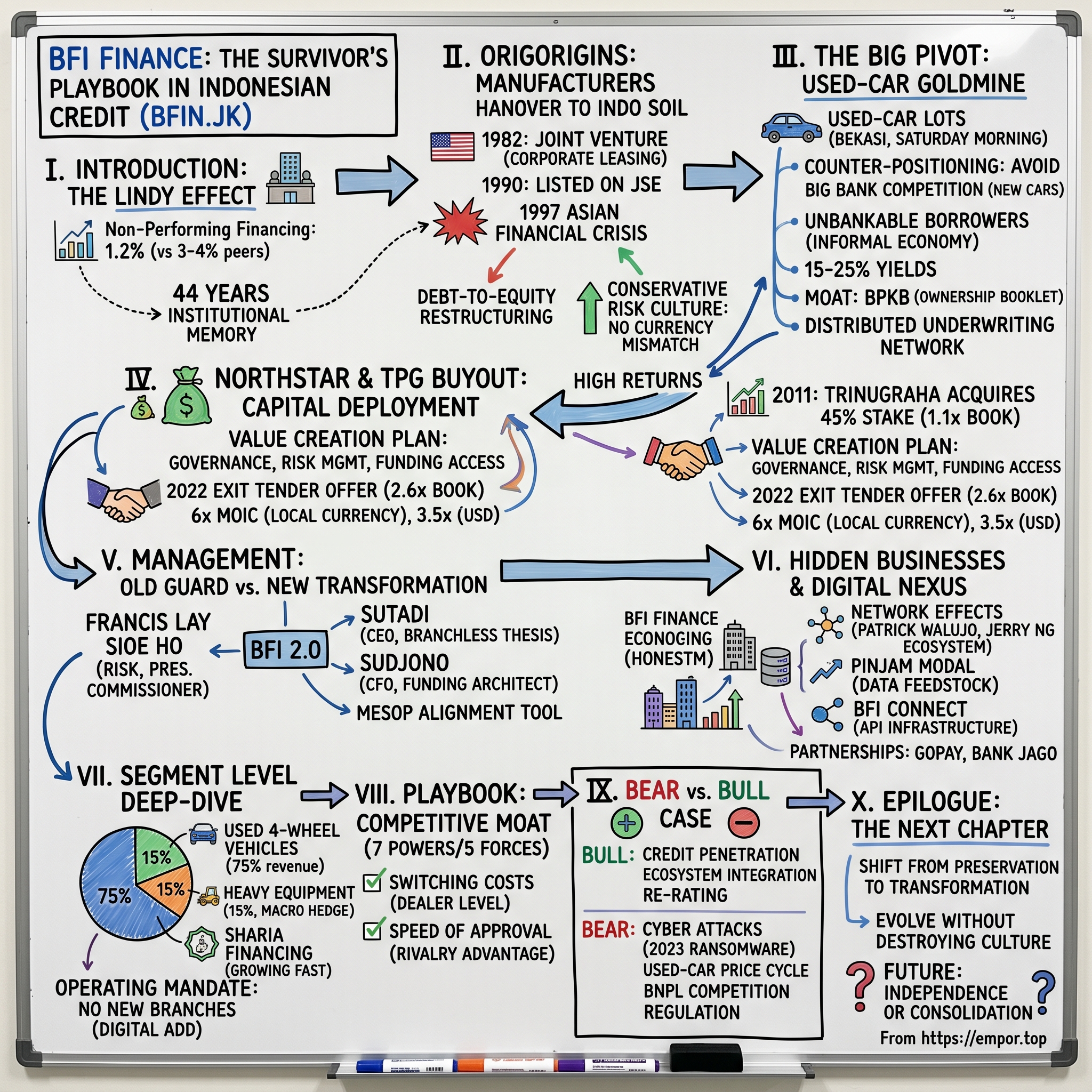

BFI Finance: The Survivor's Playbook in Indonesian Credit

I. Introduction & The "Lindy" Effect

Picture a low-slung office park on Jalan Sudirman in BSD City, just outside Jakarta. It is mid-afternoon, the heat is oppressive, and in a glass-walled conference room on the upper floor, a set of mid-level credit officers are reviewing a single line on a spreadsheet. That line reads "Non-Performing Financing: 1.2%." It is the kind of number that makes Indonesian bankers do a double-take, because across the street at any of the large universal banks, the comparable figure for multifinance exposure sits somewhere between three and four percent. The officers do not celebrate. They adjust their glasses, nod once, and move on to the next page. This is what forty-four years of institutional muscle memory looks like.

That memory belongs to PT BFI Finance Indonesia Tbk, ticker BFIN on the Jakarta Stock Exchange. It is the oldest non-bank finance company in Indonesia, a quiet giant that most foreign investors have never heard of and most Indonesian taxi drivers cannot quite name, even though a surprising number of them financed their vehicles through it. Its headquarters is not glamorous. Its billboards are rare. Its annual reports are written in the kind of measured, bureaucratic Bahasa Indonesia that puts analysts to sleep. And yet, through four decades that included the Asian Financial Crisis, a management coup, a private-equity carve-out, a controlling-stake tender, a global pandemic, a ransomware attack, and now a digital reinvention, BFI Finance has survived. More than survived — it has compounded.

The Acquired thesis on BFI is deceptively simple. This is a company that started life in 1982 as a joint venture between a New York money-center bank and a small group of Indonesian industrialists. It was never designed to last this long. Its parent, Manufacturers Hanover, would itself be absorbed into Chemical, then Chase, then JPMorgan, before anyone at the Jakarta subsidiary could finish filing the paperwork for a name change. BFI was an orphan of American banking consolidation, left in a country whose rupiah would eventually lose more than eighty percent of its value in a single year. That it still exists is already remarkable. That it has become one of the most consistently profitable consumer lenders in Southeast Asia, and a quiet node in the digital infrastructure of Indonesian consumer finance, is the story worth telling.

The themes running through this episode are three. First, multiple expansion — how a "boring" book-value lender got re-rated as a platform, and what the mechanics of that re-rating look like when a private equity sponsor holds the pen. Second, counter-positioning — how BFI built a durable franchise not by fighting the big banks where they were strong, but by running toward the parts of the credit market the big banks actively wished to avoid. And third, the Northstar and Jerry Ng ecosystem — the loose confederation of Indonesian financial assets, from Bank Jago to certain corners of the GoTo empire, in which BFI sits as a kind of credit utility, quietly underwriting while its cousins take the headlines.

What follows is the story of how a leasing desk inside a defunct American bank became, nearly half a century later, a test case for whether old-economy credit can survive the platform era.

II. Origins: From Manufacturers Hanover to Indonesian Soil

It is worth remembering just how strange the early 1980s were for foreign banks in Indonesia. The Soeharto government was in the middle of what economists would later call the oil windfall years. Rupiah liquidity was sloshing around the archipelago. Yet the domestic financial plumbing was primitive. There was no corporate bond market to speak of. Consumer credit existed mostly in the form of a handshake between a shopkeeper and a regular customer. If you wanted to lease a fleet of trucks for a palm oil estate in Riau, you either bought them with cash or you called a foreign bank.

In 1982, Manufacturers Hanover — at the time the fourth-largest bank in the United States, a venerable institution that traced its roots to a New York savings bank chartered in 1812 — partnered with a group of Indonesian investors to incorporate PT Manufacturers Hanover Leasing Indonesia. The business was initially a corporate leasing desk with the glamour of an accounting ledger. It leased factory equipment, printing presses, generators, the physical stuff of a country industrializing faster than its banking system could accommodate. The pitch to customers was not about rates. It was about structure: in a country where secured lending was legally cumbersome and operationally messy, a lease made the collateral question disappear, because the lessor simply owned the asset.

Then came 1991. Manufacturers Hanover, having stumbled through the Latin American debt crisis, merged into Chemical Banking Corporation, which a few years later merged into Chase, which would eventually become part of JPMorgan Chase. Through each of these transitions, the Indonesian subsidiary became progressively less strategic to its American parent. By the mid-1990s, the local entity had been rebranded as Bunas Finance Indonesia, listed on the Jakarta Stock Exchange in 1990, and begun quietly expanding into consumer auto financing. It was a perfectly respectable middle-tier finance company. Then the world collapsed.

The Asian Financial Crisis of 1997 is the defining trauma of modern Indonesian corporate history, and for BFI's predecessor it was an existential event. The rupiah, which had been trading around 2,400 to the dollar, plunged to 17,000 at its trough. Any Indonesian company that had borrowed in dollars to lend in rupiah — which was essentially the entire non-bank finance sector — was technically insolvent overnight. Peers did not just struggle; they evaporated. The multifinance industry saw a regulatory cull so brutal that the number of licensed companies fell by more than half in the years that followed.

BFI entered the crisis with a balance sheet that looked much like everyone else's and emerged with something fundamentally different. Between 1998 and 2001, under a restructuring negotiated with its creditors, the company converted a substantial portion of its dollar-denominated debt into equity. The restructuring diluted existing shareholders painfully, handed large blocks of stock to foreign creditors, and forced the company to operate for several years under what was effectively creditor oversight. It was humiliating. It was also survival.

What emerged on the other side was no longer really an American joint venture. The Manufacturers Hanover name had long since lost meaning, and in 2001 the company was rebranded as PT BFI Finance Indonesia. The balance sheet was cleaner. The shareholder register was a patchwork of creditors who wanted out. And the surviving management team had learned, in the most visceral way possible, that asset-liability mismatches kill. From that point onward, BFI would fund itself overwhelmingly in rupiah, lend in rupiah, and treat any hint of currency mismatch as an existential threat. Peers that re-levered in dollars during the 2000s repeated the mistake. BFI did not.

The legacy of that survival is the conservative risk culture that still runs through the company today. Francis Lay Sioe Ho, who joined as a young finance executive during the crisis years and eventually took the CEO chair, used to describe the period to junior staff as the company's "second founding." The founding story was not a garage, or a whiteboard, or a visionary product pitch. It was a rolling credit workout. That framing, more than any product decision that followed, is why BFI developed the instincts it did.

The question, once the restructuring was finally behind them in the early 2000s, was what to do next. The answer would turn out to be the most important strategic pivot in the company's history.

III. The Big Pivot: The Used-Car Goldmine

Walk into a used car lot in Bekasi on a Saturday morning. The asphalt is cracked, the corrugated roof is half-rusted, and there are maybe forty vehicles lined up in uneven rows — a 2011 Toyota Avanza with 180,000 kilometers on the odometer, a 2015 Honda Mobilio with a slightly suspicious paint job on the rear quarter panel, a 2018 Daihatsu Xenia that has clearly been used as a ride-share vehicle. A family of four is negotiating with the dealer in the shade. The father has a down payment of perhaps fifteen percent of the asking price in cash. He needs financing for the rest. He is the customer no big bank wants to talk to.

That customer is the reason BFI exists in its modern form.

In the mid-2000s, as Indonesia's economy recovered and the middle class began its long expansion, the largest domestic banks and the captive finance arms of the automakers did exactly what textbook economics predicted: they raced one another to finance new cars. Bank Central Asia, Bank Mandiri, and above all the Astra group's finance subsidiaries poured into new-vehicle loans. The logic was impeccable. The underlying asset was fresh, the paperwork was clean, the manufacturer stood behind the vehicle, and the buyer was typically a salaried employee with a verifiable income. Competition pushed spreads down relentlessly. By the late 2000s, yields on new-car financing in Indonesia had compressed to single digits in a country where the policy rate alone sat several points higher.

BFI looked at this landscape and decided to go the other way. This is the counter-positioning moment in the story, and it is worth spending time on, because the decision was neither obvious nor easy. Used-car financing in Indonesia in 2005 looked, to most bank credit committees, like a minefield. Vehicle provenance was uncertain. Odometer fraud was routine. The legal infrastructure for repossessing collateral was slow and politically sensitive. And the borrower base was exactly the segment — small business owners, independent contractors, semi-formal workers — that credit bureaus could tell you almost nothing about. It was, in the polite language of bank risk committees, "not bankable."

It was also enormously underserved, enormously profitable if you could underwrite it, and almost entirely unavailable to anyone whose business model depended on fighting the big banks head-on.

The economics are worth pausing on. A new-car loan at a big Indonesian bank in the late 2000s might yield somewhere between eight and ten percent. A used-car loan underwritten by a multifinance company, secured by the vehicle's BPKB — the ownership booklet that functions as the legal title document in Indonesia — could yield fifteen to twenty-five percent depending on the age of the vehicle and the risk profile of the borrower. Even after subtracting funding costs, provisions, and operating expenses, the net interest margin on that book was roughly double what a bank could earn on a comparable balance sheet. The reason nobody else wanted it was precisely the reason it paid.

BFI's innovation was not the discovery that used cars were more profitable. Every credit officer in Indonesia knew that. The innovation was the operating model built to underwrite them safely. The company invested, over a period of roughly a decade, in a distributed network of several hundred branches, each staffed with credit officers who physically inspected vehicles, verified BPKBs with local police and vehicle registries, and — crucially — built dense, long-term relationships with used-car dealers in their districts.

The BPKB itself became the moat. In a country where the formal credit bureau system was thin and employer income verification was unreliable, the physical ownership booklet for a vehicle, held in BFI's custody until the loan was paid, provided a piece of collateral that was both legally enforceable and emotionally powerful. Indonesian borrowers would default on many things before they defaulted on the loan that held the keys to their primary productive asset. Non-performing financing ratios on BFI's core used-vehicle book settled, through multiple economic cycles, in a range that banks could only dream about for their unsecured lending.

There is a subtler point here about what BFI actually became during this period. On paper it was a multifinance company. In practice, it was a distributed underwriting network that had solved, through a combination of local knowledge and collateral discipline, the information problem that prevents most credit from flowing to the Indonesian informal economy. The branches were not channels in the retail-banking sense. They were information gathering nodes. The dealers were not customers. They were referral partners whose own livelihoods depended on keeping the flow of financing clean.

By the late 2000s, this model was generating the kind of returns on equity that caught the attention of the world outside Jakarta. That attention would walk through the door in 2011, wearing an expensive suit and carrying a very specific thesis about what happens when professional capital meets an underappreciated emerging-markets franchise.

IV. The Northstar & TPG Buyout: Capital Deployment Masterclass

The meeting happened in Singapore, and by the time it was over, Indonesian consumer finance had its first proper private-equity buyout of a listed platform.

On one side of the table sat representatives of Northstar Group, the Southeast Asian private-equity firm founded by Patrick Walujo, and their partners at TPG, the global buyout giant whose emerging-markets franchise was then in the middle of an aggressive Southeast Asian push. On the other side sat the remaining legacy shareholders of BFI — a mix of post-crisis creditors and minority holders — who had, in one form or another, been looking for an exit since the 2001 restructuring closed. The vehicle that the buyers had set up for the transaction was called Trinugraha Capital, a special-purpose entity designed specifically to hold the BFI stake.

In 2011, Trinugraha acquired a 45% controlling stake in BFI Finance for approximately 168 million US dollars. The headline valuation was roughly 1.1 times book value. For a consumer finance company that was generating a mid-teens return on equity with a non-performing loan ratio under two percent, in a market growing at high single digits, that price was, to put it mildly, not demanding. The reason it was achievable is the reason this deal deserves its own case study: BFI, at that moment, was not viewed as a growth story or a technology play. It was viewed as a slightly ungainly legacy finance company with a complicated shareholder register and a management team that had not been professionalized in the way global institutional investors expected.

What Northstar and TPG brought was not capital — BFI had plenty of capital. What they brought was, in the jargon of the industry, a "value creation plan." In less technical language, they brought governance, discipline, and access. The board was reconstituted with independent directors from major Indonesian and regional institutions. Risk management was upgraded with systems and processes that would not have been out of place at a global bank. Internal audit was overhauled. Reporting was standardized to a level where a pan-Asian fixed income investor could pick up a BFI bond prospectus and actually understand what they were buying.

That last piece — funding access — is where the real value creation happened on the liability side of the balance sheet. Before Trinugraha, BFI funded itself primarily through bilateral bank lines extended by a handful of domestic lenders. After Trinugraha, BFI became a regular issuer in the Indonesian rupiah bond market, a name known to regional institutional investors, and a counterparty that global development finance institutions like the IFC were willing to extend long-term funding to. The effect on the cost of funds was meaningful. The effect on the stability of the funding was transformational. Multifinance companies fail in Indonesia mostly because they cannot roll their funding in a crisis. By the mid-2010s, BFI had diversified its liabilities to a degree that made a funding-side failure considerably less plausible.

The asset side also compounded. With cheaper and more stable funding, BFI could grow its book faster without compressing its margins. Return on equity, already respectable, stayed durably in the high teens and at times breached twenty percent. Earnings per share roughly tripled over the decade that Trinugraha held its stake. Book value per share compounded at a pace that, when added to the dividend stream, put BFI among the better-performing financial stocks in the region.

Then came the exit, and this is where the masterclass part of the title applies. In 2022, Trinugraha executed a partial exit via a tender offer that effectively marked the stake at around 1,200 rupiah per share, which translated to roughly 2.6 times book value at the time. That is an extraordinary re-rating from the 1.1 times book entry point eleven years earlier.

Do the arithmetic. Entry at approximately book value. Book value itself roughly tripled during the holding period through retained earnings and growth. Exit at more than double book value. The multiple on invested capital in local currency terms came out to roughly six times over eleven years, which is an internal rate of return comfortably in the mid-teens. In US dollar terms, after the rupiah's depreciation across the period, the return was closer to three and a half times, still a healthy IRR by any private equity standard, and spectacular for a deal in a mature credit business.

The question that sophisticated observers asked at the time was whether the 2.6x book exit multiple was actually defensible, or whether the incoming buyers were the ones holding the bag. The answer is more interesting than either extreme. BFI in 2022 genuinely was a different business than BFI in 2011 — it had a digital infrastructure that did not exist before, partnerships with the largest Indonesian technology platforms, and a management team that had been trained through an entire economic cycle under professional governance. The re-rating was not purely financial engineering. It was a real revaluation of what kind of company the market thought BFI had become.

That, in turn, is the cleanest illustration you will find in Southeast Asian capital markets of how private equity creates value in emerging market financials. Buy at book, professionalize the operation, compound the earnings, and exit as a platform. Write it down. Teach it in schools. It is very hard to execute and very hard to replicate, but when it works, it looks exactly like this.

The question after 2022 was what came next. The answer depended, as it often does in Indonesian business, on who was at the top.

V. Management: The Old Guard vs. The New Transformation

Francis Lay Sioe Ho is not a person you would immediately identify as a chief executive. He is soft-spoken, prefers one-on-one meetings to large gatherings, and has spent decades cultivating an almost aggressively unremarkable public persona. Friends and colleagues describe him as the kind of leader who would rather you forget he was in the room than remember what he said. For nearly four decades, he ran BFI Finance. For most of that time, the Indonesian financial press could not have picked him out of a lineup.

That understatement is part of the Francis Lay playbook, and it is inseparable from the BFI story. He joined the company in the early 1980s, worked his way through the finance function, navigated the crucible of the 1997–2001 restructuring, and emerged as the person the remaining shareholders trusted to keep the institution alive. When Trinugraha arrived in 2011, one of the more notable features of the transaction was that the new owners explicitly kept Francis in the CEO seat. They had bought a business whose culture was largely his creation, and they were smart enough not to break the thing they had just paid for.

Under his watch, the company's operating DNA cohered around three principles that he repeated until subordinates could recite them in their sleep. First, never take a currency mismatch risk again. Second, never lend against collateral you cannot physically control. Third, never grow faster than your risk systems can absorb. The first was a direct legacy of 1997. The second was a legacy of the branch-level credit disasters that had wiped out several competitors in the mid-2000s. The third was a response to what he had watched happen to multifinance peers during the 2013 taper tantrum, when several fast-growing rivals found themselves unable to roll funding and had to shrink their books rapidly at precisely the wrong moment. BFI, under his leadership, preferred to miss cycles than to blow up in them.

In 2025, that leadership chapter came to its formal end. Francis Lay Sioe Ho moved from the CEO chair to the President Commissioner seat — in Indonesian corporate governance, the functional equivalent of becoming non-executive chairman. The day-to-day leadership of the company passed to Sutadi, a long-serving BFI executive who had previously been responsible for business growth, distribution, and the digital channels that were becoming increasingly central to the company's future.

Sutadi's profile is a deliberate contrast. Where Francis built his career around risk management, Sutadi built his around distribution and transformation. Within BFI he has been the internal champion of the "branchless" thesis — the idea that the company's future hundred thousand customers should be onboarded without ever setting foot in a physical location. He is, by reputation, more comfortable with a product roadmap than with a provisioning table, more likely to quote a customer acquisition funnel than a loan loss coverage ratio. His shareholding is modest; public filings indicate he owns around 0.14 percent of outstanding shares. But his alignment is reinforced significantly through the company's management equity program.

The chief financial officer, Sudjono, represents the other half of this transition. He has been the quiet architect of BFI's post-Trinugraha funding strategy, the person who made sure the liability side of the balance sheet kept up with the asset side. With a shareholding around 0.17 percent and a reputation as the most rigorous CFO in the Indonesian multifinance sector, Sudjono is the institutional memory of why the non-performing financing ratio sits where it does. When a credit officer in a regional branch wants to push underwriting limits on a particular dealer, it is, indirectly, Sudjono's framework that tells them no.

The incentive structure binding this new team to the new chapter is the Management and Employee Stock Option Program, or MESOP, under which 290 million treasury shares were set aside in 2026 to be transferred to management and key employees as part of the "BFI 2.0" transformation. In a company where insider shareholding has historically been modest, the MESOP is a material alignment tool. It is also a signal. The board is asking the management team to behave like owners through a period of strategic reinvention, not like caretakers of a mature franchise.

The open question, naturally, is whether this alignment produces the intended behavior. Management stock programs in Indonesian listed companies have a mixed historical record. Some have driven genuine performance culture. Others have been silently priced as deferred bonus plans, detached from any serious theory of shareholder value. The answer at BFI will not be known for several years. What is known is that the structural setup is meaningfully more aggressive than at any prior point in the company's history.

Which brings the story to what the new team has actually been building — the parts of BFI that most investors, even Indonesian ones, are still learning to recognize.

VI. "Hidden" Businesses & The Digital Nexus

There is a rule of thumb in Indonesian technology investing that goes something like this: any business that matters is, in some form, touched by the loose network of people and capital associated with Patrick Walujo, Northstar, and the circle of entrepreneurs that includes Jerry Ng, Pandu Sjahrir, and the founders of GoTo. That network is not a formal entity. It has no organizational chart. But follow the shareholder registers, board seats, and co-investment patterns across enough Indonesian financial and digital companies, and a recognizable shape emerges. BFI sits inside that shape.

Consider first the subsidiary that almost no casual observer of BFI knows about: PT Finansial Integrasi Teknologi, which operates under the brand Pinjam Modal. This is BFI's peer-to-peer lending platform, licensed by the Indonesian Financial Services Authority, the OJK, under the country's rapidly tightening fintech lending framework. On the surface, the question is obvious. Why does a legacy secured lender with a pristine balance sheet want to own a P2P platform, an industry whose reputation in Indonesia has been battered by a wave of scandals, shutdowns, and regulatory crackdowns over the last several years?

The answer is data. A peer-to-peer lending platform, particularly one focused on small working capital loans to micro-enterprises, generates information about customer behavior that a branch-based secured lender simply cannot produce. Who pays on time. Who pays early when they have surplus cash. Who shifts their repayment patterns in response to local economic stress. This is the information foundation that any serious digital underwriting model requires, and the informal economy in Indonesia does not surrender it easily to anyone without a product that lives in the informal economy. Pinjam Modal is, in effect, BFI's data feedstock. It does not need to be enormously profitable on its own. It needs to generate the underlying signal that allows the rest of the company to underwrite digitally.

Then there is BFI Connect, the company's API-first infrastructure layer, which is arguably the most strategically important thing the company has built since the used-vehicle pivot. The idea behind BFI Connect is to unbundle the BFI underwriting and funding engine from the branch network and expose it as a set of programmable endpoints that any consumer-facing application can plug into. The pitch is that any app with a large customer base — a ride-hailing platform, an e-commerce marketplace, a digital wallet — can, in effect, become a BFI branch. The host application handles the customer relationship and the user interface. BFI handles the credit decision, the loan booking, the collections, and the balance sheet.

This is where the ecosystem story becomes concrete. GoPay Pinjam BPKB, the vehicle-backed lending product inside the Gojek super-app, is one of the more prominent examples of the BFI Connect model in practice. A Gojek user with a vehicle and a financing need does not have to walk into a BFI branch. They initiate the application from within the app they already use daily. The credit decision is run against BFI's underwriting engine, the collateral documentation process leverages BFI's operational infrastructure, and the loan sits on BFI's balance sheet. Gojek, in turn, does not have to become a regulated lender to offer secured consumer credit to its user base. Both sides benefit. The economics are split, and neither side has to bear the full operational cost of doing what the other side does best.

The Bank Jago connection deepens the picture. Bank Jago is the digital-first bank that has become one of the most valuable listed companies in Indonesia on the strength of its partnerships with the GoTo ecosystem. Integration between Bank Jago and BFI allows customers to automate loan repayments directly from digital wallet pockets within the Jago app, reducing friction and cutting collection costs. The strategic overlap is not an accident. Jerry Ng, who built Bank Jago into what it is today, operates in the same investor ecosystem that engineered the BFI buyout. The directories of names on the respective shareholder registers rhyme. The operational partnerships flow from that.

The question a sophisticated investor should ask is whether this digital nexus is a genuine competitive advantage or a story. The honest answer is that it is too early to be entirely sure, but the signals are promising. Customer acquisition costs through digital channels, according to the company's disclosures, sit materially below the blended cost of acquiring customers through the traditional branch network. The digital channels skew younger, which matters for lifetime value. And the partnerships allow BFI to distribute its underwriting capacity without having to build consumer-facing digital brands of its own — a task that has humbled many established financial institutions globally.

What this all adds up to is a company that, beneath the surface of its still largely traditional financial statements, is quietly transforming into a credit utility for the Indonesian digital economy. That transformation does not show up cleanly in any single reported line item. But it shows up across the shape of the book, the composition of new customer cohorts, and the infrastructure the company has been investing in since the end of the Trinugraha era.

The question of what that business actually looks like on the ground — in terms of what gets financed, where, and for whom — is the next layer to peel back.

VII. Segment Level Deep-Dive

The BFI revenue mix has, for most of its modern history, told a very consistent story. Roughly three quarters of the company's revenue is generated from the financing of secondhand four-wheeled vehicles. This is the cash cow, and understanding why the cash cow keeps producing is crucial to any forward view of the business.

The used-car book is not a single homogeneous product. It spans a range of vehicle ages, borrower profiles, and dealer relationships. At the conservative end sit financings of three-to-five-year-old vehicles to borrowers with verifiable incomes, where yields are modest but loss rates are almost negligible. At the more aggressive end sit loans on older vehicles to small-business owners who are using the proceeds for working capital as much as for the vehicle itself. Those loans carry yields that can reach into the twenties and loss rates that are meaningfully higher, but which are more than compensated for by the spread. BFI's skill, developed over two decades, is in getting the mix right across the book.

The second segment, accounting for roughly fifteen percent of revenue, is heavy equipment financing. This is a different business with a different rhythm. Mining trucks, excavators, crane equipment, and the paraphernalia of Indonesian infrastructure and commodity extraction. The loan sizes are larger, the customer base is more concentrated, and the collateral is harder to move but also harder to hide. The segment acts, in practice, as the company's macro hedge. When commodity cycles boom and the mining sector is flush with capital expenditure, the heavy equipment book grows aggressively. When commodities roll over, the book shrinks, provisions rise, and the segment becomes a drag. Over time, though, the cycles have been more additive than subtractive, because they rarely coincide with weakness in the consumer used-vehicle book.

The third, smaller but strategically significant piece is the Sharia financing business. Indonesia has the world's largest Muslim population, and the Islamic finance sub-economy is growing faster than the conventional finance sector on a percentage basis. BFI Sharia products, structured under the murabahah and ijarah frameworks, serve a customer segment that explicitly prefers — or in some cases religiously requires — non-interest-bearing contracts. The margins on Sharia products are structurally similar to conventional ones because the economic substance of a murabahah financing differs from a conventional loan primarily in form. But the customer base is distinct, and the growth runway is significant in a country where Sharia finance still accounts for a small single-digit share of total financial assets.

Running across all of these segments is the physical-to-digital transformation. BFI's current operating mandate, explicit in management commentary, is "no new branches." The existing footprint, which stretches across more than two hundred locations in the main islands of the archipelago, is treated as a fixed asset to be optimized rather than expanded. New capacity is being added digitally, through BFI Connect and the platform partnerships, rather than through the long, expensive process of opening new physical offices. This is the quiet story of how BFI's cost-to-income ratio, already favorable by multifinance industry standards, is positioned to improve gradually over the coming years without sacrificing underwriting quality.

The net effect, if the transformation plays out as designed, is a company that increasingly resembles a technology platform on the operating side while maintaining the credit discipline of a conservative legacy lender on the balance sheet side. That combination, if it actually exists, is rare and valuable.

Which raises the question of what exactly protects it from being competed away.

VIII. Playbook: Analysis & Competitive Moat

Hamilton Helmer's 7 Powers framework is the sharpest available tool for distinguishing durable competitive advantage from what Warren Buffett once called the "illusion of moat." Applied to BFI, three of the seven powers are clearly relevant, and it is worth examining each on its own merits.

Counter-positioning is the most obvious. By the structural logic of Indonesian financial services, the largest banks cannot profitably serve the used-vehicle borrower at the yields that segment actually pays. Their cost of capital is too low and their operating model is calibrated for scale at thin margins on clean collateral. If BCA or Mandiri tried to match BFI's used-car strategy, they would have to build out a branch-level field underwriting capability that their entire organizational design was built to avoid. More importantly, the returns on such a build-out would be dilutive to their core businesses, which are producing high-teens return on equity on easier assets. This is the definition of a counter-positioned franchise: the incumbent giant cannot respond without hurting itself more than it hurts you.

Switching costs, the second relevant power, operate at the dealer level rather than at the end-customer level. An individual used-car buyer is a commodity — they will finance with whoever offers them an acceptable rate and a fast approval. But the dealers who aggregate those buyers are not commodities. A BFI-affiliated used-car dealer in, say, Surabaya has a decade-long relationship with the local BFI credit officer, a workflow that feeds applications directly into BFI's underwriting system, and a commercial arrangement with commission structures, escalation paths, and service level expectations that have been tuned over repeated cycles. Breaking that and rebuilding it with a competing finance company costs the dealer time, trust, and operational risk. Multiply that by thousands of dealer relationships across the archipelago, and you have a switching-cost moat that is far stickier than it looks on paper.

Network effects are the third power in play, and they are concentrated in the ecosystem story discussed earlier. As more digital platforms integrate with BFI Connect, the underwriting data grows richer, the cost of acquiring the next platform partnership falls, and the value to existing partners increases because their shared customers have a smoother experience. This is not quite the Facebook-style network effect of a pure platform. It is closer to what might be called an infrastructure network effect, where the utility of being plugged into BFI's rails increases with the number of other things that are also plugged in. It is early, it is real, and it is defensible in ways that are hard to replicate without the years of regulatory and operational investment BFI has already sunk.

Switching to Porter's 5 Forces for a complementary lens. The threat of new entrants in the Indonesian multifinance space is, in theory, moderate — the OJK issues licenses, and new entrants appear regularly. In practice, though, the combination of capital requirements, the operational cost of building a distribution network, and the tightening supervisory posture since the P2P industry's troubles have raised the effective barriers considerably. The bargaining power of customers is low in the traditional used-car business, where BFI is often the only financing option for a given borrower-dealer combination, but rising in the digital channel, where price comparison is easier. The bargaining power of suppliers — which in a lender's case means the providers of funding — is material, since BFI depends on banks, bond investors, and occasionally multilateral institutions for its liabilities. This is mitigated by the diversification of funding sources achieved over the last decade, but it is the force that a conservative analyst should watch most closely in a rising-rate environment.

The threat of substitutes is the most interesting force, because it is where the digital transformation plot intersects with the competitive landscape. Buy-now-pay-later products, digital bank overdrafts, platform-native credit lines, and informal peer lending all compete for a share of the same Indonesian consumer's wallet. None of them is currently a clean substitute for a BPKB-secured used-vehicle loan, because the use cases and ticket sizes are different. But as digital credit products scale and underwriting models improve, the boundaries between categories will blur. BFI's defense is not to fight those substitutes directly, but to be the infrastructure provider underneath as many of them as possible.

Rivalry, the fifth force, is intense. Adira Dinamika, Astra's multifinance arm, Mandala Multifinance, and a long tail of smaller players all compete for used-vehicle dealer relationships. BFI's competitive advantage in that rivalry is its speed of approval — the service-level-agreement advantage, in industry parlance. A dealer in a regional city cares as much about the speed and reliability of the financing decision as about the headline rate, because a slow decision loses the sale. BFI's historic investment in its credit workflow and its newer investment in digital decisioning have kept it at or near the top of the industry on this dimension.

The investor-relevant KPIs that distill all of this analysis into something trackable are, on balance, a small number. Watch the non-performing financing ratio as the primary indicator of underwriting discipline through the cycle. Watch the net interest margin, particularly relative to peer averages, as the measure of whether the used-vehicle counter-positioning franchise is still earning its historical premium. And watch the share of new bookings originated through digital channels and platform partnerships, as the leading indicator of whether the BFI 2.0 thesis is actually taking hold. Those three numbers tell you, more efficiently than any other combination, whether the story is still intact.

Which brings the analysis to the honest work of weighing what could go right against what could go wrong.

IX. Bear vs. Bull Case

The bull case for BFI Finance rests on three compounding claims. First, the Indonesian credit penetration story is structurally intact. Consumer credit as a share of GDP in Indonesia remains low by regional standards, and the secular trajectory of formalization, digitization, and middle-class expansion continues to widen the addressable market for secured consumer lending. Second, BFI's counter-positioned franchise in used-vehicle financing is defensible against bank competition and is being modernized, not replaced, by the digital transformation. Third, and most speculatively, the ecosystem integration strategy — the quiet buildout of BFI as the credit utility under a set of major Indonesian consumer platforms — could drive a second leg of multiple expansion as the market begins to value BFI less as a legacy multifinance company and more as a platform-adjacent fintech infrastructure business.

Each of those claims, stacked on top of one another, suggests a company whose earnings power can compound at a respectable pace for an extended period, with a gradual re-rating of the price-to-book multiple providing an additional layer of return. Combine that with a historically disciplined capital return policy and an alignment structure that ties the new management team to long-term equity performance, and the bull case has real integrity. It is not a hype story. It is a patient compounding story.

The bear case is structurally serious and should not be waved away. The first risk is cyber-security and operational resilience. In 2023, BFI suffered a ransomware attack that disrupted its systems and forced a period of operational improvisation while the technology team rebuilt affected infrastructure. The financial impact was manageable, but the episode exposed the dependence of modern multifinance operations on digital plumbing that is, almost by definition, under continuous adversarial pressure. As BFI accelerates its digital transformation, the attack surface grows. A more severe incident in the future could damage trust with dealer partners and platform customers in ways that take years to repair.

The second risk is a used-car asset price cycle. Used-vehicle values in Indonesia, like those anywhere, respond to the price of new vehicles, the cost of replacement parts, the availability of fuel subsidies, and the macro backdrop for small-business income. A sharp decline in used-car values would compress the loan-to-value cushion on BFI's collateral book and, in a stress scenario, push non-performing financing ratios above the company's historical comfort zone. BFI has navigated previous cycles successfully, but the discipline is not free, and the current book size is many times what it was during the last major stress event.

The third risk is competition from buy-now-pay-later and platform-native credit products. These do not substitute directly for the BFI core product today, but they are bleeding into adjacent segments — small-ticket consumer financing, durable goods purchases, informal working capital — that BFI might otherwise expand into as it grows. A well-capitalized digital competitor with a lower-cost customer acquisition model and a friendlier user experience could force BFI to defend margins in newer segments, slowing the operating leverage the company is counting on from its digital strategy.

A fourth, lower-probability but higher-severity risk is regulatory. The OJK has signaled, through repeated policy communications, its intention to tighten supervision of the multifinance industry. Interest rate ceilings, capital requirements, collection practice regulations, and data-protection rules all sit on a policy shelf that could be pulled down at any time. BFI's compliance posture is strong by industry standards, which is an advantage in a tightening regulatory environment — competitors with weaker controls will suffer disproportionately — but a severe rate cap or collection restriction could compress industry economics materially for everyone.

Holistically, applying the 7 Powers and 5 Forces framework to the bull-bear balance, the picture is of a company with genuine, verifiable structural advantages in its core business, a credible but unproven thesis on extending those advantages into adjacent digital segments, and a set of risks that are real, identifiable, and partially hedged by the conservative operational culture the company has maintained for over two decades. Compared with its direct peers — Adira Dinamika, Mandala, and the captive finance arms of the automakers — BFI is more profitable, better funded, and more advanced in its digital transformation. Compared with the digital-native lenders and fintech platforms that are emerging around it, BFI is less exciting, less scalable in theory, but vastly more proven in execution.

The second-layer diligence items worth noting sit mostly on the governance and ownership side. The post-Trinugraha shareholder register is more fragmented than it was during the private-equity era, which matters for how strategic decisions get pushed through at the commissioner level. Public institutional ownership is modest, and concentrated foreign ownership is limited by regulatory constraints on multifinance companies. Auditor signaling has been clean through recent cycles, with no going-concern or qualified-opinion flags that would warrant concern. On the non-core asset side, the Pinjam Modal and BFI Connect investments are the optionality plays, and neither is currently sized in a way that would materially alter the group's risk profile if either stumbled.

The honest summary is that BFI is neither a no-brainer nor a trap. It is a well-run mid-cap emerging-markets financial with a better-than-average strategic position and an interesting digital overlay, facing a set of risks that are manageable but not trivial.

The final question, then, is what happens next.

X. Epilogue: The Next Chapter

The 2025 management transition is not just a change of titles. It is the moment at which BFI's strategic center of gravity shifts from preservation to transformation. Francis Lay Sioe Ho built an institution that survived. Sutadi and Sudjono have been handed the harder task, which is to evolve an institution without destroying the thing that made it worth inheriting.

What that looks like in practice over the next several years will involve a series of decisions about how aggressively to invest in the digital distribution stack, how far to lean into platform partnerships versus building out direct-to-consumer digital products, how to manage the inevitable tension between the traditional branch network and the new channels it is increasingly competing with, and how to price the trade-off between growth and underwriting discipline as the board's expectations, now anchored by the MESOP alignment structure, push for faster compounding.

There is also the open question of whether BFI will remain independent. Southeast Asian consumer finance is consolidating, slowly but visibly. Regional champions — Grab, Sea Limited, the Ant Group affiliates, the Japanese consumer finance giants with long histories in Southeast Asia — all have reasons to want a larger footprint in Indonesian credit. BFI is the kind of asset that fits into multiple of those strategic maps. Its current shareholder structure is fragmented enough that a well-priced tender offer could, in principle, clear. Whether one ever comes is a different question, dependent on a set of cross-border capital flows and regulatory permissions that are difficult to predict.

The broader lesson, for investors looking at Southeast Asian credit more generally, is that the formula that has worked at BFI Finance is transferable in its structure, even if the specific niche is not. Resilience as the foundation, built through surviving an existential crisis and internalizing the lessons. Niche focus as the operating strategy, built through going where the incumbents cannot profitably follow. Ecosystem integration as the growth vector, built through plugging into the platforms that are already aggregating customer attention. When those three conditions compound over a long enough holding period, the result is the kind of quiet wealth creation that makes for good case studies and underappreciated stock prices.

Four decades after a New York bank and a group of Indonesian industrialists signed the incorporation papers for a modest leasing joint venture, the business that emerged from that paperwork is still here, still compounding, and still quietly underwriting the vehicles, equipment, and small businesses that power the Indonesian economy. That, in itself, is the answer to the question the Acquired thesis opened with.

XI. Outro & Recommended Reading

For readers who want to go deeper on this story, the most useful starting points are the company's own disclosures, which are more informative than most emerging-markets financials manage to be. The 2024 BFI Finance Annual Report, filed with the Indonesian Stock Exchange, lays out the segment economics, the governance structure, and the early commentary on the digital transformation in sufficient detail to form an independent view. Northstar Group's public profile materials provide context on the buyout-era value creation thesis. Indonesian multifinance industry whitepapers, particularly those published by the Asosiasi Perusahaan Pembiayaan Indonesia and the OJK's annual industry statistics, place BFI's metrics in the appropriate peer context.

The longer read, for anyone interested in the structural history, is the literature on the 1997–1998 Asian Financial Crisis and its impact on the Indonesian financial sector. The IMF post-mortem reports and the academic histories of the crisis-era restructurings are where the BFI story acquires its deepest roots. Understanding how the crisis reshaped the country's non-bank financial institutions is the single most useful piece of background for understanding why a company like BFI developed the specific operating culture that it did.

For the ecosystem story, the public histories of GoTo, Bank Jago, and the broader Northstar-associated investment network provide the connective tissue that makes the digital nexus comprehensible. None of those companies, taken alone, tells the whole story. Taken together, they start to sketch the outline of the Indonesian consumer finance future that BFI is positioning itself inside.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube