Mitsubishi UFJ Financial Group: The Rise of Japan's Banking Colossus

I. Introduction & Episode Roadmap

Picture this: It's September 29, 2008. Lehman Brothers has just collapsed. Morgan Stanley's stock price has cratered 80% from its peak. Credit markets are frozen. In Tokyo, executives at Mitsubishi UFJ Financial Group are making a decision that will define their institution for decades—they're about to wire $9 billion to Manhattan, betting on America's financial system when everyone else is running for the exits.

That moment encapsulates everything about MUFG's journey from a collection of 19th-century Japanese merchant banks to a $2.7 trillion global financial colossus. It's a story of patient capital meeting explosive opportunity, of Eastern banking philosophy colliding with Western financial engineering, and of how a company born from Japan's feudal era became one of the world's most powerful financial institutions.

How did a bank that started by financing silk exports and samurai stipends become the lifeline for Wall Street's most prestigious investment bank? The answer lies in 140 years of calculated risks, strategic mergers, and an almost supernatural ability to turn crisis into opportunity.

This is that story—from the Meiji Restoration to artificial intelligence, from zaibatsu conglomerates to cloud computing, from financing Japan's industrialization to bankrolling Southeast Asia's digital revolution. We'll explore how MUFG navigated Japan's bubble economy, orchestrated the most dramatic bank merger in Japanese history, and positioned itself as the bridge between Asian capital and global markets.

The key themes that emerge: the power of cross-border M&A executed at precisely the right moment, the advantage of conglomerate structures in relationship banking, and how a conservative Japanese bank became one of the most aggressive digital innovators in global finance. Along the way, we'll unpack the strategic playbook that turned regional Japanese banks into a global powerhouse—and what it means for the future of international finance.

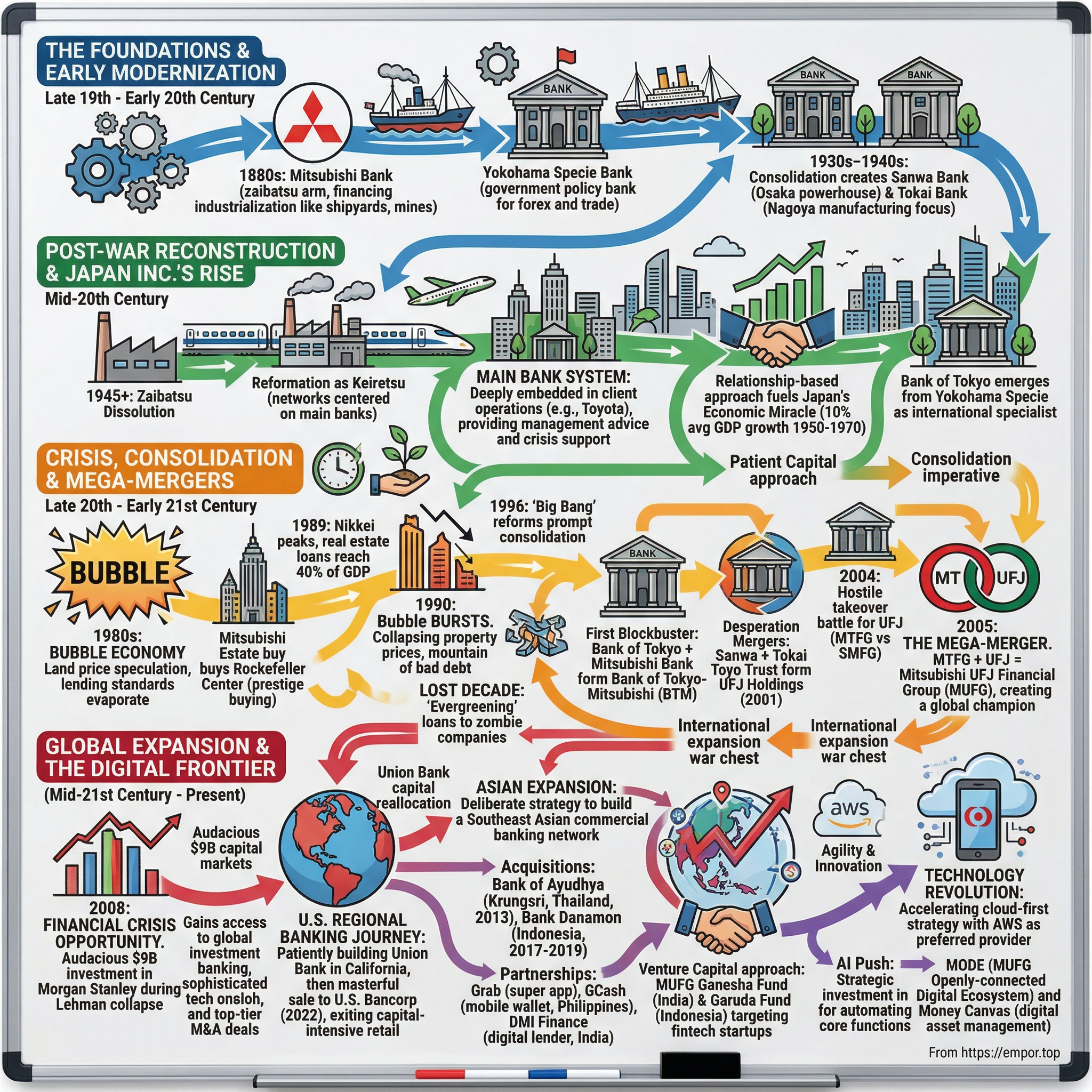

II. The Zaibatsu Origins & Post-War Reconstruction

The year is 1880. Japan has just emerged from centuries of isolation. The Meiji Emperor's government is desperately trying to modernize, sending delegations to study Western banking systems. In this fevered atmosphere of transformation, two institutions are born that will eventually form the backbone of MUFG: Mitsubishi Bank and Yokohama Specie Bank.

Mitsubishi Bank wasn't just any bank—it was the financial arm of Iwasaki Yatarō's empire. Iwasaki, a former samurai who'd built a shipping fortune, understood that controlling capital flow meant controlling Japan's modernization. His bank didn't just store money; it financed the coal mines, shipyards, and trading houses that would transform Japan from feudal backwater to industrial power. The Mitsubishi zaibatsu—that interlocking web of companies bound by cross-shareholdings and family ties—became the prototype for Japanese capitalism itself.

Meanwhile, Yokohama Specie Bank emerged as something different: a policy bank, created by the government to manage foreign exchange and finance international trade. While Mitsubishi Bank powered domestic industrialization, Yokohama Specie handled the delicate dance of international finance, managing Japan's precious foreign currency reserves and facilitating the silk and tea exports that funded the country's modernization.

The 1930s and 1940s brought consolidation. Sanwa Bank emerged in 1933 from the merger of three Osaka institutions, creating a powerhouse in Japan's commercial capital. Tokai Bank followed in 1941, consolidating Nagoya's financial institutions as Japan mobilized for war. These weren't just business combinations—they were strategic moves to concentrate capital for national purposes.

Then came August 1945. Japan lay in ruins. The occupation authorities, led by General MacArthur, viewed the zaibatsu as the financial engines of Japanese militarism. The dissolution orders came swift and harsh. Mitsubishi was shattered into pieces. The holding companies were eliminated. Cross-shareholdings were banned. It seemed like the end of an era.

But here's where the story gets interesting. The Americans, in their zeal to democratize Japanese capitalism, inadvertently created something more powerful. The zaibatsu reformed as keiretsu—looser but still potent networks centered around main banks. Mitsubishi Bank emerged as the financial heart of the new Mitsubishi Group, alongside Mitsubishi Corporation and Mitsubishi Heavy Industries—what insiders called the "Three Great Houses."

The main bank system that emerged was uniquely Japanese. Unlike American banks that maintained arm's-length relationships with borrowers, Japanese main banks became deeply embedded in their clients' operations. They didn't just lend money—they provided management advice, arranged marriages between companies, and acted as corporate therapists during crises. Mitsubishi Bank didn't just finance Toyota's expansion; it helped design their supplier networks, introduced them to international partners, and stood by them through every downturn.

This patient, relationship-based approach powered Japan's economic miracle. Between 1950 and 1970, Japan's GDP grew at an average rate of 10% annually—the fastest sustained growth in recorded economic history. The banks weren't just intermediaries; they were architects of industrial policy, channeling household savings into strategic industries with a precision that made Western economists marvel.

Yokohama Specie Bank, reorganized after the war as Bank of Tokyo, became Japan's international finance specialist. While other banks focused on domestic industrial finance, Bank of Tokyo built networks in London, New York, and Hong Kong, becoming the conduit through which Japan accessed global capital markets. It was the bank that understood both the bow of Japanese business culture and the handshake of Western finance.

By the 1970s, these institutions had evolved far beyond their origins. They weren't just banks anymore—they were the circulatory system of Japan Inc., moving capital with the same strategic purpose that samurai once wielded swords. The relationships forged in these decades—between banks and corporations, between different banks, between Japan and the world—would prove invaluable when crisis struck.

The stage was set for the bubble economy, where these same strengths would become vulnerabilities, and where the conservative banks of the Meiji era would face their greatest test.

III. The Bubble Economy & Crisis Years (1980s–1990s)

Tokyo, 1989. The Imperial Palace grounds—390 acres of gardens and buildings—are theoretically worth more than all the real estate in California. Golf club memberships trade for $3 million. Corporations borrow money not to build factories but to speculate on stocks and land. At the peak, a Ginza nightclub charges $500 for a cup of coffee, and people pay it gladly. This isn't just prosperity—it's collective madness.

The banks were at the center of it all. After the 1985 Plaza Accord forced the yen to appreciate, the Bank of Japan slashed interest rates to prevent recession. Japanese banks, flush with deposits from the country's legendary savers, needed somewhere to put that money. Real estate seemed perfect—after all, in crowded Japan, land prices had risen for forty straight years. What could go wrong?

Mitsubishi Bank, Bank of Tokyo, Sanwa, and Tokai all joined the party. Lending standards evaporated. Banks would lend up to 120% of a property's already inflated value. The collateral? More real estate. It was a circular logic that worked brilliantly—until it didn't. By 1989, outstanding real estate loans from Japanese banks reached ¥170 trillion, nearly 40% of GDP.

The most telling moment came when Mitsubishi Estate, backed by Mitsubishi Bank financing, bought Rockefeller Center in October 1989 for $846 million. Americans were horrified—the Japanese were buying America! But the real story was darker. The purchase price was twice what any rational analysis supported. It was prestige buying, enabled by banks that had forgotten how to say no.

Then, on December 29, 1989—the last trading day of the decade—the Nikkei hit 38,915. It would never see that level again.

The unraveling was spectacular. The Bank of Japan, belatedly worried about speculation, raised rates five times in 1990. Property prices collapsed 60%. The Nikkei fell 40% in nine months. But the real catastrophe was hidden in bank balance sheets. Those real estate loans, collateralized by other real estate, became a mountain of bad debt.

The "Lost Decade" that followed was actually a slow-motion crisis. Japanese banks, rather than recognizing losses, engaged in "evergreening"—extending new loans to bankrupt borrowers so they could pay interest on old loans. Zombie companies shambled through the economy, alive but not really living, kept breathing by banks that couldn't afford to let them die.

By 1995, the hidden bad loans in the Japanese banking system exceeded ¥40 trillion. Sanwa Bank alone had ¥2.2 trillion in non-performing loans. The Ministry of Finance, which had always protected banks, was paralyzed. Admitting the scale of the problem would mean admitting regulatory failure.

The crisis forced a reckoning. In November 1996, Prime Minister Hashimoto announced "Big Bang" financial reforms—Japan's markets would be "free, fair, and global." Translation: consolidate or die. The weak would be absorbed by the strong. The age of mega-mergers had begun.

The first blockbuster came in April 1996: Bank of Tokyo and Mitsubishi Bank announced their merger. It was a combination that made strategic sense—Mitsubishi's domestic strength with Bank of Tokyo's international network. But it was also a defensive move. Alone, each faced existential threats. Together, they created Japan's largest bank with ¥77 trillion in assets.

The integration was brutal. Two proud cultures, each over a century old, had to merge. Bank of Tokyo executives, who saw themselves as sophisticated internationalists, clashed with Mitsubishi's domestic-focused bureaucrats. IT systems didn't talk to each other. Customers received duplicate statements. Employee morale plummeted.

But the merged Bank of Tokyo-Mitsubishi (BTM) had one crucial advantage: scale. In a world where bad loans were measured in trillions, only the biggest could survive. BTM could absorb losses that would destroy smaller rivals. It could invest in technology when others were cutting costs. Most importantly, it could wait—that patient capital approach—for recovery.

Meanwhile, Sanwa and Tokai were struggling. Sanwa, despite its Osaka swagger, was bleeding from bad loans to small businesses. Tokai, concentrated in manufacturing-heavy Nagoya, watched its clients relocate production to China. Both needed partners. Both found salvation in Toyo Trust, creating UFJ Holdings in 2001—a three-way merger born of desperation rather than strategy.

By 2000, Japan's banking landscape was unrecognizable. The 20 major banks of 1990 had consolidated into seven mega-banks. The survivors weren't necessarily the best managed—they were the biggest, the ones with enough scale to absorb the losses and enough patience to wait for recovery.

The crisis years taught Japanese banks hard lessons. Real estate wasn't always a safe asset. Government protection had limits. Size mattered more than relationships. These lessons would prove invaluable when the next opportunity for consolidation arose—this time not from crisis but from scandal.

IV. The Mega-Merger: Birth of MUFG (2004-2005)

June 2004. The boardroom at UFJ Holdings headquarters in Osaka feels like a war room. The bank's executives know they're running out of time. UFJ had been accused by the government of corruption and making bad loans to the yakuza crime syndicates. The Financial Services Agency is circling. Bad debt ratios are spiraling. And now, two of Japan's banking giants are preparing to fight over their carcass.

In July 2004, UFJ Holdings, by then Japan's fourth-largest financial group, offered to merge with the Mitsubishi Tokyo Financial Group. It wasn't really an offer—it was a surrender. UFJ's management knew they needed a lifeline, and MTFG, the product of the 1996 Bank of Tokyo-Mitsubishi merger, had the cleanest balance sheet among Japan's mega-banks.

But here's where the drama explodes. The takeover of UFJ by the Mitsubishi Tokyo Financial Group was challenged by the Sumitomo Mitsui Financial Group which launched a competing takeover bid. SMFG's president, Yoshifumi Nishikawa, wasn't about to let his rival walk away with UFJ's 40 million retail accounts and deep corporate relationships, especially with Toyota—Japan's crown jewel corporation.

What followed was unprecedented in Japanese banking: a hostile takeover battle, complete with lawsuits, leaked documents, and government pressure. SMFG offered more money. MTFG offered certainty. UFJ's board was literally torn apart, with different factions backing different suitors. The press called it the "Battle for UFJ"—Japan's banking establishment watching in horror as their gentlemen's club turned into a street fight.

The courts got involved. Injunctions flew. At one point, UFJ executives were literally hiding documents from SMFG's due diligence team while secretly negotiating with MTFG. The Financial Services Agency, supposedly neutral, was clearly pushing for the MTFG deal—they wanted stability, not a bidding war.

MTFG ultimately prevailed in the fight, which appeared to signal an end to the clubby atmosphere that had prevailed in Japan's postwar banking industry. The victory came down to execution speed and regulatory backing. While SMFG was still arguing in court, MTFG was already integrating systems and preparing staff transfers.

The merged holding company MUFG was created in 2005 by merger between Mitsubishi Tokyo Financial Group and UFJ Holdings. On October 1, 2005, the holding company was officially formed. Three months later, on January 1, 2006, the two banks themselves—Bank of Tokyo-Mitsubishi and UFJ Bank—merged to form MUFG Bank.

The numbers were staggering. The combined entity held ¥190 trillion in assets, making it one of the world's largest banks overnight. But numbers don't capture the integration nightmare that followed. UFJ's systems were a disaster—multiple legacy platforms from Sanwa, Tokai, and Toyo Trust that barely talked to each other. MTFG's systems weren't much better—still running separate platforms from the old Bank of Tokyo and Mitsubishi Bank.

The cultural integration was even worse. UFJ employees, demoralized from years of crisis and the humiliation of being "rescued," faced off against MTFG staff who saw themselves as conquering heroes. The Osaka-Tokyo divide was real—UFJ's Osaka headquarters culture of merchant banking clashed with MTFG's Tokyo establishment mindset.

But Nobuo Kuroyanagi, MTFG's president who became MUFG's first CEO, understood something crucial: this wasn't just about creating Japan's biggest bank. It was about creating a global champion. The domestic market was saturated. Demographics were terrible. The real opportunity was using this scale to expand internationally.

The genius of the merger wasn't in the cost synergies—though they eventually reached ¥150 billion annually. It was in the strategic optionality it created. MUFG now had the balance sheet to make big international bets. It had relationships with virtually every major Japanese corporation, providing stable fee income. Most importantly, it had the capital buffer to survive another crisis.

MUFG and SMFG eventually settled the legal dispute for 2.5 billion yen in late 2006. A token payment that let everyone save face. But the real victory was already clear. MUFG had emerged as Japan's undisputed banking champion, with the scale and ambition to compete globally.

The timing, in retrospect, was perfect. The merger was completed just as global markets were heating up. Investment banking fees were soaring. Cross-border M&A was exploding. And in three years, when the financial crisis struck, MUFG would have the war chest to make the deal of the century.

V. The Morgan Stanley Gambit: Financial Crisis Opportunity (2008)

September 21, 2008. Morgan Stanley CEO John Mack is running on fumes. He hasn't slept in 72 hours. Lehman Brothers collapsed a week ago. AIG was just nationalized. Morgan Stanley's stock has fallen 42% in five days. The credit default swaps on his firm are pricing in bankruptcy. In his Times Square office, Mack is working the phones, desperate for capital. He's already called sovereign wealth funds in China, Qatar, Abu Dhabi. They all want to wait, to see if Morgan Stanley survives the week.

Then the phone rings. It's Tokyo.

On the other end is Nobuo Kuroyanagi, MUFG's president. Through a translator, he delivers a message that will save Morgan Stanley: "We are prepared to invest. How much do you need?"

The speed of what happened next defied every stereotype about cautious Japanese decision-making. On 29 September 2008, Mitsubishi UFJ Financial Group announced that it would acquire a shareholding in Morgan Stanley for US$9 billion. This wasn't some drawn-out negotiation with months of due diligence. This was crisis investing at its most audacious—MUFG had less than a week to analyze Morgan Stanley's books, assess the risk, and commit nearly $10 billion.

Why would a conservative Japanese bank bet so big on a Wall Street firm that might not exist by Monday? The answer reveals everything about MUFG's strategic genius.

First, timing. MUFG's leadership understood they were buying at the absolute bottom. Morgan Stanley's market cap had fallen from $87 billion to under $20 billion. This was like buying a Lamborghini at a garage sale—if you had the nerve and the cash.

Second, access. MUFG had tried for decades to build a global investment banking presence organically. It hadn't worked. Cultural differences, compensation gaps, and lack of brand recognition made it impossible to compete with the Wall Street giants. But owning 21% of Morgan Stanley? That changed everything. Suddenly, MUFG had access to the world's most sophisticated financial engineering, the deepest capital markets relationships, and a brand that opened doors from Silicon Valley to Saudi Arabia.

Third, relationships. This is where the Japanese approach shined. While other potential investors wanted to extract maximum value from Morgan Stanley's distress—demanding board seats, veto rights, preferential terms—MUFG took a different approach. They offered patient capital with minimal strings attached. They weren't trying to control Morgan Stanley; they wanted to be partners.

The negotiation itself was cinematic. Kuroyanagi flew to New York on September 22. While lawyers haggled over terms, the markets were melting down in real-time. Morgan Stanley's stock fell another 20% during the negotiations. Short sellers were circling. CNBC was practically writing the obituary.

But MUFG didn't blink. They had done their homework. Katsunori Nagayasu, MUFG's chief strategist, had been studying Morgan Stanley for years. He knew their prime brokerage business was solid. Their wealth management was growing. The investment banking franchise, while damaged, was salvageable. Most importantly, he understood that in financial crises, the strong don't just survive—they feast on the weak.

The structure of the deal was elegant. MUFG would buy $9 billion of convertible preferred stock with a 10% dividend. If Morgan Stanley recovered, MUFG could convert to common equity and share in the upside. If things went badly, they'd get paid first. It was heads-I-win, tails-I-don't-lose-much.

The regulatory approval process was insane. Normally, getting U.S. approval for a major foreign investment in a systemic bank takes months. MUFG got it in days. The Federal Reserve, desperate to prevent another Lehman, fast-tracked everything. Japanese regulators, usually obsessed with risk, signed off immediately. Everyone understood: Morgan Stanley's survival was at stake.

On October 13, 2008, the wire transfer went through. Nine billion dollars flowed from Tokyo to New York. Morgan Stanley was saved. The short sellers retreated. The credit markets unfroze, at least for Morgan Stanley.

But here's what made this truly genius: MUFG didn't just save Morgan Stanley—they bought a transformation. Over the next decade, this investment would give MUFG:

- Access to every major M&A deal involving Japanese companies

- The ability to offer global equity and debt underwriting to their corporate clients

- Trading capabilities that generated billions in revenue

- A wealth management platform for ultra-high-net-worth Asian clients

- Technology and risk management systems light-years ahead of Japanese peers

The cultural integration was fascinating. Unlike the forced marriage of MTFG and UFJ, this was a partnership of equals—or at least, that's how MUFG played it. They didn't flood Morgan Stanley with Japanese executives. They didn't demand strategy changes. They acted like the ultimate strategic investor: supportive, patient, valuable.

By 2011, MUFG had converted their preferred shares to common equity, becoming Morgan Stanley's largest shareholder. The investment, made at the depths of the crisis, had already doubled in value. But the real value wasn't financial—it was strategic. MUFG now had something no other Japanese bank possessed: a seat at the global finance table.

The Morgan Stanley gambit transformed MUFG from a large Japanese bank into a global financial institution. It proved they could move fast when opportunity struck. It showed they understood the value of relationships over control. Most importantly, it demonstrated that patient capital, deployed at the right moment, could achieve what decades of organic growth couldn't.

The lesson was clear: in crisis, there is opportunity—if you have the capital, the courage, and the conviction to act.

VI. U.S. Regional Banking: The Union Bank Journey (1990s-2022)

California, 1988. Bank of Tokyo's San Francisco headquarters buzzes with activity. Japanese corporations are flooding into America, buying everything from Pebble Beach to Columbia Pictures. They need a bank that understands both sides of the Pacific. Bank of Tokyo's California subsidiary is perfectly positioned—except it's too small.

The story of MUFG's American retail banking adventure is really three stories: aggressive expansion, patient building, and strategic retreat. Each phase reveals something essential about how global banks navigate foreign markets.

Mitsubishi Bank and the Bank of Tokyo each had significant banking subsidiaries in California before their 1996 merger. These weren't random acquisitions—California was the beachhead for Japanese corporate expansion into America. Every Toyota factory, every Sony studio, every Mitsubishi real estate deal needed banking services. California, with its Pacific orientation and large Japanese-American population, was the natural base.

At the time of the merger, these U.S. banks also merged to form UnionBanCal Corporation. BTM listed UnionBanCal on the New York Stock Exchange in 1999, signaling ambitions beyond just serving Japanese corporates. The bank wanted to be a real American player.

In 2008, BTMU purchased all of the outstanding shares of UnionBanCal, taking it private. The timing seemed odd—middle of the financial crisis—but MUFG saw opportunity where others saw disaster. American banks were retrenching. Competitors were failing. MUFG could grab market share while others retreated.

The rebranding to MUFG Union Bank in 2014 signaled a new phase. BTMU moved its New York-based banking operations to Union Bank, consolidating its entire U.S. commercial banking platform. This wasn't just a California bank anymore—it was MUFG's American franchise, with branches from San Diego to Seattle, commercial lending offices across the country, and ambitions to become a top-10 U.S. bank.

But here's where the story gets interesting. By 2020, MUFG Union Bank had grown to nearly 400 branches and $130 billion in assets. It was California's fifth-largest bank. The retail franchise was profitable. Corporate banking was thriving. So why sell?

The answer reveals the brutal economics of modern banking. "Given MUB's current business environment, including the need for increased technology investments as part of digital transformation, a certain scale is required to maintain and strengthen competitiveness," MUFG explained. Translation: in the age of mobile banking and AI, you need massive scale to compete. Being the fifth-largest bank in California wasn't enough when JPMorgan and Bank of America were spending billions on technology.

The negotiation with U.S. Bancorp was masterful. MUFG agreed with U.S. Bancorp to the sale of all shares in MUFG Union Bank for $5.5 billion in cash and approximately 44 million shares of U.S. Bancorp common stock. But the structure was even cleverer than the headline suggests. MUFG would receive an additional $3.5 billion in cash within five years of closing, bringing the total consideration to nearly $9 billion plus the equity stake.

The Share Transfer was completed on December 1, 2022. At transaction close, MUFG holds a minority stake of approximately 3% in U.S. Bancorp.

The strategic logic was brilliant. Instead of fighting an expensive war for U.S. retail market share, MUFG would: - Exit capital-intensive retail banking - Keep its profitable corporate and investment banking operations - Maintain exposure to U.S. banking through the U.S. Bancorp stake - Redeploy capital to higher-growth Asian markets

The numbers validated the strategy. The sale freed up roughly $8 billion in capital. The ongoing U.S. corporate banking business, freed from retail overhead, became more profitable. The U.S. Bancorp stake provided continued exposure to American retail banking without the operational headaches.

But the real genius was the timing. MUFG sold at the top—before rising rates crushed regional bank valuations, before the 2023 banking crisis that claimed Silicon Valley Bank and First Republic. They got out while the getting was good.

The Union Bank journey teaches a crucial lesson: knowing when to exit is as important as knowing when to enter. MUFG spent three decades building a major U.S. retail presence. They invested billions. They acquired, integrated, expanded. And then, at precisely the right moment, they pivoted.

The sale wasn't retreat—it was strategic reallocation. The transaction allowed MUFG to shift its focus to its retail banking business in Japan and Asia, while continuing to focus on its wholesale corporate and investment banking franchise in the United States. MUFG kept what worked—corporate banking, investment banking via Morgan Stanley—and jettisoned what didn't—subscale retail banking.

Today, MUFG's U.S. presence is leaner but more profitable. They serve Japanese and American corporations. They participate in every major capital markets transaction through Morgan Stanley. They maintain a stake in U.S. Bancorp. But they're not trying to compete with JPMorgan for checking accounts in Fresno.

The Union Bank story is really about strategic clarity. MUFG understood that in banking, as in war, you can't fight on every front. You pick your battles, concentrate your forces, and sometimes the smartest move is strategic withdrawal. The $9 billion they extracted from U.S. Bancorp is now funding expansion in Indonesia, Thailand, India—markets where MUFG can achieve real scale and generate superior returns.

The lesson for global banks is stark: in the digital age, regional scale isn't enough. You need to be either truly local or truly global. Anything in between is a recipe for mediocrity. MUFG chose global for investment banking and local for Asian commercial banking. The Union Bank sale was just the logical conclusion of that choice.

VII. Asian Expansion & Digital Transformation (2012–Present)

Bangkok, December 2013. The executives at Bank of Ayudhya (Krungsri) are about to sign papers that will transform Southeast Asian banking. MUFG Bank is making Krungsri a consolidated subsidiary in December 2013, in what would become MUFG's takeover valued at US$5.17 billion (Bt167 billion), the largest banking takeover in Thailand and also the largest Asian acquisition by a Japanese bank.

This wasn't just another acquisition—it was the opening move in MUFG's master plan to build an Asian commercial banking empire. Starting seriously around 2012-2013 with major acquisitions like Krungsri in Thailand and later Bank Danamon in Indonesia, MUFG executed a deliberate strategy to build a strong commercial banking network across Southeast Asia.

The logic was compelling. Japan's population was shrinking. Interest rates were negative. Corporate loan demand was anemic. Meanwhile, Southeast Asia offered everything Japan lacked: young populations, growing middle classes, expanding economies, and interest rates that actually generated profits. MUFG didn't just want to lend to Japanese companies operating in Asia—they wanted to become a true Asian bank.

Krungsri was the perfect platform. Krungsri is the fifth largest financial group in Thailand in terms of assets, loans, and deposits, and one of Thailand's five Domestic Systemically Important Banks (D-SIBs). It had 76 years of history, deep local relationships, and most importantly, a management team that understood both retail and corporate banking in an emerging market.

The integration was remarkably smooth. Unlike the forced marriages in Japan, MUFG treated Krungsri as a partner, not a conquest. MUFG has no plan to buy more shares in the Thai bank on top of the 72-per-cent stake it already owns, respecting the founding Ratanarak family's continued involvement.

The results spoke for themselves. The Thai bank last year contributed 26 per cent of the group's operating profit—an extraordinary return on investment. Krungsri became MUFG's laboratory for Southeast Asian expansion, testing everything from digital payments to microfinance.

Indonesia came next. In December 2017, Japan's Mitsubishi UFJ Financial Group (MUFG) bought a 19.9% stake in Danamon from Temasek Holdings for Rp 15.875 trillion ($1.17 billion). The acquisition unfolded in stages—first 19.9%, then 40%, and finally, through a complex merger with Bank Nusantara Parahyangan in 2019, MUFG Bank holds 9,196,854,799 ordinary shares of Bank Danamon, which is equivalent to a 94.1% stake.

Bank Danamon brought something different: Indonesia's 270 million population, the world's largest Muslim market, and an economy growing at 5% annually. It is the sixth largest bank in Indonesia by asset size, with particular strength in auto financing and SME lending—exactly the segments driving Indonesian growth.

But MUFG's Asian strategy went beyond just buying banks. They're building an ecosystem. In 2020, MUFG Bank signed a strategic partnership agreement with Grab, Southeast Asia's super app, integrating financial services into ride-hailing, food delivery, and e-commerce. This wasn't traditional banking—it was embedding finance into daily life. The India push accelerated dramatically. In August 2024, MUFG announced an additional investment of INR 27,988 million (approximately JPY 49 billion) in DMI Finance — a digital financial services business in India. The new capital injection brings MUFG's total investment in DMI Finance to $565 million. DMI wasn't a traditional bank—it was a digital-first lender using AI and alternative data to serve India's vast unbanked population. The company has established a unique business model in India's digital lending industry and has provided its services to a cumulative total of 15.2 million customers (as of March 2024)

The Philippines opportunity materialized in 2024 with a $393 million investment from MUFG Bank in Mynt (Globe Fintech Innovations), operator of GCash, the country's dominant mobile wallet. With 94 million users—nearly the entire adult population—GCash represents the future of banking in emerging markets: no branches, no legacy systems, just smartphones and digital payments.

MUFG's venture capital approach reveals sophisticated thinking about Asian finance. The MUFG Ganesha Fund, launched in March 2022 with a total investment limit of $300 million for India, targets fintech startups disrupting traditional banking. Indonesia's Garuda Fund follows the same playbook. These aren't passive investments—they're strategic bets on the digitization of Asian finance.

The numbers tell a compelling story. MUFG's Asian operations outside Japan now generate over 40% of group profits. Krungsri alone contributes more to earnings than most Japanese regional banks. The Indonesian franchise is growing at 15% annually. The Indian investments, while early-stage, show explosive user growth.

But the real transformation is philosophical. MUFG isn't trying to export Japanese banking to Asia—they're learning from Asia. Krungsri's digital wallet competes with Bangkok's street vendors. Bank Danamon's Sharia-compliant products serve Indonesia's Muslim majority. DMI Finance uses satellite imagery to assess creditworthiness of Indian farmers. This is banking reimagined for emerging markets.

The contrast with the U.S. strategy is stark. In America, MUFG retreated from retail banking because they couldn't achieve scale. In Asia, they're building scale through local partnerships, digital platforms, and patient capital. The difference? Growth. Southeast Asia's GDP expands 5% annually. Digital payment volumes double every two years. The unbanked population—500 million people—represents pure opportunity.

VIII. Technology Revolution & AWS Partnership (2020s)

March 2023. MUFG's Tokyo headquarters announces something that would have been unthinkable five years ago: they're moving their core banking systems to the cloud. Not some peripheral applications—the actual ledgers that track trillions in assets. MUFG is accelerating its cloud-first strategy with AWS as its preferred cloud provider, betting the future of Japan's largest bank on Amazon's servers.

The transformation journey reveals how desperately traditional banks need to evolve. MUFG's IT infrastructure was a museum of computing history—mainframes from the 1980s, databases from the 1990s, middleware from the 2000s, all held together by custom code that only a handful of aging engineers understood. Running this Frankenstein's monster cost billions annually and made simple changes take months.

The AWS partnership isn't just about cost savings, though moving from on-premises data centers to AWS reduced the cost of operating standard IT infrastructure by 20%. The real value is agility. MUFG will use AWS technologies to inform data-driven business decisions, automate processes, and develop new digital financial products. What once took months now takes days. What required armies of engineers now needs small agile teams.

The artificial intelligence push is equally aggressive. MUFG's strategic investment in LayerX via MUFG Innovation Partners, acquiring a 5% stake in the AI SaaS startup, signals serious intent. LayerX isn't building chatbots—they're creating AI that reads contracts, detects fraud, and makes credit decisions. This is automation of core banking functions, not peripheral customer service.

Money Canvas, MUFG's digital asset management platform, shows what's possible when traditional banking meets modern technology. The platform serves 2.5 million customers, offering robo-advisory services that would have required thousands of human advisors. Customers get institutional-quality portfolio management for fees that are 80% lower than traditional wealth management.

But the crown jewel is MODE—MUFG Openly-connected Digital Ecosystem. This isn't just another banking app. It's an open platform where third-party developers can build financial services using MUFG's infrastructure. Imagine Spotify, but for banking—thousands of specialized financial apps all running on MUFG's rails.

The cultural transformation required for this technological revolution can't be overstated. MUFG hired thousands of engineers, data scientists, and product managers—not from other banks, but from tech companies. They created innovation labs in Tokyo, Singapore, and San Francisco. They started measuring success not by loan volumes but by API calls and user engagement metrics.

The partnership ecosystem is vast. Beyond AWS, MUFG works with Google on AI, Microsoft on productivity tools, and dozens of fintechs on specialized services. The bank that once built everything in-house now embraces "buy, partner, or build"—in that order.

The competitive dynamics are fascinating. While Western banks worry about fintech disruption, MUFG is becoming the disruptor. They're not defending against digital attackers—they're joining them. When a new payment app launches in Thailand, Krungsri doesn't compete; it offers banking-as-a-service infrastructure. When an Indian fintech needs a banking license, DMI Finance provides regulatory cover.

The results are already visible. Digital channels now account for 70% of retail transactions. Customer acquisition costs have fallen 60%. New product launches that took years now happen in months. Most remarkably, MUFG's Net Promoter Score—a measure of customer satisfaction—has risen 40 points, reaching levels typically associated with tech companies, not banks.

IX. Playbook: Strategic & Operating Lessons

The MUFG story offers a masterclass in global banking strategy. The patterns that emerge from 140 years of evolution reveal timeless principles for building and sustaining competitive advantage in finance.

The "Patient Capital" Approach

MUFG's greatest strength is its ability to wait. The Morgan Stanley investment took five years to turn profitable. The Krungsri acquisition needed seven years to become a profit engine. Bank Danamon is still building scale. This patience—rooted in Japanese corporate culture but elevated to strategic art—allows MUFG to make investments others can't justify to quarterly-focused shareholders.

The mathematics of patient capital are compelling. While Western banks demand 15% returns in three years, MUFG accepts 10% returns in seven years. This lower hurdle rate opens opportunities others must pass on. It's not about accepting lower returns—it's about capturing returns others can't wait for.

Crisis as Opportunity

Every major MUFG breakthrough came during crisis. The 1996 merger during Japan's banking crisis. The UFJ acquisition amid scandal. The Morgan Stanley investment during global financial meltdown. The Asian expansion while competitors retreated. This isn't luck—it's preparation meeting opportunity.

The crisis playbook is consistent: maintain strong capital buffers during good times, move aggressively when others are paralyzed, and focus on strategic value not short-term profits. While competitors hoard cash during downturns, MUFG deploys it.

The Conglomerate Advantage

In an era of specialization, MUFG's conglomerate structure seems anachronistic. But the breadth creates unique advantages. Corporate banking relationships feed investment banking mandates. Retail deposits fund wholesale lending. Asian operations hedge Japanese demographic decline. The diversification isn't just risk management—it's revenue synergy.

The cross-selling opportunity is enormous. A Japanese corporation expanding to Thailand needs corporate banking, investment banking, treasury services, and employee banking. MUFG provides all four. The lifetime value of these relationships, measured in decades not quarters, justifies investments that product-focused competitors can't make.

Build vs. Buy vs. Partner Evolution

MUFG's approach to capability building has evolved dramatically. The 1990s were about building—creating internal investment banking, developing proprietary systems. The 2000s were about buying—acquiring UFJ, investing in Morgan Stanley. The 2020s are about partnering—working with AWS, collaborating with fintechs.

This evolution reflects changing competitive dynamics. When technology was a differentiator, building made sense. When scale mattered most, buying was optimal. Now, when innovation speed is critical, partnering is essential. The willingness to abandon "not invented here" thinking distinguishes MUFG from peers still trying to build everything internally.

Managing Regulatory Complexity

Operating across Japan, the United States, Europe, and Asia means navigating dozens of regulatory regimes. MUFG's approach is sophisticated: over-comply in critical markets, meet minimums in peripheral ones, and use regulatory expertise as competitive advantage.

The Morgan Stanley structure is illustrative. By maintaining minority ownership, MUFG avoids full Federal Reserve oversight while gaining strategic benefits. The Asian subsidiaries operate under local regulations but benefit from MUFG's global risk management. It's regulatory arbitrage at its most elegant.

The Importance of Timing

Every major MUFG move demonstrates exquisite timing. They merged when Japanese banking needed consolidation. They bought Morgan Stanley equity at the bottom. They sold Union Bank at the top. They're expanding in Asia while demographics are favorable.

This timing isn't coincidence—it's systematic analysis of long-term trends combined with tactical flexibility. MUFG thinks in decades but acts in moments. They prepare for multiple scenarios then move decisively when conditions align.

X. Analysis & Bear vs. Bull Case

Bull Case: The Compounding Advantages

MUFG's bull case rests on structural advantages that compound over time. Start with Japan, where MUFG holds dominant positions in corporate banking, trust banking, and securities. The relationships with Japan's blue-chip corporations—Toyota, Sony, SoftBank—are essentially unbreakable. These companies need sophisticated financial services that only MUFG can provide comprehensively.

The demographic headwinds in Japan are real, but MUFG has already adapted. Wealth management for Japan's aging population is booming. The $1,700 trillion in Japanese household financial assets needs sophisticated management as it transfers between generations. MUFG's trust banking franchise is perfectly positioned for this wealth transfer tsunami.

The Morgan Stanley partnership keeps delivering value. Every major cross-border M&A deal involving Japanese companies flows through this partnership. The investment banking revenues are growing 15% annually. The wealth management synergies are just beginning. This isn't a passive investment—it's an active revenue generator worth multiples of the original investment.

Asian expansion is hitting inflection points. Krungsri's digital transformation makes it Thailand's most innovative bank. Bank Danamon is capturing Indonesia's consumption boom. The fintech investments provide exposure to exponential growth without the capital requirements of traditional banking. If Southeast Asian GDP grows 5% annually for the next decade—a conservative estimate—MUFG's Asian profits could triple.

The technology transformation is already paying dividends. Cloud migration will reduce IT costs by $500 million annually by 2025. Digital channels are cutting customer acquisition costs 70%. AI is reducing loan processing time 90%. These aren't one-time benefits—they compound as technology improves.

Bear Case: The Structural Headwinds

The bear case starts with Japan's inexorable decline. Population falling by 500,000 annually. GDP growth near zero. Interest rates negative or barely positive. No amount of financial engineering can overcome these physics. MUFG generates 60% of revenues in Japan—that's massive exposure to structural decline.

Competition from Chinese banks in Asia is intensifying. ICBC, China Construction Bank, and Bank of China have unlimited capital and political backing. They're willing to accept returns that don't cover cost of capital. In markets like Indonesia and Thailand, Chinese banks are buying market share with below-market pricing.

Technology disruption threatens every revenue stream. Payment companies are disintermediating transaction banking. Fintechs are unbundling lending. Crypto threatens cross-border payments. Big Tech has the customer relationships and balance sheets to obliterate traditional banking. MUFG's technology investments are impressive but may be too little, too late.

The complexity of managing global operations is overwhelming. Different regulations, currencies, cultures, and systems create massive inefficiencies. The cost-to-income ratio of 70% is far higher than pure-play digital competitors operating at 30%. This complexity tax is permanent—it's the price of being a global universal bank.

Rising interest rates globally could trigger another financial crisis. MUFG's loan book has duration risk. The securities portfolio has mark-to-market losses. Credit losses are at historical lows but could spike quickly. The next crisis won't look like 2008, and MUFG might not be as well-positioned.

XI. Epilogue & "What's Next"

The India opportunity represents MUFG's next frontier. Management is prioritizing expansion in India, targeting annual returns of 20%—ambitious but achievable given India's 7% GDP growth and financial inclusion revolution. With 1.4 billion people and only 30% banking penetration, India offers the scale opportunity that China once promised but geopolitical tensions now preclude.

The artificial intelligence revolution will fundamentally reshape banking in the next five years. MUFG's partnerships with AI startups position them well, but the real question is whether traditional banks can move fast enough. When AI can perform credit analysis, detect fraud, and manage portfolios better than humans, what's the value of a banking license? MUFG must transform from a financial intermediary to a technology platform that happens to have a banking license.

Climate finance presents both opportunity and obligation. MUFG has committed $184 billion to sustainable finance by 2030. But this isn't just virtue signaling—it's business strategy. The energy transition requires trillions in capital. Carbon markets are exploding. Green bonds are mainstream. MUFG's global reach and Japanese engineering relationships position them perfectly for this transition.

Competition with Chinese banks for Asian dominance will intensify. The battle won't be fought with traditional weapons—branches and loans—but with digital platforms and ecosystem strategies. MUFG's partnerships with Grab, GCash, and other super apps are defensive moats against Chinese digital expansion.

The future of the Morgan Stanley relationship remains fascinating. As Morgan Stanley's largest shareholder, MUFG has theoretical control but exercises partnership. This delicate balance—influence without interference—will be tested as both institutions evolve. The potential for deeper integration exists, but so does the risk of culture clash.

The next decade will determine whether MUFG becomes a truly global bank or retreats to Asian regional champion. The pieces are in place—dominant position in Japan, growing Asian franchise, Morgan Stanley partnership, digital transformation. But execution in banking is everything.

The fundamental question facing MUFG is existential: what is a bank in the 21st century? Is it a holder of deposits and maker of loans? A facilitator of payments? A provider of financial advice? A technology platform? MUFG's answer—that a bank is all of these and more—is ambitious. Whether it's achievable will determine not just MUFG's future, but the future of global banking itself.

Looking ahead, MUFG stands at an inflection point. The patient capital approach that built the empire must now compete with the speed of digital disruption. The relationship banking that defined Japanese finance must evolve for algorithmic decision-making. The conservative culture that survived countless crises must embrace radical innovation.

Yet MUFG has reinvented itself before. From samurai financiers to zaibatsu bankers, from post-war reconstruction to bubble-era excess, from domestic champion to global player—each transformation seemed impossible until it was inevitable. The next transformation—from traditional bank to digital-first financial ecosystem—may be the most challenging yet.

The stakes couldn't be higher. Success means MUFG becomes the bridge between Asian capital and global markets, the platform connecting traditional finance and digital innovation, the patient capital that funds the next century's growth. Failure means slow decline into irrelevance, another former giant disrupted by nimbler competitors.

But betting against MUFG has always been a losing proposition. They've survived world wars, financial crises, and technological revolutions. They've turned every crisis into opportunity, every challenge into competitive advantage. As the financial world enters another period of fundamental disruption, MUFG's 140-year history suggests they'll not just survive but thrive.

The story of Mitsubishi UFJ Financial Group is far from over. In fact, the most interesting chapters may be just beginning.

XII. Links & Resources

The MUFG story demands deep understanding across multiple disciplines—Japanese history, global finance, technological disruption, and cross-cultural management. The following resources provide essential context and continuing education for those seeking to understand this financial colossus.

Primary Sources

MUFG's investor relations portal remains the authoritative source for financial data, strategic presentations, and regulatory filings. The annual MUFG Report combines financial statements with strategic narrative, offering management's unfiltered perspective on challenges and opportunities. For those reading between the lines, the subtle shifts in language between reports reveal strategic pivots before they become headlines.

The Bank of Japan's Financial System Reports provide crucial context for understanding MUFG's operating environment. These semi-annual publications dissect Japan's financial stability, monetary policy transmission, and banking sector health with academic rigor and regulatory authority.

Morgan Stanley's investor materials offer the American perspective on the MUFG partnership. The contrast between how each institution describes their relationship illuminates cultural differences in corporate communication and strategic emphasis.

Academic Literature

Richard Werner's "Princes of the Yen" remains the definitive account of Japanese banking's post-war evolution. His analysis of window guidance, credit creation, and the mechanics of Japan's bubble economy provides essential historical context for understanding MUFG's DNA.

Ulrike Schaede's "The Business Reinvention of Japan" examines how Japanese corporations, including mega-banks, are transforming for the digital age. Her framework for understanding Japan's "choose and focus" strategies directly applies to MUFG's portfolio decisions.

For those seeking to understand the technical aspects of international banking, "The Future of Large, Internationally Active Banks" edited by Asli Demirgüç-Kunt provides frameworks for analyzing institutions like MUFG that span multiple jurisdictions and business lines.

Historical Context

John Dower's "Embracing Defeat" brilliantly captures the post-war transformation that created modern Japanese banking. Understanding the psychological and institutional changes of the occupation period is essential for grasping why Japanese banks operate so differently from Western peers.

Gillian Tett's "Saving the Sun" chronicles the collapse and nationalization of Long-Term Credit Bank of Japan, offering a cautionary tale that influenced every major Japanese bank's risk management philosophy, including MUFG's conservative approach to international expansion.

Digital Transformation Resources

McKinsey's series on "The Future of Banking in Asia" provides ongoing analysis of digital disruption in MUFG's growth markets. Their quarterly updates track fintech funding, regulatory changes, and competitive dynamics across Southeast Asian markets.

The Monetary Authority of Singapore's fintech publications offer sophisticated analysis of digital banking evolution in MUFG's key expansion markets. Their research on embedded finance and platform economics directly relates to MUFG's partnership strategies with Grab and GCash.

Regulatory and Policy Documents

The Financial Services Agency of Japan's annual supervisory policies outline regulatory expectations for Japanese mega-banks. Reading these documents reveals upcoming compliance requirements and strategic constraints that will shape MUFG's decisions.

The Basel Committee's publications on international banking supervision provide the global regulatory framework within which MUFG operates. Understanding Basel III's evolution toward Basel IV is essential for projecting MUFG's capital allocation decisions.

Industry Analysis

S&P Global's banking industry reports offer comparative analysis of global banks, placing MUFG's performance in international context. Their credit rating methodologies explain why MUFG maintains its A1/A ratings despite Japan's challenging demographics.

The Asian Banker's research provides granular analysis of retail and commercial banking across Asia. Their country-specific reports illuminate the competitive dynamics MUFG faces in each market, from Thailand's digital banking revolution to Indonesia's Islamic finance growth.

Continuing Coverage

The Nikkei Asian Review provides daily coverage of MUFG and Japanese finance with unmatched access to management thinking. Their Japanese-language edition often breaks news days before English translation, rewarding those who invest in language skills.

The Financial Times' Lex column regularly analyzes MUFG's strategic moves with characteristic skepticism and insight. Their archived analyses of the Morgan Stanley investment and Union Bank sale provide real-time documentation of market sentiment evolution.

Bloomberg's terminal functions, while expensive, offer unparalleled data on MUFG's securities, derivatives, and loan portfolios. The ALLQ function alone provides more information about MUFG's funding structure than most annual reports.

Books for Deeper Understanding

"Zaibatsu: The Rise and Fall of Family Enterprise Groups in Japan" by Hidemasa Morikawa explains the organizational DNA that still influences MUFG's corporate culture and strategic thinking.

"Japan's Financial Crisis" by Takeo Hoshi and Anil Kashyap provides the definitive economic analysis of the bubble and bust that forged modern MUFG through crisis and consolidation.

"The House of Morgan" by Ron Chernow offers essential background on MUFG's most important international partner, illuminating why the cultures mesh despite their apparent differences.

These resources represent starting points for understanding MUFG's complexity. The institution's story spans centuries, continents, and cultures—no single source captures it all. But for those willing to dig deep, the intellectual rewards match the institution's own patient, comprehensive approach to global finance.

XIII. Recent News

MUFG's financial momentum continues into late 2024, with the bank announcing on November 14, 2024, its financial results for the interim of fiscal year ending March 31, 2025, alongside a notice regarding repurchase and cancellation of common stock and revised earnings targets and dividend forecasts. The consistent flow of strategic announcements demonstrates management's confidence in executing their transformation agenda while returning capital to shareholders.

MUFG reported strong financial performance for the first three quarters of the fiscal year ending in March 2025, highlighting record-high net operating profits (NOP) and net income, driven by robust customer segment growth, gains from equity sales, and increased earnings from equity method investments. The earnings release also addresses the impact of a recent JPY interest rate hike and provides a glimpse into expected performance for the remainder of the fiscal year. Key drivers include successful overseas acquisitions, improved net interest margins, growth in fee-based businesses, and the accounting impacts of changes at Morgan Stanley (MS) and Krungsri (KS). Record-High Net Operating Profits (NOP): MUFG achieved a record-high NOP of ¥1,714.6 billion, a ¥194.4 billion increase year-over-year (YoY).

For the nine months ending December 31, 2024, MUFG's ordinary income increased by 20.8% to 10,277,584 million yen, and profits attributable to owners of the parent rose by 34.7% to 1,748,939 million yen compared to the same period in the previous fiscal year. MUFG's financial health also showed stability with total assets amounting to 413,193,210 million yen and total net assets at 21,622,461 million yen as of December 31, 2024.

The transformation of MUFG's earnings quality deserves particular attention. Return on Equity (ROE) has increased significantly to 12.3% on a MUFG basis, surpassing their internal target of 9%. Customer segments saw a significant boost of ¥430.2 billion in NOP. Specific segments like Commercial Banking & Wealth Management (CWM), Japanese Corporate & Investment Banking (JCIB), and Global Commercial Banking (GCB) showed strong year-over-year growth. This ROE expansion while maintaining conservative risk parameters demonstrates that MUFG's digital investments and portfolio optimization are bearing fruit.

The earnings per share for the nine-month period stood at 149.85 yen, marking a substantial increase from the 108.04 yen reported at the end of December 2023. Additionally, MUFG declared a second-quarter-end dividend of 25.00 yen per share and forecasts a year-end dividend of 35.00 yen, resulting in an annual dividend of 60.00 yen per share for the fiscal year ending March 31. MUFG maintains its earnings target of 1,750.0 billion yen of profits attributable to owners of the parent for the fiscal year ending March 31, 2025.

Strategic partnerships continue to evolve. In July 2024, MUFG Bank signed a Memorandum of Understanding with the Eastern Economic Corridor Office of Thailand, deepening its commitment to Southeast Asian infrastructure development. This aligns with Thailand's ambitions to become a regional manufacturing and logistics hub, where MUFG's Krungsri subsidiary can provide crucial financial infrastructure.

The digital transformation agenda accelerates with concrete results. The announcement regarding WealthNavi Inc., where MUFG Bank commenced a tender offer, signals the bank's push into digital wealth management—a critical battleground for capturing Japan's massive retirement savings wave.

On the regulatory front, MUFG received a Financial Services Agency order to submit reports in December 2024, a reminder that even Japan's largest bank faces ongoing supervisory scrutiny as it expands globally and digitizes operations. The FSA's increased focus on operational risk management reflects concerns about cyber security and system stability as banks migrate to cloud infrastructure.

Climate finance commitments materialized into concrete action. The October 2024 announcement regarding the Net-Zero Banking Alliance's supporting note on target setting for capital markets activities positions MUFG at the forefront of sustainable finance in Asia, where the energy transition requires trillions in investment over the coming decades.

Looking ahead, In November 2024, MUFG announced a strategic plan that included an agreement with KDDI Corporation pursuant to which MUFG Bank will acquire 49% of the shares of au Kabucom Securities Co., Ltd., demonstrating continued focus on building digital financial ecosystems through strategic partnerships rather than costly organic development.

The most recent financial performance validates MUFG's strategic pivots. NOP represents 87% progress towards their fiscal year target. The earnings release paints a highly positive picture of MUFG's current financial health and future outlook. MUFG's strategy of growth in customer segments, strategic equity sales, and the positive impact of a JPY interest rate hike are clearly paying off.

These developments collectively paint a picture of a bank successfully navigating multiple transformations simultaneously—geographic rebalancing toward Asia, digital modernization, sustainable finance leadership, and shareholder value creation—while maintaining the conservative risk management that has defined MUFG for over a century. The strong financial performance provides the resources and credibility to accelerate these strategic initiatives, creating a virtuous cycle of transformation and value creation.

The story of Mitsubishi UFJ Financial Group is ultimately a story about adaptation. From financing Japan's industrialization to enabling Asia's digital revolution, from surviving domestic crisis to seizing global opportunity, MUFG has consistently transformed challenge into advantage. Today, as the financial world faces another inflection point—where artificial intelligence meets traditional banking, where climate change demands capital reallocation, where geopolitical tensions reshape global flows—MUFG's patient capital approach and relationship-based philosophy offer both ballast and sail.

The bank that began by financing silk exports now finances silicon chips. The institution that survived the zaibatsu dissolution now thrives as a global conglomerate. The conservative lender that weathered Japan's bubble now makes bold bets on emerging market fintechs. Each transformation seemed impossible until it became inevitable.

As MUFG approaches its second century and a half, the fundamental question isn't whether it will survive—history suggests it will—but what form that survival will take. Will MUFG become the bridge between traditional finance and digital innovation? Will it successfully navigate the transition from Japanese demographic decline to Asian demographic dividend? Will patient capital prove more valuable than algorithmic trading in an age of artificial intelligence?

The answers will emerge over time, written in quarterly earnings and strategic pivots, in successful acquisitions and timely exits. But if history is any guide, MUFG will not just adapt to the future—it will help finance and shape it, one patient investment at a time.

The global financial landscape is shifting beneath MUFG's feet. Central banks worldwide are normalizing monetary policy after years of ultra-loose conditions. Digital currencies threaten traditional payment systems. Climate change demands massive capital reallocation. In this environment, MUFG's strategic choices over the next five years will determine whether it remains relevant in global finance or becomes another legacy institution disrupted by technological change.

The Strategic Imperative

The mathematics of MUFG's future are stark. Japan's working-age population will decline by 20% over the next two decades. Domestic loan demand remains anemic despite recent rate increases. Meanwhile, Southeast Asia's GDP will double by 2040, India will become the world's third-largest economy, and digital finance will capture trillions in value creation. The strategic imperative is clear: succeed in Asia and digital transformation, or face irreversible decline.

Management understands this urgency. According to Yasushi Itagaki, head of Mitsubishi UFJ's global commercial banking business, MUFG's goal is to increase its investments and acquisitions in India and boost its annual returns from them to 20% over the next 10 years. Itagaki is leading MUFG's growth strategy in Asia, prioritizing expansion in India and the enhancement of digital operations across the Asia-Pacific (APAC) region, as these areas are crucial for driving higher profits for the company.

The "Mickey Mouse model" provides an elegant framework for understanding MUFG's strategy, where the face symbolizes MUFG's global banking operations, aiming for a 15% return on equity over the next 10 years. The ears represent India and its digital initiatives, both targeting annual returns of 20%. This visual metaphor captures the balanced approach—maintaining the core while pursuing aggressive growth in new frontiers.

The China Question

The elephant in every Asian boardroom is China. MUFG's minimal direct exposure to China—a deliberate strategic choice—looks prescient given geopolitical tensions and regulatory crackdowns. But avoiding China while competing with Chinese banks across Asia requires extraordinary execution. Chinese banks offer below-market pricing, unlimited capital, and political backing. MUFG counters with relationships, risk management, and technological sophistication.

The competition plays out daily in infrastructure finance across Southeast Asia. When Indonesia needs funding for a new port or Thailand requires capital for renewable energy, Chinese banks offer packages that include construction companies, technology transfer, and government support. MUFG offers transparency, environmental standards, and connection to global capital markets. Different clients value different offerings, creating a bifurcated market where MUFG must pick its battles carefully.

Regulatory Evolution

MUFG's Medium-term Business Plan (MTBP) starting from the 2024 fiscal year established seven strategies dedicated to pursuing "growth," one of which is the "evolution of an integrated GCIB/Global Markets business model." Based on MUFG's integration strategy, the GCIB Business Unit and the Global Markets Business Unit have promoted integrated operations between the overseas securities entities and MUFG Bank. However, to address the diverse challenges and needs of clients within international wholesale business, they consider it essential to transcend the traditional boundaries of banking and securities operations to allow for more integrated group-wide decisions swiftly, allocation of resources flexibly and efficiently and establishment of a platform for further advancement in business-support frameworks.

The reorganization of overseas securities entities represents this strategic evolution. At present, the business of the overseas securities subsidiaries, including MUFG Securities Americas Inc., which is already a subsidiary of MUFG Bank, is managed by MUSHD based on its expertise. With the group reorganization, the capital relationships and management framework of the overseas securities subsidiaries will be integrated under the Bank.

This structural optimization enables faster decision-making and better resource allocation across global markets. The integration of banking and securities operations—long separated by regulatory requirements—creates synergies in everything from risk management to client coverage.

Climate Finance Leadership

MUFG's environmental commitments have scaled dramatically. The new framework follows the release by MUFG earlier this year of its Medium-term Business Plan (MTBP) for the next three year period, which established the bank's efforts to drive social and environmental progress as one of its 3 key pillars. Alongside the MTBP, MUFG also announced that it was nearly tripling its 2030 sustainable finance goal to 100 trillion yen (USD$703 billion) from its prior 35 trillion yen target, including 50 trillion targeting environmental issues, based on an anticipated increase in demand.

Progress toward these ambitious targets is already substantial. In its 2024 Climate Report, MUFG revealed that it had reached 28 trillion in towards its goal as of the end of 2023. This isn't greenwashing—it's strategic positioning for the energy transition that will define the next century.

MUFG's Carbon Neutrality Declaration, a commitment to achieve net zero emissions in our finance portfolio by 2050 and our own operations by 2030, was announced in May 2021. MUFG joined NZBA in June 2021 after announcing the Carbon Neutrality Declaration. The commitment to net-zero financed emissions by 2050 fundamentally changes how MUFG evaluates credit risk, prices loans, and allocates capital.

The renewable energy financing opportunity in Asia is enormous. MUFG was again recognized as one of the top ten global Lead Arrangers in financing clean-energy in 2023, ranking #2 in the BloombergNEF 2H 2023 Clean Energy League Table. Our bank enabled the development and acquisition of renewable assets through 64 transactions, totaling an amount of $3.7 billion. These transactions took the form of construction loans, acquisition facilities, and refinancings as an underwriter and syndicator to other financial institutions.

Technology as Competitive Advantage

The technology transformation extends beyond cloud migration and digital channels. In May 2024, Link Group announced that its acquisition by Mitsubishi UFJ Trust & Banking Corporation (the Trust Bank), a subsidiary of Mitsubishi UFJ Financial Group, Inc (MUFG) has been successfully implemented. The acquisition, conducted via a scheme of arrangement, marks a significant milestone for the organisation, and sets the stage for a transformative journey forward.

Under its new ownership, Link Group will be rebranded as MUFG Pension & Market Services, comprising two market leading businesses, MUFG Corporate Markets and MUFG Retirement Solutions. The acquisition values Link Group equity at $1.2 billion and implies an enterprise value of $2.1 billion. This acquisition brings critical pension administration and corporate markets infrastructure that would have taken decades to build organically.

The WealthNavi tender offer announced in November 2024 signals MUFG's push into digital wealth management. WealthNavi's robo-advisory platform serves Japan's growing cohort of digital-native investors who demand low fees, transparency, and mobile-first experiences. Integrating WealthNavi's technology with MUFG's trust banking expertise creates a formidable wealth management platform for Japan's generational wealth transfer.

Human Capital Transformation

MUFG's transformation requires different talent. Like HSBC and DBSDY, MUFG also has its back-office business set up in India, providing support services for its global operations. Established in 2020, this unit currently employs approximately 1,500 staff. As part of its expansion plan in India, Itagaki also intends to double the workforce within the next three years.

This isn't just cost arbitrage—it's accessing India's deep pool of technology talent. The Indian operations handle everything from AI development to risk modeling, becoming MUFG's innovation engine rather than just a cost center.

Risk Management in a Volatile World

The risk landscape facing MUFG has never been more complex. Geopolitical tensions between the U.S. and China force constant navigation between competing regulatory regimes. Climate change creates both physical risks to loan portfolios and transition risks as carbon-intensive industries decline. Cyber threats escalate as digital transformation expands attack surfaces.

MUFG's response combines traditional Japanese conservatism with sophisticated risk modeling. The bank maintains capital ratios well above regulatory minimums, providing buffers against unexpected shocks. Stress testing incorporates extreme scenarios—simultaneous property crashes in multiple Asian markets, complete severance of U.S.-China financial flows, massive cyber attacks on payment systems.

The conservative approach proved valuable during recent banking turmoil. While Silicon Valley Bank and Credit Suisse collapsed from poor risk management, MUFG's fortress balance sheet never wavered. The ability to act as a source of strength during crisis—as demonstrated with Morgan Stanley in 2008—remains a competitive advantage.

The Competitive Landscape

MUFG faces competition on multiple fronts. In Japan, megabanks Sumitomo Mitsui and Mizuho compete for the same corporate relationships. In Asia, DBS and OCBC bring local knowledge and digital innovation. Globally, JPMorgan and HSBC deploy massive resources and sophisticated capabilities. From below, fintechs unbundle profitable products while big tech companies leverage customer relationships.

MUFG's competitive response is selective engagement. They don't try to beat JPMorgan at investment banking or Ant Financial at digital payments. Instead, they leverage unique strengths: Japanese corporate relationships, patient capital for infrastructure, bridge between Asian savings and global investment opportunities. It's competitive judo—using opponents' strength against them rather than meeting force with force.

Future Scenarios

Three scenarios could define MUFG's next decade:

Scenario One: Asian Century Realized Asian economies grow steadily, financial integration accelerates, and MUFG's early positioning pays massive dividends. The bank becomes the financial bridge between Asia and the world, facilitating trade, investment, and capital flows. Returns on Asian investments exceed 20%, validating the strategic pivot. MUFG emerges as a top-five global bank by market capitalization.

Scenario Two: Digital Disruption Technology companies successfully disintermediate traditional banking. Payment flows through super apps, lending happens via platforms, and wealth management becomes fully automated. MUFG's digital investments prove insufficient against native digital players. The bank retreats to a narrow niche serving large corporations and complex transactions, profitable but diminished.

Scenario Three: Fragmentation and Crisis Geopolitical tensions fracture global finance into competing blocs. Asian financial crisis 2.0 emerges from property bubbles and excessive leverage. Climate disasters trigger massive loan losses. MUFG's diversification becomes a liability as problems cascade across markets. The bank survives but spends a decade rebuilding rather than growing.

The probability-weighted outcome likely combines elements of all three. Asia will grow but with volatility. Digital disruption will transform some businesses while others remain relationship-dependent. Geopolitical tensions will create friction without complete fragmentation.

Strategic Recommendations

For MUFG to thrive in this uncertain future, several strategic imperatives emerge:

Accelerate Digital Transformation Current digital investments, while substantial, may prove insufficient. MUFG needs to think beyond digitizing existing processes to reimagining banking itself. This means more aggressive fintech partnerships, larger technology investments, and willingness to cannibalize existing businesses.

Deepen Asian Presence Market opportunity validates aggressive expansion. Mitsubishi UFJ is bullish on India's growth prospects and seeks acquisition opportunities to boost its annual returns by 20% over the next 10 years. According to Itagaki, the energy demand in India is likely to expand as the country strives to become a manufacturing powerhouse. In addition, the country has various renewable projects in its pipeline, providing valuable opportunities for MUFG as the main finance provider.

Strengthen Risk Management As complexity increases, risk management must evolve. This means investing in AI-powered risk systems, building deeper stress-testing capabilities, and maintaining conservative capital buffers even when competitors chase returns.

Cultivate Ecosystem Partnerships The future of banking is embedded finance—financial services integrated into non-financial platforms. MUFG's partnerships with Grab, GCash, and other super apps position them well, but more aggressive ecosystem development is needed.

The Path Forward

MUFG stands at an inflection point. The decisions made in the next few years will determine whether the bank thrives in the Asian Century or becomes another casualty of technological disruption. The strategic pieces are in place—dominant position in Japan, growing Asian franchise, Morgan Stanley partnership, digital transformation underway. Execution will determine success.

The challenges are formidable. Japan's demographic decline accelerates. Competition intensifies across all markets. Technology disrupts traditional advantages. Climate change demands fundamental business model changes. Any one of these challenges could derail a lesser institution.

But MUFG has survived and thrived through greater challenges. The bank that emerged from samurai finance has navigated wars, occupations, bubbles, and crashes. Each crisis strengthened rather than weakened the institution. The current transformation—from traditional bank to digital-first financial ecosystem—may be the most challenging yet, but history suggests MUFG will not just survive but emerge stronger.

The key insight from MUFG's journey is that sustainable competitive advantage in banking comes not from any single factor but from the patient accumulation of relationships, capabilities, and capital over decades. While fintech startups can disrupt specific products and Chinese banks can offer cheaper capital, MUFG's combination of trust, sophistication, and scale remains formidable.

Final Analysis

The bull case for MUFG rests on successful execution of the Asian expansion strategy combined with digital transformation that preserves relationship banking advantages while capturing efficiency gains. If management can navigate the transition from Japanese demographic decline to Asian demographic dividend while avoiding major credit losses, the rewards are substantial. A successful MUFG could achieve sustainable ROE of 15%, generate superior shareholder returns, and establish itself as the premier financial bridge between Asia and global markets.

The bear case warns of multiple threats converging simultaneously. Japanese deflation returns, Asian growth disappoints, digital disruption accelerates, and climate transition costs explode. In this scenario, MUFG becomes a zombie bank—too big to fail but unable to generate adequate returns, slowly declining into irrelevance.