Asia Commercial Joint Stock Bank (ACB): The Prudent Retail King of Vietnam

I. Introduction & Episode Roadmap

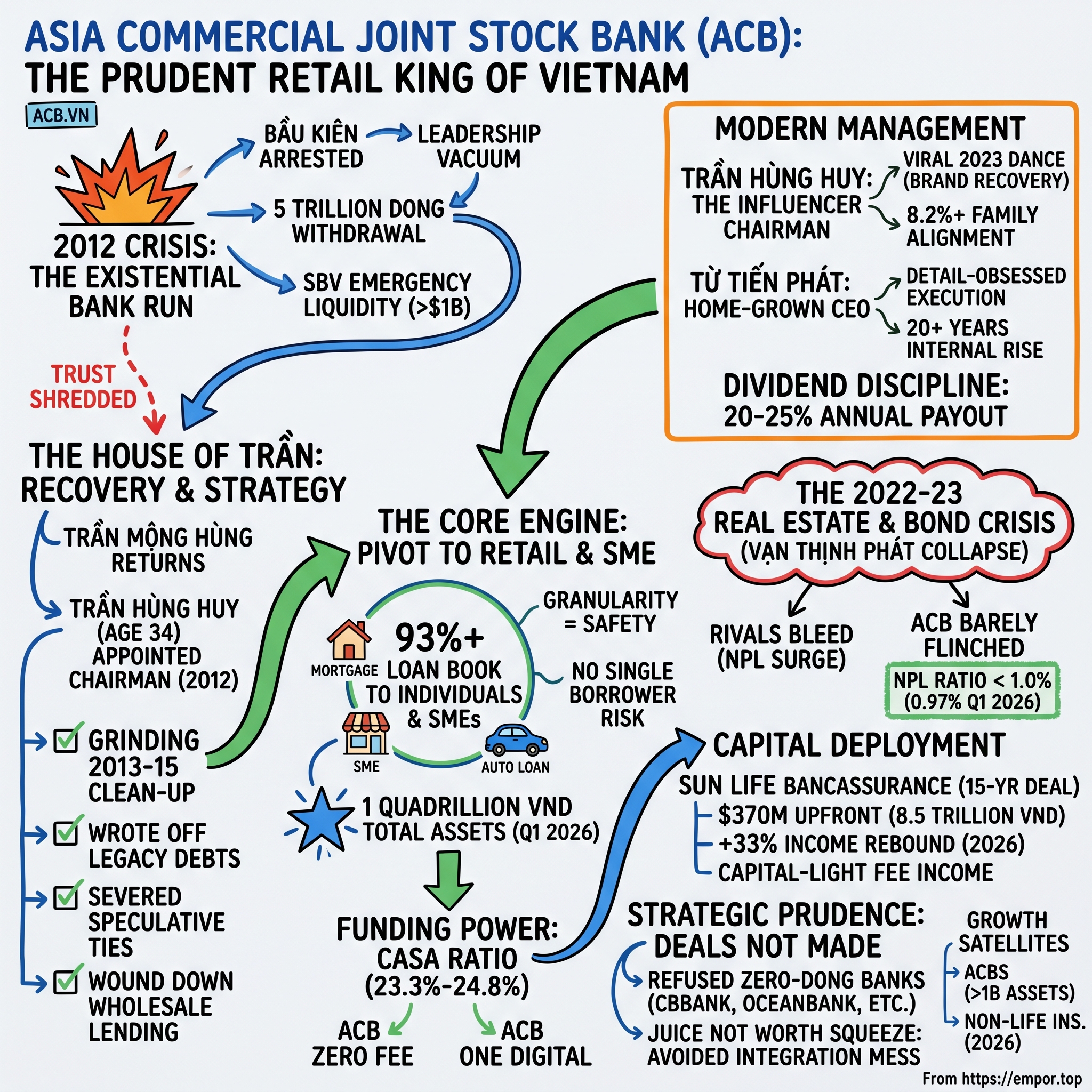

Picture a Saturday afternoon in late August 2012 in Ho Chi Minh City. The air is thick with the wet heat of the Vietnamese summer, motorbikes swarm the boulevards in their usual chaotic ballet, and outside the branches of one of the country's most respected private banks, something is happening that bankers everywhere dread above all else. There is a line. Not the ordinary line of customers paying utility bills or wiring money to relatives — this line is anxious, growing, and electric with rumor. Ordinary savers, the schoolteachers and shopkeepers and retirees who had entrusted their life savings to Asia Commercial Bank, are queuing to pull their money out. By the time the dust settled, over five trillion Vietnamese dong — more than two hundred million U.S. dollars — had walked out the door in a matter of days, and the central bank was forced to wheel in more than a billion dollars of emergency liquidity to keep the institution standing.[^1]

Here is the puzzle this episode wants to solve. How did a private bank in a frontier emerging market — a bank that suffered one of the most public, most televised, most existential bank runs in modern Asian financial history, that watched its co-founder dragged off in handcuffs, its CEO and chairman swept into a criminal dragnet — not merely survive, but go on to join the most exclusive club in Vietnamese finance? Because in the first quarter of 2026, Ngân hàng Á Châu ACB (Asia Commercial Bank, listed on the Ho Chi Minh Stock Exchange as ACB.VN) crossed one quadrillion Vietnamese dong in total assets — north of forty billion U.S. dollars — a milestone reached by only a handful of institutions in the entire country.[^3]

The answer is the central paradox of this story, and it is gloriously, almost stubbornly boring. In a banking sector that for two decades was a casino — a place where flamboyant tycoons used joint-stock banks as personal piggy banks to fund property speculation and stock punts, where cross-ownership webs tangled real estate empires into deposit franchises — ACB won by refusing to play. It won the long game by doing the unglamorous things: gathering humble retail deposits, financing the working capital of small family businesses, and guarding a balance sheet so clean it became a competitive weapon. While its rivals chased the high-yield fireworks of corporate bonds and developer loans, ACB built a fortress out of prudence.

Here is where we are going. We will open on the catastrophe of 2012 — the arrest of Bầu Kiên Nguyễn Đức Kiên, the leadership vacuum, the run, and the rescue. We will then watch a founding family reassert control and place a thirty-four-year-old son into the chairman's seat, a decision the market initially mocked. We will dissect the core engine — why retail and SME banking, granular and dull as it sounds, turned out to be the most durable business model in the country. We will examine the capital allocation choices that defined the modern era: a blockbuster bancassurance deal with Canada's Sun Life, and an even more revealing series of acquisitions the bank chose not to make. And we will close with the strategy frameworks, the bull and bear cases, and the handful of numbers that actually matter for anyone trying to understand where this institution goes next. Let's begin where the modern ACB story truly begins — at the edge of the abyss.

II. The 2012 Crisis: The Arrest of Bầu Kiên and the Existential Bank Run

To understand the earthquake, you first have to understand the fault line. Vietnamese banking in the 2000s and early 2010s was, to borrow a well-worn phrase, the Wild West. The country had thrown open its economy, foreign capital was pouring in, property prices in Hanoi and Saigon were doubling and tripling, and the stock market had its first euphoric boom-and-bust. Into this frothy environment stepped a generation of joint-stock commercial banks — privately controlled lenders that, in theory, channeled household savings into productive enterprise. In practice, far too many of them had become the financing arms of the tycoons who controlled them. Shell companies, opaque cross-ownership, related-party lending, and pyramids of speculative real estate and equity bets sat hidden inside balance sheets that looked, from the outside, perfectly respectable. Vietnamese have a wonderful, slightly mocking honorific for these larger-than-life moguls: bầu, literally "patron," the title given to the wealthy men who bankrolled the nation's beloved football clubs.

And no patron was more flamboyant than Bầu Kiên — Nguyễn Đức Kiên, the silver-haired, chain-smoking sports magnate whose distinctive shock of white hair made him instantly recognizable on television. He was a co-founder and major shareholder of ACB, a kingmaker in Vietnamese football, and a man whose web of investment companies stretched across the financial system.[^4] To the public he was untouchable, the very image of the connected insider who always lands on his feet.

So when news broke on August 20, 2012, that Bầu Kiên had been arrested, the country reeled.[^4] The charges, which would be expanded and refined over the following months, centered on illegal business operations, tax evasion, and the wonderfully Orwellian formulation of "deliberately acting against state regulations causing serious consequences." This was not a parking ticket. This was the state signaling that the era of the untouchable banking tycoon was ending, and it chose one of the most prominent men in the industry to make the point.

The problem with arresting a man at the center of a web is that the web shakes. Within days the legal dragnet widened. ACB's chief executive, Lý Xuân Hải Lý Xuân Hải, was detained, and the bank's former chairman, the eminent Trần Xuân Giá Trần Xuân Giá — a man who had once served as the country's Minister of Planning and Investment, a genuine architecture-of-the-reform-era figure — was also caught up in the proceedings.[^4] In the space of a week, a bank that prided itself on competent, professional management had lost its chief executive, its chairman, and one of its founding shareholders. The bridge of the ship was empty.

Depositors do not read footnotes. They do not parse the difference between a charge against an individual shareholder and a problem with the bank's actual loan book. What they saw on the evening news was the face of ACB's co-founder in police custody and headlines screaming crisis. And so they did the entirely rational thing that, done all at once, becomes catastrophic: they came for their money. The run was ferocious. More than five trillion dong — comfortably over two hundred million U.S. dollars — drained out of ACB's branches in days, an old-fashioned panic playing out in a modern economy.[^1][^4]

This is the moment the whole system could have unraveled. A bank run is a coordination failure: every depositor knows the bank is probably fine if everyone stays calm, but no individual can afford to be last in line if everyone else panics. Left unchecked, the fear at ACB could have leapt to every other private bank in the country, and Vietnam could have faced a 1907-style cascade. The Ngân hàng Nhà nước Việt Nam State Bank of Vietnam (SBV) understood this instantly, and it did what a lender of last resort exists to do. It opened the spigot, pumping more than a billion U.S. dollars of emergency liquidity into ACB to demonstrate, beyond any doubt, that every depositor would be paid.[^1] The signal worked. The line shortened. The money, much of it, came back.

But the damage to perception was done. ACB's shares cratered, international observers quietly wrote the bank off as another emerging-market casualty, and the very real question hanging in the humid Saigon air was whether the institution had any future at all. The deposits could be replaced; trust was another matter. And trust, for a bank, is not a soft virtue — it is the product. What ACB did over the next thirty-six months to rebuild it is the heart of this story, and it began with a phone call to a man who had stepped away from the bank he built.

III. The House of Trần: Recovery, Restructuring, and the Ascent of Trần Hùng Huy

When a house is on fire, you call the people who built it and know where the load-bearing walls are. For ACB, that person was Trần Mộng Hùng Trần Mộng Hùng, the soft-spoken co-founder who had been instrumental in launching the bank back in 1993 and who had, in the years before the crisis, drifted into the background. With depositor confidence in free fall, Trần Mộng Hùng returned to the board, and his presence sent a message that no press release could: the founding family was not running from the wreckage. It was running toward it, putting its own name and reputation on the line to vouch for the institution's survival.[^5]

Then came the decision that made the market gasp. In September 2012, in the immediate aftermath of the run, the board appointed a new chairman — and he was thirty-four years old. He was Trần Mộng Hùng's son, Trần Hùng Huy Trần Hùng Huy.[^5] The optics were, to put it mildly, debatable. The bank had just lost a chairman who had been a national-level technocrat and a CEO with deep operational chops, and its answer was to install the founder's young son. Critics had a field day. He was dismissed as a placeholder, a dynastic seat-warmer, a name chosen to reassure the family's allies rather than a leader capable of pulling an institution back from the brink.

What the critics underweighted was the substance behind the youth. Trần Hùng Huy was not a pampered heir parachuted in from a yacht. He had grown up inside the bank, had worked his way through its ranks, and crucially, he was Western-educated to a degree rare among Vietnamese executives of his generation. He held an MBA from Chapman University in California and a PhD in economics — credentials that gave him a vocabulary of modern risk management, capital discipline, and corporate governance that the old guard of relationship-driven Vietnamese banking often lacked.[^5] He was being thrown into a trial by fire, but he was not unarmed. He understood, in a way many of his contemporaries did not, that the path back to safety ran through the boring fundamentals of asset quality.

What followed between roughly 2013 and 2015 was a grinding, unglamorous, multi-year clean-up that would define the bank for a decade. Huy and his team did the equivalent of opening every closet in a haunted house and dragging the skeletons into the daylight. They wrote off enormous legacy debts tied to the crisis-era exposures. They severed the bank's entanglements with the speculative property tycoons who had treated banks as ATMs. They wound down the high-risk wholesale corporate lending that had looked so profitable on the way up and proved so toxic on the way down. This was painful — it meant accepting lower reported growth, swallowing provisions, and disappointing shareholders who wanted a quick rebound. But it was the only way to rebuild a balance sheet whose credibility had been shredded.

And here is where the recovery becomes a strategy rather than just a rescue. Huy and his team made a foundational choice about what ACB would be on the other side of the clean-up. They looked at the landscape and asked: where do we want to compete? Chasing large state-owned enterprise loans meant going head-to-head with the giant state-owned banks that had cheaper funding and political backing — a race to the bottom on price, layered with the political risk that any large, concentrated loan to a connected entity could become the next scandal. Lending to property developers meant high yields and, as ACB had just learned in the most expensive possible way, the kind of correlated, concentrated risk that can sink a bank overnight.

So they chose the other road. ACB would pivot, decisively and permanently, to retail and small-and-medium enterprise banking — millions of individual savers and borrowers, tens of thousands of small family businesses, each one too small to matter on its own and, in aggregate, almost impossible to lose money on if underwritten with discipline. It was a bet that granularity was safety, that a thousand small loans were less dangerous than one giant one, and that the unglamorous middle of the Vietnamese economy was the most defensible ground in the entire sector. That single strategic choice, born from the trauma of 2012, is the foundation on which everything that follows was built. The question was whether the young chairman who made it could also rebuild the bank's brand — and the answer, when it came, arrived in the form of a man dancing in the rain.

IV. Modern Management: The Influencer Chairman and the Executive Guard

Fast-forward to June 2023. ACB is throwing a gala to celebrate its thirtieth anniversary, and the chairman — now in his mid-forties, more than a decade removed from the crisis that defined his ascent — takes the stage. And then Trần Hùng Huy does something no Vietnamese bank chairman had ever done. He sings. He dances. He performs, energetically and without apparent embarrassment, eventually under a curtain of artificial rain, in a moment that was captured on phones and detonated across Vietnamese social media within hours.[^5] The clips went viral in the most thorough sense of the word — TikTok, Facebook, the comment sections of every news site in the country. The staid, gray, crisis-haunted bank suddenly had the most talked-about executive in Vietnam.

It is tempting to file this under "billionaire's vanity project," and a lesser story would. But look closer and the rain-dance was something more interesting: a deliberate, and stunningly cost-effective, act of brand engineering. Remember what ACB had been carrying since 2012 — a reputation for crisis, for scandal, for the bank run on the evening news. For a generation of young Vietnamese consumers entering the workforce and opening their first accounts, the most visible thing about ACB had been its near-death experience. Huy's performance overwrote that narrative in a single evening. Overnight the bank became modern, human, confident, even fun — the kind of institution a digitally native twenty-five-year-old in Da Nang would actually choose. In an industry where the most expensive thing to acquire is a new low-cost retail customer, the chairman had just generated more organic customer acquisition than a year of advertising could buy, and he had done it essentially for free.

This matters more than it might seem, because in banking, brand is not decoration — it feeds directly into the cost of funding. We will return to that mechanism shortly. For now, hold the image of the dancing chairman alongside the more important fact of his alignment with shareholders. Huy is not a hired gun playing with other people's money. He personally holds a direct stake of around 3.43% of ACB — over 153 million shares — and when you add his family and the closely related investment vehicles in the Trần orbit, including entities known as Giang Sen and Bách Thanh, the family's controlled bloc exceeds 8.2% of the bank's charter capital.[^5] On a bank worth billions of dollars, that is an enormous concentration of personal net worth riding on the institution's long-term health. When the chairman's family fortune rises and falls with the share price, the temptation to chase short-term growth at the expense of asset quality largely evaporates. His incentives and a conservative depositor's incentives point in exactly the same direction: don't blow up.

If Huy is the face and the strategist, the day-to-day machine is run by a different kind of executive entirely. In 2022, ACB appointed Từ Tiến Phát Từ Tiến Phát as chief executive officer, and his résumé tells you almost everything about the bank's internal culture.[^5] Phát did not arrive from a flashy rival or a consulting firm. He joined ACB in 2003 as an entry-level officer and spent nearly two decades climbing the ladder, learning the business from the branch floor up. His promotion to the corner office was the bank promoting its own — a signal to thousands of employees that ACB grows its leaders rather than importing them, and a reflection of the operational, detail-obsessed discipline that a retail-and-SME bank lives or dies by. The pairing is deliberate: a charismatic, outward-facing chairman who owns the strategy and the brand, and a grind-it-out, home-grown CEO who owns execution.

There is one more piece of the management philosophy worth dwelling on, because it reveals how the leadership thinks about capital. Many fast-growing emerging-market banks hoard every dong of earnings to fuel balance-sheet expansion — growth at all costs. ACB does the opposite. It runs a consistent, predictable dividend payout in the range of 20% to 25% of earnings annually, split between cash and stock.1 That is an unusual discipline, and it is a feature, not a bug. By committing to return a meaningful slice of profit to shareholders every year, management forces itself to compete for capital rather than simply spend it. It cannot grow recklessly because it has pre-committed to giving cash back. And because so many employees are themselves shareholders, the entire organization is nudged to obsess over return on equity — profit per dollar of capital — rather than the vanity metric of raw asset growth. It is a quiet but powerful alignment mechanism, and it sets up the central question of the next section: what does this disciplined machine actually do, and how does it stack up against the giants it competes with?

V. The Core Engine: Retail, SMEs, and Industry Structure

To appreciate what ACB built, you have to understand the arena it plays in, because Vietnamese banking is not a free-for-all — it is a tiered, regulated, and ferociously competitive ecosystem. At the top sit the so-called "Big 4," the dominant state-owned commercial banks that carry the prestige and implicit guarantee of the government, enjoy the cheapest deposits in the country, and handle the bulk of state-related business. Below and around them is the arena where the real entrepreneurial action happens: the private joint-stock commercial banks, a scrappy and increasingly sophisticated tier where ACB makes its home, fighting alongside a handful of formidable rivals for the wallets of Vietnam's rising consumer class.

Let's meet the competition, because ACB's strategy only makes sense in contrast to theirs. The undisputed profit king is Ngân hàng Ngoại thương Vietcombank VCB, a partially privatized state giant whose pre-tax profit reached roughly 42.2 trillion dong in 2024 atop an asset base of around 2.1 quadrillion dong.[^3] Vietcombank's superpower is its cost of funds — backed by state prestige, it gathers deposits more cheaply than anyone, which lets it lend profitably at rates others cannot match. Then there is Ngân hàng Quân đội Military Bank MBB, an absolute juggernaut of digital banking with roughly 28.8 trillion dong of pre-tax profit and assets around 1.13 quadrillion dong, whose origins in the military have given it a vast, sticky base of relationships and one of the most-used banking apps in the country.[^3]

The two rivals ACB resembles most — and competes with most directly — are Ngân hàng Kỹ thương Techcombank TCB and Ngân hàng Thịnh vượng VPBank VPB. Techcombank, with pre-tax profit near 27.5 trillion dong and assets around 979 trillion dong, became the aggressive private champion of wealth management and affluent real estate lending, and it built a sector-leading current-and-savings-account ratio north of 40.9% — a number we'll explain in a moment, but for now understand it as a measure of cheap, sticky deposits.[^3] VPBank, with roughly 24.0 trillion dong of pre-tax profit and assets around 900 trillion dong, took the high-yield, high-risk road into consumer finance and SME lending, eventually bringing in Japan's 三井住友銀行 Sumitomo Mitsui Banking Corporation (SMBC) as a major strategic shareholder.[^3]

And then there is ACB. In the first quarter of 2026, it crossed the historic one-quadrillion-dong threshold in total assets, joining the forty-billion-dollar club.[^3] It is smaller than Vietcombank or Military Bank, and on raw asset size it is in the chasing pack rather than the lead. But size was never the point. In 2024 ACB generated a pre-tax profit of around 22.3 trillion dong, with management guiding toward roughly 23 trillion dong in the 2025–2026 period — and it produced that profit with a stability and consistency that the higher-flying competitors could not match, because nearly all of it came from the granular retail and SME engine rather than from cyclical corporate bets.[^3]

Now to the mechanics, because this is where the strategy becomes tangible. Over 93% of ACB's loan book is allocated to individuals and small-to-medium businesses.1 Think about what that means. The bank's credit risk is sliced into an enormous number of tiny pieces — a mortgage here, a working-capital line for a noodle distributor there, an auto loan, a loan against a small factory's inventory. If any single customer defaults, the impact on the bank is a rounding error. This is the granularity-is-safety thesis made concrete: there is no single borrower whose failure can dent the institution. Contrast that with a bank that has lent a trillion dong to one property developer — when that developer stumbles, the whole bank shakes.

The second piece of the engine is funding cost, and here we arrive at the concept that quietly governs bank profitability: the CASA ratio. CASA stands for current and savings accounts — the money sitting in checking accounts and low-interest savings accounts, money that customers keep at the bank for convenience rather than yield. The beauty of CASA, from the bank's perspective, is that it is nearly free. A customer's checking balance earns them almost no interest, which means the bank funds its lending with money that costs it almost nothing. The higher a bank's CASA ratio, the cheaper its overall funding, and the wider its margins. ACB, through campaigns like "ACB Zero Fee" — eliminating transaction fees to make the bank stickier for everyday use — and the expansion of its "ACB ONE" digital app, has pushed its CASA ratio into a healthy band of roughly 23.3% to 24.8%.1 That is below Techcombank's flashy 40%-plus, but it is a steady, durable foundation that keeps ACB's blended cost of funds competitive without resorting to the rate wars that erode profitability.

But the real proof of ACB's model came during a crisis that hit someone else. In 2022 and 2023, Vietnam's real estate and corporate bond markets convulsed. The trigger was the arrest of property mogul Trương Mỹ Lan Trương Mỹ Lan and the collapse of her sprawling Vạn Thịnh Phát Vạn Thịnh Phát empire — a fraud of staggering scale that froze the corporate bond market and sent property developers scrambling for liquidity. Banks with heavy exposure to corporate bonds and developer loans — Techcombank and VPBank prominent among them — watched their non-performing loans surge and were forced into costly restructurings.[^3] ACB barely flinched. Because it had spent a decade after 2012 keeping virtually zero exposure to corporate bonds and high-risk developers, its non-performing loan ratio stayed consistently below 1.0% — it stood at 0.97% in the first quarter of 2026, the lowest among all private joint-stock banks in the country.1

Sit with that for a second, because it is the entire thesis in a single number. While rivals were bleeding through their loan books, ACB's NPL ratio stayed under one percent. The trauma of 2012 had inoculated it against the trauma of 2022. The discipline that looked overly cautious during the property boom — when ACB was leaving fat developer-loan yields on the table — turned out to be exactly the discipline that let it sail through the bust with a clean balance sheet, free to pick up high-quality customers as wounded competitors retreated. That, in the end, is what investors are really buying: a bank that gets paid for being boring precisely when boring is most valuable. The next question is what ACB does with the capital that discipline generates — and that takes us into the world of mega-deals and the acquisitions it deliberately walked away from.

VI. Capital Deployment and M&A: The Bancassurance Mega-Deal and Strategic Prudence

In late 2020, while the world was consumed by the pandemic, ACB closed a deal that would reshape its non-interest income for the next fifteen years. It signed an exclusive, fifteen-year bancassurance partnership with Sun Life Vietnam, the local arm of the Canadian insurance giant.[^6] Bancassurance, for the uninitiated, is a beautifully simple arrangement: the insurer pays the bank for the exclusive right to sell life insurance products through the bank's branches and to the bank's customers. The bank gets a large upfront payment plus ongoing commissions; the insurer gets distribution access to a captive, trusting customer base it could never build on its own. For a retail bank with millions of high-trust relationships, it is close to free money — fee income that requires almost no additional capital.

The numbers on the Sun Life deal were eye-catching. The arrangement involved an upfront payment of approximately 370 million U.S. dollars — around 8.5 trillion dong — landing in ACB's accounts.[^6] The natural question any investor asks is: did Sun Life overpay, and by extension, did ACB extract a great price? The way to answer that is to benchmark against the comparable deals signing across Vietnam in the same era. On one end, Sun Life had earlier paid roughly 75 million dollars for its tie-up with the smaller TPBank — a fraction of the ACB figure. But the relevant comparisons are the landmark deals among the larger banks: Vietcombank's marquee partnership with FWD came in around 400 million dollars, and VietinBank struck a major deal with Manulife in the same ballpark. Against those, ACB's 370 million dollars was not a fleecing — it was a fair-market valuation that reflected the genuine quality and affluence of ACB's customer base.[^6] Sun Life was paying for access to exactly the kind of high-income, high-trust retail savers that the rest of the industry coveted.

The deal's value did not stop at the upfront check. The bancassurance segment matured into a meaningful, recurring profit contributor, generating over one trillion dong in annual pre-tax profit, and after the industry-wide bancassurance slump of the mid-2020s — when regulators cracked down on mis-selling and forced stricter disclosure — ACB's insurance income rebounded sharply, climbing roughly 33% year-over-year in 2026 as the sector stabilized under cleaner rules.[^9] It is a textbook example of capital-light income: lend your trust, collect a fee, repeat.

But the most revealing capital allocation decision ACB made in this era was not a deal it did. It was a series of deals it refused. Between 2024 and 2025, the State Bank of Vietnam finalized one of the more consequential housekeeping exercises in the country's financial history: the mandatory transfer of four chronically troubled "zero-dong" banks — institutions so insolvent the state had previously taken them over for a nominal price of zero dong — into the arms of stronger commercial banks.2 CBBank was handed to Vietcombank. OceanBank went to Military Bank. GPBank went to VPBank. And DongA Bank went to HDBank.2

These transfers were not pure charity on the part of the acquirers. The State Bank dangled real incentives — chief among them higher credit growth limits, which in Vietnam's quota-controlled system (more on that shortly) is the single most valuable thing a bank can be granted. Taking on a zombie bank was, in effect, a way to buy permission to grow faster. Several of ACB's most ambitious peers took the deal. ACB looked at the same offer and said no.2

This is worth pausing on, because it is the clearest possible expression of the bank's character. Management weighed the regulatory perks — the precious extra credit room — against the realities of absorbing a "weak" bank: the operational nightmare of integrating broken systems, the cultural friction of merging demoralized staff, the hidden landmines lurking in a distressed loan book, and the potential dilution of a balance sheet ACB had spent over a decade scrubbing clean. And it decided the juice was not worth the squeeze. It chose to forgo the faster-growth incentive and stick to pure organic growth on its own pristine foundation. After everything the bank had been through to clean itself up, deliberately importing someone else's mess — even for a regulatory reward — was a line management would not cross. Saying no to growth is one of the hardest things for any institution to do, and ACB did it on purpose.

That is not to say ACB has stood still. It has been building out a cluster of growth satellites around the core bank, though it is important to size them honestly. ACB Securities, known as ACBS, was capitalized aggressively by the parent and rode the boom in Vietnamese retail stock trading to cross one billion dollars in assets — a serious brokerage business in its own right.[^3] And in early 2026, ACB launched a new non-life insurance subsidiary with 20 million dollars in charter capital, structured cleverly under its existing entities — roughly 91% held through ACBA and 9% through ACBS — in a way designed to optimize the group's capital adequacy ratio.[^10] These are real businesses with genuine future optionality. But the honest investment reality is that they remain secondary satellites. The core engine of taking deposits and making loans still drives well over 90% of the group's revenue and value, and any investor who gets excited about the satellites at the expense of the core is looking through the wrong end of the telescope. With the business model and capital philosophy on the table, it is time to formalize why this all works — which is where the strategy frameworks come in.

VII. Strategic Analysis: Hamilton's 7 Powers & Porter's 5 Forces

If you want to understand why ACB's prudence is not just a personality trait but a durable competitive advantage, two analytical lenses help enormously. Let's start with Hamilton Helmer's 7 Powers, the framework that asks what actually protects a business from competition over the long run.

The primary power at work here is counter-positioning, and ACB is close to a textbook case. Counter-positioning occurs when a company adopts a business model that incumbents — or in this case, rivals — cannot copy without damaging their existing business. After 2012, ACB positioned itself as the safe-haven, pure-play retail-and-SME bank. Its competitors, hungry for the fat margins of the boom years, piled into high-yield property developer debt and corporate bonds. They were not being stupid; for years, that was where the money was, and their entire growth narratives, investor expectations, and internal incentive structures became wired around it. ACB could not have lured them away from that strategy, and they could not easily abandon it without admitting their growth was built on sand. Then the property bubble burst in 2022, the corporate bond market froze, and the asymmetry revealed itself: the rivals were trapped in costly restructurings while ACB, with its clean balance sheet, could calmly absorb high-quality credit market share that the wounded were shedding. The boring strategy was not just safer — it was structurally un-copyable at the moment it mattered most.

The second power is switching costs, and it lives most powerfully in the SME franchise. A small business that runs its cash management, its payroll, and its trade finance through ACB's systems is not going to switch banks on a whim over a quarter-point of interest. Its entire operational plumbing is wired into the bank — its suppliers are paid through ACB, its employees are paid through ACB, its local trade relationships are intermediated by ACB. Ripping that out and re-plumbing it through a competitor is costly, risky, and disruptive, which means these relationships are deeply sticky and tend to compound in profitability over time as the business grows.

The third power is process power, the kind of advantage that comes from doing something repeatedly until you are simply better at it than anyone else. Over decades, ACB has accumulated proprietary underwriting data on exactly the customers most banks find hardest to assess: small retail merchants and Vietnamese SMEs that often lack pristine financial statements. That data, fed into increasingly automated credit-scoring systems, lets ACB approve loans faster and with lower default rates than a newcomer could hope to match. You cannot buy this; you can only build it, one loan and one repayment cycle at a time.

The fourth power is branding, and ACB's brand is unusually dual-sided. To depositors — especially older, conservative savers scarred by the memory of 2012 — the brand says "extreme prudence and safety," the reassuring solidity of a bank that survived the worst and emerged cleaner. To the younger, digitally native generation, the brand says "modern, accessible, even fun," the image conjured by a chairman who dances in the rain and an app that does not charge fees. Holding both of those identities at once — fortress and fresh face — is a rare and valuable thing.

Now flip to Porter's 5 Forces, which examines the structure of the industry ACB competes in. The threat of new entrants is very low, because the State Bank of Vietnam strictly rations banking licenses; you cannot simply decide to start a bank, which protects every incumbent from a flood of new competition. The bargaining power of buyers is high, however — retail depositors and borrowers have many banks to choose from, and they shop on rates, which relentlessly pressures net interest margins and forces banks into customer-retention gambits like ACB's zero-fee campaign. The bargaining power of suppliers is very high, and here the supplier is the regulator itself: the State Bank sets each bank's annual credit quota — the famous room tín dụng, literally "credit room" — which caps how much any bank is allowed to lend in a given year. This makes the central bank the ultimate gatekeeper of growth, and it is the single most important structural feature of Vietnamese banking. The one bright spot is that ACB's pristine asset quality and rock-bottom NPL ratio historically earn it favorable credit quotas, since regulators prefer to let healthy banks grow. Finally, the intensity of competitive rivalry is extremely high, with ACB, Techcombank, VPBank, and Military Bank locked in a permanent battle for the fast-growing retail and wealth segments. With the competitive architecture mapped, let's distill the transferable lessons.

VIII. Playbook: Key Business & Investing Lessons

Strip away the specifics of Vietnamese banking and three lessons emerge from the ACB story that travel well beyond Ho Chi Minh City.

Lesson one: the strategic value of saying no. In a fast-growing emerging market, the gravitational pull toward high-yield, fashionable assets is almost irresistible. When property prices are doubling and developers are begging to borrow at juicy rates, the banker who declines looks like a fool quarter after quarter — leaving money on the table, watching rivals post bigger numbers, fielding uncomfortable questions from shareholders about why growth lags. ACB's long-run outperformance is a masterclass in the compounding power of underwriting discipline, in the willingness to look stupid during the boom in order to be solvent during the bust. Its refusal to absorb a zero-dong bank for a regulatory bonus was the same instinct in a different costume. The hardest skill in finance is not finding things to buy; it is having the discipline to pass, repeatedly, on things that everyone else is buying.

Lesson two: governance and brand recovery are deeply linked, and brand equity is more resilient than it looks — if it is backed by genuine utility. The 2012 bank run could have been a death sentence. It was not, and the reason is instructive. ACB's core depositors, once the initial panic subsided, fundamentally valued the safety and service the bank provided; the franchise had real underlying utility that the scandal had obscured but not destroyed. What converted that latent loyalty back into trust was the visible, family-led restructuring — a founding family returning to put its name on the line, a transparent multi-year clean-up, a credible new generation of leadership. Brand equity, in other words, is not a marketing veneer; it is the residue of accumulated trust, and trust backed by genuine utility can survive even a catastrophe if the institution responds with transparency rather than spin.

Lesson three: charismatic leadership can be a cost-of-capital advantage, not just a PR flourish. This is the lesson that ties the dancing chairman back to the balance sheet. In banking, your brand directly determines your cost of funds, because cheaper, stickier deposits flow to the banks people trust and want to be associated with. When Trần Hùng Huy's viral, modern image pulled a wave of young customers into low-cost current and savings accounts, he was not merely winning eyeballs — he was structurally lowering the bank's cost of capital, one sticky CASA balance at a time. In most industries, a charismatic CEO is a nice-to-have. In banking, where the raw material is money itself and the price you pay for it sets your whole profit equation, charisma that converts into cheap deposits is a genuine, quantifiable competitive edge. Having drawn the lessons, the honest next step is to weigh what could go right against what could go wrong.

IX. Bull vs. Bear Case & Key KPIs to Watch

Every great business is a live argument between optimists and pessimists, and ACB is no exception. Let's steelman both sides.

The bull case rests on the rising tide of the Vietnamese consumer. Vietnam's middle class is expanding rapidly, and as households grow wealthier they take on mortgages, finance cars, and start and expand small businesses — exactly the secular demand that ACB's retail-and-SME engine is purpose-built to capture. Layer on top of that the bank's lowest-in-class risk profile, which acts as a structural shock absorber: when the next property or credit cycle turns down, as it inevitably will, ACB's clean balance sheet should once again let it gain share while rivers nurse their wounds. And there is genuine optionality in non-interest income — the maturing Sun Life bancassurance stream and the newly launched non-life insurance arm offer ways to earn more fee income off the same trusted customer relationships without consuming much additional capital. A growing market, the safest risk profile in the private tier, and an emerging fee engine: that is a coherent and durable bull thesis.

The bear case is equally coherent, and it starts with the very regulator that protects ACB from competitors. Because the State Bank caps credit growth through its annual quota, ACB's top-line expansion is structurally limited — and in an economic boom, the disciplined bank that refuses to take extra risk may simply be allowed to grow less than aggressive peers who game the system or accept distressed banks in exchange for higher quotas. Prudence, in other words, can be a ceiling as well as a floor. Second, net interest margins face relentless pressure: as the giant state-owned banks digitize and undercut on lending rates, and as buyers shop ever more aggressively, the spread ACB earns on its core business could compress. Third, the long-term disruptive threat from fintech and digital wallets could erode the transactional fee pool and chip away at the very CASA franchise that gives ACB its funding edge. None of these is fatal, but together they describe a business that may struggle to grow explosively even as it remains exceptionally safe.

So what should an investor actually watch? Resist the temptation to track everything. Three KPIs capture the essence of this institution.

First, the NPL ratio — the share of loans that have gone bad. This is the single most important number for ACB, because its entire premium over peers rests on asset quality. As long as this stays low — comfortably below 1.5% — the thesis is intact; if it begins creeping up toward the levels seen at riskier competitors, the bank would be losing the very edge that defines it.

Second, the CASA ratio — that proportion of cheap, sticky current-and-savings deposits. Watch whether ACB can push it from its current low-to-mid-twenties toward its medium-term ambition of 30% and beyond. Every point of CASA gained lowers funding costs and widens margins; it is the most direct readout of whether the brand-building and digital push are translating into real economic advantage.

Third, the annual credit growth quota granted by the State Bank of Vietnam — the room tín dụng. Because this regulatory allowance sets the absolute ceiling on how fast ACB can grow its loan book, it is the master variable for the bank's top-line trajectory in any given year. A generous quota signals regulatory confidence and unlocks growth; a stingy one caps it regardless of how much demand exists. Track these three, and you will understand ACB's story as it unfolds far better than any single headline profit figure could tell you.

X. Epilogue & Outro

The arc of this story is almost cinematic in its symmetry. In August 2012, ACB stood at the edge of the abyss — its co-founder in handcuffs, its leadership decapitated, its depositors fleeing, and the central bank pumping in over a billion dollars to keep it breathing. Fourteen years later, in the first quarter of 2026, the same bank crossed into the one-quadrillion-dong asset club, an elite tier of Vietnamese finance, having executed that whole journey under a single, unbroken thread of leadership: a father who returned to steady the ship and the son he handed it to, the once-derided thirty-four-year-old who grew into one of the most distinctive bank chairmen in Asia.

What ACB ultimately demonstrates is that in a volatile emerging market — a place tempted at every turn by speculative shortcuts and connected-lending fortunes — the unglamorous virtues compound. Corporate governance that aligns the family's fortune with the depositor's safety. Radical transparency in the face of crisis. And above all, a discipline about risk so consistent that it transformed a near-death experience into a permanent competitive moat. The bank that learned the hard way in 2012 that concentration kills built itself into a fortress of granularity, and when the next storm came in 2022 and swept through its less careful rivals, it barely got wet. That is the case study: not a tale of brilliant bets, but of disciplined refusals — the rarest and, it turns out, the most durable edge in finance.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube