Gunkul Engineering: Thailand's Power Chameleon

I. Introduction & The Hook

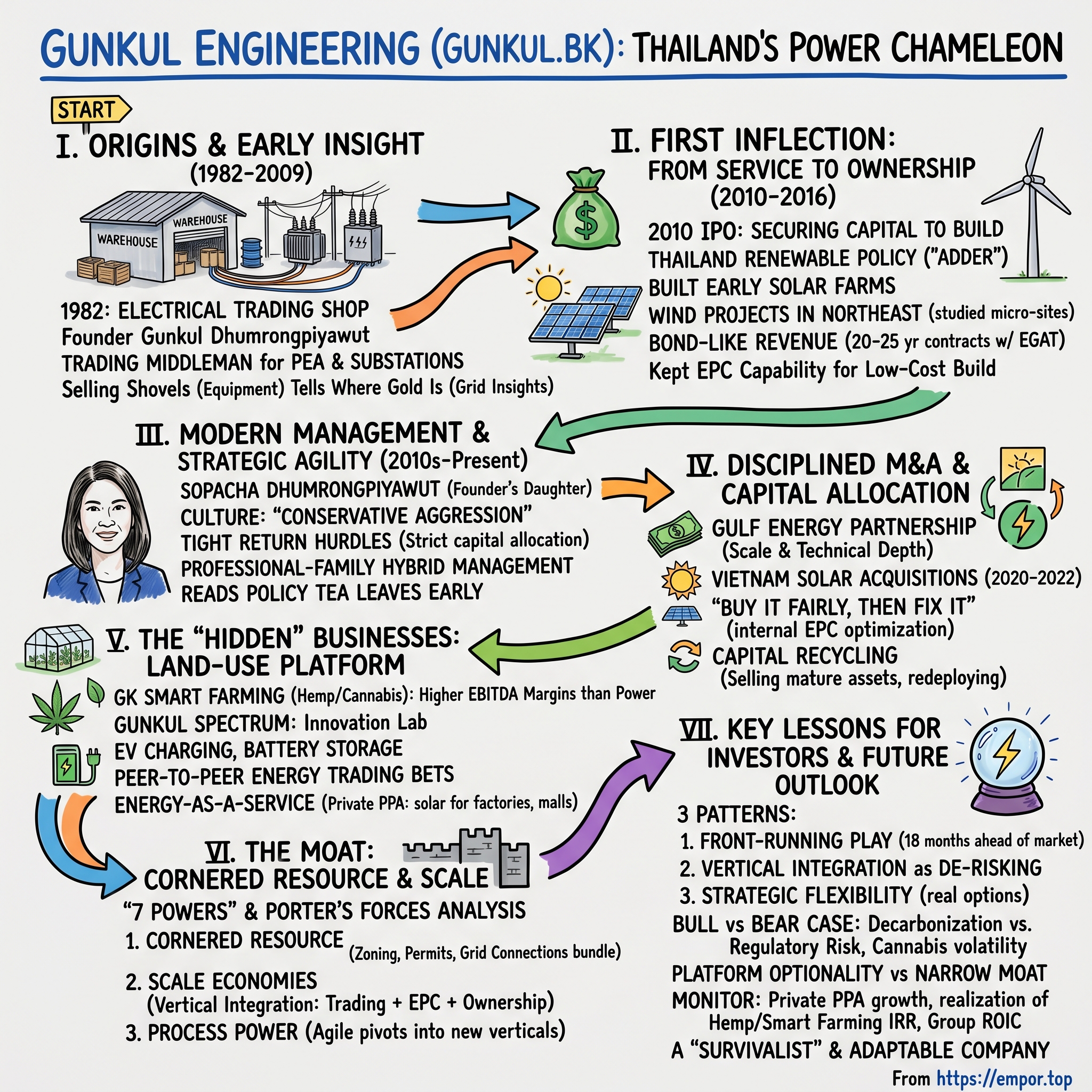

Picture a warehouse in suburban Bangkok in 1982. Outside, the air is thick with the diesel hum of a country still deciding what kind of economy it wants to be. Inside, a young electrical engineer named Gunkul Dhumrongpiyawut is unpacking crates of transformers and cable reels. He is not building anything yet. He is buying and selling—a middleman, a trader, a fixer for the Provincial Electricity Authority and the dozens of provincial substations that dot the northeast. Nothing about this scene suggests renewable energy. Nothing about it suggests wind turbines spinning across the hills of Nakhon Ratchasima, or solar farms slung across the Mekong Delta, or—most improbably of all—rows of high-tech cannabis plants flowering under LED light inside climate-controlled greenhouses leased from the company's own wind farm footprint.

But that is the thing about Gunkul Engineering. If you had drawn a line from that 1982 trading shop to any plausible future, you would not have drawn this one.

This is the story of how a provincial electrical equipment distributor metamorphosed into one of Thailand's most nimble renewable energy developers, and then—in a twist so strange that even seasoned utility analysts needed two readings of the annual report to believe it—added industrial-scale cannabis cultivation as a growth vertical. Along the way it built a joint venture with Gulf Energy, Thailand's 800-pound gorilla of power; it swept into Vietnam buying up distressed solar assets at the bottom of the cycle; it started selling electrons directly to factories through private power purchase agreements; and it quietly began laying the groundwork for EV charging and peer-to-peer energy trading in a country where both remain closer to slide-deck than to reality.

The through-line is not a product or a market. It is a posture. Call it strategic agility, call it opportunism, call it—to borrow a phrase from the Acquired playbook—a refusal to stay in your lane. Gunkul has made a living by reading the tea leaves of Thai industrial policy about eighteen months before anybody else and showing up early to whatever the government has decided to subsidize next. That is not a technology moat. It is not a brand moat. It is something subtler: a regulatory arbitrage engine, wrapped in a family-controlled holding structure, operating with the speed of a startup and the balance sheet of a mid-cap utility.

The roadmap for what follows is simple. We will start with the humble trading origins, trace the pivot from selling shovels to owning mines, meet the current CEO—the founder's daughter, now the architect of a remarkably disciplined capital allocation regime—analyze the M&A record, descend into the strange and fascinating world of their cannabis and EV bets, and finally frame the whole thing through the lens of Porter and Helmer to ask the question every investor eventually arrives at: is the moat real, or is this company just very lucky, very often?

Spoiler: the answer is more interesting than either extreme.

II. The Origins: Trading the Grid

In the Thailand of the early 1980s, electricity was still a frontier. The Electricity Generating Authority of Thailand—EGAT—had been operating for just over a decade. The Provincial Electricity Authority, known to everyone as PEA, was racing to extend distribution lines into villages that had, until recently, been lit by kerosene. The whole apparatus ran on imported equipment: transformers from Japan, switchgear from Germany, cables from whichever supplier could meet the spec and ship before the monsoon. Someone had to move that equipment from ports and factories into the hands of utility engineers at provincial substations. That someone was, increasingly, a small trading outfit founded by a 28-year-old named Gunkul Dhumrongpiyawut.

The man himself had been trained as an electrical engineer at a time when that training was a ticket to a stable civil service job. He had chosen, instead, to go into business—a choice that in the Thailand of 1982 was neither glamorous nor safe. The Baht was pegged to a basket of currencies. Capital controls were tight. Family networks mattered more than formal credit. Gunkul's first company, the precursor to what today trades on the SET, was not a power company. It was a distributor. It imported and resold electrical equipment. It bid on tenders. It cultivated relationships with PEA engineers who needed a specific reclosure rated for a specific fault current on a specific feeder. It was, by any honest accounting, a middleman business.

But middlemen in capital-intensive industries have a habit of accumulating insight that nobody else possesses. Sitting between a buyer and a seller gives you the best seat in the house for understanding where the buyer is going next. When PEA ordered a surge of medium-voltage transformers, Gunkul's traders knew which province was about to electrify. When EGAT's procurement patterns shifted toward high-voltage gear, they could infer where the transmission backbone was being reinforced. When a new industrial estate broke ground, the incoming power requirement showed up in component orders months before it showed up in the press.

That is the insight that shaped the next forty years. Selling the shovels taught the company where the gold was. And eventually, it taught them that the people digging the gold were making more money than the people selling the shovels.

The trading business also gave the company something arguably more valuable than foresight: technical DNA. By the time Gunkul Engineering pivoted toward building its own plants, its engineers already knew every specification, every approved vendor, every bureaucratic idiosyncrasy of the Thai grid code. They did not need to hire an external EPC contractor because they effectively were one. They did not need to shop around for switchgear pricing because they had been quoting it for two decades. When the opportunity came to construct a solar farm or a wind project, the company could build at a lower cost per megawatt than new entrants because they owned the supply chain from import container to commissioned plant.

To this day, the legacy trading arm still exists inside the consolidated group. It is a slow-growth, unsexy segment that rarely gets a single line of airtime on earnings calls. Analysts tend to treat it as an afterthought. That is probably a mistake. The trading business is the cash-generative sediment layer on top of which everything else—the wind farms, the Vietnam acquisitions, the cannabis greenhouses—has been constructed. It is the institutional memory. It is the relationship network into PEA and EGAT. It is, in a very real sense, the reason the rest of the story was ever possible.

And that is how we arrive at the first great pivot: from selling the pieces of the grid to actually owning pieces of it.

III. The First Inflection: From Service to Ownership

The 2010s were a strange decade for Thai energy. On one hand, the country had a voracious appetite for electricity—GDP was compounding, the industrial belt around the Eastern Seaboard was hungry for capacity, air conditioners were multiplying in every apartment block in Bangkok. On the other hand, the country's primary generation mix was still dominated by natural gas, much of it imported from Myanmar through a single vulnerable pipeline. Everybody in the Ministry of Energy knew this was a strategic problem. Nobody quite knew what to do about it.

Then came the adder.

For readers unfamiliar with Thai renewable energy policy, the "adder" was a feed-in-tariff mechanism introduced in the late 2000s and expanded through the early 2010s. In plain terms, it was a premium—denominated in baht per kilowatt-hour—that renewable generators received on top of the wholesale power price, guaranteed for a fixed number of years. The adder was generous. At its peak, solar developers could receive adders of around 8 baht per kilowatt-hour on top of the base tariff, producing economics that, for a competent developer with access to cheap panels and cheap land, were close to obscene.

Gunkul read this policy window correctly, and they read it early.

In 2010, the company took itself public on the Stock Exchange of Thailand. On paper, the IPO was a capital raise. In reality, it was a declaration of intent. The proceeds were never going to be used to expand the trading business—that was a low-multiple, low-growth activity. The proceeds were going to be used to buy land, secure PPAs, and build. The starting gun had fired.

What followed, between roughly 2012 and 2016, was a sprint. The company built solar farms across Thailand, signed into the adder regime early, and moved on wind before most domestic peers had even bothered to measure wind speeds. The conventional wisdom at the time was that Southeast Asian wind was mediocre—that the trade winds that animate the North Sea and the Great Plains of the American Midwest simply did not translate to the gentler, more seasonal flows across central Thailand. Gunkul's engineers disagreed. They studied micro-sites, especially the elevated ridgelines of the northeast where afternoon thermals and seasonal monsoon transitions produced meaningfully better capacity factors than the skeptics assumed. The result was a series of wind projects—branded internally under various "Windy" naming conventions—that, by Thai standards, were among the first utility-scale wind plants to be built by a private developer without direct state backing.

Why does this matter? Because each of these plants was not just a pile of steel and silicon. Each one was a 20 to 25-year contract with EGAT—a bond-like stream of electricity sales at a regulated price, indexed to inflation, with effectively zero counterparty risk. The company was not building widgets anymore. It was building a balance sheet full of annuities.

Here is the subtle part. The pivot from EPC services to independent power producer was not a clean break. It was more like a rotation. Gunkul kept the EPC capability because the EPC capability was the reason it could build its own plants cheaply. It kept the trading arm because the trading arm supplied the equipment. What changed was where the margin was booked. Instead of earning a modest construction spread and walking away, the company retained ownership of the completed asset and collected two and a half decades of contracted revenue. The service-to-ownership transition was, in capital allocation terms, one of the highest-ROIC moves the company ever made, because it recycled pre-existing operational capabilities into a far higher-multiple business.

By the middle of the decade, Gunkul had established itself as something unusual in the Thai renewable landscape: a mid-sized, family-controlled IPP with genuine in-house engineering capability and an appetite for aggressive, early-cycle development. That reputation is the platform on which everything subsequent was built, including the handoff to the next generation of leadership.

IV. Modern Management & The Family Office Core

If you attend a Thai energy conference and watch the Gunkul team walk into a room, the first thing you notice is how young they look. The second thing you notice is that the person clearly in charge is a woman in her forties who moves with the quiet authority of someone who has spent her entire adult life being underestimated and who long ago stopped caring.

That is Sopacha Dhumrongpiyawut, daughter of the founder, and since the mid-2010s the central operating mind of the company. She is not the only executive—Gunkul is run by a genuinely capable management bench, and several key deputies have been with the company for decades—but she is the one shareholders talk about, the one the analysts cover, and the one whose stamp is on every major capital decision of the last several years.

Her style is worth dwelling on, because it is the antidote to a stereotype. Thai family-controlled conglomerates have a reputation—sometimes earned, sometimes not—for two failure modes: dynastic rigidity, in which the founder refuses to hand over control and the company ossifies; and profligate ambition, in which a successor-generation scion inherits the balance sheet and proceeds to light it on fire chasing trophy projects. Sopacha fits neither pattern. She took operational authority in an orderly transition, not a palace coup. And her track record over the subsequent years has been the opposite of profligate. Internally, colleagues describe her stance as "conservative aggression"—a phrase that sounds like a contradiction until you watch her in a capital allocation meeting.

What does conservative aggression look like in practice? It looks like a portfolio of aggressive bets, each individually underwritten to tight return hurdles. Gunkul has a reputation in the industry for walking away from deals that bigger rivals are bidding on, specifically because the numbers do not clear an internal IRR hurdle that is widely rumored to sit in double digits on a fully risked basis. Wind projects with questionable capacity factors get killed. Solar acquisitions where the seller's EBITDA is flattered by lease arbitrage get re-underwritten. The "prestige deal"—the one that would let management stand next to the Prime Minister for a photo at a ribbon-cutting—does not appear to exert much gravity on this team. If the math doesn't math, they walk.

The shareholding structure reinforces the discipline. The Dhumrongpiyawut family, through a combination of direct and vehicle-held stakes, retains effective control of the company, with a combined economic interest that has historically hovered in the vicinity of half the equity base. This is skin in the game in the most literal sense. When Sopacha approves a capital expenditure, she is deploying, pro rata, a meaningful fraction of her own family's net worth. That is not a governance structure that encourages reckless swings, and the record suggests it hasn't.

Culturally, the company runs lean. It does not feel like a traditional utility. Utilities, as a general archetype, are slow institutions built to survive the next regulatory cycle; they prize process, documentation, and the kind of bureaucratic risk-aversion that makes them reliable but rarely exciting. Gunkul reads more like a scrappy mid-market private equity firm that happens to own power plants. Decisions get made quickly. Project teams are small and accountable. The executive floor does not look much like EGAT's.

The professional-family hybrid management model has one other useful feature: it lowers the activation energy for pivots. When the Thai government legalized certain forms of cannabis and hemp cultivation in 2019 and expanded the policy over the following years, a traditional utility might have taken a three-year task force review before deciding whether to enter. Gunkul's leadership, by contrast, appears to have run the land-use math on a whiteboard, concluded that their existing real estate footprint was sitting idle under the turbine blades anyway, and moved. That speed is the succession dividend. It is the thing that a founder-to-professional-family handoff can produce when it works well.

Which brings us, inevitably, to the question of what they have done with all that speed.

V. M&A Strategy: Benchmarking Buy vs. Build

Gunkul's deal record over the last decade is where the analytical conversation gets genuinely interesting, because it is the arena in which the company's bluff gets called. Anybody can build a solar farm. The hard part is figuring out whether to build your own at greenfield cost, acquire somebody else's at market clearing price, or enter a joint venture where you trade equity for scale. Gunkul has done all three, often within the same year, and the pattern reveals something important about how the company actually thinks.

Start with the joint venture.

The Gulf Energy partnership is the single largest strategic relationship on the Gunkul books. Gulf, for those who do not follow Thai equities closely, is the country's most aggressive private power developer—a company that, over the 2010s and into the 2020s, became the single largest non-state generator in Thailand, with a growth trajectory that has made its founder one of the wealthiest people in the country. When Gulf and Gunkul entered into a series of collaborations across renewable assets, the obvious read was that Gunkul had become the junior partner—the smaller, more specialized developer riding on Gulf's capital and relationships.

That read is partially correct and partially misleading. On a balance-sheet basis, Gulf dwarfs Gunkul. On a project execution basis, Gunkul contributes the technical depth that Gulf's leaner in-house team can draft off. The partnership works precisely because the two sides bring different things to the table: Gulf brings scale, political clout, and low-cost capital; Gunkul brings engineering pedigree, an existing equipment supply chain, and a fast project delivery track record. It is, in effect, a division of labor, and the economics of the shared projects reflect that division.

Now move to acquisitions. The most consequential deployment of acquisition capital was the push into Vietnamese solar in 2020 through 2022. Vietnam, during that period, had experienced a boom-and-bust cycle that was almost perfectly designed to produce motivated sellers. The country's feed-in tariff had triggered a construction rush; the grid had been unable to absorb the supply; curtailment risk had spooked early investors; and several developers who had built on leverage were, by 2021, looking for exits. Gunkul moved in. They acquired stakes in operating solar assets at prices that—by contemporaneous regional benchmarks—looked reasonable but not screaming bargains.

The interesting question is whether Gunkul overpaid. If you simply compare headline dollar-per-megawatt figures across Gunkul's Vietnam acquisitions and similar transactions by regional peers like B.Grimm Power and Super Energy, the numbers do not show Gunkul getting some miraculous discount. The multiples were broadly comparable. So where is the edge?

The edge is post-close. Gunkul's internal EPC team, parachuted onto the acquired assets within months of completion, has a track record of wringing out meaningful cost savings—in the neighborhood of a tenth to a fifteenth of operating expense, depending on the project—through reconfiguring balance-of-plant, renegotiating O&M contracts with vendors they already worked with on domestic projects, and occasionally upgrading inverters to newer, higher-efficiency units that pay back within a couple of years. In effect, the acquisition thesis is not "buy it cheap." The thesis is "buy it fairly, then fix it." For a vertically integrated operator with in-house engineering, this is a real and defensible source of excess return. For a purely financial acquirer, it would not be.

This is where the distinction between the buy-and-build strategies collapses into something unified: Gunkul's M&A is really a way of sourcing deals that its EPC arm can then refurbish. It is closer to a value-add real estate strategy than a classic utility roll-up.

The final piece of the capital allocation picture is recycling. Gunkul has demonstrated, on multiple occasions, a willingness to sell partial stakes in mature, stabilized assets—sometimes to infrastructure funds, sometimes to strategic partners—in order to free up capital for the next development cycle. This is the kind of behavior that, in the utility sector, separates growth companies from bond-proxy operators. A bond-proxy utility holds assets forever and clips coupons. A growth utility monetizes mature assets when the multiple is fat, redeploys the proceeds into earlier-stage, higher-return development, and repeats. Gunkul belongs to the second category. It is the behavior of a compounder, not a yield vehicle.

The obvious question, having understood the M&A discipline, is: what are they redeploying capital into now? And the answer is where the story gets strange.

VI. The Hidden Businesses: Cannabis, EVs, and Spectrum

Imagine you are a utility analyst based in Singapore. You have been covering Thai power for fifteen years. You have a mental model of what a Thai IPP's earnings deck looks like: megawatts in the ground, PPA tenures, fuel costs, capacity payments. One quarter you open Gunkul's segment disclosure and there is a new line item. Smart Farming. You scroll up. Nope, you are in the right document. You scroll back down. The EBITDA margin on this new segment is staggering—three times the margin on the core utility business. What on earth is going on?

What was going on, and continues to go on, is one of the most unusual utility pivots in Asian markets. In the wake of Thailand's progressive liberalization of medical and industrial cannabis and hemp, beginning in 2019 and expanding through subsequent policy rounds, Gunkul identified a use case for its land portfolio that essentially no other power company in the region considered seriously. The company owned or leased vast tracts of land—primarily under and around wind farm infrastructure—where, by regulatory design, the space between turbine bases is unused. You cannot farm rice under a wind turbine at commercial scale because of shadow flicker and access-road fragmentation. You cannot build another income-producing structure on most of it. The land sits there, generating no cash, serving only as a spatial buffer for blades.

Gunkul built greenhouses.

The company's indoor cultivation operation, branded internally under a smart farming banner and often referenced as G.K. Smart Farming in communications, is a high-tech, climate-controlled, LED-lit cultivation facility targeting the medical and extract-grade end of the Thai hemp and cannabis market. It is, importantly, not a recreational product business—Thai policy has oscillated on recreational use, and the company has been deliberate about staying on the medical and industrial side of the regulatory line. Scale is still small relative to the utility business. But the unit economics are a different universe. Utility-scale solar and wind, once depreciated and levered, produce EBITDA margins in the range you would expect from a mature infrastructure business—thirty-odd percent, sometimes higher depending on PPA vintage. Indoor cannabis cultivation, when executed competently and when product finds its regulated buyer, can produce EBITDA margins in the forty to fifty percent range. That is a different category of business entirely.

The strategic logic goes beyond margin arbitrage. It is a statement about how management thinks about the asset base. The core insight is that a wind farm is not just a power plant. It is a land-use platform. Once you have secured zoning, permitting, grid interconnection, and community relationships for a large rural site, you have built a kind of strategic beachhead that can host more than one business. Adding greenhouses to that footprint effectively doubles the revenue per square meter of land without requiring new permitting of the land itself. From a return-on-assets perspective, it is nearly free alpha.

Of course, "nearly free" is not "free." Cannabis cultivation is an operationally demanding business. It requires genetics expertise, horticultural science, food-safety compliance, and—crucially—off-take relationships with licensed pharmaceutical and wellness product companies. Gunkul has had to build those capabilities from near-zero. The early years have been a learning curve. Analysts tracking the segment should expect occasional quarters of volatility as the business scales. But the structural argument is real, and the return on incremental capital, for the capacity that works, is genuinely attractive.

Beyond the hemp pivot, the company has been quietly incubating a second hidden business under the Gunkul Spectrum umbrella. Spectrum is, essentially, the in-house innovation lab. The portfolio is eclectic. It includes work on peer-to-peer energy trading—a concept in which rooftop solar owners trade surplus electricity with neighbors over a blockchain-based settlement layer, bypassing the traditional utility middleman. It includes EV charging infrastructure, aimed at the stretch of Thai highways and commercial corridors where fleet electrification is beginning to move from pilot to production. It includes battery storage development, co-located with solar to firm up otherwise intermittent generation. Some of these bets will work. Some will not. But the existence of Spectrum as a formalized innovation function is itself a signal: this is not a company that thinks its runway ends with the current feed-in-tariff cycle.

Finally, there is Energy-as-a-Service. This is perhaps the most commercially important of the hidden businesses, and the least discussed. In simple terms, it is the private PPA model: instead of selling electricity to the grid under a regulated tariff, Gunkul designs, finances, builds, and operates solar installations on the rooftops and adjacent land of industrial and commercial customers—factories, shopping malls, logistics centers—and sells the output directly to those customers at a contracted price, typically below their prevailing retail electricity cost. The customer saves money without any upfront capex. Gunkul earns a contracted revenue stream from a creditworthy corporate counterparty, typically at higher returns than grid-connected utility-scale solar because the customer is willing to pay for the convenience and the stable price. This segment, sitting inside the EPC wing, has been one of the fastest-growing parts of the business. It is the natural successor to the IPP-for-EGAT model: the same developer DNA, aimed at a different customer.

Three hidden businesses, each targeting a different jumping-off point for the next decade. Together, they reframe what Gunkul is actually building—which brings us to the question of what, if anything, protects it.

VII. The 7 Powers & Porter's Five Forces

Every investment thesis eventually has to answer the "why can't somebody else do this?" question. In the case of Gunkul, the answer is not obvious. The company does not invent technology. The solar panels it buys come from the same global vendors that supply everybody else. The wind turbines it erects are made by Vestas, Siemens Gamesa, or Chinese competitors whose equipment is available to any credible developer. The cannabis business, if anything, is a commodity input with regulatory scarcity, not proprietary technology. So where, in the Hamilton Helmer framework, does the power come from?

The most defensible power, in our view, is best described as a Cornered Resource, though with an important Thai-specific twist. In classical Helmer terms, a cornered resource is an input that one company controls that others cannot acquire on equal terms. Gunkul's cornered resource is not physical land per se—there is plenty of land in Thailand—but rather a bundle of rights: the zoning approvals, grid interconnection permits, community agreements, and environmental clearances that together make a site buildable. In Thai renewable development, obtaining this bundle is genuinely hard. The process involves navigating multiple ministries, provincial governors, local authorities, and, in the case of wind, often bespoke community engagement. Doing it well requires a specific set of relationships that compound over time. Gunkul has been doing it for more than a decade. Its permit pipeline is, in effect, a proprietary asset, because an identical site acquired by a foreign newcomer today would take years longer to push through the approval process and might fail outright. That is a cornered resource.

The second power is Scale Economies, though of a particular kind. The relevant scale economy at Gunkul is not brute-force generation capacity—plenty of companies in Thailand have more megawatts. The relevant scale economy is the vertical integration of equipment distribution, EPC delivery, and asset ownership. Because the trading arm still supplies meaningful volumes of electrical equipment to the Thai market, the internal EPC team has privileged access to vendor pricing and technical support. Because the EPC team builds the IPP's own plants, the IPP wing avoids the margin leak that flows to external contractors at competitors. Each layer of the stack subsidizes the next. Replicating this would require a new entrant to simultaneously build a trading business, an engineering practice, and a generation portfolio—a task that would take a decade and tens of millions of dollars of cumulative losses before the flywheel turned.

There is a plausible case for a third power: Process Power. Gunkul's ability to pivot quickly into adjacent verticals—cannabis, private PPAs, EV infrastructure—is, arguably, a process capability embedded in the culture. But we would hold that claim lightly. It is early, and processes that look powerful in a growth environment can reveal themselves to be habits of a specific management team under specific market conditions. If the test of a process power is "does it survive the founders?"—and in Gunkul's case that would mean the current generation of family leadership—then the honest answer is that we do not yet know. It is a power to watch, not a power to count.

Now Porter. The five forces analysis of Thai renewable power, as applied to Gunkul, tells a mostly favorable story.

Bargaining power of buyers is low. The traditional offtake is EGAT, operating under long-dated PPAs that lock in pricing for two decades or more. Once a contract is signed, the buyer has essentially no negotiating leverage for the duration. On the private PPA side, industrial customers do have more optionality, because they can, in principle, sign with a competing developer. But the reality is that private PPAs are sticky once signed—contract durations run a decade or more, and the switching cost of re-permitting a rooftop system mid-contract is prohibitive. So buyer power is structurally modest.

Bargaining power of suppliers is moderate and, importantly, trending favorably. Solar panel prices have been in secular decline for two decades. Wind turbine prices have followed the experience curve. Global capex per megawatt has fallen dramatically since the early 2010s. For a developer, this is a supplier landscape in which vendors must compete for your orders—a comfortable position.

Threat of new entrants is the most interesting force. On paper, the Thai power sector is attractive enough to draw new capital—regional players from Singapore, Japanese strategics, Chinese developers looking for overseas deployment. In practice, the barriers are substantial. Permitting is slow and opaque. Land aggregation is difficult without local partners. Grid interconnection queues can stretch for years. And PPA allocation, historically, has favored incumbents with track records. So while capital can certainly enter, it cannot enter at the speed its balance sheets would suggest. That is, functionally, a moat.

Threat of substitutes is where the picture gets nuanced. Thailand's power demand is not disappearing; renewable electricity specifically is being actively substituted for gas and coal in the national generation mix. For Gunkul, the substitution dynamic runs in its favor. The wild card is technological substitution within renewables—if utility-scale battery storage or green hydrogen were to become dramatically cheaper, incumbent solar and wind assets could lose some of their scarcity premium. That is a risk worth monitoring, but not one that looks acute on current timelines.

Industry rivalry is real. Thai renewables has a handful of credible scale developers—Gulf Energy, B.Grimm, BCPG, Super Energy, GPSC, and others—all of whom compete on auctions, on private PPAs, and on M&A. Rivalry keeps returns honest. But rivalry does not, in the Thai context, have the destructive intensity of, say, global solar panel manufacturing. It is a disciplined oligopoly more than a commodity bloodbath.

So is the Gunkul moat real? It is real, but it is narrower than its proponents sometimes suggest. It is fundamentally a regulatory arbitrage moat—the ability to navigate Thai policy faster than anyone else, stacked on top of a vertically integrated operating platform. That is a valuable and defensible position. It is not, however, the kind of technology moat that produces forty-year compounders regardless of ownership. Gunkul's moat is, in a meaningful sense, a management moat. And management moats require vigilance.

VIII. The Playbook: Lessons for Investors

Step back from the specifics and Gunkul's strategic logic reduces to three repeating patterns. The first is what might be called the front-running play. In every major strategic move the company has made—the early IPP build-out under the original adder regime, the aggressive wind development before peers had the confidence to commit, the Vietnamese solar acquisitions into a distressed market, the cannabis pivot immediately after regulatory liberalization, the private PPA push ahead of the retail electricity tariff squeeze that is beginning to pressure industrial customers—the pattern is the same. Gunkul is consistently eighteen months ahead of the broader market's understanding of where the subsidy, the regulation, or the demand pool is moving.

This is not, to be clear, the same thing as being visionary. The company is not attempting to see ten years into the future. It is attempting to see the next legislative cycle clearly and to have its capital already deployed when that cycle opens. The distinction matters because it keeps the strategy grounded in a time horizon where mistakes can be corrected and feedback loops are tight. A front-runner who is eighteen months early and wrong can withdraw before catastrophic loss. A visionary who is ten years early and wrong can run out of cash waiting for the future to arrive.

The second pattern is vertical integration as de-risking. At most utilities, vertical integration is pursued for margin capture—the company wants to own more of the value chain to keep more of the profit. At Gunkul, vertical integration also serves as a risk-management tool. By owning the equipment distribution, the construction team, and the operating asset, the company insulates itself from the kind of project-execution disasters that can destroy standalone developers. When a contractor at a traditional IPP underperforms on a schedule, the IPP suffers cost overruns it cannot easily control. When a "contractor" at Gunkul underperforms, it is an internal team reporting to the same CEO as the project owner. Accountability is direct. Rework is faster. Change orders do not become litigation.

This internal alignment is especially valuable in the acquisition playbook. When Gunkul buys a distressed solar asset, the optimization work that follows is done by the same people who build greenfield. There is no contracting friction, no confidentiality wall, no need to explain the asset's quirks to a vendor who will bill hourly. That is a structural advantage a pure-play asset owner cannot replicate, and it is the quiet engine of excess return in the M&A program.

The third pattern is strategic flexibility. Thai utilities, in the main, are not built for pivots. Their cost of capital is low, their regulatory environment is stable, and their institutional culture is oriented around preservation rather than experimentation. Gunkul's willingness to be, frankly, weird—to plant cannabis under wind turbines, to incubate peer-to-peer energy trading before the regulatory framework exists to support it, to enter EV charging before Thailand's EV density justifies the capex—is, over time, how it keeps generating return on incremental capital. Every pivot is a real option. Most options expire worthless. A few pay off asymmetrically. A portfolio of options, managed with discipline, outperforms a monolithic bet.

The synthesis of the three patterns is the real playbook: be early but not reckless, integrate vertically to compress execution risk, and keep a menu of small-dollar strategic options open at all times. It is not a sexy formula. It does not make for good magazine headlines. But as a repeatable method for compounding capital in an emerging-markets utility context, it has held up remarkably well.

The question for an investor, then, is whether the playbook will continue to work. And that brings us to the final analytical step—weighing the case for and against.

IX. Analysis & The Bull vs. Bear Case

Every thesis has its skeptics, and the Gunkul skeptics are not without ammunition. The bear case starts where it always starts in emerging-markets power: regulatory risk. The Thai government has, historically, been a reasonably predictable counterparty on renewable tariffs, but "reasonably predictable" is not the same as "contractually ironclad." Adder schedules have been adjusted mid-cycle. Feed-in tariffs have been reduced for new projects. Future auction structures could be less favorable than current expectations. A developer whose pipeline economics assume a certain trajectory of tariff support can find itself suddenly stranded if a new administration decides to rebalance the subsidy regime. That is a risk that applies to every Thai renewable developer, including Gunkul, and it is not fully hedgeable.

The second bear point concerns execution risk on the non-core bets, especially cannabis. The gross margins on high-end medical cannabis are extraordinary, but extraordinary margins in an immature regulatory market tend to attract competition, compression, and occasionally political reversal. Thailand's cannabis policy has already oscillated between permissive and restrictive interpretations in the last few years, and the risk that a future government adopts a more restrictive stance is not zero. If Gunkul's cannabis segment grows to be a material profit contributor and is then impaired by a regulatory rollback, the downside is real. The charitable interpretation is that the capital at risk in the cannabis venture remains modest relative to the overall balance sheet. The uncharitable interpretation is that management's attention is a scarce resource, and every hour spent on cannabis is an hour not spent on the core utility business.

The third bear point is more structural. Gunkul's moat, as discussed, is substantially a regulatory arbitrage moat. That kind of moat works beautifully when the company is faster than its competitors at navigating policy. It works less beautifully if competitors acquire comparable agility, or if a larger player—say, Gulf Energy operating unilaterally rather than as a partner—decides that Gunkul's niche is worth muscling into. The moat is real but narrow, and narrow moats can be bridged.

Now the bull case.

The bull case begins with an observation about Thailand's decarbonization trajectory. The country has committed to carbon-neutrality targets that will require a profound transformation of the generation mix over the next two to three decades. Gas, which currently dominates, will have to give way to renewables, storage, and eventually perhaps hydrogen. The policy tailwind is not a cyclical kicker; it is a structural shift that will play out over twenty or more years. For developers who are already established, who have the permitting relationships, and who have demonstrated the operational capability to actually deliver megawatts into the grid, this is a multi-decade runway. Gunkul is one of a handful of developers that fits that description.

The second bull point is the platform optionality. If Gunkul is merely a renewable power producer, it is a solid mid-cap utility with high single-digit to low double-digit earnings growth. But if its hidden businesses scale—if private PPAs become a significant chunk of Thai commercial electricity demand, if EV charging emerges as a credible revenue line, if the peer-to-peer energy trading stack becomes a platform layer that Gunkul monetizes—then the company re-rates from utility to infrastructure platform. That is a different category of valuation. The probability that all three hidden businesses succeed is low. The probability that at least one does is meaningfully higher. That asymmetry is what makes the stock more interesting than a comparable regional utility with no such optionality.

The third bull point is management. Sopacha and her team have, over a decade, demonstrated capital allocation discipline in an industry where discipline is not the norm. That is a soft factor, hard to quantify, easy to dismiss. But in emerging markets, management quality and ownership alignment are arguably the single largest determinants of long-run shareholder returns. Gunkul scores well on both.

Holistically, looking through both the Porter and the Helmer lenses, the picture that emerges is a mid-moat, high-optionality compounder operating in a favorable structural environment, with real but manageable regulatory and execution risks. It is not a cant-lose setup. But it is a company whose management has earned the benefit of the doubt through a long history of getting the important calls right.

For ongoing monitoring, the KPIs that matter most are narrow and specific. First is the growth trajectory of the private PPA segment, which more than any other metric reveals whether the company is successfully transitioning from a traditional government-offtake IPP to a commercial energy platform. Second is the realized IRR, on a risk-adjusted basis, of the new hemp facilities and any subsequent scale-up in the smart farming segment. Investors should watch for evidence either that the early-stage margin premium is being sustained at scale, or that normalizing competition is compressing it back toward commodity returns. Third, as a sanity check, is the consolidated return on invested capital across the group. If the company is doing its job, ROIC should hold up or improve even as it deploys capital into increasingly diverse verticals. If ROIC drifts downward, it is a signal that the diversification is approaching the danger zone.

X. Epilogue & Final Reflections

There is a type of company that business historians tend to love in retrospect but find unsettling in real time. It is the survivalist company—the firm that does not have one perfect strategy but rather a sequence of good-enough strategies stitched together by a culture of adaptation. Gunkul belongs to that type. If you had asked any reasonable observer in 1990 whether a provincial electrical equipment trader would still be a relevant company in 2026, let alone one that owned wind farms and cultivated cannabis, the honest answer would have been no. Most companies like that do not survive their first generational transition. Most do not survive the end of their first big product cycle. Gunkul has survived several of each.

The takeaway is less about Thailand or about renewable energy than it is about the nature of advantage in emerging markets. The developed-market playbook for industrial companies tends to emphasize technological differentiation, brand, and scale. In emerging markets, those powers exist but are less reliable, because the regulatory and institutional environment moves too quickly and unpredictably. What works instead is something more like ecological fitness—the capacity to read the environment, adapt the business model, and recycle capital faster than the opportunity window closes. Gunkul's real genius is not in any single product or any single plant. It is in the institutional metabolism that allows it to move quickly without, at least so far, breaking the balance sheet.

There is a version of the future in which Gunkul becomes Thailand's dominant renewable-plus-adjacencies platform—a combined utility, mobility infrastructure, and agricultural biotech play whose parts reinforce each other at a level that pure-play competitors cannot match. There is also a version in which the cannabis bet disappoints, the EV charging business never finds unit economics, peer-to-peer trading remains a slide-deck concept, and the company reverts to being a competent but unexceptional Thai IPP. Both futures are possible. Both are, to some extent, already priced into the range of analyst expectations.

What is less priced—and this is perhaps the subtlest observation one can make about the company—is the probability that, in the next ten years, Gunkul will do something nobody currently expects. Not because management is whimsical, but because the company's entire operating history suggests that this is the pattern. Each decade has produced at least one pivot that the previous decade's annual reports would have considered implausible. There is no reason to expect the next decade to be different.

For long-term investors willing to underwrite the ambiguity, that is part of what they are buying. Not a clean story. Not a predictable cash flow. Something closer to a basket of options on a country's energy transition, managed by a family that has proven it can handle options with discipline. In emerging markets, the winner is rarely the one with the cleanest strategy deck. It is the one that has survived, adapted, and shown up again with the right product on the shelf when the customer was finally ready to buy.

Gunkul is, as of this writing, still that kind of company. Whether it remains so is a question that the next decade, and the next pivot, will answer.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube