Scentre Group: Australia's Temple of Retail and the Westfield Legacy

I. Introduction: The Most Recognizable Name in Australian Retail

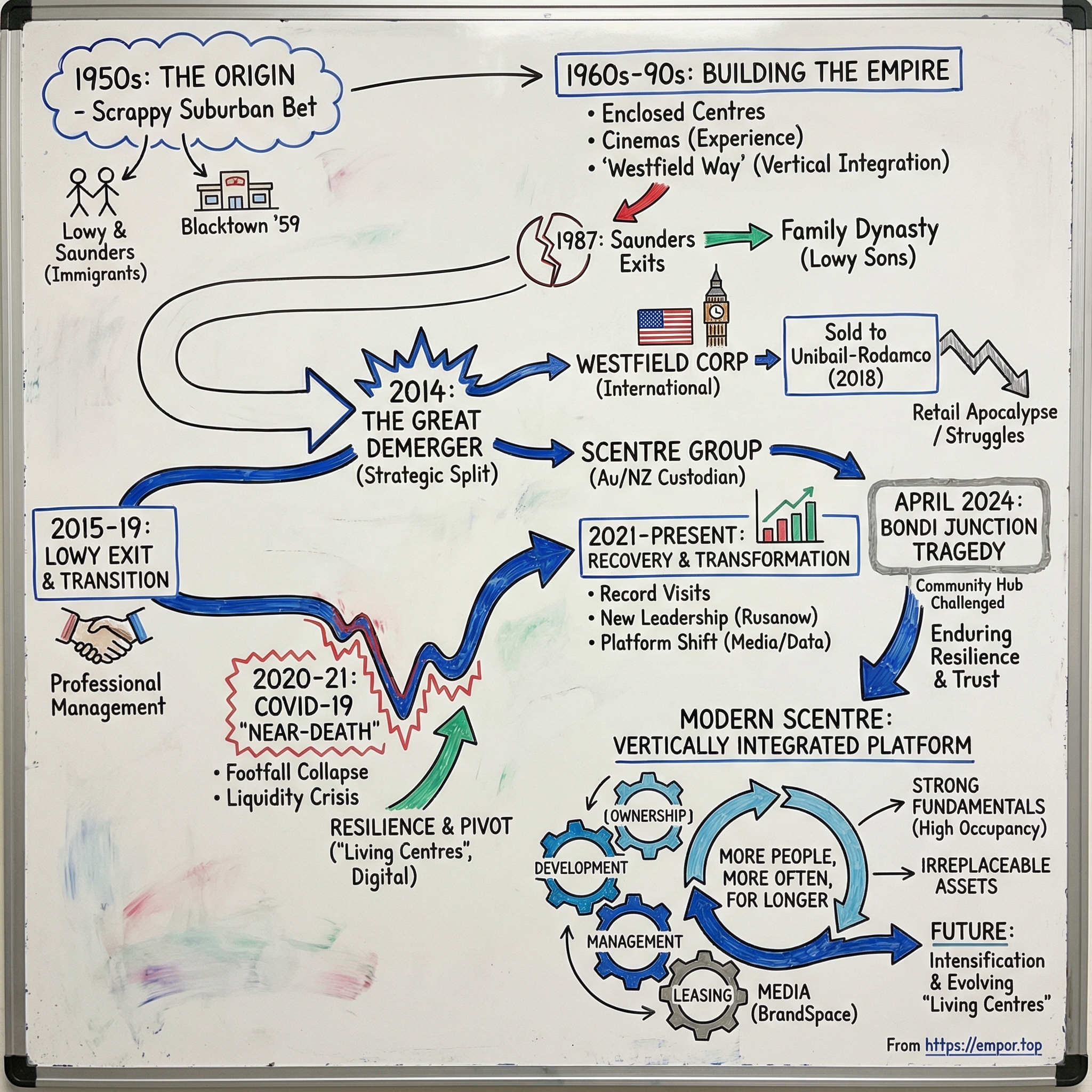

A Holocaust survivor arrives in Sydney in 1952 with little more than grit, ambition, and a past he can’t outrun. Six decades later, the name he helped build sits above the entrances to places that feel less like “malls” and more like modern town squares—destinations that draw hundreds of millions of visits a year across Australia and New Zealand. This isn’t just a business story. It’s an immigration epic, a suburban revolution, and a blueprint for turning real estate into one of the most powerful consumer brands in the Southern Hemisphere.

Today, Scentre Group owns and operates 42 Westfield destinations across Australia and New Zealand. In 2024, they welcomed 526 million customer visits—14 million more than the year before. The company’s ownership interests across the portfolio sit at roughly $35 billion, putting Scentre among the world’s heavyweight retail property owners.

But the origin story is the part that still sounds like fiction. Frank Lowy left Israel in 1952 and joined his family in Australia, where they were running a small goods delivery business. A year later, he met another immigrant, John Saunders. Two outsiders, in a fast-growing post-war country, saw the same thing: suburbs spreading outward, families piling into cars, and a looming need for a new kind of community centre. Their partnership would eventually become Westfield Development Corporation—starting with a shopping centre at Blacktown in Sydney’s west.

That’s the question at the heart of Scentre Group: how did two refugees in 1950s Sydney create what became the world’s most recognizable shopping centre brand—and what happens when that empire gets split in two?

That split came in 2014, when the original Westfield Group separated its Australia and New Zealand business from its international assets. The demerger created Scentre Group as the custodian of Westfield here at home, while the global expansion story continued elsewhere. It was one of the biggest restructures in Australian corporate history, and in hindsight, it shaped everything that followed.

Because by late 2025, Scentre isn’t just “still standing.” It’s a company that has endured COVID-era collapse in foot traffic, lived through the relentless drumbeat of e-commerce disruption, and faced an unthinkable tragedy at Westfield Bondi Junction in 2024—yet still emerged with record-high occupancy and steadily rising visits.

Along the way, we’ll trace a few big themes: immigration and entrepreneurship as founding mythology; the shopping centre as essential social infrastructure; the shift from landlord to platform; and what the so-called retail apocalypse gets wrong—at least when you’re operating at the very top end of physical retail. And we’ll hit the inflection points that define the modern era: the 2014 demerger, the Lowy family’s eventual exit, the pandemic near-death experience, and the moment Bondi Junction forced a painful question onto the entire idea of a “community gathering place.”

II. The Founders' Story: From Ghetto to Westfield

In 1952, Frank Lowy arrived in Sydney as a 22-year-old with the kind of life experience that makes “starting over” sound almost absurd. He’d been born on 22 October 1930 in Fil'akovo, in what is now Slovakia. During World War II, he lived through Nazi-occupied Europe, spending the war years in Budapest until Germany’s defeat in 1945. His father was killed at Auschwitz—beaten to death by Nazis.

Those facts aren’t just background. They explain the engine. Decades later, in 2013, Lowy funded the restoration of a railway wagon used to transport Jews to Auschwitz and oversaw its installation at the former camp, in memory of his father. It was a public act of remembrance for something that never left him.

After the war, Lowy left Europe for Israel in 1946. There, he didn’t drift into a quiet life. He joined the Haganah, then served in the Golani Brigade, and fought in the 1948 Arab–Israeli War in the Galilee and Gaza. By the time he stepped onto Australian soil, he’d learned two skills that would define his business career: how to endure, and how to move forward without waiting for permission.

Sydney in the early 1950s was changing fast. The post-war boom was pushing families out of the inner city and into new suburbs—Blacktown, Penrith, Liverpool—places built for cars, kids, and backyards. What those suburbs didn’t have was the infrastructure of daily life. If you wanted to shop like a city resident, you often had to travel like one too.

Lowy joined his family’s smallgoods delivery business. And then, in 1953, he met another immigrant: John Saunders. Like Lowy, Saunders had that outsider’s posture—nothing guaranteed, nothing to protect, everything to build.

They started small, and they financed like people who didn’t have a wealthy backer waiting in the wings. They borrowed from a local bank manager, used profits from the deli and a coffee shop they owned, and bought farmland. The idea was simple and audacious: turn cheap land on the city’s edge into a concentrated retail destination for the new suburban Australia.

They called their company Westfield Investments. The name was literal—“west” for where they were building, and “field” for what the land had been before they arrived. But it also carried something else: a sense that the future of Australia wasn’t in the CBD. It was out there, where the people were moving.

In July 1959, they opened their first centre in Blacktown: Westfield Place. It was modest by today’s standards, but it was the template. It marked the start of what would become Australia’s modern shopping centre era—and the beginning of Westfield as a brand that would eventually stretch far beyond Sydney.

In hindsight, what Lowy and Saunders saw is almost obvious. Suburban expansion creates retail deserts, and retail deserts create opportunity. But at the time, many established retailers were still thinking in terms of city streets and downtown flagships. Lowy and Saunders were betting on the everyday patterns of suburban life—and on the idea that a shopping centre could become more than a cluster of stores. It could be the place people naturally gathered.

Their partnership was the spark: two immigrants with complementary strengths and a shared willingness to take the bet. They would work together for nearly three decades before Saunders sold his interests and departed, but by then the machine was already built.

And the story quickly became a family story, too. Lowy married Shirley Rusanow in 1954, after meeting her at a Jewish dance. They had three sons—Peter and Steven, who would go on to manage the Westfield business, and David, who would later manage the family’s private investments. Over time, “Westfield” wouldn’t just be a company name. It would be a dynasty—one that shaped Australian retail for more than half a century.

III. Building the Australian Retail Empire (1960–1990)

The 1960s were when Westfield stopped looking like a clever suburban property play and started looking like a real institution. In 1960, the company listed on the Sydney Stock Exchange as Westfield Development Corporation Ltd, selling 300,000 shares at five shillings each to raise the capital it needed to move faster. It wasn’t just a financial milestone. It was permission to scale.

Scale came quickly. Westfield built another five centres across New South Wales, then pushed into Victoria and Queensland in 1966 and 1967. The pattern was simple: follow the suburbs, follow the people, and plant a centre where daily life was about to happen.

But Westfield’s advantage wasn’t just how many sites it could open. It was how tightly it controlled the whole machine. While other developers might build a centre and then hand it off, Frank Lowy wanted end-to-end ownership of the experience. Westfield would design the buildings, construct them, manage the properties, and lease the stores. That vertical integration forced the company to understand retail in granular detail: how people flowed through a space, where they slowed down, what made a visit feel effortless, and what made it worth repeating.

The redevelopments of the next few decades showed how seriously Westfield took that craft. Miranda Fair, for example, was officially opened on 16 March 1964 by NSW Premier Bob Heffron in front of 1,600 guests, with a helicopter even arriving to deliver newspapers. Developed by Myer and Farmers, it was the largest fully enclosed shopping centre in New South Wales at the time. Westfield also executed major redevelopments at Doncaster in Melbourne, and at Liverpool and Miranda in Sydney. When Miranda’s expansion was completed, it became Australia’s largest shopping centre—and the first to break the 300-store mark. That wasn’t just bigger for the sake of it. It was a statement about what a shopping centre could be: not a strip of errands, but a destination.

By the late 1980s, Westfield was building centres that reshaped entire districts. In 1987, two major Sydney destinations opened: Chatswood and Eastgardens. Eastgardens carried a small but telling innovation that would become a big industry idea later on: it featured Australia’s first cinema inside a shopping centre. Retail plus entertainment in one place wasn’t a gimmick. It was an early version of what would eventually be called “experiential retail,” decades before that phrase became common.

Then came a turning point inside the company itself. In 1987, John Saunders sold his interests and left. The partnership that began in 1953 had lasted nearly 35 years—an unusually long run for any business relationship, especially one built by two strong-willed immigrants taking big risks. Saunders’ exit closed the founding chapter. But it also cleared the runway for the next era.

With his original partner gone, Frank Lowy expanded the business beyond Australia, first into New Zealand and then the UK. At the same time, Westfield became even more of a family enterprise. Lowy’s sons, Steven and Peter, joined the business and learned the work from the inside out. Over time, they would become joint chief executives of the Westfield Group, anchoring the idea that Westfield wasn’t just a developer—it was a dynasty.

By the end of the 1980s, Westfield had essentially codified the “Westfield way”: disciplined site selection focused on where population density and growth were headed; design that made centres bright, navigable, and easy to move through; locking in major anchor tenants early; constant reinvestment so older assets didn’t get leapfrogged; and careful tenant mix management to balance fashion, food, services, and entertainment.

The result was a set of advantages that were hard to copy. Competitors could build a centre. What was far tougher to replicate was the system Westfield had built—decades of institutional knowledge about how to create places people would choose to return to, again and again.

IV. Global Expansion and the American Dream (1977–2014)

By the late 1970s, Westfield had basically solved Australia. The question Frank Lowy couldn’t ignore was what every ambitious builder eventually asks: if this model works here, does it work in the biggest retail market in the world?

In 1977, Westfield took its first real step into the United States with the purchase of Trumbull Shopping Park in Connecticut—a deal that reportedly cost $21 million. It was a long way from Blacktown, and that was the point. This wasn’t a side quest. It was the start of a second act.

From there, the company began adding centres in waves—first in 1980 with acquisitions in California, Michigan, and Connecticut, then again in 1986 with centres in California, New Jersey, and Long Island, New York. Westfield’s approach in the US was rarely about scattering pins across a map. It liked clusters: build density in a handful of markets, learn the customer, learn the retailers, then expand outward. Over time, it built considerable holdings on the East Coast and in California before pushing into the Midwest. By 2005, Westfield owned centres in 15 US states.

The moment that really proved the strategy, though, came in 1994. Westfield partnered with General Growth and Whitehall Real Estate to buy 19 centres in a US$1 billion transaction. With that single move, Westfield effectively tripled the amount of space it managed in the United States. The portfolio included major assets like Topanga and Plaza Bonita in California and Annapolis in Maryland.

This was the “Westfield way” applied at scale: buy assets that weren’t living up to their potential, reinvest heavily, upgrade the experience, reshape the tenant mix, and use better design and management to lift rents and sales. It was aggressive, capital-intensive, and it worked—at least long enough to turn Westfield into a truly multinational operator.

By the mid-2000s and into the next decade, the footprint was enormous: investment interests in 103 shopping centres spread across Australia, the United States, and a long list of markets in Europe and beyond—the Netherlands, the United Kingdom, New Zealand, Italy, France, Sweden, Austria, Germany, Spain, Croatia, Poland, the Czech Republic, and Brazil. In total, that meant roughly 23,000 retail outlets and assets under management in excess of A$63 billion.

If there was a single project that captured Westfield’s ambition in this era, it was Stratford City in London. Built as a gateway to the 2012 Olympic Games, Westfield Stratford City opened after a reported £1.75 billion development effort, delivering 175,000 square metres of retail, commercial, entertainment, and leisure space. It served a catchment of more than 4 million people. This wasn’t just another mall—it was urban infrastructure, designed to help reshape a neglected part of East London.

But scale has a shadow. Westfield’s market power increasingly drew scrutiny, especially in Australia. The Australian Competition & Consumer Commission investigated disputes between Westfield and its tenants, and in 2004 found Westfield was abusing its market and commercial power in settling disputes. Westfield was forced to formally undertake not to engage in “unconscionable conduct and intimidation” of tenants. It was a reminder that when you control the best retail real estate, you also control the leverage—and regulators notice when that leverage tips into coercion.

Lowy also learned, once, that even he had limits. In 1981, he made a rare detour outside retail property, paying Rupert Murdoch A$842 million for Australia’s smallest national TV network and other media assets. Three years later, when he sold, investors had lost A$450 million, and Lowy himself was down A$100 million. The lesson was blunt: his genius was real, but it wasn’t universal. He didn’t repeat the experiment.

By the time Westfield reached full global scale, the internal tension was becoming obvious. Australia and New Zealand were mature: stable, high-quality assets, but fewer new places to grow. The US and Europe offered bigger upside—but demanded far more capital and carried far more risk. One company, two different businesses, pulling in different directions.

And that set up the most consequential structural decision in the modern Westfield story: the 2014 demerger.

V. The 2014 Demerger: A Strategic Masterstroke

On 30 June 2014, the Westfield empire split in two. Westfield Group reshaped itself into Westfield Corporation by keeping the overseas portfolio, while its Australian and New Zealand assets were transferred into Westfield Retail Trust—renamed Scentre Group.

On paper, it was a restructure. In reality, it was a clean break between two businesses that had grown up under the same logo but were now living in different worlds. Management’s pitch was straightforward: the Australian and New Zealand business and the international business had each become large and high-quality enough to stand alone—and they’d run better, and create more value, if they did.

The path to that moment started months earlier. The plan was announced on 4 December 2013. Shareholders approved it in May 2014. And at the end of June, it clicked into place: Scentre Group took Australia and New Zealand through a merger with Westfield Retail Trust, while Westfield Corporation became the home for the US and UK assets.

Importantly, Scentre wasn’t being set up as a passive landlord with a handful of centres. It would carry over the whole “Westfield way” operating machine—ownership, property management, marketing and leasing, development design and construction, and funds and asset management—run by the existing Australian and New Zealand management team.

At launch, Scentre’s portfolio comprised interests in 47 shopping centres across Australia and New Zealand, valued at around A$28.5 billion. Those centres generated roughly A$22 billion in annual retail sales and attracted about 555 million customer visits. This wasn’t a dumping ground for leftovers. It was the foundation: the mature, high-performing assets that had made Westfield untouchable at home.

Peter Lowy later put the core problem bluntly: “Westfield owned properties in so many different jurisdictions that we actually had diseconomies of scale instead of economies of scale.” In Australia, the business was stable and steady—exactly what income-focused investors wanted. Outside Australia, Westfield was increasingly a development company, with a different rhythm, different risks, and different capital needs. Splitting the company, he argued, made each side more efficient—and easier for the market to value properly.

The early market verdict was encouraging. Dark noted that Westfield and Scentre’s stocks outperformed the average returns on the Australian Stock Exchange after the demerger. Frank Lowy, serving as chairman of both companies at the time, told shareholders that since June 2014 the combined market capitalisation of Westfield Corporation and Scentre Group had grown to more than $41 billion, representing $12 billion of value creation for securityholders who participated in the restructure.

One detail mattered more than it might sound: Scentre retained the right to use the Westfield brand in Australia and New Zealand. That licensing arrangement meant the newly independent company didn’t have to explain itself to customers. The name above the door stayed the same—and with it, decades of trust and recognition.

And that was the deeper strategic logic. Australia and New Zealand were mature assets with stable cash flows, suited to an income-oriented REIT profile. The international portfolio, especially in the US and UK, was more development-heavy and higher risk, suited to investors chasing growth. Two different growth profiles, two different risk profiles, and two very different capital allocation playbooks—forced into one structure for decades.

Now they were separate. Scentre became an internally managed retail property group focused on Australia and New Zealand, expected to be the largest Australian listed REIT and one of the top 20 ASX-listed entities by expected market capitalisation.

VI. The Lowy Exit and Leadership Transition (2015–2019)

The demerger created two companies, but at first, the story still felt familiar: the same family, the same imprint, the same gravity at the top. That began to change in October 2015, when Frank Lowy stepped down as chairman of Scentre Group after 55 years leading the broader Westfield enterprise. It was a public handover, and it signalled something bigger: the start of the Lowys stepping away from the Australian and New Zealand business entirely.

The final turn of the page came in 2019. Steven Lowy retired from the Scentre Group Board, and later that year the Lowy family sold its remaining financial interests in Scentre Group, completing a full exit.

That kind of departure leaves a very specific question hanging in the air: what does a company become when the founder-family disappears from both the boardroom and the register? For Scentre, it meant a shift from founder-led entrepreneurship to institutional ownership—and from legacy-driven leadership to governance that had to stand on process, discipline, and repeatability.

The chairmanship moved to Brian Schwartz AM. The Board appointed the deputy chair to succeed Frank Lowy, and with Schwartz came a different kind of authority: professional management experience, deep institutional relationships, and credibility built less on family history and more on modern governance.

Practically, that transition meant doing the work that founder-led companies can sometimes delay. Systems had to be formalised. Decision-making needed clearer rules. The board had to feel less like a dynasty’s oversight and more like an institution’s. Executive capability had to be developed in a way that didn’t rely on a family orbiting the centre of the company.

Frank Lowy didn’t disappear from public life. He had founded the Lowy Institute in 2003 and served as its chairman. And even as he stepped back from Scentre, he remained involved in the international Westfield business—where the risk, the capital needs, and the stakes were higher. In other words: Scentre became the professionally managed home business, while the family’s attention increasingly tilted toward the global portfolio.

Lowy’s wealth reflected just how much value that journey had created. In May 2025, his net worth was assessed at A$10.28 billion in the Australian Financial Review Rich List. And in November 2024, he and Melbourne lawyer Mark Leibler were awarded Israel’s highest civilian honour, the Israeli Presidential Medal of Honour, recognising their commitment to Israel and support of Jewish communities in Australia.

For Scentre, though, the meaning of the Lowy exit wasn’t symbolic. It was structural. The company now had to prove it could keep the Westfield machine running—without the family that built it.

VII. Westfield Corporation's Sale to Unibail-Rodamco (2018)

To understand why Scentre’s story plays out the way it does after 2014, you have to look at what happened to the other half of the empire.

In December 2017, French property giant Unibail-Rodamco agreed to buy Westfield Corporation—the company that now held Westfield’s US and UK portfolio, including 35 shopping centres. Frank Lowy framed it as the logical end point of the split: “This transaction is the culmination of the strategic journey Westfield has been on since its 2014 restructure,” he said. “We see this transaction as highly compelling for Westfield’s securityholders and Unibail-Rodamco’s shareholders alike.”

By June 2018, the deal was done. Unibail-Rodamco announced it had completed the acquisition and would rebrand the combined company as Unibail-Rodamco-Westfield—positioning it as a premier global developer and operator of flagship shopping destinations, with a portfolio valued at €62 billion across retail, offices, and convention and exhibition venues. And in a symbolic move to cement the merger, Unibail began rolling the Westfield name across parts of its existing portfolio, with 10 flagship centres adopting the brand from September 2019.

But here’s the key detail for Scentre: none of the Westfield-branded centres in Australia and New Zealand were part of the acquisition. Those assets stayed exactly where the 2014 demerger had placed them—inside Scentre Group.

That wasn’t an accident. The demerger had created optionality. It separated two businesses with fundamentally different profiles: mature, income-oriented Australian and New Zealand assets on one side, and a more development-heavy international platform on the other. Unibail-Rodamco wanted the flagship pipeline and the global footprint in major US and European markets—not a stable, domestic Australian portfolio that behaved more like an income REIT.

In hindsight, Scentre’s independence looks less like luck and more like insulation. Unibail-Rodamco-Westfield ran straight into brutal headwinds: accelerating e-commerce, then COVID-era lockdowns, and the broader “retail apocalypse” narrative that hit many American malls hard. In November 2020, supervisory-board chairman Colin Dyer resigned after shareholders rejected the board’s proposed €3.5 billion capital raise. He stayed on the board, but was replaced as chairman by former Unibail CEO Leon Bressler—who was part of a shareholder and investor consortium that had opposed the capital increase and other strategies.

While Unibail-Rodamco-Westfield was dealing with investor revolt and balance sheet strain, Scentre could stay focused: one region, one operating playbook, and the strongest retail destinations in a market it knew intimately. The 2014 demerger didn’t just unlock value. It ring-fenced Scentre from the worst of the turmoil that followed offshore.

VIII. COVID-19: The Near-Death Experience (2020–2021)

Then came the pandemic—the kind of shock that turns a steady, cash-generating property business into a stress test overnight.

In the first half of 2020, Scentre Group reported an interim loss of AU$3.6 billion as COVID-19 restrictions rippled through Australia and New Zealand and retailers struggled to pay rent. Revenue fell 16% to AU$1.1 billion. Funds from operations dropped 46% to AU$361.9 million. And underpinning it all was the uncomfortable reality that the value of a shopping centre is inseparable from the ability to fill it: Scentre booked an unrealised, non-cash reduction of AU$4.079 billion against its portfolio.

The operational hit was even more visceral. As restrictions tightened in March and April, customer visitation sank to just 39% of the prior year’s level. These were assets purpose-built to bring people together—suddenly operating in a world where together was exactly what you couldn’t be. Foot traffic evaporated. Stores went dark. The machine that had run predictably for decades started to look, for the first time, genuinely vulnerable.

Scentre’s response was fast and very visible. From 1 May 2020, the Board took a 20% reduction in base fees, and the senior leadership team took a 20% cut in fixed remuneration. In April, the Group increased liquidity to $3.1 billion—shoring up the balance sheet and signalling that the pain wasn’t going to be pushed onto tenants alone.

That mattered, because tenant support became the whole game. CEO Peter Allen pointed out the scale of what the sector was doing: “The shopping centre industry has provided over AU$1.6 billion of support for retailers during the pandemic… We have agreed arrangements with 2,438 of our 3,600 retail partners, including 1,624 SME retail partners.”

At the same time, Scentre had to adapt the centres to a new role. One pivot was positioning Westfield destinations as “essential services” hubs—places people still needed for supermarkets, pharmacies, and other basics. The other was accepting that the pandemic had pulled the future forward on omnichannel retail. Scentre rolled out a drive-up, contactless click-and-collect service across all Australian Westfield destinations, letting customers buy from multiple business partners without going inside.

Behind the scenes, liquidity became oxygen. Scentre raised or extended $5.8 billion of additional funding, including $3.4 billion of bank facilities and $2.4 billion of long-term bonds. It reported available liquidity of $4.4 billion, enough to cover maturities through to January 2023. That buffer bought time in a moment when many retail landlords around the world were facing tenant failures and capital structure pressure all at once.

And Scentre made a call that said everything about how seriously it was taking the moment: it didn’t pay an interim distribution for the six months ending 30 June 2020, choosing to preserve capital under maximum uncertainty.

Some observers argued the company was still better positioned than most. Morgan Stanley equity analyst Simon Chan noted that across the portfolio, Scentre’s centres were in wealthier catchments with stronger incomes and higher population density—and that while the portfolio’s discretionary tilt made it more exposed to consumer confidence, it would also benefit most when normal life returned.

That ended up being the quiet, validating lesson of the crisis. When restrictions eased, customers came back. And Scentre’s decades-old strategy—owning the best-located destinations in dense, affluent catchments—became an advantage again the moment people were allowed to gather.

IX. The Recovery and Transformation (2021–Present)

When restrictions lifted, the comeback was faster—and more durable—than the “death of the mall” crowd expected. By 2023, footfall was climbing again, occupancy was back to 99%, and leasing momentum returned in force. In the first nine months of 2024, customer visits rose 2.1% year-over-year to 429 million. Business partner sales increased 2.3% to $20.2 billion, and by 30 September 2024 annual sales had reached a record $28.8 billion.

By 30 June 2025, portfolio occupancy hit 99.7%, the highest since 2017. It’s the simplest proof point of what the recovery really meant: in a market with plenty of retail options, the best Westfield locations stayed full because customers kept coming.

That recovery also coincided with a leadership handover. Peter Allen, Scentre’s inaugural CEO and Managing Director, announced he would step down on 30 September 2022, after more than eight years in the role, and retire from the Group in 2023. The Board appointed Elliott Rusanow as CEO and Managing Director, effective 1 October 2022.

Rusanow wasn’t an outsider brought in to “fix” something. He joined Scentre Group in April 2019 as Chief Financial Officer, leading finance, treasury, investor relations, and capital transactions. He also brought long Westfield DNA: he joined Westfield Group in 1999 and has spent more than 25 years across retail real estate, finance, investment management, and corporate strategy in Australia, the United States, and the United Kingdom—experience that mattered as Scentre shifted from recovery mode back into long-term reinvention.

Because the post-COVID plan wasn’t simply to refill the same boxes and run the old playbook. The company’s push from “shopping centres” to “living centres” was an operating philosophy: reposition Westfield destinations as community gathering places that happen to include retail. Dining, entertainment, services, and health offerings weren’t side dishes; they were central to giving people reasons to visit more often, stay longer, and come for more than one purpose.

Financially, the momentum showed up in the numbers. For the 12 months to 31 December 2024, Scentre reported Funds From Operations of $1,132 million (21.82 cents per security), up 3.5% on the prior year. Distributions totalled $893 million (17.20 cents per security), up 3.8%.

And as the centres became more modern “town squares,” Scentre also tied the next era to a clearer sustainability agenda, announcing a net zero emissions target by 2030 across its wholly-owned portfolio of Westfield destinations—positioning the goal as both responsibility and competitive edge.

X. The Bondi Junction Tragedy (April 2024)

Some events defy business analysis.

On Saturday 13 April 2024, Westfield Bondi Junction became the scene of an unfathomable act of violence. A 40-year-old man, Joel Cauchi, entered the centre in Sydney’s eastern suburbs and stabbed at least 18 people, killing six and injuring 12 more. Five of the people he killed were women.

Six innocent people lost their lives, including one of Scentre’s security team members, and many others were impacted. Dawn Singleton, 25; Ashlee Good, 38; Jade Young, 47; Pikria Darchia, 55; Yixuan Cheng, 27; and security guard Faraz Tahir, 30, died before Cauchi was fatally shot by Inspector Amy Scott.

In the days that followed, Scentre’s response was about people first, operations second. CEO Elliott Rusanow said, after speaking at the vigil at Bondi Junction: “On Saturday, Westfield Bondi was the location of a tragedy that resulted in loss of life, including one of our security team members. A significant number of people sustained serious injuries. Many more witnessed these horrific events. We extend our deepest condolences to the families and loved ones of the victims and all those impacted by this tragedy. We want to reiterate our appreciation for the swift and brave actions of our team, members of the public, first responders and our business partners.”

The immediate priority was care. Specialists from Scentre’s employee assistance provider, Assure, delivered briefings to store managers to help them support their teams as they returned to work. Mental health counsellors were made available in-centre for team members.

Rusanow also made clear that security would be treated as a long-term commitment, not a short-term reaction. “The safety of our customers, business partners, community and people is our highest priority,” he said. “Our approach to security involves working in close partnership with law enforcement authorities, including police and relevant government agencies. We heightened security across all Westfield destinations following the events of 7 October 2023 and further enhanced this following the attack at Westfield Bondi on 13 April 2024. Whilst this has seen operating costs increase during 2024, we will continue to invest in these security initiatives.”

A year on, the NSW Government, Waverley Council, Scentre Group, and the wider community came together to observe the anniversary of the tragedy.

What Bondi Junction revealed about shopping centres is sobering, but important. These places aren’t just clusters of leases and sales per square metre. They’re public spaces where people bring their kids, meet friends, run errands, and spend time—places that function like modern civic infrastructure. That trust was violated in the most brutal way. And yet, the community response—vigils, solidarity, and the determination to return—also underscored how deeply these destinations are woven into daily life.

XI. Business Model Deep Dive: The Vertically Integrated Platform

Westfield was never built as “just” a landlord. From the beginning, the Group owned the assets, developed them, designed and constructed them, then operated them day to day—funds and asset management, property management, leasing, and marketing all under one roof. Scentre inherited that machine after the demerger, and then tightened it: more control over the whole experience, more consistency across the portfolio, and fewer handoffs where quality gets lost.

Everything rolls up to one deceptively simple mantra: “more people, more often, for longer.” It’s the lens Scentre uses to decide what to build, what to renovate, what tenants to chase, and what experiences to add. The logic compounds. More visits lift retailer sales. Higher sales support higher rents. Higher rents attract stronger brands. Stronger brands bring more visits. A great centre becomes a flywheel, not a building.

That flywheel also explains why the revenue story is broader than rent. Scentre’s retail services layer in marketing services, gift cards, centre services, and a marketing hub—tools that help business partners sell more, and give Scentre more ways to participate in that value creation. BrandSpace is the clearest example: it gives brands access to more than 1,800 full motion SuperScreens and SmartScreens, plus pop-ups and promotional touchpoints designed to connect with customers while they’re already in-market.

Once you see the centres as a media surface, not just a leasing map, the advertising opportunity becomes obvious. Westfield’s screen network—over 1,200 screens across 800 locations—was built to sit along the customer journey, turning foot traffic into something you can monetize even when a customer doesn’t walk into a particular store. Attention becomes inventory.

Behind the scenes, Scentre has also been reshaping its capital structure. In March, the Group completed the make-whole redemption of the remaining Subordinated Non-Call 2026 Fixed Rate Reset Notes totalling $1.0 billion with a margin of 4.7%. That was funded through a mix of $350 million of undrawn bank facilities and a new $650 million Non-Call 2031 Subordinated Notes at a margin of 2.0%. The Group also issued $0.4 billion of 10-year senior notes through private placement.

All of this fits into a bigger shift: the ongoing move from landlord to platform. Traditional landlords collect rent. Platforms build an ecosystem where multiple value streams meet—leasing, services, media, data, and digital relationships. Scentre’s digital initiatives, including the Westfield Plus membership program, mobile applications, and data analytics, are meant to capture more value from every visit and make the centres work harder than a simple rent model ever could.

That direct relationship with the customer is the prize. The Westfield membership program now exceeds 4.7 million members, up 600,000 over the past 12 months. It’s a meaningful asset in its own right: a way to market directly, personalize experiences, and use data to connect customers and business partners more effectively—without relying entirely on tenants as the only interface with the people walking through the doors.

XII. Porter's Five Forces Analysis

Threat of New Entrants: LOW

If you want to build a premium regional shopping centre from scratch, you’re not just competing with Scentre’s brand—you’re competing with the physics of the business. The capital required is enormous, often $500 million or more for a quality asset. And that’s before you hit the slow, grinding reality of multi-year planning approvals.

There’s also a timing problem that protects incumbents. Australia’s population is projected to grow by 1.7 million people over the next four years, but the retail development pipeline for 2024–2025 sits at just 21% of the 10-year average. In other words: demand is rising, new supply isn’t. Add zoning constraints and the near-guaranteed community backlash that comes with major developments, and the barrier gets even higher.

Then there’s the hardest piece to replicate: anchors. Myer, David Jones, Woolworths, Coles, and major international brands don’t casually sign on with a newcomer. Their long-term commitments effectively pre-let a centre and de-risk a development. Scentre has those relationships and a track record of execution. A new entrant has to earn them from zero.

Bargaining Power of Suppliers (Tenants): MODERATE

Tenants are “suppliers” in the sense that they supply the retail offering—and the power is split. The big anchors have real leverage. Department stores and the major supermarket chains matter disproportionately to foot traffic and credibility, so they can push hard on terms when leases are renewed.

But the power dynamic flips as you move into specialty retail—fashion, dining, and services. Prime space in prime catchments is scarce, and there aren’t many equivalents to a top Westfield destination. Most specialty retailers need the foot traffic more than Scentre needs any single one of them. For international brands trying to establish themselves in Australia, Westfield exposure is often part of the credibility package.

And Scentre’s tenant base is relatively resilient: with 90% of tenants rated investment-grade or equivalent, the portfolio is less exposed to the weakest end of retail.

Bargaining Power of Buyers (Consumers): MODERATE-LOW

Consumers always have options. But Scentre’s advantage is that its options tend to sit exactly where the people are. Westfield destinations are concentrated in dense, high-demand areas—37 in Australia and five in New Zealand—embedded in major urban communities and close to where most of the population lives.

Scentre also leans into habit. Dining, entertainment, and services create a kind of real-world switching cost. If your family’s default is a particular Westfield for dinner, a movie, and errands in one trip, you don’t casually rewire that routine. Convenience becomes loyalty.

Threat of Substitutes: MODERATE-HIGH

E-commerce is the obvious substitute, and it’s still growing—around 15% of Australian retail. Click-and-collect and omnichannel shopping blur the boundary even further, because consumers can buy online while still using physical destinations for pickup, returns, and service. In categories like electronics, books, and other commoditized goods, online has proven it can take meaningful share.

But substitutes hit a ceiling when the “product” is the experience. Dining, health, beauty, and entertainment are far less replaceable. You can’t eat dinner via a website. And while you can watch a film at home, that’s not the same thing as going out.

That’s why the shift toward “living centres” matters: it’s a strategic response to substitution risk by doubling down on what physical places uniquely do well. And there’s still a strong economic argument for the asset class: the data points to a 30% increase in retail turnover and a 40% discount to replacement cost for assets—suggesting these centres remain valuable precisely because they’re so hard to replicate.

Competitive Rivalry: MODERATE

Australia’s premium shopping centre market is concentrated. Scentre owns and operates the Westfield portfolio, while Vicinity Centres is the other heavyweight—collecting rent from several of the country’s best-known destinations, including Chadstone, which it co-owns with the Gandel Group. GPT Group also sits in the top tier, alongside major unlisted investment owners.

This isn’t a market where competitors constantly undercut each other on price. The assets are too scarce and too long-lived for that. Rivalry shows up instead in quality: who has the better centre, the better tenant mix, and the stronger consumer perception. And because there’s limited overlap in premium catchments, the biggest players often avoid direct, street-corner competition through geographic positioning.

When two centres do overlap, the fight is less about rent-cutting and more about winning mindshare—getting the brands, the launches, and the customer’s default choice on a Saturday afternoon.

XIII. Hamilton's Seven Powers Analysis

Scale Economies: STRONG

Forty-two centres give Scentre real operating leverage. Instead of each destination reinventing the wheel, centralized leasing, property management, marketing, and procurement teams can be deployed across the portfolio. Campaigns, systems, and vendor relationships get paid for once, then spread over millions of visits.

That scale also shows up in how Scentre recycles capital without giving up the steering wheel. During the period, the Group used its platform to establish two external trusts as joint venture owners. In June, the $310 million Tea Tree Opportunity Trust purchased a 50% share in Westfield Tea Tree Plaza. In September, the $175 million West Lakes Opportunity Trust acquired a 50% share in Westfield West Lakes in Adelaide. In both cases, Scentre retained the other 50%.

The point isn’t just the transactions themselves. It’s what they enable: monetising part of an asset, keeping operational control, and continuing to earn management fee income.

Network Effects: MODERATE

At the best centres, the dynamic is self-reinforcing: stronger retailers attract more shoppers, and more shoppers attract stronger retailers. Layer on the digital ecosystem—the Westfield app, gift cards, and the Westfield Plus loyalty program—and you get something close to a data flywheel, where insights can improve tenant performance and help attract better brands.

But these network effects have natural limits. Physical retail is bounded by geography. Catchments matter, convenience matters, and many customers simply go to the closest great option—not necessarily the biggest one.

Counter-Positioning: STRONG

Pure e-commerce players can compete on range, price, and speed. What they can’t do is replicate why people still leave the house. Amazon can deliver a product, but it can’t deliver a night out: a movie, a meal, and the unplanned browsing that turns errands into an experience.

At the same time, parts of traditional retail are constrained by legacy formats. Old-school department store models don’t always fit the “living centre” shift. By leaning harder into experiences, dining, and services, Scentre positions its destinations against both online disruption and retail formats that are slower to evolve.

Switching Costs: MODERATE-STRONG

Tenants don’t move lightly, and Scentre’s recent leasing results reflect that stickiness. In the nine months to 30 September 2025, the Group recorded average specialty rent escalations of 4.4%, completed 2,366 leasing deals, and achieved average specialty releasing spreads of +3.0%. The fact that it could re-lease space at higher rents than expiring leases is a practical signal of pricing power.

The switching costs are structural. Specialty leases are typically 5–7 years, creating contractual lock-in. Retailers also sink significant money into fit-outs to meet Westfield standards. And for a store that’s working, the biggest cost of moving isn’t the construction bill—it’s the risk of losing foot traffic by stepping down to a weaker location.

Branding: VERY STRONG

Westfield began in Sydney’s western suburbs in 1959, founded by Sir Frank Lowy and John Saunders, and grew into one of Australia’s most recognisable business success stories. That brand strength translates into economic strength, with premium positioning that can command rent premiums estimated at 15–25% versus competitors. Consumer trust and recognition remain unmatched in Australian retail property.

What’s most telling is that the brand outlived the moments that often fracture reputations: the 2014 demerger and the Lowy family’s eventual exit. Westfield still stands for a specific promise—clean, well-run centres, desirable tenants, easy parking, and comprehensive offerings. That kind of reputation is compounding, and painfully hard to copy.

Cornered Resource: STRONG

Prime urban sites are finite. Westfield destinations sit in some of the most populated cities in Australia and New Zealand, and over decades they’ve become embedded in the social fabric of their communities. You can’t simply create another Bondi Junction somewhere else. The land is taken, zoning is entrenched, and the relationships—retailers, transport links, customer routines—are the product of years.

That scarcity creates a second layer of value: optionality. Scentre is focused on driving long-term growth by adding density to its large, uniquely located strategic land holdings—building more on top of what already works, instead of trying to find new sites that don’t exist.

Process Power: MODERATE-STRONG

Scentre’s vertically integrated model isn’t just an org chart. It’s institutional memory. Decades of refining design, construction, management, leasing, and marketing processes have produced a repeatable operating system—what the company calls the “Westfield way.” Competitors can copy individual tactics, but replicating the full system, embedded in culture and relationships, takes years.

XIV. Key Metrics for Investors

If you’re looking at Scentre Group as a long-term fundamental investment, three KPIs tell you most of what you need to know about the health of the machine:

1. Portfolio Occupancy Rate

Occupancy was 99.8% as at 30 September 2025, up 40 basis points from the same period in 2024. This is the cleanest read on whether Westfield space is still in demand. When occupancy is effectively full, there’s almost no vacancy drag on earnings—and it’s a signal that, even after all the noise about e-commerce and changing consumer habits, retailers still want to be in these centres.

2. Specialty Leasing Spreads

In the first six months of 2025, average specialty rent escalations rose by 4.5%, and new lease spreads were +3.0%. Leasing spreads matter because they’re pricing power made visible. When renewals and re-leases get done at higher rates than the expiring deals, it means the space is working for tenants—and Scentre can capture more of that value. When spreads turn negative, it’s usually a warning sign that space is becoming interchangeable.

3. Customer Visitation Growth

In the 45 weeks to 9 November 2025, customer visits across Scentre’s 42 Westfield destinations reached 453 million, up 3.1%—about 13.5 million more visits than the same period in 2024. This is the fuel for everything else. More visits typically mean higher retailer sales, stronger tenant demand, and better economics for leasing and media. And when visitation growth is running ahead of population growth, it’s a real-world validation that the “living centre” shift is doing what it was meant to do.

XV. Bull Case

The bull case for Scentre Group is that a handful of advantages stack on top of each other—and together, they’re hard to dislodge.

Irreplaceable Asset Base: These centres sit on urban sites you can’t simply recreate. Between land scarcity, zoning restrictions, and the reality of community opposition to major new developments, meaningful new supply is structurally constrained. Meanwhile, the population in Scentre’s catchments keeps growing—Australia is projected to add about 1.7 million people over the next four years—creating steady, organic demand for the destinations that already exist.

E-Commerce Resilience Demonstrated: The “retail apocalypse” story played out brutally in parts of the United States, but Australia hasn’t followed the same script. Scentre came out of COVID with occupancy snapping back to extremely high levels. That’s a real-world stress test suggesting that premium, well-located physical destinations still matter—even as online shopping keeps taking share.

Transformation to Platform: Scentre is no longer trying to be a better version of an old-school landlord. The strategy is to behave more like a platform: monetising data, selling media, building membership, and expanding service revenue alongside rent. The Westfield membership program now exceeds 4.8 million members, which is the kind of direct customer relationship most property companies simply don’t have—and it comes with real optionality over time.

Capital Recycling Strategy: Selling minority stakes via joint ventures, while keeping management and operational control, is a way to free up capital without giving up the steering wheel. That capital can be reinvested into redevelopments and upgrades, helping fund growth while supporting returns.

The development engine is the next layer. Scentre continues to progress a roughly $4 billion pipeline of future retail development opportunities aimed at lifting the productivity of the existing portfolio. These projects target a 6% to 7% yield. And because they’re largely on existing land holdings, Scentre gets growth without the usual acquisition risk of buying new sites at the wrong price.

Management Track Record: Operationally, the recent results reinforce the narrative of steady execution. For the six months to 30 June 2025, Scentre reported Funds From Operations of $587 million (11.28 cents per security), up 3.2%, and distributions of $459 million (8.815 cents per security), up 2.5%. The Group also reconfirmed its 2025 FFO target of 22.75 cents per security, implying 4.3% growth for the year.

XVI. Bear Case

The bear case is that even great centres aren’t immune to the big forces reshaping retail—and Scentre’s strengths can become points of exposure when the environment turns.

E-Commerce Trajectory: Australia’s e-commerce penetration, at around 15%, still sits below the US. But the direction of travel is clear. Categories that have held up better in-store—like apparel and cosmetics—may steadily follow the path of electronics and books as fulfilment improves and consumer habits keep shifting. If online penetration were to meaningfully increase over the next decade, physical retail would feel that pressure directly.

Anchor Tenant Risk: Big anchors matter because they set the gravitational field for an entire destination. Department stores like Myer and David Jones have faced structural challenges for years, and any major closure or footprint reduction would be disruptive. Replacing a large-format anchor isn’t like swapping out a specialty tenant—it can take time, significant capital, and a complete rethink of how that part of the centre works.

Interest Rate Sensitivity: As a REIT, Scentre distributes most of its earnings to unitholders, which makes it sensitive to interest rates in two ways. Higher rates make those distributions less attractive relative to fixed income, and they can also raise borrowing costs. Scentre increased its interest rate hedging to 94% as at January 2025, with an average base rate of 2.99%. That helps in the near term, but it’s not a permanent shield.

Development Risk: Scentre’s roughly $4 billion development pipeline is a growth engine—but it’s also a source of risk. Big projects invite cost overruns, shifting tenant demand, and the possibility that the economy turns mid-build. If construction costs rise or leasing commitments soften, returns can compress quickly.

Security and Public Perception: The Bondi Junction tragedy forced security into the foreground. Scentre heightened security across all Westfield destinations and continued investing in new initiatives, which lifted operating costs. That spending protects the brand and the community, but it also weighs on margins—and the reputational downside of another high-profile incident would be difficult to contain.

Concentration Risk: Scentre is concentrated by geography and, to an extent, by tenant ecosystem. If Australian consumer spending weakens, specialty tenant sales come under pressure, and rent sustainability becomes harder to defend. And while Australia is resource-rich, it’s not isolated from global shocks—particularly those tied to its largest trading partner, China.

XVII. Competition and Industry Dynamics

Zoom out for a second and you see just how investable Australian retail real estate has become. Whether it’s a global trophy like Melbourne’s Chadstone, a heritage destination like Sydney’s Queen Victoria Building, a Westfield in the suburbs, or a smaller local mall, investors can access the category through a roster of listed players—Scentre Group, Vicinity Centres, GPT Group, Mirvac, Stockland, Charter Hall Retail REIT, Region Group, and others. Even with higher interest rates, quality retail assets have stayed on the radar for institutional capital.

For Scentre, the most relevant competitive set at the premium end is Vicinity Centres and GPT Group—though they’re not playing identical games.

Vicinity is the other retail heavyweight. With a portfolio valued at around $24 billion and about 60 shopping centres under management, it’s the second-largest listed retail property manager in Australia. Its assets include some of the country’s best-known destinations, designed to produce a diversified, resilient income stream. It even has exposure to landmark CBD retail, like The Strand Arcade in Sydney, which it co-owns.

And then there’s Chadstone—Vicinity’s crown jewel, branded “the Fashion Capital.” It’s Australia’s largest shopping centre and one of the few places that can go toe-to-toe with Westfield for prestige tenants and flagship store openings. But Vicinity’s portfolio also skews more toward sub-regional assets, which gives it a different risk-and-return mix than Scentre’s tighter focus on major metropolitan destinations.

GPT is a different animal again. It’s one of Australia’s oldest and largest diversified REITs, with material exposure across retail, office, and logistics. That diversification changes the pitch to investors: GPT isn’t just a retail call. It’s a broader bet on Australian commercial property, with retail sitting alongside offices and industrial.

What’s interesting is that the competitive dynamic here isn’t constant centre-versus-centre warfare. Catchments are local. A family in Sydney’s eastern suburbs isn’t choosing between Westfield Bondi Junction and Chadstone in Melbourne—they’re choosing between Bondi Junction and other ways to spend their Saturday. The real competition shows up in two places: winning the best tenants, especially international brands entering Australia, and winning capital—convincing institutional investors that your portfolio is the safest, highest-quality way to own the country’s retail destinations.

XVIII. What Lies Ahead

Scentre Group entered 2026 with its operating engine running at post-pandemic highs. Across its 42 Westfield destinations, customer visits in the 45 weeks to 9 November 2025 reached 453 million—up 3.1%, or about 13.5 million more visits than the same stretch in 2024. Business partner sales were climbing too: total annual sales across the portfolio to 30 September 2025 hit $29.5 billion, about $760 million higher than the comparable period a year earlier.

The strategy for the next chapter is less about buying more malls and more about extracting more value from the land it already controls. Scentre’s focus has been on intensifying development at existing destinations—adding density and layering in uses like residential, hotels, and offices above retail. The bet is that this creates growth without paying acquisition premiums, while leaning into what Westfield sites already have in abundance: convenience, traffic, and habit.

Financially, management reaffirmed its 2025 funds from operations target of 22.75 cents per security, implying 4.3% year-on-year growth, with distributions expected to rise 3.0% to 17.72 cents per security.

But the bigger question for Scentre—and for every retail landlord—is whether the post-COVID rebound is a durable return to normal, or a calm before the long-term forces of retail disruption reassert themselves. Bulls argue the world has permanently split in two: commodity purchases move online, while premium, experience-led destinations get stronger. In that view, Westfield’s best locations, serving affluent catchments, keep winning because they sell something e-commerce can’t: a place to be. Bears see the opposite slope: e-commerce penetration keeps rising, and each new wave—social commerce, AI shopping assistants, faster delivery—chips away at the convenience that physical retail used to own.

The truth is messier, and more useful: physical retail isn’t dying, but it is changing shape. The winners won’t be the centres that simply wait for foot traffic. They’ll be the ones that actively integrate digital and physical, keep giving customers new reasons to visit, and sit in locations so entrenched in daily life that demand stays resilient even when the cycle turns.

Scentre, as the heir to a Westfield legacy that began with two immigrants borrowing from a bank manager to buy farmland, has the ingredients you’d want on paper: scarce assets, a powerful brand, and a deeply practiced operating system. Whether that converts into long-term investor returns will come down to execution, the economic backdrop, and the evolving preferences of Australians and New Zealanders—whose choices ultimately decide whether Westfield remains the place more people come, more often, for longer.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube