Kaori: The Master of Heat

I. Introduction & The Hook (0:00 – 10:00)

What if there were a company in Taiwan that is simultaneously a bet on the future of Hydrogen energy and one of the critical links in keeping Nvidia's next-generation Blackwell chips from melting?

That company exists. It has 515 employees. It sits in an industrial park in Taoyuan City, about forty minutes south of Taipei. And unless you actively follow Taiwanese small-caps or dig through Bloom Energy's supply chain disclosures, you have almost certainly never heard of it.

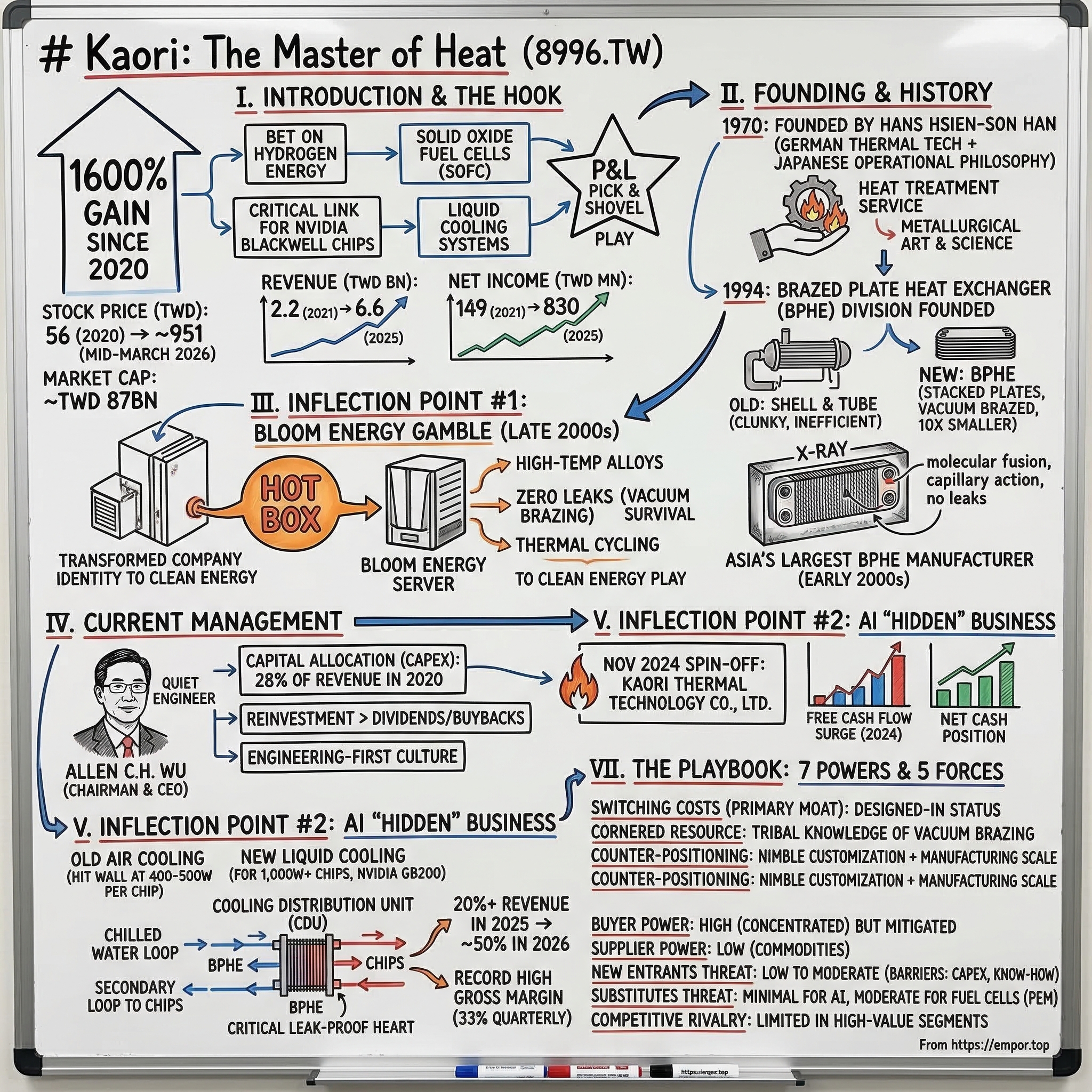

Its name is Kaori Heat Treatment Co., Ltd., ticker 8996.TW. And its stock chart over the past six years looks less like a boring industrial company and more like a Silicon Valley SaaS rocket ship. In early 2020, Kaori shares traded at roughly 56 New Taiwan Dollars. As of mid-March 2026, they sit around 951 TWD—a gain of approximately 1,600 percent. The company's market capitalization has swelled to roughly TWD 87 billion, or about USD 2.7 billion. For a heat exchanger manufacturer with a headcount smaller than a mid-size tech startup, that is a staggering valuation.

But here is the thing—this is not a meme stock story. This is not retail speculation run amok. The revenue and earnings trajectory underneath the stock price is real and accelerating. Revenue grew from TWD 2.2 billion in 2021 to TWD 6.6 billion in 2025, roughly tripling. Net income over the same period went from TWD 149 million to TWD 830 million—a more than fivefold increase. Earnings per share climbed from TWD 1.67 to TWD 9.07. This is a company that is firing on multiple cylinders, and the market has woken up to it.

The question, as always, is why. Why has a company founded in 1970 as a metal heat treatment shop suddenly become the darling of the Taiwanese stock market? The answer lies at the intersection of two of the most powerful secular trends of the 2020s: the Hydrogen economy and the insatiable power demands of Generative AI. Kaori, through decades of quiet metallurgical mastery, has positioned itself as an indispensable supplier to both.

Think of it this way. When Bloom Energy needs the most critical, highest-temperature component of its solid oxide fuel cells—the so-called "Hot Box"—it calls Kaori. When the world's hyperscale data centers need leak-proof liquid cooling manifolds and cooling distribution units capable of keeping Nvidia's 1,000-watt GB200 chips from turning into expensive paperweights, they call Kaori. The company has become what investors love to find: a "picks and shovels" play on multiple megatrends, run by engineers who have been perfecting their craft for over half a century.

This is the story of how a Taiwanese metallurgical shop became an overnight success—fifty-six years in the making. It is a story about vacuum brazing furnaces and molecular-level metal fusion, about a college professor who brought German thermal technology back to Taiwan, about the physics of heat transfer that no amount of venture capital can shortcut, and about what happens when the world's biggest technology trends finally catch up to a company that has been waiting, patiently, for decades.

The roadmap ahead: we will trace the founding and the metallurgical DNA. We will unpack the Bloom Energy partnership that transformed the company's identity. We will examine the current management team and their capital allocation philosophy. We will dive deep into the "hidden" AI liquid cooling business. And we will run the whole thing through the strategic frameworks—Hamilton Helmer's Seven Powers and Porter's Five Forces—to understand whether the moat is real or illusory. Let us begin.

II. Founding & The Succinct History (10:00 – 18:00)

Picture Taoyuan in 1970. Taiwan is deep in the throes of its industrial transformation—the "economic miracle" is just beginning to accelerate, and the government is pouring resources into building the manufacturing base that will eventually make the island synonymous with global supply chains. In this environment, a college professor named Hans Hsien-Son Han makes an unusual decision. Rather than continue his academic career, he decides to start a company.

Hans was not a typical entrepreneur. He had received his graduate education in Germany, where he immersed himself in the rigorous German tradition of thermal and metallurgical engineering. He had also grown up in the Japanese educational system in Taiwan, which instilled in him a deep respect for precision, discipline, and organizational efficiency. This blend of German technical training and Japanese operational philosophy would become the cultural DNA of Kaori—a combination that, decades later, would prove uniquely suited to solving problems that stumped far larger competitors.

The company he founded was, at its core, a heat treatment shop. The name itself—Kaori Heat Treatment—describes exactly what the business did in those early years. Heat treatment, for the uninitiated, is the process of heating and cooling metals in controlled ways to change their physical properties. Need a steel gear that is harder on the surface but flexible inside? Heat treatment. Need an alloy that can withstand extreme pressure without cracking? Heat treatment. It is one of the oldest and most fundamental processes in metallurgy, and it is far more of an art than most people realize. The difference between getting it right and getting it wrong can be a matter of a few degrees of temperature or a few seconds of timing.

Hans did not just want to run a service shop, though. He wanted to build Taiwan's metallurgical knowledge base. He founded the Taiwan Society for Metal Heat Treatment, establishing himself as a thought leader in the field. He treated his factory floor like a laboratory, constantly experimenting with new alloys, new temperature profiles, new brazing techniques. In an industry where most competitors were content to be job shops—processing whatever metal came through the door—Hans was building institutional knowledge about how metals behave at extreme temperatures. This distinction would prove decisive decades later.

The pivotal strategic shift came in 1994, when Kaori founded its Brazed Plate Heat Exchanger division. To understand why this mattered, you need to understand what a brazed plate heat exchanger actually is—and why it was a revolution in thermal management.

Think of a traditional heat exchanger as a big, clunky radiator. The old "shell and tube" design—literally a bundle of tubes inside a shell—had been the industry standard for decades. It worked, but it was bulky, heavy, and inefficient. A brazed plate heat exchanger, or BPHE, takes a radically different approach. Imagine a stack of thin, corrugated metal plates, each one stamped with a precise pattern of channels. When you stack these plates together and braze them—that is, fuse them together using a filler metal at extremely high temperatures in a vacuum—you create a compact block with an enormous surface area for heat transfer. The result is a device that can be ten times smaller than a shell-and-tube exchanger while delivering the same thermal performance.

The key word there is "vacuum." Vacuum brazing is a process where you place the stacked plates inside a massive furnace, pump out all the oxygen, and then heat the entire assembly to temperatures above 1,000 degrees Celsius. In the absence of oxygen, the filler metal melts and flows into every joint by capillary action, creating a molecular bond between the plates. No flux, no contamination, no weak points. The result is a hermetically sealed, incredibly strong heat exchanger that can operate at high pressures and temperatures without leaking.

This is where Hans's decades of metallurgical expertise became a decisive advantage. Vacuum brazing is notoriously finicky. The temperature profiles have to be precise. The alloy combinations have to be compatible. The surface preparation has to be flawless. Get any of it wrong, and you either get leaks (catastrophic in a pressurized system) or brittle joints (catastrophic everywhere). Kaori had been studying exactly these problems since 1970. When the BPHE market began to take off in the 1990s—driven by the global HVAC industry's shift toward more compact, energy-efficient equipment—Kaori was not starting from scratch. It was applying forty-plus years of accumulated metallurgical knowledge to a new product category.

By the early 2000s, Kaori had established itself as Asia's largest manufacturer of brazed plate heat exchangers. Its products were being sold into HVAC systems, refrigeration units, industrial cooling applications, and heat recovery systems around the world. It was a solid, profitable business—not flashy, but technically excellent. The company was making good money doing something it was genuinely world-class at.

But the most important thing about this era is not the revenue or the market share. It is the capability that Kaori built. Those vacuum brazing furnaces, that institutional knowledge about how different alloys behave at extreme temperatures, that culture of treating manufacturing like a science—all of it was accumulating like potential energy, waiting for the right catalyst to convert it into something explosive. That catalyst was about to arrive, in the form of a phone call from Silicon Valley.

III. Inflection Point #1: The Bloom Energy Gamble (18:00 – 35:00)

Sometime in the late 2000s, a delegation from an American startup called Bloom Energy showed up in Taoyuan with an unusual request. They needed someone who could manufacture a component so demanding, so technically extreme, that virtually every established supplier they had approached had failed.

Bloom Energy, for context, was one of the most hyped clean energy companies of the era. Founded in 2001 by KR Sridhar—a former NASA scientist who had worked on oxygen generation systems for Mars missions—Bloom was developing solid oxide fuel cells, or SOFCs. The basic concept was elegant: take natural gas (or hydrogen, or biogas), pass it over a ceramic cell at extremely high temperatures, and generate electricity through an electrochemical reaction rather than combustion. No burning, no turbines, no moving parts. Just chemistry and heat.

The problem was the "extremely high temperatures" part. A solid oxide fuel cell operates at around 800 to 1,000 degrees Celsius—hot enough to melt aluminum, hot enough to glow orange. At the heart of every Bloom Energy Server was a component called the "Hot Box," which housed the fuel cell stacks and maintained the precise thermal environment needed for the electrochemical reaction to occur. The Hot Box had to be manufactured from specialized high-temperature alloys, brazed together with joints that could survive years of continuous operation at temperatures that would destroy ordinary metals.

According to reporting by the Taipei Times, Kaori secured a deal with Bloom Energy around 2009, initially expected to generate about NT$100 million in revenue. Using technology transferred from Bloom, Kaori set up a dedicated production line for SOFC hot boxes. But the real story was not the initial contract size—it was the technical challenge that Kaori had to overcome to win it.

Think about what Bloom was asking for. They needed metal components brazed together with zero leaks, operating continuously at near-1,000-degree temperatures, with tolerances measured in fractions of a millimeter. The joints had to survive thermal cycling—heating up and cooling down repeatedly without cracking or degrading. The alloys had to resist oxidation and corrosion in an environment of superheated gas. And all of this had to be manufactured at scale, with enough consistency that Bloom could rely on Kaori as a production partner rather than a prototype shop.

This was precisely the kind of problem that Kaori's five decades of metallurgical experience had prepared it to solve. The vacuum brazing process that Hans Han had been perfecting since 1970 was, in essence, the same process needed to manufacture Bloom's Hot Boxes—just pushed to even more extreme parameters. Where a typical BPHE for an HVAC system might operate at a few hundred degrees, a Bloom Hot Box operated at nearly double that. But the fundamental physics was the same: precise temperature control, meticulous alloy selection, flawless surface preparation, and the patience to get it right.

What made Kaori's position especially powerful was something that is hard to replicate: tribal knowledge. Vacuum brazing at these temperatures is not a process you can learn from a textbook or license from a patent. It is accumulated through thousands of production runs, each one revealing subtle interactions between alloys, furnace temperatures, heating rates, and cooling profiles. Kaori's engineers had been building this knowledge base for forty years. A competitor starting from scratch would need years of trial and error just to approach Kaori's reject rates, let alone match them.

The partnership deepened over time. According to a 2024 CommonWealth Magazine report, Taiwanese firms came to account for roughly 30 percent of Bloom Energy's component supply chain, with Kaori providing fuel cell hot boxes alongside other Taiwanese suppliers like AcBel (power supplies) and Porite Taiwan (fuel cell components). At Kaori's shareholders' meeting, the production of fuel cell reaction boxes for Bloom was described as a major driver of the company's revenue.

The Bloom relationship transformed Kaori's identity. Before Bloom, Kaori was an HVAC component maker—a solid business, but one that analysts categorized firmly in the "boring industrial" bucket. After Bloom, Kaori was a clean energy play, a participant in the hydrogen economy, a company whose growth was tied to the global energy transition. The stock began to attract a different class of investor.

But there is an important nuance here that sophisticated investors should note. While Kaori has been a major supplier of hot boxes to Bloom, the supply chain landscape has evolved. MTAR Technologies, an Indian precision engineering firm, has also secured significant contracts with Bloom for hot boxes and electrolyzer units. This does not diminish Kaori's role—Bloom has been scaling rapidly and needs multiple suppliers—but it does mean that the "sole supplier" narrative requires some qualification. The relationship is deep and long-standing, but Kaori's position is better described as a primary supplier with deep design-in status, rather than an absolute monopoly.

What the Bloom partnership proved, above all, was that Kaori's capabilities extended far beyond HVAC. The company had demonstrated that its metallurgical expertise could solve problems in the most demanding thermal environments on earth. And as it turned out, there was another industry desperately searching for exactly that kind of expertise—one that was about to enter a phase of explosive growth that would make even the hydrogen economy look modest by comparison.

IV. Current Management: The Leadership Team (35:00 – 48:00)

Walk into Kaori's headquarters in Taoyuan, and you will not find the trappings of a tech company riding a 1,600-percent stock rally. No open-plan offices with ping-pong tables. No slick investor relations team crafting press releases about "paradigm shifts." What you will find is a factory floor that looks more like a laboratory, rows of vacuum brazing furnaces that cost millions of dollars each, and engineers in work clothes who have been with the company for decades.

The man at the top is Allen C.H. Wu, who serves as Chairman and Chief Executive Officer. Wu, referred to in some filings as Chih-Hsyong Wu, has overseen the company's transformation from a traditional heat treatment business into a diversified thermal technology platform. While the founder, Hans Hsien-Son Han, remains involved as Honorary Chairman and Chief Counsel—lending his name and his decades of metallurgical authority to the company's reputation—the day-to-day strategic direction has been driven by Wu and his management team.

Wu's leadership style can be described as "the quiet engineer." In an era when CEOs of high-flying companies are expected to be on CNBC every week, Wu is conspicuously absent from the media circuit. He rarely gives interviews. The company's press releases are sparse and technical. There is no hype machine. This is, in many ways, the Taiwanese way—let the products and the financials speak for themselves.

What Wu has done, quietly but decisively, is redirect the company's capital allocation toward the highest-value opportunities. Look at the numbers: in 2020, Kaori spent TWD 586 million on capital expenditures—a massive sum for a company that generated only TWD 2.1 billion in revenue that year. That represented nearly 28 percent of revenue plowed back into property, plant, and equipment. By comparison, many Western industrial companies spend 3 to 5 percent of revenue on CAPEX. In 2023, Kaori spent another TWD 352 million. These were not maintenance investments to keep the lights on. These were bets—new vacuum brazing furnaces, expanded production lines, investments in the specialized equipment needed to manufacture liquid cooling components for AI data centers.

The management team below Wu reflects this engineering-first culture. General Manager Hsin-Wu Wang, Vice General Manager Hung-Hsing Huang, and Deputy General Managers Hung-Yi Chiu and Wu-Hsing Chou are all technical leaders rather than financial engineers. Executive compensation, according to company filings, is modest by any standard—Wu's total pay was reported at roughly TWD 6 million (about USD 185,000), and the founder Hans Han at roughly TWD 8 million. These are not executives extracting value from the business. They are reinvesting it.

Perhaps the most significant management decision in recent years was the spin-off of Kaori Thermal Technology Co., Ltd. In November 2024, Kaori held an Extraordinary Shareholders' Meeting to approve the creation of a wholly-owned subsidiary that would house the company's thermal energy business—specifically, the AI data center cooling and advanced thermal solutions. Chou Wu-Hsing, one of the Deputy General Managers, was appointed President of the new entity effective January 1, 2025. The logic was clear: the liquid cooling business was growing so fast and had such different dynamics from the traditional BPHE and fuel cell businesses that it needed its own dedicated management structure, its own P&L, and its own ability to move quickly.

This is a classic move from a management team that understands the innovator's dilemma. Rather than letting the new, fast-growing business fight for resources within the parent company's existing structure, they gave it room to breathe. Kaori Thermal Technology now operates with its own website, its own branding, and its own sales team—while still drawing on the parent company's decades of vacuum brazing expertise and manufacturing infrastructure.

On the balance sheet, the results of this capital allocation philosophy are visible. By the end of 2024, Kaori's total assets had grown to TWD 6.1 billion, with property, plant, and equipment of nearly TWD 2 billion. The company had moved from a net debt position of TWD 1.2 billion in 2022 to a net cash position by the end of 2024, with TWD 1.87 billion in cash on the books. Free cash flow surged to TWD 843 million in 2024, up from negative territory just two years prior. The current ratio stood at a comfortable 2.05, and return on equity was roughly 17 percent.

The management incentive structure is also worth noting for what it is not. There are no stock buyback programs. There are no lavish stock option grants. The Han family and associates maintain significant ownership, creating alignment between management and shareholders without the need for complex compensation engineering. Dividends have been paid consistently—TWD 358 million in 2024, TWD 134 million in 2023—but the primary use of capital has been reinvestment into the business.

This is a management team that runs the company like owners, because they are owners. And in late 2024, they made their biggest bet yet—a capital expenditure plan described internally as the largest since the company's founding, with headcount set to increase by more than 40 percent. They are building capacity not for the hydrogen economy alone, but for the AI cooling opportunity that has arrived at their doorstep.

V. Inflection Point #2: The AI "Hidden" Business (48:00 – 65:00)

Here is a question that sounds like it belongs in a physics class but is actually the most important business question in the technology industry right now: How do you cool a chip that consumes 1,000 watts of power?

For decades, the answer was simple: fans. Blow air over a heat sink, and the heat dissipates. This worked fine when server chips consumed 100 or 200 watts. It even worked, with some creative engineering, when they pushed past 300 watts. But Nvidia's H100, the chip that ignited the Generative AI revolution, consumed around 700 watts. The next generation, the B200 Blackwell, pushed past 1,000 watts. And the trajectory is only going up.

To put this in household terms: a 1,000-watt chip generates roughly the same heat as a small space heater. Now imagine a data center rack packed with eight or sixteen of these chips, all running at full load, 24 hours a day, seven days a week. That is a wall of heat—and no amount of fans can efficiently dissipate it. Air cooling hits a physical wall somewhere around 400 to 500 watts per chip. Beyond that, you need liquid.

Liquid cooling for servers is not a new idea—it has been used in supercomputers since the 1960s. But it has never been deployed at the scale that AI data centers now require. The global market for data center liquid cooling systems reached roughly USD 5.5 billion in 2025 and is projected to grow to USD 10.7 billion by 2030, according to industry research reports. Some forecasts put it even higher, at USD 15.75 billion by 2030. Whatever the exact number, the direction is unmistakable: every new AI data center being built today is designed with liquid cooling, and many existing ones are being retrofitted.

This is where Kaori's story takes its most dramatic turn. Quietly, within the company's existing BPHE division, a small team had been developing products for server cooling applications. The technology was a natural extension of Kaori's core competency. A brazed plate heat exchanger—a compact, leak-proof device for transferring heat from one fluid to another—is exactly what you need inside a Cooling Distribution Unit (CDU), which is the heart of any direct-to-chip liquid cooling system.

Think of a CDU as the central nervous system of a liquid-cooled server rack. Cool water flows from a facility's chilled water loop into the CDU. Inside, a brazed plate heat exchanger transfers heat from a secondary loop—the one that runs directly to the hot chips inside the servers—to the facility water. The hot facility water is then piped away to cooling towers or chillers. The key component, the thing that makes it all work, is that heat exchanger inside the CDU. It has to handle enormous thermal loads. It has to operate 24/7 without leaking—because even a tiny leak in a data center filled with millions of dollars of equipment is catastrophic. And it has to do this for ten years or more without maintenance.

This is not something you can just slap together in a contract manufacturing facility. The brazed joints have to be flawless. The plate patterns have to be optimized for the specific flow rates and temperatures of the application. The materials have to be compatible with the coolant chemistry. This is, once again, a vacuum brazing problem—and Kaori has been solving vacuum brazing problems for over fifty years.

The market recognized this capability. A Morgan Stanley research report on liquid cooling for Nvidia's GB200 AI chips ranked Kaori among the key suppliers within the Supermicro cooling ecosystem. At COMPUTEX 2025—Taiwan's premier technology trade show, held in Taipei in May 2025—Kaori Thermal Technology showcased an impressive array of products: rear-door air-to-liquid heat exchangers, side car modules, direct-to-chip in-rack CDU systems, high-capacity in-row CDU units, immersion cooling systems, and the critical MGX liquid manifolds and hose assemblies. All of these were compatible with Nvidia's GB200, GB300, and ORV3 architectures—the building blocks of next-generation AI data centers.

According to a KGI Securities research forecast, liquid cooling products accounted for more than 20 percent of Kaori's revenue in 2025, with projections that this could climb to nearly 50 percent in 2026. The analyst report also projected roughly 80 percent growth in overall revenue. These are extraordinary numbers for a company that, just a few years ago, derived the vast majority of its income from conventional HVAC heat exchangers.

The margin profile of this new business is equally compelling. CEO Allen Wu noted in investor communications that liquid cooling products carry higher profit margins than Kaori's conventional heat exchanger products. This is visible in the financials: the company's quarterly gross margin hit a record high of 33 percent as the product mix shifted toward liquid cooling. For a manufacturing business with traditionally mid-to-high-20s gross margins, that is a meaningful step change.

The natural question is: why can't larger players simply copy this? Why can't Foxconn, with its massive manufacturing scale, or Quanta, with its deep relationships with hyperscalers, just build their own brazed plate heat exchangers?

The answer goes back to the vacuum brazing furnaces—and the decades of knowledge required to operate them effectively. A vacuum brazing furnace capable of producing server-grade heat exchangers costs millions of dollars and takes years to commission and optimize. But the real barrier is not the hardware; it is the process knowledge. Each new alloy combination, each new plate geometry, each new application requires its own set of brazing parameters—temperature curves, hold times, cooling rates—that can only be developed through extensive trial and error. Kaori has been accumulating this knowledge since 1970. A new entrant would be starting from zero. And in a market where customers need product now—because data centers are being built at a pace not seen since the dot-com era—there is no time to wait for a competitor to catch up.

The company is not just selling components, either. It is moving up the value chain from individual heat exchangers to complete CDU systems and integrated cooling solutions. This transition from "component supplier" to "system provider" is a classic strategy for capturing more value and deepening customer lock-in. When your heat exchanger is designed into a customer's CDU, switching costs are real—changing the heat exchanger means redesigning the entire thermal architecture, requalifying the system, and re-certifying it. That is a process that can take one to two years, during which the customer's data center expansion is stalled.

The convergence is remarkable. Kaori's traditional BPHE business—the cash cow—continues to generate steady revenue from the global HVAC market. The Bloom Energy fuel cell business provides exposure to the hydrogen and clean energy transition. And now, the liquid cooling business is layering on a third growth vector tied to the most capital-intensive technology buildout in history. Three distinct end markets, all served by the same core competency: the ability to fuse metals together in a vacuum.

VI. Capital Deployment & M&A (65:00 – 75:00)

One of the most telling things about Kaori is what it has not done. In an era when industrial companies are expected to grow through acquisition—rolling up competitors, buying into adjacent markets, doing transformative deals announced with breathless press releases—Kaori has done essentially none of that. There are no billion-dollar acquisitions in its history. No leveraged buyouts. No "strategic transformations" driven by investment bankers.

Instead, the company has pursued what might be called the "anti-M&A" strategy: vertical integration through internal investment. Rather than buying another company's capabilities, Kaori has built its own. Rather than paying a premium for a competitor's customer relationships, it has developed its own through technical excellence. This approach is slower and less dramatic than deal-making, but it produces a fundamentally different kind of competitive position.

Consider the capital expenditure pattern. In 2020, Kaori spent TWD 586 million on CAPEX—a year when revenue was only TWD 2.1 billion. That is a CAPEX-to-revenue ratio of nearly 28 percent. To put that in context, Alfa Laval, the Swedish industrial giant that is one of the world's largest heat exchanger manufacturers with EUR 5.4 billion in revenue, typically spends around 3 to 4 percent of revenue on capital expenditure. Kelvion, another major player in the thermal management space, operates in a similar range. Kaori was spending at a rate roughly seven times higher, relative to its size.

What was all that money going toward? Vacuum brazing furnaces. Specialized stamping equipment for heat exchanger plates. Testing and quality assurance infrastructure. Production lines for fuel cell hot boxes. And, increasingly, capacity for manufacturing liquid cooling components. Each of these investments was, in effect, a bet on the company's ability to move into higher-value applications—and a barrier to entry for anyone who might want to follow.

The math of this strategy is elegantly simple. A vacuum brazing furnace represents a multi-million-dollar investment that only pays off if you have the volume and the know-how to keep it running at high utilization. For Kaori, with its diversified base of BPHE, fuel cell, and liquid cooling products, the furnaces are running constantly—each new product line adds utilization to the existing asset base. For a competitor considering entry into, say, the AI liquid cooling market, the calculus is different: they would need to justify the furnace investment based on a single product line, with no guarantee of winning enough business to cover the fixed costs.

The most recent phase of investment has been the most aggressive yet. As noted earlier, the company described its current capital expenditure plan as the largest in its history, with plans to increase headcount by more than 40 percent. The focus is on expanding capacity for liquid cooling products to meet the exploding demand from AI data center builders. New factory space in Taiwan is being added, and the company has been positioning for potential production in other markets as well.

Was this overbuilding? The concern is understandable—any time a company ramps capacity this aggressively, there is a risk that demand does not materialize as expected. But the evidence suggests that Kaori is actually capacity-constrained, not over-built. The AI data center construction boom shows no signs of slowing, with hyperscalers like Microsoft, Google, Amazon, and Meta all committed to spending hundreds of billions of dollars on AI infrastructure over the next several years. Liquid cooling is not optional for these facilities—it is an engineering requirement driven by the laws of thermodynamics. And the number of companies in the world that can manufacture vacuum-brazed heat exchangers to the specifications required by these data centers is vanishingly small.

The balance sheet supports the investment thesis. Kaori ended 2024 with TWD 1.87 billion in cash, a net cash position (meaning cash exceeds total debt), and a current ratio above 2.0. Operating cash flow in 2024 was TWD 1.04 billion, providing ample internal funding for expansion. The company is not stretching its balance sheet to fund growth—it is investing from a position of strength.

The spin-off of Kaori Thermal Technology in late 2024 was itself a form of capital deployment—not in the monetary sense, but in the organizational sense. By giving the liquid cooling business its own management structure and operational autonomy, Kaori is ensuring that the fastest-growing part of the business gets the attention, the talent, and the decision-making speed it needs. It is a recognition that the AI cooling opportunity is big enough to warrant its own dedicated entity, while still benefiting from the parent company's manufacturing infrastructure and institutional knowledge.

VII. The Playbook: 7 Powers & 5 Forces (75:00 – 90:00)

Let us now step back from the narrative and apply some analytical rigor. When you strip away the excitement about AI and hydrogen, what is the structural competitive position of this business? Is the moat real, or is it a temporary advantage that will erode as competitors scale up?

Hamilton Helmer's Seven Powers Framework

The most compelling power that Kaori possesses is Switching Costs. This is the primary source of durable competitive advantage. If you are Bloom Energy and your Hot Box thermal architecture has been co-designed with Kaori's engineers over the course of a decade, switching to a different supplier is not a simple procurement decision. It requires a complete redesign of the thermal management system, months or years of qualification testing, and the risk that the new supplier's components will not perform identically in the field. The same logic applies to liquid cooling customers. When Kaori's brazed plate heat exchangers are designed into a CDU system—when the flow rates, the pressure drops, the thermal performance curves are all calibrated around Kaori's specific plate geometry—switching to a different heat exchanger means starting the engineering process over. Customers do not switch suppliers lightly when the cost of failure is a data center outage.

The second power is a Cornered Resource—specifically, the tribal knowledge of vacuum brazing specialized alloys. This is not a patent or a trade secret in the traditional sense. It is not written down in a document that could be stolen or reverse-engineered. It is embedded in the experience of Kaori's engineering team, in the specific temperature profiles programmed into their furnaces, in the institutional memory of thousands of production runs across dozens of alloy combinations. This kind of knowledge accumulates slowly and cannot be purchased or replicated quickly. A new entrant can buy the same furnaces Kaori uses, but they cannot buy the fifty-six years of learning that makes those furnaces productive.

The third power is Counter-Positioning. Kaori occupies an unusual strategic position: small enough to be nimble and responsive to the bespoke requirements of AI startups and mid-size fuel cell companies, but with enough scale and track record to satisfy a Fortune 500 customer like the hyperscalers that buy through Supermicro and other OEMs. Larger thermal management companies like Alfa Laval could theoretically enter the AI cooling market, but their organizational structures are optimized for high-volume, standardized products. The customization and rapid iteration required by the AI cooling market—where specifications change with every new chip generation—does not fit easily into a large multinational's operating model. Conversely, smaller or newer entrants may have the agility but lack the manufacturing scale and quality certifications that enterprise customers demand.

Porter's Five Forces Analysis

On the Bargaining Power of Buyers: this is theoretically high, because Kaori's customer base is concentrated. Bloom Energy represents a significant share of the fuel cell revenue, and the AI cooling revenue flows through a relatively small number of OEMs and hyperscalers. In a normal supplier-buyer relationship, this concentration would give buyers enormous leverage to squeeze prices. But Kaori's "designed-in" status and the high switching costs substantially mitigate this power. When you are the supplier whose component is embedded in a customer's thermal architecture, the buyer's theoretical leverage is constrained by the practical reality that replacing you is expensive and risky.

On the Bargaining Power of Suppliers: Kaori's key inputs are stainless steel, specialized alloys, and brazing filler metals. These are commodity materials available from multiple suppliers. The company does not face significant supplier concentration risk. The most critical "input" is actually the vacuum brazing furnaces themselves, which are specialized capital equipment—but once purchased, they are owned assets, not ongoing supplier dependencies.

On the Threat of New Entrants: this is low to moderate. The capital requirements (specialized furnaces), the knowledge requirements (decades of process know-how), and the qualification timelines (years to become an approved supplier for major OEMs) create substantial barriers. However, as the AI cooling market grows, it will inevitably attract well-funded competitors. The question is whether they can close the knowledge gap fast enough to matter.

On the Threat of Substitutes: for the hydrogen fuel cell business, the primary substitute threat is that a different fuel cell technology (such as PEM, or Proton Exchange Membrane fuel cells) could gain share over solid oxide fuel cells. PEM cells operate at lower temperatures and do not require the extreme thermal management that SOFCs demand. However, SOFCs have efficiency and fuel flexibility advantages that make them attractive for stationary power applications, which is Bloom's primary market. For the liquid cooling business, the substitute threat is minimal—physics dictates that liquid is a far more efficient heat transfer medium than air, and no alternative technology has emerged that can cool 1,000-watt chips as effectively.

On Competitive Rivalry: the heat exchanger market is fragmented, with large players like Alfa Laval and Danfoss competing at the high-volume, commoditized end, and smaller specialists competing in niches. Kaori's competitive environment is most intense in the traditional BPHE market, where price competition is real. But in the higher-value fuel cell and AI cooling segments, competition is limited by the technical barriers described above. The key competitors to watch are other Taiwanese thermal management companies that may try to enter the AI cooling space, as well as vertically integrated ODMs (Original Design Manufacturers) that might attempt to bring cooling component manufacturing in-house.

VIII. The Bear vs. Bull Case (90:00 – 100:00)

The Bear Case

The most obvious risk is customer concentration. While Kaori has diversified its revenue across BPHE, fuel cells, and AI cooling, the fuel cell business remains heavily tied to a single customer: Bloom Energy. If Bloom stumbles—whether due to competitive pressure from PEM fuel cells, loss of government subsidies, or execution challenges—Kaori's fuel cell revenue would be directly impacted. The fact that MTAR Technologies has secured significant Bloom contracts suggests the supplier base is broadening, which could dilute Kaori's share over time.

On the AI cooling side, the risk is different but equally real. The pace of technology change in AI hardware is ferocious. Every new chip generation brings new thermal requirements, new form factors, and new cooling architectures. Nvidia's specifications today may not be Nvidia's specifications two years from now. If the industry shifts to a fundamentally different cooling approach—say, a move toward immersion cooling that bypasses CDUs entirely, or a chip architecture that dramatically reduces power consumption—Kaori's current product portfolio could become less relevant.

Then there is the geopolitical risk that hangs over every Taiwanese company like a permanent cloud. Cross-strait tensions between Taiwan and China remain elevated, and any escalation could disrupt Kaori's manufacturing operations. While this risk is not unique to Kaori—it affects TSMC, Foxconn, and every other Taiwanese manufacturer—it is a factor that any investor must weigh. The company's manufacturing footprint is concentrated in Taiwan, and diversifying production geographically takes time and capital.

Valuation is also a concern. At a market cap of roughly TWD 87 billion against 2025 revenue of TWD 6.6 billion, Kaori trades at a revenue multiple that reflects significant growth expectations. If revenue growth decelerates—due to a slowdown in AI data center construction, a competitive response from larger players, or a cyclical downturn in the HVAC market—the multiple could compress rapidly. The stock's 1,600 percent rise since 2020 leaves little room for disappointment.

Finally, there is execution risk associated with the aggressive capacity expansion. Hiring plans to increase headcount by 40 percent, building new factory space, and ramping production of new product lines all introduce operational complexity. Quality control—always critical in vacuum brazing—becomes harder to maintain at scale. Any quality failure in a high-profile customer installation could damage the company's reputation and its "designed-in" status.

The Bull Case

The bull case starts with a simple observation: Kaori is the "arms dealer" to two of the biggest secular trends of the decade, and arguably of the century. The hydrogen economy and the AI infrastructure buildout are not cyclical trends that will reverse in a downturn. They are structural shifts driven by physics, by policy, and by the relentless demand for energy and computation. Kaori does not need to pick which trend wins—it profits from both.

The company is also moving up the value chain in a way that deepens its competitive position. The transition from component supplier (individual heat exchangers) to system provider (complete CDU solutions) is not just a revenue expansion play. It is a moat-deepening strategy. When Kaori sells a complete cooling system rather than a component, it captures more revenue per installation, it becomes more deeply embedded in the customer's infrastructure, and it raises the switching costs even further.

The financial trajectory supports the narrative. Revenue has tripled in four years. Net income has grown more than fivefold. The balance sheet has swung from net debt to net cash. Gross margins are expanding as the product mix shifts toward higher-value AI cooling products. And the company is investing aggressively in capacity at precisely the moment when demand is outstripping supply across the entire liquid cooling industry.

There is also a scarcity argument. The number of companies in the world that can manufacture vacuum-brazed heat exchangers to the specifications required by next-generation AI data centers is genuinely small. This is not a market where a new factory in China or Vietnam can undercut on price, because the technology is not commoditized. Kaori's expertise is rare, and rare things tend to command premium valuations.

Key KPIs to Track

For investors monitoring Kaori's trajectory going forward, two metrics matter above all others:

First, the revenue mix shift toward liquid cooling as a percentage of total revenue. KGI Securities estimated this crossed 20 percent in 2025 and projected it approaching 50 percent in 2026. The speed and magnitude of this shift will determine whether Kaori truly transitions from a traditional industrial company to a high-growth technology supplier. A stall or reversal in this mix shift would signal that the AI cooling opportunity is not scaling as expected.

Second, gross margin trajectory. As liquid cooling products carry higher margins than traditional BPHEs, the overall gross margin should expand as the product mix shifts. The quarterly record of 33 percent is a signpost. Sustained expansion toward the mid-30s or higher would confirm that Kaori is capturing value, not just volume, in the AI cooling market. Margin compression, conversely, would suggest price competition is intensifying faster than expected.

IX. Conclusion & Final Reflections (100:00 – 105:00)

There is a vacuum brazing furnace sitting in a factory in Taoyuan, Taiwan. It is massive—the size of a small room. When it runs, all the oxygen is pumped out, creating a near-perfect vacuum. Then the temperature rises to over 1,000 degrees Celsius. Inside, stacked metal plates, meticulously prepared and precisely aligned, begin to fuse at the molecular level. No flux, no contamination, just pure metallurgical union. When the furnace cools and the door opens, what emerges is a compact block of metal so tightly bonded that it can withstand years of extreme heat and pressure without leaking a single drop.

That furnace is a fitting metaphor for Kaori itself. For fifty-six years, the company has operated in its own kind of vacuum—sealed off from the hype cycles, the hot trends, the Wall Street narratives that drive most industrial companies to diversify into things they do not understand. Inside that vacuum, Kaori has been doing one thing: fusing metals at extreme temperatures, getting better at it every year, accumulating knowledge that cannot be replicated by money alone.

And then the world changed. Hydrogen fuel cells needed someone who could build Hot Boxes. AI chips needed someone who could build liquid cooling systems. Both problems, at their core, were metallurgical problems—problems of heat, of metal, of precision joints that cannot fail. And when the phone rang, Kaori was ready. Not because they were lucky, and not because they pivoted. Because they had been preparing, without knowing it, for exactly this moment.

Hans Han, the college professor who returned from Germany in 1970 with a head full of thermal engineering knowledge, could not have imagined that his heat treatment shop would one day be a critical link in the supply chain for artificial intelligence. But the principles he instilled—technical rigor, patient investment, the belief that understanding heat is understanding everything—those principles turned out to be timeless.

Kaori is, ultimately, a story about the compounding value of deep expertise. In a world that celebrates disruption and pivots, here is a company that never pivoted. It just kept doing what it did, better and better, until the rest of the world realized it needed exactly what Kaori had been building all along. The fifty-year overnight success—forged in a vacuum, and now impossible to ignore.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube