The Phoenix of the Gulf: How ALEC Conquered the GCC Mega-Project Arena

I. Introduction & Episode Roadmap

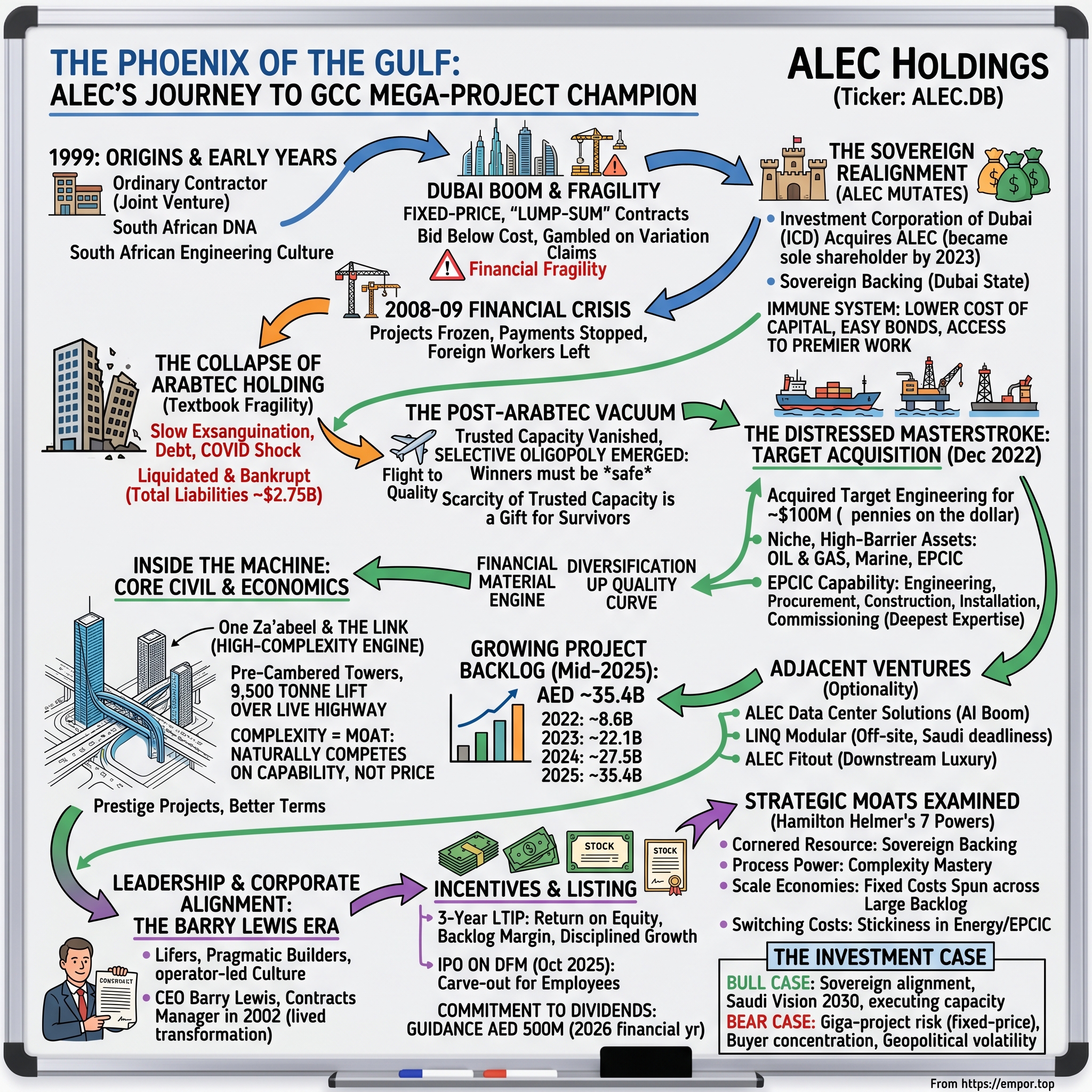

Picture the scene on Sheikh Zayed Road, Dubai's twelve-lane spine, on a humid morning in early 2024. Below, the traffic never stops — a river of SUVs and freight trucks pouring between the financial district and the old city. One hundred metres above that live highway, suspended in mid-air, hangs a steel-and-glass object the size of an aircraft carrier turned on its side. It is called The Link, and it stretches 230 metres between two leaning towers, cantilevering more than 67 metres into open sky beyond its supporting structure — a slab of engineering bravado that in March 2024 was certified by Guinness World Records as the "Longest Cantilevered Building" on the planet.1 To put the bridge sections into place, crews performed one of the heaviest lifts ever attempted in the region, hoisting roughly 9,500 tonnes of structure skyward over a matter of days — all without closing a single lane of the road beneath them.1

This is One Za'abeel, the development that announced Dubai's post-pandemic ambition to the world. And the question that opens our story is deceptively simple: who actually builds something like this? Who takes a developer's fever dream — a horizontal skyscraper floating over moving traffic — and turns it into load paths, weld sequences, and a structure that will stand for a century? The answer is أليك القابضة ش.م.ع ALEC Holdings PJSC, a company most people outside the Gulf construction world had never heard of until October 2025, when it walked onto the سوق دبي المالي Dubai Financial Market (DFM) and pulled off the largest construction-sector IPO in the history of the United Arab Emirates — raising AED 1.4 billion (about $381 million), oversubscribed more than 21 times, with order books swelling to roughly $8 billion of demand.341718

Here is the narrative we want to unpack. ALEC began its life in 1999 as an ordinary contractor — a joint venture, a balance sheet, and a stack of tender documents like a hundred others.2 Construction has historically been one of the worst businesses on earth: brutal competition, thin margins, ruinous working-capital cycles, and a graveyard of once-mighty names that over-bid, under-delivered, and went bankrupt. And yet, over twenty-five years, this particular contractor mutated into something altogether stranger and more durable — the state-backed "national champion" builder of the Gulf, a company that emerged from its October 2025 listing carrying a backlog worth tens of billions of dirhams and a balance sheet most engineering firms can only fantasize about.

How did a fragile, margin-starved contractor become a high-margin, dividend-paying, sovereign-aligned machine? That transformation is the heart of this episode.

Here is the roadmap:

- The Dubai renaissance and the slow re-wiring of who actually owns the GCC's construction industry.

- The collapse of أرابتك القابضة Arabtec Holding — the Lehman-style detonation that reset the entire regional market.

- The distressed masterstroke — ALEC's bargain acquisition of Target Engineering, and what the math of that deal tells us.

- Inside the machine — the real economics of high-complexity building, ALEC's backlog, and the war it now fights against rivals from Riyadh to Beijing.

- The Barry Lewis era — leadership, incentives, and the modern public-company playbook.

- The moat — examined through Hamilton Helmer's 7 Powers and Porter's Five Forces.

- The bull and bear case for ticker ALEC.DB, and the handful of numbers that actually matter.

Let's start where every Gulf story starts: with the city that decided to build the future faster than anyone thought possible.

II. Dubai's Renaissance & The Sovereign Realignment

To understand ALEC, you first have to understand the peculiar economics of the business it was born into — because for most of modern history, being a building contractor in Dubai was a fast way to go broke.

The company arrived in 1999 not as a grand vision but as a practical arrangement: a joint venture pairing Abu Dhabi's Al Jaber Group with the South African construction house Grinaker-LTA.2 That South African DNA matters, and it threads through this entire story — the engineering culture, the management bench, and eventually the men who would run the company all carry the imprint of that founding partnership. In its early years ALEC was simply a competent local contractor riding the most extraordinary real-estate boom the modern world had seen. Through the 2000s, Dubai poured concrete at a pace that defied belief — palm-shaped islands, the world's tallest tower, entire skylines conjured out of desert in a decade.

But booms in this region came with a vicious tail. The model that prevailed across Middle Eastern construction was structurally fragile, and it's worth dwelling on why, because this fragility is the villain of our entire narrative. A contractor typically signs a fixed-price, "lump-sum turnkey" contract: it agrees to deliver a finished building for an agreed number, full stop. If steel prices spike, if labour gets scarce, if the client changes the design halfway through, the contractor eats much of the cost. To win the work in the first place, firms bid each other down to razor-thin margins — sometimes deliberately bidding below cost just to keep their workforce employed and their cash flowing, gambling that they'd claw it back later through variation claims. Worse, the cash cycle ran against them: contractors paid wages, suppliers, and subcontractors today, but got paid by developers months later, often only after fighting over certified milestones. The entire industry essentially ran on borrowed money, and a single large client refusing to pay could topple a firm overnight.

So you had an industry of companies doing technically heroic work on financially suicidal terms. When credit was flowing and property was rising, everyone looked like a genius. When the 2008–09 financial crisis hit Dubai — and it hit Dubai harder than almost anywhere — projects froze, payments stopped, and the fragility was exposed for all to see. Property values in some Dubai districts fell by half. Foreign workers boarded planes home, abandoning financed cars at the airport. Iconic projects were quietly mothballed, their cranes left frozen against the skyline like the skeletons of a party that had ended too suddenly. The emirate ultimately needed a multi-billion-dollar bailout from neighbouring Abu Dhabi to steady itself — the kind of rescue that reorders the balance of power in a federation. The lesson of that decade was seared into every Gulf banker's brain: construction is a business where the strong and the weak are indistinguishable right up until the moment the weak vanish.

It's worth pausing here to puncture a common misconception, because it bears directly on how to read ALEC. The popular narrative outside the region is that Dubai construction is a perpetual gold rush — that anyone who shows up with a crane prints money. The reality is closer to the opposite. The sector has been a serial widow-maker, precisely because the booms attract a flood of under-capitalized entrants who bid the work down to nothing and then get annihilated by the next cyclical downturn. The firms that survive across multiple cycles are not the aggressive bidders; they are the disciplined ones with the deepest financial backstops. That distinction — between the contractor who chases revenue and the contractor who can endure — is the lens through which ALEC's entire trajectory should be read.

Now to the inflection point that changes everything. In 2017, the مؤسسة دبي للاستثمارات Investment Corporation of Dubai (ICD) — the principal investment arm and sovereign holding company of the Government of Dubai — acquired the majority of ALEC from the Al Jaber Group; by 2023 ICD had become the company's sole shareholder.5 On paper this reads like a routine change of ownership. In reality it was a mutation of the company's entire DNA.

Think about what sovereign ownership does to a business that lives and dies by trust and access to capital. Suddenly ALEC was no longer just another contractor begging banks for project finance and praying clients paid on time. It was backed by the financial fortress of the Dubai state — the same entity that owns Emirates airline, the Emirates NBD bank, and chunks of the city's most strategic assets. That backing rewires the two things that kill ordinary contractors. First, the cost of capital: a sovereign-owned builder borrows more cheaply and posts performance bonds more easily, because counterparties know who stands behind it. Second, access to work: when Dubai's own state-linked developers need someone to execute their crown-jewel projects, who do they trust with a horizontal skyscraper over a live highway? They trust the builder the state itself owns.

There is a second, subtler benefit to sitting inside ICD's portfolio, and it concerns the demand side. ICD is not a passive financial investor; it is an operating holding company that owns or controls a constellation of Dubai's most important enterprises — the airline, the banks, hospitality groups, and, critically, real-estate and development vehicles. When the entity that owns your company also owns, or sits adjacent to, the entities that commission the largest buildings in the city, a natural channel of work opens up that no independent contractor can replicate. This is the difference between fishing in the open ocean and owning the pond. ALEC still has to perform — sovereign parents do not tolerate failure indefinitely, and reputational risk runs both ways — but it fishes in waters that competitors cannot legally enter.

ALEC didn't just get a new shareholder in 2017. It got an immune system. It became insulated from the localized credit crunches that routinely wiped out competitors, and it began its slow transformation into the preferred national champion for mega-scale, sovereign-backed work. That immunity would prove its worth almost immediately — because within three years, the biggest name in the entire region was about to die.

III. The Fall of Arabtec: A Watershed Industry Re-alignment

Every industry has its bellwether — the company so large and so iconic that its health is the industry's health. For decades in Gulf construction, that company was أرابتك القابضة Arabtec Holding.

If you have ever looked up at the Burj Khalifa, the tallest building humanity has ever constructed, you have looked at Arabtec's work. If you have walked beneath the floating dome of the Louvre Abu Dhabi, marvelling at its "rain of light," you have stood inside Arabtec's portfolio.6 This was the firm that built the icons — a publicly listed giant, a household name from Cairo to Karachi, the company that seemed to embody the Gulf's physical ascent. At its peak it employed tens of thousands of workers and ran hundreds of projects simultaneously across the region. If any construction firm in the Middle East was "too big to fail," it was Arabtec.

And then it failed.

The collapse was not a single dramatic event so much as a slow exsanguination that finally became impossible to ignore. Arabtec was the textbook embodiment of every structural weakness we just described, amplified by scale. It had grown through aggressive under-bidding — winning enormous contracts on margins so thin that the slightest disruption turned them into losses. It carried a mountain of debt. It had massive sums tied up in disputed claims and unpaid receivables. And when the triple shock arrived — collapsing oil prices squeezing regional spending, and then the COVID-19 pandemic freezing construction sites and supply chains worldwide — the company's finances simply caved in. After posting a first-half net loss of roughly AED 794 million in 2020, Arabtec's shareholders voted on 30 September 2020 to liquidate the company; a Dubai court subsequently declared it bankrupt and ordered its assets sold.67 The group's total liabilities stood at around $2.75 billion.7

To appreciate the magnitude of the fall, you have to appreciate how high Arabtec had climbed. This was a company that had once attracted strategic investment tied to Abu Dhabi's own sovereign vehicles, that had at its zenith been valued in the billions, that had announced contract ambitions running to tens of billions of dollars. It was the name that international firms partnered with when they wanted to crack the Gulf market, the contractor whose order book was treated as a barometer of the entire UAE economy. Investors traded its shares as a proxy for Gulf construction itself. The hubris and the leverage that powered its rise were, in the end, indistinguishable from the forces that destroyed it — the same aggressive growth that won it the Burj Khalifa also loaded it with the obligations it could not survive.

It is hard to overstate the psychological shock. This was the region's Lehman Brothers moment for construction — the death of the institution everyone assumed was permanent. And like Lehman, its collapse sent contagion ripping through the system. Tens of thousands of workers were left in limbo, many of them low-wage migrant labourers suddenly stranded thousands of miles from home with unpaid wages and uncertain visas — a human cost that rippled out to families across South Asia who depended on those remittances. Hundreds of projects were thrown into disarray, their half-built structures suddenly orphaned, with developers scrambling to find replacement contractors willing to inherit a half-finished, poorly documented site. Subcontractors and suppliers who were owed money by Arabtec faced their own cascading insolvencies, a chain reaction that pulled smaller firms down with the giant. And the banks — the banks did what frightened banks always do. They slammed the window shut.

This is the part that matters most for our story. Arabtec's death didn't just remove a competitor; it permanently changed the rules of the game. Project-finance lenders, burned badly, stopped extending credit to anyone who couldn't demonstrate a fortress balance sheet. Developers, terrified of handing a multi-year mega-project to a contractor that might evaporate mid-build, suddenly cared far more about a builder's financial solidity than about who offered the cheapest price. Overnight, the industry's selection criteria flipped. For decades the winning bid had been the lowest bid. Now it was the survivable bid — the bid from a firm clients could be confident would still exist at the ribbon-cutting.

A vast vacuum had opened in the market for large, complex, prestige projects. The customers were still there — Dubai and Saudi Arabia were ramping up their ambitions, not shrinking them. What had vanished was the trusted capacity to deliver. And as it happened, there was one player perfectly positioned to step into that void: a contractor with a clean balance sheet, a serious technical reputation, and — crucially — the deepest pockets imaginable standing behind it.

Consider how the post-Arabtec flight to quality reshaped ALEC's competitive position almost overnight. In the old world, ALEC had to win contracts in a knife-fight against dozens of bidders willing to price the work at break-even. In the new world, the pool of contractors that developers and lenders deemed safe enough to entrust with a multi-year, multi-billion-dirham project had shrunk dramatically. When your client's overriding fear is "will my contractor still be solvent when this building tops out," the conversation stops being purely about who is cheapest and starts being about who is credible. ALEC, with its sovereign backstop and unblemished delivery record, suddenly found itself on a very short list. Scarcity of trusted capacity is, for the trusted, a gift — it means more work at better terms, the twin levers that drive the backlog and protect the margin. The collapse didn't just remove a rival; it upgraded the entire economics of being one of the survivors.

ALEC didn't cause Arabtec's fall. But it was, almost uniquely, built to profit from it. And its first move into the wreckage would turn out to be one of the shrewdest pieces of opportunism in the company's history.

IV. The Distressed Masterstroke: Benchmarking the Target Engineering Acquisition

When a giant dies, its body does not simply vanish. It gets carved up. And inside the carcass of Arabtec lay a genuine jewel — a subsidiary so valuable, so cash-generative, and so strategically distinct from the rest of the failed empire that it was almost too good to be sitting in a bankruptcy estate. Its name was Target Engineering Construction Company.

Here's why Target was special. While the rest of Arabtec poured concrete for towers, Target operated in an entirely different and far more defensible world: oil and gas, marine and offshore construction, and what the industry calls EPC — engineering, procurement, and construction — for the energy sector. This is grimy, highly technical, deeply specialized work. It means fabricating steel structures to exacting petroleum-industry standards, building jetties and offshore platforms, and sending purpose-built vessels out into Gulf waters. It is work that very few contractors on earth can do, governed by certifications and safety regimes that take years to earn. In other words, Target was the opposite of a commodity builder. It was a niche, high-barrier asset that happened to be trapped inside a corpse.

In December 2022, ALEC signed the share-purchase agreement and acquired 100% of Target Engineering for approximately $100 million.8 On paper, a tidy bolt-on acquisition. Look closer, and it was a steal — one of those deals that, in hindsight, looks almost unfair.

Let's walk through the math, because the numbers tell the story better than any adjective. Consider what $100 million actually bought. ALEC acquired an 11,000-strong specialized workforce, a dedicated fleet of more than 30 marine construction vessels, and a sprawling fabrication yard of roughly 52,000 square metres on the Abu Dhabi coast, certified to the international energy-industry standards that take years to accredit.9 Building that capability from scratch — recruiting and training thousands of specialists, commissioning a marine fleet, accrediting a fabrication facility — would take the better part of a decade and cost vastly more, assuming you could do it at all.

Now anchor that against the asset's earning power. The combination of ALEC and Target was described at the time as creating a group with roughly $2 billion in combined annual turnover.8 Against Target's own revenue base, a $100 million price tag implies an enterprise-value-to-sales multiple of well under 0.2x — a fraction of what engineering and construction businesses typically change hands for. Specialist international EPC peers generally command something in the range of half a turn of sales to nearly one full turn; even regional listings have historically fetched meaningfully more. ALEC, in other words, paid pennies on the dollar of what this asset was worth in any normal market.

And here is the historical kicker that crystallizes just how cheap it was. Arabtec itself had paid roughly AED 270 million — about $73 million — for a 60% stake in Target back in 2008, valuing the whole company north of $120 million more than a decade earlier, when it was a fraction of its eventual scale. So ALEC bought 100% of a far larger, more capable business in 2022 for less than what a partial stake had implied fourteen years before. That is the signature of a true distressed sale: a forced seller, a frozen credit market, and a buyer with the cash and the nerve to act when nobody else could.

It's worth decoding that acronym, EPCIC, because it sits at the heart of why this niche is so defensible. EPC — engineering, procurement, construction — is the standard turnkey model where a single contractor designs the facility, buys all the equipment, and builds it. The extra "IC" — installation and commissioning — extends the contractor's responsibility right through to switching the thing on and proving it works to specification. In the energy world, that final stretch is where the deepest expertise lives: installing a process module on an offshore platform in open water, then commissioning the pumps, valves, and control systems so that hydrocarbons can flow safely. Get it wrong and you don't have a snagging list; you have an environmental and human catastrophe. The clients for this work — national oil companies and the supermajors — therefore vet contractors with almost paranoid rigor, demanding track records, certifications, and safety statistics that take a decade to accumulate. That vetting wall is exactly what makes the segment so hard to enter, and exactly what ALEC bought in a single transaction.

The timing of that pivot, too, was shrewd. The UAE's energy establishment was in the middle of a massive capital-spending cycle, expanding both conventional oil-and-gas capacity and the marine infrastructure that supports it. By owning Target, ALEC positioned itself to bid for precisely the kind of long-cycle, high-barrier energy work that has nothing to do with whether a Dubai shopping mall leases up on schedule. It gave the company a second leg to stand on, planted in entirely different soil.

Why could ALEC act when others couldn't? Because of everything we established in the last two sections. The same sovereign backing that gave ALEC its immune system also gave it a war chest and a low cost of capital precisely when the rest of the industry was starved of credit. While competitors were begging banks for financing, ALEC could write a cheque. The crisis that killed Arabtec was the very thing that made Target affordable — and only a player insulated from that crisis could pounce. There is an elegant symmetry to it: ALEC reached into the wreckage of the very giant whose death had frozen the credit markets, and pulled out the one piece worth saving, at a price only the frozen market itself could have produced.

But the real significance of this deal isn't the bargain price. It's what the acquisition did to ALEC's identity. In a single stroke, the company stopped being a pure-play building contractor — a business tied entirely to the boom-and-bust of real estate — and became a diversified EPCIC powerhouse, with capabilities spanning engineering, procurement, construction, installation, and commissioning across both buildings and energy infrastructure. Suddenly ALEC could chase offshore oil-and-gas contracts, marine works, and energy projects whose economics are completely uncorrelated with whether Dubai's property market is hot or cold. For a business whose original sin was cyclicality, that diversification was strategic gold.

And it has proven to be far more than a sideshow. What might once have been dismissed as a speculative diversification has become a financially material engine: the energy and marine segment now drives a substantial share of ALEC's total turnover — on the order of 30% of group revenue — and crucially, it tends to carry higher and steadier margins than commodity building work. That last point deserves emphasis, because it inverts the usual logic of diversification. Most diversification dilutes quality — a company spreads into adjacent markets that are less attractive than its core, accepting lower returns for the sake of breadth. ALEC's energy pivot did the opposite: it diversified up the quality curve, adding a segment that is harder to enter, stickier to keep, and richer in margin than the building work that came before it. A second business that is both less correlated and more profitable than the first is the rarest and most valuable kind of acquisition there is. ALEC didn't just buy a cheap asset. It bought a second business, in a defensible niche, that smooths out the cyclicality of its first. With that engine bolted on, the company was ready to go to war in the open market — and to understand that war, we need to step inside the machine itself.

V. Inside the Machine: Core Civil Engineering, Economics, & Competitor Scale

Let's go back to that skybridge hanging over Sheikh Zayed Road, because it teaches the single most important lesson about how a contractor like ALEC actually makes money — and why some construction is a terrible business while other construction is a genuinely good one.

Here is the secret hiding in plain sight at One Za'abeel. The two towers that hold up The Link were not built straight. They were deliberately constructed leaning slightly outward, away from each other — pre-cambered, in engineering language — so that when the colossal weight of the skybridge was finally hung between them, the load would pull them gently back into perfect vertical alignment.1 Read that again. The builder had to construct two skyscrapers wrong on purpose, calculating with extraordinary precision exactly how much a 9,500-tonne object would deflect them, so that they would end up right. And the bridge itself had to be assembled and lifted into place over roughly sixteen days without ever stopping the traffic flowing beneath it.1 One miscalculation and you don't have a building; you have a catastrophe over a public highway.

That is the moat. Anyone with a concrete mixer and a labour crew can pour a residential tower — and in that commodity end of the market, contractors compete purely on price, grind their margins to nothing, and die exactly the way Arabtec died. But the number of firms on earth that can execute a pre-cambered, cantilevered skybridge over live traffic? You can count them on your fingers. High-complexity engineering is a natural barrier to entry, and the firms that can do it get to compete on capability rather than on price. They win the prestige projects, they negotiate better terms, and they keep their margins. Complexity, for a builder, is the difference between a commodity and a craft.

ALEC has spent twenty-five years climbing toward the craft end of that spectrum, and its portfolio reads like a tour of the region's most ambitious leisure and infrastructure. It built SeaWorld Abu Dhabi, one of the largest indoor marine-life parks in the world, with an aquarium of staggering scale that demands water-engineering far beyond anything in a normal building. It delivered Dubai Hills Mall, a vast retail destination, and has worked across the airports, hospitality, and entertainment assets that define Dubai's tourist economy.2 Beneath One Za'abeel it excavated the deepest basement in the Middle East — a feat of geotechnical engineering, holding back earth and groundwater at depth in a dense urban site, that is every bit as hard as the tower that rises above it, just invisible. And through Target, it now adds marine energy infrastructure to a résumé that already spanned the most demanding work on land. And the proof of where that has taken the company is in its order book. As of mid-2025, ALEC carried a project backlog of roughly AED 35.4 billion — a number worth pausing on, because of the trajectory behind it. That backlog stood at around AED 8.6 billion at the end of 2022, jumped to AED 22.1 billion a year later, reached AED 27.5 billion by the end of 2024, and then climbed to AED 35.4 billion by June 2025.10 A backlog quadrupling in two and a half years is not the picture of a sleepy contractor. It is a company aggressively converting the post-Arabtec vacuum, and the Saudi building boom, into signed contracts.

That phrase "backlog" deserves a plain-English translation, because it is the single most important concept in contractor economics. A backlog is the value of work a company has already won but not yet built — revenue that is contracted and waiting to be earned. For an investor, it's the closest thing construction offers to visibility: it tells you roughly how much business is locked in for the coming years before the firm has to win a single new tender. A growing backlog means the future is getting more certain, not less.

But ALEC does not own this arena alone. The collapse of Arabtec cleared out the weakest players, but it left behind a smaller, tougher field of survivors and state-backed giants. Let's war-game the competition.

Closest to home is شركة الشفار للمقاولات العامة ASGC (Al Shafar General Contracting), a formidable privately held UAE builder with a strong reputation in high-end hospitality and institutional work, generating an estimated AED 4–5 billion in annual revenue. ASGC is the kind of rival that competes head-to-head with ALEC on Dubai's premium projects and keeps it honest on price and quality.

Then there is the giant from the East: الشركة الصينية الحكومية لهندسة البناء CSCEC (China State Construction Engineering Corporation), whose Middle East operation generates an estimated AED 5–6 billion locally. CSCEC is the world's largest construction company by revenue, an instrument of Chinese state capacity, and it bids aggressively on high-volume infrastructure. Its weapon is scale and a low cost of capital backed by the Chinese state — a mirror image, in some ways, of ALEC's own sovereign advantage, which makes it the most structurally dangerous competitor of all. But there is a limit to its reach, and it is a revealing one. The most sensitive, most prestigious, most strategically symbolic projects — the sovereign crown jewels — tend to flow to nationally aligned builders, not to a foreign state's contractor, however cheap. CSCEC can win the volume infrastructure; it is far harder for it to win the One Za'abeels. That is the practical boundary of ALEC's cornered resource at work: it doesn't make ALEC cheaper than the Chinese, but it makes ALEC trusted for the work that matters most to the state.

The largest battleground, though, is Saudi Arabia, where the kingdom's Vision 2030 program — its sweeping effort to diversify the economy away from oil by building entire new cities and tourism destinations from scratch — has unleashed a torrent of "giga-project" spending. Here ALEC squares off against the Saudi national champions. شركة نسما وشركاهم Nesma & Partners is a civil-engineering heavyweight driving over $3 billion (north of AED 11 billion) in annual revenue across the kingdom's giga-projects. شركة البواني Al-Bawani is a diversified Saudi conglomerate with an estimated $2 billion-plus in construction turnover.

And then there is شركة السيف مهندسون مقاولون El Seif Engineering Contracting, one of Saudi Arabia's largest contractors — and here the story takes an interesting turn, because El Seif is not just a rival but a partner. The two firms formed a joint venture that in 2024 won a roughly $750 million (SAR 2.8 billion) contract to build Aquarabia, the Middle East's largest water theme park, at Qiddiya near Riyadh — a sprawling project covering some 252,000 square metres with twenty-two rides and a clutch of world-record attractions.12 This is how the smart players navigate a foreign market: rather than fight a well-connected local giant on its home turf, ALEC teamed up with one, combining its own technical execution with El Seif's local relationships and labour access. It is competition and cooperation in the same breath — the defining posture of a foreign contractor trying to ride the Saudi wave without drowning in it.

There's a strategic subtlety in how ALEC enters Saudi Arabia that's worth dwelling on. The kingdom is not a free market for foreign contractors; it actively favours local content, local employment, and local partners, and it can be a graveyard for outside firms that underestimate how different it is from Dubai. By entering through joint ventures rather than as a lone foreign bidder, ALEC gets the best of both worlds: access to the world's largest construction pipeline, with a local partner absorbing much of the political, labour, and payment risk. It also means ALEC's Saudi growth is, to a degree, shared growth — it won't capture 100% of the economics of every project it touches there. That's the price of admission, and it's a sensible one to pay. A smaller share of an enormous, lower-risk pie beats a full share of a project that lands you on the wrong side of local sentiment.

Surrounding the core building and energy businesses, ALEC has also seeded a cluster of adjacent ventures that give it real optionality without betting the company on any single one. ALEC Data Center Solutions is perhaps the most strategically resonant: the AI boom has triggered a global scramble to build data centres, and the Gulf — flush with cheap energy, capital, and political will to become an AI hub — is positioning itself as a major destination for that infrastructure. These facilities are enormously demanding in exactly the discipline ALEC excels at — the intricate mechanical, electrical, and plumbing systems that keep tens of thousands of densely packed, heat-spewing servers cooled and powered without a flicker of downtime. A data centre is, in engineering terms, far closer to a complex industrial plant than to an office block; the building shell is almost the easy part, and the value sits in the systems. That is high-margin, high-complexity work, squarely in ALEC's wheelhouse, and it rides one of the most powerful secular demand curves of the decade. If even a fraction of the Gulf's data-centre ambitions materialize, ALEC has planted itself directly in the path of the spending. LINQ Modular pushes into off-site, factory-built construction — assembling building components in a controlled facility and trucking them to site — which is precisely the kind of innovation that can accelerate Saudi giga-project timelines where skilled on-site labour is scarce and deadlines are political. And ALEC Fitout captures the lucrative downstream end of a project: the high-end interior finishing of luxury hospitality at flagship Saudi destinations like the Red Sea and Amaala resorts, where the spend per square metre — and the margin — is at its richest.

It is worth being disciplined about how to size these adjacencies, because this is exactly where construction companies historically destroy value — the dreaded "diworsification," where a firm that's good at one thing wanders into unrelated ventures and dilutes its returns. The healthy version, which ALEC appears to be pursuing, is adjacency that reinforces the core: data centres, modular, and fit-out all draw on the same project-management muscle, the same client relationships, and the same execution discipline as the main business, while capturing margin the company would otherwise hand to a third party. The unhealthy version would be ALEC deciding to, say, become a property developer or a financier and taking balance-sheet risk it doesn't understand. So far the company has stayed firmly on the right side of that line — extending the value chain rather than abandoning it. An investor's job is to keep watching that boundary.

None of these adjacencies is, on its own, the story. But together they show a company methodically extending its reach along the value chain, capturing margin at every stage from foundation to fit-out, and planting options in the fastest-growing corners of the market. The question, then, is who is steering all of this — and that brings us to the man in the corner office.

VI. Leadership & Corporate Alignment: The Barry Lewis Era

There is a particular type of corporate leader that institutional investors quietly love and that the business press tends to ignore: not the charismatic founder with a reality-distortion field, but the lifer — the executive who walked in the door as a junior, learned every inch of the business from the inside, and rose over decades to run the whole thing. ALEC's CEO, Barry Lewis, is exactly that kind of leader.

Lewis joined ALEC in 2002 as a Contracts Manager — a mid-level role that sits at the unglamorous, vital intersection of engineering and money, where someone has to understand both how the building gets built and how the company gets paid for it. This is, not coincidentally, exactly the discipline where contractors live or die: the management of contracts, claims, variations, and risk allocation. A CEO who came up through that function rather than through pure engineering or pure finance has internalized the single most important survival skill in the trade — knowing precisely what you are and aren't agreeing to when you sign. From there he worked his way methodically up through the organization over two decades, absorbing the institutional knowledge that you simply cannot hire from outside, until he was appointed Chief Executive Officer in October 2023.11 He succeeded Kez Taylor, the long-serving chief executive under whom ALEC had executed the Target deal and much of its modern expansion — a handover that, far from representing a rupture, reflected continuity of culture from one long-tenured insider to another. By the time Lewis took the top job, he had lived through the company's entire transformation — the boom years, the 2008 crisis, the ICD takeover, the Target acquisition, and the post-Arabtec land grab. He didn't read about ALEC's evolution in a briefing book; he helped build it.

That continuity reflects something deeper about ALEC's culture, which traces back to its founding partnership with South Africa's Grinaker-LTA. The South African construction tradition produced a generation of pragmatic, technically rigorous builders who exported their expertise across Africa and the Gulf, and ALEC's senior bench has long carried that imprint. It is an engineering-led culture rather than a financier-led or a relationship-led one — a culture where the people at the top have personally stood on sites and solved problems, not merely modelled them in spreadsheets. For a business where the gap between a drawing and a delivered building is where all the money is made or lost, having operators rather than dealmakers in charge is itself a competitive trait.

This matters more than it might seem, and it's worth saying plainly: in a business defined by the catastrophic risks of over-promising, deep institutional memory is itself a risk-management asset. A contractor's worst wounds are almost always self-inflicted — bidding too aggressively, mispricing complexity, taking on a client who won't pay. A CEO who has personally watched rivals destroy themselves chasing "hollow" revenue is a CEO who knows in his bones which contracts to walk away from. ALEC's leadership story is one of accumulated judgment, not founder bravado, and for a company whose fortunes hinge on disciplined bidding, that is precisely the temperament you want.

But temperament alone doesn't align a management team with shareholders — incentives do. And as ALEC stepped into public-company life, it put in place an architecture designed to make sure the people running the business get rich the same way the owners do. According to the disclosures around its listing, aggregate senior executive remuneration ran to roughly AED 15.34 million in the 2025 financial year across the executive team19 — a figure that is notably restrained for a company of ALEC's scale, signalling that the heavy lifting on alignment was meant to come not from salary but from performance pay and equity.

The centrepiece is a cash-based three-year Long-Term Incentive Plan running from 2025 through 2027, and its design is telling.19 Rather than rewarding executives simply for growing the top line — the very behaviour that has historically destroyed contractors — the plan is pegged to structural targets: return on equity, margin retention within the backlog, and disciplined growth. In other words, management gets paid for building a better business, not just a bigger one. That distinction is the whole game in construction. It is entirely possible to double your revenue and go bankrupt doing it; the LTIP is explicitly engineered to make sure ALEC's leaders never confront that temptation.

The alignment extended to the listing itself. When ALEC came to market on the DFM in October 2025, the offering carved out a dedicated tranche reserved for eligible ALEC and ICD employees, giving senior staff and site directors the chance to buy directly into the equity — so that the people pouring the concrete also own a piece of the company that bills for it.19

The mechanics of that listing are themselves revealing about ALEC's character. ICD sold one billion shares — 20% of the company — at AED 1.40 apiece, implying a market capitalization of around AED 7 billion (roughly $1.9 billion) for the whole business.17 Note what this wasn't: it was not a capital-raise where the company itself issued new shares to fund expansion. It was a sell-down by the sovereign parent, which retained the other 80%. That structure tells you two things. First, ALEC didn't need the money — its balance sheet was already strong enough that it wasn't going public to plug a funding gap, which is exactly the posture you want from a contractor. Second, ICD chose to keep the overwhelming majority of the company, signalling that this was about creating a public benchmark, a currency, and a measure of accountability — not about cashing out. A sovereign owner that keeps 80% has not lost faith; it has invited the public to ride alongside it.

And then there is the dividend, which is where the alignment becomes tangible for every shareholder, executive and outsider alike. ALEC came public promising to behave less like a cash-hungry contractor and more like a yield instrument. Its first Annual General Assembly, in March 2026, approved a dividend payout of AED 250 million.13 The company has guided to AED 500 million in dividends for the 2026 financial year, paid semi-annually, under a stated policy of distributing no less than 50% of net profit.16 For a construction firm — an industry where cash is traditionally hoarded against the next crisis or swallowed by working capital — committing to hand half of profits back to owners is a remarkable statement of confidence in the durability of the cash flows. It says, in effect: we are no longer a fragile contractor that needs to clutch every dirham; we are a financially fortified machine that can afford to pay you. Whether that confidence is justified depends entirely on the strength of the moat beneath it — so let's interrogate that moat directly.

VII. Strategic Moats: Porter's 5 Forces & Hamilton's 7 Powers

We've now seen what ALEC does and how it got here. The harder question — the one that actually determines whether this is a good long-term business or just a company enjoying a cyclical boom — is why the advantages should persist. Let's run ALEC through two of the frameworks investors use to stress-test durability: Hamilton Helmer's 7 Powers and Michael Porter's Five Forces.

Start with what Helmer would call ALEC's Cornered Resource — and this is, without question, the company's deepest and least replicable power. ALEC's controlling shareholder is the Investment Corporation of Dubai. That single fact is something no competitor can copy, buy, or out-execute. It is not a contract that can be lost or a patent that expires; it is a structural relationship with the sovereign wealth of Dubai itself. Concretely, it does three things at once. It grants privileged access to Dubai's premier state-linked developments — One Za'abeel, for instance, was developed by Ithra Dubai, itself an ICD company, which tells you everything about how this cornered resource converts into work. It confers a level of trust that lowers the company's bonding and financing costs, because counterparties know the Dubai state stands behind it. And it provides a cost of capital that private rivals simply cannot match. A private contractor can match ALEC's engineers and even its equipment; it can never match ALEC's parent. This is the power that turns a good contractor into a national champion.

The second power is Process Power — the accumulated, hard-won execution capability built over twenty-five years that cannot be written down in a manual and handed to a new entrant. The knowledge required to build the deepest basement in the Middle East, to pre-camber towers for a cantilevered skybridge, to fabricate offshore energy structures to petroleum-grade standards — this is tacit knowledge, living in the heads and habits of thousands of engineers and project managers and refined through repeated, escalating challenges. A well-funded newcomer could buy cranes and hire staff, but it could not buy the institutional muscle memory of having done the hardest jobs and learned from the inevitable mistakes. Complexity, once mastered, compounds.

The third power is Scale Economies. ALEC spreads its substantial fixed costs — corporate overhead, advanced digital design and modelling systems, and expensive specialized assets like Target's marine fleet — across a backlog now exceeding AED 35 billion. The larger the order book, the thinner those fixed costs spread per project, and the more competitive ALEC can be on any given bid while still protecting its margin. Scale begets cost advantage, and cost advantage begets more scale — a flywheel that the post-Arabtec consolidation has only accelerated.

The fourth power, Switching Costs, is selective but real. In standard commercial building, switching costs are low — a developer can swap one tower contractor for another between projects. But in the marine and energy segment that Target brought in, they are formidable. Once an offshore or EPCIC contract is underway, replacing the engineering contractor mid-stream is prohibitively expensive and carries the threat of catastrophic delay on assets where downtime is measured in millions per day. That stickiness is exactly why the Target acquisition added not just diversification but defensibility to ALEC's revenue.

It's just as instructive to name the powers ALEC doesn't have, because honesty about the limits of a moat is what separates analysis from cheerleading. ALEC has little in the way of Network Economies — its product doesn't get more valuable as more people use it, the way a marketplace or a social platform does. It has only modest Branding power in the consumer sense; a tourist visiting SeaWorld Abu Dhabi neither knows nor cares who poured the foundations, though within the narrow world of sovereign procurement, ALEC's reputation for delivery does carry real weight. And it has essentially no Counter-Positioning — it is not a disruptive upstart with a business model incumbents can't copy; if anything, ALEC is the incumbent. The honest conclusion is that ALEC's durability rests overwhelmingly on its cornered resource and its accumulated process power, buttressed by scale. That's a narrower foundation than a company with five overlapping powers — but the cornered resource is so structurally unassailable that it carries enormous weight on its own.

Now flip the lens to Porter's Five Forces, which examines the structural attractiveness of the industry ALEC competes in. The threat of new entrants is extremely low: the capital, the technical certifications, and above all the bonding capacity required to even bid for a multi-billion-dirham mega-project form a wall that almost no newcomer can scale. The threat of substitutes is essentially nil — there is no software workaround for a physical airport or a 100-storey tower; complex infrastructure simply has to be built by someone who can build it.

The bargaining power of buyers is the most genuinely two-sided force, and it cuts both ways. ALEC's clients are colossal and powerful — sovereign developers and entities like Saudi Aramco, the Public Investment Fund, Aldar, and ICD itself — and concentrated buyers of that magnitude can dictate terms. But the flip side is that for the truly complex, multi-billion-dollar scopes, those same buyers have only a handful of contractors on earth capable of delivering. When you need a horizontal skyscraper built over a live highway, your negotiating leverage as the client is real but bounded — you cannot simply threaten to take your business to a firm that doesn't exist. Power, here, is shared.

Finally, the intensity of rivalry — and this is the most important structural shift in the whole story. For decades, GCC construction was a fragmented, brutal race to the bottom, with too many contractors slashing prices until they bled out. Arabtec's collapse, and the consolidation that followed, is transforming that dynamic into something far more attractive: a disciplined oligopoly of state-aligned champions — ALEC, ASGC, CSCEC, the Saudi nationals — competing on capability and survivability rather than on suicidal pricing. An industry that punishes its participants is slowly becoming one that rewards a select few. For the survivors, that is the best news of all.

Put the two frameworks together and the picture is coherent: a company with a genuinely uncopyable cornered resource, reinforced by process power and scale, operating in an industry whose structure is shifting decisively in favour of the strong. That is the bull case in its purest form — but it is not the whole story.

VIII. The Investment Case: Bull vs. Bear Playbook

So where does all of this leave a long-term investor weighing ticker ALEC.DB? Let's lay out both sides of the table honestly, because a story this strong invites the temptation to ignore what could go wrong.

The bull case writes itself from everything we've covered. ALEC is the undisputed national-champion builder of the UAE, backed by the sovereign wealth of Dubai, riding two enormous tailwinds at once: the post-Arabtec consolidation that has thinned the field of credible rivals, and the multi-decade, multi-trillion-dollar construction wave unleashed by Saudi Vision 2030. It is hard to convey the sheer scale of the Saudi opportunity. The kingdom has committed to building entire cities from empty desert — a linear megacity at NEOM, new tourism coastlines, sports and entertainment districts like Qiddiya, and the modernization of its holy cities — a construction program with no real precedent in human history in its concentration of capital and ambition. The constraint on that program is not money; it is execution capacity — the finite number of contractors on earth who can actually deliver complex work at that scale and pace. ALEC, having proven itself on the UAE's hardest projects and having entered Saudi Arabia through partnerships with local champions, is positioned as one of the few credible suppliers of exactly the capacity the kingdom is desperate for. For a contractor, having more qualified demand than there is supply to meet it is the most favourable market condition imaginable, and it could persist for a decade or more. Its cash flows are diversified across building, energy and marine, data centres, modular, and fit-out, so a downturn in any one segment need not sink the whole. The financial profile is the kind that simply did not exist in this industry a decade ago — a near-debt-free balance sheet, a fast-growing backlog, and a commitment to return at least half of profits to shareholders. And the early public results have reinforced the narrative rather than undercut it: revenue more than doubled from AED 3.6 billion in 2022 to AED 8.1 billion in 2024, with net income reaching AED 363 million and EBITDA margins expanding to around 8%[^15]; full-year 2025 net profit nearly doubled to roughly $117.6 million following the listing14; and the first quarter of 2026 saw revenue jump 87% with net profit more than doubling year-on-year.15 This is a company executing, not just promising.

But a serious investor's job is to spend at least as much time on the bear case, and there are three risks here worth taking seriously.

The first and sharpest is what we might call giga-project risk — and it is, ironically, the dark side of the very Saudi boom that powers the bull case. Those enormous Vision 2030 contracts are frequently structured as fixed-price or lump-sum turnkey deals, which means ALEC bears much of the risk if costs run away. In an environment of raw-material inflation, regional labour shortages, and stretched supply chains, a contract priced today can become a money-loser by the time it is delivered years from now. This is precisely the mechanism that killed Arabtec, and no amount of sovereign backing fully neutralizes it — it can only be managed through disciplined bidding. The LTIP we examined is designed to enforce that discipline, but the temptation to chase the kingdom's gushing volume is exactly the kind of pressure that has destroyed contractors before.

The second risk is buyer concentration, the shadow side of ALEC's greatest strength. The same sovereign relationships that guarantee privileged access also create dependence. A meaningful slice of ALEC's pipeline flows from a small number of state-backed developers — ICD, PIF, Aldar, the giga-project authorities. If oil prices fall hard, or if Riyadh or Dubai decides to slow or re-sequence its capital-spending ambitions, that decision lands directly on ALEC's future bookings. Concentration is a wonderful thing on the way up and a dangerous thing on the way down, and it is largely outside management's control.

The third is geopolitical volatility. ALEC operates in a region where escalation is a permanent tail risk. A serious regional conflict could disrupt the international shipping that delivers materials, rattle the credit markets that underpin project finance, and freeze the very developer spending the company depends on. This is not a prediction; it is simply an ever-present overhang that any investor in Gulf infrastructure must price.

There is also an accounting dimension that any serious investor in a contractor must hold in mind, and it is not a red flag so much as a permanent feature of the terrain. Construction firms recognize revenue using the "percentage-of-completion" method — they book a portion of a contract's revenue and profit as the work progresses, based on management's estimate of how complete each project is and what it will ultimately cost to finish. That estimate is inherently a judgment call. If management is too optimistic about final costs, profit gets pulled forward that may never materialize, only to reverse in a nasty write-down later. This is not a knock on ALEC specifically; it is true of every contractor on earth. But it means the quality of reported earnings depends on the conservatism of management's cost estimates, which is one more reason the disciplined, operator-led culture and the margin-focused incentive design matter so much. The figures are only as good as the judgment behind them — and judgment is exactly what twenty-five years of institutional memory is supposed to provide.

Given all that, what should a fundamental investor actually watch? Not the noise of individual contract announcements, but a tight handful of metrics that reveal whether the machine is genuinely healthy. We'd zero in on three.

The first is the rate at which ALEC converts its backlog into revenue without margin slippage — what you might call execution velocity. A huge backlog is only valuable if it gets built profitably and on schedule; a backlog that converts slowly, or that converts into low-margin or loss-making revenue, is a warning that the company has bought growth at the expense of quality. Watching how cleanly that AED 35 billion order book turns into earnings is the single best read on whether ALEC is staying disciplined.

The second is operating and EBITDA margin retention. The entire thesis rests on ALEC being a high-quality contractor that holds its margins where commodity builders cannot. If those margins start eroding under inflationary or competitive pressure, it would signal that the moat is leakier than the story suggests. Stable-to-rising margins, by contrast, are the clearest evidence that the complexity-driven advantage is real and durable.

The third is the health of the balance sheet — net cash and working capital. ALEC's fortress finances are central to its identity, and the classic way a contractor secretly rots is through ballooning receivables: revenue booked but never collected, cash quietly draining into unpaid client invoices. Watching that the company stays in a strong net-cash position and keeps its receivables under control is the surest way to confirm that the "financially fortified machine" remains exactly that — and has not slipped back into the fragile, cash-starved model that defines the industry's history.

Track those three, and you will understand ALEC's trajectory far better than any headline contract win could tell you.

IX. Outro & Reflections

Step back from the numbers and the frameworks, and two things about this story genuinely surprise.

The first is the sheer violence and speed of the regional reset. Arabtec was not a marginal player that quietly faded; it was the company that built the tallest structure in human history, and it collapsed under $2.75 billion of liabilities in a matter of months. That an institution so iconic could die so fast — and that a single rival could move so decisively into the vacuum, scooping up a crown-jewel energy business for a fraction of its worth while the credit markets were frozen shut — is a reminder of how brutally and how quickly fortunes turn in this industry.

The second, and deeper, surprise is the alchemy at the centre of the whole tale. Construction is, almost universally, a bad business — cyclical, capital-punishing, margin-starved, and littered with bankruptcies. And yet ALEC demonstrates that when you take that same fundamentally fragile activity and align it with a sovereign parent, fortify the balance sheet, diversify into defensible niches, and impose genuine bidding discipline, you can re-engineer it into something almost unrecognizable: a high-margin, low-debt, dividend-paying machine that behaves more like a strategic state asset than a contractor. The business didn't change its trade. It changed its structure — and structure, it turns out, is destiny.

There's a final reflection worth offering for the long-term investor, and it cuts against the grain of how construction companies are usually perceived. The instinct is to treat any contractor as a cyclical bet — buy at the bottom of the building cycle, sell at the top, never fall in love. ALEC complicates that instinct. To the extent its cornered resource is real and durable, to the extent its energy and adjacency segments genuinely de-correlate its cash flows, and to the extent its sovereign parent keeps channelling the region's most ambitious work its way, ALEC may behave less like a pure cyclical and more like a quasi-infrastructure compounder with a dividend attached. "May" is the operative word — every one of those conditions is a thing to be verified over years, not assumed. But the very fact that the question is open — that a contractor could plausibly be a durable, defensive, income-generating holding rather than a trade — is itself the measure of how thoroughly ALEC has rewritten the rules of its trade.

That is the real meaning of ALEC's arrival on the Dubai Financial Market under the ticker ALEC.DB. It is not merely a builder going public. It is the institutionalization of the Gulf's physical infrastructure engine — the moment the machine that pours the concrete behind a nation's ambitions becomes a publicly owned asset that ordinary investors can hold. ALEC does not just build buildings. It builds nation-scale ambition, one pre-cambered tower at a time, and it has now invited the public to own a piece of the foundations.

References

-

One Za'abeel achieves the Guinness World Records™ title for the 'Longest Cantilevered Building' in the world — PR Newswire, 2024-03-26 ↩↩↩↩

-

ALEC Holdings Debuts on DFM in UAE's Largest-Ever Construction Sector IPO — Dubai Media Office, 2025-10-15 ↩

-

ALEC IPO raises $381m after 21x oversubscription in UAE's biggest construction listing — Arabian Business, 2025-10 ↩

-

Dubai builder Alec Holdings to sell 20% in listing — AGBI, 2025-09 ↩

-

Rise and fall of UAE Arabtec: From building Burj Khalifa in Dubai and Louvre Abu Dhabi, to filing for bankruptcy — Gulf News, 2021 ↩↩

-

ICD-owned Alec Engineering to acquire UAE company Target amid oil and gas expansion — The National, 2022-12-20 ↩↩

-

Exclusive: ALEC's CEO Kez Taylor discusses $100mn TARGET Engineering acquisition — Middle East Construction News, 2022 ↩

-

ALEC announces appointment of Barry Lewis as CEO — Zawya, 2023-10 ↩

-

El Seif-ALEC JV Inks $750mn Deal For KSA's First Water Theme Park In Qiddiya — MEP Middle East, 2024 ↩

-

ALEC Holdings' first Annual General Assembly approves AED 250mln dividend payout — Zawya, 2026-03-26 ↩

-

ALEC Holdings net profit more than doubles to $117.63 million following high-profile listing on DFM — Economy Middle East, 2026 ↩

-

ALEC Holdings Finalizes IPO At AED 1.40 Per Share — Construction Business News Middle East, 2025 ↩

-

Alec Holding raises $381m in Dubai IPO — The National, 2025-10-01 ↩↩

-

Alec IPO orders hit $8bn on global investor demand — AGBI, 2025-10 ↩

-

ALEC IPO prospectus and offering details — ALEC Holdings ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube