Sunrise Energy Metals: The Green Mining Machine

Introduction and Episode Roadmap

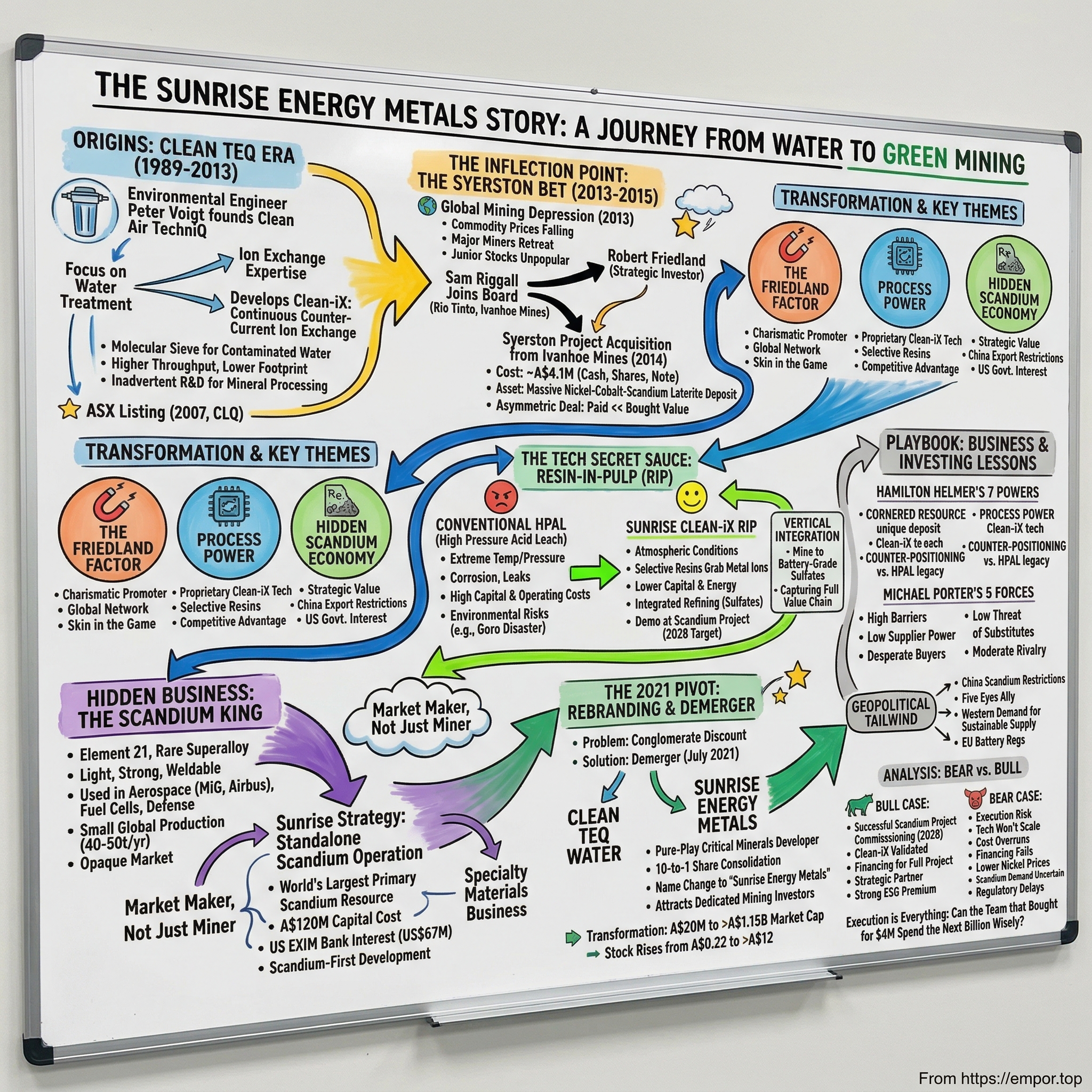

How did a small-cap Australian water treatment company end up owning the world's largest primary scandium deposit and one of the most strategically important battery metal projects in the Western world, for essentially four million dollars?

The answer involves a convicted drug dealer who once roomed with Steve Jobs, a river full of dead fish in Colorado, a six-billion-dollar mining disaster in the South Pacific, and a proprietary technology originally designed to clean drinking water. It is, in many ways, the quintessential mining story: part geological lottery, part technological ingenuity, part sheer audacity from a cast of characters who have spent decades operating at the volatile intersection of natural resources and capital markets.

Sunrise Energy Metals, listed on the ASX under the ticker SRL, sits today at a market capitalization of roughly A$1.15 billion. Its share price rocketed from around twenty-two cents to over twelve dollars in less than a year, a move of approximately five thousand percent. The company employs thirty-seven people. It has never produced an ounce of anything. And yet, some of the most sophisticated mining investors on the planet believe it could become the Western world's benchmark producer of sustainably sourced nickel, cobalt, and scandium for the next half-century.

Three themes run through the Sunrise story, and they are worth naming at the outset because they recur at every critical juncture.

The first is the "Friedland Factor," the gravitational pull exerted by Robert Friedland, arguably the most successful and controversial mining promoter alive, whose fingerprints are on every major decision the company has made.

The second is Process Power, the idea that in an industry where geology determines what you have, technology determines what you can do with it, and Sunrise possesses a proprietary processing technology that its competitors do not.

The third is the hidden economy of scandium, an element so obscure that most investors have never heard of it, yet so strategically valuable that China recently restricted its export, and the United States government has offered to help finance its production in Australia.

This is the story of how all three of those threads wove together, and what it means for the future of critical minerals.

Before diving in, a word on scale. The Sunrise project, at full development, would produce over 21,000 tonnes of nickel and 4,400 tonnes of cobalt per year for at least twenty-five years, plus scandium in quantities that would dwarf current global output. The deposit contains nearly a billion tonnes of ore. The feasibility study shows a net present value exceeding US$1.3 billion. And the whole thing was acquired for less than the cost of a family sedan. That asymmetry, between what was paid and what was bought, is the central tension of the Sunrise story. Understanding how it happened requires going back to the beginning.

Origins: The Clean TeQ Era

In 1989, in a nondescript office park somewhere in Melbourne's industrial southeast, an environmental engineer named Peter Voigt founded a small company called Clean Air TechniQ. The name tells you everything about its original ambition: this was a business born to solve mundane industrial problems, cleaning pollutants from air and water using specialized chemical processes. There were no visions of world-class mines or billion-dollar deposits. Voigt was building a services business, the kind of company that bids on municipal water contracts and sells engineered solutions to factories with wastewater problems. For a decade, it operated in quiet obscurity, generating modest revenues and attracting no attention from the broader investment community.

The business formally incorporated in 1990 and spent the next several years developing expertise in a family of technologies broadly known as ion exchange. The concept is elegant in its simplicity, and understanding it is essential to understanding everything that follows.

Imagine a filter made of tiny resin beads, each one chemically programmed to attract and hold specific atoms or molecules. Run contaminated water through the filter, and the resin grabs the unwanted particles, arsenic, heavy metals, dissolved salts, while letting the clean water pass through. It is, in essence, a molecular sieve, a technology that sorts atoms the way a coin machine sorts quarters from dimes.

Ion exchange itself was not new. The technology had been used in water softeners and industrial purification for decades. What made Clean TeQ's approach distinctive was a refinement called continuous counter-current ion exchange, eventually branded as Clean-iX.

Traditional ion exchange systems work in batches: you fill a column with resin, run water through until the resin is saturated with captured particles, then stop everything to flush and regenerate the resin before starting over. It is the same principle as wringing out a sponge, except the wringing process requires shutting down the entire system.

Clean-iX eliminated the stop-and-start cycle entirely. The resin and the liquid flowed continuously in opposite directions through the system, like two escalators moving past each other, one carrying dirty water down and one carrying loaded resin up. The process never needed to pause. For water treatment, this meant higher throughput, lower chemical consumption, and smaller physical footprints. A Clean-iX plant could process the same volume of water as a conventional system using a fraction of the equipment.

It was a genuinely clever piece of engineering. But in the water treatment market of the early 2000s, clever engineering alone did not translate to outsized returns. The industry was fragmented, margins were thin, and competition from established players like Veolia and Suez made it difficult for a small Australian firm to build meaningful scale.

The company listed on the ASX on November 8, 2007, under the ticker CLQ, as Clean TeQ Holdings Limited. The IPO was modest. The market barely noticed. At its listing price, Clean TeQ was valued at a few tens of millions of dollars, a rounding error in the context of the global water industry.

What nobody outside a small circle of metallurgists and process engineers had yet realized was that the same technology designed to pull impurities out of drinking water could, with some adaptation, pull high-value metals out of crushed rock.

The resin beads did not care whether they were grabbing arsenic from a municipal water supply or nickel ions from a slurry of laterite ore. The chemistry was fundamentally the same. The selectivity of the resins, their ability to target specific metal ions while ignoring everything else, worked just as well on mining feedstock as on contaminated groundwater.

Clean TeQ's water treatment business had been, without anyone quite intending it, a multi-year research and development laboratory for what would become a proprietary mining technology. Every contract to clean industrial wastewater, every pilot project for a municipal treatment plant, was also a field trial for the resin chemistry, the column designs, and the continuous flow engineering that would eventually underpin a multi-billion-dollar mineral processing concept.

The water business was paying the bills while inadvertently building the foundation for something far larger.

There is a parallel here to other great technology transfers in industrial history. The skills that Corning Glass developed making lightbulb envelopes for Thomas Edison in the 1880s eventually led to fiber optic cables a century later. The precision manufacturing techniques that Swiss watchmakers perfected over generations became the foundation for the country's medical device industry. In each case, a capability developed for one purpose turned out to be far more valuable when applied to a different problem. Clean TeQ's continuous ion exchange expertise, honed on water treatment contracts that generated tens of thousands of dollars in revenue, would eventually be applied to a mineral deposit worth billions.

But at the time, nobody saw it. Clean TeQ was a small, thinly traded company in a competitive industry with no obvious path to transformational scale. The resin chemistry was interesting. The continuous flow engineering was clever. But water treatment companies do not become mining giants. That is not how the world works.

The question was whether anyone would ever connect those dots. In 2013, someone did. And that someone had a track record of connecting dots that most people could not even see.

The Inflection Point: The Syerston Bet

To understand the Syerston acquisition, you first need to understand two things: the man who orchestrated it, and the market conditions that made it possible. Together, they created one of the most asymmetric deals in recent mining history.

By 2013, the global mining industry was deep into one of its periodic depressions. The China-driven commodity supercycle that had sent prices soaring from 2003 to 2011 was decisively over. Iron ore, copper, nickel, coal, everything was falling. Mining companies were slashing exploration budgets, writing down billions in impaired assets, and laying off workers by the tens of thousands.

The major diversified miners, BHP, Rio Tinto, Glencore, were in full retreat mode, canceling expansion projects and returning capital to shareholders. Junior mining stocks, the most speculative corner of the market, were being treated like toxic waste. The S&P/ASX 300 Metals and Mining Index had fallen roughly sixty percent from its 2011 peak. Nobody wanted to own a pre-production mining asset. Nobody wanted to fund one. The mood at industry conferences like PDAC in Toronto and Mines and Money in London was somewhere between funeral and bankruptcy auction.

Into this environment walked Sam Riggall. At first glance, his decision to join the board of a small-cap Australian water company seemed like a baffling step down. He held degrees in law and economics from the University of Melbourne, plus an MBA from Melbourne Business School. He had spent over a decade at Rio Tinto, one of the world's largest mining companies, working across exploration, project development, and capital allocation in roles that gave him a front-row seat to how the industry's biggest players evaluated and developed mineral assets.

From Rio Tinto, Riggall had moved to Ivanhoe Mines, where he served as Executive Vice President of Business Development and Strategic Planning under the company's legendary founder, Robert Friedland. At Ivanhoe, Riggall had negotiated mine development agreements with national governments and parliaments, defended against nationalization and expropriation attempts in politically volatile jurisdictions, and learned the art of turning geological discoveries into funded projects. He had earned the Honour Medal of Economic and Financial Service from the Government of Mongolia for his work on the Oyu Tolgoi copper-gold mine.

He was, by any measure, dramatically overqualified to be running a small-cap Australian water company. Which was precisely the point. Riggall did not join Clean TeQ to run a water business. He joined because he and Friedland had identified the company as the ideal vehicle for a very specific asset.

Riggall was appointed to the board as Chairman on June 4, 2013. His arrival was the first signal that something unusual was happening. The second signal came eighteen months later.

In November 2014, Clean TeQ announced it had agreed to acquire the Syerston nickel-cobalt-scandium project from a wholly-owned subsidiary of Ivanhoe Mines. The project sat in the Fifield district of central New South Wales, roughly 450 kilometers west of Sydney, on a laterite deposit within the Tout Intrusive Complex. The deposit covered approximately four kilometers by four kilometers, with economic mineralization extending to sixty meters depth, a massive footprint that hinted at the scale of what lay beneath the surface.

The deal terms were, in retrospect, extraordinary. Clean TeQ paid A$100,000 in cash, issued A$1 million in CLQ shares, and signed a A$3 million zero-coupon promissory note payable in three years. The total upfront consideration was approximately A$4.1 million. In exchange, Ivanhoe retained a 2.5 percent gross revenue royalty on the project and, critically, stayed in as a major shareholder.

To a casual observer, this looked like Ivanhoe dumping a worthless asset on a willing buyer. The reality was more nuanced and far more interesting.

Ivanhoe Mines, under Friedland's leadership, was then laser-focused on its massive African copper assets, particularly the Kamoa-Kakula discovery in the Democratic Republic of Congo, which would prove to be the largest high-grade copper discovery in African history. Syerston was a legacy holding, a laterite nickel project at a time when nickel prices were in the doldrums and every laterite project on the planet carried the stigma of the industry's catastrophic processing failures. Ivanhoe needed to deploy capital toward its highest-conviction assets. Syerston, despite containing a world-class resource, was not the priority.

For Riggall and Clean TeQ, it was the opportunity of a lifetime. They were acquiring a deposit containing 962 million tonnes of ore grading 0.71 percent nickel and 0.09 percent cobalt, plus what would later be confirmed as the world's largest primary scandium resource, for less than the price of a modest house in Sydney's eastern suburbs.

When the 2018 Definitive Feasibility Study valued the project at a post-tax net present value of US$1.39 billion using an eight percent discount rate, the acquisition price turned out to be roughly three-hundredths of one percent of that figure. It is the kind of deal that belongs in any textbook on buying distressed assets at the absolute bottom of the cycle.

But the most important subtlety of the transaction was structural. Ivanhoe did not walk away. Friedland kept his shares and his royalty. He was not a distressed seller dumping an unwanted asset; he was a sophisticated capital allocator rotating resources toward his primary focus while maintaining full exposure to the upside. The deal's equity component and royalty retention ensured that Ivanhoe's interests remained tightly aligned with Clean TeQ's success.

This was not an arm's-length transaction between strangers. It was a carefully choreographed handoff between allies, with Friedland simultaneously positioning himself as the single largest shareholder of the acquiring company.

With Syerston secured, Clean TeQ began its transformation from a water company with a side interest in mining to a mining company with a proprietary processing technology. Riggall became Chairman and CEO effective July 1, 2015, consolidating operational control. Robert Friedland was appointed Co-Chairman in September 2016, making the power structure explicit.

A preliminary DFS was completed in October 2016, valuing the project at A$912 million. The full Definitive Feasibility Study followed in June 2018, projecting average annual EBITDA of US$344 million, production of 21,300 tonnes per year of nickel and 4,400 tonnes per year of cobalt, plus 80 tonnes per year of scandium oxide, over an initial twenty-five-year mine life with sufficient reserves for forty-plus years. The internal rate of return was 19.1 percent.

The Syerston project was rebranded as the "Clean TeQ Sunrise Project," a name that foreshadowed the corporate identity change that would come six years later.

The pivot then unfolded in stages. First came the "Scandium Play" narrative, as investors noticed the unusual mineral endowment at Syerston and recognized that the deposit contained something far rarer than nickel. Then came the "Battery Metal Giant" narrative, as the electric vehicle revolution, accelerated by Tesla's Model 3 ramp and the proliferation of national EV mandates across Europe and China, transformed the demand outlook for nickel and cobalt from stable to explosive.

Each narrative attracted a different cohort of investors. Scandium specialists came first, drawn by the geological uniqueness. Battery metal funds followed, attracted by the nickel-cobalt tonnage. And value investors circled, recognizing the staggering gap between what was paid for the asset and what it was worth.

Clean TeQ was riding a wave that was only beginning to build, and it had acquired its surfboard for less than the cost of a used car.

But there was a problem. The market could not quite figure out what Clean TeQ was. Was it a water company? A mining company? A technology play? A scandium story? A battery metals story? The confusion would persist for years, suppressing the share price and frustrating management. Resolving it would require a radical corporate restructuring that would not come until 2021. In the meantime, the hidden gem within the Sunrise deposit, the scandium that most investors overlooked entirely, was quietly becoming the most strategically important part of the story.

Hidden Business: The Scandium King

Most investors who encounter Sunrise Energy Metals for the first time fixate on the nickel and cobalt. That is understandable. Nickel trades on the London Metal Exchange. Cobalt has a published spot price. Both are essential battery metals with clear demand trajectories tied to electric vehicle adoption. They are commodities that institutional investors understand, that analysts can model with discounted cash flow spreadsheets, and that offtake partners can price and hedge.

Scandium is none of those things. And that is precisely why it might be the most valuable part of the entire Sunrise story.

Scandium is element twenty-one on the periodic table, a silvery-white transition metal that, in its pure form, is unremarkable. Most people have never heard of it. It does not appear in everyday products, does not trade on any exchange, and has no futures contracts or published benchmark prices. To call the scandium market "illiquid" would be generous; it barely exists as a market at all.

But when alloyed with aluminum at concentrations as low as one-tenth of one percent, scandium produces materials with properties that border on the miraculous. Think about what aluminum already does well: it is light, it conducts heat efficiently, and it is relatively easy to form into complex shapes. Now imagine a version of aluminum that is dramatically stronger, that resists corrosion better, that welds more cleanly without the weakening "heat-affected zone" that plagues traditional aluminum joints, and that maintains its structural integrity at temperatures where conventional aluminum alloys begin to soften.

That is what scandium does. A tiny pinch of scandium transforms ordinary aluminum into a superalloy.

The Soviet military understood this decades before the commercial world caught on. The MiG-29 fighter jet, one of the most successful combat aircraft of the Cold War, incorporated scandium-aluminum alloys in its structural components. Soviet submarine hulls used the same materials for their combination of strength, lightness, and resistance to the corrosive effects of seawater.

Today, the aerospace industry is rediscovering what the Soviets knew. Airbus has developed a proprietary alloy family called Scalmalloy, an aluminum-magnesium-scandium formulation designed specifically for additive manufacturing, or 3D printing. Scalmalloy offers extraordinary fatigue resistance and toughness, ideal for producing complex structural aircraft components that would be impossible to manufacture using traditional methods. Boeing is conducting its own multi-year qualification programs for scandium-aluminum alloys in airframe applications.

Beyond aerospace, scandium-stabilized zirconia serves as an electrolyte in solid oxide fuel cells, where its superior ionic conductivity improves cell efficiency. Bloom Energy, one of the leading fuel cell manufacturers, scaled production of scandium-based electrolytes in 2025. The applications extend to 3D-printed automotive components, high-performance bicycle frames, and next-generation defense systems.

The problem, and the opportunity, is supply.

Global scandium production amounts to roughly forty to fifty tonnes per year. To put that in perspective, world gold production exceeds three thousand tonnes per year. Even indium, one of the more obscure industrial metals, sees annual production of several hundred tonnes. Scandium output is tiny because virtually all of it is produced as a byproduct of other mining operations: uranium processing in Kazakhstan, rare earth extraction in China, titanium dioxide refining in Russia. China alone accounts for roughly two-thirds of global output. There has never been a dedicated primary scandium mine operating anywhere in the world.

And there is no transparent market. Scandium oxide is not traded on the London Metal Exchange, the Shanghai Futures Exchange, or any other public platform. Every transaction is a private negotiation between buyer and seller at undisclosed prices and quantities. When analysts quote a scandium oxide price, typically in the range of US$633 to US$715 per kilogram for high-purity material, they are essentially reporting rumors gathered from a handful of traders willing to share information.

This illiquidity is both a curse and a blessing. The curse is obvious: without a transparent market, producers cannot easily secure financing, buyers cannot hedge costs, and analysts have no reliable data. The blessing is subtler but potentially more powerful. Anyone who can establish reliable, large-scale primary supply at competitive costs has the opportunity not just to participate in a market, but to create one. Sunrise is not just a potential miner. It is a potential market maker.

In September 2025, Sunrise released an updated mineral resource estimate that doubled the contained scandium at the Syerston deposit. At a 300 parts-per-million cutoff grade, the deposit now contains 45.9 million tonnes of measured and indicated resource at an average grade of 414 ppm scandium, holding 19,007 tonnes of scandium metal. At a higher 600 ppm cutoff, contained scandium grew by 161 percent.

To put 19,007 tonnes in context: at current global consumption rates, the Sunrise deposit alone contains enough scandium to supply the entire planet for roughly five centuries. Demand will grow, with projections suggesting consumption could exceed 110 tonnes per year by 2026 and the overall market reaching US$2 billion by 2031. But even with aggressive demand growth, Sunrise's resource position is overwhelming. This is not a company hoping to carve out a niche. It is a company that could dominate global supply for generations.

The strategic pivot to scandium-first development was perhaps the most consequential decision management has made. Rather than waiting for the multi-billion-dollar nickel-cobalt project to secure financing, the company fast-tracked a standalone scandium operation. The feasibility study, completed in March 2026 by GR Engineering Services, envisions production of sixty tonnes per year of high-purity scandium oxide over a thirty-two-year mine life, at a capital cost of A$120 million and average life-of-mine operating costs of A$534 per kilogram.

That A$120 million price tag deserves emphasis. The full nickel-cobalt-scandium project carries a pre-production capital cost of US$1.33 billion. The standalone scandium operation costs less than a tenth of that. It is a way to begin generating revenue, prove the processing technology at commercial scale, establish customer relationships, and build operational credibility, all while the larger project waits for better market conditions. In startup language, it is a minimum viable product for a mining company.

In April 2025, China imposed export licensing restrictions on scandium, a move that sent shockwaves through the small community of Western aerospace and defense companies that depend on Chinese supply. Suddenly, the strategic case for a non-Chinese, non-Russian scandium supply was not merely theoretical. It was urgent.

The US Export-Import Bank responded by issuing a letter of interest in September 2025 for up to US$67 million in financing toward the Sunrise scandium project, roughly half its total capital cost. When the world's largest economy offers to help finance your mine, the geopolitical tailwind could hardly be more explicit.

There is an important lesson here about market creation versus market participation. When a company mines copper, it is participating in an existing market with established prices, logistics, and customer relationships. When Sunrise begins producing sixty tonnes of scandium oxide per year, it will be doing something closer to what De Beers did with diamonds in the early twentieth century or what Intel did with microprocessors in the 1970s: not just selling a product, but actively working with downstream industries to design that product into their manufacturing processes.

The company has been engaged in exactly this kind of market development work for years, collaborating with aerospace companies on alloy qualification, with fuel cell manufacturers on electrolyte formulations, and with aluminum smelters on master alloy development. Each customer relationship that Sunrise develops before production begins is a future revenue stream that competitors cannot easily replicate, because the customer's product designs will be built around Sunrise's specific scandium oxide specifications.

This is what makes the scandium business fundamentally different from a commodity play. It is a specialty materials business hidden inside a mining company's shell. The margins on specialty materials are typically much higher than on commodities, the customer relationships are stickier, and the pricing power is greater. A nickel buyer can switch suppliers with a phone call. An aerospace company that has spent five years qualifying a specific scandium-aluminum alloy formulation cannot switch suppliers without restarting the entire qualification process.

For investors, the scandium story is what makes Sunrise genuinely unique. Many companies have nickel deposits. Many have cobalt. Nobody else has scandium at this scale, in this jurisdiction, with this processing technology. It is the hidden business inside the visible one, the specialty chemical margin engine concealed within a commodity mining shell.

The Tech Secret Sauce: Resin-In-Pulp

To appreciate why Sunrise's processing technology matters so profoundly, you need to understand why the conventional approach to processing laterite nickel ores has been, to put it charitably, a catastrophe of historic proportions.

Nickel exists in two broad types of deposits, and the distinction is crucial.

Sulfide deposits sit deep underground, typically in ancient volcanic formations. They produce high-grade ore that can be smelted using well-understood, century-old pyrometallurgical technology. Essentially, you heat the ore in a furnace until the nickel melts out. These are the mines that built the modern nickel industry: Sudbury in Ontario, the Norilsk complex in Siberia, the Kambalda operations in Western Australia. Underground sulfide mining is expensive to develop because you need shafts, tunnels, ventilation, and rock reinforcement. But once operating, the metallurgy is relatively straightforward.

Laterite deposits are a fundamentally different beast. They sit near the surface, in tropical and subtropical regions, formed by millions of years of weathering that leached nickel out of the underlying ultramafic rock and concentrated it in layers of clay, iron oxides, and silicate minerals. They are cheap to mine, often just scraping the surface with bulldozers and excavators.

The problem is what comes after. The nickel in laterite ore is not sitting in discrete mineral grains that can be physically separated. It is chemically incorporated into the crystal structure of the host minerals, locked inside the lattice in a way that makes extraction extraordinarily difficult. You cannot smelt it out. You cannot float it. You have to chemically dissolve the entire mineral matrix to free the nickel.

Laterites account for roughly seventy percent of the world's known nickel resources. They are the future of nickel supply, whether the industry likes it or not. And the industry, for the most part, does not like it at all.

The technology that was supposed to unlock laterite nickel is called High Pressure Acid Leach, or HPAL. The concept is straightforward: crush the ore, mix it with concentrated sulfuric acid, and cook the mixture in massive pressure vessels called autoclaves at temperatures exceeding 250 degrees Celsius and pressures approaching fifty atmospheres. Under these extreme conditions, the acid dissolves the nickel and cobalt from the mineral matrix into a solution, which is then processed through a series of precipitation and purification steps to produce a saleable metal concentrate.

In the laboratory, HPAL works beautifully. At commercial scale, it has been one of the mining industry's most expensive and humiliating failures.

The poster child is Vale's Goro nickel project in New Caledonia. Originally developed by Inco and budgeted at roughly US$1.4 billion, the project's costs ballooned to over US$6 billion by the time Vale inherited it through its acquisition of Inco. The plant was designed to produce 60,000 tonnes of nickel per year. It opened in 2010 after years of delays.

What followed was a decade of operational misery. Five recorded acid leaks. A six-month complete shutdown in 2012 after major spills. In May 2014, 100,000 liters of toxic effluent leaked into North Bay Creek, killing approximately a thousand fish and triggering violent local protests. In ten years of production, Goro never exceeded roughly seventy percent of its design capacity.

Vale recorded a US$1.6 billion impairment charge in late 2019 and eventually sold the operation in 2021, providing a US$1.1 billion support package just to get the buyer to take it off their hands.

Goro was not an isolated case. BHP's Ravensthorpe in Western Australia was budgeted at US$1.05 billion and completed at US$2.2 billion. BHP suspended operations months after opening and eventually sold for US$340 million, roughly fifteen cents on the dollar. Ravensthorpe was permanently closed in May 2024.

In Madagascar, the Ambatovy project consumed approximately US$5.5 billion, roughly triple its original budget. Sherritt International wrote down US$1.6 billion and exited entirely. The Murrin Murrin operation, budgeted at US$1 billion and completed at US$1.6 billion, has operated since 1999 without ever reaching its design capacity of 45,000 tonnes per year.

The pattern is consistent and devastating. There is an industry truism that captures the collective experience: anyone claiming sub-billion-dollar construction costs for an HPAL plant is, according to veteran operators, delusional or worse.

The problems are both chemical and mechanical, and understanding them in some detail is essential because they explain why Sunrise's alternative approach has such transformative potential.

Start with the autoclaves themselves. These are enormous pressure vessels, often twenty meters long and five meters in diameter, lined with titanium because no other commercially available material can withstand concentrated sulfuric acid at 250 degrees Celsius for extended periods. Titanium lining is extraordinarily expensive, and even titanium corrodes under these conditions, requiring regular inspection and replacement. The seals and gaskets that maintain pressure integrity are subjected to thermal cycling and chemical attack that degrades them far faster than design specifications predict.

The discharge system is arguably the weakest link. When the superheated, highly acidic slurry exits the autoclave through pressure let-down valves, the sudden depressurization creates extreme erosion. Valve seats wear out. Pipe bends thin. Flash tanks, which allow the slurry to cool and depressurize, accumulate scale deposits that reduce their effectiveness and require frequent mechanical cleaning.

Then there is the chemistry itself. Acid consumption varies wildly depending on the mineralogy of the specific ore being processed. Clay minerals in the feed consume acid without contributing to metal extraction, a problem that is difficult to predict from bore-hole samples and that often worsens as the mine progresses into different zones of the deposit. And the environmental footprint is enormous: HPAL produces twenty-four to twenty-seven kilograms of CO2 equivalent per kilogram of nickel, roughly double the emissions of sulfide processing, primarily due to the energy required to maintain extreme temperatures and pressures.

This is the context in which Sunrise's Clean-iX technology becomes extraordinary. The resin-in-pulp process takes a fundamentally different approach.

Think of it this way. HPAL is like demolishing an entire building to recover the copper wiring inside the walls. You bring in a wrecking ball, reduce everything to rubble, then sift through the debris to find what you want. It works, but it is violent, wasteful, and extraordinarily expensive. Clean-iX is like sending in a team of electricians who can pull the wiring out without touching anything else. The building stays intact. The job gets done with a fraction of the equipment and energy.

Technically, instead of extreme temperatures and pressures, the Clean-iX resin-in-pulp process operates at atmospheric conditions. Instead of dissolving everything in acid and then trying to separate what you want from the resulting chemical soup, it uses selective ion exchange resins that grab only the target metal ions directly from the leached ore pulp.

The resins are chemically tuned to adsorb specific metal ions while ignoring everything else in the slurry. The loaded resin is then eluted, meaning the captured metals are washed off using a chemical solution, producing a high-purity concentrate. The company's patented U-column elution technology produces eluate of such purity that subsequent refining steps are dramatically simplified.

Where an HPAL operation needs massive counter-current decantation circuits, multiple precipitation stages, and extensive purification trains, the Clean-iX process can skip or shrink many of those steps. The result is lower capital costs, lower operating costs, lower energy consumption, and a much smaller physical footprint.

This technological advantage enables Sunrise to envision something most laterite projects cannot: vertical integration from mine gate all the way to battery-grade nickel and cobalt sulfates, the specific chemical products that battery cell manufacturers actually purchase.

Most laterite operations produce an intermediate product, a mixed hydroxide or mixed sulfide precipitate, that must be further refined by a third party, often in China, before entering the battery supply chain. Each additional processing step adds cost, reduces margin, and introduces dependencies. By producing finished sulfate products directly, Sunrise could capture the full value chain and deal directly with battery OEMs, eliminating middlemen and the geopolitical risks that come with them.

The standalone scandium project, with its 2028 commissioning target, will serve as the first commercial-scale demonstration of the Clean-iX platform. If it performs as designed, it validates not just the scandium economics but the entire processing philosophy, dramatically reducing technology risk for the larger nickel-cobalt expansion.

The significance of this cannot be overstated. The single biggest question mark hanging over the Sunrise story is whether Clean-iX works at industrial scale. Every feasibility study, every NPV calculation, every projected cost metric depends on the answer. The scandium project is designed to answer that question definitively, at a fraction of the cost and risk that a full-scale nickel-cobalt operation would entail.

It is worth noting what the technology does not do. It does not eliminate the need for acid leaching entirely. The ore still needs to be leached to liberate the metal ions into solution. What Clean-iX eliminates is the extreme pressure and temperature regime that makes HPAL so dangerous, expensive, and unreliable. The leaching step can be conducted at atmospheric pressure using less aggressive conditions, and the ion exchange step that follows is inherently more selective, more controllable, and more scalable than the precipitation and separation processes used in conventional flowsheets.

For a mining industry that has been burned, repeatedly and expensively, by the promise of novel processing technologies, the proof will be in the commissioning. Words and feasibility studies are cheap. Operating plants are not. But if the scandium operation performs as designed, it will represent the most important validation of atmospheric-pressure laterite processing since the technology was first conceived.

Management and The Friedland Factor

In mining, management matters more than in almost any other sector. A mine is a multi-decade, multi-billion-dollar commitment that cannot be relocated, repriced, or easily restructured once construction begins. The decisions made early in a project's life, the choice of processing technology, the selection of engineering contractors, the structure of financing, reverberate for decades. Get them wrong, and you end up with a Goro. Get them right, and you build a Voisey's Bay.

Sunrise Energy Metals is led by two people who have collectively been involved in some of the most spectacular mining deals and discoveries of the past three decades.

Robert Friedland's biography reads like a novel that no publisher would accept as plausible fiction. Born in 1950 in Chicago to Holocaust survivors, his father Albert having endured three years in Auschwitz, young Robert showed early signs of the rebellious intensity that would define his career. He enrolled at Bowdoin College in Maine, where he was expelled after federal authorities discovered him in possession of an estimated $100,000 worth of LSD. He served two years in federal prison, an experience that, by his own account, only sharpened his appetite for risk and unconventional thinking.

After his release, Friedland transferred to Reed College in Portland, Oregon, graduating with a degree in political science in 1974. Reed in the early 1970s was a hotbed of countercultural experimentation, and it was there that Friedland crossed paths with a young Steve Jobs, who was drifting through the campus as an unofficial auditor.

The two formed an unlikely friendship rooted in shared interests in Eastern spirituality, vegetarianism, and unconventional approaches to conventional boundaries. Friedland managed a property called All One Farm, an apple orchard and commune south of Portland owned by his millionaire uncle Marcel Muller. Jobs would come on weekends to help tend the trees.

The orchard is widely cited as the inspiration for the name of the company Jobs would later co-found. Daniel Kottke, an early Apple engineer who knew both men, has stated that Jobs' famous "reality distortion field" was partly inspired by Friedland's charismatic intensity. If that attribution is even partly accurate, Friedland's influence on the modern technology industry extends far beyond mining.

Friedland's own path into resources was serendipitous. In 1978, he and Jobs formed an investment partnership to acquire timberland in Oregon. A flashlight inspection of an abandoned gold mine on the property sparked what would become a lifelong obsession with mineral wealth. He moved to Vancouver's junior mining scene in 1980.

His first major venture was spectacularly controversial. As CEO of Galactic Resources, Friedland operated the Summitville gold mine in Colorado's San Juan Mountains using heap-leach cyanide extraction. Against contractor advice, he pushed operations through winter conditions. When the winter of 1991-1992 overwhelmed the waste-water recovery system, a toxic mixture of heavy metals and cyanide drained into the Alamosa River, killing every living thing along a seventeen-mile stretch of waterway.

The EPA estimated total cleanup costs exceeding US$200 million. The site became a Superfund location. Friedland relocated to Singapore shortly before Galactic Resources filed for bankruptcy. He eventually paid US$20.75 million toward restoration in 2001. The disaster earned him a nickname that has followed him for three decades: "Toxic Bob."

A lesser operator would have been finished. The environmental destruction, the bankruptcy, the federal investigation, the public vilification, any one of these would have ended most careers permanently. In the buttoned-up world of institutional mining finance, the Summitville disaster made Friedland persona non grata in many boardrooms and capital allocation committees.

But Friedland possessed something that his critics consistently underestimated: an absolute, unshakeable belief in his own ability to identify and develop world-class mineral assets, combined with a charisma so potent that he could, time and again, convince investors to back him despite the baggage. He was not chastened by Summitville. He was educated by it. And he took that education to Labrador.

In 1992, he co-founded Diamond Fields Resources with Jean-Raymond Boulle. Contracted geologists discovered a massive nickel-copper-cobalt deposit at Voisey's Bay in Labrador in 1993-1994, estimated at 141 million tonnes grading 1.6 percent nickel. What followed was one of the great bidding wars in mining history.

Inco and Falconbridge competed furiously for the asset while Friedland orchestrated the process with the showmanship of a Hollywood talent agent, flying potential bidders over the deposit in helicopters and methodically ratcheting up the price. Inco ultimately paid C$4.3 billion for Diamond Fields Resources in 1996, a staggering sum for an undeveloped deposit.

He went on to found Ivanhoe Mines, discover the Oyu Tolgoi copper-gold deposit in Mongolia, and create a new Ivanhoe Mines focused on Africa, where the Kamoa-Kakula copper discovery proved to be the largest high-grade copper discovery in African history. That mine is now on track to become the world's third-largest copper producer.

Friedland's famous quote captures his philosophy: "Promoting a stock is like making a movie. You've got to have stars, props, and a good script." He has raised more than US$10 billion on world capital markets. He was named Canada's Developer of the Year in 1996, Mining Person of the Year in 2006, Australia's Dealmaker of the Year in 2011, and received Mongolia's Order of the Polar Star in 2023.

For Sunrise, Friedland holds approximately fourteen to fifteen percent of the company. He is not a passive board member. He is the promoter-in-chief: the person who opens doors with sovereign wealth funds, introduces management to potential offtake partners, and provides the credibility that comes from having discovered and developed some of the most important mineral assets on the planet.

Sam Riggall complements Friedland's visionary intensity with something equally valuable: operational discipline. Where Friedland is the showman, the dealmaker, the man who can command a room with the force of his conviction, Riggall is the engineer's CEO, methodical, detail-oriented, and deeply conversant in the technical complexities of mine development.

His decade at Rio Tinto gave him rigorous analytical training. His time at Ivanhoe gave him deal-making instincts and the relationship with Friedland himself. At Sunrise, Riggall holds roughly two percent of the company, worth tens of millions at current prices, with additional performance rights tied to final investment decision and construction milestones.

His total compensation in fiscal 2025 was A$522,070, modest by the standards of companies at this market capitalization, reflecting a structure where the real payoff comes from equity appreciation. This is not a management team collecting salaries while waiting for something to happen. Their personal wealth is directly tied to execution.

The Friedland-Riggall partnership mirrors other successful pairings in business history where a visionary promoter is paired with a disciplined operator. Think of Walt Disney and Roy Disney, or Steve Jobs and Tim Cook. The visionary provides the narrative, the ambition, and the external credibility. The operator provides the process, the rigor, and the execution capability. Neither is sufficient alone. Together, they create something that is greater than the sum of its parts.

In Sunrise's case, this partnership is particularly important because the company is approaching the most critical phase of its existence: the transition from project developer to project builder and, eventually, to producer. During the development phase, promotional skill is paramount, you need to attract capital, convince regulators, and build excitement among potential partners. During the construction and commissioning phase, operational discipline becomes everything, you need to manage contractors, control costs, and solve the inevitable technical problems that arise when theory meets reality. Sunrise needs both capabilities simultaneously, and it has them.

The combination of Friedland's promotional genius, global network, and track record with Riggall's operational competence and institutional rigor is unusually powerful for a company of this size. It is a non-founder management team that behaves exactly like founders, with genuine skin in the game and decades of experience at the highest levels of global mining.

The 2021 Pivot: Rebranding and Demerger

By 2020, Clean TeQ Holdings had a problem that was entirely self-inflicted, and management knew it. The company was trying to be two things at once: a water treatment technology provider and a battery metals mining developer. For investors, this dual identity was maddening.

Mining analysts who wanted exposure to the Sunrise nickel-cobalt project did not want to spend their time trying to value a water treatment business with its own customer base, competitive dynamics, and growth trajectory. Technology investors who were intrigued by the Clean-iX platform did not want exposure to the capital-intensive, high-risk timeline of mine development. The company was falling between two stools, unable to attract the dedicated investor base that either business deserved.

The problem showed up directly in the share price. Clean TeQ traded at a persistent "conglomerate discount," where the market valued the combined entity at less than the sum of its parts. Analysts could not agree on how to categorize it. Was it a water company? A mining company? A technology company? The confusion suppressed valuation multiples and made capital raising inefficient.

The solution was a demerger, executed with surgical precision. Announced on February 22, 2021, the plan called for the water treatment business to be spun off into a separately listed entity retaining the Clean TeQ name. The mining business would keep the Syerston project and rebrand as Sunrise Energy Metals Limited.

The name change, executed in March 2021 concurrent with a 10-to-1 share consolidation and the termination of the company's secondary TSX listing in Canada, was far more than cosmetic. It was a deliberate signal to a very specific audience.

Consider the naming from a capital markets perspective. "Clean TeQ" sounded like a water purification startup or an environmental services company. Institutional mining investors who screened the ASX for battery metals exposure would never have found it. "Sunrise Energy Metals" is explicitly and unmistakably a critical minerals company. "Sunrise" pointed directly at the project. "Energy Metals" told electric vehicle investors exactly what the company produced. There was no ambiguity. The name itself was a pitch.

The 10-to-1 share consolidation was similarly calculated. Before the consolidation, Clean TeQ shares traded at a few cents each, the kind of price that institutional investors associate with penny stocks and speculative punts. After consolidation, the share price moved into dollar territory, making it psychologically easier for fund managers with minimum price thresholds to take a position. It was cosmetic in one sense, the market capitalization did not change, but it mattered enormously in terms of the company's accessibility to the institutional capital it needed to attract.

The demerger was completed on July 1, 2021. Shareholders received one Clean TeQ Water share for every two Sunrise shares held. The water business was demerged with A$15 million in cash and no debt, a clean starting position.

The strategic logic was sound for both entities. Clean TeQ Water could pursue its own path without being overshadowed by a multi-billion-dollar mining project. Sunrise could present itself as a pure-play critical minerals developer at precisely the moment when the world was waking up to battery metal supply chain vulnerabilities.

What made the demerger particularly elegant was the ongoing relationship. Clean TeQ Water retained the ion exchange technology expertise. Sunrise retained the mining project. In January 2026, Clean TeQ Water secured an engineering contract for the Syerston scandium project, ensuring that the technological know-how remained directly accessible without corporate complexity.

The market responded. Freed from the conglomerate discount, Sunrise began attracting dedicated mining fund managers. The scandium-first strategy gave them a clear near-term catalyst. And then the geopolitical dominoes fell: China's scandium export restrictions, the US EXIM Bank's financing interest, the resource estimate doubling contained scandium.

In late 2025, Sunrise raised A$46 million in a November placement at A$4.25 per share, followed by A$32.5 million in December at A$6.50 per share. Total capital raised in those two months was A$78.5 million, earmarked for pre-construction activities on the scandium project. The stock continued climbing, eventually exceeding A$12.

The speed of the re-rating is worth pausing on, because it illustrates a phenomenon that is common in mining but rare in other sectors: the transition from "ignored" to "discovered." For years, Sunrise had been a stock that nobody followed. It had no revenue, no production, no analyst coverage worth mentioning. The share price languished in the low cents, reflecting the market's complete indifference to a pre-production mining developer during a commodity downturn.

Then, in the space of roughly twelve months, a series of external catalysts, the China export restrictions, the resource upgrade, the EXIM Bank interest, the completed feasibility study, combined with the internal catalyst of the demerger and the scandium-first strategy to create a perfect storm of investor attention. The stock moved from A$0.22 to over A$12, a roughly five-thousand-percent appreciation. The market capitalization expanded from approximately A$20 million to over A$1.15 billion.

This kind of re-rating does not happen in mature industries. It happens in mining, where the gap between "what a project is worth on paper" and "what the market is willing to pay for it before production" can persist for years before snapping shut with startling violence. The snap, when it comes, rewards the patient and punishes the late.

For a company valued at a few million dollars just two years earlier, the transformation was breathtaking. But the harder question is whether the current valuation, roughly A$1.15 billion for a company that has never produced anything, is pricing in execution that has not yet occurred. That question leads directly to the strategic analysis.

Playbook: Business and Investing Lessons

Hamilton Helmer's Seven Powers framework maps onto Sunrise with unusual clarity. Three of the seven powers are directly applicable, and their interaction creates a defensive moat that is difficult for competitors to replicate.

The most obvious power is Cornered Resource. The Sunrise deposit combines nickel and cobalt with the world's largest primary scandium resource at grades that no other known deposit matches. Mineral deposits cannot be replicated by well-funded competitors. You cannot decide to build a scandium deposit. You have to find one. And nobody else has found anything comparable. The 19,007 tonnes of contained scandium, sitting in a stable jurisdiction with established rule of law, represents a geological endowment that is irreproducible.

The second power is Process Power. Even if a competitor discovered a comparable deposit, they would face the same processing challenge that has destroyed tens of billions in shareholder value across HPAL projects. Sunrise's resin-in-pulp technology represents decades of accumulated ion exchange know-how. It is embodied not just in patents but in equipment designs, operating procedures, resin formulations, and the institutional memory of a team with over twenty years of refinement. Replicating that from scratch would take years and hundreds of millions in development spending.

The third power is Counter-Positioning. This is perhaps the most interesting and least intuitive of the three. Established nickel laterite producers, the Vales, the BHPs, the Glencores, have invested billions in HPAL infrastructure. Their engineers are trained on HPAL. Their operating procedures are built around HPAL. Their capital budgets are committed to HPAL maintenance and debottlenecking.

Pivoting to a fundamentally different processing technology would require writing off existing assets, retraining workforces, redesigning flowsheets, and accepting years of development risk on an unproven approach. For an incumbent CEO managing quarterly earnings expectations, that pivot is essentially impossible, even if the alternative technology is demonstrably superior. The organizational inertia, the sunk cost psychology, and the career risk of championing an untested approach all militate against change.

Sunrise faces none of these constraints. It is building from a blank slate, free to choose the best available technology without legacy commitments. It is building for the next fifty years. The incumbents are managing the last twenty years of deployed capital. This asymmetry is structural, durable, and extremely difficult for competitors to overcome.

Michael Porter's Five Forces analysis reinforces the picture.

Barriers to entry are formidable: geological luck, billions in capital, years of permitting, and processing technology with a documented catastrophic failure rate. Buyer power is limited because battery OEMs are desperate for diversified, non-Chinese supply chains. The European Union's Battery Regulation, effective since 2024, requires carbon footprint disclosure and responsible sourcing, shifting pricing power toward sustainable producers.

Supplier power is moderate. Sulfuric acid is a commodity, though specialized resins and engineering services create some concentration risk. The threat of substitutes is real but manageable: sodium-ion and LFP batteries reduce nickel demand in some applications, but high-energy-density applications still require nickel-rich cathodes. Scandium has no direct substitute in its primary applications.

Competitive rivalry is paradoxically low. In scandium, Sunrise would be the only large-scale Western primary producer. In nickel, the landscape has been reshaped by Indonesia's dominance, which has driven Western competitors to the exits rather than intensifying competition.

The broader industry context amplifies these dynamics. Since early 2024, the Australian nickel industry has experienced near-total collapse. Indonesia, controlling roughly sixty-two percent of global refined nickel output, flooded the market with cheap nickel from Chinese-financed HPAL plants powered by coal. BHP suspended all Nickel West operations, taking A$3.8 billion in impairments. Panoramic Resources suspended Savannah. Ravensthorpe closed permanently. Avebury went on care and maintenance.

This carnage paradoxically strengthens Sunrise's position. Indonesian nickel carries significant ESG baggage: coal-powered processing, deforestation, deep-sea tailings disposal, and roughly double the carbon emissions. Western manufacturers, under regulatory and reputational pressure, are actively seeking alternatives. The "green price premium" for sustainably produced nickel has moved from speculation to active policy discussion.

Sunrise, with atmospheric-pressure processing, Australian jurisdiction, and integrated refining capability, is positioned to be exactly what Western OEMs need. The scandium-first strategy allows it to begin proving that case with manageable capital at risk.

There is one additional competitive dynamic worth highlighting: the "myth versus reality" of Indonesian nickel as a permanent solution to the world's battery metal needs. The consensus narrative holds that Indonesia has solved the nickel supply problem through massive HPAL expansion, and that Western laterite projects are therefore unnecessary. The reality is more complicated.

Indonesian HPAL operations produce Class 1 nickel at low cash costs, but those costs do not include the environmental externalities of coal-fired power, deforestation, and deep-sea tailings disposal. As carbon border adjustment mechanisms take effect in Europe and as battery passport regulations tighten globally, the "true cost" of Indonesian nickel is likely to rise. Several major automakers have already publicly stated that they are seeking to reduce or eliminate Indonesian nickel from their supply chains due to sustainability concerns.

Moreover, Indonesia's dominance creates its own risks. Supply concentration in any single jurisdiction is a vulnerability that sophisticated procurement teams recognize and actively work to mitigate. The COVID-19 pandemic taught the world painful lessons about supply chain fragility. The current geopolitical environment, with rising tensions between China and the West, makes dependence on Chinese-financed operations in Southeast Asia increasingly uncomfortable for Western manufacturers.

Sunrise's value proposition is not just about producing nickel. It is about producing nickel that Western companies can use without regulatory, reputational, or geopolitical complications. That positioning carries a premium that transcends the commodity price cycle.

Analysis: Bear versus Bull Case

The bull case rests on a sequence of catalysts that, if they materialize, could transform a billion-dollar developer into a multi-billion-dollar producer.

The first catalyst is the successful commissioning of the standalone scandium project, targeted for the first half of 2028. At sixty tonnes per year of high-purity scandium oxide, Sunrise would immediately become the world's largest primary scandium producer. The A$120 million capital cost is partially backstopped by the US EXIM Bank's letter of interest for US$67 million. If the operation achieves its target operating cost of A$534 per kilogram against spot prices of US$633-715, margins would be attractive even before factoring in potential price increases from aerospace and fuel cell demand growth.

The second catalyst is commercial-scale validation of Clean-iX technology. The scandium project is a proof of concept for the entire processing platform. Success would dramatically de-risk the larger nickel-cobalt expansion by demonstrating that atmospheric-pressure ion exchange works at industrial scale.

The third catalyst is the final investment decision on the full project. A tier-one OEM partner providing equity or long-term offtake could transform the financing and timeline. In a world where automakers are scrambling for supply chain security, the strategic value is enormous.

The geopolitical tailwind is real. China's April 2025 export restrictions on scandium, Australia's status as a Five Eyes ally, and active government programs in the US, EU, and Australia to diversify critical mineral supply chains create a policy environment that is unusually supportive.

It is worth noting how rare this alignment of factors is. A geologically unique deposit. A proprietary processing technology. A management team with a track record of multi-billion-dollar mining successes. A geopolitical environment that actively favors Western critical mineral production. Government financing interest from the world's largest economy. And a market capitalization that, while it has grown dramatically, remains a fraction of the project's assessed value. Each of these factors alone would be interesting. Their convergence at a single company is extraordinary.

But extraordinary potential does not guarantee extraordinary outcomes. The history of mining is littered with projects that had every advantage on paper and failed in execution. Which brings us to the bear case.

The bear case is equally concrete.

Execution risk is paramount, and it deserves the most attention because it is the risk most likely to determine the outcome.

Clean-iX has never been operated at commercial scale for mineral processing. The technology has been proven at pilot scale, and the engineering team has decades of ion exchange experience. But the jump from pilot to production is where mining projects most frequently stumble.

Pilot plants process tonnes of ore. Commercial operations process thousands of tonnes per day. Equipment that performs flawlessly in a controlled test environment can behave unpredictably when subjected to the variability of real ore feeds, the wear of continuous operation, and the thousand small things that go wrong on a working mine site. Ore variability across different zones of the deposit may introduce processing challenges that the feasibility study, based on representative samples, did not fully capture.

Mining project construction costs have a well-documented tendency to escalate beyond initial estimates. A study by Ernst and Young found that the average mining project experiences cost overruns of roughly thirty percent, with complex hydrometallurgical projects often exceeding that figure. Even A$120 million, the relatively modest capital cost of the scandium project, could grow significantly if unexpected engineering challenges emerge during construction.

Financing risk is structural, and it is the risk that most directly determines the company's fate in the near term. The scandium project needs A$120 million. The full nickel-cobalt project needs over US$1.3 billion. The company's cash position at the end of fiscal 2025, before the late-2025 capital raisings, was approximately A$10.7 million, and accumulated losses total A$313 million, reflecting over a decade of pre-revenue development spending.

The late-2025 raisings brought in A$78.5 million, and the US EXIM Bank's letter of interest covers up to US$67 million. But a letter of interest is emphatically not a binding commitment. It is a statement of willingness to negotiate, subject to due diligence, satisfactory project documentation, regulatory approvals, and the Bank's own budgetary and political constraints. The gap between "letter of interest" and "signed loan agreement with funds drawn" is a gap that many mining projects have fallen into and never climbed out of.

Beyond the scandium project, the full nickel-cobalt development would require project finance on a scale that few junior miners have ever achieved. Significant equity dilution, substantial project debt, or strategic investment from an OEM partner, most likely some combination of all three, is inevitable.

Market risk cuts in multiple directions simultaneously.

On the nickel side, depressed prices from continued Indonesian oversupply could undermine the economics of the larger project regardless of how efficient the processing technology is. Nickel traded below US$16,000 per tonne for much of 2024-2025, well below the levels assumed in the 2018 DFS. While prices have recovered somewhat, there is no guarantee that Indonesian supply discipline will tighten sufficiently to sustain higher prices over the multi-decade time horizon that a mine investment requires.

On the scandium side, the market is tiny and opaque. Demand projections are based on assumed adoption rates for aluminum-scandium alloys in aerospace and automotive applications that remain unproven at commercial scale. If Airbus or Boeing delay their scandium alloy qualification programs, or if alternative alloy systems emerge, the demand thesis could weaken. And there is no price hedge available for a product that does not trade on any exchange, meaning Sunrise bears the full commodity price risk on its most important near-term revenue stream.

Regulatory risk exists and should not be underestimated, even in a mining-friendly jurisdiction like Australia. The project requires state and federal approvals including environmental impact assessments, water access licenses, biodiversity offset agreements, and Aboriginal heritage clearances under both New South Wales and Commonwealth legislation.

The Fifield district has a long mining history, which generally helps with community acceptance, but any large-scale open-pit operation will face scrutiny. Water usage in a semi-arid region is politically sensitive. And the Aboriginal heritage clearance process, while well-established, can introduce delays if previously unrecorded sites are identified during pre-construction surveys. None of these risks are unusual for an Australian mining project, but each represents a potential source of timeline slippage that could cascade through the construction schedule and financing arrangements.

And the Friedland factor has a bearish dimension. His promotional intensity, while invaluable for capital raising, can inflate expectations. The Summitville history, while decades past, illustrates a pattern of pushing hard against constraints. The gap between promotional vision and operational reality has, at points in his career, been wider than investors expected.

For investors tracking this story, three metrics matter more than any others.

First: the funding gap. The difference between committed, binding capital and total required capital for the scandium project, and eventually the full project. This captures whether Sunrise is transitioning from developer to builder. Watch for signed loan agreements, binding offtake contracts, and strategic equity investments, not letters of interest.

Second: scandium project milestone adherence. Track actual progress against the stated timeline: FID in Q2 2026, construction starting H2 2026, commissioning H1 2028. The magnitude and pattern of any slippage reveals execution capability and forecast reliability.

Third: scandium oxide price realization. Once production begins, the actual price per kilogram achieved versus feasibility assumptions will determine whether the standalone business generates margins sufficient to fund operations, service any debt, and build credibility for the larger expansion.

These three metrics, taken together, tell you everything you need to know about whether the Sunrise thesis is working. The funding gap tells you if the company can build. Milestone adherence tells you if the company can execute. Price realization tells you if the product commands the value that the feasibility study assumes. If all three trend positively, the investment case strengthens dramatically. If any one of them deteriorates materially, the thesis faces serious challenges.

One final consideration for the analytically minded: the accounting treatment of Sunrise's development expenditures. As a pre-revenue mining company, Sunrise capitalizes exploration and evaluation costs rather than expensing them. The accumulated losses of A$313 million reflect years of development spending that has not yet generated income. When production eventually begins, the capitalized costs will be amortized over the mine life, creating a non-cash depreciation charge that will reduce reported earnings but not affect cash flow. Investors accustomed to evaluating profitable companies by earnings per share need to adjust their framework for a pre-production miner, where cash flow, not accounting profit, is the relevant metric.

Final Reflections

The story of Sunrise Energy Metals is, at its core, a story about patience, optionality, and the willingness to look foolish for a very long time before being proven right.

Robert Friedland used a tiny Australian water treatment company as a vehicle to warehouse a world-class mineral deposit during the worst bear market in a generation. He paid almost nothing for it. He kept his shares and his royalty. He installed a management team with the credibility and competence to develop it. And then he waited, through years of nickel price depression, through the collapse of the Australian nickel industry, through the geopolitical upheaval that turned critical mineral supply chains into matters of national security.

He waited until the world came to him.

There is a concept in value investing called "time arbitrage," the idea that patient investors can earn superior returns by being willing to hold positions through periods when the market is unwilling to assign fair value. Friedland's play with Sunrise is time arbitrage taken to its logical extreme. He identified a world-class asset during a period of maximum pessimism, acquired it through a vehicle with a proprietary technology advantage that the market did not understand, and held through years of indifference while the macro environment slowly rotated in his favor. The patience required to execute this strategy, to watch a stock languish in the low cents while knowing that the underlying asset is worth billions, is not something that most investors or corporate operators possess. It requires a particular combination of conviction, financial resilience, and tolerance for being ignored.

Whether Sunrise becomes the "Voisey's Bay of the 2020s," as some of Friedland's more enthusiastic supporters have suggested, depends entirely on execution. Voisey's Bay was a discovery monetized quickly through a competitive auction. Sunrise is a development project that must be built, financed, and operated over decades. The comparison is aspirational, not precise.

What is worth reflecting on is the broader implication. The most successful mining companies of the future may look very different from those of the past. They will not simply dig rock out of the ground and sell it into commodity markets. They will process it using proprietary technologies that produce finished, high-specification chemical products for demanding industrial customers. They will operate in jurisdictions meeting increasingly stringent environmental standards. They will manage geological, technological, market, and geopolitical risk simultaneously.

Sunrise Energy Metals, with its Clean-iX processing platform, its pure-play critical minerals focus, its geologically unique deposit, and its management team forged at the frontier of global mining, is an early and ambitious attempt to build exactly that kind of company.

Consider the timeline that lies ahead. If Sunrise achieves final investment decision for the scandium project in the second quarter of 2026, begins construction in the second half of 2026, and commissions the plant in the first half of 2028, it will have taken roughly thirteen years from the Syerston acquisition to first revenue. Thirteen years of development spending, capital raising, feasibility studies, permitting, and market development, all without a single dollar of production revenue. That is the reality of building a mine from scratch, and it is a timeline that most investors, accustomed to the quarterly cadence of software companies and consumer brands, find difficult to stomach.

But the prize, if execution succeeds, is a business with a multi-decade mine life, irreplaceable geological assets, proprietary processing technology, and exposure to some of the most powerful secular trends in the global economy: electrification, decarbonization, defense modernization, and the reshoring of critical mineral supply chains.

The deposit sits in the red earth of central New South Wales, patient and immense, holding nineteen thousand tonnes of a metal most people have never heard of and nearly a billion tonnes of ore containing the metals that will power the electric vehicles and defense systems of the coming decades. Above it, thirty-seven employees and two of the most experienced mining operators alive are working to turn that geological endowment into a functioning business.

The team that bought one of the world's most important mineral assets for four million dollars now needs to spend the next billion wisely. In mining, that has always been the hardest part.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube