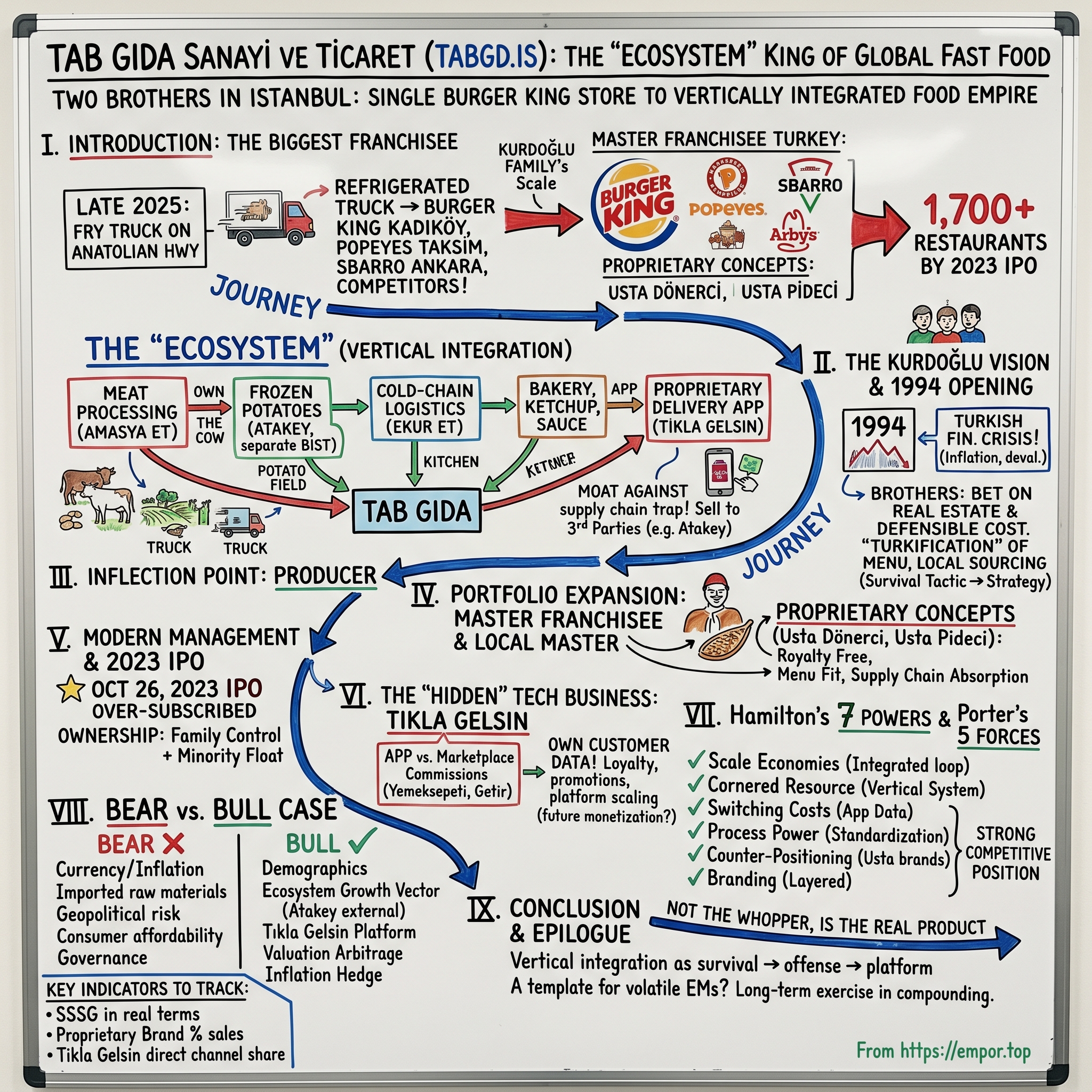

Tab Gida: The "Ecosystem" King of Global Fast Food

I. Introduction: The Biggest Franchisee You've Never Heard Of

It is late 2025, and somewhere on the Anatolian highway between Afyonkarahisar and Istanbul, a refrigerated truck rumbles east, its trailer humming at precisely minus eighteen degrees Celsius. Inside, thousands of kilograms of par-fried, golden potato sticks—cut to an exact nine-millimeter dimension that most diners will never consciously notice—bounce gently over the asphalt. In roughly fourteen hours, those fries will land in a Burger King in Kadıköy, a Popeyes near Taksim Square, a Sbarro in an Ankara mall, and, most tellingly, in the kitchens of several rival burger chains that would rather not advertise where their potatoes come from.

That truck, the potatoes inside it, the farm that grew them, the processing plant that cut them, the cold chain that moves them, and the restaurants that serve them all ultimately lead back to one company listed on the Borsa Istanbul under the four-letter ticker TABGD—Tab Gida Sanayi ve Ticaret A.Ş.

Ask the average American consumer about Burger King and they will picture an old-school Miami drive-through, a paper crown, maybe a flame-broiled Whopper. Ask a Turk, and they will describe something altogether different: not an American restaurant chain, but a local institution so thoroughly domesticated that younger Turks sometimes assume it is a Turkish brand. The reason is a family name most global investors have never heard: Kurdoğlu.

Here is the scale the Kurdoğlu brothers built. Tab Gida operated more than 1,700 restaurants across Turkey by the time it listed in 2023—making it, by store count, the single largest Burger King franchisee anywhere in the world, bigger than any operator in the United States, Brazil, or Western Europe. It is also the master franchisee for Popeyes, Sbarro, and Arby's in Turkey, and the creator of two proprietary concepts—Usta Dönerci and Usta Pideci—that sell traditional Turkish street food through modern quick-service kitchens.

But the restaurants are only the visible tip. What sits beneath them is the real story: a vertically integrated supply empire most outsiders call, somewhat grandly, "The Ecosystem." Meat processing at Amasya Et. Frozen potato production at Atakey (itself a separately listed BIST company with its own equity story). Cold-chain logistics through Ekur Et. A ketchup and sauce business. A bakery operation. A proprietary delivery platform called Tıkla Gelsin that competes directly with Yemeksepeti and Getir. Put simply: Tab Gida does not just flip burgers—it owns the cow, the potato field, the truck that moves them, the kitchen that cooks them, and the app that delivers them.

The thesis of this episode is elegant and, if you are a global consumer investor, worth sitting with for a minute. Most emerging-market franchise operators get destroyed by the same three-headed monster: currency devaluation that wrecks import-heavy cost structures, food inflation that outpaces menu repricing, and logistics fragility that turns every supply contract into a renegotiation. Tab Gida looked at that monster in the early 2000s and decided the only defensible answer was to absorb the supply chain entirely, then turn it around and sell its output to third parties. What began as a defensive crouch against Turkish macro volatility became an offensive moat, and eventually, a business model that global brands like RBI and Jubilant Foodworks now openly study as a template.

To understand how any of this happened, you have to start before the first Whopper was ever sold in Istanbul, with two brothers who made a bet on a burger in the middle of a currency crisis.

II. The Kurdoğlu Vision & The 1994 Opening

Picture Istanbul in the early 1990s. Inflation was running in the double digits on its way to triple digits. The Turkish lira was being devalued so routinely that merchants updated prices weekly, sometimes daily. The Istanbul skyline was still dominated by minarets and mid-rise apartment blocks, not the skyscrapers that now crowd the Bosphorus. And the idea of a Turk paying the equivalent of a day's wage for an American-style hamburger would have struck most observers as either foolish or, at best, extremely premature.

Into that environment walked Erhan and Korhan Kurdoğlu. The brothers came from a merchant-class Istanbul family that had operated in trade and industrial goods for decades—not in restaurants, not in food, not in anything consumer-facing. What they had was something harder to acquire than industry expertise: a deep, visceral understanding of operating under Turkish macroeconomic volatility, a network of relationships across Anatolian manufacturing, and the particular psychological temperament that allows an entrepreneur to see opportunity in a currency crisis.

Erhan, the elder brother, was the strategic architect—a systems thinker who, according to people who worked with him in the early years, would rather spend three weeks modeling a procurement decision than three days. Korhan was the operator, the one who walked the floors, who memorized unit economics down to the gram of lettuce, and who, legend holds, could tell you within two lira what a store's daily food cost would be before the register closed. Together they formed the classic high-functioning sibling duo that shows up surprisingly often in long-lived family empires.

In 1994, they acquired the master franchise rights for Burger King in Turkey. The timing was, on paper, disastrous. Turkey was deep in the 1994 financial crisis, with the lira losing more than half its value against the dollar inside a single year, interest rates spiking to near-triple digits, and a full-blown banking panic gripping the country. Any conventional investment banker would have told the brothers to wait. They opened the first Burger King in Istanbul anyway.

The reasoning, which becomes central to understanding everything that followed, was counterintuitive but proved prescient. The Kurdoğlus bet that the real estate they needed would be cheapest exactly when nobody else wanted it. They bet that the franchise economics they were negotiating with Burger King's international arm would be most favorable when the dollar-denominated royalty stream looked riskiest to the franchisor. And they bet that by the time Turkey stabilized—which it always eventually did, in their view—they would own the plum locations and the most defensible cost structure in the category.

All three bets paid off. But the more important decision was not where to open, it was how. From almost the first store, the Kurdoğlus refused to treat Turkey as a pure cut-and-paste export market for the American model. They pushed hard on "Turkification"—introducing menu items adapted to local palates, accepting modifications to the global playbook that Burger King's corporate parent tolerated only because emerging-market frontier stores were considered experimental, and crucially, insisting from the very beginning on local sourcing for inputs that other global franchisees would have simply imported.

That insistence was not driven by any grand strategic vision yet; it was driven by math. Importing frozen beef patties from Europe cost two to three times what equivalent locally produced patties cost, and currency devaluation meant those import costs were also a moving target. In a country where a Whopper had to be priced to a local wage base—not an American one—importing inputs was not just expensive, it was structurally impossible if you wanted to scale.

In other words, before vertical integration was a strategy, it was a survival tactic. And that tactical seed, planted in the soil of a currency crisis, would over the next three decades grow into one of the most impressive vertically integrated consumer operations anywhere in the emerging markets.

What happened next was the inflection point where a franchisee stopped being a franchisee and started becoming something else entirely.

III. The Inflection Point: From Franchisee to Producer

By the early 2000s, Tab Gida had grown from a single Istanbul Burger King into a few hundred locations across Turkey. It was, by any honest accounting, already a highly successful franchise operation. The Kurdoğlus could have stopped there, collected their fees, paid their royalties, and run a nice profitable middle-market business. Most franchisees do exactly that.

But they kept running into the same wall. Every time the lira cracked—and it cracked repeatedly, with notable episodes in 2001 and again during the 2008 global financial crisis—their gross margins evaporated overnight. A store that was profitable on Monday could be structurally unprofitable by Friday if beef prices from a European supplier repriced. Their 3PL logistics providers, operating at scale across industries, quoted rates that assumed dollar-linked fuel, dollar-linked equipment financing, and dollar-linked replacement costs, all of which got passed directly to Tab Gida.

There is a concept in emerging-market consumer investing sometimes called the "Supply Chain Trap." It describes the situation where a franchisee or licensee is locked into a global brand's quality and consistency standards—you cannot serve a Whopper that looks nothing like a Whopper—but has no control over the cost base that produces those standards. You are forced to deliver a globally consistent product using locally volatile inputs. The franchisor keeps its royalty. You keep the currency risk. Over time, either you raise menu prices beyond what local consumers will pay, or you compress your margins toward zero.

The Kurdoğlus' insight, and the thing that separates Tab Gida from the hundreds of other emerging-market franchise operators that never escaped the trap, was recognizing that the only durable answer was to own the inputs themselves. Not to hedge them, not to diversify suppliers, but to build the supply chain.

The first and most important move came with Amasya Et Entegre, the company's integrated meat processing facility in Amasya, a north-central Turkish province with strong cattle farming traditions. Rather than buy finished patties from European processors, or even buy finished Turkish beef from local abattoirs, Tab Gida built an operation that receives live cattle, handles slaughter and butchering to internationally recognized HACCP and ISO standards, and produces a portfolio of formed meat products—burger patties, breakfast sausage, chicken items processed in segregated lines—tailored directly to the needs of its restaurant concepts.

The economics here are worth pausing on. Meat is typically the single largest cost line in a fast-food restaurant's food cost, often 30 to 40 percent of total food spend. By controlling slaughter through processing, Tab Gida captured the margin that would otherwise have gone to three or four intermediaries, and more importantly, it neutralized its currency exposure on beef. Cattle are purchased in lira from Turkish farmers. Feed, labor, and processing are paid in lira. The only dollar-linked elements are some equipment, some packaging, and some additives—a minority of the cost stack.

Then came Atakey Patates Gıda, the potato processing facility in Afyonkarahisar, a region in western Anatolia whose climate and soil composition happens to be exceptionally well suited to growing the Russet-style potatoes that produce the long, stiff fries Western QSR menus demand. Atakey takes raw potatoes from contracted Turkish farmers, washes and cuts them to precise specifications, par-fries them, freezes them, and packages them for distribution. It is a capital-intensive operation—a serious French-fry plant costs in the hundreds of millions of dollars to build and equip—but once running, it produces fries at a cost structure that, by industry estimates, ran roughly 25 to 35 percent below the landed cost of imported frozen fries from European suppliers like Lamb Weston or McCain.

Atakey was strategically important for two reasons beyond cost. First, it gave Tab Gida genuine leverage over a category—frozen fries—where global supply is dominated by a handful of Western giants with their own pricing power. Second, and this is where the story starts getting interesting for investors, Atakey was built with excess capacity. That excess was not a mistake. It was a plan. Tab Gida intended from the outset for Atakey to sell into the broader Turkish foodservice market, including to Tab Gida's direct competitors. Why? Because fry supply from a Turkish plant with local scale was genuinely cheaper than import, and every kilogram of Atakey product sold to a competing burger chain was a kilogram that made Atakey's fixed-cost absorption better, lowered the effective cost of Tab Gida's own fries, and subtly degraded competitors' cost advantage against Tab Gida.

Atakey was eventually carved out and listed separately on the BIST, becoming its own public-markets story. That spin-and-list move accomplished two things simultaneously: it unlocked embedded value in a subsidiary that investors could finally price on its own multiples, and it established Atakey as a credible independent supplier in the eyes of third-party customers who might have been reluctant to buy fries from a fully captive affiliate of a burger chain.

Rounding out the early ecosystem, Ekur Et provided the cold-chain logistics layer—refrigerated trucking, distribution centers, and the temperature-controlled warehouse network that connects the Amasya and Afyon plants to 1,700-plus restaurants across a country that stretches roughly 1,600 kilometers from Edirne to Kars. Cold chain is the quiet infrastructure of any national QSR system, and its quality determines everything from food safety to menu consistency. By running cold chain in-house, Tab Gida eliminated one more pocket where a third-party provider could either fail during a lira-crunch or charge a dollar-linked premium that would eventually destroy the P&L.

What emerged from these moves—Amasya Et, Atakey, Ekur Et, and a supporting cast of bakery, sauce, and ingredient operations—was something more ambitious than cost engineering. It was a fully closed loop: a restaurant company that could, in principle, be cut off from the global food supply chain tomorrow and continue operating with almost no disruption. In a country whose macro history teaches every businessperson to plan for the worst, that optionality is not a theoretical luxury. It is the entire point.

And with that infrastructure in place, Tab Gida was no longer just running one brand. It was ready to run a portfolio.

IV. Portfolio Expansion: Popeyes, Sbarro, and Local Mastery

There is a moment in the life of every successful franchisee where the operator looks up from their one brand, surveys the capability they have built, and asks a dangerous question: what else could we run on this platform? Dangerous, because the graveyard of emerging-market consumer companies is littered with operators who took that step and discovered that their capability was less portable than they thought. Running Burger King is not the same as running a Thai-food concept, and a cold chain calibrated to beef patties may not be the right system for handling live seafood.

Tab Gida answered that question carefully. Starting in 2007, the company added Popeyes Louisiana Kitchen to its portfolio as the Turkish master franchisee, giving it a chicken-focused concept that shared kitchen DNA with Burger King but hit a different menu occasion. Popeyes rode the global chicken sandwich boom—a category that exploded across the 2010s and early 2020s as consumer preferences shifted away from beef for a mix of health, price, and cultural reasons. In a country where chicken consumption grew faster than beef for most of the past decade, adding Popeyes was less a diversification bet than a hedge on Turkish protein preferences.

Then came Sbarro, the American-Italian pizza-and-pasta chain, bringing mall-food-court economics into the portfolio. Malls were, and largely still are, the primary high-traffic QSR real estate channel in Turkey's largest cities, and controlling multiple concepts within the same food court gave Tab Gida real pricing power in lease negotiations. Arby's, focused on roast beef and sandwiches, added another wedge. Each brand paid its royalty to its respective US or global parent, but each brand also plugged into Tab Gida's pre-existing supply chain—Amasya's meat, Atakey's potatoes, Ekur's logistics—giving the new concepts a cost advantage from day one that a standalone local franchisee could never have matched.

But the more interesting move, and the one that reveals the most about management's strategic evolution, was the launch of proprietary concepts. Usta Dönerci brought the classic Turkish döner kebab—the spit-roasted lamb or chicken carved onto bread or rice plates that is arguably the national QSR dish—into a modern, branded, standardized format. Usta Pideci did the same for pide, the boat-shaped Turkish flatbread often described in Western menus as Turkish pizza. Both were built from scratch, owned entirely by Tab Gida, and sold exclusively through Tab Gida's own infrastructure.

Why build proprietary brands when you already have a stable of successful imported ones? Three reasons, each of which matters for how investors should think about Tab Gida's long-run margin structure.

First, royalty economics. A typical master franchise relationship sends meaningful royalties—often in the mid-single-digit percentage of system sales—back to the US or global parent. For Burger King, that means Restaurant Brands International (RBI). For Popeyes, also RBI. For Sbarro, its corporate parent. Those royalties are the price of access to a globally recognized trademark and system, and they are worth paying, because local operators cannot realistically build equivalent brand awareness at that cost. But every lira of sales that runs through a proprietary brand like Usta Dönerci flows back to Tab Gida entirely. Over time, as the proprietary concepts scale, the weighted-average royalty load on the system drops, and reported margins improve without any changes to unit-level economics.

Second, menu and cultural positioning. Turkey has one of the world's great street-food traditions. Döner, pide, köfte, lahmacun, mantı—these are not fringe ethnic items for Turkish consumers the way they are in Western markets. They are mainstream, daily-consumption food. By offering Turkish food through a QSR format, Tab Gida captured consumption occasions that Burger King and Popeyes could never win, particularly at lower price points and in smaller-town markets where an American brand still carries a modest price premium.

Third, and most strategically, supply chain absorption. Proprietary concepts could be designed, from the menu up, to maximize use of Tab Gida's existing ecosystem. A pide concept needs flour (in-house bakery), meat (Amasya), vegetables (contracted), and cheese. That utilization lowers the unit cost of every input for every other concept in the system, because fixed costs at Amasya and the bakeries get absorbed across a larger production volume.

The segment-level implication is that Tab Gida's reported margins are not a single, homogeneous figure. They are a blend of the anchored-but-royalty-paying international brands, which are lower margin per dollar of sales but offer enormous brand pull and store-opening velocity, and the proprietary Turkish concepts, which are higher margin but require more internal brand-building investment. As the proprietary mix grows, the weighted blend quietly improves. It is the kind of embedded operating leverage that does not show up cleanly in headline revenue growth but compounds meaningfully into EBITDA over a decade.

This portfolio construction—international anchors plus proprietary growth engines, all sharing the same vertical supply chain—is the real moat. And it is precisely the kind of moat that becomes investable only when a company is ready to tell its story to public markets.

V. Modern Management & The 2023 IPO

On October 26, 2023, the opening bell of the Borsa Istanbul rang for Tab Gida. After more than a decade of rumored public offerings, internal debates about timing, and the rolling chaos of a Turkish lira that had shed roughly three-quarters of its value against the dollar over the preceding half-decade, the Kurdoğlu family finally took their company public. The IPO was heavily oversubscribed, reflecting intense domestic demand for listed consumer assets and, to a lesser extent, foreign investor interest in a rare, scaled, vertically integrated emerging-market QSR operator.

The decision to list was not made lightly. Erhan Kurdoğlu, by then in his capacity as Chairman, had reportedly been reluctant for years. Family-controlled Turkish conglomerates have a long and somewhat ambivalent relationship with the BIST—public listings bring capital and currency (BIST shares are a real form of M&A currency in domestic deals), but they also bring disclosure, scrutiny, and the continuous pressure of quarterly markets in a country whose macro volatility makes quarterly stability essentially impossible to promise.

Several things shifted the calculus by 2023. First, the sheer scale of the enterprise—1,700 restaurants, a multi-plant vertical supply chain, thousands of employees, and increasingly complex intra-group transactions—meant that keeping the business private was creating its own governance costs. Second, Atakey had already been listed separately, creating a partial template for how public disclosure could work inside the ecosystem without destroying strategic optionality. Third, and perhaps most importantly, Turkish retail investors had developed a voracious appetite for domestic equities during the lira-depreciation cycle, with equity ownership serving as a partial inflation hedge. Launching into that demand environment gave the IPO its oversubscription.

The post-IPO ownership structure preserved the Kurdoğlu family's effective control while bringing in a meaningful float. The family retained majority economic ownership, with their interests held through holding vehicles, and floated a minority stake into the BIST. That structure is common among Turkish family conglomerates and important for understanding governance. Minority public shareholders are co-owners with the family, not independent majority owners of the enterprise. For long-term investors, that is neither automatically good nor bad—plenty of family-controlled businesses generate outstanding long-run returns, and plenty do not—but it does mean capital allocation decisions will reflect family preferences, not pure short-term shareholder-value optimization.

The management team is a mix of Kurdoğlu family members in strategic chairmanship and board roles, and professional executives in day-to-day operating leadership. This professionalization trend has been gradual but real. In the early years, Tab Gida was substantially run on family judgment; by the time of the IPO, the operating functions—supply chain, restaurant operations, digital, finance—were led by professional managers recruited from multinational FMCG companies, global QSR brands, and Turkish banking. The Chairman's role became more about capital allocation, major M&A decisions, and the overall ecosystem strategy, rather than daily operating calls.

There is a particular incentive structure inside Tab Gida that is worth flagging, because it is not always obvious from the outside. Restaurant managers in most global QSR systems are incentivized primarily on top-line sales growth and store-level profitability. Tab Gida's system layers on ecosystem-level metrics—what percentage of a store's inputs came through internal supply, what waste rates looked like against the integrated benchmark, how efficiently the store's operating schedule aligned with delivery-platform demand peaks. The intent is to make restaurant managers think like ecosystem operators, not just store operators, and to prevent the classic franchisee pathology where store managers optimize their P&L at the expense of system-level efficiency.

A brief aside on governance. In any family-controlled Turkish holding, investors should always read the related-party transaction disclosures carefully. Tab Gida's structure naturally involves significant intra-group flows—meat from Amasya to the restaurants, fries from Atakey, logistics from Ekur, and so on. The company discloses these flows in its annual and quarterly filings, and the transfer pricing is audited. But the sheer density of internal transactions means minority investors have to trust, to some meaningful degree, that intra-group pricing is set at arm's length and does not systematically disadvantage the listed entity in favor of other family-held vehicles. This is not unique to Tab Gida; it is a feature of virtually every vertically integrated holding-company structure. It is simply something to monitor over time.

With public-markets discipline now layered on top of the Kurdoğlu legacy, attention has shifted toward what may be the next phase of value creation: the digital and platform side of the business.

VI. The "Hidden" Tech Business: Tıkla Gelsin

If Amasya Et is the most visible arm of the Ecosystem and Atakey is the most financially interesting, then Tıkla Gelsin—literally "Click and Let It Come"—is the most quietly subversive. It is Tab Gida's proprietary digital ordering and delivery platform, and while it does not attract the breathless coverage that a venture-backed Turkish food-delivery startup would, it may well be the asset within the group with the highest long-run optionality.

To understand why Tıkla Gelsin matters, you have to understand the Turkish delivery landscape. For most of the 2010s, food delivery in Turkey was dominated by Yemeksepeti, a local pioneer that built a strong two-sided marketplace and was eventually acquired by Delivery Hero in a landmark transaction. Alongside it emerged Getir, the ultra-fast grocery and food-delivery platform that became briefly one of the most valuable private companies in Europe during the 2021 venture bubble, before retrenching dramatically during the subsequent global correction. Both of these platforms had scale, both had consumer brand recognition, and both sat between restaurants and their customers, taking a cut of every order and, more importantly, owning the customer relationship.

For a chain the size of Tab Gida, that dynamic was untenable. Every order placed through Yemeksepeti or Getir generated a commission leakage—typically in the mid-teens to low-twenties percent of order value—that compounded across millions of orders per year into a serious P&L drag. Worse, every order through a third-party marketplace meant the customer's ordering behavior, frequency, menu preferences, and lifetime value belonged to the platform, not to Tab Gida. The restaurant brand was being disintermediated.

Tıkla Gelsin was the answer. Originally built as a modest in-house ordering system, it evolved into a full consumer-facing app available across iOS and Android, integrated with all of Tab Gida's restaurant concepts, backed by the company's own riders and logistics where feasible and by third-party riders where not, and crucially, tied to a unified loyalty and promotion infrastructure that only the company itself could operate.

The economics of owning the platform are stark. Every order that moves from a third-party marketplace to Tıkla Gelsin saves the commission that would otherwise be paid to the marketplace. At Tab Gida's scale, even a modest percentage shift in channel mix compounds into meaningful operating income. But the more important benefit is data. When an order flows through Tıkla Gelsin, Tab Gida knows—at the household level, over time—who is ordering, what they are ordering, how their preferences change, how sensitive they are to promotions, and when they are most likely to churn. That data feeds back into menu design, promotional targeting, new-location analysis, and, increasingly, into advertising partnerships with CPG brands that want access to specific consumer segments.

There is also a simple but underrated economic point: in a digital platform, fixed costs scale much better than marketplace commissions. A third-party marketplace takes a percentage of every order forever. A proprietary platform has engineering and infrastructure costs that are largely fixed and amortize across a growing order base. As Tıkla Gelsin's order volume grows, the unit cost of processing each order declines, while marketplace commissions would have stayed roughly constant as a percentage of order value.

For investors, the most useful mental model is to think of Tıkla Gelsin as a Trojan horse inside what looks like a restaurant company. The headline business is QSR. The hidden business is a direct-to-consumer data platform with tens of millions of customer touchpoints per year, proprietary ordering flow, first-party payment data, and an addressable market that extends beyond Tab Gida's own restaurant brands. The long-run optionality—opening the platform to third-party restaurants, layering in retail media monetization, partnering with CPG brands—is real, even if none of it is yet priced into the equity.

Layering Tıkla Gelsin onto the physical ecosystem produces something closer to a consumer operating system than a fast-food company. And that framing matters enormously for how any serious competitive analysis of the business should be structured.

VII. Playbook: Hamilton's 7 Powers & Porter's 5 Forces

Tab Gida's moat is one of the most textbook-worthy case studies in emerging-market consumer investing, precisely because the company's advantages are so clearly decomposable along the standard frameworks. Running Tab Gida through Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces is not just an academic exercise—it reveals why the business has proven so difficult for local and global challengers to attack.

Start with scale economies, the most obvious of the seven powers. Tab Gida operates more than 1,700 restaurants in a single country, which means when it procures beef, potatoes, chicken, flour, or packaging, it does so at a volume no Turkish competitor comes close to matching. That scale shows up twice: first in direct procurement leverage with third-party suppliers, and second in the utilization of its own internal plants. A meat plant or fry plant that runs at 90 percent capacity has materially lower per-unit costs than one running at 60 percent. Competitors face a brutal catch-22—they would need Tab Gida's scale to justify building their own ecosystem, but they cannot build Tab Gida's scale without the cost advantage that the ecosystem provides.

Cornered resource is the next and most interesting power in this case. The "Ecosystem" itself functions as a cornered resource. No other Turkish QSR operator owns the entire value chain from livestock to delivery app. Even global giants operating in Turkey through their local partners typically rely on a mix of third-party suppliers, imported inputs, and external logistics. Tab Gida's integrated closed loop cannot be replicated on a reasonable timeline or at a reasonable cost. Even if a well-capitalized competitor decided to try, they would need roughly a decade to build comparable plants, contract comparable farmer networks, develop comparable logistics, and train comparable operating teams. Ten years in the Turkish QSR market is forever.

Switching costs show up most clearly inside Tıkla Gelsin. The loyalty program, the saved payment credentials, the household-level order history, and the promotional targeting built on that data all raise the effective cost to a consumer of switching to a rival platform. Switching costs in food delivery have historically been lower than in, say, software or banking, but they compound quietly over time, particularly when paired with systematic promotional investment aimed at lock-in.

Process power is the most underrated of Tab Gida's moats and the hardest for competitors to observe from the outside. The company has industrialized the process of opening new restaurants, standardizing everything from site selection criteria to kitchen equipment specifications to staff training curricula. A new Burger King can go from signed lease to open door in a matter of weeks—an operating cadence that most franchise systems cannot match, particularly in regulated emerging-market environments with complex local permitting. The accumulated, tacit knowledge embedded in those operating manuals, training programs, and internal systems is a form of process power that does not appear on any balance sheet.

Counter-positioning is where the proprietary brands Usta Dönerci and Usta Pideci come in. Traditional kebab shops and pide restaurants in Turkey have operated on a time-honored model: independent, owner-operated, variable quality, cash-heavy, and largely un-digitized. That model has enormous cultural authenticity but terrible scaling economics. By applying modern QSR operational discipline to traditional Turkish food, Tab Gida occupies a position that legacy local operators cannot credibly attack—imitating Tab Gida's systems would require those operators to abandon the exact qualities (independence, artisanship) that differentiate them in the first place.

Branding shows up as a layered asset. Burger King, Popeyes, and Sbarro contribute their globally recognized brand equity, at the cost of royalties. The proprietary Turkish brands are building local brand equity from scratch but royalty-free. Tıkla Gelsin builds a different kind of digital brand. The blend is unusually diversified for a QSR operator.

Network economies, the seventh power, are weaker in Tab Gida's case than the others, though they exist in attenuated form within Tıkla Gelsin, where a larger customer base attracts more restaurant partners, which in turn attracts more customers.

Running the Porter's Five Forces lens reinforces the conclusion. Supplier power is low for Tab Gida because the company has absorbed most of its strategic suppliers; the ones it has not—packaging, certain additives, some equipment—are commoditized or come from multiple competing sources. Buyer power is fragmented, since individual consumers have minimal bargaining leverage against a scaled QSR chain. Threat of new entrants is high in aggregate—QSR is an easy space to enter with a single store—but low at scale, because no new entrant can plausibly build 1,700 stores, an integrated ecosystem, and a digital platform without decades of capital and operating commitment. Threat of substitutes is real and ever-present: traditional Turkish street food, home cooking, cloud kitchens, and new entrants all compete for the same consumer stomach share. Industry rivalry among the existing global QSR operators in Turkey is real but bounded, since each player has its own brand niche.

The net picture is a company whose competitive position looks genuinely durable on frameworks that, by design, are quite skeptical. That still leaves the question of whether the business can compound through the next decade of Turkish macro turbulence and global consumer shifts.

VIII. The Bear vs. Bull Case

There is a particular intellectual honesty that investors in emerging-market consumer stocks eventually develop, which is the ability to hold the bear and bull cases simultaneously without flinching from either. Tab Gida, more than most names, rewards that kind of balanced view. The company is genuinely excellent at what it does; it also operates in an economy where excellence alone is not always enough.

The bear case begins with the single most important risk for any Turkish equity: currency devaluation and inflation. Over the 2018 to 2023 window, the Turkish lira lost roughly 80 percent of its value against the US dollar. For a company with dollar-linked obligations—most notably royalty payments to international franchise parents on Burger King, Popeyes, Sbarro, and Arby's sales—every lira of devaluation directly inflates the cost of those obligations in local terms. Tab Gida's vertical integration mitigates this pressure substantially by reducing the dollar exposure embedded in input costs, but it does not eliminate the royalty line, and it does not insulate the company from lira-denominated menu repricing lagging behind cost inflation. Any period where Tab Gida cannot pass through its input cost increases quickly enough produces margin compression.

Related is the risk that imported raw materials and capital goods, the residual dollar exposures, rise faster than the company can absorb. Packaging, specialty additives, equipment, and certain franchise-mandated inputs still come from abroad. In severe devaluation scenarios, those costs can spike even when the core beef and potato inputs are stable.

There is also geopolitical and regulatory risk. Turkey operates at the crossroads of several political flashpoints, and policy swings on everything from capital controls to foreign investment rules to tax regimes have historically been sharper than in most developed markets. A Turkish consumer business is, almost by definition, a bet on Turkey's long-run institutional stability, and reasonable people can disagree about that bet.

A subtler bear-case element is consumer affordability. QSR pricing has to track, roughly, what the Turkish middle class can afford as a daily or weekly treat. When real wages lag behind food inflation, which has happened repeatedly over the past several years, traffic softens even as the ticket size rises. Headline revenue growth during high-inflation periods can mask volume declines that eventually matter.

Finally, governance and related-party transaction risk deserve to be listed even if there is no current evidence of any issue. Family-controlled conglomerates with complex intra-group flows always carry the structural possibility that decisions favor the broader family interest rather than minority shareholders specifically. Long-term investors should read every related-party disclosure with care and track whether the public entity receives arm's-length economic treatment in its dealings with family-held siblings.

The bull case is just as substantial. Start with demographics. Turkey has one of the youngest, most urbanizing populations in the OECD orbit, with a median age in the low thirties and a continuing rural-to-urban migration trend. Young urban consumers are precisely the QSR target demographic, and Turkey still has meaningful white space for chain QSR expansion relative to more saturated Western European and North American markets.

Second, the Ecosystem is a growth vector, not just a cost shield. Atakey, now listed independently, is actively selling potato products to third-party customers inside and outside Turkey, effectively turning a former internal support function into a growing external revenue stream. Amasya Et, while primarily feeding the internal system, has capacity to serve external customers as well. The bakery, sauce, and other operations have similar optionality. Over time, the Ecosystem's internal scale advantage can become an external B2B business that is larger, higher-margin, and more stable than the restaurant operation that birthed it.

Third, Tıkla Gelsin's platform optionality is real and, as argued earlier, largely unpriced. A meaningful scaling of the platform into third-party merchants, retail media, and adjacent digital commerce would represent a step-change in how the market values the overall franchise.

Fourth, valuation arbitrage. Tab Gida trades on Turkish-market multiples, which tend to be significantly below those of comparable consumer operators in less volatile emerging markets. Jubilant Foodworks, the Indian Domino's master franchisee, typically commands a substantially higher EV/EBITDA multiple. Zamp (Burger King Brazil) operates in a different but comparable framework and has commanded higher valuations in its strong years. Even acknowledging the legitimate discount that Turkish macro risk deserves, the spread has historically been wide enough to reward investors willing to underwrite the macro risk.

Fifth, the inflation hedge characteristic of the business itself. QSR operators with strong pricing power and vertically integrated inputs are among the more resilient public-market exposures an investor can hold during inflationary episodes. That resilience is not unique to Tab Gida, but it is particularly pronounced in its case.

If you are trying to compress all of this into a small number of indicators to track over time, three stand out. The first is same-store sales growth in real (inflation-adjusted) terms—headline nominal growth in Turkey is deceptive, and the real figure tells you whether the business is actually gaining traffic and ticket, or merely repricing. The second is the proprietary-brand share of system sales, including Usta Dönerci, Usta Pideci, and any new domestic concepts, because that mix drives the weighted royalty load and thus the structural margin of the business. The third is Tıkla Gelsin order volume and direct-channel share, since the migration of orders away from third-party platforms to proprietary platform is one of the clearest near-term levers on both margins and the long-run equity story.

The Kurdoğlu story, and the Tab Gida story, has never been a single-moment story. It has been a thirty-year exercise in compounding small, patient decisions into an infrastructure that is now, clearly, more than the sum of its parts.

IX. Conclusion & Epilogue

Three decades after Erhan and Korhan Kurdoğlu opened the first Burger King in Istanbul during the middle of a currency crisis, the question that hangs over Tab Gida is not whether the company is well built. That question has been answered, in operating detail, many times over. The real question is whether Tab Gida is something more interesting: the template for how consumer businesses should be constructed in every emerging market where macro volatility, import dependency, and infrastructure fragility have historically made long-term consumer compounding almost impossible.

The Kurdoğlu answer—vertical integration as survival, then as offense, then as platform—is not obvious in the way most successful strategies are not obvious until they succeed. In the 1990s it would have seemed absurd for a Burger King franchisee to build a meat plant. In the 2000s it would have seemed excessive to build a fry plant. In the 2010s it would have seemed quixotic to build a proprietary delivery platform against well-capitalized venture rivals. Each step, viewed in isolation, looked like a franchisee overreaching its mandate. Viewed together, they look like a coherent, multi-decade thesis being patiently implemented.

The human story underneath matters. Erhan and Korhan built this not by following a Western consumer playbook, but by adapting that playbook for a country whose operating reality the playbook's original authors never had to face. They preserved family control long enough to execute the long-horizon capital plans that institutional boards would likely have rejected, and they professionalized management at the moment when the business outgrew family judgment alone. They timed an IPO for the moment when domestic retail-investor demand was at peak depth and when the enterprise was complex enough to genuinely benefit from public-market scrutiny.

For global investors, Tab Gida is neither a simple QSR bet nor a simple Turkish macro bet, and anyone trying to analyze it through only one lens will get it wrong. It is a vertically integrated consumer ecosystem with a proprietary digital distribution layer, attached to a Turkish macro environment that remains volatile enough to deter many international institutional flows. Those two characteristics are permanently in tension. In some environments the ecosystem dominates the narrative and the multiple; in others the macro dominates and the multiple compresses regardless of operating performance. Over a long enough horizon, operating excellence has historically won that contest, though not always smoothly, and not always on a schedule that would suit a patient investor's timeline.

Were you to sit in the CEO's chair tomorrow, the agenda would write itself. First, continue the slow migration of the business mix toward proprietary brands and proprietary channels, because every point of royalty saved and every point of platform commission internalized compounds for years. Second, begin to internationalize selected Ecosystem assets—Atakey's potato operation in particular has obvious export potential into nearby markets that lack comparable supply infrastructure. Third, treat Tıkla Gelsin as a platform company, not a restaurant feature, and invest in it with the capital and talent allocations that framing implies. Fourth, maintain the discipline that has defined the last three decades: do not chase adjacent categories that break the ecosystem thesis, do not overpay for growth, and do not let public-market pressure force decisions that the long-term strategy would reject.

The deepest lesson of Tab Gida may be the simplest. When your operating environment is volatile in ways you cannot control, the most valuable thing you can build is an internal system so self-sufficient that external shocks become survivable, and eventually, a source of advantage. The Kurdoğlu brothers figured that out in 1994, on the morning they decided to open a burger restaurant in the middle of a currency crisis. Everything since has been the long, patient unfolding of that original insight.

Which, in the end, is what makes Tab Gida one of the most interesting consumer stories in the global emerging markets today—and why the Ecosystem, not the Whopper, is the real product.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube