Wilmar International: The Invisible Empire of the Global Kitchen

I. Introduction: The Cargill of the East

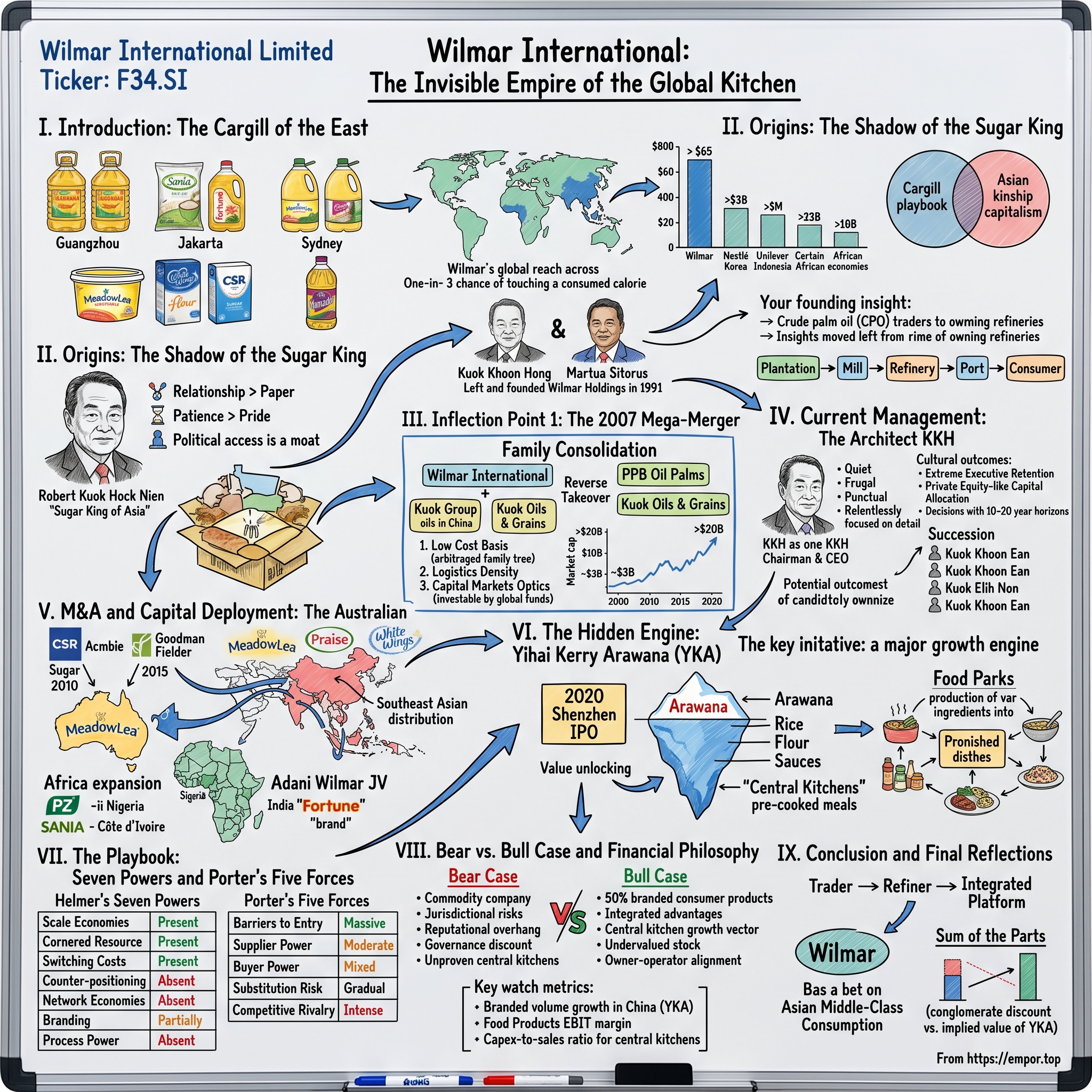

Walk into a wet market in Guangzhou before dawn and you will see the stall-keepers stacking golden five-liter jugs of cooking oil under a harsh fluorescent glow. The label reads "Arawana"—a stylized dragon fish curling over three Chinese characters. Walk into a Carrefour in Jakarta by mid-morning and you will find shelves lined with "Sania" rice and "Fortune" palm oil. Walk into a Coles supermarket in Sydney by afternoon tea time and you will find "MeadowLea" margarine, "White Wings" flour, and "CSR" sugar. Walk into a crowded canteen in Lagos at dinnertime, and a ladle of "Mamador" vegetable oil sizzles over jollof rice.

Four continents. Four different languages on the packaging. One company collecting the margin.

That company is Wilmar International, headquartered in a glass tower on Neil Road in Singapore, and if you have consumed a calorie today that was not grown in your own garden, there is a roughly one-in-three chance Wilmar touched it somewhere between the farm and your fork. The company crushes soybeans in Shandong, refines palm oil in Sumatra, mills wheat in Mumbai, ferments sugar in Queensland, and trucks instant noodles to high-rises in Chongqing. Its revenue in the most recent fiscal year was north of sixty-five billion US dollars—larger than Nestlé Korea, larger than Unilever Indonesia, larger than the entire economy of several of the African countries where it operates.

And yet, if you stopped ten people on Wall Street and asked them to name the company, nine would shrug. That anonymity is not an accident. It is the architecture of the business. Wilmar is what happens when you take the Cargill playbook—vertical integration, commodity scale, capital discipline—and graft it onto the particular soil of Asian kinship capitalism. The result is an organism unlike any of its Western peers: owner-operated, family-entangled, politically dexterous, and allergic to the branded-goods vanity that consumes the quarterly earnings calls of the Nestlés and Unilevers of the world.

Here is the thesis. In 1991, a quiet Singaporean businessman named Kuok Khoon Hong—the nephew of the legendary "Sugar King of Asia," Robert Kuok—left his uncle's empire and started a tiny palm oil trading shop with an Indonesian partner named Martua Sitorus. Over the next thirty-five years, that shop became the integrated-agribusiness benchmark for an entire region. They did it by systematically moving down the value chain from the tree, through the mill and the refinery and the port, and up the value chain into branded consumer packs, specialty oleochemicals, and now, in a move that would have seemed absurd a decade ago, pre-cooked meals delivered to the Chinese urban middle class.

This episode is about how a "trader" became an "operator," how an operator became a "consumer brand," and how a consumer brand is quietly becoming something closer to the Nestlé of Asia. It is also about the architecture of a company that trades on the Singapore Exchange at what many long-term investors believe to be a persistent discount to the sum of its parts—a discount partially crystallized by the 2020 Shenzhen IPO of its Chinese subsidiary, Yihai Kerry Arawana.

We will walk through the Kuok family legacy, the Great Recombination of 2007, the Australian gamble, the Arawana phenomenon, the seven powers that make the moat nearly unassailable, and the bull and bear debates over whether Wilmar is a commodity trader in disguise or a consumer-goods giant trapped in a commodity trader's valuation. Grab a cup of coffee. The tree this story begins under is oil palm, and its roots run deep.

II. Origins: The Shadow of the Sugar King

The oldest business lesson in Southeast Asia is delivered, not in classrooms, but in the small dining rooms of Chinese-diaspora patriarchs—and in the Kuok family, the patriarch was Robert Kuok Hock Nien. Born in 1923 in Johor Bahru, the son of a Fujianese rice-and-sugar trader, Robert Kuok built an empire that spanned sugar, shipping, hotels (Shangri-La), media (the South China Morning Post, at one point), and property from Kuala Lumpur to Beijing. By the 1970s he controlled an estimated ten percent of the global sugar trade. The Malaysian press crowned him the "Sugar King of Asia," and the nickname, by the 1980s, had become simply "Uncle Robert."

You cannot understand Wilmar without understanding what "Uncle Robert" taught the next generation. Three lessons matter. First: in Asia, the contract is the relationship—not the paper. Second: the commodity business rewards patience, but punishes pride; never overpay for trophies, never fall in love with an asset. Third: political access is a moat, not a sin. Navigate it with dignity, hire locally, pay taxes, keep your name out of the newspapers. Those three lessons became the operating system of every business the Kuok family touched. They became, eventually, the operating system of Wilmar.

Kuok Khoon Hong, the protagonist of our story, is Robert's nephew—the son of Robert's elder brother Philip. Born in 1949 in Johor Bahru, "KKH" (as he is universally known inside the company) trained as an accountant, joined the family-controlled Perlis Plantations in the 1970s, and spent roughly fifteen years inside the Kuok Group cutting his teeth on Malaysian palm estates, edible oils trading, and the first forays into China after Deng Xiaoping's 1978 reforms. By 1991, he was a quiet forty-something executive with encyclopedic knowledge of the palm oil value chain and a clear view that the family conglomerate was too diversified, too consensus-driven, and—by his reckoning—missing the China opportunity.

So he left. Not with drama. Not with acrimony. With, one imagines, a long dinner and a respectful bow. And he took with him a partner he had met on the refinery circuit in Medan: Martua Sitorus, a North Sumatran ethnic-Chinese Indonesian, twelve years his junior, who knew every planter, every port master, and every customs official on the eastern coast of Sumatra. Together, in 1991, they founded Wilmar Holdings—the name a portmanteau of "William" (a Kuok family name) and "Martua." Initial capital was modest. Their first office, in Singapore, was less than a thousand square feet.

The founding insight was small, technical, and in hindsight, world-historical. At the time, the palm oil trade was dominated by traders who bought crude palm oil (CPO) at the mill gate, shipped it, and sold it to Western refiners—Unilever, Procter & Gamble, Cargill—who would refine it, bleach it, deodorize it, and fractionate it into the olein and stearin streams that consumer goods companies actually used. The margin, in other words, was captured by whoever owned the refinery, not whoever traded the raw crude. KKH and Martua looked at that structure and asked a simple question: why should the margin flow offshore? The Indonesian planters produced the oil. The Asian consumers ate the oil. Why was the refining value being booked in Rotterdam?

So they built refineries. First one, then three, then a dozen, scattered across Indonesia and later Malaysia, each one strategically sited next to a port with deep-water access. By the mid-1990s, Wilmar was no longer a trader—it was a processor. And the processor margin, even in a commodity business, compounds.

Then came the China bet. In 1992, while Cargill and ADM were still debating the risks of investing in a country that had just experienced Tiananmen, KKH signed a joint venture with the state-owned China Grain Reserves Corporation (which would later become COFCO) to build an edible-oil refinery in Shenzhen. That first refinery—the Nanhai plant—became the template. Refineries followed in Qingdao, Tianjin, Shanghai, and eventually nearly every coastal province. By 2000, Wilmar had what no Western competitor had: a physical, integrated, on-the-ground presence in the single largest edible-oil consumption market in the world, in partnership with an entity that would later become the dominant state food trader. The "Kerry" name—borrowed from Uncle Robert's Hong Kong property vehicle, Kerry Properties—became the brand under which the China oils business operated.

None of this was glamorous. There were no business school case studies written about Wilmar in the 1990s. But by the end of the decade, the company was the largest edible-oil refiner in Asia, and KKH had done something quietly remarkable: he had built, without fanfare, the dominant processor in the two largest palm-oil-producing countries in the world and the dominant consumer-oil refiner in the world's largest consuming country. What remained was to stitch it all together.

That stitching would happen in 2007. And it would change the definition of "agribusiness" in Asia forever.

III. Inflection Point 1: The 2007 Mega-Merger

The deal was announced on December 14, 2006, and closed on June 29, 2007. On paper, it was a reverse takeover: Wilmar International, already listed on the Singapore Exchange, would absorb the edible-oils, grains, and plantation assets of the Kuok Group and its related entity PPB Oil Palms, in a series of share-and-cash transactions valued, in aggregate, at approximately four-point-three billion US dollars.

On paper, that is what it was.

In reality, it was a family consolidation—and one of the cleverest pieces of corporate architecture ever executed in Southeast Asia.

To understand why, you have to understand what was actually being combined. By 2006, the Kuok agribusiness universe was a sprawling, federated thing. There was Wilmar itself (palm refining, oils trading, China distribution). There was PPB Oil Palms in Malaysia (around 573,000 hectares of oil palm plantations and the associated mills). There was the Kuok Group's edible-oils business in China. There was Kuok Oils & Grains (trading, shipping). There were sugar and flour interests. All of these were run by different Kuok nephews, cousins, or professional managers, with different cost structures, different auditors, and different shareholder bases. The family had, in effect, recreated a mini-Cargill across half a dozen corporate vehicles, with all the inefficiencies that implied.

KKH's pitch was elegantly simple. Put it all under one roof. Use the listed Wilmar vehicle as the consolidator. Pay fair but not premium multiples, because the counterparty is family and the logic is strategic integration, not competitive bidding. And in one stroke, create the first truly vertically integrated agribusiness giant in Asia: plantation, mill, refinery, trader, shipper, consumer brand—all in one corporate entity, all listed, all auditable, all investable by global institutional money.

Why did it matter that much? Three reasons.

First, cost basis. By consolidating plantation assets at what was effectively book value plus a modest uplift—rather than the twelve- or fifteen-times EBITDA multiples that would have applied in a competitive auction—Wilmar walked away with a plantation cost basis per hectare that its Western competitors simply could not match. Cargill, Bunge, and ADM would spend the next decade trying to build comparable upstream positions in Indonesia and Malaysia, and every time they priced a deal, they were pricing against bidders who paid post-consolidation prices. Wilmar had, in effect, arbitraged its own family tree.

Second, logistics density. Before 2007, a Wilmar refinery in Dumai and a PPB plantation in Sabah might have been in the same biosphere but in different accounting universes. After 2007, they were in the same supply chain. A gallon of crude palm oil could move from tree to mill to refinery to port to China without ever crossing a third-party invoice. That is the mathematical definition of integration, and in a low-single-digit-margin commodity business, integration is everything. Every basis point of logistics efficiency drops straight to the bottom line.

Third, capital markets optics. A consolidated entity on the Singapore Exchange, with audited financials and a single CEO, became investable by index funds, sovereign wealth funds, and long-only managers who would never have touched a private-family federated structure. The market cap went from around three billion US dollars pre-merger to more than twenty billion within eighteen months. Robert Kuok, though never the executive chairman of Wilmar, became—through the family trust—one of the largest single beneficial owners of a listed agribusiness anywhere in the world.

The subtle genius of the 2007 deal was that it did not look like a masterstroke at the time. The financial press covered it as a "reorganization." The Singapore exchange filings were dry. Analysts debated whether Wilmar had overpaid for Martua Sitorus's smaller stakes in some of the Indonesian mills. But a decade later, when Bunge was writing down its Indonesian assets and ADM was retreating from Southeast Asia, the true cost-basis advantage of the 2007 recombination became visible. You cannot out-compete a family that already owns the tree.

With integration complete, Wilmar had, by 2008, become the dominant agribusiness player between the Arabian Sea and the Pacific. Revenue, which had been around six billion US dollars in 2005, crossed twenty-nine billion by 2008. The global financial crisis arrived shortly after, and in a moment when Cargill and ADM pulled back, Wilmar did the opposite: it bought. Rice mills in Vietnam. Flour mills in India. Sugar assets in China. The playbook was now clear, and the architect was just getting started.

IV. Current Management: The Architect KKH

Walk into the lobby of Wilmar's headquarters at 56 Neil Road in Singapore and the first thing you notice is what is missing. There is no soaring atrium. There is no sculpture of a tree. There is no wall of framed magazine covers celebrating the CEO. The lobby is small, functional, and lined with linoleum. A receptionist in a cardigan greets visitors with a clipboard. The elevators are slow. The carpets are, politely put, tired.

This is deliberate. It is, in fact, the most important thing to know about Kuok Khoon Hong's management style.

KKH is now in his mid-seventies. He is the Chairman and Chief Executive Officer of a company with over ninety thousand employees and operations in more than fifty countries. His personal stake, held directly and through family trusts, is roughly thirteen percent of the company—worth, depending on the day, somewhere in the neighborhood of four to five billion US dollars. He is, by any reasonable measure, one of the wealthiest individuals in Southeast Asia. And yet, colleagues who have known him for thirty years describe his working life in the same handful of words: quiet, punctual, frugal, and relentlessly focused on operational detail.

The frugality is not performative. KKH is famous, inside the company, for flying economy on short-haul Asian routes into his late sixties, for eating at the employee canteen when he is in the Singapore headquarters, and for personally scrutinizing capex requests above a certain threshold. The story that circulates—corroborated by multiple former executives, though never officially confirmed—is that during the 2008 financial crisis, when Wilmar was deciding whether to proceed with a planned refinery expansion in China, KKH personally drove from plant to plant, walked the sites, and approved or killed individual line items on a clipboard. This is, to put it mildly, not how Paul Polman ran Unilever.

What this style produces, culturally, is something unusual in the commodity world: extreme executive retention. Wilmar's C-suite and senior operating layer have, in many cases, been with the company for more than two decades. The CFO, the COO of the oilseeds segment, the heads of the China, India, and Africa regions—these are lifers, some of whom joined before the 2007 merger, some of whom followed KKH out of the Kuok Group in the early 1990s. Stock-based compensation is disciplined. Cash bonuses are tied to business-unit return on invested capital, not stock price. The effect is that, unlike many modern multinationals where the C-suite functions as a rotating cast of mercenaries, Wilmar's senior team behaves like what it largely is: a group of partners who have worked together for a generation and who own, collectively, a meaningful piece of the enterprise.

This is what makes Wilmar behave, in the capital allocation sense, more like a private equity fund than a commodity trader. Decisions are made with ten- and twenty-year horizons, not quarterly ones. A refinery that will not earn its cost of capital for five years is approved, because the executive team believes—and is staked on the belief—that the cost-basis advantage will compound for thirty. A branded-goods acquisition that looks expensive on current EBITDA is closed, because the acquiring team knows, in a way that can only come from decades of operating experience, how the distribution synergies will actually flow through.

The flip side of this model is, of course, the succession question. KKH is not young. Martua Sitorus stepped back from day-to-day operations in 2017 and has since diversified his own holdings. Robert Kuok, still living at age 102 as of this writing, remains the spiritual anchor of the family but has not been operationally active in Wilmar for years. The next generation of Kuoks—KKH's sons and nephews, including the increasingly visible Kuok Khoon Ean and others—hold roles across the broader Kuok empire. Inside Wilmar specifically, the board has been gradually professionalizing, but the question of who will sit in KKH's chair in 2030 is not one the company has publicly resolved.

For investors, the "owner-operator premium"—the willingness of long-term shareholders to pay up for management whose personal wealth is tied directly to the stock—is one of Wilmar's most valuable and most fragile assets. The premium exists because KKH is KKH. The premium could erode the day he retires. Whether the culture he has built is institutional or personal is, perhaps, the single most important strategic question facing the company.

That question becomes all the more pointed when one considers how aggressive Wilmar has become under his watch—particularly in the markets most foreign to Asian commodity traders, namely Australia and Africa. It is to those expansions we now turn.

V. M&A and Capital Deployment: The Australian Gamble

For a company so culturally Asian, Wilmar's largest consumer-goods acquisitions outside of China have, strangely, happened in Australia. The story of why is a story about distribution arbitrage.

The first move was CSR Sugar. In July 2010, Wilmar completed the acquisition of the sugar division of CSR Limited—an Australian industrial conglomerate whose sugar business, Sucrogen, was one of the largest raw sugar producers in the Asia-Pacific region, with cane milling operations up and down the Queensland coast. The price was roughly 1.75 billion Australian dollars, or about 1.5 billion US dollars at then-prevailing exchange rates. Strategically, it accomplished two things at once: it gave Wilmar a genuine, scaled upstream position in sugar (to go with its existing refining and trading capabilities), and it planted a flag in the Australia-New Zealand region that would support further expansion.

The second, more interesting move came four years later. In March 2015, Wilmar, together with the Hong Kong–based private equity firm First Pacific, completed the acquisition of Goodman Fielder—an Australia-New Zealand branded-foods company whose portfolio included MeadowLea margarine, Praise mayonnaise, White Wings flour, Meadow Fresh dairy, and a thicket of heritage bread brands. Goodman Fielder was, at the time of the deal, widely considered a struggling company. It had cycled through CEOs. Its margins had collapsed. Analysts called it a "fixer-upper." The total deal value was approximately 1.3 billion US dollars, split fifty-fifty with First Pacific.

On its face, Goodman Fielder was a classic value trap. The Australian grocery market is one of the most concentrated duopolies in the developed world (Coles and Woolworths), which means private-label competition was eating brand-name margins alive. Goodman Fielder's own management had, over the preceding five years, failed to stabilize the business. The consensus view on the street was that Wilmar had bought a melting ice cube.

That consensus view missed the point.

Wilmar did not buy Goodman Fielder for the Australian grocery margins. Wilmar bought Goodman Fielder for the Chinese and Southeast Asian distribution arbitrage. The MeadowLea brand, properly positioned in a Hong Kong or Singapore supermarket, commands a premium unavailable to it in Sydney. The White Wings flour brand, reformulated for Chinese home baking—a category that exploded in the 2015-to-2020 period—has a runway in Shanghai that it never had in Perth. Wilmar has the refinery, the mill, the ship, and the ground-level distribution to push Goodman Fielder heritage brands into middle-class kitchens from Jakarta to Chongqing. No one else could do that deal. Only Wilmar.

This is what strategic M&A looks like when the acquirer is an integrated operator rather than a financial buyer. The headline multiple looked rich. The strategic multiple, measured against distribution synergies that a standard DCF model simply cannot capture, was a bargain. By 2024, Wilmar had bought out First Pacific's remaining stake, taking full ownership of Goodman Fielder, and was in the process of rolling the Australian heritage brands into its broader Asian consumer-packs business.

The same playbook—buy integrated assets, plug them into Asian distribution—was applied, with regional variation, to Africa. In Nigeria, Wilmar's joint venture with PZ Cussons, called PZ Wilmar, operates oil palm plantations, refineries, and consumer oil brands including Mamador and Devon Kings. In Côte d'Ivoire, Wilmar's subsidiary SANIA operates one of the largest edible oil refineries in West Africa. In Ghana and Uganda, further downstream refining and packing operations extend the footprint. The African business is, in absolute terms, small compared to China or India, but it is growing faster than either, and it follows the same recipe that worked in Indonesia in the 1990s: own the refinery, own the brand, own the distribution, be patient.

The India story is its own universe. Through the Adani Wilmar joint venture—formed in 1999, listed on the Bombay Stock Exchange in early 2022, and operating under the "Fortune" brand—Wilmar is the largest branded edible-oil player in India, a country whose per-capita oil consumption is rising in lockstep with its middle-class formation. The JV with Adani is, politically, a masterpiece of partnership: Adani provides the ports, the logistics, the government relationships, and the distribution muscle; Wilmar provides the refining technology, the commodity trading expertise, and the global sourcing reach. That partnership has survived multiple political cycles in India, has navigated the 2023 Hindenburg-related volatility in Adani-group equities, and as of the most recent disclosures, remains the backbone of Wilmar's Indian presence.

Taken together, the Australia–Africa–India expansions reveal something essential about Wilmar's capital allocation philosophy. The company does not buy brands. It buys distribution-accretive platforms. The distinction is subtle but decisive. A brand, bought in isolation, is a marketing asset. A platform, bought for its ability to ride Wilmar's integrated supply chain into fast-growing Asian and African markets, is a compounding machine. Most of Wilmar's acquisitions, when examined through this lens, reveal an internally consistent logic that is almost invisible to outsiders.

Nowhere is this more true than in China, where the company is doing something unprecedented—and where most of its future optionality now resides.

VI. The Hidden Engine: Yihai Kerry Arawana

There is a subsidiary inside Wilmar, listed separately on the Shenzhen Stock Exchange since October 2020, that deserves an entire episode to itself. Its full name is Yihai Kerry Arawana Holdings Company Limited. Most analysts shorten it to "YKA." Most consumers in China know it simply as "Arawana"—the dragon fish on the bottle. And most investors outside of Asia have never heard of it, despite the fact that it is one of the largest consumer-packaged-goods businesses in China.

The Arawana brand was launched in the early 1990s by Kerry Oils, the China joint venture that would later be consolidated into Wilmar. The insight was that China, as it urbanized, would move away from loose, bulk cooking oil sold out of drums in wet markets and toward pre-packaged, hygienically sealed, branded oil sold in supermarkets. The insight was correct, the timing was prescient, and the execution was ruthless. By the mid-2000s, Arawana was the single best-selling branded cooking oil in China. By the mid-2010s, it commanded roughly forty percent of the total branded cooking oil market, with its nearest competitor at perhaps half that share.

But Arawana is only the tip of the iceberg. YKA, the listed entity, consolidates Wilmar's entire China food business. That includes not just branded oils (Arawana, Orchid, Golden Dragon Fish) but also rice (branded and bulk), flour (home-use and food-service), sauces and condiments, and—the fastest-growing category—"central kitchen" pre-cooked meals and food-service ingredients for the institutional food market. YKA is, in effect, the Chinese Nestlé-plus-Sysco hybrid that most Western investors did not know existed.

The October 15, 2020 IPO on the Shenzhen ChiNext board was the moment this hidden empire became visible to the public market. The offering was oversubscribed several hundred times. On the opening day, YKA's stock more than doubled. At the post-IPO peak in early 2021, the market capitalization of YKA alone briefly exceeded the entire market capitalization of Wilmar International on the Singapore Exchange—a gap so absurd it became a case study in the "sum of the parts" mispricing that plagues conglomerate structures.

What the IPO actually did was unlock value that the Singapore market had been ignoring for a decade. Wilmar still owns approximately eighty-nine percent of YKA, which means the public float on the Shenzhen side is small. But the listing accomplishes two critical things. First, it gives YKA a China-listed currency that can be used, over time, for acquisitions, employee incentives, and strategic moves inside China without having to transit through the Singapore parent. Second, and more importantly, it forces the market to assign a consumer-goods multiple to the consumer-goods half of Wilmar. For years, Wilmar had been valued as a commodity trader; YKA's separate listing, even with the post-2021 correction, clarified that roughly half of Wilmar's earnings power came from a branded FMCG business that deserved a structurally higher multiple.

The YKA story does not end at cooking oil. The company is currently executing on what KKH has, in recent annual reports, called the most important strategic initiative of the next decade: central kitchens. A "central kitchen" in the Wilmar taxonomy is a massive, industrial-scale food preparation facility—think airline-catering meets food-factory meets cloud-kitchen—that produces pre-cooked, ready-to-eat and ready-to-cook meals, sauces, seasonings, and meal kits for restaurants, corporate canteens, schools, e-commerce meal delivery platforms, and eventually, retail consumers.

Why does this matter? Because the Chinese food market is undergoing a structural shift from "raw ingredients cooked at home" to "prepared meals consumed on the go or reheated at home." Food service as a share of total food spending in China has been climbing for fifteen years. Wilmar, which already sells the oil, rice, flour, and seasonings that go into every commercial kitchen, is moving one step further up the value chain: selling the actual finished dish—the braised pork, the kung pao chicken, the hotpot base—to those kitchens, and eventually, directly to consumers through Meituan, Alibaba's grocery arms, and retail supermarkets.

YKA has been building these central kitchens as massive "food parks"—integrated facilities that colocate oil refining, rice milling, flour production, packaging, and now pre-cooked meal production on a single industrial site. The first flagship food parks came online in Hangzhou, Xingping, Chongqing, and Tianjin, among others. Each park represents several hundred million US dollars of capex. The thesis is that by colocating every stage of food production, from commodity input to finished meal, Wilmar can achieve a cost structure that no pure-play food-service player (whose cost of goods is someone else's margin) can match.

This is the single most interesting thing happening inside Wilmar today, and it is almost entirely invisible to Western media. The company that started by refining palm oil in Medan is, thirty-five years later, building the largest pre-cooked meals platform in the world's largest food-consuming nation. If it works, it redefines what Wilmar is. If it stumbles, it becomes an expensive reminder that commodity processors are not, historically, great at marketing to consumers. The next five years of YKA's central-kitchen buildout are, in the author's view, the single most important variable in the long-term Wilmar story.

And with that, we step back and ask the structural question: what actually protects this empire from competition?

VII. The Playbook: Seven Powers and Porter's Five Forces

The framework that Hamilton Helmer developed in 7 Powers is, in the view of many serious long-term investors, the cleanest language available for describing why some businesses earn persistently above-cost-of-capital returns while others do not. Applied to Wilmar, three of Helmer's powers are unambiguously present, a fourth is partially present, and the remaining three are essentially absent. That combination—three strong powers, one partial, three absent—is, perhaps surprisingly, characteristic of most great compounding businesses. No business has all seven. What matters is whether the ones present are durable.

The first and most obvious power Wilmar possesses is scale economies. A palm oil refinery, once built, has a fixed cost base; every additional ton processed drops the per-unit cost. A shipping fleet, once owned, benefits from route density; every additional port call on a Wilmar-owned vessel lowers the cost of every other port call. A distribution network into Chinese wet markets, once built, adds marginal cost per additional SKU approaching zero. Across every major vertical—oilseeds crushing, sugar milling, flour production, rice processing, consumer-pack distribution—Wilmar operates at or near the largest scale of any player in Asia. The specific numbers vary by segment, but the intuition is consistent: a new entrant trying to replicate Wilmar's integrated Asian footprint would face negative unit economics for roughly a decade before achieving scale parity. That is not a moat you bridge with capital alone; it is a moat you bridge with capital plus time, and time is the one asset no incumbent can be out-competed on.

The second power is cornered resource, and here the story gets more interesting. Wilmar, through its plantation subsidiaries, controls a strategic land bank of oil palm estates in Indonesia, Malaysia, and Africa, much of which was acquired at favorable prices during the 1990s and 2000s, before the explosion of Asian and global palm oil demand drove land prices to multiples of historical levels. More importantly, Indonesian and Malaysian regulations have made new large-scale plantation development progressively more difficult—through moratoriums, sustainability certifications, and political scrutiny—which means that incumbents with existing, certified, productive plantation land enjoy a resource position that new entrants cannot replicate regardless of how much capital they have. The cornered resource is not just the land; it is the combination of the land, the certifications (RSPO, ISPO), and the decades-long community and governmental relationships that allow the land to be productive. This power is strongest upstream and fades as one moves downstream into refining and consumer products.

The third power, and the one most underappreciated by casual observers, is switching costs—not for the bulk palm oil buyer, whose switching costs are essentially zero, but for the specialty oleochemicals customer. Wilmar's oleochemicals business supplies fatty acids, fatty alcohols, glycerin, soap noodles, and specialty esters to customers that include Procter & Gamble, Unilever, L'Oréal, and nearly every major consumer goods multinational. These specialty products are formulated into shampoos, detergents, cosmetics, and personal-care products under supplier quality specifications that can take years to qualify. Once a consumer goods company has a Wilmar oleochemical in its approved supplier list for a specific product, the cost of switching—testing, recertifying, formulation adjustment, regulatory refiling—can easily run into the tens of millions of dollars per product line. That is a meaningful switching cost, and it applies to a surprisingly large slice of Wilmar's profit pool.

The remaining four Helmer powers—counter-positioning, network economies, branding, and process power—are largely absent, which is a feature of Wilmar's business model, not a bug. Agribusiness is, at its core, a physical-scale game; the firms that dominate are the firms that operate at lowest unit cost across the longest integrated supply chain. Arawana is a real brand, but branding alone is not Wilmar's core moat; the brand is a distribution amplifier on top of a cost-advantaged supply chain.

Now apply Michael Porter's Five Forces. Barriers to entry are massive, for the reasons already discussed—integrated CAPEX required to replicate Wilmar's footprint in China, India, or Southeast Asia is, at this point, economically prohibitive. Supplier power is moderate; palm planters are numerous and commoditized upstream, though downstream specialty inputs carry more supplier leverage. Buyer power is a mixed picture; bulk industrial buyers are price-sensitive, but consumer households are brand-loyal in categories like branded cooking oil. Substitution risk is real but gradual; soybean oil substitutes for palm oil at the margin, rapeseed oil substitutes for both, and regulatory shifts around saturated-fat content or deforestation can shift demand curves. Competitive rivalry is intense—COFCO in China, Adani in India (a frenemy rather than pure competitor), Cargill and ADM globally—but Wilmar's integrated cost structure means it typically wins on efficiency during downturns and holds its share during upturns.

The composite picture is a business with structural advantages that are difficult to erode, operating in an industry where discipline and patience consistently outperform flash. That is, fundamentally, why Wilmar trades the way it does—and why it remains a perennial subject of bull-and-bear debate.

VIII. Bear vs. Bull Case and Financial Philosophy

Every long-term shareholder of Wilmar has at some point stared at the stock chart and asked the same question: why is this stock so cheap? The bear and bull cases both begin with that question, and they diverge sharply in how they answer it.

The bear case, in its cleanest form, runs as follows. Wilmar is, despite management's protestations, a commodity company. Its results swing with palm oil prices, soybean crush margins, and sugar futures. It operates in jurisdictions—Indonesia, Malaysia, China, India, various African states—with real political, regulatory, and ESG risks. Its palm oil footprint is a lightning rod for deforestation-related NGO campaigns, and although the company has made significant sustainability commitments (NDPE policies, RSPO certifications), the reputational overhang is persistent. Its governance structure, with KKH holding concentrated influence and a family-linked strategic orientation, commands a justifiable minority discount in public markets. Its central kitchen bet in China is unproven, capital-intensive, and operating in a category (pre-cooked meals) where Chinese consumer acceptance is still being established. And crucially, its listed YKA subsidiary has, since the 2021 peak, underperformed as the Chinese consumer story has cooled. For a bear, Wilmar is a low-margin commodity processor dressed in consumer-brand clothing, deserving a high-single-digit P/E and nothing more.

The bull case, equally coherent, runs the other way. Roughly half of Wilmar's earnings come from branded, repeat-purchase consumer products—cooking oil, flour, rice, sugar—sold to hundreds of millions of Asian households under brands that have compounded shelf space for thirty years. Those earnings deserve a consumer-goods multiple, not a commodity multiple. The other half—the oilseeds crushing, the palm refining, the sugar milling—benefits from integration with the consumer business in ways that pure-play commodity firms cannot replicate. The central kitchen initiative is the most exciting growth vector in Asian food in 2026, with an addressable market measured in hundreds of billions of dollars, and Wilmar is the only player with the integrated upstream-to-plate supply chain to execute on it. The stock, at its prevailing multiple of operating cash flow, is priced as if the consumer business does not exist. And for the patient investor, the owner-operator alignment of KKH means capital allocation will continue to reflect twenty-year horizons, not quarterly earnings pressure.

Between these two framings, the single most important debate is segment-level: where does Wilmar's true economic engine sit? The company reports in three primary segments: Food Products (consumer packs, bulk, and food ingredients), Feed and Industrial Products (oilseeds and grains, sugar, oleochemicals, biodiesel), and Plantation and Sugar Milling (upstream). Food Products has structurally higher margins but lower volume. Feed and Industrial has structurally lower margins but much larger volume, and it generates the tonnage that the consumer business rides on top of. Plantation results swing wildly with CPO prices. The bull's strongest point is that Food Products, viewed in isolation, looks like a consumer-goods business; the bear's strongest point is that it cannot be cleanly separated from the commodity infrastructure beneath it.

A "secret" moat that deserves more attention than it typically gets is Wilmar Ship Holdings, the company's in-house shipping fleet. Wilmar operates one of the largest privately owned agribusiness shipping fleets in the world, with vessels ranging from handy-size bulk carriers to specialized palm-oil and chemical tankers. Owning the ships allows Wilmar to internalize freight margins, to guarantee capacity during shipping tightness (as occurred during the 2021-2022 container crisis), and to avoid spot-market volatility that damaged peers. This is the kind of asset that does not appear as a line item in a sum-of-the-parts analysis but contributes meaningful structural cost advantages to every downstream segment.

Three KPIs, in the view of serious long-term Wilmar watchers, matter more than anything else on the financial statements. The first is branded consumer-pack volume growth in China, reported through YKA. This is the clearest single indicator of whether the consumer thesis is alive. The second is the Food Products segment EBIT margin for the parent entity, which smooths through commodity volatility and shows whether downstream economics are expanding or contracting. The third is capex-to-sales ratio during the central kitchen buildout, which will determine whether the ambitious investment in pre-cooked meals is generating the returns that justify it. Readers should track these three metrics in the half-year and annual reports; they tell the Wilmar story more honestly than any single headline P/E ratio.

One final point on financial philosophy. KKH's stated approach to capital—confirmed across multiple investor days and annual reports—is that Wilmar maintains a conservative balance sheet, avoids speculative commodity positions, prioritizes reinvestment over dividends during high-growth phases, and returns capital primarily through steady, rising dividends during mature phases. The dividend policy has been remarkably consistent: a payout ratio generally around thirty to forty percent of earnings, with occasional special dividends tied to monetization events (like the YKA IPO). This is not a stock that will ever print a massive buyback announcement. It is a stock that compounds, quietly, in the way that KKH compounds—punctually, frugally, and over decades.

And that brings the story, at last, to the grading table.

IX. Conclusion and Final Reflections

Step back from the segment analyses and the Porter frameworks and the KPI discussions, and consider what, in fact, Wilmar is.

It is a company that, over thirty-five years, has executed one of the most patient and integrated pieces of corporate strategy in modern Asian business history. It began as a small palm oil trader. It became a refiner. It became a plantation owner through an elegantly engineered family consolidation. It became a Chinese consumer-goods giant. It became an Australian, African, and Indian heritage-brands consolidator. And it is now, quietly, attempting to become something without precedent: a vertically integrated, upstream-to-plate, finished-meals provider for the largest urban population on Earth. If even half of that ambition plays out, Wilmar in 2035 will look structurally different from Wilmar in 2026, in the way Wilmar in 2015 looked structurally different from Wilmar in 2005.

As an "acquisition machine"—the Acquired framing—Wilmar's record is distinctive. The company does not do flashy, premium-priced, brand-trophy deals. It does not engage in bidding wars. It does not pay twenty-times EBITDA for marketing-driven consumer companies. What it does, repeatedly and patiently, is identify integrated platforms that compound into its existing supply chain, buy them at prices that reflect current economics (not distribution-synergy economics), and then spend five to fifteen years extracting the full integration value. The 2007 recombination, the CSR Sugar deal, the Goodman Fielder acquisition, the Adani Wilmar joint venture, the steady African platform buildouts—these are not home runs in the ballpark sense; they are slow, high-conviction, singles-and-doubles with compounding over time. That pattern is the acquisition philosophy, and it has produced, measured over three decades, returns on invested capital that consistently exceed Wilmar's weighted average cost of capital.

The question for the next decade is whether Wilmar can transition from the "invisible ingredients" company to something more visible—something that might credibly be called the Nestlé of Asia. The transition is not purely a branding exercise. It requires the company to convince global investors that a meaningful share of its earnings deserves a consumer-goods multiple, to execute the central kitchen expansion without the capital intensity overwhelming the returns, to manage succession from KKH to the next generation of operators, and to do all of this while navigating a geopolitical environment in which Asian agribusiness is increasingly caught between US-China decoupling pressures, European sustainability regulation, and local food-security politics.

There is also a simpler, more investor-friendly frame. Wilmar is, at its foundation, a bet on Asian middle-class consumption. The company is structurally positioned such that, as hundreds of millions of households in China, India, Indonesia, Vietnam, Nigeria, and the Philippines move up the consumption curve—from loose oil to branded oil, from home cooking to food service, from basic nutrition to convenience meals—Wilmar will be the supplier of choice at nearly every step of that journey. The thesis does not require Wilmar to win in every category. It requires only that Asian middle-class formation continues at something approaching its historical trajectory, and that Wilmar's integrated supply chain continues to convert that consumption into earnings at something approaching its historical margins.

The myth versus reality tension that runs through Wilmar's story is worth restating one more time. The myth, held by many public market investors, is that Wilmar is a commodity trader—volatile, margin-thin, and deserving of a low single-digit multiple. The reality is that roughly half the business is a branded consumer goods company with some of the strongest distribution moats in Asia, and that the "commodity" half is itself an integrated cost leader whose volatility is smoothed by scale and internalized logistics. The gap between that myth and that reality is, in the view of many long-term shareholders, why the stock has, at various points, traded at a material discount to a cleanly decomposed sum-of-the-parts value. Whether that gap closes is a function partly of management action (further separation of YKA, investor communication, segment disclosure) and partly of the broader willingness of the Singapore Exchange to attach consumer-goods multiples to companies that, at first glance, look like commodity plays.

Stripped down, then, to its most basic form: Wilmar is a study in the quiet, compounding power of integration. It is a company built by a CEO who flies economy, a family philosophy that prioritizes longevity over flash, and an operating culture that has retained its senior team for decades. It is not a glamorous story. It is not a Silicon Valley growth narrative. It is something older, quieter, and arguably, more durable: the patient assembly of a global food-system platform, executed over thirty-five years, and still—if KKH's central-kitchen ambition plays out—only in the middle innings of its arc.

X. Epilogue and Further Reading

For listeners and readers interested in going deeper, several sources are essential.

The Robert Kuok Memoirs (2017, co-authored with Andrew Tanzer) remains the single best primary-source window into the Kuok family's operating philosophy, their approach to navigating political environments across Malaysia, Indonesia, Hong Kong, and China, and the cultural foundation upon which Wilmar was built. KKH is mentioned in the memoir, and the chapters on sugar, shipping, and the family's early China investments are indispensable for understanding the DNA of Wilmar.

The Adani Wilmar joint venture, which has been listed on the National Stock Exchange of India and the Bombay Stock Exchange since February 2022, deserves its own extended analysis. The JV operates under the Fortune brand, dominates branded edible oils and increasingly the branded wheat flour and rice categories in India, and represents Wilmar's single largest distribution platform outside of China. The Adani Group's own well-documented controversies—including the January 2023 Hindenburg Research short report and its aftermath—have occasionally spilled over into Adani Wilmar's trading dynamics, but the underlying food business has continued to expand.

For industry-structural analysis, the standard references on the "integrated agribusiness model" include academic and industry white papers on vertical integration in palm oil, the evolution of Chinese food-service supply chains, and comparative studies of Wilmar versus Cargill, Bunge, ADM (the "ABCD" traders), and Louis Dreyfus Company. Readers will find the Rabobank and Oil World research particularly useful for contextualizing palm oil market dynamics, and the USDA Foreign Agricultural Service reports on Chinese oilseed imports and crushing capacity provide invaluable quantitative backdrop on the soybean-complex economics that underpin Wilmar's Feed and Industrial segment.

Finally, for investors who want to track the company in real time, the most information-dense disclosures come from Wilmar's semiannual results briefings and the annual report, both available on the company's Singapore Exchange listing page. The segment-level disclosures have improved substantially over the past decade, and the company's ESG reporting—particularly around its No Deforestation, No Peat, No Exploitation (NDPE) commitments—has become increasingly comprehensive.

The invisible empire of the global kitchen continues to grow. Most consumers will never know the name. That, more than anything else, is the point.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube