Sony: From Walkman Empire to Gaming & Entertainment Colossus

I. Introduction & Episode Roadmap

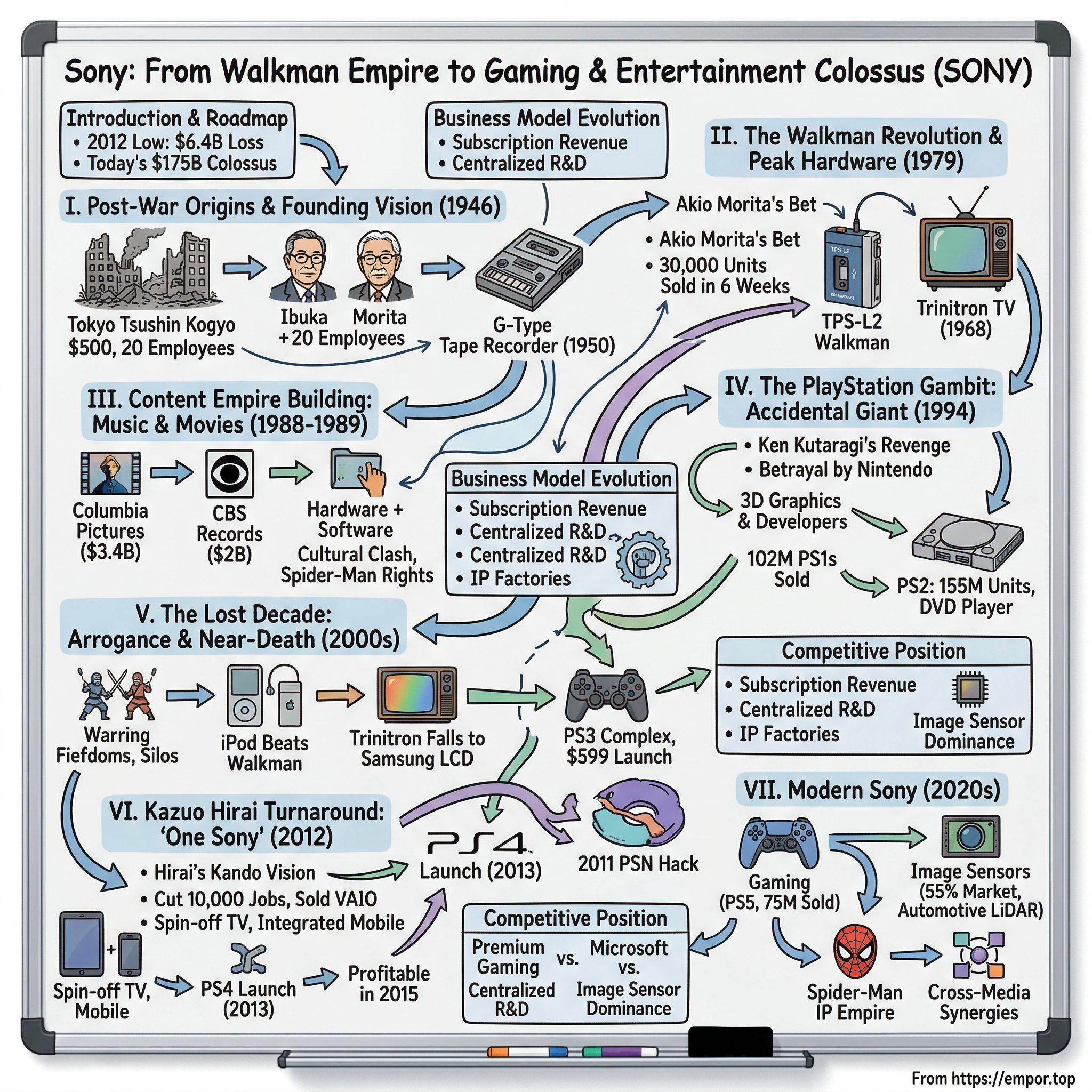

Picture this: It's March 2012, and Sony Corporation is bleeding money at a rate that would make even the most hardened turnaround specialist wince. The company that invented portable music is watching Apple count its iTunes billions. The brand that defined consumer electronics excellence is posting a record $6.4 billion annual loss. Credit rating agencies are circling like vultures, and in the gleaming towers of Tokyo's Minato district, executives are wondering if this is how one of Japan's greatest corporate stories ends—not with innovation, but with irrelevance.

Fast forward to today. Sony commands a $175 billion market cap, its PlayStation division prints money with the reliability of a Swiss watch, and its image sensors quietly power the smartphone revolution from inside nearly every iPhone and high-end Android device. The company that nearly died trying to be everything to everyone has transformed into something far more interesting: a focused entertainment and technology colossus that touches your life in ways you probably don't even realize.

How did a company founded in the rubble of post-war Tokyo by two men with $500 and a borrowed room become the world's largest gaming platform holder? How did the inventors of the Walkman miss the iPod revolution so spectacularly, only to reinvent themselves as the backbone of modern smartphone photography? And perhaps most intriguingly—in an era where American tech giants seem invincible, how has this 78-year-old Japanese company not just survived but thrived through multiple technology transitions that killed its peers?

The answer isn't found in any single product launch or acquisition, though we'll explore plenty of both. It's a story of cultural collision—Japanese craftsmanship meeting Hollywood excess, engineering precision clashing with creative chaos, and the constant tension between hardware heritage and software future. It's about how a company can be simultaneously brilliant and blind, innovative and ossified, global and insular.

We'll trace Sony's journey through five distinct eras: the post-war miracle years when "Made in Japan" transformed from insult to aspiration; the Walkman revolution that created personal entertainment; the content empire building that saw a Japanese electronics maker buy Columbia Pictures and CBS Records; the PlayStation accident that became destiny; and the near-death experience that forced a fundamental reimagining of what Sony could be.

Along the way, we'll meet characters worthy of a prestige drama: Masaru Ibuka, the dreamer engineer who believed in doing what others wouldn't; Akio Morita, the salesman-philosopher who made the world want Japanese products; Ken Kutaragi, the "Father of PlayStation" whose revenge project against Nintendo created a $30 billion gaming empire; Howard Stringer, the Welsh-American journalist who became Sony's first foreign CEO at its darkest hour; and Kazuo Hirai, the company lifer who broke down the silos and saved the company by teaching it to work as "One Sony."

This isn't just a business story—it's a meditation on reinvention, a cautionary tale about the price of success, and ultimately, a masterclass in how patient capital and cultural adaptability can overcome even the most existential threats. Because if there's one thing Sony's journey teaches us, it's that in technology and entertainment, the only constant is change, and the only sustainable advantage is the ability to transform yourself before the market transforms you.

II. Post-War Origins & The Founding Vision

The story begins in a bombed-out department store in Tokyo's Nihonbashi district, October 1945. Japan has surrendered just two months earlier, and amid the rubble and occupation, two men are sketching the blueprint for what would become one of the world's most iconic companies. Masaru Ibuka, 37, a naval engineer who spent the war developing heat-seeking missiles, sits across from Akio Morita, 24, heir to a 300-year-old sake brewing dynasty who chose technology over tradition. They have 190,000 yen (about $500), twenty employees, and absolutely no idea what product they're going to make.

What they did have was a philosophy that would seem almost quaint in today's growth-at-all-costs startup culture. Ibuka's founding prospectus, handwritten on a single page, declared their purpose: "To establish a place of work where engineers can feel the joy of technological innovation, be aware of their mission to society, and work to their heart's content." No mention of market share, no TAM analysis, no path to profitability. Just pure, almost naive belief in the power of engineering excellence.

Their first product? Rice cookers. Wooden rice cookers, to be precise, that consistently produced either undercooked mush or burnt crusty disasters. They sold exactly zero units. Their second attempt—an electric blanket—fared marginally better, moving a few dozen units before they realized Japan's post-war electricity grid was too unreliable to support it. By any modern venture capital metric, Tokyo Tsushin Kogyo (Tokyo Telecommunications Engineering Corporation) was a failure waiting to happen.

But then came the tape recorder. In 1946, Ibuka saw an American Dictaphone at NHK (Japan Broadcasting Corporation) and became obsessed. The problem? Magnetic tape didn't exist in Japan. So they made their own—from paper. Morita would later describe watching Ibuka and his engineers hand-coating strips of paper with ferric oxide powder, using brushes made from the fur of Japanese weasels because nothing else would apply the magnetic material evenly enough. It took four years, but in 1950, they released Japan's first magnetic tape recorder, the G-Type, weighing 35 kilograms and costing 160,000 yen—roughly half the price of a small house.

The Japanese market's response was devastating indifference. Who needed to record sound? What was the use case? Morita, displaying the marketing genius that would define Sony's rise, didn't wait for customers to figure it out. He personally lugged the massive machine to schools, showing teachers how they could improve language instruction. He demonstrated to courts how testimony could be preserved. He convinced government offices they needed audio documentation. By sheer force of will and shoe leather, they sold 200 units in the first year.

The transistor changed everything. In 1952, Ibuka traveled to the United States and learned that Western Electric was licensing the transistor patent from Bell Labs for $25,000. The technology was being used primarily for hearing aids—tiny, niche, medical. Ibuka saw something else entirely: the future of consumer electronics. Despite MITI (Japan's Ministry of International Trade and Industry) initially refusing the foreign currency allocation, calling it "frivolous," Morita convinced them this technology could transform Japan's electronics industry.

What followed was two years of what can only be described as obsessive iteration. Sony's engineers, working in a converted warehouse with no air conditioning, went through over 100 transistor prototypes. They had to develop their own methods for growing germanium crystals, purifying materials to levels unheard of in Japanese manufacturing. When they finally succeeded in 1955, producing Japan's first transistor radio, the TR-55, they had leapfrogged most of their Western competitors in miniaturization and quality.

But Morita knew that technical excellence meant nothing without market acceptance, particularly in the West. In 1955, he took the transistor radio to New York, targeting the American market with an audacity that seemed delusional for a company from a nation still under partial occupation. His first major buyer, Bulova, offered to purchase 100,000 units—on one condition: they would be sold under the Bulova brand. For a cash-strapped startup, it was a life-changing order. Morita said no.

"Our company name is a brand," he told a bewildered Bulova executive, about a company nobody in America had heard of. It was either visionary or suicidal, depending on your perspective. The decision to build a global brand rather than be an OEM supplier would define everything that followed.

The name "Sony" itself was Morita's creation, a stroke of marketing genius. Derived from "sonus" (Latin for sound) and "sonny" (American slang for young boy), it was pronounceable in any language, meant nothing specific in any culture, and therefore could mean anything they wanted it to mean. In 1958, Tokyo Tsushin Kogyo officially became Sony Corporation. The four-letter name fit perfectly on products, advertisements, and most importantly, in the minds of consumers worldwide.

By 1960, Sony had established Sony Corporation of America, the first Japanese company to be listed on the New York Stock Exchange (1961), and was selling transistor radios that were not just matching Western quality but exceeding it. The TR-63 pocket radio, released in 1957, was marketed with a brilliant bit of manipulation—Sony salesmen were given shirts with slightly enlarged pockets to demonstrate the radio's "pocketability."

The Trinitron television, launched in 1968, represented the culmination of this first era. Using a single-gun, three-cathode ray tube design that produced dramatically brighter and sharper images than conventional TVs, it was a masterpiece of engineering that would dominate the premium television market for the next 25 years. Sony would sell over 280 million Trinitron units, and the technology would win an Emmy Award—the first ever given to a product rather than a program.

What Ibuka and Morita had built by the end of the 1960s wasn't just a successful electronics company. They had systematically dismantled the Western assumption that Japanese products were cheap imitations. They had created a brand that stood for miniaturization, quality, and innovation. And most remarkably, they had done it while maintaining the founding principle that engineers should "feel the joy of technological innovation."

But the real revolution—the one that would transform Sony from electronics manufacturer to cultural icon—was about to begin with a simple request from the company's co-founder for something to listen to on his long flights to America.

III. The Walkman Revolution & Peak Hardware Dominance

The scene was Sony's audio division laboratory in early 1979. Masaru Ibuka, now 71 and serving as honorary chairman, shuffled in with a specific request that would have seemed absurd to any reasonable product manager. He wanted a portable stereo cassette player for his frequent trans-Pacific flights—but here's the catch—it didn't need to record anything. Just play music. His engineers thought he'd lost his mind. Who would want a tape recorder that couldn't record?

The prototype they cobbled together was essentially a neutered version of Sony's Pressman recorder, a device popular with journalists. They ripped out the recording mechanism and speaker, added a stereo amplifier, and slapped on two headphone jacks (because Ibuka thought people would want to share music—a feature that would prove utterly wrong and be quickly abandoned). The resulting device was about the size of a paperback book, weighed 14 ounces, and ran on two AA batteries.

When they presented it to Sony's new president, Norio Ohga, a former opera singer turned executive, his reaction was visceral: "This is perfect for my morning jogs." But the marketing department was horrified. Their research showed nobody wanted it. Retailers were skeptical—a cassette player that couldn't record for 33,000 yen ($150) when a boom box that could do everything cost the same? It was market suicide.

Akio Morita, now chairman, overrode everyone. In a move that would seem insane by today's data-driven standards, he guaranteed the company would sell 30,000 units in the first year. If they failed, he would resign. He even dictated the price—33,000 yen, deliberately low to encourage adoption even if it meant initial losses. The product name in Japan would be "Walkman"—nonsensical English that the American division hated so much they tried to call it "Soundabout" (while the UK went with "Stowaway").

July 1, 1979: The TPS-L2 Walkman launched in Japan. First month sales: 3,000 units. The marketing department's pessimism seemed justified. Sony's stock price dipped. Retailers started returning inventory. The revolution appeared to be dead on arrival.

Then Morita did something brilliant. He didn't buy more ads or cut the price. Instead, he had staff members ride the Tokyo subway system wearing Walkmans, conspicuously enjoying their music. He gave units to celebrities and had them photographed wearing the distinctive orange foam headphones. He created "Walkman squads"—young Sony employees who would demonstrate the device in public spaces, letting curious onlookers try it for themselves.

The experiential marketing worked. By August, Sony couldn't manufacture them fast enough. The initial production run of 30,000 sold out in six weeks. By the end of 1979, they'd sold 200,000 units in Japan alone. When it launched in the US in June 1980, the entire initial shipment of 30,000 units sold out before they hit store shelves.

What Sony had accidentally discovered was that they weren't selling a stripped-down tape recorder—they were selling a entirely new human behavior: the personalization of public space. For the first time in history, you could overlay your own soundtrack onto the world. You could be physically present but aurally absent. The Walkman didn't just play music; it created a bubble of privacy in an increasingly crowded world.

The cultural impact was immediate and controversial. Japanese newspapers worried about "Walkman syndrome"—young people disconnecting from society. American sociologists fretted about the death of communal listening. But consumers didn't care. By 1983, cassette tapes were outselling vinyl records for the first time, driven largely by Walkman adoption. The word "Walkman" entered the Oxford English Dictionary in 1986, a generic term for any portable cassette player—the ultimate compliment and nightmare for a brand.

The numbers were staggering: 1.5 million units sold in 1980, 2.5 million in 1981, 7 million in 1982. By the 10th anniversary in 1989, Sony had sold 50 million Walkmans. By the time production finally ceased in 2010, over 400 million units had been sold across 300 different models. The Walkman wasn't just a product; it was a license to print money.

But Sony wasn't content to rest on the Walkman's success. In 1982, they partnered with Philips to develop and launch the Compact Disc—a technology that would revolutionize not just portable music but the entire recording industry. The story of why CDs hold exactly 74 minutes of music is peak Sony: Norio Ohga insisted that a CD must be able to hold Beethoven's Ninth Symphony in its entirety on a single disc. That requirement—based on a 1951 performance conducted by Wilhelm Furtwängler—determined the physical dimensions of every CD ever made.

The CD Walkman (later branded Discman) launched in 1984, and while bulkier and more skip-prone than its cassette predecessor, it offered pristine digital sound quality. Sony controlled both the hardware (CD players) and was building a position in software (they would acquire CBS Records in 1988), creating what seemed like an unassailable competitive moat.

Through the 1980s, Sony's product lineup read like a greatest hits of consumer electronics innovation. The Handycam (1985) democratized home video recording. The Watchman (1982) put television in your pocket. The Betamax—despite losing the format war to VHS—pushed the boundaries of home video recording quality. Each product followed the same formula: take existing technology, miniaturize it, make it personal, and wrap it in distinctive Sony industrial design.

By 1990, Sony was the undisputed king of consumer electronics. The company that had started in a bombed-out department store was now worth $35 billion. Their products were status symbols from Tokyo to New York. The Walkman had become so ubiquitous that competitors' products were called "Walkman-style" players. Sony's brand was so powerful that they could charge a 30% premium over functionally identical competitors and consumers would happily pay it.

The hardware dominance seemed permanent. After all, who could challenge the company that had invented portable music, perfected the television, and was simultaneously a technology innovator and a cultural tastemaker? The answer, as it turned out, was a computer company from Cupertino that didn't even make consumer electronics—yet.

But before that reckoning would come, Sony would make two massive bets that would transform it from a hardware company into something else entirely: they would buy their way into the content business, and almost accidentally, they would create the future of gaming.

IV. Content Empire Building: Music & Movies

The Columbia Pictures lot in Culver City was in chaos on September 25, 1989. Japanese executives in dark suits walked through the historic studio gates—the same gates that had welcomed Clark Gable, Rita Hayworth, and Frank Capra—while Hollywood lawyers frantically photocopied contracts and assistants whispered about whether they'd still have jobs tomorrow. Sony had just agreed to pay $3.4 billion for Columbia Pictures Entertainment, and nobody in Hollywood quite knew what to make of their new Japanese overlords.

The acquisition was Norio Ohga's masterstroke—or folly, depending on who you asked. The opera-singer-turned-executive had watched Sony's Betamax VCR lose to the technically inferior VHS format and learned a brutal lesson: the best hardware in the world is worthless without content to play on it. "Hardware without software is like a car without gasoline," he would repeatedly tell skeptical board members in Tokyo. The Columbia acquisition wasn't just about buying a movie studio; it was about controlling the entire entertainment value chain.

But first, Sony had dipped its toe in the content waters a year earlier. In January 1988, they'd acquired CBS Records from CBS Inc. for $2 billion—at the time, the largest Japanese acquisition of an American company ever. The music industry thought CBS had fleeced the naive Japanese buyers. After all, CBS Records' biggest asset was its back catalog, and everyone knew the music business was about discovering new talent, not milking old recordings.

Everyone was wrong. The CD revolution that Sony had co-created was about to transform those dusty back catalogs into gold mines. Consumers were replacing their entire vinyl collections with CDs, paying $15.99 for albums they already owned. CBS Records' catalog—containing everyone from Bob Dylan to Bruce Springsteen—would generate billions in pure profit over the next decade. The acquisition would pay for itself in just five years.

The Columbia Pictures deal was different—messier, more complex, and far more culturally fraught. The price tag itself caused outrage: $3.4 billion plus assumption of $1.6 billion in debt for a studio that had produced exactly one big hit ("Ghostbusters") in the previous five years. But the real drama was cultural. This was barely 45 years after Pearl Harbor, and a Japanese company was buying Columbia, the studio that had produced American propaganda films during World War II.

The headlines were brutal. "Japan Invades Hollywood" screamed Newsweek. Editorial cartoons showed the Columbia torch lady wearing a kimono. Members of Congress called for investigations into foreign ownership of American cultural assets. The acquisition became a lightning rod for American anxieties about Japanese economic power—this was the era when Mitsubishi was buying Rockefeller Center and Japanese investors were snapping up Pebble Beach.

Sony's response was shrewd: they hired Peter Guber and Jon Peters, two of Hollywood's most successful (and expensive) producers, to run the studio. The deal to extract them from Warner Bros. cost Sony an additional $500 million in settlements and swaps—a detail that somehow escaped mention when the acquisition was announced to Tokyo. Guber and Peters were everything the Sony executives weren't: flashy, excessive, and completely comfortable with Hollywood's culture of creative accounting.

The early years were a disaster. Guber and Peters spent money like drunken sailors on shore leave—$100 million on renovations to the Columbia lot, private jets, lavish parties, and a string of expensive flops. "Hudson Hawk," "Radio Flyer," "Last Action Hero"—each failure more expensive than the last. By 1994, Sony was forced to take a $2.7 billion write-down on the Columbia acquisition, one of the largest corporate write-offs in history. The Japanese financial press called it "Sony's Vietnam."

But hidden in the wreckage was an asset that would prove invaluable: Columbia's film library and, crucially, a character named Spider-Man. Sony had acquired the film rights to Marvel's web-slinger as part of the Columbia package, though nobody thought much of it at the time—superhero movies were considered dead after the Batman franchise had flamed out.

The synergy strategy—using Sony hardware to distribute Sony content—never quite worked as planned. The company developed the MiniDisc as a successor to the cassette Walkman, but the format failed partly because Sony Music was reluctant to license its catalog to competitors' devices. Different divisions had different priorities: the hardware teams wanted open standards to drive adoption, while the content teams wanted proprietary systems to protect intellectual property.

This tension reached its apotheosis with the digital music revolution. Sony was perfectly positioned to create iTunes—they had the best portable music players (Walkman), a massive music catalog (Sony Music), and the engineering capability to build an elegant digital ecosystem. Instead, they created a byzantine system of competing standards, incompatible software, and DRM restrictions so onerous that even Sony artists complained.

The Connect Music Store, launched in 2004 as Sony's answer to iTunes, was a masterpiece of corporate dysfunction. It only worked with Sony devices, used a proprietary ATRAC audio format that nobody wanted, and required users to install software so bloated and slow that it became a running joke in tech forums. Meanwhile, Steve Jobs was signing deals with all the major labels—including Sony Music—for iTunes, using Sony's own content to destroy Sony's hardware business.

Yet despite the execution failures, the content acquisition strategy wasn't entirely wrong. By 2000, Sony Music was generating over $5 billion in annual revenue. Sony Pictures, after the Guber-Peters debacle, had stabilized under new management and was producing hits like "Men in Black" and "Jerry Maguire." The company now had three major revenue streams—electronics, music, and movies—providing some insulation from the brutal cycles of the consumer electronics business.

More importantly, Sony had learned valuable lessons about managing creative businesses. The most important: you can't run a Hollywood studio or a record label like a Japanese electronics manufacturer. Creative industries require different metrics, different timelines, and most importantly, different types of leadership. The rigid consensus-building culture that worked in Tokyo was poison in Hollywood, where quick decisions and strong personalities ruled.

The content empire would never achieve the seamless synergy that Ohga had envisioned. But it would provide something else—diversification, intellectual property, and most unexpectedly, the foundation for Sony's transformation into an entertainment powerhouse. Those Spider-Man rights that came with Columbia? They would generate over $8 billion in box office revenue alone. The music catalog that seemed overpriced in 1988? It would become the backbone of the streaming economy, generating hundreds of millions in annual licensing fees.

But while Sony was learning to navigate the treacherous waters of content creation, a small team in Tokyo was working on something that nobody at headquarters was paying much attention to—a video game console born from spite, rejection, and the wounded pride of a single engineer.

V. The PlayStation Gambit: Accidental Gaming Giant

Ken Kutaragi was not supposed to be at the Consumer Electronics Show in June 1991, and he definitely wasn't supposed to be watching Nintendo's press conference with murderous rage in his eyes. The Sony engineer, known internally as a difficult genius who'd already been relegated to the corporate equivalent of Siberia for his unconventional ideas, watched as Nintendo unveiled their new Super Nintendo Entertainment System—without any mention of the CD-ROM add-on that Sony had spent three years developing. The partnership was dead, killed in a backroom deal between Nintendo and Philips, and Sony had found out the same way as everyone else: through a public humiliation on the CES stage.

The betrayal stung particularly because Kutaragi had fought tooth and nail within Sony just to work with Nintendo in the first place. In 1988, he'd designed the sound chip for the Super Famicom (Super Nintendo) as a side project, against the wishes of Sony executives who thought video games were toys beneath their dignity. The CD-ROM project was supposed to be the next evolution—a device that would play both Super Nintendo cartridges and Sony's new "Super Disc" format. Sony had even shown a prototype, called the Nintendo Play Station (two words), at CES just one day before Nintendo's betrayal.

Most companies would have written off the investment and moved on. But Norio Ohga, still smarting from the Betamax loss, saw an opportunity for revenge. "If Nintendo wants to betray us," he reportedly told the board, "then we'll show them what Sony engineering can really do." He gave Kutaragi a budget, a team, and more importantly, air cover from the Sony executives who thought entering the video game business was insane.

The skeptics had good reasons. The video game industry in 1991 was dominated by two Japanese companies—Nintendo and Sega—who controlled everything from hardware to software distribution. The conventional wisdom was that you needed iconic characters (Mario, Sonic) to sell consoles. Sony had none. You needed relationships with game developers. Sony had none. You needed retail distribution specifically designed for the unique economics of video games. Sony had none.

What Sony did have was superior technology and a chip on its shoulder. Kutaragi's team, working in a small office in Sony's Aoyama district, designed a console built around 3D graphics—a huge gamble since most games were still 2D sprites. They used CD-ROMs instead of cartridges, which meant games could be larger and cheaper to produce. Most radically, they designed the development kit to be remarkably developer-friendly, a direct contrast to Nintendo's notoriously difficult programming environment.

The PlayStation launched in Japan on December 3, 1994, priced at ¥37,000 (about $370). The killer app wasn't a Sony game—it was "Ridge Racer" from Namco, a 3D racing game that looked like nothing anyone had seen on a home console. The entire initial production run of 100,000 units sold out on day one. By March 1995, they'd sold one million units in Japan alone—faster than any console in history.

But the real test would be America, where Nintendo and Sega had spent decades building brand loyalty. Sony's solution was brilliant in its simplicity: they wouldn't compete for Nintendo's younger audience. Instead, they'd create a new market—older teenagers and young adults who'd grown up with Nintendo but wanted something more mature. The marketing campaign, with its edgy "U R Not E" (You Are Not Ready) tagline and ads in magazines like Rolling Stone rather than GamePro, positioned PlayStation as the console for people who thought they'd outgrown gaming.

The September 1995 U.S. launch was a masterclass in disruption. Price: $299, undercutting Sega's competing Saturn by $100. Launch titles: a carefully curated mix including "Battle Arena Toshinden," "Rayman," and "ESPN Extreme Games." But the real coup was yet to come. At the first E3 (Electronic Entertainment Expo) in May 1995, Steve Race, president of Sony Computer Entertainment America, walked on stage for Sony's pricing announcement. His entire presentation consisted of nine words: "Two hundred and ninety-nine dollars." He then walked off stage to thunderous applause. Sega, which had just announced Saturn at $399, was dead in the water.

By 1997, PlayStation had captured 47% of the global console market. By 1998, it was 61%. Nintendo, the company that had betrayed Sony, saw its market share collapse from 80% to under 30%. The PlayStation would go on to sell 102 million units, becoming the first home console to break the 100 million barrier.

But the real masterstroke was the PlayStation 2, launched in March 2000. Kutaragi, now running Sony Computer Entertainment with near-total autonomy, made another bold bet: the PS2 would be a DVD player as well as a game console. At $299, it was cheaper than many standalone DVD players, making it the Trojan horse that brought gaming into millions of homes that had never owned a console.

The PS2 was a phenomenon that's hard to comprehend in today's fragmented entertainment landscape. It sold 155 million units, making it the best-selling console of all time. Grand Theft Auto: Vice City sold 20 million copies. Final Fantasy X sold 10 million. The console was so successful that Sony kept manufacturing it until 2013—thirteen years after launch, an eternity in technology terms.

Sony had also solved the software problem through patient relationship building and strategic acquisitions. Naughty Dog (Crash Bandicoot, later Uncharted), Insomniac Games (Spyro, Ratchet & Clank), and Polyphony Digital (Gran Turismo) became first-party studios creating exclusive content. The company that had no gaming DNA in 1991 now had some of the industry's most talented developers.

The financial impact was transformative. By 2002, PlayStation was generating over $7 billion in annual revenue and was Sony's most profitable division. Gaming, the business that Sony executives had thought beneath them, was now keeping the entire company afloat as the consumer electronics business faced increasing pressure from Korean competitors.

The PlayStation 3, launched in 2006, would test Sony's gaming dominance. Kutaragi, now drunk on his own success, created a console that was a technical marvel but a commercial disaster at launch. The Cell processor was so complex that developers couldn't figure out how to program for it. The launch price—$599 for the premium model—prompted infamous memes about working "three jobs" to afford it. Sony's arrogant marketing, suggesting that consumers would buy it regardless of price because it was PlayStation, backfired spectacularly.

Microsoft's Xbox 360, launched a year earlier at a lower price with better online features, ate into Sony's market share. Nintendo's Wii, with its motion controls and $249 price point, outsold both of them by targeting casual gamers Sony had ignored. The PS3 would eventually recover, selling 87 million units, but it was a humbling reminder that technical superiority alone doesn't guarantee success.

Yet even this stumble couldn't kill PlayStation's momentum. The division had become too important, contributing nearly 30% of Sony's operating profit by 2010. When the rest of Sony was crumbling in 2012, PlayStation was one of the few divisions still making money. The PlayStation 4, launched in 2013 under new leadership, would return Sony to dominance, selling 117 million units and reestablishing PlayStation as the premium gaming platform.

The accidental gaming giant born from Nintendo's betrayal had become Sony's most important business. But while PlayStation was printing money, the rest of Sony was falling apart, victim to the very success that had made it great.

VI. The Lost Decade: Arrogance, Silos, and Near-Death

The meeting at Sony headquarters in January 2001 should have been a victory lap. Engineers from the Walkman division had gathered to demonstrate their latest creation—a hard-drive based digital music player, two years before Apple would announce the iPod. The device held 60GB of music, had a beautiful color screen, and bore the iconic Walkman brand that had defined portable music for two decades. The executives killed it. Why? Because Sony Music didn't want a device that could enable piracy, Sony's PC division wanted to control any hard-drive product, and the Memory Stick division saw it as competition for their proprietary format. The prototype went back on the shelf, where it would gather dust while Steve Jobs prepared to eat Sony's lunch.

This wasn't an isolated incident—it was symptomatic of a disease that had metastasized throughout Sony. The company had evolved into a collection of warring fiefdoms, each with its own P&L, its own agenda, and its own definition of success. The electronics division wouldn't talk to the entertainment division. The computer team actively sabotaged the consumer electronics team. Sony Music sued Sony Electronics' customers for piracy. It was corporate schizophrenia on a massive scale.

The roots of this dysfunction traced back to Sony's very success. Each breakthrough product had spawned its own division with its own president, manufacturing, and marketing. By 2000, Sony had 70 separate business units, each defending its turf with samurai intensity. The company that Morita and Ibuka had built on collaboration had become a confederation of competing kingdoms.

Howard Stringer's appointment as CEO in 2005 was supposed to fix this. The Welsh-born former journalist was Sony's first foreign CEO, a shock to the Japanese corporate establishment that demonstrated how desperate the board had become. Stringer had successfully run Sony's American operations, turning around the music and film divisions. Surely, the thinking went, an outsider could break down the silos that were killing the company. Stringer's reality was far more complex. He later famously described his experience: "Running a big company is like running a cemetery: there are thousands of people beneath you, but no one is listening. It was a bit like that at Sony." He specifically lamented that Sony had a "not invented here" mentality that did not suit an increasingly digital world, and which Stringer was unable to shake off. The Japanese engineering culture that had been Sony's greatest strength had calcified into its greatest weakness.

The iPod disaster perfectly encapsulated the problem. When Apple launched the iPod in October 2001, Sony had every advantage: the Walkman brand, superior hardware engineering, a massive music catalog through Sony Music, and years of experience in portable music. Their response? The Network Walkman NW-MS7, which held a pathetic 60 minutes of music using Sony's proprietary ATRAC format and Memory Stick storage. It cost more than an iPod, held less music, and required proprietary software so user-hostile that installing it felt like digital root canal. The TV business was even worse. Sony had pioneered flat-panel displays with the Trinitron, but by 2005, they were being destroyed by Samsung and LG, who could produce LCD panels at half the cost. Sony's response was to double down on premium pricing, creating beautiful but absurdly expensive televisions that nobody bought. The TV division alone lost $10 billion over 10 years.

The 2008 financial crisis accelerated the decline. Sony hit record earnings of 8.87 trillion yen in sales and 369.4 billion yen in after-tax profits in March 2008, but it was a peak built on sand. The yen's appreciation made Sony's products uncompetitive globally. The Thailand floods of 2011 disrupted production. And most devastatingly, the company suffered a massive cyberattack on the PlayStation Network in April 2011, compromising 77 million accounts and forcing a 23-day shutdown that cost hundreds of millions in remediation and destroyed consumer trust.

By 2012, the numbers were catastrophic. Sony forecast a record 520 billion yen ($6.4 billion) net loss for the year ending March 2012—double the 220 billion yen loss they had forecast just two months earlier in February. This was the fourth straight year the company finished in the red. The stock price had fallen 75% from its peak. Credit rating agencies were preparing downgrades. Media reports indicated Sony would cut 10,000 jobs—around 6 percent of its global workforce.

The PlayStation 3, which should have been Sony's savior, had become another millstone. Ken Kutaragi's Cell processor architecture was so complex that developers nicknamed it "the PlayStation 3-year development cycle." The launch price of $599 for the 60GB model prompted Kutaragi to infamously suggest that consumers should "work more hours to afford it." The console launched a year after Xbox 360, giving Microsoft a crucial head start. By the time PS3 found its footing, the damage was done—market share lost, developer relationships strained, and billions in losses accumulated.

The company that had invented portable music couldn't make a digital music player. The company that had created the most successful gaming platform couldn't launch a console properly. The company that had defined premium televisions was losing money on every set sold. Sony wasn't just failing—it was failing at everything it had once dominated.

In April 2012, Kazuo Hirai took over as CEO from Howard Stringer, inheriting what looked like a corporate death spiral. The 51-year-old Sony lifer, who had successfully run the PlayStation division through its darkest period, faced an almost impossible task: save Sony from itself. The prescription would be radical surgery—cutting away decades of accumulated dysfunction to find the healthy core that might, just might, still exist underneath.

VII. The Kazuo Hirai Turnaround: "One Sony" Renaissance

Kazuo Hirai stood before 300 Sony executives in April 2012, holding a single sheet of paper with one word written in both English and Japanese: "Kando"—the power to move people emotionally. "We've forgotten why we exist," he said, his voice carrying a mix of disappointment and determination. "We make products, but we've stopped creating experiences that move people. That changes now."

Unlike Stringer, who had tried to manage Sony from 6,000 miles away while commuting between New York and Tokyo, Hirai was a Sony creature through and through. He'd joined the company's music division in 1984, helped launch the PlayStation business in America, and saved the PS3 from complete disaster. Most importantly, he understood both the Japanese engineering culture and the Western content business—he was bicultural in a way Stringer never could be. His first move was symbolic but powerful: Hirai and six other top executives returned all performance-based pay received for 2011 to the company and promised that all seven would forgo bonuses in 2012. The message was clear—leadership would share the pain of restructuring.

The "One Sony" strategy, announced in March 2012, focused on three electronic pillars: digital imaging, games, and mobile. These weren't random choices—they were the only divisions consistently making money. Everything else would be restructured, sold, or killed.

The cuts were brutal by Japanese standards. 10,000 jobs were eliminated despite the Japanese tradition of employing staff for life—6% of the global workforce. The VAIO PC division, once Sony's pride, was sold to Japan Industrial Partners in 2014. The TV business, which had lost money for a decade straight, was spun off into a separate company, allowing it to source panels from competitors and finally compete on cost.

But Hirai's genius wasn't just in cutting—it was in integration. The silos that had paralyzed Sony were systematically demolished. The TV business, previously autonomous, was placed under Hirai's direct oversight. Mobile, imaging, and gaming divisions were forced to share technology and resources. The Xperia phone team started using image sensors from the Alpha camera division. PlayStation's streaming technology was integrated into TVs and phones.

The PlayStation 4 launch in November 2013 exemplified the new Sony. Instead of Kutaragi's exotic Cell processor, they used standard PC architecture, making it easy for developers. Instead of arrogant pricing, they undercut Microsoft's Xbox One by $100. Instead of focusing on technical specs, they emphasized games and social features. Mark Cerny, the PS4's lead architect, gave developers exactly what they wanted: a powerful but familiar platform.

The results were immediate. PS4 sold one million units on launch day, becoming the fastest-selling console in PlayStation history. By 2017, it had sold over 73.6 million units, thoroughly defeating Xbox One and reestablishing PlayStation's dominance.

Meanwhile, Sony's image sensor business was quietly becoming a juggernaut. Hirai recognized that while Sony couldn't compete in finished smartphones, they could dominate the components that powered them. By 2015, Sony sensors were in every iPhone, most high-end Android phones, and increasingly in automotive and security applications. The division that barely registered in financial reports a decade earlier was generating billions in high-margin revenue. By 2015, the turnaround was undeniable. Sony's operating profit doubled to 178.3 billion yen ($1.52 billion) in the October-December quarter, well above estimates of 96.6 billion yen in a Reuters poll. Sales rose 6 percent to 2.56 trillion yen, above consensus estimates of 2.38 trillion yen. The TV business, which hadn't made money in a decade, posted three straight quarters of profit. Every single business unit was profitable for the first time in years.

In 2016, Sony posted a 666.5 percent rise in pretax profit for its full fiscal year, helped by cost cutting in its smartphone business and the continued popularity of the PlayStation 4. The gaming division saw operating income rise 84.3 percent to 88.7 billion yen, with PS4 sales topping 35 million units.

The financial recovery was matched by cultural transformation. The company that had been paralyzed by consensus-building started making bold decisions quickly. When virtual reality emerged as the next frontier, Sony didn't committee it to death—they launched PlayStation VR in 2016, becoming the first major console maker to embrace VR.

The Spider-Man franchise, dormant since the Andrew Garfield films flopped, was revitalized through an unprecedented deal with Marvel Studios. Sony retained the film rights while allowing Spider-Man to appear in the Marvel Cinematic Universe. "Spider-Man: Homecoming" (2017) grossed $880 million worldwide, validating the collaborative approach.

By 2017, Sony was consistently profitable, with operating profit topping ¥285 billion—19% higher than forecast. It marked the second straight year operating profit had topped $2 billion, the longest such streak since 2001. The stock price, which had bottomed at ¥900 in 2012, climbed above ¥5,000 by 2018.

Hirai's transformation went beyond financial metrics. He had changed Sony's DNA from a hardware company that happened to make content to an entertainment company that also made hardware. The image sensor business wasn't just selling components—it was enabling the global smartphone camera revolution. PlayStation wasn't just selling consoles—it was building digital communities. Even the struggling mobile division had found its niche, focusing on high-margin premium phones rather than chasing market share.

In February 2018, Sony announced that Hirai would step down as CEO, to be replaced by CFO Kenichiro Yoshida. Unlike Stringer's departure in disgrace, Hirai left as a hero, having saved Sony from near-certain death and positioned it for a future that looked nothing like its past.

The "One Sony" initiative had worked, but not in the way anyone expected. Instead of forcing divisions to work together through corporate mandate, Hirai had given them a common enemy—irrelevance—and a common goal—survival. The company that emerged from this crucible was leaner, more focused, and paradoxically, more innovative than it had been in decades.

VIII. Modern Sony: Gaming, Sensors, and Spider-Man

The conference room at Sony Interactive Entertainment's San Mateo headquarters erupted in nervous laughter when Shawn Layden, then-chairman of SIE Worldwide Studios, asked the question everyone was thinking: "So we're really going to let Insomniac make a Spider-Man game that has nothing to do with the movies?" It was 2014, and Sony was about to make one of the most important creative decisions in its gaming history—trusting its most valuable IP to a studio it didn't even own.

The resulting game, Marvel's Spider-Man, released in September 2018, would sell 20 million copies and spawn a franchise worth billions. But more importantly, it represented the new Sony—one that understood IP value, platform exclusivity, and the power of letting creative teams do what they do best without corporate interference. The PlayStation 5 launch in November 2020 should have been a disaster. COVID-19 had disrupted supply chains globally, semiconductor shortages were crippling production, and Sony was launching a $499 console during a global recession. Instead, it became the largest launch in PlayStation history, with two weeks after launch, Sony declared the largest launch in PlayStation history, surpassing the PlayStation 4's 2.1 million units in its first two weeks in 2013.

The PS5's success wasn't accidental—it was the culmination of lessons learned from the PS3's hubris and PS4's recovery. Mark Cerny, the console's lead architect, designed a system that was powerful but developer-friendly, using standard AMD architecture rather than exotic custom chips. The pricing was aggressive but not arrogant. Most importantly, Sony had learned that exclusive content, not technical specifications, sold consoles.

By 2024, Sony had reached a milestone of 40 million PS5 consoles sold through to gamers since launch, despite unprecedented supply chain challenges. In December 2024, the manufacturer reported an installed base of 75 million units worldwide. With 75 million units sold by the end of 2024 and a total of 77.8 million by March 31, 2025, the PlayStation 5 confirmed its place as one of the most successful consoles of its generation.

More impressively, between when the PS5 launched in late 2020 and now, it's generated $106 billion in sales, and a total operating profit of $10 billion, making it the most successful PlayStation console ever—achieving in less than four years what took the PS4 seven years to accomplish.

But gaming was only one pillar of modern Sony's success. The image sensor business had evolved from a footnote in financial reports to a cornerstone of the company's profitability. By 2020, Sony controlled 55% of the global image sensor market, with their sensors in virtually every flagship smartphone. The iPhone 12 Pro's advanced camera system? Sony sensors. Samsung's Galaxy S21 Ultra's 108-megapixel camera? Sony sensor. Google's computational photography magic in the Pixel? Built on Sony hardware. The automotive sector represented the next frontier. The automotive image sensor market is forecasted to increase from US$2.3 billion in 2023 to US$3.2 billion by 2029 with a 5.4 percent CAGR, and Sony was positioning itself to capture a significant portion. Their sensors weren't just for backup cameras anymore—they were enabling the autonomous driving revolution, with each self-driving car requiring dozens of high-resolution sensors for navigation and safety.

Sony had pushed back its target to capture a 60% revenue market share in image sensors, originally set for 2025, but even at their current roughly 50% share, they dominated the market. The global image sensor market is expected to be valued at USD 20.66 billion in 2024 and is projected to reach USD 29.62 billion by 2029, at a CAGR of 7.5% from 2024–2029, meaning Sony's sensor business alone could be worth $15 billion annually by decade's end.

The Spider-Man franchise had evolved from a movie property into a multi-billion dollar transmedia empire. "Spider-Man: No Way Home" (2021) grossed $1.9 billion worldwide despite pandemic restrictions. The animated "Spider-Verse" films redefined what superhero movies could be, with "Across the Spider-Verse" (2023) grossing over $690 million while costing a fraction of live-action blockbusters. The PlayStation Spider-Man games had sold over 33 million copies combined. Sony had turned a single character into an ecosystem worth more than many entire studios.

The synergies that had eluded Sony for decades were finally materializing, but not in the way anyone had predicted. PlayStation games were becoming HBO shows ("The Last of Us"). Sony Pictures was producing films based on PlayStation properties ("Uncharted," "Gran Turismo"). The image sensor division was enabling new forms of content creation through computational photography and AI-enhanced imaging. Even the struggling music division had found new life in the streaming era, with Sony Music's catalog generating consistent high-margin revenue from Spotify, Apple Music, and YouTube.

But perhaps the most significant transformation was cultural. The company that had once operated as warring fiefdoms now functioned as a coordinated enterprise. When Apple announced its Vision Pro AR headset, Sony didn't panic or rush to copy—they leveraged their existing strengths, providing the micro-OLED displays that powered Apple's device while simultaneously developing PlayStation VR2 for their own ecosystem.

The modern Sony bore little resemblance to the consumer electronics giant of the 1980s or the bloated conglomerate of the 2000s. It was leaner, more focused, and paradoxically more diversified—not in terms of products but in terms of value creation. Gaming, sensors, and entertainment weren't just business divisions; they were platforms for innovation that reinforced each other in unexpected ways.

By 2024, Sony's transformation was complete. The company that had nearly died trying to be everything to everyone had found success by becoming indispensable in a few critical areas. They didn't make the phones, but they powered the cameras. They didn't dominate theatrical distribution, but they owned some of the most valuable IP in entertainment. They weren't the biggest gaming company by revenue, but PlayStation defined premium gaming experiences.

IX. Business Model Evolution & Strategic Lessons

The boardroom at Sony's Tokyo headquarters in 2019 looked nothing like it had in 1999. Gone were the rows of identical dark-suited executives nodding in choreographed agreement. In their place sat a diverse group including a former Apple Japan president, the head of a pharmaceutical company, and remarkably, executives who openly disagreed with each other. This wasn't just cosmetic change—it represented a fundamental reimagining of how Sony created and captured value.

The transformation from hardware manufacturer to platform owner didn't happen overnight, and it certainly didn't follow any Harvard Business School playbook. Instead, it was a messy, often painful evolution driven by near-death experiences, lucky accidents, and the gradual recognition that Sony's greatest asset wasn't its engineering prowess but its ability to create emotional connections with consumers.

Consider the economics of the PlayStation business model evolution. The original PlayStation in 1994 was a traditional razor-and-blades model: sell hardware at a loss, make money on software royalties. Simple, proven, effective. By the PS2 era, Sony had added backward compatibility and DVD playback, transforming the console into a trojan horse for the living room. The PS3 nearly broke this model with its complex Cell processor and $599 launch price—a case study in how technical superiority without economic sense equals disaster.

But the PS4 and PS5 generations revealed Sony's new understanding: the platform wasn't just about the hardware or even the software—it was about the network. PlayStation Plus, launched in 2010 as a premium service, had evolved into a $3.8 billion annual revenue stream by 2023. With over 47 million subscribers paying $60-120 annually, it generated higher margins than hardware sales ever could. The real genius? These subscribers weren't just paying for online multiplayer—they were paying for community, for curated experiences, for the privilege of being part of the PlayStation ecosystem.

The component business told a different story about value creation. Sony's image sensors weren't commodities—they were platforms for innovation that others built upon. When Apple wanted to revolutionize smartphone photography with computational imaging, they needed Sony's sensors as the foundation. When Tesla needed reliable cameras for Autopilot, they turned to Sony. The company had learned that sometimes the most profitable position isn't selling the final product but being the indispensable ingredient everyone else needs.

This shift required a fundamental rethinking of R&D investment. In the old Sony, each division jealously guarded its research budget, leading to duplicate efforts and missed synergies. The new Sony created centralized research initiatives that multiple divisions could leverage. The AI and robotics research that started for PlayStation's gesture recognition ended up improving camera autofocus algorithms. The audio processing developed for headphones enhanced the spatial audio in PlayStation VR.

The content strategy represented perhaps the most radical departure from traditional Japanese corporate thinking. Sony Pictures and Sony Music weren't just profit centers—they were IP factories that fed multiple revenue streams. A Spider-Man movie wasn't just box office revenue; it was merchandise, streaming rights, theme park attractions, video games, and brand equity that enhanced the value of the entire Sony ecosystem. The company had finally understood what Disney had known for decades: content is king, but IP is emperor.

The financial engineering behind this transformation was equally sophisticated. Sony Financial Holdings, often overlooked by Western analysts, generated over $10 billion in annual revenue by 2023, providing stable cash flows that buffered the volatility of entertainment and electronics. This wasn't the sexy part of Sony, but it was the ballast that allowed the company to take creative risks elsewhere.

The subscription economy transformation extended beyond PlayStation Plus. Sony's various services—from Crunchyroll (anime streaming) to PlayStation Now (game streaming) to music streaming revenues—generated over $7 billion annually in recurring revenue by 2024. This wasn't just income; it was predictable, high-margin revenue that Wall Street loved and that provided the financial stability to invest in long-term projects.

But perhaps the most important business model innovation was Sony's approach to creative talent. Unlike the old days of trying to force Hollywood executives to follow Japanese corporate protocols, Sony learned to create semi-autonomous creative units with their own cultures and incentive structures. Santa Monica Studio (God of War) operated differently from Polyphony Digital (Gran Turismo), which operated differently from Columbia Pictures. The corporate umbrella provided resources and distribution, but creative decisions were pushed down to the people who understood their specific markets.

The "patient capital" approach that had seemed like a weakness during the Stringer era—the inability to make quick, decisive cuts—became a strength when properly directed. While competitors chased quarterly earnings, Sony could spend five years developing a single game (The Last of Us Part II) or a decade building a sensor fabrication facility. This patience, combined with the financial cushion from diverse revenue streams, allowed Sony to play a different game than purely quarterly-focused competitors.

The network effects in gaming had become Sony's most powerful moat. Every exclusive title increased the value of owning a PlayStation. Every PlayStation owner increased the value for developers to create for the platform. Every developer creating for the platform increased the value for other players to join the ecosystem. It was a virtuous cycle that Microsoft, despite spending $70 billion to acquire Activision Blizzard, still struggled to replicate.

The management philosophy had evolved from consensus-building (which really meant conflict avoidance) to what Yoshida called "creative tension"—productive disagreement in service of better outcomes. Engineers could challenge marketers. The game studios could push back on corporate mandates. This wasn't the Japanese way, but it was becoming the Sony way.

Risk management had also transformed. The old Sony took massive, bet-the-company risks on formats (Betamax, MiniDisc, Memory Stick) that locked them into rigid strategies. The new Sony diversified its bets, partnering when necessary (Blu-ray with others, streaming services with multiple platforms), and killing products quickly when they didn't work (PlayStation Vita, Sony Reader).

The lesson for other companies wasn't just about business model transformation—it was about cultural evolution. Sony had learned that in creative industries, you can't manage through spreadsheets and org charts. You need to create environments where talent wants to work, where creative risks are rewarded, and where failure is learning, not career death.

By 2024, Sony's business model had become a complex symphony of interrelated parts: gaming platforms generating recurring revenue, components enabling others' innovations, content creating cultural moments, and financial services providing stability. It wasn't the simplest strategy to explain to Wall Street, but it was proving to be remarkably resilient. The company that had almost died from trying to be everything had found success in being essential—not everywhere, but in the places that mattered most.

X. Competitive Analysis & Market Position

Jim Ryan, then-CEO of Sony Interactive Entertainment, stood before a packed auditorium at CES 2023 and did something unprecedented for a Sony executive: he publicly congratulated Microsoft on their Activision Blizzard acquisition. "Competition makes us all better," he said with a slight smile, knowing that behind closed doors, Sony's legal team had spent months trying to block the $69 billion deal. This wasn't corporate politeness—it was recognition that the competitive landscape had fundamentally changed, and Sony's response wouldn't be to match Microsoft's checkbook but to play an entirely different game.

The gaming battlefield in 2024 looked nothing like it had even five years earlier. Microsoft's acquisition spree—Bethesda for $7.5 billion, Activision Blizzard for $69 billion—had transformed them from a distant third place into an existential threat. They owned Call of Duty, World of Warcraft, Candy Crush, Elder Scrolls, Fallout, and dozens of other franchises. Their Game Pass subscription service, with over 25 million subscribers, was Netflix-ifying gaming. Phil Spencer, Xbox head, wasn't even talking about Sony anymore—his stated competitors were Google, Amazon, and Apple. Sony's response was quintessentially Japanese: they didn't try to outspend Microsoft; they focused on what they did best. The numbers told the story: The PlayStation 5 has sold 24.54 million units in the US in 50 months, while the Xbox Series X|S sold 16.41 million units. The PlayStation 5 has a 59.9 percent marketshare (+2.1% year-over-year), compared to 40.1 percent for the Xbox Series X|S (-2.1% year-over-year). Globally, the gap was even more pronounced, with PS5 sales reaching 67.7 million units globally compared to the Xbox series X|S which sold 31.2 million, giving Sony's PS5 the big lead of 36.49 million units.

But the real competitive advantage wasn't hardware sales—it was ecosystem lock-in. PlayStation's first-party studios had become the envy of the industry. Santa Monica's "God of War" (2018) and "God of War Ragnarök" (2022) weren't just games; they were cultural events. Naughty Dog's "The Last of Us Part II," despite controversy, sold 10 million copies and swept award shows. These weren't just products; they were reasons to buy PlayStations.

Nintendo, meanwhile, operated in a parallel universe where Sony and Microsoft's arms race was irrelevant. The Switch, with its 2017-era mobile processor, had sold over 143 million units by 2024, making it one of the best-selling consoles ever. Nintendo's strategy—unique hardware, unmatched first-party games, and complete indifference to technological superiority—was the antithesis of everything Sony had traditionally stood for, yet it was devastatingly effective.

Sony's response to Nintendo was perhaps the smartest non-response in gaming history: they didn't compete. There was no PlayStation Switch competitor, no portable hybrid. Instead, Sony focused on experiences Nintendo couldn't deliver—photorealistic graphics, mature narratives, technically demanding games that required serious hardware. The two companies had effectively divided the gaming market without firing a shot at each other.

In the entertainment space, Sony faced a different set of competitors. Disney remained the IP juggernaut, with Marvel and Star Wars dwarfing even Spider-Man's impressive numbers. Netflix and Amazon were spending tens of billions on content, making Sony Pictures look like a boutique operation. Yet Sony had found its niche—mid-budget films that consistently profit, prestige television through Sony Pictures Television ("Breaking Bad," "The Crown"), and strategic IP exploitation that maximized value without Disney-level investment.

The streaming wars presented a unique challenge. Sony had no Disney+, no HBO Max, no Netflix competitor. Instead, they became the arms dealer, licensing content to everyone. Sony's film and TV library generated billions in licensing fees from streaming services desperate for content. When Netflix needed anime, they turned to Sony-owned Crunchyroll. When Disney+ needed Spider-Man movies, they paid Sony. It was less glamorous than owning a streaming service, but far more profitable given the infrastructure costs.

In components, the competitive landscape was shifting rapidly. Samsung remained a formidable competitor in image sensors, and Chinese companies were rapidly improving their capabilities. Sony's response was to move upmarket—developing specialized sensors for automotive, medical, and industrial applications where quality mattered more than price. The strategy mirrored what they'd done in consumer electronics: when you can't compete on cost, compete on capability.

The metaverse and AR/VR represented the next competitive frontier, and here Sony's position was precarious. Meta (formerly Facebook) was spending over $13 billion annually on Reality Labs. Apple's Vision Pro, despite its $3,500 price tag, represented a technological leap that Sony's PSVR2 couldn't match. Microsoft's HoloLens had captured the enterprise market. Sony's advantage—gaming content and a large installed base—might not be enough if the paradigm truly shifted.

Yet Sony had learned from past transitions. They weren't betting everything on VR being the future; they were hedging. PSVR2 was an enthusiast product, not a mass-market play. They were suppliers to competitors (providing displays for Apple's Vision Pro) while developing their own capabilities. It was a strategy born from the hard lessons of Betamax, MiniDisc, and Memory Stick—sometimes it's better to be part of everyone's success than to fail at creating your own standard.

The China challenge loomed large across all divisions. Chinese companies were rapidly moving up the value chain in components, creating compelling games for global audiences, and even challenging in content creation. Sony's response was nuanced—partnering where beneficial (Genshin Impact on PlayStation), competing where necessary (image sensors), and leveraging their brand premium where Chinese companies couldn't yet match them.

By 2024, Sony's competitive position could be summarized as: dominant in premium gaming, critical in components, profitable in entertainment, and cautiously optimistic about emerging technologies. They weren't the biggest in any category except gaming, but they were profitable in all of them. In a world where Amazon could lose billions on gaming (Luna), where Meta could burn $13 billion annually on VR, where Microsoft could spend $69 billion on acquisitions, Sony's ability to generate consistent profits from focused excellence seemed almost quaint—and remarkably effective.

The greatest competitive threat wasn't any single company but the pace of technological change itself. As gaming moved toward cloud streaming, as AI transformed content creation, as new platforms emerged, Sony's carefully constructed competitive advantages could evaporate. But for now, in 2024, Sony had found a sustainable position: not trying to dominate every market, but being indispensable in the markets that mattered most.

XI. Bear vs. Bull Case

The investment committee at Fidelity's Tokyo office was in its fourth hour of debate on a seemingly simple question: Is Sony a buy at ¥16,800 per share? The bear case presenter, a veteran analyst who'd covered Sony since the Walkman era, was methodically dismantling the bull thesis with the precision of a PlayStation exclusive boss fight. "Look at the fundamentals," she argued, pulling up a slide showing global smartphone shipments declining for the fifth consecutive year. "Their sensor business is tied to a mature market. Gaming margins are compressing as development costs explode. And they're about to face the most challenging competitive environment in their history."

The Bear Case: Structural Headwinds and Strategic Vulnerabilities

The bear thesis started with an uncomfortable truth: hardware margins across the industry were in terminal decline. Sony's gaming hardware, which barely broke even in the best of times, faced a future where Moore's Law was slowing, component costs were rising, and consumers were increasingly resistant to premium pricing. The PS5 Pro's $700 price tag had generated significant backlash, suggesting Sony had hit the ceiling of what the market would bear.

Microsoft's acquisition spree represented an existential threat that markets hadn't fully priced in. With Activision Blizzard, Microsoft now owned Call of Duty, which historically drove 10-15% of PlayStation Store revenue through game sales and microtransactions. Even with regulatory agreements keeping COD on PlayStation, Microsoft could slowly strangle Sony through a thousand cuts—exclusive content, delayed releases, Game Pass perks that PlayStation couldn't match.

The gaming consolidation wave was just beginning. If Microsoft's Activision deal was the appetizer, what happened when Apple, Amazon, or Google decided they wanted in? Sony, with a market cap of $115 billion, couldn't compete in an acquisition arms race against companies worth trillions. Every major independent studio that got acquired was one less exclusive Sony could secure.

China's component competition was accelerating faster than analysts appreciated. Chinese image sensor manufacturers, backed by government subsidies and with access to a massive domestic market, were improving at a rate reminiscent of Korean companies in the 1990s. Sony's 50% sensor market share looked dominant today, but Kodak had once dominated film, and Nokia had ruled mobile phones.

The content business faced its own challenges. The streaming wars had turned into a war of attrition, with even Disney struggling to make streaming profitable. Sony's strategy of licensing to everyone worked when everyone was desperate for content, but as streamers consolidated and became more selective, Sony's lack of a direct-to-consumer platform could become a critical weakness.

The bears pointed to Sony's latest financial reports with concern. Despite record gaming revenue, operating margins had compressed from 13% to 9% as game development costs spiraled. Spider-Man 2 cost $300 million to develop, three times the cost of the original. The math was brutal: games needed to sell 10+ million copies just to break even on AAA productions.

Geographic concentration risk was understated. Sony generated 30% of its revenue from Japan, a market with a declining population and stagnant economy. Another 30% came from the United States, where regulatory scrutiny of Big Tech was intensifying and could easily expand to gaming ecosystems. Europe, facing its own economic challenges, represented another 25%. Sony had minimal presence in the high-growth markets of India, Southeast Asia, and Africa.

The AI disruption to content creation posed an existential threat. If generative AI could create games, music, and even films at a fraction of current costs, what happened to Sony's content moat? Smaller competitors could suddenly produce PlayStation-quality games without Sony's massive studios. The barriers to entry that protected Sony's businesses were crumbling.

The Bull Case: Undervalued Assets and Transformation Upside

The bull presenter, a younger analyst who'd made his reputation calling the gaming sector's COVID boom, countered with equal conviction. "You're looking at yesterday's Sony," he argued. "The market cap is up 57% in the past 12 months to $176 billion for a reason. This isn't a hardware company anymore—it's a platform and IP powerhouse trading at a discount to its sum-of-parts value."

The bulls started with valuation. At 15x forward earnings, Sony traded at a significant discount to Microsoft (30x), Disney (25x), and even struggling Intel (20x). The gaming division alone, generating $30 billion in revenue with 30% operating margins on software and services, could justify a $100 billion valuation. Add the sensor business, entertainment assets, and financial services, and Sony looked cheap at current prices.

The sensor dominance story was far from over. Yes, smartphones were mature, but automotive was just beginning. Each autonomous vehicle needed 20-40 image sensors compared to 3-4 in a smartphone. The automotive sensor market was projected to grow from $2.3 billion to $8 billion by 2030. Sony's 50% market share in a growing market was worth far more than bears acknowledged.

PlayStation's ecosystem moat was underappreciated. With 120 million monthly active users and 47 million paying subscribers, PlayStation had network effects that money couldn't buy. Microsoft might own Call of Duty, but Sony owned the relationship with the most valuable gaming customers—those willing to pay $500 for hardware and $70 for games.

Content library value was exploding in the streaming era. Sony's 3,500-film library and television production capabilities generated predictable, high-margin licensing revenue. As streaming services consolidated, content became more valuable, not less. The Spider-Man franchise alone had generated $10 billion in revenue and was still growing.

The transformation under Hirai and Yoshida had fundamentally changed Sony's DNA. This wasn't the siloed, slow-moving giant of 2012. PlayStation Studios operated with startup agility. The sensor division moved at semiconductor speed. The company had proven it could adapt, cut costs, and focus when necessary.

Emerging markets represented massive untapped potential. PlayStation had minimal presence in India, where gaming was growing 30% annually. The sensor business had barely scratched the surface of medical and industrial applications. Sony's brand, still powerful in emerging markets, could unlock billions in new revenue.

The subscription revenue transformation was still early. PlayStation Plus at 47 million subscribers had room to double. Crunchyroll dominated anime streaming with pricing power still to be realized. Sony's various subscription services could generate $15 billion annually by 2027, up from $7 billion today. The technical analysis added another layer of complexity. Based on analysis of 6 Wall Street analysts, SONY has a bullish consensus with a median price target of $30.83 (ranging from $30.50 to $35.82). The overall analyst rating is Strong Buy (9.2/10). Based on short-term price targets offered by five analysts, the average price target for Sony comes to $25.25. The forecasts range from a low of $23.00 to a high of $27.54. The average price target represents an increase of 8.88% from the last closing price of $23.19.

Capital allocation had improved dramatically. Sony was generating sufficient cash flow to invest in growth (new game studios, sensor fabrication), return capital to shareholders (dividends and buybacks), and maintain a fortress balance sheet. The company's net cash position provided flexibility to weather downturns or make opportunistic acquisitions.

The Verdict: A Complex Value Proposition

The investment committee's debate stretched into its sixth hour, with neither side claiming clear victory. The truth, as it often is, lay somewhere in the middle. Sony wasn't a simple growth story like Nvidia, nor was it a value trap like Intel. It was something more complex—a transformation story in its middle chapters, with both significant risks and underappreciated opportunities.

The bear case was right about the challenges: margin compression, competitive threats, and technological disruption were all real. But they underestimated Sony's proven ability to adapt and the value of its entrenched positions. The bull case was right about the undervaluation and transformation potential, but perhaps too optimistic about Sony's ability to navigate every transition successfully.

For investors in 2024, Sony represented a fascinating proposition: a company trading at a reasonable valuation with multiple ways to win but also multiple ways to disappoint. It wasn't a momentum play for growth investors or a deep value play for contrarians. It was a GARP (Growth at a Reasonable Price) opportunity for those who believed in the power of platforms, the value of IP, and the resilience of companies that had survived multiple near-death experiences.

The committee finally reached a consensus: Sony was a buy for investors with a 3-5 year horizon who could stomach volatility and appreciated complex turnaround stories. It wasn't for those seeking the next ten-bagger or those who needed predictable, steady returns. It was for investors who understood that in technology and entertainment, the companies that survive and thrive are those that can reinvent themselves while maintaining their core strengths.

As the meeting concluded, the senior portfolio manager summarized: "Sony at current prices isn't about betting on any single outcome. It's about buying a portfolio of real options—on gaming's future, on sensor ubiquity, on content value, on Japanese corporate transformation. Some will expire worthless, but others could be worth multiples of today's market cap. That's not a trade; it's an investment."

XII. Epilogue: Lessons for Founders & Investors

The cherry blossoms were in full bloom outside Sony's headquarters in April 2024 as Kenichiro Yoshida, Sony's current CEO, addressed a gathering of entrepreneurs and investors. "People ask me what Sony's secret is," he began, his voice carrying the weight of nearly 80 years of corporate history. "They expect me to talk about innovation or vision or strategy. But the real secret is simpler and harder: we learned how to fail without dying."

This wasn't false modesty—it was earned wisdom. Sony's journey from post-war startup to global entertainment colossus offers lessons that transcend industry boundaries, speaking to fundamental truths about innovation, adaptation, and corporate mortality.

Lesson 1: The Danger of Success

Sony's greatest failures came not during struggles but at peaks. The Walkman's dominance bred the arrogance that missed the iPod. PlayStation 2's success created the hubris that nearly killed PlayStation 3. The company's electronics supremacy in the 1980s fostered the silos that almost destroyed it in the 2000s.

Success creates antibodies to change. It validates existing strategies, calcifies organizational structures, and breeds contempt for emerging competitors. Sony learned this lesson repeatedly and expensively: the moment you believe you've won is the moment you start losing.

For founders, this means building organizations that remain paranoid even in triumph. For investors, it means being most skeptical when everyone agrees a company is invincible.

Lesson 2: Platform Transitions Are Existential

Every major platform transition represented life or death for Sony. They caught the transistor wave and rode it to glory. They missed the digital music transition and paid dearly. They accidentally created the gaming platform that saved them. Each transition wasn't just about technology—it was about reimagining the entire business model.

The lesson is brutal in its simplicity: missing one platform transition can erase decades of success (ask Kodak or Blackberry), while catching one can create decades of prosperity. The challenge is that platform transitions often look like toys or niche markets until suddenly they don't.

For entrepreneurs, this means taking seemingly small technological shifts seriously. For investors, it means watching not just current performance but positioning for the next platform.

Lesson 3: Patient Transformation vs. Radical Change

When Sony was dying in 2012, conventional wisdom demanded radical surgery—sell divisions, exit businesses, become a focused pure-play. Instead, Hirai chose patient transformation: keeping the company together while slowly breaking down silos, maintaining investment in R&D while cutting costs elsewhere, evolving the culture while respecting its core.

This Japanese approach—gradual, consensus-building, face-saving—seemed weak compared to American-style creative destruction. Yet it worked precisely because it preserved capabilities that would have been lost in radical restructuring. The sensor business that now generates billions was once a money-losing division that activist investors would have demanded be sold.

The lesson challenges Silicon Valley orthodoxy: sometimes patient evolution beats rapid revolution, especially in complex organizations with interdependent capabilities.

Lesson 4: Content and IP Appreciate; Hardware Depreciates