Aksigorta: Navigating the High-Stakes World of Turkish Risk

I. Introduction: The "Float" in a Hyper-Inflationary World

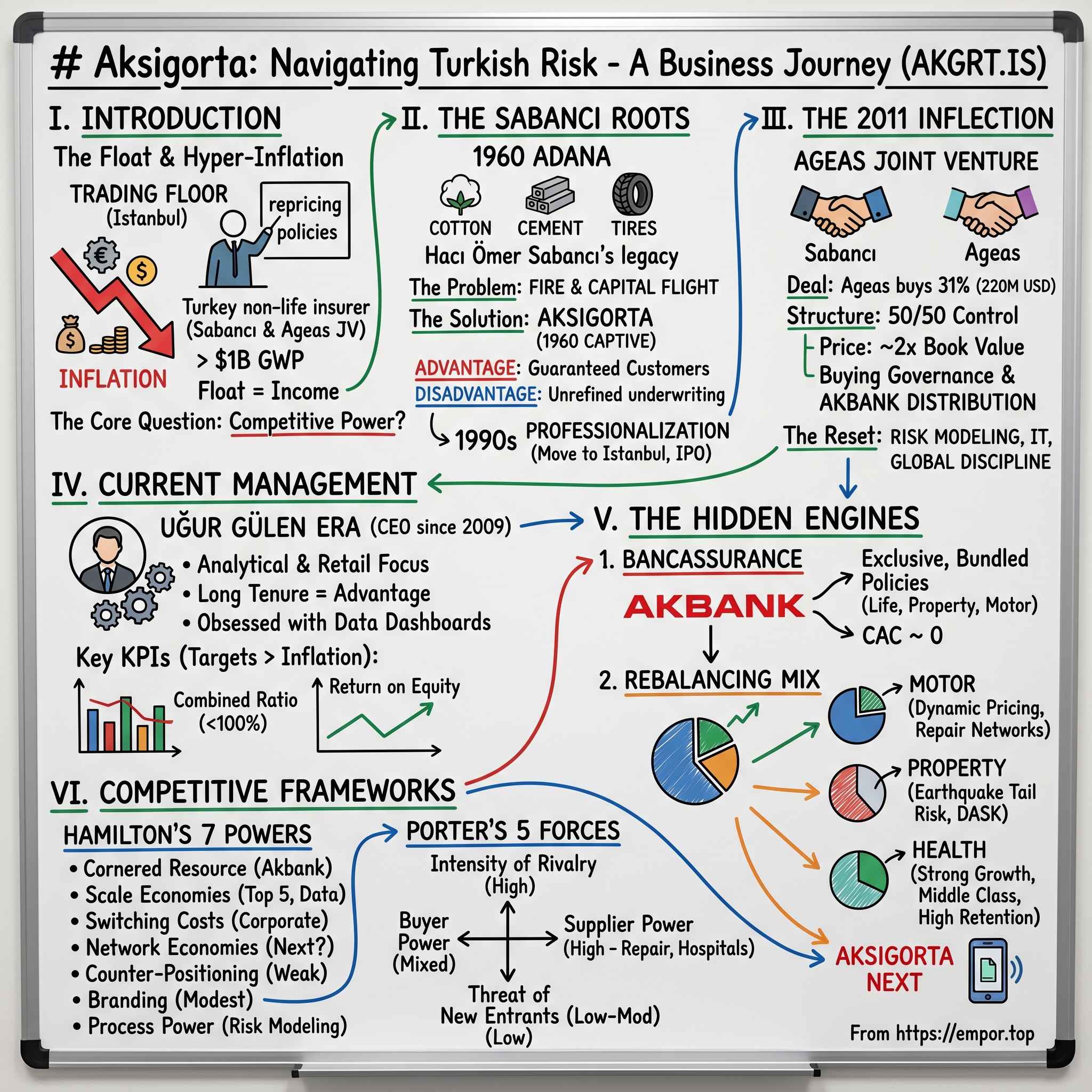

Picture a trading floor in Istanbul on a Tuesday morning in late 2022. The Turkish Lira has just crossed another psychological threshold against the dollar, bank economists are rewriting their year-end forecasts before lunch, and a young actuary at an insurance company in the Levent financial district is doing something that would look absolutely bizarre to her counterpart in Zurich or London. She is not updating a quarterly model. She is not revising an annual pricing grid. She is repricing motor insurance policies for tomorrow morning. Again.

This is the daily reality at Aksigorta A.S., and it is the first clue that Turkish insurance is not the sleepy, regulated utility business most Western investors imagine. In a country where headline inflation has at times blown past 70%, where the cost of a single imported brake caliper can leap 15% in a week, and where the central bank has spent half a decade being the most interesting monetary authority on the planet, insurance is not a boring business. It is an extreme sport.

The statistics, in isolation, paint a respectable mid-cap financial services company. Aksigorta is one of the five largest non-life insurers in Turkey, part of the sprawling Sabancı Holding empire, owned fifty-fifty in a joint venture with Belgian-Dutch insurance giant Ageas, and writing more than a billion dollars in gross written premiums annually. But statistics alone miss the point. The story of Aksigorta is really a story about how you build durable competitive advantage—what Hamilton Helmer would call "Power"—in a commodity product, sold in a currency that refuses to hold still, inside a country where the rules rewrite themselves every couple of quarters.

And here is the quiet secret most retail investors overlook. When inflation runs hot and interest rates run hotter, a well-capitalized insurance company is not really an insurance company anymore. It is a lightly regulated asset manager with negative working capital, a captive distribution moat, and an embedded call option on every earthquake, hailstorm, and fender-bender in the country. The technical term is "float," the Buffett-popularized idea that premiums collected today can be invested for years before claims come due. In a country where overnight deposit rates have recently sat in the mid-forties, that float is not a rounding error on the income statement. It is the income statement.

The theme of this episode is how Aksigorta, starting as a modest captive insurer for a family conglomerate in Adana in 1960, has navigated sixty-five years of Turkish economic drama—coups, currency crises, IMF programs, AKP-era booms, pandemic shutdowns, devastating earthquakes—and emerged as a global joint-venture powerhouse. The central question is deceptively simple. In a market that eats lazy operators for breakfast, what are the sources of Power that let this one company keep compounding equity faster than inflation? The answer involves a Belgian multinational, a distribution deal with one of Turkey's largest banks, a CEO with a fifteen-year tenure that would make any governance scorecard blush, and a quietly obsessive data culture that would not feel out of place at Progressive or GEICO.

Let's start where every good conglomerate story starts: with a patriarch, a province, and a very long memory.

II. The Sabancı Roots & The Old Guard

The year was 1960, the place was Adana in southern Turkey, and Hacı Ömer Sabancı had been dead for exactly nine years. His sons—six of them, with the eldest, Sakıp Sabancı, already emerging as the strategic mind of the family—were running an industrial empire that their father had built from a single cotton brokerage. Textiles, cement, cooking oil, eventually synthetic fibers, tire cord, banking. The Sabancı name in the Adana of that era was not just a corporate brand. It was woven into the economic fabric of Çukurova, the agricultural heartland of Anatolia, the way the Rockefellers had been to Cleveland or the Agnellis were to Turin.

And like every industrial family running a manufacturing empire in the mid-twentieth century, the Sabancıs had a problem that kept them awake at night. Fire. A single warehouse blaze at a cotton gin could vaporize a quarter's profits. A cement kiln accident could idle a plant for months. Western insurers were happy to sell them policies, but the premiums were punitive, the coverage was limited, and—more importantly—the capital kept leaving the country. Every lira of insurance premium paid to a London or Zurich underwriter was a lira that did not circulate within the family ecosystem.

So in 1960, the Sabancıs did what every good industrial dynasty eventually does. They founded their own insurance company. Aksigorta, initially capitalized modestly, was not a growth venture in any conventional sense. It was a captive. Its first customers were Sabancı factories. Its first underwriters were family associates. Its first actuarial mission was straightforward: insure the conglomerate cheaper and better than foreign carriers would, and keep the float inside the house.

For roughly the first three decades of its life, Aksigorta operated in exactly this mode. It was a corporate appendage, sold policies almost exclusively to Sabancı group companies and their business partners, and collected premiums in a lira that, to be charitable, had a complicated relationship with inflation even in that era. The advantages were obvious. A guaranteed customer base. Low distribution costs. A built-in information advantage about the specific risks at hand. The disadvantages were equally obvious. It never had to sharpen itself against independent competition. It never had to build real underwriting muscle for the mass market. It was, in Michael Porter's vocabulary, a classic case of "stuck in the middle"—not really a standalone business, not really a pure cost center.

The shift started quietly in the 1980s and early 1990s, as Turkey began its painful and halting transition from an import-substitution economy to an export-oriented one, and as the Sabancı family itself began professionalizing. Sakıp Sabancı, by then the public face of the group and arguably the second most famous businessman in the country, moved the headquarters of the holding company from Adana to Istanbul. The Sabancı Center twin towers in Levent, completed in 1993, became the visible symbol of the transformation. And with that move came a subtle but profound reframing of what Aksigorta was supposed to be.

Sakıp and the next generation of family managers started asking a question that, in retrospect, changed everything. What if insurance was actually a better business than textiles? Textiles required constant capital reinvestment, cutthroat pricing from low-cost Asian competitors, and exposure to raw material volatility. Insurance, done right, required capital discipline, pricing intelligence, and distribution. And insurance had something that manufacturing did not: negative working capital. The customer paid you upfront, and you paid the claim sometimes years later. Between those two events, the money was yours to invest. In a country where real interest rates were often double digits, that was not a nice side benefit. That was the whole game.

By the late 1990s, Aksigorta had been spun into a more formal standalone subsidiary, had listed its shares on the Istanbul Stock Exchange (as the exchange was then called), and had started competing seriously in motor insurance, property, and the early stages of health. The family had grasped something fundamental. An insurer is essentially a leveraged bet on disciplined underwriting plus asset management, and in a country with Turkey's macro profile, that was a structurally advantaged business model. But to really make it work, the company needed two things it did not yet have at scale: world-class actuarial technology, and distribution that extended far beyond the walls of Sabancı Center.

The answer to both came knocking on the door in Brussels.

III. The 2011 Inflection Point: The Ageas Marriage

The conversation reportedly started, as these things often do, over a long dinner. The year was 2010, and Fortis had just become Ageas—the Belgian-Dutch insurance group that had emerged, battered but alive, from the wreckage of the 2008 financial crisis. Ageas, under the restructuring leadership of Bart De Smet, was explicitly pivoting away from its old banking entanglements and toward being a pure insurance play, with a particular appetite for emerging markets. Asia was already well-developed in its portfolio, with successful joint ventures in China, Malaysia, and Thailand. The missing piece was a bridge market between Europe and Asia, and Turkey, with its young demographics, low insurance penetration, and complicated but ultimately bankable institutions, kept coming up in every strategic review.

On the other side of the table, Sabancı Holding was executing its own pivot. The family had already partnered with foreign financial giants—think of the Sabancı-Citigroup stint at Akbank, or the various ventures in retail and energy with European and American counterparts. The playbook was clear. In businesses that required deep global expertise and heavy technology investment, the family was happy to share ownership with a best-in-class foreign partner, provided the distribution, brand, and local governance stayed under Sabancı stewardship.

The deal that closed in July 2011 was, at the time, one of the largest insurance M&A transactions ever completed in Turkey. Ageas purchased a 31% stake in Aksigorta from Sabancı Holding for approximately 220 million US dollars. That, combined with the 31% that Sabancı retained, created a 50/50 joint control structure via a holding entity, with the remaining stake floating on the public market. The headline valuation put Aksigorta at roughly two times book value. For a Turkish insurer in 2011, with the Lira trading at around 1.8 to the dollar and motor insurance pricing still tightly regulated, that was a full price. European peers were trading at closer to one times book at the time. Skeptics muttered about overpayment.

In hindsight, the skeptics were looking at the wrong line on the model. Ageas was not buying a book of motor policies. Ageas was buying two things that are extraordinarily hard to replicate: governance proximity to Sabancı Holding, and the cornered resource that is a distribution agreement with Akbank. We will come back to Akbank in a moment, because it deserves its own treatment, but the point for now is that the true underwriting of the Ageas deal was not about the 2011 combined ratio. It was about buying a permanent seat at the table of one of the most strategically located insurance markets in the Eastern Mediterranean basin.

The cultural reset that followed was, arguably, more important than the capital injection. Ageas did not parachute in a Belgian CEO. It did not demand a rebranding. What it did do—quietly, patiently, and over the course of several years—was install the risk modeling, reinsurance negotiation practices, Solvency II-style capital management, and IT backbone that a global insurer expects as table stakes. Turkish actuaries were sent to Brussels for training. European catastrophe models were calibrated for Turkish seismic risk, pulling in the hard-won lessons of the 1999 Marmara earthquake and the more recent tremors. Management reporting shifted from lira-denominated quarterly snapshots to multi-currency, risk-adjusted, rolling twelve-month frames.

For investors, the meta-lesson of the Ageas transaction is worth pausing on. In emerging markets with volatile macro regimes, the best-run local subsidiaries of global financial firms often out-earn both their foreign parents and their domestic pure-play peers. The reason is structural. They get global-grade risk technology and capital discipline, combined with local relationships and information advantages that no foreign entrant can build from scratch. Aksigorta post-2011 became a live case study in that thesis. It was no longer purely a Sabancı captive, and it was no longer just another Turkish insurer. It was something hybrid and, if you squinted at the numbers correctly, uniquely positioned.

Which brings us to the man who has been quietly orchestrating this hybrid for more than a decade and a half.

IV. Current Management: The Uğur Gülen Era

There is a certain archetype of executive that emerging market investors learn to love: the quiet, long-tenured CEO who was promoted from within, speaks fluent finance without being an investment banker, and has survived enough currency crises to have calluses on his calluses. Uğur Gülen, Aksigorta's CEO since 2009, fits that archetype almost to the point of parody. And the "almost" is what makes him interesting.

Gülen joined the Aksigorta world in the late 1990s, spent years rotating through underwriting, actuarial, and corporate strategy functions, and took the CEO chair in 2009—before the Ageas deal, meaning he is the rare executive who led the company through both the pre-joint-venture captive era and the post-joint-venture globalized era. For the math nerds keeping score, that is a tenure now pushing seventeen years at the helm of the same institution. In a market where the median CEO tenure in financial services runs closer to four or five years, that longevity is its own form of competitive advantage. He remembers where every body is buried, every motor portfolio hand grenade, every corporate client that deserves special handling, and every regulatory relationship that matters.

His management style, by reputation, is best described as "obsessively analytical with a retail sensibility." Colleagues talk about his habit of requesting weekly dashboards on the real-time loss ratio in the auto book, broken down by vehicle make, postal code, and policy distribution channel. When supply chain disruptions caused spare part inflation to outrun headline CPI in 2022 and 2023, Gülen was said to be on the phone with repair shop networks personally, pushing for volume contracts that could dampen the pass-through to claim severities. He is not a charismatic CEO in the American mold. He is a detail operator who believes that, in insurance, edge is earned through a thousand small disciplined decisions, not a single big strategic pivot.

The incentive structure under which Gülen and his senior team operate tells you almost everything you need to know about how the company is actually run. The two dominant KPIs, repeated in nearly every investor presentation, are Combined Ratio and Return on Equity. Combined Ratio, for those outside the insurance trenches, is a simple but ruthless metric: the ratio of claims paid plus operating expenses to premiums earned. Anything below 100% means the company made underwriting profit before investment income. Anything above means it depended on investments to turn a net positive. Aksigorta has targeted—and, across most cycles, achieved—a combined ratio comfortably under 100%, which in the Turkish context is non-trivial given that some competitors run persistently above.

Return on Equity is where the Turkish twist comes in. Under normal conditions, a global insurer might benchmark ROE against, say, 10-year local government bonds plus a spread. In Turkey, with inflation running in the double digits for years and nominal interest rates having crossed 50%, the ROE hurdle is defined explicitly against inflation. Management bonuses and long-term compensation are structured so that outperforming inflation by a multiple is the bar, not merely generating a positive nominal number. This is a much harder bar than it looks. A nominal ROE of 40% sounds enormous until you realize inflation ate 60% of it.

The philosophical evolution under Gülen has also been meaningful. The old Aksigorta, even into the early 2010s, was essentially a product-centric insurer. Agents sold policies. Actuaries priced them. Reinsurers took the catastrophic risks. The new Aksigorta describes itself, almost to the point of buzzword fatigue, as a data-centric risk manager. What that actually means in practice is machine learning-driven pricing for motor, with continuous model updates using telematics-adjacent data, repair shop cost feeds, and localized accident frequency heat maps. It means health underwriting that pulls in anonymized demographic and utilization data to segment at a resolution that would have been inconceivable ten years ago. It means the CEO's own quarterly calls spending more time on model hit rates and customer lifetime value than on gross written premium growth.

For investors, the takeaway on management is less about genius and more about alignment. When the same operator has been running the same business for the same controlling shareholders through both a captive era and a JV era, with compensation indexed to an inflation-adjusted return target rather than a nominal one, the governance risk that sinks so many emerging market financials is materially reduced. The question, then, is whether the structural advantages Gülen and his team have to work with are strong enough to keep compounding. Which forces us to look at the engines humming underneath.

V. The "Hidden" Engines: Bancassurance & Digital Next

Imagine you are a foreign insurer looking at Turkey in 2024. The demographics are attractive—a population north of 85 million, a median age in the early thirties, motor insurance penetration still meaningfully below European norms. You have deep pockets, sophisticated actuarial models, and a willingness to lose money for five years to buy market share. You fly to Istanbul, set up an office in a gleaming tower, hire a local management team, launch a slick consumer campaign, and start buying Google ads for "otomobil sigortası."

And then you run into the wall that is Akbank.

Aksigorta's bancassurance agreement with Akbank is the kind of cornered resource that keeps strategic planners at competing firms awake at night. Akbank, also a Sabancı-affiliated institution and one of Turkey's three or four most systemically important private banks, has a branch network, a digital app, and a customer relationship manager army that covers roughly every meaningful economic artery in the country. Under a long-standing exclusive arrangement, when an Akbank customer opens a business account, takes a mortgage, registers a vehicle, secures a personal loan, or even just logs into the mobile app to check a balance, the Aksigorta product offering is woven directly into the user experience. Life coverage bundled with mortgages. Property insurance triggered by home loans. Motor policies offered at the exact moment of auto loan approval. Travel insurance as a one-click add-on to a foreign exchange transaction.

The economics of this channel are brutal for competitors to contemplate. Customer acquisition cost for an insurance product sold through a traditional agency can easily hit 15% to 25% of first-year premium when you factor in commissions, marketing, and administrative overhead. Customer acquisition cost for a product sold through an embedded bancassurance pipe, with the bank already having done the KYC, the relationship-building, and the context-setting, is a small fraction of that—in practice, often well under 10%, and with dramatically higher conversion rates because the product is being offered precisely when the customer's need for it is most salient.

As the prose snippet in the original outline puts it: "Every time someone opens a bank account or takes a mortgage at Akbank, one of the biggest banks in the country, the Aksigorta policy is right there, integrated into the app. It's a customer acquisition cost of near zero. That is the Hidden Engine that makes the Ageas JV so brilliant; they didn't just buy a company, they bought a permanent seat at the table of Turkish commerce."

But bancassurance is only half of the hidden engine story. The product mix inside Aksigorta has been quietly rebalancing in ways that are arguably more consequential than any single distribution deal. The three segments that matter most are motor, property, and health.

Motor insurance, specifically the regulated Traffic (third-party liability) and semi-deregulated Kasko (comprehensive) lines, remains the bread and butter of the book and has historically been the most operationally demanding line. The loss ratios in Turkish motor are extraordinarily sensitive to two things: spare part inflation, which is largely imported and dollar-linked, and regulatory caps on Traffic premiums, which governments of all stripes have used as a cost-of-living management tool. When the Lira weakens sharply and spare part costs spike, motor combined ratios can get ugly fast unless the company has the pricing sophistication to reprice policies frequently and the scale to negotiate parts pricing with repair networks. Aksigorta has invested heavily in both.

Property insurance, driven in part by mandatory earthquake coverage administered through the DASK pool and in part by voluntary homeowner and commercial policies, has been a steadier performer but comes with the ever-present tail risk of a major seismic event. The devastating February 2023 earthquake that struck the Kahramanmaraş region was a brutal reminder. For Aksigorta and the broader Turkish insurance sector, the event triggered large claims, but the reinsurance architecture built over the prior decade—precisely the kind of infrastructure the Ageas partnership had catalyzed—largely did its job. The industry absorbed the shock. The retention the primary insurers kept on their own balance sheets was painful but manageable.

And then there is health, the hidden gem within the hidden engine. Private health insurance in Turkey has been growing at rates that would make a Silicon Valley SaaS founder smile. The dynamics are structural. The Turkish public health system, while ambitious in coverage, is stretched. Wait times in major urban centers for specialist appointments and elective procedures have pushed middle-class families toward private hospital networks. Private hospital capacity, in turn, has expanded rapidly, with groups like Memorial, Acıbadem, and Medical Park building hundreds of new beds. The missing piece in this triangle is payment intermediation, and that is where private health insurance steps in.

Aksigorta's health book has been growing at rates well into double digits—at times flirting with triple-digit year-over-year growth in new policy issuance for certain products. The loss ratios are tighter than motor, the margins more defensible, and the cross-sell potential into the rest of the product suite is enormous. This is the line that most closely resembles a consumer subscription business, with recurring annual renewals, high retention, and a customer lifetime value that compounds as households age into the system.

Layered on top of all of this is "Aksigorta Next," the internal digital-native initiative that the company launched as an attempt to leapfrog itself into the direct-to-consumer era. The positioning is explicit: usage-based, mobile-first, designed for younger customers who would never walk into a bank branch or call an agency. The products being piloted include pay-as-you-drive motor insurance, modular health add-ons, and embedded microcoverage for things like phone damage or travel. It is, in essence, Aksigorta trying to build an internal challenger to itself before an external challenger does. Whether Next scales into a material business line or ends up as a strategic option remains genuinely open. But the willingness to fund it, even during years when inflation and regulatory pressure were making life hard on the core book, speaks to a management team that is not interested in letting the moat atrophy.

Which is a useful segue, because any honest assessment of how durable that moat actually is requires a framework. Two frameworks, really.

VI. Hamilton's 7 Powers & Porter's 5 Forces

Hamilton Helmer's 7 Powers framework is the cleanest modern lens for thinking about durable competitive advantage, and it is particularly useful for a business like Aksigorta where the moat is not obvious to casual observers. Run through the list.

Cornered Resource. This is the clearest and strongest Power in the Aksigorta stack. The Akbank distribution agreement is not replicable. Akbank itself was partially owned at various points by Citigroup and is now effectively controlled by Sabancı Holding and the Sabancı family foundation. The insurance distribution exclusivity flows from a tightly integrated ownership structure and decades of relationship. A competitor cannot simply outbid for it. This is the textbook definition of a cornered resource: an asset whose value accrues disproportionately to its current holder, and whose transfer to a competitor is structurally blocked.

Scale Economies. Turkey is a large enough insurance market that the top five players enjoy real scale advantages in loss adjustment, reinsurance negotiation, IT spend, and data. Aksigorta, sitting in that top cohort for decades, has accumulated a proprietary data set on Turkish motor risk that any new entrant—even a global giant like Allianz, AXA, or Zurich, all of whom operate in Turkey—would take years to replicate at comparable granularity. Scale matters especially in the long tail of exotic risks, like niche commercial lines, where pricing with small data sets is treacherous.

Switching Costs. This one is more nuanced. For a retail motor customer, switching costs are genuinely low. Buying a new policy takes ten minutes online, and loyalty to any particular insurer is thin. But for corporate clients—especially those embedded in the Sabancı ecosystem, where an industrial group has its fire, liability, employee health, and fleet coverage all bundled through a single master relationship—the cost of disentangling and re-tendering is significant. There is also a subtler switching cost in health insurance, where medical histories, prior authorizations, and network relationships create stickiness.

Network Economies. Arguably weak in traditional insurance, but worth watching in the Aksigorta Next initiative, where any move toward ecosystem plays—partnerships with ride-share platforms, connected car manufacturers, or digital health providers—could introduce network dynamics over time.

Counter-Positioning. Not particularly relevant here. Aksigorta is not a disruptor with a business model that incumbents cannot copy.

Branding. Modest. In Turkish retail financial services, the Sabancı name carries weight, and Aksigorta benefits from the halo. But brand is not the decisive lever it is in, say, luxury goods.

Process Power. This is where the story gets quietly interesting. The risk modeling and claims handling operation that has been built over the past decade—in no small part thanks to the Ageas technology transfer—is legitimately a process-based advantage. The ability to reprice policies on very short cycles, to adjust reserves dynamically to inflation, and to use machine learning to detect fraud and triage claims is not something a competitor can bolt on overnight. It took years to develop, and it is embedded in the operating DNA of the firm.

Shift now to Porter's Five Forces, which tells a slightly different but complementary story.

Rivalry among existing competitors is intense. The Turkish non-life market is crowded, with dozens of licensed insurers, and motor in particular has stretches where the entire industry runs at or near underwriting loss, relying on investment income to stay whole. This is Porter's "red ocean," and any investor who does not respect the difficulty of operating in it is going to get educated. Aksigorta's defense is a combination of the scale and process powers above, plus the distribution cornered resource.

Bargaining power of buyers is mixed. Retail customers individually have low bargaining power but collectively shop aggressively on price, thanks to comparison aggregators. Corporate customers, especially large ones, have significant negotiation leverage, which is why relationship continuity and bundled offerings matter.

Bargaining power of suppliers is high, and this is one of the underappreciated stressors on the business. In motor insurance, the real suppliers are auto repair shops and spare parts importers, whose pricing is dictated by global supply chains and the Lira. In health, the suppliers are hospital networks and pharmaceutical distributors, whose pricing has been rising steadily. Aksigorta's counter-move is scale—negotiating master contracts with large repair networks and hospital groups to get volume discounts and price predictability—but the baseline pressure is real.

Threat of new entrants is low to moderate. The capital requirements, regulatory licensing, and distribution requirements create meaningful barriers. Foreign entrants typically come in via joint ventures or acquisitions rather than greenfield, and even then they often struggle to compete with entrenched local players.

Threat of substitutes is low. There is no plausible non-insurance substitute for insurance at scale, though self-insurance by very large corporate groups is a marginal factor.

Pulling these frameworks together, the picture that emerges is of a business with two strong Powers—the Akbank cornered resource and the process edge in risk modeling—supported by scale, set inside an industry with genuinely difficult competitive dynamics. The Powers are the reason the company has managed to earn returns above cost of capital even in brutal years. The industry difficulty is the reason the margins are not richer than they are.

VII. The Playbook: Lessons in Resilience

So how does this actually play out, day to day, in an environment where the ground keeps shifting under everyone's feet? The Aksigorta playbook, observed from the outside across multiple macro cycles, has three recurring moves that are worth cataloging in detail.

The first is dynamic pricing. In a stable-currency, stable-inflation environment, a motor insurer might update its pricing grid two or three times a year, after careful actuarial review. In Turkey, during the worst stretches of 2021 through 2023, Aksigorta was effectively updating motor prices on a near-continuous basis. The mechanism is built on a combination of real-time feeds—spare part inflation trackers, exchange rate moves, repair shop cost indices, and loss development triangles that are recalibrated weekly rather than quarterly. The underwriting engine then pushes adjusted premiums out through the broker network and the digital channels. Customers buying policies on a Monday afternoon may be paying materially different rates than customers who bought on the prior Friday, even for identical risk profiles.

The strategic implication of dynamic pricing is underappreciated. It is not just a defensive mechanism against inflation. It is a Power amplifier. Competitors without the technology and data discipline to reprice continuously either run at underwriting losses or retreat from hard-hit lines entirely. Aksigorta, by maintaining the infrastructure to keep repricing, can hold share in exactly the moments when less-equipped competitors are pulling back. The insurance world has a dynamic that is subtly similar to semiconductor capital spending cycles: the firms that keep investing and adapting through the downturns emerge with disproportionate share when the cycle normalizes.

The second playbook move is sophisticated capital deployment on the investment portfolio. This is where the "float as fuel" dynamic really pays off in a Turkish context. Insurance float is, in essence, an interest-free loan from policyholders that sits on the asset side of the balance sheet. What Aksigorta does with that float is determined by a combination of regulatory capital requirements, asset-liability matching constraints, and investment discretion. Under the current Turkish macro regime, with government bonds yielding rates that would be inconceivable in developed markets, a disciplined insurer can generate substantial investment income on a portfolio that is, by regulation, heavily weighted toward liquid government securities.

The nuance here is critical. In years when the lira weakens sharply and nominal rates spike, the investment income line at an insurer like Aksigorta can temporarily balloon, masking softness in underwriting. In years when rates normalize downward and the currency stabilizes, that investment income shrinks, and any underwriting weakness becomes visible fast. A sophisticated reader of the financials does not just look at net income. They look at the decomposition between underwriting profit and investment profit, and they ask whether the underwriting engine can stand on its own. Aksigorta's history is generally one of a combined ratio below 100%, meaning underwriting is positive, with investment income layered on top. But the quality of earnings varies meaningfully from year to year, and any investor who treats the peak earnings years as the steady state is setting themselves up for disappointment.

The third playbook move is what we will, borrowing Charlie Munger's term, call the "Lollapalooza" effect. It describes the moments when multiple structural advantages compound simultaneously. In Aksigorta's case, the Lollapalooza windows have been the ones where digital transformation, the Ageas partnership benefits, and the Akbank distribution engine all hit at once. The most obvious example was the period from roughly 2017 to 2019, when the core underwriting disciplines had matured, the bancassurance push was accelerating, and the macro environment—while always challenging—had not yet hit the extreme volatility of the early 2020s. Premium growth, profitability, and ROE all moved up together.

The more recent Lollapalooza window, arguably beginning around 2023 as the macro environment started normalizing under Mehmet Şimşek's stewardship at the Finance Ministry and Hafize Gaye Erkan's brief but consequential tenure at the central bank, saw a similar alignment. High nominal interest rates juiced investment income. The health book hit an inflection as private hospital capacity continued to expand. Dynamic pricing in motor finally caught up with spare part inflation. Aksigorta Next started showing the early signs of scaling. Each of these alone is a tailwind. Together, they compound.

The implication for anyone watching the business is that the operating leverage is asymmetric. In difficult years, the firm can hold on thanks to its structural advantages. In aligned years, the earnings power steps up materially. Over a full cycle, if the playbook holds, equity compounds faster than inflation. Which is, not coincidentally, exactly the KPI management is compensated on.

VIII. Bear vs. Bull Case

Any serious analysis of Aksigorta has to stare directly at the genuine risks. There are real reasons thoughtful investors have stayed away from Turkish financials for stretches, and those reasons have not magically disappeared.

Start with the bear case. The single most significant risk is regulatory. The Turkish government, across multiple administrations, has treated mandatory motor Traffic insurance pricing as a tool of cost-of-living management. When the cost of auto repair shoots up and insurance rates threaten to follow, the default policy response has been to cap premium increases below what underwriting math would require. The result is an industry that periodically runs Traffic at a structural loss, subsidized by voluntary Kasko and other lines. This is not a hypothetical risk. It is a recurring feature, and it means the path for motor profitability is always at the mercy of political calculations that have nothing to do with actuarial science.

The second bear case factor is catastrophe risk, and more specifically earthquake risk. Turkey sits on the North Anatolian and East Anatolian Fault systems, and the risk of a major seismic event near Istanbul—a city of 16 million people, with a significant portion of the country's economic activity—is not a tail risk investors can ignore. The February 2023 earthquake in southeastern Turkey, while tragic on a human scale, was geographically distant enough from the major insured property base that the industry absorbed the shock. A major event in the Marmara Sea region would be a different calculation entirely. Reinsurance programs exist to absorb most of the peak loss, but reinsurance in Turkey has gotten materially more expensive post-2023, which flows through to either lower retention (less risk held) or higher ceded premiums (less margin retained).

The third bear case factor is macro itself. Even with the policy normalization that began in mid-2023, Turkey remains a country whose currency can move 15% in a quarter on a political headline. For any investor measuring returns in dollars or euros, the structural drag from lira weakness over long periods is real. A company that compounds equity at 80% in lira terms, in an environment where the lira loses 40% of its value against the dollar, is compounding in dollar terms at a much less exciting rate. Turkish insurance is not a dollar asset, no matter how well the underlying business is run.

The fourth bear case factor is concentration risk. A very large portion of Aksigorta's economic value rests on the ongoing health of the Akbank distribution relationship and the broader Sabancı Holding ecosystem. Any significant dislocation at Akbank—whether from its own credit cycle, governance changes, or regulatory action—would directly impair the value of the bancassurance channel. This is an interconnectedness risk that does not show up in standard insurance ratios.

Now the bull case, which has its own structural weight.

The single most compelling bull argument is insurance penetration. Turkey's non-life insurance penetration, measured as premiums as a percentage of GDP, sits well below European averages and below many of its emerging market peers. Life insurance penetration is even lower. Health insurance, despite the rapid growth, is still nascent as a percentage of households. Every one of these gaps represents multi-decade runway. As the middle class grows, as urbanization continues, as regulatory mandates expand, the share of the economy that flows through insurance premiums is structurally biased upward. An insurer with Aksigorta's distribution and data advantages is positioned to capture a disproportionate share of that growth. As the original outline put it, Aksigorta is the toll booth on that transition.

The second bull argument is the asset management nature of the business in a high-rate regime. So long as Turkish government bonds yield materially above global averages, and so long as Aksigorta's regulatory-mandated asset allocation requires it to hold meaningful quantities of those bonds, the investment income engine has a structural tailwind that is hard to replicate in developed markets. Even as rates normalize, the spread between nominal rates and inflation remains positive in most base cases, which means real returns on float are positive.

The third bull argument is the combination of global-grade capital discipline—courtesy of Ageas—with local-grade distribution and information advantages. Very few competitors can match both. Foreign entrants have the capital discipline but lack the cornered distribution. Local independents have the distribution but lack the capital discipline and technology. Aksigorta sits at the intersection.

The fourth bull argument is optionality. Aksigorta Next is a live call option on a digital-native future that may or may not scale, but it costs relatively little to maintain and has genuine upside. The health segment has structural growth that is just beginning. Any future consolidation in the Turkish insurance sector—which is arguably overdue—would likely see Aksigorta as a consolidator rather than a consolidatee, giving it strategic optionality on M&A.

What are the one to three KPIs an investor should actually track to follow this story? In order of importance. First, the Combined Ratio, specifically broken out between motor and non-motor lines, because that is the cleanest measure of underwriting discipline in a volatile environment. Second, Return on Equity measured against trailing inflation, because that is the metric management is incentivized against and the one that ultimately determines whether equity compounds in real terms. Third, gross written premium growth in health and in the Aksigorta Next segment, because those are the structural growth lines that will determine the shape of the book a decade from now.

A brief second-layer diligence aside is worth flagging. Any investor serious about Turkish financials should watch the credit rating trajectory of the sovereign and of the major Turkish banks, because insurance companies' capital adequacy is intertwined with banking sector health through both shared distribution and cross-holdings. Watch for any signaling from BDDK (the banking regulator) or the insurance regulator about capital rules changes. Watch for earthquake reinsurance renewal pricing every January, because it is a real-time proxy for how the global market is pricing Turkish catastrophe risk. And keep an eye on Sabancı Holding's broader capital allocation stance, because a decision to rotate out of financial services would be a structural headwind that no operating metric can fully offset.

IX. The Grade

How to think about Aksigorta as a long-duration compounder? The honest answer is that it depends entirely on the currency in which the investor keeps score.

In Turkish lira terms, the story over the decade-plus since the Ageas partnership closed is one of a well-run compounder inside a brutally difficult macro environment, with equity growing at rates that have, across most periods, outpaced domestic inflation. Dividends have been paid consistently, reinvested at attractive nominal rates, and the company has repeatedly demonstrated the ability to defend margins in hostile conditions. On a purely local-currency basis, the record is what any long-term equity investor would want.

In dollar terms, the same record looks materially different, because the lira's trajectory against the dollar has been, to put it politely, unkind. Anyone who bought shares in 2011 at the peak of the Ageas deal excitement and held in dollar terms has lived through stretches where the currency drawdown more than offset the operating performance. In other stretches—particularly windows where lira stabilization aligned with operating strength—dollar returns have been respectable. The binary lesson is that investing in Turkish equities without a thesis on the currency is investing with one eye closed.

The more interesting question is not how the past has looked, but what the base rates suggest going forward. The company has a cornered distribution resource, a process edge in risk modeling, a disciplined management team with long tenure and aligned incentives, and a structurally under-penetrated market. It also has real regulatory, catastrophe, and currency risks that are outside management's control. The skill of the investor is not in predicting which of these forces will dominate in any given year. It is in sizing the position to the uncertainty and being willing to hold through cycles.

The meta-point that Aksigorta illustrates, and that the Acquired.fm framework is particularly good at surfacing, is that durable competitive advantage can exist in the most unlikely places. A commodity product, sold in a volatile currency, inside a politicized regulatory environment, can still generate above-cost-of-capital returns over long periods if the operator has genuine Power. The Akbank distribution moat is genuine Power. The Ageas-calibrated risk infrastructure is genuine Power. The seventeen-year CEO tenure with incentives indexed to inflation-plus is genuine Power.

Whether that combination translates into attractive forward returns depends on exogenous factors no one can perfectly forecast. But the underlying machine, examined on its own terms, is one of the more interesting case studies in emerging market financial services that does not get nearly the attention it deserves from global investors.

X. Outro

The synergy between Sabancı and Ageas, struck at the bottom of Europe's post-crisis insurance malaise, turned out to be one of the more successful cross-border joint ventures in the emerging markets insurance world. Neither partner has seriously reopened the ownership question in the years since, which, given how many JVs collapse within a decade, is itself a form of endorsement. The Belgian risk technology and the Turkish distribution engine have, across most cycles, proven genuinely complementary rather than redundant, and the governance architecture has been stable enough to survive both internal management transitions and external macro shocks.

There is a broader thought worth leaving with. Insurance companies, done right, are arguably the most information-dense window into a country's macro economy that any investor can own. Claims data tells you about accident frequency, which tells you about traffic, which tells you about economic activity. Health utilization data tells you about demographic shifts, income distribution, and hospital capacity. Property claims tell you about construction quality, climate exposure, and urbanization patterns. Float invested in the local sovereign tells you about term structure, inflation expectations, and political risk premia. Dividend capacity tells you about regulatory stance and solvency regimes. You can, in principle, understand a significant portion of an emerging economy just by reading the annual reports of its top three insurers with care.

Aksigorta is, among other things, a remarkably rich such window into modern Turkey. The company that started in 1960 as a family captive in Adana, that was professionalized through the Sabancı move to Istanbul, that was globalized through the 2011 Ageas transaction, and that has been operationally honed through more than fifteen years of steady leadership, now sits as one of the more sophisticated risk and asset management platforms in its region. What it does next, how it navigates the coming cycle of macro normalization, regulatory evolution, digital disruption, and demographic change, is a story that any patient observer of emerging market finance would do well to keep reading.

Because in a commodity business, in a moving-target currency, in a country that insists on being interesting, the companies that quietly accumulate Power over decades are often the ones that, in the fullness of time, turn out to have been the best stories all along.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube