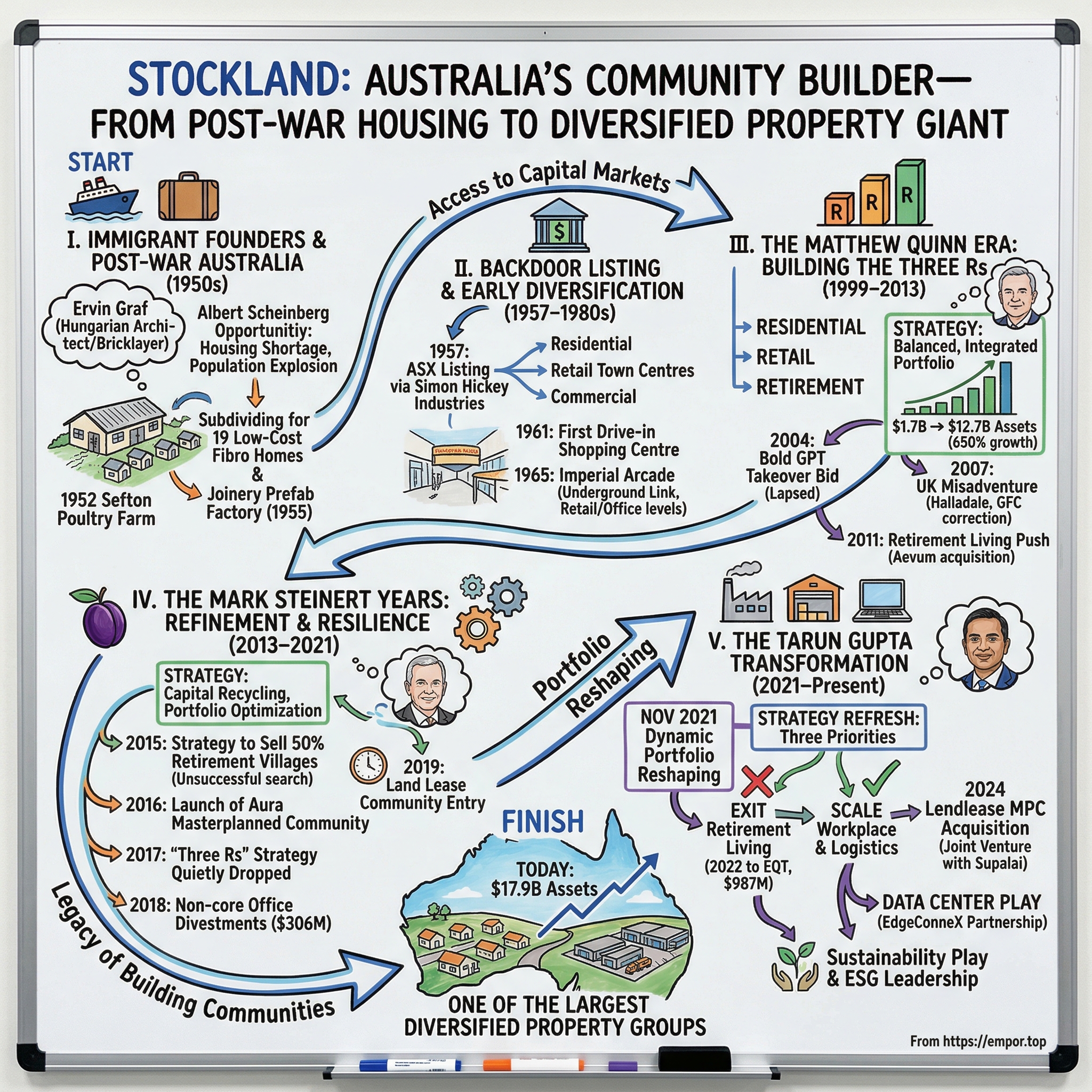

Stockland: Australia's Community Builder—From Post-War Housing to Diversified Property Giant

I. Introduction & Episode Roadmap

Picture Sydney in the early 1950s. The war is over, soldiers are returning home, and the greatest migration wave in Australian history is reshaping the nation. Ships arrive weekly at Circular Quay, disgorging thousands of European refugees—Italians, Greeks, Poles, Hungarians—each carrying little more than a suitcase and an outsized dream. Among them, a Hungarian immigrant named Ervin Graf steps onto Australian soil with a vision that would eventually reshape the suburban landscape of an entire continent.

What Graf saw in post-war Australia was not chaos but opportunity. A country desperately short of housing. A government incentivizing homeownership. A population explosion that demanded someone—anyone—to build shelter. And so in 1952, Graf partnered with fellow Hungarian Albert Scheinberg and Australian John Hammond to form Stocks & Holdings Ltd, a company that would begin by subdividing a poultry farm and grow into one of the largest property groups in the Southern Hemisphere. Today, Stockland stands as one of the largest diversified property groups in Australia with more than $17.9 billion of real estate assets. The company owns, funds, develops and manages one of Australia's largest portfolios of residential and land lease communities, retail town centres, and workplace and logistics assets. For more than 70 years, the company has built a proud legacy, helping more Australians achieve the dream of home ownership, and enabling the future of work and retail.

The central question that animates this story is deceptively simple: How did a company started by Hungarian immigrants subdividing a poultry farm become one of Australia's most important shapers of suburban life—and how is it now reinventing itself for the twenty-first century?

To answer that question, we need to traverse more than seven decades of Australian history: the post-war housing boom, the emergence of shopping center culture, the globalization of capital, the Global Financial Crisis, and now the digital transformation reshaping logistics, residential development, and even how Australians think about aging. We will meet three very different CEOs—Matthew Quinn, Mark Steinert, and Tarun Gupta—each of whom left an indelible mark on the company's strategy and culture.

This is a story about diversification and focus, about knowing when to expand and when to contract, about the peculiar challenges of building communities in a country where the suburbs sprawl endlessly but quality land is surprisingly scarce. It is also a story about capital efficiency, about how a property company transforms itself from a pure developer and owner into a platform that attracts billions in third-party capital.

Let us begin where all good Australian property stories begin: with immigrants, ambition, and a patch of dirt in Western Sydney.

II. The Immigrant Founders & Post-War Australia

The year is 1952. Sydney is a city transformed. The war is over, but its aftershocks ripple through every aspect of Australian life. Ships arrive constantly at Circular Quay and Fremantle, carrying waves of displaced Europeans—Greeks, Italians, Poles, Hungarians, Yugoslavians—fleeing the rubble of the Old World for the promise of the New. Australia's population, which had stood at just seven million in 1945, would nearly double over the following two decades. These new arrivals needed homes, and Australia had precious few to offer. Ervin Graf was a Hungarian architect who had been sent to a German labor camp during World War II. After the war, his initial application to enter Australia as an architect was rejected, and he successfully reapplied as a bricklayer, arriving in 1950. This detail matters more than it might first appear. Graf was not merely an immigrant; he was a survivor, a man who had seen civilization collapse and been forced to rebuild himself from nothing. When he looked at the housing shortage in Sydney, he saw not just a problem but an opportunity—the kind of opportunity that only someone who has lost everything can fully appreciate.

In 1952, Graf subdivided a poultry farm in Sefton and built 19 houses, doing much of the labor himself. Meeting the postwar demand for low-cost housing, Graf expanded his projects and, with partner Albert Scheinberg, formed the Stocks & Holdings development company in 1952, later to become Stockland.

Think about this for a moment: a Hungarian architect, rejected by Australian immigration authorities as a professional, enters the country as a bricklayer and within two years is subdividing land and building homes. The company's origins were rooted in addressing the acute post-World War II housing shortage in Australia, where rapid urbanization and population growth created strong demand for low-cost homes. The first project involved subdividing a poultry farm in Sefton, western Sydney, into blocks for 19 affordable fibro homes, marking Stockland's entry into project housing.

The fibro homes of the 1950s were modest structures—timber frames clad in asbestos cement sheeting, the material of choice for affordable housing in that era. They were not glamorous, but they were homes, and for the millions of new Australians arriving on those ships, they represented something precious: a stake in the New World, a place to raise children, a foundation for the future.

By 1955, the company had established an off-site prefabrication factory for joinery to streamline construction efficiency amid the housing boom. This early move toward prefabrication demonstrated the pragmatic, efficiency-focused mindset that would characterize Stockland for decades to come. Rather than simply scaling up traditional construction methods, Graf and Scheinberg looked for ways to industrialize the process, to turn homebuilding from a craft into a system.

The founders had a vision to "not merely achieve growth and profits but to make a worthwhile contribution to the development of our cities and great country." This statement, preserved in company archives, captures something essential about the immigrant entrepreneur mindset. For Graf and Scheinberg, business success and national contribution were not separate goals but two aspects of the same endeavor. They were building homes, yes, but they were also building Australia—and in doing so, earning their place in their adopted country.

Graf pioneered a number of Australian innovations, including medium-density housing; Australia's first drive-in shopping centre, in 1961; and Sydney's first underground pedestrian link, in the Imperial Arcade. The innovations that Graf brought to Australian property development reflected his European training and his willingness to import ideas from overseas. Medium-density housing, commonplace in European cities, was a novelty in the sprawling Australian suburbs. The drive-in shopping center, already transforming American retail, had not yet crossed the Pacific. Graf saw opportunities that native-born Australians, accustomed to doing things a certain way, might have missed.

The immigrant founder story is a familiar one in business history—think of Andrew Carnegie, Sergey Brin, or Elon Musk. What makes Graf and Scheinberg's story particularly relevant is how it shaped Stockland's corporate DNA. The company that emerged from a poultry farm in Sefton was pragmatic rather than ideological, opportunistic rather than strategic, focused on execution rather than vision statements. These qualities would serve it well in the volatile world of Australian property development, where cycles of boom and bust reward the nimble and punish the rigid.

The post-war Australian context also matters enormously. The government of Robert Menzies was actively promoting homeownership as the cornerstone of Australian society. Immigration policies favored Europeans who could be assimilated into the Anglo-Australian mainstream. Banks were regulated but stable, providing reliable mortgage finance. And most importantly, land on the urban fringe was cheap and plentiful—or so it seemed. In reality, the land that was easy to develop had limited supply, and those who moved early to acquire and subdivide it would enjoy advantages that compounded over decades.

As the 1950s drew to a close, Stocks & Holdings had established itself as a credible player in Sydney's residential development market. But Graf and Scheinberg had larger ambitions. They wanted access to the capital markets, the ability to raise funds from outside investors, and the credibility that came with being a publicly listed company. The question was how to achieve that listing—and the answer, as we shall see, would come through one of the classic maneuvers of mid-century corporate finance.

III. The Backdoor Listing & Early Diversification (1957–1980s)

In the corporate finance playbook of 1950s Australia, there existed a maneuver so common it had become almost routine: the reverse takeover. For a private company seeking a public listing, the traditional path—filing a prospectus, engaging underwriters, enduring months of regulatory scrutiny—was time-consuming and expensive. The faster route was to find a company already listed on the exchange, preferably one that was small, struggling, or simply looking for new direction, and acquire it. The private company would absorb the public shell, the founders would gain a listing, and the shareholders of the acquired company would gain exposure to a more dynamic enterprise.

In 1957 Stockland listed on the Australian Securities Exchange by acquiring a controlling interest in Simon Hickey Industries Ltd, the smallest company then listed. There is something almost poetic about this detail. Graf and Scheinberg, the immigrant outsiders who had entered Australia through the back door of the immigration system, now entered the capital markets through another back door—acquiring the smallest, most marginal company available.

The choice of Simon Hickey Industries was deliberate. A small company meant a manageable acquisition cost and less resistance from existing shareholders. But it also meant that Stockland was not inheriting any meaningful operating business, just the listing itself. From day one on the exchange, Stockland's value would derive entirely from what Graf and Scheinberg could build.

In the same year, Stockland's activities became more diversified, moving into commercial development, initially with retail projects in suburbs of Sydney. The timing is significant. Having secured access to public capital markets, Stockland immediately began expanding beyond its residential roots. The logic was straightforward: residential development was inherently cyclical, tied to interest rates, immigration flows, and consumer confidence. Commercial development—particularly retail—offered more stable income streams and the opportunity to build long-term asset value.

The suburban retail projects of the late 1950s and early 1960s were modest by today's standards: strips of shops serving newly developed residential areas, small supermarkets and pharmacies and banks. But they represented Stockland's first steps into a sector that would eventually dominate its portfolio for decades.

In 1965 Stockland opened its first big commercial development—the redeveloped Imperial Arcade, Sydney in Sydney's CBD, which offered the first underground link to David Jones, four retail levels and six levels of office space. This was a leap of ambition. From suburban strips to a major CBD development, from ground-floor retail to a multi-level complex integrating shopping and office space, Stockland was demonstrating that it could compete at the top tier of Australian property development.

The underground link to David Jones deserves particular attention. David Jones was (and remains) one of Australia's most prestigious department store chains, the kind of anchor tenant that could make or break a retail development. Creating a direct pedestrian connection between Imperial Arcade and the David Jones flagship store meant that Stockland had negotiated a significant commercial relationship with one of the country's most powerful retailers. It also meant that the arcade would capture foot traffic from one of Sydney's busiest retail destinations.

The strategic logic of diversification was both defensive and offensive. On the defensive side, a company with residential, retail, and commercial exposure could weather downturns in any single sector more easily than a pure-play residential developer. When housing markets softened, retail rents might remain stable. When office markets cooled, residential demand might surge. The portfolio effect provided a cushion against volatility.

On the offensive side, diversification allowed Stockland to pursue opportunities wherever they emerged. A company known only for housing might be overlooked for commercial deals; a diversified property group could be a credible bidder for any type of asset. The relationships built in one sector—with councils, with financiers, with construction firms—could be leveraged in others.

The decades from the late 1960s through the 1980s were a turbulent period for Australian property. The resources boom of the early 1970s fueled speculative development across the country. The global oil crisis and subsequent recession of 1974-75 triggered a brutal correction. The recovery of the late 1970s gave way to the excesses of the 1980s, culminating in the crash of 1987 and the recession of the early 1990s.

Through these cycles, Stockland survived and grew. The company's conservative financial management—a legacy, perhaps, of founders who had experienced real catastrophe—kept it from the overleveraged positions that destroyed many competitors. The diversified portfolio provided income stability even when development profits evaporated. And the patient accumulation of land, year after year, decade after decade, created optionality for future development that would prove enormously valuable.

By the late 1990s, Stockland had built a substantial enterprise, but it was not yet the property giant it would become. That transformation required a new kind of leader—someone who could articulate a strategic vision, pursue transformational acquisitions, and navigate the opportunities and risks of an increasingly globalized capital market. In 1999, Stockland found that leader in an unlikely candidate: a British accountant named Matthew Quinn.

IV. The Matthew Quinn Era: Building the Three Rs (1999–2013)

Matthew Quinn arrived at Stockland in 1999 as only the company's third managing director in nearly 50 years of operation. The stability of leadership was remarkable—Australian property companies of that era typically churned through executives with the regularity of political administrations—but it also reflected a certain conservatism, a reluctance to disrupt what was working. Quinn was a Briton by origin, beginning his career in the United Kingdom and moving to Australia in 1987 with PriceWaterhouse. A year later, he joined Western Australian property group, the Rockingham Park Group before joining Stockland in 1999. In 2000, he was appointed to managing director.

What Quinn found when he arrived was a respectable but unremarkable property company—diversified, certainly, but lacking a clear strategic identity. Under Quinn's helm, the company grew from $1.7 billion in assets in 2000 to $12.7 billion—a roughly 650% increase over just over a decade. The question is: how did he do it?

The answer lay in what became known as the "Three Rs" strategy. Quinn spearheaded Stockland's "three Rs" strategy—a focus on the retail, retirement and residential sectors. This framework—Retail, Retirement, and Residential—became the company's defining identity for over a decade. Each "R" represented a distinct asset class with its own risk profile and return characteristics, but together they formed an integrated portfolio designed to weather any storm.

Retail provided stable, recurring income from long-term tenant leases. Residential offered development profits and exposure to Australia's insatiable demand for new housing. Retirement—the most innovative element of Quinn's strategy—positioned Stockland to capture the demographic wave of aging Baby Boomers seeking lifestyle-oriented village living.

The Bold GPT Takeover Bid

Five years into his tenure, Quinn made what would prove to be the most audacious move of his career. In late 2004, he launched a takeover bid for General Property Trust (GPT), a major Australian real estate investment trust that had been Lend Lease's "mini-me"—a smaller version of the larger property group that had spun it off.

Lend Lease said it did not intend to improve its bid for GPT, which was subject to a takeover offer from Stockland, another Australian developer. Greg Clarke, Lend Lease's chief executive and managing director, admitted that the failure of the merger was a blow.

A Stockland-GPT merger would have created an approximately $15 billion entity in 2005—a true Australian property giant with dominant positions across multiple sectors. The market price of GPT units rose approximately 15% following the announcement. The meeting of GPT unitholders held on 17 November to approve the Lend Lease Proposal failed to achieve the required 75% of units present and voting to enable the merger to proceed and the proposal lapsed.

The failure of the GPT bid remains one of the great "what ifs" of Australian corporate history. Had Stockland succeeded, it would have emerged as the dominant force in Australian property, with a portfolio rivaling the largest global REITs. Instead, the bid fizzled, and Stockland was forced to pursue growth through other means.

The UK Misadventure

Perhaps emboldened by the near-success of the GPT bid, perhaps seeking growth opportunities that the Australian market could not provide, Quinn made another bold move in 2007. In 2007 Quinn steered the group's entry into the UK with a £170 million ($A430 million) takeover of Halladale Group plc.

The timing could not have been worse. The Global Financial Crisis, which would erupt in full force in 2008, was already brewing in the overheated UK property market. However two years later, Stockland announced it would progressively wind-down in the UK after the business posted an operating loss of $0.7 million and wrote down $186 million.

The Halladale disaster offers a cautionary tale about geographic expansion. Property development is, at its core, a local business. Success depends on understanding local markets, maintaining relationships with local councils and contractors, and reading the subtle signals of local demand. A company that excels in Sydney's western suburbs may founder in London's commuter belt, not because of any lack of capability, but because the tacit knowledge that drives success simply does not transfer.

Building the Retirement Living Business

If the UK venture represented Quinn's greatest failure, the build-out of the retirement living business represented his most far-sighted achievement. In the same year, Stockland made strategic investments in FKP and Aevum and in 2011, followed up with a $266 million takeover of retirement village company Aevum, which doubled the size of Stockland's retirement business.

The logic behind the retirement push was demographically compelling. Australia's Baby Boom generation—born between 1946 and 1964—was entering its sixties and seventies, a phase of life when many people seek to downsize from the family home, simplify their lives, and relocate to purpose-built communities offering social connection and access to care services. Stockland aimed to capture this wave by building a national network of retirement villages offering lifestyle-oriented living.

Under the strategy of "Residential, Retail and Retirement," Stockland became one of the nation's largest retirement village operators. The Aevum acquisition alone added dozens of villages to the portfolio, creating a platform that could be scaled further through development and additional acquisitions.

Quinn's legacy is complex. He built enormous scale and established a coherent strategic framework that would guide the company for more than a decade. He transformed Stockland from a mid-tier property company into a genuine industry leader. But he also left unresolved questions about portfolio complexity, capital efficiency, and whether the "Three Rs" framework would remain relevant in a changing market. When he announced his retirement in 2012, following a "family board meeting" as he described it, the company was positioned for success—but the strategic choices ahead would fall to his successor.

V. The Mark Steinert Years: Refinement & Resilience (2013–2021)

Mark Steinert inherited a company at an inflection point. The Global Financial Crisis had revealed the vulnerabilities of overleveraged property companies and reminded investors that real estate, for all its apparent solidity, could be just as volatile as any financial asset. The "Three Rs" strategy had served Stockland well, but the world had changed, and questions were emerging about whether the framework remained fit for purpose. Steinert had deep experience in property and financial services including eight years in direct property primarily with Jones Lang LaSalle and 10 years in listed real estate with UBS where he held numerous senior roles including Head of Australasian Equities, Global Head of Research and Global Head of Product Development and Management for Global Asset Management. His background was analytical and financial rather than developmental—a signal that Stockland was entering an era of portfolio optimization rather than empire building.

Where Quinn had been an acquisitive builder of scale, Steinert was a refiner, a pruner, a capital allocator. He inherited a sprawling portfolio that included world-class assets alongside mediocre ones, high-return development opportunities alongside capital-intensive businesses struggling to achieve acceptable returns. His task was to separate the wheat from the chaff.

The Retirement Living business exemplified both the opportunity and the challenge. During this period, the business grew to more than 9,500 homes and apartments across 69 villages in five states, with a value in excess of $1.1 billion. The scale was impressive, but the returns were not. When Steinert joined in January 2013, the return on assets was just 4%. The successor CEO of the retirement division had the objective of building the return to 8% by 2018. But then the ABC's Four Corners program ran a critical exposé of the retirement village industry in June 2017, and return on assets for Stockland Retirement was knocked back to 4%—and has stayed there.

The Four Corners episode was a watershed moment for the entire Australian retirement village industry. The program highlighted confusing fee structures, concerns about residents' rights, and allegations of poor treatment. Consumer sentiment toward retirement villages soured, sales slowed, and the industry's reputation suffered damage that would take years to repair.

Steinert's response was characteristically pragmatic. The sale of non-core assets aligned with an active capital recycling strategy, focusing on reshaping the portfolio and looking at opportunities to reinvest across the broader business. The company began selling underperforming villages—those in poor locations, with aging infrastructure, or limited development potential—and reinvesting the proceeds into higher-returning assets.

In October 2015 Stockland announced a strategy to investigate selling 50% of the villages for $1 billion and gave themselves six months to find a partner. The search proved unsuccessful—potential investors balked at the age of the portfolio, with a majority of villages over 25 years old and requiring significant capital investment.

A significant achievement of the Steinert era was the 2016 launch of the Aura masterplanned community in Queensland, one of Australia's largest masterplanned communities emphasizing eco-friendly design and long-term environmental stewardship. Aura represented the kind of large-scale, long-duration project that Stockland did best—communities designed from scratch with schools, parks, town centers, and thousands of homes, built out over decades rather than years.

Divestments accelerated in 2018 with the sale of commercial office assets totaling $306 million, part of a broader strategy to exit non-core holdings. The sales reflected a strategic judgment that office assets, particularly those outside prime CBD locations, offered inferior returns compared to residential development and essential retail.

Perhaps the most symbolically significant change came in 2017, when the "Three Rs" strategy was quietly dropped. The framework that had defined Stockland for more than a decade was retired without fanfare, a tacit acknowledgment that the world had changed and the company needed to change with it. Retail was under pressure from e-commerce. Retirement was struggling with both reputational damage and structural challenges. Only Residential remained unambiguously strong.

In February 2019 Steinert announced that Stockland would enter the land lease community market, with three sites across Townsville and the Sunshine Coast. He said at the time that Stockland was "finding it hard to compete" against land lease communities with the retirement village product. This admission was remarkable for its candor. The CEO of one of Australia's largest retirement village operators was acknowledging that a competing model—one offering simpler fee structures and clearer value propositions—was winning in the marketplace.

When Steinert announced his intention to retire in June 2020, after seven and a half years in the role, he left behind a company that was leaner, more focused, and better positioned for transformation. As Chief Executive Officer and Managing Director, Steinert oversaw the development of Australia's leading residential business, reshaped and expanded the workplace and logistics portfolio, and significantly repositioned the town centre business.

But the biggest decisions—what to do with Retirement Living, how aggressively to pursue logistics, whether to transform Stockland from a traditional developer-owner into a capital-light platform company—would fall to his successor. The stage was set for the most dramatic strategic transformation in Stockland's history.

VI. The Tarun Gupta Transformation (2021–Present)

In June 2021, Tarun Gupta stepped into the CEO role at Stockland, bringing with him a biography that embodied Australia's transformation over the preceding decades. He came to Australia as an international student 29 years ago. Today, Gupta heads one of the largest real estate development companies in Australia and is the first Indian-origin CEO of Stockland. Growing up in India, he lived at different places in Uttar Pradesh as his father was employed in a transferrable government job. Gupta studied at St Joseph College, a boarding school in Nainital, then later at DPS Mathura Road School in New Delhi. After graduating from Delhi's Sri Venkateswara College, he came to Australia for study abroad.

The early years were not glamorous. Gupta's early working life included a stint as a chef in an Indian restaurant in Newcastle—the kind of immigrant hustle familiar to generations of newcomers building their credentials in a new country. He worked his way through an MBA at the University of Newcastle, then into property, joining Lend Lease in the early 1990s.

Gupta held a wide range of senior roles during his 26 years at Lendlease including most recently as the Group Chief Financial Officer. Earlier in his career, he held the position of Chief Executive Officer, Property (Australia). The breadth of this experience—spanning development, investment management, and finance—gave him a perspective that few property executives could match.

The November 2021 Strategy Refresh—A Defining Moment

Just five months after taking the helm, Gupta unveiled what would prove to be the most comprehensive strategic reset in Stockland's modern history. Managing Director and CEO Tarun Gupta stated: "Our strategy is designed to build on Stockland's strong platform and to capitalise on structural long term trends including urbanisation and urban renewal; growth in institutional capital; digital acceleration and the continued momentum in ESG."

The strategy articulated three key priorities, the most important of which was to dynamically reshape the portfolio. Stockland would reduce its exposure to Retail and Retirement Living and scale Workplace and Logistics.

The indicative five-year targets were stark: Grow Residential, Workplace & Logistics from 50% to over 70% of the portfolio. Down-weight Retail and Retirement Living from 50% to less than 30% of the portfolio.

This was not incremental change. This was a fundamental reimagining of what Stockland would become. For more than a decade, Stockland had defined itself through the "Three Rs." Under Gupta, one of those Rs—Retirement—would be eliminated entirely, while another—Retail—would be dramatically reduced. In their place would rise Logistics and Workplace, sectors underpinned by e-commerce growth and the evolving nature of work.

Exit from Retirement Living—End of an EraIn February 2022, Stockland entered into a sale agreement with EQT Infrastructure to divest its Retirement Living business for $987 million. Under the terms of the agreement, EQT would acquire Stockland's portfolio of 58 established Retirement Living villages, 10 development projects underway and in planning, along with the associated management platform. As a result of the transaction, over 300 employees transferred to EQT with the business.

The transaction valued the retirement business at roughly 1.9% below book value—not the premium that might have been hoped for, but a clean exit from a sector that had consumed management attention and capital without delivering acceptable returns. The disposal delivered on Stockland's strategy to release capital for redeployment into higher growth opportunities and refocus the Communities business.

But Stockland was not abandoning the over-55 demographic entirely. Instead, it was pivoting to a different model. Stockland had been looking to move away from retirement villages in favour of land lease communities. The company completed its $620 million acquisition of Halcyon Group, a specialist land lease operator, and announced a long-term partnership with Japanese giant Mitsubishi Estate Asia to develop and own land lease communities.

The land lease model is an alternative housing option for many older Australians looking to downsize from their current family home. It gives homeowners the opportunity to free up capital with no hidden costs, stamp duty or deferred management fees, and retain all capital gains.

The difference between land lease and traditional retirement villages is crucial to understanding Stockland's pivot. In a retirement village, residents typically pay an entry price and a deferred management fee—a percentage of the sale price that is deducted when they leave, which can run to 30-40% after extended residency. The village operator also typically captures any capital gains. In land lease, residents own their home outright and pay a ground rent to the landowner. No deferred fees, no capital gains surrender, and a simpler, more transparent value proposition.

The Logistics Pivot and Development PipelineThe logistics pivot represented perhaps the most consequential strategic shift. Stockland's national $6.5 billion logistics development pipeline of modern, flexible, and future-proofed facilities has become essential to driving the economies of cities and suburbs.

CEO Commercial Property Louise Mason captured the ambition: "We have been focused on building the scale and quality of our Logistics portfolio in recent years. We are now entering a period of accelerated delivery of our extensive development pipeline. We expect to undertake an average of approximately $400 million of Logistics development per annum over the next five years—more than double the average approximately $150 million per annum in the five years to 30 June 2021."

Masterplanning undertaken on the existing landbank resulted in a doubling of the Logistics development pipeline to approximately $6.4 billion. Stockland has launched its first flagship multi-storey logistics facility—Stockland Momenta, a 15,000 square metre two-storey warehouse development in south Sydney. The circa $3.7 billion logistics portfolio delivered an FFO of $168 million over FY24, up 20.8% on FY23, with an occupancy rate by income of 98.2%.

The e-commerce tailwind and supply chain reshoring trends driving logistics demand show no sign of abating. Australia's increasing e-commerce penetration is driving the need for more freight, warehousing and manufacturing space, with the per person space requirement on the eastern seaboard expected to continue growing.

VII. The 2024 Lendlease Acquisition—Doubling Down on ResidentialIn November 2024, Stockland and Supalai Australia Holdings Pty Ltd. completed the acquisition of 12 Masterplanned Communities (MPC) from Lendlease Group for approximately AUD 1 billion. The acquisition comprised approximately 27,600 lots to build homes as well as schools, hospitals and shopping centres, achieving immediate scale for the partnership.

Sixty per cent of the projects are in Queensland, 21 per cent are in Victoria, 15 per cent in NSW and 4 per cent in WA. The communities were acquired by the Stockland Residential Communities Partnership (SRCP), which is 50.1 per cent owned by Stockland with 49.9 per cent held by Supalai.

The ACCC chose not to oppose the acquisition after accepting a court-enforceable undertaking. The undertaking required Stockland to divest the Forest Reach masterplanned community project in the Illawarra region of New South Wales. ACCC Commissioner Dr Philip Williams stated: "Without the divestment, the proposed acquisition would bring together the two largest masterplanned community projects in the already concentrated Illawarra market. This could have resulted in increased prices, delayed supply, or reduced quality of housing lots in the Illawarra region, to the detriment of prospective homeowners."

If the deal got the relevant approvals, it would take Stockland's landbank to approximately 95,600 lots, representing a potential increase in settlement volumes of around 2,500 lots annually.

The deal positions Stockland at the heart of Australia's housing crisis solution. Australia's housing undersupply is exacerbated by ongoing constrained land supply amid a rapid population boost driven by net overseas migration. As the nation grapples with housing affordability and availability, companies with the land banks and development capability to bring new supply to market quickly hold a strategic position that transcends normal business considerations.

The joint venture structure with Supalai is noteworthy. The Thai group has been in a strategic partnership with its Australian counterpart since mid-2020 when it committed $52.5 million for half ownership of master-planned community Katalia in Melbourne's north. This capital partnerships model—bringing in third-party capital to fund growth while retaining management and development capabilities—represents a fundamental evolution in how Stockland approaches its business.

VIII. The Data Center Play—Looking to the FuturePerhaps the most forward-looking element of Stockland's transformation is its entry into data center development. Stockland CEO Tarun Gupta announced "an exclusive arrangement to partner with EdgeConneX, a leading global data center provider backed by EQT Infrastructure, to develop, own, and operate a portfolio of Australian data centers." He stated: "Subject to documentation and approvals, this collaboration marks a significant step forward with a high-quality operator in hyperscale infrastructure."

The 50:50 joint venture will combine "Stockland's land, development and project management expertise with EdgeConneX's technical capabilities and hyperscaler relationships." Stockland added that it has secured power and zoning for a 100MW+ data center development at MPark Stage 2, in New South Wales. Construction commencement is anticipated in FY 2027.

Located in the Macquarie Park Innovation District, M_Park is a $2 billion mixed-use precinct—the company has previously developed a data center in an earlier phase of the park. Stockland noted further pipeline opportunities targeted across its landholdings, and has identified "several sites" across Sydney and Melbourne.

The data center play represents a natural evolution for a company with substantial logistics landholdings. Data centers share many characteristics with logistics facilities: they require large footprints, excellent power infrastructure, and strategic locations. Stockland's existing land bank and development expertise can be leveraged for data center development without radical transformation of capabilities.

Moreover, the partnership structure with EdgeConneX allows Stockland to enter the sector without having to build technical expertise in data center operations—arguably the most challenging aspect of the business. EdgeConneX brings hyperscaler relationships and operational know-how; Stockland brings land, development capability, and local market knowledge.

The capital partnerships model extends across the entire business. Stockland has raised $2.9 billion of third-party equity to fund growth since announcing its refresh strategy in November 2021. The company continues to engage with high-quality institutional investors on new opportunities across its platform.

This evolution from pure developer/owner to platform and fee generator represents a fundamental shift in the Stockland business model. Rather than deploying its own capital for every project, Stockland increasingly acts as a manager and developer, earning fees for its expertise while sharing the capital burden with partners.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube