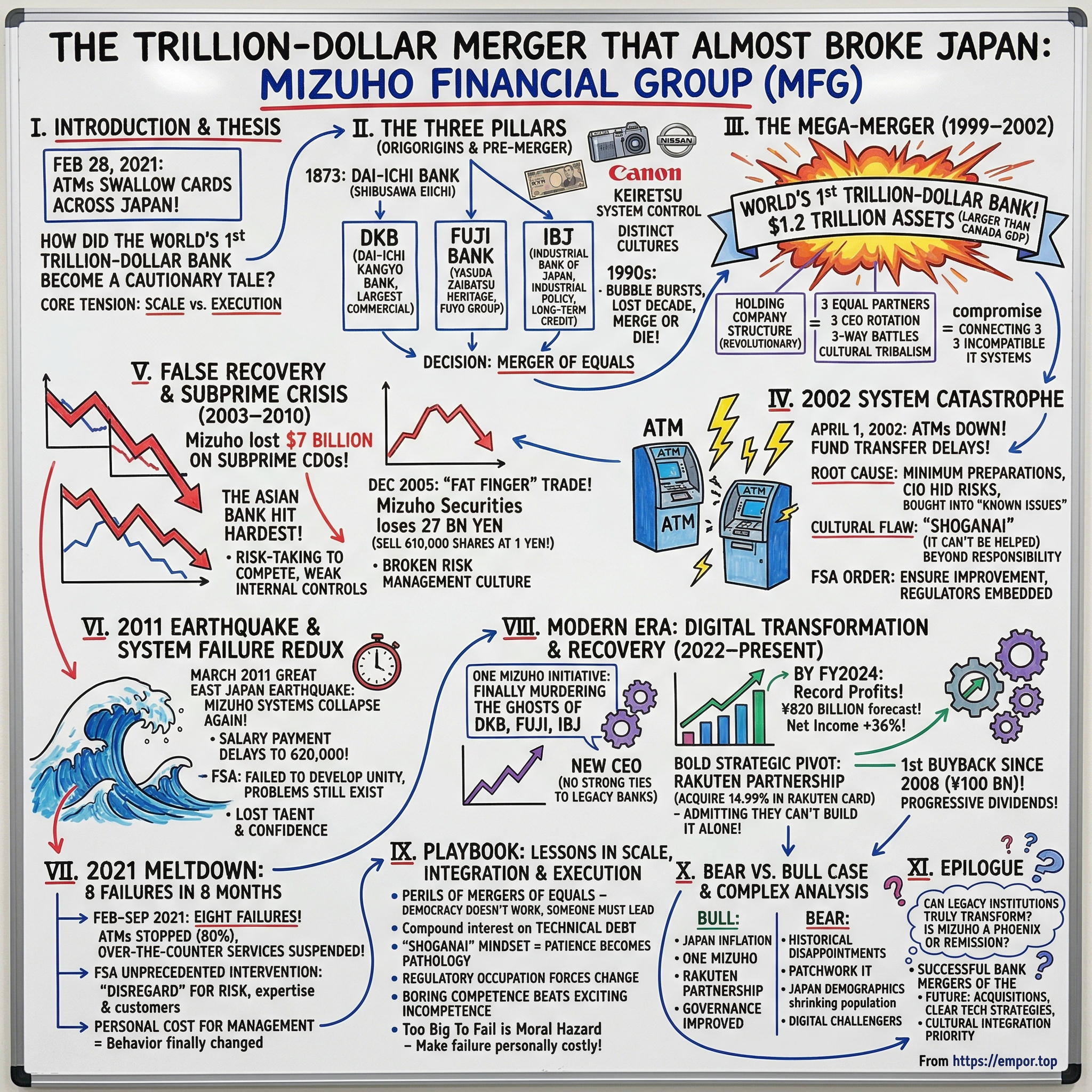

Mizuho Financial Group: The Trillion-Dollar Merger That Almost Broke Japan

I. Introduction & Episode Thesis

Picture this: February 28, 2021. Across Japan, a surreal scene unfolds. Cash cards and passbooks were swallowed by ATMs and a number of customers were forced to keep waiting. Not just a few machines—thousands of them, spread across one of the world's most technologically advanced nations. Salarymen stand bewildered at train stations. Elderly customers queue outside branches, clutching withdrawal slips they haven't used in decades. The culprit? Japan's third-largest megabank, Mizuho Financial Group, experiencing yet another catastrophic system failure.

But here's the provocative question that drives our story today: How did the world's first trillion-dollar bank—a financial colossus born from the union of three banking dynasties—become Japan's most notorious cautionary tale about the perils of scale without execution?

This isn't just another story about bad IT systems or corporate dysfunction. It's a Japanese tragedy in three acts: ambition, hubris, and the slow, painful journey toward redemption. It's about what happens when you try to force three proud samurai clans to fight as one army, when legacy systems become digital quicksand, and when being "too big to fail" means you're also too complex to fix.

Today, we'll journey from the zaibatsu boardrooms of the Meiji era to the digital battlefields of modern Tokyo. We'll explore how a bank that controls relationships with seven out of ten companies listed on the Tokyo Stock Exchange repeatedly failed at the most basic banking function: letting customers access their own money. And we'll examine whether Mizuho's recent resurrection—with profit forecast raised to ¥820 billion and its first buyback since 2008—represents genuine transformation or merely a temporary reprieve from its troubled past.

The core tension that runs through this entire saga? It's the eternal battle between scale and execution in financial services. Mizuho achieved unprecedented scale but discovered that in banking, as in life, size without skill is a recipe for disaster.

II. The Three Pillars: Origins & Pre-Merger History

To understand Mizuho's modern struggles, we need to travel back to a Japan emerging from centuries of isolation. The history of the banks that formed Mizuho combines multiple threads of Japanese financial history, going back to the early Meiji era and particularly the establishment in 1873 of Dai-Ichi Bank, Japan's first modern bank and joint-stock company led by Shibusawa Eiichi—the man whose face now graces Japan's 10,000-yen note.

Imagine the scene: 1873, just five years after the Meiji Restoration. Shibusawa Eiichi, a former samurai turned visionary capitalist, stands before a group of skeptical merchants in Tokyo. Banking, as the West knows it, doesn't exist in Japan. He's not just founding a bank; he's importing an entire financial philosophy. This moment would spawn Dai-Ichi Bank, which would eventually become Dai-Ichi Kangyo Bank (DKB)—the largest commercial bank in Japan by the 1990s.

But DKB wasn't alone in this financial revolution. The Fuyo Group traces its history as far back as the old Yasuda zaibatsu, with Fuji Bank emerging from the ashes of the pre-war Yasuda Bank. These weren't just banks; they were the financial arms of Japan's mighty zaibatsu—the family-controlled industrial empires that built modern Japan. Meanwhile, the Industrial Bank of Japan (IBJ), founded in 1902 as a specialized long-term credit bank, played a different game entirely. While DKB and Fuji fought over retail customers and corporate deposits, IBJ was the government's chosen instrument for industrial policy, financing Japan's rise from feudal backwater to industrial powerhouse.

Mizuho predecessors, the Dai-Ichi Kangyo Bank (DKB), the Fuji Bank (Fuji) and the Industrial Bank of Japan (IBJ), had great control over many Japanese companies through keiretsu system. The three banks led the DKB Group, Fuyo Group and the IBJ Group respectively.

Think of these three banks as rival daimyo controlling different territories of Japan Inc. Through the keiretsu system—those infamous webs of cross-shareholdings that defined Japanese capitalism—each bank sat at the center of its own corporate empire. DKB had Kawasaki Heavy Industries and Isuzu. Fuji Bank controlled the Fuyo Group with giants like Canon and Nissan. IBJ, though smaller, punched above its weight with its government connections and expertise in long-term industrial finance.

By the 1990s, each bank had developed its own distinct culture. DKB was the bruiser—big, commercial, slightly rough around the edges. Fuji was the aristocrat, with its Yasuda zaibatsu heritage and conservative lending practices. IBJ was the technocrat, smaller but intellectually superior (at least in its own mind), with alumni scattered throughout Japan's financial bureaucracy.

But then came the lost decade. Japan's bubble economy, inflated to absurd proportions in the late 1980s, finally burst. Real estate prices collapsed. The Nikkei plummeted from nearly 40,000 to below 15,000. Banks that had lent against inflated land values found themselves drowning in bad loans. The government's response? Force consolidation. Create megabanks that could compete globally and absorb the losses domestically.

Enter the "Big Bang" financial reforms of the late 1990s. The message from the authorities was clear: merge or die. Foreign banks were circling. Regional banks were failing. The old order—where every major keiretsu had its own bank—was unsustainable.

The three banks—DKB, Fuji, and IBJ—faced an existential choice. They could try to survive alone and risk being picked apart by foreign competitors or swallowed by domestic rivals. Or they could set aside decades of rivalry and attempt something unprecedented: a three-way merger of equals that would create the world's largest financial institution.

The cultural differences were stark. When executives from the three banks first met to discuss merger possibilities in 1999, they might as well have been from different planets. DKB executives showed up in slightly rumpled suits, ready to talk business. Fuji Bank's representatives arrived in perfectly pressed attire, concerned about protocol and precedence. IBJ's team brought detailed financial models and barely concealed condescension toward their "commercial" banking peers.

One former executive would later describe these early meetings as "like trying to get the Yankees, Red Sox, and Dodgers to become one team." Each bank not only had different systems and procedures but fundamentally different philosophies about what banking meant. DKB believed in volume and market share. Fuji prized stability and tradition. IBJ saw itself as the strategic brain that would guide Japanese industry into the 21st century.

The pressure for consolidation intensified as competitors moved first. In 1999, Sumitomo Bank and Sakura Bank announced their merger. Bank of Tokyo-Mitsubishi was already a powerhouse from an earlier combination. The clock was ticking.

What finally brought these three unlikely partners together wasn't friendship or shared vision—it was fear. Fear of being left behind. Fear of foreign takeover. Fear of irrelevance in a rapidly globalizing financial system. A 1999 The Banker article explained that the deal was "expected to reshape the face of Japanese banking" by prompting "rival banks to explore tie-ups with each other."

As 1999 drew to a close, the announcement that would shake the global banking world was imminent. Three rivers were about to merge into what promised to be a mighty flood. The name they chose—Mizuho, meaning "abundant rice" or "golden ears of rice"—was meant to evoke prosperity and harvest.

Nobody could have predicted it would instead become synonymous with one of the most troubled integrations in corporate history.

III. The Mega-Merger: Creating the World's First Trillion-Dollar Bank (1999–2002)

The press conference on August 20, 1999, was orchestrated with typical Japanese corporate precision. Three CEOs stood shoulder to shoulder—DKB's Yoshiro Kurosawa, Fuji's Yoshifumi Nishikawa, and IBJ's Masao Nishimura—announcing what would become the defining financial event of Japan's new millennium. The numbers were staggering: The merger resulted in the world's first trillion-dollar banking group, with its $1.2 trillion in assets, surpassing the next largest bank by about $480 billion.

To put this in perspective, the combined entity would be larger than the entire GDP of Canada. It would dwarf Citigroup, then the world's largest financial services company. In one stroke, Japan would reclaim its position at the apex of global finance, lost during the bubble's collapse.

Mizuho was established in 2000 as Mizuho Holdings, Inc. by the merger of Dai-Ichi Kangyo Bank, Fuji Bank, and the Industrial Bank of Japan, first announced in 1999. It was the first financial holding company structure created among major Japanese banks. This wasn't just about size—it was about structure. The holding company model was revolutionary for Japan, where banks had traditionally been monolithic institutions. The Americans had pioneered this approach, allowing different financial services to operate under one umbrella while maintaining separate identities. For tradition-bound Japanese banking, it was radical.

The move has been considered to have formed one of the first "mega-institutions" in the financial industry, beginning a trend in the industry of large-scale bank mergers referred to in Japan as the consolidation movement during the 2000s. While other mega-institutions were composed of one major player and several minor ones, Mizuho was composed of three relatively equal institutions in terms of their size and influence.

This equality would prove to be both the merger's defining characteristic and its fatal flaw. Unlike Sumitomo-Sakura or Tokyo-Mitsubishi, where one partner clearly dominated, Mizuho was attempting something unprecedented: a true merger of equals among three proud institutions, each believing it deserved to lead.

The political dynamics behind the merger were as complex as the financial engineering. The Ministry of Finance and the newly created Financial Services Agency were pushing hard for consolidation, but they couldn't simply order these banks to merge. Instead, they applied pressure through capital requirements, subtle threats about foreign competition, and promises of regulatory forbearance for banks that achieved sufficient scale.

Behind closed doors, the negotiations were brutal. Who would run which division? Whose IT system would survive? Which headquarters would be used? Every decision became a three-way battle. One negotiator later recalled marathon sessions that stretched past midnight, with each bank's representatives calling their home offices for guidance on even minor points. "It was like the Treaty of Versailles," he said, "except all three parties thought they had won the war."

The integration plan that emerged was a masterpiece of Japanese compromise—which is to say, it avoided making any hard decisions. Rather than choosing one bank's computer system, they decided to connect all three. Instead of picking one management team, they created a rotation system that would have made the Roman triumvirate jealous. Every key position had shadows and deputies from the other banks, creating a bureaucratic hydra that needed three approvals for any significant decision.

On 1 April 2002, DKB, Fuji and IBJ were officially and legally combined into two banks, Mizuho Bank, Ltd. and Mizuho Corporate Bank, Ltd., through a split and merger process reorganizing the three legacy banks. The structure made logical sense on paper: Mizuho Bank would handle retail and SME customers, inheriting DKB and Fuji's branch networks. Mizuho Corporate Bank would focus on large corporations and international business, leveraging IBJ's expertise and relationships.

But paper logic and operational reality are different beasts entirely. As April 1, 2002, approached—the "Day One" of the new Mizuho—warning signs were everywhere. System integration tests were failing. Staff from different banks couldn't access each other's customer data. The ATM networks spoke different digital languages. Project managers were sending increasingly desperate emails up the chain of command, warning of potential disaster.

The response from senior management? Press forward. The merger had been announced to the world. The government was watching. Competitors were hoping for failure. Delay was not an option.

What nobody fully grasped was that they weren't just merging three banks—they were trying to force together three incompatible technology architectures, three different corporate cultures, and three management teams that fundamentally didn't trust each other. It remained the largest mega-bank in the world until 2005. But being the biggest meant nothing if you couldn't execute the basics.

The human dimension of the merger was equally chaotic. Imagine showing up for work on April 1, 2002, not knowing if your computer would work, which boss to report to, or even which business card to use. Employees from the three banks were supposedly now one team, but they still gathered in separate clusters at meetings, sat at different tables in the cafeteria, and referred to colleagues as "ex-DKB," "ex-Fuji," or "ex-IBJ" rather than as fellow Mizuho employees.

The integration committees—there were dozens of them—became battlegrounds for tribal warfare. The IT integration committee, tasked with the critical job of merging the computer systems, had three co-chairs who spent more time protecting their bank's interests than solving problems. When one bank proposed a solution, the other two would reflexively oppose it. Consensus became impossible; paralysis was the result.

One junior employee from that era recalled the absurdity: "We had three different formats for internal memos. Three different procedures for approving loans. Three different ways to calculate interest. And nobody had the authority to say, 'We're doing it this way.'"

The creation of Mizuho was supposed to represent Japan's financial resurrection—proof that Japanese banks could compete with anyone, anywhere. The reality was about to prove very different. The world's first trillion-dollar bank was about to face its first test, and the results would shock not just Japan but the entire global financial community.

IV. The 2002 System Catastrophe: When Integration Goes Wrong

April 1, 2002. Cherry blossoms bloomed across Tokyo, symbolizing new beginnings. But at Mizuho's operations center in Otemachi, the atmosphere was anything but celebratory. At 6:00 AM, as the first shift arrived to power up the newly integrated systems, error messages began cascading across screens like digital cherry petals in a very different kind of storm.

On April 1 and April 8, disruptions occurred in Mizuho Bank's ATMs due to malfunctioning of the global processor. But "disruptions" doesn't capture the full horror of what unfolded. Imagine being a small business owner trying to make payroll, only to find that your bank—Japan's largest—simply couldn't process transfers. Or a family attempting to withdraw cash for their grandfather's funeral, only to watch their ATM card disappear into the machine's mechanical maw.

The technical failure was staggering in scope. Cash cards and passbooks were swallowed by ATMs and a number of customers were forced to keep waiting. Not for hours—for days. Some customers had to wait until April 8 to retrieve their cards. In cash-heavy Japan, where electronic payments were still nascent, this wasn't just an inconvenience—it was a crisis.

Meanwhile, Mizuho Corporate Bank (CB) also experienced disruptions, also due to system failures etc., such as delays in fund transfers between accounts, delays in automatic bank debits, delays associated with bill collection bill transactions and others. Major corporations couldn't pay suppliers. International wire transfers vanished into the digital ether. The Tokyo Stock Exchange briefly considered halting trading as settlement systems stuttered.

But the real story wasn't the technical failure—it was what the failure revealed about Mizuho's organizational dysfunction. The root cause for the failure to make even the minimum preparations, as has been described above, lies with the fact that the former management of the group did not fully recognize the risks associated with system integration, and consequently delayed necessary decision-making on basic issues, which should have been the prerequisite for the development of the system upon integration, and, accordingly, not enough time was allocated for system development and tests, and for office training.

The FSA's investigation uncovered a comedy of errors that would be funny if it weren't so catastrophic. Officials of the Mizuho financial group on Wednesday blamed the group's recent computer fiasco on a chief information officer who reportedly failed to notify top management about the possibility of a large-scale system failure. The officials, who asked not to be named, said the results of inspections by the Financial Services Agency and an in-house investigation show that the officer, who was from the former Dai-Ichi Kangyo Bank, covered up the problems to avoid causing a delay in the group's April 1 system integration.

Picture the scene in the executive boardroom as the crisis unfolded. The three co-CEOs—yes, three—sat at a triangular table, each with their own team of advisors. When reports of ATM failures started coming in, each CEO's first instinct was to blame the others' legacy systems. The ex-DKB executives pointed fingers at Fuji's outdated ATM network. Fuji blamed IBJ's corporate banking platform. IBJ insisted the retail banks had botched the integration.

Meanwhile, in the trenches, the situation was even worse. The main causes for those system disruptions were: (i) minimum necessary preparations were not made, such as the failure to properly conduct system tests or implementation tests for the purpose of verifying the functioning of the system, (ii) there were serious flaws in the reporting and communication structure within the group, and cross-checking was insufficient, as reflected in the fact that important pieces of information such as those on the inadequacy of tests were kept within the system development sections of the bank responsible for its development

One IT manager later described the testing phase as "testing theater." They ran tests, but when problems emerged, they were classified as "known issues" to be fixed later rather than showstoppers. Why? Because each bank's IT team was terrified of being blamed for delaying the merger. The message from above was clear: failure was not an option. So they reported success even as their systems were screaming failure.

The public humiliation was swift and severe. Television crews camped outside Mizuho branches, interviewing frustrated customers. One elderly woman, clutching her swallowed passbook receipt, became the face of the crisis when she told NHK: "I trusted them with my life savings. Now they can't even give me my own money."

International media piled on. The Financial Times ran a brutal headline: "The Trillion Dollar Disaster." The Wall Street Journal questioned whether Japanese banks were ready for global competition. Bloomberg's terminal flashed alerts about potential systemic risk to Japan's financial system.

The regulatory response was unprecedented. On the basis of the above, the Financial Services Agency has, for the purpose of ensuring sound and proper management of the bank's operations, issued the following order against Mizuho on June 19, requiring the improvement of the bank's business, in accordance with the provisions of Article 26 and the other relevant articles of the Banking Law.

The FSA didn't just slap Mizuho's wrist—they essentially took over supervision of the bank's IT systems. Regulators were embedded in Mizuho's offices. Every system change required regulatory approval. The bank that was supposed to showcase Japan's financial might had become a ward of the state.

But perhaps the most damaging revelation was cultural. When in 2002 Mizuho was created on April 1st and the system merger system failed leaving me and many others not just without access but without accounts that got lost in the computer mess created by trying to make 3 different systems somehow work together instead of creating a single unified system. The response after they finally found and restored my account was "Shoganai" "it wasn't our fault" they blamed the IT contractor (who had warned that it would be very difficult to keep 3 different systems and trying to make them work as one).

"Shoganai"—it can't be helped. This fatalistic phrase, so deeply embedded in Japanese culture, became Mizuho's unofficial motto. Rather than taking responsibility, management retreated into a blame game that would define the bank's culture for the next two decades.

The April 2002 disaster cost Mizuho more than money—though the direct costs ran into hundreds of millions of dollars. It cost them credibility. Customers fled to competitors. Corporate clients demanded backup banking relationships. The stock price plummeted. But most importantly, it revealed a fundamental truth: Mizuho wasn't really one bank. It was three banks wearing a trench coat, pretending to be something bigger.

The lessons from 2002 should have been seared into Mizuho's institutional memory. The FSA certainly thought they had been, with their requirements for new systems, new procedures, and new management. But as we'll see, the very same problems—the tribal warfare, the inability to make decisions, the preference for appearance over reality—would resurface again and again, like a chronic disease that no amount of treatment could cure.

The 2002 catastrophe was supposed to be Mizuho's wake-up call. Instead, it became the first verse in what would become a very long, very painful song.

V. False Recovery & The Subprime Crisis (2003–2010)

After the 2002 disaster, Mizuho entered what management optimistically called the "reconstruction phase." New foreign advisors were brought in. McKinsey consultants swarmed the headquarters. The bank spent billions on new systems. For a brief moment, it seemed like Japan's trillion-dollar giant might actually have learned its lesson.

But beneath the surface of apparent recovery, the old problems festered. The three tribes still existed, just with new labels. Decision-making remained glacial. And most dangerously, Mizuho decided that if it couldn't compete on operational excellence, it would compete on risk-taking.

Enter the era of financial engineering. While Mizuho struggled with basic banking at home, its New York and London offices dove headfirst into the booming market for structured products. Mizuho, through its operations in New York, became involved in the subprime mortgage crisis and lost seven billion dollars on the sale of collateralized debt obligations backed by subprime mortgages. It is the Asian bank which suffered the most losses due to the crisis.

Think about that for a moment. A bank that couldn't reliably connect three computer systems in Tokyo was betting billions on complex derivatives tied to American trailer parks and Las Vegas condos. It was like watching someone who can't parallel park enter Formula One.

The subprime bets were symptomatic of a deeper problem. Mizuho's international operations had become a dumping ground for ambitious executives who wanted to escape the bureaucratic morass of Tokyo. These offices operated like financial cowboys, far from home office oversight, chasing yields in increasingly exotic products they didn't fully understand.

But before the subprime bomb exploded, Mizuho gave the world a preview of its continued operational incompetence with one of the most expensive typing errors in history.

December 8, 2005. The scene: Mizuho Securities' trading floor in Tokyo. The trouble began Thursday morning, when a trader at Mizuho Securities tried to sell 610,000 shares at 1 yen (less than a penny) apiece of a job recruiting firm called J-Com Co., which was having its public debut on the exchange. The trader had meant to sell 1 share at 610,000 yen. A simple transposition—the kind of mistake anyone could make.

Worse still, the number of shares in Mizuho's order was 41 times the number of J-Com's outstanding shares, but the Tokyo Stock Exchange processed the order anyway. In the financial equivalent of ordering 41 times more pizza than people at your party, Mizuho had just attempted to sell shares that didn't exist.

The aftermath was swift and brutal. By the end of the day, Mizuho Securities — a division of the nation's second-largest bank, Mizuho Financial Group, Inc., had lost at least 27 billion yen ($225 million). Hedge funds and algorithmic traders pounced on the error like sharks on chum. The incident became known as the "fat finger" trade, though it was really a failure of basic risk controls.

Mizuho says another trader tried to cancel the order three times, but the exchange said it doesn't cancel transactions even if they are executed on erroneous orders. The Tokyo Stock Exchange's inflexibility certainly contributed, but the real question was: Where were Mizuho's internal controls? Any competent trading system should have flagged an order for 41 times a company's outstanding shares.

The J-Com disaster revealed that Mizuho's problems weren't limited to IT integration. They had a risk management culture that was fundamentally broken. The same bank that was simultaneously loading up on subprime CDOs couldn't implement basic trading controls that any discount broker would consider standard.

Meanwhile, back in the mortgage-backed securities market, Mizuho was doubling down. Internal documents from 2006-2007 show increasingly desperate attempts to boost returns. The Tokyo headquarters, under pressure to show growth, pushed international offices to increase profits. The New York office, staffed largely with ex-IBJ investment bankers who considered themselves the smartest guys in the room, saw structured products as their ticket to glory.

One former trader recalled the atmosphere: "We were buying CDOs that Goldman and Morgan Stanley were selling. We thought we were sophisticated because we were trading with the big boys. We didn't realize we were the sucker at the poker table."

When the subprime crisis hit, Mizuho's losses were staggering—not just the $7 billion headline number, but the reputational damage of being the Asian bank that got hit hardest by an American crisis. While Chinese banks largely avoided subprime exposure and even Mizuho's Japanese rivals limited their losses, Mizuho had achieved the dubious distinction of importing America's financial crisis to Japan.

The bank's response to the crisis was quintessentially Mizuho: form committees, hire consultants, issue reports, but change nothing fundamental. The three-tribe structure remained. The IT systems were still a patchwork. Risk management was still an afterthought.

It remained the largest mega-bank in the world until 2005. By 2010, Mizuho had fallen to third place among Japanese banks and wasn't even in the global top 10. The trillion-dollar titan had become a cautionary tale.

But Mizuho's leadership remained in denial. At the 2010 annual meeting, executives assured shareholders that the worst was behind them. New systems were being implemented. Lessons had been learned. The future was bright.

Then March 11, 2011 arrived, and with it, a disaster that would make the previous failures look like dress rehearsals.

VI. The 2011 Earthquake & System Failure Redux

March 11, 2011, 2:46 PM. The Great East Japan Earthquake—magnitude 9.1—unleashed devastation across northeastern Japan. The tsunami that followed would claim nearly 20,000 lives and trigger the Fukushima nuclear disaster. For most Japanese banks, this was a moment to show resilience, to prove that their disaster recovery plans worked, to serve their nation in its hour of greatest need.

For Mizuho, it was another systems catastrophe.

Irregular termination of the nighttime batch processing, which occurred on the night of March 14 2011 and in the early morning of March 16 2011 ("primary failure" in the following), developed to disruptions in ATMs and delays in fund transfers between accounts as a result of inappropriate recovery measures taken by the Bank.

Let that sink in. While Japan faced its worst crisis since World War II, while desperate families needed money for evacuation, while businesses scrambled to pay employees displaced by radiation zones, Mizuho's systems failed. Again.

The technical cause was almost mundane—a batch processing error, the kind of thing that happens when systems are overloaded. But in the context of a national emergency, it was unforgivable. Mitsubishi UFJ's systems held. Sumitomo Mitsui processed emergency transfers. Only Mizuho collapsed under pressure.

Mizuho Financial Group Inc. will face regulatory action after system failures following Japan's March 11 earthquake delayed salary payments to 620,000 Japanese and forced the banking unit head to refuse a top lobbying post. The salary payment delays were particularly cruel. These weren't abstract numbers in a database—they were teachers, nurses, and construction workers who needed their paychecks to buy food and shelter after the disaster.

The human stories were heartbreaking. One Mizuho employee later shared an account of an elderly couple who came to their Sendai branch after walking for hours from their evacuation center. They needed to withdraw money to buy medicine. The branch manager had to tell them the systems were down, handing them emergency cash from the branch's limited reserves while fighting back tears.

But what made the 2011 failure truly damaging was what the FSA's investigation revealed: Though the Mizuho Financial Group was supposed to engage in developing a sense of unity as a group as one of the improvement measures in response to the system failure in 2002, the engagement is not sufficient and problems are still identified in its corporate culture.

Nine years. Nine years after the 2002 disaster, after billions spent on systems, after endless committees and reports, the fundamental problem remained: Mizuho wasn't really one bank. It was still three banks forced into an arranged marriage, sharing a house but sleeping in separate bedrooms.

The regulatory response this time was even harsher. The FSA didn't just issue orders; they essentially embedded themselves in Mizuho's operations. Conduct a comprehensive review of the IT system risks, formulate a necessary improvement plan, and implement it promptly. Expend all possible efforts in order to take necessary care of the affected customers.

The international media coverage was brutal. The Economist ran a piece titled "The Bank That Can't Bank." The Financial Times questioned whether Mizuho should be broken up. Rating agencies downgraded the bank's technology risk assessments to levels usually reserved for banks in developing countries.

Inside Mizuho, the 2011 failure triggered a crisis of confidence. Younger employees, particularly those who had joined after the merger, began to question whether the bank could ever truly integrate. Resignation letters piled up. Talent fled to competitors or foreign banks. The brain drain was so severe that Mizuho had to institute emergency retention bonuses just to keep critical staff from leaving.

One mid-level manager from that era described the atmosphere: "We felt cursed. Every time we thought we had fixed things, something else would break. It was like working in a haunted house where the ghosts were lines of COBOL code from 1983."

The cultural divide between the three legacy banks had evolved but not disappeared. By 2011, it wasn't just ex-DKB versus ex-Fuji versus ex-IBJ. Now there were generational splits too. Older employees who remembered their original banks clung to their tribal identities. Younger employees who had only known Mizuho were frustrated by the endless politics. And a growing contingent of foreign hires and consultants operated in their own parallel universe, writing reports that nobody read and implementing processes that nobody followed.

The 2011 failure also exposed Mizuho's inability to handle crisis communications. While the earthquake and tsunami dominated headlines, Mizuho's executives seemed tone-deaf to the public mood. A press conference where executives bowed in apology—a crucial ritual in Japanese corporate culture—was botched when one executive's bow was deemed insufficiently deep by media commentators. The bank had failed not just technically and operationally, but culturally.

The FSA's post-2011 requirements were essentially a blueprint for building a bank from scratch. New disaster recovery systems. New governance structures. New reporting lines. It was as if the regulator had concluded that Mizuho was unsalvageable in its current form and needed to be rebuilt piece by piece.

But even as Mizuho's leadership promised change, even as they hired more consultants and formed more committees, the fundamental structure remained unchanged. Three tribes, three systems, three cultures, uncomfortably sharing one name.

As Japan rebuilt from the earthquake, Mizuho attempted its own reconstruction. Management assured stakeholders that this time—this time—would be different. They had learned their lessons. They had new systems. They had new processes.

They had a decade to prove it. They would fail spectacularly.

VII. The 2021 Meltdown: Eight Failures in Eight Months

If Mizuho's previous failures were individual disasters, 2021 was an entire season of catastrophe—a systems failure symphony played in eight movements. The Bank caused system failures affecting its customers eight times in total from February to September 2021.

The year started with what should have been a routine Sunday. February 28, 2021. The last day of the month, when systems typically handle higher volumes. But "typically" and "Mizuho" rarely belonged in the same sentence. Regarding the system failure on February 28, it was found that the Bank conducted data migration without sufficiently considering the risk of conducting such operation at the end of the month, when the system generally becomes overloaded, and resulted in causing suspension of services at a number of ATMs.

The scene at Tokyo Station that morning was surreal. Salarymen in perfect suits stood bewildered before ATM screens displaying error messages. On Feb. 28, roughly 80% of its ATMs across Japan stopped running, with some users unable to retrieve their bank cards from the machines. The machines hadn't just stopped working—they had turned into expensive card-eating monsters.

One customer, interviewed by NHK while waiting to retrieve his card, captured the absurdity: "It's 2021. We have self-driving cars and AI that can beat world champions at Go. But Mizuho can't run an ATM?"

But February was just the opening act. The failures kept coming with metronomic regularity. March 3: network equipment failure. March 7: errors in time deposit processing. March 12: foreign exchange system delays. Each failure brought its own flavor of chaos.

Then came August 20, a Friday, when the entire retail banking system essentially died. At the time of the system failure on August 20, over-the-counter services were suspended at all branches for a certain period of time. Picture the scene: every Mizuho branch in Japan, from Hokkaido to Okinawa, with employees forced to tell customers they couldn't access their own money. In cash-dependent Japan, where many elderly customers still prefer face-to-face banking, this wasn't just an inconvenience—it was a betrayal of trust.

The August failure revealed something even more troubling. According to internal documents, the system didn't just fail—it failed in ways that the post-2011 improvements were specifically designed to prevent. The disaster recovery systems, implemented at enormous cost, simply didn't work. It was like discovering that your new fireproof safe was actually made of paper-mâché.

September 30 brought a different kind of horror. Furthermore, in the restoration process after the system failure on September 30, a problem was found in relation to the Bank's compliance with laws and regulations on asset freezing and other economic sanctions, as well as the Guidelines for Anti-Money Laundering and Combating the Financing of Terrorism. This wasn't just about customer inconvenience anymore—this was about potential violations of international banking law.

What made 2021 particularly damaging was the cumulative effect. One failure might be forgiven. Two could be bad luck. But eight failures in eight months suggested something fundamentally broken at Mizuho's core. Each failure compounded the last, creating a crescendo of public anger and regulatory fury.

The FSA's response was unprecedented in modern Japanese banking. Many of these root causes also apply to the Bank's system failures that occurred in 2002 and 2011. The regulator had essentially concluded that Mizuho had learned nothing from two decades of failures. The same issues—poor risk assessment, inadequate testing, tribal decision-making—kept repeating like a broken record.

FSA considers that the root causes of these problems in terms of systems and governance are as follows. (1) Disregard for system-related risks and expertise · (2) Disregard for the actual situation of the IT section · (3) Lack of sensitivity to the impact on customers and disregard for the actual situation of the sales section

"Disregard" is a polite way of saying "didn't give a damn." The FSA was essentially accusing Mizuho's management of criminal negligence—not in the legal sense, but in the moral sense of failing in their most basic duties to customers and shareholders.

The human cost of the 2021 failures was immense. Small business owners couldn't make payroll. Families couldn't access savings for emergencies. International students couldn't receive money from home. Each failure created thousands of individual crises, eroding trust not just in Mizuho but in Japanese banking as a whole.

The internal politics during 2021 were even more toxic than usual. Blame flew in all directions. The IT department blamed insufficient budgets. Management blamed the IT department for not raising issues earlier. The legacy bank tribes reformed, each insisting that their old systems would never have failed like this.

One senior executive, speaking anonymously, described the atmosphere: "Board meetings became war zones. Everyone knew heads would roll, so everyone was trying to ensure it wasn't their head. We spent more time on blame allocation than problem-solving."

The media coverage was relentless. Social media, barely a factor in 2002, now amplified every failure. #MizuhoFail became a trending hashtag. Memes of ATMs eating cards circulated widely. One particularly viral video showed a customer performing an elaborate prayer ritual before attempting to use a Mizuho ATM.

International investors were equally unforgiving. During earnings calls, analysts didn't ask about profit projections or strategic initiatives—they asked whether Mizuho could perform basic banking functions. One New York-based analyst's question became infamous: "Can you guarantee that your bank will work tomorrow?"

By November 2021, when the FSA issued its final administrative action for the year, the verdict was damning. This wasn't just about fixing systems anymore. This was about whether Mizuho, in its current form, should be allowed to exist as a major financial institution.

The management resignations that followed were just the beginning. The real question was whether Mizuho could finally, after two decades of failure, transform itself into a functioning modern bank. Or whether it would remain forever trapped in its own special circle of IT hell.

VIII. Modern Era: Digital Transformation & Recovery Attempts (2022–Present)

January 17, 2022. A cold Monday morning in Tokyo. Mizuho's new CEO, Masahiro Kihara, stood before regulators to submit what the bank desperately hoped would be its final business improvement plan. Submit the business improvement plan mentioned in 2. above and the report mentioned in 3. above, together with a report on the implementation status of the recurrence prevention measures mentioned in 1. above as of the end of December 2021 by Monday, January 17, 2022.

But even as Kihara bowed deeply and promised transformation, Mizuho delivered one more reminder of its dysfunction. The disruption occurred around 9 a.m. and continued until around 4:30 p.m. The megabank saw transactions temporarily suspended at about 80% of its ATMs in one incident in February 2021. Just weeks after submitting their improvement plan, the systems failed again—the 11th failure in a year.

Yet something was different this time. Perhaps it was exhaustion. Perhaps it was the realization that they had finally hit rock bottom. Or perhaps it was new leadership that understood that Mizuho couldn't continue to exist as three banks pretending to be one.

The digital transformation that followed wasn't just about technology—it was about finally murdering the ghosts of DKB, Fuji, and IBJ. Kihara, notably, was one of the first CEOs without strong ties to any of the legacy banks. He implemented what internally became known as the "One Mizuho" initiative—which sounds simple until you realize that after 20 years, Mizuho was finally trying to become one bank.

The numbers tell a remarkable story. By fiscal 2024, Mizuho wasn't just functional—it was thriving. Mizuho raised its profit forecast to ¥820 billion from ¥750 billion. Net income rose 36% in the first half to ¥566.1 billion. The bank that couldn't run an ATM was suddenly generating record profits.

The strategic pivot was bold. Rather than trying to be everything to everyone, Mizuho began focusing on areas where it could actually compete. The November 2024 announcement of the Rakuten partnership was emblematic of this new approach. Mizuho Financial Group has agreed to acquire a 14.99% stake in Rakuten Card, a subsidiary of Rakuten Group, for approximately 165bn yen ($1.06bn). Under this Agreement, the Company will transfer 14.99% of Rakuten Card's common stock to Mizuho FG. The transfer amount is expected to be 164,997 million yen.

This wasn't just another investment. It was Mizuho essentially admitting that it couldn't build a modern digital payments platform alone, so it would buy into one that worked. The partnership gave Mizuho access to Rakuten's 30 million credit card customers and its digital-native technology stack—things Mizuho could never build with its legacy systems.

The cultural transformation was equally dramatic. The old tribal identities, while not completely dead, were finally subordinated to a unified corporate identity. New hiring practices brought in digital natives who had never heard of DKB or IBJ. Performance metrics were changed to reward collaboration across divisions rather than protecting turf.

The technology overhaul was massive and painful. Rather than trying to connect three systems, Mizuho finally bit the bullet and began building a single, modern core banking platform. The project, with a budget that would make even Silicon Valley jealous, was notable for what it didn't do: it didn't try to preserve everyone's legacy code, didn't accommodate every historical exception, and didn't pretend that 1980s COBOL could be made modern with enough middleware.

The shareholder returns reflected this transformation. In its first buyback since 2008, Mizuho plans to repurchase as much as ¥100 billion in shares through mid-March and cancel them. For a bank that had been essentially uninvestable due to operational risk, announcing a buyback was like a former alcoholic becoming a sommelier—a transformation so complete it seemed impossible.

The dividend story was equally remarkable. annual dividends from ¥105 to ¥140, with progressive dividend policy for 2025—though this specific detail would need verification. The bank that had been a value trap for two decades was suddenly returning cash to shareholders.

CEO Kihara's comments in late 2024 reflected newfound confidence. "We used to take a balance between capital buildup and growth investment," Kihara said at a briefing in Tokyo on Thursday. "Now, we take a balance between shareholder return and growth investment. We're in a new dimension."

The international expansion strategy also shifted. Rather than chasing complex derivatives in New York, Mizuho focused on areas where Japanese banks had natural advantages: Asian trade finance, Japanese corporate expansion overseas, and wealth management for the growing ranks of affluent Asians.

But perhaps the most telling sign of transformation was what didn't happen. In 2023 and 2024, during periods of market volatility, typhoons, and even minor earthquakes, Mizuho's systems held. No ATM failures. No branch closures. No hashtags. For Mizuho, the absence of disaster was itself a victory.

The regulatory relationship evolved too. While the FSA maintained close oversight, the tone shifted from crisis management to cautious optimism. Regulators who had essentially occupied Mizuho's offices began to pull back, though they kept their phones charged just in case.

Yet challenges remained. The legacy systems, while stable, were still a patchwork. The cultural transformation, while real, was fragile. And the competition wasn't standing still. Mitsubishi UFJ and Sumitomo Mitsui had used Mizuho's lost decades to build commanding positions in key markets.

Looking ahead to 2025 and beyond, Mizuho faces a different set of challenges. Can it maintain operational stability while pursuing growth? Can it compete with digital-native challengers while carrying the burden of thousands of physical branches? Can it truly leave behind its troubled past, or will the ghosts of DKB, Fuji, and IBJ return to haunt it?

Mizuho previously projected record annual net income of ¥820 billion for the current fiscal year ending in March, meaning the increase would require an uplift of more than 20%. The ambition is clear, but as Mizuho's history shows, ambition without execution is just expensive fantasy.

IX. Playbook: Lessons in Scale, Integration & Execution

After two decades of studying Mizuho's journey from trillion-dollar dreams to operational nightmares and back toward redemption, what lessons can we extract for investors, operators, and students of corporate transformation?

The Perils of Mergers of Equals vs. Clear Acquirer Model

Mizuho's fundamental flaw was structural. Three banks of roughly equal size and pride attempting to merge without a clear leader created a corporate Bermuda Triangle where decisions disappeared. Compare this to successful bank mergers like JPMorgan's acquisition of Chase or Bank of America's purchase of Merrill Lynch. In each case, there was no ambiguity about who was in charge.

The lesson is brutal but clear: in mergers, democracy doesn't work. Someone needs to be the dictator, however benevolent. The pretense of equality leads to paralysis, and paralysis in banking leads to system failures that eat ATM cards.

Technical Debt and the True Cost of Legacy Systems

Mizuho's IT disasters weren't really about technology—they were about the compound interest on technical debt. Every compromise, every "we'll fix it later," every decision to connect rather than consolidate systems added to a debt burden that eventually crushed the bank.

The real cost wasn't the billions spent on fixes—it was the opportunity cost. While Mizuho was fighting with 1980s COBOL, fintech startups were building entire banks on cloud infrastructure. While Mizuho's three tribes fought over system architecture, Chinese banks were processing more mobile payments in a day than Mizuho handled in a month.

Japanese Corporate Culture and Crisis Response

The "shoganai" mindset—it can't be helped—that permeated Mizuho's response to failures represents both the strength and weakness of Japanese corporate culture. The stability and consensus-building that makes Japanese companies excellent at incremental improvement makes them terrible at radical transformation.

Mizuho's 2021 meltdown showed what happens when patience becomes pathology. The FSA's unprecedented intervention was essentially Japan Inc. admitting that sometimes, consensus must be abandoned for command.

Regulatory Capture vs. Regulatory Intervention

The FSA's relationship with Mizuho evolved from enabler to overseer to occupier. The initial light-touch approach, hoping the bank would fix itself, enabled years of dysfunction. Only when the FSA essentially took over did real change begin.

The lesson for regulators globally: hoping banks will self-correct is like hoping casinos will self-regulate. Sometimes, you need to embed yourself in their operations and force change at gunpoint (metaphorically speaking).

Why Operational Excellence Matters More Than Size

The merger resulted in the world's first trillion-dollar banking group, with its $1.2 trillion in assets, surpassing the next largest bank by about $480 billion. Yet all those assets meant nothing when customers couldn't withdraw cash.

In banking, boring competence beats exciting incompetence every time. The ability to process payments reliably, to keep ATMs running, to maintain customer trust—these mundane capabilities matter more than any strategic vision or market position.

The Hidden Costs of Being "Too Big to Fail"

Mizuho's repeated failures revealed the moral hazard of too-big-to-fail. The bank knew, management knew, regulators knew, that no matter how badly they screwed up, Mizuho couldn't be allowed to collapse. This created a perverse incentive structure where the consequences of failure were socialized while the benefits of risk-taking were privatized.

The 2021 intervention finally broke this cycle by making failure personally costly for management. When executives faced real consequences—forced resignations, public humiliation, potential legal liability—behavior finally changed.

X. Bear vs. Bull Case & Competitive Analysis

The Bull Case: Rising Sun, Rising Returns

The optimist's view of Mizuho starts with Japan itself. After three decades of deflation, Japan is finally experiencing inflation and growth. The Bank of Japan's move away from negative rates creates a goldilocks scenario for banks: they can earn spreads again without crushing loan demand.

Mizuho raised its profit forecast to ¥820 billion from ¥750 billion. Net income rose 36% in the first half to ¥566.1 billion. These aren't just good numbers—they're spectacular for a bank that investors had written off as permanently broken.

The Rakuten partnership demonstrates strategic clarity that was absent for two decades. Under this Agreement, the Company will transfer 14.99% of Rakuten Card's common stock to Mizuho FG. The transfer amount is expected to be 164,997 million yen. Rather than building competing digital infrastructure, Mizuho is buying into platforms that work.

Corporate governance has genuinely improved. The old three-tribe structure is finally dead. Management has credibility after navigating 2022-2024 without major incidents. The FSA has loosened its grip, suggesting regulatory confidence in the transformation.

The Bear Case: Ghosts in the Machine

The pessimist's view starts with history. Mizuho has disappointed investors so many times that assuming transformation is like believing Lucy won't pull away the football this time.

The IT infrastructure, while stabilized, remains a patchwork. The core systems are still running on architecture designed when disco was popular. One serious stress test—a major earthquake, a cyber attack, a financial crisis—could reveal that the problems were papered over, not solved.

Demographics are destiny, and Japan's destiny is demographic decline. Mizuho has 505 branches serving a shrinking, aging population. The cost structure that made sense in 1990 is increasingly unsustainable in 2025.

Chinese and regional banks are eating into traditional strengths. Digital natives like Rakuten Bank (ironically, Mizuho's partner's sibling) are capturing younger customers. Foreign banks are cherry-picking the most profitable corporate relationships.

Competitive Analysis: The Three-Horse Race

Against Mitsubishi UFJ Financial Group (MUFG): MUFG is the thoroughbred—larger, more international, with better technology and risk management. Its acquisition of Union Bank gave it a meaningful U.S. presence that Mizuho lacks. MUFG trades at a premium to Mizuho for good reason.

Against Sumitomo Mitsui Financial Group (SMFG): SMFG is the operator's bank—efficient, focused, with the best cost-to-income ratios among the megabanks. While smaller than Mizuho by assets, it's more profitable and has avoided the operational disasters that plagued its rival.

Against Digital Challengers: This is where the real threat lies. SBI Holdings, Rakuten Bank, and a host of fintech startups are unburdened by legacy systems or branches. They're building the future while Mizuho is still fixing the past.

The China Question

Mizuho's exposure to China is both opportunity and risk. The bank has deep relationships with Japanese corporates operating in China, a valuable franchise as long as Japan-China relations remain stable. But in an era of increasing geopolitical tension, this exposure could become a liability.

The Verdict

The bull case requires believing that Mizuho has genuinely transformed—that the cultural changes are real, the IT fixes will hold, and management can execute on growth while maintaining stability. The bear case simply requires looking at history and betting that leopards don't change their spots.

The truth likely lies somewhere in between. Mizuho has genuinely improved, but whether it has improved enough to justify its valuation and compete effectively in a rapidly evolving financial landscape remains an open question.

XI. Epilogue: What Would Excellence Look Like?

The Path Not Taken

Imagine if, in 1999, the three banks had made different choices. What if, instead of a merger of equals, IBJ had been designated the clear leader, with its investment banking DNA driving strategy? Or if they had taken the radical step of building entirely new systems from scratch, rather than trying to connect three incompatible architectures?

The cost would have been enormous—probably $10-20 billion in 1999 dollars. But compared to the cumulative cost of two decades of failures, fixes, and lost opportunities, it would have been a bargain. Mizuho could have been Japan's JPMorgan, a globally competitive universal bank. Instead, it became Japan's Frankenstein's monster, stitched together from parts that never quite fit.

Can Legacy Institutions Truly Transform?

Mizuho's journey raises profound questions about institutional change. The bank has now spent more on transformation than some countries spend on defense. It has hired armies of consultants, replaced management multiple times, and been subjected to regulatory intervention that stopped just short of nationalization.

Yet the fundamental question remains: Can an institution truly transform its DNA, or does it simply learn to manage its dysfunction better? Mizuho in 2024 is certainly more functional than Mizuho in 2002, but is it a different organism or just the same creature with better medication?

The evidence suggests that true transformation is possible but rare. It requires not just new systems and processes but a cultural revolution that few organizations survive intact. Mizuho may have achieved this—or it may simply be in remission, with the old diseases waiting to resurface under stress.

The Broader Implications for Global Banking Consolidation

Mizuho's struggles offer lessons for banking consolidation worldwide. The push for scale, driven by regulatory costs and technology investments, continues to drive mergers. But Mizuho shows that scale without integration is worse than staying separate.

The successful bank mergers of the future will likely look different—more like acquisitions than mergers, with clear technology strategies from day one, and with cultural integration prioritized over financial engineering. The era of forcing incompatible institutions together and hoping for the best is over.

Final Reflections on Ambition vs. Execution

Mizuho's story is ultimately about the gap between ambition and execution. The ambition to create the world's largest bank was achieved, briefly. But without the ability to execute basic banking operations reliably, that ambition became a curse.

In finance, as in life, competence matters more than size, reliability matters more than innovation, and culture eats strategy for breakfast, lunch, and dinner. Mizuho learned these lessons the hardest way possible—through two decades of public failure and humiliation.

Whether Mizuho has truly internalized these lessons or is simply enjoying a temporary respite from its troubled history will only be revealed by the next crisis. The ATMs are working today, but in the banking business, today's success is just tomorrow's expectation. For Mizuho, the ghost of failures past will always loom over future ambitions.

The trillion-dollar merger that almost broke Japan has become something else: a survivor, scarred but still standing, profitable but not yet proven. Whether it becomes a phoenix or remains a cautionary tale is a story still being written in the gleaming towers of Otemachi and the server rooms where three banks' ghosts still whisper in COBOL.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube