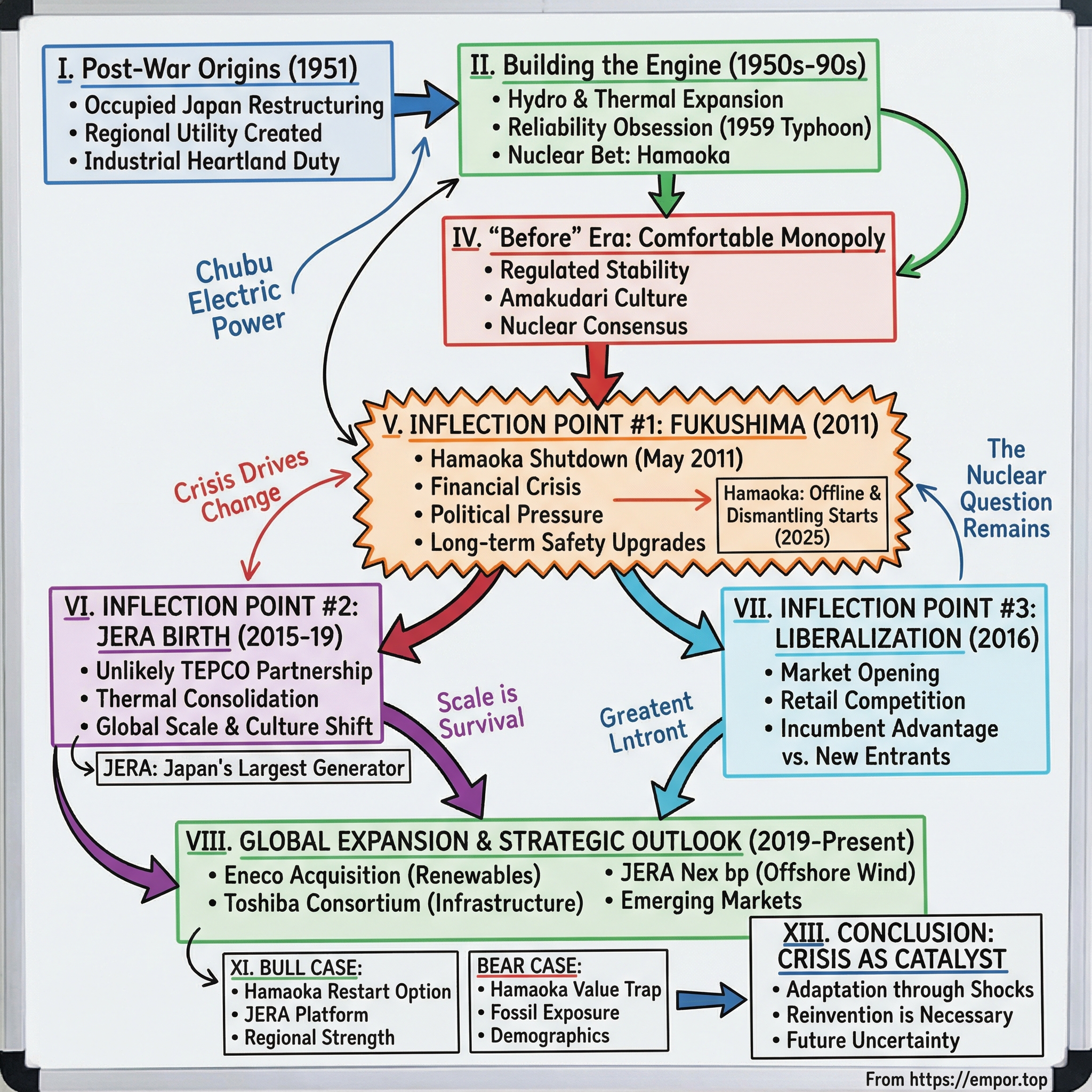

Chubu Electric Power: Japan's Post-War Energy Titan and the Fukushima Pivot

I. Introduction: The Utility Born from Occupation

Picture a boardroom in Nagoya in May 2011. Japan was still reeling from the earthquake and tsunami that triggered the Fukushima Daiichi disaster. And inside Chubu Electric Power, the question on the table wasn’t about quarterly performance or next year’s capex plan.

It was about whether to turn off Hamaoka.

Prime Minister Naoto Kan had personally asked Chubu to shut down the Hamaoka Nuclear Power Plant—not because it had suffered damage, but because of where it sat: in an area experts believed was uniquely exposed to a major quake. The government’s concern was blunt. With an estimated 87% probability of a magnitude 8.0-class earthquake in the region over the next thirty years, Hamaoka wasn’t just another nuclear plant. It was a national flashpoint.

On May 9, 2011, Chubu Electric agreed to comply. And in one stroke, the company accepted the loss of roughly one-fifth of its generating capacity. That single decision kicked off a chain reaction: an immediate scramble to replace power, a rethinking of what the company could be without its nuclear backbone, and—eventually—the creation of one of the most consequential partnerships in Japan’s energy industry. Chubu would go from a comfortable regional monopoly to a company forced to compete, improvise, and expand.

On paper, Chubu Electric is straightforward: Japan’s third-largest electric utility by generation capacity, electricity sold, and annual revenue. In Nagoya, it’s one of the city’s “four influential companies,” alongside Meitetsu, Matsuzakaya, and Toho Gas. It serves more than 16 million customers across about 39,000 square kilometers in central Japan—Aichi, Gifu, Mie, and Nagano, plus the western side of Shizuoka. The name says it all: Chubu means “central.”

But the numbers aren’t the point. The real story is the arc. Chubu Electric was literally created by post-war restructuring under U.S. occupation. It grew up inside a highly managed system built for stability, not risk-taking. And then, in the span of a few years, the ground shifted beneath it—first by disaster, then by politics, then by market reform—until reinvention stopped being an option and became the job.

That’s the question driving this story: how did a utility born from post-war occupation-era design become a global energy player, largely because crisis left it no other choice?

Along the way, we’ll hit the big themes that show up whenever a protected, capital-intensive industry gets shaken awake: what monopoly comfort does to organizational culture; how disaster forces change faster than any strategic plan ever could; how rivals become partners when survival is at stake; and the permanent, unresolved nuclear question—an asset that can be priceless in one decade and politically unusable in the next.

II. Post-War Origins: Born from Occupation

It’s 1951. Japan is still, technically, under U.S. occupation. The country is rebuilding its economy, its institutions, and its sense of itself. And one of the most consequential rebuilds of all is happening in an industry most people never think about until it fails: electricity.

That year, nine private electric utilities are created at once. Not because a set of founders saw an opening in the market, but because the occupation authorities did. The goal was straightforward and deeply political: restore industrial capacity, but prevent the kind of concentrated economic power that had supported wartime militarism.

Chubu Electric Power is established in May 1951—one of those nine, formed as part of the postwar restructuring of Japan’s energy industry.

The system the occupation government helped design is a kind of engineered compromise. These utilities are private companies, but they operate as part of a national machine. With the exception of Okinawa, their power systems are interconnected so electricity can flow where it’s needed for stability and efficiency. And because electricity is treated as a public necessity, key decisions—especially rates—sit under the supervision of the Ministry of International Trade and Industry, MITI.

Chubu’s territory is central Japan: Aichi, Gifu, Mie, Nagano, and the part of Shizuoka west of the Fuji River. At launch, it has shareholders’ equity of ¥29.4 billion and generating capacity of 1.03 million kW.

And Chubu gets something else, too: geography.

Inland, the Japanese Alps rise to roughly 3,000 meters. The rivers that cut down those mountains create an unusually reliable source of hydroelectric power—an advantage that will matter for decades. The region itself becomes one of Japan’s industrial cores, ultimately accounting for about 20% of the country’s industrial output.

This isn’t just a local utility serving households. Chubu Electric is being positioned as the power source for a manufacturing heartland—one that would go on to include Toyota and a dense ecosystem of suppliers and factories. If Japanese manufacturing surged, Chubu would have to surge with it.

But Chubu’s starting point is shakier than the headline capacity suggests. Almost immediately, it becomes clear the inherited equipment is old enough that the “real” usable output is far lower—closer to 600,000 to 700,000 kW. Then the Korean War hits, and demand spikes as Japan becomes a rear base for U.S. forces.

The war’s outbreak in 1950 changes Japan’s trajectory overnight: from defeated nation to strategic industrial partner. Factories roar back to life. And Chubu is suddenly responsible for powering that revival with an electrical system that, in practical terms, can’t keep up.

What comes next sets the template for the company’s identity: huge investment, often supported by government-backed financing, executed with discipline—and a culture built around one obsession above all else: reliability.

III. Building the Engine: 1950s–1990s

Chubu’s response to the early capacity crunch was classic utility triage: reduce demand today, build supply for tomorrow.

On the demand side, it ran a public campaign urging customers to save electricity. On the supply side, it started pouring concrete. First came the Hiraoka hydroelectric plant in 1952, then the Oigawa hydroelectric plant, followed by coal-fired additions at Mie and Shin-Nagoya. By the latter half of the 1950s, the panic eased. Supply and demand finally met.

But balancing the grid wasn’t just an engineering problem. It was a financing problem.

Over a decade, Chubu spent ¥210 billion expanding generating capacity—an enormous commitment for the era. Much of that money came from the Japan Development Bank, a government-backed lender designed to funnel capital into industries deemed essential to Japan’s recovery. Foreign capital helped too, reflecting how closely Japan’s reconstruction—and its power supply—was tied to the postwar global order.

Then, in 1959, the company got a brutal lesson in what “reliability” really means.

In September, a typhoon tore through Chubu’s service area. One power plant was badly damaged. Another, on the coast, was flooded and stayed underwater for months. Chubu’s response was immediate and total. Under the slogan, “Electric power is the generator of recovery,” it mobilized an all-out restoration effort—work that earned the company an award from the Disaster Committee Headquarters, the only one given to a private-sector company.

Inside Chubu, this moment hardened into something like doctrine: the utility’s job wasn’t just to deliver kilowatt-hours. It was to be there when everything else wasn’t. Decades later, when executives talked about their “unchanging mission” of stable supply, it wasn’t corporate poetry. It was institutional memory.

From there, the story settles into the rhythm of Japan’s postwar miracle. Through the 1960s, 70s, and 80s, Chubu expanded capacity under regulated, rate-of-return economics. It leaned more heavily on thermal generation and, like the rest of the country, grew increasingly dependent on imported fuel.

The generation mix shifted accordingly. Chubu built out a large thermal fleet—11 separate thermal power stations totaling 23,969 MW. Major facilities like the Kawagoe Power Station, a natural gas combined-cycle plant with 4,802 MW of capacity, and the Chita Thermal Power Station became the industrial backbone of the region.

And then came nuclear.

Chubu’s nuclear bet took shape at the Hamaoka Nuclear Power Plant on Japan’s Pacific coast in Shizuoka Prefecture. In hindsight, the location would become infamous: it sat above a major subduction zone. But in the 1970s and 80s, with Japan importing more than 90% of its energy, nuclear looked less like a gamble and more like strategy—an essential pillar of national security, and a way to power an industrial economy without being held hostage by global fuel markets.

IV. The "Before" Era: Comfortable Monopoly Culture

To understand what Chubu Electric became after 2011, you first have to understand what it was before 2011: a regulated regional monopoly, operating inside a system that was intentionally built to minimize competition.

For decades, Japan’s electricity business was effectively carved into territories. Ten vertically integrated utilities—often called the former regional utilities—each controlled generation, transmission, distribution, and retail inside their home region. Prices weren’t whatever the market would bear. Rate hikes required government approval, and after reforms in the 1990s, rate cuts generally didn’t.

This setup did exactly what it was supposed to do: it produced stable power, stable returns, and stable institutions. It also produced a very specific kind of corporate reflex. One JERA executive later described it with unusual bluntness: "Electric companies have many talented people, but their long history in a regulated industry responsible for the stable supply of electricity, combined with negative aspects of the seniority and lifetime employment systems, has definitely resulted in a tendency toward stability—a fear of failure and an aversion to taking on big challenges."

And to be fair, the results were hard to argue with.

Chubu Electric built a reputation for reliability that borders on obsessive. From 2001 to 2023, it averaged about 0.12 outages per customer per year, based on the System Average Interruption Frequency Index (SAIFI). In a service area that lives with earthquakes and typhoons as a fact of life, keeping outage frequency consistently below 0.2 per household—even through severe weather—is a real operational achievement.

That number is also a clue to the deeper story. Reliability at that level doesn’t happen by accident. It comes from redundancy, maintenance discipline, and constant infrastructure spending. Japan’s geography should make dependable power delivery brutally hard; the regional utilities made it feel routine.

But that’s where the trap snaps shut: when stability becomes the product, stability becomes the culture.

By the early 2000s, Japan’s utilities looked like the definition of comfortable monopolies—profitable, predictable, slow to change, and tightly entwined with regulators. The closeness had a name: amakudari, literally “descent from heaven,” the long-running practice of senior bureaucrats retiring into executive or advisory roles at the very companies they once oversaw.

Nuclear power fit neatly into this world. Japan began generating electricity from nuclear energy in 1966, and by the time Fukushima happened, nuclear provided roughly a third of the country’s power. After the nationwide shutdown that followed the accident, the share eventually returned—but only to 9.9% by 2024.

Chubu was fully bought into the nuclear consensus. In early 2011—just weeks before the earthquake—it even announced plans to build a new 3,000 to 4,000 MW nuclear plant by 2030.

Then March 11, 2011 arrived.

V. Inflection Point #1: Fukushima and the Hamaoka Shutdown (2011)

On March 11, 2011, Japan’s energy system met a kind of failure it hadn’t planned for.

At 2:46 p.m. local time, a magnitude 9.0 earthquake—the strongest ever recorded in Japan—struck off the coast of Tōhoku. Then came the tsunami. At Fukushima Daiichi, waves around 14 to 15 meters high overwhelmed the site, knocking out grid power and crippling backup systems that were supposed to keep the reactors safe when everything else went wrong.

Everything else went wrong.

Three of the plant’s six reactors suffered core melts in the first days. The accident was later rated Level 7, placing it in the same category as Chernobyl and making it the second-worst nuclear accident in the history of commercial nuclear power. The human tragedy was immediate and enormous: roughly 20,000 people were killed or went missing from the earthquake and tsunami, and about 120,000 people were evacuated due to radiation risk.

The immediate corporate casualty was TEPCO, which would require a government bailout and restructuring. But the deeper shockwave hit every utility in Japan. For Chubu Electric, Fukushima didn’t just change public sentiment. It rewrote the rules of what could be operated, where, and under what political conditions.

Why Hamaoka Was Different—and Vulnerable

Hamaoka’s problem wasn’t that it had failed. It was that it sat in the wrong place.

The plant was built near a subduction zone at the junction of tectonic plates, in a region long associated with the risk of a major Tōkai earthquake. Even before Hamaoka was approved, researchers and official earthquake-prediction bodies had flagged the possibility of a large, shallow quake in the area. In 2004, Professor Katsuhiko Ishibashi, a former member of a government panel on nuclear reactor safety, went further—calling Hamaoka “considered to be the most dangerous nuclear power plant in Japan.”

For decades, those warnings hadn’t been enough to overcome the national nuclear consensus. The economics, the energy-security logic, and the institutional inertia all pointed in the same direction: keep running.

Fukushima broke that alignment.

After the disaster, the estimated likelihood of a magnitude 8.0-class earthquake hitting the area within 30 years—87%—became impossible to ignore. On May 6, 2011, Prime Minister Naoto Kan requested that Chubu shut Hamaoka down to avoid a repeat of Fukushima.

Kan’s request came with conditions that were as much political as technical: Chubu was told to develop and implement mid-to-long-term plans to ensure the reactors could withstand the projected Tōkai earthquake and any triggered tsunami, and to keep the reactors out of operation until those measures were in place.

The pressure was intense. So was the backlash. The Yomiuri Shimbun criticized Kan’s move as “abrupt,” pointing to the blow it would deal to Chubu Electric’s shareholders.

But Chubu complied. Units 4 and 5 were shut down in mid-May 2011. Hamaoka went dark—and with it, a pillar of Chubu’s generation portfolio.

The Immediate Financial Crisis

Turning off a nuclear plant doesn’t turn off demand. It just forces you to replace the electricity—fast—and, in Japan’s post-Fukushima reality, that meant fossil fuels.

In June 2011, Chubu Electric received a ¥100 billion loan from the Development Bank of Japan to finance natural gas purchases to make up the shortfall caused by the Hamaoka shutdown. This wasn’t a growth investment. It was emergency oxygen—money to buy fuel, right now, because the grid doesn’t wait for anyone’s balance sheet.

And fuel was only the first bill.

To have any chance at restarting Hamaoka, Chubu had to rebuild its defenses for a post-Fukushima standard of safety. Between 2011 and 2013, breakwater walls roughly in the 18-to-20 meter range were constructed around the plant, part of a broader package that grew over time. The measures expanded to include an even higher seawall—eventually raised to 22 meters—along with waterproofing seawater pumps, installing additional water pumps in building basements, and a long list of other upgrades aimed at withstanding extreme earthquakes and tsunamis.

Units 3, 4, and 5 entered a long-term shutdown. From 2011 to 2017, they underwent significant safety upgrades designed to harden the plant against the kinds of compound disasters Fukushima made terrifyingly real.

In 2014, Chubu submitted an application to resume power generation. But the review by the Nuclear Regulation Authority moved slowly—and was still ongoing as of 2024.

More than a decade after the decision that opened this story, Hamaoka remained offline. And then came a milestone that underscored how permanent “temporary” can become in nuclear: on March 17, 2025, dismantling work began on Hamaoka’s Number 2 Reactor—the first operation of its kind in Japan.

There’s a harsh lesson here, and it isn’t about engineering. It’s about permission.

Hamaoka’s reactors weren’t shut because they broke. They became politically unacceptable in the wake of Fukushima, and in a regulated industry that serves the public by mandate, that can be the difference between a world-class asset and a stranded one.

VI. Inflection Point #2: The Birth of JERA — Sleeping with the Enemy (2015-2019)

If Fukushima was the shock, JERA was the counterpunch—one of the most improbable corporate marriages in modern Japanese industry.

JERA was born in the aftermath of the Great East Japan Earthquake, as a joint venture between Tokyo Electric Power Company (TEPCO) and Chubu Electric. After Fukushima, the old assumptions started to crack. As one account put it: “There were people at Chubu and TEPCO who questioned this trend, however, and the Fukushima Daiichi Nuclear Power Plant disaster in March 2011 brought them to the forefront.”

To grasp why JERA mattered, you have to appreciate how unnatural it was. TEPCO and Chubu weren’t competitors in the usual sense—Japan’s regional utility system meant they didn’t fight head-to-head. But they also didn’t collaborate. Each utility operated like a self-contained kingdom, protective of its territory, its assets, and its autonomy.

Then Fukushima rewired the incentives. Nuclear plants across Japan went offline. Thermal generation became the default. Fuel procurement suddenly became existential. And scale—real scale—started to look less like a luxury and more like survival.

The idea that eventually became JERA crystallized inside TEPCO. Yukio Kani, one of the project’s architects and later JERA’s CEO, described how the crisis created space for plans that would have been politically impossible before. His proposal was sweeping: separate out resource development, fuel procurement, transport, and thermal power generation, modernize an aging thermal fleet, and build a platform that could compete globally across the value chain. The logic was simple: if Japan was going to depend on thermal power for the long haul, the companies that bought the fuel and ran the plants needed to stop doing it piecemeal.

The Creative Workaround

Even with the logic, there was a problem: Japan’s unwritten rules.

The postwar system didn’t just discourage competition between regional utilities—it made it culturally and politically radioactive. And yet Chubu could see demand just over the border. It had been getting inquiries from industrial customers in the Kanto region, frustrated by TEPCO’s rising rates. Chubu wanted in. But marching into TEPCO territory to build plants and directly serve those customers wasn’t how the game was played.

So Chubu tried something clever and awkward at the same time. It proposed building a coal-fired unit on the grounds of TEPCO’s Hitachi-Naka Thermal Power Station, with TEPCO selling the electricity on Chubu’s behalf.

That workaround did what it needed to do: it created a reason to talk. And those talks quickly expanded from “how do we do this one project” to “what if we did all of it together?”

In April 2015, JERA launched as a 50-50 joint venture between TEPCO Fuel & Power (a wholly owned TEPCO subsidiary) and Chubu Electric. The new company took over ownership and operation of the parents’ thermal power stations—creating a combined fleet of about 67 GW, including capacity under construction. Overnight, JERA became Japan’s largest power generation company.

That number isn’t trivia. It meant JERA controlled a huge share of the country’s thermal generation capacity—enough to reshape procurement leverage, operating economics, and ultimately Japan’s post-Fukushima energy reality.

The Phased Integration

This wasn’t a one-day merger. It was a careful, step-by-step integration designed to reduce execution risk and survive regulatory scrutiny.

JERA started where the payoff was immediate: upstream resource development and fuel procurement, plus the planning process for new thermal plants and for retiring obsolete ones, both in Japan and internationally. The plan was explicit from the beginning: unify the value chain first where coordination mattered most, then broaden the scope—bringing in existing upstream assets, fuel contracts, and overseas power businesses.

The integration deepened in the years that followed. In 2017, the companies signed an agreement to integrate their fossil fuel power plants under JERA, and the Fair Trade Commission approved the plan later that year. By 2019, the transfer was essentially complete: Chubu moved its entire thermal power generation business, including coal assets, into JERA.

By then, JERA described the transfer as completing “unification of the full value chain from upstream fuel business and procurement through power generation and wholesaling of electricity/gas.” It held tens of gigawatts of fossil fuel generation across dozens of sites, not just in Japan but internationally too, and set its sights on expanding further.

The Unique Corporate Culture

Scale was only half the story. The other half was culture.

JERA was intentionally designed to feel different from its parents. Its board included multiple non-Japanese outside directors—rare in Japan’s electric power sector. Executives brought in experience from power and trading companies outside Japan. The point wasn’t window dressing. It was a deliberate attempt to break the monoculture of the old regional utilities and build an organization capable of competing globally.

One executive captured the contradiction perfectly by calling JERA “a hulking start-up.” Asset-heavy and enormous, but trying to act fast, hire differently, and take risks that the traditional utility model was never built for.

For Chubu Electric, the twist is almost poetic. The Hamaoka shutdown had forced it deeper into thermal power at exactly the moment thermal fuel became expensive and strategically fraught. JERA turned that vulnerability into leverage: instead of being a regional utility scrambling for LNG, Chubu became co-owner of Japan’s dominant thermal generation and fuel-procurement platform.

A crisis that started in March 2011 didn’t just change how Chubu generated electricity. Within less than a decade, it changed who Chubu could be.

VII. Inflection Point #3: Japan's Electricity Market Liberalization (2016)

If Fukushima forced Japan’s utilities to rethink how they generated power, liberalization forced them to rethink what they were.

On April 1, 2016, amendments to the Electricity Business Act took effect, opening Japan’s retail electricity market to competition. For the first time, every customer—including households and small businesses—could choose a provider and a plan from any registered electricity retailer. This was the second stage of reforms set in motion after 2011, aimed at bringing in new entrants and, with them, downward pressure on prices.

In practical terms, it meant something simple but radical: Japanese consumers went from having one default electricity company in their region to having hundreds of options.

The opening was enormous in scale—one of the biggest electricity-market reforms in Asia. Japan wasn’t just tweaking rules around the edges; it was trying to unwind a postwar system designed around regional monopolies and stability.

But once the market was “open,” the real world didn’t behave like the theory.

The Paradox of "Deregulation"

Japan’s retail market was liberalized, but not flattened.

The ten regional utilities—the same legacy companies born out of the 1951 restructuring—still controlled roughly 80% of the market. Meanwhile, hundreds of new retailers fought over the remaining slice.

By September 2016, more than 340 retailers had registered. Yet switching lagged far behind the flood of new brands. According to OCCTO, the cross-regional grid coordinator created as part of the reforms, about 1.675 million households had changed providers by that point—a meaningful number, but nowhere near the stampede you’d expect from a newly competitive market.

Part of that was cultural. Japan’s electricity system worked. When outages are rare and service is reliable, “better” is hard to define—and the downside of choosing wrong feels bigger than the upside of saving a little. If the lights always stay on, why gamble on an unfamiliar company?

Then the stress test arrived.

In January 2021, spot power prices surged. In 2022, Russia’s invasion of Ukraine drove global fuel prices higher, and Japan’s wholesale power prices stayed elevated for more than a year. That environment was brutal for many new retailers. Without their own generation assets or long-term fuel contracts, they were exposed to wholesale volatility; when prices spiked, margins didn’t just compress—they disappeared.

Teikoku Databank later found that by March 2024, dozens of the 706 new electricity providers had gone bankrupt or shut down, with many more exiting the market or suspending new contracts. And as weaker players stumbled, customers drifted back toward the incumbents.

The irony was sharp: deregulation created competition, but volatility rewarded scale and integration—the exact advantages the old regional utilities already had.

For Chubu Electric, the new rules cut both ways. Liberalization was a threat because customers could now leave. But it was also an opening, because Chubu could finally pursue customers beyond its home region without relying on creative workarounds.

It had started positioning early. In August 2013, Chubu announced it would acquire an 80% stake in Diamond Corp, a Tokyo-based electricity supplier—its first real foothold in the Kanto market, long treated as TEPCO’s home turf.

And with JERA now handling the thermal backbone, Chubu wasn’t just defending its territory anymore. It was preparing to play offense.

VIII. Global Expansion & Strategic Investments (2019-Present)

By the late 2010s, Chubu Electric had done the hard part at home: it had stabilized around a new reality where nuclear was uncertain, thermal was consolidated into JERA, and retail competition was now permanent. The next question was what to do with the company’s balance sheet, capabilities, and ambition when the old regional-utility playbook no longer defined the ceiling.

After 2019, the answer became clearer: go global, place bets on the energy transition, and buy options in the technologies and partners likely to matter next.

The Eneco Acquisition

In November 2019, a consortium of Mitsubishi (80%) and Chubu Electric (20%) acquired Dutch utility Eneco for €4.1bn ($4.5bn), a deal value often described as roughly 500 billion yen.

Eneco wasn’t a legacy fossil-heavy utility being dragged into renewables. It was already an integrated energy company leaning into renewable generation, and it had built a customer-facing retail business around helping consumers use energy more sustainably and intelligently.

For Chubu, that distinction mattered. This wasn’t a distressed rescue or a restructure. It was a premium-priced foothold in European renewables and modern retail energy—capabilities Japan’s incumbent utilities historically didn’t need to develop, because they didn’t have to compete for customers.

Eneco, owned by 44 Dutch municipalities, entered a privatization process in December 2018. In 2019, it generated 11.3 TWh of electricity and delivered energy across multiple products: power, gas, and heat. In other words, it wasn’t a single-asset renewables developer. It was a full-stack utility business, operating in a market where competition and decarbonization had already been forcing reinvention for years.

That partnership kept expanding. In February 2024, Chubu Electric and Eneco agreed that Chubu would acquire a 30% stake in Ecowende, a joint venture between Eneco and Shell developing the Hollandse Kust West offshore wind farm. Eneco said it planned to recycle the proceeds into additional renewable projects, reinforcing the basic logic of the relationship: Chubu gets exposure and learning in offshore wind and European renewables, and Eneco gets capital to keep building.

The Toshiba Consortium

Then there was a very different kind of deal.

On 18 September 2022, Chubu Electric announced it would participate in an investor consortium led by Japan Industrial Partners to acquire Toshiba. Chubu committed ¥100 billion toward a deal valuing Toshiba at about ¥2 trillion (USD 15.2 billion).

Chubu’s stated rationale was straightforward: Toshiba has long been a supplier to Japan’s critical infrastructure, including equipment and systems that touch nuclear, thermal, renewables, grids, and broader social infrastructure. Toshiba’s energy, infrastructure, and digital businesses were described as having “high affinity” with Chubu’s own footprint.

But the subtext was in the caution. Chubu noted the potential for synergies if collaboration opportunities emerged, while also making clear there were no specific agreements or finalized plans at the time.

That careful phrasing says a lot. This wasn’t a merger story. It was an optionality story—putting capital into a strategically important industrial platform, keeping relationships close, and preserving the ability to partner later without overpromising what collaboration would actually look like.

Emerging Market Bets

Chubu also started placing smaller, targeted bets in fast-growing markets. In May 2022, it acquired a stake in Indian solar energy company OMC Power. In November 2024, it expanded that investment, framing it as part of supporting the energy transition in India.

Compared to a European utility acquisition, these are modest moves. But strategically, they’re classic portfolio building: establish presence early in high-growth regions and learn the market through minority positions before committing to something larger.

The JERA Nex bp Joint Venture

The most consequential recent move in renewables has flowed through JERA—where Chubu remains a co-owner—rather than through Chubu alone.

BP and JERA agreed to combine their offshore wind businesses into a new standalone company, later formed as JERA Nex bp. The 50:50 joint venture brought together operating assets and development projects totaling 13 GW of net potential capacity, and the partners said they planned to invest a combined $5.8 billion by the end of 2030 to advance projects and pursue new opportunities.

The structure signaled intent: a dedicated offshore wind platform, headquartered in London, with a management team drawn from both organizations—built to compete in a global market, not just add a few renewable projects on the side.

But offshore wind in the 2020s has been anything but smooth. In October 2025, JERA Nex bp decided to reduce its activities in the US to a minimal level and close its operating activities there, citing unfavorable market conditions and saying it saw no viable path forward for its Beacon Wind project. The company said it would maintain the lease and wait for a more favorable moment to resume development.

The pullback was a reminder of the new world Chubu and JERA were entering. Renewables may be the destination, but the road is messy: supply chain constraints, rising costs, and policy uncertainty can break projects even for well-capitalized players with global partners.

IX. The Nuclear Question: Hamaoka's Long Wait

More than fourteen years after Prime Minister Naoto Kan asked Chubu to shut Hamaoka down, the plant is still offline. And for Chubu Electric, that one reality hangs over everything—from strategy to valuation—because nuclear isn’t just another generation source. It’s the swing factor.

The Nuclear Regulation Authority’s review has moved steadily, but slowly. As of the start of 2024, it was still ongoing, without a clear end date in sight. Chubu’s position, meanwhile, hasn’t changed: it intends to restart Hamaoka and bring it back as a core source of power.

The politics around that goal have also been shifting. In February 2025, the Cabinet approved the “Seventh Strategic Energy Plan” and the “GX2040 Vision,” both of which leaned into the idea of “optimal use of renewable energy and nuclear power,” with safety as the prerequisite. In other words, the national mood at the policy level has been moving toward nuclear as a necessity again—at least on paper. Chubu ties its own stance to Japan’s basic energy policy framework of “S+3E,” with safety first, and says it’s aiming for an early restart of Hamaoka.

On the regulatory front, there was real progress in October 2024, when the NRA approved the plant’s tsunami standards. It was a meaningful milestone—but only one gate in a long sequence. The broader review still spans seismic assessments, verification of safety systems, emergency preparedness, and, crucially, the consent of local governments. Every one of those steps has proven time-consuming in Japan’s post-Fukushima regulatory environment.

At the same time, Hamaoka is no longer just a restart story. It’s also a decommissioning story. The site’s oldest units are already on the dismantling clock: Unit 1 (a 540 MW BWR) and Unit 2 (an 840 MW BWR) entered decommissioning on November 18, 2009, with completion targeted for FY2042.

That leaves the real prize—and the real question—sitting with Units 3, 4, and 5, which together total roughly 3,600 MW. If they restart, the economics would be dramatically better than running on imported fuels; the cost advantage over thermal generation could translate into a meaningful margin lift.

But over the last decade, “if restarted” has become the story. Progress at Hamaoka matters not just for Chubu, but as a signal for Japan’s broader nuclear trajectory—alongside other closely watched plants like Tomari. For now, the wait continues.

X. Financial Performance and Strategic Outlook

Recent Results

By FY2024, Chubu Electric was operating in the new normal: nuclear uncertainty, retail competition, and a fuel market that can swing from windfall to whiplash.

For the fiscal year, consolidated revenue came in at 3,669.2 billion yen. Net sales rose versus the prior year, driven mainly by higher electricity sales volume, even as fuel-cost adjustments and other factors moved in the opposite direction. Ordinary income was 276.4 billion yen, down sharply year over year. The company attributed the decline to a familiar post-crisis pattern: the fade of “time-lag” benefits, weaker cost-reduction effects after changes to the supply portfolio at Miraiz, and higher expenses tied to supply-and-demand balancing at Power Grid.

That flowed through to the bottom line. Profit attributable to owners of the parent fell about 50% to 202.09 billion yen for the fiscal year ended March.

The key concept here is the “time-lag margin.” Electricity rates don’t instantly reflect changes in fuel costs. When fuel prices drop quickly, utilities can temporarily earn outsized profits before the pricing mechanism catches up. When that effect normalizes—as it did in FY2024—earnings can fall even if the underlying business is steady.

Looking to FY2025, management expected continued pressure. Net sales were forecast at 3,550 billion yen, a year-over-year decline largely driven by lower fuel prices and a reduced fuel-cost adjustment impact, helped along by a stronger yen. Ordinary income was projected at 230 billion yen. Even with a pickup in time-lag gains and higher profits from JERA, the company still expected ordinary income to fall by roughly 46 billion yen from FY2024.

And yet, Chubu’s internal yardstick was more optimistic. In FY2025—the final year of its medium-term management target—the company expected “time-lag removed” income of around 210 billion yen, above its stated goal of 200 billion yen or more. In other words: less noise, better underlying performance.

Capital Allocation

Chubu’s capital story is starting to sound more like a modern public company and less like a traditional monopoly.

The company set a target ROIC of 3.0% or more, then raised it in April 2024 to 3.2% or more—an explicit push toward capital-efficiency-focused management. By global standards, that’s not a high hurdle. But in the context of Japanese utilities, which historically optimized for stability and continuity over returns, setting and raising a ROIC target is a signal of where management believes expectations are headed.

Shareholder returns, meanwhile, remained measured. In 2024, Chubu’s payout ratio was 26.99%, and it paid an annual dividend of 50 JPY.

That sub-30% payout reflects the constant tension in this business: returning cash while funding heavy, unavoidable commitments—grid investment, long-running safety and regulatory work at Hamaoka, the realities of owning a share of JERA, and the push into renewables. For Chubu, capital allocation isn’t just a finance decision. It’s strategy under constraint.

XI. Investment Framework: Bull and Bear Cases

The Bull Case

Hamaoka restart optionality: The three long-idled units at Hamaoka add up to roughly 3,600 MW of potential capacity. If Chubu clears the remaining regulatory hurdles and wins the political consent required to restart, the financial impact could be meaningful. Nuclear power is simply cheaper to run than importing fuel for thermal generation, and Japan’s policy posture has been tilting back toward nuclear for both carbon goals and energy security. In that context, every milestone in the Nuclear Regulation Authority process—including the October 2024 approval of tsunami standards—matters because it incrementally reduces the “never restarts” tail risk.

JERA as a platform: Chubu owns half of JERA, the biggest power generator in Japan—and that scale is a strategic asset in a world where fuel procurement and operating flexibility can make or break profitability. JERA’s size gives it leverage in procurement, optionality across a huge thermal fleet, and a base to expand internationally. In 2024, JERA reported $22.4 billion in revenue, 72.7 GW of generation capacity, and operations spanning 15 countries. And through JERA Nex bp, it also has a purpose-built vehicle to pursue offshore wind, extending the platform beyond fossil generation.

Regional economic strength: Chubu Electric’s home market is one of Japan’s few regions with deep, export-oriented industrial gravity. This is Toyota country—an ecosystem of automotive and manufacturing suppliers that has historically meant large, steady loads and high expectations for power quality. The region spans five prefectures, has a population of more than 18 million, and represents about 14% of Japan’s GDP. And with the Chuo Shinkansen (Linear Maglev) terminal planned for Nagoya Station, the area has another potential catalyst for business activity and electrification.

Data center demand: Japan has been seeing a wave of data center development, and data centers have a simple requirement: massive, uninterrupted power. That plays directly to a utility’s core strength—reliability at scale—and it creates a rare pocket of demand growth in an otherwise mature market.

The Bear Case

Hamaoka as a value trap: The most obvious downside is also the simplest. Hamaoka has been offline for 14 years, and time doesn’t just pass—it compounds uncertainty. The longer the restart takes, the higher the chance it never happens at all. With Units 1 and 2 already in decommissioning, the site is no longer just a restart narrative; it’s a dismantling narrative too. If Units 3, 4, and 5 never come back, years of safety-upgrade spending risk being remembered as sunk cost rather than invested optionality.

JERA fossil fuel exposure: JERA’s scale is a strength, but the mix is a vulnerability. As of FY2023, fossil fuels made up 97% of JERA’s global installed capacity and almost all of its domestic operations. Renewables were only 3% globally and 0.2% in Japan. If global decarbonization accelerates faster than JERA can pivot, a fleet built for thermal dominance can start to look like a stranded-asset portfolio. And while JERA has promoted ammonia co-firing as a bridge, the technology still hasn’t proven itself at commercial scale.

Liberalization pressures: Japan’s liberalization hasn’t toppled the incumbents, but it did end the old certainty. Transmission has already been legally unbundled, and further structural separation is always a possibility. If reforms continue to push against integrated advantages—procurement, generation portfolios, retail bundling—the legacy players could find the rules shifting again.

Demographic headwinds: Japan’s population decline is structural, and efficiency keeps improving. The result is a market where demand is flat and expected to remain so through 2030. In a capital-intensive industry, flat demand isn’t neutral—it means constant pressure on utilization and fewer “easy” growth paths to absorb fixed costs.

Porter's Five Forces Assessment

Supplier power: High, especially for LNG and other fuel inputs. JERA’s procurement scale and long-term contracting help, and JERA has been described as the world’s largest LNG buyer—but fuel remains a strategic dependency.

Buyer power: Rising as liberalization matures, though incumbent retention is still strong. Industrial customers, with negotiated contracts and large loads, have far more leverage than households.

Threat of new entry: Low in generation because of capital intensity and permitting complexity. More meaningful in retail, where 700-plus entrants have registered since 2016—though many have since exited or stopped taking new contracts.

Threat of substitution: Medium-term pressure from distributed generation like rooftop solar and battery storage, but limited near-term displacement of bulk industrial demand.

Competitive rivalry: Historically muted under the regional monopoly system, but clearly intensifying. The paradox remains: incumbents still hold around 80% share, while hundreds of competitors fight over the rest.

Hamilton Helmer's 7 Powers

Scale economies: Most visible through JERA’s generation footprint and LNG purchasing power.

Network effects: Limited. Electricity is fundamentally a commodity.

Counter-positioning: JERA itself is a form of counter-positioning—a break from the traditional standalone utility model in order to compete at global scale.

Switching costs: Low for most households, where the process is relatively frictionless. Higher for industrial customers with customized pricing, terms, and reliability requirements.

Branding: Minimal. Utilities rarely win on brand in the way consumer businesses do.

Cornered resource: Hamaoka becomes a potential cornered resource only if restarted—high-value, hard-to-replicate capacity in a fuel-importing country.

Process power: Chubu’s long-running reliability record—around 0.12 outages per customer per year on average from 2001 to 2023—signals real operational excellence, even if it’s difficult to monetize directly.

XII. Key Performance Indicators

If you’re trying to keep score on Chubu Electric from the outside, three signposts tell you most of what you need to know:

1. Hamaoka NRA Review Milestones: Every additional step cleared in the Nuclear Regulation Authority process shrinks the “will it ever restart?” uncertainty. The October 2024 approval of the plant’s tsunami standards was one of those steps, but it’s not the finish line. The real tells to watch are future NRA announcements, the pace of consultations with local governments, and any change in Chubu’s own guidance on timing.

2. JERA Profitability and Dividends: Chubu owns half of JERA, so JERA’s performance isn’t a side note—it’s a major input into Chubu’s results. The drivers are the unglamorous ones: wholesale margins, fuel procurement costs, and how hard the fleet is running. If you’re listening to quarterly earnings, the important work is in the segment detail: what’s happening inside JERA, and whether cash is flowing back up to shareholders through dividends.

3. Renewable Capacity Growth: Chubu has set a clear ambition: add at least 3,200 MW of renewable capacity by around 2030 compared with the end of FY2017. As of the latest update, it reported roughly 35% progress toward that goal. In a company shaped by big, long-cycle infrastructure decisions, this is the execution metric—proof that the post-Fukushima reinvention isn’t just talk, but buildout.

XIII. Conclusion: Crisis as Catalyst

Chubu Electric Power’s story is, at its core, a story about adaptation. It began as a company designed by occupation-era restructuring. It matured inside the comfort—and constraints—of a protected monopoly. And then, crisis by crisis, it learned how to change without abandoning the one thing it was built to do: keep the power on.

The 1959 typhoon wasn’t just a disaster; it became a formative memory that hardened Chubu’s obsession with restoration and reliability. Fukushima was the rupture that made nuclear power politically fragile and turned fuel procurement into a survival problem. The Hamaoka shutdown didn’t merely remove capacity—it forced Chubu into a different posture entirely, one where partnering with TEPCO through JERA became a way to turn vulnerability into scale. And retail liberalization ended the old certainty that customers had nowhere else to go, pushing Chubu to think beyond its historical borders.

That’s the pattern: each shock became a forcing function. Not a detour—an upgrade.

Today, Chubu sits in a strange middle ground. It’s stable enough to be profitable, but pressured enough to keep moving. It has real optionality—especially around Hamaoka—but that optionality comes with real uncertainty. The restart remains the biggest potential swing factor in the story, and also the most unpredictable.

For long-term investors, the exposure is clear: an industrial heartland in central Japan, a stake in JERA’s procurement and generation scale, and a growing set of bets in renewables and international platforms. The risks are just as clear: regulation that can change the economics overnight, a thermal-heavy reality that must bend toward decarbonization, and structural demand headwinds from demographics.

Chubu itself has acknowledged the moment. It has said the environment around the company is “changing dramatically,” driven by competition after liberalization and by national policy shifts like the GX2040 Vision and the Seventh Strategic Energy Plan. In response, it revised its Corporate Philosophy in April 2025, at the start of the new fiscal year, framing the goal as sustainable growth alongside stakeholders.

That revision reads like a quiet admission that the next chapter won’t be a continuation of the last. Chubu has reinvented itself before—more than once, and not by choice. Whether it can do it again, in a world defined by decarbonization, geopolitics, and less patience for slow change, will determine whether this utility born from occupation-era design can keep thriving in the decades ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube