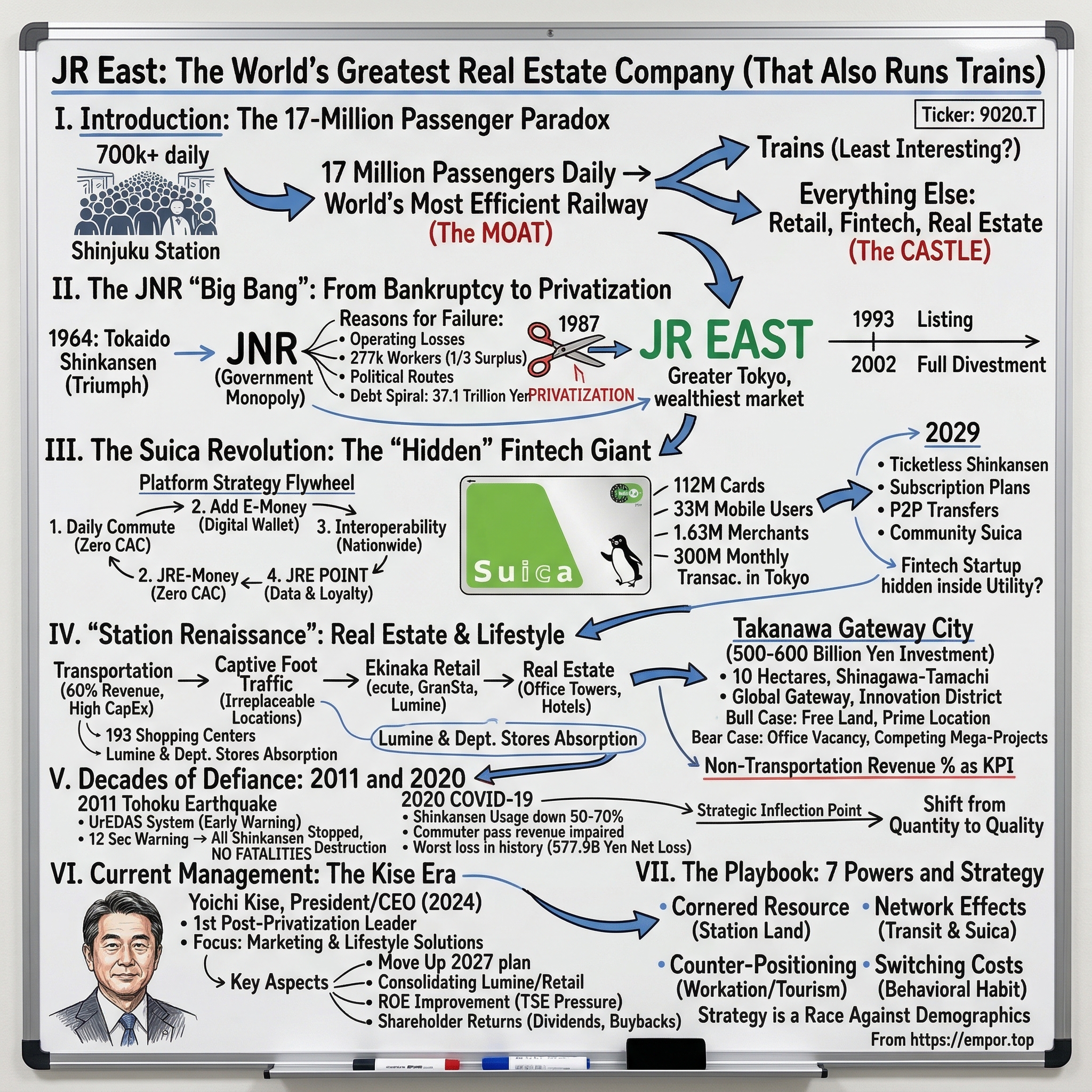

JR East: The World's Greatest Real Estate Company (That Also Runs Trains)

I. Introduction: The 17-Million Passenger Paradox

Picture Shinjuku Station at 8:14 on a Monday morning.

The world's busiest railway station is not a quiet place. Nearly 700,000 people will pass through this single building today, more than the entire population of Washington, D.C. White-gloved attendants push commuters into carriages with practiced precision. The doors close. The train departs exactly on time, to the second. In a few minutes, another wave arrives. And another. And another.

Now zoom out. This is not one station's story. Across 1,676 stations and 7,401 kilometers of track stretching from the neon canyons of central Tokyo to the snow-covered mountains of Tohoku and the rice paddies of Niigata, East Japan Railway Company moves roughly 17 million passengers every single day. That is the entire population of the Netherlands, transported with 99.9% punctuality, repeated five days a week, fifty-two weeks a year. No airline, no bus network, no subway system on Earth comes close.

But here is the paradox that makes JR East one of the most misunderstood companies in global capital markets: transportation, the thing the company is famous for, is arguably the least interesting part of the business.

When those 17 million passengers step off their trains, they walk through a gauntlet of retail, convenience stores, bakeries, coffee shops, and luxury boutiques — all owned by JR East. They tap their Suica cards — a JR East product — to pay for their morning latte, their lunchtime bento, their evening beer. The data from those taps flows into JR East's loyalty engine. And the ground those passengers stand on, the buildings above them, the office towers and hotels rising from station plazas — that real estate belongs to JR East too.

The thesis is simple but powerful: JR East is not a railroad company. It is a massive data, fintech, and real estate conglomerate that uses the world's most efficient railway as a customer acquisition funnel. The railroad is the moat. Everything else is the castle.

This is the story of how a bankrupt government monopoly became one of the most sophisticated infrastructure businesses on the planet — from the chaotic 1987 privatization that created it, through the Suica revolution that turned a train ticket into a digital wallet, to the post-COVID strategic pivot that may define its next half-century.

Along the way, we will examine the $4 billion bet on Takanawa Gateway City, the quiet genius of station retail economics, and why a company trading at roughly 18 times earnings with a market capitalization of about $27 billion might be either profoundly undervalued or a slow-motion demographic trap.

The answer, as with most great businesses, depends entirely on which version of JR East you believe in.

Before we begin, a note on comparisons. There is no true global analog to JR East. MTR Corporation in Hong Kong comes closest — a transit operator that makes significant money from property development — but MTR operates in a city-state, not across an entire region. The US Class I railroads (Union Pacific, BNSF, CSX) are freight operations with entirely different economics. European national railways remain largely government-owned and subsidy-dependent. JR East is sui generis: a privately listed, formerly state-owned passenger railway that doubles as a fintech company, a real estate developer, a hotel operator, and a retail conglomerate, operating in the world's third-largest economy with the world's most transit-dependent urban population.

Understanding JR East requires holding multiple mental models simultaneously. It is a utility and a growth company. It is a physical asset business and a digital platform. It is a beneficiary of Japanese urban density and a victim of Japanese demographic decline. The tension between these identities is not a flaw in the investment thesis; it is the investment thesis.

II. The JNR "Big Bang": From Bankruptcy to Privatization

To understand JR East, you have to understand the catastrophe that created it. And to understand that catastrophe, you have to go back to 1964 — the year Japan opened the world's first high-speed rail line, the Tokaido Shinkansen, just in time for the Tokyo Olympics. It was a triumph of engineering, a source of immense national pride, and the beginning of a financial disaster that would take two decades to metastasize.

Japanese National Railways — JNR — was a government-owned monopoly that operated every rail line in Japan. In 1964, the year the bullet train debuted, JNR posted its first operating loss. Nobody panicked. The Shinkansen was a marvel. Japan's economy was booming. Losses were a rounding error in the national budget.

But the losses never stopped. JNR was run like a government ministry, not a business. Labor unions wielded enormous power — at one point, JNR employed 277,000 workers, of whom an estimated 93,000 were surplus. Think about that ratio: roughly one in three employees was, by the government's own assessment, unnecessary. These were not lazy people; they were products of a system where job creation was considered a social good, where firing a government employee was politically unthinkable, and where union agreements locked in staffing levels that bore no relationship to operational needs.

Politically motivated route expansions built lines to rural districts that would never generate enough riders to cover operating costs, let alone capital investment. A Diet member from a remote prefecture could secure a new rail line as a form of pork-barrel spending, knowing that the costs would be absorbed by JNR's balance sheet rather than by local taxpayers. Fare increases required Diet approval, a process so politically toxic that fares chronically lagged inflation.

And the debt compounded. Year after year, decade after decade, JNR borrowed to cover operating losses, borrowed to build new lines, borrowed to service existing borrowings.

By the mid-1980s, JNR's cumulative debt had reached 37.1 trillion yen — at the time, one of the largest corporate debts in human history, exceeding the GDP of most nations. The organization had become a textbook case of what happens when you combine a monopoly's complacency with a government's inability to make hard decisions. The trains still ran, but the institution was rotting from within.

To put 37.1 trillion yen in perspective: at the 1986 exchange rate, this was roughly $240 to $280 billion — a figure that dwarfed the national debts of many developing nations. JNR was, quite literally, the most indebted organization on the planet. The interest payments alone consumed a staggering share of revenue, creating a vicious cycle where borrowing to pay interest required more borrowing, which generated more interest. It was a debt spiral with no market discipline to arrest it, because the government kept guaranteeing the bonds.

Prime Minister Yasuhiro Nakasone, a reformer with a Thatcherite bent, decided to act. The plan was radical: break JNR into pieces, privatize the pieces, and let market discipline do what political will could not. Nakasone faced fierce opposition. The railway labor unions, among the most powerful in Japan, saw privatization as an existential threat — and they were right. The breakup would eliminate tens of thousands of jobs and shatter the unions' bargaining power. Political allies in rural districts feared that private operators would abandon unprofitable rural lines. Within the Liberal Democratic Party itself, factions aligned with the unions fought the plan at every stage.

But Nakasone prevailed through a combination of political skill and public outrage. A series of illegal strikes by JNR workers in the 1970s and 1980s had eroded public sympathy for the unions. Nakasone skillfully framed privatization not as an attack on workers but as a rescue of the railways from bureaucratic decay. The legislation passed, and on April 1, 1987, JNR ceased to exist. In its place stood seven new companies — three passenger operators on the main island of Honshu (JR East, JR Central, JR West), three on the smaller islands (JR Hokkaido, JR Shikoku, JR Kyushu), and one freight company.

The debt was carved up with surgical pragmatism. About 60 percent — roughly 25.5 trillion yen — went to the JNR Settlement Corporation, a government entity created specifically to manage the toxic legacy. The remaining 40 percent was divided among the Honshu companies and JR Freight. The three island companies were exempted entirely; their markets were too thin to bear the burden. Even after years of asset liquidation, roughly 16.7 trillion yen in residual debt was ultimately absorbed by Japanese taxpayers.

But here is where the story gets interesting, because not all pieces of the breakup were created equal.

JR East won the geography lottery. When the map was drawn, JR East inherited the Tokyo metropolitan area — the densest, wealthiest, most transit-dependent commuter market on Earth.

Consider what this means in practical terms. The Yamanote Line, the circular artery that connects Tokyo's major business districts — Shinjuku, Shibuya, Ikebukuro, Tokyo, Ueno — carries more passengers daily than the entire London Underground. The Chuo Line, the Sobu Line, the Keihin-Tohoku Line — these are the arteries that funnel millions of suburban commuters into the capital every morning and disperse them every evening. Greater Tokyo, with roughly 37 million residents, is the largest metropolitan area in human history, and its population density makes private automobile commuting impractical for most workers. The train is not a choice; it is a necessity.

And critically, JR East received the Tohoku Shinkansen (running north from Tokyo to Sendai and beyond) and the Joetsu Shinkansen (connecting Tokyo to Niigata and the ski country). JR Central got the Tokaido Shinkansen — the golden Tokyo-Osaka route, the busiest high-speed rail corridor in the world — but JR East got everything else in the nation's economic heartland. The Tohoku Shinkansen, in particular, would prove enormously valuable as tourism to northern Japan grew and as extensions to Shin-Aomori and later Shin-Hakodate-Hokuto connected Tokyo to previously remote destinations.

The cultural transformation was arguably harder than the financial restructuring. JNR's workforce had spent decades in a government bureaucracy where customer satisfaction was an afterthought and accountability was diffuse. The classic example: JNR ticket clerks were notorious for their indifference, sometimes ignoring passengers or responding to questions with bureaucratic condescension. Station restrooms were poorly maintained. Information boards were confusing. The attitude was that of a monopoly that knew its customers had no alternative.

Overnight, these same workers were expected to become "customer-obsessed" employees of a profit-seeking corporation. The early years were a struggle of identity. Old habits died hard. Union politics remained complicated. But the pressure of public listing — JR East's shares began trading in 1993, and the government fully divested its stake by 2002 — created a relentless gravitational pull toward commercial discipline.

The transformation was visible in small details that, cumulatively, amounted to a revolution. Station restrooms were renovated to hotel-like standards. Platform attendants were trained in customer service. Information systems were redesigned with the passenger's perspective in mind. The famous white gloves worn by platform staff — originally a practical measure to keep hands clean — became a symbol of JR East's obsessive attention to detail. By the late 1990s, foreign visitors to Japan regularly cited the train system as one of the most impressive aspects of the country. What they were witnessing was not some inherent Japanese cultural trait; it was the result of a deliberate, painful corporate transformation that took a decade to accomplish.

The Shinkansen lease arrangement was a particularly elegant piece of financial engineering — and understanding it illuminates how JR East's balance sheet came to look the way it does today.

Initially, the bullet train infrastructure was not given to the JR companies. It was held by a separate entity, the Shinkansen Holding Corporation, and the JR companies paid lease fees to use the tracks and facilities. This was a deliberate design: it allowed the government to retain the most valuable assets while testing whether the newly private companies could manage themselves responsibly.

In 1991, four years after privatization, these assets were sold to the operating companies, with JR East taking ownership of the Tohoku and Joetsu lines. The purchase price was structured to allow the debt to be serviced from operating cash flows, but it loaded JR East's balance sheet with long-term obligations that took years to work down. Even today, the legacy of this acquisition is visible in JR East's debt levels — the company carries nearly 5 trillion yen in total debt, a figure that partly reflects the original Shinkansen purchase financing and subsequent infrastructure investments.

By 2002, when the government sold its final shares, JR East had completed one of the most remarkable corporate transformations in postwar Japan. The stock, which had begun trading on the Tokyo Stock Exchange in 1993, had proven its viability to public market investors. The company was generating consistent operating profits, its safety record was exemplary, and it had built a reputation for customer service that contrasted starkly with the JNR era.

It had gone from a piece of a bankrupt government monopoly to a fully independent, publicly listed company. But the leaders who engineered that transition understood something that outside observers often missed: running trains well was necessary but not sufficient. The real opportunity was in what happened around the trains.

That insight would take another decade to fully flower — and it would start with a small plastic card.

But before we get to that card, it is worth pausing on what JR East had actually achieved by the early 2000s. The company had reduced its workforce from the bloated JNR-era levels to a lean, commercially focused organization. It had invested heavily in station renovations, turning grimy commuter hubs into clean, well-lit, architecturally thoughtful spaces. It had introduced the "Green Car" premium class on commuter lines, capturing higher-yield passengers willing to pay for a guaranteed seat and quiet carriage. And it had begun, tentatively, to experiment with retail operations inside its stations — the early seeds of what would become the ekinaka revolution.

The company's first president, Masatake Matsuda, set the tone: safety first, customer second, profit third — but all three were non-negotiable. His successor, Mutsutake Otsuka, accelerated the commercial pivot. By the time Satoshi Seino took the presidency in 2000, the strategic question had shifted from "can we survive as a private company?" to "what kind of company should we become?" The answer would be delivered not by a management consultant or a strategic planning committee, but by a small plastic card with a penguin on it.

III. The Suica Revolution: The "Hidden" Fintech Giant

On November 18, 2001, JR East introduced a small contactless smart card called Suica — short for "Super Urban Intelligent Card." The penguin mascot was cute. The technology, based on Sony's FeliCa near-field communication chip, was state-of-the-art. The initial use case was modest: tap the card at a turnstile instead of feeding a paper ticket into a slot. No more fumbling for exact change. No more studying fare tables. Just tap and go.

It sounds trivial now, in an age of Apple Pay and contactless everything. But in 2001, this was genuinely revolutionary. The world's first large-scale contactless transit payment system. To appreciate why, consider what the alternative looked like. Before Suica, a Tokyo commuter buying a train ticket had to check the fare map — an enormous, color-coded grid hanging above every ticket machine — find their destination, calculate the correct fare, insert coins or bills, and collect their magnetic strip ticket. At busy stations during rush hour, the queue for ticket machines could stretch twenty deep. The entire process took one to three minutes per person. Suica reduced it to 0.2 seconds — the time for the FeliCa chip to communicate with the reader through near-field communication, a form of short-range radio technology that works when the card is held within about ten centimeters of the reader. No authentication required. No PIN. No signature. Just proximity and speed.

And what happened next is a masterclass in platform strategy — one that predates the Silicon Valley playbook by nearly a decade.

The first insight was speed of adoption. Within three years, JR East had distributed over 10 million Suica cards. The reason was structural: JR East did not need to convince people to adopt a new behavior. People already rode trains every day. The card simply made an existing behavior faster and more pleasant. This is the dream of every fintech founder — distribution that requires zero customer acquisition cost because the customer is already standing in your store.

The second insight was the pivot. In 2004, JR East added electronic money functionality to Suica. Now the card was not just a train ticket; it was a wallet. Commuters could use it to buy a coffee at the station kiosk, a newspaper at the convenience store, a sandwich from the bakery. The transaction was instant — a fraction of a second to tap, far faster than inserting a credit card or counting coins. In a culture that prizes efficiency and abhors wasted time, this speed was not a feature. It was the product.

The third insight was interoperability — and this is where JR East displayed strategic patience that would make any platform strategist envious.

In March 2007, Suica became compatible with PASMO, the IC card used by Tokyo's private railways and subway systems. This was not a trivial negotiation. PASMO was operated by a consortium of JR East's competitors — the private railways and metro operators that ran parallel and connecting services in the Tokyo area. Getting them to agree to interoperability meant convincing rivals that a shared platform was better for everyone, even though JR East, with its larger network and earlier launch, would inevitably be the primary beneficiary.

By March 2013, JR East had extended this interoperability nationwide across ten major IC card systems — PASMO, ICOCA, TOICA, manaca, Kitaca, SUGOCA, nimoca, hayakaken, and PiTaPa. A single Suica card now worked on virtually every major transit system in Japan, plus at a growing network of retail merchants.

The network effect was extraordinary: every new merchant that accepted Suica made the card more valuable to every cardholder, and every new cardholder made the network more attractive to every merchant. This is the same dynamic that powered the growth of credit card networks in the twentieth century, but Suica achieved it faster because the installed base of daily commuters provided instant critical mass.

By 2016, Apple came knocking. When Apple launched the iPhone 7 in Japan in September of that year, Suica was integrated directly into Apple Pay. This was not a concession by JR East to Apple's ecosystem; it was a recognition by Apple that Suica's installed base and transaction velocity in Japan were too large to ignore.

The integration was technically elegant. Users could add their Suica card to the Apple Wallet app and use their iPhone or Apple Watch to tap through turnstiles and make purchases — no separate card needed. For Apple, it was a way to drive iPhone adoption in Japan, one of the few markets where the company had to adapt to local infrastructure rather than impose its own. For JR East, it was a distribution multiplier: suddenly, every iPhone user in Japan was a potential Suica user, without JR East having to manufacture or distribute a single physical card.

Mobile Suica — originally launched for FeliCa-equipped flip phones back in 2006, a decade before Apple Pay existed — had found its ultimate hardware partner.

Today, there are over 112 million Suica cards in circulation, more than double the roughly 43 million PASMO cards issued by competitors. Approximately 33 million Mobile Suica accounts are active. Over 1.63 million merchants across Japan accept Suica payments. Monthly transaction volumes in Tokyo alone exceeded 300 million by mid-2024. To put that in context: Suica processes more contactless transactions in the Tokyo metropolitan area than most national payment networks handle across entire countries.

But the numbers only tell part of the story. The real asset is the data.

When a Suica holder taps into Shinjuku Station at 7:42 AM, buys a latte at BECK'S COFFEE SHOP at 7:48, arrives at Tokyo Station at 8:15, and purchases a bento at GranSta at 12:30 — JR East sees all of that. The company knows where its customers travel, when they travel, where they shop, what they buy, and how much they spend. This is first-party behavioral data of staggering richness, collected passively from millions of people every day.

The JRE POINT ecosystem ties it all together. By registering a Suica card with JRE POINT, users accumulate loyalty points across the entire JR East universe — train rides, station retail, online shopping, credit card purchases through the JR East-branded VIEW Card. Points can be redeemed for Suica balance top-ups, merchandise, or services.

Think of it as JR East's version of the Amazon Prime flywheel, but built on physical infrastructure rather than e-commerce logistics. The more you use JR East's services, the more points you earn. The more points you earn, the more incentive you have to stay within the JR East ecosystem for your next purchase. It is a closed-loop flywheel: ride the train, earn points, spend points at JR East properties, ride the train again. Every revolution of the wheel deepens the customer's dependency on — and satisfaction with — the JR East platform.

And JR East is just getting started. The Suica roadmap through 2029 reads like a fintech startup's pitch deck, and each milestone represents a meaningful expansion of the platform's capabilities and monetization potential.

By autumn 2025, ticketless Shinkansen travel via Suica was expected to launch — eliminating the need for separate bullet train tickets and further embedding Suica into the travel experience. By autumn 2026, code-based payments will remove the current 20,000 yen (roughly $130) ceiling on Suica balances, a limitation that has prevented the card from competing with credit cards for larger purchases. This single change could dramatically expand Suica's addressable transaction volume.

By spring 2027, the service area will expand across seven regions, bringing Suica's convenience to parts of Japan that currently rely on cash or legacy ticket systems. And by 2029, the plans become genuinely ambitious: subscription fare plans with discounts of up to 50 percent, walk-through gates that use smartphone location data instead of requiring a tap, and peer-to-peer money transfers that would position Suica as a competitor to apps like PayPay and LINE Pay.

Perhaps most intriguing is the "Community Suica" concept — integration with municipal services such as library cards, local government payments, and health services. If realized, this would transform the card from a transit-and-shopping tool into a civic infrastructure layer, embedding JR East's platform into the administrative fabric of daily life in eastern Japan.

The analogy that best captures what JR East has built is not another railway company. It is WeChat Pay — but deployed through physical infrastructure rather than a social media app, and backed by a century of trust in Japanese rail reliability. JR East beat the banks at their own game not through regulatory arbitrage or aggressive marketing, but through the quiet accumulation of habitual daily use. When 17 million people tap the same card every morning, you do not need to advertise.

The question for investors is whether this fintech platform is properly valued. Currently, it sits buried inside a conglomerate that the market prices as a railroad utility.

Consider the contrast. If Suica were a standalone company with 112 million cards, 33 million mobile accounts, and 300 million monthly transactions, venture capitalists would be climbing over each other to invest. In the late 2010s and early 2020s, payment companies with a fraction of Suica's scale — fewer cards, fewer transactions, less data — commanded valuations in the tens of billions of dollars. Square (now Block), Stripe, and PayPay all built billion-dollar businesses on the promise of ubiquitous digital payments. Suica has been delivering on that promise since 2004, but the market assigns it no separate value.

Instead, it is a line item in JR East's "IT & Suica Services" segment — the fastest-growing, lowest-capital-intensity part of the business, hidden behind the lumbering bulk of track maintenance and rolling stock depreciation.

That asymmetry between perception and reality is, arguably, the single most important thing to understand about JR East as an investment.

There is one more dimension worth exploring: the competitive landscape. Japan's other major IC cards — PASMO (operated by the consortium of private railways and metro operators in Tokyo), ICOCA (JR West), and TOICA (JR Central) — all use the same FeliCa technology and are all interoperable. But none have achieved Suica's scale or mindshare. PASMO has roughly 43 million cards in circulation — less than half of Suica's 112 million. The reason is partly distribution (JR East's network is larger) and partly timing (Suica launched first and captured the behavioral habit before competitors could match it). There is a first-mover advantage in daily habits that is nearly impossible to overcome once established. Ask any consumer psychologist: the hardest behavior to change is the one performed unconsciously, every day, at the same time, in the same place. Suica owns that behavior for tens of millions of Japanese.

The banks, for their part, have watched this unfold with a mixture of admiration and alarm. Japan's banking sector spent decades trying to move the country from cash to electronic payments. Suica accomplished it in station corridors and convenience stores before the banks could deploy their own contactless solutions. The irony is rich: a railway company, not a financial institution, built Japan's most successful digital payment platform. It is a reminder that in platform businesses, distribution trumps sophistication every time.

IV. The "Station Renaissance": Real Estate and Lifestyle

Walk into Tokyo Station's GranSta shopping area and you might forget you are in a train station. The lighting is warm. The flooring is polished stone. The tenants include high-end patisseries, artisanal sake shops, curated gift boutiques, and restaurants with Michelin-starred pedigrees. There are over 150 retailers spread across a subterranean complex that stretches from the Marunouchi side to the Yaesu side of the station. On a busy day, foot traffic rivals the Champs-Élysées.

This is not an accident. It is the product of a deliberate, decades-long strategy that JR East executives call the transition from "Transportation" to "Life-style Support." The logic is disarmingly simple: if 17 million people walk through your properties every day, you have two choices. You can charge them a train fare and wave goodbye, or you can capture a share of every other transaction in their day — their coffee, their lunch, their gifts, their groceries, their dry cleaning, their gym membership, their hotel stay. JR East chose the second path, and the results have been transformative.

The "ekinaka" concept — literally "inside the station" — was formalized in the early 2000s. Rather than treating stations as utilitarian transit nodes, JR East began reimagining them as destinations. The idea was deceptively simple but operationally challenging: convert underused spaces within the paid fare zone — the area between the ticket gates where passengers wait for trains — into high-quality retail environments.

The ecute brand, launched at major terminal stations in the Tokyo area, was the proof of concept. It turned ticket-gate-adjacent dead space into curated retail environments featuring bakeries, flower shops, and specialty food retailers. GranSta, which opened at Tokyo Station in 2007, elevated the concept further, creating a subterranean shopping and dining landmark that rivaled purpose-built department stores. And Lumine — perhaps the crown jewel of the portfolio — positioned station-adjacent commercial complexes as fashion-forward retail destinations targeting young professional women, with locations at Shinjuku, Ikebukuro, Omiya, and other key stations.

Lumine's success deserves particular attention because it illustrates a counterintuitive insight about station retail economics. Conventional wisdom says that the best retail locations are purpose-built malls or high-street storefronts where shoppers go with the intent to browse. Station retail, by contrast, captures people in transit — commuters who have five minutes to kill, travelers waiting for a connection, workers grabbing dinner ingredients on the way home. These are not leisurely shoppers; they are time-pressed, decision-fatigued people who want convenience and quality in equal measure.

It turns out that this is an incredibly valuable customer profile. Conversion rates at station retail properties tend to be exceptionally high because the foot traffic is captive and recurring. A commuter who walks past the same bakery at 7:50 every morning is not browsing; she is making a purchase decision with extremely low friction. The revenue-per-square-foot figures at top-performing ekinaka properties are among the highest in Japanese retail — and Japanese retail already benchmarks well above global averages. Consider the advantage from a landlord's perspective: JR East does not need to spend money on marketing to drive foot traffic to its retail properties. The trains do that automatically, every day, for free. Every retailer in a JR East station benefits from the same captive audience. This is a structural advantage that standalone malls, high-street retailers, and even airport concessions cannot match.

There is also a curation element that distinguishes JR East's retail strategy from generic mall development. Lumine, for instance, refreshes its tenant mix frequently, rotating in new brands and pop-up concepts to keep the shopping experience dynamic. The company tracks purchasing patterns through Suica and JRE POINT data, using those insights to optimize tenant selection and store placement. A bakery that generates high morning foot traffic is positioned near the entrance closest to the ticket gates. A gift shop that sees evening spikes is placed along the exit corridor used by homebound commuters. This is retail science applied with Japanese precision, informed by a depth of consumer data that most retailers would envy.

JR East now operates 193 shopping centers. In April 2021, the company consolidated four group retail companies into JR East Cross Station, integrating NewDays convenience stores, BECK'S COFFEE SHOP, vending machine operations, and ekinaka facilities under a single management structure. In February 2025, JR East went further, announcing the full absorption of Lumine Co. and JR East Department Store Co. as wholly-owned subsidiaries. The message was clear: station retail is not a side business. It is core strategy.

The segment-level economics tell a compelling story, and understanding them is essential for anyone trying to value JR East properly.

Transportation accounts for roughly 60 percent of consolidated revenue, but it is enormously capital-intensive. The company spent over 770 billion yen on capital expenditure in fiscal year 2025, much of it on track maintenance, rolling stock replacement, and station infrastructure upgrades. This is the segment that generates the headlines but also consumes the lion's share of capital.

Retail and services, by contrast, generate high margins on relatively modest capital. The infrastructure already exists — the stations are built, the foot traffic is guaranteed — so each incremental retail dollar flows through with minimal additional investment.

Real estate — office towers, hotels, and commercial developments built on station-adjacent land — is the highest-margin segment of all, because the underlying land was effectively acquired for free during the 1987 privatization. Every yen of rental income from a station-adjacent office building drops almost entirely to the bottom line, net of operating expenses and depreciation on the building itself. The land contributes nothing to the cost base because it was never purchased at market rates.

And then there is IT and Suica — the smallest segment by revenue but the highest-growth, lowest-asset-intensity part of the business. This is the segment with the most optionality, and the one where the gap between current contribution and future potential is widest.

Which brings us to Takanawa Gateway City, the single largest capital deployment decision in JR East's history.

The project occupies roughly 10 hectares of former rail yard between Shinagawa and Tamachi stations on the Yamanote Line. This was industrial land — sidings, depots, maintenance facilities — that JR East inherited in 1987 and held on its books for decades at historical cost, which is to say, nearly nothing. The development plan calls for five major buildings, including THE LINKPILLAR 1, a 46-story office and commercial tower that opened on March 27, 2025, and THE LINKPILLAR 2, a mixed-use complex scheduled for completion in spring 2026. NEWoMan TAKANAWA — Lumine's largest facility, with approximately 180 stores — opened on September 12, 2025. The total investment is estimated at 500 to 600 billion yen, or roughly $3.3 to $4 billion.

Is this a trophy project or a calculated masterstroke?

The bear case is straightforward: Tokyo's office market already has significant vacancy, remote work has structurally reduced demand for premium commercial space, and a $4 billion bet on a single development concentrates risk uncomfortably. Other Tokyo mega-developments — Mori Building's Azabudai Hills, Mitsubishi Estate's Marunouchi renovations — are competing for the same pool of premium tenants. Supply is rising. Demand is uncertain.

The bull case rests on location and irreplaceability. Takanawa Gateway sits on the Yamanote Line between Shinagawa — a Shinkansen hub and the future terminal for JR Central's maglev Chuo Shinkansen, which will eventually connect Tokyo to Nagoya in 40 minutes — and central Tokyo. The site is a five-minute train ride from Tokyo Station and directly connected to Haneda Airport via the Keikyu Line at Shinagawa.

You cannot create this land. You cannot replicate this connectivity. And JR East is positioning the development not as conventional office space but as an innovation district — a "global gateway" with smart-city features including autonomous transport, robotic services, and digital infrastructure designed to attract international businesses and startups. The vision is explicitly modeled on the idea that physical proximity still matters for innovation, even in an age of remote work, and that the companies willing to pay premium rents are precisely those that value the serendipitous collisions that dense, well-designed urban environments produce.

The financial logic ultimately comes down to yield. If JR East can generate a 4 to 5 percent cap rate on a development whose land cost is effectively zero, the returns on invested capital become extremely attractive — even before accounting for the increased retail and transit revenue from the station itself. Takanawa Gateway Station, which opened on March 14, 2020, adds a new node to the Yamanote Line and a new catchment area for JR East's entire commercial ecosystem.

For investors, the key metric to watch in this segment is non-transportation revenue as a percentage of total revenue. In fiscal year 2025, JR East generated approximately 2.89 trillion yen in total revenue. If the company can push non-rail revenue toward 50 percent of the total — driven by Takanawa Gateway, Suica platform expansion, and retail consolidation — it fundamentally changes the earnings quality and valuation multiple the market should assign.

The hotel business, while smaller than retail and office real estate, deserves a mention as well. JR East operates hotels totaling 9,190 guest rooms, strategically located at or near major stations. The Hotel Metropolitan brand serves business travelers; the JR East Hotel Mets brand caters to budget-conscious guests; and the higher-end properties at developments like Takanawa Gateway target international visitors and premium corporate travel. The inbound tourism boom — fueled by the weak yen and Japan's post-pandemic reopening — has been a powerful tailwind for this segment. Hotel occupancy rates in Tokyo have surged, and JR East's station-adjacent locations give it a structural advantage over competitors whose properties require a taxi ride from the nearest transit hub.

The broader point is this: every piece of JR East's non-transportation business — retail, real estate, hotels, Suica — benefits from the same underlying asset: captive foot traffic at irreplaceable locations. The question is not whether these businesses are good. They are clearly excellent. The question is whether they can grow fast enough, and large enough, to redefine JR East's earnings profile before demographic gravity pulls the core transportation business into secular decline.

The answer to that question was shaped by two events that tested the company's resilience more severely than anything since privatization.

V. The Decades of Defiance: 2011 and 2020

At 2:46 PM on March 11, 2011, the Pacific seafloor lurched. A magnitude 9.0 earthquake — the most powerful ever recorded in Japan — sent seismic waves racing westward at kilometers per second toward the Tohoku coast and, beyond it, the dense rail corridors of eastern Honshu. At that exact moment, 33 Shinkansen trains were operating on JR East's network, 19 of them in motion at speeds of up to 275 kilometers per hour.

What happened in the next twelve seconds may be the single most important engineering story in modern rail history.

JR East's Urgent Earthquake Detection and Alarm System — UrEDAS — comprised seismometers at 97 locations along its rail network. The sensor at Kinkazan, closest to the epicenter, detected the initial P-waves at 2:46:38 PM. By 2:47:02 — roughly 24 seconds later — the system had analyzed the waveform, estimated the earthquake's magnitude and location, and transmitted emergency stop commands to every Shinkansen train on the network. Power to the overhead catenary lines was cut simultaneously. The trains began braking before the destructive S-waves arrived.

Not a single passenger was killed. Not a single Shinkansen derailed.

Let that sink in. At 275 kilometers per hour, with 24 seconds of warning, the trains had already begun decelerating when the ground started shaking violently beneath them. In the entire history of Japan's Shinkansen — over six decades of operation since 1964 — there has never been a single passenger fatality due to derailment or collision. The 2011 earthquake was the system's most extreme test, and it passed flawlessly.

The conventional rail network was less fortunate. The tsunami that followed the earthquake devastated the Pacific coast of Tohoku. Twenty-three stations were destroyed. 325 kilometers of conventional rail lines were washed away. Five passenger trains derailed. Track was displaced at 2,590 locations. Over 1,150 electrification masts were broken or damaged. The physical destruction was immense. JR East recorded a special loss of 5.8 billion yen that fiscal year and held earthquake insurance with a maximum payout of 71 billion yen.

But the recovery was extraordinary. The Tohoku Shinkansen resumed full operations just 49 days after the earthquake — a feat of logistical coordination that stunned the global engineering community. Conventional lines took longer, and some coastal routes were permanently rerouted to higher ground, a decision that reflected a fundamental shift in JR East's risk calculus. The company invested heavily in enhanced seismic reinforcement, particularly for Shinkansen viaducts and bridge piers, accepting the enormous capital cost as the price of the resilience that had saved thousands of lives.

The 2011 earthquake proved that JR East's safety culture — inherited from the engineering-led traditions of JNR and hardened through decades of investment — was not just a corporate talking point. It was a genuine operational capability, stress-tested under the most extreme conditions imaginable.

To understand the significance of UrEDAS, a brief technical explanation helps. Earthquakes produce two types of seismic waves. P-waves (primary waves) travel fast but cause relatively little damage — they are the tremor you feel first, the rumble that makes windows rattle. S-waves (secondary waves) travel slower but carry the destructive energy that collapses buildings and derails trains. The time gap between P-wave arrival and S-wave arrival is typically seconds to tens of seconds, depending on distance from the epicenter. UrEDAS exploits this gap. By detecting and analyzing P-waves at the speed of computation, it can issue emergency commands before the destructive S-waves arrive. It is, in essence, a system that trades on the speed difference between two types of waves — buying precious seconds of warning through pure physics and fast processing. For a Shinkansen traveling at 275 kilometers per hour, those seconds translate to hundreds of meters of braking distance.

After 2011, JR East invested aggressively in next-generation seismic technology, including more sensitive coastal seismometers and faster computational algorithms. The company also undertook a massive structural reinforcement program for Shinkansen viaducts, a multi-year effort costing hundreds of billions of yen. The decision was made with a clear-eyed understanding that earthquakes are not "if" events in Japan — they are "when" events — and that the reputational and human cost of a Shinkansen derailment would be existential.

But the earthquake also revealed a deeper vulnerability: JR East's revenue was overwhelmingly dependent on people physically riding trains. When the trains stopped, everything stopped. Tourism to Tohoku collapsed. Business travel evaporated. The regional economy, heavily dependent on the rail network, contracted sharply. JR East found itself not just repairing infrastructure but financing regional recovery, a burden that would have been unthinkable for a private company in most other countries but was expected — even demanded — of JR East, given its quasi-public role in eastern Japan's economic life.

That lesson would return with devastating force nine years later.

When COVID-19 hit Japan in early 2020, the impact on JR East was swift and brutal. Consider the economics of a railway system during a pandemic. Unlike a factory that can idle production lines and lay off workers, a railway cannot simply stop running. The track must be maintained. The signals must operate. The stations must be staffed for safety. The trains must run — even if nearly empty — because the railway is essential infrastructure. The costs are almost entirely fixed, but the revenue is almost entirely variable. When ridership drops, the operating leverage that makes railways profitable in good times becomes a financial guillotine.

Daily ridership, which had been running at roughly 17 million passengers, collapsed. Shinkansen usage plummeted 50 to 70 percent. Even commuter lines — the bedrock of the business — saw ridership fall by 40 percent as companies adopted remote work and the Japanese government declared states of emergency. Golden Week 2020, normally a peak travel period, saw Shinkansen ridership drop by over 90 percent compared to the prior year. Stations that ordinarily teemed with thousands of commuters per minute fell eerily silent.

The financial results were unprecedented.

In fiscal year 2021, ending March 2021, revenue cratered to 1.765 trillion yen — a decline of roughly 40 percent from pre-pandemic levels. The operating loss was 520.4 billion yen. The net loss was 577.9 billion yen — the worst in JR East's history and a staggering figure for a company that had been consistently profitable for three decades. To put the scale of loss in perspective: JR East lost more money in a single year during COVID than most Japanese companies earn in a decade.

The following year brought another operating loss of 153.9 billion yen, meaning JR East endured two consecutive years of operating losses for the first time in its existence as a private company. S&P Global downgraded the company's credit rating to A+, reflecting the deterioration in financial metrics.

JR East raised over a trillion yen in new debt during fiscal year 2021 to fund the cash burn, pushing total debt from roughly 4.4 trillion yen to levels that would peak near 5 trillion yen. The company issued bonds and drew down credit facilities at a pace it had never before contemplated. For a company already carrying significant legacy debt from the Shinkansen acquisition, this was an uncomfortable expansion of leverage.

But there was no alternative. A railway cannot shut down. The costs kept running. The revenue did not.

But here is where the story turns. COVID-19 was not merely a crisis for JR East; it was the most important strategic inflection point since privatization. When ridership dropped 90 percent at the trough, the company's leadership confronted a reality that had been slowly building for years but was easy to ignore as long as trains were full: the traditional commuter model — predicated on millions of salarymen riding the same route five days a week, fifty weeks a year — was structurally weakening.

Japan's working-age population has been declining since the late 1990s — a demographic trend that had been easy to ignore when train carriages were still packed at rush hour, but impossible to dismiss when those same carriages were empty.

Remote work, once culturally unthinkable in Japan, proved viable during the pandemic. Companies that had required daily office attendance began offering two or three days of remote work per week. The five-day commuter pass, once the foundation of JR East's revenue model, was losing relevance.

Management's response was to pivot from "quantity" to "quality" — from maximizing the volume of passengers to maximizing spending per passenger. This was not merely a tactical adjustment; it was a fundamental reimagining of the company's relationship with its customers.

The pivot meant accelerating every non-transportation initiative: station retail, real estate development, Suica monetization, tourism promotion, and a new concept called "workation" — blending work and vacation by encouraging travelers to use JR East's network for leisure trips to onsen towns, ski resorts, and rural retreats in the Tohoku and Niigata regions. JR East began marketing packages that combined Shinkansen tickets with hotel stays and local experiences, effectively becoming a travel platform rather than merely a transportation provider. The company introduced new premium Shinkansen services, upgraded onboard amenities, and invested in regional destination marketing that promoted the underappreciated beauty of Tohoku — the dramatic coastlines, the hot spring villages, the autumn foliage — to both domestic and international travelers.

The recovery trajectory tells the story of that pivot. Fiscal year 2023 revenue rebounded to 2.406 trillion yen, with a return to operating profitability at 140.6 billion yen — a relief for a company that had just posted two consecutive years of operating losses for the first time in its history.

Fiscal year 2024 saw further acceleration to 2.730 trillion yen and operating income of 345.2 billion yen, driven by strong Shinkansen and tourism revenue. By fiscal year 2025, revenue reached 2.888 trillion yen — approximately 98 percent of pre-pandemic levels — with operating income of 376.8 billion yen and net income of 224.3 billion yen.

But the composition of that revenue had shifted meaningfully toward non-transportation sources. The recovery was not a simple return to the old normal; it was a restructured earnings base that reflected the "quality over quantity" strategy in action.

The pandemic did not break JR East. It forced the company to become, at an accelerated pace, the diversified lifestyle platform that its most forward-thinking leaders had always envisioned.

There is a myth in financial markets that JR East's COVID recovery was simply a reversion to mean — that people went back to offices and trains filled up again. The reality is more nuanced. Commuter ridership on JR East's metropolitan network has recovered to roughly 85 to 90 percent of pre-pandemic levels, but it has not returned to 100 percent, and management does not expect it to. The five-day-a-week commuter pass — once the single largest revenue line in the transportation segment — has been permanently impaired by hybrid work. What has recovered more strongly, and in some cases exceeded pre-pandemic levels, is discretionary travel: Shinkansen tourism, weekend getaways, and the growing inbound foreign tourist market. JR East's busiest stations tell the story. In fiscal year 2024, Shinjuku recorded 666,809 daily boarding passengers, up 2.5 percent year over year. Ikebukuro reached 499,128, up 1.9 percent. Tokyo Station, the hub for Shinkansen services and a magnet for tourists, posted 434,564 daily boardings — up 7.6 percent, a figure boosted by the tourism boom.

The composition of recovery matters enormously for the investment case. A tourist who takes the Shinkansen to Tohoku, stays at a JR East hotel, shops at a station mall, and pays for everything with Suica generates far more revenue per trip than a commuter who rides the same suburban line five days a week on a discounted monthly pass. The "quality over quantity" pivot is not just a slogan; it is visible in the unit economics of JR East's post-pandemic recovery.

The question now is whether this transformation is deep enough, and fast enough, to outrun Japan's demographic headwinds.

VI. Current Management: The Kise Era

Yoichi Kise took the helm as President and CEO of JR East on April 1, 2024, and his appointment carries a significance that extends beyond the routine rotation of Japanese corporate leadership. Born in 1964, Kise joined JR East in April 1989 — two years after privatization. He never worked at JNR. He has no memory of the government monopoly's bureaucratic culture, its labor battles, its institutional paralysis. He is, in a very literal sense, the first leader of JR East whose entire professional identity was forged within the privatized company.

This matters because JR East's leadership succession has followed a discernible arc. The first generation of presidents were JNR veterans who shepherded the transition from government entity to listed company. They were engineers and administrators who understood the physical railroad in their bones and prioritized safety, operational reliability, and the methodical repayment of legacy debt. The second generation, leaders like Tetsuro Tomita (president from 2018 to 2024), began the strategic pivot toward non-transportation revenue while maintaining the engineering culture's primacy. Kise represents the third generation — a leader whose formative experiences were not in rail operations but in corporate planning, human resources, and commercial strategy.

His career path is revealing. Kise started at the front lines — Ueno Station, Shinjuku Station — learning the operational basics that every JR East executive is expected to understand. In the JR East culture, no matter how senior you become, the expectation is that you understand what it feels like to stand on a platform at 7:30 AM during rush hour, managing the flow of thousands of commuters with precision and composure.

But Kise spent the core of his career not in operations but in strategy and investment planning roles. He was promoted to Executive Officer in 2015, Executive Director in 2018, and Executive Vice President in 2021 — a rapid ascent through the corporate hierarchy that reflected his role as a strategic architect rather than an operational specialist. As General Manager of the Management Planning Department, he was instrumental in formulating the "Move Up 2027" management vision. Most recently, before his appointment as president, he led the Marketing Headquarters, overseeing the growth strategies for JR East's Lifestyle Solutions businesses — retail, real estate, Suica, and digital services.

The signal is unmistakable: JR East's board selected a commercially minded leader, not an operations purist. This is a company that believes its next chapter will be written in real estate yield, digital platform economics, and customer lifetime value, not in incremental improvements to on-time performance (which is already near-perfect) or marginal reductions in maintenance costs.

Kise inherited the "Move Up 2027" plan, originally launched in 2018 as a ten-year management vision. The plan's core thesis — that JR East must transform from a transportation company into a lifestyle platform — proved prescient, though COVID-19 forced an unplanned stress test of the diversification strategy. Under Kise, the plan has entered its execution phase, with several concrete financial commitments.

The total shareholder return ratio target is 40 percent, combining dividends and buybacks. The dividend payout ratio is currently targeted at 30 percent, with plans to gradually increase to 40 percent by fiscal year 2028 as the Takanawa Gateway investment cycle matures.

These targets may sound modest by American standards, where capital return programs often exceed 100 percent of earnings. But in the context of Japanese corporate governance — where many companies historically viewed dividends as a necessary evil and buybacks as borderline improper — they represent a meaningful cultural shift. JR East is signaling that it understands the capital markets' expectations and is willing to balance long-term investment with near-term shareholder returns.

The Tokyo Stock Exchange's 2023 initiative — requesting all listed companies to take concrete action on cost-of-capital-conscious management — has added external pressure to this internal pivot. JR East trades at roughly 1.4 to 1.5 times book value, above the psychologically important 1.0x threshold that the TSE specifically called out. But the company's return on equity of approximately 7.8 percent in fiscal year 2025 remains below the 8 percent benchmark that many institutional investors consider minimum. Closing that gap — through a combination of earnings growth, capital efficiency, and shareholder returns — is a defining challenge of the Kise era.

JR East's shareholder base is predominantly institutional. Management's increasing focus on ROE, buybacks, and capital discipline reflects a broader shift across corporate Japan, but for a company of JR East's scale and legacy, every incremental point of ROE improvement requires moving enormous amounts of capital more efficiently. The consolidation of Lumine and JR East Department Store, the Suica platform expansion, and the Takanawa Gateway commercialization are all, at their core, ROE improvement initiatives — ways to generate higher returns on the vast asset base that JR East accumulated over four decades.

There is an important organizational detail that often gets lost in high-level strategy discussions. JR East is not a simple holding company with autonomous subsidiaries; it is an integrated operating company where the same management team oversees both the railway and the commercial businesses. This creates both advantages and risks. The advantage is strategic coherence: decisions about station design, retail tenant mix, Suica functionality, and real estate development are all made with full awareness of their impact on the transportation network and vice versa. The risk is distraction — the challenge of managing a world-class railway while simultaneously building a fintech platform, a real estate empire, and a retail conglomerate.

Kise's organizational restructuring has attempted to address this by creating clearer accountability for non-transportation businesses while maintaining integrated planning at the top. The Marketing Headquarters, which he led before becoming president, was designed to be the commercial engine — the team that figures out how to monetize the railway's captive audience. Under Kise, this function has gained influence relative to the traditional railway operations hierarchy, a shift that some long-time JR East employees view with unease but that the board clearly considers necessary.

Whether Kise can deliver on these ambitions while maintaining the safety and operational culture that makes the railroad valuable in the first place is the fundamental management question. The history of conglomerates attempting strategic pivots is littered with examples of leaders who chased growth in new areas while allowing the core business to deteriorate. Kise's challenge is to avoid that trap — to build the digital future without sacrificing the analog excellence that 17 million daily passengers depend on.

VII. The Playbook: 7 Powers and Strategy

Hamilton Helmer's "7 Powers" framework — the taxonomy of durable competitive advantages that separate extraordinary businesses from merely good ones — is a useful lens for analyzing any potential long-term investment. The framework identifies seven sources of strategic power: scale economies, network effects, counter-positioning, switching costs, branding, cornered resource, and process power. Most companies can credibly claim one or two. JR East possesses at least four, and arguably five. That concentration of strategic power is rare in any industry, and it is worth examining each one carefully.

Cornered Resource is the most obvious and the most powerful. JR East owns the land under and around Shinjuku Station, Tokyo Station, Ikebukuro Station, Ueno Station, and dozens of other irreplaceable nodes in the world's largest metropolitan rail network. This is not real estate that a competitor can replicate. You cannot build another Shinjuku. You cannot create another Yamanote Line.

The 1987 privatization handed JR East a portfolio of urban land assets that had been accumulated over a century of government railway construction, much of it acquired when Tokyo was a fraction of its current size and land values were a fraction of current levels. Some of these station sites were originally farmland or marshland purchased in the Meiji era for negligible sums. Today, land around Shinjuku Station alone is worth a fortune that defies easy calculation.

These assets sit on JR East's balance sheet at historical cost, which means the gap between book value and market value is vast — and largely invisible to investors who look only at reported financials. The company's total property, plant, and equipment is recorded at approximately 7.79 trillion yen, but the market value of the station-adjacent real estate portfolio alone could plausibly exceed that figure. This is the hidden balance sheet that makes JR East's reported book value misleading as a measure of intrinsic worth.

Think of it this way: if JR East's core rail network is a moat, the station real estate is the castle, and the land under the stations is the bedrock. No amount of capital can recreate it.

Switching Costs manifest through the Suica and JRE POINT ecosystem. Once a consumer has a Suica card linked to their phone, registered with JRE POINT, connected to a VIEW credit card, and integrated into their daily commute-shop-commute routine, the cost of switching to an alternative payment or transit system is not financial — it is behavioral. The entire rhythm of daily life in Tokyo is built around tapping a Suica card. Switching means disrupting every transaction in your day, from the morning train to the evening grocery run. The ecosystem is not locked by contract; it is locked by habit, which is far more durable.

Network Effects operate on two dimensions simultaneously, and this dual-network structure is what makes JR East's competitive position so unusual. On the payment side, every merchant that accepts Suica makes the card more valuable to every holder, and every new Suica holder makes acceptance more attractive to every merchant. This is the classic two-sided network effect that drives payment platform economics — the same dynamic that made Visa and Mastercard into trillion-dollar companies. The difference is that Suica's network effect is reinforced by physical infrastructure. You do not choose to accept Suica because a salesperson convinced you; you accept it because your store is in a train station where every customer already has one.

On the transportation side, the network effect is geographic: the more destinations accessible via JR East's rail network, the more people use it, and the more people who use it, the more economically viable it is to develop station-adjacent commercial properties, which in turn attract more riders. This creates a virtuous cycle that has been compounding for decades. When JR East opens a new retail facility at a station — as it did with NEWoMan TAKANAWA — it does not just generate retail revenue. It makes the station itself a destination, which increases ridership, which increases the value of nearby real estate, which attracts more retail investment. The flywheel spins.

Counter-Positioning is JR East's most creative strategic move, and it relates directly to the post-COVID pivot. The conventional competitor in Japanese transit — airlines for long-distance, private railways for urban — competes on the same dimension: moving people from point A to point B. JR East is counter-positioning by redefining what it sells. The "workation" concept — promoting rail travel to regional destinations for blended work-and-leisure trips — attacks the assumption that rail revenue requires daily commuters. By investing in tourism marketing, regional revitalization, and lifestyle experiences along its rural routes in Tohoku and Niigata, JR East is creating demand that did not previously exist. Airlines cannot replicate this because they do not own the destinations. Private railways cannot replicate it because they lack the Shinkansen's reach.

Scale Economies are present but nuanced. JR East's 7,401-kilometer network and 68,769 employees create cost advantages in procurement, maintenance, and technology development that smaller operators cannot match. The company's annual depreciation and amortization of roughly 419 billion yen reflects the scale of its physical asset base — but also the capital intensity that constrains returns. Scale is a double-edged sword: it creates cost advantages but also creates enormous fixed costs that must be covered regardless of ridership levels, as the pandemic painfully demonstrated.

From a Porter's Five Forces perspective, JR East's position is equally formidable. Barriers to entry are essentially insurmountable — no new entrant can build a competing rail network in the Tokyo metropolitan area. Supplier power is moderate; JR East is the dominant buyer of rolling stock and rail equipment in eastern Japan, giving it significant negotiating leverage. Buyer power is limited; commuters have few alternatives for their daily transit needs. Substitute threats are the most significant concern — remote work is a genuine structural substitute for commuting, and ride-hailing services nibble at the margins. Competitive rivalry is low in core commuter markets (no overlap with JR Central or JR West in the Tokyo area) but higher in discretionary travel, where airlines and private railways compete.

The strategic vulnerability — and this is critical for any honest assessment — is that JR East's greatest strengths are tied to a geographic market, Japan, that is experiencing demographic decline. The population peaked in 2008. The working-age population has been shrinking for even longer. Tokyo continues to grow through internal migration, which partially offsets national trends, but the math is inexorable: fewer people means fewer riders, and the trend is measured in decades, not quarters.

One power that JR East arguably does not possess, and the absence is instructive, is Process Power — the kind of proprietary operational advantage that Toyota holds in manufacturing or Amazon holds in logistics. JR East's operational excellence is extraordinary, but it is not proprietary. The techniques that make Shinkansen operations world-class — precision scheduling, UrEDAS earthquake detection, meticulous maintenance protocols — are well-documented and, in theory, replicable. JR Central and JR West operate their own Shinkansen lines with comparable safety and punctuality records. The difference is not in how JR East runs trains; it is in where it runs them and what it has built around them.

Similarly, Branding in Helmer's framework does not fully apply. Suica has strong brand recognition, but it is not a lifestyle brand in the way that Apple or Nike creates emotional attachment. Passengers use Suica because it is convenient, not because they love the penguin mascot. If a superior alternative appeared with equivalent coverage and interoperability, switching costs — not brand loyalty — would be the primary retention mechanism.

JR East's strategy is, in essence, a race against demographics. Can the company grow non-transportation revenue fast enough to offset the slow structural decline in commuter ridership? Can the Suica platform, the Takanawa development, and the tourism pivot generate enough incremental value to keep total returns growing? The powers framework says the moat is real and deep. The question is whether the castle inside the moat can be rebuilt for a smaller population.

There is a useful thought experiment for framing this question. Imagine JR East in 2045, when Japan's population will have fallen by 15 to 20 million from today's level. Tokyo's metropolitan population will likely be stable or only modestly lower, thanks to continued internal migration. The commuter base will be smaller, but the survivors — the riders who remain — will be higher-value, because they will be the workers in Tokyo's knowledge economy who cannot or will not work remotely. Meanwhile, Suica will have evolved through two decades of platform development. Takanawa Gateway City will be a mature, cash-generating asset. The hotel and tourism businesses will have benefited from two decades of growing inbound travel. In this scenario, JR East's non-transportation earnings could reasonably exceed its transportation earnings, and the company's identity — and valuation — would be fundamentally different from what it is today.

That is the bull case in its purest form: not that JR East avoids demographic decline, but that it transforms itself into a different kind of company before the decline erodes its foundation. The bear case is that transformation takes too long, costs too much, and generates too little incremental return to offset the structural headwind. The truth, as always, will be revealed by the numbers — quarter by quarter, year by year, measured in the two KPIs that matter most.

VIII. Analysis: Bear vs. Bull Case

The Bear Case

Japan's population was approximately 125 million in 2024 and is projected to fall below 100 million by the 2050s. The working-age population is declining even faster. For a company whose core business is moving commuters, this is not a cyclical headwind; it is a secular structural shift. Every year, there are fewer potential riders, and the trend accelerates as Japan's demographic pyramid inverts.

Remote work compounds the problem. Pre-pandemic, the assumption was that Japanese corporate culture — with its emphasis on physical presence, after-work socializing, and hierarchical face time — was immune to the remote work trends reshaping Western economies. COVID-19 proved otherwise.

Major Japanese corporations, including many headquartered in JR East's service area, now offer hybrid work arrangements. NTT, one of Japan's largest employers, made remote work the default for most office workers. Even traditional manufacturers began offering two or three days of flexibility. A commuter who works from home two days a week represents a 40 percent reduction in fare revenue — and that reduction is permanent. It is not a demand shock that will reverse with economic recovery; it is a structural change in how Japanese white-collar workers organize their lives.

The capital expenditure burden is relentless. JR East spent 771 billion yen on capex in fiscal year 2025, exceeding its operating cash flow of 732 billion yen. The resulting free cash flow was negative 39 billion yen. This is not a growth investment problem; much of this spending is maintenance capex — repairing tunnels bored in the 1960s, replacing bridges built in the Showa era, upgrading signaling systems designed before smartphones existed. Japan's infrastructure is aging, and the cost of keeping it safe and functional is enormous and non-discretionary.

The balance sheet carries approximately 4.97 trillion yen in total debt against equity of roughly 2.86 trillion yen. Annual interest expense was nearly 75 billion yen in fiscal year 2025. While this is manageable at current interest rates, Japan's monetary policy environment is shifting. The Bank of Japan has begun normalizing rates after decades of zero and negative interest rate policy. Every 50 basis points of rate increase on JR East's debt stack adds tens of billions of yen in annual interest expense.

The regulatory and accounting environment also warrants attention. JR East's balance sheet carries property, plant, and equipment at approximately 7.79 trillion yen — a massive figure that reflects decades of accumulated infrastructure investment recorded at historical cost. The depreciation policies for railway assets are inherently judgmental: how long does a tunnel last? A bridge? A viaduct? Small changes in useful life assumptions can shift hundreds of billions of yen in depreciation expense, meaningfully affecting reported earnings. Investors should understand that JR East's reported profits are, in part, a function of accounting choices about asset lives that may or may not reflect economic reality.

There is also the quasi-regulatory obligation of public service. JR East operates many rural and regional lines in northern Japan that are structurally unprofitable — routes that serve shrinking communities in Tohoku and northern Kanto where ridership has fallen below any reasonable threshold of commercial viability. Unlike a purely private company that could simply close these routes, JR East faces intense political and social pressure to maintain service. The cost of operating these "social railway" lines is a persistent drag on profitability, and it constrains management's freedom to optimize the network purely for shareholder returns.

Finally, there is concentration risk. Takanawa Gateway City is a $4 billion bet on a single location. If Tokyo's office market softens, if the development fails to attract premium tenants, or if the project experiences cost overruns, the financial impact could be material relative to JR East's total earnings.

The Bull Case

Start with what cannot be replicated. JR East owns the rail infrastructure serving the Tokyo metropolitan area — the world's largest urban economy. Tokyo's GDP, measured on a metropolitan basis, exceeds that of most countries. It is larger than the national GDP of the Netherlands, Switzerland, or Saudi Arabia.

Even as Japan's total population declines, Tokyo continues to attract internal migrants, and the metropolitan area's population remains relatively stable. The city is a magnet for talent, capital, and corporate headquarters, and this gravitational pull shows no signs of weakening.

International tourism to Japan has surged, reaching record levels in 2024 and 2025, driven by the weak yen and Japan's growing reputation as a premier travel destination. Visitor numbers exceeded 30 million annually, and the spending per visitor has increased substantially as Japan attracted higher-spending tourists from across Asia, Europe, and North America. JR East's Shinkansen and regional rail networks are the primary transportation infrastructure for tourists visiting northern Japan — and unlike airlines, JR East captures revenue not just from the journey but from every stop along the way.

The Suica-as-a-platform opportunity is the most under-appreciated growth vector. If JR East executes its 2029 roadmap — subscription fare plans, walk-through gates, peer-to-peer transfers, municipal service integration — Suica evolves from a transit card into a comprehensive digital infrastructure layer for daily life in eastern Japan. The monetization potential of 112 million cards and 33 million mobile accounts, through transaction fees, data analytics, and financial services, is substantial and largely unpriced by the market.

Takanawa Gateway City, for all its risks, sits on effectively free land. The development cost is significant, but the land cost — which typically represents 30 to 50 percent of a real estate project's total investment in central Tokyo — is essentially zero because JR East has held the site since 1987. If the project achieves even a modest cap rate, the returns on invested capital will be attractive. And the development creates a new node in JR East's commercial ecosystem — a new source of retail revenue, hotel revenue, and transit revenue that did not exist before.

The international consulting opportunity, while speculative, is worth noting. JR East's operational expertise — safety systems, Shinkansen technology, station development — is in demand globally. India's high-speed rail project, inspired by the Shinkansen, and growing interest in rail infrastructure in the United States and Southeast Asia, could create consulting and technology licensing revenue streams. These would be small relative to the core business but high-margin and strategically valuable.

On the M&A front, JR East's approach to acquisitions and investments reveals a disciplined strategic logic. The company does not make splashy, headline-grabbing deals. Instead, it acquires capabilities — small technology companies, regional businesses, and service providers — that can be plugged into its massive existing distribution network. JRE Startup, the company's corporate venture initiative, invests in early-stage companies working on robotics, AI, mobility services, and station-related innovations. The thesis is classic corporate venture capital: rather than trying to build every technology in-house, JR East identifies promising external capabilities and integrates them into its ecosystem, where the 17-million-passenger-per-day distribution network acts as an accelerant. A robot that serves coffee is interesting on its own; a robot that serves coffee in the world's busiest train station is a business.

This approach extends to international opportunities. JR East has provided consulting and technical expertise to India's Mumbai-Ahmedabad High Speed Rail project, modeled on the Shinkansen. The company has also explored partnerships in Southeast Asia, the United Kingdom, and the United States, where aging rail infrastructure creates demand for Japanese engineering expertise. These international ventures are currently immaterial to revenue, but they represent optionality — high-margin consulting and technology licensing that could become meaningful if global demand for rail modernization accelerates, as climate commitments and urbanization trends suggest it will.

On valuation, JR East trades at approximately 18 times earnings and 1.4 to 1.5 times book value. For a company with irreplaceable assets, a world-class operational track record, and a credible path to higher non-transportation earnings, this does not appear to be a demanding multiple. Compared to global infrastructure peers — companies like MTR Corporation in Hong Kong, which trades at a premium for similar transit-plus-property strategies, or even US Class I railroads like Union Pacific and CSX, which command rich multiples for their freight monopolies — JR East's valuation reflects a "Japan discount" that may or may not be justified.

If the market begins to value the Suica platform and real estate portfolio separately from the railroad — a sum-of-the-parts exercise that some analysts have begun to undertake — the implied value of the individual pieces may exceed the current market capitalization. The Suica platform alone, valued on a transaction-multiple basis comparable to payment companies, could be worth a meaningful fraction of JR East's entire enterprise value. The station real estate, valued at market rather than historical cost, represents another layer of hidden value. And the railway itself, with its regulatory protection and captive customer base, provides a floor on the downside.

The KPIs That Matter

For investors tracking JR East's ongoing transformation, two metrics matter above all others:

Non-transportation revenue as a percentage of total revenue. This is the single best measure of whether JR East's diversification strategy is working. If this ratio moves steadily toward 50 percent and beyond, it signals that the company is successfully reducing its dependence on commuter fares and building a more resilient, higher-margin earnings base. If it stagnates, the bear case gains credibility.

Revenue per passenger. This captures the "quality over quantity" pivot in a single number. As commuter volumes face structural headwinds, JR East's strategy depends on extracting more value from each person who enters the system — through retail spending, Suica transactions, premium services, and tourism. Rising revenue per passenger, even against flat or declining total ridership, would validate the transformation thesis.