Amman Mineral: The $10 Billion Copper Pivot

I. Introduction & The "Batu Hijau" Hook

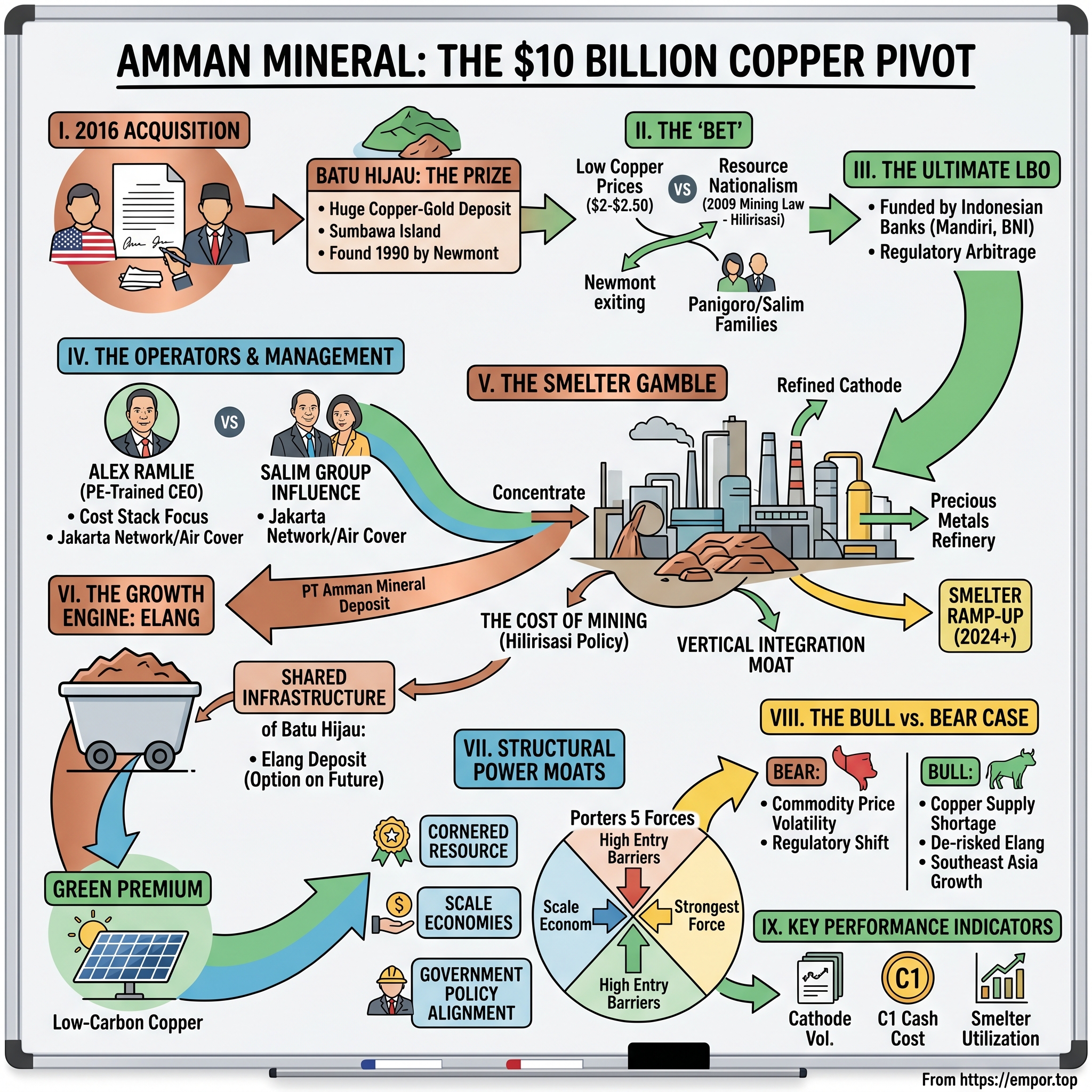

On a humid morning in November 2016, in a sterile conference room at a Jakarta law firm, a small group of Indonesian businessmen signed a stack of documents that would, in retrospect, look like one of the most asymmetric bets in Southeast Asian corporate history. On one side of the table sat representatives of an American mining titan, Newmont Mining Corporation, eager to walk away from a long-running political and regulatory headache. On the other sat the principals and bankers of a newly formed Indonesian vehicle called PT Amman Mineral Nusa Tenggara, backed by two of the country's most storied business families — the Panigoros of Medco Energi and the Salim Group of the late Liem Sioe Liong.12

The asset changing hands was simple to describe and almost impossible to replicate: Batu Hijau, literally "Green Stone," an enormous open-pit copper and gold porphyry deposit carved into the volcanic spine of Sumbawa Island in West Nusa Tenggara province. It had been discovered in 1990 by Newmont geologists, built up over a decade at a cost of more than $1.8 billion in 1990s dollars, and by the mid-2010s ranked among the largest copper-gold mines in the world.3

But the timing felt apocalyptic. Copper prices were sliding through their worst stretch in a decade, hovering around $2.00 to $2.50 per pound, down nearly 50% from the post-financial-crisis super-cycle peaks. Jakarta had passed a new Mining Law in 2009 that demanded foreign miners both divest equity to local owners and stop exporting "raw dirt" — they would have to build domestic smelters or lose their export permits.4 To Newmont's American shareholders, Indonesia looked like a regulatory swamp; to the Indonesian buyers, it looked like a once-in-a-generation chance to own a Tier-1 ore body at a cyclical low.

The thesis of this episode is straightforward and also slightly subversive. PT Amman Mineral Internasional Tbk — the listed holding company that emerged from that 2016 transaction and went public on the Indonesia Stock Exchange in July 2023 under the ticker AMMN — is not really a mining company in the conventional sense.5 It is a masterclass in three overlapping disciplines: capital allocation across a deeply cyclical commodity, the navigation of "resource nationalism" in the world's fourth-largest country, and the orchestration of an integrated industrial complex — a mine, a port, a power plant, a smelter, and a town — at the edge of the Pacific Ring of Fire. The question we want to answer is whether the company that paid roughly $2.6 billion for a 56% stake at the bottom of the cycle has built something durable, or simply ridden one wave of the copper price.1

Here is the roadmap. We will travel back to the American "discovery" era to understand what was actually built at Batu Hijau, then walk through Indonesia's Hilirisasi (downstreaming) policy and why it pushed Newmont toward the exit. We will examine the 2016 acquisition as the leveraged buyout it really was — funded by a syndicate of Indonesian state-linked banks that Western lenders had largely declined. We will meet Alexander Ramlie, the private-equity-trained operator running the company, and explore why his background in deal-making, rather than in pit operations, may be exactly the right profile for this moment. We will look hard at the $3-billion smelter complex at Sumbawa that turned on in 2024, the still-undeveloped Elang deposit that could be the second act, and the renewable-energy bets layered on top. And finally, we will weigh all of this through Porter's Five Forces and Hamilton Helmer's 7 Powers framework — because in a business like this, structure is destiny.

Let us begin where every great mining story begins: with a rock, a satellite image, and a long, slow walk across a remote island.

II. Context: The Newmont Era & Resource Nationalism

The story of Batu Hijau does not start with a boardroom. It starts in 1986, when a small Australian geologist named Bob Pollard, on contract to Newmont Mining, was studying old Indonesian government stream-sediment surveys of southwest Sumbawa. The surveys hinted at anomalous copper readings around a stream the locals called Air Hijau — "green water" — where the rocks themselves were tinted faintly green by oxidized copper minerals. Newmont obtained a Contract of Work concession from the Indonesian government in 1986, and over the next four years drilled out what would turn out to be one of the great porphyry copper-gold deposits of the late twentieth century. The discovery was formally declared in 1990, and proved up over the following years at more than a billion tonnes of ore at attractive grades — enough to support a multi-decade mine life.3

Then came the construction marathon. Between 1996 and 1999, in the middle of the Asian Financial Crisis, Newmont and its Japanese partners at Sumitomo Corporation poured roughly $1.8 billion into building a fully integrated industrial city on the southwestern tip of Sumbawa. They built a deep-water port at Benete Bay capable of receiving Capesize vessels, a coal-fired power station to run the concentrator, a 120,000-tonne-per-day concentrator complex, a tailings disposal system into the deep Senunu submarine canyon, an airport, a township for thousands of workers, schools, a hospital, and the access roads to connect all of it.3 When the mine poured first concentrate in 2000, it was operating at scale on an island where, a decade earlier, much of the population had no grid electricity.

For the next fifteen years, Batu Hijau ran as a classic foreign-operated extractive operation. The local entity, PT Newmont Nusa Tenggara, was majority owned by Newmont USA and Sumitomo, with smaller stakes held by a local Indonesian partner. It produced an average of around 250,000 tonnes of copper and 500,000 ounces of gold annually in its strong years, sold concentrate primarily to Japanese, Korean, and Chinese smelters, and paid royalties and corporate taxes to Jakarta under the terms of its 1986 Contract of Work.3 The mine became, by some distance, the dominant economic engine of West Nusa Tenggara province.

The inflection point arrived in 2009 with the passage of Indonesia's new Mining Law (Law No. 4 of 2009), which fundamentally rewrote the rules of foreign ownership and value capture. Two clauses mattered above all. The first required foreign-controlled mining concessions to progressively divest equity to Indonesian parties — eventually up to 51% — over the life of the project. The second, and more economically painful, banned the export of unprocessed mineral ores and concentrates from 2014 onward, with the explicit goal of forcing miners to build domestic smelters and capture downstream value inside Indonesia. This package of policies became known, collectively, as Hilirisasi — downstreaming — and it became the centerpiece of Indonesia's industrial strategy under presidents Susilo Bambang Yudhoyono and, even more aggressively, Joko Widodo (Jokowi).46

For Newmont, this was an existential change in the business case. Building a copper smelter in Indonesia was a multi-billion-dollar undertaking with thin economics on a standalone basis — smelters are notoriously low-margin businesses globally, and the only reason to build one in Sumbawa was to keep the upstream mine running. The 2014 export ban produced an immediate cash-flow crisis at Batu Hijau, with the mine effectively shutting concentrate sales for months until the company negotiated a temporary export permit conditional on smelter construction commitments.7 Meanwhile, divestment requirements forced repeated, contentious negotiations over what price the Indonesian government — and which Indonesian partners — would pay for stakes in the mine.

By 2015 and 2016, Newmont's leadership in Denver had quietly concluded that Indonesia was no longer a strategic geography. The company was simultaneously rationalizing its portfolio toward the Americas — divesting Australian and African assets — and Batu Hijau's combination of falling ore grades from the upper benches of the pit, looming smelter capex, and ever-shifting regulatory ground made it a perfect candidate for exit. The question was simply: who in Indonesia had the capital, the political coverage, and the appetite to buy it?

The answer would arrive from an unlikely consortium that combined oil money, food-empire money, and a private-equity playbook — and that combination is what the next chapter is really about.

III. The 2016 Acquisition: The Ultimate LBO

The deal that closed in November 2016 is best understood not as a mining transaction but as a domestic leveraged buyout, structured in the way that LBOs are structured the world over — except that almost every counterparty, every lender, and every shareholder was Indonesian.

The buyer of record was PT Amman Mineral Internasional, a vehicle assembled for the purpose, with PT Medco Energi Internasional and entities linked to the Salim Group as the principal economic sponsors. Medco — controlled by the Panigoro family, founded by Arifin Panigoro in the early 1980s as an oil-services contractor and later transformed into Indonesia's most prominent independent oil and gas company — provided the operating credibility and the energy-sector relationships. The Salim Group, the sprawling conglomerate built by 林绍良 Liem Sioe Liong (Indonesian name: Sudono Salim) from the 1960s onward and now run by his son Anthoni Salim, provided distribution power, banking relationships, and the kind of political weight in Jakarta that only a few families in Southeast Asia possess.12

The headline number was approximately $2.6 billion for Newmont and Sumitomo's combined 82.2% stake (Newmont held 48.5% and Sumitomo 35%) in PT Newmont Nusa Tenggara, although the deal structure included assumed debt and contingent payments that made the cash component lower at signing.1 The Reuters wire from June 30, 2016, when Medco first announced the indicative agreement, framed it as one of the largest mining transactions ever executed by Indonesian buyers and one of the few times that a foreign Tier-1 mine had been acquired entirely by domestic capital.1

Was it a good price? This is where Acquired-style "benchmarking the bet" becomes interesting. On a copper-equivalent basis, Batu Hijau's reserve and resource base in 2016 implied that the buyers were paying somewhere in the range of two to four U.S. cents per pound of contained copper in the ground — well below the implied multiples being paid for comparable Tier-1 assets in Chile, Peru, or even in Indonesia's neighboring jurisdictions during the same window. The reason for the discount was not geology; it was country risk, smelter capex overhang, and the structural ambiguity of the divestment process. The Indonesian buyers were, in effect, being paid by the seller to take on regulatory risk that they were uniquely positioned to manage.

The financing side is what makes the deal so distinctly Indonesian. Western project-finance banks had largely sat the transaction out — the combination of commodity price weakness, an unfinished smelter, and the country's reputation for regulatory volatility made the credit committees in London and New York skittish. Instead, the buyers turned to a syndicate of large Indonesian banks, anchored by Bank Mandiri and Bank Negara Indonesia (BNI), supplemented over time by additional state-linked and private domestic lenders. This was not unusual for Indonesian mega-deals in the post-2010 era, but the size — multiple billions of dollars of acquisition and refinancing facilities — represented a deliberate test of the local banking system's capacity to backstop a national-champion-scale transaction.8

There are two pieces of analysis worth pausing on, because they explain why this deal looks different from a standard mining LBO. First, the buyers were not paying for a developed asset to operate as-is; they were paying for an option on a much bigger, vertically integrated business. The same regulations that scared off Newmont — the smelter mandate, the divestment requirements, the export licensing regime — were features rather than bugs for an Indonesian owner with relationships in Jakarta and access to domestic capital. The smelter that Newmont saw as a billion-dollar tax on its margins, Amman saw as a once-built moat against future competitors.

Second, the deal was structured around the eventual public listing of the holding company. From day one, the sponsors understood that the equity check they were writing would only generate the returns they wanted if they could eventually monetize the asset in the Indonesian capital markets at multi-billion-dollar scale. That patience would be rewarded in 2023.

But before we get to the IPO, we need to understand the people who actually ran the asset after Newmont walked away — and in particular, the architect of the post-acquisition strategy.

IV. Current Management: The "New Guard"

If you sat across the table from Alexander Ramlie at a Jakarta business lunch, you would be forgiven for assuming you were meeting a private equity managing director rather than the President Director of a mining company. The cadence is more capital-markets than copper-pit: discussions of EV/EBITDA multiples, smelter throughput rates, syndicated loan covenants, and Bloomberg consensus models. That is not an accident.

Ramlie came to Amman Mineral from the Indonesian private equity world — most notably from Northstar Group, the Jakarta-based PE firm founded by Patrick Walujo (now CEO of GoTo) that has long specialized in carve-outs, consolidation plays, and complex regulatory situations across Southeast Asia. He earlier held roles in investment banking and at PT Saratoga Investama Sedaya, the listed investment company associated with Sandiaga Uno. His professional pedigree is essentially the opposite of a traditional mining-engineer-rises-through-the-ranks profile, and that mismatch is the point.9

What does a PE-trained operator bring to a Tier-1 copper-gold mine? Three things. First, an obsessive focus on the cost stack — the all-in sustaining cost per pound, the ratio of strip waste to ore, the diesel and grinding-media inputs that make up the bulk of a porphyry mine's operating cost. Second, an investor-relations sensibility that treats every quarter as a conversation with the capital markets, not just a production report — relevant once the company became publicly listed. Third, and most subtly, an instinctive comfort with structured transactions: smelter project financing, prepayment deals with offtake partners, hedging programs, and the issuance of dollar bonds into international markets, the kind of activity that a more traditional miner might have outsourced or avoided.5

The ownership structure tells you who Ramlie answers to. The publicly listed holding company, PT Amman Mineral Internasional Tbk, sits above the operating mine company at Batu Hijau and the smelter company at Sumbawa. Above the listed entity, control is concentrated in PT Amanat Nusa Bakti — a closely held Indonesian vehicle through which the original sponsor group exercises strategic direction — along with affiliated holdings linked to Medco's Panigoro family and the Salim Group. The IPO in July 2023 floated only a small minority of the shares, which means that despite the more than $5 billion of market value of public float, the company's strategic decisions are made by a tight, founder-controlled board.5[^10]

The Salim influence is worth a brief detour, because it is genuinely distinctive. Anthoni Salim runs a conglomerate that touches Indonesian daily life at almost every node — Indofood's instant noodles (Indomie is the world's largest brand of instant noodles by volume), the Indomaret convenience store network, palm oil through First Pacific's subsidiaries, telecoms through PLDT in the Philippines, and a sprawling banking and infrastructure footprint. The political and logistical "air cover" that comes with being a Salim-adjacent enterprise is hard to quantify but easy to observe in moments of regulatory tension: smelter permits, export licenses, land acquisition negotiations, and labor issues tend to be resolved with a speed and predictability that purely foreign operators historically did not enjoy at the same site.10

There is a deeper management philosophy embedded here that distinguishes Amman from its predecessor. Under Newmont, Batu Hijau was a foreign subsidiary — a remote operation whose reporting lines went to Denver and whose strategic decisions were taken thousands of miles from Sumbawa. Under Amman, the mine and the smelter are being run as a single integrated industrial system whose strategy is set in Jakarta and whose growth is bound up with national policy goals. The shift is from "foreign extractor" to "national champion," and it shapes everything from procurement decisions (more local content) to community relations (heavier investment in regional development) to capital allocation (a willingness to underwrite projects with non-mining strategic value).

The most visible expression of that philosophy is the smelter project itself — which is where the story turns from acquisition into industrial transformation.

V. The Smelter Gamble & Hilirisasi

To understand why Amman Mineral spent more than $3 billion building a copper smelter in a remote corner of Sumbawa, you have to first understand that, on its own merits, almost no rational miner in 2020 would have built a copper smelter in Indonesia.

Copper smelting is, globally, a low-margin, capital-intensive, environmentally complex business. The industry's economic returns are typically thinner than upstream mining, and the world's existing smelter capacity — concentrated in China, Japan, South Korea, and Chile — already produces refined copper at scale and at cost. Most miners around the world deliberately don't integrate downstream into smelting; they sell concentrate and let specialists handle the chemistry. The Treatment and Refining Charges (TC/RCs) that smelters earn are set annually in benchmark negotiations between Chinese smelters and global miners, and in tight concentrate markets — which is the world we have entered with the AI and electrification boom — those charges have actually collapsed toward zero, making standalone smelter economics worse than ever.11

So why did Amman build one? The short answer is that the smelter is not a smelter — it is the cost of remaining a miner. Under the 2009 Mining Law and its successor regulations, export permits for copper concentrate were conditional on demonstrable progress toward domestic smelting capacity. The original deadline of 2014 had been extended repeatedly, and the Jokowi administration's signature Hilirisasi push made it clear that any miner that wanted to keep selling concentrate abroad in the medium term needed to put concrete in the ground. For Amman, building the smelter at Sumbawa's industrial estate was the price of holding onto Batu Hijau's export franchise — and, more importantly, the price of being treated as a strategic national asset rather than a regulatory problem.46

The project's scale was substantial. The single-line copper smelter at Sumbawa, with a design capacity of around 220,000 tonnes per year of refined copper cathode plus associated precious-metals and sulfuric-acid byproduct streams, was budgeted at more than $3 billion when fully accounting for the integrated precious metals refinery, the port upgrades, and the associated infrastructure. Financing came from a multi-billion-dollar syndicated facility led by domestic and regional banks, supplemented by the IPO proceeds in 2023, which were specifically earmarked toward smelter capex and the refinancing of acquisition-era debt.5812

Construction proceeded through 2022 and 2023, with the Jakarta Post reporting in March 2024 that the smelter was on track to begin operations in mid-2024.12 The project did encounter some of the cost overruns and timing slips that are nearly universal in greenfield smelter construction globally — supply-chain disruptions through 2022 and a fire at the precious-metals refinery section in late 2024 caused additional delays — but by the end of 2024 the smelter was ramping production toward steady-state.12

The strategic logic, once you peel back the regulatory motivation, is genuinely interesting. By integrating the mine with the smelter, Amman captures value that previously leaked to Japanese, Korean, and Chinese refiners — not just the TC/RC margin but, more importantly, the precious-metals refining margin on the gold and silver that ride along in copper concentrate. Batu Hijau's ore is unusually rich in gold for a copper porphyry, and the recovery of that gold inside Indonesia under Amman's roof, rather than at a third-party smelter abroad, is a meaningful component of project economics. Beyond that, vertical integration creates optionality around product mix — refined cathode versus blister copper versus concentrate — that allows the company to flex toward whichever market is paying best at any given moment.

There is also a softer strategic benefit that is easy to underestimate. By aligning its capital deployment so completely with the Jokowi administration's industrial policy, Amman bought itself a category of relationship with the state that competitors who resisted Hilirisasi — including, historically, foreign-controlled operations elsewhere in the archipelago — were never able to access. Being seen as a "model" downstreaming case has tangible benefits in tax incentives, permitting, and policy stability that compound over time. The smelter is, in this sense, both a physical asset and a political instrument.

That alignment with the state matters all the more because the next major growth driver in the portfolio — the still-undeveloped Elang deposit — will require an even bigger capital cycle.

VI. The Hidden Growth Engine: Elang & Beyond

If Batu Hijau is the cash cow of the Amman Mineral story, then the Elang deposit is the option that makes the whole equity case interesting for long-term investors. And if you are unfamiliar with porphyry copper geology, the right mental model is this: Batu Hijau and Elang are two giants sitting under the same volcanic arc, formed by the same deep magmatic processes, separated by roughly 60 kilometers of jungle and ridgelines. One has been mined for a quarter of a century. The other has barely been touched.

Elang is one of the largest undeveloped copper-gold porphyry deposits in the world. The published resource statements describe a multi-billion-tonne system at lower grades than Batu Hijau but at a scale that, once developed, could extend Amman's production profile for decades. The deposit sits within the same concession area as Batu Hijau, which is a non-trivial advantage: the access roads, the port, the power plant, the township, the tailings management infrastructure, and the smelter that the company has already built for Batu Hijau can, in principle, be leveraged to bring Elang to production at a fraction of the per-tonne capex that a standalone greenfield project would require.13

The cash-cow side of the equation, meanwhile, runs on a sequence of mine phases. Batu Hijau is currently in what the company describes as Phase 7 mining, with Phase 8 — the extension of the open pit further down into the ore body — already underway. Each phase is essentially a stripping campaign, in which the company removes a large volume of overburden waste rock to expose the next slab of high-grade ore at depth. Phase 7 in particular has been the focus of a significant capital cycle, because the strip ratios are temporarily elevated and the access ramps have to be re-engineered to allow continued production at depth. Phase 8 is expected to underpin Batu Hijau's production through the late 2020s, after which the development of Elang becomes the company's central growth narrative.5[^15]

There is a layer of optionality on top of the geology that the market has only begun to price in. Amman has been investing in solar PV capacity and other renewable-energy infrastructure to reduce the carbon intensity of its operations. The Batu Hijau power plant has historically been coal-fired — a perfectly rational choice when the asset was designed in the late 1990s and there was no premium for green copper — but the global copper market has begun to bifurcate. Major Western automotive and electronics buyers, under pressure from their own decarbonization commitments, have started to pay incremental premiums for refined copper produced with low Scope 1 and Scope 2 emissions. By layering solar generation onto the Batu Hijau site, Amman is positioning itself to participate in that emerging "green premium" market as it deepens.[^16]

Why does this matter so much in 2026? Because the demand-side macro for copper is, by consensus, the most attractive it has been in a generation. The combined demands of vehicle electrification, grid build-out, data-center electrification (the AI compute boom is, in unglamorous terms, mostly a copper-and-transformers boom), and renewables installation have stacked structural growth on top of cyclical replacement demand. On the supply side, copper grade declines at the world's existing mega-mines in Chile and Peru, water constraints in the Atacama, declining capital intensity discipline among major miners, and a near-empty greenfield project pipeline have left the industry short of new ounces just as demand has accelerated. Bringing Elang into production over the late 2020s and into the 2030s — in a permissive jurisdiction, with shared infrastructure, on a low-cost basis — is, by any reasonable measure, a strategically valuable position.

The risk, of course, is execution. Greenfield copper projects routinely overrun their budgets and timelines, and Elang will not be cheap. The capital cycle ahead — to extend Batu Hijau, develop Elang, complete the smelter ramp, and build out renewable generation — implies several billion dollars of additional investment over the second half of the decade. That capital intensity is the central tension in the equity story, and it is what makes structural moats — the topic of the next section — so important to understand.

VII. Porter's 5 Forces & Hamilton's 7 Powers

Let us put Amman Mineral on the analytical X-ray table and look at it through two complementary frameworks: Michael Porter's classic Five Forces and Hamilton Helmer's more contemporary 7 Powers. The interesting thing about an integrated, jurisdiction-specific copper miner is that it scores very differently on the two frameworks — and where it scores well is exactly where you would want it to.

Start with the 7 Powers framework. The most obvious power Amman holds is what Helmer calls Cornered Resource — the exclusive long-term access to a critical input that is not available to competitors at the same cost. Batu Hijau and Elang are, geologically, what they are: irreplicable concentrations of copper and gold mineralization, formed by specific igneous processes tens of millions of years ago, held under Indonesian government concession agreements that grant Amman exclusive extraction rights for decades. You cannot disrupt an ore body the way you can disrupt a software product. Either you have the rocks or you do not, and Amman has them.

The second power is Scale Economies, and this is where the 2016 acquisition's value really compounds. The infrastructure that Newmont and Sumitomo spent $1.8 billion building in the 1990s — the port, the power plant, the concentrator, the township, the airport — is essentially impossible to replicate at current construction costs. A new entrant trying to build an equivalent integrated operation in 2026 would face replacement costs that would likely run several times higher in inflation-adjusted terms, and would face permitting timelines measured in years. Amman inherited that infrastructure at a fraction of replacement cost as part of the 2016 deal, which means its long-run unit economics are structurally lower than any plausible competitor could achieve on the same island.

The third power, and one that does not appear explicitly in Helmer's framework but functions identically in emerging markets, is what we might call Government Policy Alignment. By aligning its capital plan so completely with the Jokowi administration's Hilirisasi doctrine — building the smelter, hiring local, supporting downstream value capture — Amman has placed itself on the strategically protected side of the regulatory ledger. In an environment where foreign or recalcitrant operators routinely face permit renegotiations, export bans, and tax disputes, the company that is seen as the "model citizen" of the policy enjoys a real and durable moat. Whether this power survives a future change in administration is the central political risk, but as of 2026 it is a meaningful structural advantage.

Where Amman is weaker on the Helmer scorecard is in Switching Costs (copper is a commodity; buyers can and do switch suppliers easily), Network Economies (there are no positive network effects to mining), and Branding (no consumer-facing brand here, though the LME-grade and green-copper certifications matter at the margin). Process Power and Counter-Positioning are arguable — there are operational efficiencies that come with running an integrated complex, but they are not unique enough to constitute a true Process Power moat.

Now flip to Porter's Five Forces, where the analysis runs differently. Barriers to entry are extraordinarily high — by some measures the highest in any industrial sector. The combination of capital intensity (multi-billion-dollar greenfield projects), regulatory complexity (multi-year permitting cycles, environmental impact studies, community consent processes), and the geological prerequisite of actually finding the ore body in the first place make new entry nearly impossible at the relevant timescale. This is the single strongest structural feature of the industry. Buyer power is mixed: copper is sold into a deep, global, transparent market with hundreds of customers, so no single buyer has pricing power, but the buyer base as a whole is sophisticated and price-takes from LME. Supplier power is interesting and asymmetrically distributed: physical input suppliers (equipment, energy, labor) have moderate power, but the dominant "supplier" of the right to operate is the Indonesian state, whose royalty rates, tax treatments, and regulatory decisions can swing project economics dramatically. Threat of substitutes is structurally low — aluminum substitutes for some electrical applications at the margin, but copper's conductivity, ductility, and corrosion resistance keep it irreplaceable in most uses. Industry rivalry at the commodity level is intense (every producer is a price-taker), but at the project level rivalry is essentially absent — Amman does not compete with Antofagasta or Freeport on any meaningful operational dimension.

Put these together and you get a picture of a business with extremely strong structural attractiveness on the macro forces (high barriers, low substitution, irreplicable resource) coupled with extremely high concentration of two specific risks: commodity price and political regime. The bull case and the bear case both fall out of that asymmetry, which is exactly what we want to wrestle with next.

VIII. Playbook & Bear/Bull Case

Step back from the operational detail for a moment and look at the playbook that the Panigoro and Salim families have run since 2016. It distills into three principles that are worth naming explicitly because they generalize beyond Amman Mineral and explain a lot of how Indonesian national champions tend to be built.

The first principle is buy when there is blood, or at least boredom. The 2016 acquisition was executed at the bottom of a brutal copper bear market, against a backdrop of regulatory paralysis and the perception that Indonesia was a hostile jurisdiction. Western buyers were either unwilling to underwrite the country risk or had already exited the region. By acting countercyclically — and by structuring the deal with domestic capital that did not need Denver or London credit-committee approval — the sponsors bought a Tier-1 asset at a multiple of "dollars per pound in the ground" that would be inconceivable in a normal copper cycle.

The second principle is local advantage is more durable than operating advantage. Mining is full of companies that win on technology, throughput, or cost-curve positioning. Those advantages are real, but they tend to erode as competitors catch up. Local advantage — meaning the ability to navigate the specific regulatory, political, and community environment of a given jurisdiction — is much harder to copy and tends to compound over time as relationships deepen. Amman's bet, implicit in everything from the choice of Indonesian financing to the speed of smelter commitment to the depth of Salim Group involvement, is that knowing how to navigate Jakarta is a more durable competitive edge than knowing how to navigate a pit.

The third principle is infrastructure as a moat. The town, the port, the power plant, the access roads, the airstrip, the tailings system — none of these are accounted for as moats on the balance sheet, but together they constitute an enormous, irreplicable competitive position. Any potential new entrant on Sumbawa would need to negotiate land access, build a separate port, secure power generation, and import a workforce — at costs that would dwarf the original Newmont-era construction budgets. The fact that Amman gets to use this infrastructure not just for Batu Hijau but eventually for Elang as well is what makes the long-run capital efficiency of the franchise so attractive.

Now to the bear case, because there are several legitimate ones and an honest investor should hold them in mind.

The most direct bear case is commodity price volatility. Copper prices can move 30% to 50% in a year on macro shifts — Chinese property demand, recession fears, dollar strength, speculative positioning. Amman is fundamentally a price-taker, and a sustained period of weak copper (say, sub-$3.50 per pound, which is far below 2025-2026 trading ranges) would compress earnings dramatically given the operating and financial leverage in the business. The smelter project carries its own debt service, and the Elang development will require multi-year capex commitments that look very different at $5/lb copper than at $3/lb.

The second bear case is regulatory shift. As of 2026, the Prabowo Subianto administration has broadly continued the Hilirisasi policy framework inherited from Jokowi, but Indonesian political regimes can pivot quickly, and the specific tax, royalty, and export-permit treatment of large mining projects has been a source of repeated renegotiation over the past decade. A future administration that decides to renegotiate Contracts of Work, raise royalty rates, or impose new windfall taxes on commodity producers would directly hit Amman's cash flows. The same political alignment that is currently a moat could become a liability under a different government.

The third bear case is execution risk on Elang. Greenfield porphyry copper projects are infamous for capex overruns and schedule slippage. Industry benchmarks suggest that large greenfield copper projects globally have routinely come in 30% to 50% over budget and one to three years late. Elang's eventual development will be a multi-billion-dollar project on difficult terrain in a remote jurisdiction. Execution discipline, contractor management, and disciplined capital allocation will all matter.

The fourth bear case is balance sheet — the legacy acquisition debt, the smelter construction debt, and the prospective Elang development debt stack up at a time when global rates are higher than they were when much of this leverage was put on. The company has actively termed out and refinanced its facilities, including through its IPO and post-IPO bond issuance, but the absolute debt load is meaningful and pressures dividend flexibility in down cycles.8

The bull case is the mirror image — and it is, on a structural read, more compelling.

The most important bull factor is the copper supply-demand setup itself. The world is short copper. Demand from EVs (each EV uses three to four times the copper of an internal-combustion vehicle), grid build-out for renewables, data center electrification, and electrification of industrial processes is structural and accelerating. Supply, meanwhile, is constrained by declining ore grades at incumbents, water restrictions in major producing regions, social-license challenges, and a permitting cycle that means greenfield projects approved today won't produce metal until the 2030s. In that environment, every owner of a Tier-1 producing asset with a credible growth pipeline is, almost by definition, in a strong position.

The second bull factor is jurisdictional diversification. Western and Asian end-buyers are actively trying to diversify their copper sources away from politically concentrated regions, particularly given concerns about Chilean water policy, Peruvian community unrest, and the supply-chain risks of overreliance on any single country. Indonesia, with its political stability relative to Latin America's recent volatility and its embrace of long-term industrial policy, is an increasingly attractive jurisdiction for that diversification flow.

The third bull factor is the integrated business model. As the smelter ramps and as Amman captures value across the mine-to-cathode chain, the company's margin structure should improve relative to pure upstream miners. The precious-metals refining of Batu Hijau's gold-rich concentrate inside the integrated complex is a particularly attractive economic driver that the market has historically discounted because it depends on operational execution.

The fourth bull factor is optionality on Elang. Even if Batu Hijau's production declines into the early 2030s, the cost-leverage of bringing Elang online with shared infrastructure makes the long-run NAV of the franchise far higher than a pure single-asset operator. Investors are essentially getting one large operating mine, one smelter, and one massive option on the next mine — and the option strike is set by shared infrastructure costs rather than by greenfield economics.

For long-term fundamental investors trying to keep score, the key performance indicators are narrower than they look. The first KPI to track is copper cathode production volume — both at the mine concentrate level and, increasingly, at the smelter output level — because this is where the integrated model either proves its case or does not. The second KPI is C1 cash cost per pound of copper, net of by-product credits, because this tells you everything about how Amman is positioned on the global cost curve and how resilient its cash flows are in a downturn. A third, more strategic KPI worth watching is the smelter ramp-up curve — utilization rate against nameplate capacity through 2025 and 2026 — because the gap between the smelter as a regulatory cost and the smelter as a value driver depends on operational execution at this specific asset.

Myth versus reality is also worth a brief detour. The most common myth about Amman Mineral is that it is fundamentally a "play on Indonesian politics" — that the entire investment thesis depends on the continuation of a specific regulatory framework. The reality is more nuanced. Yes, regulatory alignment is a moat, but the underlying ore body, the integrated infrastructure, and the scale of contained metal are real economic assets that would have material value under almost any plausible political regime. A second myth is that the smelter is uneconomic and dilutes returns — the reality is that the smelter's standalone economics are thin but its integrated economics, particularly via precious-metals refining, are meaningfully better than the standalone framing suggests.

This brings us to the closing question that any Acquired-style episode ends on.

IX. Conclusion

Step back from the operational layers and the regulatory weeds, and what Amman Mineral really is, in 2026, is a portrait of how the global mining industry's center of gravity has been quietly migrating. For most of the twentieth century, the largest copper mines in the world were owned, financed, and operated by a small group of Western multinationals — Anaconda, Phelps Dodge, Rio Tinto, BHP, Newmont — with capital flowing from London and New York and operating decisions made in distant headquarters. The 2016 transaction at Batu Hijau was, in retrospect, one of the cleanest expressions of a different model: domestic capital, domestic relationships, and domestic strategic intent acquiring a Tier-1 asset from foreign owners who could no longer make the math work under local regulatory constraints.

What makes the story specifically interesting, rather than just illustrative, is the way the buyers leaned into the regulation rather than against it. Newmont saw Hilirisasi as a tax on its margins; Amman saw it as a moat to be built. Newmont saw the divestment requirements as a forced sale; Amman saw them as the price of admission to a multi-decade industrial position. The smelter that the previous owners had resisted as uneconomic, Amman accepted as the strategic cost of keeping a Tier-1 mine running under domestic ownership — and in doing so converted a regulatory headache into a piece of integrated industrial infrastructure that competitors will struggle to replicate.

The capital-allocation discipline that has run alongside the operational story is the part that most resembles a private-equity playbook. Buying countercyclically at the bottom of a copper bear market. Financing through domestic banks when Western lenders would not show up. Patiently building toward an IPO that did not arrive until seven years after the original acquisition. Using public-market proceeds to refinance acquisition-era debt and fund the smelter. And, as the smelter approaches steady state, beginning to articulate the next leg of the story around Elang — an asset whose development cost is meaningfully de-risked by the infrastructure already built for Batu Hijau. None of these decisions are flashy on their own. Stacked together, they describe a coherent multi-decade industrial strategy.

The unresolved questions are real. Whether Elang can be brought into production on time and on budget. Whether the Hilirisasi policy framework that underpins Amman's regulatory alignment survives changes in administration intact. Whether the copper supercycle that the AI, EV, and electrification booms are propelling proves as durable as bulls believe, or whether it punctuates into a deeper cyclical correction. Whether the integrated smelter actually delivers the precious-metals margin uplift that the project economics imply at full ramp. The honest answer to each of these is that the next three to five years of operating execution will tell us more than any number of analyst notes today.

What is no longer ambiguous, however, is the underlying nature of the company. Amman Mineral is not a foreign-owned subsidiary running a remote operation under contract. It is an Indonesian national industrial champion, with the geological endowment of one of the world's premier copper-gold districts, the regulatory blessing of the state's signature industrial policy, the operational infrastructure inherited at a discount from a previous era of foreign ownership, and the capital-allocation sensibility of a private-equity-trained leadership team. Whether one chooses to call that the Standard Oil of copper in Asia, the Reliance Industries of mining, or something else entirely is a matter of taste. The substance underneath the metaphors is that a small group of Indonesian capital providers, in 2016, looked at a depressed commodity price and a complex regulatory environment and saw a once-in-a-generation industrial position. A decade later, with the smelter humming and the Elang option still ahead, the bet looks very different than it did the morning the deal was signed.

The Acquired audience knows the cadence here. What you build, who you build it with, when you build it, and how you finance it — those four decisions, in the right combination, can compound into something durable. Amman Mineral is the rare case where all four lined up at the same time in the same jurisdiction, and where the resulting business now sits at the intersection of three of the most powerful structural forces in the global economy: the energy transition, the AI compute build-out, and the re-industrialization of Southeast Asia. What happens from here will be a story about execution, but the structural setup is one of the most attractive in the global mining industry, and that is a position that Newmont and Sumitomo, ten years ago, did not realize they were selling.

References

References

-

Indonesia's Medco Energi to buy Newmont's Indonesian mining unit — Reuters, 2016-06-30 ↩↩↩↩↩

-

Ada Grup Salim di balik IPO raksasa Amman Mineral — CNBC Indonesia, 2023-07-07 ↩↩

-

Indonesia's commodity giant ambitions rest on downstreaming — Bloomberg, 2023-08-15 ↩↩↩

-

PT Amman Mineral Internasional Tbk — IPO Prospectus, 2023 ↩↩↩↩↩

-

Indonesia's Downstreaming Policy (Hilirisasi) Explained — Bloomberg, 2023-08-15 ↩

-

Amman Mineral (AMMN) raih pinjaman untuk proyek smelter — Kontan.co.id ↩↩↩

-

Ada Grup Salim di balik IPO raksasa Amman Mineral — CNBC Indonesia, 2023-07-07 ↩

-

Analysis of the Elang Deposit Potential — S&P Global Market Intelligence ↩

-

Amman Mineral smelter to start operating in June — The Jakarta Post, 2024-03-25 ↩↩↩

-

Analysis of the Elang Deposit Potential — S&P Global Market Intelligence ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube