SAM Engineering: The Precision Backbone of Global Skies and Silicon

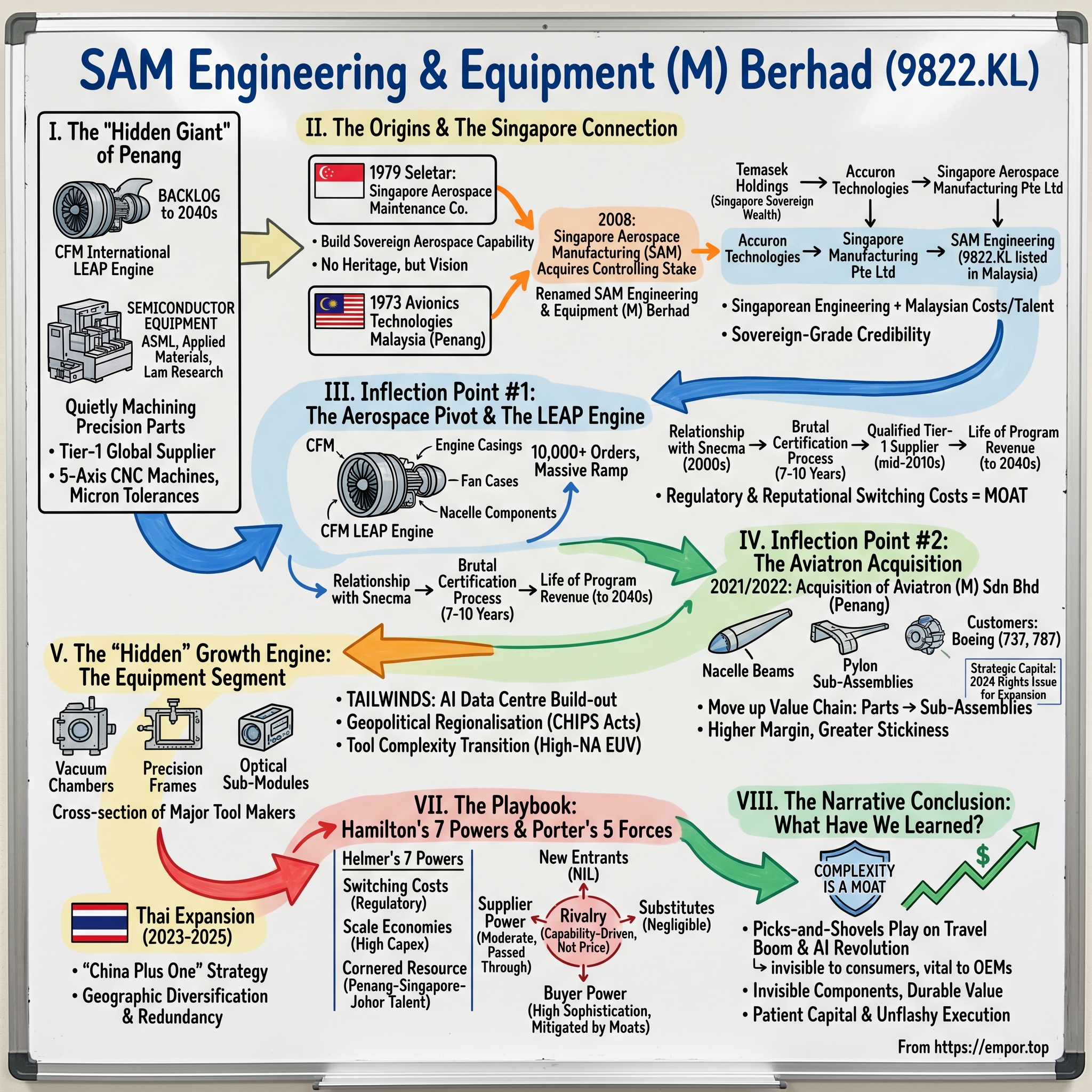

I. The "Hidden Giant" of Penang

Stand on the tarmac at Kuala Lumpur International Airport on any given Tuesday morning and watch the parade: an AirAsia A320neo taxiing for take-off, a Malaysia Airlines 737 MAX easing onto the runway, a Cathay freighter rumbling in from Hong Kong. Listen to the whine of the engines as they spool up. That particular, high-frequency shriek—the one that has become the background music of modern aviation—comes almost entirely from one family of powerplants: CFM International's LEAP engine. It is the single most successful commercial jet engine program in history, with a backlog measured not in hundreds of units but in the tens of thousands, stretching toward the 2040s.

Now drive 350 kilometres northwest to Bayan Lepas, the free industrial zone on the southeastern flank of Penang Island. Past the Intel campus, past the old Motorola facility, past the new Lam Research fab-tool plant, sits a cluster of low-rise factories wrapped in cream-coloured cladding. Inside, white-gloved technicians lean over five-axis CNC machines the size of minivans, coaxing titanium and Inconel into shapes with tolerances measured in microns. No logos on the finished parts. No branding. Just quiet, obsessive precision.

This is SAM Engineering & Equipment (M) Berhad, and this is where a meaningful share of the world's LEAP engine casings, fan cases, and nacelle components are actually made. It is also where a surprising fraction of the metal frames, vacuum chambers, and sub-modules that go inside the semiconductor capital equipment built by ASML, Applied Materials, and Lam Research quietly get machined before being shipped to Veldhoven, Santa Clara, or Fremont.

The hook of SAM is this: while retail investors chase the chip designers with household names and the aerospace OEMs with glittering logos, the actual physical complexity—the stuff that has to not fail when a fan blade rotates at 3,000 rpm or when a photon travels 13.5 nanometres through a mirror polished to atomic smoothness—gets outsourced to a very small number of Tier-1 precision shops around the world. SAM is one of them.

And here's where the story gets strange. SAM is listed on Bursa Malaysia, trades under the ticker 9822.KL, reports in ringgit, and is headquartered in Penang. But it is not, in any meaningful sense, a Malaysian company. It is the publicly-listed Malaysian operating arm of Singapore Aerospace Manufacturing Pte Ltd—itself a subsidiary of Accuron Technologies, which is in turn owned by Temasek Holdings, the sovereign wealth fund of the Republic of Singapore. Which means the Penang machinists bending over those Inconel rings are, several layers up, working for the same shareholder that owns stakes in Singapore Airlines, DBS Bank, and ST Engineering.

The thesis of this episode is that SAM represents one of the most fascinating corporate hybrids in Asian industrial history: a Singaporean state-linked engineering bloodline, grafted onto a Malaysian cost base and talent pool, serving two of the most certification-heavy, capital-intensive, and geopolitically sensitive supply chains on the planet. It is a picks-and-shovels play on both the post-pandemic aerospace super-cycle and the AI-driven semiconductor capex boom, sitting at the precise geographic and political intersection where Western OEMs want their supply chains to live in the 2020s.

Over the next roughly 145 minutes of podcast time—or whatever the reading equivalent turns out to be—we are going to unpack how SAM got here, what the moat actually looks like when you poke it, and why the numbers tell a story of patient capital deployment that is notably un-Malaysian and notably un-Singaporean in its own weird, hybrid way.

Let's start at the beginning, which as always is never quite where you think it is.

II. The Origins & The Singapore Connection

The origin story of SAM does not begin in Malaysia. It begins in 1979, on a stretch of reclaimed land in Seletar, on the northern edge of Singapore island, where the government of Lee Kuan Yew had decided—against essentially all conventional industrial wisdom of the day—that a newly-independent city-state with no aerospace heritage, no OEM, and no obvious factor endowments should nevertheless build a sovereign aerospace maintenance and manufacturing capability.

The original entity was called Singapore Aerospace Maintenance Company, and its initial mandate was embarrassingly modest: overhaul the engines of the Republic of Singapore Air Force's fighter fleet. From that seed, over four decades, grew a sprawling ecosystem that today includes ST Engineering Aerospace (the publicly listed MRO giant) and a parallel manufacturing lineage that eventually became Singapore Aerospace Manufacturing, or SAM. The key architectural decision, made quietly somewhere in the mid-1990s by Temasek-aligned industrial planners, was that Singapore itself would become too expensive to host actual metal-bending at scale. The machining, the welding, the grinding, the cleanroom assembly—all of that would need to migrate across the Causeway or further afield, while Singapore retained the engineering IP, the customer relationships, and the certification authority.

The Malaysian listed vehicle that investors today know as 9822.KL actually started life in 1973 as a company called Avionics Technologies Malaysia, a very small outfit doing exactly what its name suggested: basic avionics work in Penang. It went through several corporate incarnations, a listing on Bursa Malaysia in the 1990s, and a period of relative obscurity as a general precision engineering firm competing on price with dozens of similar Penang shops. The inflection came in 2008, when Singapore Aerospace Manufacturing acquired a controlling stake and renamed the entity SAM Engineering & Equipment (M) Berhad. That moment—the reverse-takeover-ish injection of Singaporean aerospace DNA into a sleepy Malaysian precision shop—is the real birth of the modern company.

Why did this matter? Because being a Temasek-adjacent subsidiary, even several rungs down the family tree, conferred something that no amount of capex could buy: what you might call sovereign-grade engineering credibility. When a Boeing or a CFM International or an ASML procurement team evaluates a new supplier, the due diligence is brutal. Quality systems, financial stability, geopolitical exposure, intellectual property security, continuity of ownership—all of it gets stress-tested. Being owned, ultimately, by the government of Singapore is a dramatically different conversation than being owned by a family office or a private equity fund with a seven-year exit horizon. It signals patient capital, long-time horizons, and a reputational backstop that nobody is going to squander for a short-term margin grab.

The geographic choice was equally deliberate. Penang by the late 2000s had already transformed itself from a 1970s-era low-cost electronics assembly hub—the "Silicon Valley of the East" tagline was always marketing more than reality—into something much more interesting: a dense ecosystem of precision engineering talent, built up over decades of hosting Intel, AMD, Motorola, Agilent, and dozens of tier-two semiconductor equipment suppliers. By the time SAM arrived in force, Penang had roughly the same density of skilled machinists, tool-and-die makers, and quality engineers as Taichung in Taiwan or Hsinchu's outer ring. Wages were still a fraction of Singapore's, English was widely spoken, and—crucially—the regulatory environment was welcoming, stable, and non-Chinese, which would matter enormously a decade later.

So by the early 2010s, you had the ingredients in place: Singaporean engineering heritage, Malaysian manufacturing cost base, access to Penang's skilled labour pool, and a shareholder with a fifty-year time horizon. What the company did not yet have was a genuine reason for global OEMs to bet their programs on it. That reason would arrive in the form of a single engine program, and it would change everything.

III. Inflection Point #1: The Aerospace Pivot & The LEAP Engine

In 2008, CFM International—the fifty-fifty joint venture between General Electric and France's Safran—announced that it was going to replace its venerable CFM56 engine with a new design called LEAP. The CFM56 had been the single best-selling commercial jet engine in aviation history, powering essentially the entire narrow-body fleet of the 1980s, 1990s, and 2000s. Replacing it was not a decision taken lightly. The new LEAP promised fifteen percent better fuel burn through a combination of a much higher bypass ratio, an all-new core with ceramic matrix composite turbine shrouds, and a fan module built around 3D-woven composite blades. It was, and remains, one of the most technologically ambitious commercial engines ever certified.

CFM's problem was not the technology. It was the ramp. By the mid-2010s, the order book for LEAP-powered aircraft—primarily the Boeing 737 MAX and the Airbus A320neo family—had exploded past ten thousand engines. No single existing supply chain could build that many complex titanium and Inconel components in that many variants fast enough. CFM had to find, qualify, and certify a whole new generation of Tier-1 partners, and it had to do it in a global rather than purely Western footprint, both for cost reasons and for political hedging against future trade frictions.

This is where SAM walked through the door. The company had been building relationships with Snecma—Safran's engine division—since the late 2000s. The initial work was modest, largely around the CFM56 legacy program, sub-contracted engine casings and support brackets. Nothing glamorous, nothing that ever got mentioned in an investor presentation. But what was happening was a much slower, much more important process: SAM was going through the certification process. For those unfamiliar with how aerospace supply chains work, the certification process is roughly the industrial equivalent of a priesthood ordination. You do not simply send a machined part to Safran and hope they like it. You submit your quality system, your process controls, your material traceability, your heat-treatment audit trail, your non-destructive testing protocols, and your facility itself, to years of review. Then, even after you are certified, every individual part number—and there are thousands on a single engine—requires its own dedicated first-article inspection, process qualification, and serialisation regime.

The average time from being a prospective supplier to being certified for flight-critical parts on a new engine program is seven to ten years. Which means the relationships that would generate revenue in 2023 were locked in by conversations that happened in 2013. This is the central fact of aerospace economics that flashy investors chronically underestimate: it is not a market where disruption happens. It is a market where position is inherited across decades.

By the mid-2010s, SAM had become a qualified Tier-1 supplier for a widening portfolio of LEAP components. The most critical of these were the engine casings themselves—the structural rings and shrouds that sit around the combustor and turbine sections and that must physically contain a turbine blade if, in the very rare but catastrophic event of a blade separation, the blade comes loose at full thrust. Aviation regulations require that a fan-blade-out or turbine-blade-out event be fully contained within the engine nacelle. The physics of containing a piece of titanium moving at supersonic tangential velocities is non-trivial. The casings that do this job are among the most analytically designed and manufacturing-tolerance-sensitive components in the entire engine. A scratch of the wrong depth in the wrong place can compromise containment. The heat-treatment must be perfect. The weld seams, if any, must be flawless. The dimensional accuracy must be maintained through thermal cycles from minus-fifty to plus-six-hundred Celsius.

SAM does this. And once you are certified to do this, for a specific part number on a specific engine program, you will continue to do it, essentially without competition, for the twenty-to-thirty-year service life of that engine family plus the associated spare parts tail. There is no "cheaper supplier in Vietnam next year" scenario. The qualification cost is too high, the switching risk is too catastrophic, and the regulatory friction with the Federal Aviation Administration and the European Union Aviation Safety Agency is too intense. Once you are in, you are in for the life of the program.

This is what analysts mean when they describe aerospace precision manufacturing as having a "moat." It is not brand loyalty, not network effects, not intellectual property in the patent sense. It is pure regulatory and reputational switching costs, embedded in a multi-decade program cycle. The LEAP, at current delivery rates and backlog, will still be rolling off lines in 2040. Which means that the certification work SAM did in the mid-2010s is still generating revenue today, and will continue to do so for the better part of another two decades.

For SAM as a company, the LEAP inflection did something more than generate a revenue stream. It reframed the business. Pre-LEAP, SAM was a precision engineering firm that happened to do some aerospace work. Post-LEAP, SAM was an aerospace Tier-1 that happened to also serve semiconductor equipment customers. The valuation implications were profound—and they would set up the next strategic move, which was to climb one rung further up the aerospace value chain.

IV. Inflection Point #2: The Aviatron Acquisition – Strategic Masterstroke or Overpayment?

By 2020, SAM had a problem most companies would kill for: its aerospace order book was rising faster than its ability to convert it into revenue. The LEAP ramp was real, Safran's allocation to SAM was rising, and the company's Penang facilities were running at high utilisation. The question the board faced was how to grow the aerospace franchise beyond the engine component slot the company had carved out.

The answer, landed in 2021 and closed in early 2022, was the acquisition of Aviatron (M) Sdn Bhd—a Penang-based specialist in nacelle beams, engine pylon components, and sub-assemblies for Boeing, with a book of business built around the 737 and 787 programs. The deal brought SAM roughly 200 million ringgit of additional revenue potential and, more importantly, a set of capabilities that SAM did not previously possess in-house: large-scale aluminium machining, composite-metal interface work, and sub-assembly integration at the nacelle and pylon level.

To understand why this mattered, you have to understand the difference between "parts" and "sub-assemblies" in aerospace economics. A Tier-1 parts supplier ships individual components—a casing here, a bracket there, a flange somewhere else—to the engine OEM, which then integrates them. The margin is decent but bounded by the fact that the OEM captures the integration value. A Tier-1 sub-assembly supplier ships a pre-integrated module—say, an entire nacelle beam assembly—that the OEM bolts onto the airframe. The margin is structurally higher, the revenue per airframe-shipset is three-to-five-times larger, and the customer stickiness is dramatically greater because replacing a sub-assembly supplier requires re-qualifying the entire module, not just a single part.

Aviatron was SAM's ticket up the value chain. It moved the company from making the things that go inside the jet engine to also making the things that attach the jet engine to the wing. Narratively, SAM went from being "one of several dozen" engine parts suppliers to being "one of a handful" of nacelle sub-assembly partners in the Asia-Pacific region.

The financial question was whether the price was sensible. The transaction consideration, around 260 million ringgit in cash and stock for a business generating perhaps 20-25 million ringgit of EBITDA at pro-forma run-rate, implied an EV/EBITDA multiple in the low-to-mid teens—not cheap by Malaysian industrials standards but fairly in line with where global aerospace Tier-1 peers were trading at the time. Senior plc, the UK-listed aerostructures firm, was changing hands at roughly eight-to-ten times EBITDA. Meggitt, before its acquisition by Parker Hannifin, had been bid at roughly fourteen times. The premium SAM paid reflected the strategic scarcity of Penang-based Boeing-certified nacelle capability, and management argued—credibly, in hindsight—that the integration synergies and the multi-year Boeing ramp would re-rate the economics favourably over a five-year horizon.

What the Aviatron deal really revealed, though, was something deeper about SAM's capital deployment philosophy. This was not a company doing a bolt-on for earnings accretion. This was a company using its balance sheet, its parent-company credibility, and its access to rights issuance proceeds to systematically acquire strategic positioning in a twenty-year industrial cycle. The 2024 rights issue—which raised roughly 300 million ringgit at a modest discount to then-prevailing share price—was explicitly earmarked for capacity expansion in Thailand and Penang, and implicitly for further inorganic opportunities in the aerospace and semi-equipment space. Treating equity as strategic capital rather than as a precious, dilutive resource is a hallmark of Temasek-influenced governance, and it showed up clearly in the way SAM structured its financing.

The bear argument on Aviatron, which surfaced in research notes at the time, was straightforward: Boeing exposure at the wrong moment. The 737 MAX had been through two crashes, a nineteen-month global grounding, and the ongoing production quality issues that culminated in the January 2024 Alaska Airlines door-plug event. A Boeing-heavy acquisition in early 2022 could have looked very different had the 737 MAX program failed to recover. The bull argument, which has largely played out, was that the 737 MAX's problems were execution issues at Boeing's final assembly, not demand issues at the airline level—and that any Tier-1 supplier positioned for the eventual recovery would be handsomely rewarded. SAM's subsequent years of rising nacelle revenue have vindicated the bet, though the 2024 Boeing slowdown did cost the company roughly a year of expected deliveries.

By the time the dust settled on the Aviatron integration, SAM's aerospace segment had roughly doubled in scale and had shifted meaningfully up the value chain. The question then became: what about the other, quieter half of the business?

V. The "Hidden" Growth Engine: The Equipment Segment

There is a recurring pattern in SAM's investor communications that you only notice if you read several years' worth of annual reports in sequence. Aerospace gets the headlines. LEAP gets the bulleted accomplishments. Boeing gets the glossy photography. And tucked toward the back of the operating review, in a quieter and shorter section, is the Equipment segment—a grab-bag description covering precision frames, vacuum chambers, optical sub-modules, and metrology bases for the global semiconductor capital equipment industry.

For a long time, Equipment was the smaller, cyclical, less celebrated half of the business. In revenue terms, Aerospace has consistently been the larger contributor. But in terms of growth rate, in terms of incremental capital allocation, and—increasingly—in terms of what the story will look like three and five years out, Equipment is where the genuinely interesting stuff is happening.

To understand why, you have to take a detour into how semiconductor equipment actually gets made. Companies like ASML, Applied Materials, Lam Research, KLA, and Tokyo Electron sit atop a supply chain that, unlike Apple's or Tesla's, remains shockingly vertically disaggregated. ASML's extreme ultraviolet lithography machines—each one weighing roughly 180 tonnes, costing upwards of 300 million US dollars, and containing 100,000-plus components—are not meaningfully built by ASML itself. ASML is, in essence, a systems integrator and an optical physics company. The mirrors come from Zeiss. The light source is built on technology originally from Cymer. The vacuum chambers, the precision frames, the metal housings, the base plates that have to be machined to submicron flatness—those come from a global constellation of Tier-1 and Tier-2 precision suppliers.

SAM is one of them. And while the company does not publicly disclose customer-level revenue concentration—for obvious and entirely reasonable contractual reasons—it is widely understood in the Penang industrial ecosystem that SAM's equipment segment serves a cross-section of the world's largest front-end and back-end semiconductor tool makers. The parts SAM ships include things like vacuum chamber bodies, metrology frames, electron-beam system sub-assemblies, and the kinds of large precision-machined aluminium and steel structures that form the physical skeletons of wafer fab equipment.

Here is the layman's way to think about it: a cutting-edge semiconductor tool is essentially a scientific instrument the size of a small bus. It needs to hold optical elements steady to within atomic-scale vibration budgets, in a vacuum, while running thousands of wafer cycles a day. The mechanical frame that does this job has to be rigid, thermally stable, dimensionally flawless, and manufactured with a surface quality that most general-engineering shops cannot achieve. SAM's equipment segment is in that business.

The tailwinds, as of 2026, are extraordinary. The global semiconductor capital equipment market, which had been cruising along at a respectable low-double-digit growth rate through the 2010s, has been turbocharged by three mutually reinforcing forces. First, the AI-driven data centre build-out is consuming advanced-node capacity at a rate nobody forecasted even in 2022—Nvidia's and AMD's data-centre accelerator programs alone have pulled forward years of TSMC, Samsung, and Intel fab capacity. Second, the geopolitically-driven regionalisation of semiconductor manufacturing, spurred by the US CHIPS Act, the European Chips Act, and similar programs in Japan, Korea, and India, has created redundant fab capacity that has to be equipped from scratch rather than upgraded in place. Third, the transition to high-NA EUV lithography, gate-all-around transistors, and advanced packaging is driving tool complexity—and therefore per-tool content—meaningfully higher.

For SAM, all of this translates into what operations people call "structural tailwind": an environment where the primary constraint on equipment segment revenue is not customer demand but SAM's own installed manufacturing capacity. Which is precisely why the company made the decision, announced in 2023 and executed through 2024 and 2025, to expand aggressively into Thailand.

The Thailand expansion is one of the more interesting strategic moves in Southeast Asian industrial policy of the last several years, and it has not received nearly enough analytical attention. On paper, the move is framed as geographic diversification. In practice, it is something more specific: a direct response to the "China Plus One" sourcing mandate that has been imposed—quietly but firmly—on most Western and Japanese semiconductor equipment OEMs by their own customers and governments. Tier-1 suppliers are being asked to hold incremental capacity outside of China and outside of Taiwan, in jurisdictions that are political neutral, US-aligned or at least US-tolerated, and physically distinct from the flashpoint geographies. Malaysia checks most of those boxes. Thailand checks all of them, with a different regulatory regime and a different labour pool, providing an internal hedge for SAM itself against the possibility that Malaysia's own political environment ever becomes complicated.

The Thai operations, as of early 2026, are still scaling. Revenue contribution from the Thailand facilities was modest in the financial year ended January 2026, but the footprint, the customer base, and the hiring trajectory all point toward meaningful contribution by the 2028-2029 timeframe. In the meantime, the mere existence of the Thai option is a commercial asset: it allows SAM to win contracts that specify multi-country manufacturing redundancy as a condition of award.

Taken together, the Equipment segment is shifting from being the quieter cousin of Aerospace to being the segment that will likely determine SAM's re-rating over the next five years. Which leads to the obvious question: who is actually running this company, and how are they making these decisions?

VI. Modern Management: The Professional Technocrats

There is a particular type of Asian industrial company—and SAM is very much one of them—where the CEO is not a charismatic founder, not a celebrity operator, not a visionary in the Silicon Valley sense, but a quietly competent professional manager who has spent twenty-plus years inside the industry, knows the customers by their first names, and runs the business the way a conductor runs a chamber orchestra: meticulously, unglamorously, and without needing to be the loudest person in the room.

Jeffrey Logidha, who has served as Group CEO of SAM Engineering since 2019, fits this archetype almost perfectly. Logidha's career before SAM was built inside the Asia-Pacific operations of global industrial firms, with a background that mixes engineering training and operational management rather than finance or consulting. He is not a public figure in the way that, say, a Morris Chang or a Pat Gelsinger is. He does not do television interviews. His LinkedIn presence, as of mid-2026, is characteristically spartan. But inside the Penang precision engineering community, and inside the procurement organisations of CFM International, Boeing, Safran, and the major semiconductor tool OEMs, he is a known and trusted quantity.

The management culture at SAM reflects Logidha's style and, more broadly, the Singaporean parent's governance preferences. This is a Management-by-Objectives organisation, not a Founder's Cult. Decisions get made through documented processes. Capital allocation is reviewed quarterly against a set of return-on-invested-capital hurdles that are explicitly set higher than cost of capital. Executive compensation is weighted significantly toward ROIC and free cash flow metrics rather than toward top-line revenue growth, which is a meaningful differentiator in an industry where it is genuinely tempting to chase volume at the expense of returns.

The shareholder register tells the rest of the story. Singapore Aerospace Manufacturing, the direct Singaporean parent, holds roughly seventy percent of SAM's outstanding shares. Accuron Technologies sits above that. Temasek Holdings, ultimately, sits at the top of the pyramid. This ownership structure has several consequences that are worth thinking through carefully. It means the free float is small—roughly thirty percent—which suppresses trading liquidity and keeps SAM off the radar of most large institutional investors. It also means that any hostile activity, proxy contest, or opportunistic takeover is essentially impossible. SAM is not going to be bought out tomorrow, it is not going to be LBO'd, and it is not going to be subject to the kind of short-term activist pressure that periodically destabilises Western industrials.

For long-term fundamental investors, this ownership concentration is a feature, not a bug. The parent company's governance standards are demonstrably high. The reporting discipline is comparable to Singapore-listed peers. The dividend policy has been consistent but modest, reflecting a management team that treats retained earnings as reinvestment capital rather than as a return-to-shareholders obligation. And the parent's time horizon is measured in decades, which aligns almost perfectly with the twenty-plus-year cycle time of the aerospace programs SAM serves.

There are trade-offs, of course. A seventy-percent parent stake means minority shareholders have essentially no influence over strategic direction. The occasional related-party transaction with the parent group must be taken on trust, and SAM's related-party disclosures, while compliant with Bursa Malaysia requirements, are not lavish. The potential for the parent to someday take the Malaysian entity private, at some future moment when the minority premium is deemed unnecessary, is a theoretical risk that surfaces in analyst conversations from time to time, though it has not shown any signs of becoming concrete.

A note on key personnel dynamics: the senior engineering leadership at SAM has been notably stable through the last five years, with turnover in critical program roles running below industry norms. In an industry where certification knowledge walks out the door with each departed engineer, this retention is itself a quiet competitive advantage. The Penang talent market is tight, and the rise of new Lam Research and Bosch capacity on the island has raised the competitive floor for experienced precision engineers, but SAM's compensation bands and internal mobility tracks have largely held.

With the management and ownership structure understood, the question becomes: how defensible is this franchise, really, when you put it through the analytical frameworks that serious long-term investors use to separate durable moats from mere incumbent inertia?

VII. The Playbook: Hamilton's 7 Powers & Porter's 5 Forces

When analysts trained in the Helmer framework look at SAM, the first power that leaps off the page is switching costs, and in SAM's case, the switching cost is not a normal commercial switching cost—it is a regulatory one, which is a much stronger form. In aerospace, once you have been certified as a sole-source or dual-source supplier for a flight-critical part on a specific engine program, the cost of switching suppliers is not measured in dollars of re-tooling. It is measured in years of re-qualification, in millions of dollars of first-article inspection work, and, most critically, in regulatory risk exposure for the OEM and for the airframe customer. Nobody replaces a certified Tier-1 casings supplier to save three percent on unit cost. The math simply does not work. The result is that once SAM is in on a program, the program stays with SAM for the life of the engine family.

The second power is scale economies, though of a subtle kind. SAM's capital base is not gigantic by global industrial standards—the balance sheet shows a few hundred million ringgit of net property, plant and equipment—but within its specific category of large-format, tight-tolerance precision machining for aerospace and semi-equipment, the capex profile is genuinely forbidding for would-be entrants. A single large five-axis CNC machine capable of handling titanium at the tolerances required for LEAP casings runs into the millions of dollars. The cleanroom requirements for semi-equipment sub-assembly work are not trivial. The inspection infrastructure—coordinate measuring machines, optical comparators, X-ray and dye-penetrant inspection bays—is a further multi-million dollar investment. A new entrant cannot meaningfully compete without a nine-figure capex commitment and a seven-to-ten year qualification runway, during which period the incumbent continues to move up the experience curve.

The third power is what Helmer calls a cornered resource, and SAM's version of it is the Penang-Singapore-Johor talent triangle. Precision engineering of the type SAM does is not a commodity skill. It requires a combination of mechanical engineering training, metallurgical intuition, process discipline, and the particular kind of OCD-level attention to detail that takes a decade to cultivate. Penang and its surrounding Malaysian industrial belt have one of the highest concentrations of such talent outside of Taiwan, Japan, and Germany. The parent's Singapore operations provide the upstream engineering and R&D backbone. Replicating this talent base in, say, Vietnam or Indonesia or the Philippines is achievable over a generation, but not over a product cycle.

The other Helmer powers—branding, network effects, process power, counter-positioning—are either not especially relevant to SAM's business model or are present only in weaker forms. SAM does not have a consumer brand. It does not benefit from network effects in any direct sense. Its process power is real but bounded by the fact that most of its key processes are known to the broader aerospace supply chain, even if execution excellence remains scarce.

Running the Porter 5 Forces analysis in parallel gives a similar picture with different texture. The bargaining power of buyers is, on paper, very high: CFM International, Boeing, Safran, ASML, Applied Materials, and Lam Research are some of the most sophisticated and demanding procurement organisations in the industrial world. They have the analytical tools, the supply chain scale, and the alternative-supplier relationships to extract favourable pricing. In practice, however, the buyer power is significantly mitigated by the dual-source or sole-source nature of many of SAM's key part numbers, by the switching cost discussed above, and by the fact that any pricing squeeze that jeopardises supplier financial health is itself a risk the OEM wants to avoid.

The threat of new entrants is essentially nil over any investable time horizon. The threat of substitutes is negligible—nobody is going to replace an Inconel casing with a 3D-printed polymer or a ceramic substitute within the LEAP's program life. Supplier power over SAM—meaning the raw material and equipment suppliers upstream—is moderate: the titanium and Inconel markets are consolidated and can move price, but SAM's raw material costs are a contractually passed-through component of most long-term agreements with OEMs.

The intensity of rivalry within SAM's specific niche is the most nuanced element. Globally, there are perhaps ten to twenty credible Tier-1 aerospace precision machining houses and perhaps a similar number of semi-equipment frame and sub-assembly specialists. The rivalry is not pricing-driven; it is capability-driven. The firms compete on qualification speed, program responsiveness, and engineering depth rather than on quoted unit price.

With all of this said, it is worth putting the bull and bear cases side by side. The bull case for SAM rests on four pillars. First, the LEAP program and the broader narrow-body recovery have a runway measured in decades, with installed-base spare parts providing a long tail of higher-margin revenue. Second, the China Plus One supply chain rearrangement makes Malaysia and Thailand structurally favoured destinations for incremental capex by Western and Japanese OEMs. Third, the AI-driven semiconductor capex super-cycle is, by any reasonable estimate, in its middle innings rather than its late innings, with high-NA EUV, advanced packaging, and memory capacity build-outs providing multi-year visibility. Fourth, the parent's patient capital structure and the management team's ROIC discipline mean that the growth is being funded in a way that does not destroy long-term value.

The bear case is equally coherent. SAM is capital-intensive, and returns on invested capital, while healthy, are not at the level of an asset-light software business; any major capex misstep can erode returns for years. Customer concentration is real—a small number of OEMs drive a large share of revenue, and any of them could, in extremis, decide to re-source or re-allocate. The semi-equipment cycle, while structurally favourable, is still cyclical, and SAM's equipment segment will experience the full brunt of any global semi downturn. The aerospace segment carries its own tail risks: a future 737 MAX-style crisis at Boeing, or a prolonged Airbus production disruption, would flow through directly to SAM's top line with a lag of about six to nine months. And finally, the currency translation exposure—revenues increasingly in USD, costs partially in ringgit, baht, and Singapore dollars—introduces a volatility layer that can mask underlying operating performance quarter to quarter.

On the myth-versus-reality front, it is worth correcting a few pieces of consensus narrative that show up in retail investor discussions. The myth that SAM is "a play on Malaysia's tech boom" misses the point that SAM is really a play on two specific global industrial cycles that happen to transit through Malaysia. The myth that the company is "exposed to Chinese geopolitical risk" is nearly the opposite of the truth: SAM's footprint is precisely what Western OEMs are seeking in order to reduce such exposure. And the myth that "aerospace is a low-growth business" confuses the airframe manufacturing cycle with the engine component supply cycle, which behave quite differently in terms of growth and margin structure.

For investors tracking SAM's performance in real time, a small number of KPIs carry disproportionate signal value. Three in particular are worth watching closely. First, quarterly revenue split between the Aerospace and Equipment segments, because the mix shift will drive the company's risk profile and its valuation multiple over time. Second, capacity utilisation at the Thailand and expanded Penang facilities, which is the single best real-time indicator of whether the 2024 rights-issue-funded capex is being absorbed by demand at the expected pace. Third, the trajectory of the aerospace order book, specifically the LEAP-linked backlog and any new-program qualifications, because these are leading indicators of revenue that will not show up in the P&L for three to five years. Working capital intensity and the ratio of operating cash flow to reported EBITDA are secondary but important cross-checks; in a heavy precision engineering business, working capital can absorb a surprising amount of cash during ramp phases, and the quality-of-earnings signal from cash conversion is non-trivial.

One second-layer consideration worth flagging briefly: the 2024 rights issue, while accretive to long-term capacity, was modestly dilutive in the near term and will need to be earned back through incremental ROIC on the deployed capital. The parent company's participation in the issuance, at its pro-rata share, was a positive signal of alignment rather than cash-out. No auditor or going-concern signals have surfaced in recent filings. ESG considerations are largely neutral—aerospace has its own emissions footprint debates, but SAM sits upstream of that conversation as a component supplier—though investors focused on scope-3 categories should note that SAM's indirect exposure to aviation emissions is effectively the same as the rest of the Tier-1 supplier base.

VIII. The Narrative Conclusion: What Have We Learned?

Step back from the segment data, the acquisition multiples, the capacity expansion narratives, and the 7 Powers analysis, and the story of SAM Engineering reduces to a single, durable idea: complexity is a moat. The harder something is to make, the longer it takes to learn how to make it, and the more regulatory and reputational weight sits on the act of making it, the safer the business of making it becomes. This is not a novel observation—it is, in many ways, the central insight of the industrial investing tradition going back to Charlie Munger's observations about the cement industry and Warren Buffett's remarks about See's Candies—but it is an observation that rewards careful application.

SAM is the Asian industrial embodiment of this idea. The company does not sell anything glamorous. It does not own a consumer brand. Its end-products are invisible to the people who ultimately fly on the planes and use the devices built on the chips. And yet the specific combination of capabilities it has assembled—certification pedigree in aerospace, scale in semi-equipment, geography in Malaysia and Thailand, ownership by Temasek—is not easily replicable. Not by any number of ambitious new entrants, not by state-directed Chinese industrial policy, not by aggressive Western consolidators. It took forty years of quiet, incremental capability accumulation to build, and it would take something similar to dislodge.

The legacy dimension of the story is worth pausing on. In some real sense, SAM is the most sophisticated expression of Singaporean state-linked engineering prowess, dressed in a Malaysian corporate wrapper. It is what happens when a small, wealthy, technocratic city-state decides, over four decades, that it is going to build a sovereign-grade industrial capability in the most demanding supply chains in the world, and then methodically executes on that decision across cycles, governments, and CEO transitions. The fact that the outcome is listed on Bursa Malaysia rather than the Singapore Exchange is a historical accident of the reverse-takeover structure chosen in 2008. The fact that the talent, the capital, and the customer relationships are distributed across two countries is a feature of how the region's industrial geography has evolved in practice.

For the long-term fundamental investor, SAM presents one of the more interesting picks-and-shovels narratives in Asia-Pacific industrials. The travel boom that followed the end of the pandemic is still feeding the narrow-body production ramp, which still has years of backlog. The AI revolution is driving semiconductor capex at levels that were inconceivable five years ago, and that capex has to flow through physical precision-engineered tools built, in meaningful part, in places like Bayan Lepas. Sitting at the intersection of those two cycles, with a durable set of moats and a patient shareholder, is not a bad place to be.

None of this is to say the road forward is friction-free. Boeing's production issues, the cyclicality of the semi-equipment market, the currency exposure, the capex intensity, the customer concentration—all of these are real considerations, and all of them will show up in the quarterly data at various points over the next several years. Capital-intensive precision manufacturing is not a business that generates serene, monotonic earnings growth. It generates lumpy, program-driven, cycle-sensitive cash flows that require an investor temperament willing to look through noise.

But the central proposition—that SAM is in a structurally favoured position in two of the most important industrial supply chains of the 2020s and 2030s, that it is run by a competent and aligned management team, and that its moats are genuine rather than cosmetic—seems, on the evidence, to be on firm ground. The company's own 2024 decision to raise substantial capital and deploy it into Thailand and Penang expansion is the clearest possible signal that the people who know the business best are maximally bullish on the coming decade of demand for precision engineering.

It is hard, in a world saturated with narratives about disruption and platform economics, to get excited about a company that machines Inconel rings in Penang. But that, in a way, is exactly the point. The quiet businesses, the ones that sit in the physical middle of complex supply chains, the ones whose customers have no practical choice but to keep ordering—those businesses compound value in ways that rarely make the headlines but that, over twenty and thirty years, tend to deliver outcomes that the headline-grabbing names struggle to match. SAM is one of those businesses. The picks-and-shovels play for the travel boom and the AI revolution alike.

The story, like the supply chains it lives inside, is a long one. The chapter being written in the 2020s is just the latest of many. And if the patterns of the last four decades are any guide, the people sitting atop the Temasek pyramid, and the people inside the Penang factories, are writing the next chapter with the same patient, unflashy, precision-obsessed approach that got them here in the first place.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube