BIWASE: The Utility Roll-Up of Vietnam's Industrial Heartland

I. Introduction: The "Water King" of Vietnam

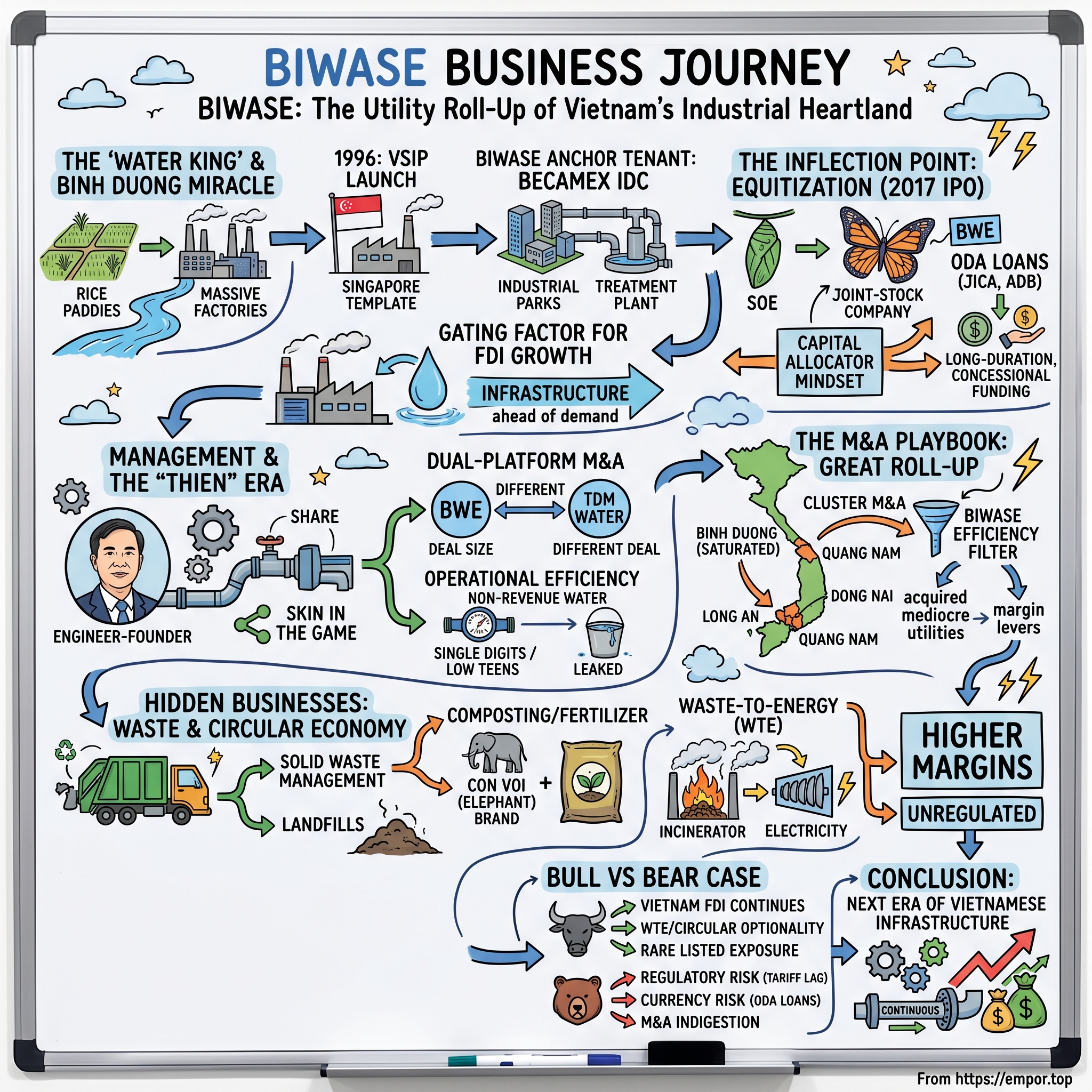

Picture a rice paddy north of Ho Chi Minh City, sometime in the late 1990s. The land is flat, the sky is heavy, and the only sound is the slow drip of irrigation water bleeding through earthen dikes. Now hit fast-forward. Twenty-five years later, that same patch of land is covered in factory shells the size of airport hangars. The companies inside make smartphones for Samsung, sneakers for Nike, semiconductors for Intel, and furniture for IKEA. The landscape is unrecognizable. The electricity grid is heavier. The sky is the same. But something else has changed, quietly, in the ground: under those factories runs a lattice of steel and PVC pipes, pumping millions of cubic meters of treated water every single day.

In the world's fastest-growing manufacturing hub, what is the one truly "un-disruptable" asset? It is not the factories. Factories move. Samsung can shift a line to India in eighteen months. Nike can re-source a contract in a quarter. It is not the labor. Labor arbitrage is a shifting sand dune. It is not even the land. Land gets rezoned, relocated, reclaimed. The one thing that does not move is the water. You cannot export a river. You cannot fax a sewer line. And whoever owns the pipes that feed the factories has a seat at every industrialization story that country ever tells.

That is the opportunity behind the subject of today's deep dive: Binh Duong Water – Environment Corporation, ticker BWE on the Ho Chi Minh City Stock Exchange, better known to locals as BIWASE1. On paper, BIWASE is a provincial utility. In practice, it is a roll-up machine, a waste-to-energy experiment, and one of the very few ways an institutional investor can buy a liquid, exchange-listed claim on the urbanization and industrialization of Vietnam through a company that behaves less like a sleepy water monopoly and more like a disciplined, founder-led compounder.

The thesis we are going to unpack is deceptively simple. BIWASE figured out that in a country adding a Singapore's worth of industrial GDP every two to three years, the scarce asset is not capital, and it is not concrete. It is the right to operate a water concession. Once you have that right in one province, you have a cash-flow engine. Once you have it in five, you have a regional utility. Once you stitch those together with waste treatment, fertilizer, and waste-to-energy, you have something that looks suspiciously like a small environmental conglomerate, trading at multiples more appropriate to a bond than a compounder.

This is the story of how a provincial pump station in Binh Duong became a multi-province roll-up with ambitions that rhyme more with Berkshire's early utility plays than with a typical state-owned enterprise. It is also a story about the specific cultural and regulatory geometry of Vietnam, where the line between public and private ownership is still being drawn in real time, and where a handful of operators with a "founder-owner" mindset are learning to exploit that ambiguity. Let us start where every great utility story starts: with geography.

II. The Binh Duong Miracle: Context for the Kingdom

Binh Duong Province does not look, on first glance, like the kind of place that would produce a listed compounder. It is wedged immediately north of Ho Chi Minh City, bordered by the Saigon and Dong Nai rivers, historically a land of rubber plantations and pottery kilns. In the late 1980s, when Vietnam's Đổi Mới reforms began to tiptoe toward market economics, Binh Duong's GDP per capita was a rounding error. What the province had, however, was two things money cannot easily manufacture: flat, stable, well-drained land, and a provincial government that decided, early and aggressively, to bet the entire future of the province on foreign direct investment.

The bet was executed through a provincial champion, Becamex IDC, a state-owned industrial developer that began acquiring and zoning enormous tracts of land for industrial parks. Then came the masterstroke. In 1996, Becamex partnered with a consortium of Singaporean investors led by Sembcorp to launch the Vietnam Singapore Industrial Park (VSIP) in Binh Duong2. VSIP imported something more valuable than capital: it imported Singapore's operating template. Zero-corruption one-stop permitting. Reliable power. Predictable water. English-speaking customer service. For a Korean or Japanese manufacturer comparing Vietnam to Indonesia or the Philippines, VSIP made the decision easy.

Fast forward through a decade of compounding FDI. By the mid-2010s, Binh Duong had become, in effect, the Silicon Valley of factories for Southeast Asia. It regularly ranked as Vietnam's number-one or number-two province for FDI attraction, despite not having a port, an international airport, or a meaningful domestic consumer base. The factories came for VSIP's template. But factories are thirsty. A single semiconductor line can consume as much water as a town of 20,000 people. A paper mill drinks more. A textile dye house drinks even more than that, and then hands back effluent that must be treated before it touches the Saigon River.

That is where BIWASE enters. Established in its modern form out of the provincial public utility, the company grew up feeding exactly this industrial build-out. Its customers were not, initially, households. They were the industrial parks ringing the provincial capital of Thu Dau Mot. Every time a new VSIP phase broke ground, BIWASE had to either expand an existing plant or build a new one. Every time Samsung added a phone line in VSIP II, BIWASE had to size up its distribution network. Becamex, the industrial park developer, effectively became BIWASE's anchor tenant relationship. That symbiosis between land developer, industrial tenant base, and utility operator is the single most important structural feature of BIWASE's story, and it explains why the company's growth curve looks so different from a typical public-water utility in, say, Europe or the United States.

The critical insight is that in Binh Duong, water infrastructure was not a lagging indicator of growth. It was a gating one. If BIWASE had failed to build ahead of demand, the province's FDI narrative would have stalled. The political economy of the province therefore demanded a utility that could scale at the speed of a tech startup, but with the capital intensity and permanence of a Roman aqueduct. That is an unusual brief. It requires a management team comfortable borrowing in foreign currencies from development banks, willing to lay pipe to empty fields, and politically protected enough to earn an adequate return on that pipe once the factories arrive.

For two decades, BIWASE quietly executed that brief inside a state-owned shell. The real story, the one that matters for investors, begins when the shell finally cracked.

III. The Inflection Point: Equitization and the 2017 IPO

There is a specific kind of corporate chrysalis moment that happens only in transitioning economies. It is called equitization, Vietnam's local variant of privatization, in which a state-owned enterprise restructures into a joint-stock company, sells a slice of itself to strategic investors, and eventually lists on a public exchange. On paper, equitization is a legal formality. In practice, it is a personality transplant.

BIWASE's personality transplant began in 2016, when the company converted from a purely state-owned enterprise into Binh Duong Water – Environment Joint Stock Corporation. Shares began trading on the Ho Chi Minh Stock Exchange (HOSE) in 2017 under the ticker BWE3. The Binh Duong provincial People's Committee, through Becamex and affiliated entities, retained a controlling stake. But for the first time, there were outside shareholders in the room. For the first time, there were quarterly financials. For the first time, management had to stand in front of sell-side analysts and explain the difference between non-revenue water and capex accretion.

Why did this matter so much? Because the incentive structure inside a state utility is fundamentally about service continuity and political stability. You do not get promoted at an SOE for generating a high return on invested capital. You get promoted for not having a water-main break during a provincial party congress. Equitization, at its best, changes that calculus. When outside shareholders show up, so does an expectation of compounding. When debt gets priced by a public market instead of being allocated by a state bank, the cost of capital starts to bite.

The 2017 listing gave BIWASE its second identity: not just a service provider, but a capital allocator. The distinction is everything. Service providers build what they are told to build. Capital allocators decide what to build, when to build, and when to buy instead. Almost immediately after the IPO, BIWASE's capex cadence started to look less like a government five-year plan and more like the product roadmap of a private-sector operator trying to stay one step ahead of its largest customer.

The centerpiece of that capex cadence was the expansion of the Di An and Tan Hiep water treatment plants, the hydraulic backbone of southern Binh Duong. These plants drew raw water from the Dong Nai and Saigon river systems, treated it, and fed it into the industrial trunk lines. Capacity was expanded in stages well before nominal demand justified it, a classic build-ahead-of-the-curve move that is usually financially suicidal, unless you are confident the demand is going to show up. BIWASE was confident, because they could see the lease agreements Becamex was signing at the other end of the pipe. That information asymmetry, sitting inside the Binh Duong industrial ecosystem, was one of the first durable edges BIWASE developed over a generic utility investor.

Financing this build-out was its own clever piece of engineering. Vietnam's state-owned banking system could provide local currency debt, but the scale and tenor required for greenfield water plants were better served by multilateral lenders. BIWASE leaned heavily into Official Development Assistance (ODA) loans, particularly from the Japan International Cooperation Agency (JICA) and later the Asian Development Bank (ADB)4. These were long-duration, concessional loans, typically denominated in Japanese yen or US dollars, with interest rates that no commercial borrower in Vietnam could hope to match. The trade-off, of course, was currency risk. A yen-denominated loan is cheap when the dong is stable against the yen, and painful when it is not. We will come back to that in the bear case.

The point, for now, is that by the time BIWASE had been public for two or three years, the foundations of a different kind of company were visible. The balance sheet was bigger. The capacity was underutilized (on purpose). The management team was starting to think like owners rather than operators. And Binh Duong's FDI story, far from slowing down, was accelerating, as manufacturers fleeing rising Chinese labor costs and trade-war uncertainty poured across the border. The water pipes built in 2017 and 2018 were, by 2020, running closer to their design capacity than anyone had dared to forecast. That is the luxury of being right.

But being right in one province only gets you so far. By the early 2020s, BIWASE management was looking at a map and seeing something uncomfortable: Binh Duong was saturated. The compounding engine would need a new fuel. That realization is the bridge to the next part of the story, and it centers on a single man and his unusual way of thinking about a boring utility.

IV. Management and the "Thien" Era

Walk into BIWASE's headquarters in Thu Dau Mot and the first thing you notice is what is not there. There are no marble lobbies, no plaques announcing strategic partnerships, no glossy brochures about sustainability journeys. It is a working utility. The second thing you notice is that the person running it does not talk, dress, or behave like a typical utility bureaucrat. He behaves like a founder.

Mr. Nguyen Van Thien has been the defining figure of the BIWASE era, serving in senior executive and chairmanship roles through the company's transformation from provincial SOE to multi-province roll-up5. Thien's background is operational. He came up through the plants, through the pipes, through the unglamorous work of keeping water moving under pressure twenty-four hours a day. He is not an MBA. He is not a career politician. He is an engineer who learned capital allocation on the job, and his operating style reflects that. In investor meetings, colleagues describe him as quick with operational numbers and slow with promises. When he commits to a capex program, he tends to deliver it. When he commits to an acquisition target, he tends to close it.

The "founder-owner" label is not throwaway. Unlike many equitized Vietnamese SOEs, where professional management cycles through on five-year rotations, BIWASE's senior leadership has been remarkably stable, and compensation is structured with meaningful skin in the game through the joint-stock ownership structure. The effect is that decisions get made on a multi-decade horizon. You can see it in the willingness to take on foreign-currency debt in size, in the willingness to build ahead of demand, and, most visibly, in the willingness to deploy capital across provincial borders when the instinct of a typical local utility would be to stay home.

The second piece of the management puzzle is more subtle, and it is structural rather than personal. It is the relationship with TDM Water, ticker TDM on HOSE, a separately listed water utility focused initially on Thu Dau Mot and nearby areas6. BIWASE and TDM have a long-standing, cross-holding, symbiotic relationship: TDM is a significant shareholder in BIWASE, and BIWASE holds a substantial stake in TDM. The two companies share board members, coordinate on source-water arrangements, and operate in complementary geographies. To an outsider, this can look like an accounting curiosity. To an insider, it is an elegant governance arrangement that lets the broader BIWASE group pursue aggressive M&A while keeping each listed vehicle's balance sheet and governance discipline intact.

Think of it this way: if you want to buy a small water concession in another province, you can do it through BWE, or you can do it through TDM, or you can do it through a non-listed subsidiary of either. Each route has different implications for leverage, for minority investors, and for the group's blended cost of capital. Having two listed platforms is, in effect, having two different types of currency. BIWASE can use BWE shares when share-based consideration makes sense for a large deal, and it can use TDM when a smaller, more tightly-controlled platform fits the target. Most provincial water companies in Vietnam have exactly one of these tools. BIWASE has two, and it knows how to use them.

The third defining management trait is a near-obsessive focus on operational efficiency, measured most visibly through the metric every water operator hates to discuss in public: non-revenue water. Non-revenue water is the share of treated water that disappears between the plant and the meter, through leaks, theft, metering error, or unbilled municipal use. In poorly run utilities across emerging markets, non-revenue water routinely runs above thirty or forty percent. In BIWASE's core Binh Duong network, the company has historically reported non-revenue water rates in the single digits to low teens, comparable to well-run utilities in Singapore, Japan, and Northern Europe7. That is a stunning number. It tells you that behind the M&A glamour, there is an engineering culture that cares about pressure management, pipe replacement schedules, and the unsexy arithmetic of a utility that actually collects on what it produces.

That engineering culture, combined with Thien's founder-mindset and the dual-platform TDM structure, set the stage for what happened next: the moment BIWASE stopped being a Binh Duong story and became a Vietnam story.

V. The M&A Playbook: The Great Roll-Up

Every roll-up has an origin moment. For BIWASE, that moment was the quiet realization, somewhere around 2020-2022, that Binh Duong was running out of room. Not literally: the pipes still had decades of incremental demand ahead of them. But structurally, the province's market share math was tapped out. BIWASE already dominated the Binh Duong concession. Adding another industrial park customer was, at the margin, a 2% volume bump. The growth curve, in the provincial sandbox, was going to flatten.

Vietnam, thankfully, had a map. Fifty-plus other provinces, most of them served by local water companies that had been equitized at various points over the prior decade, trading at modest valuations, running with higher non-revenue water rates, lower capacity utilization, and weaker capex programs. Each one was, in its way, a candidate for what BIWASE had already mastered at home. Apply the operating playbook, refinance the balance sheet, build out the network, and harvest the efficiency gains. It was, in effect, a domestic emerging-markets roll-up, running on an operator's edge rather than a financial one.

The opening moves came in Long An Province, immediately west of Ho Chi Minh City, a fast-industrializing region with a patchwork of small, municipal-scale water operators. In 2023, BIWASE announced plans to acquire strategic stakes in multiple Long An water companies, an unusual, deliberately broad-based bid to consolidate the provincial market8. Instead of chasing one large target, the company moved on a cluster. The logic was the same logic Henry Singleton taught at Teledyne: in a fragmented market, the prize is not any single asset; it is the density. Own five small water companies in the same province and you can share treatment capacity, standardize billing, optimize pumping, and apply the BIWASE efficiency filter across all of them simultaneously.

Almost in parallel, the company expanded in Dong Nai, the industrial province just east of Binh Duong and home to its own sprawling FDI ecosystem, and in Quang Nam in central Vietnam, a province with a different growth story driven by tourism, light manufacturing, and a growing urban population around Da Nang9. The Quang Nam move was particularly revealing. For a company that had built its entire identity around industrial customers in the Saigon hinterland, pushing into central Vietnam signaled a willingness to underwrite a different kind of demand curve, anchored on residential and commercial growth rather than factory throughput.

The obvious question at this point is the one every skeptical investor asks of every roll-up: are they overpaying? The acquisition math in a regulated utility is always harder to read than in an unregulated business, because the "price" paid is not just the enterprise value; it is the blended cost of capital, the rate case trajectory, and the capex needed to bring the acquired network up to operating standards. What we can observe from disclosures is that BIWASE has tended to buy these provincial water companies at multiples that, on a replacement-cost basis, compare favorably to what it would take to build equivalent treatment capacity from scratch10. Put simply: buying a legacy water plant with an existing concession tends to be cheaper than greenfielding a new one, because the concession itself is often the scarcest resource.

Once an asset is inside the BIWASE tent, the playbook is consistent. Step one, drive down non-revenue water through targeted pipe replacement and pressure management. Step two, refinance the asset's debt, often leveraging the group's ODA relationships. Step three, expand the distribution network into underpenetrated zones. Step four, push the treatment plant closer to design capacity. Each of those steps is, on its own, a margin lever. Stacked, they turn a mediocre provincial utility into a contributor to group returns.

BIWASE is not, of course, operating in a vacuum. The Vietnamese water sector has its own emerging consolidator in DNP Water, a subsidiary of DNP Corp, which has been pursuing a similar roll-up thesis across different provincial clusters11. The competitive dynamic between BIWASE and DNP Water is worth watching, because it mirrors what happened in, for instance, the US cable industry in the 1990s or the Indian telecom tower industry in the 2010s. When two consolidators start chasing the same targets, pricing discipline gets tested. So far, BIWASE's preference has been to move in clusters where it can achieve operational density rather than to chase trophy assets across the country, and that discipline has, to date, kept its return on invested capital from deteriorating in the way that typical roll-ups do as they age.

The roll-up, impressive as it is, is still only one of the two narratives that define modern BIWASE. The other hides in plain sight on the income statement, under a segment that most analysts skim over and that, in the company's strategic vision, may end up generating the most interesting incremental returns of the next decade.

VI. The Hidden Businesses: Waste and the Circular Economy

When you scroll past the water segment in BIWASE's annual report, something unexpected appears: trucks, landfills, composting lines, an incineration plant, and a fertilizer brand with an elephant on the bag. It is, at first, jarring. A water utility owns a fertilizer business? A pipe company runs a waste-to-energy plant? Yes. And understanding why reveals the strategic imagination that separates BIWASE from a pure-play water utility.

The water supply segment is still the main engine, generating roughly two-thirds to three-quarters of revenue depending on the year, and more of the company's regulated asset base12. But the Waste Treatment and Fertilizer segment, smaller in absolute terms, has been growing faster, carries higher gross margins, and is less constrained by provincial water-price regulation. It is the segment where BIWASE gets to behave most like a private-sector operator rather than a regulated utility.

The origin story of this segment is almost accidental. Provincial governments in Vietnam, as they industrialize, inherit a massive solid-waste problem. Landfill space runs out. Informal dumps contaminate groundwater. Industrial parks generate waste streams that household municipal systems are not designed to handle. In Binh Duong, the provincial answer in the 2000s and 2010s was to bundle solid-waste management into the same vehicle that was already running the water system: BIWASE. The logic was operational, not strategic: both businesses required truck fleets, logistics networks, treatment facilities, and relationships with the same industrial customer base.

What started as a cost-plus municipal contract, however, quietly transformed into something much more interesting. BIWASE built composting and material-recovery facilities that began converting organic waste into agricultural inputs. Those inputs were branded and sold back into the market under the "Con Voi" ("Elephant") fertilizer line, which today is a recognizable brand in the southern Vietnamese agricultural sector13. The economics of this shift are fascinating. A utility that was previously paid to dispose of waste is now, on the same throughput, also being paid to sell a value-added product made from that waste. It is the cleanest example of circular-economy arithmetic you will find on a Vietnamese stock exchange.

Then came the capstone: waste-to-energy (WTE). In 2020, the Asian Development Bank signed a loan facility supporting BIWASE's expansion of municipal solid waste management infrastructure, including waste-to-energy capacity, one of the earlier large multilateral financings for this segment in Vietnam4. The facility generates electricity from non-recyclable combustible waste, reduces landfill volumes, and qualifies, under evolving Vietnamese environmental regulation, for premium tariffs and potential carbon-related incentives. From a strategic standpoint, WTE closes the loop. The waste stream now produces three outputs: electricity, fertilizer, and the regulatory reputational tailwind of being the province's "clean" waste solution.

Zoom out, and the vertical integration becomes obvious. BIWASE owns the water pipe that feeds the factory. It owns the sewer line that takes the effluent away. It owns the waste truck that hauls the solid garbage. It owns the composting yard that turns organic waste into fertilizer. It owns the incinerator that burns the rest. And it owns the turbine that spits electricity back into the grid. In a developed-market utility, these segments would likely live inside five different companies, each with its own listed equity and its own regulator. In BIWASE, they sit inside one balance sheet, cross-subsidizing one another through shared infrastructure, shared billing, shared customer relationships, and shared management bandwidth.

For investors, the implication is that BIWASE's economic engine is less like a pure regulated water utility and more like a diversified environmental-services conglomerate, with the water business providing the stable, bond-like base load, and the waste/WTE business providing a smaller but faster-compounding growth layer. The strategic risk, of course, is that ventures outside the core water business are always at higher risk of capital-allocation missteps. The saving grace, so far, has been that all of the adjacencies share the same underlying customer base and the same physical logistics network, which is exactly the definition of "within the circle of competence."

That question of circle of competence is the right bridge into a more formal analytical frame: how does BIWASE actually create and defend value, and what are the structural forces keeping new entrants out?

VII. The Playbook: 7 Powers and 5 Forces

Hamilton Helmer's framework of seven business powers is, for investors used to thinking about moats, a useful lens to stress-test BIWASE's durability. The company does not have all seven powers, but it has a striking concentration of the three that matter most for regulated infrastructure.

The first and most obvious is Cornered Resource. BIWASE holds the exclusive water-supply concession for Binh Duong Province, together with a large slice of its wastewater and solid-waste handling rights14. Those concessions are not traded in an open market. They are granted by provincial authorities, under a legal framework descending in part from Government Decree 117/2007 on clean-water production and supply, which established the regulatory scaffolding for investor-owned water utilities in Vietnam15. Within that province, there is no "second option." Geography is destiny, and BIWASE is on the right side of it.

The second power is Economies of Scale. Water treatment plants have enormous fixed costs and low marginal costs. Once the concrete is poured, the turbines installed, the pipes buried, each incremental cubic meter is essentially a variable-cost question. A competitor trying to attack BIWASE's Binh Duong footprint would need to build an entire parallel network, with parallel river intakes, parallel treatment capacity, and parallel distribution. That is a capex bill that rules out essentially every imaginable entrant, including very large ones. The same logic, on a smaller scale, applies in each province BIWASE consolidates.

The third power is Switching Costs. Once an industrial park is hooked into BIWASE's pipes, with meter relationships, cross-subsidized tariff structures, and emergency-response agreements, the cost of re-plumbing a factory to a different water source is effectively infinite. You do not move your semiconductor fab to a different water provider. You move your fab, period, and those decisions are made over years and capital cycles, not quarters.

The other four powers, counter-positioning, branding, process power, and network economies, are weaker or absent in BIWASE's case, which is what you would expect from a regulated utility. Process power does show up in the non-revenue water data: BIWASE has clearly built an engineering culture that extracts more from a given pipe network than most peers, and that skill is hard to replicate from outside. But you would not build an investment thesis on process power alone.

Porter's Five Forces round out the picture in the same direction. The threat of new entrants in the Vietnamese water utility sector is structurally near zero, because both the regulatory barriers (provincial concessions) and the capex barriers (greenfield plants) are prohibitive. The bargaining power of customers is low at the household level, and moderate-to-low at the industrial level, capped not by competition but by provincial price regulation, which is the binding constraint. The bargaining power of suppliers is mixed: domestic suppliers of pipes, pumps, and chemicals are plentiful, but energy costs and raw-water source rights are both policy-sensitive variables that can shift unpredictably. The threat of substitutes is low; you cannot substitute for piped water at industrial scale. And rivalry among existing competitors is, within any given provincial concession, essentially absent, while between consolidators like BIWASE and DNP Water at the national M&A level, rivalry is real but not (yet) value-destroying.

The net effect is that BIWASE sits inside one of the most defensible industry structures in Southeast Asia. The real risk to value creation is not that somebody takes the market away. It is that the regulator, or the macro environment, changes the economics of the market itself. Which brings us to the part where the bear case gets its day.

VIII. Bear vs. Bull Case

The bear case starts, as it always does for regulated utilities, with the regulator. Vietnam's provincial authorities set water tariffs through a formal process that, like most rate cases, tries to balance three goals: affordability for households, adequacy of returns for investors, and political stability. When any of those three pulls hard, tariff decisions can lag inflation. The single largest earnings risk for BIWASE is a multi-year tariff freeze during a period of high input cost inflation, which would compress gross margins on the core water business even as volumes continue to grow. This is not a theoretical risk; it has happened to water utilities in multiple emerging markets, and nothing about the Vietnamese regulatory structure rules it out.

The second bear-case risk is currency. BIWASE's capex program has leaned heavily on concessional ODA loans denominated in Japanese yen and US dollars4. When the Vietnamese dong weakens against those currencies, the dong-equivalent value of the debt grows, and the dong cost of servicing it grows with it. In years where the State Bank of Vietnam is defending the currency against global dollar strength, this can create sudden, visible FX-related hits to earnings. Management has historically mitigated this through a combination of natural hedges (local-currency revenues with long-duration, low-interest liabilities) and timing of refinancings, but the exposure is real and recurring.

The third bear-case risk is what we might call M&A indigestion. Roll-ups, as a class, are prone to a specific failure mode: the company grows faster than its ability to integrate, quality of acquired assets deteriorates, and returns on invested capital quietly erode while headline revenue growth continues. BIWASE's discipline so far has been impressive, but the further it expands from Binh Duong, the more the operational edge dilutes, and the more the thesis has to rest on governance and integration capability rather than pure local knowledge. A misstep in Long An, Dong Nai, or Quang Nam would not sink the company, but a pattern of misses could compress the group multiple meaningfully.

Layered on top of these specific risks are several broader overlays that deserve short mention. Climate and ESG considerations are rising globally and will increasingly touch water utilities, both as operational risk (drought frequency, raw water quality) and as financing tailwinds (green-finance instruments for WTE and sanitation). Vietnam's own climate vulnerability, particularly salinity intrusion in the Mekong Delta and the broader South, has direct implications for the raw-water quality BIWASE must treat. On the governance side, investors should track shifts in strategic shareholdings around BIWASE, Becamex, and TDM, because cross-holding structures like this one can be either accretive or dilutive depending on how related-party transactions are priced over time.

Now the bull case. Three pillars stand out.

The first is that Vietnam's FDI story is not over. Every major global manufacturer reviewing its China+1 or China+N supply chain strategy has Vietnam somewhere near the top of the list, and within Vietnam, Binh Duong and its neighboring industrial provinces dominate the shortlist. As long as that pipeline continues, the demand curve for industrial water in BIWASE's core markets continues to push outward. This is the simplest, most quietly powerful tailwind in the thesis.

The second is the waste-to-energy and circular-economy optionality. Unlike the water business, which is capped above by tariff regulation, the WTE and fertilizer businesses can participate in electricity pricing, in eventual carbon market mechanics, and in branded agricultural inputs. These are segments where BIWASE has already built capacity, relationships, and regulatory familiarity, and where upside is far less visible to consensus than the water story.

The third, and perhaps most investor-specific, is that BIWASE is one of the very few liquid, publicly listed ways for institutional capital to gain exposure to Vietnam's urbanization and industrialization story through a utility. Most FDI-linked exposures in Vietnam are either unlisted, concentrated in foreign multinationals, or mediated through industrial park developers whose own financials are messier. A listed, equitized, disciplined water-and-waste consolidator operating in the country's premier industrial province is a rare asset in the Asian emerging-markets universe.

If the thesis could be compressed into two or three key performance indicators that a long-term owner of BWE should watch, it would be these. First, non-revenue water rates, both in the core Binh Duong network and, critically, in the newly acquired provinces, because that number is the cleanest public readout of whether the operational playbook is actually traveling. Second, utilization of installed treatment capacity, which tells you whether the build-ahead-of-demand strategy is still being validated by FDI inflows. And third, the segment margin trajectory of waste treatment and WTE, which tells you whether the circular-economy narrative is translating into real, durable economics or remains a rounding error.

With those in hand, an investor can cut through most of the noise around quarterly fluctuations, currency swings, and acquisition announcements, and focus on whether the underlying compounding engine is still working.

IX. Myth vs Reality

There are three consensus narratives about BIWASE that deserve to be tested, because they get repeated in sell-side notes and investor calls without much scrutiny.

The first myth is that BIWASE is "just a Binh Duong story." That framing made sense in 2018. By 2026, with operational footprints spanning Long An, Dong Nai, Quang Nam, and others, it is materially out of date. The correct framing is that BIWASE is a multi-province consolidator whose operational center of gravity still sits in Binh Duong. Missing that distinction causes investors to under-weight the incremental growth runway from provinces where BIWASE currently has below-average market share.

The second myth is that water utilities are a "dividend play" and therefore inherently slow-growth. Most equitized Vietnamese water utilities are precisely that. BIWASE is not. The company has, for multiple consecutive years, reinvested a meaningful share of operating cash flow into capex and M&A rather than distributing it, and the compounding of book value and invested capital reflects that. Expecting BIWASE to behave like a European water dividend stock is a category error.

The third myth is that the waste segment is a rounding error or a distraction. At current group scale, it is small. At the direction of travel, it may be the most strategically important bet BIWASE has made since the 2017 IPO. The combination of waste-to-energy, fertilizer branding, and vertical logistics integration is exactly the kind of adjacency that compounds quietly for years and then, in a single regulatory or energy-price cycle, re-rates the parent's multiple.

What these myths have in common is that they compress BIWASE into the mental model of a generic utility. The company does not operate like a generic utility. It operates like a founder-owned environmental services platform that happens to sit behind a regulated water tariff. Getting that distinction right is the first job of any serious investor in the name.

X. Conclusion: The Next Era of Vietnamese Infrastructure

Step back, one last time, from the pipes and plants and acquisitions and ODA loans, and look at BIWASE from a distance. What you see is a company that took a specific local opportunity, the unique symbiosis between Binh Duong Province's industrial miracle and its need for reliable water and waste infrastructure, and compounded it into a national platform. Along the way it did three things most state-owned utilities fail to do. It built an engineering culture with genuine operational edge, visible in leakage and utilization numbers that would not embarrass a well-run Japanese or Singaporean peer. It built a governance structure, through the TDM cross-holding and the Thien-era management continuity, that lets the group allocate capital across borders and across segments with more agility than any single-province utility could muster. And it built a waste-and-energy adjacency that quietly converts the company from a pure-play water operator into a diversified environmental services group.

None of this guarantees continued compounding. Regulatory cycles bite. Currency shocks happen. Acquisitions fail. The bear case is not hypothetical; it is just priced. But for a long-term investor trying to find genuinely durable franchises in Southeast Asian infrastructure, BIWASE offers something rare: a legitimate moat, a real operator, an underpriced adjacency, and a liquid listing. Whether that combination is the "next era" of Vietnamese infrastructure or simply a well-executed provincial roll-up with national ambitions depends on decisions that will be made over the next several years, inside a building in Thu Dau Mot that does not look, from the outside, like the headquarters of a compounder.

Which is, if you think about it, exactly how the best ones usually look.

References

-

JICA and BIWASE: Cooperation in Water Infrastructure — JICA Vietnam ↩

-

ADB approves $20 million loan for BIWASE Waste-to-Energy project — Asian Development Bank, 2020-11-25 ↩↩↩

-

Nguyen Van Thien Profile & Shareholding — VNDirect Stock Archive / Vietstock ↩

-

The Relationship between TDM and BWE: A Structural Deep Dive — VietFirst Securities ↩

-

Vietnam Water Sector Report: The Consolidation Trend — Rong Viet Securities (VDSC), 2023-Q4 ↩

-

BIWASE's Acquisition of 5 Water Companies in Long An — CafeF, 2023-04-12 ↩

-

Biwase (BWE) Expansion into Quang Nam Water — Tin Nhanh Chung Khoan, 2023-09-20 ↩

-

Binh Duong Water (BWE) Strategy for 2024-2030 — Vietstock, 2024-03-15 ↩

-

Vietnam Water Sector Report: The Consolidation Trend — Rong Viet Securities (VDSC), 2023-Q4 ↩

-

Analysis of BWE's Waste Treatment Segment Growth — SSI Research, 2024-01-10 ↩

-

Analysis of BWE's Waste Treatment Segment Growth — SSI Research, 2024-01-10 ↩

-

Vietnamese Government Decree 117/2007 on Clean Water Production & Supply — Government of Vietnam ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube