Leapmotor: The Security Camera Giant's Electric Vehicle Moonshot

I. Introduction & Episode Roadmap

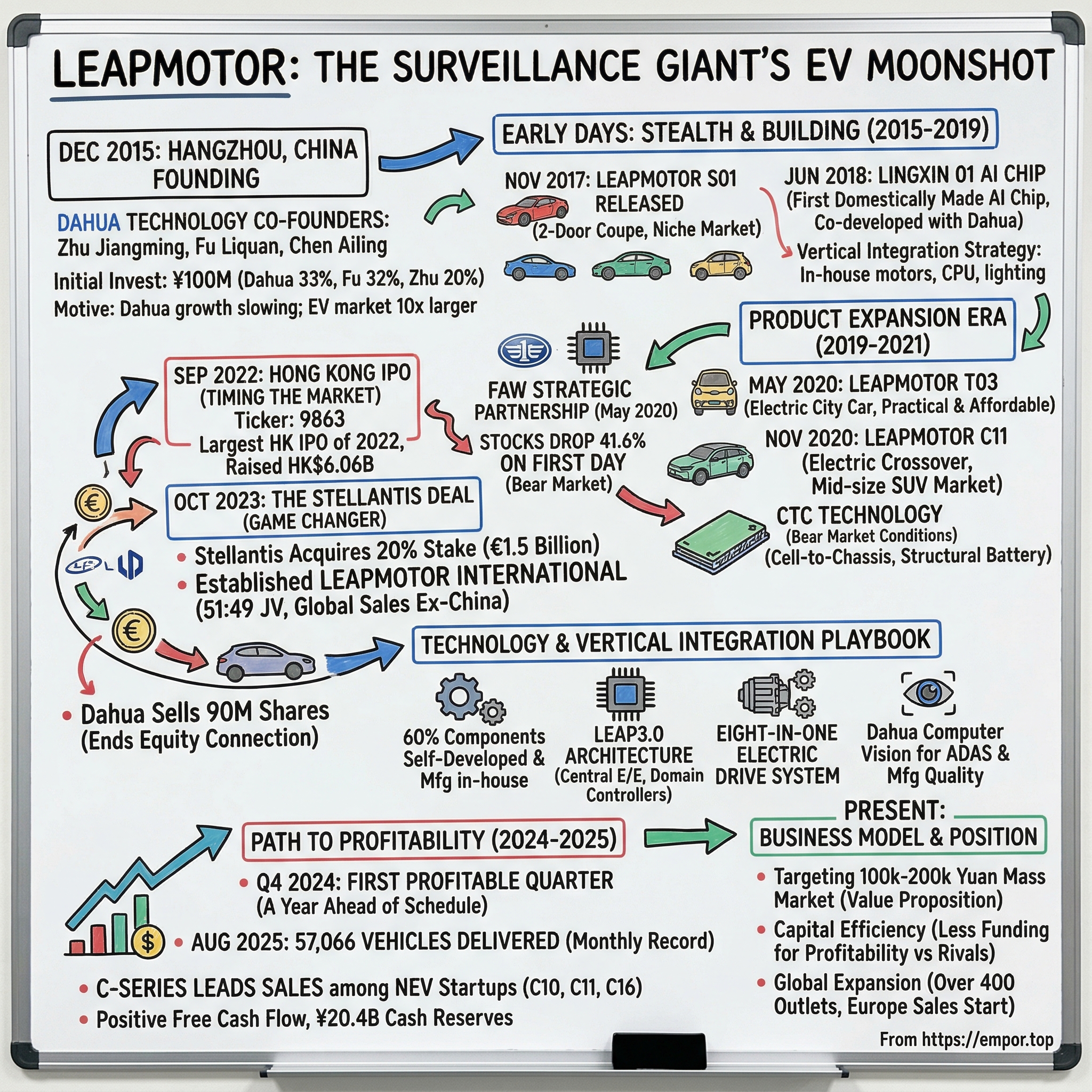

Picture this: It's December 2015 in Hangzhou, China. In a nondescript office building, two men who built a surveillance technology empire worth billions are sketching designs for something completely different—an electric car. Not just any electric car, but one that would leverage artificial intelligence, vertical integration, and the kind of cost discipline learned from making security cameras that watch over half the world's cities. This is the moment Zhejiang Leapmotor Technology was born.

The question that hangs in the air: Why would Zhu Jiangming, co-founder of surveillance giant Dahua Technology, walk away from a company generating billions in revenue to start from zero in the brutally competitive electric vehicle market? The answer reveals something profound about how technology convergence creates unlikely opportunities—and how a company that started selling its first vehicle in 2019 would, within five years, outsell established EV pioneers and attract a €1.5 billion investment from one of the world's automotive titans.

This is a story about vertical integration taken to its logical extreme—where a company manufactures 60% of its vehicle components in-house, from AI chips to electric motors. It's about timing markets so badly that your IPO drops 41% on the first day, only to see the stock triple within three years. Most surprisingly, it's about how a Chinese startup convinced Stellantis—maker of Jeep, Ram, and Peugeot—to bet its global EV future on technology developed by former security camera engineers.

What makes Leapmotor fascinating isn't just its rapid rise from zero to 57,000 vehicles delivered monthly by August 2025. It's how the company represents a new playbook for automotive disruption: technology-first thinking applied to century-old manufacturing, Chinese innovation scaling globally through Western partnerships, and the audacious bet that making your own chips and batteries isn't just possible—it's essential for survival. As we'll see, every major inflection point in Leapmotor's journey reveals larger truths about where the global auto industry is heading.

II. The Dahua Connection & Founding Story

The story begins in a Hangzhou conference room in December 2015, where surveillance technology was about to collide with automotive ambition. Dahua Technology, together with controlling shareholder Fu Liquan and director Zhu Jiangming, founded Zhejiang Leapmotor Technology Co., Ltd. What made this moment extraordinary wasn't just the founding of another EV startup—China had dozens of those. It was who was doing it, and why.

Fu Liquan and Zhu Jiangming are also co-founders of Dahua Technology. Their journey to this moment stretched back to 1993, when Zhu and his friend Fu Liquan started their entrepreneurial journey with a startup capital of 5,000 yuan, primarily selling telecommunications equipment, programmable switchboards—a product that Huawei and ZTE also started with. From those humble beginnings selling telecom equipment, they'd built Dahua into the second-largest video surveillance company in the world in terms of revenue, after Hikvision.

The Dahua empire they built was formidable. Dahua was founded in 2001 by former defense industry technician Fu Liquan, who serves as the company's chairman and the Secretary of its Communist Party committee. By 2015, the surveillance giant had achieved remarkable scale—Since its IPO in Shenzhen in 2008, Dahua has achieved a compound annual growth rate of 47.67%. Now it is worth more than ¥38 billion ($5.52 billion) and has footprints in more than 180 countries. The company's cameras watched over cities from London to Los Angeles, monitoring everything from traffic flows to retail stores.

But Zhu Jiangming saw something others missed. The convergence happening in technology—artificial intelligence, computer vision, edge computing—meant that cars were becoming computers on wheels. And who better to build those computers than engineers who'd spent decades perfecting the art of capturing, processing, and analyzing visual data in real-time? Zhu Jiangming is executive VP of Dahua and a co-founder of the firm, bringing deep technical expertise that would shape Leapmotor's DNA.

The initial capital structure revealed both ambition and careful alignment. Total investment is ¥100 million and the shareholder structure is: a ¥33 million investment by Dahua for 33% of the shares, ¥20 million by Zhu for a 20% share and ¥32 million by Fu for 32%. This wasn't a corporate spinoff in the traditional sense—the founders were putting their own capital at risk alongside the company they'd built. In December 2015, Dahua, Fu, Zhu, and other shareholders jointly established Leapmotor, holding shares of 33%, 32%, and 20%, respectively.

The decision to enter the automotive industry came from a sobering realization about Dahua's own limitations. Dahua's decision to make NEVs is due to practical considerations. Its core business is slowing alongside the world economy, and the size of the entire security industry is only $100 billion. China expects to have 5 million NEVs on the roads by 2020, so the company saw an opportunity and kicked off the NEV project in 2015. The surveillance industry, despite its growth, had a ceiling. The automotive industry represented a market ten times larger.

What distinguished Leapmotor from the dozens of other EV startups sprouting across China was its technology-first approach rooted in Dahua's engineering culture. Relying on the strong financial strength of Dahua and its mature experience in technology research and development, process system and quality management, the company emphasizes the culture of engineers and has the ultimate pursuit of technological innovation, industrial design, and process quality.

The name itself—Leapmotor, or "Ling Pao" (零跑) in Chinese—carried dual meaning. "Zero emissions is another reason why our new brand is called 'Ling Pao,'" explained Zhu. Zero emissions, but also starting from zero—a deliberate acknowledgment that despite their surveillance technology empire, they were beginners in automotive.

Fu Liquan's background added another layer to the story. Fu Liquan, chairman and president of Dahua, was born and raised in a peasant family near the Qiantang River. He demonstrated the entrepreneurial spirit of Zhejiang businessmen by establishing Dahua in 2001. This wasn't Silicon Valley venture capital chasing the next unicorn—this was Zhejiang entrepreneurship, built on decades of manufacturing experience and a deep understanding of hardware-software integration.

The surveillance technology background would prove both blessing and curse. On one hand, Dahua's expertise in AI chips, image processing, and embedded systems provided Leapmotor with capabilities most automotive startups could only dream of. Dahua, a leading player with over two decades of expertise in digital intelligence, had extensive experience in fields such as intelligent transportation and automotive electronics. This background accelerated Leapmotor's product development, channel expansion, and branding efforts.

Yet this same background carried baggage. On October 15, less than a week after the US sanctioned Dahua and Hikvision for human rights abuses, Dahua VP Zhu Jiangming told the PRC's National Business Daily newspaper that: The fact that we are under the US control list shows that we indeed have a strong technological capability While Zhu attempted to spin sanctions as validation of technological prowess, the reality was more complex—Dahua's international reputation would cast a shadow over Leapmotor's global ambitions.

The ownership structure revealed another crucial detail about Chinese tech entrepreneurship. Dahua Technology is majority owned by Fu Liquan and his wife Chen Ailing. As of 31 December 2020, Fu owned 34.18% shares as the largest shareholder, while Chen owned 2.38%. This was family wealth being deployed into a moonshot bet on electric vehicles—not institutional capital chasing quarterly returns.

As 2015 turned to 2016, Leapmotor operated in stealth mode, building its team and technology foundation. Since then, Leapmotor has become Zhu's primary focus. The surveillance giant's engineers began their transformation into automotive pioneers, carrying with them a unique perspective: they didn't see cars as mechanical devices with some electronics added. They saw them as mobile computing platforms that happened to have wheels.

III. Early Days: Building in Stealth Mode (2015–2019)

March 17, 2017, marked Leapmotor's public debut—not with a car, but with a promise. In March 2017, the Leapmotor brand was officially launched. At a new energy vehicle show in Jinhua, Zhejiang province, Zhu Jiangming took the stage to reveal what had been brewing in secrecy for over a year. The venue choice wasn't accidental—Jinhua would become home to Leapmotor's first factory, a massive bet on manufacturing capability before selling a single vehicle.

The factory itself told a story of ambitious vertical integration. In 2017, Leapmotor launched its first factory in Jinhua, Zhejiang Province. With an investment of 2 billion RMB and covering an area about 380,000 square meters (570 mu), construction of the factory began in July 2017 and completed in 2019, with production commenced in 2021. While other startups outsourced manufacturing or acquired distressed facilities, Leapmotor was building from scratch—a ¥2.5 billion commitment to owning its production destiny.

November 2017 brought the first tangible evidence of Leapmotor's vision: In November 2017, Leapmotor released its first product, the Leapmotor S01. But this wasn't a traditional product launch with immediate sales. The S01 represented a statement of intent—a sleek, two-door electric coupe that looked nothing like the practical, conservative vehicles Chinese automakers typically produced. It was aspirational, almost impractical, the kind of car a tech executive might design if unconstrained by market research.

The real technological breakthrough came six months later at CES Asia 2018, where Leapmotor revealed its ace card. On June 13, 2018, at CES Asia, Leapmotor announced that the first domestically made artificial intelligence (AI) chip, dubbed "Lingxin 01", has entered the integration phase. The AI chip was co-developed by Leapmotor and Zhejiang Dahua Technology Co., Ltd (Dahua Technology), and was expected to be tested on vehicles in the second quarter of 2019. The Lingxin 01 is designed for autonomous vehicles, and features the capability of deep learning and leading computing power.

This wasn't just another car company claiming AI capabilities—Leapmotor had actually developed its own silicon. The Lingxin 01 chip represented something profound: while Tesla was grabbing headlines with Autopilot, a Chinese startup backed by surveillance technology expertise was quietly building the semiconductor foundation for autonomous driving. The Dahua connection provided more than capital; it provided two decades of experience in computer vision and edge computing.

The company vertically integrates high margin components by developing and building its own components such as electric traction motors, vehicle CPU, and LED lighting. This vertical integration strategy emerged from Zhu's fundamental belief: to compete globally, Chinese automakers couldn't just assemble parts from suppliers. They needed to own the technology stack.

Behind the scenes, the engineering culture inherited from Dahua shaped every decision. In 2002, Zhu led his team to develop one of the first 8-channel real-time DVRs (digital video recorders) based on an embedded platform. With its leading technological products, Dahua quickly accelerated its growth, successfully listing on the stock market in 2008 and reaching the second-largest global market share by 2015, second only to Hikvision. The same obsession with real-time processing that made Dahua's surveillance systems world-class now drove Leapmotor's approach to vehicle computing.

The path to production proved more challenging than anticipated. While the Jinhua factory construction proceeded on schedule, turning renderings into road-worthy vehicles exposed the vast gulf between surveillance cameras and automobiles. LeapMotor will invest ¥2.5 billion in a production plant and the construction of the production facilities in Jinhua has already gotten approval in February. The construction and equipment buyoff is planned to be completed by the end of this year, and pilot production is scheduled to start in June 2018. At full capacity, the factory will have capacity to produce up to 50,000 EVs annually.

By early 2019, Leapmotor had reached a critical juncture. At that time, the company had raised RMB 380 million in capital, and construction of the factory had started. The capital raised—while substantial—paled in comparison to the billions flowing into competitors like NIO and Xpeng. Leapmotor needed to prove it could actually deliver vehicles to customers, not just impressive technology demonstrations.

June 2019 marked the moment of truth: In June 2019, the first product, the Leapmotor S01 electric 2-door coupe, is launched on the Chinese market. After three and a half years of development, Leapmotor's first production vehicle hit Chinese roads. The launch, however, quickly revealed the difference between building a prototype and mass production.

The S01's market debut turned into a cautionary tale about the importance of execution. After the launch of the S01, Leapmotor was eager to showcase their latest innovation with media test drives, a common rite of passage for new models. They entrusted a service provider with the seemingly simple task of obtaining temporary license plates. However, in a turn of events straight out of a cautionary tale, the provider cut corners and used counterfeit plates. Unbeknownst to the journalists, their thrilling test drive had a sting in the tail—a traffic stop where the unsuspecting editor behind the wheel racked up a shocking 12 penalty points from the traffic police.

The counterfeit license plate fiasco became a metaphor for Leapmotor's early struggles—brilliant technology undermined by operational naivety. Despite being marketed as "fully self-developed," the S01 did not impress with its product capabilities. Although it featured an intelligent driving chip co-developed with Dahua and offered advanced features like facial recognition and fingerprint unlocking, many consumers reported issues. The facial recognition that worked flawlessly in Dahua's controlled surveillance environments struggled with the variability of automotive use cases.

Sales numbers told a harsh story. While NIO was delivering thousands of ES8s and Xpeng was ramping up G3 production, the S01 struggled to find buyers. The two-door coupe format—while bold—proved too niche for Chinese consumers prioritizing practicality. Leapmotor had built an engineer's car, not a customer's car.

Yet within this apparent failure lay crucial lessons. The S01 served as Leapmotor's graduate education in automotive reality. Every quality issue, every software bug, every manufacturing hiccup taught the company what surveillance camera production hadn't: cars operate in hostile environments, carry human lives, and must function flawlessly for years. The engineers who'd spent careers ensuring cameras captured clear footage now grappled with ensuring batteries didn't catch fire and airbags deployed correctly.

The financial pressure intensified through 2019. While competitors raised billions in flashy funding rounds, Leapmotor operated on a relative shoestring. The company's burn rate accelerated as it maintained a full R&D team, operated a factory, and attempted to build a sales network. The question wasn't whether Leapmotor had superior technology—it was whether they'd survive long enough for that technology to matter.

IV. The Product Expansion Era (2019–2021)

The S01's lukewarm reception forced a reckoning at Leapmotor headquarters. Engineers had built their dream car; now they needed to build what customers actually wanted. The pivot came swiftly and decisively: if Chinese consumers wanted practical, affordable electric vehicles, Leapmotor would deliver exactly that—but with a technology twist their competitors couldn't match.

On May 11, 2020, Leapmotor officially launched its second mass-production EV, the Leapmotor T03 electric city car. The vehicle was launched with a total of 3 models, the price range after subsidy is 65,800-75,800 yuan (~US $9,280 – US $10,691). The T03 represented everything the S01 wasn't: practical, affordable, and aimed squarely at first-time EV buyers. But beneath its humble exterior, the T03 packed surprising technology—The Leapmotor T03 is equipped with a battery pack with a capacity of 36.5 kWh, and a 403 km (250 mi) NEDC cruising range.

The transformation was remarkable. Where the S01 had been a statement of ambition, the T03 was a masterclass in constraint-driven innovation. Leapmotor's engineers applied their vertical integration philosophy to cost reduction, designing and manufacturing components in-house to hit price points competitors using third-party suppliers couldn't match. The facial recognition features that had been gimmicky in the S01 were refined into practical conveniences in the T03.

Market response validated the strategy. Young urban buyers, particularly in tier-two and tier-three cities, embraced the T03 as their entry into electric mobility. Sales began climbing from hundreds to thousands per month. For the first time, Leapmotor had product-market fit.

But Zhu Jiangming wasn't content with just building a better cheap car. November 2020 brought Leapmotor's most ambitious vehicle yet: In November 2020, Leapmotor officially launched the third mass-production EV, the Leapmotor C11 electric crossover, based on the 2019 C-More concept. The C11 targeted the heart of China's EV market—the mid-size SUV segment where Tesla's Model Y and NIO's ES6 battled for supremacy.

The C11's specifications revealed Leapmotor's technological maturation: The C11 is powered by dual electric motors jointly rated at 400 kW (536 hp) and 720 N⋅m (73.4 kg⋅m; 531 lb⋅ft) of torque. The Leapmotor C11 have around 600 km (373 mi) of driving range. These weren't just competitive numbers—they exceeded what many established luxury brands offered. More importantly, the C11 showcased Leapmotor's integrated approach to vehicle architecture, with systems designed to work together rather than sourced from disparate suppliers.

The year 2020 also marked a strategic shift in partnerships. In May 2020, Leapmotor and state-owned Chinese automaker FAW forged a strategic partnership to jointly develop intelligent electric vehicle models. The agreement also involves the joint cooperation on R&D, manufacture, production and application of intelligent electric vehicle core parts, and the further research on the development of key basic technologies and the innovation of production measures. This wasn't just a manufacturing deal—FAW, one of China's automotive giants, was validating Leapmotor's technology platform.

The product expansion accelerated through 2021, with Leapmotor demonstrating it could develop and launch vehicles at a pace that would make traditional automakers dizzy. Each new model refined the formula: aggressive pricing enabled by vertical integration, technology features that exceeded the price point's expectations, and gradual improvement in build quality and reliability.

Sales momentum built steadily. From the hundreds of S01s struggling to find buyers, Leapmotor climbed to delivering over 20,000 vehicles in 2021. While still trailing the headline-grabbing trio of NIO, Xpeng, and Li Auto, Leapmotor had quietly established itself as a serious player in China's EV revolution.

The technology developments during this period went beyond individual vehicles. Leapmotor was architecting an entire ecosystem—developing its own battery management systems, motor controllers, and crucially, the software stack that would differentiate its vehicles. The company's engineers, drawing on their Dahua heritage, understood that in the age of software-defined vehicles, owning the code was as important as owning the factory.

Financial pressure, however, continued to mount. At the end of 2020, Leapmotor secured over 4 billion RMB in committed funding, closing a 4.3 billion RMB Series B financing in early 2021, which was 13 billion RMB over-subscribed. Dahua Technology chairman Mr. Fu Liquan and Mr. Zhu Jiangming also increased their stakes. The oversubscribed funding round validated investor confidence, but also highlighted a crucial reality: Leapmotor needed access to public markets to fund its ambitious expansion plans.

The competitive landscape grew increasingly brutal through 2021. Tesla's Shanghai Gigafactory was hitting full stride, cutting prices aggressively. The established trio of Chinese EV startups were pulling away in sales volumes and brand recognition. New entrants backed by tech giants—Xiaomi's upcoming EV venture, Huawei's automotive partnerships—threatened to reshape the market again.

In this environment, Leapmotor made a crucial strategic decision: rather than compete directly on brand prestige or flashy features, it would win through technological depth and cost efficiency. The goal wasn't to build the most desirable EVs, but the smartest ones—vehicles where every component was optimized, every system integrated, every cost justified.

This philosophy crystallized in Leapmotor's development of Cell-to-Chassis (CTC) technology, eliminating the traditional battery pack structure by integrating cells directly into the vehicle chassis. While BYD grabbed headlines with its Blade Battery, Leapmotor quietly pioneered structural innovations that would reduce weight, increase range, and lower costs—the trinity of EV competitive advantage.

By late 2021, Leapmotor stood at a crossroads. The company had proven it could build and sell electric vehicles, develop proprietary technology, and compete with better-funded rivals. But the next phase—scaling to hundreds of thousands of vehicles annually, expanding internationally, achieving profitability—would require capital markets access. The IPO decision was no longer optional; it was existential.

V. The Hong Kong IPO: Timing the Market (2022)

On March 17, 2022, officially kicked off IPO application on Hong Kong Stock Exchange with CICC, Citi, J.P. Morgan Chase, and CCB International as co-sponsors—the date itself carried symbolism. Exactly five years after launching the Leapmotor brand, Zhu Jiangming was taking his company public. But the timing couldn't have been worse.

Global markets were in freefall. The Federal Reserve had begun its aggressive rate-hiking cycle. Chinese tech stocks were being hammered by regulatory crackdowns. The Hang Seng Index had lost nearly 40% from its peak. In this environment, Leapmotor was attempting to raise capital for an unprofitable, capital-intensive automotive startup. Investment bankers privately called it either brave or foolish.

The roadshow revealed the challenge. Institutional investors, burned by the collapse of Chinese tech valuations, questioned everything. Why should they believe Leapmotor could achieve profitability when NIO, with far greater resources, still bled cash? How could the company compete with Tesla's manufacturing efficiency or BYD's battery advantage? Most pointedly: wasn't this exactly the wrong time to go public?

Zhu Jiangming's response was characteristically engineer-like: he presented data. Vertical integration had reduced Leapmotor's bill of materials by 15-20% versus competitors. The company's R&D spend per vehicle was a fraction of NIO's or Xpeng's. Most importantly, Leapmotor's path to profitability didn't require miracles—just scale.

On September 29, 2022, Leapmotor debuted on the Hong Kong Stock Exchange, becoming the fourth NEV startup listed after XPENG, Li Auto, and NIO. This was also the largest IPO on the Hong Kong exchange that year, raising a net amount of 6.06 billion HKD. The achievement came with a brutal asterisk: shares were priced at HK$48, the bottom of the marketed range, and the offering was barely covered.

The first day of trading turned into a bloodbath. Shares tumbled as much as 41.6% from the offer price, a shocking repudiation for what was supposed to be a milestone moment. Retail investors who'd subscribed to the IPO watched their investment evaporate within hours. The financial media had a field day—another Chinese EV startup discovering that public markets were less forgiving than venture capitalists.

The numbers painted a stark picture of market sentiment. Hong Kong IPO volumes had fallen nearly 90% year-over-year. Global funds were pulling money from emerging markets at the fastest pace since the 2008 financial crisis. In this context, Leapmotor hadn't just mistimed the market—it had walked into a category-five financial hurricane.

Yet beneath the headlines, something interesting was happening. The IPO, despite its disastrous optics, had achieved its core objective: Leapmotor now had HK$6.06 billion in fresh capital, enough to fund operations through the crucial scaling phase. The company also gained something equally valuable—public market discipline. No longer could Leapmotor burn cash pursuing moonshot projects; every dollar would be scrutinized by increasingly skeptical investors.

The stock's subsequent journey proved even more dramatic than its debut. By October 2022, shares hit an all-time low of HK$17.50—a stunning 64% below the IPO price. Long-suffering investors watched their stakes shrink to barely a third of their original value. The company that had pitched itself as the smart money's EV play looked like the dumbest trade of 2022.

But Leapmotor's leadership, hardened by decades of building Dahua through various crises, understood something about market cycles. The same factors crushing the stock price—recession fears, China pessimism, EV skepticism—were temporary. The fundamental transition to electric vehicles wasn't stopping. If anything, the shakeout would eliminate weaker competitors, leaving more market share for survivors.

The company's behavior during this period revealed its character. Rather than pursuing desperate pivots or flashy announcements to boost the stock, Leapmotor doubled down on execution. Production continued ramping. New models proceeded through development. Cost reduction initiatives accelerated. It was as if management had decided the stock price was noise—what mattered was the business.

This discipline extended to capital allocation. While competitors with stronger balance sheets pursued expensive autonomous driving moonshots or luxury brand aspirations, Leapmotor focused ruthlessly on its core mission: building affordable, technologically advanced EVs at scale. Every spending decision was filtered through a simple question: does this help us achieve positive gross margins?

The IPO also triggered an unexpected benefit: transparency. As a public company, Leapmotor had to reveal its true financial position, technology roadmap, and competitive strategy. This transparency, initially painful as it exposed the company's cash burn, gradually built credibility. Investors could see exactly how vertical integration translated to cost advantages, how R&D investments were allocated, and most importantly, the concrete steps toward profitability.

By early 2023, with the stock languishing below HK$25, few observers would have predicted what came next. The company that had chosen the worst possible time for an IPO, that had seen its valuation crushed, that competed in the most brutal automotive market on earth, was about to secure one of the most significant cross-border automotive partnerships in history.

The lesson from Leapmotor's IPO disaster was counterintuitive: sometimes the worst market conditions create the best opportunities. The company had been forced to prove its resilience, demonstrate capital efficiency, and show it could survive without endless fundraising. These qualities, forged in the furnace of a bear market, would prove irresistible to a European automotive giant looking for a Chinese partner.

VI. The Stellantis Deal: Game Changer (2023)

Carlos Tavares had a China problem. The CEO of Stellantis—the automotive conglomerate formed from the merger of PSA Group and Fiat Chrysler—watched with growing alarm as Chinese EV makers devoured market share in what would soon be the world's largest automotive market. Stellantis's attempts to compete through joint ventures with local partners had produced mediocre results. The company needed a radical solution.

In October 2023, Stellantis expressed its interest in Leapmotor by acquiring a 20% stake valued at approximately EUR 1.5 billion. The announcement sent shockwaves through the automotive world. This wasn't a token investment or technology licensing deal—Stellantis was betting €1.5 billion that a Chinese startup most Western consumers had never heard of held the key to its electric future.

The structure of the deal revealed sophisticated strategic thinking on both sides. This strategic partnership led to the establishment of Leapmotor International, a joint venture company with a 51:49 ratio, facilitating the distribution and production of Leapmotor cars in global markets outside China Stellantis would control the international joint venture, giving it operational control, while Leapmotor retained full ownership of its Chinese operations. It was a have-your-cake-and-eat-it-too structure that solved both companies' strategic dilemmas.

This will be an industry-first global electric vehicle relationship between a leading automaker and a Chinese pure-play NEV OEM. The precedent-setting nature of the deal mattered. While Volkswagen had partnered with Chinese EV makers for the domestic market and Geely had acquired Volvo, no Western automotive giant had previously structured such a comprehensive global partnership with a Chinese pure-play EV company.

For Tavares, the logic was compelling. Stellantis could spend billions and years trying to develop competitive EV technology from scratch, or it could partner with a company that had already cracked the code on affordable electric vehicles. Developed with our in-house, full-suite technology capabilities, Leapmotor brings to the market the best-in-class EV products in a most cost competitive way. We believe in win-win partnerships formed by strong players in the fast-evolving environment.

The financial engineering behind the deal was equally clever. Leapmotor raised HK$8.51 billion ($1.1 billion) by selling newly issued shares to Stellantis at a 19% premium to the closing price the previous day. At the same time, longtime stakeholder Zhejiang Dahua Technology sold 90 million of its Leapmotor shares to Stellantis, equivalent to 6.73% of Leapmotor's stock after the new share issue.

Dahua's exit was particularly significant. Dahua's share sale formally ended its equity connection with Leapmotor, though it continues to supply the EV maker with intelligent cockpit controllers, intelligent driving controllers, software and other related technologies. The surveillance giant had played its role in incubating Leapmotor; now it was taking profits and stepping aside for a global automotive partner. It has washed its hands of Leapmotor and said it expects to its exit to yield a profit of 4.55 billion yuan

Market reaction to the deal proved volatile. Investors initially cheered the deal, with Leapmotor's shares surging 11.4% when the Hong Kong market opened that day. But the rally quickly went into reverse, and Leapmotor's shares actually ended down 11% on the day as earlier worries about the company's future quickly overshadowed excitement over the new tie-up.

The skepticism was understandable. Automotive history is littered with failed East-West partnerships. Cultural differences, technology transfer disputes, and misaligned incentives had doomed countless joint ventures. Why would this one be different?

The answer lay in the deal's structure and timing. Unlike traditional joint ventures where Western companies provided capital and technology to Chinese partners, this was an inverse model—Stellantis was acquiring Chinese technology for global deployment. The partnership aims to further boost Leapmotor's sales in China, the biggest market in the world, while leveraging Stellantis' established global commercial presence to significantly accelerate Leapmotor brand sales in other regions, starting with Europe. Stellantis intends to leverage Leapmotor's highly innovative, cost-efficient EV ecosystem in China to help meet core Dare Forward 2030 electrification targets

The European expansion plan was particularly ambitious. It will start sales in Europe from September 2024, covering Belgium, France, Italy, Germany, Greece, the Netherlands, Romania, Spain, Portugal and other countries. Starting from the fourth quarter of 2024, Leapmotor International will enter India and the Asia-Pacific, the Middle East and Africa (Turkey, Israel, French Overseas Territories) and South America (Brazil, Chile). This wasn't just badge engineering or limited distribution—Stellantis was committing its global network to Leapmotor's success.

Manufacturing arrangements added another layer of complexity. It was decided that the Leapmotor T03 city car would be assembled at the FCA Poland plant in Tychy. European production would help navigate the EU's increasingly strict tariffs on Chinese-made EVs, while giving Stellantis valuable experience with Leapmotor's manufacturing techniques.

The governance structure ensured alignment. Stellantis will have two seats on Leapmotor's Board of Directors and will appoint the CEO of the Leapmotor International joint venture. This gave Stellantis meaningful influence without control, while the joint venture CEO appointment ensured operational leadership aligned with Stellantis's global standards.

For Zhu Jiangming, the partnership represented validation of his technology-first strategy. On October 31, Leapmotor said in an announcement that its founding team had pledged not to transfer or reduce their stake in the company in any way over the next 10 years. This unprecedented commitment—a decade-long lock-up—signaled absolute confidence in the partnership's potential.

The technology transfer aspects were particularly intriguing. Leapmotor was the world's first pure-play EV company to implement Cell-to-Chassis technology on a large scale, and its 'Four-Leaf Clover' Leap 3.0 central-controlled new electric and electronic architecture achieves seamless and efficient collaboration within the core components of smart EVs. Its unique vertical integration model maximizes scalability, enabling Leapmotor to quickly respond to customer needs.

Yet challenges emerged almost immediately. In November, as Poland voted in line with EU tariffs on Chinese-made EVs, production of T03 in the country was already put under question. It was also reported that Leapmotor International and Stellantis have cancelled the plan of manufacturing the B10 model in Poland and decided to move its production to Slovakia and Germany. In March the following year, European T03 production was already terminated. The geopolitical headwinds that Stellantis hoped to navigate through local production proved more challenging than anticipated.

Still, the strategic logic remained compelling. Stellantis gained access to a complete EV platform developed at a fraction of Western costs. Leapmotor gained a global distribution network that would have taken decades and billions to build independently. Both companies could focus on their strengths—Leapmotor on technology development, Stellantis on global operations.

The deal's ripple effects extended beyond the two companies. Other Western automakers began urgently seeking Chinese EV partners. Chinese startups previously dismissed as regional players suddenly fielded calls from Detroit, Stuttgart, and Tokyo. The Stellantis-Leapmotor partnership had proven that Chinese EV technology wasn't just cheap—it was globally competitive.

VII. Technology & Vertical Integration Playbook

Inside Leapmotor's Hangzhou headquarters, a whiteboard displays a striking statistic: 60%. That's the percentage of total vehicle cost that comes from self-developed and self-manufactured components—a level of vertical integration that would make even Elon Musk envious. While Tesla famously makes its own seats to control quality, Leapmotor has taken the principle to its logical extreme.

The journey to this extraordinary level of self-sufficiency began with a simple observation from Zhu Jiangming: traditional automotive supply chains are optimized for internal combustion engines, not electric vehicles. Every tier-one supplier's component included margins stacked upon margins, intellectual property licensed from other companies, and designs compromised to work across multiple manufacturers. For an EV startup trying to achieve cost parity with gasoline vehicles, this traditional model was a death sentence.

The LEAP3.0 architecture represents the culmination of Leapmotor's integration philosophy. Unlike traditional vehicle platforms that bolt together discrete systems, LEAP3.0 is conceived as a unified computational platform. The central integrated electronic/electrical (E/E) architecture doesn't just reduce wiring complexity—it fundamentally reimagines how vehicle systems communicate. Where a traditional car might have 70+ separate electronic control units, Leapmotor's architecture consolidates functions into domain controllers, reducing cost, weight, and potential failure points.

The Cell-to-Chassis (CTC) technology showcases this thinking at its most radical. Traditional EVs stack cells into modules, modules into packs, and packs into the vehicle structure—each layer adding weight, cost, and complexity. Leapmotor's CTC eliminates the intermediate steps, integrating battery cells directly into the chassis structure. The floor of the vehicle becomes the battery pack, saving nearly 100 kilograms of weight and increasing range by 10% with the same cell capacity.

But CTC's advantages go beyond weight savings. By eliminating the traditional battery pack housing, Leapmotor reduced parts count by 20% and assembly time by 15%. The technology required reimagining everything from crash structures to thermal management, but the payoff was substantial: a structural cost advantage that no amount of supplier negotiation could match.

The Eight-in-One Electric Drive System represents another breakthrough. Where competitors might source motors from one supplier, inverters from another, and gearboxes from a third, Leapmotor integrated eight major components into a single unit. The system combines the electric motor, reducer, motor controller, DC/DC converter, on-board charger (OBC), power distribution unit (PDU), battery management system (BMS), and vehicle control unit (VCU) into one compact package.

This integration wasn't just about packaging efficiency. By designing all components together, Leapmotor's engineers could optimize interfaces, eliminate redundant functions, and achieve system-level efficiencies impossible with discrete components. The motor controller could be tuned precisely for the motor's characteristics. Cooling systems could be shared across components. Software could orchestrate the entire system as a unified whole.

The Dahua heritage proved invaluable in developing autonomous driving capabilities. Where other startups struggled with perception algorithms and sensor fusion, Leapmotor's engineers brought two decades of computer vision expertise. The same algorithms that could identify faces in grainy surveillance footage could detect pedestrians in challenging lighting conditions. The edge computing capabilities developed for smart city applications translated directly to real-time vehicle decision-making.

Leapmotor's approach to AI chips exemplified its vertical integration philosophy. Rather than rely on Nvidia's expensive autonomous driving platforms or Mobileye's black-box solutions, the company developed custom silicon optimized for its specific needs. The Lingxin chip family, co-developed with Dahua, provided just enough computational power for Leapmotor's autonomous features—no more, no less. This "right-sizing" of technology reduced costs while maintaining functionality.

Manufacturing integration extended beyond components to production processes. Leapmotor's Jinhua factory implemented lights-out manufacturing for key processes, using Dahua's surveillance technology to monitor quality in real-time. Computer vision systems that might inspect products in other industries were repurposed to detect paint defects or panel gaps. The factory became a showcase for how surveillance technology could enhance manufacturing precision.

The software stack represented perhaps the deepest moat. While hardware integration could theoretically be copied, Leapmotor's unified software architecture—developed entirely in-house—coordinated every aspect of vehicle operation. Over-the-air updates could modify not just infotainment features but fundamental vehicle characteristics: throttle response, regenerative braking strength, even suspension settings in air-suspended models.

This software-defined vehicle approach meant Leapmotor could continuously improve vehicles after sale. Early T03 customers received updates that increased range by optimizing battery management algorithms. C11 owners saw their autonomous driving capabilities enhanced through pure software updates. The vehicle became a platform for continuous improvement rather than a static product.

The vertical integration strategy wasn't without risks. Developing everything in-house required massive upfront investment and engineering resources. When a supplier component failed, Leapmotor couldn't simply switch vendors—they had to fix it themselves. The approach demanded excellence across disciplines from semiconductor design to mechanical engineering, a breadth of expertise few companies possess.

Critics argued that Leapmotor was violating the fundamental principle of comparative advantage—why make your own door handles when specialized suppliers could do it better? The answer lay in system-level optimization. That door handle wasn't just a mechanical component but part of the vehicle's security system, integrated with facial recognition, smartphone connectivity, and the central vehicle computer. By controlling every element, Leapmotor could create experiences impossible with off-the-shelf parts.

The financial impact of vertical integration became clear as Leapmotor scaled. While gross margins remained negative during the low-volume years, each doubling of production volume improved margins by 3-5 percentage points. The fixed costs of developing components in-house were spread across more units, while variable costs remained lower than sourcing from suppliers. The path to profitability wasn't through raising prices—it was through scaling production of internally developed components.

By 2024, Leapmotor's vertical integration had evolved from a cost-saving measure to a competitive weapon. When battery raw material prices spiked, Leapmotor could optimize cell chemistry and pack design to minimize impact. When chip shortages crippled competitors, Leapmotor's custom silicon and direct foundry relationships ensured continued production. The strategy that seemed risky in isolation proved remarkably resilient in practice.

The ultimate validation came from competitors. BYD, long the king of Chinese EV integration, began studying Leapmotor's CTC technology. Tesla engineers were spotted at Leapmotor showrooms, examining the Eight-in-One drive unit. Even traditional automakers, long dismissive of startup innovations, began questioning whether their supplier-dependent model could survive the EV transition.

VIII. The Path to Profitability (2024–2025)

The morning of January 12, 2025, marked an extraordinary moment in Leapmotor's boardroom. The company that had struggled to sell a few hundred S01 coupes just five years earlier had achieved net income of RMB 80.9 million ($11.1 million) in the fourth quarter of 2024, its first positive quarterly bottom line since its 2015 inception. Zhu Jiangming allowed himself a rare smile—the path from surveillance cameras to profitable electric vehicles was complete.

The transformation was nothing short of remarkable. The company achieved its goal of making a quarterly profit turnaround one year ahead of schedule, making it the second of China's new car-making forces to achieve profitability. Behind this achievement lay a masterclass in operational excellence and strategic focus that had transformed Leapmotor from a cash-burning startup to a lean profit machine.

The numbers told the story of relentless improvement. Leapmotor's gross margin was a record 13.30 percent in the fourth quarter, up 6.6 percentage points from the fourth quarter of 2023 and up 5.2 percentage points from the third quarter of last year. This wasn't achieved through price increases—if anything, China's brutal price war had intensified. Instead, Leapmotor's vertical integration strategy had finally reached critical mass.

The product mix shift proved crucial. Leapmotor's C-series models delivered 225,071 vehicles in 2024, an increase of 112.9 percent over 2023. Sales of C-series models contributed 76.6 percent of the year's deliveries, a 3.3 percentage point improvement over 2023. These higher-margin vehicles, particularly the C11 and C16 SUVs, commanded premium prices while leveraging the same underlying technology platform, maximizing profitability per unit.

Full-year 2024 results showcased the momentum building throughout the year. On March 10, Leapmotor released its 2024 financial report, logging annual revenue of 32.16 billion yuan, marking a year-on-year surge of 92%. The company achieved a record-high gross margin of 8.4%, while both operating and free cash flow turned positive. The company that had burned through billions reaching scale now generated cash from operations.

The quarterly progression through 2024 revealed accelerating improvement. Notably, in the fourth quarter (Q4) of 2024, Leapmotor delivered over 40,000 vehicles per month on average, achieving a quarterly gross margin of 13.3% and turning profitable in a single quarter a year ahead of schedule. Each quarter brought better margins, higher volumes, and improved operational efficiency—the virtuous cycle every automotive startup dreams of but few achieve.

Investment in technology continued despite the focus on profitability. Notably, Leapmotor's R&D investment continues to grow, reaching a record RMB 895 million in the fourth quarter, up 43.77 percent year-on-year and up 14.76 percent from the third quarter. This wasn't the profligate spending of the cash-burning years but targeted investment in next-generation platforms and manufacturing efficiency.

The ambitions for 2025 reflected newfound confidence. Leapmotor is targeting sales of 500,000 to 600,000 units in 2025, the company's management said on an earnings call yesterday. The company will strive to achieve its goal of full-year profitability in 2025, its management said. Full-year profitability—the holy grail that had eluded even Tesla for over a decade—was within reach.

International expansion through the Stellantis joint venture added another growth vector. By December 2024, Leapmotor International, the joint venture between the Chinese carmaker and Stellantis, had established over 400 international sales and service outlets, including more than 350 in Europe, surpassing its annual target. In 2025, Leapmotor International aims to expand its network to over 550 locations. Each European sale carried higher margins than domestic Chinese sales, improving the overall profit mix.

First-quarter 2025 results confirmed the momentum wasn't temporary. Leapmotor's gross margin was a record 14.90 percent in the first quarter, an improvement of 16.30 percentage points year-on-year and 1.6 percentage points from last year's fourth quarter. Leapmotor reported a net loss of RMB 130 million for the first quarter, a year-on-year decrease of 87.17 percent. While seasonally weaker, the trajectory toward sustained profitability remained intact.

The ultimate validation came in the first half of 2025. Leapmotor achieved a net income of RMB 30 million ($4.21 million) in the first half of 2025, marking its first positive half-year net income, according to its financial report released last month. This makes Leapmotor the second Chinese NEV maker after Li Auto (NASDAQ: LI) to achieve half-year profitability. The company that had IPO'd at the worst possible time, been written off by analysts, and competed against better-funded rivals had achieved what most thought impossible.

August 2025 brought the exclamation point on Leapmotor's transformation. Leapmotor delivered 57,066 vehicles in August, up 88 percent from a year earlier and the highest monthly total in its history, the Chinese carmaker said on Monday. It was the sixth straight month the company led sales among China's NEV startups. The company once dismissed as "just another Chinese EV startup" now outsold NIO, Xpeng, and every other new entrant.

The achievement reflected more than just operational excellence. The company crossed 900,000 cumulative deliveries in August and reported its first half-year net profit, becoming only the second Chinese NEV startup to achieve profitability on that basis, after Li Auto. Each milestone—monthly sales leadership, profitability, cumulative deliveries—validated Zhu Jiangming's technology-first, vertical integration strategy.

Manufacturing efficiency had reached world-class levels. The Jinhua factory, once criticized for its massive upfront investment, now operated at utilization rates exceeding 85%. Lights-out manufacturing zones reduced labor costs while improving quality consistency. The same computer vision technology that powered Dahua's surveillance systems now caught paint defects invisible to human inspectors.

The cost structure transformation was remarkable. Where competitors spent 3-5% of revenue on sales and marketing, Leapmotor achieved growth with less than 2%. Administrative expenses as a percentage of revenue had fallen by half since the IPO. Every non-essential cost had been eliminated, every process optimized. This wasn't the glamorous side of the EV revolution, but it was the foundation of sustainable profitability.

The supply chain strategy proved prescient. While competitors scrambled for batteries during shortages, Leapmotor's direct relationships with cell manufacturers ensured steady supply. The company's flexible chemistry approach—able to use LFP or ternary cells depending on availability and cost—provided resilience others lacked. Vertical integration wasn't just about cost; it was about control.

Cash generation transformed the company's strategic options. Leapmotor ended the year with 20.42 billion yuan in cash reserves. No longer dependent on capital markets for survival, Leapmotor could invest countercyclically, accelerate R&D during downturns, and negotiate from strength rather than desperation.

The product portfolio evolution reflected strategic maturity. The B10 SUV, launched in 2024, targeted the volume sweet spot of 130,000-150,000 yuan. The upcoming Lafa 5, set for September 2025 debut, would push into premium segments. Each model leveraged the same underlying platform and components, maximizing economies of scale while appearing distinct to consumers.

European operations through Stellantis provided valuable lessons. Founder and Chief Executive Officer Zhu Jiangming said export sales remain among the strongest in the sector, with European orders recently hitting a record. Western consumers, initially skeptical of Chinese automotive brands, were won over by Leapmotor's technology-forward approach and competitive pricing.

Yet challenges remained. The European production plans had stumbled on geopolitical realities. Competition in China intensified daily, with price wars eroding industry margins. The need for continuous technology investment, particularly in autonomous driving, threatened to consume the hard-won profits. Leapmotor had proven it could achieve profitability; sustaining it while scaling would be the next test.

The transformation from cash-burning startup to profitable automaker represented more than financial engineering. It validated a fundamental thesis: that technology companies could successfully enter traditional industries by reimagining the entire value chain. Leapmotor hadn't just built electric cars; it had built a new model for automotive manufacturing.

IX. Business Model Analysis & Competitive Position

The whiteboard in Leapmotor's strategy room displays a deceptively simple equation: Revenue per vehicle minus cost per vehicle equals profit. But beneath this simplicity lies one of the most sophisticated business models in global automotive—a fusion of Silicon Valley platform thinking, Chinese manufacturing excellence, and old-fashioned vertical integration that would make Henry Ford proud.

Revenue streams at Leapmotor break down into three distinct but synergistic categories. Vehicle sales represent 95% of revenue, but this understates the sophistication of the model. Unlike traditional automakers who sell a car and lose the customer, Leapmotor maintains continuous revenue through over-the-air updates, charging services, and insurance partnerships. The remaining 5% comes from component sales to other manufacturers and technology licensing—segments poised for explosive growth as the Stellantis partnership matures.

The pricing strategy reveals strategic discipline. Currently, Leapmotor has 7 models on sale: T03, B10, C01, C10, C11, and C16, with a price range covering 100,000 - 200,000 yuan. This isn't random market coverage—it's surgical targeting of the fastest-growing segment of China's EV market. By avoiding both the ultra-budget segment (dominated by Wuling) and the premium segment (where NIO and Li Auto battle), Leapmotor focuses where volume and margins intersect.

The "half-price Li Auto" positioning, initially seen as weakness, has evolved into strategic advantage. While Li Auto's L9 starts at 400,000 yuan, Leapmotor's C16 offers similar size and features at 180,000 yuan. As of August 2025, the C10 has ranked first in the sales of mid - size SUVs among new - energy vehicle startups for three consecutive months, while the C16 has ranked first in the sales rankings of mid - to - large SUVs priced below 200,000 yuan for eight consecutive weeks. Consumers get 80% of the experience at 50% of the price—a value proposition that resonates powerfully in price-conscious markets.

Manufacturing economics tell the real story of Leapmotor's model. Traditional automakers operate on a 5-7% gross margin for volume vehicles. Premium brands like Mercedes achieve 15-20% through brand markup. Leapmotor has achieved 14.9% gross margins not through brand premium but through fundamental cost advantages. When you make your own motors, batteries, and chips, every layer of supplier margin stays in-house.

The comparison with Tesla's approach reveals crucial differences. Tesla pursued vertical integration to control quality and innovation speed. Leapmotor pursues it for cost advantage. Tesla builds Gigafactories costing $5 billion; Leapmotor's Jinhua facility cost $2 billion for similar capacity. Tesla develops full self-driving capabilities requiring thousands of engineers; Leapmotor develops practical ADAS features with hundreds. Both approaches work, but Leapmotor's is profitable at far lower volumes.

Platform economics provide hidden leverage. The LEAP3.0 architecture underlies every vehicle from the tiny T03 to the large C16. Development costs amortize across hundreds of thousands of units. A software update improving battery management deploys across the entire fleet. A manufacturing improvement in motor production benefits every model. This platform approach, borrowed from smartphone manufacturing, treats cars as hardware instances of a common software platform.

The international expansion model through Stellantis creates unique economics. The deal also outlines the formation of Leapmotor International, a 51/49 Stellantis-led joint venture that has exclusive rights for the export and sale, as well as manufacturing, of Leapmotor products outside Greater China. Leapmotor receives 49% of international profits without the massive capital investment required for global expansion. Stellantis provides distribution, manufacturing, and brand credibility—services that would cost billions to replicate.

Distribution strategy reflects Chinese digital-native thinking. Leapmotor's Q2 financial report released this year shows that as of June 30, 2025, Leapmotor's sales and service network covers 286 cities, with 88 new cities added. It has 806 sales stores and 461 service stores, and the efficiency of each store has increased by more than 50% year - on - year. But these aren't traditional dealerships—they're experience centers with digital integration, minimal inventory, and direct-to-consumer pricing. The model eliminates dealer margins while providing better customer experience.

The competitive positioning becomes clear when mapped against rivals. NIO pursues the premium strategy with battery-swapping infrastructure and concierge services—brilliant but capital-intensive. Xpeng focuses on autonomous driving leadership—technically impressive but expensive to develop. Li Auto dominates the extended-range segment—profitable but potentially transitional technology. Leapmotor pursues accessible technology—less sexy but more sustainable.

Capital efficiency emerges as the decisive competitive advantage. From founding to profitability, Leapmotor raised approximately $3 billion in total funding. NIO has raised over $10 billion and remains unprofitable. Xpeng has raised $7 billion with persistent losses. The difference? Leapmotor's vertical integration and platform approach deliver more output per dollar invested.

The China EV landscape increasingly favors Leapmotor's positioning. As subsidies disappear and price wars intensify, only the most efficient survive. Bloated cost structures can't hide behind government support. Technology advantages get commoditized rapidly. In this environment, Leapmotor's lean operations and cost leadership become decisive advantages.

Supply chain strategy provides resilience competitors lack. By manufacturing critical components internally, Leapmotor avoids the semiconductor shortages that crippled rivals. Direct relationships with raw material suppliers eliminate multiple markup layers. The company can switch battery chemistries based on material costs, use alternative chips when specific ones are unavailable, and adjust specifications without supplier negotiations.

The services ecosystem, while nascent, shows promise. Insurance partnerships through platforms like SunCar Technology create recurring revenue streams. SunCar, which has operated Leapmotor's insurance platform since February 2025, provides AI-powered auto insurance solutions to Leapmotor's customers. The company is focusing on optimizing insurance purchasing processes, enabling rapid claim settlements, and improving customer experience to support Leapmotor's growth and global expansion plans. Charging network partnerships provide convenience without capital investment. Software subscriptions for advanced features generate high-margin recurring revenue.

Financial metrics validate the model. Return on invested capital has turned positive—rare for automotive startups. Asset turnover exceeds established automakers through lean operations. Working capital management, particularly inventory turns, approaches best-in-class levels. These aren't exciting metrics, but they're the foundation of sustainable competitive advantage.

The risk lies in the model's demands for flawless execution. Vertical integration means every problem is your problem. Platform economics require massive scale to work. Cost leadership positions are vulnerable to new entrants with deeper pockets. The partnership with Stellantis could constrain strategic flexibility. Success requires threading multiple needles simultaneously.

Yet the model's elegance lies in its alignment. Every element—vertical integration, platform architecture, cost leadership, international partnership—reinforces the others. It's not the flashiest business model in EVs, but it might be the most sustainable. In an industry littered with failed startups and struggling incumbents, Leapmotor has found a formula that actually works.

X. Bear vs. Bull Case

The investment committee room is divided. On one wall, charts showing Leapmotor's stunning delivery growth and pathway to profitability. On the opposite wall, graphs of China's brutal EV price war and rising geopolitical tensions. The bear and bull cases for Leapmotor aren't just academic exercises—they represent two radically different visions of the automotive future.

The Bear Case: Racing Toward a Cliff

The bears begin with market structure. China's EV market has become a gladiatorial arena where only the strongest survive. Over 40 brands competed in 2018; fewer than ten remain viable today. Price wars have intensified to the point where companies sell vehicles at losses just to maintain factory utilization. In this environment, Leapmotor's thin profit margins offer no cushion for error.

Competition from established giants poses existential threats. BYD, with its massive scale and battery advantages, can undercut any competitor on price while maintaining profitability. BYD has invested 100 billion yuan and expanded its personnel scale by 10 times in two years to achieve remarkable results. When a competitor can invest 100 billion yuan in R&D while you scrape by on thin margins, how long can technology parity last?

The technology gap in autonomous driving grows daily. While Leapmotor focused on cost optimization, competitors invested heavily in AI and self-driving capabilities. From 2019 - 2024, its cumulative R & D investment was 7.07 billion yuan. Of the 2.37 billion yuan invested in 2024, 72% of the funds were used for the compatibility transformation of the old platform, and only 28% was invested in the R & D of the new architecture. This underinvestment in future technology could prove fatal as autonomous features become table stakes.

Geopolitical risks loom large. The EU's tariffs on Chinese EVs have already disrupted Leapmotor's European production plans. The U.S. market remains effectively closed. As Western governments increasingly view Chinese automotive exports as threats to domestic industry, Leapmotor's international expansion could face insurmountable barriers.

The Stellantis dependency creates strategic vulnerability. With exclusive rights to international markets held by the joint venture, Leapmotor has essentially outsourced its global future to a Western partner. If Stellantis struggles—and traditional automakers face massive challenges—Leapmotor's international ambitions collapse. The partnership that seemed brilliant could become a straitjacket.

Technology commoditization accelerates. What seems like competitive advantage today—vertical integration, platform economics—becomes table stakes tomorrow. When every Chinese EV maker adopts similar strategies, Leapmotor's edge evaporates. The company that disrupted through integration gets disrupted by the next innovation wave.

Margin pressure appears inevitable. Although it has become the second company after Li Auto to achieve semi - annual profitability, Leapmotor only has a net profit of 33 million yuan. A profit of 33 million yuan on revenues of over 24 billion represents a 0.14% net margin—one supply chain hiccup, one recall, one factory shutdown away from losses.

The bears see a company that achieved profitability through unsustainable cost cutting rather than fundamental competitive advantage, exposed to technological disruption, geopolitical risk, and competitive pressures that will only intensify.

The Bull Case: The Awakening Giant

The bulls counter with momentum. Leapmotor has officially secured the No. 1 position among China's new energy vehicle (NEV) startups in August 2025, delivering a record-breaking 57,066 vehicles and + 13.8% vs July 2025. Six consecutive months of sales leadership isn't luck—it's validation that Leapmotor has cracked the code on what Chinese consumers want.

The profitability inflection point changes everything. Being the second Chinese EV startup to achieve profitability after Li Auto puts Leapmotor in rarefied company. While competitors burn cash hoping for eventual profits, Leapmotor generates cash to invest in growth. In capital-intensive industries, cash generation is the ultimate competitive advantage.

Stock performance validates the bull thesis. From the October 2022 low of HK$17.50 to August 2025 high of HK$76.30, the stock has more than quadrupled. Markets are forward-looking, and they see something bears miss—a company hitting its stride just as weaker competitors falter.

Vertical integration, dismissed by bears as table stakes, provides enduring advantages. When supply chains strain, Leapmotor continues production. When raw material prices spike, internal manufacturing cushions the impact. When new regulations require component changes, Leapmotor adapts without supplier negotiations. This control premium compounds over time.

The Stellantis partnership is just beginning to bear fruit. By December 2024, Leapmotor International, the joint venture between the Chinese carmaker and Stellantis, had established over 400 international sales and service outlets, including more than 350 in Europe, surpassing its annual target. Four hundred outlets in year one suggests massive potential as the network matures. European consumers seeking affordable EVs have few options—Leapmotor fills this gap perfectly.

Market positioning aligns with mega-trends. As EV adoption moves from early adopters to mainstream consumers, price becomes paramount. Leapmotor's 100,000-200,000 yuan sweet spot captures the mass market's shift to electric. The "half-price Li Auto" positioning that seemed like weakness is actually shrewd market segmentation.

Technology sufficiency beats technology leadership. Consumers don't need Level 5 autonomy—they need adaptive cruise control that works. They don't need 1,000-kilometer range—they need 400 kilometers at an affordable price. Leapmotor's pragmatic approach to technology aligns with what consumers actually buy versus what generates headlines.

Platform scalability provides exponential economics. Every doubling of volume improves margins through fixed cost absorption. The R&D invested in LEAP3.0 architecture pays dividends across every future model. Software improvements deploy instantly across the entire fleet. This operating leverage is just beginning to manifest.

The balance sheet strength enables strategic flexibility. With over 20 billion yuan in cash and positive cash flow, Leapmotor can weather downturns, invest countercyclically, or pursue acquisitions. This financial strength, rare among EV startups, provides options competitors lack.

Management's track record inspires confidence. The same team that built Dahua into a global surveillance leader has navigated Leapmotor from concept to profitability. Their engineering-first culture, cost discipline, and long-term thinking have delivered results. Why bet against them now?

The bulls see a company that has survived the EV startup shakeout, achieved sustainable profitability, and positioned itself perfectly for the mass-market EV adoption wave about to sweep global markets.

The Verdict: Probability-Weighted Outcomes

Reality likely lies between extremes. Leapmotor faces real challenges—intensifying competition, technology transitions, geopolitical headwinds. But it also possesses genuine advantages—cost leadership, vertical integration, global distribution through Stellantis, and most importantly, profitability.

The key question isn't whether challenges exist—they do. It's whether Leapmotor's advantages provide sufficient moat to navigate these challenges while scaling profitably. The answer depends on execution, market evolution, and some degree of luck.

For investors, Leapmotor represents a fascinating risk-reward proposition. The downside—a return to losses and eventual consolidation—is real but manageable given the company's balance sheet strength. The upside—becoming a global EV force through the Stellantis partnership while maintaining Chinese cost advantages—could generate extraordinary returns.

The bear and bull cases aren't fixed—they evolve with each quarterly result, each new model launch, each geopolitical development. What matters is that Leapmotor has options, flexibility, and most crucially, time. In the brutal world of EV startups, survival itself is victory. Profitability is dominance.

XI. Key Inflection Points & Lessons

Every successful company has moments where everything changes—decisions that seem minor at the time but redirect the entire trajectory. For Leapmotor, five critical inflection points transformed a surveillance engineer's EV dream into a profitable global automaker.

Inflection Point 1: The Pivot from Dahua (2015-2017)

The decision to leave Dahua wasn't just about starting a car company—it was about transplanting an entire technological DNA. While other EV startups hired automotive veterans, Zhu Jiangming brought surveillance engineers. This seemed like madness, but it contained genius. The computer vision expertise that tracked faces in crowds would detect pedestrians. The edge computing that processed video streams would manage battery systems. The cost discipline from selling cameras to price-sensitive governments would enable affordable EVs.

The lesson: Revolutionary advantage often comes from applying expertise from unrelated fields. Automotive insiders think in automotive paradigms. Outsiders see possibilities insiders miss.

Inflection Point 2: Product-Market Fit with T03 (2019-2020)

The S01's failure could have killed Leapmotor. Instead, it triggered radical introspection. Engineers wanted to build a sports coupe; customers wanted practical transport. The pivot to the T03—unglamorous but useful—saved the company. This wasn't just a product decision but a philosophical shift from engineering elegance to customer value.

The T03 taught Leapmotor that in emerging markets, sufficiency beats excellence. A good-enough product at an excellent price beats an excellent product at any price. This insight, painful for engineers to accept, became central to Leapmotor's strategy.

Inflection Point 3: IPO in Terrible Market (2022)

Listing when the stock immediately crashed 41% seemed like disaster. In retrospect, it was discipline-forcing genius. The brutal market reception eliminated any temptation for vanity spending. Every decision was scrutinized through the lens of survival. This forced austerity, initially painful, created the lean operations that enabled profitability.

The lesson: Sometimes the worst conditions create the best habits. Companies that IPO into bull markets often develop sloppy practices hidden by rising valuations. Bear market IPOs force excellence from day one.

Inflection Point 4: Stellantis Partnership (2023)

Selling 20% to a Western automaker could have been seen as surrender—admission that Leapmotor couldn't compete globally alone. Instead, it was strategic jujitsu. Rather than spend billions building international operations, Leapmotor accessed Stellantis's global network instantly. Rather than fight tariffs and local politics, Leapmotor became a partner, not a threat.

The structure—keeping China operations separate while joint-venturing international—was masterful. Leapmotor maintained control of its core market while outsourcing the expensive, risky international expansion. This wasn't just a partnership but a new model for Chinese companies going global.

Inflection Point 5: Achieving Profitability (2024-2025)

The shift from losses to profits wasn't just an accounting milestone but a psychological transformation. Employees who'd accepted lower salaries for equity saw validation. Suppliers who'd extended credit saw reliability. Investors who'd endured stock price volatility saw vindication. Profitability changed Leapmotor from speculative bet to sustainable business.

More importantly, profitability came from operational excellence, not financial engineering. This wasn't achieved through one-time gains or accounting tricks but through systematic improvement in margins, efficiency, and scale. Sustainable profitability is far rarer and more valuable than momentary profits.

Meta-Lessons: Patterns of Transformation

Several patterns emerge from these inflection points:

Timing Matters Less Than Execution: Leapmotor consistently had terrible timing—entering EVs as subsidies peaked, launching products into downturns, IPOing into bear markets. Yet excellent execution overcome poor timing repeatedly. The lesson: don't wait for perfect conditions; create them through execution.

Vertical Integration as Competitive Moat: Every inflection point reinforced vertical integration's value. When the S01 failed, internal manufacturing enabled rapid pivot to T03. When markets crashed, cost advantages from integration maintained viability. When partnering with Stellantis, technology ownership ensured value capture. The lesson: in technology transitions, owning the stack matters more than optimizing individual layers.

Technology-First in Traditional Industries: Leapmotor succeeded by thinking like a technology company that happens to make cars, not a car company that uses technology. This manifested in platform thinking, software-defined products, and continuous improvement through updates. The lesson: industry boundaries blur during technological disruptions; thinking across boundaries creates advantage.

Strategic Partnerships Accelerate Expansion: The Stellantis deal shows how Chinese companies can globalize without the traditional model of building everything themselves. By partnering strategically, Leapmotor achieved in months what would take decades independently. The lesson: in globalized markets, the right partnership can be more valuable than independence.

The Survival Power of Profitability: Achieving profitability transformed Leapmotor's strategic options. No longer dependent on capital markets, the company could invest countercyclically, pursue long-term projects, and negotiate from strength. The lesson: in capital-intensive industries, profitability isn't just about returns—it's about strategic freedom.

The Anti-Patterns: What Leapmotor Avoided

Equally instructive is what Leapmotor didn't do:

- No massive autonomous driving moonshot consuming billions

- No luxury brand pretensions requiring massive marketing spend

- No battery swapping infrastructure or other capital-intensive differentiators

- No pursuit of the US market despite its size

- No acquisition sprees to buy growth

These non-decisions were as important as the actions taken. In industries where everyone zigs, sometimes the winning strategy is to zag.

The Fundamental Insight

Leapmotor's journey reveals a profound truth about innovation: success doesn't require being first or best at everything. It requires being right about a few crucial things and executing relentlessly. Leapmotor was right about vertical integration, right about the mass market's price sensitivity, right about partnering for global expansion, and right about prioritizing profitability over growth.

In Zhu Jiangming's view, selling 500,000 vehicles allows a company to survive, selling one million vehicles gives it vitality and the advantages of scale, and to survive in the long run, it needs to sell three million vehicles. This clarity about what matters—scale, efficiency, sustainability—guided every inflection point.

The ultimate lesson from Leapmotor's inflection points: in industries undergoing technological disruption, the winners aren't necessarily the most innovative or best-funded. They're the ones who correctly identify the few crucial success factors and maintain unwavering focus on achieving them, regardless of market conditions, competitive pressure, or conventional wisdom.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube