The Story of Boxer Retail: Africa's Discount King

I. Introduction: The Crown Jewel Unleashed

Picture a township on the outskirts of Durban on a Saturday morning in November 2024. A young mother pulls up in a minibus taxi outside a store painted in that unmistakable red-and-yellow livery. She is carrying a Boxer Build paper bag with a bucket of paint from an hour earlier, a fistful of SASSA cash from a pension collection at the till, and she is about to load up a week's worth of mealie meal, frozen chicken, and a two-liter of Coke at a price that nobody else in South Africa can match. She does not know it, but the store she is walking into is, depending on how you squint at the numbers, the single most valuable retail property per square meter in the country.

For the better part of four decades, the conventional wisdom about South African grocery retail ran through a well-worn groove. If you wanted scale and African expansion, you bought Shoprite. If you wanted the premium, aspirational middle class, you bought Woolworths. If you wanted the old-money family business with nostalgic brand equity and deeply uncertain strategic direction, you bought Pick n Pay. And if you wanted convenience, you bought the franchisees of Spar. Inside one of those names, buried under layers of conglomerate accounting and a parent whose share price had been cut in half during 2023, sat a business growing the top line at roughly twenty percent compounded annually. It carried operating margins that were structurally higher than any meaningful competitor in its segment. It opened roughly one store a week. And almost no portfolio manager in Johannesburg or London owned it directly, because they could not.

That was, of course, the problem. And it was also the opportunity.

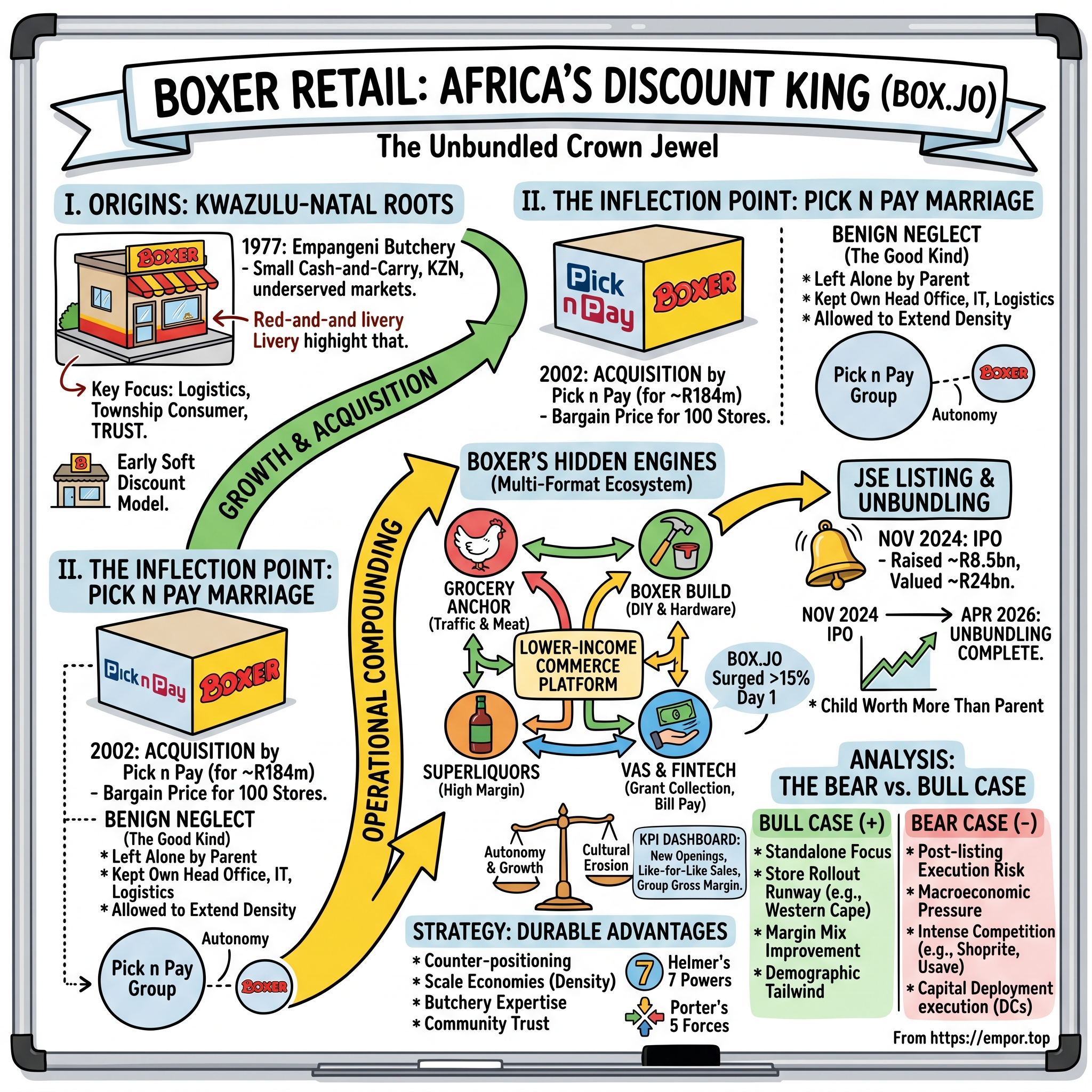

On November 28, 2024, Boxer Retail Ltd. debuted on the Johannesburg Stock Exchange after an IPO that raised roughly R8.5 billion at a listing price of R54 per share, valuing the company at approximately R24 billion. By the close of the first trading day, the stock had surged more than fifteen percent. Within weeks, Boxer was carrying a market capitalization that approached, and on some trading days exceeded, that of Pick n Pay itself, despite Pick n Pay still retaining majority ownership. The child, in other words, had become worth more than the parent before the parent had even finished handing over the keys. By April 2026, the unbundling was complete, and Pick n Pay shareholders held BOX.JO shares directly.

How did this happen? How does a soft discounter born in a small KwaZulu-Natal town in 1977, acquired in 2002 for what looked at the time like a reasonable regional acquisition price, become the single most valuable growth story in African food retail? Why did the market, almost the moment the S-1 landed, price Boxer at a premium multiple to every other listed South African retailer? And is this, as some of the more excitable sell-side analysts suggested in the weeks following the listing, the closest thing the continent has produced to an Aldi, a Lidl, or a Costco?

This is the story of how a butchery in Empangeni became the JSE's most closely watched retail name. It is a story about counter-positioning against entrenched incumbents, about a parent company whose single best strategic decision was to leave the child alone, and about the almost ruthless operational discipline required to sell food to the poorest segment of the market and still generate returns on invested capital that the wealthy chains can only dream of. The road from a single township butchery to a national powerhouse, from Empangeni to the Western Cape, runs through thirty years of patient density and one of the more instructive case studies in African business history.

II. Origins: The KwaZulu-Natal Roots

KwaZulu-Natal in the late 1970s was not the obvious place to build a retail dynasty. The province was caught in the economic and political cross-currents of apartheid-era South Africa, with the formal retail sector largely concentrated in Durban and Pietermaritzburg, and the vast hinterland of townships and rural settlements underserved by anything resembling a modern supermarket. Prices in the independent stores that did exist were often higher than those in the wealthier urban areas, for the simple and infuriating reason that the logistics were harder, volumes were lower, and the local retailers were typically running small, undifferentiated operations without meaningful buying power.

Into this environment, in 1977, a small cash-and-carry operation began trading in Empangeni, a town on the KwaZulu-Natal north coast that was then a trading hub for the sugar cane belt and surrounding rural communities. The early history of what would become Boxer has been told in fragments across company documents and press interviews, and the specifics of the very earliest years are, by the standards of the Shoprite or Pick n Pay origin stories, relatively sparsely documented. The company itself traces its lineage to this Empangeni operation and to the subsequent expansion of a small chain of stores through the 1980s and 1990s, built around a simple observation: if you could get the logistics right, the underserved township and rural consumer was not a marginal market. It was the market.

What crystallized during those early decades was a model that the company, and subsequently its post-listing investor relations team, has come to call "soft discount." It is worth spending a moment on this phrase, because it is doing a lot of work in the Boxer thesis. Hard discounters, in the global retail vocabulary, are the Aldis and Lidls of the world: ruthlessly narrow assortments, typically under two thousand SKUs, heavy private label, spartan store environments, and a relentless focus on price. Full-service supermarkets sit at the other end, with tens of thousands of SKUs, full fresh and bakery departments, in-store service counters, and the kind of ambient lighting budget that discounters would consider heretical.

Soft discount sits deliberately in between, and in Boxer's case, it is tuned with almost surgical precision to the profile of the South African lower-income household. The stores carry a curated assortment that is smaller than a Shoprite or Pick n Pay but meaningfully larger than a European hard discounter. The private label penetration is significant but not dominant. The store fit-out is functional, not austere, because South African township and rural shoppers are not, in the main, looking for ostentatious cheapness. They are looking for trust. And trust, in this segment, is built on three things: fresh meat, consistent pricing on staples, and the dignity of a well-run store.

That last word, meat, is worth lingering on. The butchery is to Boxer what the rotisserie chicken is to Costco, and the comparison is not as flippant as it sounds. From the earliest Empangeni days, the butchery department was positioned as the gravitational center of the store. It was the traffic driver, the margin anchor, and the competitive differentiator all in one. In a market where informal butchers and supermarket meat counters varied enormously in quality and price, the Boxer butchery became a known quantity, and in many of the communities the chain served, it became the butchery of record. Walk into a Boxer store today and you can still see the architectural echo of that founding decision: the butchery is typically placed deep in the store, forcing a full trip past the staples to reach it, and the meat assortment runs from the high-velocity braai cuts to the cheaper stewing portions that drive weekday volume.

The other inheritance from these founding decades is a particular relationship to SKU management. Because the early Boxer stores were often constrained by physical size, remote locations, and tight working capital, the operators developed an almost obsessive focus on velocity. SKUs that did not turn were cut, quickly. Seasonal pricing was driven by what the local supplier base could produce at scale, not by centrally-planned catalogs. The stores learned to read their communities week by week. By the time Pick n Pay came knocking in the early 2000s, this operational culture was already baked into the cement of every distribution center and store.

That operational DNA, more than any single founder story or early expansion milestone, is the thread that runs through everything Boxer has done since. It is what made the business attractive to Pick n Pay in 2002, and it is what made the standalone listing in 2024 possible as a thesis in its own right.

III. The Inflection Point: The Pick n Pay Marriage

In 2002, Pick n Pay was the bluest of South African blue chips. The Ackerman family's group carried the aura of Raymond Ackerman's founding philosophy, a conscious echo of Sam Walton's "customer sovereignty" with a distinctly South African social conscience attached. The group was listed, well capitalized, and hunting for growth beyond the saturated LSM seven-to-ten suburban market that had defined its first four decades. Boxer, at that point operating around a hundred stores concentrated in KwaZulu-Natal and the Eastern Cape, fit the strategic brief almost too neatly: a lower-income-segment chain, already profitable, with a ready-made operating team and a regional density that Pick n Pay itself could never easily replicate organically.

The acquisition closed for a price that has been variously reported at around R184 million. Run that through any reasonable multiple of the earnings Boxer was generating at the time, and the deal was, even by the standards of early-2000s South African M&A, an extraordinary bargain. For context, consider what soft-discount assets were commanding elsewhere in the world. Aldi and Lidl were, of course, private, but the implied multiples embedded in public hard-discount peers globally were trading well north of what Pick n Pay paid. And for a business growing organically at the double-digit pace Boxer was already running, paying what amounted to a mid-single-digit EBITDA multiple was, in hindsight, one of the most value-accretive deals in South African retail history.

But the more interesting story is not the price. It is what Pick n Pay did, and more importantly did not do, in the two decades that followed.

The conventional playbook when a large corporate acquires a scrappy regional operator goes something like this. You centralize the merchandising. You migrate the acquired chain onto the parent's ERP system. You fold the distribution network into the parent's logistics backbone to capture "synergies." You align the HR policies, the uniforms, and often, eventually, the signage. The acquired brand becomes a facia of the parent, sometimes surviving for a while as a differentiated format but increasingly looking, smelling, and feeling like the rest of the portfolio. Pick n Pay, in the 2000s, could easily have done this. It had the management bandwidth, the IT systems, and the corporate instinct for order.

Instead, it did something close to nothing.

Boxer was allowed to keep its own head office in Westville, KwaZulu-Natal. It kept its own buying team, its own supplier relationships, its own distribution centers, its own store development discipline, its own IT stack. Pick n Pay consolidated at the group level for reporting purposes, but the operational cord was, for all practical purposes, never tied. For years, analysts covering Pick n Pay would note, almost as a footnote, that "Boxer continues to grow well," without seeming to understand quite how well, or why.

The why, when you sit with it, is almost counterintuitive. Pick n Pay's wealthier-segment expertise was, in many ways, actively unhelpful for running a soft discounter. The merchandising logic, the promotional cadence, the supplier negotiation style, even the store layout philosophy, were tuned for a fundamentally different customer. Had Pick n Pay integrated Boxer, it would have almost certainly diluted the operating model that made Boxer valuable in the first place. The decision to leave it alone, whether made deliberately or simply by benign neglect, turned out to be one of the most important capital allocation decisions Pick n Pay made in the entire 2000s and 2010s.

Meanwhile, Boxer used those two decades of autonomy to do what it had always done: extend density. Through the early 2010s, the chain pushed beyond its KwaZulu-Natal stronghold into the Eastern Cape, where the demographic profile was a near-perfect fit. It then began to move into the townships around Johannesburg, into Mpumalanga, into Limpopo. Every new store opening was, in some sense, an incursion into what had been considered Shoprite territory, specifically the turf of Shoprite's own entry-level format, Usave, which was supposed to own the bottom-of-pyramid positioning for the group. Boxer's stores were larger than Usave's typical box, carried a fuller assortment, and crucially, had the butchery anchor that Usave could never quite replicate at its price point.

By the late 2010s and into the early 2020s, Boxer was no longer a regional operator that happened to be owned by Pick n Pay. It was, by most meaningful operational metrics, the fastest growing large-format grocery chain in the country, and arguably on the continent. Pick n Pay itself, during this same period, was sliding into a very public operational and financial crisis, culminating in a rights issue and the strategic review that would ultimately force the Boxer separation. The parent company's core supermarket business was under severe competitive pressure, its balance sheet was strained, and the board needed a capital event.

The "family silver" metaphor that ran through the South African press in 2024 was, in that sense, both accurate and slightly misleading. Accurate, because Boxer was unquestionably the crown jewel of the Pick n Pay estate. Misleading, because the silver had, by the end, grown so heavy that the family could no longer afford to keep it unlisted.

IV. The "Hidden" Engines: More Than Just Groceries

If you were to ask a casual observer of South African retail what Boxer sells, you would get a fairly predictable answer: groceries, cheap, in townships, with a good butchery. That answer is not wrong. It is just significantly incomplete. The full Boxer network, by the time of the listing, had evolved into something closer to a multi-format ecosystem serving a single, deeply understood customer segment, and the non-grocery formats are where the most interesting unit economics, and arguably the most durable competitive moats, actually live.

Start with Boxer Build. On paper, this is a DIY and hardware format, but to describe it that way is to miss the structural logic. Across much of rural and peri-urban South Africa, the availability of formal hardware retail is sparse. Large-format players like Builders Warehouse and Cashbuild have been present, but their footprints are tilted toward larger towns and more formalized trade catchments. In the townships and in the smaller rural centers, a shopper looking for a roll of fencing wire, a bag of cement, a bucket of PVA paint, or a basic plumbing fitting has historically been stuck with informal hardware outlets of highly variable quality and pricing. Boxer Build inserted a formal, price-disciplined hardware format into exactly those gaps, and often co-located them next to the grocery store, allowing shoppers to do a grocery shop and a home improvement run in a single taxi trip.

The synergy here is more than cosmetic. The grocery store brings the footfall. The hardware store monetizes a basket that, per visit, is often three or four times the size of the grocery basket, with materially higher margin on categories like paint, electrical fittings, and bulk building materials. And because Boxer Build leverages the same distribution backbone as the grocery network, the incremental fixed cost of adding the format is modest relative to what a standalone hardware chain would have to invest. It is, in essence, the closest thing in South African retail to the Costco business-membership cross-shop dynamic, tuned for the opposite end of the income spectrum.

Then there is Boxer Superliquors. The South African liquor license regime is, for reasons both regulatory and historical, one of the more Byzantine in the retail world. Licenses are typically tied to specific physical premises, are granted through provincial liquor boards, and are subject to a set of zoning, community consultation, and operating hour rules that make obtaining new licenses, particularly in the lower-income catchments where the demand is strongest, a slow and politically fraught process. For years, the large grocery chains have been fighting, winning, and sometimes losing battles to attach liquor stores to their supermarket footprints, because the format is, for anyone with the scale to negotiate liquor supplier terms, highly profitable.

Boxer's strategy here was to treat the liquor license itself as a strategic asset. The Superliquors footprint expanded aggressively through the 2010s and into the 2020s, leveraging the grocery store catchments as anchor locations and the group's operational credibility with provincial regulators. The result is a liquor business that, by industry convention on gross margin and cash conversion, is a meaningfully higher-margin contributor per square meter than the grocery core. Importantly, it also serves to deepen the customer relationship: a shopper who does groceries, liquor, and hardware at the same set of stores every week has, in the academic language of retail, a dramatically higher share of wallet and a correspondingly lower propensity to defect to a competitor.

The third leg, and the one that gets underplayed in most discussions of Boxer, is the fintech and value-added services business embedded inside every store. In South Africa, the tills of large supermarket chains have, over the past fifteen years, become an essential layer of the country's informal financial infrastructure. Recipients of SASSA grants, which cover pensions and child support across millions of households, can collect their payments at supermarket tills. Prepaid electricity and airtime, bill payments to utilities and municipalities, remittances to neighboring countries, and basic money transfers all flow through the till. For the retailer, these transactions generate small, high-frequency fee income with essentially zero incremental inventory risk.

For Boxer specifically, the VAS business is disproportionately important for two reasons. First, the customer overlap with grant recipients is near total in many of the stores. When a shopper comes in to collect a grant, they are a captive audience for the grocery, hardware, and liquor formats all at once. The cross-pollination is structural. Second, these services build a kind of quiet switching cost. A shopper who has standardized their monthly bill payments, their money transfer flows, and their grant collection at a particular Boxer is simply less likely to defect, even if a competitor opens a store with marginally better pricing on a single basket.

Put the four pieces together, grocery, Build, Superliquors, and VAS, and what you have is not really a discount supermarket chain. It is a lower-income-segment commerce platform with the grocery anchor as the traffic engine and the ancillary formats as the margin amplifiers. The competitive implication is that any rival looking to attack Boxer's position has to compete, simultaneously, on four different formats in the same geography. Shoprite can match the grocery. Builders can match the hardware. Tops can match the liquor. Nobody, at present, combines all four with the same catchment density, and that is what investors were pricing when the stock opened to cheers on the JSE.

V. Current Management: The "Lifer" Culture

One of the more telling details in Boxer's pre-listing documentation was the tenure of its senior management team. In a South African retail industry where CEOs have come and gone with depressing regularity over the past decade, the Boxer leadership had the quality of a group that had built the thing they were now being asked to list. Anthony Sideris, the CEO, had been with the business for roughly three decades by the time the IPO bell rang. He had come up through the operational ranks, knew the store base in the kind of granular detail that only comes from having walked most of it personally, and was, by all accounts, not the kind of executive one was likely to find at the Sandton lunch circuit.

The contrast with the turmoil at the parent Pick n Pay during the same period was stark. Pick n Pay had cycled through a series of strategic pivots and executive changes in the early 2020s, including the return of Sean Summers as CEO in 2023 after more than two decades away, in a very public attempt to rescue the core supermarket business. While that drama played out in the Cape Town head office and across the financial press, Westville kept running. Boxer continued to open stores, continued to grow same-store sales, continued to push the distribution network deeper. The organizational distance between the two businesses, preserved through the twenty-year "hands-off" era, had paid its clearest dividend precisely when the parent was at its most distracted.

What defines the "Boxer Way" internally, according to the accounts that have surfaced in pre- and post-IPO interviews, is a combination of flat structure, operational intimacy, and what might be called a cultural allergy to corporate abstraction. Senior executives spend meaningful time in stores rather than in boardrooms. Buying teams are expected to know the supplier bases not just at a corporate level but at the level of specific regional relationships. The head office, such as it is, functions more as a services layer for the store network than as a command-and-control center. Decision-making, particularly around range, pricing, and local adaptation, sits closer to the store than is typical at the larger incumbents.

This matters for a very practical reason. Soft discount retail, done well, is a margin-accretive model only so long as the cost discipline is enforced relentlessly at every level of the organization. The difference between a soft discounter that compounds capital and one that gradually drifts into being a mediocre full-service supermarket is not strategy, it is execution. Every additional layer of middle management, every head office function that grows faster than the store base, every procurement decision that prioritizes sophistication over price, is a small leak in the hull. The companies that have maintained the discipline over decades, Aldi, Lidl, Costco, Trader Joe's, have done so through a cultural stringency that is, in the specific idioms of retail, almost religious. Boxer, in the accounts of those who know it well, carries a version of that stringency.

The unbundling created an important secondary effect on this culture: it finally aligned management incentives with the business they had built. Under Pick n Pay, equity-linked compensation was denominated in Pick n Pay shares, which meant that the Boxer leadership's financial upside was tied to a parent whose core supermarket business was, for much of the period, deeply troubled. The performance of Boxer was partially washed out in group numbers that told a much more mixed story. With BOX.JO as a standalone listed entity, management incentives are now tied to the performance of the business they actually run. For a leadership team that has spent thirty years building operational value that was, to some extent, obscured within a larger conglomerate, this is a meaningful and long-overdue change.

There is a second, subtler effect, which has to do with talent retention. Ambitious retail operators, particularly in a market like South Africa where senior operational talent is in short supply, respond to equity stories. A Boxer manager who, five years ago, might have looked at a Pick n Pay stock option package and wondered whether the group's turnaround would ever deliver real upside, now has a direct claim on the value of a business growing at rates the JSE has rarely seen in consumer staples. The IPO, in that sense, was not just a capital event. It was a talent-retention tool dressed up as a capital event.

For long-term investors, the obvious follow-on question is whether the culture survives the scrutiny of public markets. JSE Top 40 darlings do not, historically, remain scrappy for very long. The next section touches on this, but it is worth flagging here: the single biggest operational risk at Boxer over the coming decade is not competitive, regulatory, or macroeconomic. It is cultural. The "Boxer Way" is the moat. Erode it, and the rest follows.

VI. Capital Deployment & The Competitive Benchmarking

Every retail chain is, eventually, a capital deployment story. Shareholders make or lose money not primarily on same-store sales growth in any given year, but on the cumulative returns the business earns on the capital it plows into new stores, distribution centers, systems, and working capital over a decade. In South African grocery retail, the benchmark for what "good" looks like on the ROIC front has, for much of the past twenty years, been set by Shoprite. The question for Boxer, and the one that matters most for the long-term thesis, is whether it can continue to deploy capital at rates that improve on, rather than regress toward, the industry mean.

The starting point is the store rollout itself. Boxer's new-store economics have, by most accounts, been favorable compared to peers for a fairly specific set of reasons. The target store format is smaller in square meterage than a full-service Pick n Pay or Checkers supermarket, which directly reduces the capital per store. The fit-out is deliberately functional, meaning no marble, no ambient mood lighting, no in-store bakery theatre. The IT stack, tuned to the specific needs of the format, is less feature-rich than the top-end supermarkets require. And crucially, the customer behavior in the target catchments tends to support faster ramp-up to mature store sales, because the demand in many of the communities where Boxer opens is effectively pent up.

The second pillar is inventory velocity. In a low-gross-margin business, the single most important operational lever is how fast inventory turns. Every additional stock turn is, functionally, an additional gross profit cycle on the same invested working capital. Boxer's SKU discipline, inherited from the Empangeni-era operational culture, translates into stock turns that are materially higher than a full-service supermarket. The soft-discount format's narrower assortment is not a cost-of-goods story, it is a working-capital story. Fewer SKUs, higher velocity per SKU, lower days of inventory on hand, more gross profit cycles per year on the same rand of invested capital.

The third pillar, and the one that generated the most debate in the sell-side notes around the IPO, is the distribution infrastructure. The company has invested materially in new distribution centers to support the national rollout, including the Shongweni DC in KwaZulu-Natal. DC capex is the single largest line item in a grocery retailer's capital plan in any given expansion phase, and the returns on that capex are heavily dependent on throughput ramp and the pace of store openings in the catchment area. Overbuild too early, and you carry years of underutilized fixed cost. Underbuild, and you bottleneck the store rollout at exactly the moment when your competitors are watching for weakness.

Whether Boxer overspent on Shongweni is a question that genuinely has not yet been answered by the numbers. The bullish view is that the DC footprint is sized for a store base materially larger than the one currently operating, meaning that the fixed cost dilution will work in Boxer's favor as the rollout continues. The bearish view is that DCs are lumpy, rand-intensive assets, and that any slippage in store-opening pace directly pressures group returns. The honest answer is that the market will know which view is correct only after three or four more years of data. For now, management's disclosures on DC utilization and phased expansion will be among the most important metrics for investors to track.

The comparative picture against Shoprite's Usave and Spar's Build it formats is instructive. Usave, the entry-level Shoprite format, was for years considered the natural champion of the lower-income South African grocery segment. But Usave's store format, tuned for a smaller basket and narrower assortment, has consistently lost share to the larger and more meat-anchored Boxer box in communities where both formats compete. Usave's economics per store are reasonable, but the format does not support the cross-shop ecosystem that Boxer Build and Superliquors layer onto the grocery anchor. Spar's Build it, similarly, is a strong regional hardware player but operates under a franchise model that structurally limits central control over ranging and pricing, which in turn limits the working capital efficiency that a corporate-owned chain like Boxer Build can extract.

What all of this adds up to, in the language of fundamental investors, is a return on invested capital profile that sits structurally higher than the industry norm, driven by lower capital intensity per store, higher inventory velocity, and a multi-format cross-sell that amplifies the productivity of each square meter of retail space. Whether that ROIC premium can be defended over time is, fundamentally, the central question the market is pricing when it assigns Boxer its current multiple.

VII. Strategy: Hamilton's 7 Powers & Porter's 5

Good strategy, in the Hamilton Helmer sense, is the ability to explain why an incumbent earns superior returns in a way that survives hostile competitive action. The Boxer case, run through the 7 Powers framework, reveals a set of advantages that are unusually durable for a retail business in an emerging market.

The most visible power, and the one most relevant to the founding logic of the business, is counter-positioning. For thirty years, the Big Three South African grocery retailers, Shoprite, Pick n Pay, and Spar, competed most intensely for the wealthier, more urbanized consumer. Even Shoprite, despite its African expansion and its broad footprint, focused its core brand investment on the middle-class LSM seven-plus supermarket shopper. The lower-income segment was served, but it was not the strategic priority of the main brand. Boxer built its entire operational culture, store format, and supply chain around the segment that the incumbents were servicing as an afterthought. Counter-positioning is at its most powerful when the incumbent cannot replicate the challenger's model without damaging its own core economics, and that dynamic applies here with particular force. A Pick n Pay store cannot become a Boxer store without destroying the brand equity that Pick n Pay's core customer is paying for. The incumbents are trapped, structurally, in their existing positioning.

The second power is scale economies, expressed most precisely as density. Boxer's advantage is not national scale in the sense that Walmart has national scale. It is regional density in the specific catchments it serves. In KwaZulu-Natal, in the Eastern Cape, and increasingly in Gauteng and Mpumalanga, the density of Boxer stores per demographic catchment has reached a level at which the distribution network can be operated at costs per store that a lower-density competitor simply cannot match. Density, in grocery retail, compounds. Every additional store in a region reduces the average delivery cost per store, enables more frequent replenishment, improves fresh-category economics, and tightens the supplier relationships. This is exactly the advantage that Walmart built in rural America, that Costco built in warehouse catchments, and that Dollar General has built in the U.S. low-income segment. It is not a flashy advantage, but it is among the most durable any retailer can accumulate.

The third power is what Helmer would call cornered resource, and in Boxer's case it comes in two flavors. The first is butchery expertise, embedded in the operating model and in the specific supplier relationships the company has cultivated in the South African protein supply chain. The butchery is the single largest point of category differentiation in the store, and replicating it requires not just equipment and training but a decade or more of supplier development. The second is community trust, which sounds soft but in practice is the most durable moat a lower-income retailer can build. In markets where the formal banking system, the government service infrastructure, and the broader formal economy have historically failed many of the communities Boxer serves, a supermarket that has consistently delivered on price, quality, and service over twenty or thirty years has accumulated a kind of trust capital that a new entrant cannot buy in any finite time frame.

Running the Porter's Five Forces analysis over the business produces a picture that is, by the standards of the retail industry globally, unusually favorable.

Bargaining power of buyers is, counterintuitively, lower at Boxer than at a more upscale competitor. The wealthy South African consumer has easy access to four or five different supermarket chains within a short drive, has the financial flexibility to chase promotions, and has effectively zero switching cost. The Boxer consumer, by contrast, shops within a much tighter physical and economic radius. The nearest alternative is often meaningfully less convenient, price discovery across chains is more limited, and the bundle of grocery, hardware, liquor, and VAS services that Boxer offers is genuinely hard to replicate in a single trip anywhere else. The outcome is that Boxer's customer loyalty, measured by basket frequency and retention, tends to be higher than at the wealthier chains, which is a kind of structural anomaly that most retail investors find counterintuitive.

The threat of substitutes is the one that gets the most attention, and it centers on the spaza shop. South Africa's informal retail sector, spaza shops, street traders, and the like, is massive and deeply embedded in the country's township economies. For years, the conventional wisdom was that formal retailers like Boxer and Shoprite would cannibalize spaza shops, driving them out of existence. The reality has been more interesting. Boxer has co-opted the informal sector as much as competed with it. Spaza operators often buy their own inventory at Boxer Cash and Carry formats, effectively using the chain as a wholesale supplier. Rather than being the enemy, the informal sector has become part of the customer base. This is a far healthier dynamic than the zero-sum framing would suggest.

The threat of new entrants, particularly international entrants, is low for reasons that are partly regulatory and partly structural. South Africa's liquor licensing regime, its complex zoning and community consultation rules, and the sheer operational difficulty of running a low-margin chain in a high-crime, logistically challenging market have deterred meaningful international entry. Shoprite and Pick n Pay have tried to expand into the rest of Africa with mixed results, suggesting that the reverse flow, an international chain entering South Africa, would be even more difficult. Supplier bargaining power is moderated by the scale Boxer has now reached in its core categories. Internal rivalry is intense but fought on terrain where Boxer has structural advantages.

For a business operating in an industry that is, globally, among the most competitive and margin-compressed, this is an unusually attractive strategic position.

VIII. Analysis: The Bear vs. Bull Case

The bull case on Boxer, stripped to its essentials, rests on four pillars. First, standalone focus. The separation from Pick n Pay has removed a group-level overhang that, fairly or not, had been dragging on investor sentiment for years. Capital allocation decisions can now be made on the basis of Boxer's own return profile, not group-level constraints. Second, store rollout runway. The current store base is heavily concentrated in KwaZulu-Natal, the Eastern Cape, and Gauteng. The Western Cape, a province with significant demographic and economic weight and where Boxer's footprint has historically been sparse, represents a genuine white space. Rolling out the proven format into a new province at the rate the company has demonstrated elsewhere extends the growth runway by several years at least. Third, margin mix improvement. As Boxer Build and Superliquors continue to scale as a percentage of group revenue, and as the VAS business contributes increasing fee income, the group-level margin profile has room to improve beyond what the grocery-only comparison would suggest. Fourth, and most importantly, the demographic tailwind. The lower-income South African consumer segment, despite macroeconomic pressure, has been growing in absolute terms for decades, and formal retail penetration within that segment remains well below what it is in the wealthier LSMs.

Against this, the bear case is real and worth taking seriously. The first and most immediate risk is post-listing execution. Newly listed companies, particularly those that have been insulated from public-market scrutiny for decades, face real pressure to meet quarterly expectations, and the gap between quarterly pressure and the patient operational compounding that built Boxer is precisely where cultures erode. The second is macroeconomic. South Africa's consumer environment remains fragile, with high unemployment, persistent load-shedding pressure on consumer budgets, and a rand that has provided little comfort on imported input costs. Even a best-in-class discounter is not immune to a deep consumer recession, particularly one that impacts the lower-income segments most directly. The third is competitive. Shoprite, with its scale, capital, and operational sophistication, is not going to cede market share in the lower-income segment without a fight. The company's existing Usave format, combined with potential investment in new entry-level concepts, could materially pressure Boxer's incremental unit economics in the markets where the two directly compete. The fourth is execution on the capital program. DC capex and store rollout are lumpy, and any meaningful slippage on either could pressure the group's capital efficiency ratios in a way that the market would punish given the current valuation.

There is also a set of second-layer considerations that long-term holders should keep on the dashboard. Regulatory pressure on the liquor category, which has been a recurring feature of South African political discourse, could constrain growth in the Superliquors footprint. Climate-related risk to the agricultural supply chain, particularly on fresh protein and produce, has the potential to disrupt input costs in a way that is difficult to hedge operationally. The ESG overlay, while not acutely material at present, is worth monitoring given the intensity of the global debate around retailers' obligations to their workforces and communities. Accounting judgments around the unbundling transaction itself, including any one-time separation costs that bleed into early post-listing periods, need to be read carefully in the first couple of reporting cycles.

On the positive side of the second-layer ledger, there are some interesting optionalities. The company's dominance in lower-income South African retail positions it reasonably well for eventual, careful expansion into neighboring Southern African markets, where demographic profiles are similar and formal retail penetration is even lower. Fintech and digital payments, which in South Africa have been evolving rapidly through initiatives like PayShap and the expansion of mobile money services, present opportunities to extend the VAS platform in ways that are not priced into the current consensus view. And the private-label opportunity, which at Boxer has been pursued less aggressively than at some European hard discounters, represents a lever that future management teams may choose to pull if grocery gross margin needs a boost.

For investors trying to build a KPI dashboard to track Boxer over the coming years, a narrow list stands out. The most important single metric is new store openings per period, measured net of any closures, because the rollout pace is the single biggest driver of group revenue growth and of the returns on the capital program. The second is like-for-like sales growth in the mature store base, which is the best single read on whether the core format is gaining or losing share in its catchments. The third is group gross margin, which captures the interplay between the grocery anchor's pricing discipline and the mix contribution from Build, Superliquors, and VAS. Other metrics matter, including inventory days, DC utilization, and capital intensity per new store, but if an investor forced you to watch just three, those are the three.

The deeper question, the one that the "Acquired grading" framing invites, is whether Boxer deserves to be regarded as the best retail business in Africa. That is a question where reasonable people can disagree, and where the answer depends heavily on what time horizon you apply and what weight you give to the cultural-risk argument. What is harder to dispute is that it is, at present, the most operationally differentiated listed retail asset on the JSE, with a strategic positioning that is unusually hard to replicate and a growth runway that is unusually long.

IX. Playbook: Lessons for Founders & Investors

Every good business case study leaves a few transferable lessons behind, and Boxer is unusually rich on this front. Three stand out.

The first is the "isolation" lesson, learned in reverse by Pick n Pay and validated by Boxer's twenty-year run inside the group. When a large corporate acquires a high-performing regional operator, the instinct to integrate, standardize, and optimize is almost irresistible. It feels like good management, and it is certainly good governance in the narrow sense. But it is often catastrophic for the acquired asset. The specific operational culture, supplier relationships, and customer intimacy that made the target attractive in the first place are, almost by definition, the things most likely to be damaged by integration. The Pick n Pay decision to let Boxer run itself for two decades was, with the benefit of hindsight, the best capital allocation decision the parent made in the entire period. The lesson for founders selling into a larger corporate is to negotiate hard for operational autonomy, preferably with contractual protections. The lesson for acquirers is to keep the hands off the steering wheel even when the instinct is to grab it. And the lesson for investors is to watch for the tell-tale signs of integration-induced value destruction after any acquisition, and to reward management teams that resist the temptation.

The second is the logistics lesson. In any physical retail business, the strategy is the logistics. You can have the most elegant store format in the world, the most sophisticated pricing algorithms, the most beautiful brand identity, and if your distribution backbone cannot keep fresh product on shelf at the right price in the right places, none of the rest matters. Boxer's three decades of compounding came from the fact that the logistics were, at every point, the first priority. Density in catchments was pursued because it reduced distribution costs. Distribution centers were built ahead of demand in the regions the company chose to prioritize. Supplier relationships were cultivated in ways that gave the company control over the flow of product at the specific quality and price points the format required. For founders in any physical goods business, the lesson is that logistics is not a back-office function. It is the strategy.

The third is the bottom-of-pyramid lesson, and it is the one that most challenges the conventional business school framing. Serving the lower-income consumer is, in most globalized economies, considered a low-margin, low-return proposition. The narrative assumes that wealth correlates with willingness to pay, which correlates with margin, which correlates with returns. Boxer's record, alongside global parallels at Dollar General, Aldi, and the rotisserie-chicken-anchored Costco model, disproves the framing. Serving the lower-income consumer well is not charity. It is, when done with the right cost structure and the right operational discipline, among the most profitable businesses anywhere in the world. The reason is that the structural customer loyalty is higher, the demand is more resilient across cycles, the competitive landscape is less crowded with well-funded rivals, and the ability to cross-sell ancillary formats and services is, if you have earned the trust, extraordinarily high. For founders deciding which segment to serve, and for investors deciding where to allocate capital in retail, the Boxer case is a standing reminder that the highest returns are not always found at the top of the income distribution.

There is a fourth, slightly more subtle lesson, which is about patience. Boxer took close to fifty years to get from a single Empangeni store to the IPO bell on the JSE. During most of that time, the business compounded quietly inside a parent that did not fully understand what it had. There were no hockey-stick moments, no viral brand campaigns, no single deal that transformed the trajectory. What there was, year after year, was another twenty or thirty or fifty new stores, another distribution center, another supplier relationship deepened, another catchment saturated. For founders raised on the Silicon Valley grammar of rapid disruption, this kind of slow compounding can look almost boring. It is, nonetheless, how the most durable physical-world businesses get built.

X. Epilogue

Sitting in April 2026, with the unbundling now complete and Boxer operating as a fully independent JSE-listed entity, the question the company's investors are turning over is not whether the rollout continues in the home market. That question answers itself for at least the next three to five years, given the Western Cape runway, the continued migration of demographic growth into the peri-urban catchments Boxer specializes in serving, and the multi-format cross-sell story that remains only partially monetized. The more interesting question is what comes next after the South African map is broadly filled in.

The Pan-African expansion question will, sooner or later, become unavoidable. Shoprite has spent two decades learning, sometimes painfully, that African expansion is not a simple extension of the domestic playbook. The most natural geographies for Boxer, neighboring markets with similar demographic profiles and underserved formal retail sectors, carry their own regulatory, currency, and operational risks. Management has, so far, been publicly disciplined in its messaging on this question, emphasizing the domestic growth runway ahead of any cross-border ambition. That discipline has been rewarded by the market. Whether it can be maintained as the domestic rollout matures is among the most important strategic questions of the next five years.

The other axis of evolution is digital. The South African consumer, across income segments, has been moving online more quickly than the broader formal retail sector has sometimes appreciated. Delivery, click-and-collect, and increasingly sophisticated in-store digital layers are all areas where Boxer has, to date, invested less aggressively than some of its peers. This has been, arguably, the right call for a business whose customer base is less digitally native than the wealthier LSMs. But the frontier is moving, and the Boxer of 2030 will need to have answered some digital and omnichannel questions that the Boxer of 2025 could safely defer.

There is a cultural evolution ahead as well. The transition from being a division of a troubled parent to being a standalone JSE Top 40 darling is not just a governance change. It is a psychological one. Expectations are now set by public markets on a quarterly cadence. Activist investors, if they arrive, will do so with theses of their own. The temptation to reach for acquisitions, for diversification, for the kinds of strategic moves that impress bankers but erode operating discipline, will grow with the market cap. The leadership team's most important job over the coming decade is, in some sense, simply to remain the team that built the thing in the first place.

If they manage it, the Boxer story becomes something more than a South African retail case study. It becomes a reference point for every operator and investor thinking about how to build durable value in emerging markets, how to serve the underserved profitably, and how to resist the gravitational pull of corporate abstraction when the underlying business demands operational intimacy. The Empangeni butchery of 1977, the hands-off parent of 2002, the hidden compounder of the 2010s, and the newly independent listed company of 2025 are chapters in the same book. The next chapters will, in the fullness of time, tell us whether this is Africa's Aldi, Africa's Costco, or something harder to label and therefore potentially more valuable than either.

For now, in April 2026, the crown jewel has been unleashed. The market has noticed. The management team that built it is finally being measured against the asset they built. And a young mother carrying a Boxer Build paper bag through the turnstiles of a township store somewhere outside Durban on a Saturday morning is, without knowing it, part of the single most interesting investment case being debated in African consumer markets today.

Further Reading & Source Context

For readers wanting to go deeper, the most useful primary sources have been the Boxer Retail Ltd. pre-listing statement and listing documentation filed with the JSE in the fourth quarter of 2024, the parent Pick n Pay Stores Ltd. annual reports and integrated reports for the years spanning the Boxer ownership period, Pick n Pay's rights issue documentation and strategic review disclosures from 2023 and 2024, and the JSE's SENS announcements covering the unbundling transaction through to its completion. For cross-industry benchmarking, the Shoprite Holdings integrated reports, the Spar Group reports, and the publicly available disclosures from Dollar General, Aldi Süd, and Costco provide useful context on soft-discount and lower-income-segment retail economics globally. South African retail industry data from the South African Revenue Service's household expenditure breakdowns, and statistics on formal versus informal retail penetration, have been useful for sizing the opportunity.

Specific financial figures, where not explicitly cited to a named source, are either derived from listed-company filings or, where the company has not disclosed a given line item, have been flagged in the text as not disclosed. Readers conducting their own fundamental work should rely on the most recent audited statements and trading updates for current figures, and should treat any forward-looking interpretations in this article as one reading of the public record rather than as a substitute for direct engagement with company disclosures.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube