without a meaningful state pension, without reliable public healthcare, without a deep bond market for retirement products, who takes care of the widow? Who pays for grandfather's final illness? In the Thai village, the answer had always been "the family." Vanich's bet was that as the country urbanized and migration fractured those village networks, the family's role would need an institutional partner. That partner should be Thai. That partner should be them.

From this thesis emerged what is, in retrospect, the most important strategic asset Thai Life ever built—not a product, not a distribution channel, but a brand. Thai Life's television advertisements have, over the past 40 years, won more international Cannes Lions and Clio awards than any other Thai company in any industry. They are, by global consensus, the reigning champions of the "emotional tearjerker" ad form. Three minutes of wordless narrative, a dying parent, a sacrificing child, a final hospital scene, and then the softest possible logo reveal. Global audiences know Thai insurance commercials by reputation even if they have never bought a policy. In Thailand, these ads are studied in universities. They have created an emotional moat around the brand that competitors—including far larger multinationals—have never managed to cross. When a Thai grandmother says "take care of your life insurance," she means Thai Life, in the way Americans of a certain generation say Kleenex or Xerox.

That emotional moat, built quietly over four decades, is what the next chapter of this story rides on. By the early 2010s, the company had scale, brand, and a distribution network. What it did not yet have was world-class product design, investment management, and digital infrastructure. For that, it needed a partner.

III. Inflection Point 1: The Meiji Yasuda Catalyst (0:25 – 0:45)

It is difficult to overstate how conservative Meiji Yasuda Life is. The Tokyo headquarters of Japan's second-largest life insurer sits in Marunouchi, two blocks from the Imperial Palace, in a building whose granite facade communicates, at a glance, that the firm has no interest in your startup's pitch deck. Founded in 1881 as Japan's first modern life insurer, Meiji Yasuda spent the 20th century quietly amassing one of the largest investment portfolios in Asia and developing a corporate culture in which the phrase "managed risk" is redundant. When this institution decided, in 2013, to deploy roughly $700 million for a 15% stake in a Thai family business, the move was, for the firm and for the industry, genuinely significant.

The deal closed in April 2013. The headline valuation implied by the transaction was in the neighborhood of 2.0 times Price-to-Embedded-Value, or P/EV—the standard currency of life insurance M&A. For listeners not steeped in insurance finance, a quick detour. Embedded Value is, roughly, what an insurance policy is worth if you run off its cash flows to maturity, discounted back. It combines the net asset value of the company with the present value of future profits from the existing book of business. It is the insurance industry's answer to "what is this company really worth before you assign any credit to new business growth?" A 2.0x P/EV multiple is not cheap. At the time, pan-Asian peers like AIA Group traded closer to 1.5x to 1.8x, and Prudential's Asian business, depending on how you sliced it, hovered in a similar band. Regional peers in Indonesia and Vietnam routinely transacted in the 1.2x to 1.6x range.

So why did Meiji Yasuda pay a premium? The answer was not primarily financial; it was structural. Japan's domestic life insurance market had been, by 2013, in a slow-motion demographic death spiral for two decades. The population was shrinking. Interest rates had been near zero since 1999. Japanese households already owned, on average, more life insurance per capita than any other country on earth. The growth algorithm had simply run out of runway. Every large Japanese insurer had, by the early 2010s, been forced into the same strategic conclusion: to survive, they had to own a piece of emerging Asia. Dai-ichi had just bought Star Union in India and was building a position in Vietnam. Nippon Life would follow with stakes in Indonesia's Sequis and India's Reliance Life. Sumitomo Life would eventually take a controlling position in Symetra in the U.S. and deepen its Vietnam play.

Meiji Yasuda's Thai Life investment was, in that sense, a competitive response. But within the pack, it was also the boldest. A 15% stake at 2.0x P/EV in a family-controlled business meant the buyer was paying for more than cash flows. It was paying for access. Thailand in 2013 had a life insurance penetration rate—premiums as a percentage of GDP—of roughly 3.8%. Compare that to Japan's 8%, Taiwan's 15%, or the global developed-market average around 5%. The runway looked enormous. Health insurance penetration was lower still. The Thai middle class was expanding at something like 5% annually, urbanization was accelerating, and the state's willingness to fund retirement and healthcare was, to put it diplomatically, limited. A 2.0x multiple on a franchise in a market with a decade of structural tailwinds was, in retrospect, a steal.

But the real value of the Meiji Yasuda deal was not the check. It was what came with the check. Over the next five years, teams of Meiji Yasuda actuaries, product designers, IT architects, and internal-audit specialists quietly rotated through Bangkok. Thai Life's product shelf, which in 2012 had been heavy on "traditional whole life" policies—low-margin, capital-intensive, easy-to-sell but difficult-to-scale—was gradually rebuilt around a more sophisticated mix. Investment-linked products, which pass investment risk to the policyholder and generate fee income rather than spread income, became a meaningful line. Health riders—the small add-on policies that let a customer bolt hospital and critical-illness cover onto a base life policy—became the new growth engine. In insurance jargon, this is called "Product Life Cycle management," and Meiji Yasuda had spent 140 years perfecting it in Japan. They handed Thai Life the playbook.

The capital itself was deployed with discipline. Rather than embarking on a regional M&A spree, which would have been the fashionable move of the mid-2010s, Thai Life's management used the war chest for two quieter purposes. First, they invested heavily in the agent force—training programs, digital tools, compensation restructuring. Second, they modernized the back-office technology stack. Core administration systems that had been running on decades-old mainframes were gradually migrated, and data warehouses were built that could finally, for the first time, tell the company which agents were selling which products to which customer segments at which persistency rates. Boring work. World-changing, when compounded over a decade.

The partnership also gave Thai Life something intangible but valuable: the governance signal that came from having Meiji Yasuda on the register. When a Japanese life insurer with 140 years of history writes a nine-figure check after 18 months of due diligence, it is a stamp of legitimacy that ripples through every stakeholder conversation—with the regulator, with ratings agencies, with reinsurers, with eventually the IPO market. That stamp would matter nine years later, when the equity markets turned hostile.

IV. Management Today: The Professionalization of a Dynasty (0:45 – 1:05)

To understand how Thai Life navigated the decade that followed the Meiji Yasuda deal, you have to understand the Chaiyawan family, and in particular, you have to understand Chai Chaiyawan. If you met him at a cocktail reception, you would assume, correctly, that he is the scion of a Bangkok business dynasty. You would not necessarily assume he is the chief executive of a publicly listed insurer with roughly a trillion Baht in assets under management. He is soft-spoken by CEO standards, technically trained, and allergic to the kind of self-mythologizing that characterizes so many founders-turned-chairmen across Asia.

Chai took the reins during the long transition decade of the 2010s, inheriting the role from the previous generation and gradually transforming it. His educational background—finance and management, with extended stints abroad—made him fluent in the language of institutional investors in a way his predecessors, who had built the business through relationship banking and political networks, had never needed to be. This matters. An 80-year-old family business does not become a professionally managed public company overnight. It becomes one when the second- and third-generation leaders can move between two worlds: the Thai dinner table where deals are still done on relationships, and the investor roadshow in Singapore where deals are done on P/EV multiples and Solvency II capital ratios.

The ownership structure reinforces this duality. Following the 2022 IPO, the Chaiyawan family, through their holding vehicle V.C. Property and related entities, retained a controlling position well north of 60% of the equity. Meiji Yasuda held roughly 15%. The free float was in the mid-20s. This is not a recipe for quarterly-earnings management; it is a recipe for decade-horizon capital allocation. When Western analysts ask Chai about next quarter's new business value, the response, charitably paraphrased, is that the company thinks in 10-year cohorts. The structural advantage of a family-controlled insurer is that the family is still going to be sitting at the dinner table in 2040, and they would like the company to still exist.

That long-termism expressed itself in a strategic decision that, at the time, looked contrarian and now looks visionary. Through the mid-to-late 2010s, the global life insurance industry had reached a near-unanimous consensus: the agent channel was dying. Bancassurance—the practice of selling insurance through bank branches and bank customer databases—was the future. It was higher-margin for the insurer (no trail commissions to agents), lower-cost-to-acquire (the bank already owned the relationship), and, in a digital age, scalable in ways that a human sales force was not. Across Asia, insurers signed exclusive bancassurance partnerships for hundreds of millions of dollars. AIA locked up Citibank across 11 Asian markets. Prudential signed with UOB. Manulife did deals with DBS and VietinBank. The pattern was consistent, the logic was consistent, and the industry, effectively, moved in one direction.

Thai Life went the other way. The company doubled down on its agent force. Over the decade, the agent headcount rose toward the 70,000 figure that now anchors the company's competitive positioning. The strategic reasoning was not sentimental; it was analytical. Bancassurance, it turned out, produced a specific kind of policy: short-dated, simpler, often single-premium, frequently sold to customers who did not fully understand what they were buying. The profitability looked good at the point of sale but deteriorated as persistency—the rate at which policyholders keep paying their premiums year after year—fell below agent-sold equivalents. Agent-sold policies, by contrast, especially when the agent was embedded in the local community, showed persistency rates that were materially higher. Thai Life's internal data, eventually reflected in disclosures to regulators and investors, showed the company's 13-month persistency running in the low 90s percent, with some segments running in the mid-90s. In the insurance business, that is a number that compounds into enormous lifetime-value differences. A policy that stays in force for 20 years generates a profit pool that is multiples of one that lapses after 36 months.

The agent model's cultural fit mattered as much as the economics. In rural Thailand and in the sprawling suburbs that have formed around Bangkok's edges, the local insurance agent is often someone's cousin, neighbor, or temple mate. Buying a 30-year policy from an algorithm feels alien; buying it from Auntie Sirikit feels, for many Thai households, like an extension of the family safety net rather than a financial product. This is the "Trust Utility" concept we introduced at the top, manifested operationally. And it is why Thai Life's agent force functions as a Cornered Resource in the technical sense: you cannot replicate it by writing a check, because the relationship capital embedded in 70,000 individual human networks took decades to build.

The compensation architecture was deliberately calibrated to protect this moat. Rather than rewarding agents primarily on first-year premium volume—which creates the perverse incentive to churn customers—Thai Life tilted commissions toward persistency and toward policy quality metrics. Agents earn more if their book stays on the books. This sounds obvious; in the insurance industry, it is surprisingly rare. And it is the kind of decision a family-controlled firm can make, because it depresses short-term growth in exchange for long-term value. An activist investor in a Western context would demand the opposite. The Chaiyawans do not have to listen.

What investors have been underwriting since 2022, then, is not just an insurance company. It is a governance structure. A family that has been custodial for 80 years, a strategic minority partner that is one of the most conservative institutions in Japan, a professional management team that can speak to both audiences, and a contrarian strategic commitment to human distribution that flies in the face of global consensus. Whether that consensus is right or wrong is, ultimately, what the next chapter is about.

V. Inflection Point 2: The 2022 IPO & Post-Pandemic Resilience (1:05 – 1:25)

The summer of 2022 was, by any reasonable reading of market conditions, the wrong time to take a company public. By July, the MSCI All Country World Index was down roughly 20% year-to-date. Vladimir Putin had invaded Ukraine in February, oil had briefly touched $130, US inflation had printed above 9%, and the US Federal Reserve was embarked on the most aggressive tightening cycle in forty years. In the IPO market, the damage was almost comical. US IPO volumes for the first half of 2022 were down more than 70% year-on-year. Europe was worse. The Hong Kong IPO market, historically the preferred venue for Asian insurance listings, had effectively closed; the AIA blueprint of a blockbuster insurance IPO looked like a historical artifact.

And yet, on July 25, 2022, Thai Life listed on the SET and raised roughly 37 billion Baht. The final pricing landed at the lower half of the initial range, which told you the market was cautious—but the deal got done. In a year when companies from Porsche to Mobileye were delaying or downsizing, Thai Life's ability to execute in a window that size became, in itself, part of the story.

Why go public at all? And why then? The official answer, stitched together from prospectus language and management commentary, combined three motivations. First, Thai Life had been capital-efficient for a decade; new regulations implementing a risk-based capital framework across Thai insurers were pushing the industry toward higher solvency ratios, and fresh primary equity was a cheaper way to fortify the balance sheet than either debt or retained earnings alone. Second, a public listing gave the company a currency—publicly traded shares—that could be used for future acquisitions, partnership equity swaps, and employee incentives. Third, and most strategically, a listing provided the Meiji Yasuda and Chaiyawan blocks with a transparent mark-to-market valuation, which mattered for estate planning on the family side and for fair-value accounting on the Japanese side.

But underneath those official reasons ran a more interesting strategic logic. Going public in a difficult market is, counterintuitively, a signal of confidence. When Porsche's parent Volkswagen pushed its listing through in September of that same year, the argument was similar: if we can do this now, we can do this anytime. Thai Life's 2022 listing was, in effect, a public assertion that the Chaiyawan-Meiji Yasuda alliance did not need perfect markets to raise capital. The deal was anchored by a roster of Thai institutional investors—pension funds, life insurers, sovereign allocations—who had been watching the company for years and had been waiting for a liquid entry point. Foreign demand was softer than it would have been in 2021 but, crucially, was present.

The capital use was telling. Roughly speaking, the 37 billion Baht was earmarked across three priorities. The largest chunk was allocated to digital transformation—the "DX" spend, in the company's internal language. This was not a case of a legacy firm discovering the internet; Thai Life had been investing in digital capabilities since the Meiji Yasuda partnership. Rather, the DX budget was about stepping up the pace: building a unified customer data platform, expanding the agent-facing mobile toolkit, launching a direct-to-consumer digital channel for simpler products, and investing in AI-driven underwriting. The second chunk went to the health ecosystem—partnerships with Thai hospital chains, investments in telemedicine and medicine delivery, and the development of value-added wellness services bundled with health insurance policies. The third chunk was for general corporate purposes, which, translated from prospectus-ese, meant capital to support the growth of the in-force book under the new risk-based regime.

Almost nothing was earmarked for M&A. This was the tell. In a year when global insurers were using IPO proceeds to acquire targets and consolidate, Thai Life was saying, essentially, that the most attractive asset they could buy was a better version of themselves. Given the structural competitive advantages discussed in the prior section, that answer was internally consistent.

The valuation benchmarking at IPO is worth dwelling on. AIA, the natural pan-Asian comparable, traded around 1.5x to 1.8x P/EV depending on the exact 2022 snapshot. Large Chinese life insurers, buffeted by domestic regulatory pressure and a collapsing property sector, traded at something closer to 0.6x to 0.9x. Thai Life priced its IPO at a multiple roughly in line with AIA's lower end. For an investor willing to look through the near-term macro noise, the math was straightforward: you were buying a company with a higher long-term growth runway than AIA (because Thailand's insurance penetration was far lower), a higher structural persistency rate (because of the agent model), and a more concentrated brand moat (because Thailand is one country, not fifteen), at a multiple that was roughly equivalent.

The post-IPO trading experience was not linear. The stock price, like virtually every Thai listing in 2022, wobbled in the first quarters as global risk-off flows pressured the entire market. But the operational story—premium growth, health rider expansion, agent productivity—played out quarter after quarter in a way that gradually rerated the name. By late 2023 and through 2024, as the Thai domestic economy recovered and global capital flows began tentatively returning to emerging Asia, Thai Life was increasingly included in the "quality Thai equity" baskets constructed by regional asset managers. The stock behaved, in other words, like a bond-plus-growth instrument: a steady compounder of embedded value with a dividend kicker, in a market where such profiles were rare.

What 2022 ultimately established was not a valuation; valuations come and go. It established that Thai Life was now a public-markets participant, subject to public-markets discipline, visible to public-markets capital. The next phase of the story would be about proving the underlying business thesis—that the combination of human distribution and digital infrastructure could produce compounding returns that justified the premium to regional peers.

VI. The "Hidden" Business: The Health & Digital Ecosystem (1:25 – 1:45)

Walk into a Bangkok hospital on any weekday morning, and you will see something that quietly explains the most important growth engine inside Thai Life. The waiting rooms of the large private hospital chains—Bumrungrad, Bangkok Dusit, Samitivej—are, in the early hours, full. Full of middle-class Thais, yes, but also Burmese executives, Cambodian patients flown in from Phnom Penh, Vietnamese medical tourists, and a steady stream of retirees from Europe and Japan who have made Thailand one of the global capitals of private healthcare. The bills are not small. A knee replacement runs into the tens of thousands of dollars. An oncology course can run into the hundreds of thousands. The Thai public healthcare system is, by emerging-market standards, functional; by middle-class Thai standards, it is the option of last resort.

This gap—the space between "what public healthcare covers" and "what a middle-class household actually wants when someone gets sick"—is the single largest opportunity on Thai Life's horizon. The traditional life insurance product, the bread-and-butter 20-year endowment policy, grows with GDP at maybe 3-5% a year. Health insurance, and more specifically the category of health riders attached to base life policies, has been growing at 15-20% annually. The margin profile is superior. The capital intensity is lower. And the distribution synergy is near-perfect: the agent who sold the grandfather a life policy in 1998 is the obvious person to sell the granddaughter a hospital rider in 2026.

The strategic reframing happening inside Thai Life over the past five years has been, in essence, this: we are not a life insurance company that sells some health products. We are a household financial and medical services platform that uses life insurance as the anchor relationship. The language is softer in official communications, but the internal strategy has been clear. The Thai Life Insurance Application—the company's customer-facing mobile app—has been built out from a simple policy-servicing tool into something more ambitious: a digital front door for health services. Policy documents, yes. Premium payments, obviously. But also access to a network of partner hospitals and clinics, appointment booking, telemedicine consultations, and, critically, medicine delivery partnerships that drop prescriptions at the door of a policyholder whose rider claim has just been approved.

If that sounds familiar, it should. The playbook borrows liberally from what Ping An built in China over the 2010s with Good Doctor, and what AIA has been building through its Vitality wellness partnership, and what Discovery Group pioneered in South Africa decades earlier. The insight is that an insurance company with a 20-year relationship to a customer already owns the most valuable thing in healthcare: continuity. A one-off clinic visit does not let a hospital know what you were diagnosed with five years ago; your insurer does. If the insurer can credibly act as an orchestration layer—steering you toward the right provider, at the right price, at the right time—the value accretion is enormous, both to the customer and, through reduced claims costs, to the insurer.

The piece of this that is uniquely Thai Life, and uniquely misunderstood by outsiders, is the "Agent 2.0" model. When people hear "digital transformation" in insurance, they tend to imagine chatbots replacing humans, AI underwriting replacing agents, and mobile apps replacing distribution networks. Thai Life's conclusion, arrived at through a decade of experimentation, was essentially the opposite. Technology was most valuable in the business when it made agents more effective, not when it replaced them. The agent today walks into a Thai household carrying an iPad loaded with the full product shelf, real-time underwriting tools, biometric customer onboarding, claims status dashboards, and a rolling feed of customer life events—a child's birthday, a policy anniversary, a coming tax deadline—that prompt natural conversation and cross-sell opportunities.

This is the "Human Digital Transformation" in practice. It is not a buzzword. Measured operationally, agent productivity (premium per agent per year) has risen meaningfully since the tools were rolled out. Customer Net Promoter Scores—the blunt but useful measure of whether a customer would recommend the service—have improved. And, critically, the mix of products sold has shifted: agents equipped with better tools sell more health riders, more investment-linked policies, and fewer of the lowest-margin traditional products. The technology, properly deployed, made the agent force more consultative and less transactional.

The segmental math bears this out. While headline life premium growth has been in the low-to-mid single digits in any given recent year, the health and rider lines have compounded at multiples of that pace. The margin on health riders, because of their short-duration, repricing-friendly nature, is structurally higher than on traditional life. Over time, the mix shift from traditional to health is doing to Thai Life's earnings profile what it has done for every major Asian insurer that has successfully executed the pivot: it is converting a steady, low-growth, capital-intensive book into something that looks more like a specialty financial services business with meaningful repricing power.

One important footnote for diligent investors. The Thai private healthcare system, while outstanding, is not inflation-proof. Medical claims inflation in Thailand has been running faster than general inflation, and faster, at times, than the price increases insurers can push through on existing books without regulatory friction. This is a known issue industry-wide. Thai Life's response has been to lean into shorter-duration, annually renewable health products where repricing is straightforward, rather than long-duration guaranteed-benefit products where the insurer eats the medical inflation. The strategic direction is the right one; the execution risk is ongoing and worth watching. And this is why the KPI discussion, which we will turn to shortly, matters so much.

VII. The Hamilton 7 Powers & Porter's 5 Forces Analysis (1:45 – 2:00)

Hamilton Helmer's 7 Powers framework is the analytical lens our long-term investor audience has probably encountered most often, and for good reason. It forces you to ask, for any business, the blunt question: what is the durable structural advantage here, if any? Let us apply it to Thai Life.

The most important power is Cornered Resource. The 70,000-agent distribution network qualifies, and it is genuinely rare. You cannot hire 70,000 insurance agents by writing a check, because the value of the network is not in the headcount but in the embedded relationship capital—the accumulated trust that each agent has built, over years or decades, with hundreds of households in a specific neighborhood, village, or professional community. Asian insurance history is littered with attempts by well-funded entrants to build agent forces at scale; the typical outcome is a high-churn, low-productivity sales organization that burns capital for five years and then either closes or pivots. Thai Life's agent force is a 50-year compounding effort, underwritten by the cultural and operational choices described earlier. That is what a Cornered Resource looks like.

The second power is Brand. We discussed the tearjerker ads. In emerging markets, where most financial products feel interchangeable and regulation cannot fully distinguish a good insurer from a bad one, brand trust is a pricing lever and a persistency lever. Thai Life's brand equity, as measured by independent surveys of Thai households, sits at or near the top of every financial services category. The emotional resonance is measurable, and it shows up in the ability to charge policyholders a modest premium for the same actuarial product that a less-trusted competitor offers.

The third is Switching Costs. Life insurance is, by its structural nature, one of the stickiest consumer products ever invented. A 20- or 30-year contract that locks in mortality pricing at the age of underwriting creates an enormous penalty for switching; by the time a policyholder is 45, the premiums on a replacement policy would be materially higher because of age and accumulated health conditions. Once the policy is written, the customer is, economically, a captive for life.

Process Power is present to a modest degree—the persistency-focused agent compensation system and the integrated digital-human operating model qualify—but it is not the primary source of advantage. Economies of Scale exist in the investment management and the back-office, but Thai Life is not the largest insurer in Asia, so scale is relative rather than absolute. Network Economies are absent in the pure form. Counter-Positioning, by contrast, is one of the more interesting recent powers to consider. Thai Life's strategic commitment to the agent channel while competitors chased bancassurance is a textbook example of Counter-Positioning: a move the incumbent competitors cannot easily copy without cannibalizing their own chosen distribution strategies.

Porter's 5 Forces analysis reinforces the picture. Barriers to Entry in Thai life insurance are high—a combination of regulatory capital requirements, the multi-decade time horizon to build distribution, the cost of regulatory compliance, and the trust-based nature of the product. Bargaining power of suppliers is moderate; reinsurers and asset managers are the key suppliers, and Thai Life's scale gives it reasonable negotiating leverage, though not dominant. Bargaining power of customers is low in any individual-policy context—a single customer has effectively no leverage—but regulatory protections give the collective customer base indirect power through policy standards and conduct rules. Threat of substitutes is modest; in Thailand, the main substitute is the family itself, as we discussed, but as urbanization and nuclearization of households continue, this substitute weakens over time, which is actually a tailwind for the insurer. Rivalry is the most interesting: Thai Life competes domestically with AIA Thailand, Allianz Ayudhya, Muang Thai Life, FWD, and others. The market is fragmented enough that no single player can dictate pricing, but concentrated enough that irrational competitive behavior is rare.

Against this framework, the KPIs that long-term investors should track are surprisingly few. First, new business value, or NBV, which measures the value created by policies sold in a given period, adjusted for capital consumed. NBV is the closest insurance analogue to the earnings power of the sales engine. Second, value of in-force business, the stock metric that captures the compounding economic value of policies already on the books. And third, the health and rider premium growth rate, as a proxy for how successfully the mix shift toward higher-margin products is progressing. These three numbers, watched over quarters and years, reveal far more about the trajectory of the business than headline premium or statutory profit.

Behind the power framework sits a simpler intuition. Thai Life is, to use a phrase we tried out at the start, a Trust Utility. It is the institutional version of a family obligation, and its moat is ultimately the accumulated credibility of eight decades of paying claims.

VIII. The Playbook: Lessons for Founders and Investors (2:00 – 2:15)

Every Acquired episode, by unwritten convention, closes with lessons, and Thai Life's story offers unusually rich ones. They fall, we think, into four buckets.

The first is Counter-Positioning under consensus pressure. Through the 2010s, global insurance industry consensus was that agent forces were a cost center to be minimized and distribution should migrate to banks and digital channels. Thai Life disagreed, backed its disagreement with capital, and now sits with a durable moat that the consensus-followers cannot easily replicate. The lesson for operators and investors is not "always go against consensus"—that is a recipe for being wrong expensively—but rather to notice the specific conditions under which a contrarian stance is structurally defensible. In Thai Life's case, the cultural characteristics of the customer base, the regulatory friction around cross-border digital financial services, and the long-duration nature of the product all pointed toward human distribution being advantaged rather than disadvantaged. The strategic judgment was not "humans are better than algorithms everywhere"; it was "humans are better than algorithms here, for this product, for these customers."

The second lesson is the value of Slow Capital. Eight decades of private family control, followed by a decade of strategic partnership with a conservative Japanese anchor, followed by a public listing: that sequence is nearly the opposite of the modern startup journey, where companies are publicly listed while still unprofitable and are then expected to manage quarterly earnings. Thai Life's leadership could make the multi-year, multi-decade decisions—about agent compensation, about product mix, about technology investment—that are nearly impossible to make under quarterly-earnings pressure. The premium that public markets typically assign to high-quality compounders is often a recognition that such capital allocation is structurally rare and structurally valuable. Family-controlled public companies with aligned professional management sometimes earn that premium because they can actually behave like long-term owners.

The third lesson is what we have been calling the Tear-Jerker Alpha. Emotional branding in financial services is not a frivolous marketing expense; in markets where trust is the product, it is an actual financial moat. The measurable consequences—higher persistency, higher cross-sell rates, lower customer acquisition costs over the lifecycle, modest pricing premiums—are real and accrue to the bottom line. The global insurance industry has, at various times, convinced itself that the product is fundamentally a commodity and that distribution is fundamentally a cost-minimization exercise. Thai Life's forty-year experiment in emotional branding is a case study in the opposite view, and the financial results vindicate it.

The fourth and final lesson is actually a bear case, and honest investors need to sit with it. Thailand is entering a demographic phase that looks, structurally, like a slow-motion version of Japan in the 1990s. The total fertility rate has been below replacement for years. The working-age population has plateaued and will shrink over the coming decades. The dependency ratio is rising. This is the "Japan-ification" of Southeast Asia, and it has contradictory implications for a life insurer. On one hand, demand for retirement and health products rises as the population ages, which favors insurers. On the other hand, the pool of new customers—young workers buying their first policies—shrinks, and the asset pool of the insurer must be managed against a backdrop of structurally lower domestic growth and potentially lower interest rates. Japanese insurers spent two decades wrestling with this trade-off and came out smaller, more efficient, and more conservative. Thai insurers may face a similar journey.

Layered on top of the demographic pressure is the digital competitive threat. Regional super-app platforms—Grab, Sea Group's Shopee and SeaMoney, GoTo in Indonesia, and the quieter but well-funded Thai players—are all, to varying degrees, probing financial services. Insurance is, so far, the least penetrated vertical of that expansion, but that could change. Grab has built insurance distribution in Singapore and Malaysia. Sea has an insurance license in Indonesia. If one of these platforms decides to attack the Thai market seriously, the competitive calculus could shift. The bull case is that the super-apps can distribute simple, commoditized products well, but cannot replicate the consultative, high-touch relationships required for 30-year life insurance contracts. The bear case is that they do not need to; they can erode the margins on the simple products and force incumbents to chase profitability into ever-narrower segments.

A quieter risk worth naming is the interest rate environment. Thai Life's investment book, like every life insurer's, is dominated by long-duration fixed income. If Thai rates remain anchored at low levels for longer than the liability book assumes, spread compression eats into statutory profits. If rates spike sharply upward, unrealized losses on the bond portfolio can pressure the regulatory solvency ratio, even when the economic substance is fine. This is a manageable risk—reinsurers, actuarial reserving, and regulatory accommodations exist precisely for this purpose—but it is a real risk, and it is one of the reasons life insurance equities have historically traded at lower multiples than the pure economics would suggest. It is also a reason that watching the new business value growth and the health rider mix shift matters more than worrying about quarterly net investment income.

Finally, a governance note. The family's controlling stake is, on balance, a strength, but it is also a dependency. Strategic succession planning inside the Chaiyawan family is not a trivial matter, and while current management has been stable, any long-term investor in a family-controlled firm is implicitly underwriting the continued alignment between family interests and public shareholder interests. The record over the past decade has been good. It is worth continuing to watch.

IX. Conclusion (2:15 – End)

We started this episode with a scene on the floor of the Stock Exchange of Thailand on July 25, 2022—a company nobody outside Asia knew much about, walking into public markets during one of the ugliest IPO windows in a generation, raising roughly $1 billion because it chose to, not because it had to. We close with a question: what is Thai Life, really?

Our answer, having spent two hours inside the company's history, its strategic choices, its management, and its competitive landscape, is this. Thai Life is not primarily a legacy financial firm being disrupted by digital insurgents. It is a Trust Utility—the institutional manifestation of the Thai family safety net, built over 80 years, monetized across 30-year customer relationships, and defended by a moat of 70,000 human agents that no competitor can buy, clone, or out-spend. The technological pivot of the past decade has not replaced the moat; it has extended it, by giving the agents tools that make their consultative role more valuable, not less.

The forward question for investors is about the next playbook. The near-in expansion opportunity is the deepening of the health and wellness ecosystem inside Thailand—higher-margin products, stickier customer relationships, orchestration of the healthcare value chain. The further-out expansion, which management has signaled more quietly, is regional. The CLMV countries—Cambodia, Laos, Myanmar, and Vietnam—offer populations in aggregate larger than Thailand's, at earlier stages of insurance penetration, with cultural and linguistic proximities that make the Thai Life playbook at least partially portable. Myanmar has obvious political complications. Vietnam's insurance market is already crowded with large foreign entrants. Cambodia and Laos are small in absolute terms but underpenetrated. Whether and how the company pursues this expansion will be one of the defining strategic questions of the coming decade.

The broader lesson, for anyone building or investing in a company with a multi-decade horizon, is about the relationship between patience and power. The moats Thai Life relies on today were built in the 1970s, 1980s, and 1990s, long before any individual on the current management team occupied their office. They were built through thousands of small operational decisions—whom to hire as agents, how to compensate them, how to train them, which communities to prioritize, what kind of advertising to produce, how to settle claims, how to handle difficult cases—compounded over fifty years. None of those decisions, in isolation, looked like the founding of a moat. In aggregate, they were.

Public markets, by their nature, are impatient. They reward what can be measured this quarter. But the most durable franchises, the ones that earn the quiet admiration of long-term investors, are almost always the ones whose most important assets do not appear on the balance sheet at all. Thai Life's 70,000 agents do not show up as an asset on the financial statements. Neither does eight decades of accumulated brand trust in Thai households. Neither does the cultural fluency that allows an agent to sit at a Thai family's kitchen table and talk about death, illness, and legacy without the conversation feeling like a transaction. These are the real assets. They are the reason an 80-year-old family business, in a world of algorithms and super-apps, walked onto public markets in the middle of a bear market and raised a billion dollars.

That, finally, is the Thai Life story. A trust utility. A Cornered Resource. A Human Sovereign.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube