ASX Ltd: The Unlikely Monopolist of the Southern Hemisphere

I. Introduction: The Paradox at the Heart of Australian Finance

Picture a company so embedded in a nation’s financial life that nearly every IPO, every everyday share trade, and a huge portion of retirement savings ultimately depends on its systems working flawlessly. Now add one twist: that company is listed on the very exchange it runs.

That’s ASX Ltd. It sits in a rare position in global finance—operator and participant, gatekeeper and client. It helps enforce the rules of the market, while also living under them. In plain terms, it’s the referee… and it’s on the field.

By the numbers, ASX is enormous. It oversees an Australian market with average daily turnover of about A$4.685 billion and a total market capitalisation around A$1.6 trillion—big enough to place it among the world’s major exchange groups, and the largest in the southern hemisphere. But the real story isn’t scale. It’s structure.

Because the question isn’t “how did ASX get big?” The question is: what happens when a country’s market plumbing is effectively controlled by one company—and that company starts acting like nothing can really threaten it?

That tension shows up again and again in ASX’s modern history. When a foreign exchange tried to buy it, politicians stepped in and called it a matter of “national interest.” When ASX staked its crown-jewel settlement system on a bold new technology direction and stumbled, the fallout wasn’t just an internal project failure—it turned into a public trust issue, with regulators eventually stepping in.

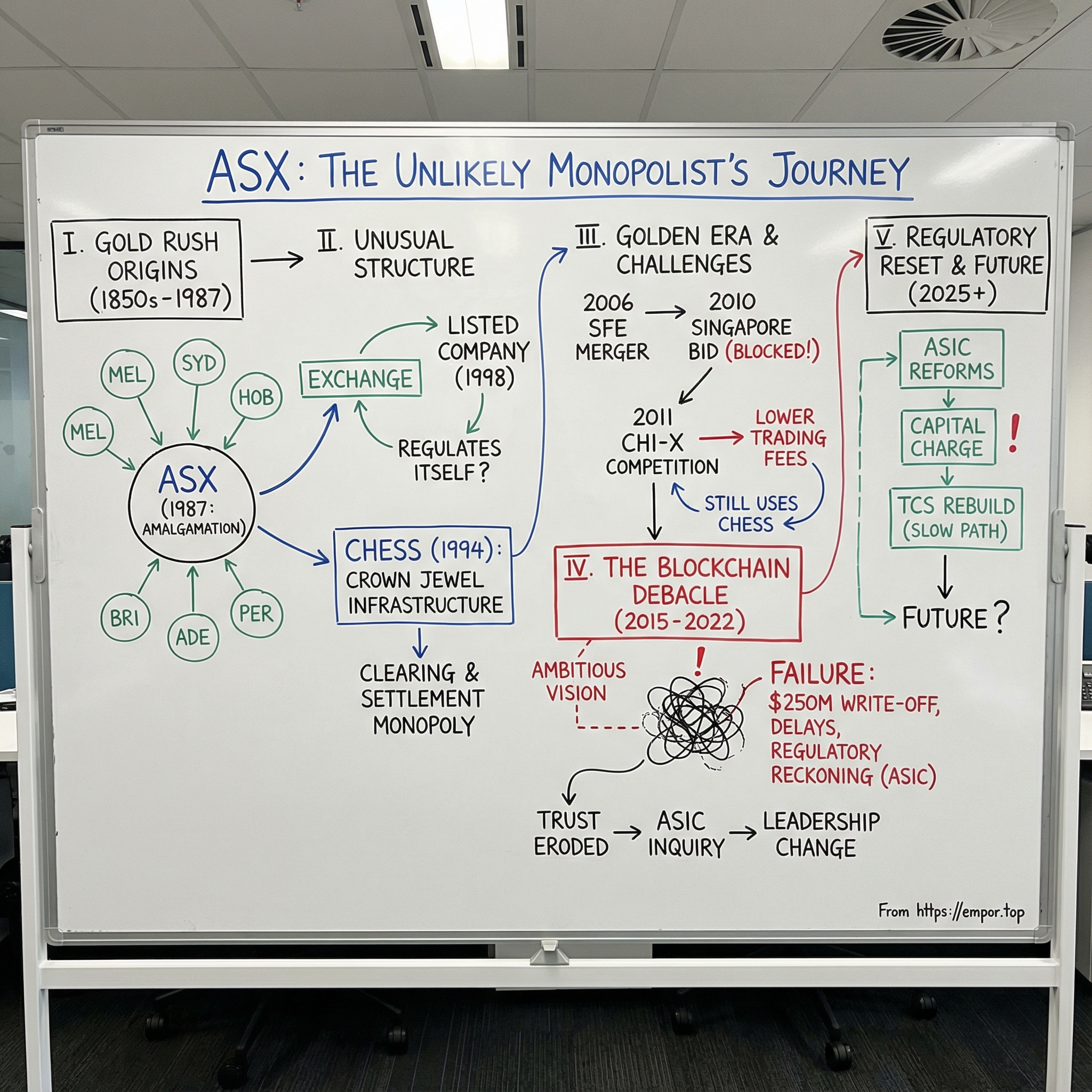

The roots of that power go back to a deliberate decision. ASX, as we know it, was created on 1 April 1987, when the Australian Parliament incorporated a new national exchange by amalgamating six state-based securities exchanges into one. That act didn’t just streamline a fragmented market. It produced something unusually concentrated: a single, unified hub for Australian equities infrastructure.

That’s the thesis of this story. Australia’s decision to consolidate what had been a patchwork of state exchanges created one of the world’s most profitable financial infrastructure businesses. But the same conditions that made ASX formidable—its centrality, its regulatory moat, its lack of true end-to-end competition—also made it vulnerable to complacency. And complacency, in critical infrastructure, is expensive.

Over the course of this deep dive, we’ll move from gold-rush-era exchanges in colonial outposts to the first exchange in history to list on itself. We’ll walk through the $8.4 billion merger that might have reshaped Asia-Pacific capital markets, and then into the technology bet that turned into a reputational crisis—one that cost shareholders roughly a quarter of a billion dollars and put ASX’s credibility on the line.

ASX’s story is ultimately a story about monopoly power in the most sensitive place possible: the machinery of trust. And what happens when that machinery starts to wobble.

II. The Gold Rush Origins: When Six Became One

Colonial Capitalism Rises from the Goldfields (1851-1890)

To understand ASX, you have to start with gold—and with how fast gold turned a scattering of British colonies into something that suddenly needed real capital markets.

In the 1850s, Victoria was the epicentre of Australia’s gold rush. The population surge was dizzying: from roughly 80,000 people in 1851 to around 540,000 a decade later. This wasn’t a gentle swell. It was a stampede. Ships arrived packed with fortune-seekers. Boomtowns spread outward. New businesses sprang up to sell picks, shovels, food, lodging—anything you could charge for when half the world was convinced there was gold in the ground with their name on it.

And once people started staking claims, the next thing they needed was capital.

That’s the practical origin story of Australia’s first stock exchange, formed in Melbourne in 1861. It wasn’t born out of abstract ideals about “efficient markets.” It was a tool. Prospectors and mining ventures needed funding. Investors wanted a way to get exposure to the gold boom without going into a mine themselves. An exchange became the meeting point between the two.

The early markets were physical and noisy. Brokers clustered around “posts” on the trading floor where certain stocks were traded. Employees known as “chalkies” wrote bids, offers, and completed sales in chalk on blackboards—prices literally appearing through dust and elbow grease. Paper certificates changed hands. Voices carried the market.

From there, the pattern repeated across the continent. Separate exchanges were established in the state capitals: Melbourne (1861), Sydney (1871), Hobart (1882), Brisbane (1884), Adelaide (1887), and Perth (1889). Each colony built its own marketplace, shaped by distance, local politics, and the reality that Australia was less a single economy than a set of far-flung regional ones.

Some of Australia’s most iconic corporate stories grew up alongside these exchanges. The Broken Hill Mining Company—founded by a syndicate of seven men from the Mount Gipps Station—was incorporated two years later as the Broken Hill Proprietary Company Limited, better known as BHP. In 1885, BHP listed on the Melbourne Stock Exchange. It’s hard to overstate the symbolism: the country’s future corporate titan and the country’s market infrastructure starting to lock into place at the same time.

The Path to National Unity (1903-1987)

For decades, these exchanges ran like separate fiefdoms. Listing in one city didn’t automatically open the door to investors in another. Brokers operated under different rules depending on the exchange. It was messy and inefficient—but it also matched Australia’s pre-Federation identity: regional, political, and fragmented.

The first real attempt at coordination came in the early 20th century. From 1903, the state stock exchanges met informally. Then in 1937, those meetings solidified into the Australian Associated Stock Exchanges (AASE), with Sydney taking the lead in formalising the group the year before. The AASE created more uniformity—common listing rules and standardised commissions—but it didn’t create one exchange. The states still held their own turf.

True consolidation took another fifty years, and it arrived when multiple forces hit at once.

By the 1980s, financial deregulation was reshaping markets across the developed world. Electronic trading was making geography feel increasingly irrelevant. And Australia’s superannuation system was beginning the long transition into the powerhouse it would become—creating a growing, steady pool of retirement savings that needed deep, liquid markets to put money to work.

The result was the Australian Stock Exchange: a national exchange created on 1 April 1987 through Commonwealth legislation. The Australian Stock Exchange and National Guarantee Fund Act 1987 didn’t just tidy up a fragmented system. It effectively rewired Australia’s market structure.

Getting there took real political and institutional negotiation. Each state exchange had its members, its physical footprint, its entrenched relationships, and its own way of doing things. Bringing them under one roof meant bargaining over rules, governance, and whose norms would win. The timing mattered, too: ASX launched only months before the October 1987 crash—a brutal early stress test for a brand-new institution.

But the bigger consequence was structural. Australia ended up with something unusually concentrated: a unified monopoly at the centre of an entire developed nation’s equity market. The United States had multiple major exchanges. Europe stayed fragmented for far longer. Australia, partly through geography and partly through political timing, created one national hub—an exchange that would become immensely profitable, and incredibly hard to dislodge.

III. The Pioneer: First Exchange to List on Itself

The Demutualisation Revolution (1996-1998)

For most of their history, stock exchanges weren’t really “companies” in the modern sense. They were mutuals: clubs owned by the brokers who used them, run to serve those members. That made perfect sense when trading meant showing up on a floor and yelling orders across a crowd.

But once trading started moving onto screens, the exchange stopped being a room and became a technology business. And technology businesses need capital—big, steady investment in systems, security, and scale. The old club model started to creak.

In 1996, ASX’s members voted to demutualise. The exchange was incorporated as ASX Limited, and in 1998 it took the final, almost surreal step: it listed on its own exchange, with the Australian Securities & Investments Commission enforcing the listing rules for ASX Limited.

That decision carried a philosophical flip. Before, the exchange existed to serve broker members. After, it existed to serve shareholders. A dollar saved through efficiency wasn’t automatically a dollar returned to members through lower fees; it could now become profit.

ASX became the first exchange in the world to quote its own shares on its own market, listing on 14 October 1998. And that created a governance paradox that still defines it: ASX writes listing rules that it must follow. It monitors market conduct, including its own. When ASX releases an announcement that moves its share price, it is, at the same time, an issuer and the operator of the market reacting to it.

The financial logic worked. In the years after demutualisation, ASX operated as a for-profit, shareholder-owned entity with easier access to capital for infrastructure and operations. Research on the period showed a sharp improvement in profitability, including return on assets rising from about 2.5% before demutualisation to above 10% over the following five years.

The payoff wasn’t just bigger profits. It was optionality. Being a listed company gave ASX a new currency—its own stock—to fund acquisitions and big strategic moves.

CHESS: The Crown Jewel Infrastructure

To understand ASX’s real moat, you have to understand CHESS.

CHESS—the Clearing House Electronic Sub-register System—rolled out in 1994. It replaced paper certificates with electronic settlement and an issuer subregister. Settlement began at T+5 and later shortened, cutting processing friction and operational risk along the way.

It’s hard to overstate what CHESS actually is: the integrated clearing and settlement backbone for Australian equities at the client account level. It handles the machinery behind the trade—clearing, settlement, depository functions, and registry services—inside a secure system that’s become deeply embedded in how the entire market operates.

And here’s the key point: in Australia, trades don’t truly “finish” until they run through CHESS.

That creates a very particular kind of power. A broker can route orders to competing venues, but when it’s time to clear and settle, those trades flow back through ASX’s infrastructure. Even when Chi-X launched in 2011 to compete with ASX on trading, it still depended on ASX’s clearing and settlement rails. Chi-X—now Cboe Australia—became both competitor and customer.

This is lock-in at the infrastructure layer. The legal ownership of shares, the movement of cash against securities, the shareholder records—all of it sits on CHESS. Unwiring from it isn’t like switching software vendors; it’s like trying to replace the foundation of a building while the building is still occupied. And as competition grew, CHESS didn’t become less relevant—it became the toll road everyone still had to drive on, including the alternative venue that, on its own, handled close to A$2 billion a day in trades.

Building the Modern Exchange (2000-2006)

By the early 2000s, ASX had done two things that transformed it from an institution into a modern exchange group: it had become shareholder-owned, and it had built critical market infrastructure that everything else depended on. Next came expansion.

In 2000, ASX replaced the All Ordinaries Index with the S&P/ASX 200. On paper, that sounds like a branding refresh. In reality, it was a power move. The S&P/ASX 200 quickly became the benchmark institutions cared about: the index superannuation funds tracked, the one futures contracts referenced, the one the media reported every day. Partnering with Standard & Poor’s gave the index global credibility—and made ASX’s definition of “the market” the one everyone used.

Then, in 2006, ASX merged with the Sydney Futures Exchange. Announced on 27 March 2006 as an all-stock deal, it created a vertically integrated operator spanning equities, derivatives, and the post-trade stack. The Australian Competition and Consumer Commission approved the merger on 24 May 2006, pointing to the complementary nature of the two markets and minimal anti-competitive effects.

Strategically, the merger broadened ASX from a cash equities exchange into a multi-asset platform, adding futures, options, and over-the-counter derivatives through what became the ASX 24 platform. It also diversified the business into higher-margin post-trade services, with derivatives growing from about a fifth of turnover before the deal to more than 30% by 2010.

By 2006, ASX wasn’t just a marketplace. It was a fortress: equities trading, derivatives, clearing, settlement, and the benchmark index at the centre of institutional Australia. Its systems were so embedded that even competitors had to plug into them.

So the obvious question wasn’t whether ASX could defend itself. It was what the next real threat would look like—competition at the edges, or a foreign buyer trying to take the whole thing.

IV. The Singapore Gambit: The $8.4 Billion "What If"

The Offer That Could Have Changed Everything (October 2010)

By the end of the 2000s, the exchange business had turned into an arms race for scale. Across the world, big venues were trying to stitch themselves together—London talking to Canada’s TMX, Deutsche Börse circling NYSE Euronext. The pitch was always the same: bigger footprint, more products, more liquidity, lower unit costs.

In that environment, the Singapore Exchange saw a once-in-a-generation opening. In late October 2010, SGX and ASX announced they’d entered into a merger agreement that would create Asia’s second-largest exchange group, behind Hong Kong Exchanges and Clearing. SGX’s offer valued ASX at the equivalent of about US$8.8 billion.

The logic, on paper, was hard to argue with. SGX wanted reach. Australia offered a deep, sophisticated investor base, including institutions and hedge funds—and, most importantly, a superannuation system that had created an odd global outlier: a country with a relatively small population, but an enormous, largely domestic pool of retirement capital.

For Singapore, buying ASX meant plugging into that pipeline. For ASX, the deal promised access to faster-growing Asian markets and the benefits of scale in a consolidating industry. If you believed exchanges would keep merging until only a handful remained, this was ASX getting ahead of the wave rather than being swallowed by it later.

The Political Battle

Then the deal collided with a different reality: ASX isn’t just a business. It’s national infrastructure.

In April 2011, Australian Treasurer Wayne Swan blocked the merger on national interest grounds. His argument was blunt: foreign ownership of an entity so dominant in clearing and settlement would raise economic sovereignty issues, and create material supervisory and regulatory risks. It was the kind of direct political intervention Australia rarely used—something not seen since the Howard government stopped Royal Dutch Shell’s bid for Woodside in 2001.

The government’s concerns weren’t abstract. One sticking point was Temasek’s 23.5% stake in SGX. Even if Temasek wasn’t “running” the exchange day-to-day, the optics of Australia’s market plumbing being controlled—indirectly—by a foreign government-owned investor set off alarms.

There were also structural hurdles. The deal would have required special legislation to move past the usual 15% ownership limit for a single holder of a financial institution. And, inevitably, there was the fear—spoken and unspoken—that high-value jobs and decision-making would drift north to Singapore.

On 8 April 2011, Swan made it official: no deal. SGX withdrew and went looking for growth elsewhere.

The Road Not Taken

The rejection echoed for years. At a time when exchanges globally were joining forces to spread fixed costs, ASX stayed put—protected, independent, and still sitting atop the most valuable asset in Australian market infrastructure: clearing and settlement.

Critics called it a strategic own goal. Professor Alex Frino argued the decision signaled that Australia was unwilling to embrace global markets—that it wanted the prestige of being a regional financial centre while stepping away from the very combinations that could create one.

But there’s a counterpoint that matters just as much: for ASX itself, the block may have been a gift.

Instead of becoming part of a Singapore-controlled group, ASX kept its monopoly position intact. And the decision sent a message to every would-be acquirer worldwide: this isn’t a normal target. The value here isn’t just earnings and market share—it’s the implicit political and regulatory protection that comes with being “too important” to sell.

For investors, that was the real reveal. ASX sits at the intersection of national interest and commercial enterprise. That positioning can be incredibly stabilizing. But it also creates a different kind of risk: dependence on government goodwill, regulatory relationships, and the assumption that the moat stays protected. Those aren’t line items you can model cleanly—but they’re core to understanding what ASX is, and why it has been able to remain so dominant for so long.

V. Enter the Challenger: Chi-X Breaks the Monopoly

Competition Finally Arrives (October 2011)

For twenty-four years after the 1987 amalgamation, ASX had the Australian equities trading business to itself. That run ended in October 2011, when Chi-X Australia launched as a rival venue for trading ASX-listed shares.

And the mere threat of that launch was enough to change behavior.

Before Chi-X even executed its first trade, ASX moved to protect its turf by cutting prices. Trading fees dropped from 0.28 basis points to 0.15 basis points per side—nearly halved. Competition, even in preview mode, was already doing its job.

Chi-X began small, with just eight stocks available to trade. But it leaned on fast technology and aggressive pricing and quickly proved there was room for an alternative. One study estimated Chi-X delivered about $215 million in net benefits to the market in its first year, largely through lower trading costs.

Over time, that foothold turned into real share. By January 2024, the venue that started with eight names had grown to more than 21% market share in cash equities. Today it operates as Cboe Australia, running on Cboe’s global matching engine technology.

The Competitive Dynamic

Here’s where Australia’s market structure gets wonderfully strange.

Cboe Australia now handles roughly a fifth of total equity market turnover—close to $2 billion in trades a day. It’s been in the market since 2011 as Chi-X, and in June 2021 it was acquired by Cboe Global Markets, bringing it into the orbit of one of the world’s largest exchange operators.

But for all that trading success, Cboe’s trades still have to clear and settle through ASX’s CHESS system. In other words: the competitor is also the customer.

That single fact explains a lot about why ASX’s moat has been so durable. ASX can lose some trading revenue as orders migrate to a cheaper venue, then still earn clearing and settlement revenue when those trades come home to CHESS. So yes—competition in execution pushed fees down, improved service, and forced innovation, exactly as economic theory would predict. But because ASX remained vertically integrated at the post-trade layer, the most defensible, highest-stakes part of the stack stayed effectively unchallenged.

The Cboe Takeover and New Era

Cboe’s 2021 acquisition of Chi-X didn’t just bring deeper pockets. It brought credibility—and eventually, regulatory permission to widen the battlefield.

ASIC approved Cboe Australia’s listing market application on 7 October 2025. ASIC also said it would work closely with Cboe throughout the sale process to promote an orderly transition of Cboe Australia to a suitable buyer.

ASIC’s view was straightforward: competition has delivered innovation, resilience, greater liquidity, and lower costs, benefiting investors, companies, and the broader economy. In that framing, Cboe hasn’t been a nuisance—it’s been an important counterweight.

The biggest implication is what comes next. With approval to operate as a listing market, Cboe can now compete for IPOs, not just secondary trading. That’s a meaningful escalation, because listings are about more than fees—they’re about brand, prestige, and where companies believe they’ll get the deepest investor attention.

Whether issuers will actually choose a challenger venue when ASX’s liquidity pool and identity are still so dominant is an open question. But for the first time in modern Australian market history, they have a real choice. And for ASX shareholders, that turns a decade-old story—trading fee pressure—into something broader: pressure on the franchise itself, and on how ASX competes on service, pricing, and innovation from here.

VI. The Blockchain Debacle: When Innovation Becomes Hubris

The Bold Vision (2015-2017)

By the mid-2010s, CHESS had done its job for two decades. It was stable, deeply integrated, and trusted—but it was also old. A replacement wasn’t optional. The only real question was what ASX would replace it with.

ASX’s answer was the most ambitious one available. In December 2017, it announced it would replace the CHESS equities clearing and settlement system with a blockchain-style distributed-ledger platform built with Digital Asset Holdings LLC, led by former JPMorgan banker Blythe Masters. The exchange said the new post-trade system would go live by the first quarter of 2021.

The industry reaction was electric. A major exchange group was effectively saying: we’re going to run national market infrastructure on distributed ledger technology, and we’re going to do it first. The plan had been flagged as early as 2016, and it was widely treated as a milestone moment—an early, high-profile endorsement of DLT for something mission-critical.

ASX didn’t frame this as routine maintenance. Management described it as “innovative re-engineering,” promising lower costs for participants, new functionality, and a position at the cutting edge of financial market technology.

The Slow Motion Disaster (2018-2022)

At first, it looked like a familiar story: a big project, moving slower than hoped. Then the delays started stacking up—and the explanations started to sound less like “complexity” and more like “loss of control.”

In March 2020, ASX pushed the planned April 2021 launch. On 30 June 2020, it delayed again, shifting the target by another year to April 2022. Eventually, by the end of 2021, the project was carrying a “red” status internally—meaning material delivery risk against the required timeframe. In early February 2022, the ASX audit and risk committee was informed of that rating.

And then came the moment that turned a troubled technology program into something much bigger.

On 10 February 2022, ASX made public statements saying the CHESS replacement remained “on-track for go-live” in April 2023 and was “progressing well.” Six weeks later, ASX announced a likely delay. That gap—between the optimistic statements and the rapid reversal—became central to what followed.

Accenture’s independent review landed like a wrecking ball. Specifications and milestones had repeatedly shifted. A formal design was never completed. ASX and Digital Asset operated in silos without a shared understanding of what they were building. And the project’s core objectives were never properly formalised before major work began.

In November 2022, after around seven years of effort, ASX shelved the original blockchain-based CHESS replacement. It wrote off roughly A$255 million (about $170 million pre-tax), effectively admitting the world-first had become a world-class failure.

Regulatory Reckoning

Once CHESS replacement became a trust issue, the regulator couldn’t ignore it.

ASIC commenced proceedings in the Federal Court against ASX Limited, alleging ASX made misleading statements about the CHESS replacement project. The focus was the 10 February 2022 announcements: that the project was “on-track for go-live” in April 2023 and “progressing well.” ASIC alleges those statements implied the project was tracking to ASX’s plan and would meet its future milestones.

ASIC Chair Joe Longo put the stakes plainly: “ASX’s statements go to the heart of trust in the integrity of our markets.”

“We believe this was a collective failure by the ASX Board and senior executives at the time. Companies and market participants rely on what the ASX says about its operations to make their own decisions and investments.”

The scrutiny wasn’t limited to CHESS. On 7 March 2024, ASIC said ASX had paid a $1,050,000 penalty after an investigation into its compliance with market integrity rules, in a separate matter related to order information transparency—another reminder that, for regulators, ASX’s operational discipline isn’t a nice-to-have.

In August 2024, ASIC sued ASX after a long investigation into the CHESS replacement disclosures. The case remains in the Federal Court.

The Restart with TCS

After scrapping the blockchain build and absorbing the write-off, ASX still had the same underlying problem: CHESS wasn’t getting any younger, and the market still needed a credible path to replacement.

ASX’s reset was a pivot away from “world-first” and toward “proven product.” In November 2023, it announced it would proceed with a product-based solution design to replace CHESS. Tata Consultancy Services (TCS) was selected to deliver the solution using its TCS BaNCS Market Infrastructure product, a modular platform for clearing and settlement. Accenture was chosen as a delivery partner to add capability, capacity, and industry expertise.

TCS BaNCS is used for clearing and settlement by the New Zealand Stock Exchange, as well as national exchanges in South Africa and Finland. Even with a more established technology base, ASX chief executive Helen Lofthouse warned the implementation would be lengthy—potentially leaving the legacy system in place until 2032.

ASX planned the rollout in two releases: Release 1 for clearing services, then Release 2 for settlement and subregister services. Over 2024, ASX consulted extensively with industry on scope and timing. On 28 February 2025, the Release 1 Industry Test Environment opened for the AMO Build and Test phase. An indicative timeline shows a go-live date of 20 April, aligned with an April 2026 window, and a “go decision” in late March.

The lesson for investors is brutal in its simplicity. ASX tried to rebuild the most systemically important piece of Australian equity-market plumbing on an unproven approach, at a scale no other exchange had attempted. When it didn’t work, the direct financial hit was huge, but the deeper cost was credibility—with regulators, with participants, and with the people who rely on the market to settle correctly every day.

And the clock keeps running. If the replacement completes around 2028 or 2029, CHESS—built in the early 1990s—will have been in service for roughly 35 years before it’s finally retired.

VII. Porter's Five Forces & Hamilton's Seven Powers Analysis

Understanding ASX's Competitive Position

To make sense of ASX as a business, it helps to separate two different questions.

First: what does the industry structure look like—who has power over whom, and where do profits naturally pool? That’s where Porter’s Five Forces is useful.

Second: what are ASX’s specific, durable advantages—if it’s so entrenched, what are the actual mechanisms that keep it that way? That’s where Hamilton Helmer’s Seven Powers comes in.

Together, they explain why ASX has been able to look almost unassailable for decades… and why the cracks that have appeared in the last few years matter so much.

Porter's Five Forces

Threat of New Entrants: LOW

Running an exchange isn’t like launching an app. You need an ASIC licence, serious capital, and a compliance machine that never sleeps. But the real barrier is simpler and more brutal: liquidity.

Markets are winner-take-most. Traders go where the other traders are. Liquidity begets liquidity, and without it, spreads widen, execution gets worse, and participants leave. That makes it extraordinarily hard to bootstrap a new venue against an incumbent unless you have either heavy regulatory help or a willingness to lose money for a very long time.

Cboe Australia has proven entry is possible at the margin—it’s now around a fifth of equity turnover. But even after more than a decade in-market, it still has no share of clearing and settlement. That’s the key point: the challenger can take slices of trading, but the deepest moat sits underneath the trade.

Regulators are also clearly more supportive of competition than they were in the past. ASIC approved Cboe Australia’s listing market application on 7 October 2025, opening up a new competitive front: IPOs and primary listings, not just secondary trading.

Bargaining Power of Suppliers: LOW

ASX buys technology, data-centre capacity, and professional services like everyone else. But it buys them as a large, regulated, well-capitalised customer with options.

The CHESS replacement saga underlined that dynamic. When ASX lost confidence in Digital Asset’s ability to deliver, it walked away and reset with TCS. For most suppliers, ASX is a prized client—but not an irreplaceable one. And ASX can switch.

Bargaining Power of Buyers: MODERATE

ASX’s customers fall into a few buckets, and they don’t all have the same leverage.

Listed companies need a listing venue, and for most Australian-focused issuers the ASX remains the default choice because that’s where the domestic institutional capital is. Brokers need access to the main liquidity pool, which means connecting to ASX is non-negotiable. Retail investors have essentially no bargaining power at all.

Where the leverage shows up is with large institutional investors and high-volume traders. They can route order flow to Cboe, and that gives them some influence—mostly on trading fees. And in theory, the biggest companies could consider listing overseas in places like Singapore, Hong Kong, or London, but those alternatives come with real regulatory and practical friction if the goal is to stay plugged into Australian investors.

Threat of Substitutes: LOW-MODERATE

There are substitutes, but none that fully replicate what ASX provides.

Private markets are growing, but they’re not a replacement for deep, liquid public equity trading. Crypto and DeFi can move money fast, but they don’t provide a regulated venue for mainstream institutional securities. Overseas listings exist, but for many Australian companies they create distance from the investor base that matters most.

So substitutes can nibble at the edges. They don’t yet replace the core.

Industry Rivalry: LOW-MODERATE

In practice, Australia is close to a duopoly at the trading layer. ASX still handles the majority of volume, while Cboe has become the credible alternative. That rivalry has been real—most visibly in fees, which fell sharply once competition arrived.

But the fight is asymmetric. Trading is where the competition is; clearing and settlement is where the control is. ASX can lose some execution business and still remain the toll-collector on the post-trade highway.

Hamilton's Seven Powers

Scale Economies: STRONG

Exchanges have huge fixed costs—technology, cyber, compliance, risk management—and very low incremental costs per additional trade. Once the system is built, adding volume is cheap. That naturally advantages the largest player, because it spreads those fixed costs across the most activity.

Network Effects: VERY STRONG

This is the flywheel at the heart of every major exchange, and it’s especially potent here.

Liquidity attracts liquidity. Listings attract investors. Investors attract more listings. And the data produced by the market becomes more valuable as participation grows. These effects compound over time, making it incredibly hard for a challenger to win the centre of gravity without years—or decades—of sustained effort.

Counter-Positioning: MODERATE

ASX’s incumbency makes some forms of disruption difficult. In highly regulated market infrastructure, “move fast and break things” isn’t a viable operating model.

But there’s a twist: incumbents can also hurt themselves by trying to preempt disruption too aggressively. ASX’s attempt to jump early onto distributed-ledger technology for CHESS is the cautionary tale here. Trying to “future-proof” the moat with an unproven approach didn’t weaken competitors—it weakened trust in the incumbent.

Switching Costs: VERY STRONG

CHESS is the ultimate switching-cost engine.

The market’s plumbing—broker systems, issuer processes, shareholder records, regulatory reporting—has been built around ASX’s interfaces and settlement workflows for decades. Changing that isn’t like migrating software; it’s rewiring the financial system while it’s running. That’s measured in years, and the bill is measured in billions.

Branding: MODERATE

ASX is, for many people, the Australian share market. That brand carries real weight with retail investors and provides a default sense of legitimacy for issuers and global institutions.

But brand in market infrastructure is ultimately a proxy for trust—and trust took a hit. The CHESS replacement failure, the regulatory scrutiny, and the criticism that ASX prioritised shareholder returns over investment in critical systems all eroded confidence. Over the past five years, ASX paid out a very high share of profits as dividends while technology upgrades and staffing investment were perceived to lag. Whether that interpretation is fully fair or not, the reputational impact is real.

Cornered Resource: STRONG

CHESS is not just an advantage—it’s a cornered resource.

ASX is the monopoly provider of clearing and settlement for Australian cash equities, and it’s obligated to keep those services reliably available. That position is reinforced by long-built regulatory relationships and the practical reality that the system sits at the centre of market functioning.

Process Power: DAMAGED

For a long time, ASX’s process power—its operational competence in running critical infrastructure—was part of the story. Then the CHESS replacement program exposed serious weaknesses: project governance, vendor oversight, risk management, and how leadership communicated delivery confidence.

The June 2025 inquiry led by an expert panel put that bluntly, identifying shortcomings in governance, capability, risk management, and culture that required urgent attention. ASX still has expertise and scale. But the idea that it will always execute well simply because it’s the incumbent no longer holds.

VIII. The Regulatory Reset: December 2025 and Beyond

The ASIC Inquiry Findings

By December 2025, years of unease had crystallised into something formal: a regulator-led reset aimed at restoring confidence in ASX and Australia’s critical market infrastructure. ASIC released the interim report from the Inquiry into the ASX Group—an inquiry announced in June 2025 and led by an expert panel—and paired it with a package of measures designed to give the market clarity on what “fixing this” would actually mean.

The panel’s diagnosis was uncomfortable and direct. It identified shortcomings in ASX’s governance, capability, risk management, and culture—issues it said required urgent attention and response.

This wasn’t a light-touch review. The inquiry conducted around 140 stakeholder interviews, reviewed written submissions, undertook international benchmarking, held staff focus groups, and examined nearly 10,000 documents.

And ASIC’s message was blunt: some progress had been made, but it wasn’t enough. As ASIC put it, “more of the same is not an option.” The report argued the transformation required was too large to be delivered through tactical, incremental changes or business as usual.

The Reform Package

ASIC’s response matched the tone of the findings: sweeping, structural, and expensive.

A $150 million capital charge would be implemented by 30 June 2027, and held until work under ASX’s “Accelerate” program was completed to ASIC’s satisfaction. ASIC also imposed an additional $150 million capital charge on ASX Limited, aimed at ensuring ASX maintained robust financial resources until remediation was complete.

The reform package focused on two big moves. First: tightening the independence and governance of ASX’s clearing and settlement functions. Second: forcing a strategic reset of Accelerate, ASX’s multi-year transformation program.

ASX committed that the boards of the clearing and settlement facility licensees would be “fully comprised of only independent, non-ASX Limited directors.” ASX said it would implement this via an orderly board renewal process, supported by dedicated resources and clearly defined shared-services arrangements across the broader ASX group.

The financial implications were real. The higher regulatory capital requirement would weigh on returns: ASX revised its medium-term underlying ROE target range to 12.5% to 14.0%, down from 13.0% to 14.5%. ASX also flagged its FY26 expense profile would rise due to additional operating costs tied to responding to the ASIC inquiry.

Leadership Response

Helen Lofthouse had been in the CEO seat since August 2022—arriving after the CHESS replacement saga had already unravelled, and then leading the pivot to the TCS-based rebuild. She joined ASX in September 2015 and had held multiple senior executive roles before taking the top job. Before ASX, she was based in London, including time as a managing director at UBS and earlier roles at JPMorgan.

Her background was in cash equity and debt markets, listed and OTC derivatives, and clearing and settlement—deep market infrastructure experience, even if not a pure “enterprise technology transformation” profile. In an organisation whose existential risk had become technology modernisation, that could be read as an imperfect fit. But ASX’s challenge by 2025 wasn’t just technical delivery. It was credibility. And her relationships with regulators and market participants mattered in navigating the inquiry process.

ASIC Chair Joe Longo framed the moment as a line in the sand. Urgent action was needed, he said, to set ASX on the right path. ASX needed to embrace “a new era of accountability, investment, and stewardship” to rebuild confidence and meet the expectations of the market and the Australian public.

He also made one thing clear: there would be no quick fixes. Many of the problems, the report found, took years to develop. Some immediate actions would land fast, but the core issues would take time and resources to resolve. No shortcuts.

IX. Financial Performance and Investment Considerations

Recent Results

Even with the noise of inquiries, write-offs, and rebuilds, the underlying business kept doing what market infrastructure businesses tend to do: collect tolls.

Operating revenue rose to $1.11 billion, driven by growth across Markets, Technology & Data, and Securities & Payments. Listings revenue was steady, with early signs that IPO and listing activity was starting to thaw.

ASX also continued to lean into what many shareholders have come to expect: a high payout. The fully franked dividend payout ratio was 85%, and the total dividend per share for FY25 was 223.3 cents, up 7.4%. For income investors, that reliability is part of the appeal. The catch is that the new capital charge requirements are designed to change the balance between “pay it out” and “reinvest it,” which may put natural limits on future payout ratios.

Trading activity, meanwhile, stayed lively. Early FY26 opened with strong cash-equities momentum: total value traded in July 2025 was up 20% versus July 2024, helped by shifting expectations around interest-rate cuts and bursts of volatility tied to geopolitical events. Derivatives were softer: total futures and options-on-futures volumes fell 5% year over year in July 2025.

The Investment Thesis: Bull vs. Bear

The Bull Case:

ASX is still one of the most defensible businesses in Australian finance. The network effects in liquidity reinforce themselves, the switching costs are enormous, and the clearing-and-settlement monopoly remains effectively intact. Competition has pressured trading fees, but it hasn’t broken the underlying economics of the franchise—especially because so much of the system still runs through ASX’s post-trade rails. And Australia’s superannuation system continues to grow, steadily pushing more capital into markets that ASX, structurally, remains at the centre of.

There’s also a version of this story where the regulatory reset becomes a long-term positive. Forced investment, stronger governance, and a more disciplined modernization program could leave ASX more resilient than the version that tried to “innovatively re-engineer” CHESS with an unproven approach. The TCS rebuild, while slower than the original blockchain vision, is framed as the more achievable path.

In that light, the pitch is simple: investors get a critical national infrastructure asset with strong cash generation, limited true end-to-end competition, and a historically reliable dividend stream—though one that may be moderated as capital requirements rise.

The Bear Case:

ASX is also a case study in what can happen when a monopolist starts to lose its edge.

Regulators’ critique was not just that CHESS replacement failed—it was that, over time, ASX prioritised shareholder returns while under-investing in the stability and renewal of critical infrastructure. Over the past five years, ASX paid out 88% of underlying profit and 95% of statutory profit as dividends, even as technology upgrades and staffing investment were perceived to lag.

CHESS itself is old by modern technology standards. The abandoned blockchain program burned years and roughly $250 million while the legacy system kept aging underneath it. And not everyone is convinced the restart is the clean fix: critics argue the TCS replacement is moving too slowly and costing too much, and question whether the program team has enough deep capital-markets infrastructure experience. With a timeline that leaves CHESS in place for several more years, those critics worry the market is being asked to accept extended exposure to outage and delivery risk—and ask whether the board has truly absorbed the governance lessons of the first failure.

Regulatory scrutiny, too, has intensified rather than faded. In mid-June, ASIC said it would commence a compliance assessment and inquiry into how well ASX is meeting its obligations as both a market licensee and a clearing and settlement licensee. It also appointed an expert panel to examine governance, capability, and risk management frameworks across the group. This is broad, deep oversight—exactly the kind that reduces strategic freedom and raises operating cost.

And then there’s competitive pressure. Trading competition continues to grind down high-margin execution revenue. With Cboe now approved to operate a listing market, competition has the potential to spread into what was once ASX’s most protected territory: winning the listing in the first place. Finally, the $150 million capital charge directly reduces the returns available to shareholders.

Key Performance Indicators to Watch

For investors tracking whether ASX is stabilising—or slipping—three indicators carry the most signal:

-

CHESS Replacement Progress: The TCS program milestones are the clearest proxy for execution credibility—Release 1 clearing go-live targeted for April 2026, followed by Release 2 settlement and sub-register in 2028–2029. Slippage or major cost escalation would be a warning that the core problem hasn’t been fixed.

-

Market Share vs. Cboe: Watch where volume migrates. ASX still holds the majority of value traded, while Cboe has made deeper inroads in number of trades. The gap between those two metrics is a live read on how intense price competition has become and where liquidity is concentrating.

-

Listings Activity: New listings, delistings, and secondary raisings are the heartbeat of the primary market. If Cboe’s listing-market capability starts to matter—or if issuers look offshore—you’ll see it here first.

X. Conclusion: The Unlikely Monopolist at a Crossroads

ASX’s story is what you get when regulatory protection and national importance create extraordinary advantages—and then demand extraordinary stewardship in return.

It began in gold-rush chaos, matured through federal consolidation, and was later shielded from foreign takeover on “national interest” grounds. Along the way, ASX built what would be close to impossible to recreate today: deep liquidity, entrenched market relationships, and a post-trade monopoly anchored by CHESS. It isn’t just a strong business. It’s an economic fortress with a public mission hiding inside a listed company.

And then came the lesson that monopolies keep relearning the hard way: insulation can dull urgency.

The CHESS replacement saga didn’t fail because ASX lacked ambition. It failed because ambition outpaced discipline. The project exposed weak governance, blurry accountability, and a widening gap between what was being said publicly and what was being seen internally. Once that gap became visible, it stopped being a “technology program” and turned into a trust problem—exactly the kind regulators can’t shrug off.

ASIC Chair Joe Longo described the reform package as a “circuit-breaker,” aimed at an operator that had, in ASIC’s view, underestimated the extent of change required. And ASIC’s oversight won’t be theoretical: it will work with the RBA to form a joint supervisory team dedicated to monitoring ASX’s transformation.

For investors, this is the classic infrastructure trade-off in its most intense form. The moat is real—network effects, switching costs, and CHESS’s central role. But so are the headwinds: heavier supervision, higher required capital, and a competitive perimeter that’s slowly widening. The dividend has historically been a feature, but the new capital charges are designed to shift the balance back toward resilience and reinvestment.

So the real bet isn’t “will Australia keep needing ASX?” Australia will. The bet is whether ASX can deliver a multi-year, mission-critical technology transformation under close regulatory supervision while continuing to run an aging system with near-zero tolerance for failure. That’s not a simple operating challenge. It’s a test of management execution, vendor delivery, and the market’s patience.

It also casts the 2011 Singapore merger in a different light. Blocking SGX preserved ASX’s independence—and, arguably, some of the urgency that global consolidation might have imposed. Competitive pressure can be uncomfortable, but it has a way of forcing institutions to evolve. ASX largely avoided it, and then discovered that the bill eventually comes due anyway.

Now the next chapter is being written in real time: in the TCS BaNCS migration, in ASX’s response to ASIC’s reforms, and in the slow expansion of competition—from trading into listings. If ASX executes, it can emerge as a modernised, more resilient steward of Australia’s market plumbing. If it doesn’t, the “unlikely monopolist” won’t collapse overnight—but it could gradually lose the confidence, and then the ground, that its fortress was built on.

Material Legal and Regulatory Considerations:

- ASIC lawsuit over allegedly misleading CHESS statements remains pending in Federal Court

- $150 million additional capital charge to be accumulated by June 2027

- ASIC Inquiry final report due by March 31, 2026

- CHESS Release 1 (clearing) targeted for April 2026; Release 2 (settlement) for 2028-2029

- Governance reforms requiring independent clearing and settlement facility boards underway

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube