James Hardie Industries: From Asbestos Empire to Fiber Cement King

I. Introduction & Episode Roadmap

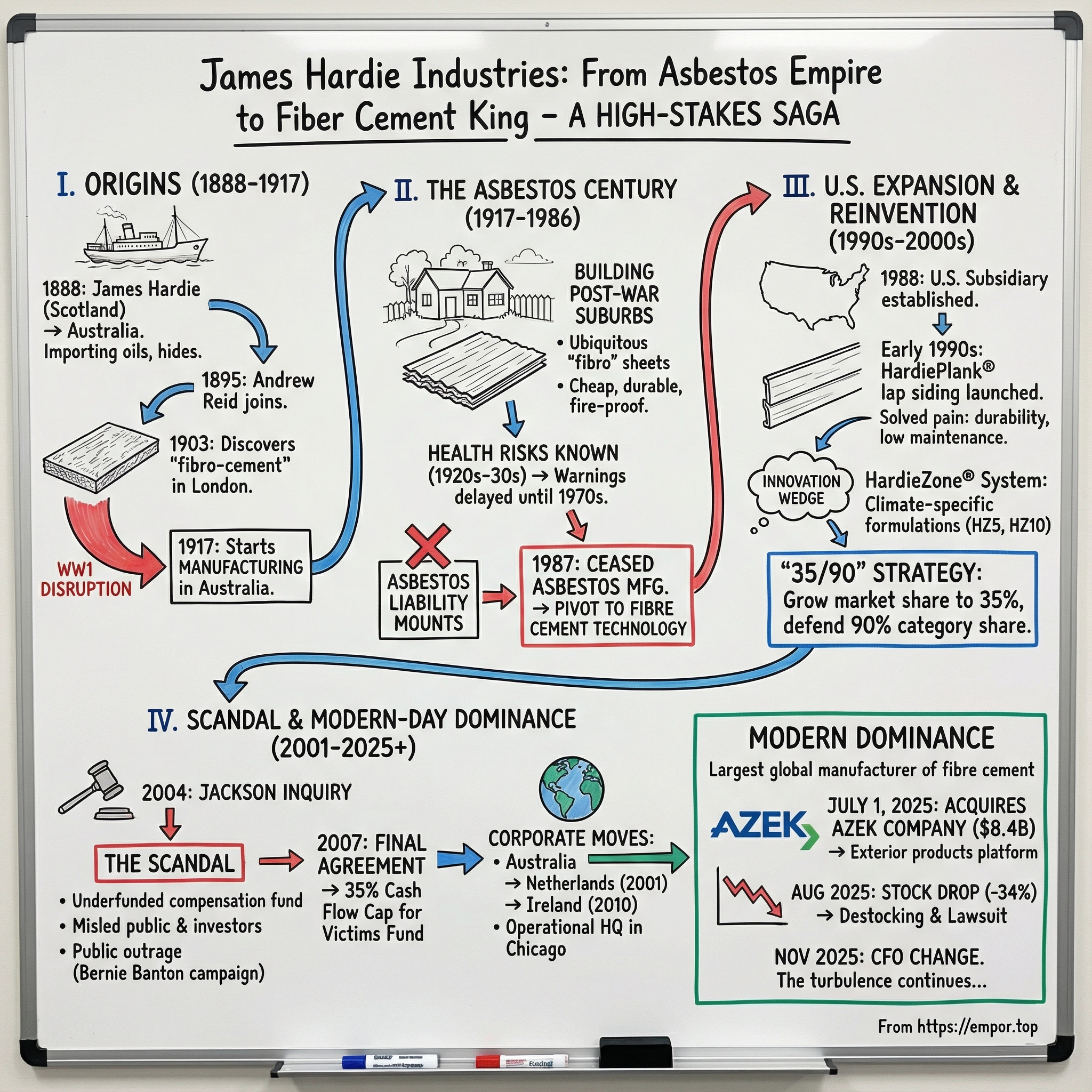

Picture this: it’s 2004, and one of Australia’s most recognizable corporate names is being hauled into a judicial inquiry. What comes out isn’t a minor governance slip-up. It’s an attempt—at least in the eyes of the public and eventually a commission of inquiry—to cut loose from a deadly legacy.

James Hardie is the company whose products quite literally built the post-war suburbs: the ubiquitous “fibro” sheets, the roofs and walls and fences that went up fast and cheap across a booming country. But the same material that made that expansion possible also left a trail of workers and families with asbestos-related disease. And now, in the early 2000s, many victims are being told the money set aside for compensation isn’t there.

Fast forward to today, and the twist is almost hard to believe: James Hardie isn’t just still standing. It’s a global building materials powerhouse—the largest global manufacturer of fibre cement products—headquartered in Ireland and cross-listed on the Australian and New York Stock Exchanges. And on July 1, 2025, it doubled down on the American exterior-products market by completing its acquisition of The AZEK Company in a cash-and-stock transaction representing an implied value of $8.4 billion, including the value of share-based awards and the repayment of AZEK’s outstanding debt.

So here’s the thesis of this deep dive—simple to say, staggering to unpack: how did an Australian company built on asbestos, one of the deadliest industrial materials in history, not only survive but become the global leader in fiber cement siding, effectively dominating the American housing market?

The modern answer starts with a deceptively plain slogan: “35/90.” It’s their plan to grow fiber cement’s share of the wood-look siding market from about 22% to 35%, while defending roughly 90% share of the fiber cement category itself. That kind of grip is rare outside the most winner-take-most markets. In North America—the company’s main geography—James Hardie holds about 90% of the fiber cement category, and that region contributes about 80% of group operating income.

Along the way, we’re going to hit some big themes: reinvention under existential pressure; one of the most significant corporate governance scandals in Australian history; the quiet power of material conversion in an otherwise sleepy building-products world; and a globe-spanning corporate footprint shaped by geographic and tax arbitrage across three continents. Ultimately, this is the playbook for how a company becomes synonymous with a category—and what it costs when the past refuses to stay buried.

And no, this isn’t a neat redemption arc. Even in 2025, the turbulence keeps coming. On August 19, 2025, James Hardie revealed that its North American fiber cement sales declined 12% during the quarter, driven by destocking first identified “in April through May” as customers worked back toward normal inventory levels. The company also said it expected that destocking to continue impacting sales for the next several quarters. The market punished the update immediately: the stock fell $9.79 per share—more than 34%—from $28.43 on August 19, 2025, to $18.64 on August 20, 2025. A securities class action lawsuit followed. And then, on November 17, 2025, James Hardie announced another jolt: CFO Rachel Wilson had decided to step down.

This is a company that has made a habit of surviving moments that should have ended it. Let’s unpack how it got here.

II. Origins: A Scottish Immigrant's Bet on a New Material (1888-1917)

In 1888, a Scottish tanner named James Hardie stepped off a ship in Australia and started a small importing business—oils, animal hides, the unglamorous inputs of industry. It was the kind of venture that could have stayed modest forever. Instead, it became the first move in a chain of decisions that would echo through more than a century of building, manufacturing, and—eventually—reckoning.

Hardie had been born in Linlithgow, Scotland, in 1851, into a tanning family. He learned the trade with his father, worked as an office manager and bookkeeper, and even became a partner in the family business before leaving for Melbourne, likely drawn by a milder climate and better commercial prospects. By early 1887, he was in Melbourne setting up an office importing machinery and chemicals for local tanneries. This was a man trained to keep the books clean and the risks measured.

That temperament mattered. Hardie wasn’t a swashbuckling founder. He was methodical, precise, financially conservative—someone whose idea of boldness was making a careful bet before anyone else had noticed the table. That approach helped build the company. It also imprinted a DNA that, decades later, would collide disastrously with the moral realities of what the company sold.

In 1895, Andrew Reid—also from Linlithgow—joined Hardie in Melbourne and became a full partner. It turned out to be a complementary pairing. Hardie was reserved; Reid brought charm, energy, and vision. Together, they had both the discipline to run a tight operation and the drive to push it into something bigger.

Then, in 1903, came the discovery that changed everything. On a trip to London, Hardie came across “fibro-cement”—a new roofing and lining slate made in France. The origin story has the texture of company folklore: samples sitting forgotten in the office of the firm’s London agents, until someone sold them to Hardie for £100.

Whether romanticized or not, the decision that followed was real. Hardie began importing fibro-cement into Australia. It was cheap, durable, fire-proof, and easy to transport—traits that fit Australia’s climate and construction needs perfectly. Demand surged. And as fibro-cement took off, James Hardie became the largest dealer of asbestos cement of its time.

Hardie’s edge was pattern recognition: spotting an emerging material before the market understood what it could become. Fibro-cement was unfamiliar in Australia, and importing it was a risk. But it quickly became a go-to option for sturdy, affordable building.

And then the world broke.

World War I didn’t just disrupt trade—it scrambled the basic mechanics of commerce. Shipping seized up. Markets closed. Capital flows slowed. Imports were cut off. For a company built on importing, it was the most serious threat imaginable.

So James Hardie did what defining companies do in defining moments: it changed its business model. Instead of importing fibro-cement products, the Reid-led firm decided to manufacture them in Australia. It still needed imported machinery at first, but by 1917 the company had started fibre-cement production at its own plants. What looked like a crisis response became a foundation for the next era—one that would boom after the war.

By then, the founder himself was already stepping away. James Hardie retired in 1911 and sold his half of the business to Andrew Reid. In 1912, he sold his interest in James Hardie & Co. to Reid for £17,000. The name stayed. But from that point on, it was the Reid family—leading the company from 1911 until 1995—that would drive the expansion through the century ahead.

The early playbook, in hindsight, is simple: find the overlooked material, then build the machinery—and the organization—to scale it. In the decades that followed, that same instinct would make James Hardie huge. It would also tie the company to one of the deadliest industrial legacies in history.

III. The Asbestos Century: Building Australia's Suburbs (1917-1986)

In the decades after World War I, James Hardie completed its first great transformation: from an importer of fibro-cement into a full-scale Australian manufacturer. What began as a wartime necessity became a machine for mass production—perfectly timed for a country about to build, and build fast.

By the mid-twentieth century, that machine was enormous. James Hardie had become Australia’s largest manufacturer and distributor of asbestos-containing products—building materials, insulation, pipes, and even brake linings. It ran asbestos plants across the country: New South Wales, Queensland, South Australia, Victoria, and Western Australia. If you lived or worked in a modern Australian building in that era, chances are some piece of it passed through Hardie.

To understand the company’s grip on the culture, you have to understand what “fibro” meant in Australia. The fibro house was the postwar shortcut to home ownership: affordable, fast to put up, and marketed as fire-resistant. It wasn’t just a material; it was a look, a lifestyle, a physical symbol of the suburban boom. Homes, schools, factories, commercial buildings—millions of structures ended up wrapped in Hardie-made sheet, roofing, fencing, and pipes.

The business story, at least on paper, looked like a classic industrial winner. James Hardie listed on the Sydney Stock Exchange in 1951, by which point asbestos cement sheet and related building materials were central to what it made and sold.

And it kept pushing the technology. The company invested in more modern equipment in 1937. It expanded upstream into mining too, forming Asbestos Mines Pty Ltd. in 1944 alongside CSR’s Wunderlich. It developed a new production method—the autoclave, or steam-curing, process—and launched it in 1959, helping scale output and standardize quality.

It also diversified well beyond sheets and pipes. In 1961, it merged its brake lining division with Turner & Newall’s Ferodo, taking a 60% stake in Hardie-Ferodo, then buying the remaining 40% in August 1980. In 1978, it acquired the Australian publishing and paper operations of Reed International. This wasn’t a company content to be a one-product manufacturer; it wanted to be a conglomerate.

But running under the success narrative was the part of the story that would eventually define the company’s name for a generation: the risks of asbestos weren’t a mystery. Asbestosis had been identified in the 1920s. The link between asbestos and lung cancer was recognized by medical experts in the 1930s. And yet product warnings didn’t appear until the 1970s.

Inside the company, the alarms were louder than the public ever heard. A safety officer repeatedly pushed management to improve working conditions and put warnings on products. In 1964, he wrote to senior leaders that asbestos was “one of the most dangerous of all industrial poisons.” The response, effectively, was to carry on.

By 1978, the consequences were becoming visible—pleural abnormalities and other asbestos-related diseases emerging among former mine workers. James Hardie wasn’t the only company involved in asbestos, most notably CSR. But the legal shadow concentrated heavily on Hardie: more than half of the claims made to the Dust Diseases Tribunal of New South Wales in 2002 were brought against companies in the James Hardie group.

The scale of exposure was staggering. Around 90% of Australia’s asbestos consumption occurred in cement manufacturing—underscoring just how deeply embedded asbestos was in everyday construction. Estimates suggest roughly 30% of Australian homes built before 1982 contained asbestos products, with even higher use in public buildings like schools.

And yet, even as the evidence mounted—and even as the future liability became harder to ignore—James Hardie was already building the off-ramp. In the mid-1980s, it developed asbestos-free fibre cement technology. It began moving toward what would become the modern formula: largely Portland cement, sand, and wood fibres.

In 1987, James Hardie ceased all asbestos manufacturing, replacing asbestos cement sheet with asbestos-free fibre cement—the core product it still sells today. This was a technical breakthrough, and later it would be framed as a moral pivot too.

But the more brutal reading is simpler: this wasn’t a sudden awakening. It was the business reality catching up—regulation tightening, lawsuits rising, and asbestos becoming commercially and legally untenable. Hardie had built the country’s largest asbestos business while the dangers were known. Now it was trying to exit the product line.

The pivot to fibre cement was brilliant strategy. What it did—and didn’t do—for the people harmed by the asbestos era would become the fight that defined the next chapter.

IV. The U.S. Expansion: The Real Transformation (1990s-2000s)

James Hardie’s reinvention doesn’t really happen in Australia. It happens in the U.S.—and it starts with a bet that very nearly failed.

In 1988, the company set up a U.S. subsidiary with a simple ambition: take the asbestos-free fibre cement technology it had developed back home and introduce it to the American building market. The U.S. housing industry was enormous, fragmented, and hungry for materials that could last. If Hardie could win there, it wouldn’t just find growth—it would find a new identity.

Using the manufacturing and technical expertise it had built in Australia, James Hardie expanded operations in the United States and began positioning itself as a specialised producer of fibre cement building materials.

Then, in the early 1990s, it brought a flagship product to market: HardiePlank® lap siding. It landed because it solved real pain. Homeowners and builders didn’t need a lecture on “materials science”—they needed something that held up, didn’t demand constant upkeep, and could take a beating from weather. HardiePlank promised durability, low maintenance, and strong resistance to the elements. In a category full of compromises, it felt like a step-change.

Still, the early years were rough. Fibre cement wasn’t a familiar category in America. That meant James Hardie wasn’t just selling a product—it was trying to teach a market how to buy. Contractors were skeptical. Distributors hesitated. The initial performance was underwhelming enough that a less patient management team might have pulled the plug.

That patience mattered. If James Hardie had exited the U.S. after those first disappointing years, it likely never would have become the giant it is today.

The turning point was innovation—not as a buzzword, but as a wedge. In the 1990s, Hardie kept refining fibre cement for American conditions and then pushed a breakthrough that made the product feel purpose-built, not generic: the HardieZone® System, with siding formulated for the weather demands of a home’s specific geography. With U.S. operations based in Chicago, the company backed this approach with a research and development budget in the tens of millions of dollars annually—among the largest in the siding industry.

The idea was straightforward and surprisingly powerful: climates aren’t the same, so siding shouldn’t be either. Much like fuel blends that vary by region, Hardie engineered different fibre cement formulations for different parts of the country. The HardieZone System evaluates eight climatic variables that affect long-term performance and translates them into 10 distinct zones. From there, James Hardie designed product lines around lived reality: HZ5® for much of the Midwest and Northeast, where snow, ice, and big temperature swings punish building exteriors; and HZ10® for much of the South and Southwest, where heat, humidity, sun, and heavy rain create a different kind of wear.

As one former James Hardie Director of Products and Segments put it: "Fiber cement siding became the leading siding choice in the United States since its introduction in the early 1990s because it provided a better alternative to vinyl, wood-based and aluminum siding, the norm for that time."

And because James Hardie was the first manufacturer to go all-in as an exclusive fibre cement pure-play, it started to own the category in the public mind. “Hardie” became shorthand for fibre cement. In building products, that kind of mental real estate is rare—and once you have it, it becomes a compounding advantage.

By the late 1990s, the U.S. business had turned into the growth engine. By May 2003, at the end of its fiscal year, a streamlining effort appeared to be working: the company reported profits of $170 million on sales of more than $800 million. It had also become the clear leader in U.S. fibre cement, and by then the American operation accounted for more than 85 percent of the group’s annual sales.

But success created a new problem—one that didn’t show up in product reviews or contractor feedback. It showed up in the corporate structure.

As U.S. earnings grew, James Hardie ran into financial inefficiencies tied to its existing setup and its predominantly Australian shareholder base. To maintain dividends and meet obligations in Australia, the company would have needed to repatriate profits from the U.S.—and that would have triggered significant U.S. withholding taxes. The end result: lower after-tax earnings and less cash available for distributions.

This tax friction became the stated rationale for a restructuring. And that restructuring would soon collide with something far bigger than dividends: the company’s attempt to manage— and, critics would argue, escape—its asbestos-era liabilities.

V. The Asbestos Scandal: Corporate Infamy and Redemption (2001-2012)

This is the part of the James Hardie story that could fill an entire Acquired episode by itself—one of the most notorious corporate governance scandals in Australian history, and the moment when the company’s attempt to engineer a clean break from its past collided with public reality.

The Separation Scheme (2001)

To make sense of what happened, you have to start with the plumbing.

Since the 1930s, James Hardie operated as a parent company sitting above a web of subsidiaries. The asbestos business—and critically, the responsibility for compensation—lived down in those subsidiaries, principally James Hardie and Coy and Hardie-Ferodo (later known as Jsekarb). And in the late 1990s, as asbestos liabilities grew more visible, the group began shifting assets out of those operating companies. The subsidiaries were later renamed Amaca and Amaba. They were left holding most of the asbestos liabilities, but with far fewer assets to match.

Then came 2001.

James Hardie created the Medical Research and Compensation Foundation, or MRCF, and seeded it with $293 million. The company’s public line was clear: this fund would meet all future asbestos claims. And with that set up, James Hardie moved offshore—relocating to the Netherlands—leaving the MRCF behind to handle the legacy.

CEO Peter McDonald reinforced the message in public announcements: the MRCF had sufficient funds, and James Hardie would not provide further substantial funding. On paper, it even looked plausible at first. The foundation’s net assets were $293 million—mostly real estate and loans—and this exceeded the “best estimate” of $286 million in liabilities from an actuarial report commissioned by James Hardie.

The problem was that the “best estimate” wasn’t just wrong. A judge would later call it “wildly optimistic.”

The Funding Shortfall Exposed

The cracks showed quickly.

Not long after the restructure and offshore move, another actuarial report put likely asbestos liabilities at $574 million. The MRCF asked James Hardie for additional support. James Hardie offered $18 million in assets. The foundation rejected it.

And then the numbers kept climbing. The estimate was revised to $752 million in 2002, and then to $1.58 billion in 2003.

In other words: the foundation was established with $293 million, and within just a couple of years the scale of expected obligations had ballooned into the billions. The MRCF’s money ran out. James Hardie refused to top it up. The result was predictable and explosive—fierce criticism from unions, governments, and the media, with the company painted as trying to walk away from the people its products had harmed.

The Jackson Inquiry (2004)

By early 2004, it had escalated beyond a corporate dispute. On 12 February 2004, the Government of New South Wales commissioned a judicial inquiry. NSW Premier Bob Carr set it up with powers similar to a royal commission, and appointed David Jackson, QC, to lead it.

The Commission sat for nearly 200 hearing days, taking evidence from former directors, employees, actuaries, and solicitors. After detailed submissions, Jackson delivered a two-volume report—devastating in both tone and content.

The inquiry found that James Hardie deliberately underfunded the compensation foundation as part of a corporate restructuring designed to limit its asbestos liabilities. Jackson’s report went further: it concluded that Hardie’s senior managers systematically and deliberately misled the actuaries, misled the board, misled the foundation, misled the stock exchange, misled the Supreme Court, and misled victims and unions—while repeatedly assuring everyone that the foundation was fully funded.

Jackson estimated that, on the projections at the time, the foundation would be exhausted by 2007, and that total liabilities would be at least A$1.5 billion. The report also concluded that the “best estimate” had been “wildly optimistic,” and that the liability estimates were “far too low.”

And crucially, it wasn’t framed as an honest mistake. The Commissioner found the MRCF was created for commercial reasons—specifically, to rid the group of asbestos liabilities so it could raise capital and list on the U.S. Stock Exchange. He found the MRCF was massively underfunded, that CEO Peter McDonald knew it, and that the Board ought reasonably to have known it. Jackson also found that the actions of James Hardie, McDonald, and CFO Peter Shaffron were in breach of the law.

Bernie Banton and Public Pressure

Corporate scandals often turn on documents and board minutes. This one turned on a human face.

Bernie Banton became the public symbol of the campaign to force James Hardie to pay compensation to victims—people who developed asbestos-related diseases after working for the company or being exposed to its products. Bernard Douglas Banton AM (13 October 1946 – 27 November 2007) had been a builder, and later became a social justice campaigner. In January 1999, he was diagnosed with asbestosis and asbestos-related pleural disease—decades after working at James Hardie making asbestos lagging.

Banton’s exposure came from his time at Hardie’s insulation factory from 1968 to 1974, where he worked as a plane operator producing asbestos insulation blocks and pipe sections. He described what it was like: “I was often covered in a fine white dust. It was on my face, skin, hair and clothes. There was so much dust on my clothes that I used compressed air to get rid of the dust…. There was so much dust around, that getting dust in my eyes and nose was just a part of the routine.”

He told the ABC: “I’ve said right from the beginning of this fight that until they put me in a box, I’ll be out there fighting.”

The pressure campaign became enormous. In 2004, major mobilisations targeted the parent company. Unions including the AMWU and CFMEU played leading roles, with rallies of tens of thousands under the banner “Make James Hardie Pay.” Construction unions announced bans on Hardie products at worksites. Governments boycotted James Hardie products. Unions threatened to push a global union movement refusing to handle Hardie products.

Hardie had tried to make this a contained corporate restructuring. It became a national political crisis.

The Final Agreement (2007)

Eventually, the company came to the table. James Hardie agreed to guarantee a fund of $4 billion to cover future obligations to asbestos victims. Prosecutions of James Hardie board members and senior executives followed.

A key element of the agreement was the mechanism that still defines this saga today: the cash-flow cap. Each year, an independent actuary assesses expected liabilities based on the estimated number of asbestos victims. James Hardie must then meet that obligation through contributions to the Asbestos Injuries Compensation Fund (AICF), subject to a limit of 35 per cent of its cash flow. The logic, as described at the time, was that “this percentage figure strikes a three-way balance of appeasing investors, allowing the company to still prosper and ensuring adequate funds are available to continue compensating claimants now and into the future.”

In February 2007, 99.6% of shareholders voted in favour of the scheme, and it began operating days later.

Director Convictions

The legal consequences didn’t end with the agreement.

In 2009, the Supreme Court of New South Wales found that directors had misled the stock exchange about James Hardie’s ability to fund claims. They were banned from serving as board members for five years. Former chief executive Peter Macdonald was banned for 15 years and fined $350,000 for his role in forming and publicising the MRCF.

In May 2012, the High Court upheld the 2009 decision and found that seven former James Hardie non-executive directors did mislead the stock exchange over the asbestos victims compensation fund.

Bernie Banton didn’t live to see that final vindication. He died of mesothelioma on 27 November 2007. He was 61. Greg Combet, then formerly Secretary of the ACTU and a key figure in the campaign, said that without Banton the company might never have been brought to account: “Without Bernie, there may have been people with asbestos diseases today who would not have access to compensation. Bernie had a rare capacity, a capacity to connect with people and to inspire in them the same passion for justice that he himself felt and he moved the Australian community.”

For investors, the James Hardie asbestos scandal is the corporate governance lesson written in permanent marker: clever legal structures can shift liabilities around on paper, but they can’t erase moral obligations. The only question is the price of the reckoning—and whether the company survives long enough to pay it.

VI. The Modern Era: Geographic Shift and Market Dominance (2010-2022)

Once the compensation deal was in place, James Hardie kept doing what it had already proven unusually good at: moving its corporate shell while keeping the operating engine pointed squarely at the U.S.

The company had relocated its headquarters to the Netherlands in December 2001. But by 2010, it moved again—this time re-domiciling to Ireland.

The reason wasn’t brand or symbolism. It was friction. In the Netherlands, James Hardie faced a requirement that management be located there, plus what it described as an ongoing risk of costly disputes with the IRS—disputes that could have carried annual penalties of up to US$50 million. The Board looked at alternatives, including moving the domicile to the U.S. or back to Australia, but Dutch corporate law made a clean exit hard. One path required acceptance by 95% of the entire issued share capital—seen as practically impossible. Another path allowed a move within the European Union with a more realistic hurdle: 75% of votes cast. After extensive review, that was the route the company pursued, landing in Ireland.

The offshore chapter came with its own aftershocks. The Netherlands move produced tax savings of $86 million over seven years, but in 2009 the Australian Taxation Office issued an amended assessment for $172 million, plus interest and penalties. James Hardie successfully appealed the assessment.

If the corporate address kept changing, the center of gravity didn’t. The company’s management team ended up in Chicago, Illinois, reflecting what had become the core reality of the business: James Hardie was now, operationally, an American housing story. It operates a corporate office in Chicago and runs more than a dozen manufacturing plants around the world.

And the moat it built in the U.S. wasn’t just brand. It was physical. James Hardie established an unusually dense manufacturing footprint—10 manufacturing sites across the United States—so it could stay close to customers and deliver product with minimal lag. In construction, where schedules are unforgiving and delays cascade, that logistics advantage matters. It also makes life hard for smaller fibre cement competitors who can’t match the same proximity and reliability.

The broader market moved in Hardie’s direction too. Over the five years to 2022, Census Bureau data shows fibre cement gaining share in new U.S. home construction, with fibre cement used on 23% of new house completions in 2022.

Just as important: the company widened its focus beyond new builds. Historically, James Hardie’s base was new construction, working closely with builders and contractors. Over the past decade, it found growing traction in repair and renovation by reaching homeowners more directly. Around 65% of its volume now comes from the R&R market. With roughly 40 million North American homes older than 40 years—a common age for major renovations—James Hardie sees R&R as its biggest long-term growth opportunity. And with homeowner wealth and equity at all-time highs, the company believed the spending power for those projects was there.

Even its pricing strategy reflected the posture of a category leader. With plenty of alternatives available, James Hardie aimed to keep pricing competitive, while protecting margins through cost efficiencies that come with volume. And it signaled a willingness to let margins fall if that helped win share—a very different stance from the typical building-products playbook of defending price at all costs.

The Aaron Erter Era

In September 2022, James Hardie appointed Aaron Erter as Chief Executive Officer, effective immediately. Erter joined from a long run in large North American industrial and consumer businesses: CEO of PLZ Corp, Global President at Sherwin-Williams for its consumer and industrial businesses, and senior vice president and general manager of Valspar’s consumer business, along with earlier sales and marketing leadership roles at Stanley Black & Decker. He holds a bachelor’s in economics from The Wharton School at the University of Pennsylvania and an MBA from the University of Notre Dame.

The hire signaled intent. With a background steeped in premium coatings brands, Erter fit the direction James Hardie had been leaning into: a more consumer-centric company, pushing harder on end-homeowner engagement and an 80/20 style of prioritization—concentrating resources on the initiatives that move the needle most.

VII. The AZEK Acquisition: Doubling Down on America (2025)

The AZEK acquisition was a defining moment—James Hardie’s clearest statement yet that its future would be built around the American homeowner.

On July 1, 2025, James Hardie Industries plc completed its previously announced acquisition of The AZEK® Company in a cash-and-stock deal: $26.45 in cash plus 1.0340 ordinary shares of James Hardie for each AZEK share, totaling $54.18 per share. All in, it represented an implied value of $8.4 billion, including the value of share-based awards and the repayment of AZEK’s outstanding debt.

Strategically, the logic was simple: expand from “siding and trim” into a broader exterior home-products platform. Together, James Hardie and AZEK pitched a business with faster growth, peer-leading profitability, and strong cash generation.

The combined portfolio now spans a lineup of high-performance, low-maintenance exterior brands: Hardie®, TimberTech®, AZEK® Exteriors, Versatex®, StruXure®, Ultralox® and Intex®. In practical terms, it meant James Hardie could walk up to a builder—or a homeowner—and offer a more complete package: siding, decking, trim, railing, and pergolas that could be designed to work together.

That’s the heart of the deal: James Hardie’s siding and trim muscle paired with AZEK’s leadership in decking and outdoor living, creating a one-stop exterior solutions provider for cohesive, high-end designs.

The acquisition also broadened the company’s ambition. Management said it expanded James Hardie’s total addressable market in North America to $23 billion. The company projected at least $125 million of cost synergies and $500 million of commercial synergies, translating to at least $350 million of additional annual adjusted EBITDA, with the full run-rate impact expected three to five years after closing.

There was also a capital-markets clean-up tied to the new era. The previously announced termination of James Hardie’s American Depositary Share program took effect on July 1, 2025, and the company’s ordinary shares began trading on the NYSE under the symbol “JHX.”

Leadership continuity was part of the message. As previously announced, Aaron Erter and Rachel Wilson stayed on as CEO and CFO after the deal closed. The company also named key AZEK-related roles: Jon Skelly was appointed president – AZEK Residential; Sam Toole joined as chief marketing officer, AZEK brands; and Chris Russell joined as VP, global strategy and corporate development. Jesse Singh, Howard Heckes, and Gary Hendrickson joined the James Hardie Board of Directors.

The August Shock

And then, almost immediately, the story swerved.

On August 19, 2025—just weeks after closing the transformational AZEK acquisition—James Hardie told the market its North American fiber cement sales had declined 12% during the quarter. The culprit, it said, was destocking first identified “in April through May,” as customers worked to return to more normal inventory levels. The company also warned that the destocking was expected to keep weighing on sales for the next several quarters.

Investors didn’t wait around for the longer explanation. The stock dropped hard, falling $9.79 per share—more than 34%—from $28.43 on August 19, 2025, to $18.64 on August 20, 2025.

The timing made it worse. The complaint alleges that management knew by April and early May 2025 that distributors were aggressively destocking, but continued to mislead investors by touting sales that were allegedly inflated by inventory loading rather than genuine demand.

A class action lawsuit followed. Then, on November 17, 2025, the company announced that Rachel Wilson would step down as CFO. Ryan Lada was appointed Chief Financial Officer in November 2025. Before joining James Hardie, Lada served as CFO at Watts Water Technologies, and immediately prior to that as CFO at AZEK, where he led the finance function through operational transformation and strategic portfolio evolution that culminated in the acquisition by James Hardie.

So, almost as soon as James Hardie completed the deal meant to define its next chapter, it found itself managing another crisis—different in nature from the asbestos scandal, but destabilizing in its own way. The stock turned volatile. Litigation added uncertainty. And for long-term investors, the question became a familiar one in building products: was this simply a temporary channel reset, or a warning flare about underlying demand?

VIII. Playbook: Business & Investing Lessons

Lesson 1: Existential Crisis Can Force Reinvention

The asbestos scandal could have ended James Hardie. Instead, the company survived because it had already built a different core: asbestos-free fibre cement. The shift from “asbestos cement” to “fibre cement” was technical, yes—but it was also strategic, and it changed what kind of business Hardie was. None of this excuses the moral failure. It’s simply the hard lesson: when a company hits an existential wall, the ones that make it through often do so by becoming something else entirely.

Lesson 2: Geographic Arbitrage and Tax Optimization

James Hardie’s corporate migrations—Australia to the Netherlands to Ireland, while the operating center of gravity moved to the U.S.—show a company willing to rewire its structure to reduce friction and preserve after-tax earnings. In 2000, it transferred its registration to Amsterdam to benefit from more favorable tax treaty treatment with the United States; under the Australian-U.S. tax treaty, the company said nearly 75 percent of shareholder profits were taken up by taxes. The maneuver was controversial, but the broader point is clear: geography can be a balance-sheet lever, and Hardie pulled it—repeatedly.

Lesson 3: The Power of Becoming Synonymous with a Category

James Hardie is, for many people, fibre cement. It pioneered the technology for the construction industry beginning in the 1970s and then scaled it into dominance in the U.S., where the siding segment became a Hardie-led world. When you own the category in the customer’s mind, you don’t just sell product—you shape the shelf, the contractor habits, and the default choice. That brings real advantages: distribution pull, contractor loyalty, and the kind of mindshare competitors struggle to dislodge.

Lesson 4: Patient Capital in New Markets

The U.S. expansion wasn’t an immediate win. In the early years, performance was weak enough that a less committed company could have walked away. If James Hardie had exited the U.S. market after that rocky start, it likely never would have become the industry giant it is today. The lesson for operators and investors is simple: patient capital isn’t about tolerating underperformance forever—it’s about staying in the fight long enough to earn the right to win.

Lesson 5: The Manufacturing Footprint as Moat

In building products, proximity matters. Local manufacturing doesn’t just cut freight costs—it reduces lead times and improves reliability, which can make or break a jobsite schedule. James Hardie’s ten manufacturing sites across the U.S. function as more than capacity; they’re a moat. They enable faster delivery and support climate-specific products, and they create an operational advantage that smaller fibre cement competitors can’t easily replicate.

Lesson 6: Stakeholder Capitalism Under Duress

The asbestos compensation framework is an unusually explicit form of ongoing stakeholder obligation. Under the 35% cash flow cap, James Hardie is required to fund claims through contributions to the Australian asbestos victims compensation fund, with that arrangement running until 2045. What’s notable isn’t just that the obligation exists—it’s that the company has remained profitable and grown while carrying it. This is what balancing stakeholders looks like when it isn’t a slogan: victims, shareholders, and employees all pulling on the same finite pool of cash, year after year.

IX. Framework Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's Five Forces

1. Threat of New Entrants: LOW

Fibre cement is not a garage-startup business. Building plants is expensive, distribution is hard, and earning contractor trust takes years. James Hardie operates six production plants in the United States and has continued expanding capacity, which raises the bar even further for anyone trying to break in. On top of that, the market beyond Hardie is fragmented—smaller players tend to appear and disappear—while regulatory requirements, testing, and safety certifications add yet another layer of friction.

2. Bargaining Power of Suppliers: MODERATE

Inputs like cement, pulp, and sand are largely commodities, and there are multiple suppliers globally—so no single vendor should have the company over a barrel. James Hardie also keeps sourcing local: about 83 percent of its raw materials are purchased within 100 miles of its plants. That strategy lowers freight costs and reduces supply chain risk, but it doesn’t eliminate exposure to broader input-cost swings.

3. Bargaining Power of Buyers: MODERATE

The buyer dynamic is split. Big builders have leverage, but they also care deeply about reliability and jobsite execution—missed deliveries and inconsistent quality are expensive in ways that don’t show up on an invoice. At the same time, James Hardie has worked to pull demand from the other end of the chain by marketing directly to homeowners, emphasizing durability, design, and overall value. As homeowners increasingly influence materials choices—not just contractors—brand and perceived quality help sustain premium positioning.

4. Threat of Substitutes: MODERATE-HIGH

Over the past two decades in the U.S., fibre cement has steadily taken share from vinyl, brick, and wood, largely because it holds up better and delivers stronger curb appeal than cheaper options like vinyl. But substitutes still matter. Vinyl remains meaningfully cheaper, and in a recession consumers can trade down. So while the trend has favored fibre cement, the category still competes against “good enough” alternatives—especially when budgets tighten.

5. Competitive Rivalry: LOW-MODERATE

Globally, fibre cement has several large players. The top four manufacturers—James Hardie, Etex Group, Swisspearl Group, and Mahaphant—collectively account for about 24% of global market share, suggesting a market that’s not perfectly consolidated but not a free-for-all either. In the U.S. specifically, James Hardie is the clear leader, supported by a broad product portfolio and an established distribution network across North America (and reach into Europe and Asia-Pacific). That leadership position tends to dampen price wars—but it doesn’t eliminate competition, especially around the edges.

Hamilton Helmer's 7 Powers Analysis

1. Scale Economies: STRONG

James Hardie’s scale shows up in the fundamentals. It has kept gross margin steady at around 35% through big swings in end-market activity. Part of that is manufacturing leverage, and part is product positioning: its fibre cement exterior products offer attributes that many buyers view as superior to alternatives, and in the U.S. it holds roughly 90% share of the fibre cement category.

2. Network Effects: WEAK

There’s no classic network effect here—siding doesn’t get more valuable because your neighbor bought it. But there is a softer kind of reinforcement: contractor familiarity. The more a product becomes the default on jobsites, the more it builds an “ecosystem” of habits, training, and preference that tilts repeat business in its direction.

3. Counter-Positioning: STRONG (Historically)

As one former James Hardie Director of Products and Segments put it: "Fiber cement siding became the leading siding choice in the United States since its introduction in the early 1990s because it provided a better alternative to vinyl, wood-based and aluminum siding, the norm for that time." That shift is classic counter-positioning. Incumbent vinyl and wood players couldn’t easily pivot into fibre cement without undermining the very businesses that made them successful.

4. Switching Costs: MODERATE

Switching costs aren’t contractual for every customer, but they are real in practice. Contractors who are trained on James Hardie products often prefer to stick with what they know. Builders with established supplier relationships and operating rhythms face friction when switching. And multi-year exclusive agreements with major builders can lock in demand and raise the cost of experimenting with alternatives.

5. Branding: STRONG

James Hardie is the #1 brand of siding in North America. That matters more than most people think in building materials, where both contractors and homeowners tend to prefer known quantities—especially when the decision is expensive, visible, and hard to reverse.

6. Cornered Resource: MODERATE

James Hardie pioneered asbestos-free fibre cement technology in the mid-1980s. Today, its proprietary formulations, climate-specific engineering, and manufacturing processes represent meaningful know-how and intellectual property. It’s not a single “owned” resource no one else can access, but it is a durable advantage built over decades.

7. Process Power: STRONG

The HardieZone System, built around eight climatic variables that affect long-term siding performance, is a good example of process power: accumulated learning translated into product design, manufacturing discipline, and quality control. That kind of refinement is difficult to replicate quickly—even for well-funded competitors.

Key Metrics for Ongoing Monitoring

For long-term fundamental investors tracking James Hardie, three KPIs are especially worth watching:

-

North American Fiber Cement Volume Growth: This is the clearest read on share gains—and on whether the “35/90” strategy is working. The key signal is whether Hardie grows faster than underlying housing activity; that divergence usually means share capture.

-

EBIT Margin in North America: Management targets around 30% EBIT margins. Staying above that level suggests pricing power and strong execution; sustained compression can indicate competitive pressure, cost inflation, or an unfavorable mix shift.

-

Free Cash Flow After AICF Contributions: The asbestos funding framework matters. Because contributions to the Asbestos Injuries Compensation Fund are capped at 35% of cash flow, investors should focus on the cash that remains after those payments—what’s actually available for dividends, buybacks, and growth.

Current Legal Overhang

One more thing investors can’t ignore: the pending securities class action lawsuit filed after the August 2025 stock drop. The suit alleges misleading statements about inventory levels. James Hardie has denied wrongdoing, but litigation can still create uncertainty and expense. The CFO transition—Rachel Wilson stepping down, with Ryan Lada appointed in November 2025—adds another variable for markets to interpret as this plays out.

Final Observations

James Hardie Industries has one of the most complicated corporate stories in building materials. It helped build Australia’s suburbs with a product that later proved devastating. It then tried to draw a hard corporate line between itself and the people harmed by that legacy—only to be pulled back by public outrage, politics, and the courts. And somehow, after all of that, it remade itself into the dominant force in American fibre cement siding.

The AZEK acquisition is the newest turn in that reinvention: a move from being primarily a siding-and-trim company into a broader exterior and outdoor living platform. But the timing also underscored a hard truth about this business. Even the category leader isn’t immune to the messy mechanics of the channel. The August 2025 destocking shock—and the litigation that followed—was a reminder that cyclicality, inventory swings, and execution risk can hit fast, even when the long-term strategy makes sense.

Zoom out, and the backdrop is still attractive. The global fibre cement market is expected to reach 35.59 million tons in 2024 and grow at a 6.24% CAGR to 51.18 million tons by 2030. James Hardie sits squarely in the middle of that growth, with advantages—brand, manufacturing footprint, contractor mindshare, climate-specific product know-how—that took more than a century to assemble.

And hovering over everything is the obligation that never really goes away: asbestos compensation. The requirement to contribute up to 35% of cash flow through at least 2045 is both a continuing burden and the closest thing this story has to a structural form of accountability. The company that once tried to ring-fence victims now operates under a framework designed to keep paying them, year after year, while still allowing the business to invest and return capital.

So the investment question is straightforward, even if the story isn’t. You’re betting on fibre cement continuing to take share in the U.S., on the AZEK integration delivering what the deal promised, and on management navigating the current headwinds without losing the category leadership the company fought so hard to build. James Hardie has survived crises that should have ended it. Whether this moment is a temporary digestion phase or the start of something more serious is the next chapter.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube