Electro Optic Systems (EOS): The Laser-Guided Turnaround

I. Introduction: The "Near-Death" Hook

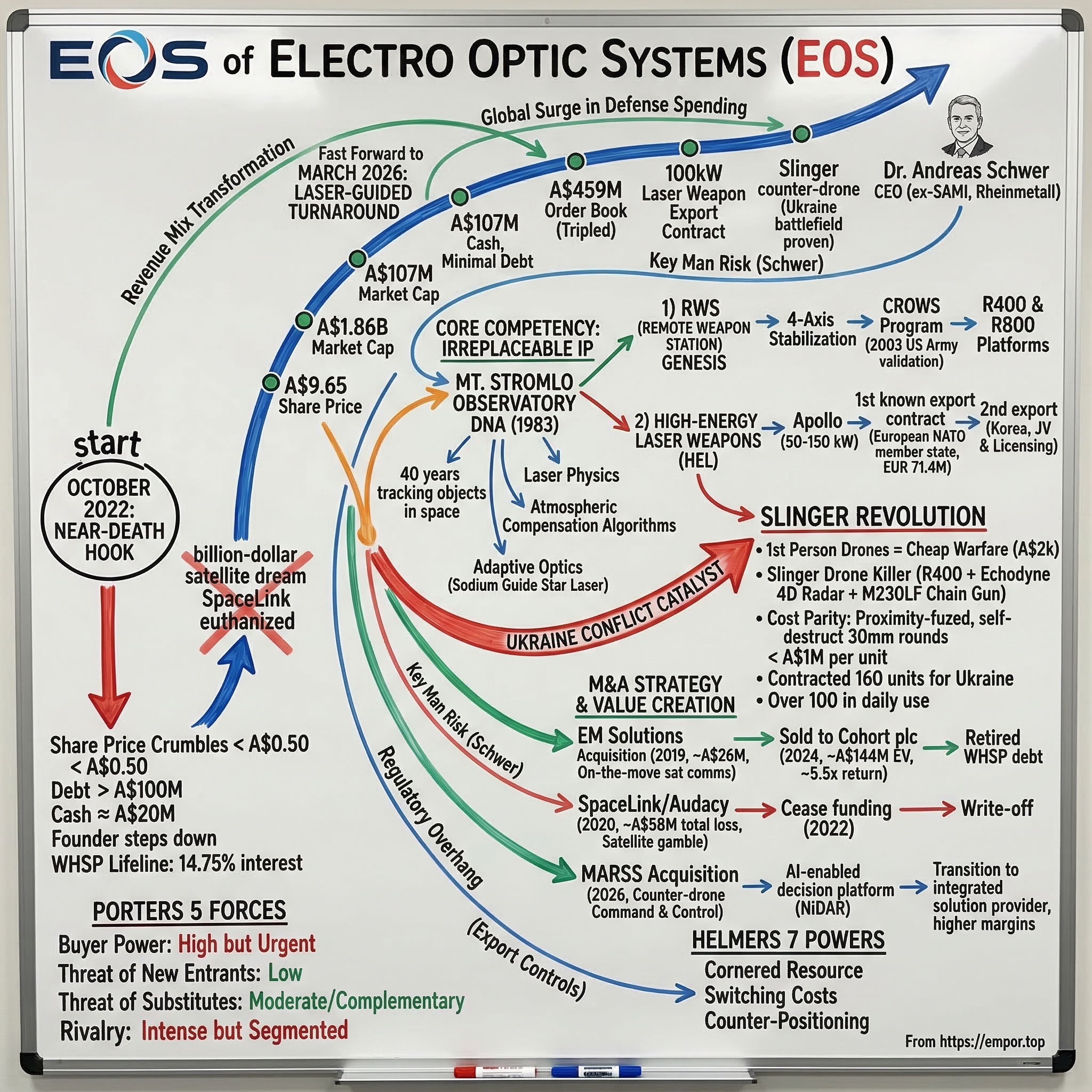

Picture a boardroom in Canberra, Australia, late 2022. The walls are lined with framed patents and photographs of laser telescopes pointed at the stars. Outside, the eucalyptus trees sway in the dry Canberra wind. Inside, the mood is funereal.

Electro Optic Systems Holdings, the company that once tracked satellites for NASA and built the world's first remote weapon station, is staring into the abyss. The share price has cratered from nearly ten dollars to under fifty cents — a decline of more than ninety percent. A billion-dollar satellite dream called SpaceLink has just been euthanized. The balance sheet carries almost a hundred million dollars in debt against barely twenty million in cash. The founder, a space physicist who has run the company for nearly four decades, is stepping aside. And Washington H. Soul Pattinson, one of Australia's oldest investment houses, has thrown a lifeline — but the interest rate on that lifeline is the kind you associate with payday lenders, not blue-chip financiers.

The analysts have written their obituaries. The short sellers are circling. The employees — many of them physicists with PhDs who joined because they believed in the science — are updating their resumes. In the corridors of the Australian defense establishment, the whisper is that EOS, once the country's most promising defense technology company, is finished.

Fast forward to March 2026. EOS trades at A$9.65, giving it a market capitalization of A$1.86 billion — a roughly twenty-six-fold increase from the December 2022 trough. The company sits on A$107 million in cash with minimal debt. Its order book has exploded to A$459 million, more than triple the level from just twelve months earlier. It has delivered the world's first 100-kilowatt laser weapon export contract. Its counter-drone system, Slinger, is battle-proven in Ukraine, with over one hundred units in active daily use against Russian drones. And the man running the show, Dr. Andreas Schwer, is a former CEO of Saudi Arabian Military Industries and a Rheinmetall board veteran who took options at fifty cents that are now worth nearly twenty times that.

What happened? How did a company go from the edge of bankruptcy to the center of the global defense industry's most important technology revolution in just three years?

This is a story about how a group of space physicists from an Australian observatory built what might become the "Intel Inside" of remote weapon stations and directed energy weapons — and survived a near-death experience to lead the next era of laser warfare.

It is a story about the tension between scientific ambition and commercial discipline, about the difference between a founder-led research lab and a globally-scaled defense prime, and about what happens when the geopolitical winds shift so dramatically that a niche Australian optics company suddenly finds itself at the center of the most important military technology revolution since precision-guided munitions.

The thesis is simple but powerful: EOS possesses four decades of irreplaceable intellectual property in laser physics, atmospheric compensation, and electro-optic fire control. This IP was developed not in a defense laboratory but in the pursuit of tracking objects in space — a pursuit that, as it turns out, produces precisely the capabilities needed to shoot down drones with bullets and lasers.

The company nearly destroyed itself chasing a satellite constellation that was always too capital-intensive for a mid-cap defense firm. But the new management, armed with ruthless cost discipline and deep defense industry relationships, has refocused the business on the sweet spot where EOS's technology meets the world's most urgent military need: cheap, effective ways to kill cheap, ubiquitous drones.

The question for investors is whether EOS can convert a record order book into sustained profitability, scale its laser weapon manufacturing from prototype to production, and navigate the treacherous waters of sovereign defense procurement — all while maintaining the scientific edge that makes its products unique. That is what makes this story worth telling.

But to understand why this company is different — why its technology cannot simply be replicated by a well-funded competitor — you have to go back to the beginning. You have to go to Mount Stromlo.

II. Origins: The Mount Stromlo DNA

In 1969, while most of the world watched Neil Armstrong set foot on the Moon, a young Australian physics student named Ben Greene was watching something else entirely. He was watching the ground stations — the network of satellite tracking facilities scattered across the Southern Hemisphere that made the entire Apollo program possible.

Australia, by virtue of its geography, hosted some of the most critical tracking infrastructure in NASA's global network. The huge radio dishes at Parkes and Honeysuckle Creek relayed Armstrong's famous words to a watching world. But it was the laser tracking stations — quieter, less photogenic, but arguably more consequential — that captivated Greene. These stations bounced laser pulses off tiny reflectors mounted on satellites and measured the return time to picosecond precision, determining the satellite's position to within centimeters from thousands of kilometers away.

The precision was staggering: imagine standing in Sydney and measuring the distance to a playing card in Perth, accounting for the curvature of the Earth, atmospheric distortion, and the fact that the card is moving at seven kilometers per second. Most people saw the Moon landing as the triumph of rocketry. Greene saw it as the triumph of measurement — and he wanted to spend his life making those measurements even more precise.

Greene earned his PhD in physics from the University of Hull in the UK in 1980, specializing in satellite geodesy — the science of measuring the Earth's shape and gravitational field using satellite data. He returned to Australia and joined the government's satellite tracking programs, where he rose to become Director of Australia's national space tracking programs, running bilateral US-Australia space sensing operations. His expertise spanned weapon system design, laser tracking, quantum physics, satellite design, and the metrology of time — the science of ultra-precise timekeeping that underpins all satellite navigation.

His team made a discovery that sounds almost mundane but was foundational: they figured out how to measure continental drift and gravitational fields using satellite laser ranging data. By bouncing lasers off reflectors on satellites and measuring the return time with extraordinary accuracy, they could detect that the Australian continent was moving northward at several centimeters per year. The precision required — accounting for atmospheric distortion, Earth's rotation, tidal forces, gravitational anomalies — is the kind of precision that, decades later, would prove invaluable for an entirely different application: pointing weapons.

In 1983, the Australian government decided to privatize its satellite tracking operations as part of a broader push toward smaller government. Greene and a group of fellow scientists took the opportunity to form Electro Optic Systems. The name itself reveals the DNA: "electro optic" is the intersection of electronics and optics, the discipline of using light — lasers, telescopes, sensors — as the primary medium for measurement and control.

The company set up shop near Canberra, eventually building and operating autonomous observatory facilities at Mount Stromlo in the Australian Capital Territory and Learmonth in Western Australia. It was a classic privatization story: a group of government scientists who knew more about their field than anyone on Earth decided that if the government no longer wanted to fund their work, they would fund it themselves — by finding customers who would pay for the precision they could deliver.

Mount Stromlo deserves a moment of description, because it is not just EOS's headquarters — it is the source code of the company's competitive advantage. Perched on a hilltop above Canberra, surrounded by eucalyptus forest, the observatory houses a 1.8-meter telescope — one of approximately forty-two satellite laser ranging stations worldwide. On a clear night, the telescope can track objects in orbit with millimeter-level accuracy, firing green laser pulses into the sky that look, to a passing observer, like something from a science fiction film.

The facility operates day and night, in all weather conditions, feeding data to space agencies and defense organizations around the world. It is here, over four decades of continuous operation, that EOS's scientists developed the atmospheric compensation algorithms that would become the company's most valuable intellectual property.

To understand why these algorithms matter, imagine trying to shine a flashlight at a specific point on the bottom of a swimming pool while someone is making waves. The water distorts the beam, bending and scattering it in unpredictable ways. Now imagine the pool is one hundred kilometers deep (the distance to the mesosphere), the waves are atmospheric turbulence cells that change a thousand times per second, and the target is a satellite reflector the size of a coin moving at orbital velocity.

That is the problem EOS's physicists solve every day. Their solution — adaptive optics using a sodium Guide Star Laser that creates an artificial reference point in the upper atmosphere, feeding real-time corrections to a flexible mirror — is the same technology that would later enable them to fire a high-energy laser weapon through the atmosphere with enough precision to burn a drone at three kilometers.

For the first decade, EOS was a pure space company. It built telescopes, dome enclosures, and laser tracking systems for government and academic clients. The business was small, specialized, and deeply technical. But Greene and his colleagues began to notice something that would change the company's trajectory forever.

The core problem they solved every day — pointing a laser or sensor at a moving object in space with sub-milliradian precision, while compensating for atmospheric turbulence, platform vibration, and target dynamics — was functionally identical to a problem the military desperately needed to solve: pointing a weapon at a target from a moving vehicle.

The insight that transformed EOS from a space instrumentation boutique into a defense company was elegant in its simplicity: if you can track a coin-sized satellite reflector a thousand kilometers away through a turbulent atmosphere, you can build the world's most accurate gun sight. The physics is the same. The algorithms are the same. The hardware — stabilized platforms, precision actuators, adaptive optics — is the same. What changes is the output: instead of a pulse of laser light measuring distance, you get a burst of cannon rounds hitting a target at two kilometers.

In the early 1990s, EOS began developing what it called a Remote Weapon Station, or RWS. For those unfamiliar with the concept, think of it as a robotic turret mounted on top of an armored vehicle. An RWS allows a soldier inside to aim and fire an externally-mounted weapon using cameras, thermal imagers, and a ballistic computer — all without ever exposing themselves to enemy fire. It is the difference between playing a video game and standing in front of the screen.

Before remote weapon stations, the gunner had to stand up through a hatch in the roof of the vehicle, physically gripping the weapon and sighting through their own eyes. In Iraq and Afghanistan, this made gunners the most vulnerable soldiers on the battlefield — exposed to sniper fire, improvised explosive devices, and rocket-propelled grenades. An RWS changes everything: the operator sits inside the hull behind armor, watches screens showing day and night imagery from the weapon's sensor package, designates a target with a joystick, and fires. The system handles stabilization, ballistic computation, and fire control automatically.

What made EOS's RWS fundamentally different from anything else on the market was its four-axis stabilization system. Most competing systems used two axes — think of it like a camera gimbal that can pan left-right and tilt up-down. EOS's system added two more degrees of freedom by decoupling the sensor unit from the weapon, so the operator's view remains locked on target even when the vehicle hits a pothole, takes a sharp turn, or the weapon recoils after firing.

The practical impact was roughly thirty percent better first-round hit probability at longer ranges than any competitor. For a soldier in combat, that is the difference between hitting the target on the first shot and giving the enemy time to shoot back.

The landmark validation came through the U.S. Army's Common Remotely Operated Weapon System program, known as CROWS. In 1993, EOS partnered with U.S. firm Recon Optical to develop the system. Trial units were delivered to the Army and deployed for testing in Iraq and Afghanistan beginning in 2003. In 2004, the CROWS I entered full production, with five hundred units delivered directly to U.S. Army combat units.

This was extraordinary. Consider the competitive dynamics for a moment. In 2003, the global defense industry was dominated by companies like General Dynamics, Raytheon, BAE Systems, and Thales — firms with tens of billions in revenue, armies of lobbyists in Washington, and decades of institutional relationships with the Pentagon. EOS had none of that. What it had was superior technology, born from the unlikely marriage of space physics and weapons engineering, and a willingness to deploy systems to a combat zone faster than the procurement bureaucracy thought possible.

The CROWS victory proved something important about EOS's DNA: the company could compete and win against the world's largest defense contractors when the evaluation criteria favored technology over relationships. It was a lesson that would be repeated, with variations, over the next two decades.

The victory was not permanent. In 2007, the U.S. Army was required to re-bid the CROWS contract under competitive procurement rules, and the award went to Norway's Kongsberg with its Protector system. Kongsberg went on to deliver over twenty-four thousand units to thirty-one nations over the next two decades, becoming the dominant player in the RWS market globally.

The loss stung — EOS had created the category, proven the concept in combat, and then watched a competitor capture the franchise. It is a pattern that repeats throughout the history of defense technology: the innovator creates the market, and the incumbent with deeper relationships and a larger sales force captures it.

But the CROWS experience gave EOS something no amount of money could buy: credibility with the world's most demanding military customer, a proven product architecture, and deep institutional knowledge of what it takes to manufacture and support a weapon system at scale. It also delivered a painful lesson in the realities of defense procurement — where the best technology does not always win, and incumbent relationships and procurement politics matter enormously.

EOS responded by refining its product line. Today, the company offers the R400 (under 400 kilograms, supporting 30mm cannon, machine guns, automatic grenade launchers, and anti-tank guided missiles) and the R800 (a heavier platform mounting the Bushmaster Mk44S 30x173mm cannon with STANAG Level 2-4 armor protection options). Both feature the signature four-axis stabilization, modular weapon swap capability in under one hour, and what EOS claims is the lightest weight in class — the R800 is described as "half the size and weight of a traditional turret." The Australian Army selected the R400 for its new Redback Infantry Fighting Vehicle in 2025, and 251 Bushmaster vehicles carry EOS weapon systems. The product line had found its market — even if the U.S. franchise had slipped away.

For investors, the origins section reveals the single most important fact about EOS: its technology did not emerge from a defense R&D program that can be replicated with enough funding. It emerged from forty years of fundamental science — tracking objects in space through a turbulent atmosphere — that happened to produce the exact capabilities needed for modern warfare. This accidental origin is the source of EOS's competitive moat, and it is what makes the company's story fundamentally different from that of a typical defense startup.

But having world-class technology and building a world-class business are two very different things. The next chapter of EOS's story would demonstrate, painfully, the gap between the two.

III. The Middle East Whale and The SpaceLink Gamble

Every defense company has a "whale" — a single contract so large that it funds the entire enterprise for years. For Boeing, it is the fighter jet programs. For Thales, it is the submarine contracts. For EOS, the whale was a massive export deal in the Middle East.

The specifics remain closely held — defense export agreements rarely invite publicity, and sovereign customers in the Gulf demand confidentiality as a condition of doing business. But the broad strokes are clear from EOS's financial filings: through the 2010s, a multi-year, multi-hundred-million-dollar agreement to supply remote weapon stations and related systems to a Middle Eastern sovereign customer became the financial backbone of the company.

This single customer relationship generated the revenue and cash flow that allowed EOS to hire additional physicists, invest in new products, expand its manufacturing footprint, and maintain its R&D edge against competitors with vastly larger budgets.

The problem with whale contracts, as every defense industry veteran knows, is concentration risk. When a single customer represents an outsized share of revenue, the company becomes hostage to that customer's budget cycles, political dynamics, and strategic priorities. Middle Eastern defense procurement is particularly unpredictable — contracts can be accelerated or frozen based on oil prices, regional conflicts, changes in leadership, or shifts in diplomatic relationships with supplier nations.

If the customer delays a payment, the cash flow impact for a company of EOS's size is not a headache — it is a crisis. If the customer cancels or restructures, the company faces an existential threat.

This dynamic — the tension between the transformative upside of a massive contract and the fragility it creates — was building quietly through the 2010s, even as EOS's revenue and share price climbed. The stock market, always forward-looking and often forgetful of risk, celebrated the top-line growth without fully pricing the concentration risk beneath it. EOS was a one-customer company wearing a multi-segment disguise.

Flush with whale-contract cash and emboldened by decades of laser physics expertise, EOS made a bet in 2020 that was either visionary or hubristic, depending on whom you ask. The company announced SpaceLink, a plan to build a Medium Earth Orbit satellite constellation for optical data relay.

To understand the ambition, consider what SpaceLink was supposed to do. The explosion of low-earth-orbit satellite constellations — Starlink, OneWeb, Planet Labs, and dozens of others — was creating a bottleneck: all of these satellites needed to get their data to the ground, but they could only communicate with a ground station when passing directly overhead.

SpaceLink would serve as a "switchboard in the sky" — a network of satellites parked in medium earth orbit, roughly ten thousand kilometers up, that would relay data between LEO satellites and ground stations using laser communications. Think of it as fiber-optic internet, but through space. The total investment required was estimated at approximately A$1.2 billion.

The foundation for SpaceLink was the May 2020 acquisition of Audacy Corporation, a U.S. space communications company, for US$10 million. Audacy's key asset was not its hardware or team — it was a Federal Communications Commission spectrum license authorizing the use of specific microwave frequencies for satellite-ground communication in MEO. In the telecommunications world, spectrum licenses are like waterfront real estate: scarce, government-regulated, and enormously valuable if you can build on them.

By September 2020, EOS had established SpaceLink as a subsidiary and was actively seeking external investors to fund the constellation build. The pitch was compelling on paper. EOS secured conditional financing of up to US$80 million from Export Finance Australia, the government's official export credit agency. German satellite manufacturer OHB Systems invested US$25 million. The constellation design leveraged EOS's core competency in laser communications.

If it worked, SpaceLink could become the backbone of the global space data economy, generating billions in recurring relay fees. If it did not work, a mid-cap defense company would have bet its balance sheet on a satellite venture requiring a thousand times its annual free cash flow. The risk-reward was asymmetric in both directions — enormous upside, but also the very real possibility of corporate death.

The timing was catastrophic. COVID-19 disrupted global supply chains, pushing satellite manufacturing timelines out by months and then years. The broader equity market correction of 2022, driven by rising interest rates, made growth-stage space companies toxic to investors. SpaceX's Starlink, with its own inter-satellite laser links, was rapidly building the very capability that SpaceLink proposed to sell as a service.

And the fundamental math was always challenging: A$1.2 billion is an enormous capital commitment for a company with a market capitalization already in freefall. EOS needed an equity partner — a sovereign wealth fund, a strategic investor, a private equity firm — to share the capital burden. In the risk-averse environment of 2022, with space SPACs collapsing across the board, no partner materialized.

The 2022 crash was a perfect storm of compounding failures. The Middle East whale contract hit payment delays, creating cash flow pressure at precisely the wrong moment. SpaceLink was consuming approximately A$25 million per year in operating costs with no revenue in sight and no funding partner on the horizon.

The share price, which had peaked near A$10 in early 2020 on the wave of space industry enthusiasm, collapsed to A$1.14 in June 2022 — a single-day drop of twenty-six percent. By December 2022, shares were trading at forty-eight cents, valuing the entire company at less than the cost of a single satellite.

The financial picture was dire. EOS reported a net loss of A$114.5 million for the fiscal year, including A$62 million in discontinued operations losses related to SpaceLink. Operating cash outflow was negative A$55.7 million. Total debt stood at A$97 million against just A$21.7 million in cash. The company was, by any conventional measure, approaching insolvency.

Enter Washington H. Soul Pattinson — WHSP for short — one of Australia's oldest and most storied investment houses, with roots stretching back to a Sydney pharmacy in 1903. WHSP provided a three-year A$35 million term loan and an eighteen-month A$15 million working capital facility.

The terms were punishing by any measure: secured against the group's entire asset base, laden with financial covenants and minimum earn-out requirements, and carrying an interest rate that reflected the desperation of the borrower rather than any reasonable assessment of fair value.

In the defense industry, where companies regularly access government-backed credit facilities at near-sovereign rates, the WHSP terms were a stark reminder of how far EOS had fallen. The company that once supplied weapon systems to the U.S. Army was now borrowing money on terms that a distressed retailer might find onerous. A subsequent dispute over a A$4.5 million fee claim — resolved in December 2023 with full payment — underscored the adversarial nature of this rescue financing.

The WHSP financing bought EOS time, but it also forced a reckoning. In November 2022, the company announced it would cease funding SpaceLink entirely. The total write-off: approximately A$58 million, representing the cumulative investment in Audacy and SpaceLink combined. The FCC spectrum license, which required satellite launches by June 2024 to remain valid, became worthless. SpaceLink entered an Assignment for the Benefit of Creditors — the corporate equivalent of a funeral.

What remained was a defense business with world-class technology, a depleted balance sheet, and a founder who had finally, reluctantly, acknowledged that the company needed a different kind of leader. The era of the scientist-CEO was over. The question was whether what came next would be a turnaround or a liquidation.

For investors who study corporate near-death experiences, EOS in late 2022 presented the classic pattern: a technology company with genuine, differentiated IP that had been mismanaged into a liquidity crisis by overreach. The technology was never the problem — the space physics, the adaptive optics, the fire control algorithms were all real and all valuable. The problem was capital allocation: a founder who believed so deeply in the potential of his technology that he bet the company's survival on a venture that required resources far beyond its means. It is the same pattern that has destroyed hundreds of promising technology companies throughout history. What makes EOS's story different is what happened next.

IV. The "Adult in the Room": The Andreas Schwer Era

When the EOS board began searching for a new CEO in mid-2022, they were not looking for another physicist. They needed someone who had built defense businesses at a global scale, who understood the baroque procurement processes of sovereign militaries around the world, who could walk into a meeting with a Middle Eastern defense minister or a NATO four-star general and command instant credibility.

The candidate needed to speak the language of defense procurement — offsets, countertrade, technology transfer, ITAR compliance, export licenses — as fluently as EOS's engineers spoke the language of photons and adaptive optics. They found Andreas Schwer.

Schwer's biography reads like a curriculum vitae designed to produce the ideal defense CEO. Born in Germany, he studied aerospace engineering at the University of Stuttgart from 1987 to 1992 — the era when European aerospace was consolidating from national champions into what would become Airbus and EADS. He then earned a PhD in system modeling and numerical optimization, giving him the rare combination of technical fluency and mathematical rigor that allows a CEO to challenge engineers on their own terms without pretending to be one of them.

He spent fourteen years at Airbus Group in increasingly senior positions, learning the European aerospace ecosystem from the inside — the complex web of government relationships, multinational joint ventures, and technology-sharing agreements that define the European defense industry.

He then moved to Rheinmetall, the German defense giant famous for its armored vehicles and ammunition, where he spent five years gaining deep expertise in land systems, weapon systems, and the operational realities of defense manufacturing at scale.

But the defining chapter of Schwer's career came in 2018, when he was appointed the inaugural CEO of Saudi Arabian Military Industries, or SAMI. This was not a normal CEO job. SAMI was a cornerstone of Saudi Arabia's Vision 2030 economic diversification program — an attempt to build a domestic defense industry in a country that had historically imported essentially all of its military equipment.

Starting from a greenfield, Schwer's mandate was to create a functioning defense industrial enterprise in one of the most complex geopolitical environments on earth. The role required navigating Saudi politics (which is to say, royal family dynamics and competing power centers within the kingdom), managing expectations from a customer base that was also his shareholder (the Saudi government), recruiting talent from global defense companies to relocate to Riyadh (not an easy sell for engineers accustomed to Munich or Washington), and building manufacturing capabilities, supply chains, and quality management systems from scratch.

The SAMI experience gave Schwer something that very few defense executives possess: a deep, intuitive understanding of what non-Western sovereign customers actually want. Most Western defense executives think in terms of technical specifications and contract terms. Schwer learned to think in terms of national pride, technology transfer, industrial participation, and the political capital that a defense minister earns by building domestic manufacturing capability. This understanding would prove invaluable at EOS, where the customer base spans the Middle East, Europe, Asia-Pacific, and the United States — each with fundamentally different procurement cultures and strategic priorities.

Schwer was appointed EOS CEO in August 2022 and elevated to Managing Director in December 2023. His mandate was blunt: stop the bleeding, focus the business, and turn EOS from a research lab that occasionally sold products into a defense company that occasionally did research.

The distinction matters enormously. In a research lab, the scientists decide what to build and the salespeople figure out how to sell it. In a defense company, the customer decides what they need and the engineers figure out how to build it. The product roadmap is driven by procurement requirements and threat assessments, not by scientific curiosity. Schwer's job was to invert the culture without destroying the technical magic that made EOS unique.

His first moves were surgical and sent an unmistakable signal about the new regime's priorities. He cut headcount by over one hundred employees — roughly a fifth of the workforce — delayered management, and closed two facilities. The restructuring generated approximately A$25 million in annual cost savings, which for a company bleeding cash at the rate EOS was, represented the difference between survival and insolvency.

He ensured the SpaceLink shutdown was swift, clean, and final — no "strategic review," no "exploring options," no corporate euphemisms designed to preserve optionality and management ego. SpaceLink was dead and everyone knew it.

He narrowed the strategic focus to three areas where EOS had genuine competitive advantage: counter-drone systems, high-energy lasers, and space domain awareness. Everything else was either divested or deprioritized. The message to the organization was simple: EOS would no longer try to be all things. It would be the best in the world at a narrow set of capabilities where its Mount Stromlo heritage gave it an unfair advantage, and it would say no to everything else.

The incentive structure Schwer negotiated reveals a great deal about both his confidence and the board's alignment. His base salary was set at approximately A$1.08 million — modest by global defense CEO standards, reflecting the company's distress at the time of hiring. But his total compensation was heavily weighted toward equity: seventy-two percent of his roughly A$2.72 million total package came from bonuses and stock options.

The critical detail is the strike price — A$0.50 per share, granted when the stock was trading near its all-time lows. At the current share price of A$9.65, those options represent a nearly twenty-fold return. When a CEO negotiates options at the bottom, it tells you either that he is confident or that he is foolish. The subsequent twenty-six-fold increase in market capitalization suggests the former.

Schwer and other executives exercised a combined 3.4 million options under the long-term incentive plan after meeting performance and service hurdles for fiscal years 2024 and 2025. But the incentive story has a revealing twist. When Schwer announced plans to sell up to 2.5 million shares to fund personal tax obligations related to the option exercises — a routine and entirely reasonable action — the stock dropped approximately fifteen percent in a single session.

The market, it seems, is hyper-sensitive to any signal that insiders might be heading for the exits. When a single individual's share sale moves the stock by fifteen percent, the investment case is tied to that individual to a degree that should give long-term investors pause.

To address this concern, EOS implemented a mandatory shareholding policy effective January 2026: the CEO must hold shares valued at four times their fixed annual remuneration within three years, and the CFO and COO must hold three times. This forces management to maintain significant personal wealth tied to the company's share price over the long term, not just enjoy a windfall from option exercises and walk away.

The transition from Ben Greene to Andreas Schwer represents something deeper than a change in leadership. It represents a change in organizational identity. Greene, the space physicist, saw EOS as a platform for world-changing scientific innovation. Schwer, the defense executive, sees EOS as a platform for delivering mission-critical weapon systems to sovereign customers at scale and on time.

Greene remains at EOS as Founder and Head of Innovation, drawing a salary of approximately A$870,000, with a charter to pursue the kind of long-horizon research — space debris clearing, next-generation laser architectures — that does not fit neatly into a quarterly earnings cadence. His continued presence is both a bridge to the company's intellectual heritage and a reminder that EOS's competitive advantage was built in an observatory, not a boardroom.

The dual leadership structure — Schwer for execution, Greene for innovation — is itself a bet on whether a company can serve two masters. History suggests it is difficult. Lockheed's Skunk Works operated with similar semi-independence from the parent company, but Kelly Johnson had the advantage of operating within a firm with virtually unlimited resources. Greene operates within a firm with 496 employees and a market capitalization smaller than some defense primes' quarterly marketing budgets. Whether the structure produces the best of both worlds or the worst depends entirely on whether Schwer and Greene can maintain mutual respect across fundamentally different worldviews. So far, the evidence suggests they can — but the real test will come when resources are constrained and priorities conflict.

V. M&A Strategy: The "Golden" vs. "Gamble"

If you want to understand how a management team thinks about capital allocation — the single most important determinant of long-term shareholder value — do not read their investor presentations. Study their acquisitions. EOS's M&A history contains one masterclass, one write-off, and one ambitious bet — and together, they tell the complete story of the company's strategic evolution.

The masterclass is EM Solutions. In October 2019, EOS acquired one hundred percent of EM Solutions Pty Limited, a Brisbane-based company that was a world leader in on-the-move satellite communications.

To understand what EM Solutions did, picture a naval destroyer cutting through heavy seas at thirty knots. The ship needs a continuous, high-bandwidth satellite communication link for everything from navigation to weapons targeting to secure voice calls with the fleet commander. But the ship is pitching, rolling, and yawing in three dimensions simultaneously, while the satellite it needs to talk to is a tiny point in the sky thirty-six thousand kilometers away.

EM Solutions built the hardware that solved this problem — microwave satellite antennas and receivers mounted on stabilized platforms that could maintain a rock-solid lock on a satellite regardless of the ship's movement. The technology was specialized, the market was niche, and the company was too small to attract attention from the global defense primes — which made it exactly the kind of acquisition that creates extraordinary returns.

The price was modest: 4.27 million EOS shares plus A$1.485 million in cash, valuing the deal at approximately A$26 million. It was structured primarily as a scrip deal, preserving the balance sheet while giving EM Solutions' founders meaningful upside. Under EOS's ownership, the business scaled steadily, winning contracts with NATO navies and expanding into land-based military satellite communications. By fiscal year 2023, EM Solutions was generating revenue of A$43.1 million with EBIT of A$11.5 million — a healthy twenty-seven percent margin.

In November 2024, EOS entered a binding agreement to sell EM Solutions to Cohort plc, a UK-listed defense technology group, for an implied enterprise value of A$144 million. At the time of sale, EM Solutions carried an order book of A$175 million — a pipeline that would continue generating revenue for Cohort for years to come. The transaction generated a gain of approximately A$90.5 million for EOS. On the original A$26 million investment, that is a 5.5-times return in five years — a result that would make any private equity firm proud, and one achieved by a management team that was simultaneously fighting for the company's survival.

The timing of the sale was as important as the price. Schwer's team recognized that EM Solutions, while profitable and growing, was not core to the refocused strategy of counter-drone systems, high-energy lasers, and space domain awareness. It was a satellite communications business, valuable but peripheral. And EOS needed cash — desperately — to retire the WHSP rescue debt and fund the scaling of Slinger and Apollo.

The return on investment, impressive as it is, understates the strategic significance. The proceeds were what allowed EOS to repay all of its WHSP debt, eliminate the punishing interest expense, and enter 2025 with a clean balance sheet and over A$100 million in cash. Without this divestiture, the turnaround would have remained a financial fiction — a company with impressive technology still shackled to rescue debt.

The write-off is Audacy — the US$10 million acquisition that served as the on-ramp to SpaceLink. When the satellite constellation was killed, Audacy's FCC spectrum license lost its value. The total loss on SpaceLink and Audacy combined was approximately A$58 million.

In hindsight, was the Audacy bet wrong? The answer is nuanced. Spectrum-based options bets are standard practice in telecommunications and space — companies routinely acquire licenses speculatively, hoping to build on them or sell them at a premium. The Audacy license could have been worth multiples of the purchase price had SpaceLink attracted funding. The bet was not wrong in principle; it was wrong in context. A billion-dollar constellation requires a billion-dollar balance sheet, or at minimum, a billion-dollar partner willing to share the risk. EOS had neither. The lesson for investors is to watch carefully when a management team's ambitions outpace its financial capacity — and to give credit when the new management has the discipline to recognize and correct the overreach.

The ambitious new bet is MARSS. In January 2026, EOS announced the acquisition of MARSS Group, a Europe-based provider of command-and-control systems for counter-drone applications. Founded in 2006 in Monaco, MARSS developed a proprietary technology called NiDAR — an AI-enabled decision-making platform that orchestrates sensors and effectors in a counter-drone engagement.

To understand why NiDAR matters, think about how a counter-drone engagement actually works. First, a radar detects an incoming object. Then, software must classify it — is it a bird, a commercial airliner, a friendly drone, or an enemy attack drone? Then, a decision must be made — engage or hold fire? Then, the appropriate weapon must be selected and aimed.

All of this happens in seconds, under extreme stress, with catastrophic consequences for getting it wrong. Shoot down a friendly aircraft and you have an international incident; fail to shoot down an enemy drone and your troops die. NiDAR is the "brain" that automates and accelerates this entire decision cycle, fusing data from multiple sensors, applying AI-based classification algorithms, and directing weapons onto targets.

The deal structure is US$36 million upfront in cash, plus an earnout linked to new MARSS sales that is capped at EUR 100 million. The upfront payment alone represents roughly a third of EOS's cash balance — a meaningful commitment that signals management's conviction. The earnout structure, capped but potentially substantial, aligns the MARSS founding team's interests with EOS's growth objectives: they make more money if the combined platform wins more contracts.

The strategic logic is compelling and worth dwelling on, because it reveals how Schwer thinks about value creation. Without MARSS, EOS is a component supplier — it makes the weapon (Slinger) or the laser (Apollo), but the customer needs a separate command-and-control system from a different vendor to tie everything together. The customer evaluates each component independently, compares prices, and can substitute one vendor's weapon for another at the next procurement cycle. Margins are under constant pressure.

With MARSS, EOS becomes an end-to-end counter-drone solution provider. The customer buys an integrated system: detection, classification, decision-making, and engagement in a single package, from a single vendor, with a single support contract. Integrated solutions command significantly higher margins because the customer is not buying parts — they are buying capability. And the lock-in is profound: once a military builds its counter-drone doctrine around a specific integrated platform, switching to a different vendor means retraining every operator, rewriting every procedure, and retesting every interface.

The MARSS acquisition also signals where Schwer believes value will migrate. Hardware faces margin pressure as competitors invest and catch up. Software and AI — the algorithms that fuse data, classify threats, and optimize engagements — are where the durable margin resides. If EOS can become the "platform" on which counter-drone operations run globally, the business model transforms from project-based defense contracting into something closer to a software-enabled platform. That is the difference between being valued like a defense contractor and being valued like a defense technology company.

VI. "Hidden" Businesses and The Slinger Revolution

The Ukraine conflict, which began with Russia's full-scale invasion in February 2022, has rewritten the textbook on modern warfare. The lessons are many, but none is more consequential for the defense industry than this: drones have fundamentally changed the economics of warfare.

A first-person-view attack drone — essentially a racing quadcopter strapped to a mortar round — costs roughly two thousand dollars to build. A surface-to-air missile costs between five hundred thousand and three million dollars. If you use missiles to kill drones, you lose the economic war even when you win every engagement. It is like paying a hundred dollars to swat a fly.

By late 2025, Russian drone and missile strikes on Ukraine had reached approximately six thousand per month, with drones accounting for roughly seventy-five percent of all strikes. The Ukrainian Ambassador to Australia, Vasyl Myroshnychenko, put it starkly: "Missiles cost millions. Drones cost two thousand dollars. It is about the cost."

The world's militaries — from NATO members to Middle Eastern kingdoms to Pacific nations watching China's drone capabilities grow — were suddenly desperate for a cheap, effective counter-drone solution. Traditional air defense systems, designed to shoot down manned aircraft and cruise missiles, were spectacularly ill-suited to the task. The US Army's Stinger missile, for example, costs approximately four hundred thousand dollars per round — two hundred times the cost of the drone it is trying to destroy. Israel's Iron Dome, the gold standard of missile defense, costs roughly fifty thousand dollars per interceptor. Even at that price, the economics do not work against a swarm of fifty-dollar hobby drones carrying hand grenades.

This was the demand signal that transformed EOS.

EOS answered with Slinger, unveiled in May 2023 and designed from the ground up as a "drone killer" that restores cost parity. The system is built on the R400 remote weapon station platform and combines three elements into a package weighing just 376 kilograms — light enough to mount on a pickup truck.

The first element is an Echodyne 4D targeting radar — an ultra-compact, solid-state active electronically scanned array that detects and tracks incoming drones at ranges measured in kilometers. Unlike a traditional rotating radar dish, the Echodyne unit has no moving parts: it steers its beam electronically, scanning the entire sky hundreds of times per second.

The second element is the M230LF 30-millimeter chain gun — a lightweight, link-fed cannon originally designed for the Apache helicopter. The third is EOS's proprietary four-axis stabilization, which keeps the weapon pointed at the target with the same sub-milliradian precision originally developed to track satellites.

But the real innovation — the part that makes Slinger fundamentally different from a soldier with a machine gun shooting at the sky — is in the ammunition.

Slinger fires radio-frequency proximity-fused, high-explosive fragmentation rounds. That is a mouthful of military jargon, so here is what it means in plain English. Each round carries a tiny radio transmitter embedded in its nose. As it flies toward the target, it continuously emits radio waves. When those waves bounce back from a nearby object — the drone — the return signal triggers the fuze, detonating the round. The explosion sends a cloud of high-velocity metal fragments into the drone's path, shredding its rotors, electronics, and airframe.

The critical advantage is that the round does not need to score a direct hit. Hitting a small, fast-moving drone with a bullet is extraordinarily difficult — like hitting a clay pigeon with a single rifle shot while driving over rough terrain. But a proximity-fused round only needs to pass within a few meters. The fragment cloud does the rest.

The rounds also incorporate a self-destruct mechanism: after traveling a set distance without encountering a target, they detonate harmlessly. This is essential for operations near populated areas, where rounds that miss and continue traveling could cause civilian casualties. The combination of proximity fuzing and self-destruct makes Slinger suitable for urban environments — a major advantage over traditional anti-aircraft guns that scatter high-velocity rounds across the landscape.

Cost per engagement: one hundred to one thousand dollars, depending on ammunition type and rounds expended. You do not need a million-dollar solution to a two-thousand-dollar problem.

The entire system costs less than A$1 million per unit — roughly one-fiftieth the cost of a typical short-range air defense missile system — and can be delivered from factory to battlefield in months rather than the years typical of major defense programs. Speed of deployment matters in a conflict: Ukraine does not have the luxury of waiting five years for a development program. It needs solutions that work now, at scale, at a price that a wartime economy can sustain.

In September 2023, EOS contracted to supply 160 Slingers to Ukraine: 110 mounted on M113 armored personnel carriers and 50 on Practika light mine-resistant vehicles. The systems were supplied through U.S. security assistance programs, giving EOS a direct pipeline to the world's largest defense budget.

By early 2026, over one hundred EOS products were in active daily use in the conflict zone. Ukraine became the proving ground that no marketing budget could replicate. When a NATO general watches video of a Slinger destroying Russian Shahed drones on the front lines, the sales conversation is already over.

The order book tells the story. In fiscal year 2025, EOS booked eighteen new contracts totaling A$420 million in order intake — a 238 percent increase year-over-year. New customers included Middle Eastern, American, and European militaries. The total order book reached A$459 million. EOS is establishing a US production facility in Huntsville, Alabama, to meet rising American demand. European naval orders for maritime-configured Slinger systems are delivering through 2025 and 2026.

While the defense segment is the engine, the space segment remains a hidden gem. EOS's Space Systems division operates in Space Domain Awareness — essentially air traffic control for everything in orbit. As object counts have exploded past tens of thousands (with hundreds of thousands too small to track), precise monitoring has become critical.

A single collision between two satellites creates thousands of new debris fragments, each capable of destroying another satellite in a cascading failure called the Kessler Syndrome. EOS, operating from Mount Stromlo and Learmonth with forty-plus years of laser ranging heritage, holds contracts with NOAA and participates in the UK's Spaceflux-led consortium covering all three major UK government space surveillance contracts.

The more speculative but potentially transformative capability is laser debris clearing. The concept is deceptively simple: using a ground-based high-power infrared laser, EOS can nudge a piece of orbital debris just enough to avoid a predicted collision. The laser does not destroy the debris — it imparts a tiny momentum change through photon pressure, like blowing on a feather to change its path. The debris continues orbiting, but on a slightly different trajectory that misses the predicted collision point.

What makes EOS's approach unique is the efficiency. Thanks to the adaptive optics developed at Mount Stromlo, the company achieves the required orbital modification with only five percent of the laser power previously thought necessary. This is the payoff from four decades of atmospheric compensation research: by correcting for atmospheric turbulence in real time, EOS can deliver a tightly focused laser beam to an object hundreds of kilometers up with far less energy waste than any competitor.

The commercial implications are significant. Every satellite operator — from SpaceX to OneWeb to national space agencies — faces collision risk that grows with each new launch. Space insurance premiums are rising. A reliable, commercially available debris mitigation service could become a multi-billion-dollar market. And EOS, with its unique combination of laser technology, adaptive optics, and space tracking infrastructure, has no real competitor in this domain.

The third business unit generating enormous excitement is High Energy Lasers. On August 5, 2025, EOS announced the world's first known export contract for a 100-kilowatt-class high-energy laser weapon system. The customer was an undisclosed European NATO member state. The contract was valued at EUR 71.4 million (approximately A$125 million), covering manufacturing, integration, testing, training, and spare parts.

The weapon, unveiled under the name Apollo at the DSEI UK defense exhibition in September 2025, represents decades of laser research crystallized into a deployable product. Apollo is scalable from 50 to 150 kilowatts, provides full 360-degree coverage including vertical engagements directly overhead, can engage over twenty Group 1 drones (the small, commercially-available type that dominates the Ukraine battlespace) per minute at typical swarm-attack distances, and stores over two hundred engagements when operating independently on internal power.

With an external power supply — a generator, a vehicle's electrical system, or a fixed installation's grid connection — Apollo fires indefinitely. Every shot costs essentially nothing beyond the electricity to power the laser. For a military planner staring at a budget line for surface-to-air missiles that costs millions per engagement, the economics of a laser weapon are transformative. The ammunition is literally light.

In December 2025, EOS secured a second export contract with the Republic of Korea, valued at US$80 million. This deal went further than a simple equipment sale. It included the formation of a joint venture with the Korean customer to develop and supply lasers for the Korean defense market, plus licensing of EOS's laser patents and proprietary know-how.

The joint venture structure is strategically significant: it gives EOS a permanent foothold in the Korean defense market, generates recurring licensing revenue (the highest-margin revenue stream in the defense industry), and creates a local advocate for EOS technology within the Korean military establishment. Korea, facing a North Korean threat that includes mass drone capabilities, is a natural market for counter-drone lasers.

Manufacturing for both contracts takes place at EOS's new Laser Weapon Manufacturing Facility in Singapore — deliberately positioned outside both Australian and US export control jurisdictions for non-AUKUS customers.

The combined HEL order value — roughly A$245 million — represents a business line that did not exist eighteen months earlier. For context, that is nearly double EOS's entire fiscal 2025 revenue of A$128.5 million. The laser weapon has gone from science project to the company's largest single revenue opportunity in the space of a year. The phrase "directed energy weapons" has appeared in defense budgets for decades, always seeming to be five years away from deployment. For EOS, that future has arrived — and it is a line item on a purchase order, not a slide in a research presentation.

For investors, the significance is this: the Slinger, Apollo, and space businesses represent three distinct growth vectors, each driven by different customers, different geographies, and different budget lines. The Slinger is a near-term cash generator driven by urgent operational demand. Apollo is a medium-term margin enhancer driven by strategic defense modernization budgets. And space domain awareness is a long-term option on the commercialization of space safety. This diversification — all built on the same core electro-optic IP — is precisely what makes EOS's technology platform so valuable.

VII. The Playbook: 7 Powers and 5 Forces Analysis

To understand whether EOS's competitive position is durable, it helps to apply two rigorous strategic frameworks: Hamilton Helmer's Seven Powers and Michael Porter's Five Forces.

Start with Helmer. The most powerful advantage EOS possesses is what Helmer calls a Cornered Resource — an asset competitors cannot replicate through spending. EOS's cornered resource is forty years of accumulated intellectual property in atmospheric compensation, adaptive optics, and electro-optic fire control.

Why is this "cornered" rather than merely "difficult"? Because the knowledge is tacit rather than codifiable. It lives in the heads of physicists who have spent careers watching lasers interact with Earth's atmosphere — who understand intuitively how turbulence patterns shift with altitude, humidity, and temperature. A well-funded competitor could hire laser physicists and spend a billion dollars. But they cannot hire forty years of continuous observation data from Mount Stromlo. They cannot replicate the institutional memory of thousands of failed experiments. The path through the observatory is the only path to the capability.

The second power is Switching Costs. Once an EOS remote weapon station is integrated into a military platform — Bushmaster, Boxer, Hawkei, Redback — the cost of switching is enormous. Not just the hardware swap, but the software integration, sensor recalibration, crew retraining, recertification testing, and logistical infrastructure for spare parts and maintenance. Military platforms have lifecycles measured in decades. An RWS integration decision made today generates revenue for twenty to thirty years.

The third power is Counter-Positioning. This is perhaps the most underappreciated advantage. EOS's nimbleness is a structural advantage against the defense primes — not because EOS is faster in some vague sense, but because the primes' organizational structures actively prevent them from competing in the same way.

Lockheed Martin, Raytheon, and Rheinmetall are optimized for programs of record — multi-billion-dollar, multi-decade contracts with extensive requirements documentation, formal milestone reviews, and layers of quality assurance. These structures exist for good reason: when you are building a nuclear submarine or a fighter jet, you cannot afford shortcuts. But those same structures make it nearly impossible to rapidly develop and deploy a sub-million-dollar counter-drone system in response to an active conflict.

EOS developed Slinger, deployed it to a war zone, and iterated on battlefield feedback in a timeline that a prime contractor's internal review board would still be debating scope definitions. This is not a cultural difference that a prime can fix with a memo or a reorganization — it is structural, embedded in procurement processes, compliance frameworks, and organizational incentive systems that would need to be fundamentally redesigned to match EOS's speed. That redesign would undermine the primes' core business, which is exactly why counter-positioning works as a durable competitive advantage.

Now layer on Porter's Five Forces to stress-test these advantages from a different angle.

The bargaining power of buyers is high — EOS sells to sovereign nations, which are the most sophisticated and demanding buyers in the world. Defense ministries employ teams of procurement specialists, technical evaluators, and contract negotiators whose job is to extract maximum value from suppliers. But this power is offset by urgency. When drone swarms are an active threat, militaries do not conduct five-year evaluations. The Ukraine conflict shifted power from buyer to seller in ways unusual for defense procurement. This urgency window will not last forever, but it has fundamentally accelerated procurement cycles globally.

The threat of new entrants is low. Building a competitive RWS requires ITAR compliance (or deliberate ITAR-free alternatives), sovereign export approvals, vehicle integration partnerships, and years of testing. Turkey's ASELSAN has shown new entrants can break through with aggressive pricing and government backing, but the timeline is decades. In high-energy lasers, the barriers are even higher — the physics, thermal management, and regulatory frameworks are genuinely formidable.

Supplier power is moderate and worth watching carefully as EOS scales. The company depends on specialized components — high-power laser diodes, precision optics, the Echodyne radar module in the Slinger system — from a limited number of global suppliers. The Echodyne radar, for instance, is a sole-source component: there is no second vendor who can provide an equivalent unit on short notice. EOS mitigates this partly through vertical integration — manufacturing much of its optics and fire control hardware in-house at its Canberra and Singapore facilities — and partly through strategic inventory management.

But the risk grows as the order book scales. Converting A$459 million in orders to delivered systems requires a reliable, high-volume supply chain. A single component shortage — a batch of defective laser diodes, a trade restriction on a precision optic, a delivery delay from Echodyne — could cascade into missed delivery milestones, customer penalties, and reputational damage that takes years to repair. Supply chain management has destroyed more defense programs than enemy action.

The threat of substitutes is the most interesting force. Electronic warfare solutions — jamming and spoofing — are the primary substitute for kinetic counter-drone systems. They are cheaper and carry less collateral damage risk. DroneShield, an Australian competitor, has built a significant business on this approach. But electronic warfare has a fundamental limitation: it fails against autonomous drones navigating by visual recognition or pre-programmed GPS rather than real-time radio links.

As drone autonomy increases — and it is increasing rapidly — kinetic and directed-energy solutions become complements to electronic warfare, not competitors. The emerging doctrine, validated in Ukraine, is "layered defense": electronic warfare for easy targets, kinetic systems for those that get through, directed energy for volume engagements. EOS's portfolio spans the kinetic and directed-energy layers, and MARSS provides the command layer orchestrating all three.

Rivalry among competitors is intense but segmented in ways that currently favor EOS.

In remote weapon stations, Kongsberg holds incumbency with over twenty-four thousand Protector units deployed globally — a formidable installed base that generates decades of maintenance and upgrade revenue. But Kongsberg has been slower to develop counter-drone and directed-energy capabilities, leaving the fastest-growing segment of the market open.

In high-energy lasers, the competitive field is active but no one else has reached the finish line first. Raytheon has demonstrated its HELWS system, which the British Army fired in December 2024. Rafael and Elbit are developing Iron Beam for Israel, backed by a US$500 million contract from the Israeli Ministry of Defense. MBDA's DragonFire program in the UK received GBP 316 million in government funding, with delivery targeted for 2027. Rheinmetall and MBDA have formed a joint venture in Germany with a target of 2029. But EOS delivered the first 100-kilowatt export contract — to an actual paying customer, not a government-funded demonstrator. In the defense industry, the gap between "demonstrated in a test" and "delivered under contract" is measured in years and hundreds of millions of dollars.

No competitor currently offers the same end-to-end, multi-layer counter-drone solution combining kinetic weapons, directed energy, and AI-enabled command and control under a single integrated platform.

The strategic implication is clear. EOS occupies a defensible niche at the intersection of three powerful trends: the proliferation of drones as a primary threat, the global surge in defense spending, and the maturation of directed-energy weapons from laboratory curiosity to production system. The company's competitive advantages — cornered resource in laser physics, switching cost moat in RWS integrations, and counter-positioning speed — are real but not impregnable. They require continuous investment, flawless execution, and a management team that can resist the temptation to overextend. The SpaceLink debacle is a reminder of what happens when ambition outpaces financial capacity.

VIII. Analysis: Bear vs. Bull

The bear case rests on three substantial pillars.

First, revenue lumpiness and cash flow. Defense contracts are inherently lumpy — a single large order can double revenue in one year, and its absence can halve it the next. EOS's fiscal year 2025 revenue of A$128.5 million was down forty-one percent from fiscal year 2023's A$219.3 million, even as the order book tripled. Operating cash flow was negative A$24.2 million, and free cash flow was negative A$44.2 million. EOS has been operating cash-flow negative in four of the last five fiscal years.

The new A$100 million credit facility with WHSP, maturing February 2028 at an average all-in rate of 14.75 percent, provides a safety net — but the cost of capital is extraordinary. If backlog conversion is slower than expected, EOS will be borrowing at rates that would make a subprime mortgage lender blush.

Second, sovereign risk concentration persists. Despite the welcome geographic diversification of the order book — with new customers now in Europe, the US, and Korea joining the established Middle Eastern relationships — EOS's revenue remains materially exposed to a small number of sovereign customers. This is the nature of the defense industry: you sell to governments, and governments are political entities with political priorities.

A new defense minister who favors a domestic supplier over an Australian import. A budget crisis triggered by falling oil prices that forces a Gulf state to defer capital expenditures. A diplomatic rupture between Australia and a customer nation over a human rights dispute or a foreign policy disagreement. Any of these — and defense industry veterans have seen all of them — could create a sudden cash flow crisis for a company of EOS's scale. The diversification helps, but the fundamental vulnerability of selling big-ticket items to a small number of sovereign customers remains embedded in the business model.

Third, the cost of maintaining a technology edge. Rheinmetall generated over EUR 7 billion in 2024 revenue. Raytheon's R&D budget alone exceeds EOS's market capitalization. Rafael's Iron Beam is backed by Israel's existential defense commitment. MBDA's DragonFire received GBP 316 million in UK government funding. The risk is that a prime decides to compete seriously in EOS's markets, bringing resources EOS cannot match.

There is also a regulatory overhang worth noting. Australia's Defence Trade Controls Amendment Act 2024 tightened export controls on Australian defense technology. While the AUKUS ITAR exemption (finalized December 30, 2025) streamlines trade between Australia, the US, and UK by eliminating license requirements for over 700 approved entities, it does nothing for EOS's growing customer base in the Middle East, continental Europe, and Asia-Pacific. Many European NATO members explicitly exclude ITAR-controlled goods from their tenders — which is precisely why EOS built its R500 RWS in Singapore as an ITAR-free alternative and located its Apollo laser manufacturing there as well. The regulatory chess game between Australian export controls, US ITAR requirements, and customer demands for sovereign, unrestricted supply chains adds complexity, cost, and risk to every deal EOS pursues outside the AUKUS umbrella.

There is also the key-man risk that cannot be ignored. The fifteen-percent stock drop when Schwer announced a planned share sale demonstrated how tightly the investment case is tied to a single individual. If Schwer departs — whether voluntarily, through headhunting by a larger firm, or for any other reason — a significant de-rating is likely. This is not unusual for turnaround stories, but it is a risk that investors must price explicitly.

The bull case is equally compelling.

The structural tailwind is what some defense analysts have called the "golden age of defense spending" — the largest, most sustained increase in global military budgets since the end of the Cold War. The numbers are remarkable. In 2014, only three NATO members met the 2 percent of GDP defense spending target. By 2025, all thirty-two members were expected to meet or exceed it. The new NATO target, agreed in principle, is 3.5 percent of GDP by 2035 for core defense capabilities, with an additional 1.5 percent for infrastructure — a total of 5 percent of GDP devoted to defense.

The country-level figures tell the story even more vividly. Germany, which spent decades underinvesting in its military, expects to double its defense budget to EUR 162 billion by 2029. Poland already spends roughly 4 percent of GDP on defense. Lithuania has committed to an extraordinary 5-6 percent through 2030. Australia's defense budget sits at approximately A$59 billion for fiscal 2025-26, with growth expected through the decade driven by AUKUS submarine and advanced capability commitments.

The directed-energy weapons market is projected to grow from US$7.1 billion in 2024 to US$21.5 billion by 2031 — a compound annual growth rate exceeding 17 percent. The remote weapon station market is expanding at nearly 10 percent annually. EOS sits at the intersection of these growing markets with battle-proven, first-to-market products.

The company-specific catalyst is the margin transformation underway. MARSS adds high-margin software. The Korea JV introduces IP licensing revenue. Apollo carries technology margins, not manufacturing margins. As the mix shifts, profitability should improve materially. Analysts expect revenue to reach approximately A$227 million in fiscal 2026 and A$336 million in fiscal 2027, with a return to net profitability in fiscal 2027 — though estimates carry wide bands reflecting genuine uncertainty.

The balance sheet transformation is perhaps the most concrete evidence that the turnaround is real rather than aspirational. From A$97 million in debt and A$21.7 million in cash at end of fiscal 2022, EOS ended fiscal 2025 with A$29.5 million in debt and A$106.9 million in cash — a swing of over A$140 million in net financial position. The Altman Z-Score of 8.07 (well above the 3.0 threshold that separates "safe" from "distressed") confirms that the near-death experience is firmly in the past. The question now is not survival but performance.

One myth worth dispelling: the narrative that EOS is a "turnaround play" that has already delivered its returns. The twenty-six-fold increase from the 2022 trough is eye-catching but misleading as a forward-looking indicator. The 2022 price reflected near-zero probability of survival. The current price reflects survival plus moderate expectations for growth. The gap between moderate expectations and the potential outcome — if the A$459 million backlog converts, if Apollo scales, if MARSS integration succeeds — is where the remaining opportunity (or risk) lies.

For those tracking EOS as an ongoing position, two KPIs matter above all others.

The first is backlog-to-revenue conversion rate: the percentage of the order book that converts to recognized revenue each quarter. Management has guided for 40-50 percent of the A$459 million backlog to convert in calendar 2026, implying A$180-230 million in revenue from existing orders. Tracking actual conversion against this guidance reveals whether EOS can execute or whether the backlog is inflated by conditional contracts that never materialize.

The second is operating cash flow. EOS has been cash-flow negative from operations in four of the last five fiscal years — a pattern that reflects the structural realities of defense contracting (high upfront costs, long manufacturing cycles, payment on delivery) but also the legacy of SpaceLink and the restructuring costs that followed. Revenue growth without cash generation is just a more expensive path to insolvency.

The path to a sustainable business requires operating cash flow to turn decisively positive and stay there — not as a one-quarter anomaly driven by a large progress payment, but as a consistent, structural feature of the business model. Defense companies with healthy operations typically generate operating margins of 8-12 percent, and the best-in-class integrators achieve 15 percent or more. EOS's current operating margin is negative, though improving. The trajectory matters more than the current level.

When these two metrics align — backlog converting on schedule and operating cash flow turning positive — the investment thesis is validated. Until then, it remains compelling but unproven.

IX. Epilogue: The Future Written in Light

There is a photograph — widely shared on Australian defense Twitter — of a Slinger system mounted on a vehicle in what appears to be eastern Ukraine, its barrel elevated against a grey winter sky. The operator is invisible, safely inside the vehicle, watching screens that show thermal imagery of the surrounding airspace. Somewhere above, a drone is inbound. The image captures something essential about EOS's position in the world: a technology born from tracking stars in the Southern Hemisphere sky, now defending soldiers on the deadliest battlefield in Europe.

Is EOS the "Lockheed of the Southern Hemisphere"? That title is premature by any honest measure. Lockheed Martin generates over US$65 billion in annual revenue with 116,000 employees. EOS generated A$128.5 million with 496 people. The comparison is flattering but absurd in scale — a ratio of roughly five hundred to one on revenue.

What EOS might become — and this is the more interesting question — is a specialized "Tech Prime": a company that dominates a specific technology vertical so thoroughly that the global primes become its partners and customers, not its competitors.

In remote weapon stations, EOS's four-axis stabilization is the benchmark. In 100-kilowatt laser weapons, EOS holds the only delivered export contract on earth. In counter-drone command and control, MARSS positions EOS as the integrator connecting sensors, AI, and weapons into a single platform.

If the company can execute across all three simultaneously — a significant challenge for a 496-person organization operating across manufacturing facilities in Australia, Singapore, and the United States — it becomes the indispensable component that every major prime needs but none can easily replicate. Think of it as the Qualcomm of defense: not the company that builds the phone, but the company that makes the chip inside every phone.

The hardest lesson embedded in EOS's forty-year history is one that resonates far beyond the defense industry. It is about the transition from a founder-scientist culture to a global-execution culture — the moment when a company must decide whether it is a laboratory that occasionally sells things or a business that occasionally invents things.

Ben Greene's genius was in seeing the connection between satellite tracking and weapon systems before anyone else, in having the audacity to chase a billion-dollar satellite constellation when his company's market cap was a fraction of that, and in building a body of intellectual property over four decades that competitors literally cannot reproduce because the knowledge was created through continuous scientific observation, not through any process that can be purchased or licensed.

Andreas Schwer's genius is in knowing which ambitions to kill, which to scale, and how to structure a business so that brilliant technology actually reaches the battlefield on time and on budget.

The tension between these two modes — the lab and the factory, the visionary and the operator, the PhD and the P&L — is the defining challenge of every technology company that tries to cross the chasm from research breakthrough to production at scale.

Apple navigated it with the transition from Jobs' creative intensity to Cook's supply chain discipline — and even that nearly failed in the late 1990s before Jobs returned. Intel navigated it with Andy Grove's famous pivot from memory chips to microprocessors. SpaceX navigated it by keeping Musk's ambition tethered to Gwynne Shotwell's operational rigor.

The question for EOS is whether it can achieve the same balance in sovereign defense — a domain where the stakes are not market share or quarterly earnings but national security and human lives. A software bug at Apple means a phone crashes. A software bug in a counter-drone system means soldiers die. The margin for error is zero, and the tolerance for "move fast and break things" is nonexistent. Scaling a defense technology company requires not just speed and innovation but absolute reliability — and that is the hardest combination to achieve.

The world these two men have jointly built is one where drones are shot down by proximity-fused rounds at a hundred dollars per kill. Where hundred-kilowatt laser beams, corrected for atmospheric turbulence by algorithms born in an Australian observatory, burn through drone swarms at the speed of light. Where every satellite in orbit is tracked by laser ranging stations in the bush, and orbital debris is nudged out of harm's way by photon pressure from the ground.

It is a world where the physics of light — the oldest force in the universe — becomes the newest weapon of war.

And a small Australian company, born from a government satellite tracking lab on a hilltop outside Canberra, staffed by physicists who started their careers measuring the distance to the stars, is building the tools to make it happen. The journey from Mount Stromlo to the battlefields of Ukraine, from tracking satellites to killing drones, from a broken balance sheet to a billion-dollar order book, is one of the most improbable stories in the modern defense industry.

Whether EOS can convert that remarkable technological position into a durable, profitable business at scale is the question that will determine whether this story ends as a triumph or a cautionary tale.

The ingredients are extraordinary: irreplaceable IP born from four decades of space science, a CEO who has built defense businesses on three continents, battle-proven products in the fastest-growing segments of the defense market, a record order book, and the structural tailwind of the largest increase in global defense spending since the Cold War.

The risks are equally real: lumpy revenue, sovereign customer concentration, a history of cash consumption that has yet to turn positive, key-man dependence on a single executive, and the ever-present threat that a defense prime with fifty times EOS's resources decides to compete in earnest.

The record order book says triumph. Four years of negative operating cash flow says prove it.

The next twelve months — as the A$459 million backlog hits its conversion window and Apollo enters series production — will provide the answer.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube