Agesa: The Bancassurance Playbook and Turkey's Savings Revolution

I. Introduction: The "Hidden" Compounding Machine

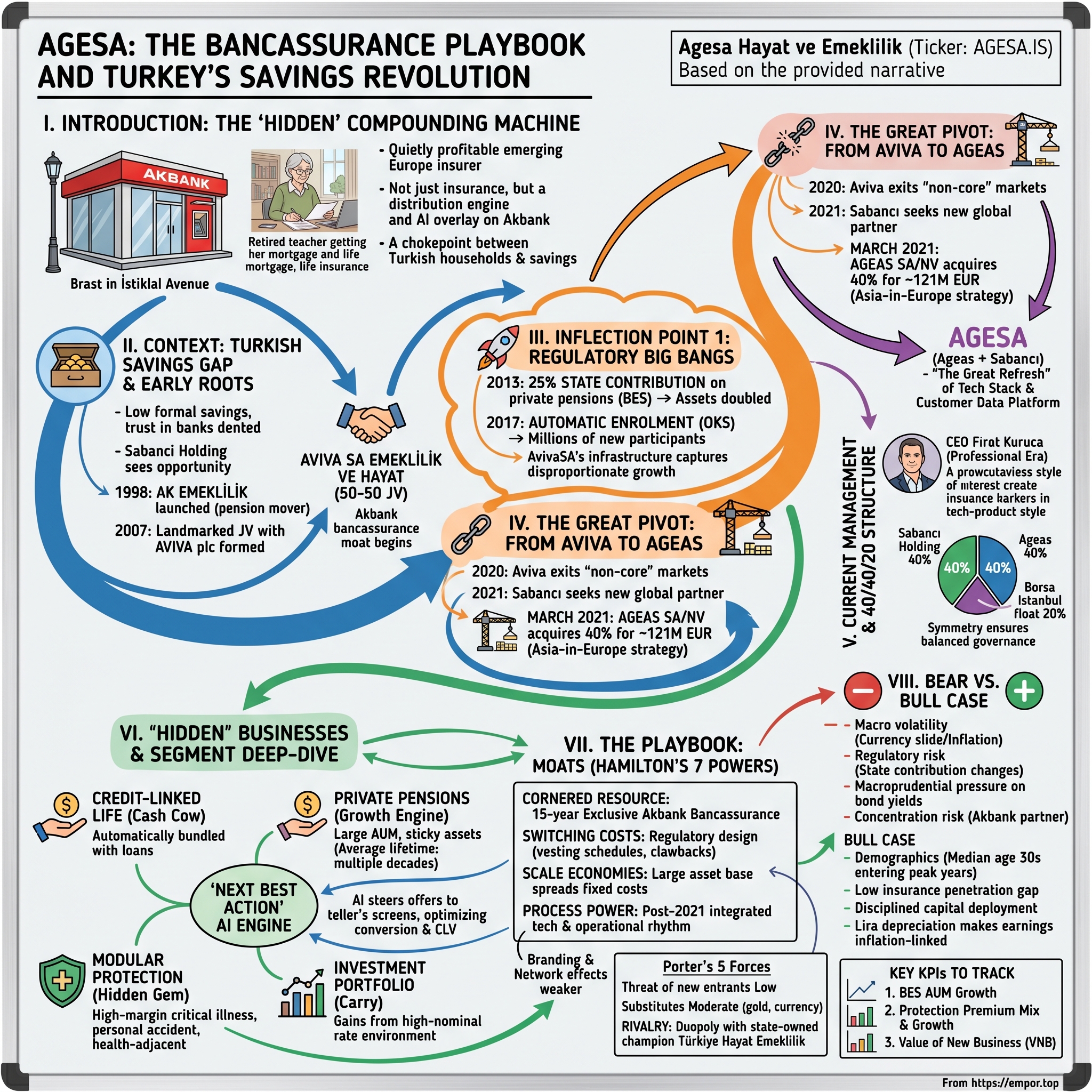

Picture an Akbank branch on İstiklal Avenue in Istanbul on a cold Tuesday morning in 2025. A retired schoolteacher walks in to renew her mortgage extension. The teller, a twenty-something with a headset and a tablet, taps a few screens. Before the customer has even finished her tea, the system has already scored her risk profile, identified a gap in her life-insurance coverage, flagged that her eldest daughter is eligible for a new private-pension contract under the state-contribution window, and surfaced a modular critical-illness rider priced to the nearest Turkish lira. The customer says yes to two of the three suggestions. She leaves thinking she has just renewed a loan. In reality, she has just become a premium-paying customer of one of the most quietly profitable insurance operations in all of emerging Europe.

That company is Agesa Hayat ve Emeklilik, traded on Borsa Istanbul under the ticker AGESA.IS. And this is the story of how a modest Sabancı–Aviva joint venture set up two decades ago became the operating system for the Turkish savings economy.

Here is the puzzle that makes Agesa so interesting. Turkey, as a macro environment, is the equivalent of trying to run a marathon on a trampoline. Inflation in the last four years has routinely printed above 40%, the lira has lost more than 80% of its dollar value since 2018, and interest rates have whiplashed from single digits to 50% and back down again. Under those conditions, a financial institution is supposed to be fighting for its life. And yet Agesa, through most of that period, compounded its technical profit at double-digit real rates, kept its return on equity consistently near the top of the European insurance league tables, and built a pension book that is now deep enough to matter to sovereign bond markets.

The thesis of this episode is that Agesa is not really best understood as an "insurance company." It is a distribution engine. It is a behavioural-nudge machine. It is an AI overlay sitting on top of the branch network of Turkey's largest private bank, which also happens to be controlled by the same family conglomerate that owns half the company. It is, in short, a carefully engineered choke point between Turkish households and their savings.

We will trace the arc from the Ak Emeklilik days, through the transformational marriage with Aviva, the 2007 bancassurance deal with Akbank that quietly built the moat, the 2013 and 2017 regulatory big bangs that turned pensions from a luxury into a utility, the dramatic Aviva-to-Ageas pivot in 2021, and the current era under CEO Fırat Kuruca, where the company is deploying machine-learning models to the teller's screen and modular health products to a rising urban middle class. Along the way, we will ask the Acquired questions. Does it have Hamilton Helmer's 7 Powers? Is it a Category King? And most importantly, what are the one or two KPIs that will tell a fundamental investor whether this compounding machine is still compounding.

Settle in. This one has layers.

II. Context: The Turkish Savings Gap & Early Roots

To understand why Agesa matters, start with a kitchen drawer in a middle-class Istanbul apartment. For most of the twentieth century, that drawer, or the space under the mattress, or a discreet safety deposit box, is where a Turkish family kept its retirement plan. Gold bracelets received at weddings. A handful of dollar bills tucked into a children's book. Maybe a plot of land in a grandmother's village. The savings rate, at least the formal one that flows through the financial system, was one of the lowest in the OECD. Trust in banks had been dented repeatedly through currency crises, and the concept of a long-duration, lira-denominated retirement product was, to put it politely, a hard sell.

Sabancı Holding, the industrial dynasty founded by Hacı Ömer Sabancı that grew into one of the two great Turkish family groups alongside Koç, understood this gap long before most. Through the 1990s Sabancı had built Akbank into a formidable consumer franchise, and by the end of that decade the group recognized that demographic arithmetic was about to turn against Turkey's pay-as-you-go social security system. If retirements were going to be funded, the private sector would have to step up. In 1998 they launched Ak Emeklilik, an early-mover pension company, and in parallel ran a life insurance arm called Aksigorta Hayat. These were scrappy, brand-forward but technically under-capitalized vehicles. Selling life insurance in a country where many customers did not fully trust the institution of insurance itself required more than domestic brand equity. It required global best practice, actuarial horsepower, and a product shelf designed for long-duration savings.

Which is where the British arrived. In 2007 Sabancı inked its landmark joint venture with Aviva plc, the FTSE-listed British insurance heavyweight, to merge the group's life and pension assets under a combined entity eventually known as AvivaSA Emeklilik ve Hayat. The logic was almost too clean. Sabancı brought the distribution, the local brand, and the crown jewel: an exclusive bancassurance agreement giving the joint venture access to Akbank's branch network. Aviva brought actuarial rigor, modern product design, IT systems built for decades-long liability matching, and a governance template that satisfied European regulators. The ownership was split roughly 50-50 between the two partners, with a minority public float added later through the 2014 IPO on Borsa Istanbul.

This two-pillar governance model, a Turkish conglomerate on one side, a Western insurance specialist on the other, was not an accident of history. It was a deliberate structure. A pure Turkish player would have struggled with actuarial discipline and reinsurance relationships. A pure foreign player would have struggled with regulatory access and branch-level trust. The hybrid worked because each parent brought something the other could not easily build.

What was being built, though neither founder fully articulated it at the time, was the infrastructure for what would soon become a mass-market savings product. Because just a few years later, the rules of the Turkish pension game were about to change dramatically.

III. Inflection Point 1: The 2013/2017 Regulatory Big Bang

If you want to see how a government can re-engineer the savings behaviour of an entire nation in a single policy document, look at what Ankara did in 2013. For years, the Turkish private pension system, known by the acronym BES, had been a slow-burn product. Sold mostly to upper-middle-class professionals who could shoulder the tax-advantaged contributions, it had reached a few million participants, modest in the context of an eighty-million-person country. The product worked, but it felt like something for people who already had accountants.

Then the Turkish Treasury did something remarkable. On January 1, 2013, it replaced the old income-tax-deduction model with a direct 25% state contribution on top of every lira a citizen put into a licensed pension fund. To earn the full match, a participant had to keep the money locked up for ten years and retire from within the system. Partial withdrawals earlier triggered partial clawbacks of the state portion. In effect, the government said: we will pay you a quarter of every lira you save, but only if you become a long-duration saver. The generosity was calibrated to nudge behaviour, and it worked. Industry-wide assets under management doubled within a few years, and AvivaSA, as it was then known, rode the wave, adding participants at a pace no competitor in the West Europe region was achieving.

Then came the second big bang. In January 2017, Turkey introduced automatic enrolment, known locally as Otomatik Katılım Sistemi or OKS. Every employer over a certain size was required to automatically enrol its eligible workers in a pension plan, with employees retaining an opt-out right in the first weeks. For the first time, the default setting of the Turkish labour market was "saving." Overnight, millions of new participants hit the system. Importantly, the state contribution was preserved, and an additional one-off bonus was layered in at the point of retirement for long-stayers.

Here is where the Sabancı-Aviva decision to build infrastructure a decade earlier really paid off. When OKS hit, many smaller Turkish pension companies scrambled. They needed to build employer onboarding portals, payroll-integration files, defaulted fund menus, and call-centre capacity to handle the inevitable tidal wave of opt-out requests. AvivaSA, by contrast, already had the scaffolding. The Aviva side of the JV had brought in pension administration systems originally built for UK workplace schemes, and the Sabancı side had the corporate relationships at the top end of the BIST-100 index and beyond. The company did not just participate in the gold rush. It captured a disproportionate share of it.

There is a subtle point here worth lingering on for any investor trying to understand the category. In most Western markets, a private pension is a voluntary affair that competes for share-of-wallet against mutual funds, ETFs, and real estate. In post-2017 Turkey, a private pension is closer to a public utility, because it is the default, it is state-sweetened, and it is regulated to the point of being almost a semi-public service. That shift fundamentally changed the economics of companies like AvivaSA. Growth was no longer driven by selling a luxury product to the willing. It was driven by being the plumbing for a mandated national savings system.

By the end of the 2010s, AvivaSA was no longer a mid-tier life insurer with a pension sideline. It was one of the pillars of the Turkish retirement system. Which made its sudden orphaning in 2021 all the more dramatic.

IV. The Great Pivot: From Aviva to Ageas

The call came in, by most accounts, during a rainy London afternoon. Aviva plc, under Amanda Blanc, the no-nonsense Welsh chief executive who had taken the reins in mid-2020 with a clear mandate to simplify, had been working through a list of "non-core" markets to sell. The official language was about focus on the UK, Ireland, and Canada. The unofficial language, as anyone reading between the lines of the Aviva investor days could tell, was that the British parent was shedding anything that did not contribute at scale to group capital or group growth. Singapore, Italy, France, Poland, and eventually Turkey all went onto the block.

For Sabancı, the news landed with a mix of opportunity and anxiety. Aviva had been a constructive partner, but it was now effectively a motivated seller. There were two plausible paths. Sabancı could buy out its partner and take full control, or it could find a new foreign insurer willing to step into Aviva's shoes. The group, true to its conglomerate philosophy, picked door number two. Insurance, in the Sabancı worldview, is a business best run in partnership with a global specialist who brings underwriting depth and international reinsurance clout. The search began.

The winner was Ageas SA/NV, the Brussels-listed insurance group that had risen from the ashes of the old Fortis conglomerate after the 2008 financial crisis. Ageas, under chief executive Hans De Cuyper, had spent a decade carefully rebuilding itself into a focused life and non-life insurer with a distinctive emerging-markets growth engine, particularly its iconic joint ventures in Asia with Fosun in China, IDBI Federal in India, and Muang Thai Life in Thailand. For Ageas, the Turkish opportunity fit the template almost perfectly. A bancassurance-driven business, controlled alongside a local industrial partner, operating in a demographically young market with under-penetrated insurance density. It was, in strategic language, Asia-in-Europe.

In March 2021 the deal was announced. Ageas agreed to acquire Aviva's 40% stake in the joint venture for a price reported at roughly 121 million euros, a number that drew more than a few raised eyebrows across the European insurance analyst community. On a headline price-to-book basis the multiple looked punchy, and the peer deal benchmark, most often cited as the privatization and subsequent evolution of the state-controlled Türkiye Hayat Emeklilik, suggested a cheaper per-unit-of-AUM comparable. But Ageas was not buying a static pool of capital. It was buying access to Turkey's only truly integrated bancassurance platform, with a fifteen-year exclusive distribution runway through Akbank and an AI-enabled cross-sell engine that most European incumbents were still only slide-deckingly aware of. For a buyer with a long time horizon and a growth mindset, the price was defensible. For anyone modelling off next year's lira-denominated earnings alone, it looked expensive.

The deal closed in 2021, and within months the company began the transition from AvivaSA to Agesa. It was far more than a re-branding exercise. The Turkish management team used the moment to execute a full refresh of the technology stack, replace legacy Aviva-era middleware with a cloud-native, microservices-oriented architecture, and standardize on a single customer data platform that could feed both the bank branch and the direct-to-consumer mobile app. The new name itself, a portmanteau of Ageas and Sabancı, was an almost literal advertisement of the governance model: two anchors, one boat.

There is an interesting counterfactual worth pausing on. Had Sabancı gone the buyout route instead, Agesa today would likely be a pure-play domestic insurer with less actuarial depth and weaker access to global reinsurance treaties. The Ageas marriage kept the two-pillar discipline intact, while swapping a retrenching partner for an expanding one. In hindsight, it may be remembered as the most important capital allocation decision the company made in its modern history.

Which raises the natural question: who exactly is running the ship now?

V. Current Management: The "Professional" Era

Fırat Kuruca took over as chief executive of Agesa in the spring of 2022, stepping into a role that blended the aesthetics of an old-line insurance executive with the operating style of a software-product manager. A Turkish national with a finance background and a career spent in senior roles across Sabancı's broader financial-services footprint, Kuruca is not a flashy public figure. He rarely appears on the cable-TV business circuits that some of his peers favour. He speaks carefully, writes spreadsheets himself when he wants to sanity-check an assumption, and, by multiple accounts from analyst conferences, runs his leadership meetings more like quarterly OKR reviews than like board updates.

The executive team under him reflects that cultural mix. The chief financial officer, the chief commercial officer, and the head of digital all sit effectively at the same seniority, a flatter structure than you find in most comparably sized European insurers. The head of actuarial, historically a role stuffed into a back office, reports directly to the CEO and is involved in product pricing from the whiteboard stage rather than at the sign-off moment. The tone is closer to a Turkish fintech than to a Victorian life office.

This managerial philosophy shows up in how the company frames itself externally. When Agesa talks to equity analysts, it does not lean heavily on gross written premium as a hero metric. Top-line premium, in the insurance world, can be inflated by cheap, low-margin business that consumes capital without building long-term value. Instead the company emphasizes Value of New Business, known as VNB, a metric that captures the present-value economics of policies written in a given period net of the capital they tie up. Management compensation, to the extent that it is disclosed, is tilted toward VNB growth and protection-product growth, meaning pure-risk products like term life and critical illness rather than savings products where the margin gets shared with the customer.

The shareholder structure is the other half of the story. After the Ageas transaction, the cap table settled into what is colloquially known inside the company as the 40/40/20: Hacı Ömer Sabancı Holding owns 40%, Ageas owns 40%, and 20% floats on Borsa Istanbul. That symmetry is not decorative. It is the operational embodiment of the two-pillar philosophy. Neither anchor shareholder can unilaterally dominate. Board appointments are negotiated. Capital allocation decisions, including dividends, are reached through a process of structured consensus. Minority shareholders, represented by the float, benefit from the tension between two sophisticated institutional owners who each have reasons to protect economic value.

But the most valuable item on Agesa's balance sheet does not appear on the balance sheet at all. It is the 15-year exclusive bancassurance agreement with Akbank, Turkey's largest private bank by various measures and itself a Sabancı-controlled entity. The agreement gives Agesa exclusive access to distribute life insurance and pension products through Akbank's branch network, call centre, and digital channels. For a banking customer walking into any one of Akbank's more than seven hundred branches, Agesa is the only insurance brand on offer for these categories. That is a cornered resource in the purest Hamilton Helmer sense, and we will return to it shortly.

Incentive alignment, in this setup, is the quiet superpower. Akbank earns commission on every policy it distributes, so it wants Agesa to price competitively and design products that customers actually want. Agesa wants Akbank's tellers to be well-trained and their digital journeys to be slick, so it invests in sales enablement. Both parents share the upside. This is not a marriage of convenience. It is a joint venture where the two sides literally need each other to eat dinner.

Which brings us to what is actually being sold inside those branches.

VI. "Hidden" Businesses & Segment Deep-Dive

Walk into any Turkish retail bank and ask for a mortgage. Somewhere in the stack of paperwork that accompanies the loan will be a document, usually barely glanced at by the customer, called a credit-linked life policy. It pays off the outstanding principal of the loan if the borrower dies or becomes permanently disabled. The premium is modest, often rolled into the loan itself. The underwriting is largely automated, relying on data the bank already has about the customer's age, income, and health declarations. And here is the critical bit: the margins are beautiful.

This is Agesa's cash cow. Credit-linked life insurance, sold as a near-automatic adjunct to Akbank's consumer lending engine, produces a stream of premium income that scales with whatever the bank is lending at any given moment. When Turkish consumer credit is booming, Agesa's credit-linked premium booms. When lending contracts, there is still a long tail of in-force policies paying renewal premiums. The loss ratio is stable, the acquisition cost is close to zero, and because the underlying distribution is a captive bank branch, the cost-to-serve is minimal. In Acquired parlance, it is the business equivalent of a royalty stream on Turkey's consumer credit cycle.

The growth engine, though, is elsewhere. It is the private pension business, BES, and its auto-enrolment cousin OKS. Here Agesa operates as an asset gatherer rather than a pure risk insurer. The company manages a pool of assets under management that places it consistently among the top private pension providers in Turkey. The fees are lower in percentage terms than risk products, but the base is vastly larger, and the stickiness is remarkable. A customer who has been in the system for five or seven years has deferred contribution credit from the state that they do not want to forfeit. A customer who has been in for ten years is, practically speaking, a lifetime customer. The average lifetime of an Agesa pension participant, according to what management has shared on investor calls, is measured in multiple decades.

Inside the BES book, there is a mix shift underway that matters more than it first appears. For years, the default fund allocations were heavily tilted toward short-duration government bonds, reflecting both conservative customer preferences and a regulatory nudge. Over the last several years, both customer behaviour and regulatory guidance have evolved toward higher allocations to equities, foreign-currency-denominated funds, and thematic products including gold and commodity-linked vehicles. Because fee rates on equity-heavy funds are higher than on money-market-style funds, every percentage point of mix shift toward equities is a direct margin upgrade for Agesa, at no additional capital cost. Management has been quietly encouraging this mix shift, and the impact on fund-management earnings has been a meaningful tailwind.

Then there is the hidden gem of the portfolio: modular personal accident, critical illness, and health-adjacent protection products. This is the fastest-growing and highest-margin part of the book. These are risk products, pure-protection in the insurance sense, with no savings component. They pay lump sums if a customer is diagnosed with a specified illness, suffers an accident, or requires hospitalization outside of the state health system. In a country where private healthcare is increasingly seen by the urban middle class as a must-have rather than a luxury, and where the social security system is under visible demographic pressure, these products are riding a secular tailwind. Management has, at various analyst meetings, described growth rates in this segment in the high double digits, with margin profiles that dwarf standard life. These are the products that the "Next Best Action" AI engine is most aggressively steering toward at the teller's screen.

That AI engine is itself a product of the post-2021 tech rebuild. Agesa's Next Best Action model ingests data from Akbank's core banking systems, Agesa's own policy systems, and third-party signals, and produces, in near-real time, a ranked list of offers customized to each customer walking into a branch or logging into the app. Think of it as a recommendation engine, not unlike what Netflix or Spotify uses, except the item being recommended is an insurance or pension product, and the success metric is a combination of conversion rate and long-term customer value. Management has repeatedly flagged that NBA has meaningfully lifted per-visit conversion, though the absolute uplift numbers are not always disclosed. For a tech-curious investor, this is the piece of the story that separates Agesa from its state-owned Turkish peers, who are still largely running scripted sales playbooks.

Underneath all of this sits the investment portfolio, an often under-appreciated source of value in any insurance company. Agesa runs a substantial asset book of policyholder reserves, and in a high-nominal-rate environment like Turkey, the carry on those assets is a material earnings engine in its own right. When short-term Turkish lira rates are 40% or 50%, even a defensively positioned money-market-style portfolio generates enormous nominal returns, part of which flows to policyholders and part of which sticks with shareholders. The skill is in matching asset duration to liability duration without taking excessive currency or credit risk, and this is precisely the kind of discipline Ageas brought to the party.

So we have a cash cow, a growth engine, a hidden gem, and a data product. Now the question is whether any of this is durable.

VII. The Playbook: Hamilton's 7 Powers & Porter's 5 Forces

Hamilton Helmer's 7 Powers framework is the cleanest lens for stress-testing whether a business has structural moats as opposed to merely temporary advantages. Run Agesa through it.

Start with the most obvious: cornered resource. The fifteen-year exclusive bancassurance agreement with Akbank is, by any reasonable definition, a cornered resource. Akbank operates the largest private-bank branch network in Turkey, serves tens of millions of customers across retail and SME segments, and has consistently ranked among the most digitally advanced banks in the country. No competing insurer can replicate this. A new entrant could theoretically try to sign up one of the other big private banks, but those are all either tied up with their own insurance affiliates or locked in long-duration exclusivities of their own. The physical and digital footprint that Akbank puts at Agesa's disposal is the single most defensible asset the company possesses.

Next, switching costs. The BES system is designed, by regulatory architecture, to punish customers who leave. The 25% state contribution vests on a ten-year schedule. A participant who has been in for four years and moves their balance out forfeits the entire state-contribution accrual. Even a partial transfer, moving the account from one provider to another, while technically allowed, involves paperwork, a reset of internal customer-relationship scoring, and occasionally short lockout windows. The practical effect is that attrition rates in Agesa's pension book are remarkably low compared to what a Western mutual-fund company would consider healthy. The customer, once in, tends to stay in, not because they love the brand but because the regulatory architecture effectively makes them stay.

Scale economies form a third power. Insurance is a fundamentally fixed-cost business. Actuarial systems, policy administration platforms, reinsurance relationships, and regulatory-compliance teams all cost roughly the same whether you are administering one million policies or five million. Agesa, sitting on one of the largest private-pension AUM pools in Turkey and one of the largest bancassurance-sourced life books, spreads those fixed costs over a base that its sub-scale competitors simply cannot match. This translates directly into a lower expense ratio, which in turn allows the company to either price more aggressively or bank the difference as margin. Management has historically chosen a mix of the two, depending on the competitive context.

A fourth power worth naming is process power, though it is the most contested. Agesa has built, through its post-2021 tech rebuild, an operating rhythm where pricing, distribution, and customer-data signals all flow in near-real time through the Next Best Action engine. Replicating that operating system is not just a matter of buying software. It requires years of behavioural learning, teller training, data-cleansing, and iteration. Is it a permanent moat? Probably not at the scale of the bancassurance exclusivity. But it is a durable operating advantage that competitors are multiple product cycles behind on.

Branding and network effects are weaker. The Agesa brand is respected but it is not a consumer love-mark. Insurance rarely is. Network effects, in the Facebook sense, do not really apply. Counter-positioning, Helmer's subtle power around business models that incumbents cannot copy without cannibalizing themselves, is not particularly relevant here either.

Now flip the lens to Porter's 5 Forces. Threat of new entrants is low. Turkish insurance licensing is capital-intensive, regulated by both the Insurance and Private Pension Regulation and Supervision Agency, known as SEDDK, and to some extent the Capital Markets Board, or SPK. Getting a pension license, negotiating a bancassurance deal with a relevant bank, and building the actuarial and technology infrastructure from scratch would be a multi-year, multi-hundred-million-dollar project with no guarantee of success. Substitutes are moderate. Mutual funds, real estate, gold, and foreign currency all compete for the Turkish household's savings wallet, but the tax-and-state-contribution architecture of BES makes it structurally more attractive than most of those alternatives for long-horizon retirement money.

Supplier power is worth pausing on. The key suppliers to Agesa are reinsurers, global entities like Munich Re and Swiss Re, who provide catastrophe and large-risk cover. These are sophisticated counterparties, but the relationship is long-standing and, through Ageas's global scale, Agesa likely benefits from group-level bargaining power. Customer bargaining power is weak at the individual level but strong at the corporate level, since employer-sponsored OKS mandates are negotiated at the HR-director level of large Turkish corporates and commissions can be pressured there.

The most interesting force is rivalry. The competitive landscape includes private players like Allianz Yaşam ve Emeklilik, the local subsidiary of German giant Allianz, and a handful of other bank-linked insurance companies including Garanti Emeklilik. But the 800-pound gorilla in the rivalry conversation is Türkiye Hayat Emeklilik, the state-controlled combined entity formed by merging several publicly-owned life and pension arms, distributed through the state banks Ziraat, Halkbank, and VakıfBank. Türkiye Hayat benefits from a similarly cornered distribution resource on the public-sector side of Turkish banking, and in some metrics, particularly total BES participant count, it has overtaken private players. The rivalry with this state-owned champion is the single most important competitive dynamic to watch. It is not a zero-sum game, because the Turkish savings pie is still expanding, but pricing discipline and market-share allocation between the private and state-affiliated camps will shape sector returns for years to come.

Put it all together and Agesa looks like a business with two strong Helmer powers, one decent third, and a competitive structure that is rivalrous but defensively fenced. That is a rare combination in emerging-markets financials.

VIII. Bear vs. Bull Case

The bear case starts, as every bear case on a Turkish asset does, with the macro. Turkey's currency has been on a near-continuous depreciation path against the dollar and euro for the better part of a decade. For a domestic insurer whose assets under management are denominated in Turkish lira, that currency slide is, in dollar terms, a constant headwind. A pension pool that grows 40% in lira terms in a year can still shrink in hard-currency terms if the lira halves. Foreign investors looking at Agesa through a dollar lens have to mentally translate every nominal growth metric through an exchange-rate filter, and the translation is rarely flattering.

Regulatory risk is the second pillar of the bear case. The Turkish state contribution to BES is legislative, meaning it can be changed by legislative act. Successive Turkish governments have, in fact, tweaked it: the original 25% was in some periods temporarily raised to 30% to stimulate participation, and there have been periodic discussions about means-testing or capping the match. Any materially adverse change to the state contribution would immediately reduce the attractiveness of the pension product and, at the margin, increase lapse rates and depress new business volumes. Similarly, changes to the tax treatment of life insurance premiums, to investment-portfolio allocation rules, or to commission caps on bancassurance agreements could all hit Agesa's economics. Turkey is not a jurisdiction where an insurance investor can confidently assume a stable regulatory regime over the full lifetime of a long-dated liability.

Macroprudential pressure is a third concern. In extreme scenarios, Turkish authorities have, in the past, nudged institutional investors to absorb government bonds at administered yields that do not fully compensate for inflation. If that pressure were to intensify, insurance companies, with their large domestic fixed-income books, would be obvious candidates for such arm-twisting. The result would be policyholder returns trailing inflation for extended periods, which, in turn, would erode consumer trust in the entire savings product.

A quieter but real concern is concentration risk. Agesa's economics are anchored to a single bancassurance partner, Akbank. Any disruption to Akbank's operations, any shift in its strategic priorities, or any unexpected friction in the bancassurance relationship would have outsized consequences. The 15-year exclusivity is a moat when the partner is healthy. It is a vulnerability if the partner stumbles.

Now the bull case. And it is, if anything, more compelling in its structural simplicity.

Start with demographics. Turkey has one of the youngest populations in the OECD, with a median age in the early thirties and a large cohort now entering peak earning years. Those earners will, over the next two decades, become savers, and the only viable vehicle for long-horizon formal retirement savings, once you strip out informal gold and real estate, is the private pension system. This is the demographic tail the bulls point to, and it is a powerful one. The Turkish state pension system, meanwhile, is under mounting fiscal strain, with dependency ratios deteriorating and periodic early-retirement windows creating gaps that private savings will increasingly be expected to fill. Private pensions, in this reading, are not an optional financial product. They are becoming the de facto middle path to a middle-class retirement.

Insurance penetration in Turkey, measured as premium to GDP, remains well below both Western European and even Central European peer levels. Life insurance penetration is particularly under-developed. That gap, for a dominant distribution franchise like Agesa, is pure white space. Every incremental point of penetration growth flows disproportionately through the bancassurance channel, because it is the easiest on-ramp for a first-time insurance customer.

Capital deployment has been disciplined. Agesa has historically run with a strong dividend payout, returning meaningful cash to its two anchor shareholders and the float, while simultaneously funding the technology rebuild and new-product build-out from internal cash generation. Management has been clear that reinvestment in digital and in modular protection products takes priority over any inorganic growth ambition, and this capital discipline has kept return-on-equity among the most compelling in the European insurance universe.

The currency story has a subtle twist that bulls emphasize. While lira depreciation hurts reported dollar metrics, Agesa's technical earnings are, in structure, inflation-linked. Pension management fees are struck as a percentage of AUM, and AUM rises with both participant growth and nominal investment returns. Credit-linked insurance premiums scale with nominal loan volumes, which themselves track inflation. Investment-portfolio carry, in a high-rate environment, compounds. The net effect is that Agesa is one of the cleaner domestic hedges against Turkish inflation available to a local investor, even if the same quality makes it look less attractive through a hard-currency prism.

Weigh all of this together and the bull case is essentially a bet that the Turkish middle-class savings pool will continue to formalize, that the bancassurance moat will hold, and that management will continue executing on product mix shift and digital enablement. The bear case is a bet that macro or regulatory volatility will overwhelm those operational gains.

For investors tracking this debate, the two or three KPIs that matter most are, first, the growth of private pension AUM and participant count for Agesa relative to the broader Turkish BES system, which reveals market-share dynamics against the state-affiliated champion; second, the mix and growth of protection-product premiums, including the modular personal-accident, critical-illness, and credit-linked lines, which drive margin quality; and third, Value of New Business and its implied margin, which captures whether the company is growing economically profitable business or merely accounting premium. Those three, tracked over time, will tell a long-term investor more about Agesa's trajectory than any single quarterly reported earnings number.

IX. Conclusion

There is a version of this story that could have gone very differently. In an alternate universe, Ak Emeklilik stays a standalone Sabancı pension arm, never marries Aviva, and, when the 2013 and 2017 regulatory big bangs hit, finds itself technologically and operationally unprepared for the scale shift. It muddles through, loses share to the state-affiliated consolidated vehicle, and ends up a mid-tier also-ran in an industry that, ironically, ends up much bigger than anyone thought.

That did not happen. What happened instead is that two sophisticated, very different institutions, a Turkish industrial dynasty and a British, then Belgian, insurance specialist, built the infrastructure a decade before the tailwind arrived, then pivoted their foreign partner when the first one lost conviction in the market, and quietly turned a joint venture into the operating system for Turkish savings. That narrative arc, from branch of a UK insurer to operating system for a nation's retirement, is the single best lens for understanding the company as it exists today.

Is Agesa a Category King in the Acquired sense? It depends on how narrowly the category is drawn. In bancassurance-distributed life and pension products in Turkey, it is, depending on the metric, the top or near-top private player, with a moat structure that is difficult to replicate. In the broader Turkish pension system, it faces a formidable state-affiliated rival that is often larger on participant count, which makes the category a duopoly with state asymmetries rather than a pure one-winner market.

What stands out across the history is the quality of the partnership choices. Sabancı's 2007 decision to bring in Aviva, the 2021 decision to replace Aviva with Ageas when the strategic fit shifted, and the ongoing decision to maintain the two-pillar governance structure, each one reveals a discipline around owning the distribution but renting the actuarial and global expertise. That pattern, picking the right partner at each inflection, is the quiet thread that ties the entire narrative together. Combined with a bancassurance platform that acts as a choke point for a fast-formalizing savings economy, it produces a business whose compounding characteristics are, as we said at the opening, hidden in plain sight behind a macro backdrop that most investors have trained themselves to avoid.

The Turkish savings revolution is not over. It is, arguably, still in its early innings. And the company sitting at the intersection of the country's largest industrial group, its largest private bank, and one of Europe's most disciplined insurance specialists is uncommonly well-placed to intermediate whatever comes next.

X. Outro & Reading List

For those who want to go deeper, the primary sources on the Turkish pension and insurance system are worth the time. The Capital Markets Board of Turkey, known as the SPK, publishes periodic sector reports that cover fund-level flows and regulatory changes. The Pension Monitoring Center, EGM, maintains participant-level statistics on BES and OKS that are the single best source for market-share analysis across providers. The Insurance and Private Pension Regulation and Supervision Agency, SEDDK, publishes supervisory updates relevant to solvency and conduct. Agesa's own annual reports and investor presentations, filed with Borsa Istanbul in both Turkish and English, walk through the technical-earnings bridge and the shift in product mix in considerable detail.

For the parent-company angle, Hacı Ömer Sabancı Holding's investor-relations archive provides a rich history of the group's financial-services pivot, from the early Akbank buildout through the Ak Emeklilik origins to the modern bancassurance era. Ageas's group reports, meanwhile, offer the useful comparative lens of how Turkey is positioned within their emerging-markets portfolio alongside the Asian joint ventures, which is the cleanest benchmark available for understanding how a global sponsor thinks about capital deployment into a market like this.

And for anyone tempted to treat Turkish financial assets as merely a macro trade, the Agesa story is a reminder that underneath every volatile currency chart there can sit a compounding operating machine, built patiently by partners who picked each other well and then executed for a decade and a half. The macro will do what it does. The operating system keeps running.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube