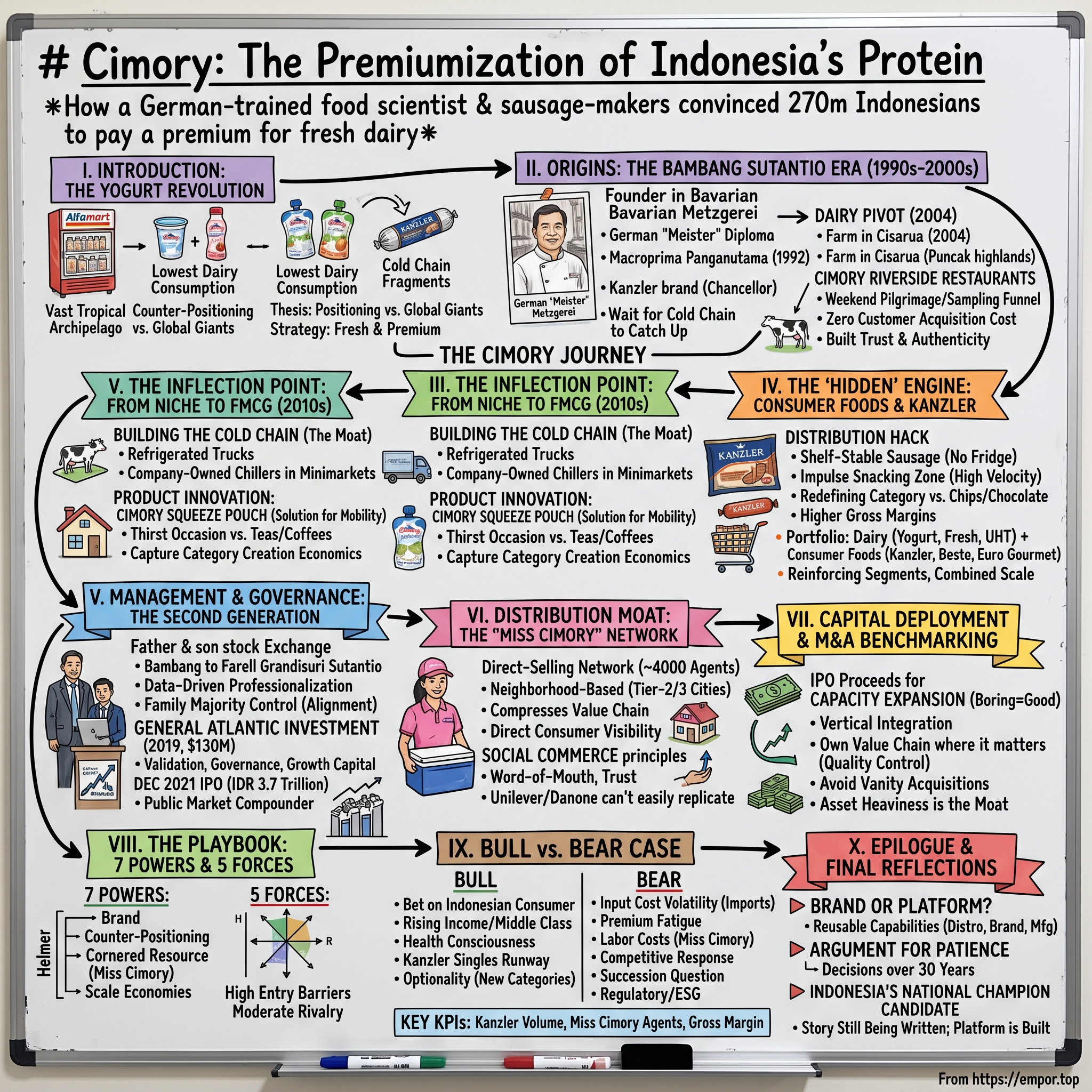

Cimory: The Premiumization of Indonesia's Protein

I. Introduction: The Yogurt Revolution

Step into an Alfamart in suburban Bekasi at 6 PM on any weeknight in 2026. The fluorescent lights hum over a cooler cabinet that, just fifteen years ago, would have been unthinkable in an Indonesian convenience store — a chilled, refrigerated unit humming quietly in the tropical humidity, stocked floor-to-ceiling with yogurt drinks, fresh milk pouches, and squeeze-top strawberry yogurts in bright, playful packaging. Above that cooler, on the warm shelf, sits an equally revolutionary product: a single-serve, ready-to-eat sausage wrapped in foil like a granola bar, priced at around five thousand rupiah — roughly thirty US cents — and sold to schoolkids and ojek drivers as casually as a pack of chewing gum.

Both of those products — the refrigerated yogurt and the shelf-stable sausage — bear the same parent company logo. And both, in their own way, represent one of the most audacious premiumization bets in the history of Southeast Asian consumer goods.

The company is PT Cisarua Mountain Dairy Tbk, known to every Indonesian household simply as Cimory, ticker CMRY.JK on the Indonesia Stock Exchange. It is, simultaneously, the country's largest premium yogurt brand, its largest premium processed meat brand, and — perhaps most importantly — the owner of a distribution army of roughly four thousand women who sell dairy products door-to-door in cities where modern retail does not reach.

The hook for this story is a paradox. Indonesia is a vast tropical archipelago of 17,000 islands, 270 million people, and — famously — one of the lowest per-capita dairy consumption rates in all of Asia. The country is dominated by shelf-stable, heavily sweetened condensed and powdered milk, a legacy of Dutch colonial nutrition programs that never quite evolved into a fresh-dairy culture. The cold chain is fragmented. The climate is hostile to refrigerated logistics. And yet, into this environment, a family business led by a man with a German "Meister" diploma built a company that convinced Indonesian consumers to pay a 50% to 100% premium over mass-market brands for a cup of yogurt.

How?

That is the thesis of this episode. Cimory is not, in the final analysis, a dairy company at all. It is a masterclass in what Hamilton Helmer calls Counter-Positioning — a deliberate, structural strategy of offering a product that the incumbent giants (Nestlé, Danone, Frisian Flag, Indofood) cannot easily replicate without cannibalizing their own cash cows. Cimory chose "Fresh and Premium" while the global giants were locked into "UHT and Mass-Market." And in doing so, it created one of the most defensible FMCG franchises in emerging Asia.

The arc runs from 1992 — when founder Bambang Sutantio set up a small meat-processing plant in a Jakarta suburb — through the opening of the now-iconic Cimory Riverside restaurants in the Puncak highlands, the quiet build-out of the "Miss Cimory" direct-selling network, the 2019 pre-IPO investment from US-based General Atlantic, the December 2021 IPO that raised roughly IDR 3.7 trillion, and the post-IPO era in which founder's son Farell Grandisuri Sutantio has turned the business into a data-driven FMCG machine.

Along the way, we will unpack why Kanzler sausages became a "distribution hack" rather than a dinner ingredient, how a network of four thousand women beat Danone's multibillion-dollar marketing budget, and why one of the world's most prestigious private equity firms bet on a dairy company in Puncak instead of a fintech unicorn in Jakarta.

Let us begin where every great consumer company begins — with a founder who saw something that nobody else saw.

II. Origins: The Bambang Sutantio Era

Picture West Germany, sometime in the late 1970s. A young Indonesian food-science student named Bambang Sutantio is on his hands and knees in a traditional Bavarian Metzgerei — a butcher shop — learning how to hand-stuff a bratwurst from a master sausage-maker who has been doing this since before Bambang was born. The Meister doesn't speak English; Bambang's German is functional but unpolished. What he is learning is not just technique. He is learning an entire philosophy of food: that quality is not a marketing claim but a tactile discipline, built from a thousand small decisions about casing, fat ratio, smoke temperature, and maturation time.

Bambang returns to Indonesia in the 1980s with something few Indonesian entrepreneurs of his generation had: a European "Meister" certification in processed meat and dairy. He also returns with a conviction that would shape the next forty years of his life — that there is a vast, untapped middle-class Indonesian market that will, eventually, pay a premium for "real" food. Not yet. But eventually.

In 1992, he founded PT Macroprima Panganutama, a small meat-processing operation in the industrial hinterland west of Jakarta. The first brand was Kanzler — chosen deliberately, because it is the German word for "Chancellor," and because in 1992 Indonesia, the word "German" on a sausage label was a guarantee of premium quality in a category dominated by low-grade, starch-padded local frankfurters.

To understand how radical this was, you need to understand Indonesia in the early 1990s. The Suharto-era economy was liberalizing. A nascent middle class was emerging in Jakarta and Surabaya. But the food culture was still overwhelmingly traditional: wet markets, warungs, rice-and-side-dish meals built around tempe, tahu, and small amounts of chicken. Western-style processed food was a luxury category, and dairy — in particular — was dominated by sweetened condensed milk brands like Indomilk and Frisian Flag, consumed primarily as a sweetener for tea or coffee rather than as a standalone food. Fresh milk was virtually non-existent outside of five-star hotels. Yogurt was, charitably, an aspirational curiosity.

Bambang's early bet was not dairy. It was meat. Kanzler sausages, sold through supermarkets and hotels, were his beachhead — a way to build manufacturing expertise, supplier relationships, and brand credibility in the premium segment while the cold-chain infrastructure for dairy caught up. This is a critical strategic insight that most analysts miss: Cimory is older as a meat company than as a dairy company. The "dairy" brand arrived in 2004, a full twelve years after Kanzler.

The dairy pivot came via an almost accidental insight. In the early 2000s, Bambang began experimenting with fresh milk and yogurt production at a small farm he had acquired in Cisarua, in the mountainous Puncak region south of Jakarta — a cool, highland area that had been a colonial-era getaway for Dutch planters and was, even in the 2000s, the weekend-escape destination for millions of Jakartans fleeing the lowland heat. The farm was originally a hobby. It became the brand.

Here is where the strategy gets clever. Rather than trying to force fresh dairy into a supermarket cold chain that didn't exist, Bambang built a restaurant on the farm — Cimory Riverside — overlooking a scenic mountain stream. He fed Jakartans grilled sausages from his meat plant, fresh yogurt from his cows, and fresh milk still warm from that morning's milking. The restaurant became a weekend pilgrimage site. And every family that drove up the winding Puncak Pass road to eat bratwurst over a trout stream left with shopping bags full of Cimory dairy products to take home.

This is what you might call a "Destination Strategy." Where a traditional FMCG playbook would spend hundreds of millions of dollars on television ads to build brand awareness, Cimory built a restaurant. The customer acquisition cost was, effectively, zero — the diners paid Cimory to try its products. And because Puncak is the single most concentrated weekend leisure destination for Jakarta's middle and upper-middle class, the restaurants acted as a sampling funnel aimed with surgical precision at the exact demographic that could eventually afford premium yogurt.

By the late 2000s, the Cimory brand had the one thing money cannot easily buy: trust. Trust that the dairy in the cup was fresh, trust that it came from a real farm in a real place, trust that the German-trained Meister standing behind it was not just another marketing abstraction. It was aspiration dressed up as authenticity — and it was about to become the foundation of a national FMCG franchise.

What Bambang had built, without quite realizing it, was a platform. The next decade would be about figuring out how to take it to scale.

III. The Inflection Point: From Niche to FMCG

If the 2000s were about building the brand through the restaurants, the 2010s were about something far harder: taking a product that required refrigeration at every step from the cow to the consumer and pushing it into tens of thousands of retail locations across a nation of seventeen thousand islands, split across a three-hour time zone span, in which the "last mile" of distribution is often a teenager on a motorbike in ninety-degree tropical heat.

This is the story of the cold chain — and it is the single most underappreciated moat in Cimory's business.

Consider what the Indonesian retail landscape looked like around 2010. Organized modern trade — supermarkets and minimarkets like Alfamart and Indomaret — was growing rapidly, but still accounted for a minority of packaged food volumes. The vast majority of consumer goods still moved through "general trade": warungs, traditional grocery shops, street-corner kiosks, most of which had, at best, a domestic-grade refrigerator in the back powered by unreliable grid electricity. For Unilever or Indofood selling shelf-stable instant noodles and condiments, this was a manageable problem. For a company selling fresh yogurt that spoils in hours if broken from the cold chain, it was an existential one.

Cimory's solution was to essentially build its own infrastructure. Rather than waiting for Indonesia's cold chain to mature, the company invested aggressively in its own refrigerated trucks, distribution centers, and — most critically — the chillers that sit inside Alfamart and Indomaret stores. A Cimory-branded cooler in a minimarket is not just a fridge; it is a miniature beachhead, a piece of company-owned infrastructure that guarantees shelf space, controls merchandising, and forces competitors to either match the investment or cede the category.

This is an important point for investors to internalize: the cold chain is the moat. It looks like an ordinary capital expenditure on a balance sheet. It functions like a patent. Any competitor wanting to sell fresh yogurt in Indonesian minimarkets must replicate a distribution and refrigeration network built over a decade of patient capital investment. Nestlé and Danone can write the check; they cannot compress the time.

The second critical move in this decade was product innovation, and the single best case study is the Cimory Squeeze yogurt pouch — a flexible, re-sealable plastic pouch containing flavored yogurt, launched in the mid-2010s as a portable snack rather than a breakfast item.

Let us pause on the "Jobs to be Done" framing here, because it is a beautiful piece of product thinking. The Indonesian consumer does not, generally, sit down to a leisurely Western-style breakfast with a bowl of yogurt and granola. Indonesian consumption is mobile, on-the-go, eaten one-handed in a traffic jam or between classes. A cup of yogurt with a foil lid and a spoon is, in that context, a logistical disaster — it requires two hands, a flat surface, and a disposal plan. A pouch you squeeze directly into your mouth while riding an ojek is not a dairy product; it is a solution to a very specific mobility problem.

The Squeeze format also solved a second, quieter problem: price-point architecture. A small pouch at a low unit price gives the consumer permission to try. Once they try, they convert to the larger cup and bottle formats, which carry higher margins. This is the classic FMCG "sachet strategy" that built Unilever in India, applied to the premium dairy category in Indonesia.

By the late 2010s, Cimory had done something that no other dairy player had managed to do in a sustained, profitable way in Indonesia: it had taken fresh yogurt from a niche, tourist-souvenir curiosity and turned it into a mass-market staple available in virtually every urban minimarket in the country. The yogurt drink category, in particular, became a runaway hit — a high-protein, sweetened-but-manageably-so, cold beverage that slotted neatly into the Indonesian "thirst occasion" against ready-to-drink teas and coffees.

And the financial implications were enormous. Because the category did not really exist at scale before Cimory created it, the company was not fighting for market share; it was capturing category creation economics. That is the most lucrative position any consumer brand can occupy, and it is why the margin profile of Cimory's dairy business remained structurally superior to its global peers operating in mature, commoditized markets.

But here is the twist. For all the attention paid to yogurt and fresh milk, the real financial engine of the company was not dairy at all. It was something the market underestimated for years — and it was sitting in a foil wrapper on a warm shelf, right next to the cashier.

IV. The "Hidden" Engine: Consumer Foods & Kanzler

Walk into any Indomaret or Alfamart in any Indonesian city in 2026 and look at the checkout area. Next to the gum, the candy bars, and the single-serve coffee sachets, you will find a small, unassuming display of foil-wrapped sausages. They are individually packaged, about the size of a king-size chocolate bar, branded Kanzler Singles, and they retail for a price that makes them accessible to a teenager with pocket money. They do not need refrigeration. They do not need cooking. They are a complete, high-protein snack, ready to be torn open and eaten in three bites.

This is not a sausage. This is a distribution hack dressed as a sausage.

And it is, quietly, the most important product innovation in Cimory's entire portfolio.

To understand why, you have to appreciate the structural economics of Indonesian convenience retail. Alfamart and Indomaret together operate tens of thousands of stores across the archipelago. Each store has finite shelf space, particularly in the high-velocity impulse zones near the cashier. Winning that impulse zone is the holy grail of Indonesian FMCG, because it captures the ojek driver grabbing a snack, the schoolkid on the way home, the office worker between meetings. It is the highest-turnover, highest-margin real estate in the country.

Traditional fresh meat products are locked out of that zone entirely — they require refrigeration, meal preparation, a kitchen. Kanzler Singles broke that constraint. By engineering a sausage that was shelf-stable at ambient tropical temperatures, individually packaged, flavored to appeal to a snacking palate rather than a dinner palate, and priced to compete with chocolate bars rather than with chicken, Cimory created a product that could sit on the counter of forty thousand convenience stores.

The genius move was category redefinition. Kanzler Singles does not compete against other sausages. It competes against Chitato potato chips, against Beng-Beng chocolate wafers, against the entire Indonesian pantheon of salty-sweet impulse snacks. And in that category, a high-protein, "healthy-adjacent" product with a premium German brand name has a structural advantage — particularly as Indonesian middle-class consumers become more health-conscious and more willing to pay for perceived nutritional value.

The financial implications are profound. Sausage snacks at impulse price points carry significantly higher gross margins than commodity meat products, and because the addressable "shelf space" in convenience retail is effectively infinite — every new store that opens creates new shelf — the category has a very long runway before saturation. The consumer foods segment, which now contributes meaningful share of group revenue and an even larger share of profit, has been the rocket stage that propelled Cimory's overall margin profile well above what a pure dairy business could generate.

Let us map out the broader portfolio, because the company structure matters for how you think about the business.

The Dairy segment includes several sub-categories. There is the yogurt line — cups, squeeze pouches, and drinking yogurts in a range of flavors tuned to the Indonesian palate, heavier on tropical fruit notes and lighter on the tart-European style. There is Cimory Fresh Milk, the pasteurized fresh milk line sold in cold chains. There is Cimory UHT, the shelf-stable version that allows the brand to play in general trade where refrigeration is unreliable. And there are ancillary products like cheese and cream for the food-service and bakery channels.

The Consumer Foods segment is built around Kanzler for premium processed meats, Besto for the mid-market tier, and Euro Gourmet for the super-premium hotel and restaurant channel. Within Kanzler, the product line spans from family-pack dinner sausages through bratwurst and smoked meats to the all-important Singles SKU that anchors the convenience-retail strategy.

What is elegant about this portfolio is that the two segments reinforce each other. The manufacturing competence in dairy and meat processing share underlying disciplines — cold-chain management, microbiology, food safety, regulatory compliance — that create operating leverage across the factory base. The distribution network built for one segment carries the other. The brand halo of "German-trained, premium quality" transfers seamlessly between bratwurst and yogurt because they both live in the same consumer mental category: "food that is better than the local default."

This dual-segment structure is also what has made Cimory so difficult for competitors to attack. A pure-play dairy company like Frisian Flag cannot replicate the Kanzler distribution edge. A pure-play meat company cannot build the yogurt category. And neither can match the combined manufacturing, distribution, and brand scale that Cimory has compounded across three decades.

The shift in this portfolio was dramatic over the 2020–2024 period, as Kanzler Singles volumes exploded and the consumer foods segment grew faster than dairy. The market, which had initially valued Cimory as a dairy business with a meat side-hustle, had to re-rate it as an integrated premium FMCG platform. That re-rating was not a gift; it was earned by a company that understood its own economics better than the analysts covering it.

But a portfolio this ambitious required a new generation of management to scale — and that story begins with a handover.

V. Management & Governance: The Second Generation

There is a photograph that circulated in Indonesian business media around the time of Cimory's 2021 IPO. It shows Bambang Sutantio, the founder, standing on the trading floor of the Indonesia Stock Exchange next to his son Farell Grandisuri Sutantio, who was then in his late twenties, holding the ceremonial opening ticker. Father in a dark suit and traditional Indonesian songkok cap, visibly emotional. Son in a crisper, more Western-cut suit, smiling more composedly. The image is almost cinematic in its symbolism: one generation handing the reins of a family empire to the next, in front of the ticker tape of public markets.

The transition from founder-led to second-generation leadership is, historically, the single most dangerous inflection point in any family business. The data on the survival rates of family companies into the third generation is brutal. And yet, the Cimory transition is, so far, a case study in how to do it well.

Bambang Sutantio, the founder, is in many ways the classic Indonesian "self-made industrialist" archetype — technically trained, personally frugal, obsessively focused on product quality, and deeply suspicious of financial engineering. His management style was famously hands-on; he spent time on factory floors, in sales calls, at the Puncak restaurants. He built the company over three decades with discipline that verged on stubbornness, refusing for years to take outside capital even as Indonesian peers raised aggressive rounds of private equity funding. The business he handed over was conservatively capitalized, vertically integrated, and — critically — profitable at every stage of its growth.

Farell, the second-generation CEO, brought a different skill set. Educated overseas, fluent in the language of public-market investors, comfortable with the discipline of quarterly reporting and institutional governance, he represents what you might call the "Indonesian next-gen" — children of the first-generation industrialists who came of age during the country's 2010s boom and learned to run companies as professionalized, data-driven operations rather than as extensions of a family's intuition.

The philosophical shift is subtle but important. Under Bambang, decisions were often based on a deep, accumulated feel for the Indonesian consumer — a feel developed over forty years of personally tasting products, visiting stores, and watching shoppers. Under Farell, the company has layered that intuition with systematic consumer research, A/B testing of SKUs, data-driven trade marketing, and more rigorous capital allocation frameworks. The result is not a break from the founder's vision but an operational professionalization of it — the same strategy, executed at FMCG-industry standards rather than at family-business standards.

The ownership structure post-IPO is a clue to how the family thinks about the business. The Sutantio family, through holding vehicles, retained a controlling majority stake after the IPO — roughly in the range that signals long-term founder control rather than a cash-out event. This matters enormously for investors. In markets like Indonesia, where minority-shareholder protections are historically weaker than in developed markets, the alignment of founder interests with public-market shareholders is one of the single most important governance variables.

Cimory is about as well-aligned as these situations get. The family's wealth is overwhelmingly concentrated in the company's equity, meaning that value destruction at Cimory is value destruction for the Sutantios personally. There are no obvious related-party transactions draining value to private family entities. The dividend policy — not explicitly disclosed as a formal payout ratio but reflected in distributions since listing — suggests a company comfortable returning capital to shareholders rather than hoarding it for empire-building.

Which brings us to the other critical governance variable: General Atlantic.

In 2019, the US-based global growth equity firm General Atlantic — an investor in some of the most successful consumer and technology companies of the past three decades, from Facebook to Adyen to Byju's — invested approximately $130 million in Cimory in a pre-IPO round. The deal was transformative for Cimory in three ways. First, it validated the company to institutional investors who had previously dismissed it as a regional family business. Second, it brought governance discipline — board seats, audit practices, KPI frameworks — that professionalized the company ahead of its public-market debut. Third, it provided growth capital that accelerated the capacity expansion across dairy and meat processing.

Why did General Atlantic, which could have invested in virtually any fintech, e-commerce, or SaaS company in Southeast Asia, choose a dairy and sausage business in Puncak? The answer reveals something important about consumer economics in emerging markets. When GDP per capita crosses certain thresholds — roughly $4,000 to $5,000 USD — consumer spending patterns shift dramatically toward premium packaged food and branded protein. Indonesia, with a population of 270 million and a GDP per capita approaching that threshold in the late 2010s, represented one of the largest premiumization opportunities on earth. And Cimory was the default platform to capture it.

General Atlantic's involvement also signaled something to the broader market: this was no longer a family hobby. It was an institutional-grade FMCG company on a path to public listing. The December 2021 IPO that followed, raising approximately IDR 3.7 trillion (roughly $260 million USD at the time), was one of the largest consumer-sector listings of the year on the Indonesia Stock Exchange and marked the company's full transition from private family enterprise to public-market compounder.

But management and capital were only half the story. The other half — arguably the more interesting half — was a distribution strategy that nobody else in Indonesian FMCG had quite figured out how to replicate.

VI. Distribution Moat: The "Miss Cimory" Network

On a dusty Tuesday morning in a residential neighborhood in Bandung, a middle-aged woman in a pink-and-white branded polo shirt rings a doorbell. She is carrying an insulated cooler bag. When the door opens, she greets the homeowner by name, asks about the children, and hands over a weekly order of yogurt drinks, fresh milk, and a sample of a new seasonal flavor the company just launched. Payment is collected in cash or through a mobile-wallet transfer. The entire transaction takes four minutes. The woman then walks two houses down and repeats the process.

She is a Miss Cimory, and she is quietly one of the most interesting distribution innovations in emerging-market consumer goods.

The Miss Cimory program is a direct-selling network of roughly four thousand agents — predominantly women, many of them housewives or secondary earners, operating in their own neighborhoods in Tier-2 and Tier-3 Indonesian cities where modern retail penetration is thin. They purchase product from Cimory at wholesale, sell to end consumers at retail, and keep the margin. They are not employees. They are not franchisees in the formal sense. They are a hybrid — a community-rooted, relationship-driven, commission-based sales force that functions as Cimory's long tail of distribution.

To appreciate how radical this is, compare it to how the global FMCG giants distribute in Indonesia. A Danone or a Nestlé operates through a conventional two-step wholesale system: products ship from the factory to a regional distributor, from the distributor to a wholesaler, from the wholesaler to a retailer, from the retailer to the consumer. Each layer takes a margin. Each layer introduces friction, shrinkage, and — critically — distance between the brand and the end customer.

The Miss Cimory model compresses that entire chain. Product moves from the Cimory factory to the agent. The agent sells directly to the household. Cimory captures more of the end-consumer price than a traditional distribution model allows. And — here is the genius — the company gets direct visibility into consumer behavior, neighborhood by neighborhood, in parts of Indonesia where sell-through data from traditional channels is essentially nonexistent.

This is social commerce before social commerce had a name. Long before TikTok Shop and Shopee Live began dominating Indonesian consumer headlines, Cimory had built a word-of-mouth, community-embedded, trust-based sales network that functioned on exactly the same principles: personal relationships, neighborhood presence, product discovery through someone you know rather than through an ad.

The unit economics are compelling. The fixed cost of a Miss Cimory agent to the company is essentially zero — agents purchase on their own behalf and earn their income from retail margins. The variable cost is captured in the wholesale-to-retail spread, which is structured to give the agent enough economic incentive to stay active while preserving adequate margin for the manufacturer. The result is a distribution model that scales almost without operating overhead on Cimory's side — the incremental agent adds revenue with almost no incremental fixed cost to the company.

And the moat is enormous. The obvious question — why doesn't Danone just copy this? — has a surprisingly deep answer. Replicating the Miss Cimory network is not a matter of capital. It is a matter of trust, community embedding, and local operational complexity that takes years to build. You cannot parachute four thousand door-to-door agents into Indonesian neighborhoods overnight. You have to recruit them, train them, equip them with cold-chain cooler bags, manage their inventory, settle their payments, support them through stock-outs and seasonal demand shifts. It is a human operations challenge at a scale that global HQ-driven competitors are structurally ill-equipped to execute.

There is also a subtler cultural point. Indonesia is a relationship economy. Commerce happens through networks of trust — neighborhood, religious, family. A brand that distributes through a housewife you know and trust is, in many ways, more credible than a brand that advertises on national television. The Miss Cimory agents are not just selling yogurt; they are extending the brand's "trust envelope" into communities that would otherwise require tens of millions of dollars in advertising to penetrate.

In Hamilton Helmer's framework, this is a textbook Cornered Resource — a valuable asset (in this case, the four-thousand-person distribution network) that the competitor cannot replicate without the same decade of patient investment. Combined with the physical cold-chain infrastructure and the Kanzler shelf placements in convenience retail, Cimory has built what is arguably the most formidable FMCG distribution moat in Indonesia.

But moats require capital, and moats require continued investment. Which brings us to the question of what Cimory has done with the money it raised.

VII. Capital Deployment & M&A Benchmarking

Every time a family-run consumer company does an IPO, there is a moment of truth. The founder, who has spent decades building the business with the patient discipline of an owner-operator, suddenly has a war chest — hundreds of millions of dollars of fresh capital — and the full expectations of public markets pushing for growth. The temptation, historically, has been to deploy that capital in the worst possible ways: vanity acquisitions, unrelated diversification, empire-building M&A that destroys value while satisfying CEO ego.

What has Cimory done with its IPO proceeds? The answer is boring — and that is exactly the point.

The bulk of the approximately IDR 3.7 trillion raised in the December 2021 listing was earmarked for capacity expansion: new dairy processing lines, expanded meat-processing capacity, additional cold-chain infrastructure, and working capital to support the growth in the Miss Cimory network and modern-trade shelf penetration. In other words, the capital was deployed into the exact same playbook that had built the company — just at a larger scale.

This is harder than it sounds. Public markets typically reward visible, exciting M&A announcements. They often punish, or at least yawn at, "boring" organic capacity expansion. A CEO under pressure to show growth has every incentive to make a splashy acquisition. Farell and the Cimory board, to their credit, have largely resisted that temptation.

The capital-deployment philosophy at Cimory can be summarized in one phrase: own the value chain where it matters; do not overpay for what you can build. Unlike global FMCG peers that have, in recent decades, spent enormous sums acquiring "trendy" niche brands at optically high valuations — oat milk startups, plant-based protein companies, organic yogurt lines — Cimory has focused overwhelmingly on vertical integration within its existing categories. Own the dairy plants. Own the meat plants. Own the cold-chain distribution. Own the relationship with the farmer supplying the raw milk, the slaughterhouse supplying the meat inputs, the distributor pushing product into minimarkets.

The logic is elegant. In an emerging market where raw-material supply chains are volatile, vertical integration is not just a margin play — it is a quality-control play. Premium positioning requires absolute certainty about what goes into the product. Depending on third-party suppliers for critical inputs means outsourcing the single most important variable in a premium brand's economics. By owning more of the value chain, Cimory protects both the margin and the brand promise simultaneously.

This is also where the company's CAPEX-heavy model deserves a critical second look. The legitimate bear-case concern is that a dairy and meat business with high fixed-asset intensity is structurally less attractive than an asset-light branded-product business like a global beverage franchise. Cimory has to keep investing in plants, trucks, chillers, and cold-chain infrastructure. That capital intensity suppresses return on capital compared to an idealized asset-light FMCG comparable.

The counter-argument is that the capital intensity is the moat. An asset-light branded dairy business in Indonesia would be immediately commoditized by any competitor willing to outsource production to contract manufacturers. The asset heaviness is what keeps competitors out, guarantees product quality, and captures the vertical margin. In emerging-market consumer goods, some of the most durable moats are built on exactly this kind of "patient capital" foundation that asset-light investors tend to underestimate.

There is also a quieter strategic benefit to the build-not-buy approach. In markets like Indonesia, where strategic M&A targets are often family-controlled and valuation expectations are frequently disconnected from operational reality, the discipline of refusing to overpay has been one of the most value-creating stances a management team can take. Every deal Cimory has not done is, in a sense, a small act of value creation.

Which is not to say the company is opposed to deal-making. Periodic partnerships, co-manufacturing arrangements, and selective capacity investments have been part of the playbook. What has been absent is the empire-building "transformative" deal that destroys more value than it creates.

The signal to investors here is simple: this is a management team that behaves like owners because they are owners. The Sutantio family's economic interests are so concentrated in Cimory that the wrong capital-allocation decision would directly cost them personal wealth. That alignment is rare in emerging-market public companies and should be weighted heavily in any long-term ownership case.

With the capital strategy framed, we can now turn to the harder question: how durable is the moat, really?

VIII. The Playbook: 7 Powers & 5 Forces

One of the most useful mental exercises in analyzing a consumer business is to subject it to the rigor of two of the most enduring strategy frameworks in modern business literature — Hamilton Helmer's Seven Powers and Michael Porter's Five Forces. Cimory, when stress-tested against both, reveals a business whose competitive advantage is deeper and more multi-layered than a casual look at its financial statements would suggest.

Start with Helmer's Seven Powers. A company can be considered to have a genuine competitive moat only if it possesses at least one of the seven — and the strongest companies typically compound multiple Powers simultaneously.

The first Power that Cimory clearly possesses is Brand. The Cimory name, built over two decades through the restaurants, the Miss Cimory network, the consistent product quality, and a careful marketing positioning, functions as a trust proxy in Indonesian consumer minds. A mother in Surabaya buying yogurt for her children is not really buying a cup of fermented milk; she is buying the promise that the product is safe, premium, and fresh. That promise is encoded in the brand name, and it allows Cimory to charge a price premium that competitors cannot match without first investing years in building equivalent trust.

The second Power, and arguably the most interesting, is Cornered Resource. The Miss Cimory network — four thousand agents, deeply embedded in their local communities, holding relationships that took years to build — is a textbook example. A competitor cannot simply throw capital at this problem; the resource is inherently local, relational, and time-bound.

The third Power is Counter-Positioning, which in many ways is the core thesis of the entire Cimory story. The global dairy incumbents in Indonesia — Nestlé, Danone, Frisian Flag — built their Indonesian franchises on shelf-stable, heavily sweetened, mass-market dairy. That product architecture is highly profitable. To compete with Cimory in fresh, premium dairy, they would have to invest in cold chain, fresh-processing capacity, and a premium brand positioning that directly cannibalizes their existing mass-market businesses. The incumbent is structurally reluctant to make that move. Cimory exploits that reluctance.

A fourth Power, Scale Economies, is emerging. As the company's manufacturing base and distribution network grow, the fixed-cost leverage across dairy and meat categories creates a cost position that new entrants cannot match. Each new minimarket chiller, each additional meat-processing line, each marginal Miss Cimory agent adds incremental volume without proportional fixed-cost growth.

The remaining three Powers — Switching Costs, Network Economies, and Process Power — are more marginal in Cimory's case. Consumer switching costs in dairy are low, which is why the brand Power has to do the heavy lifting. There are no network effects in the traditional software sense. Process Power — the accumulated operational excellence in cold-chain management and food safety — is real but difficult to quantify. Still, four of seven Powers present at meaningful strength is a strong position by any framework.

Now pivot to Porter's Five Forces, which ask a different set of questions about industry structure.

Barriers to Entry are high. The cold chain, the brand equity, the distribution network, the manufacturing scale — all of these require years of patient capital investment that a new entrant cannot compress. A well-funded startup could, in theory, enter premium yogurt, but it would find itself fighting for shelf space against an incumbent that already owns the chiller and the relationship with the retailer.

Bargaining Power of Suppliers is a real risk vector. Indonesia does not produce enough raw milk to meet domestic demand, meaning that significant portions of Cimory's dairy inputs come from imported milk powder and other dairy derivatives. Global dairy prices, driven by New Zealand, Australia, and European supply dynamics, can swing meaningfully, and those swings pass through to Cimory's cost structure. The company's vertical integration with domestic dairy farms mitigates but does not eliminate this exposure.

Bargaining Power of Buyers — meaning the modern-trade retailers like Alfamart, Indomaret, and the supermarket chains — is a constant tension in FMCG. Indonesian modern trade is consolidating, and that consolidation gives the big chains increasing leverage over their suppliers. Cimory's counter to this is product differentiation and category creation — if the retailer needs the Cimory brand to drive traffic into the dairy or processed-meat aisle, the bargaining position reverses. The Miss Cimory direct-selling channel also provides a useful hedge, giving Cimory an alternative route to consumers that does not depend on modern-trade gatekeepers.

Threat of Substitutes is nuanced. In pure beverage terms, yogurt drinks compete with ready-to-drink teas and coffees, coconut water, traditional beverages, and sugary sodas. In the snacking category, Kanzler Singles competes with chips, chocolate, biscuits, and other impulse snacks. The substitute universe is vast. But Cimory has increasingly positioned its products against the "healthy snacking" and "functional protein" subcategories, which have been growing faster than the conventional impulse categories and in which Cimory's premium positioning gives it a structural edge.

Rivalry Among Existing Competitors is moderate. The premium dairy and premium processed-meat categories in Indonesia are not crowded. Cimory has a dominant share in both. Global players have been slow to respond, and local imitators lack the brand equity and distribution scale. The category is, effectively, Cimory's to lose — a position that is economically enormously valuable as long as the company continues to execute.

The combined picture is of a business with a layered, multi-dimensional moat that is rare in emerging-market FMCG. It is not a single-powered monopoly. It is a carefully constructed portfolio of Brand, Counter-Positioning, Cornered Resource, and emerging Scale Economies, all anchored in a cold-chain infrastructure that functions as the physical equivalent of a patent.

That does not mean there are no risks. And the next section is where we dwell on them.

IX. Bull vs. Bear Case

Every well-analyzed stock deserves both its optimistic and pessimistic narratives laid out with intellectual honesty, because the gap between them is typically where investor conviction is either earned or lost.

The Bull Case

The bull case on Cimory is, at its core, a bet on the Indonesian consumer.

Indonesia has one of the lowest per-capita dairy consumption rates in Asia — substantially below Malaysia, Thailand, Vietnam, and of course the developed markets of Japan, Korea, and China. The reasons are historical (no strong traditional dairy culture), economic (dairy has historically been a premium category for most households), and logistical (the cold chain has limited penetration). But all three of those constraints are softening simultaneously. Per-capita income is rising. The middle class is expanding. Modern retail and cold-chain infrastructure are scaling. Health consciousness is growing. Urbanization is accelerating.

In that environment, Cimory is positioned as the default premium choice. It is not competing for the mass-market consumer who buys sweetened condensed milk for their morning tea; it is competing for the rising middle-class consumer who is trading up to something cleaner, fresher, and higher in protein. That trade-up is a demographic tailwind that will compound for a decade or more.

Layered on top of that dairy bull case is the consumer-foods story, which is arguably even more attractive. Kanzler Singles, and the broader family of ambient-shelf-stable premium snacks the company has built around it, has a runway that is essentially defined by the continued expansion of convenience-store networks across Indonesia. Every new Alfamart store is a new shelf. Every new Indomaret store is a new point-of-sale. And the category is still nowhere near saturation relative to more developed snack markets.

The Miss Cimory distribution network continues to extend reach into Tier-2 and Tier-3 cities where the competition is thinnest. As Indonesia's economic growth lifts household incomes in those secondary cities, Cimory will be there, agent-by-agent, household-by-household, capturing premium protein demand that the global giants simply cannot reach.

The capital-allocation discipline of the Sutantio family — conservative leverage, vertical integration, disciplined M&A — suggests that the compounding potential of the business is unlikely to be squandered on ego-driven deals. The governance profile is tighter than typical Indonesian family businesses, partly due to General Atlantic's imprint.

Finally, there is the optionality. Cimory has demonstrated the capability to launch and scale new categories — the Squeeze pouch, the yogurt drink, Kanzler Singles. The next decade will likely see further category expansion: ready-to-drink coffee with a dairy base, protein bars, functional foods for specific consumer occasions. Each new category, leveraged over the same manufacturing and distribution base, creates incremental value with declining marginal cost.

The Bear Case

The bear case is more subtle but deserves careful consideration.

The first and most material risk is input cost volatility. Because Indonesia does not produce enough raw milk domestically, Cimory depends on imported milk powder and other dairy inputs priced in global markets. A sustained spike in international dairy prices, or a weakening of the Indonesian rupiah against the US dollar, directly compresses gross margin. The company can pass some of that cost through to end consumers, but pricing power has limits, particularly in a price-sensitive emerging-market consumer base.

The second risk is premium fatigue. Cimory's entire thesis rests on the willingness of Indonesian consumers to pay a meaningful premium over mass-market dairy. In a benign macro environment — low inflation, rising real incomes — that premium is palatable. In a high-inflation, stagnant-income environment, premium positioning becomes a liability. The consumer trades down to cheaper alternatives, and the top-line growth stalls. Periods of acute macro stress in Indonesia, particularly around currency crises or commodity-driven inflation, are the periods when Cimory's model is most vulnerable.

The third risk is distribution model scalability. The Miss Cimory network is a magnificent asset, but it is also a labor-intensive one. As Indonesian labor costs rise with economic development, and as alternative income options for housewives expand (particularly through digital platforms like Shopee, TikTok Shop, and gig economy apps), the economic attractiveness of being a Miss Cimory agent may erode. The network will need to continuously evolve its compensation structure and digital tooling to stay competitive as a labor opportunity.

The fourth risk is competitive response. So far, the global dairy giants have been slow to contest Cimory's premium positioning, constrained by the counter-positioning dilemma. But nothing in strategy is permanent. A well-funded, committed global competitor — Danone, Nestlé, or a new entrant from China or Korea — could, over a decade, build the cold chain, acquire a local brand, and mount a serious challenge. The risk is not immediate, but it is real over longer horizons.

The fifth risk is the succession question. Cimory is mid-way through a generational transition. Farell appears, on all available evidence, to be an extremely capable next-generation operator. But family-business history is littered with companies that thrived for a generation and then faltered in the second or third. The governance structures, board composition, and institutional discipline that allow the company to outlast any individual leader are the variables that matter most here — and those are works-in-progress.

Sixth, there is the regulatory and ESG overlay. Indonesian food and dairy regulation has tightened over the past decade. Halal certification, labeling requirements, and food-safety standards have all evolved. Cimory has, so far, navigated these well, but regulatory risk is a live variable. Additionally, dairy farming and meat processing are industries with non-trivial environmental footprints, and global investor interest in ESG metrics may, over time, create reporting and operational burdens that previously did not exist.

Key Performance Indicators

For long-term investors tracking Cimory, three KPIs deserve close attention above all others:

First, volume growth in the Consumer Foods (Kanzler) segment — because this is the highest-margin, most convenience-driven growth engine, and its performance reveals the strength of the ambient snacking thesis.

Second, active agent count and productivity-per-agent in the Miss Cimory network — because this distribution asset is the hardest-to-replicate moat, and its scaling trajectory tells you whether the direct-selling model remains economically compelling to participants.

Third, gross margin across the company — because it captures, in a single number, the interaction of raw-material costs, pricing power, premium positioning, and vertical integration. Sustained gross margin at premium-FMCG levels is the leading indicator of the Cimory thesis holding together; material gross margin erosion would be the earliest signal of trouble.

These are the three dashboards to watch. Everything else is secondary.

X. Epilogue & Final Reflections

There is a question that sits at the center of every great consumer-company analysis: is this a brand or is this a platform?

A brand is a single promise, a single market position, a single category. It can be enormously valuable — think of Hermès or Harley-Davidson — but its value is bounded by the category it occupies. A platform, by contrast, is a set of reusable capabilities — manufacturing, distribution, brand equity, consumer relationships — that can be redeployed across categories, generating compounding returns on the core asset base.

Cimory has, over thirty years, quietly become a platform.

Consider what the company actually owns. It owns a cold-chain distribution infrastructure that reaches tens of thousands of modern-trade locations and thousands of traditional retail points. It owns a direct-selling network of four thousand women embedded in local communities across Indonesian cities. It owns two of the most trusted premium food brands in Indonesia, spanning the dairy and processed-meat categories. It owns vertically integrated manufacturing capacity in both categories. And it owns, perhaps most importantly, a thirty-year track record of disciplined capital allocation, quality obsession, and patient compounding.

Any of those assets, in isolation, would be valuable. Combined — and deployed across an Indonesian consumer market whose premiumization curve still has decades of runway — they form a platform that can keep launching new products, entering new categories, and capturing new consumer occasions for a very long time.

The story of how that platform got built is, in the end, a story about time. Bambang Sutantio made decisions in 1992 that only fully paid off in 2016. He built restaurants in Puncak that only made commercial sense when the weekend Jakartan middle class reached a certain scale a decade later. He invested in cold-chain infrastructure that only became a moat when organized retail penetrated deeply enough to reward it. He built a meat brand in a Muslim-majority country where processed meat was a niche category, and he waited patiently for the category to grow into his capacity.

Almost everything about Cimory's thirty-year arc is an argument for patience — for making decisions whose payoffs are multi-decade and whose logic only becomes clear in retrospect. That is an incredibly rare quality in a public-market environment that rewards quarterly performance and punishes long-horizon bets. It is also, historically, the quality that distinguishes generational consumer winners from the long tail of forgotten also-rans.

And yet — and this is the Acquired.fm instinct to challenge the consensus narrative — one should also resist the temptation to treat the Cimory story as a simple heroes' journey. The company has real vulnerabilities. The input cost structure is exposed. The premium consumer is sensitive to macro shocks. The succession transition is incomplete. The competitive landscape will not remain static forever.

What the history shows is not that Cimory is invulnerable, but that it has, so far, navigated each inflection point with a discipline that most of its peers lacked. The 2004 dairy pivot. The 2010s retail expansion. The 2019 General Atlantic partnership. The 2021 IPO. The 2022-onward generational transition. Each of those could have been the moment when the story went sideways. None of them did.

In the Acquired.fm framework, there is a concept worth returning to: the "National Champion." Every large, resilient emerging market eventually produces one or two consumer companies that become the default, trusted, mass-market premium brand for an entire nation. In the Philippines, it is Jollibee. In India, it is companies like Nestlé India and Britannia. In China, it is Yili and Mengniu. In Mexico, Bimbo and FEMSA. These businesses share a set of characteristics: deep local distribution, strong founder or family ownership, disciplined capital allocation, and a product that becomes culturally embedded in the country's daily life.

Cimory is Indonesia's candidate for that role in protein — both the fresh kind in the cooler and the ambient kind on the convenience-store counter. Whether it fully claims that mantle over the next decade will depend on execution, on macro conditions, on competitive dynamics, and on the continued judgment of a family that has so far shown remarkable stewardship.

What can be said with some confidence is this: the building of Cimory is one of the most quietly impressive FMCG stories in emerging Asia. It did not win by outspending global giants. It did not win by chasing trends. It did not win by financial engineering. It won by understanding, better than anyone else, what Indonesian consumers wanted, what Indonesian infrastructure could deliver, and what patient capital could build — and by aligning those three variables across three decades of disciplined execution.

From a family garage startup in 1992 to a public-market compounder valued in the billions of US dollars by 2026, Cimory is proof that in consumer goods, as in few other industries, time remains the most powerful compounding engine. And in the premiumization of Indonesia's protein — the fresh yogurt in the chiller, the German sausage on the shelf, the Miss Cimory agent at the door — you can see, in real time, what three decades of compounding actually look like.

The story is still being written. But the platform is built.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube