SoftBank Corp.: The Cash Engine of the SoftBank Empire

I. Introduction & Episode Roadmap

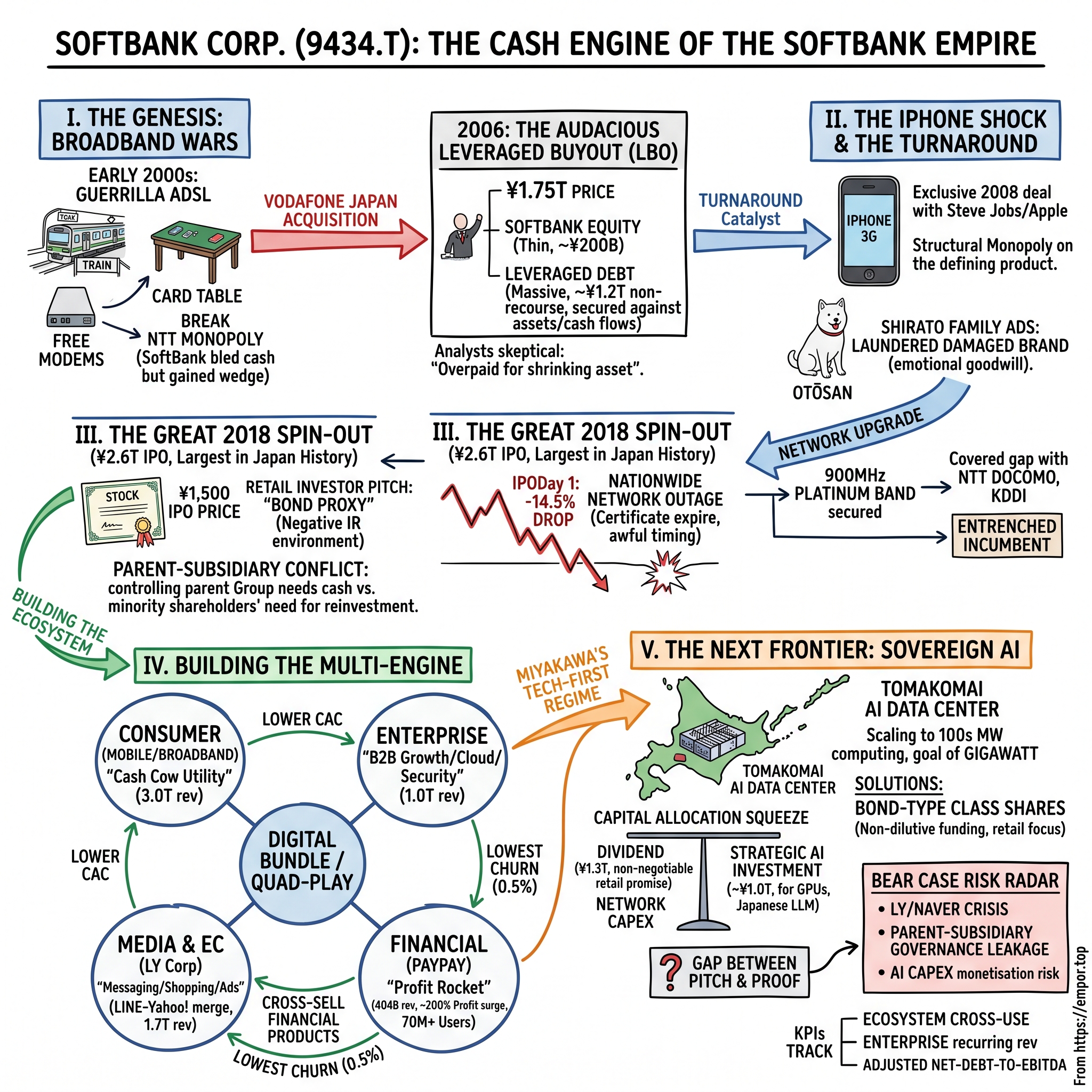

On the morning of December 19, 2018, a small ceremonial bell rang on the floor of the Tokyo Stock Exchange, and one of the strangest blue-chip debuts in Japanese history began. ソフトバンクグループ株式会社 SoftBank Group Corp. had just carved out its domestic telecom business, ソフトバンク株式会社 SoftBank Corp. (9434.T), and floated it in an offering that raised roughly ¥2.6 trillion, or about $23.5 billion — at the time the largest IPO in Japanese history and one of the largest ever completed anywhere.1 To the retail investors who lined up for shares, it looked like a straightforward bet: buy a piece of a boring, reliable phone company and collect a fat dividend. To 孫正義 Masayoshi Son, it was something else entirely — a way to convert two decades of patiently built cash flow into ammunition for the global venture-capital blitz he was running through the SoftBank Vision Fund.

That tension — utility on the outside, financing vehicle on the inside — is the whole story. Here is the paradox worth sitting with. This is a company that began life as a debt-choked broadband insurgent, handing out free modems on Tokyo street corners to break a state monopoly, and somehow ended up as a defensive, high-yield dividend stock that Japanese pensioners hold as a bond substitute. How does a business complete that transformation? And having completed it, how does it now hold two contradictory identities at once — a slow-growing cash cow paying out roughly 85% of its profits, while simultaneously pledging to build the data centers, the domestic large language models, and the AI-native network that Japan hopes will keep it technologically sovereign?

The thesis we will test across this episode is that SoftBank Corp. is no longer a "dumb pipe." Through a decade of acquisitions it has wrapped Japan's dominant messaging app, its leading web portal, and its most-used QR payment network around a mobile subscriber base, building a digital bundle few rivals can match. That is the bull framing management itself uses. Our job is to hold it to account: to separate what the ecosystem demonstrably does — suppress churn, cross-sell financial products — from what management merely asserts it will do. And to weigh the real, unresolved risks: a governance structure where a controlling parent's interests diverge sharply from minority holders', a geopolitically radioactive ownership fight over LINE with South Korea's 네이버 NAVER, and an AI capital-expenditure program whose payoff is a promise, not a fact.

Here is the roadmap. First, the genesis — the broadband wars and the audacious ¥1.75 trillion leveraged buyout of Vodafone Japan. Second, the iPhone shock that rebranded a failing carrier into a growth machine. Third, the mechanics and drama of the 2018 spin-out. Fourth, the multi-engine ecosystem: Yahoo! Japan, LINEヤフー株式会社 LY Corporation, and the improbable rise of PayPay. Fifth, the management transition to an engineering-led regime under 宮川潤一 Junichi Miyakawa. Sixth, a segment-by-segment look at where the money actually comes from. Seventh, the strategic playbook and competitive frameworks. And finally, the stress test — the bear case, the activist critique, and the handful of numbers that actually matter.

II. The Genesis: Broadband Wars & The Vodafone Gamble

Picture Tokyo in the early 2000s: a country with world-class fiber ambitions but broadband prices that made dial-up feel reasonable, all of it orbiting the gravitational mass of 日本電信電話株式会社 Nippon Telegraph and Telephone Corporation (NTT), the former state monopoly that still controlled the copper running into nearly every home. In 2001, Masayoshi Son — then known primarily as a software distributor and dot-com investor who had been spectacularly rich and then spectacularly less rich after the tech crash — launched Yahoo! BB, a high-speed ADSL service priced to detonate the incumbent's margins.

What followed became business folklore. Son's teams set up card tables outside train stations and electronics stores and simply gave the modems away — press a flyer into a commuter's hand, sign them up on the spot, worry about the economics later. The strategy was pure guerrilla warfare, and it was expensive; SoftBank bled cash for years. But it worked as a wedge. By forcing NTT to open its local loops and by dragging Japanese broadband prices down to among the cheapest in the developed world, Son established the pattern that would define him: use aggressive, often reckless-looking tactics to pry open a market controlled by a complacent giant, and absorb enormous short-term losses to buy long-term position.

Broadband, though, was never the endgame. Son wanted mobile — the higher-margin, stickier prize — and the door opened in 2006. Vodafone Japan, the local arm of the British telecom giant, was quietly failing. The parent had bought its way into Japan through the old J-Phone business, then misread the market almost completely: it pushed global handset models that Japanese consumers found dull next to the feature-rich domestic "Galapagos" phones, dragged its feet on 3G, and watched subscribers churn to NTT DOCOMO and KDDI. Vodafone wanted out.

Son wanted in — and the way he financed it is the part that made rival executives choke on their coffee. In March 2006, SoftBank agreed to acquire Vodafone Japan for about ¥1.75 trillion, roughly $15.5 billion, then the largest corporate acquisition in Japanese history.2 The audacity was in the capital structure. Against that ¥1.75 trillion price, SoftBank itself put up only around ¥200 billion of common equity. The overwhelming majority was a non-recourse leveraged buyout — on the order of ¥1.1 to ¥1.2 trillion of debt secured against the acquired carrier's own assets and future cash flows, supplemented by preferred shares and seller financing from Vodafone Group. In plain English: Son borrowed against the target's future phone bills to buy the target, ring-fencing the debt so that if the whole thing collapsed, the lenders could seize the carrier but not sink the rest of SoftBank.

Analysts were merciless. The consensus was that Son had overpaid — roughly 7.5 times EBITDA for a shrinking asset when stable Western telecoms traded lower — and that the debt load would eventually drag the entire group under. On the raw numbers, the skeptics had a point: paying a premium multiple for a business losing customers is not obviously smart. What the skeptics could not see was that Son was not really buying Vodafone Japan's present. He was buying a nationwide spectrum license and subscriber base that he intended to weaponize with a product nobody in Japan had yet held in their hands. The turnaround that followed would send the return on that thin sliver of equity into the stratosphere — but only because of a handshake Son was about to secure eleven time zones away.

III. The Turnaround: The iPhone Shock & Rebranding Japan's Telco

The most valuable meeting in SoftBank's history may have been one for which no minutes survive. By Son's own retelling, he flew to California and sat down with Steve Jobs before Apple had publicly shown the iPhone, and pitched him a sketch of exactly the kind of internet-in-your-pocket device Jobs was secretly building. Son's ask was audacious: give me exclusive rights to sell it in Japan. Jobs, the story goes, told him he was crazy — Son didn't even own a mobile carrier yet. Son's reply was that he would go get one. He did, and when Apple was ready, SoftBank held the keys.

The payoff arrived in 2008, when SoftBank launched the iPhone 3G in Japan with total exclusivity. It is hard to overstate how disruptive this was to the domestic order. Japan's mobile market had evolved in a hothouse — elaborate feature phones with mobile wallets and TV tuners, tuned to carrier-controlled ecosystems, brilliant and utterly incompatible with the rest of the world. The iPhone blew a hole in that model. High-spending, tech-forward customers — precisely the high-ARPU users every carrier covets — began migrating to SoftBank because it was the only place to get the device everyone suddenly wanted. For roughly three years, Son had a structural monopoly on the most desirable product in the industry, and he used it to convert a churning, second-rate network into a growth story.

But a growth story built on a borrowed reputation had a problem: the network Son inherited was widely seen as cheap and unreliable, a hangover from the Vodafone years. His answer was not just more base stations — it was one of the most effective branding campaigns in the history of Japanese advertising. In 2007 SoftBank introduced the 白戸家 Shirato family, a fictional household whose father was a white Hokkaido dog named Otōsan. The surreal premise — nobody in the family blinks at the fact that dad is a dog — made the ads irresistible, and the campaign ran for well over a decade, becoming a genuine piece of national pop culture. The strategic point is easy to miss under the whimsy: Son used entertainment to launder a damaged brand into a beloved one, buying emotional goodwill that ARPU spreadsheets can't purchase.

The whimsy was backstopped by capital. A network reputation cannot be fixed with a dog; it has to be fixed with radio. SoftBank poured money into densifying its footprint and, critically, fought to secure 900MHz spectrum — the so-called "Platinum Band" whose lower frequency travels farther and penetrates buildings better, exactly the coverage weakness that had plagued the Vodafone-era network. Winning that spectrum let SoftBank close much of the coverage gap with NTT DOCOMO and KDDI, converting "cheap but flaky" into a credible third pillar of Japan's mobile oligopoly. By the mid-2010s SoftBank was no longer the insurgent; it was an incumbent — profitable, entrenched, and generating exactly the kind of predictable cash flow that Son would soon need for something far more ambitious. The question was how to get that cash out.

IV. The Great Spin-Out: The $23.5B Parent-Subsidiary Conundrum

By 2018, Masayoshi Son had a new obsession and a new math problem. The obsession was the SoftBank Vision Fund, the roughly $100 billion vehicle through which he was firing enormous checks into WeWork, Uber, and dozens of other private tech companies. The math problem was that the world's most valuable stable cash flow — the Japanese telecom business — was trapped inside the parent company, its worth obscured by the group's sprawling, hard-to-value structure. Son's solution was elegant and slightly cynical: sell the public a direct piece of the boring, reliable telecom, keep control of it, and use the proceeds to feed the venture machine.

The pitch to Japanese retail investors was engineered for a specific historical moment. This was the era of the Bank of Japan's negative interest rates, when domestic savers could earn essentially nothing on cash or government bonds. Into that vacuum SoftBank Corp. offered itself as a "bond proxy": a stock promising a dividend payout ratio around 85% and a yield north of 5%.3 For a saver starved of yield, it was seductive — a household-name brand paying more in a year than a bank deposit would pay in a generation.

Then reality intruded, with almost theatrical timing. On December 6, 2018 — days before the IPO priced — SoftBank's network suffered a nationwide outage lasting about four and a half hours, knocking out service for millions of subscribers. The cause was a software certificate that had been allowed to expire in equipment supplied by Ericsson. The optics could hardly have been worse: a company about to sell itself to the public as a reliable utility, splashed across the national news for being anything but. The debut confirmed the jitters. Priced at ¥1,500 per share, the stock fell sharply on its first day of trading on December 19, closing around ¥1,282, down roughly 14.5% — an unusual and painful stumble for an offering marketed so heavily to first-time retail buyers who had trusted the brand.1

The rocky start eventually gave way to years of steady dividends, but the deeper issue it exposed never went away: the parent-subsidiary conflict baked into the structure. SoftBank Group retained a controlling stake — roughly 40% of SoftBank Corp. after subsequent sell-downs — which means the company operates as a listed subsidiary of a listed parent, the "double listing" arrangement that corporate-governance reformers in Japan have spent years trying to stamp out.8 The conflict is not theoretical. SoftBank Group has a structural, standing incentive to maximize the cash pulled upstream through dividends to fund its speculative investments, while the minority shareholders of SoftBank Corp. — the retail buyers, the pension funds — need that same cash reinvested in network infrastructure and new growth. Every yen is contested. When a controlling parent sits on both sides of that table, minority investors are right to ask whose interests win when they diverge. Hold that question; it recurs. First, though, we need to understand what management chose to build with the cash it did retain.

V. Building the Multi-Engine: Yahoo! Japan, LY Corporation, & The Rise of PayPay

Every mobile executive on earth eventually confronts the same grim slide: the one showing average revenue per user flattening and then bending down as connectivity becomes a commodity. You can only sell so many gigabytes to a saturated country. SoftBank's management read that slide early and made a strategic bet that would define the modern company: if the pipe is commoditizing, own everything that flows through it. Own the messaging, the search, the shopping, the payments — the customer's entire digital day.

The first engine was Yahoo! Japan, the dominant domestic web portal that, unlike its faded American namesake, remained a genuine powerhouse of search, news, and e-commerce traffic in Japan. Consolidated through Z Holdings, it gave SoftBank a media and advertising business and, crucially, a shopping platform to pair with what came next. The second engine was the blockbuster one. In 2021, Z Holdings merged with LINE Corporation, the messaging app that is less an app than a piece of Japanese social infrastructure — the way tens of millions of people text, call, pay, and read the news. The combined entity, later renamed LINEヤフー株式会社 LY Corporation, brought together the country's leading portal and its leading messenger under one roof.4

But the merger carried a structural complication that would later detonate. LINE had been controlled by South Korea's 네이버 NAVER, and the deal left LY Corporation jointly controlled by SoftBank and NAVER through a 50-50 joint venture called A Holdings. On paper, a balanced partnership. In practice, a fault line running straight through a company that holds the private messages of most of Japan — and, as we'll see, one that Japanese regulators would come to regard as a national-security problem.

The third engine was the one almost nobody predicted would work: PayPay. Japan in 2018 was still a stubbornly cash-based society, a country of ATMs and coin purses where credit-card penetration lagged the developed world and previous attempts to popularize mobile payments had fizzled. PayPay's strategy for cracking it was brute-force generosity. Launched in October 2018, it ran cash-back campaigns of almost comic aggression — most famously a ¥10 billion giveaway that refunded users a portion of their spending, occasionally all of it, until the money ran out in days. It was, transparently, buying market share with the parent's cash, torching money to build a habit.

The genius was in what the habit connected to. PayPay was woven directly into Yahoo! Japan shopping and into LINE, so that using the payment app fed the commerce platforms and vice versa — the flywheel management had been assembling piece by piece. And then, remarkably, the money furnace turned into a profit engine. Over its first several years PayPay accumulated large losses, exactly as designed. But as the user base matured, the economics inverted. By the fiscal year ended March 31, 2026, PayPay had grown into a genuinely profitable financial platform: annual profit surged roughly 201% to about ¥117.8 billion, on total gross merchandise value of around ¥19.4 trillion, with a registered user base exceeding 70 million — a scale that, in a country of 125 million people, approaches ubiquity.[^14] The strategic lesson is one investors should weigh carefully: PayPay validated the thesis that a payment network, once it achieves critical mass, becomes a distribution channel for far higher-margin financial products — credit, banking, brokerage, insurance. Whether that justified the years of subsidy is a question of who paid for it, and much of the early bill was footed by the parent. The engines were built. The question by 2021 was who would run them.

VI. Under New Management: Miyakawa's Tech-First Regime

For most of SoftBank Corp.'s life, its operational soul belonged to 宮内謙 Ken Miyauchi — a Son loyalist of the old school, a sales-and-marketing animal who could be trusted to take one of the founder's wild visions and grind it into commercial reality. Miyauchi was the executioner: the man who won the iPhone customers, priced the plans, and out-hustled the competition on the ground. In April 2021 he stepped up to Chairman, and the top job passed to a very different kind of executive.8

宮川潤一 Junichi Miyakawa was an engineer, not a salesman — the former Chief Technology Officer, a builder of networks rather than a mover of handsets. His elevation to President and CEO was a deliberate signal about where management believed the next decade of value would come from. Where Miyauchi's era was about winning the subscriber war, Miyakawa's would be framed around infrastructure, data, and artificial intelligence — the company recasting itself, in its own telling, from a marketing-led telecom into an engineering-led technology firm. It is a nice story; the investor's job is to check it against behavior, and here the behavior is at least partly persuasive.

Start with skin in the game. Miyakawa's compensation is structured to reward performance rather than tenure: for the fiscal year ended March 31, 2025, his total pay was reported at roughly ¥654 million, the large majority of it — around ¥515 million — tied to short-term performance targets rather than fixed salary.8 More striking is the equity story. The company maintains a guideline requiring the CEO to hold shares worth at least three times base salary, and Miyakawa clears that bar by a wide margin, holding a very large personal position in the stock — on the order of 175 million shares as disclosed in the company's filings.8 The detail that management likes to emphasize is that he borrowed money to buy a large block of shares at the leadership transition, deliberately levering himself into the same stock the retail minority owns. Personal alignment of that kind does not guarantee good decisions, but it does mean the man setting capital policy feels the dividend and the share price in his own balance sheet.

And the capital policy is where Miyakawa's credibility will ultimately be judged. His track record so far shows a balancing act: honoring the roughly 85% payout ratio that the whole retail investment case rests on, while keeping the balance sheet from spiraling — holding the adjusted net-debt-to-EBITDA ratio in the mid-2x range even as the business funds heavy network capex and a new AI buildout.3 That is a genuinely difficult trick, because a high fixed payout and a capital-hungry growth ambition pull in opposite directions. Whether he can keep threading that needle as the AI bill comes due is one of the central open questions of the story — and to judge it, we need to see exactly where the cash is generated.

VII. The Financial Spine: Segment Performance & Unit Economics

Strip away the branding and the ecosystem poetry, and SoftBank Corp. is a machine that turned over about ¥7,038.7 billion in revenue in the fiscal year ended March 31, 2026, generated ¥1,042.6 billion in operating income, and delivered ¥550.8 billion in net income — both revenue and net income at record highs, growing 8% and 5% respectively.3 Where that money comes from tells you what the company actually is, so let's walk the five engines.

The Consumer segment is the cash cow that funds everything else. It is the mobile and broadband business — the roughly ¥3,015 billion in revenue that the whole edifice rests on, and by far the largest single contributor to group operating income.38 This is the utility: predictable, high-margin, slow-growing, and responsible for producing the free cash flow that pays the dividend and the network bills. When SoftBank pitches itself as a bond proxy, this is the bond. The strategic read is straightforward — as long as Japanese mobile stays a rational oligopoly, this segment is the ballast. The risk is equally clear: it is mature, and its growth is largely borrowed from the other four engines.

The Enterprise segment is the B2B growth engine. Selling cloud, security, and digital-transformation services to Japanese corporates generated roughly ¥1,003 billion in revenue, and management guided it toward around 20% growth in the following year.3 The appeal here is margin and durability: enterprise IT contracts behave like recurring, SaaS-style revenue that is far stickier than a consumer phone plan, and Japan's corporate sector — famously behind on digitization — represents a long runway. This is the segment where the AI ambitions are meant to eventually monetize, selling compute and Japanese-language AI services to businesses.

The Media & EC segment is LY Corporation. Advertising and e-commerce fees produced roughly ¥1,668 billion in revenue, but its operating income actually fell about 7% year over year — a decline management attributed almost entirely to a one-time system outage at ASKUL Corporation; excluding that, the segment would have grown around 6%.3 It is a reminder that "media" here is a mature, cash-generative but low-growth business, and one that carries the LY/NAVER governance overhang we will return to.

The Financial segment is the high-beta rocket. Powered by PayPay, PayPay Bank, and PayPay Securities, it turned in roughly ¥404 billion in revenue, but the number that matters is the trajectory: segment operating income roughly doubled, growing about 107% year over year.3 This is monetization of the payment base finally kicking in — the eKYC-verified user base being cross-sold credit, brokerage, and other financial products at high incremental margins. If any segment can bend the company's growth curve upward, it is this one, though from a still-modest revenue base.

The Distribution segment (SB C&S) is the low-margin plumbing. It distributes ICT hardware and software, booking roughly ¥1,056 billion in revenue but only a thin sliver of income — a reminder that not everything under the SoftBank roof is a high-margin platform; some of it is honest, competitive, commodity distribution.3

Zoom out and the competitive picture comes into focus. SoftBank is one of three, soon arguably four, players in a Japanese mobile market long prized for its discipline. Against NTT DOCOMO and KDDI it competes on ecosystem and price tiering rather than pure network bragging rights. The disruptive variable has been 楽天モバイル株式会社 Rakuten Mobile, which entered with rock-bottom pricing and forced industry ARPU down. SoftBank's defense has been segmentation: a premium SoftBank brand, a value Y!mobile brand, and the online-only LINEMO brand, letting it meet price-sensitive customers without cannibalizing premium ones. The proof that the defense is working shows up in one number management returns to again and again — an industry-leading churn rate around 0.5% a month, meaning it loses only about one subscriber in two hundred each month.8 Ultra-low churn is the single best evidence that the ecosystem bundling actually changes customer behavior rather than merely sounding good on a slide. That defended cash base is what lets management contemplate its most expensive bet yet.

VIII. The Next Frontier: Sovereign AI, Computing Infrastructure, & Capital Allocation

In April 2025, on a 700,000-square-meter plot in Tomakomai, Hokkaido, SoftBank held a groundbreaking ceremony for what it intends to become one of Japan's largest AI data centers — a facility designed to run on locally procured renewable power and to scale toward hundreds of megawatts of computing capacity, with the company floating the possibility of reaching a full gigawatt over time.9 The choice of Hokkaido — cool climate, available land, renewable generation — is a tell about how seriously the physics of AI compute now shape corporate strategy. Miyakawa's master plan reframes the entire company around a single idea: that SoftBank Corp. should be the foundational infrastructure for artificial intelligence in Japan.

The problem is that this ambition collides head-on with the dividend promise, and the collision is a matter of arithmetic. Over its multi-year plan, SoftBank projects generating a large pool of operating cash flow, but the claims on that pool are enormous and competing. Telecom capex — keeping the core network current, rolling out 5G — consumes the largest slice. Base-station leases take another chunk. The dividend, non-negotiable given the retail investment thesis, requires a cumulative commitment on the order of ¥1.3 trillion.3 And on top of all that, management wants to fund an aggressive strategic AI investment program approaching ¥1.0 trillion: data centers like Tomakomai, thousands of NVIDIA GPUs, the development of a domestic Japanese-language large language model, and "AI-RAN," the effort to embed AI processing directly into the radio-access network.79 You cannot pay all of those bills out of the same cash flow without either cutting the dividend, levering up, or finding money somewhere else.

Management's answer to that squeeze is financial engineering — and it is genuinely clever, if not without cost. Rather than issue common equity and dilute the shareholders it has spent years courting, SoftBank has raised capital through so-called Bond-Type Class Shares: securities listed on the Tokyo Stock Exchange that behave like bonds, offering yield-seeking retail investors a fixed-style return while functioning as non-dilutive funding for the company.[^12] It is the same instinct that structured the Vodafone LBO two decades earlier — reach for the capital structure that gets you the money without giving up control or diluting the common. Investors should recognize both the ingenuity and the pattern: this is a company that habitually funds its ambitions with cleverly structured claims on future cash, which works beautifully until the future cash disappoints.

Why go to all this trouble for AI at all? The strategic logic rests on the idea of sovereignty. Japan has real cultural, linguistic, and regulatory reasons to want AI systems that natively understand Japanese business norms, legal frameworks, and language — rather than depending entirely on models trained and hosted by American hyperscalers. SoftBank's argument is that it is uniquely positioned to serve that demand: it has the data pipelines, the enterprise relationships, the domestic data centers, and now, through a joint venture with OpenAI announced in 2025, a channel to frontier models adapted for the Japanese market.10 If that thesis is right, it would give SoftBank a structural, hard-to-replicate position in Japanese enterprise AI. But notice the tense: "would." Every piece of the sovereign-AI case is currently a forecast. The data centers are being built, the models are being trained, the enterprise demand is being courted — and none of it has yet been proven to generate the returns that would justify a trillion-yen bet. That gap between the pitch and the proof is exactly where the skeptics live.

IX. The SoftBank Corp. Playbook: Key Strategic & Investing Lessons

Step back from the chronology, and three transferable lessons emerge — the strategic DNA that runs from the ADSL modems on the street corners to the GPUs in Hokkaido.

Lesson 1: Leverage is an operating weapon, not just a financing trick. The Vodafone buyout is taught as a feat of financial engineering, but the deeper lesson is that leverage is only safe when it is bolted to two things: predictable, utility-like cash flows to service the debt, and a structural catalyst to drive the upside. Son had both — a subscriber base that pays its phone bills like clockwork, and the iPhone exclusivity that turned a shrinking asset into a growth engine. Debt without either of those is just a way to go bankrupt faster. The playbook is repeatable, but only for those who actually possess the cash flow and the catalyst; SoftBank's own history shows how thin the equity cushion can be when both are present, and how catastrophic the same structure would be without them.

Lesson 2: The ecosystem "quad-play" is a defense against commoditization. Pure connectivity is a race to the bottom — a commodity where the only variables are price and coverage. SoftBank's response was to wrap connectivity (mobile) together with messaging (LINE), commerce and search (Yahoo), and payments (PayPay) into a single bundle whose discounts and loyalty points make leaving economically irrational. The mechanism is concrete and measurable: it lowers customer acquisition cost, because each service feeds the others, and it drives churn toward zero, because unwinding from a bundle is a hassle. The evidence — that 0.5% churn — is what separates this from the empty "synergy" language that plagues most conglomerates. But it is worth naming the cost: the bundle was assembled through years of acquisitions and subsidies, much of it funded by a parent whose interests are not the minority's.

Lesson 3: Understand what you own — the subsidiary is not the parent. For public investors, SoftBank offers an unusually clean natural experiment. The parent, SoftBank Group, is pure exposure to volatile global tech equity — venture bets, mark-to-market swings, the drama that makes headlines. The subsidiary, SoftBank Corp., is the opposite: a domestic operator offering dividends, downside protection, and boring operational execution. They trade as different animals for good reason. The lesson is that "SoftBank" is not one investment but two radically different ones, and confusing them — buying the utility expecting venture upside, or buying the venture expecting utility stability — is a category error. The catch, which the next section presses on, is that the two are not fully separable: the parent's grip on the subsidiary means the utility can never be entirely insulated from the venture.

X. The Stress Test: Bear vs. Bull & Strategic Position

Now we war-game it. A durable investment case has to survive a hostile reading, so let's run SoftBank Corp. through the standard strategic frameworks and then hand the microphone to the skeptic.

Hamilton Helmer's 7 Powers

Network Economies (Very Strong). This is SoftBank's most genuine source of durable advantage, and it lives in two places. PayPay's tens of millions of users and its merchant acceptance network create a classic two-sided flywheel: more users make the app more valuable to merchants, and more merchants make it more valuable to users, until the leader's position becomes nearly unassailable. LINE's grip is even more absolute — a messaging network where the value is entirely in the fact that everyone else is already on it, the textbook definition of network lock-in. These are real, and they are hard to attack.

Switching Costs (High). The bundle does its work here. A consumer who has a SoftBank phone plan, a home internet line, PayPay for daily payments, and Yahoo Shopping points accumulating in the background faces a genuine cost — financial and psychological — to unwind it all and move to a rival. The churn data confirms this is not hypothetical.

Cornered Resource (Moderate, and Fading). Historically this was the iPhone exclusivity — a textbook cornered resource that lasted only as long as Apple allowed. Today management points to its privileged access to the consumer data flowing through LINE and Yahoo as the raw material for proprietary AI. That is a plausible claim, but a softer one: data advantages are real but rarely as durable as management hopes, and the regulatory scrutiny of exactly that data (see below) shows the resource is contested, not cornered.

Porter's 5 Forces

Threat of New Entrants (Low). Building a nationwide wireless network costs a fortune and requires government-allocated spectrum that simply is not available to newcomers. The best evidence is Rakuten Mobile itself: a well-capitalized, determined entrant that spent years and enormous sums and still struggled to reach financial sustainability. If Rakuten found it that hard, the barrier is doing its job.

Bargaining Power of Buyers (Moderate). Japanese regulators have deliberately increased consumer power — mandating easier number portability, capping handset subsidies, pushing price transparency — all of which lets customers shop around more aggressively than before. That genuinely pressures ARPU. But the ecosystem bundling is the counterweight, and the standoff between regulatory pressure and switching costs is roughly where the market sits today.

The frameworks paint a company with real moats. But frameworks are where bull cases go to feel comfortable, so here is the adversarial read.

The Skeptical Investor / Activist Stress Test & Risk Radar

1. The LY Corporation / NAVER crisis is the sharpest overhang. After a significant data leak at LINE, Japan's 総務省 Ministry of Internal Affairs and Communications issued unusually forceful 行政指導 administrative guidance, demanding that LY Corporation overhaul its security and — pointedly — reduce its technical and capital reliance on NAVER, the Korean company that co-controls it.[^6] What began as a cybersecurity matter escalated into a geopolitically charged fight, with SoftBank reportedly seeking to take control of LY away from NAVER while the Korean government and public reacted angrily to what looked like state-pressured expropriation of a Korean-built asset.56 For SoftBank Corp., this is a genuine bind: it is being pushed to spend heavily to decouple the two companies' IT systems while negotiating a sensitive and, as of this writing, unresolved equity restructuring. It is a risk that is simultaneously regulatory, financial, and diplomatic — the worst kind to underwrite.

2. Parent-subsidiary governance leakage is the structural risk. Return to the conflict from Section IV. The standing danger of the double-listing is that SoftBank Group, when it needs cash or wants to rescue one of its own investments, can pressure SoftBank Corp. into overpaying for assets or entering unfavorable related-party deals — with minority holders footing the bill. Nothing about the structure prevents this; it relies on governance discipline and the reputational cost of abuse. Investors are being asked to trust that the controlling shareholder will restrain itself, which is not the same as being protected.

3. AI capex overhang is the execution risk. If the sovereign-AI thesis fails to monetize — if Japanese enterprises don't buy localized LLMs and AI-RAN services at the scale and price management assumes — then SoftBank is left holding a very expensive collection of data centers and depreciating GPUs, funded partly by cleverly structured debt-like instruments that still have to be serviced. AI infrastructure is a bet on demand that does not yet exist at scale, and the history of telecom is littered with expensive infrastructure built ahead of demand that never fully arrived.

The Core Investment KPIs to Track

Cutting through the noise, three metrics tell you whether the story is working:

1. Ecosystem cross-use. The share of SoftBank mobile subscribers who actively use PayPay and Yahoo services. This is the single best proxy for whether the bundle is real, because it is the direct driver of the low churn and rising lifetime value that the entire quad-play thesis depends on.

2. Enterprise/AI recurring revenue growth. Whether the high-margin corporate IT and AI platform pivot is actually converting into durable, recurring revenue — the proof or disproof of the sovereign-AI bet.

3. Adjusted net-debt-to-EBITDA. The discipline metric. If AI and network capex push leverage decisively beyond the roughly 2.5x zone management has held, the dividend — the whole reason retail owns this stock — comes into question.

The Bull vs. Bear Case

The bull case is that the engines fire in sequence: PayPay's high-margin financial monetization compounds from here, the enterprise and AI businesses successfully capture Japan's demand for sovereign corporate AI, and the core mobile utility keeps throwing off the predictable cash that funds a steadily rising dividend. In that world, SoftBank Corp. is a rare combination — a defensive yield stock with a genuine growth option attached — and the market re-rates it upward toward its more richly valued peers.

The bear case is that the overhangs win. Regulatory pressure over LY Corporation escalates into a costly, value-destroying decoupling and a bad settlement with NAVER; the AI investments become stranded assets that never earn their cost of capital; Rakuten Mobile finally makes its price war sustainable and grinds down industry margins; and the parent-subsidiary conflict keeps a permanent discount stapled to the valuation relative to KDDI and NTT DOCOMO. In that world, the dividend is defended only by stretching the balance sheet, and the "bond proxy" turns out to carry a lot more equity risk than its buyers were promised. The truth, as usual, will land somewhere between — and which way it leans depends almost entirely on the three numbers above.

XI. Outro & Epilogue

There is a temptation, when telling the SoftBank story, to make it entirely about Masayoshi Son — the gambler, the visionary, the man who bet the company on a handshake with Steve Jobs and won. But the company that carries the SoftBank name on the Tokyo Stock Exchange under the ticker 9434 is, in a sense, the part of the empire that was built to outlast his gambles. It is the operational survivor: the business that generated the cash for every wild swing, absorbed a leveraged buyout that analysts swore would sink it, weathered a humiliating IPO-week outage, and emerged as the steady utility at the center of tens of millions of Japanese digital lives.

The final contrast is the one worth carrying out of this episode. SoftBank Group captures the world's attention with its dramatic venture bets and its founder's outsized ambitions. SoftBank Corp., under the quieter, engineer's hand of Junichi Miyakawa, does something less glamorous and more essential — it keeps Japan connected, paid, and online, and it is now attempting to build the AI backbone the country will run on for the next half-century. Whether that quiet ambition pays off, or whether the governance conflicts and capital tensions catch up with it first, is the story still being written. For now, the cash engine keeps running — and the whole empire, glamorous and unglamorous alike, still depends on it.

References

-

SoftBank's mobile unit IPO raises $23.5 billion, fully allocated — Reuters, 2018-12-10 ↩↩

-

SoftBank to buy Vodafone Japan for $15.5 billion — Reuters, 2006-03-17 ↩

-

SoftBank Corp. FY2025 Earnings: Record Net Income and Revenue Achieved, Continued Growth Forecasted — SoftBank Corp., 2026-05-11 ↩↩↩↩↩↩↩↩↩

-

SoftBank's LY Corp aims to end Naver IT dependence following security breach — Reuters, 2024-06-25 ↩

-

SoftBank's Telco Aims to Take LY Control from Naver After Breach — Bloomberg, 2024-05-08 ↩

-

Tensions rise over Japan's pressure on Naver to sell LY Corp stake — Financial Times, 2024-05-20 ↩

-

SoftBank Corp plans to invest ¥150 billion in AI supercomputers — Reuters, 2024-05-09 ↩

-

SoftBank Corp. Integrated Report 2025 — SoftBank Corp., 2025 ↩↩↩↩↩↩

-

Laying the Foundation for the AI Era: Construction Begins on "Hokkaido Tomakomai AI Data Center" — SoftBank Corp., 2025-05-01 ↩↩

-

SoftBank Corp. Q2 FY2025 Earnings: Joint Venture with OpenAI Launched — SoftBank Corp., 2025-11-05 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube