JD.com: China's Supply Chain Emperor

I. Introduction & Episode Roadmap

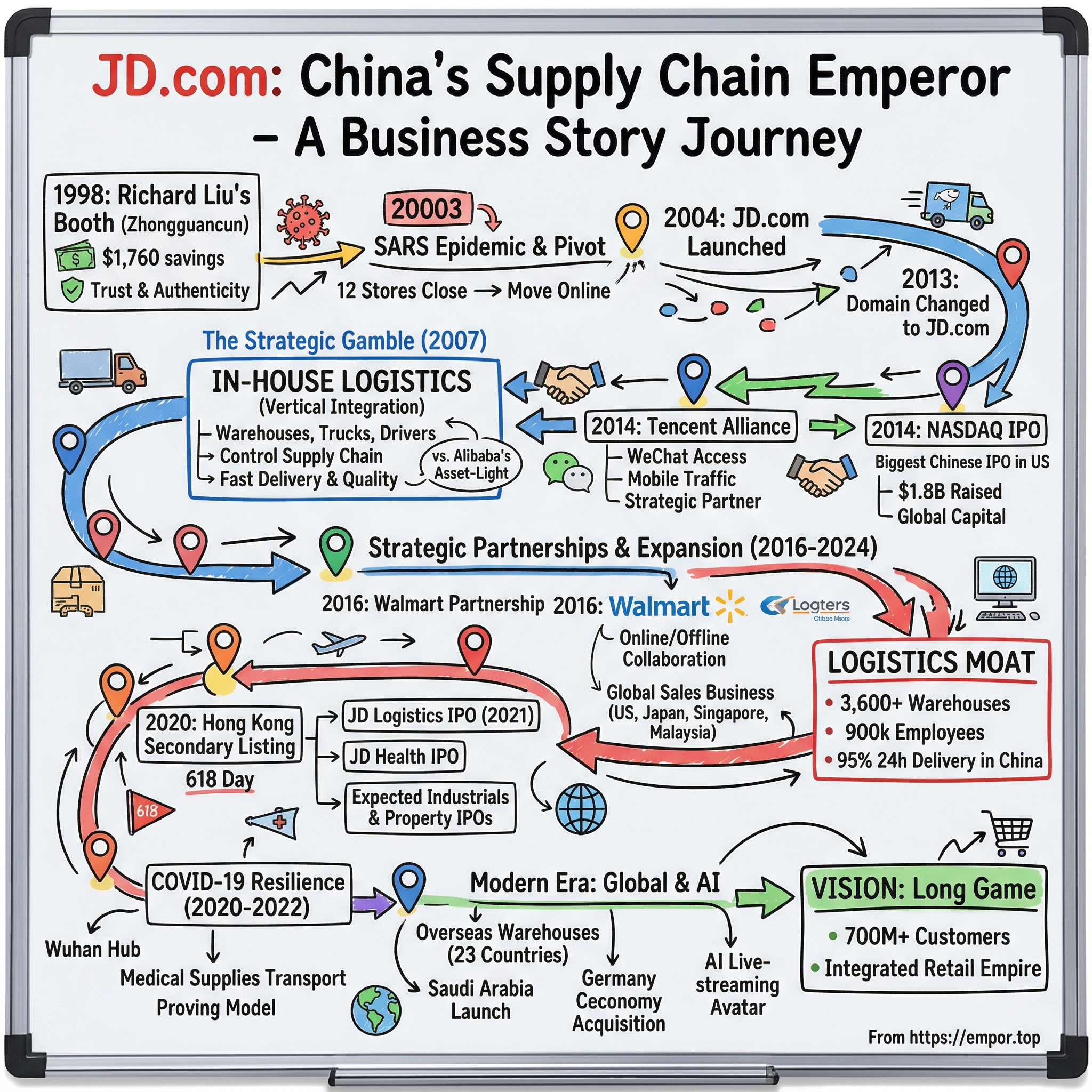

Picture this: A single 4-square-meter booth in Beijing's Zhongguancun electronics district, 1998. Inside stands a 25-year-old with $1,760 in savings and a radical idea—what if customers could trust an electronics retailer to never cheat them on price or sell them counterfeit goods? That young man was Richard Liu Qiangdong. Today, the company he founded generates more than $158 billion in annual revenue, employs nearly 900,000 people, operates over 3,600 warehouses, and ranks 44th on the Fortune Global 500.

JD.com is the largest retailer in China, a member of the NASDAQ100 and a Fortune Global 500 company.

The question at the heart of this story is simple yet profound: How did a poverty-stricken villager transform a tiny electronics stall into one of the world's most sophisticated supply chain operations—one that delivers over 90% of orders same-day or next-day to a population of 1.4 billion people?

The answer lies in a strategic gamble that nearly everyone thought was insane. While Alibaba's Jack Ma was building an asset-light marketplace that connected buyers and sellers without touching inventory, Richard Liu went in the opposite direction. Thanks to its substantial investment in tangible assets, JD has secured a unique stance that's hard to replicate. It's among the select global companies that can match or potentially exceed Amazon in aspects like supply chain efficiency, logistics technology, and vast infrastructure.

This is the story of the "anti-Alibaba" model—a vertically integrated retail empire built on warehouses, delivery trucks, and the radical premise that trust could be a competitive advantage in a market long plagued by counterfeits.

The article traces JD.com's journey through several key inflection points: the SARS epidemic that forced Liu online in 2003, the contrarian decision to build in-house logistics in 2007 when everyone said it would bankrupt the company, the transformative Tencent alliance of 2014, the record-breaking Nasdaq IPO, strategic partnerships with Walmart and Google, the COVID-19 pandemic that proved the model's resilience, and the company's current global expansion into Europe, the Middle East, and beyond.

For investors, JD.com presents a fascinating case study: a company with razor-thin margins that has somehow built one of the most defensible moats in global e-commerce. Let's dive in.

II. Richard Liu: The Hungry Entrepreneur

Born in 1973 in the small village of Chang'an outside Suqian in China's Jiangsu province, Richard Liu, the founder of JD, had humble beginnings. Growing up, his family lived in poverty and the entire village lacked basics such as running water and electricity. Liu recalls having pork, one of his favorite dishes, only once or twice a year. He aspired to become the village leader as a child and dreamed of providing pork more frequently to Chang'an residents.

It's a remarkably specific childhood dream—to become village leader so he could make sure his neighbors ate pork more often. But it reveals something essential about Liu's psychology: even as a child, he thought in terms of systems and scale. How do you solve hunger? Not by getting one family more food, but by changing the entire village's circumstances.

Liu Qiangdong was born on March 10, 1973, in Suqian, Jiangsu province. He graduated from primary school in the Jiangsu province and enrolled in the department of sociology in the Renmin University of China 1992. He graduated from Renmin University with a Bachelor of Laws with a major in sociology in 1996.

The choice of sociology was deliberate. Liu wanted to understand systems—how societies functioned, how institutions could be reformed, how ordinary people could improve their lives. Mr. Liu received his bachelor's degree in sociology from Renmin University of China in 1996 and an EMBA from China Europe International Business School in 2011.

After graduation, Liu's first entrepreneurial venture was a restaurant—and it was a disaster. He lost all his savings after employees allegedly stole from him. The failure taught him a painful lesson about trust and management that would later shape JD.com's employee-centric culture.

Following the restaurant failure, Liu worked at Japan Life, a health products company, for two years. It was tedious corporate work, but it allowed him to save 12,000 yuan—approximately $1,760 at the time. On June 18th, 1998, Liu took his 12,000 yuan (about $1,760) he had saved during his two years at Japan Life and used it to purchase inventory and rent a 4-square-meter booth in one of the many technological bazaars in Zhongguancun.

He possesses the characteristics of a hungry and driven entrepreneur with a grand vision. One of his most notable traits is his commitment to creating value for the entire JD ecosystem, including customers, suppliers, employees, partners, and investors. This approach has fostered a strong relationship with the Chinese government, as they both prioritize the benefit of society as a whole over individual companies.

What made Liu different from countless other booth operators in Zhongguancun? In an era when haggling was universal and counterfeit products were rampant, Liu made two revolutionary decisions. At the time Liu started his business, it was common for shops to overcharge customers and pass off counterfeit goods. Liu saw an opportunity to establish a new kind of business based on trust and honesty. His shop was the first in northwestern Beijing's Zhongguancun high-tech neighborhood to use price tags to avoid haggling with buyers.

Fixed prices and authentic products—concepts so basic they seem obvious today, but genuinely radical in 1990s China. Liu's booth didn't just sell magneto-optical drives; it sold something far more valuable: reliability.

In reference to Liu's ranking, Fortune remarked that Liu had "few of the trappings of a celebrity CEO" and little corporate ego. Liu is often invited to speak at some of the largest forums in the world such as the World Economic Forum in Davos on topics such as the ecommerce industry, and technological advancements, and to share his business development story as a means to inspire others, but even with this and working 16 hour days, he still spends one day a year working as a delivery person for JD.com.

That last detail—a billionaire spending one day each year making deliveries—speaks volumes about Liu's management philosophy. He never stopped thinking of himself as the guy running the 4-square-meter booth. The company he built would reflect that same scrappy, trust-obsessed mentality, only at continental scale.

Liu achieved his childhood dream of supporting his village by setting up JD's customer service center there, and he remains committed to its growth. The village also acts as the hub for JD's drone operations.

From a village without running water to a Fortune Global 500 company—and then using that company's technology to transform the very village where he grew up. It's the kind of arc that makes for great founder mythology, but it's also genuinely instructive about what drives Liu's decisions. This wasn't abstract empire-building; it was personal.

III. The Founding: A 4-Square-Meter Booth (1998-2003)

Zhongguancun in the late 1990s was China's version of Silicon Valley—if Silicon Valley were a sprawling, chaotic electronics bazaar where shouted negotiations echoed off warehouse walls and counterfeit merchandise mixed freely with legitimate goods. It was the place where ambitious young entrepreneurs went to make their fortunes, and it was absolutely cutthroat.

Calling the company Jingdong, this was the start of what would eventually become JD.com, and the date on which he opened up shop has become known as "618" day and accompanies a promotional blitz that has become a nationwide phenomenon rivaling the United States' Black Friday. Before all that though, he was simply a one-man booth selling magneto-optical drives, a type of optical disc drive similar in appearance to a floppy disk capable of having data written and rewritten upon it.

The choice of magneto-optical drives was strategic. These were specialized products—not the cheap knockoffs flooding the market, but authorized equipment for professionals who needed reliable data storage. Liu positioned himself not as a general electronics vendor, but as a specialist in authentic products.

In contrast to other dominant e-commerce brands in China that provide platforms for companies and consumers to sell directly to each other and leave the handling of goods to outside delivery companies, JD.com sources goods directly from suppliers and resells to shoppers. The practice allows JD to verify the authenticity of goods being sold and hence has increased consumer trust in China's e-commerce industry. Liu's focus on reliability helped JD.com grow into China's biggest Internet-based direct retailer. This is a powerful selling point for Chinese consumers who have endured repeated scandals over fake products.

The trust thesis was working. Liu's reputation spread through word-of-mouth, and customers began seeking him out specifically because they knew they wouldn't get cheated. In 1998, Liu set up Jing Dong Company in Beijing to sell electronic products. The company expanded to 12 chain stores in Beijing, Shanghai, and Shenyang by 2003, earning annual revenues of 60 million RMB.

By 2003, Liu had transformed his single booth into a legitimate retail chain. Twelve stores across three major cities, 60 million RMB in annual revenues—roughly $7.5 million at the time. For a company born from $1,760 in savings, this represented extraordinary growth.

But Liu was still running a traditional brick-and-mortar operation. The internet existed, of course, but e-commerce in China was primitive. Most consumers didn't trust online shopping—ironic, given that they didn't really trust physical retailers either. Liu had built his business on face-to-face trust, on customers being able to see him, talk to him, and hold the products in their hands.

Then came SARS.

IV. Inflection Point #1: SARS and the Pivot to E-Commerce (2003-2004)

In early 2003, a mysterious respiratory illness began spreading through southern China. By spring, SARS had exploded into a full-blown public health crisis. Cities locked down. Streets emptied. Fear of human contact became the defining emotion of daily life.

For Richard Liu, watching his 12 stores go silent, it felt like the end of everything he had built.

The SARS outbreak in 2003 kept staff and clients of Jingdong at home and forced Liu to rethink the business model and divert to online business. Due to the outbreak, Liu's business lost over 8 million yuan.

Eight million yuan—more than $1 million at the time—vanished as foot traffic disappeared. Liu's entire competitive advantage had been built on personal relationships and face-to-face trust. Now, faces were hidden behind masks, and trust seemed like a luxury nobody could afford.

In 2003, Richard Liu's business hit a snag when the SARS epidemic caused widespread fear and panic, with most consumers electing to stay home in order to avoid catching or spreading the virus.

Desperation breeds innovation. Liu began experimenting with an idea that seemed absurd: what if he could reach customers online? At the time, the internet was still a place people were wary of purchasing items from, but Liu's work building a trustworthy brand enabled him to get a head start in gaining the trust of the consumers. Nonetheless, he worked extremely hard to build JD.com into a premiere e-commerce service, launching JD.com in early 2004.

Liu launched his first online retail website in 2004, and founded JD.com (short form for Jingdong) later that year. In 2005, Liu closed off all brick-and-mortar stores and became an e-commerce business.

The decision to go all-in on e-commerce was audacious. Liu didn't just add an online channel; he shuttered all 12 physical stores and bet the entire company on the internet. In 2005, Chinese e-commerce was still in its infancy, plagued by fraud and logistics nightmares. Most rational observers would have called it suicide.

He elected to live in his office in order to save money on rent, and wrote the initial code for the website himself. He wanted to get to know his customers and their needs as closely as possible, and so he alone answered all of the customer inquiries that came through. In order to make sure no questions went very long unanswered, Liu would set an alarm clock for himself to go off every two hours during the night so that he could wake up and answer any questions that had been asked. He even handled much of the deliveries himself.

This is founder dedication taken to almost absurd extremes. Liu sleeping in his office, coding the website, answering customer questions at 2 AM, then waking up again at 4 AM to answer more questions, then personally delivering packages during the day. He wasn't just building a company; he was becoming the company.

In 2005, Liu received an offer to sell JD.com for 18 million yuan, which he rejected.

Eighteen million yuan—more than $2 million—for a barely-profitable e-commerce startup run by a guy sleeping in his office. Many founders would have taken the money and run. But Liu saw something that the buyer didn't: online retail in China wasn't a niche market; it was the future of all retail. And he intended to own it.

The SARS crisis had nearly destroyed JD.com. Instead, it created JD.com as we know it today—not a chain of electronics stores, but a pure e-commerce company positioned to ride China's internet revolution.

V. The Full-Category Expansion & Building the Moat (2007-2013)

By 2007, JD.com had proven the viability of online electronics retail in China. By 2007, sales revenue had reached 360 million RMB. That's approximately $45 million—a six-fold increase from the brick-and-mortar days.

But Liu was already thinking bigger. Much bigger.

In 2007, Liu employed a full-category strategy for JD.com, changing the company's business model from selling consumer electronics to large variety of goods.

The full-category strategy meant JD.com would no longer be just an electronics specialist. It would sell everything—apparel, books, groceries, appliances, beauty products, the works. In essence, Liu was declaring war on Alibaba's Taobao marketplace and positioning JD.com as China's answer to Amazon.

But here's where Liu made the decision that would define JD.com for the next two decades:

Unlike Alibaba's asset-light model, JingDong built a vertically integrated system. It purchases and warehouses inventory, operates its own fulfilment centres, and employs delivery staff. This has made JingDong synonymous with reliability and fast shipping. While capital intensive, it differentiated JD as a platform that could guarantee authenticity, in a market long plagued by counterfeits.

In 2007, JD.com established its in-house logistics department. The decision was met with near-universal skepticism. China already had third-party logistics companies. Why would an e-commerce platform take on the massive capital expense of building warehouses, buying trucks, and hiring drivers?

JD.com, on the other hand, adopted a merchant intermediary approach, prioritizing direct sales and meticulous control over its supply chain. By establishing its own logistics network in 2007, JD.com significantly improved delivery speed and quality control, reducing average inventory holding time from 50 days in 2011 to just 28 days by 2021.

The logic was simple, even if the execution was brutally difficult: if JD.com controlled the entire supply chain from warehouse to doorstep, it could guarantee what third-party logistics couldn't—speed, reliability, and authenticity. In a market where customers had been burned repeatedly by fake goods and delayed shipments, these guarantees were worth their weight in gold.

Liu insisted that JD build its own national logistics system to avoid losing or damaging items during delivery, and to provide good service to the "last mile." By the end of 2014, JD had established 3,210 delivery and pickup stations in 1,862 counties, two-thirds the total number of counties in China. In 2014, Amazon switched from using third-party logistics firms to making "last mile" deliveries itself, emulating JD's China model in the U.S. market.

That last detail is remarkable: Amazon, the company that invented modern e-commerce, looked at what JD.com was doing in China and decided to copy it. JD.com had built something that even the world's most advanced e-commerce company found worth emulating.

The rivalry between Alibaba and JD.com extends beyond market share—it represents two distinct business philosophies. Alibaba's ecosystem-driven approach connects consumers and merchants through data and services, while JD.com's vertically integrated model focuses on direct sales and supply chain control.

The history of these two companies shows the 'growth flywheel' that Bezos described in operation. Alibaba essentially works in the 'information intermediary' market whilst JD.com is more of a typical 'merchant intermediary'. It is this fundamental difference in their e-commerce business models which gave birth to their individual distinctive flywheel structures, and which has directly led to the rivalry between the two for nearly two decades.

By 2013, the contours of China's e-commerce war had become clear. Alibaba owned the marketplace model, connecting hundreds of millions of buyers with millions of sellers and taking a cut of every transaction. JD.com owned the integrated retail model, controlling everything from sourcing to delivery and accepting the thin margins that came with holding inventory.

The company changed its domain from 360buy.com to JD.com in 2013, signaling its ambition to become a global brand. Liu had transformed his 4-square-meter booth into China's largest online direct retailer. But the hardest challenges—and the biggest opportunities—still lay ahead.

VI. Inflection Point #2: The Tencent Alliance (2014)

By early 2014, JD.com faced a strategic problem. The company had built impressive logistics infrastructure and earned a reputation for authenticity, but it was fighting a two-front war: against Alibaba for e-commerce dominance and against irrelevance in the mobile era. China's consumers were rapidly shifting from desktop computers to smartphones, and Tencent's WeChat had become the center of digital life for hundreds of millions of people.

JD.com needed mobile traffic. Tencent needed e-commerce expertise.

Tencent first invested in JD.com in 2014, after retreating from its own e-commerce meant to compete with China's No 1 player in the market, Alibaba Group Holding, owner of the South China Morning Post. At the time, Tencent acquired a 15 per cent stake in JD, which took over the operations of Tencent's QQ Wangguo and PaiPai shopping platforms.

As part of the deal, JD will acquire Tencent's QQ Wanggou B2C and PaiPai C2C marketplace businesses and a minority stake in Yixun. It also has the right to acquire the remaining stake of Yixun in the future.

The deal was transformative. Tencent was essentially admitting defeat in e-commerce—its QQ Wanggou and PaiPai platforms had failed to gain meaningful market share against Alibaba—and betting that JD.com could succeed where Tencent had failed. In exchange, JD.com got something money couldn't buy: prominent positioning on WeChat, the app that China's consumers opened dozens of times per day.

That makes it a popular partner for any company that wants to counter Alibaba's growth. That's why Tencent bought a 15% stake in JD when it went public in 2014, and subsequently boosted that stake to nearly 20%. Tencent merged the data of its WeChat users with JD's customer shopping histories last year. The partnership let WeChat users buy products from JD, while JD used the data to make product suggestions and help merchants promote their products. JD also granted customers discounts at partnered brick-and-mortar retailers when they used WeChat Pay.

Tencent acquired a 15% stake in JD.com in 2014 by paying cash and handing over its e-commerce businesses Paipai & QQ Wanggou plus a stake in Yixun to JD.com, to build a stronger competitor to Alibaba Group Holding Ltd. In 2015, JD.com and Tencent announced the launch of the "Jingteng Plan" (Chinese: 京腾计划), a portmanteau of the two companies' names, which allows merchants to establish a brand and promote marketing effectiveness by linking JD.com consumption data with Tencent social data.

The "Jingteng Plan" represented something unprecedented in Chinese tech: two giants setting aside competitive instincts to focus on a common enemy. Alibaba had dominated by playing monopoly; JD and Tencent would compete by building an alliance.

JD.com, China's second largest e-commerce player, has extended its partnership with tech giant Tencent Holdings for three more years in a deal that will continue to give WeChat users easy access to the shopping platform, helping it maintain a unique advantage in driving online sales. The renewed cooperation will preserve short-cut access to JD.com on Tencent's dominant chat app, which has 1.29 billion monthly active users, as the companies continue to collaborate in marketing and advertising, technology services and other fields.

The WeChat integration was like having a retail store planted in the middle of every Chinese consumer's living room. JD.com suddenly had access to nearly a billion potential customers, all just a tap away from placing orders. For Alibaba, which had built its own ecosystem precisely to avoid dependence on external traffic sources, the Tencent-JD alliance represented an existential threat.

The companies' ties grew closer as competition with Alibaba intensified, leading to JD.com enjoying prominent positioning on WeChat.

The alliance proved durable. Even after Tencent distributed most of its JD.com shares to shareholders in 2021, the commercial partnership continued. Tencent was previously the largest shareholder in JD.com until December, when the social media giant offloaded US$16 billion worth of shares in the e-commerce company to distribute as a special dividend among investors. Tencent's stake in the company fell to 2.3 per cent from 17 per cent after the transfer.

The Tencent alliance taught JD.com a crucial lesson: in platform competition, you don't have to win alone. Sometimes the smartest strategy is finding partners who share your enemies.

VII. Inflection Point #3: The Nasdaq IPO & Going Global (2014)

The Tencent deal closed in March 2014. Just two months later, JD.com would enter the global capital markets with one of the most anticipated IPOs in years.

JD.com, China's largest online direct sales retailer and second largest B2C e-commerce company with more than $20 billion in gross merchandise volume (GMV), raised $1.8 billion by offering 93.7 million ADSs at $19, above the $16 to $18 range. JD.com raised 12% more proceeds than expected and, at its offer price, now commands a fully diluted market cap of $27.3 billion and an enterprise value of $22.6 billion.

Chinese e-commerce site JD.com went public in an initial offering on the Nasdaq Stock Market that raised $1.78 billion and claimed the title of biggest IPO in the US by a Chinese company, to date. "This moment belongs to every member of the JD.com family," JD CEO and founder Richard Liu said.

Online retailer JD.com raised $1.8 billion after pricing its IPO following the US close on Wednesday, the largest ever US stock market listing by a Chinese company. Its 93.7 million American Depository Receipt deal was priced at $19 per unit, exceeding expectations and surpassing the initial $16 to $18 range. Pre-greenshoe, the group offered 6.9% of its enlarged share capital with a split of 74% primary shares and 26% secondary shares. The institutional book is said to have closed 15 times oversubscribed.

Fifteen times oversubscribed. Investors couldn't get enough. The appetite for Chinese internet companies was insatiable, and JD.com—with its Amazon-like business model and massive growth trajectory—was precisely what they wanted.

Tencent, which has entered into a strategic partnership with JD.com, invested $1.3 billion in a concurrent private placement at the IPO price and now owns a 20% stake.

Not only was Thursday's listing the biggest IPO in the US by a Chinese company to date; it also gave the firm a foothold in the US market ahead of its much larger rival, Alibaba Holdings Group Ltd, China's No 1 e-commerce firm. Alibaba's IPO, expected to be held later this year, could exceed $20 billion, according to some estimates.

The timing was strategic. By going public before Alibaba, JD.com established itself as the primary alternative for investors who wanted exposure to Chinese e-commerce. When Alibaba's massive IPO finally arrived in September 2014, investors who wanted diversification naturally looked to JD.com.

JD.com, China's largest online direct sales company, broke new records for a Chinese company listing its shares in the U.S. On Wednesday evening, the company sold 93.7 million American depositary receipts for $19 each, raising $1.78 billion. The initial public offering values JD.com at about $26 billion.

The IPO transformed JD.com from a Chinese company to a global one. It had the capital to accelerate its logistics buildout, the credibility to attract top talent, and the currency to make acquisitions. In September 2024, JD.com launched its global sales business in the United States, Japan, Singapore, and Malaysia.

VIII. Inflection Point #4: The Walmart Partnership (2016-2024)

In June 2016, JD.com announced a partnership that sent shockwaves through global retail: Walmart, the world's largest company by revenue, was betting on JD.com to win China.

Bentonville, Arkansas and Beijing – June 20, 2016 – Walmart (NYSE:WMT), and JD.com (Nasdaq:JD), China's largest e-commerce company by revenue, today announced that they have formed a strategic alliance to better serve consumers across China through a powerful combination of e-commerce and retail. The agreement between the companies includes a wide range of business initiatives, covering both online and offline retail.

As part of the agreement, Walmart will receive 144,952,250 newly issued JD.com Class A ordinary shares, amounting to approximately 5 percent of total shares outstanding.

The partnership between the two companies began in 2016, when Walmart sold its Chinese online grocery store, Yihaodian, in return for a 5 percent stake in JD, as part of broader push to gain a foothold in China's rapidly growing online shopping market.

The deal was complex but elegant. Walmart handed over Yihaodian, its struggling Chinese e-commerce platform, in exchange for a stake in JD.com. Sam's Club opened a flagship store on JD.com. Walmart stores became pickup points for JD deliveries. The two companies shared data and coordinated supply chains.

That's why it sold Yihaodian to JD and initially took a 5% stake in the e-commerce leader. It subsequently doubled that stake to more than 10%. Over the years, Walmart and JD worked together to expand their delivery services.

The Walmart-JD.com marriage got a strong reception, with both stocks rallying on the news. By the end of that year, Walmart had increased its JD.com stake to 10%, and Walmart's sales on JD.com tripled one year after the partnership.

For eight years, the partnership thrived. But by 2024, circumstances had changed.

The partnership between the two companies began in 2016, when Walmart sold its Chinese online grocery store, Yihaodian, in return for a 5 percent stake in JD, as part of broader push to gain a foothold in China's rapidly growing online shopping market. Walmart had no equity stake in JD as of Aug 20, the Chinese firm said in a filing to the Hong Kong bourse last week. JD also said it is full of confidence in future cooperation between the two sides. Walmart said in a statement that JD has been a valued partner over the past eight years, and the US retailer was committed to a continued commercial relationship with the Chinese e-commerce giant. "This decision allows us to focus on our strong China operations for Walmart China and Sam's Club, and deploy capital toward other priorities," Walmart said.

On Aug. 21, Walmart formalized a divorce of sorts with its partner of eight years when it sold its 9.4% stake in JD.com. The timing of the separation coincides with the end of an eight-year non-compete agreement between the two in the massive Chinese e-commerce market. "This decision allows us to focus on our strong China operations for Walmart China and Sam's Club, and deploy capital toward other priorities," Walmart said after announcing the separation, adding it would continue its strategic partnership with JD.com. Walmart received about $3.6 billion from the sale.

Walmart's exit wasn't a repudiation of JD.com; it was a statement about Walmart's own evolution. Sam's Club also generates about half of its sales online in China -- it no longer needs to rely on JD or other Chinese e-commerce marketplaces to drive its digital sales. As a result, Walmart's sales in China grew at an impressive compound annual growth rate (CAGR) of 10% from fiscal 2019 to fiscal 2024. During the same period, Walmart's total revenue grew at a CAGR of 5%. Walmart raised about $3.7 billion in cash by liquidating its stake in JD, and it plans to reinvest a lot of cash into expanding Sam's Club across China.

The Walmart partnership had served its purpose. JD.com gained global retail expertise and supply chain best practices. Walmart gained a foothold in Chinese e-commerce during a critical growth period. Now, both companies were strong enough to go their separate ways—while maintaining the commercial relationship that continued to benefit both.

IX. Inflection Point #5: Hong Kong Secondary Listing & Spin-offs (2020-2025)

By 2020, JD.com faced a new strategic imperative. U.S.-China tensions were escalating, and Chinese companies listed on American exchanges faced unprecedented regulatory scrutiny. The solution: a secondary listing closer to home.

JD.com has issued 133,000,000 new Class A ordinary shares as part of its Hong Kong offering. The e-commerce giant said the gross proceeds will total approximately 30.05 billion Hong Kong dollars ($3.87 billion). The company plans to use the money raises to "invest in key supply chain based technology initiatives to further enhance customer experience while improving operating efficiency." "The supply chain based technologies can be applied to the Company's key business operations including retail, logistics, and customer engagement."

Published June 11, 2020 · Chinese e-commerce retailer JD.com has priced its shares at HK$226 each and raised about $3.87 billion (3.04 billion pounds) in its Hong Kong secondary listing. The float, the biggest in the city this year, comes as Chinese companies are putting off plans for U.S. listings as tensions between the world's top two economies rise, while those listed in New York are seeking to return to exchanges closer to home.

The timing—June 18, 2020—was no accident. It was "618 Day," the anniversary of JD.com's founding and the company's signature shopping festival. The symbolism was perfect: listing in Hong Kong on the same day the company was born.

JD is expected to begin trading in Hong Kong on June 18, the same day as the company's founding and the final day of its annual shopping blitz in China known as 618. JD is China's second largest e-commerce company behind rival Alibaba, according to research firm Emarketer. Both companies are fending off upstart Pinduoduo, which launched in 2015 and has become the third largest e-commerce player in the country. JD's Hong Kong listing comes as tensions between the United States and China are on the rise.

The Hong Kong listing was just the beginning. JD.com had built a sprawling conglomerate, and management believed the parts were worth more than the whole. A series of spin-offs would unlock that hidden value.

In 2021, JD Logistics, the supply chain management and logistics delivery arm of JD.com, raised HK$24.6 billion ($3.2 billion USD) for its initial public offering, which was the second-largest IPO in 2021. Shares rose by 18% on its first day of trading.

JD Logistics Inc. rose as much as 18% on its first day of trading after raising $3.2 billion in Hong Kong's second-largest initial public offering this year.

The JD Logistics IPO validated Liu's 2007 decision to build in-house logistics. The division that skeptics said would bankrupt the company was now worth tens of billions of dollars as a standalone business.

JD.com raised $3.2 billion through the Hong Kong IPO of JD Logistics in 2021.

Additional spin-offs followed: JD Health went public in Hong Kong. JD Industrials and JD Property filed for IPOs, though market conditions delayed their debuts. 2020-2021 – JD Health IPO. 2025-2026 – Expected IPOs of JD Industrials and JD Property.

The group led by founder and chairman Richard Liu aims to list Jingdong Industrials, an asset-light provider of industrial supply chain technology and services and a partner of the JD Logistics fulfilment network, according to the Sunday filing. The most recent prior application, submitted in March of this year, lapsed after six months, as did the ones filed in October 2024 and March 2023. Beijing-based JD.com intends to retain Jingdong Industrials as a subsidiary after the listing, with the parent group and entities owned by Liu as the controlling shareholders. JD.com currently holds a 78.84 percent stake in the unit.

The spin-off strategy served multiple purposes: it provided independent capital for each business unit, created currency for acquisitions, established transparent valuations, and gave investors the ability to choose which parts of the JD ecosystem they wanted to own.

X. The Logistics Moat: Building China's Amazon Fulfillment

To understand JD.com's competitive position, you have to understand its logistics network. This isn't a side business or a cost center—it's the core of everything the company does.

As of June 30, 2025, including cloud warehouses operated by third parties, JD Logistics manages over 3,600 warehouses, with a total area exceeding 34 million square meters. Its comprehensive service coverage spans nearly all regions, towns, and populations across China.

Thirty-four million square meters. That's roughly 366 million square feet of warehouse space—larger than the total footprint of many countries' entire logistics industries. And JD.com built this from scratch, starting with that first warehouse in 2007.

It operates over 3,600 warehouses and can deliver 95% of first-party orders within 24 hours in China.

Ninety-five percent same-day or next-day delivery in a country of 1.4 billion people spanning 3.7 million square miles. To put this in perspective: Amazon Prime's two-day delivery was considered revolutionary when it launched. JD.com delivers faster, to more people, across a larger geography.

As of June 30, 2025, JDL has operated over 130 bonded warehouses, direct mail warehouses, and overseas warehouses in total, with a total managed area exceeding 1.3 million square meters. Its overseas warehouses cover 23 countries and regions worldwide. Meanwhile, built upon its overseas warehouses, JDL has been further developing its global supply chain network that integrates overseas warehouse networks, international transit hubs, local transportation and distribution networks in overseas countries, and cross-border line-haul transportation networks.

Its workforce has grown from 100,000 to approximately 900,000 employees by Q1 2025, including delivery couriers, customer service teams, and other vital roles.

Nearly a million employees. JD.com isn't just an e-commerce company; it's one of China's largest employers. Those delivery drivers aren't gig workers—they're JD employees with benefits and job security, a deliberate choice that creates loyalty and consistency.

The automation investment has been equally impressive:

In the first half of 2025, the "Zhilang" system, an efficient intelligent warehousing solution independently developed by JDL, has entered into the stage of large-scale nationwide application. It has been deployed in various types of warehouses across key cities such as Beijing, Guangzhou, Chengdu, and Fuzhou, marking JDL's acceleration of intelligent advancement. The "Zhilang" system integrates core components such as handling robots, ladder-climbing robots, and stereoscopic racks, along with auxiliary facilities including automated storage and sorting workstations, as well as automated empty container return lines, which enables it to fully utilize the 12-meter clear height of warehouses to achieve high-density storage. The implementation of "Zhilang" has also significantly increased in-warehouse operational efficiency, allowing order sorting to be completed in as fast as seconds, even in warehouses with tens of thousands of SKUs.

The public debut, while falling short of analyst estimates, is a milestone for for JD Logistics as it shoots for a bigger slice of China's $2.3 trillion logistics market and eyes overseas expansion. The IPO "helps [JD.com] crystallize the value of its logistics arm, which it had invested in heavily for more than a decade," says Vey-Sern Ling, an analyst at Bloomberg Intelligence. JD.com has differentiated itself in China's fiercely competitive e-commerce space by creating an in-house distribution network that extends across the country. Owning more links in the delivery supply chain has given the online retailer an advantage over rivals—one that proved especially handy during the COVID-19 online shopping boom, when heightened demand overwhelmed other delivery networks.

The global expansion accelerated dramatically in 2024-2025:

In 2025, JD Logistics will complete a "2-3 Day Delivery" service circle. This will enable clients and consumers in 19 countries to enjoy fast logistics service through JD Logistics' more than 50 self-operated overseas warehouses. By that time, the total overseas warehouse floor area will achieve a 100% increase.

In particular, in June 2025, JDL launched its self-operated express delivery brand "JoyExpress" in Saudi Arabia, officially commencing local delivery operations. With this, JDL has established a comprehensive logistics network in Saudi Arabia, covering everything from warehousing and sorting to last-mile delivery, marking a further enhancement of JDL's localized operating capabilities for overseas business.

For investors evaluating JD.com's moat, the logistics network is the answer to almost every question. Why can JD.com guarantee product authenticity when competitors can't? Because JD controls the entire supply chain. Why can JD.com deliver faster than Alibaba? Because JD.com owns its own warehouses and delivery fleet. Why is this advantage sustainable? Because replicating this infrastructure would cost tens of billions of dollars and take a decade.

XI. COVID-19 and Proving the Model (2020-2022)

The COVID-19 pandemic was the ultimate stress test for JD.com's supply chain thesis. When China locked down in early 2020, most logistics networks collapsed under the strain. JD.com's did not.

It is worth mentioning that the regional distribution center (RDC) of JD.com for the entire central China region is located in Wuhan, the core city of COVID‐19 in China; therefore, it plays a critical role in the logistics network of JD.com.

JD.com's central distribution hub was located in Wuhan—the epicenter of the global pandemic. While other logistics providers shut down, JD.com kept moving.

JD Logistics transported 50 million medical supplies, and JD Health collaborated with over 13,000 offline pharmacies to provide 30-minute delivery service. JD's supply chain also helped 3,900 tons of agricultural products that risked becoming unsellable due to the coronavirus outbreak to be delivered to consumers nationwide.

JD donated 1.08 million facial masks and tens of thousands of medical supplies to Hubei Charity Federation and Wuhan Hospital at the start of the pandemic. From January 21 to March 31, JDL transported more than 70 million medical emergency supplies for free, with a total weight of more than 30,000 tons, and delivered more than 10,000 tons of medical emergency supplies and daily necessities from all over the world to Hubei Province. In addition, JDL sent nearly 30,000 pieces of luggage from the medical assistance teams in Hubei to more than 30 provinces across the country for free.

Cost per delivery for Chinese e-commerce giant JD.com reached an "all-time low" in the first quarter of 2020, due to the increased order volume caused by the pandemic and cost controls, according to CFO Sidney Huang on a Friday earnings call. "Another positive contribution to the fulfilled gross margin was from JD Logistics, where the productivity gains from higher-than-expected orders more than offset the additional cost from the operational disruption, higher wages and staff protective measures," said Huang. E-commerce's share of total retail sales in China jumped from 20.7% in 2019 to 23.6% in Q1 2020, according to JD.com, which cited the National Bureau of Statistics of China. Revenue for the company in Q1 was up 21% year over year and it expects another 20-30% year-over-year increase in Q2. In Q1, JD.com launched a fresh produce delivery service sourcing directly from farms and expanded the product range within its medical delivery business.

The pandemic permanently shifted consumer behavior toward online shopping, and JD.com was perfectly positioned to capture that shift. But the pandemic also triggered a leadership transition.

In April 2022, Lei Xu became CEO of JD.com, and Liu stepped into the role of chairman, continuing to focus on the company's long-term strategies. Sandy Ran Xu became CEO of JD.com in May 2023.

Richard Qiangdong Liu has been the chairman of our company since inception and served as our chief executive officer until April 2022. He founded JD.com in 2004 and has guided its development and growth since then.

The leadership transition reflected both Liu's desire to step back from day-to-day operations and the company's maturation into a professionally managed enterprise. In April 2022, Liu stepped down as CEO of JD.com, appointing Lei Xu as his successor, while he continued to serve as chairman. This transition reflects a broader trend among Chinese tech entrepreneurs amid regulatory changes. Despite stepping back from daily operations, Liu remains influential in the company's strategic decisions.

When Xu Lei departed after just one year, Sandy Ran Xu—previously the CFO—became CEO, marking the first time a woman held the top role at JD.com. The company was proving it could thrive under professional management while Liu focused on long-term strategy from the chairman's seat.

XII. The Modern Era: Global Expansion & AI (2023-2025)

By 2023, JD.com had conquered China. The question became: could it conquer the world?

In October 2023, JD.com began a 4-hour delivery service in Hong Kong. In September 2024, JD.com launched its global sales business in the United States, Japan, Singapore, and Malaysia. In July 2025, JD.com agreed to acquire German electronics retailer Ceconomy, parent of MediaMarkt, for US$2.5 billion (€2.2 billion).

The Ceconomy acquisition was the most aggressive move yet. JD.com today announced that it decided to make a voluntary public takeover offer, through a wholly-owned indirect subsidiary JINGDONG Holding Germany GmbH (the "Bidder"), to all shareholders of CECONOMY AG ("CECONOMY"), the parent company of leading European consumer electronics retailers MediaMarkt and Saturn, to acquire all issued and outstanding bearer shares in CECONOMY for a cash consideration of EUR 4.60 per share. The Bidder and CECONOMY have also signed an investment agreement regarding the Takeover Offer and their intended cooperation after completion of the Takeover Offer. CECONOMY is a European retail leader in the field of consumer electronics. Its main brands MediaMarkt and Saturn operate omni-channel retail businesses, combining strong e-commerce presence with more than 1,000 retail stores in 11 countries.

September 19, 2025 — Germany's Federal Cartel Office has officially approved the acquisition of a controlling stake in Ceconomy, the parent company of Europe's largest electronics retailer MediaMarkt/Saturn, by Chinese company JD.com. The transaction is valued at approximately €4 billion.

JD.com and Ceconomy make important commitments to the staff: there will be no layoffs, there will be no store closures, management will remain in place, the organizational structure will not change in the next five years, and the current consultation and participation model will be respected for the next three years.

The Ceconomy deal gave JD.com something it had never had before: physical retail presence in developed Western markets. MediaMarkt and Saturn's 1,000+ stores across Europe could become testing grounds for JD.com's supply chain expertise, potentially transforming European electronics retail the way JD.com had transformed Chinese retail.

Simultaneously, JD.com embraced AI with characteristic ambition:

The avatar of JD.com founder and chairman Richard Liu Qiangdong hosted two live-streaming sessions on the platform on April 16, 2024. Chinese e-commerce giant JD.com is ratcheting up the use of artificial intelligence (AI) on its platform, as the avatar of founder and chairman Richard Liu Qiangdong debuted as host of two live-streaming sessions on Tuesday. Liu's avatar, powered by JD.com's own ChatRhino large language model (LLM), not only succeeded in replicating the company founder's appearance, voice and accent, but also his known habit of waving his hands as he speaks. Still, the inaugural live-streaming sessions hosted by Liu's avatar were a success, as the two campaigns – each lasting less than an hour to promote consumer electronics devices and groceries – generated more than 20 million views combined.

During a groundbreaking livestream on April 16th, JD.com introduced an AI digital representative of its founder, Richard Liu (Qiangdong Liu), known as "procurement and sales manager Brother Dong." Liu's digital avatar appeared in JD Home Appliances and JD Supermarket's live-streaming rooms, attracting over 20 million views within the first hour and generating RMB 50 million in sales throughout the entire livestream.

The AI avatar wasn't just a gimmick—it represented JD.com's vision for the future of e-commerce. In a market where live-streaming has become central to online retail, AI-powered hosts could operate around the clock, never get tired, never make mistakes, and scale infinitely.

The purpose of these digital avatars is not to replace human talent but to enhance their capabilities. JD.com's analytics indicate that this strategy can boost order conversion rates by 30% during off-peak hours.

On November 13, 2025, JD.com released its Q3 2025 financial results, demonstrating a strong performance and healthy progress across our diverse business lines. Our cutting-edge supply chain capabilities continue to drive exceptional customer experiences and pioneering industry innovation, marked by a remarkable milestone: surpassing 700 million annual active customers by October.

Seven hundred million annual active customers. In a country of 1.4 billion people, JD.com now serves half the population.

XIII. Financial Performance & Investment Considerations

JD.com's recent financial results demonstrate the business model's power at scale:

Net revenues were RMB347.0 billion (US$147.5 billion) for the fourth quarter of 2024, an increase of 13.4% from the fourth quarter of 2023. Net revenues were RMB1,158.8 billion (US$158.8 billion) for the full year of 2024, an increase of 6.8% from the full year of 2023.

The approved annual cash dividend for 2024 is US$0.5 per ordinary share, or US$1.0 per ADS, totaling approximately US$1.5 billion. JD.com's net income attributable to ordinary shareholders grew by 71.1% to RMB41.4 billion (US$5.7 billion) for the full year 2024.

Net revenues increased to RMB301.1 billion (US$41.5 billion) by 15.8% for the first quarter of 2025 from RMB260.0 billion for the first quarter of 2024. Net product revenues increased by 16.2%, while net service revenues increased by 14.0% for the first quarter of 2025.

Net revenues were RMB356.7 billion (US$149.8 billion) for the second quarter of 2025, an increase of 22.4% from the second quarter of 2024.

The 22.4% year-over-year growth in Q2 2025 marked an acceleration—the company's highest growth rate in years. Revenue Growth: Total revenue reached RMB356.7 billion ($49.8 billion), up 22.4% year-on-year (YoY), exceeding expectations and marking the highest YoY growth rate in the recent three years.

Income from operations was RMB8.5 billion (US$1.2 billion) for the fourth quarter of 2024, compared to RMB2.0 billion for the fourth quarter of 2023. Operating margin was 2.4% for the fourth quarter of 2024, compared to 0.7% for the fourth quarter of 2023.

The Competitive Landscape

JD.com operates in an intensely competitive market:

While Alibaba's Taobao and Tmall, along with JD.com, continue to dominate China's e-commerce space, newer platforms like Pinduoduo are gaining significant ground. By mid-2023, Pinduoduo's market share had surged to 19 percent, up from 7.2 percent in 2019, according to Yinma Data Research. In comparison, Alibaba's Taobao and Tmall held a combined 44 percent, while JD.com had 24 percent. Other players, such as Douyin (leading the growth in live-streaming and short-video e-commerce) and Little Red Book, are also carving out strong niches.

PDD, which also owns Chinese discount shopping app Pinduoduo has a market-cap of about $208 billion, compared with Alibaba's $196 billion, according to LSEG data. JD.com is a distant third with a market-cap of $48 billion.

Pinduoduo, having temporarily overtaken Alibaba's market capitalisation in 2024, recalibrates its "thousand-billion support" plan to relieve merchant cost pressures after margin contraction linked to higher US tariffs. JD.com sustains double-digit revenue growth by leveraging premium fulfilment and first-party inventory control, positioning itself as the trusted choice for authentic goods.

Porter's Five Forces Analysis

Threat of New Entrants (Low): The capital requirements for replicating JD.com's logistics network are enormous—tens of billions of dollars and years of development. New entrants face regulatory barriers in China and lack the supplier relationships JD.com has cultivated over two decades.

Bargaining Power of Suppliers (Moderate): JD.com's scale gives it leverage with most suppliers, but the company depends on major brands (Apple, Samsung, etc.) for traffic-driving products. The direct retail model means JD.com bears inventory risk that pure marketplace operators avoid.

Bargaining Power of Buyers (High): Chinese consumers are notoriously price-sensitive and have multiple platform choices. Customer loyalty is achieved through service quality and trust rather than lock-in.

Threat of Substitutes (Moderate to High): Live-streaming commerce (Douyin, Kuaishou), social commerce (Pinduoduo), and direct-to-consumer sales from brands all represent alternatives to traditional e-commerce platforms.

Competitive Rivalry (High): The three-way battle between Alibaba, JD.com, and Pinduoduo keeps margins compressed across the industry. New entrants like Douyin add further pressure.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: JD.com's logistics network exhibits clear scale economies—as volume increases, fixed costs (warehouses, technology, management) spread across more orders, reducing per-unit costs. Huang said logistics is a business built on scale. "So, as we continue to grow in scale, our margin will naturally trend better."

Network Effects: Limited. Unlike pure marketplaces where more buyers attract more sellers (and vice versa), JD.com's direct retail model doesn't benefit from traditional network effects.

Counter-Positioning: JD.com's vertically integrated model represents classic counter-positioning against Alibaba. For Alibaba to match JD.com's service quality, it would have to abandon its asset-light marketplace model—destroying its margin structure in the process.

Switching Costs: Low for individual purchases, moderate for merchants who have integrated their systems with JD.com's backend.

Branding: Strong. JD.com's reputation for authenticity and fast delivery represents genuine brand power in a market scarred by counterfeit scandals.

Cornered Resource: JD.com's 3,600+ warehouses, proprietary logistics technology, and trained workforce represent a cornered resource that cannot be easily replicated.

Process Power: JD.com's supply chain management capabilities—from demand forecasting to inventory optimization to delivery routing—represent proprietary processes developed over nearly two decades.

Key Performance Indicators

For investors tracking JD.com, three KPIs matter most:

-

Quarterly Active Customers (QACs) and Shopping Frequency: This measures both reach and engagement. In addition, most of our product categories as well as key metrics such as our quarterly active users and shopping frequency saw strong double-digit growth year-on-year in Q4.

-

Inventory Turnover Days: This measures supply chain efficiency. Lower is better, and JD.com's approximately 28-day inventory turnover is among the best in global retail.

-

Fulfillment Cost as Percentage of Revenue: This measures logistics efficiency. As scale increases and automation advances, this ratio should decline. Fulfillment expenses, which primarily include procurement, warehousing, delivery, customer service and payment processing expenses, increased to RMB19.7 billion by 17.4% for the first quarter of 2025. Fulfillment expenses as a percentage of net revenues was 6.6% for the first quarter of 2025, compared to 6.5% for the first quarter of 2024.

Bull Case

- China's e-commerce market continues growing toward $3 trillion by 2028

- JD.com's logistics moat is widening, not narrowing, as automation and global expansion accelerate

- The Ceconomy acquisition opens vast European markets with minimal integration risk

- Government consumption stimulus programs benefit JD.com's categories (appliances, electronics)

- Undervaluation: JD.com trades at approximately 9x forward earnings versus Alibaba's higher multiples, despite stronger growth metrics

Bear Case

- Pinduoduo and Douyin are stealing market share, particularly among price-sensitive consumers

- Thin operating margins leave little room for error or competitive response

- Global expansion carries execution risk—European retail is notoriously difficult for outsiders

- Regulatory uncertainty in both China and the U.S. creates headline risk

- Key-man risk: Despite stepping back, Liu remains central to strategy and culture

Material Legal/Regulatory Considerations

JD.com faces ongoing regulatory scrutiny in both its home market and abroad. China's antitrust regime has already impacted Alibaba significantly; JD.com has so far avoided major penalties but remains subject to platform economy regulations. The dual-listing structure (Nasdaq and Hong Kong) provides some protection against single-market regulatory risks but also creates compliance complexity.

XIV. Conclusion: The Long Game

Richard Liu started with $1,760 and a 4-square-meter booth. Today, JD.com operates one of the world's most sophisticated supply chains, serves over 700 million annual active customers, and is expanding across Europe, the Middle East, and Asia.

The company's journey illustrates a profound truth about business strategy: sometimes the obvious path isn't the right one. When Liu decided to build in-house logistics in 2007, the obvious move was to outsource to third parties like everyone else. The obvious move was wrong.

JD.com bet that in a market defined by distrust, controlling the entire supply chain would create a sustainable competitive advantage. That bet has paid off spectacularly. The COVID-19 pandemic proved that when supply chains matter most, JD.com's matters more than anyone else's.

The question for investors is whether this advantage can be sustained and extended. JD.com's global expansion represents both enormous opportunity and significant risk. The Ceconomy acquisition, if successful, could make JD.com a genuine global retail power. If it fails, it will have diverted billions of dollars from a market where JD.com already has a winning formula.

What's clear is that JD.com has built something remarkable: a vertically integrated retail empire that combines the best elements of Amazon (logistics and reliability) with deep understanding of Chinese consumers. The 4-square-meter booth has become a continental-scale logistics network serving half a billion people.

The hungry entrepreneur from Chang'an village now leads one of the world's largest retailers. He's provided pork—and much more—to millions of families who once couldn't afford such luxuries. Some childhood dreams, it turns out, can scale.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube