Banpu: The Great Carbon Pivot

I. Introduction: The Elephant in the Room

Picture a corporate boardroom in Bangkok, somewhere on the upper floors of a glass tower along Rama I Road. On the walls hang photographs spanning four decades. One of them, taken in 1983, shows a dusty open-pit mine in Lampang province, northern Thailand. Men in hard hats squint into a harsh tropical sun, a single conveyor belt snaking down a reddish hillside. Another photograph, dated forty-three years later, shows a gleaming natural gas processing plant in Barnett, Texas, with pump jacks stretching to the horizon. A third image shows a fleet of electric ferries crossing the Chao Phraya River, their silent motors gliding past the grand old temples of Bangkok. Three photographs, one company. And between them lies one of the most audacious corporate transformations in Asian business history.

This is the story of Banpu Public Company Limited. The name "Ban Pu" in Thai literally translates to "crab village"—a quaint, almost rustic label for what grew into a ten-country energy conglomerate with a market value that has at times flirted with 150 billion baht and fallen back again with the ruthless rhythms of commodity cycles. Founded as a small lignite miner to feed Thailand's industrializing economy, Banpu today owns natural gas fields in Pennsylvania, lithium-ion battery stakes in Singapore, solar farms across China and Japan, wind assets in Vietnam, e-tuktuk fleets in Thailand, and a Texas-listed subsidiary called BKV Corporation that aspires to be America's first "carbon-negative" gas producer.

How does a Southeast Asian coal titan convince Wall Street, Singapore institutional money, and a skeptical ESG community that it is actually a tech-forward, forward-thinking, green energy platform? That is the puzzle at the heart of this episode. Because on paper, Banpu should be a dinosaur. The world has declared war on coal. European banks have divested. Insurance companies will no longer underwrite new thermal coal mines. Index providers have quietly moved thermal coal out of the mainstream. And yet Banpu has not shrunk into irrelevance. Instead, under the stewardship of the Vongkusolkit family and a sequence of determined CEOs, the company has spent the last decade methodically redeploying its coal cash into natural gas, renewables, battery technology, and mobility services.

This is, in essence, a capital allocation story. It is the story of a family-controlled conglomerate using a sunset industry to fund a sunrise industry. It is the story of a Thai company discovering that the cheapest way to enter the American energy market was to buy distressed shale gas assets from Devon Energy and ExxonMobil at cycle lows. It is the story of a CEO transition—from the operational powerhouse Somruedee Chaimongkol to Sinon Vongkusolkit, a next-generation scion educated in strategy and finance rather than rock mechanics and haulage.

The roadmap for this episode takes us from the 1983 origin in the village of Ban Pu to the "Greener & Smarter" pivot of 2015, through the controversial Centennial Coal acquisition in Australia, into the Barnett and Marcellus shale basins of Texas and Pennsylvania, and finally into the lithium batteries, e-ferries, and carbon capture wells that will define the company's next chapter. By the end, a question: is Banpu a value trap dressed in green, or one of the most underrated compounders in Asia?

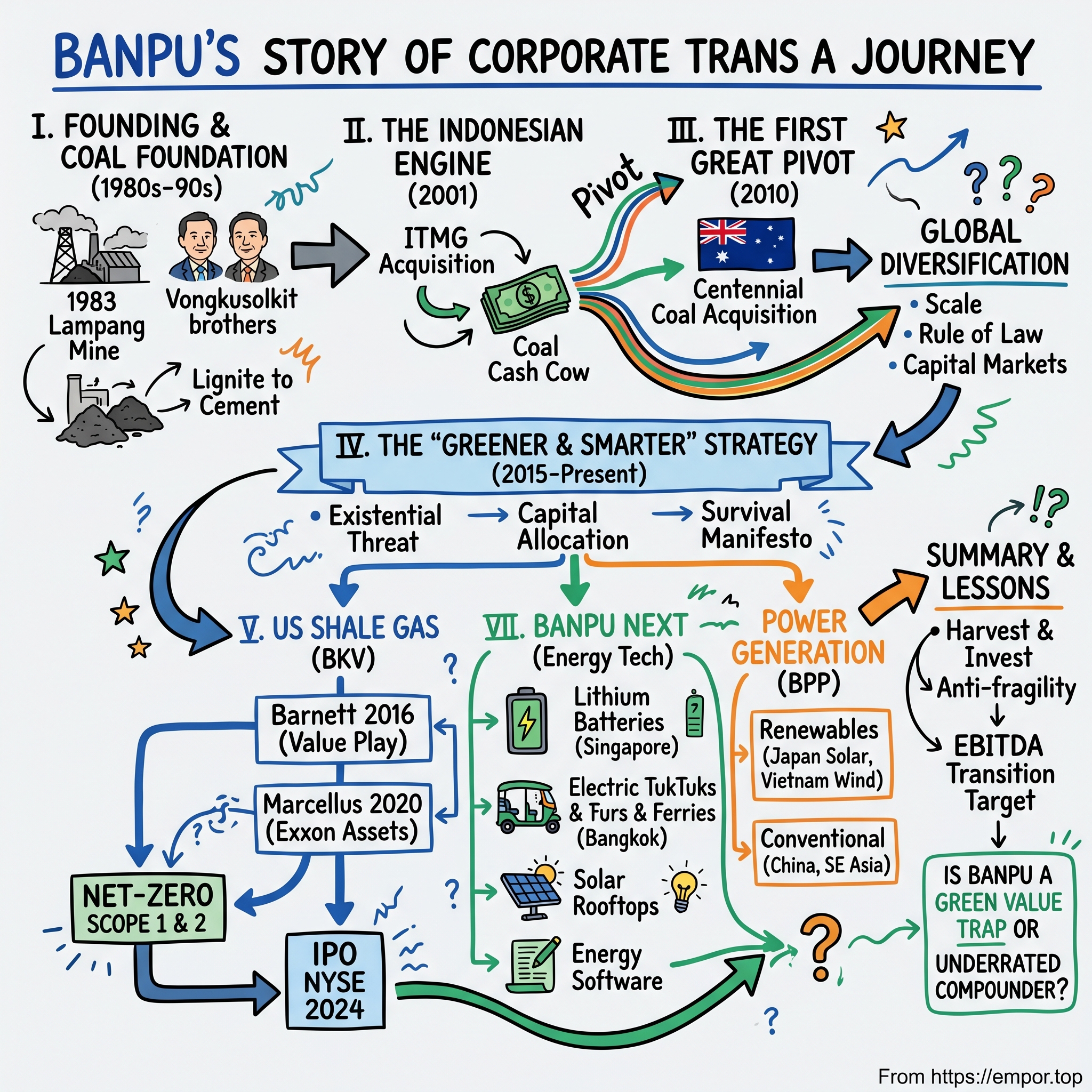

II. Founding & The Coal Foundation

The year is 1983, and Thailand is in the middle of a transformation that has not yet captured global headlines. The country is shedding its image as an agricultural backwater and laying the rails—literal and metaphorical—for what Western economists would soon call the "Asian Tiger" moment. Factories are being built in the Eastern Seaboard. The Chao Phraya plain is dotted with new cement kilns, textile mills, and food processing plants. And all of that industrial heat requires fuel. Thailand has little oil and not much natural gas infrastructure to speak of. What it does have, tucked into the hilly northern provinces, is lignite—a soft, brownish coal that is lower in energy content than its Australian or Indonesian cousins but plentiful, domestic, and crucially, cheap.

Into this moment walk the Vongkusolkit brothers. Isara Vongkusolkit, a businessman from a Sino-Thai trading family with interests in sugar and construction, had spotted an opportunity. If Thailand's factories were going to run on lignite, someone needed to dig it out of the ground, wash it, grade it, and deliver it to the cement plants and power stations that would need it by the trainload. The family, together with partners from the Thai industrial establishment, founded the Ban Pu Coal Company in the village of Ban Pu in Lampang. The initial operation was almost charmingly humble—a single open-pit mine, a handful of trucks, a rudimentary processing facility, and perhaps a few hundred employees.

What turned this small lignite miner into a regional empire was a combination of timing, temperament, and tactical patience. The 1980s and 1990s were, in retrospect, a golden era for commodities. Thailand's GDP was compounding at roughly 8% a year. China was awakening. And Indonesia—the country that would become Banpu's true cash engine—was in the middle of opening up its enormous coal fields under the Soeharto-era "coal contract of work" regime. Banpu noticed. In 2001, the company acquired a controlling stake in PT Indo Tambangraya Megah, or ITMG, an Indonesian thermal coal producer with some of the lowest-cost operating mines in all of Asia.

The ITMG deal is one of those quiet transactions that only looks obvious in hindsight. At the time, thermal coal was trading at around $25 to $30 per ton. Indonesia's regulatory environment was a confusing patchwork of central and provincial rules. Foreign investors were nervous. Banpu paid what was, by later standards, almost nothing. Within a decade, as China's appetite for imported thermal coal exploded and seaborne coal prices tripled, ITMG turned into a printing press. By 2011, at the peak of the commodities supercycle, ITMG alone was generating more than a billion dollars a year in EBITDA, and its shares on the Indonesian Stock Exchange had made Banpu one of the wealthiest industrial families in Thailand.

But here is the subtle part, the part that gets lost when critics reduce Banpu to "just a coal company." The Vongkusolkits understood, even in the roaring years, that coal was a cyclical, politically vulnerable business. They did not pay themselves the entire cash flow in dividends. They did not over-lever the balance sheet chasing megaprojects. Instead, they built what the family would later describe, in more mystical moments, as a "war chest"—retained earnings that could be deployed when the cycle turned, as it inevitably would. The cash cow was not the point. The cash cow was the source of capital for whatever came next.

By the mid-2000s, the company had begun to sense the shape of its own future. Domestic Thai lignite was plateauing. Indonesian coal was still spectacular but politically fragile. And the world was beginning to whisper about something called "carbon." The old Banpu, the Banpu of a single mine and a handful of trucks, had to die so that a bigger, more diversified Banpu could be born. The question was simply: where would the first great pivot take it?

III. The First Great Pivot: Going Global

In October 2010, the Australian coal industry was in the grip of a gold rush. Thermal coal prices had roared back from the Global Financial Crisis, Chinese buyers were signing long-term offtake agreements at premium prices, and everyone from BHP to Glencore was writing checks for Australian assets. Into this frothy market walked Banpu, announcing what was at the time one of the largest outbound acquisitions in Thai corporate history: the roughly two billion Australian dollar takeover of Centennial Coal, a New South Wales thermal and coking coal producer with mines feeding directly into domestic Australian power stations and the Newcastle export terminal.

The Centennial deal felt audacious on announcement. A Thai company, headquartered in Bangkok, buying a flagship Australian miner at what many analysts quietly conceded was the top of the cycle. The logic, as articulated by then-CEO Chanin Vongkusolkit, was that Banpu needed scale, needed geographic diversification, and needed exposure to the "high calorific value" export market that Indonesian lignite and Thai domestic coal simply could not match. Australia also offered something more intangible but arguably just as valuable: rule of law, established mining jurisdictions, and the kind of English-language capital markets credibility that would make future financings cheaper and easier.

Did they overpay? With the benefit of sixteen years of hindsight, the honest answer is: probably, at that specific moment. Thermal coal peaked in 2011 and then proceeded to grind lower for almost a decade, bottoming below $50 per ton in 2016. Centennial's earnings came under pressure almost immediately. Impairments followed. And for years, Centennial was the asset that skeptics pointed to when they wanted to argue that the Vongkusolkits had succumbed to commodity cycle euphoria.

But "did they overpay" is the wrong question for a capital allocator with a thirty-year horizon. The more interesting question is: what did Banpu learn? And the answer shaped everything that came next. Three lessons, in particular, became foundational.

First, Banpu learned that being a "local player" was not enough. Regional cash generation was fine for a while, but in a world where the marginal buyer of thermal coal was a Japanese utility or a Chinese state-owned enterprise, you needed to own assets on both sides of the trade, in multiple jurisdictions, priced in multiple currencies. Volatility in any single market could not be allowed to threaten the group's balance sheet. Diversification was not a slogan. It was a survival requirement.

Second, Banpu learned that owning mines was not the same as owning an energy business. Centennial's revenue was tied to the price of coal, full stop. There were no hedges in the rock. The downstream power stations that bought Centennial's product had long-term contracts that insulated them from price swings, but Centennial the miner absorbed the full volatility. If Banpu wanted stability, it needed to move down the value chain—into power generation, into grid-connected assets with long-term power purchase agreements, into the kind of businesses whose cash flows looked more like utilities and less like commodities.

Third, and most importantly, Banpu learned that scale begets access. The Centennial deal put Banpu on the radar of global investment banks. Suddenly, when Macquarie or Credit Suisse were shopping distressed coal assets—or, later, distressed gas assets—Bangkok got a phone call. The company became a credible bidder. A decade later, when it would be the turn of American shale gas to get "unloved," Banpu's reputation as a disciplined, cash-generative buyer would pay dividends no Australian coal mine ever delivered.

By the early 2010s, the shape of the problem was clear. The company had built an extraordinary coal franchise spanning Thailand, Indonesia, and Australia. The core asset base was generating enormous cash. But the world was turning against thermal coal faster than anyone inside the industry wanted to admit. If Banpu continued to be a pure-play coal company, no amount of operational excellence would save the share price from a slow-motion de-rating. The second great pivot was not optional. It was existential.

IV. The "Greener, Smarter" Strategy

If you walk into Banpu's annual investor presentation for the fiscal year 2015, you will see the moment the company changed its soul. It is not a number. It is a slogan. Two words, clean typography, understated graphic design: "Greener & Smarter." On their own, those words sound like a marketing exercise, the kind of forgettable corporate-speak that populates every ESG report from Tokyo to London. But inside Banpu, "Greener & Smarter" was not PR. It was a survival manifesto, internally debated for years, personally championed by the family, and—crucially—attached to real capital allocation decisions.

The backdrop mattered. By 2015, the global coal industry was in the middle of what is now called the "coal crash." Peabody Energy, the largest American coal producer, would file for bankruptcy the following year. Arch Coal had already filed. Chinese domestic coal consumption was showing signs of plateauing. And the Paris Climate Agreement was being negotiated and signed that December, sending a generational signal that the fossil fuel industry had not received since the 1970s oil shocks. Banpu's executives did not need a McKinsey consultant to tell them that the business model was under existential threat. They needed to decide what to do about it.

The "Greener & Smarter" strategy, articulated publicly in late 2015 and refined in subsequent years, was built around a simple but radical reallocation of capital expenditure. Historically, Banpu had spent the vast majority of its capex on mining—draglines, trucks, shafts, processing plants, port infrastructure. Going forward, a progressively larger and eventually dominant share would flow into three non-coal pillars.

The first pillar was Banpu Power Public Company Limited, ticker BPP on the Thai exchange, the group's dedicated power generation arm. Banpu had been in the power business for years through stakes in Chinese coal-fired IPPs and Laotian hydro, but BPP was spun off and listed in 2016 specifically to become the vehicle for the new strategy. The thesis was straightforward. Conventional thermal generation in China and Southeast Asia still produced steady, contracted cash flows. Renewables—solar in Japan and China, wind in Vietnam—were the growth leg. And by housing all of this in a separately listed entity, Banpu could attract dedicated power-sector capital and assign a power multiple, typically higher than the mining multiple, to a growing portion of its asset base.

The second pillar was what the company eventually rebranded as Banpu NEXT, the "energy technology" division. This is the venture-capital-adjacent arm that invests in solar rooftops, battery storage, electric mobility, and smart energy management. NEXT does not look like a mining business. It looks like a Singaporean or Californian clean-tech holding company, with stakes in start-ups, joint ventures with Japanese trading houses, and partnerships with universities. More on NEXT shortly.

The third pillar, and the one that has arguably moved the needle most in pure financial terms, was natural gas. Banpu made an explicit strategic decision that natural gas was the "bridge fuel" of the energy transition—cleaner than coal, more dispatchable than renewables, and, crucially, trading at depressed prices in the United States due to the shale revolution. The entry vehicle for this ambition became BKV Corporation, and the story of BKV deserves its own chapter.

Taken together, the three-pillar structure can be summarized in the internal segmentation the company now uses in its annual reports. Energy Resources covers coal and natural gas—the extraction business, still the biggest engine in absolute EBITDA terms in most years. Energy Generation covers thermal and renewable power. And Energy Technology covers everything under NEXT. The key metric the family began to emphasize was not total revenue or total EBITDA, but the percentage of EBITDA coming from non-coal sources—a KPI that has climbed steadily from single digits a decade ago to a target of more than half the group by the end of the decade.

The elegance of "Greener & Smarter" lies in what it did not do. It did not shut down the coal business. It did not divest ITMG at a fire-sale. It did not sign an ESG pledge that bound the company to net zero by some unrealistic date. Instead, it treated the coal franchise as a declining but still valuable source of capital—a cash cow to be milked responsibly, with the proceeds reinvested in the businesses that would, eventually, replace it. This is the part that ESG critics often miss. The point was not to perform virtue. The point was to finance a transition with the only currency that actually mattered: free cash flow.

V. The Texas Tea: The US Shale Expansion

Every great corporate story has a moment of nerve. For Banpu, that moment came in the Barnett Shale in 2016.

Consider the scene. It is the spring of 2016, and the American shale industry is in the worst downturn since the fracking boom began a decade earlier. WTI crude has cratered below thirty dollars a barrel. Henry Hub natural gas is barely above two dollars per million BTU. Continental Resources, Chesapeake, Whiting Petroleum, SandRidge—the marquee names of the first shale generation—are in various stages of distress. Devon Energy, a blue-chip Oklahoma City producer, is trying to shed non-core assets to protect its balance sheet. One of those non-core assets is its position in the Barnett Shale, the original shale play, the basin where George P. Mitchell cracked the fracking code back in the late 1990s. Barnett in 2016 is what Wall Street would call "unloved." It is mature. It is gassy. It sits in and around Fort Worth, Texas—developed terrain, not the frontier. Devon is a motivated seller.

Into this scene walks a Thai delegation. Not a Thai delegation you might have expected. Not a trading house, not a sovereign wealth fund, but a mining conglomerate from Bangkok, represented by a brand-new American subsidiary called BKV Corporation, headquartered in Denver, Colorado. In late 2016 and into 2017, BKV closed a purchase of Devon's Barnett assets for approximately 750 to 770 million dollars, acquiring roughly 4,200 producing wells and the pipeline and gathering infrastructure to match.

On the day, the headlines were polite but skeptical. A Thai coal company paying nearly a billion dollars for some of the oldest shale acreage in America? Why not a younger, liquids-rich play? Why not the Permian, where all the excitement was? The answer, in the quiet calculus of Banpu's boardroom, was simple. The Permian was crowded and expensive. Liquids-rich plays were glamorous but cyclically priced. The Barnett was mature, depressed, and full of producing wells that generated cash from day one. It was a classic value play. Banpu was buying time-tested PDP (proved developed producing) reserves at a fraction of replacement cost.

Three years later, BKV doubled down. In 2020, amid the COVID-era energy meltdown, BKV closed the acquisition of ExxonMobil's XTO Energy assets in the Marcellus Shale of northeast Pennsylvania for roughly 750 million dollars. The Marcellus, unlike the Barnett, was considered prime acreage. But Exxon, deep into its own capital discipline overhaul, wanted out of positions it did not consider core to its portfolio. Once again, Banpu was the bidder who showed up with cash and certainty of close when the majors were in portfolio-cleanup mode.

Layer in subsequent tuck-in deals and joint ventures, and by the mid-2020s, BKV had assembled one of the largest pure-play natural gas production footprints in the United States, with material positions in both the Barnett and the Marcellus, a midstream gathering business, a power generation arm with combined-cycle gas plants, and an emerging carbon capture and sequestration business that sits at the frontier of energy transition economics.

The financial benchmark matters here. At the time of the Barnett deal, multiples on mature dry-gas acreage were hovering around 3 to 4 times forward EBITDA. Peers like EQT and Chesapeake were trading at similar or higher multiples in much less distressed market conditions. When Banpu wrote the check, it was, in effect, buying at the bottom of a commodity cycle, with the implicit belief that American natural gas would eventually revalue upward—either through export via LNG, through domestic power demand, or through the retirement of coal capacity. Whether that call was brilliant or merely lucky is a debate that will occupy ten-Ks and analyst reports for another decade. What is indisputable is that it was a contrarian, cash-backed bet, the kind that the Vongkusolkit "war chest" had been assembled for.

The final twist in the BKV story is the carbon capture angle. BKV has committed publicly to achieving net-zero Scope 1 and Scope 2 emissions from its own operations, and it has built a dedicated carbon capture and sequestration business that injects CO2 from its own and third-party gas processing plants into deep saline formations in Texas. The economics of CCS remain debated—the Inflation Reduction Act's expanded 45Q tax credit is the critical input variable—but the strategic logic is unmistakable. If natural gas is going to compete with renewables over the long run, it will have to be "decarbonized" gas. BKV is positioning to be one of the producers that can credibly make that claim, monetizing both the gas and the carbon storage underneath it.

The capstone event was the successful initial public offering of BKV Corporation on the New York Stock Exchange in September 2024. The IPO priced below the initial indicative range—a reminder that gas-sector investor appetite remains choppy—but it nonetheless gave Banpu a public, U.S.-listed vehicle for its American ambitions and crystallized, for the first time, a market value for an asset that had been buried in the parent company's consolidated accounts. The question of whether BKV re-rates over time from "value gas stock" to "energy-transition platform" is arguably the single most important swing factor in Banpu's sum-of-the-parts valuation today.

VI. Current Management: The New Guard

Every great family business eventually faces the succession question. For Banpu, that question came into sharp focus over the last five years, as one of the most consequential CEOs in modern Thai corporate history handed the reins to the next generation.

Somruedee Chaimongkol was not a Vongkusolkit. She was, by background, an accountant—trained in finance, promoted through the CFO ranks, and appointed Chief Executive Officer in 2015 at a moment when the company needed financial discipline more than it needed industrial flash. Somruedee was by all accounts an operator. She managed capital allocation with a near-obsessive focus on return metrics. She pushed the organization toward the "Greener & Smarter" pivot not as a brand exercise but as a financial reallocation. And she oversaw some of the most consequential deals in the company's history, including the early BKV acquisitions in the United States.

What made Somruedee distinctive was the cultural signal her appointment sent. Banpu was a family-controlled business in a country where family-controlled businesses often appoint family members to the top job regardless of qualifications. By entrusting the CEO role to a professional manager without a family surname, the Vongkusolkits signaled that meritocracy and operational excellence mattered more than bloodline. That cultural norm—captured succinctly in the governance phrase "family ownership, professional management"—became one of the less visible but more durable competitive advantages the group enjoys.

The transition to Sinon Vongkusolkit, who stepped into the Chief Executive Officer role, represented something new, not a reversion. Sinon is a next-generation scion, a nephew of the founding brothers' generation, but his profile is worlds apart from the industrial patriarchs who built the coal business. Educated abroad, trained in strategy and finance rather than mine engineering, Sinon represents the "Strategic/Financial" turn in Banpu's leadership DNA. Under Somruedee, the company made big financial bets executed operationally. Under Sinon, the expectation is that Banpu becomes even more explicitly a capital allocator, less a mine operator, more a holding company that orchestrates businesses across coal, gas, power, and technology.

The family's collective hand on the wheel remains unmistakable. Isara Vongkusolkit, one of the founding generation, continues to chair the board and anchor the controlling shareholder structure. The family's holdings are organized through a constellation of private vehicles—holding companies, family offices, and affiliated industrial businesses in sugar and agribusiness—that together preserve an unusually cohesive ownership bloc. Thai corporate governance lawyers who have studied family-controlled industrials often point to the Vongkusolkit structure as an example of what they call "unity"—a deliberate refusal to allow family dilution to fragment control, which in turn allows the group to take multi-decade capital bets that a more fragmented ownership would block.

The incentive structure has evolved in parallel with the strategy. Under the old coal-centric model, management KPIs were dominated by production metrics—tons of coal mined, stripping ratios, cost per ton, realized sales prices. Under "Greener & Smarter," and increasingly so under Sinon's tenure, the KPI set has been deliberately reoriented. Today the metrics that drive executive compensation include the percentage of EBITDA from non-coal businesses, absolute and intensity-based carbon reduction, return on capital employed across segments, and milestones in the development of specific transition projects such as CCS wells, battery deployments, and renewable capacity additions. The signal is clear. The company is paying its executives to transition, not to optimize the legacy business in isolation.

Underlying the management philosophy is a concept that comes up repeatedly in internal communications and investor presentations: "anti-fragility." Borrowed in spirit from Nassim Taleb, the idea is that Banpu should not merely survive shocks—it should be structured to benefit from them. Geographic diversification across ten countries is one expression of this philosophy. Business-line diversification across coal, gas, power, and technology is another. And the deliberate cash-heavy posture during commodity peaks, followed by counter-cyclical deployment during troughs, is a third. Whether this philosophy can survive a prolonged, simultaneous downturn in coal, gas, and Thai equity multiples remains the great stress test for the new guard.

VII. The "Hidden" Businesses: Banpu NEXT

If the coal franchise is the engine and the U.S. shale business is the throttle, then Banpu NEXT is the steering wheel pointed at the horizon. It is also, depending on how you look at it, either the most interesting or the most overlooked part of the Banpu story.

Banpu NEXT was established in 2019 as a joint venture between the parent company and Banpu Power, functioning as the group's dedicated energy technology and smart energy solutions arm. In plain English, it is the subsidiary charged with building the non-fossil-fuel future. The bet underpinning NEXT is that the integrated energy system of the 2030s and 2040s will not be organized around giant centralized generation and long-distance transmission, the way the twentieth-century grid was. Instead, it will be a distributed web of rooftop solar, behind-the-meter batteries, electric vehicles, shared mobility platforms, and trading algorithms that match supply and demand in real time. NEXT wants to own pieces of as many of those layers as possible.

The portfolio reads like a clean-energy venture fund's dream list. On the battery side, Banpu holds a significant stake in Durapower Holdings, a Singapore-headquartered lithium-ion battery manufacturer that produces cells and packs for commercial vehicles, marine applications, and stationary storage. Durapower gives Banpu something almost no other Thai listed conglomerate has—direct exposure to the battery value chain at a time when the bottleneck in electrifying Southeast Asia is not vehicles but the batteries to power them.

On the mobility side, the portfolio is a roll-call of small but strategically interesting bets. MuvMi, an electric tuk-tuk ride-hailing service operating in several Bangkok neighborhoods, offers a view into how electrification might reshape the iconic three-wheeler. Electric ferries crossing the Chao Phraya River in central Bangkok represent the first serious attempt to decarbonize Thailand's public water transit, which moves millions of commuters annually. Battery-swapping networks for electric motorcycles target the vast two-wheeler population across the region. None of these are, today, needle-moving at the group level. But collectively they represent an option on urban mobility electrification that few Southeast Asian incumbents have bothered to assemble.

On the solar side, NEXT and its sister company Banpu Power operate rooftop solar installations across commercial and industrial customers in Thailand, Indonesia, Vietnam, and Japan. The distributed-generation business is particularly attractive because it sidesteps the utility-scale tender process, which has become ultra-competitive and low-margin, in favor of bilateral contracts with corporate off-takers who increasingly demand renewable energy for their own ESG scorecards.

And finally, there is the energy trading and optimization software business—less sexy but arguably more strategic. NEXT has invested in platforms that aggregate distributed energy resources, optimize battery dispatch, and participate in ancillary services markets. In a grid that is increasingly volatile because of intermittent renewables, software that decides when to charge, when to discharge, and when to sell is going to be enormously valuable.

The honest caveat for investors is that NEXT, for all its strategic importance, remains small in absolute EBITDA contribution today. Thousands of e-tuktuks and hundreds of rooftop solar systems do not yet move the dial against a group whose coal and gas operations throw off billions in annual cash flow. So why does NEXT matter so much to the equity story? Because of the multiple.

Public markets, rightly or wrongly, assign very different price-to-earnings multiples to different kinds of businesses. A Thai coal miner might trade at 5 to 7 times earnings. A regulated power utility at 12 to 15 times. A renewable developer at 20 times. A battery or energy technology platform at 25 to 40 times. If Banpu can demonstrate that an increasing portion of its earnings comes from the higher-multiple segments, the weighted-average multiple of the entire group should mathematically expand—even if the absolute earnings of the legacy segments stay flat. NEXT is, in that sense, the part of the company designed to do multiple expansion. It is the narrative as well as the numerator. And it is worth watching closely, because the moment it stops being a rounding error and starts being a material contributor is the moment the equity story reaches a genuine inflection point.

VIII. The Playbook: Seven Powers & Business Lessons

Step back from the individual business lines and ask a harder question. What is the actual source of competitive advantage for a company like Banpu? Is there a durable "moat" underneath the narrative? Hamilton Helmer's Seven Powers framework offers a useful lens here, and when applied honestly to Banpu, three of the seven powers emerge as meaningfully present.

The first is Cornered Resource. Banpu's Indonesian coal assets, held principally through its majority stake in ITMG, sit in what are among the lowest-cost thermal coal mines in Asia. Low-cost production is not just nice to have. In a commodity business where the global clearing price is set by the marginal producer, being in the bottom quartile of the cost curve means the mine makes money even when prices collapse. That cost position is structural. It derives from favorable geology, proximity to export terminals, low stripping ratios, and decades of operating experience. Competitors cannot simply replicate it by spending more. This cornered resource, more than anything else, is what has funded the entire transition. Every contrarian bet Banpu has made—Australia, the U.S. shale purchases, NEXT—was ultimately financed by the cash spun off from Indonesian coal. That is not just a business. That is, in Helmer's language, a genuine power.

The second is Counter-Positioning. This is the subtler and, in some ways, more interesting power that Banpu wields. A pure-play renewables startup, or a pure-play battery company, typically funds itself through repeated equity raises. Every dollar of growth capital dilutes existing shareholders. Every year spent pre-profit means more dependence on capital markets that can slam shut during risk-off moments. Banpu, by contrast, funds its green transition using cash flow from its legacy coal and gas businesses. It does not need to sell shares at inopportune moments. It does not have to cut R&D when sentiment turns. It can patiently build a battery business or a CCS well over ten years, funded internally. Pure-play green startups literally cannot replicate this, because they do not have a legacy cash cow to harvest. That asymmetry, is counter-positioning in its clearest form.

The third is Switching Costs, although these apply more at the Banpu Power level than at the parent. Long-term power purchase agreements with Thai, Chinese, Vietnamese, and Japanese grid operators and industrial off-takers, once signed, become almost impossible to unwind for a decade or more. The counterparties are often state-backed utilities with byzantine procurement processes; switching from a contracted generator to another generator is not a matter of flipping a switch. That stickiness gives BPP's power assets a cash flow profile that looks more like infrastructure than like commodities.

Turning to Michael Porter's Five Forces lens, the picture is more nuanced. The threat of substitution—renewables eating into coal and eventually gas demand—is the most material medium-term risk and the central reason for the entire "Greener & Smarter" pivot. The bargaining power of governments, which set both the ESG rules and the power tariffs, is high and arguably rising. The threat of new entrants into coal is essentially zero, because no one sane is financing new greenfield coal mines in 2026. Industry rivalry in gas is intense but rational; in renewables, the rivalry is ferocious and margin-compressing. And the bargaining power of buyers, which includes long-term utility off-takers, is mixed—stable in contracted businesses, volatile in merchant exposure.

The ultimate capital allocation lesson of Banpu's forty-three-year arc is deceptively simple: Harvest and Invest. Take a profitable but declining legacy business. Do not milk it for maximum short-term dividends. Do not pretend it is a growth business. Instead, extract cash responsibly, preserve balance sheet flexibility, and systematically redeploy that cash into the businesses that will replace the legacy ten or twenty years from now. This is the strategy that a handful of capital allocators—the kind of investors whose long-form letters circulate on Twitter for years—have articulated in more celebrated contexts. Banpu is executing it in one of the harder arenas in global business: a regulated, commoditized, ESG-scrutinized, politically charged energy industry. That it has done so while surviving multiple cycles is, on its own, worth studying.

IX. Myth vs. Reality, Bull vs. Bear, and the KPIs That Matter

Every public company accumulates a layer of consensus narrative that, on inspection, turns out to be partly mythology. Banpu is no exception. The most common myth is that Banpu is "just a coal company trying to greenwash." The reality, as the previous sections have laid out, is that Banpu has, for more than a decade, been systematically reallocating capital away from coal and into gas, power, and technology, with non-coal segments steadily climbing as a share of group EBITDA. You do not have to love coal to see that the trajectory is real. A second common myth is that the U.S. shale bet was lucky timing. The reality is that the bet was sized, structured, and timed deliberately against the prevailing market sentiment—classic contrarianism, which always looks like luck in hindsight. A third myth is that family-controlled Thai conglomerates cannot execute global capital allocation. The evidence of the Centennial, ITMG, Devon, and XTO deals, whatever their individual outcomes, suggests otherwise.

With those corrections on the table, the bull and bear cases come into clearer focus.

The bull case begins with valuation. Banpu on most conventional metrics trades at a low to mid single-digit multiple of expected EBITDA, a discount to Asian power and gas peers and a steep discount to any global energy transition peer group. Embedded in that multiple are several distinct asset pools whose stand-alone values, summed together, plausibly exceed the current enterprise value of the parent. The listed BKV subsidiary has its own public market price. The listed BPP subsidiary has its own. ITMG, listed in Jakarta, has its own. The private Banpu NEXT portfolio has a notional value inside annual reports that may or may not reflect its true marginal worth. If one simply builds a sum-of-the-parts model, attaches reasonable multiples to each piece, and subtracts net debt, the implied equity value has often sat meaningfully above the parent company's market capitalization. The bull case says this holding-company discount narrows over time as the transition progresses, as the non-coal segments become harder to ignore, and as BKV potentially re-rates from "value gas" to "transition platform." In the most optimistic framing, Banpu becomes the "Berkshire of Southeast Asian energy"—a disciplined capital allocator buying cash-flowing energy assets at cycle lows and reinvesting in the next generation of the industry.

The bear case begins with the same raw material—the coal business—and reaches a darker conclusion. In the bearish view, the energy transition is accelerating faster than Banpu's pivot. ESG divestment, insurance unavailability, and bank lending restrictions on thermal coal compound upon each other year after year, grinding the multiple on any business associated with coal downward regardless of actual cash flow. BKV's U.S. gas business, while cash-generative, is exposed to Henry Hub prices that could stay structurally depressed if LNG export capacity lags, if pipeline constraints bite, or if renewables-plus-storage economics improve faster than expected. The NEXT portfolio, beloved in strategic presentations, remains too small to materially re-rate the entire group for years. And underlying all of it is the conglomerate discount—the stubborn refusal of public markets to fully credit a holding company whose sub-businesses span coal, gas, power, batteries, and mobility. In the worst framing, Banpu is a value trap dressed in green, where the coal liabilities bleed out faster than the transition assets can scale.

Reality, as usual, will sit somewhere in between. Which brings the analytical frame to the metrics that actually matter. For a long-term fundamental investor, there are three KPIs worth tracking relentlessly.

The first is the percentage of group EBITDA from non-coal sources. This is the single cleanest gauge of whether the transition is actually happening at a pace that matches the narrative. A number in the low thirties would suggest slower execution than the company's own targets. A number above fifty would signal the transition has crossed the Rubicon. The trajectory matters more than any single year's print.

The second is BKV's realized natural gas price net of hedges, and the trajectory of its Scope 1 and Scope 2 carbon intensity. BKV is now a public company, and its quarterly disclosures will determine how the U.S. shale bet is ultimately judged. If realized prices trend upward—thanks to LNG exports, power demand, or simply supply discipline—and if the CCS business begins to generate meaningful 45Q tax credit monetization, the "unloved gas" thesis pays off. If prices stagnate and the CCS economics remain elusive, the bet does not fail, but it fails to shine.

The third is return on capital employed at the group level. This is the ultimate discipline metric for any capital allocator. A company that harvests one business to invest in another must demonstrate that the investments actually earn a return at least as high as the cost of capital. If group ROCE expands as the non-coal share grows, the harvest-and-invest strategy is working. If group ROCE erodes even as the green share grows, the transition is destroying value rather than creating it.

Second-layer diligence is worth briefly flagging. Banpu operates in ten countries, which means it is exposed to a mosaic of regulatory and climate regimes. Indonesian coal export policy, Thai electricity tariff reform, Australian carbon pricing, U.S. federal 45Q rules, Chinese power purchase agreement revisions—any of these could move the needle in a given quarter. Foreign-exchange translation, particularly the Thai baht against the U.S. dollar, can introduce meaningful reported-earnings volatility that has nothing to do with operating performance. Auditor commentary on asset impairment assumptions, particularly in coal, is always worth reading carefully in the annual report. And concentrated family ownership, while a strategic advantage in many respects, is itself a governance risk factor that minority shareholders should monitor at AGMs and in related-party transaction disclosures.

X. Epilogue & Closing Thoughts

Step back, one last time, and consider the sweep of it all.

Forty-three years ago, in the dusty hills of northern Thailand, a handful of entrepreneurs from a Sino-Thai trading family opened an open-pit lignite mine to feed cement kilns. Today, that same company operates combined-cycle gas plants in Texas, fracks the Marcellus in Pennsylvania, runs electric tuk-tuks through the narrow sois of Bangkok, invests in Singaporean battery manufacturers, owns solar farms in Japan and wind assets in Vietnam, and is listed on two stock exchanges through major subsidiaries. Ten countries, four business lines, three generations of family leadership, and one of the most deliberate corporate transformations anywhere in Asia.

What makes Banpu's journey underrated is precisely how undramatic it has been. There was no single "bet the company" moment. There was no charismatic founder announcing a pivot on stage at a product launch. There was no viral mission statement. Instead, there was a series of sober, sometimes contested board decisions, executed over two decades, that cumulatively amount to one of the most thorough capital reallocation exercises in emerging market industrial history. A Thai family-controlled conglomerate, quietly using Indonesian coal cash to buy Texas gas, to seed Singapore batteries, to float American subsidiaries on the NYSE.

Whether the next ten years validate the pivot or reveal its limits will depend on variables largely outside the company's control—commodity cycles, regulatory regimes, technological trajectories, geopolitical shifts. What is within the company's control is the continued discipline of capital allocation, the integrity of the family-meets-professional management structure, and the pace at which non-coal businesses scale into genuinely material contributors. Those levers, if pulled with the same patience that has defined the Vongkusolkit era, will continue to produce outcomes worth watching.

For fundamental investors who believe that the best emerging market stories are the ones the consensus is not paying attention to, Banpu remains a case study in how an "old economy" company can, with enough discipline and enough patience, earn the right to become a "new economy" company without abandoning the cash engine that made the transition possible in the first place. Not every old-guard energy conglomerate will manage the trick. The ones that do will likely look, a decade from now, a lot like Banpu has been trying, quietly and methodically, to look for the last decade and counting.

That is the Banpu story. A village mine, a war chest, a Texas pivot, and a family that refused to let the world's easy narrative about coal decide its own fate. Whether the great carbon pivot ultimately earns the "top tier capital allocator" label depends less on what happens in Bangkok than on what happens in Fort Worth, Jakarta, Hanoi, and the trading floors that price the future of energy in real time.

The elephant in the room, it turns out, is learning to fly.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube