FPT Corporation: The Story of Vietnam's Sovereign Tech Titan

I. Introduction & Episode Roadmap

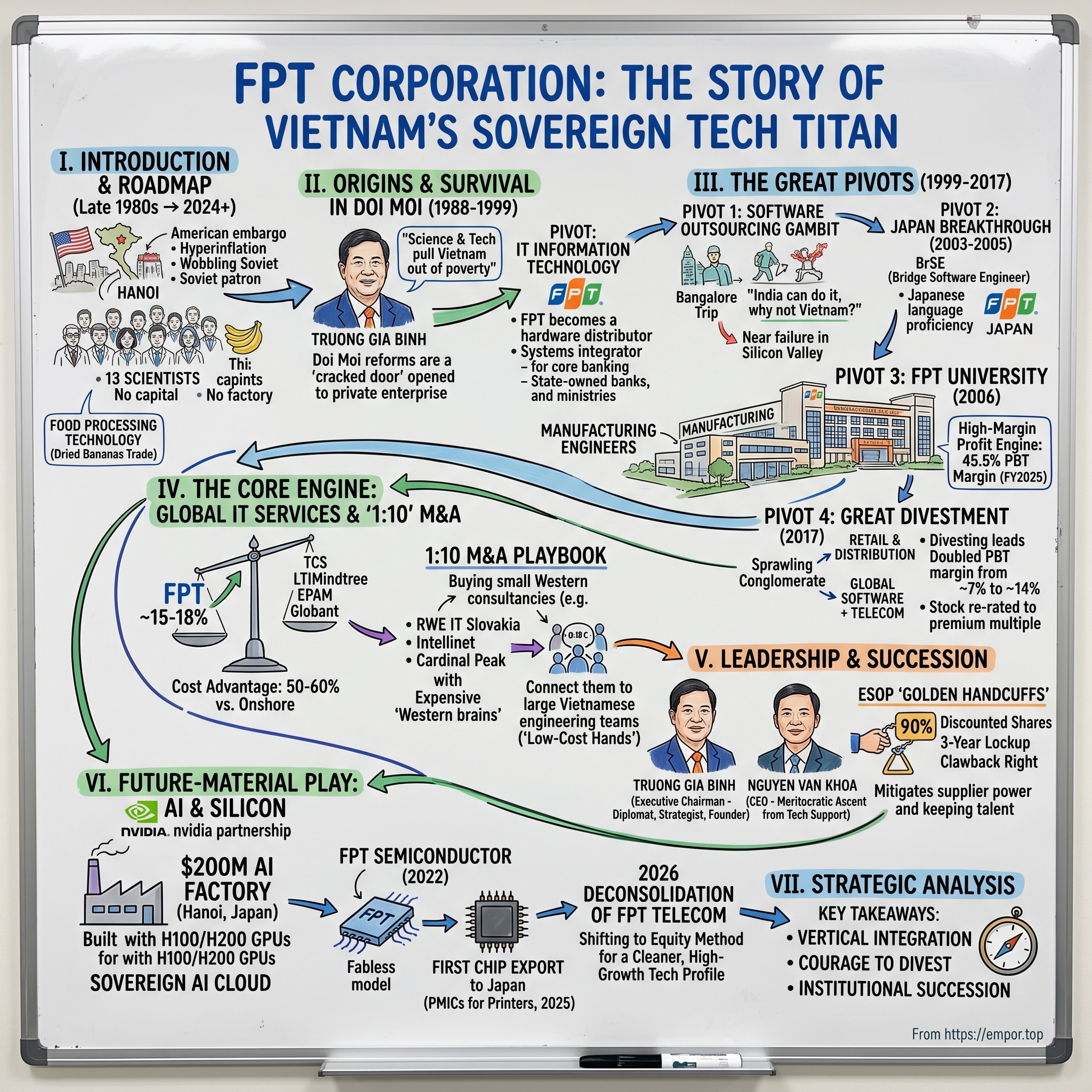

Picture Hanoi in the late 1980s. The American trade embargo still hangs over the country like a curfew. Inflation is not measured in single digits but in triple digits—prices roughly tripling in a year, savings evaporating, the dong barely worth the paper it is printed on. The Soviet Union, Vietnam's great patron, is wobbling toward collapse, and with it the guaranteed export markets that kept the planned economy limping along. Into this landscape walks a group of thirteen scientists—mathematicians, physicists, engineers trained in Moscow and Eastern Europe—with no capital, no factory, and no obvious product. They borrow money. They name their company, of all things, the Food Processing Technology company. And they begin, improbably, by trading dried bananas and exporting whatever they can scrape together to the Eastern Bloc.

Now fast-forward to 2024. That same company—still led by the same founder—stands on a stage with 黄仁勋 Jensen Huang's NVIDIA, announcing a $200 million "AI Factory" stuffed with the most coveted silicon on Earth.[^1] A year later, in December 2025, it ships its first batch of commercially designed power-management microchips into Japan—the most quality-obsessed industrial market in the world—for use inside office printers.1 Somewhere between the dried bananas and the H100 GPUs lies one of the great untold business stories of the emerging-market era.

This is the story of Công ty Cổ phần FPT (FPT Corporation, HOSE: FPT.VN), headquartered in Hanoi at fpt.com.vn. By mid-2026 it is a roughly $2.85 billion-revenue technology group and, by market value, one of the largest companies in Vietnam—a country most global investors still file under "frontier."

What makes FPT worth two hours of your attention is not just that it grew. Plenty of emerging-market firms grow. What makes FPT a genuine case study is how it solved the single hardest problem in the technology services business: talent. The bottleneck in software outsourcing has never been demand—it has always been finding enough skilled, foreign-language-capable engineers to throw at the demand. FPT's answer was audacious. Rather than fight competitors in the open labor market, it built its own accredited university system to manufacture engineers the way Toyota manufactures cars. Then it layered on a second insight: instead of buying cheap offshore code shops, it bought small, expensive Western consulting boutiques and bolted them onto a vast, low-cost Vietnamese engineering machine—what insiders call the "1:10 hybrid delivery model." One consultant onshore in Atlanta or Düsseldorf; ten engineers in Hanoi or Da Nang.

Our roadmap runs the full arc: the survival years of Vietnam's Đổi Mới reforms, when FPT was just trying not to die; the pivots into hardware distribution and then global software outsourcing; the breakthrough in Japan that nobody expected; the radical decision to build a university; the courageous 2017 divestment that shed 60% of revenue to double the profit margin; the Western M&A engine; the meritocratic handover from a charismatic founder to a professional CEO who started in tech support; and finally the AI-and-silicon pivot that is rewriting what FPT is supposed to be. Let's start at the beginning—with food, science, and survival.

II. The Origins: Food, Science, and Survival in Doi Moi Vietnam (1988–1999)

September 1988. A small group of scientists gathers in Hanoi to do something that, in a still-socialist economy, is almost subversive: start a business. The country has just begun Đổi Mới—literally "renovation"—the set of reforms launched at the Sixth Party Congress in 1986 that cracked open the door to private enterprise and a "socialist-oriented market economy." But a cracked door is not an open one. There is no real banking system to lend to a startup, no venture capital, no functioning equity market, and an American embargo choking off trade and technology. The men founding this company are not businessmen. They are academics from the Institute of Mechanics and similar state research bodies—people who could derive a differential equation but had never written an invoice.

Their leader was Trương Gia Bình, a mathematician who had earned his doctorate in physics and mathematics in Russia and returned home convinced that science and technology were the only forces capable of dragging Vietnam out of postwar poverty. Bình is the soul of this story, so it is worth lingering on him. Charismatic, intellectually restless, and relentlessly optimistic, he had the rare quality of being able to make penniless researchers believe they could build something world-class out of nothing. There is also a detail that Vietnamese readers know well: Bình had married into the family of General Võ Nguyên Giáp, the legendary military commander—a connection that gave the young venture a certain gravitational pull in a society where relationships are everything. But connections do not pay salaries. Revenue does.

And so we arrive at the wonderful irony baked into the company's very name. To get a license and generate cash, the founders needed a business the authorities would approve and that could actually move goods. Food processing fit the bill. The company was registered as the Food Processing Technology company—FPT—and its earliest activities were a grab-bag of pure survival trading: importing chemicals and fertilizer, exporting dried agricultural products to the Soviet Union and Eastern Europe, dabbling in textiles. One oft-repeated story has the young FPT trying to dry bananas for export. This is not the glamorous origin of a tech titan; it is the origin of a company that simply refused to go out of business while it figured out what it actually wanted to be.

What it actually wanted to be revealed itself as the world changed around it. The Soviet bloc dissolved between 1989 and 1991, vaporizing FPT's natural export markets but also loosening the ideological grip on private enterprise at home. And in 1994, the pivotal external event arrived: U.S. President Bill Clinton lifted the trade embargo against Vietnam, reopening the country to American technology and capital. For a company full of scientists who had always been more interested in computers than in cassava, this was the starting gun.

FPT pivoted hard into information technology, and it did so by becoming the indispensable middleman between global hardware giants and a country that had almost no computers. Through the 1990s, FPT secured distribution rights to act as the national channel for the era's titans—HP, IBM, Apple, Compaq, and Microsoft—putting their machines and software into Vietnamese offices for the first time. Simultaneously, FPT's engineers won the contracts that mattered most for a developing state: building the foundational IT and core banking systems for Vietnam's state-owned banks, wiring up the telecommunications networks, and computerizing government ministries. If you used a bank in Vietnam in the 1990s, there was a decent chance FPT had built the system behind the teller's window. The company became a genuine household name, synonymous with computers themselves.

But here is where the founders' scientific habit of mind paid off. Most companies, having become the dominant computer retailer and systems integrator in a fast-growing country, would have simply ridden that wave. FPT's leadership looked at the economics and felt uneasy. Distribution was a treadmill. Margins were thin, the business devoured working capital to finance inventory, and—most galling for proud scientists—FPT's fate was hostage to the pricing whims and channel decisions of foreign manufacturers who could replace it at will. They were, in essence, renting their success from HP and IBM. To build something durable and truly Vietnamese, FPT needed a high-margin, infinitely scalable business that the world would actually buy from Vietnam, not just sell into it. The answer would require looking 2,500 miles west, to a city in southern India that was busy proving an emerging nation could export brains instead of bananas.

III. The Great Pivots: How a Local Trader Rebuilt Itself as a Global Tech Titan (1999–2017)

Pivot 1: The Software Outsourcing Gambit (1999–2003)

The trip that changed everything was a trip to Bangalore. In the late 1990s, Trương Gia Bình traveled to India and to Silicon Valley and saw something that lit him on fire: Infosys and Wipro, companies built in a poor country, were generating fortunes by writing software for American and European corporations. The model was elegant. You did not need oil, factories, or natural resources—just educated people, an internet connection, and a wage structure a fraction of the West's. Bình returned with a slogan that became company gospel: "India can do it, why not Vietnam?"

In 1999, FPT Software was born to chase that dream. And the first chapter was a humbling, near-total failure. FPT did the logical thing—it went where the customers were. It planted offices in Silicon Valley and in Bangalore itself, marching straight into the lion's den to compete for American contracts. The result was close to zero. The language barrier was brutal; Vietnamese engineers, however brilliant, could not yet sell or specify complex projects in fluent English. The cultural gap was wide. And, fatally, FPT had no credibility—why would a Fortune 500 CIO hand a critical system to an unknown firm from a country Americans mostly associated with a war, when the established Indian players were right there with decades of references? FPT burned through precious capital and won almost nothing. The gambit, on its original terms, had flopped.

But failure is data. The lesson FPT extracted was not "outsourcing doesn't work for Vietnam." It was "we picked the wrong customer." The United States was crowded, English-default, and locked up by India. FPT needed a market where its specific disadvantages mattered less—and its hidden advantages mattered more.

Pivot 2: The Japan Breakthrough (2003–2005)

That market was Japan—and the choice was a masterstroke of strategic self-awareness. Consider what Japan offered that the U.S. did not. Japan was sliding into a structural shortage of software engineers as its population aged and its enormous manufacturing and financial sectors digitized. Japanese enterprises were notoriously reluctant to offshore to India, put off by the language and a working culture they found abrasive. And crucially, Japan prized exactly the things Vietnamese culture supplied in abundance: meticulousness, patience, deference, and long-term relationship-building over transactional speed. Vietnam and Japan also shared deep historical and cultural affinities and a similar regional sensibility. Where FPT looked like an unknown upstart in California, in Tokyo it looked like a diligent, humble, hungry partner.

Bình made a decision that sounds almost eccentric until you see the logic: he mandated that FPT's software engineers learn Japanese. Not as a nice-to-have, but as a core professional skill. The company poured resources into language training, and in 2005 it formally established FPT Japan to put boots on the ground in Tokyo. The operational innovation that unlocked the market was the role of the bridge software engineer, or BrSE—a Vietnamese engineer fluent in Japanese who sat onshore with the client, absorbed business requirements in Japanese, translated them into precise specifications, and relayed them to the large, low-cost delivery centers back in Hanoi and Da Nang. The BrSE solved the trust problem and the language problem at the same time. The Japanese client dealt with someone who spoke their language and understood their exacting standards; the heavy engineering happened cheaply offshore.

It worked spectacularly. Japan became, and remains, FPT's single largest export market, accounting for more than 30% of global IT services revenue—the foundation on which everything else was built.2 More than two decades later, when FPT chose to ship its first commercial microchips somewhere, it chose Japan again. The relationship runs that deep.

Pivot 3: FPT University (2006) — Manufacturing the Cornerstone Resource

By 2006, FPT Software had a problem that most companies would kill for: it was growing faster than it could hire. Demand from Japan and a recovering global market was outrunning the supply of qualified engineers who could code and speak a foreign language and meet international quality standards. Vietnam's public universities, still rebuilding, simply could not produce them at the rate or quality FPT needed. The conventional response would have been to slow down, raise wages, and fight competitors for the same scarce graduates—accepting talent as a hard ceiling on growth.

FPT did the opposite. It decided to manufacture its own engineers. In 2006 it founded Trường Đại học FPT (FPT University), an accredited private institution whose entire reason for existing was to feed the company's hunger for talent. This was vertical integration of the most radical kind—a software company building a university the way a steelmaker might buy an iron mine. The curriculum was engineered backward from FPT Software's actual project needs: computer science and software engineering, yes, but taught alongside intensive English and Japanese, soft skills, and real industry projects. Students did not just graduate job-ready; they graduated FPT-ready, culturally pre-aligned and language-capable from day one.

The genius of the move compounds over time, and it is best understood through Hamilton Helmer's idea of a "cornered resource"—exclusive access to a coveted asset on terms that competitors cannot match. The coveted asset in IT services is elite young engineering talent. While rivals like CMC or Rikkeisoft must fight in the open market, pay rising recruitment fees, and watch their best people get poached, FPT runs a captive feeder system that hands it first pick of a steady stream of pre-trained graduates. It is a structural insulation against the two diseases that plague the outsourcing industry: high engineer turnover and relentless wage inflation.

And here is the part that makes investors sit up: the university is not a cost center subsidized by the software business. It is one of the most profitable things FPT owns. By fiscal 2025, FPT Education served well over 150,000 full-time students and threw off a profit-before-tax margin of around 45.5%—reported at roughly VND 2,792 billion of pre-tax profit on about VND 6,132 billion of revenue.3 Read that again. A university with margins that would make a software company blush. FPT found a way to make its talent pipeline a high-margin profit engine in its own right—a cost solved and a cash cow created in a single stroke. We will return to why this matters so much when we war-game the competition.

Pivot 4: The Great Divestment of 2017 — The Courage to Shrink

By the mid-2010s, FPT had a different and subtler problem: it had become a sprawling conglomerate, and the market hated it for that. Bolted onto the high-margin software and telecom businesses were two enormous, low-margin retail and distribution arms—FPT Retail (the FPT Shop chain of electronics stores) and FPT Trading (the wholesale distribution business). Together these consumer businesses generated well over 60% of group revenue. That sounds great until you look at quality. They ran on razor-thin EBITDA margins of under 3%, devoured working capital to finance mountains of inventory, and dragged the entire group's blended profitability down into mediocrity. Institutional investors looked at FPT and saw a confusing mash-up: a world-class software exporter trapped inside a low-multiple electronics retailer. The stock was valued accordingly—cheaply.

So in 2017, FPT made the kind of decision that separates disciplined companies from empire-builders. It chose to shrink its revenue in order to grow its value. It sold a majority stake in FPT Trading to Taiwan's 聯強國際 Synnex Technology International—one of the world's largest IT distribution groups—rebranding the business as Synnex FPT.[^5] And it deconsolidated FPT Retail, selling down its majority stake via a private placement to the respected funds Dragon Capital and VinaCapital, followed by a public listing of FPT Retail (ticker FRT) in 2018.4

The financial alchemy that followed is the whole point. When you strip two giant, low-margin businesses out of your reported financials, your top line falls—and for an ego-driven conglomerate, falling revenue is unthinkable. But FPT's leadership understood that revenue is vanity and margin is sanity. With the retail and distribution drag removed, FPT's pre-tax profit margin roughly doubled, from around 7% to around 14%. Overnight, the financial profile transformed from "bloated trader" to "lean, high-growth technology and telecom champion." The market re-rated the stock from a low-multiple conglomerate to a premium-multiple tech company, and the cash windfall from the sales gave FPT a war chest to fund the global acquisition engine that would define its next decade. The courage to divest is one of the great recurring lessons of this story—and it sets up the question of what, exactly, FPT did with all that focus and all that cash.

IV. The Core Engine: Global IT Services & The "1:10" M&A Playbook

Let's ground ourselves in scale, because scale tells you where FPT actually sits in the global pecking order. In fiscal 2025, FPT's global IT services business generated revenue on the order of $1.34 billion, with signed contracts heading toward and beyond $1.5 billion, growing at a healthy mid-teens clip.25 That is a serious business—but let's be honest about where it ranks. India's 塔塔 Tata-owned TCS does roughly $29 billion. LTIMindtree does around $4.6 billion. The digital-engineering specialists FPT most wants to be compared to—EPAM Systems at roughly $5.5 billion, and the Latin American digital-native Globant at around $2.45 billion—are all bigger.

But size is a snapshot; the slope of the line is the story. FPT has been compounding its global IT services revenue at roughly 15–18% a year. In 2025, Globant grew about 1.6%. EPAM, buffeted by its heavy exposure to Eastern Europe, has been roughly flat. So FPT is not the biggest fish, but it is one of the fastest-swimming, and it is closing the gap on Globant with every passing quarter. For a frontier-market company, "smaller than the giants but growing several times faster than the mid-caps" is an enviable place to be.

Why can FPT grow so fast and so profitably? The first answer is the boring, powerful one: cost. Software engineering delivered from Vietnam carries roughly a 50–60% cost discount relative to onshore engineering in the U.S. or Japan, and—critically—a 15–20% discount even relative to India, with quality that is at least as good in the modern tech stacks that matter most today: cloud, IoT, automotive, and embedded systems. Vietnam, in other words, undercuts even the original low-cost king. That is the raw material. But a cost advantage alone is a commodity, and commodities don't earn premium multiples. The real magic is in how FPT packages that cost advantage—and that brings us to the acquisition playbook.

The "1:10" Strategy: Buy the Brain, Attach the Hands

Most people assume a company like FPT grows by acquiring other offshore code shops—more cheap engineers, more capacity. FPT does almost the exact opposite. Its M&A doctrine is to buy small, high-end onshore consulting and product-engineering boutiques in the West—typically just 100 to 300 employees—the firms that sit in the room with Fortune 500 clients and design the strategy. FPT then plugs these expensive Western "brains" into its vast, cheap Vietnamese "hands." For every one high-cost consultant the boutique fields onshore, FPT can attach roughly ten low-cost engineers offshore. The consultant wins and shapes the work; Vietnam delivers it at a fraction of the cost. The blended economics are extraordinary—you get Western client access and credibility with Vietnamese delivery margins.

Walk through how this doctrine evolved, deal by deal, because each one taught FPT something.

RWE IT Slovakia (2014) was FPT's first outbound acquisition, and it was structured with real cunning. FPT didn't just buy a generic IT shop; it executed a carve-out of the internal IT department of the German utility giant RWE, picking up roughly 400 Slovakian engineers. The masterstroke was the attached commitment: a guaranteed multi-year IT services contract reportedly worth well over $100 million. In one move FPT bought itself an instant, de-risked, high-credibility foothold in the European utility sector—a captive anchor client and a European delivery base in a single transaction. This was the template: don't just buy people, buy a relationship and a revenue stream.

Intellinet (2018) sharpened the doctrine toward the front end of the value chain. FPT acquired a 90% stake in the U.S. management consulting firm Intellinet in a deal valued at up to $50 million—a price that worked out to a meaningful premium, roughly 1.67 times Intellinet's revenue.6 Why pay a premium for a small consultancy? Because FPT wasn't buying revenue; it was buying positioning. Intellinet's consultants sat at the strategy table with American enterprises, designing digital transformations. Each of those engagements became a doorway through which FPT could march its offshore Vietnamese developers. The premium on the front-end "brain" pays for itself many times over in the offshore "hands" it pulls along behind it.

The 2023 North American expansion scaled the model into nearshore delivery. FPT committed around $100 million to deepen its product-engineering and nearshore capabilities, acquiring Cardinal Peak, a U.S. product-engineering and embedded-IoT firm, and Intertec International, which brought nearshore delivery centers in Costa Rica and Colombia.7 These were bought at disciplined multiples in the range of 1.2 to 1.7 times revenue. The Costa Rica and Colombia centers gave FPT a "nearshore" option in the same time zones as U.S. clients—useful for work that needs real-time collaboration—while Cardinal Peak added hardware-adjacent embedded engineering that would prove prescient as FPT moved toward semiconductors.

Now, the part that makes this a genuinely clever piece of financial engineering. FPT's own stock trades at a premium valuation in Vietnam—a price-to-earnings multiple in the low-to-mid 20s. It uses that expensive currency, plus its robust cash flow, to buy Western boutiques at low single-digit revenue multiples. The instant FPT folds an acquired firm into its higher-multiple structure and supercharges its margins with offshore Vietnamese leverage, value is created out of the spread. Buy cheap private boutiques, run them through a high-multiple public vehicle, and pump up their EBITDA with the 1:10 model—that is multiple arbitrage and margin arbitrage stacked on top of each other. It is the financial expression of the same instinct that built the university: control the inputs, capture the spread, and never compete on the buyer's terms when you can change the terms.

A small but real second-layer caution belongs here. The whole 1:10 model rests on the seamless integration of Western consultants with Vietnamese delivery, and culture clashes in cross-border services acquisitions are the rule, not the exception. FPT's deals have so far been small and digestible, which is itself a discipline—it has never bet the company on a single mega-acquisition. But the integration risk is the quiet counterweight to all this cleverness, and we will return to it in the bear case.

V. Leadership & The Meritocratic Succession Playbook

Here is a sentence you do not get to write about many emerging-market conglomerates: FPT is widely regarded as one of the most transparent, professionally managed, Western-style public corporations in Southeast Asia. In a region where too many large companies are family fiefdoms, run for the benefit of a founding clan or wired into political patronage, FPT institutionalized itself. Understanding how it did that means understanding two men and one very clever compensation scheme.

The first man is the one we have followed since the dried bananas: Trương Gia Bình, now Executive Chairman and the company's spiritual anchor. Bình long ago stopped running day-to-day operations and reinvented himself as FPT's chief diplomat and strategist-in-chief—the man who flies to Silicon Valley to shake hands with Jensen Huang, who sits on national technology councils helping shape Vietnam's digital policy, and who personally brokers the marquee partnerships that open doors no salesperson could. He owns roughly 6.89% of FPT, a stake worth somewhere in the range of $320 million to $470 million depending on the day's price. The detail that tells you everything about his mindset: he has reportedly never sold a single share since FPT's IPO in 2006. In a world of founders cashing out at the first liquidity event, Bình's iron grip on his original stake is a costly, credible signal of extreme long-term alignment—his wealth lives or dies with the public shareholders'.

The second man is the more revealing one, because his story is the real governance achievement. Nguyễn Văn Khoa was appointed CEO of FPT Corporation in March 2019. Khoa is not a founder. He is not family. He is, in the local shorthand, a member of the "7X generation"—born in 1977—and his career is a pure meritocratic ascent. He joined FPT in 1997 as a low-level technical support employee. Let that sink in: the man now running a multi-billion-dollar technology group started by answering support tickets. Over twenty-two years he climbed every rung—rising to lead FPT Telecom, then FPT Information System, building a reputation as a hard-driving operator obsessed with execution—before being handed the keys to the entire corporation. He owns a comparatively modest 0.32% stake, worth roughly $15 million.

Why does this matter to an investor? Because the graveyard of emerging-market business is filled with companies that thrived under a charismatic founder and then disintegrated when he died, retired, or handed the company to an unqualified son. FPT's deliberate transition from the visionary, deal-making founder to a disciplined, internally-groomed, non-family professional manager is a textbook case of de-risking a company's most dangerous single point of failure. Bình still sets the vision and opens the doors; Khoa runs the machine. The charisma and the execution have been institutionally separated, which is exactly what you want when you are betting on a company lasting decades.

The Golden Handcuffs: FPT's ESOP

The third piece of the leadership puzzle is how FPT keeps its talent from walking out the door into a competitor's arms—and it is one of the most elegant retention mechanisms in the business. Every year, FPT runs an Employee Stock Ownership Plan, but with a twist that turns it into a powerful set of golden handcuffs.

ESOP shares are issued to selected employees at par value—VND 10,000 per share—which represents a staggering discount of more than 90% to the market price. That is an enormous, life-changing gift of value to the recipient. But it is strictly rationed and strictly conditional. The plan targets senior leaders and standout contributors, and the allocations are gated on the company hitting its net-profit targets, so the reward is tied to collective performance, not just tenure. And then comes the catch that makes it work: the shares are locked up for a strict three-year period. If an employee resigns or is terminated during that window, FPT has the right to buy the unvested shares back at the original par value—essentially clawing back the gift.

Think about what this does to a star engineer's decision to jump ship. A domestic rival comes calling with a higher salary. But leaving means forfeiting a fortune in deeply-discounted, not-yet-vested FPT stock, handed back to the company for pennies. The math usually keeps them in their seat. In an industry where the entire competitive game is talent, and where poaching is the primary weapon, FPT engineered a structural reason for its best people to stay—mitigating the single greatest source of supplier power in its industry. This is the same philosophy as the university, expressed in compensation rather than education: don't fight the talent war on the open market's terms; rig the board in your favor. With its people locked in and its leadership institutionalized, FPT was free to make the boldest bet of its history—on artificial intelligence and silicon.

VI. The Future-Material Play: NVIDIA, Sovereign AI, and Silicon

For most of its life, FPT sold human effort—engineers writing code for clients. Between 2024 and 2026, it began trying to become something categorically different: a company that owns AI infrastructure and designs physical hardware. This is the riskiest and most ambitious chapter yet, and it rests on a concept worth explaining plainly: sovereign AI.

Here is the idea in everyday terms. When a Vietnamese bank or a government ministry wants to use a powerful AI model, it has a problem. The best models and the cloud data centers that run them mostly sit overseas, controlled by American hyperscalers. Sending sensitive national or financial data to a server in another country to be processed is, for many governments, a non-starter—a matter of security, regulation, and national pride. "Sovereign AI" means keeping the entire stack—the chips, the data, the trained models—physically inside national borders, under national control. It is the digital equivalent of insisting that your nation's gold stays in your own vault rather than someone else's.

The NVIDIA Partnership and the $200 Million AI Factory

In April 2024, FPT announced a partnership with NVIDIA—the company whose GPUs are the picks and shovels of the entire AI gold rush—to build a $200 million AI Factory in Vietnam.[^1] An "AI Factory," in NVIDIA's framing, is essentially a specialized data center purpose-built to do one thing: train and run AI models at massive scale. FPT's facility would be packed with NVIDIA's H100 Tensor Core GPUs, the most coveted AI chips on the planet at the time, and offered as a sovereign cloud—letting Vietnamese enterprises and government agencies train their own localized large language models on Vietnamese-language data, securely, without that data ever leaving the country.

For Bình, this was the diplomatic deal of a lifetime: it positioned FPT not as a vendor but as the foundational infrastructure provider for Vietnam's entire AI ambition. And FPT did not stop at home. By late 2024 it extended the model abroad, launching an AI Factory in Japan built around NVIDIA's even more powerful H200 GPUs—directly targeting the same sensitive, sovereignty-conscious AI demand in its most important market that it had spent twenty years cultivating. The logic was identical to the BrSE playbook: meet a high-trust market on its own terms, on its own soil.

FPT Semiconductor and the First Chip Export

The second leg of the future bet is silicon, and FPT's approach is defined as much by what it refuses to do as by what it does. FPT established FPT Semiconductor in 2022. Crucially, it did not try to build chip fabrication plants—the staggeringly expensive, capital-devouring foundries where companies like 台積電 TSMC turn sand into chips and where a single fab can cost more than FPT's entire market value. Competing with TSMC on fabrication would be corporate suicide. Instead, FPT chose the fabless model: it designs chips and outsources the actual manufacturing. Designing chips is a brain-and-software business—exactly FPT's wheelhouse—rather than a capital-and-real-estate business. To accelerate, it partnered with Taiwan's 世芯 Alchip to build an overseas design center.

Then came the milestone. In December 2025, FPT shipped its first batch of commercial chips into Japan—specifically, power management integrated circuits, or PMICs.1 In plain language, a PMIC is the chip that acts as the careful electrician inside a device: it manages and stabilizes the internal power supply, protects delicate components from voltage and current spikes, and keeps everything running reliably under heavy load. FPT's PMICs were designed for high-performance multi-function office printers, and they were delivered through Restar, a major Japanese electronics distributor, with plans reportedly to distribute up to 10 million FPT-designed chips across the Asia-Pacific region by 2027.1

Now, the honest materiality check: this is, today, a rounding error in FPT's revenue. Nobody should pretend a few batches of printer chips move a $2.85 billion company's numbers. The significance is strategic, not financial—at least not yet. The fact that a Vietnamese-designed "Make in Vietnam" chip passed Japan's notoriously brutal industrial-grade quality, reliability, and safety standards is a proof of capability that money cannot buy.1 And it lands at exactly the right moment in history, as global electronics manufacturers scramble to diversify their hardware supply chains away from concentration in China—the "China Plus One" strategy. FPT is positioning Vietnam, and itself, as a credible "Plus One" not just for software but for silicon design. The path from rounding error to material business is long and uncertain, but for the first time it is visible.

The 2026 Deconsolidation of FPT Telecom

The final piece of the future-shaping is an accounting maneuver that is really a strategy in disguise. In early 2026, FPT restructured its telecommunications arm, FPT Telecom, shifting it from full consolidation onto the equity method of accounting. The mechanics matter less than the motive. FPT Telecom is a wonderful business—it is one of Vietnam's largest broadband providers—but it is asset-heavy: building and maintaining a physical fiber-optic network requires enormous, lumpy capital expenditure, and that asset-intensity weighs on the kind of clean, capital-light financial profile that software investors prize.

By moving telecom to the equity method, FPT effectively lifts the asset-heavy telecom revenue and assets off its consolidated top line, leaving behind a leaner financial statement dominated by global IT services, AI, and software. The intent is unmistakable: to present FPT to the public markets as a "pure-play" global AI and software services company, the kind of business that commands the rich valuation multiples of a Western software firm rather than the more modest multiples of a diversified Asian conglomerate. It is the 2017 divestment logic applied with an accountant's scalpel instead of a banker's gavel—reshaping not the business itself so much as how cleanly the market can see the business it wants you to see. Whether the market grants that re-rating is one of the central open questions in the FPT story, and it leads us straight into the strategic war-gaming.

VII. Strategic Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Strip away the narrative and ask the cold question a long-term investor must ask: what, structurally, stops a competitor from doing to FPT what FPT did to the incumbents? To answer it, let's run FPT through two frameworks—Hamilton Helmer's 7 Powers and Michael Porter's Five Forces—not as an academic exercise but as a war game.

Hamilton's 7 Powers Applied to FPT

The Cornered Resource — FPT University. We have met this already, and it is, in this author's reading, FPT's single most durable power. A company that owns the factory producing its scarcest input—elite, multilingual young engineers—has changed the game from "compete for talent" to "harvest talent." Competitors must bid in an open market growing more expensive every year; FPT skims the cream off a captive pipeline of 150,000-plus students before that market ever sees them. Powers are only valuable if they are hard to replicate, and replicating an accredited, profitable, two-decade-old university system is a feat measured in years and reputations, not dollars. This is the moat beneath all the other moats.

Scale Economies. FPT is the undisputed number-one IT company in Vietnam, fielding a software engineering force of more than 30,000 people. That scale is not just bragging rights—it is a gate. Sovereign-level government contracts, nationwide banking transformations, and massive multinational enterprise deals require a bidder who can credibly throw thousands of engineers at a problem and stand behind a decade-long commitment. Smaller domestic rivals like CMC and Rikkeisoft, however capable, simply cannot write that bid. Scale lets FPT play in a league with far less competition than the crowded small-shop tier.

Switching Costs. Once FPT has woven its proprietary middleware, cloud architecture, or deeply-customized ERP systems into the beating heart of a client's operations—the core banking platform, the manufacturing backbone—ripping it out becomes a nightmare of cost, risk, and operational disruption. The deeper FPT embeds, the more switching becomes unthinkable, and the more pricing power FPT quietly accrues over the life of the relationship.

Counter-Positioning. This is the power that built the company, and it is worth naming precisely. In the early 2000s, FPT positioned itself against the dominant Indian and Western giants by offering something they structurally would not: highly competent, Japanese-fluent engineering at a 40–50% cost advantage, aimed at the mid-tier Japanese and American enterprises that an Accenture or a TCS found too small to bother with. The incumbents could not easily copy this without cannibalizing their own higher-priced model or building a Japanese-language capability from scratch—so they ceded the ground. FPT grew up in the blind spot of giants.

Porter's Five Forces

Threat of New Entrants — Low to Moderate. Anyone can start a software shop in a garage in Hanoi tomorrow. That is the moderate part. But scaling that shop into a global enterprise with delivery centers across the U.S., Europe, Japan, and Latin America, backed by its own university and decades of Fortune 500 references—that requires billions in capital, twenty years of relationship-building, and a brand earned one delivered project at a time. The barrier is not to entry; it is to meaningful entry.

Bargaining Power of Suppliers — High, but Mitigated. In a people business, the "suppliers" are the engineers, and skilled developers hold enormous leverage in a globally tight market. This is the structural threat to every outsourcing firm. FPT's entire strategy can be read as a sustained assault on this single force: the university suppresses the cost and secures the supply of new engineers, and the ESOP golden handcuffs lock the experienced ones in place. FPT does not eliminate supplier power, but it has built more defenses against it than perhaps any competitor on Earth.

Bargaining Power of Buyers — Moderate. Enterprise clients have options and they negotiate hard, especially on commodity coding work. But as FPT climbs the value chain—from writing code to designing the digital strategy via Intellinet and Cardinal Peak, to running mission-critical cloud architecture—the relationship shifts from interchangeable vendor to embedded partner, and buyer power erodes against the switching costs described above.

Threat of Substitutes — Low to Moderate, and Rising. Here is the force that should worry investors most. Generative AI tools can now automate a growing share of basic coding—the very bread-and-butter work that fills the seats of a large offshore developer army. If a machine can write the code a junior Vietnamese engineer used to write, the substitute threat goes straight to the heart of FPT's model. FPT's response is to run toward the threat: declaring itself an "AI-first" company, embedding AI tools into its own engineers' workflows to roughly double their productivity, and racing up-market into high-end chip design and sovereign AI infrastructure where human judgment is still indispensable. Whether it can climb faster than the machines can automate beneath it is the defining question of the bear case.

Intensity of Competitive Rivalry — High. FPT is squeezed from above by the Indian giants and the digital-natives like EPAM and Globant, and from below by hungry domestic and regional rivals. The industry is genuinely competitive. FPT's edge in the scrum is the combination only it possesses: the lowest credible cost base (Vietnam, undercutting even India), the unique Japanese-language franchise, and the captive talent factory. That cocktail is hard to assemble, which is precisely why the rivalry, however intense, has not eroded FPT's growth.

VIII. Playbook: Key Lessons, Bear vs. Bull, & KPIs to Track

The Durable Business & Investing Lessons

Lesson one: solve your own bottleneck. When FPT hit the wall of engineer scarcity, it did not write a white paper begging the government to fix the education system. It built a university. The deeper principle for investors is that the most powerful moats are often born from a company's most painful constraints. A bottleneck that everyone else accepts as a cost of doing business can, with enough audacity and capital, be converted into a proprietary asset—and even, as FPT proved, into a high-margin profit center in its own right.

Lesson two: the courage to divest. The natural gravity of every conglomerate is toward empire—toward hugging low-margin revenue because big top-line numbers feel like success. FPT's 2017 decision to amputate 60% of its revenue in order to double its margin and earn a re-rating is the antidote, and it is a discipline most management teams talk about and few actually execute. The 2026 telecom deconsolidation shows the same instinct still alive. Watch what a company is willing to give up; it tells you more than what it acquires.

Lesson three: institutionalize the succession. The transition from a charismatic founder to a tech-support-employee-turned-CEO, with the founder stepping into the role of diplomat rather than clinging to operational control, is how a company built around one extraordinary person becomes a company that can outlive him. For long-term holders, governance quality is not a soft factor; in emerging markets it is frequently the entire ballgame.

The Bull vs. Bear Case

The bull case writes almost itself from everything above. As the global supply chain reorganizes around "China Plus One," FPT is a prime beneficiary in both software and, increasingly, silicon—the trusted, lower-cost, geopolitically-neutral alternative. Its Japanese franchise keeps compounding; its U.S. nearshore and onshore footprint keeps expanding. The NVIDIA-backed AI factories scale into a genuine sovereign-cloud business, and FPT Semiconductor parlays its printer-chip beachhead into a real designer of IoT and automotive chips for a hardware-hungry world. The university keeps minting elite engineers at a fraction of competitors' costs, holding FPT's superior margins steady even as the industry's wages climb. And the 2026 telecom deconsolidation finally convinces the market to value FPT as the pure-play global software-and-AI company it is becoming, dragging its multiple toward Western software levels. In this scenario, FPT is not a frontier-market curiosity but a structurally advantaged compounder hiding in plain sight in Hanoi.

The bear case is equally coherent, and it is the one that pivots on a single word: automation. If generative AI automates basic and intermediate software engineering faster than FPT can climb up the value chain, the company's greatest asset—a 30,000-strong offshore developer army—becomes its greatest liability, a fixed cost base of skills the market no longer needs to rent. Layer on the integration risk: cross-border consulting acquisitions are notorious for culture clashes, and a stumble in folding expensive American consultants into a Vietnamese delivery culture could blunt the entire 1:10 model. Add the threat that the very success of Vietnam's tech sector triggers domestic wage inflation steep enough to erode the cost advantage that is FPT's foundation—and that FPT University, for all its strengths, fails to retool fast enough to produce the specialized AI and chip-design talent the next era demands rather than the general-purpose coders of the last one. In the bear scenario, FPT is a brilliant champion of an era that is ending, racing against a clock it may not beat.

The truth, as usual, lives in the tension between these two stories—which is exactly why a disciplined investor watches a small number of specific signals rather than the noise.

The 1–3 KPIs That Matter Most

If you track only a handful of things about FPT, track these.

First, global IT services signed-contract revenue growth. This is the cleanest leading indicator of the whole thesis—it tells you in advance whether FPT is still winning large-scale global work and gaining share, or whether demand and the cost advantage are fading. Sustained growth comfortably above 20% says the engine is healthy; a deceleration toward the low teens or single digits would be the first hard evidence the bear case is arriving. Signed contracts lead reported revenue, so this is the number that moves first.

Second, FPT Education's enrollment and pre-tax-profit margin. This is the health monitor for the cornered resource at the foundation of everything. Enrollment holding above 150,000 students confirms the talent pipeline is still flowing; a PBT margin staying north of 40% confirms the pipeline remains a profit engine rather than a subsidized cost. If either metric cracks—enrollment stalling, margins compressing—the moat beneath the moats is weakening, and you would want to know early.

Third, the onshore-to-offshore leverage ratio. This is the profitability dial of the entire international business—roughly one onshore consultant to ten or more offshore engineers. The more offshore leverage FPT can sustain per onshore consultant, the fatter the margins on every Western deal. If that ratio compresses—if FPT finds it needs more expensive onshore bodies per project, whether because of AI disruption, client demands, or integration friction—the margin story quietly deflates. It is the single best gauge of whether the 1:10 magic is still working.

IX. Epilogue & Outro

FPT is, in the end, the story of Vietnam's economic rise written in code. Thirty-eight years ago, thirteen scientists with borrowed money and a name about food processing set out to use science to pull their country out of poverty. They survived by trading whatever they could, pivoted into the computers they actually loved, and then—through a failed American gambit, a triumphant Japanese pivot, a university built from scratch, a conglomerate courageously dismantled, a meritocratic succession, and now a bet on AI and silicon—they built one of the most strategically coherent technology companies to ever emerge from a frontier market.

The deepest lesson is that FPT found a way out of what might be called the labor-arbitrage trap. Most emerging-market outsourcers are forever vulnerable: their only edge is cheap labor, and cheap labor inevitably gets less cheap, or gets automated, or gets undercut by the next poorer country. FPT escaped that trap by vertically integrating the entire stack of its own advantage—educating its talent, owning its consulting front-end, controlling its delivery engine, and now reaching into AI infrastructure and chip design. Each layer reinforces the others into something far harder to replicate than a low wage bill: a self-sustaining, sovereign technology ecosystem.

If you want to understand where global technology infrastructure is moving next, don't just look at Silicon Valley or Bangalore—keep your eyes on Hanoi, Da Nang, and FPT.

References

-

FPT Makes First Commercial Chip Delivery into Japan Market — FPT Software, 2025-12-30 ↩↩↩↩

-

FPT Education Segment Milestones and Student Growth — Sands Capital, 2025-10-15 ↩

-

FPT Divests from FPT Retail and FPT Trading — Vietnam News, 2017-08-15 ↩

-

FPT recorded profit before tax of VND 9,540 billion, up 17.6% year-on-year — FPT Corporation, 2025 ↩

-

FPT Corporation Stock Profile & Corporate Structure — The Investor (Vietnam Investor Network) ↩

-

FPT Acquisition of Cardinal Peak — Cardinal Peak Press Release, 2023-11-06 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube