PLS: From Tantalite Explorers to Lithium Empire

I. Introduction & Episode Roadmap

In the sun-scorched red earth of Western Australia’s Pilbara region, about 140 kilometres from the dusty port town of Port Hedland, sits an ore body that helped kick off one of the most dramatic resource stories of the last decade. Pilgangoora is among the world’s largest hard-rock lithium deposits. And the company that controls it, PLS, formerly Pilbara Minerals, pulled off something rare in modern Australian mining: it went from hopeful explorer to global-scale producer in a market that whipsaws between euphoria and despair.

The question at the heart of this story sounds simple: how did a group of university friends hunting for tantalite, a niche metal most investors couldn’t pick out of a lineup, end up building a lithium giant worth billions? The answer is a mix of geology, timing, and a stubborn refusal to die. It’s also a story about making big bets when the evidence is still fuzzy, then holding on when the world decides you’re wrong.

On paper, Pilbara Minerals became one of the best-performing resources stocks in recent years, with its share price more than 1500 per cent higher than three years ago. Returns like that grab headlines. But the real story is what had to happen underneath: the financing, the operational grind, and the strategic choices that separated PLS from the many would-be lithium winners that didn’t make it through the downcycle.

A few themes run through everything that follows. Timing, first: the pivot from tantalite to lithium landed just as the electric-vehicle narrative went mainstream and projects like Tesla’s Gigafactory made “battery metals” a household category in markets that had never cared. Conviction, second: from 2018 to 2020, lithium prices fell hard, and the company’s leadership later described the period as “the lithium winter.” Survival wasn’t guaranteed; it had to be earned. And strategy, third: PLS didn’t just dig and ship rock. It built relationships and partnerships, including with South Korea’s POSCO, to move closer to the downstream value that usually accrues somewhere else.

By the end of this journey, even the name changed. Pilbara Minerals Limited became PLS Group Limited in November 2025, a signal that the business had grown beyond a single Australian asset. With the acquisition of the Colina lithium project in Brazil and an 18% stake in a South Korean lithium hydroxide facility, PLS positioned itself as a multi-jurisdiction player in the global battery materials supply chain.

This story matters because PLS sits right at the intersection of the biggest forces reshaping industrial economics: electrified transport, grid-scale storage, and a geopolitical race to secure critical minerals outside of Chinese control. If you want to understand what the energy transition looks like in the real world, not in a slide deck, you could do a lot worse than following one company’s path from a patch of Pilbara dirt to the center of the lithium trade.

II. The Founding Story: Five Geologists and a Tantalite Dream

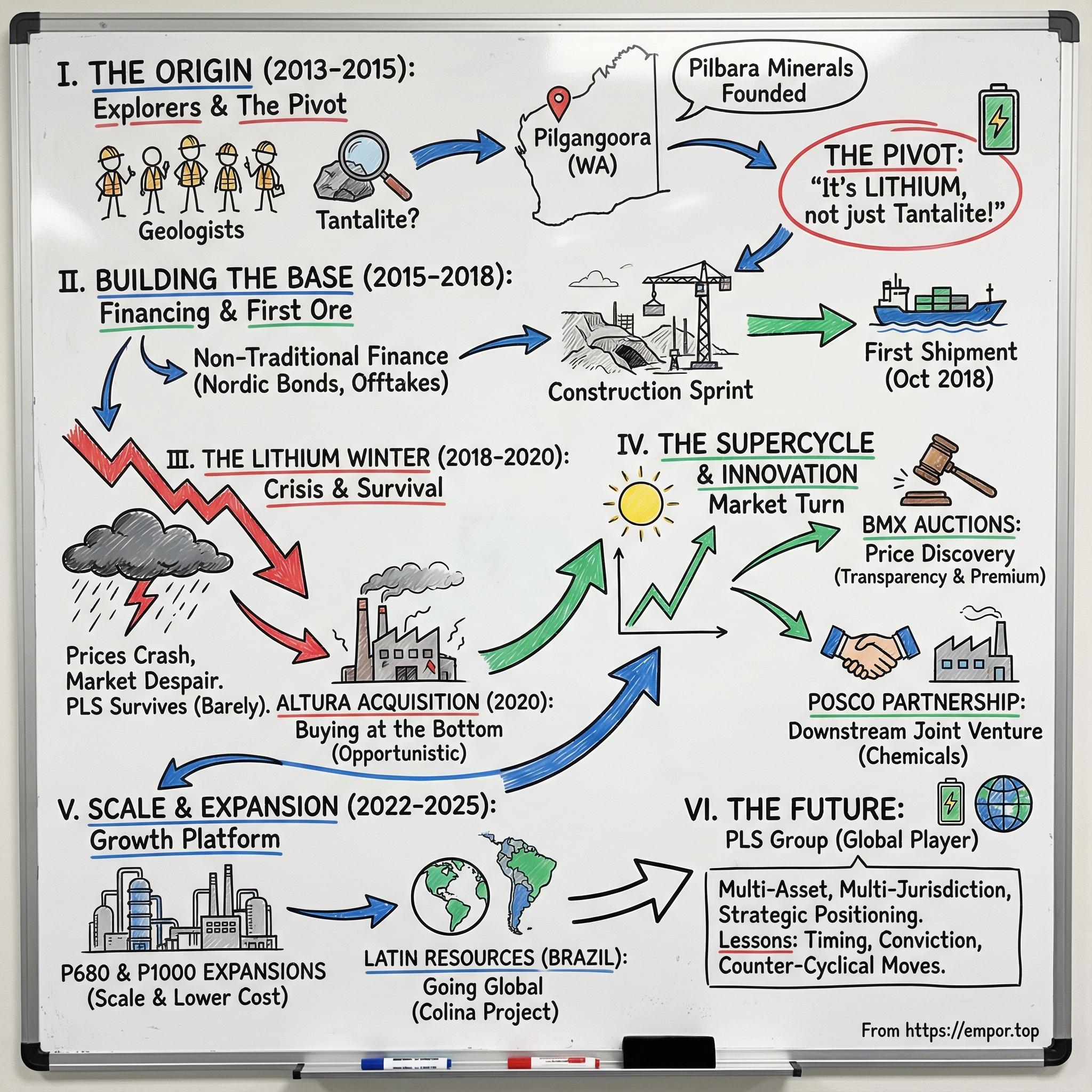

To understand PLS, you have to rewind to 2013. Lithium wasn’t a dinner-table topic, “battery metals” wasn’t a category, and electric vehicles still felt like a Silicon Valley science project. That year, a group of five university-trained geologists teamed up and founded what would become Pilbara Minerals. That detail isn’t just trivia. It shaped the company’s DNA: technically led, willing to hold an unpopular view, and held together by a level of trust you don’t often see once markets get rough.

In the beginning, the dream wasn’t lithium. As early as 2013, with Pilgangoora still just an exploration story, founders John Young and Neil Biddle were hunting for tantalite. Tantalite is the ore used to produce tantalum, a specialty metal that ends up in electronics and high-temperature alloys. The Pilbara had a track record in tantalum, so the bet looked sensible: find the right ground, prove it up, build a business around a niche that the region already knew how to supply.

And Pilgangoora wasn’t some blank spot on the map. The pegmatite field was first discovered in 1905. Over the decades, different operators came and went, mining the area intermittently for alluvial tin and tantalite until 1975, then shifting into larger-scale alluvial operations. The geology kept pulling people back: pegmatites are coarse-grained igneous rocks that can concentrate rare elements, and that promise was enough to keep prospectors circling for more than a century.

Most of that later activity focused on tin and tantalum. There were bouts of small-scale hard rock, eluvial, and alluvial mining, particularly between 1947 and 1978, followed by larger-scale alluvial and eluvial tin-tantalum campaigns in 1978–1982 and again in 1992–1996, run by a series of junior companies. By the time the Pilbara Minerals founders showed up, the area was well-known and well-mapped. It just wasn’t yet widely appreciated for what would become its biggest prize.

In May 2014, Pilbara Minerals acquired the Pilgangoora Project for its lithium potential. Since then, the company drilled more than 1,450 holes for roughly 120,000 metres. The key point is what that acquisition represented: the founders looked at ground everyone associated with tin and tantalite, and they valued it through a different lens. Those same pegmatites also contained spodumene, a lithium-bearing mineral that was about to matter a lot more than almost anyone in Australian mining was prepared to admit.

The setting matters, too. The Pilbara is huge, remote, and brutally dry. It’s famous for ancient landscapes, deep Aboriginal history, and the iron ore machine that feeds a big chunk of the world’s steel. But beneath that red earth are some of the oldest rocks on the planet, and in the right places those ancient formations host lithium-rich pegmatites.

Geologically, Pilgangoora sits within the Archean North Pilbara Craton and the East Strelley Greenstone Belt, made up of steeply dipping mafic metavolcanic rocks and amphibolites. It’s the kind of sentence that can sound like pure jargon, but it’s the underlying reason this story exists at all: the deposit is the product of very specific conditions that concentrated valuable minerals into mineable shapes.

When Pilbara Minerals bought in, the project covered about 31 square kilometres: three Mining Leases—M45/78, M45/333, and M45/511—and two Exploration Licences—EL45/2232 and EL45/2241. At the time, it was a tidy land package with potential. In hindsight, it was the footprint of something that would grow into one of the world’s largest independent hard-rock lithium operations.

For anyone trying to make sense of PLS, the founding story is the first clue. Big resource outcomes often start with small groups of technical people who can read rocks better than markets can read narratives. In this case, the shared university background created an unusual level of alignment—something that would become priceless when the cycle turned and survival became the job.

III. The Lithium Pivot: From Tantalite to the Battery Metal

The inflection point came in 2015, in a hotel conference room a long way from the Pilbara. John Young attended the World Lithium Conference and walked out seeing Pilgangoora through a new lens. Lithium wasn’t just another specialty metal; it was starting to look like a cornerstone of the renewable energy shift. And the timing, in hindsight, was immaculate. Tesla had announced plans for its Gigafactory the year before. A small set of analysts were beginning to run the numbers on what rapid EV adoption would do to battery supply chains.

Back then, though, this was not consensus thinking—especially not in Australia. The local market understood iron ore, coal, and gold. Lithium sounded speculative. So when Pilbara Minerals needed real money to build Pilgangoora, it had to get creative. In 2016, the company raised financing on the Nordic bond market, a pretty clear signal of how indifferent—or skeptical—Australian capital was about lithium at the time.

Putting the funding together became its own engineering project: a structured mix of debt, equity, and customer commitments that, together, made the project bankable. Pilbara Minerals raised A$130 million through a senior secured bond issue, plus an A$80 million share placement and an A$15 million share purchase plan. The Clean Energy Finance Corporation, a corporate entity of the Australian Government, subscribed to the bonds. And a key part of the equity came from Jiangxi Ganfeng Lithium, the company’s offtake partner, which committed about A$27 million as part of the placement.

That Ganfeng participation mattered far beyond the dollars. It was outside validation from the part of the world that actually processed lithium at scale. Chinese converters were willing to back new spodumene supply before most Western investors were ready to believe the story.

Pilbara moved quickly to lock in customers, too. By March 2016, it had signed memoranda of understanding with eight potential customers spread across China, Korea, Japan, North America, and Europe. Not long after, those conversations tightened into binding offtake deals for the Stage 1 project: China’s General Lithium agreed to buy up to 140,000 tonnes per year of 6% chemical-grade spodumene concentrate from Q1 2018 for an initial six-year term, while Ganfeng agreed to buy up to 160,000 tonnes per year under an agreement initially spanning ten years.

At the center of this push was a new leader brought in at exactly the moment the company needed to shift from exploration-mode optimism to construction-grade execution. Ken Brinsden joined in January 2016 as Chief Executive Officer and was appointed Managing Director and CEO in May 2016. A mining engineer with decades of experience across surface and underground operations—plus hard-won lessons from building in the Pilbara at Atlas Iron—Brinsden led Pilgangoora from first drill hole to production in under four years.

The pace was, by mining standards, almost absurd. In roughly four years, Pilgangoora went from early drilling to first production. And within a few more years, Pilgangoora had grown into a meaningful source of global hard-rock lithium supply.

This is the pivot that made PLS what it became. A technically led founding team spotted a demand curve before the market did. Management then solved two problems that kill most would-be miners: funding and customers. Non-traditional capital, plus credible offtake partners, turned a contrarian geology bet into a buildable business—right before the industry learned just how brutal the lithium cycle could be.

IV. The Race to Production & Immediate Crisis: 2017-2020

Dale Henderson walked into Pilbara Minerals in 2017 as chief operating officer with the wind at his back. The EV story was hardening from narrative into numbers, lithium prices looked healthy, and new mines were racing to be first. As he put it later, “the sky looked bright, (and) I believed the story.” He arrived right when Pilbara needed to stop being an explorer with a great deck and become a builder with a deadline.

Henderson was an engineer with the kind of resume you want when you’re about to commission a mine in the Pilbara: operations and development experience across multiple commodities, in both brownfields and greenfields environments, and time spent inside major operators like Fortescue Metals Group, Chevron, and Occidental Petroleum. He’d seen what “scale-up” really feels like, including at Fortescue during its breakneck growth years. Pilgangoora would demand that same mix of speed, discipline, and improvisation.

On the ground, the team executed. Pilbara Minerals’ wholly owned Pilgangoora lithium-tantalum project is in Western Australia’s Pilbara region. Stage one development wrapped in July 2018, and the first shipment of spodumene concentrate went out in October 2018. Four years after acquiring the project, Pilbara had done the thing most juniors never do: it made the jump to production.

And then, almost immediately, the floor dropped out.

Henderson later described the timing with a kind of grim disbelief: the mine was built “just in time for the lithium downturn in 2018,” the period the team came to call “the lithium winter.” “We went straight into this chapter of what we phrase, ‘the lithium winter’, and it was cold, bitter and it just kept going.”

The epicenter was China, where policy had been turbocharging demand. When the Chinese government began pulling back EV purchase subsidies, demand retreated, and the shock rippled through the entire battery supply chain. Subsidies were cut and then cut again—reductions that hit between 2017 and 2020—and what followed was exactly what you’d fear: lower battery demand, weaker conversion economics, and lithium prices collapsing just as new supply was coming online.

Across Australia’s hard-rock sector, producers reacted the only way they could: by pulling back. Between 2018 and 2020, there were curtailments at Bald Hill and Wodgina, and production reductions at Pilgangoora and Mt Cattlin. The industry had sprinted into the boom and suddenly found itself with too much capacity and nowhere for it to go at anything resembling a profitable price.

At Pilbara, the numbers got ugly fast. Henderson said the company operated for only about 30 per cent of the 2019–20 financial year, finished FY20 with a A$100 million cash loss, and still had the Nordic debt facility hanging over it. This is the nightmare scenario for a new mine: you’ve just spent the capital, you’re still carrying the financing, and the commodity price moves against you before you’ve had a chance to build momentum.

But Pilbara didn’t break. It bent, cut back, and stayed alive long enough for the cycle to shift. “We managed to survive the storm,” Henderson said. “And come late-2020, the ice was thawing, there were some signs of spring, and we were starting to have some confidence in the outlook.”

That’s the hard part of this story: not the boom, but the gap between “we shipped first product” and “this is a real business.” The lithium winter was the crucible. It forced Pilbara to learn, quickly, what every commodity company eventually learns: markets turn, policy changes, and survival often comes down to flexibility and endurance more than brilliance.

V. The Altura Acquisition: Opportunistic Consolidation

The very bottom of the lithium winter didn’t just test Pilbara Minerals. It handed them a once-in-a-cycle opening.

In October 2020, Altura Mining—Pilbara’s neighbour at Pilgangoora—shut down. Its operation, including the processing plant that would later be renamed Ngungaju, was the last major cutback before the market began to recover in 2021. Altura had simply run out of financial runway.

Pilbara moved fast. On October 26, 2020, Pilbara Minerals Limited signed an implementation deed to acquire Altura Lithium Operations Pty Ltd. for about $180 million. At the time, that took real conviction. Prices were still down, sentiment was still awful, and nobody could honestly promise the recovery was close.

The deal ultimately closed at $201 million, finalising Pilbara’s acquisition of Altura’s lithium project in Western Australia. It was, in every sense, a distressed sale—assets that would have cost far more to build from scratch changing hands because the seller couldn’t keep going.

Henderson later summed up how it felt from inside the business: “Coincident with that time, the neighbouring operation, Altura, ran out of rope with their lenders so we acquired it. We had to max the credit card and the overdraft, but we got the deal done.” This wasn’t a victory lap acquisition. It was a calculated bet placed while Pilbara itself was still bruised.

The logic, though, was straightforward. “Having ownership of two processing plants provides the flexibility to both blend products to suit customer/market requirements, as well as dial production up or down as required to meet customer needs and market conditions,” Henderson said. Two plants meant options: operational redundancy, product flexibility, and capacity you could bring back when conditions improved—without waiting years to permit and build.

Industry observers saw the same consolidation dynamic playing out. “Spodumene mergers and acquisitions make complete sense and begin to simplify the lithium rush of 2016 into fewer but bigger producers,” said Benchmark Mineral Intelligence managing director Simon Moores. He argued the Altura deal “sets Pilbara Minerals on the path to become the world’s dominant lithium producer.”

Ken Brinsden put a finer point on it at the time, calling the transaction a milestone not just for Pilbara, but for the Australian lithium sector. “This is a historic day in Pilbara Minerals’ relatively short history as a lithium producer,” he said, “and marks an important moment, not just for our shareholders, but also for the lithium industry in Australia.” He described it as “one of the most compelling transactions seen in the lithium sector in recent times.”

Ngungaju would go on to matter—but not forever. The plant had a nameplate capacity of roughly 180,000 to 200,000 tonnes per year of spodumene concentrate, but it ran smaller and higher-cost than Pilbara’s primary Pilgan plant. In the 2023–2024 price downturn, Pilbara decided it would focus solely on production from Pilgan, estimating the shift would improve cashflow by about A$200 million. “While the Ngungaju plant has undergone significant upgrades since it was acquired from Altura Mining, it does not match the scale or processing capability of the Pilgan plant,” the company said.

As a case study, the Altura acquisition is counter-cyclical M&A in its purest form: buy when nobody wants the asset, survive long enough for the cycle to turn, and let time do the work. Pilbara really did “max the credit card” at the bottom—and when lithium came roaring back, that decision looked less like a gamble and more like the move that separated survivors from winners.

VI. The Market Turns: 2020-2022 Lithium Supercycle

By late 2020, the ice really was thawing. China’s demand started to come back. Europe, chasing climate targets and using post-COVID stimulus as a lever, rolled out fresh EV incentives. And almost overnight, the lithium market swung from “too much supply” to “not enough,” with a speed that caught plenty of people flat-footed.

Pilbara didn’t just benefit from the rebound. It changed how the product got sold.

In mid-2021, the company ran its first spodumene concentrate auction through a new platform it had built: the Battery Material Exchange, or BMX. The inaugural event lasted three hours. Seventeen bidders showed up. Sixty-two bids flew in. And by the end, a 10,000-tonne cargo had cleared at US$1,250 per dry metric tonne, free-on-board—well above where contracted pricing was sitting.

That was the point. For years, spodumene had been sold through quiet, one-on-one negotiations, with pricing formulas that often lagged what was happening in the real market. BMX dragged that process into the open. It created transparent, real-time price discovery in a market that had largely operated behind closed doors. And once buyers had to compete in public, the clearing prices did the talking.

The numbers escalated quickly. Pilbara later sold an 8,000-tonne SC5.5 cargo for US$2,240 per tonne via BMX, a result that would have sounded absurd during the lithium winter. BMX had become a live scoreboard for a tightening market.

The platform itself was built in collaboration with Perth technology company GLX Digital. The idea was simple: offer current and future unallocated spodumene concentrate to the spot market in a structured, competitive process. In practice, it created a venue where buyers could no longer rely on opacity—and where Pilbara could capture value that might otherwise have leaked to intermediaries or been diluted by slow-moving contract benchmarks.

By the time Pilbara ran its ninth auction, the market had moved from “recovery” to something closer to frenzy. That auction attracted a bid equivalent to about US$7,708 per dry metric tonne. In November 2022, prices peaked at around US$7,805 per dmt, before easing slightly to roughly US$7,505 in a subsequent result. The broader point wasn’t the week-to-week wiggle. It was the arc: in roughly 16 months, auction outcomes had risen by about an order of magnitude from where BMX started.

Ken Brinsden offered three explanations for what everyone was watching in real time. First, a straightforward one: “it’s just a genuine shortage.” Second, expectations: buyers might believe prices were still going higher, so paying up now made sense. And third, pressure: a buyer could be contractually committed downstream—having to deliver chemicals without enough raw material secured upstream.

For investors, BMX is one of those rare innovations that looks obvious only after it works. Pilbara didn’t change the geology or reinvent processing. It rewired the commercial mechanism. By pulling price discovery into the open, it gave itself a way to realize premium pricing when the market was tight—and it signaled something else, too: PLS wasn’t just a producer riding a supercycle. It was shaping how the lithium market functioned.

VII. The POSCO Partnership: Moving Downstream

BMX proved Pilbara could win on pricing. But while the auctions were resetting how spodumene got sold, the company was also working on a harder, more strategic shift: stepping beyond digging and shipping rock, and into the chemical conversion step where a lot of the industry’s margin has traditionally lived. The vehicle for that move was a partnership with South Korea’s POSCO.

The relationship started in a very conventional way. In 2018, POSCO Holdings bought a 4.75% stake in Pilbara Minerals and signed a 20-year contract for stable supply of lithium ore from Pilgangoora. For POSCO, it was a straightforward supply-chain play: lock up high-quality feedstock early, before the rest of the world woke up to how tight lithium could get.

But it didn’t stay an offtake-and-equity story for long. In 2021, the two companies formed POSCO Pilbara Lithium Solution, a joint venture with an 82:18 shareholding split—POSCO holding 82%, Pilbara 18%. The concept was simple: import Australian lithium ore into South Korea and convert it into lithium hydroxide for secondary battery materials, closer to the battery makers that actually need it.

The result was a lithium hydroxide facility in Gwangyang. At full capacity, it has the potential to produce up to 43,000 tonnes per year of lithium hydroxide—enough for batteries for around one million electric vehicles. More importantly, it’s meaningful scale outside the gravity well of China’s processing dominance.

The ownership split also tells you how the partnership worked in practice. POSCO brought downstream processing know-how and relationships with Korean battery customers. Pilbara brought what mattered most upstream: secure, long-life feedstock from Pilgangoora.

A ceremony in Gwangyang marked the completion of construction of Train 2 of the Lithium Hydroxide Monohydrate Chemical Facility, which includes Train 1 and Train 2—an event POSCO and Pilbara described as the delivery of Korea’s first lithium hydroxide plant. The facility also put the joint venture in a small club: lithium chemicals producers operating at scale outside of China.

“Our partnership with POSCO began six years ago in 2018 with a bold vision to diversify global battery chemicals production. We are looking forward to continuing our long and prosperous partnership with POSCO in the many years to come. Together, we are working to make a difference in the world by enabling a cleaner and more sustainable energy future.”

By the June quarter referenced, PLS’s 18% stake in the facility was no longer just a strategic slide. The partners sold 3,070 tonnes of battery-grade product to three customers from Train 1, while certification of product from Train 2 was underway.

Zoom out, and you can see why this mattered beyond the immediate tonnage. Western governments and battery manufacturers have been pushing hard for supply chains that don’t depend entirely on Chinese processing capacity. A South Korean lithium hydroxide plant, fed by Australian hard-rock concentrate, checks that box in a way few projects can.

For investors, the lesson is the playbook: you don’t have to vertically integrate alone to reach downstream value. An 18% stake in a world-class conversion facility is far less capital-intensive than trying to build one from scratch—yet it still gives Pilbara exposure to the chemical stage of the supply chain, and a seat at the table where battery-grade product gets made.

VIII. Expansion & Scale: P680, P1000, and Beyond

BMX and the POSCO partnership were about capturing more value from the lithium market. The next chapter was about something more fundamental: scale. With demand back and cash flows repaired, Pilbara set out to make Pilgangoora not just a successful mine, but a platform. The roadmap was staged on purpose—P680, then P1000, and a much bigger P2000 concept kept on the drawing board—because in a commodity business, the worst mistake is building tomorrow’s capacity with yesterday’s price assumptions.

First came P680. With an estimated investment of A$103 million, it was the step that lifted Pilgangoora’s capacity to about 680,000 tonnes per year of spodumene concentrate. Not a moonshot—an incremental, buildable upgrade that made the operation meaningfully larger without betting the company.

Then came the bigger leap: P1000. Pilbara took a final investment decision on the A$560 million project at Pilgangoora, targeting a move from roughly 680,000 tonnes a year to about one million tonnes—an increase of around 47% in nameplate capacity. It wasn’t just more tonnage; the work involved a major upgrade to the Pilgan plant’s concentrator and supporting infrastructure, designed to improve economies of scale and lower future operating costs.

That investment translated into real operational momentum. Pilbara achieved first ore at the P1000 expansion project, and in the quarter referenced, production volume reached 221,000 tonnes—up 77% on the prior quarter—driven by increased output from the optimized Pilgan plant following completion of the P1000 expansion.

By the time management spoke about it in its AGM materials, the message was clear: FY25 marked the end of a heavy investment phase at Pilgangoora. Across P680, P1000, and other site investments, Pilbara said it had deployed about A$1.9 billion in growth capital. The spending was substantial, but the intention was simple: build a lower-cost, scalable operating base that could perform through both booms and winters.

And it wasn’t done thinking about what “scale” could ultimately mean. The P2000 pre-feasibility study concluded that Pilgangoora could be expanded to more than 2 million tonnes per annum, with an average forecast annual spodumene concentrate production over the first ten years of about 1.9 million tonnes per year, at an average grade of roughly SC 5.2%. It’s a dramatic expansion—more than doubling again from P1000—but Pilbara has been careful about timing. The feasibility study for P2000 is expected in the 2027 financial year, and the company has noted that no near-term investment decision was likely given market conditions.

Importantly, Pilbara didn’t carry the expansion story alone. The company secured A$250 million in loans—A$125 million each from the Northern Australia Infrastructure Facility and Export Finance Australia—support that signaled lithium production had moved from “hot commodity” to “strategic national interest” in Australia’s eyes.

Management’s own summary of the transformation captured what these projects were really trying to achieve:

With the completion of both the P680 and the P1000 projects, the Pilgan operation has been fundamentally transformed. We've added 420,000 tonnes of production capacity, improved operational flexibility and delivered a lower cost scalable platform. Most importantly, this transformation positions us to capture margin through the cycle, enabled by improved efficiency, stronger resource utilization and a greater adaptability to market conditions.

The investor takeaway is less about any single expansion number and more about the sequencing. Pilbara scaled in steps, banked the benefits, and kept the next big build as an option—not an obligation. In a business defined by cycles, optionality is its own kind of competitive advantage.

IX. Recent Developments: Latin Resources & Global Expansion

After all the work to scale Pilgangoora, PLS made its biggest bet in years: it went looking for a second pillar.

That came through Latin Resources. Pilbara Minerals Limited (ASX:PLS) completed its acquisition of Latin Resources Limited (ASX:LRS) on February 4, 2025, after signing a binding Scheme Implementation Agreement on August 15, 2024, valuing the deal at about A$560 million. The result was simple and consequential: for the first time, Pilbara owned a meaningful lithium asset outside Australia, giving it a foothold in the Americas.

With 100% of Latin Resources folded in, Pilbara gained the Salinas Project in Brazil, in the mining jurisdiction of Minas Gerais. Pilbara renamed the project Colina, and flagged that it would be put through a review process to inform project design and development studies. The company’s message was that this wasn’t just another exploration add-on; it was intended to become a second major hard-rock operation.

“We are excited to announce the acquisition of Latin Resources,” the company said. “This acquisition is on-strategy, diversifying the business with what we believe is a counter-cyclical, accretive extension that further builds out Pilbara Minerals' position as one of the leading lithium materials suppliers globally. The acquisition will deliver our second 100% owned, Tier 1, hard rock lithium asset, which is expected to be low-cost and accretive for our shareholders.”

Colina already came with scale on paper. Its resource estimate, covering the Colina and Fog’s Block deposits, stands at 77.7 million tonnes at 1.24% lithium oxide—enough to be taken seriously as a future production centre once it moves through studies and development.

Not everyone loved the move. Citi’s analysts noted that while Minas Gerais is mining-friendly, the market might need convincing that Brazil diversification makes sense given the “less-than-stellar” track record of some ASX miners offshore. RBC Capital Markets pointed to “limited operational synergies,” and cautioned that the deal could weigh on near-term earnings.

Inside PLS, the rationale was less about synergies and more about resilience and options. “One of the attractions of Latin Resources was the strong foundation of community support that has been established. We look forward to continuing this collaboration with the community and all key stakeholders in Brazil.” Henderson also framed the asset as a way to sequence future supply and broaden the company’s reach into lithium growth markets like Europe and North America.

Then came the branding to match the new reality. Following shareholder approval at the 2025 Annual General Meeting, the company officially changed its name from Pilbara Minerals Limited to PLS Group Limited. The change took effect from 27 November 2025, with ASX implementation expected to follow from 3 December 2025. It was a small corporate act with a big signal: this was no longer meant to read as a single-asset Pilbara story.

All of this happened against a tougher price tape. In the 2024–2025 lithium downturn, FY25 revenue fell to about A$769 million, down from A$1.25 billion in FY24 and A$4.06 billion in FY23. Net profit swung from a A$257 million profit in FY24 to a A$196 million loss in FY25, reflecting weaker prices and impairments.

Operationally, though, the core machine kept running. Full-year production of 755,000 tonnes came in above the top end of guidance, and unit costs of A$627 per tonne were within the company’s forecast range. The cash margin from operations for the year was A$192 million, and PLS ended June with about A$1 billion in cash.

That combination—expanding globally while staying financially intact through a downcycle—is the real headline. PLS didn’t buy Brazil from a position of desperation. It bought it as a deliberate move to become a multi-asset lithium company, with enough balance-sheet strength to wait for the cycle to come back around.

X. Playbook: Business & Investing Lessons

PLS reads like a checklist of what has to go right in resources—and what you can do when it doesn’t. A few lessons stand out for anyone trying to underwrite a miner beyond the commodity price chart.

Timing and Conviction: The founders pivoted from tantalite to lithium before the EV thesis became mainstream, when the idea still sounded speculative in Australia. Then, when lithium prices collapsed for years, they didn’t flinch into a forced sale. Being early is one thing; staying solvent and committed long enough to get paid is the rarer skill.

Counter-Cyclical M&A: The Altura acquisition is the cleanest example in the story of buying at the bottom. Pilbara paid roughly A$200 million for a neighbouring operation and processing plant that would have cost far more to replicate in a hotter market. The real advantage wasn’t bravado. It was having enough financial flexibility to move while everyone else was cutting to survive.

Capital Discipline: PLS didn’t “out-optimism” the downturn. It managed through it. Over the past 18 months, the company strengthened its position by suspending dividend payments (since September 2023), cutting planned capex (February 2024), reducing its workforce (March 2024), and transitioning to the P850 operating model (September 2024). The point isn’t any single lever—it’s the willingness to pull all of them early enough to protect cash and keep options alive.

Strategic Partnerships: The POSCO relationship shows a practical route to downstream exposure without betting the company on a brand-new chemical plant. Pilbara’s 18% stake in the South Korean lithium hydroxide facility gives it a seat in the conversion economics while letting a partner with deeper processing experience carry most of the capital and execution load.

Innovation in Pricing: BMX was a commercial move disguised as a technology project. By running transparent auctions in a historically opaque market, Pilbara captured pricing that might otherwise have been negotiated away or lost in lagging benchmarks. It didn’t just sell concentrate—it changed the rules of how the market discovers price.

Geographic Diversification: The Colina acquisition is a direct answer to single-asset risk. If all of your value sits in one pit, one jurisdiction, one operating plan, you’re always one surprise away from a very bad year. A multi-jurisdiction portfolio doesn’t eliminate risk, but it does keep any one problem from becoming an existential one.

XI. Porter's Five Forces & Hamilton's Seven Powers Analysis

Porter's Five Forces

Threat of New Entrants: MODERATE-LOW

Breaking into lithium mining isn’t like launching a software startup. New projects require enormous upfront capital, long permitting timelines that can stretch for years, and, most importantly, the right rock. Lithium deposits vary wildly in grade, metallurgy, and operating cost, and those details decide who survives when prices fall.

Then there’s the commercial hurdle: you don’t just sell spodumene to anyone. Converters and battery-linked customers have qualification processes, and those relationships take time to build. Trust is an asset.

Still, the 2020–2022 boom flooded the sector with exploration and development capital. Plenty of projects were pushed forward. The real filter is whether they can secure funding and make it to production at today’s pricing, not whether they can draw a boundary on a map.

Bargaining Power of Suppliers: LOW

For an upstream miner, the biggest “input” is the ore body—and PLS owns its own. That removes the classic supplier squeeze you see in manufacturing.

What remains are mining services, equipment, consumables, and labour. On equipment and contracting, there are usually multiple options, which keeps supplier power in check. Labour is the one pressure point: Western Australia is competitive, and remote operations come with structural cost challenges.

Bargaining Power of Buyers: MODERATE-HIGH

On the other side of the table, buyers are more concentrated. Chinese converters have dominated global spodumene demand, and even when miners negotiate long-term offtakes, the pricing mechanisms tend to anchor back to lithium chemical prices set in China. That limits how much control miners have over the “reference price” of their own product.

This is why BMX mattered. By pushing uncontracted tonnes into a transparent, competitive auction, Pilbara created a way to claw back some leverage—at least when the market was tight and buyers had to compete in public.

Threat of Substitutes: LOW (short-term) / MODERATE (long-term)

In the near term, lithium-ion is the default chemistry for EVs and grid storage. There isn’t a like-for-like substitute ready to displace it at scale.

Longer term, the threat is less “lithium disappears” and more “lithium intensity declines.” New chemistries could reduce how much lithium is required per kilowatt-hour even as total battery demand grows. Sodium-ion is emerging in certain niches, but it doesn’t yet replace lithium-ion across the mainstream. Solid-state doesn’t remove lithium at all; it may actually reinforce demand.

Competitive Rivalry: HIGH

Hard-rock lithium is a tough arena. Australia has several major spodumene operations—Greenbushes, Pilgangoora, Wodgina, plus smaller producers and restart candidates—and most are chasing the same set of converters and end-market credibility.

When prices are high, everyone expands. When prices fall, cost position becomes destiny. That dynamic drives intense rivalry around operating efficiency, reliability, and product consistency, because those are the levers that keep you operating while weaker mines curtail.

Hamilton's Seven Powers

Scale Economies: PLS benefits meaningfully from scale. The P1000 expansion was designed to spread fixed costs across larger volumes and improve unit economics. Management expected unit operating costs to fall to around A$580 per tonne FOB, from A$627 per tonne in FY25, once the expanded system—including ore sorting—ran through a full year. The bigger P2000 concept could extend that advantage, if and when the cycle supports it.

Network Economies: Limited fit here. Lithium mining isn’t a network-driven business.

Counter-Positioning: BMX is the clearest example. The industry had long relied on bilateral deals and opaque pricing formulas. Pilbara introduced transparent auctions that, by design, disrupted the old comfort of private price-setting. Not every producer was eager to follow, because changing the system risks upsetting customer relationships that took years to build.

Switching Costs: Moderate. Converters do need to qualify feedstock, and consistency matters, which creates some stickiness. But spodumene is still a specification product, and buyers can source from multiple producers if supply is available.

Branding: Minimal. This is commodity material sold to a chemical spec, not a consumer brand.

Cornered Resource: This is where PLS is hardest to copy. Pilgangoora is a world-class ore body, and the scale is its own form of defensibility. A resource upgrade to 446 million tonnes at 1.28% lithium oxide put Pilgangoora ahead of Greenbushes as the world’s largest hard-rock lithium resource. You can build a plant. You can’t easily replicate a deposit like that.

Process Power: PLS has accumulated operating advantages that aren’t flashy but compound. Ore sorting, plant optimisation, and the ability to adjust the mine plan and processing blend give it incremental flexibility—exactly the kind that matters most in a volatile commodity market.

Competitive Position Summary

PLS is in a strong position, but not a monopoly-like one. Its core moat is geological: Pilgangoora is enormous, high quality, and scalable. The POSCO partnership adds a valuable downstream angle that few peers can match. And despite the downcycle, the balance sheet has remained a source of resilience.

The risks are the ones you’d expect in a business like this: lithium price volatility, execution risk as Colina moves from acquisition to development in a new jurisdiction, and the constant question of timing—how aggressively to expand, and when, so that new capacity lands into demand rather than into another winter.

Key Performance Indicators for Investors

If you’re tracking PLS as an investment, it helps to keep the scorecard simple. Three metrics do most of the explaining:

1. Unit Operating Costs (A$/tonne FOB)

This is the clearest read on where PLS sits on the cost curve—which, in lithium, is the difference between merely suffering through a downturn and being forced to shut in production.

In the June quarter, Henderson said Pilgangoora “shot the lights out,” with production jumping 77% to 221,300 tonnes of spodumene concentrate while unit costs fell 10% to $397 per tonne. Don’t over-index on any one quarter, but do watch the trend line. Over time, cost direction tells you whether expansions like P1000 are translating into a structurally stronger operation.

2. Spodumene Concentrate Price (US$/tonne)

On the revenue side, everything starts with realized price—whether that comes through long-term offtakes or the more transparent BMX auctions.

A useful habit is to compare what PLS actually receives against the benchmark indices. If PLS is consistently outperforming, that’s real pricing power. If it’s lagging, it’s a signal that product mix, contract structure, or market positioning is working against them. Spot pricing around US$800–900 per tonne sat well below the 2022 extremes, but still above the roughly US$600 level where large parts of the industry start to look genuinely stressed.

3. Cash Balance / Total Liquidity

In a commodity business, liquidity isn’t just a comfort blanket. It’s strategic oxygen.

PLS carried about A$1.1 billion in cash, even while working through near-term headwinds. That matters because it buys time: time to keep operating through weak pricing, time to choose when to invest, and time to let cost improvements from P1000 show up in the numbers. Watching how the cash balance moves through the cycle is one of the fastest ways to judge management discipline—especially when the market is trying to tempt everyone back into overbuilding.

Material Risks and Legal/Regulatory Considerations

For all the scale, optionality, and clever commercial moves, this is still a lithium producer. That means the biggest risks are the ones that come with commodities, concentration, and execution.

Investors should keep an eye on several factors:

Commodity Price Volatility: Lithium prices can move violently, sometimes swinging by more than 80% within a single year. PLS’s earnings and cash generation are highly exposed to a price it doesn’t control, which means outcomes can change fast even if operations stay steady.

Chinese Market Dependence: A large share of global spodumene concentrate still ends up in Chinese conversion plants. That makes PLS indirectly exposed to Chinese policy and market conditions: regulatory changes, trade friction, or a sudden shift in demand can flow through to realized pricing and volumes.

Execution Risk on Colina: Colina is a major strategic step, but it’s also the company’s first development project outside Australia. Different permitting processes, labour dynamics, and operating conditions in Brazil add real uncertainty. The prize is geographic diversification; the risk is that first-time execution in a new jurisdiction rarely goes perfectly.

Short Interest: FNArena’s “Short Report” for the week ending 20 November 2025 placed PLS among the 10 most shorted stocks on the ASX, with short interest near 11.8%. Historically, Pilbara/PLS has often ranked near the top of short-interest tables, rising above 20% in prior cycles. That level of shorting signals meaningful bearish conviction among sophisticated investors—and a stock that can be volatile around price moves, quarterly results, or sentiment shifts.

Accounting Considerations: The FY25 loss included impairments tied to asset write-downs during the downturn. The key issue isn’t just the headline loss; it’s how asset carrying values are set, what price assumptions sit behind them, and how sensitive the balance sheet is if lithium prices stay weak—or fall further.

Conclusion

PLS is, in many ways, the cleanest version of the modern commodity success story: the right rock, read correctly; a pivot made before it was fashionable; a near-death experience when prices collapsed; and then a scale-up into the top tier when the market turned.

What started as a tantalite hunt became a lithium business because the founders and management team made a sequence of decisions that were hard in the moment and obvious only later. They financed Pilgangoora when Australia still shrugged at lithium. They kept the lights on through the lithium winter. They bought Altura when nobody wanted the asset. They created BMX to drag price discovery into the open. And they partnered with POSCO to get exposure to the chemical step without taking on all the risk alone.

The real question for investors now is less “is Pilgangoora a great resource?”—it is—and more “can PLS keep converting advantage into durable performance as the lithium market matures?” The building blocks are there: an exceptional resource base at Pilgangoora, downstream optionality through POSCO, a second growth pillar in Brazil with Colina, and a balance sheet that, so far, has been managed with an eye toward survival, not just expansion.

But lithium remains lithium. Prices can move fast enough to turn disciplined plans into emergency meetings. The same volatility that created the opportunity can also punish even well-run operators—especially when new supply arrives, policy shifts, or demand growth pauses.

So the wrap is this: if you believe electrification continues to compound over the long run, PLS is one of the highest-quality public vehicles to ride that theme, with real scale and a proven ability to stay standing when the cycle turns. If you don’t—if you think the next few years are mostly about oversupply, weak pricing, or simply too much uncertainty—then the risks here aren’t subtle. In commodities, the asset can be world-class and the stock can still be painful. The only antidote is humility about cycles, and sizing that respects how quickly they can change.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube