Aurora Design: The "Tiffany & Co." of Thailand Meets FinTech

I. Introduction: The Golden Empire in the Mall

Walk into almost any air-conditioned shopping mall in Thailand on a Saturday afternoon and you will notice a curious phenomenon. Past the Uniqlo, past the Starbucks, past the food court thick with the smell of basil and chili, there is almost always a corner lit up in red and gold. The counters gleam. The staff wear crisp uniforms. A uniformed guard stands near the door. Inside, under spotlights calibrated to make 23-karat gold glow like liquid sunset, Thai families are not browsing. They are transacting. A grandmother hands over an old necklace she bought her daughter decades ago. A young couple debates a wedding set. A man in a Grab Driver polo shirt slides a chunky bracelet across the counter and walks out, not with jewelry, but with cash.

This is Aurora. And it is the most interesting retailer on the Stock Exchange of Thailand that most international investors have never heard of.

The thesis of this episode is simple, but it takes a full two and a half hours to really defend. Aurora Design Public Company Limited—ticker AURA.BK—is not, or at least not anymore, a jewelry company. It looks like one. It smells like one. Its largest line item on the P&L is the sale of gold jewelry. But the pulse of the business, the thing that drove the re-rating from a sleepy family goldsmith to one of the most-watched small caps on the SET, has almost nothing to do with what a tourist buying a gold pendant at Siam Paragon would recognize. The pulse is a financial services engine. A lending book. An asset-backed, physically-collateralized, high-turnover pawn business dressed in the wedding clothes of a retail brand.

The big question for this episode is whether the market understands that. The stock has traded at times like a volatile gold miner, at times like a specialty retailer, and at times like a non-bank financial. Three different kinds of multiples. Three different kinds of investors. Which is correct?

To answer that, we have to go back. Way back. Not to the founding of Aurora in the 1970s, but to something even older: the 5,000-year-old human obsession with a soft yellow metal that refuses, stubbornly, to rust. Gold is not a product in Thailand the way a handbag is in New York. Gold is infrastructure. It is savings, dowry, emergency fund, inheritance, superstition, and status, collapsed into a single object you can wear around your neck.

The Aurora story is the story of what happens when a second-generation operator looks at that infrastructure, sees through it to the commercial logic underneath, and asks a deceptively simple question: what if we branded it? What if we standardized it? What if we turned it into a fintech? And what if, while everyone else was focused on the shiny object in the window, we quietly built the most valuable part of the company in the back room, where the scale and the pawn tickets live?

By the time you finish this episode, you will never look at a gold shop in a Thai mall the same way again. That bright red and gold beacon is not just selling jewelry. It is a customer acquisition funnel, a distribution channel, and a collateralized lending machine, all stacked into one 40-square-meter retail box. And the holding company that owns the whole operation is, in the most literal sense, a bank in a jewelry box.

Let's get into it.

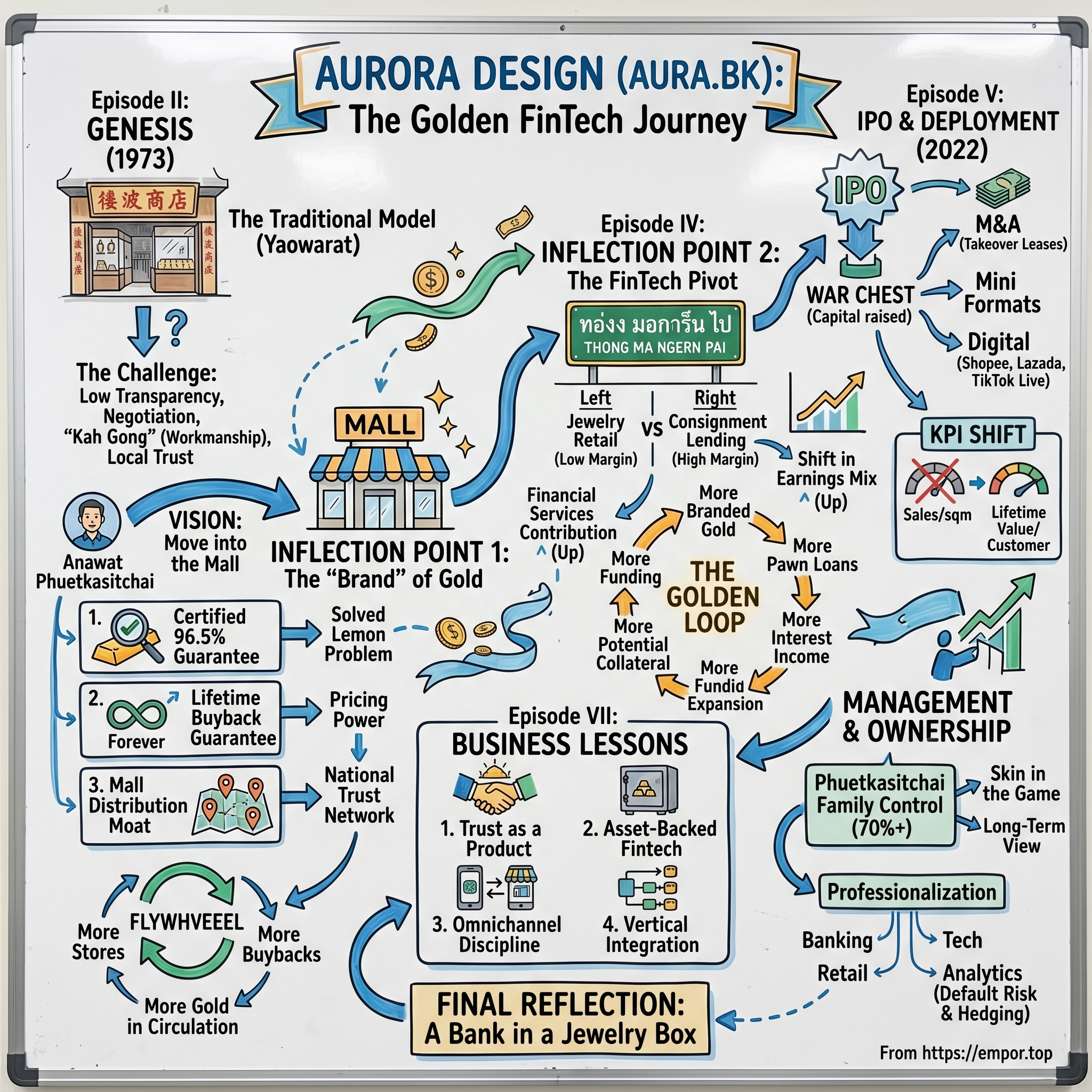

II. Genesis: From Yaowarat to the World

Before Aurora was Aurora, it was a stall.

To understand the origin story, you have to understand Yaowarat. This is Bangkok's Chinatown, a dense grid of streets a mile or so east of the Chao Phraya River where, for more than a century, the Thai-Chinese merchant class built fortunes out of rice, textiles, traditional medicine, and above all, gold. The street is physically and atmospherically the opposite of a Thai mall. The shophouses are narrow, three and four stories high, signage stacked vertically in gold-painted Chinese characters. The pavements smell of fried garlic and incense. And at street level, sometimes three and four per block, are the gold shops.

The traditional gold shop model in Yaowarat was, and to a large extent still is, a triumph of relationship capitalism and an utter failure of consumer transparency. You walked in. You knew the owner, or your parents did. The gold was priced off the daily Gold Traders Association quote, but the workmanship charge—the "kah gong"—was a matter of negotiation and vibes. If you wanted to sell back, the shop would probably buy it, but at a discount that depended on whether they remembered your mother. The purity was, in principle, 96.5 percent—the famous "tong baht" standard that has defined Thai gold jewelry for generations—but in practice, trust was local. You did not take a necklace bought in Yaowarat to a shop in Chiang Mai and expect full value.

It was into this world, in 1973, that the Phuetkasitchai family opened a modest gold trading business. Thailand at the time was still recovering from a turbulent decade. The Vietnam War was in its final, bitter phase just across the border. The country had just emerged from the October 14 student uprising. Inflation was double digits. And gold, in the peculiar psychology of Thai households, was doing what gold always does in Thailand during uncertain times: appreciating, in both price and cultural weight.

The first generation of the family operated the way almost every Yaowarat shop operated: craft-heavy, inventory-light, relationship-driven. They bought gold when prices were low, melted and designed pieces by hand, sold to a local clientele, and accumulated a reputation over decades by not cheating anyone. This is an easy sentence to write but a brutal business to run, because the margins are razor thin, the capital intensity is enormous (you are, by definition, sitting on inventory that is simultaneously your product and your raw material), and the risk of a single bad reputation moment—one customer who claims you sold them underweight gold—can erase a generation of goodwill.

For roughly three decades, that is what the business was. A respected but not particularly remarkable shop, or cluster of shops, doing what dozens of other Yaowarat families did, collecting modest wealth, and quietly assuming the next generation would inherit the same model.

The person who blew that assumption up was Anawat Phuetkasitchai.

Anawat is the archetype of the second-generation Asian family business operator who is polite and soft-spoken in interviews, dresses conservatively, and is, underneath that surface, a pathological long-term thinker who is willing to risk the family name on a contrarian strategic bet. He did not want to run the family business as it had been run. He had grown up watching Thailand's consumer economy change around him. By the late 1990s and into the 2000s, the Thai middle class was no longer shopping on the sidewalks of Yaowarat or the old department stores of Silom. They were being drawn, irresistibly, into the glittering new temples of Thai consumer capitalism: Central, Robinson, The Mall, Siam Paragon, MBK, CentralWorld. "Modern Trade," in the jargon, was eating traditional retail alive.

Anawat looked at this and concluded something heretical. He concluded that the gold shop, too, had to leave Yaowarat. Not literally—the flagship stayed—but strategically. The center of gravity had to move into the mall.

This was a bet-the-family-name decision and it was wildly unpopular inside the clan. Why? Because everything about moving into a mall broke the economics that Yaowarat had taught them to respect. Mall rent was, conservatively, five to ten times street rent. The mall demanded uniform fit-outs, standardized signage, air-conditioned cases, and a degree of visual merchandising that traditional gold shops, which often displayed hundreds of pieces crammed into glass trays, were philosophically opposed to. And perhaps most threateningly, the mall shopper was not the loyal Yaowarat customer. She was a walk-in. She had no relationship. She was just as likely to be comparing prices on her phone as listening to the salesperson.

Anawat's insight was that all of those "costs" were features in disguise. The walk-in customer was, in venture capital language, an enormous expansion of the top of the funnel. Uniform fit-outs and signage were not expensive overhead; they were brand. And mall rent, which traditionalists saw as a margin-killer, was in fact the acquisition cost for the most valuable customer base in the country: the Thai middle class at the moment of aspiration, walking past your window on the way to the cinema.

By the mid-2000s, Aurora had begun to aggressively take mall locations. By the 2010s, the pace had accelerated. What had been a handful of shops turned into dozens, and what had been dozens turned into a footprint that, by the middle of this decade, stretched to every major mall operator in the country. The company had physically and spiritually left Yaowarat. But as we will see in the next section, the real transformation was not geographic. It was conceptual.

III. Inflection Point 1: The "Brand" of Gold

Here is something that sounds obvious if you grew up in New York or Paris and completely bizarre if you grew up in Bangkok: a branded luxury item sells for more than an unbranded one.

Why bizarre? Because in Thailand, gold is not a luxury item. It is a commodity. The price of a one-baht gold necklace—"baht" being both the currency and, confusingly, the traditional Thai unit of gold weight equal to about 15.2 grams—is printed on a lit-up LED ticker outside every gold shop in the country. The ticker updates when the Gold Traders Association updates, usually multiple times per day. If the spot is 41,000 baht per baht-weight, then every shop, from the grubbiest Yaowarat stall to the most polished mall counter, is selling the underlying metal at essentially the same price. The only thing you can charge extra for is the workmanship. And the workmanship charge, historically, was measured in small percentages.

So when Aurora decided to brand its gold, it was not trying to convince customers that Aurora gold was better gold. Chemically, it was not. 96.5 percent purity is 96.5 percent purity; the Thai metric is a national standard. It was trying to convince customers that Aurora gold, bought from Aurora, backed by Aurora, and buyable-back by Aurora, was a different asset than identical gold sold by a nameless shop.

The first pillar of the strategy was the Certified 96.5 Guarantee. This sounds small; it was enormous. Across the Thai gold industry, the dirty secret had always been that stated purity and actual purity did not always match. A small shop under pressure might, over years, drift to 95 percent or lower. It was rarely caught, because customers never assayed their own gold, and because the secondary market discounted everyone's gold anyway. By tying its name to a publicly verifiable, continuously assayed 96.5 standard, Aurora was effectively telling the market: we will destroy our reputation if we ever cheat you, and because we have a reputation worth destroying, you should trust us more than the shop that does not.

The second pillar, and the one that is load-bearing for everything that follows in this story, was the Lifetime Buyback Guarantee.

Stop and think about what this actually meant. In a traditional gold shop, when you sold back a piece you had bought years earlier, you took a double hit. You lost the workmanship charge you originally paid, and you often took a further discount for wear, for uncertainty about the origin, for whatever reason the shopkeeper chose. Aurora's pitch was: if you bought from us, we will buy it back at a published, standardized rate tied to the spot price, with a small, predictable spread, forever. No relationship required. No receipt drama. Any Aurora branch, nationwide.

What Aurora had done, in economics language, was solve the Lemon Problem. The gold resale market was infested with information asymmetry—the seller knew how pure the gold was, the buyer did not, so everyone discounted everyone. By standing behind its own supply chain, Aurora unilaterally created a private resale market in which its customers were not lemons. The consequence was not just customer loyalty. It was pricing power. Aurora could charge a modestly higher workmanship premium than the Yaowarat average, and customers would pay it, because they were not buying gold; they were buying gold with an embedded put option back to Aurora.

This is, if you squint, the same logic that makes a Hermès bag worth more than a nameless leather handbag, except that in the Aurora case the "brand premium" is underwritten by a hard, dollar-denominated resale contract. It is luxury economics applied to a commodity substrate, with a balance sheet guarantee attached.

The third pillar was real estate. If the Lifetime Buyback was the product, mall distribution was the moat. Aurora spent the 2010s doing something that the traditionalists called foolish and that now, with hindsight, looks like one of the great cornered-resource plays in recent Thai retail history. They went to Central Pattana, to The Mall Group, to Siam Piwat, and they locked in locations. Anchor positions. Prominent windows. The kind of spots where, once you occupy them, a new entrant cannot displace you without paying ransom.

The branch count went from single digits at the turn of the millennium to a hundred, then to two hundred. The math on each new location was brutal but the logic compounded. Each new mall store was not an island; it was a node in the buyback network. A customer in Chiang Mai who bought a necklace at Central Chiang Mai could, ten years later, sell it back at Central Bangna without a receipt, and the store could trust the piece because Aurora had sold it in the first place. Every new store made the buyback promise more credible and therefore made every existing store more valuable.

The transformation from "jewelry retailer" to "national trust network" was happening quietly, in plain sight, and the vast majority of Thai retail analysts were still valuing Aurora like a specialty store. That mispricing would persist, at least partially, for another decade. And it set up the second, larger inflection point, which is where the story gets genuinely fun.

IV. Inflection Point 2: The FinTech Pivot

Every gold shop in Thailand, whether it admits it or not, is already a pawnbroker.

For as long as the trade has existed, customers have walked into gold shops not to buy jewelry, but to convert existing jewelry into cash. Sometimes they sell outright. But far more often, in a less formal arrangement, they hand over the piece, take a cash advance at a discount to its gold value, and return weeks or months later to pay the advance plus a small fee and reclaim the item. It is, in all but name, a collateralized loan. It has happened across Yaowarat counters for generations, under the euphemism of "temporary consignment" or simply "leaving the gold with uncle."

The problem was that the informal version did not scale. It depended on handshake agreements, handwritten ledgers, and the emotional bandwidth of a shopkeeper who remembered every customer. A store could carry, maybe, a few hundred active "temporary consignments" at any given time. Beyond that, the paperwork drowned the operation and the default risk exploded.

Around 2019, Aurora began to productize this. The consumer-facing brand was "Thong Ma Ngern Pai"—literally, "Bring Gold, Cash Goes"—and the idea was stupidly simple and, in execution, extremely hard. Take the centuries-old informal pawn, strip out the handshake, wrap it in a digital back-end, standardize the loan-to-value ratios, set predictable interest schedules, price the service transparently, and deliver it through every mall branch in the network.

The insight behind the pivot was not that Thais needed pawn loans. Thais had always needed pawn loans. Thailand is a cash-heavy, partly unbanked economy in which millions of small-business owners, gig workers, farmers, and households sit outside the easy reach of commercial banks. For them, physical gold has always been the working-capital asset of last resort. You wear it as a necklace in good times; you pawn it when the rains fail or the cash register is short. The insight was that nobody had ever done this at scale, with a recognized brand, in a place the middle class already frequented, on the same counter where they also bought jewelry.

And this is where the genius of the Aurora architecture becomes visible. A customer walks into an Aurora store in a Central mall. On one side of the counter, she can browse necklaces and earrings. On the other side, she can hand over a necklace bought a decade ago and walk out with cash in an envelope, knowing that as long as she pays the fee she can come back and reclaim the piece. It is, from the store's perspective, two different revenue streams at two very different margin profiles, sharing the same rent, the same staff, the same security guard, and the same customer.

Retail gold is low margin and high volume. Aurora sells a lot of it. But because the underlying metal price moves one-for-one with the global gold market, the gross margin on the retail side is structurally constrained to the workmanship charge plus a modest spread. Good retailers in the space earn, depending on the year and the mix, a high-single-digit gross margin on their jewelry business. It is a decent business. It is not a magical one.

Consignment lending, in contrast, is high margin and, for the last several years, startlingly high growth. The customer pays a monthly fee on the loan, expressed as a percentage of the principal, and Aurora collects this fee for as long as the loan is outstanding. Because the loan is fully collateralized by gold the company itself appraised, defaults are functionally contained; in a worst case, Aurora simply keeps the gold and recycles it into new jewelry inventory, at a small operational cost and essentially zero principal loss. The net interest margin on the book, once you factor in the cost of capital, scales in a way that retail gross margins cannot.

The data story, which for serious investors is really the whole story, is that the consignment and lending segment's compound growth rate has been running materially above the retail segment's, and its contribution to both gross profit and return on equity has been climbing faster than its contribution to revenue. In other words, the mix is shifting. Aurora is earning more of its dollars from financial services, even though it is still selling most of its units in gold jewelry. The multiple the market pays for each dollar of financial services earnings is different—generally higher, when the market is paying attention—from the multiple it pays for each dollar of jewelry earnings. A blended multiple on a shifting mix is, mathematically, a re-rating waiting to happen.

The second-order consequence is that the retail store is no longer really a retail store. It is a loan origination channel disguised as a jewelry counter. Every piece of gold sold at retail is, ten or fifteen years later, a potential loan collateral. Every piece bought back is an inventory replenishment for the lending book. The flywheel spins: more retail stores produce more branded gold in circulation; more branded gold in circulation produces more eligible collateral; more eligible collateral produces more loans; more loan volume produces more interest income; more interest income funds more retail stores. Aurora did not invent this loop. They just closed it and scaled it, on a network that their competitors could not match.

For investors trying to understand why the stock began trading differently around the pivot, this is the answer. The market had to stop looking at Aurora as a goldsmith with a ticker. It had to start looking at Aurora as a specialty finance company that happens to acquire customers, source collateral, and hold branch real estate through a branded jewelry business.

Which leads us, inevitably, to the capital markets.

V. M&A and Capital Deployment: The IPO War Chest

For most of its history, Aurora was a private family business that funded itself the way Thai-Chinese family businesses have always funded themselves: cash flow, bank lines, and the patience of patriarchs. That model was sufficient when the business was building a mall footprint at a measured pace. It was insufficient the moment the lending book started compounding.

Here is the structural problem a growing, collateralized lender always runs into. Every new loan you write ties up capital. The capital is, by definition, not reusable until the borrower repays. If you grow the loan book by, say, 50 percent year over year, you must, in effect, grow your capital base by roughly 50 percent year over year, or you starve the most profitable segment of your business. Banks solve this by taking deposits. Specialty finance companies solve it by borrowing wholesale. Aurora, in 2019 and 2020, had neither luxury at the scale it needed.

The IPO solved it. In 2022, Aurora listed on the Stock Exchange of Thailand, raising capital into a market that was, at the time, hungry for anything with a "new economy" flavor in the Thai consumer space. The framing, importantly, was not "we are going public to fund mall expansion." The framing, articulated repeatedly in the prospectus and the roadshow, was that the proceeds would fund the lending book, expand the branch network to support origination, and professionalize the back office that a financial services business at scale requires.

Investors who had been paying attention to the mix shift understood immediately. Investors who had not been paying attention bought the stock as a Thai retail story and then had to recalibrate as the subsequent disclosures made the financial services angle more and more explicit. The result was a shareholder base that, over time, has mixed consumer retail funds, financial sector funds, and, as the story matured, dedicated emerging-markets specialty finance investors. That is an unusual cap table for a Thai mid-cap, and it is one of the quieter signals that the underlying business is harder to categorize than it looks.

Post-listing, the capital deployment has been interesting to watch. Aurora has not gone on an aggressive, headline-grabbing acquisition spree. What they have done, instead, is smaller and more durable. They have taken over the leases of smaller mall gold kiosks whose operators could not survive the competitive intensity. They have absorbed second-tier branded gold shops in provincial cities where Aurora did not yet have a flagship. They have rolled out so-called "mini" formats—smaller-footprint branches that combine the lending service with a stripped-down jewelry counter—into secondary malls and community shopping centers where the full-size box does not pencil out.

Every one of these moves, viewed correctly, is a customer and collateral acquisition. A gold kiosk in a Tesco Lotus in Nakhon Pathom is not a strategic asset because of the jewelry it sells. It is a strategic asset because, over a multi-year horizon, it enters thousands of customers into the branded Aurora ecosystem, and every one of those customers is a future source of gold in circulation that can be re-pawned, re-sold, or re-bought at an Aurora counter.

There is a natural question that investors skeptical of the strategy raise at this point. Is Aurora overpaying for mall real estate, for kiosk leases, for the branded network? The back-of-envelope comparison is unflattering. A Yaowarat street shop pays a fraction of a Central mall rent. A kiosk in a Tesco Lotus is a meaningful fixed cost against thin retail margins. By any traditional retail productivity metric—sales per square meter, for instance—Aurora's mall branches look expensive.

The answer, of course, is that traditional retail productivity metrics are measuring the wrong thing. If the store is a loan origination funnel, then sales per square meter is not the KPI. The KPI is lifetime value per customer, where lifetime includes not just the wedding set bought at age 25 but the pawn loan taken against that set at age 40, the new anniversary piece bought at age 50, the estate-planning buyback at age 70. On that metric, Aurora's unit economics, internally, appear to justify the rent. The company's inventory turnover is reportedly several multiples of the traditional industry average, which, if accurate, is precisely the financial signature you would expect of a store that is doubling as a financial services branch: inventory moves faster because it is being recirculated through the lending book, not merely sold once and forgotten.

There is a second, subtler capital allocation challenge that bears mentioning. Aurora, by construction, carries a very large gold inventory. At any given moment, the value of the gold in its cases and vaults is a material fraction of its balance sheet. Global gold prices move. When they move up, the book value of inventory rises and reported margins benefit; when they move down, the inverse is true. Any investor in Aurora is, implicitly, running a long position in gold, whether they wanted one or not. Management has spoken at various points about hedging policies and the use of derivatives to smooth out price volatility, but the company has not, as of the most recent disclosures, eliminated this exposure entirely, nor is it obvious that doing so would be in shareholders' interest given the correlation between gold prices and customer pawn demand.

All of which sets up the question of who, exactly, is steering this ship.

VI. Management & Ownership: The Anawat Era

If you have ever attended an Aurora investor day, you will notice something unusual. The CEO does not talk like a CEO.

Anawat Phuetkasitchai speaks quietly, almost shyly, in the cadence of a family patriarch addressing relatives at a New Year dinner rather than a chief executive addressing a room of institutional fund managers. He is not charismatic in the Western, quotable-quote sense. He does not produce viral soundbites. He does not put his face on billboards. What he does is slowly, methodically, walk through the evolution of the business, with the occasional dry joke about how his father would have hated the idea of putting a gold shop inside a mall.

That temperament matters. It matters because family control in Thai listed companies is, depending on the family, either the best thing about the company or the single largest risk factor. The Phuetkasitchai family retains a substantial majority of Aurora's shares—on the order of seventy percent, though the precise figure fluctuates with pledged-share arrangements and disclosures. That is enormous skin in the game. It is also, in theory, enormous potential for minority abuse. The signal investors look for is whether the controlling family treats minority shareholders as partners or as passengers.

The Aurora evidence so far, if one weighs it honestly, has tilted toward partners. Dividends have been paid consistently since listing. Related-party transactions have been disclosed in line with SET requirements. Capital has been reinvested into the core business rather than siphoned into tangential family ventures. The independent directors, while part of a slate the family controls, have included individuals with credible financial sector and capital markets backgrounds, which at least suggests the board has hands on board that know how to read a loan book.

Anawat himself has publicly emphasized a slow-and-steady generational mindset. He has, in interviews, described the transition from a traditional goldsmith to a modern financial-services-enabled retailer as something he expects to take decades, not quarters, to fully realize. That is a deeply unfashionable posture in modern capital markets, where quarterly earnings discipline rules, but it is also probably the right posture for a business whose core asset—trust—compounds on a multi-decade clock.

The structural question this raises is succession. Thai family businesses have a complicated history with generational handoffs. The canonical risk is that the second generation, having built the professional expansion, hands off to a third generation that either lacks the operational hunger or cannot agree on direction. Aurora is at the moment still clearly in the Anawat era, but investors should, over time, be watching for early signals about how the family is preparing for the next transition—who is being groomed, whether outside professional management is being integrated meaningfully, whether governance provisions exist for disputes.

On the professionalization front, there is a visible shift that has accelerated post-listing. Aurora has, over the last several years, brought in managers with banking, consumer retail, and technology backgrounds. The company has built analytics capabilities that did not exist a decade ago, including, according to management commentary, systems that track store-level lending performance, forecast gold price movements at a granularity useful for hedging and inventory management, and model customer default risk at the individual loan level. That last piece is particularly important. A pawn book that is not actively monitored will, over time, quietly accumulate low-quality collateral and over-extended loans; a pawn book that is actively monitored can be grown aggressively without catastrophic risk. The difference, in the long run, is between a well-run specialty finance company and a slow-motion disaster.

The incentive design for branch managers is a small detail that tells you a lot about the strategic direction. Traditional Thai gold shops compensate staff almost entirely off jewelry sales volume. Aurora, per company commentary, compensates branch managers on a blended scorecard that includes both retail gross profit and the growth and quality of the lending portfolio originated at their branch. That single change—paying people not just for selling necklaces but for building a loan book and keeping it clean—is the management-layer expression of the pivot. You cannot become a financial services company if your front-line staff are rewarded only for selling retail.

Which is a useful bridge, because it suggests that the real Aurora playbook is not any single tactic. It is the systematic layering of conventional retail best practices onto a commodity that the rest of the Thai industry still treats like a family secret.

VII. The Playbook: Business Lessons

Four lessons fall out of the Aurora story that any operator, in any industry, can steal.

The first is that trust is a product. In most industries, trust is treated as a qualitative overlay on top of a "real" product—a nice-to-have, a marketing element, a thing you add after you have designed the thing you actually sell. In the Aurora world, trust is the thing itself. The physical necklace is, chemically, the same as a necklace sold at any other licensed Thai gold shop. What Aurora sells, on top of that chemistry, is the certainty that the gold is what it says it is, that the buyback price will be what the company says it is, and that these promises will be honored at any of hundreds of branches decades from now. That wrapping is the differentiated product. It is also, crucially, impossible to reproduce without the distribution, balance sheet, and longevity to back it up—which is why Aurora's moat widens, not narrows, as the brand ages.

The lesson generalizes beyond gold. In any category where the underlying good is commoditized and where information asymmetry plagues the customer, there is an opportunity to invent a branded product whose real ingredient is trust. Organic food. Pre-owned luxury. Secondary art. Used cars. The companies that win in these categories do not necessarily have better sourcing or better design. They have better warranties, better return policies, and better longitudinal credibility. Aurora's Lifetime Buyback is the gold industry's equivalent of Costco's return policy: on paper, it looks like an operational cost; in practice, it is the product.

The second lesson is the power of asset-backed fintech. Unsecured consumer lending in emerging markets is an exceptionally difficult business. Credit bureaus are patchy, underwriting data is thin, fraud is rampant, and collections are politically sensitive. The default rates can destroy an entire origination vintage if management takes its eye off the ball. Asset-backed consumer lending, in contrast, offloads much of this risk onto the collateral itself. Aurora does not have to predict whether a customer will repay a loan; Aurora only has to be confident that, if the customer does not repay, the collateral on the table can be melted, remade, or resold without material principal loss. When the collateral is physical gold of a purity Aurora assayed itself, sourced through a network Aurora controls, that confidence is exceptionally well founded.

The broader point is that in economies where credit data is weak, collateralized lending against portable, liquid, globally priced assets is a durable business model. Gold is the cleanest such asset in most of Asia. Property is the cleanest in most of the West. The interesting frontier businesses in emerging market fintech are those that, like Aurora, can originate collateralized loans at consumer scale without looking like banks.

The third lesson is omnichannel discipline. Aurora was, by Thai retail standards, aggressive on digital. They moved onto Shopee and Lazada when other gold shops were still treating e-commerce as a sideline. They embraced livestream commerce on platforms like TikTok and Facebook Live when skeptics said customers would never buy gold sight-unseen. They built a mobile app that lets customers check real-time pricing, reserve pieces, and, importantly, initiate pawn-style transactions before walking into a store.

What is striking is that none of this cannibalized the physical network. If anything, the digital surface drove traffic to the physical network, because the most financially consequential transactions—buying a wedding set, pawning a family heirloom—still require walking into a branch, seeing the gold, handing it over. Digital is the top of the funnel; physical is where the revenue and the trust both land. That sequencing is the opposite of the "digital replaces physical" story that consumed so many legacy retailers. Aurora's playbook, properly described, is "digital accelerates physical." And it is accelerating physical in a country where the mall is still, culturally, a core piece of Saturday.

The fourth lesson is vertical integration. At a time when most Thai consumer companies outsource everything possible, Aurora controls design, retail, buyback, inventory financing, consignment lending, and, to a significant degree, marketing. This is expensive in the short run; vertical integration almost always has a higher unit cost than a well-run supply chain. It is extremely valuable in the long run, because each vertical tier reinforces the credibility of the others. A customer who buys a design from Aurora, pawns it through Aurora, and sells it back to Aurora has, in the aggregate, done business with one brand in every stage of the gold life cycle. That single-counterparty experience is the trust product again, compounding.

Put all four lessons together and you get the real Aurora playbook. Which is less a playbook than an industrial thesis: that the way to disrupt a 5,000-year-old commodity market is not to sell the commodity differently, but to sell everything around the commodity with the discipline of a modern retailer and the balance sheet of a modern lender.

VIII. Framework Analysis: 7 Powers & 5 Forces

It is time to put the business through the standard lenses and see what holds up.

Hamilton Helmer's 7 Powers framework asks, for any given business, which of seven distinct strategic powers the company actually possesses. Aurora has, depending on how strictly one applies the definitions, three to four of them.

Brand power is the most obvious. By any reasonable measure of Thai consumer recognition, Aurora sits at or near the top of the unaided-recall list for "where would you buy or sell gold." That level of salience, in a country where gold is both a household asset and a cultural object, is an enormous moat. Brand power here is not about image, it is about default-choice status. When a Thai household makes the rare, high-stakes decision to convert savings into gold or gold into cash, the default destination is a known name. Aurora has become that default for a substantial slice of the urban middle class.

Cornered resource power is the second. The mall locations. There is only so much prime retail frontage inside a top-tier Thai mall, and a meaningful share of it is already leased to Aurora or its peers. New entrants cannot simply decide to compete; they have to wait for a lease rotation, negotiate with mall operators, and, even then, often get relegated to inferior floors or corners. This is a real and underrated barrier. It is also a depleting barrier; if the Thai mall model itself declines—say, because younger consumers shift entirely online—the value of locked-in mall space declines with it. The moat is wide today; whether it remains wide in 2035 is, legitimately, a question.

Switching costs are the third and the most intellectually interesting. On first glance, there is no obvious switching cost in buying a gold necklace; you could buy your next one from anyone. But the Lifetime Buyback Guarantee creates a slow-burn switching cost that only manifests decades later. A customer who has bought from Aurora for twenty years has accumulated, in their jewelry box, a portfolio of pieces whose optimal resale value is realized only at an Aurora counter. Leaving Aurora means either paying a premium-to-market spread to sell those pieces elsewhere, or carrying them until you return. That is a subtle but durable form of lock-in. It is economic in mechanism, and it is cultural in enforcement.

Process power, the fourth, is more debatable. Aurora has built operational capabilities—real-time inventory management across hundreds of branches, centralized pricing, automated loan underwriting, hedging discipline—that are ahead of the traditional industry. Whether these capabilities constitute "process power" in Helmer's strict sense, or merely represent a temporary operational advantage that competitors can eventually copy, depends on how quickly the rest of the industry professionalizes. The honest answer is that process power at Aurora is probably real but not permanent.

Scale economies, counter-positioning, and network effects, the remaining three of Helmer's seven, are harder to argue for in this specific business. Gold, as a commodity, does not exhibit strong sourcing scale advantages. Traditional gold shops are not operating a business model that Aurora can out-flank through structural asymmetry. And while the branded buyback network has some network-effect flavor—more Aurora stores make the buyback promise more credible—it is a weaker form than true two-sided network effects.

Now to Michael Porter's 5 Forces, which asks about the structural attractiveness of the industry itself.

Bargaining power of suppliers is low. Gold is the most fungible commodity on earth. Aurora can source from global bullion markets, domestic refineries, and recycled pieces flowing through its own buyback program. No supplier has meaningful leverage; Aurora can always walk across the street.

Bargaining power of buyers is, paradoxically, also low, even though the end customer is an individual consumer. This is because the underlying price is transparent but the secondary services—buyback, consignment lending, in-branch expertise—are not commoditized. Customers do not negotiate workmanship charges. They accept the posted rate, because the posted rate is backed by a branded promise.

Threat of new entrants is moderate. A new gold shop can, theoretically, open tomorrow. But a new gold shop with Aurora's national mall footprint, nationwide buyback network, and accumulated brand equity cannot. The barrier is not regulatory; it is capital and time. Any competitor who wanted to replicate the model would need years of buildout and substantial capital, during which Aurora would continue compounding.

Threat of substitutes is the most interesting force in the 5 Forces analysis, because it is where the real bear case lives. We will return to this in the next section, but briefly: digital gold, gold ETFs, cryptocurrency, and generalist fintech pawn-style apps all represent potential substitutes for the core Aurora proposition. None has yet broken through in Thailand at scale. All are worth watching.

Rivalry among existing competitors is high in gross terms but low in terms of direct brand competition. Thailand has dozens of gold shops. Very few have built national mall-first retail networks with modern branding. The Hua Seng Heng's of the world are respected and credible, particularly in wholesale, but they are operating under a different model. In the modern-retail-plus-lending segment Aurora has effectively defined, competition is surprisingly thin.

Net-net, the frameworks say something consistent. This is a structurally attractive competitive position in a specific niche that Aurora largely built itself. The risks are real but primarily concentrated in longer-horizon substitute threats and in the cultural evolution of the Thai consumer.

IX. The Bear vs. Bull Case

Every interesting business deserves a serious bear case, and Aurora has several that deserve genuine consideration rather than hand-waving.

The first bear case is simply gold price exposure. Aurora carries a large physical gold inventory and holds gold collateral against its lending book. In a scenario in which the global gold price falls materially and stays down for an extended period, Aurora experiences several simultaneous headwinds. Reported earnings from inventory revaluation decline. Retail demand softens, because Thai consumers historically buy more gold when prices are rising and less when prices are flat or falling. Pawn demand can, counterintuitively, also fall, because the value of a household's existing gold as collateral declines. Management has articulated a hedging strategy, but no hedge fully insulates a business this large from multi-year cycles in its primary commodity exposure. This is not a criticism of management; it is a structural reality that any shareholder must underwrite.

The second bear case is competition from banks and non-bank lenders entering gold-backed lending. Thailand already has well-capitalized, publicly traded specialty finance players such as Srisawad and Muangthai Capital, whose core business is vehicle title lending and related consumer collateralized credit. These companies have lower cost of funds than Aurora, larger balance sheets, and nationwide branch networks of their own. If they decide to push aggressively into gold-backed consumer lending—and there is nothing stopping them—they will compete on price. Aurora's response has to be a combination of network density (more convenient than a finance-company branch), service quality (a gold shop is, culturally, a more comfortable place to pawn a necklace than a finance office), and the vertical integration advantage of also being the original seller of the collateral. Those are defensible advantages, but they are not invulnerable to a well-funded competitor willing to take low-margin share for long enough.

The third bear case is generational. Thai millennials and Gen Z consumers have grown up with digital payments, mobile banking, crypto, and a dramatically lower cultural affinity for physical gold as a savings asset than their parents' generation. If the long-arc decline in gold-as-savings among younger Thais accelerates, Aurora's customer base ages into a demographic cliff. This is not a five-year problem; it is a fifteen- to twenty-year problem. But it is a real one, and it is why Aurora's digital and adjacent strategies—including the expansion into "Aurora Diamond," targeting younger, more aspirational consumers with a slightly different value proposition—are strategically important even when they are not immediately earnings-accretive.

The fourth, more technical bear case is regulatory. Collateralized consumer lending in Thailand is subject to evolving regulation from the Bank of Thailand and related agencies. Rate caps, disclosure requirements, and capital requirements for non-bank lenders have tightened over the years. Any significant regulatory move—for instance, a cap on fees for gold-backed loans that is materially below current industry practice—would compress the margins of Aurora's most profitable segment. This is not an imminent threat based on publicly disclosed regulatory agendas, but it is an always-present tail risk in any specialty finance exposure.

Against these, the bull case has to earn its place, and here it is.

The first bull case is the unbanked and underbanked opportunity. Thailand's banking system, however modern in Bangkok, still leaves millions of households dependent on informal credit. Gold has been their financial instrument for generations. A branded, mall-distributed, digitally-integrated, transparent lender against that gold solves a real problem that the banking system has not, in thirty years of growth, solved. The addressable market for this service is not the jewelry market. It is a meaningful slice of the household credit market.

The second bull case is adjacent category expansion. The Aurora Diamond extension is the most visible example; diamond and colored stones carry structurally higher gross margins than gold jewelry, albeit with different inventory dynamics and without the pawn-demand flywheel. The broader point is that Aurora, having built a premium retail network and a trust-based brand in a commodity category, has optionality to extend into adjacent premium-jewelry categories that the Yaowarat-era gold shop could never have served. This is not guaranteed value; diversification can dilute focus. But management has so far moved cautiously in this direction, which is encouraging.

The third bull case is the compounding flywheel. Every incremental retail branch increases the installed base of branded gold in Thai households. That installed base is, in economic terms, the forward pipeline of pawn collateral and buyback activity. The company is, in a very real sense, creating its own future inventory of business. That is structurally different from a retailer whose only future business is what it can originate from scratch each year.

The fourth and perhaps most underappreciated bull case is platform optionality. A network of hundreds of branches, each staffed, secure, trusted, and frequented by customers who are, by definition, in the middle of making a financial decision, is an unusually valuable physical footprint. Could Aurora, over time, distribute adjacent financial products—insurance, savings programs, remittances, other secured lending products—through the same network? There is no disclosed plan for this today. There is also no structural reason it could not happen.

So what should an investor actually track? Among the many metrics, two or three stand out as the real signal. The first is the growth rate of the consignment/lending book, both in absolute terms and relative to retail jewelry revenue. This directly measures the pace of the fintech pivot. The second is the net interest margin on that book, because margin compression would be the first signal that competitive dynamics are shifting. The third, more qualitative but important, is store productivity on a blended retail-plus-lending basis, rather than retail alone, because that is the number that expresses the whole thesis. Whether analysts will continue to disaggregate and publish those numbers is itself a test of how well the market understands the business.

A quick myth-vs-reality check is worth doing here, because this is a business that is consistently described in the Thai market in terms that do not quite capture what it is. The consensus myth, even today, is that Aurora is a gold jewelry retailer whose earnings move with the gold price and the Thai retail cycle. The reality, visible in segment disclosures, is that a growing and now substantial share of gross profit comes from financial services, that the retail side is better understood as an origination and sourcing channel for the financial services side, and that the multiple investors pay should, in principle, reflect this blended nature. Whether the market is pricing this correctly at any given moment is not something we will opine on; we will only say that investors who understand the business on its actual terms are operating with a different model than those who continue to treat it as a retail stock.

X. Conclusion & Final Reflection

Step back for a moment and look at the long arc.

In 1973, a family in Yaowarat opened a gold shop. They did what gold shops had done for generations. They sold jewelry by weight, they bought back when they could, they kept meticulous manual records, and they hoped the next generation would inherit a respected name. By the standards of 1973 Thailand, that was the definition of a successful family business.

Half a century later, that shop has become something that nobody, in 1973 Yaowarat, could have predicted. It is a listed public company with hundreds of branches in every major Thai mall. It is quietly operating one of the largest asset-backed consumer lending businesses in the country. It is building digital channels that reach Thai consumers who may never walk into one of its physical stores. It is integrating vertically across design, retail, buyback, and financing in a way that makes it structurally different from every other gold shop on the national map.

The most compact way to summarize Aurora is this. The company took the oldest trade in human history—the trade in gold—and applied two disciplines that the trade had never been fully subjected to: modern retail and modern finance. The first discipline gave them a brand, a network, and a customer funnel. The second discipline gave them a lending engine, a margin structure, and a flywheel. The two disciplines, stacked together, turned a commodity into a proprietary asset and a family shop into a piece of financial infrastructure.

When you walk past the red-and-gold beacon in a Bangkok mall on your next visit, here is what you are actually looking at. You are looking at a retail brand whose product is trust. You are looking at a financial services company whose branches are jewelry stores. You are looking at the modern expression of a very old human instinct—the instinct to hold wealth in the palm of your hand—translated into a business model that compounds quietly, over decades, on a flywheel of customer acquisition, collateral recirculation, and generational loyalty.

The next time someone tells you that fintech is about apps and payments rails and neobanks, tell them about the shop in the mall where grandmothers pawn wedding necklaces under spotlights, and where the CEO's grandfather would not have believed what the family company has become.

You are not looking at a jewelry store. You are looking at a financial services company dressed in a jewelry box.

XI. Top Links & References

- Aurora Design Public Company Limited, Annual Report and Form 56-1 One Report filings, available via the Stock Exchange of Thailand disclosure portal.

- Gold Traders Association of Thailand, historical daily gold price data and industry commentary on the Thai 96.5 percent purity standard.

- Academic and historical studies of the Yaowarat gold trade, including work on Thai-Chinese merchant families and the evolution of Bangkok's commercial districts.

- Research on Thai consumer behavior regarding physical gold as a household savings instrument, including surveys published by Thai financial regulators and consumer research firms.

- Comparable company disclosures from Srisawad Corporation (SAWAD) and Muangthai Capital (MTC) for context on the Thai specialty finance and collateralized consumer lending landscape.

- Bank of Thailand regulatory bulletins regarding non-bank lender supervision and disclosure frameworks.

- Stock Exchange of Thailand historical filings relating to Aurora's 2022 initial public offering, including prospectus materials and post-listing investor communications.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube