Daiichi Life Group: Unlocking Japan's Financial Giant

I. Introduction & Episode Roadmap

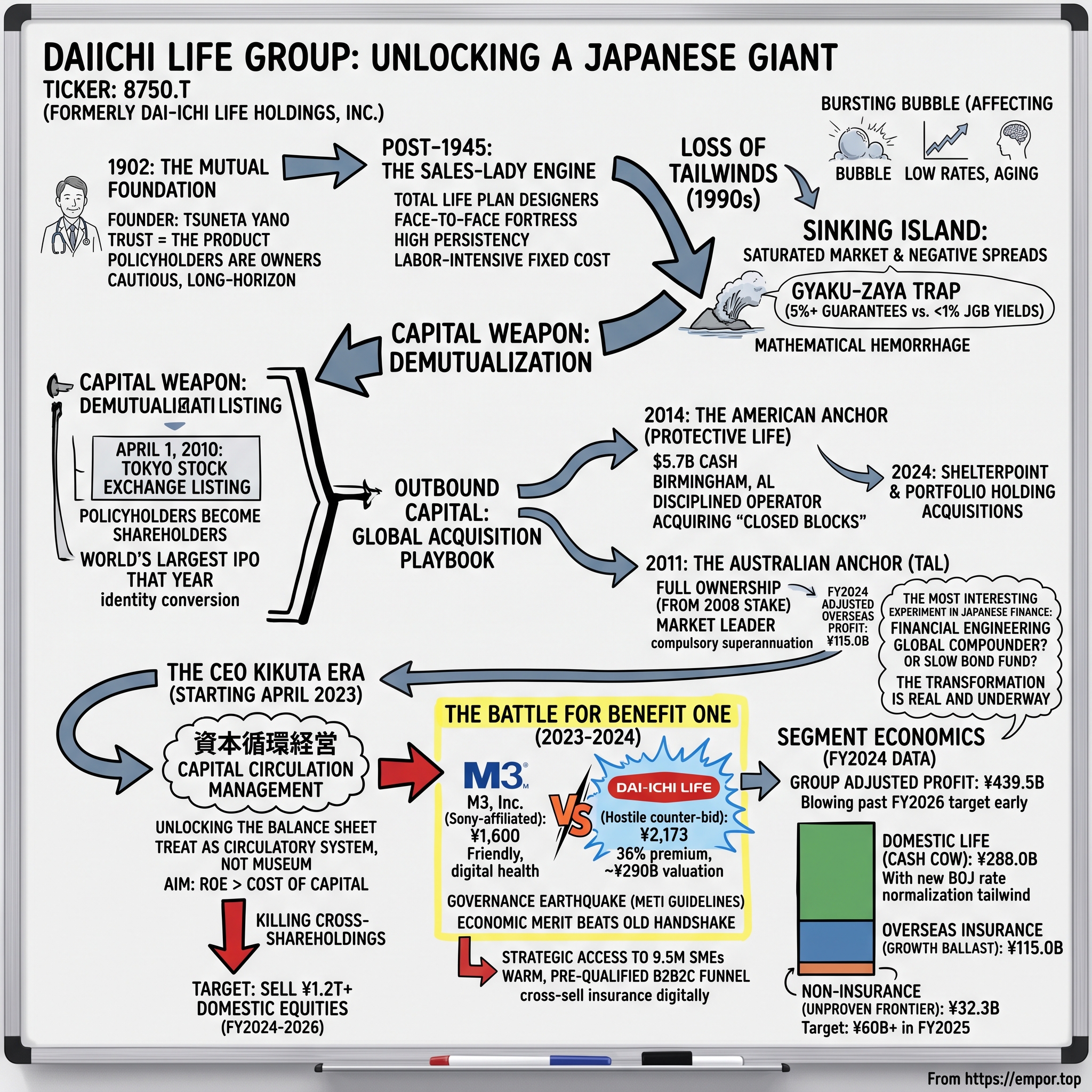

Start with the scale, because the scale is the reason any of this matters. The entity that trades in Tokyo under ticker 8750.T — known until April 2026 as 第一生命ホールディングス株式会社 Dai-ichi Life Holdings, Inc. and now as 第一生命グループ株式会社 Daiichi Life Group, Inc. — sits atop an asset pool of well over ¥65 trillion, north of $400 billion.9 For fiscal 2024, the group posted adjusted profit of ¥439.5 billion, blowing through the ¥400 billion target it had set for FY2026 two full years early.1 It owns the number-one life insurer in Australia, a top-tier US life and annuity platform in Alabama, a 49% stake in one of Japan's largest asset managers, and — since 2024 — a corporate-benefits network reaching roughly 9.5 million Japanese members.5

To feel the scale differently, consider what a life insurer actually is. It is a bank that runs backwards. A normal bank takes deposits it must repay on demand and lends long. A life insurer collects small premiums today against enormous promises decades away, and in the meantime it becomes one of the largest pools of investable capital in its national economy. Daiichi does not merely sell insurance in Japan; it is one of the biggest single owners of Japanese government bonds and, historically, of Japanese equities. When a company like this reallocates its portfolio, it moves markets. When it decides its cross-shareholdings are dead capital and starts selling, corporate Japan notices. The insurer is not a passenger in the Japanese financial system — it is part of the plumbing.

The thesis of this story is not that Daiichi Life is a great company. It is that Daiichi Life is the most interesting experiment in Japanese finance: a test of whether a legacy domestic insurer, staring down the most severe demographic decline in the developed world, can financially engineer its way into a genuinely global, capital-efficient compounder — or whether it is simply a slow-moving bond fund wearing an insurer's clothes. For most of the past decade the market's answer leaned toward the second interpretation: like most Japanese financials, the stock spent years trading below the book value of its own net assets, the market's way of saying it did not believe the company could earn its cost of capital. The entire modern strategy is, in effect, an argument with that verdict.

The engine of the whole story is one structural fact. In 2010, Daiichi did something none of its giant peers — 日本生命保険相互会社 Nippon Life, Sumitomo Life, Meiji Yasuda — has done to this day. It demutualized. It stopped being owned by its policyholders and started being owned by shareholders, listing on the 東京証券取引所 Tokyo Stock Exchange.2 That single act converted a capital straitjacket into a capital weapon, and everything that follows — the US and Australian acquisitions, the balance-sheet surgery, the perks-platform raid, the buybacks — flows from it.

Here is the route. We begin in 1902 with a doctor-turned-bureaucrat and a radical idea about who insurance is for. We move through the lost decades, the "negative spread" trap that killed several of Daiichi's peers, and the historic escape of 2010. We watch the company build offshore platforms in the US and Australia to outrun a shrinking home market. We meet 菊田 徹也 Tetsuya Kikuta, the CEO who decided the balance sheet itself was the product, and coined 資本循環経営 capital circulation management. We sit ringside for the Benefit One bidding war. Then we take the whole thing apart — segment by segment, force by force, bull versus bear — and ask the only question that matters for a long-term owner: from here, does this win, and what breaks it?

To understand why 2010 was such an earthquake, you first have to understand the century of mutual identity it overturned.

II. The Mutual Foundation & Tsuneta Yano (1902 – 1945)

Picture Japan at the turn of the twentieth century: a country barely three decades into the Meiji Restoration, sprinting to industrialize, importing everything from railway gauges to legal codes, and utterly captivated by the machinery of the modern West. Into this ferment stepped 矢野 恒太 Tsuneta Yano, a physician by training who had drifted into insurance regulation inside the government. Yano had studied the European insurance systems closely, and he had come back convinced that the joint-stock insurance companies then sprouting across Japan had the incentives exactly backwards.

A stock insurance company, Yano reasoned, exists to make a profit for its shareholders — and the cleanest way to profit from insurance is to collect premiums and pay out as little as possible. The policyholder and the owner sit on opposite sides of the table. That was a fine arrangement for selling fire coverage on a warehouse. It was, to Yano, a moral and practical disaster for life insurance, a product whose entire value is a promise to a family that may not be collected for forty years. Trust was not a marketing feature; it was the product itself.

Yano was not a typical Meiji businessman. Trained as a physician, he had worked inside the government's insurance-regulation bureau, which gave him a rare vantage point: he had seen, from the supervisor's chair, how insurers behaved and misbehaved. He had also travelled and studied the German and British mutual systems, where policyholder-owned insurers had matured into some of the most trusted institutions in their societies. He came away with a conviction that bordered on the ideological — that life insurance was less a business than a piece of social infrastructure, closer to a public utility than to a trading house. This is worth dwelling on, because it explains a corporate personality that would persist for more than a century: cautious, long-horizon, allergic to speculation, and instinctively suspicious of the idea that shareholders should come first. When Kikuta, four generations of managers later, tries to instill a "shareholder mindset," he is fighting the founder's own DNA.

The pamphlet and the promise

So in 1902 Yano founded 第一生命保険相互会社 The Dai-ichi Mutual Life Insurance Company — Japan's first mutual life insurer.2 Before he launched it, he did something telling for a man who thought of insurance as a civic act: he wrote and circulated a pamphlet titled Characteristics of My Company, laying out plainly why the mutual structure was superior.2 In a 相互会社 mutual company, there are no external shareholders. The policyholders are the owners. Surplus is returned to them as dividends. The company's only masters are the people it insures.

This was not merely idealism, though it was that too. It was a shrewd read of Meiji-era Japan. In a young nation building trust in modern institutions from scratch, a structure that could credibly say "we have no shareholders to enrich at your expense" was a formidable selling proposition. By 1906, Dai-ichi was already paying policyholder dividends; by 1932 it had grown into Japan's second-largest life insurer.2 The mutual model and the nation-building project of modern Japan grew up entwined — long-term, paternalistic, patient, and profoundly conservative.

The sales-lady engine

The other half of Dai-ichi's DNA was forged after 1945, in the rubble of defeat. Japan's men were dead, demobilized, or absorbed into the reconstruction; millions of war widows needed work. The life insurers, Dai-ichi prominent among them, hit upon a distribution model that would define the industry for the next half-century: they recruited armies of women — many of them homemakers and widows — to sell insurance face-to-face, desk by desk in corporate offices and door by door in neighborhoods.

These were the 生涯設計デザイナー Total Life Plan Designers, known universally, and not always kindly, as the "sales ladies." They were a distribution machine of extraordinary reach and stickiness. A sales lady did not merely sell a policy; she visited the same office floor every month for years, knew the workers' families, handled the paperwork, delivered small gifts, and made cancelling a policy feel like a personal betrayal. It was a human network that no competitor could replicate quickly and no customer could easily leave — the kind of proprietary asset a strategist would later label a cornered resource, though everyone at the time just called it the reason the premiums kept coming.

The mechanics of this channel are worth understanding, because they explain both its strength and the trap it would eventually become. Postwar Japan built its social contract around the large corporation. A salaryman joined a firm in his early twenties and, in the classic model, expected to stay for life. The insurers plugged directly into that structure: they negotiated access to company offices, and the sales lady effectively became a fixture of the workplace, signing up new recruits practically as a rite of passage and up-selling them at every life stage — marriage, a first child, a mortgage. The relationship was emotional as much as commercial, which is precisely what made the resulting policies so profitable and so durable. Persistency — the share of policies that stay in force year after year — is the lifeblood of insurance economics, and a channel built on personal loyalty produced persistency that pure price competition never could.

But every one of those virtues carried a cost that only became visible later. The sales-lady model is labor-intensive and therefore expensive. It scales with headcount, not software. And it is culturally load-bearing: tens of thousands of women, many with decades of service, whose livelihoods and dignity are bound up in a channel that the arithmetic of a shrinking, digitizing Japan is slowly rendering uneconomic. You cannot simply switch it off. This is the paradox the whole modern story keeps circling back to — the greatest asset of the twentieth-century business is the heaviest fixed cost of the twenty-first.

For decades this combination — mutual trust plus a face-to-face fortress — looked unbeatable. The weakness was invisible because the environment never tested it: it depended on a growing population, rising incomes, and interest rates high enough to fund the generous guarantees the sales ladies were promising at the kitchen table. Take those away, and the fortress becomes a prison. In 1990, all three began to disappear at once.

III. Saturated Island, Negative Spreads, and the 2010 Demutualization

The 1980s were the years Japan believed it was buying the world. Tokyo land was said to be worth more than all of California; the Nikkei brushed 39,000; and life insurers, flush with premiums and euphoric about the future, competed for customers by promising guaranteed policy yields as high as 5% to 6%. Those guarantees were multi-decade contracts. A policy sold to a thirty-year-old salaryman in 1988 locked the insurer into funding a 5.5% return until that man was in his seventies. In a world of 8% bond yields, easy. In the world that was coming, catastrophic.

On the first trading day of 1990, the bubble began to deflate, and it did not stop for a generation. The Nikkei fell by more than half. Land values followed. And the 日本銀行 Bank of Japan, fighting deflation, pushed interest rates down and down until the yield on ten-year Japanese Government Bonds — the safe asset an insurer buys to fund its promises — sank toward zero, and eventually, in the 2010s, below it.

The gyaku-zaya trap

This produced the single most important concept for understanding Japanese insurance in this era: 逆ざや gyaku-zaya, the "negative spread." The mechanics are brutally simple. An insurer had promised policyholders, say, 5%. The bonds it could now buy yielded less than 1%. Every year, on those old policies, the company bled the difference — guaranteeing a return it could no longer earn, subsidizing the gap out of capital.

Think of it as a mortgage you took out where you pay the bank 5% while the bank invests your money at 1% — forever, on a book worth trillions of yen. This was not a rough patch; it was a slow, mathematically certain hemorrhage. And several insurers did not survive it. Between 1997 and 2001, a string of mid-sized Japanese life insurers — Nissan Mutual, Chiyoda, Kyoei and others — collapsed outright, the first insurance failures in postwar Japan. The negative spread was not a theoretical risk. It was killing companies.

What made the trap so insidious was its invisibility on the surface. A large insurer with a growing block of new, low-guarantee policies and a healthy investment portfolio could report perfectly respectable numbers while, underneath, the legacy high-guarantee policies quietly consumed capital every single year. The industry entered a long twilight in which the healthy new business subsidized the sick old business, and the whole edifice depended on the assumption that rates would eventually recover. They did not. For the better part of two decades, running a Japanese life insurer meant managing a controlled bleed and praying the transfusion — new premiums — kept pace. Dai-ichi, larger and more conservatively reserved than the firms that failed, survived. But survival is not a strategy, and management knew it. The company was running to stand still on an island that was, demographically and financially, sinking beneath it.

The straitjacket

Here the mutual structure that had served Dai-ichi so nobly for ninety years revealed its fatal flaw. A mutual company cannot issue stock. It has no shares to sell to raise fresh capital when losses mount, and no shares to use as acquisition currency to buy its way into faster-growing markets abroad. Its only capital is retained surplus, accumulated slowly over decades. Facing a structural profit drain at home and a shrinking customer base, Dai-ichi was a company that desperately needed to raise and deploy capital, wearing a legal structure specifically designed to prevent it from doing either.

April 1, 2010

The escape took years to engineer and was approved by a policyholders' vote, but the destination was audacious: on April 1, 2010, Dai-ichi demutualized and listed on the Tokyo Stock Exchange.2 Policyholders received shares; the company raised on the order of ¥1 trillion — roughly $11 billion at the time — in what was the largest IPO in the world that year and the biggest Japan had seen in nearly a decade.2 Overnight, the patient mutual became a public company with a stock price, quarterly scrutiny, and shareholders demanding a return on capital.

Demutualization is not a simple corporate maneuver; it is closer to a constitutional convention. Millions of policyholders had to be converted from owners of a mutual into shareholders of a joint-stock company, each allotted shares based on the value of their contributed surplus. The company had to appraise itself, satisfy regulators that policyholders were being treated fairly, and win their formal approval — all while promising that the protection they had bought would be unaffected. The timing, too, tells you something about conviction: Dai-ichi went public in the spring of 2010, with the scars of the global financial crisis still fresh and equity markets skittish. This was not opportunistic peak-cycle listing. It was a company that had decided its very structure was the problem and was willing to list into a difficult market to fix it.

The strategic significance was not the cash, enormous as it was. It was the conversion of identity. Dai-ichi now had a currency — its own equity — and a discipline — the market's — that its rivals lacked. And here is the divergence that defines the modern investment case: Nippon Life, Sumitomo Life, and Meiji Yasuda looked at the same demographic cliff and chose to stay mutual. They remain unlisted to this day, competing on scale and balance-sheet heft, insulated from activist pressure but also frozen out of the equity-funded, M&A-driven game Dai-ichi was about to play. Whether that game creates or destroys value is the open question of this entire story — but only Dai-ichi got to place the bet.

With fresh capital and a shrinking home island, the obvious move was to spend that capital somewhere the population was still growing.

IV. Outbound Capital: The Global Acquisition Playbook

Every strategic decision Dai-ichi has made since 2010 traces back to one chart that no amount of financial engineering can fix: Japan's population peaked in 2008 and has been declining ever since, aging faster than any large society in human history. For a life insurer, this is not a headwind; it is a structural ceiling. Fewer young families means fewer new protection policies. An aging in-force book means more claims and fewer premiums. Organic domestic growth, in the base business, is not slow — it is arithmetically over.

So the demutualized company did the only thing a public insurer with capital and a shrinking home market can do: it exported the capital. But it did so with a specific, and initially unfashionable, discipline. The trap that had ensnared earlier waves of Japanese acquirers — from 1980s Rockefeller Center trophies to overpriced tech deals — was buying glamorous assets at peak prices and then trying to run them from Tokyo. Dai-ichi's playbook was the inverse: buy competent, boring, well-run platforms at reasonable multiples, and then leave the local management almost entirely alone.

The American anchor

The centerpiece landed in 2014. Dai-ichi agreed to buy Protective Life Corporation, a Birmingham, Alabama life and annuity company, for $5.7 billion in cash — $70 a share — in what was then one of the largest-ever acquisitions of a US insurer by a Japanese buyer.3 The deal closed in early 2015.4 What made Protective the right target was precisely that it was not a trophy. It was a disciplined, mid-tier operator with a specific and unglamorous skill: acquiring "closed blocks" of run-off policies from other insurers and administering them at rock-bottom cost.

A closed block is a portfolio of old policies no longer being sold — a stream of future obligations and the assets backing them. To most insurers it is dead weight. To an efficient administrator like Protective, buying these blocks at a discount and squeezing out cost is a repeatable, capital-generative machine. Dai-ichi grasped the key insight: it did not need to teach Protective anything. It needed to fund Protective's acquisitions and get out of the way. Under Japanese ownership, Protective kept rolling up the American market — buying the Disability Benefits Law and paid-leave specialist ShelterPoint in 2024, and agreeing to acquire the reinsurance-services firm Portfolio Holding in a deal that closed on January 1, 2026.1112 For FY2024, Protective contributed ¥57.4 billion of adjusted profit — the single largest overseas engine.1

There is a subtler reason the US anchor mattered so much beyond the profit line. American interest rates, for most of the past fifteen years, were structurally higher than Japan's, and the US life-and-annuity market is vastly deeper and more liquid than Japan's. For a Japanese insurer starved of yield at home, owning a well-run US platform was a way to import higher returns onto the group's consolidated income statement — a portable answer to the domestic negative-spread problem. The trade-off, which we will weigh later, is that it also imported American credit and real-estate risk. But the strategic logic was sound: if you cannot earn a decent return on capital in your home market, buy a business in a market where you can, and let people who understand that market run it. The contrast with the 1980s generation of Japanese acquirers — who bought American assets to plant a flag and then smothered them with Tokyo oversight — is the whole point. Dai-ichi bought cash flows, not flags.

The Australian anchor

The second platform was assembled earlier and even more patiently. Dai-ichi first took a stake in Australia's Tower Australia in 2008, then moved to full ownership by 2011, rebranding it TAL.2 Australia was a shrewd choice: an English-speaking, well-regulated market with a compulsory retirement-savings system — superannuation — that funnels the entire working population into group life insurance. Under Dai-ichi, TAL grew into the number-one life insurer in Australia, dominating both the direct channel and, crucially, the institutional group-life business of insuring super funds' members.2 In FY2024 TAL contributed on the order of ¥42 billion of adjusted profit.1

Building the holding company

The expansion was not confined to two anchors. Dai-ichi built a spread of smaller Asian footholds — in Vietnam, Indonesia, Thailand, Cambodia, and India — plugging into markets where insurance penetration was low and populations were young, the mirror image of Japan. In 2022 it acquired New Zealand's Partners Life, extending the Australasian franchise.2 And it broadened the non-insurance and asset-management wings, folding US alternative-credit manager Canyon Partners into the group to deepen its investment capabilities.1 Not every one of these bets will pay off, and small international insurance operations have a long history of disappointing their owners; the discipline of the strategy is that no single one of them is large enough to sink the group if it fails.

By 2016, the corporate architecture needed to catch up with the reality. Dai-ichi reorganized into a holding company — 第一生命ホールディングス Dai-ichi Life Holdings — sitting above the legacy Japanese operating company, the overseas platforms, and the asset-management arm.2 The point of a holding structure is subtle but important: it separates the slow, regulated, capital-heavy legacy insurer from the faster-growing international and non-insurance businesses, so capital can be allocated between them at the top rather than trapped inside one operating entity. Housed within that structure was a 49% stake in アセットマネジメントOne株式会社 Asset Management One, one of Japan's largest asset managers, formed as a joint venture with みずほフィナンシャルグループ Mizuho Financial Group.2 Asset management matters strategically because it is capital-light: it earns fees on other people's money rather than bearing insurance risk on its own balance sheet, which is exactly the kind of high-return-on-capital business a company chasing capital efficiency wants more of.

The playbook, then, was coherent and — on the evidence of the segment profits — genuinely additive: use the home market as a cash cow, buy platforms not trophies, and let locals run them. What it did not yet do was address the elephant sitting inside the Japanese balance sheet itself: hundreds of billions of yen of capital locked in low-returning legacy holdings. Fixing that would require a different kind of leader.

V. Tetsuya Kikuta & the Era of "Capital Circulation Management"

In April 2023, the top job passed to 菊田 徹也 Tetsuya Kikuta, a career Dai-ichi man who had spent years in corporate planning and risk management — the parts of an insurer where you learn, viscerally, how much capital sits idle.14 That pedigree matters. A CEO who rose through sales might have reached instinctively for the top line — more agents, more policies, more premium. A CEO who came up through risk and planning sees the company as a portfolio of capital charges and returns, an optimization problem more than a growth story. Kikuta's whole framework flows from that lens: he does not talk about Dai-ichi the way an insurance salesman would, but the way a capital allocator would. In a Japanese corporate culture where the president is often a ceremonial consensus-keeper serving a short term, positioning himself as an active portfolio manager of the group's balance sheet was itself a statement of intent.

Kikuta inherited a company that was, in a sense, a victim of its own history: asset-rich, trusted, globally diversified, and yet chronically capital-inefficient. Its adjusted return on equity trailed what a shareholder could get from far simpler businesses. The balance sheet was full of value that was not working.

Kikuta's answer was a phrase that has since become the organizing idea of the whole group: 資本循環経営 capital circulation management. Strip away the corporate poetry and it means something concrete and, for Japan, almost radical. Stop treating the balance sheet as a museum of accumulated assets to be preserved. Treat it as a circulatory system: identify capital trapped in low-return uses, free it by selling those assets or reducing the risk they carry, and pump it into higher-returning uses — or hand it back to shareholders. The stated goal, repeated across investor materials, is to reach a state where the group's capital efficiency consistently exceeds its cost of capital by FY2026.[^13]

Unlocking the dead shares

The richest vein of trapped capital was hiding in plain sight: 政策保有株式 policy-holding shares — cross-shareholdings. For generations, Japanese insurers and their corporate clients held each other's stock as a gesture of relationship, a way to cement commercial ties and discourage anyone from rocking the boat. Dai-ichi sat on trillions of yen of these strategic equity stakes in domestic companies. They generated modest dividends, tied up enormous amounts of risk capital, and gave the insurer essentially no control. To a capital-circulation mind, they were dead money.

So Kikuta committed to killing them, aggressively. Under the FY2024–2026 medium-term plan, Dai-ichi pledged to sell roughly ¥1.2 trillion of domestic equities — around 30% of the equity book — and signaled it would keep selling through FY2027–2030, targeting a residual domestic equity balance of no more than ¥1.5 trillion by the end of FY2030.10 In aggregate the program frees on the order of ¥2 trillion-plus of capital. This is not a rounding error on the strategy; it is the strategy's fuel.

Kikuta was not acting in a vacuum. He had a powerful ally in the 東京証券取引所 Tokyo Stock Exchange itself, which in 2023 began publicly pressing companies trading below book value to publish concrete plans to fix it — a landmark shove that turned "improve capital efficiency" from a foreign investor's complaint into an official expectation. Unwinding cross-shareholdings became the signature move of the whole reform era across corporate Japan, and Dai-ichi, as one of the largest holders of such stakes, was both a major seller and a symbol of the shift. There is an irony worth naming: the insurer was dismantling the very web of relationship-shareholdings its own century of relationship-based business had helped weave. The cross-holding system had once been a feature — a way to lock in commercial ties and keep foreign raiders out. In the new regime it was a bug, a monument to capital that answered to nobody.

Where the billions go

The freed capital flows to three destinations, and the split reveals what management actually believes. First, domestic liability hedging: as the Bank of Japan finally exited negative rates and JGB yields rose, Dai-ichi could reinvest into long-dated Japanese bonds yielding something real, locking in a positive spread on the domestic book for the first time in a generation — the exact inverse of the gyaku-zaya nightmare that nearly sank the industry. The historical resonance here is hard to overstate. For thirty years, higher rates were the thing every Japanese insurer prayed for and none received; the entire industry was built around surviving their absence. Now, as the BOJ normalizes policy after the longest experiment with zero and negative rates in monetary history, the prayer is finally being answered — and Dai-ichi has deliberately positioned itself, by selling equities and buying long bonds, to capture it. Second, growth M&A: funding Protective's US roll-ups and domestic non-insurance bets. Third, and most visible to shareholders, capital return: the group committed to a dividend payout ratio of 45% or higher, backed by large and deliberately flexible buybacks, with a stated path toward 50% as capital efficiency improves.[^12] The flexibility of the buyback is a feature, not vagueness — it lets management repurchase stock opportunistically when the shares are cheap and capital is abundant, rather than committing to a fixed schedule that could force buying at the wrong time.

Skin in the game

There is a cultural tell worth pausing on. Traditional Japanese executives were paid flat salaries — seniority, not performance. Kikuta's reported compensation of around ¥190–193 million for FY2024 is weighted heavily toward performance-linked and restricted-stock pay, roughly 60% variable.15 In FY2024 the group also extended stock-based compensation to domestic employees, trying to instill an ownership mindset in a workforce raised on the mutual, salaried ethos.1 Whether this genuinely aligns behavior or merely dresses up the org chart is a fair question — but the direction of travel is unmistakably toward shareholder capitalism.

A neutral observer should note the tension inside all of this. "Capital circulation" is an elegant narrative, and management has, so far, hit or beaten its headline targets. But the plan's success is not yet proven; it rests on two bets — that rates stay high enough to make JGB reinvestment attractive, and that the growth M&A actually earns its cost of capital. The second bet was tested, spectacularly and in public, in late 2023.

VI. The Great Bidding War: The Battle for Benefit One (2023 – 2024)

For most of 2023, the sale of 株式会社ベネフィット・ワン Benefit One Inc. looked like a done deal. Benefit One ran a corporate employee-benefits platform — the kind that lets a company offer its staff discounted gym memberships, travel, dining, and wellness perks through a single subscription — and its parent, staffing group パソナグループ Pasona Group, wanted out. The natural buyer had already stepped forward: エムスリー株式会社 M3, Inc., the Sony-affiliated digital-healthcare giant, which launched a friendly tender offer that autumn. Pasona had agreed to back it. The deal had a logic everyone understood — digital health meets corporate wellness. Doors closing.

Then, on December 7, 2023, Dai-ichi Life kicked the doors back open. It launched an unsolicited, competing all-cash tender offer at ¥2,173 per share — a stunning premium of roughly 36% over M3's ¥1,600 bid, valuing Benefit One at around ¥290 billion, about $2 billion.5[^7] In a market where the unwritten rules still frowned on gate-crashing another company's agreed deal, a century-old life insurer had just done exactly that, and done it to a company backed by Sony. To grasp how out of character this was, remember the corporate personality we sketched earlier: Yano's cautious, relationship-first, consensus-driven institution, the very archetype of the Japanese company that does not make waves. That such a firm launched the boldest contested takeover of the year tells you how completely the demutualized, capital-efficiency-obsessed Dai-ichi had rewired its own instincts.

Why an insurer wants a perks platform

The obvious question — the one skeptical analysts asked immediately — is what a life insurer was doing bidding for an employee-discount business at all. Kikuta's answer went to the heart of the demographic problem. Benefit One sat at the center of a network of thousands of Japanese small and mid-sized enterprises, reaching roughly 9.5 million individual members.5 That is a vast, warm, pre-qualified B2B2C funnel — exactly the sort of low-cost digital access to customers that the expensive, aging, ~37,000-strong face-to-face agent army could never economically deliver.

The strategic bet was that Dai-ichi could cross-sell medical, cancer, and wellness insurance digitally into Benefit One's membership at a fraction of the acquisition cost of a sales-lady visit. In other words, buy the distribution channel of the future rather than continue subsidizing the distribution channel of the past. It was a coherent thesis — and also, critically, an unproven one, because insurance cross-sell into a benefits platform had never been executed at this scale in Japan.

The governance earthquake

What happened next was, in its quiet way, as significant as the bid itself. Pasona and Benefit One's board reconsidered. The timing was not coincidental: in 2023 Japan's Ministry of Economy, Trade and Industry had issued new guidelines on corporate takeovers that pressed target boards to give sincere consideration to bona fide offers and to act in shareholders' interests rather than reflexively protecting an incumbent bidder or entrenched management. Those guidelines turned what would once have been an unwritten courtesy — "we shook hands with M3, so we honor it" — into a governance liability. Faced with a materially superior economic offer and this new regulatory backdrop, Pasona and Benefit One abandoned the M3 agreement and swung behind Dai-ichi.7 M3, which had built its bid on the strategic logic of merging corporate wellness with its own digital-health platform, declined to escalate into a bidding war and bowed out. The tender offer succeeded in March 2024, and Benefit One became a wholly owned Dai-ichi subsidiary in 2024.68 For students of Japanese corporate governance, the episode was a milestone: economic merit had beaten the old handshake, and it had done so with the explicit blessing of the state's own reform agenda.

Did they overpay?

Now the uncomfortable part, which no neutral account should skip. At ¥2,173 a share, Dai-ichi paid a rich multiple on Benefit One's current earnings — and cross-sell synergies are the most notoriously over-promised, under-delivered numbers in all of M&A. There is a genuine irony that a company preaching capital efficiency and disciplined, sane-multiple acquisitions — the entire lesson of the Protective playbook — turned around and paid a premium-to-a-premium in a competitive auction for a business outside its core. The two behaviors are not obviously consistent. One reading is that Benefit One was a genuinely scarce strategic asset worth stretching for; another, more skeptical reading is that the auction dynamic and the fear of losing to M3 pushed the price past where cold discipline would have stopped. Kikuta defended the price as strategically essential and projected that the group's "non-insurance" segment profit would roughly double, toward ¥60 billion in FY2025.1 But projection is not proof. The bear case writes itself: pay a full price today for synergies that arrive slowly, or not at all, and you are left with a goodwill balance waiting to be impaired. As of this writing, hard evidence that Benefit One's members are actually converting into insurance policyholders remains thin — a point we will return to when we stress-test the story.

The acquisition also became the symbol of the company's new identity, and it got a name to match. On April 1, 2026, the company dropped its hyphen and formally became 第一生命グループ株式会社 Daiichi Life Group, Inc., signaling that it no longer thought of itself as merely an insurance holding company but as a unified financial, wellness, and B2B services group.9 A rebrand is cheap; the strategy behind it is expensive. To judge whether the expense is warranted, we have to open up the machine and look at where the profit actually comes from.

VII. Inside the Machine: Segment Economics & Competitor Dynamics

Behind the corporate poetry, Daiichi Life is fundamentally three businesses stapled together by a holding company, and the FY2024 numbers show exactly how the profit is distributed — and where the risk concentrates. Group adjusted profit of ¥439.5 billion, against an original FY2026 target of ¥400 billion, tells you the plan is running ahead of schedule; the segment breakdown tells you why, and whether it is sustainable.1

Segment one: Domestic Life — the cash cow with a new tailwind

The domestic life business generated roughly ¥288 billion of adjusted profit, close to two-thirds of the group total.1 It runs on three brands aimed at three channels. 第一生命保険株式会社 The Dai-ichi Life Insurance Company is the legacy career-agent book — the sales-lady fortress, high-margin and sticky but structurally in slow decline. 第一フロンティア生命保険株式会社 The Dai-ichi Frontier Life Insurance Co., Ltd. is the bancassurance arm, selling individual savings-type annuities through banks — a channel that lets Daiichi reach customers without paying for a face-to-face visit. And ネオファースト生命保険株式会社 Neo First Life is the digital-native medical brand aimed at younger buyers.

The three-brand structure is itself a strategic answer to the sales-lady problem. Rather than force one channel to serve everyone, Daiichi segments distribution by customer and cost. Bancassurance — selling through bank branches — deserves a moment of explanation because it is central to the economics. When you walk into your bank to roll over a deposit and the teller suggests a savings-type annuity, that annuity is often manufactured by a specialist insurer like Frontier Life and simply distributed by the bank, which earns a commission. For the insurer, this is a dramatically cheaper way to acquire a customer than dispatching a career agent for repeated face-to-face visits: the bank already has the relationship, the foot traffic, and the trust. It is, in effect, renting someone else's distribution rather than maintaining your own standing army. The trade-off is thinner margins and a customer who belongs, emotionally, to the bank rather than the insurer — but for savings products where price and convenience dominate, that is an acceptable bargain.

The economics of the segment overall are turning in Daiichi's favor for reasons that have nothing to do with brilliance and everything to do with the Bank of Japan. Domestic policy volume is flat-to-declining — that is demographics, and it will not change. But rising domestic interest rates are a genuine, structural tailwind: they widen the investment spread on a multi-trillion-yen bond portfolio and, as old high-guarantee policies roll off and new bonds are bought at higher yields, they quietly relieve the negative-spread burden that defined the industry for thirty years. The key competitor, Nippon Life, remains the unlisted mutual giant, fighting on sheer scale and a legacy agent force of 50,000-plus. It is worth being precise about the rivalry: on pure size and domestic reach, Nippon still leads, and its mutual structure gives it a genuine advantage in patience — it never has to explain a soft quarter to a hostile analyst. Daiichi's counter is not that it is bigger. It is that it is more flexible: bank-channel strength via Frontier, a genuinely global earnings base, and — the recurring theme — the ability to optimize its balance sheet using public-market capital and public-market currency that Nippon, Sumitomo, and Meiji Yasuda structurally cannot access. Which model wins is not obvious; it is the central experiment.

Segment two: Overseas Insurance — the growth ballast

The overseas insurance segment delivered ¥115.0 billion of adjusted profit, roughly a quarter of the group.1 Protective in the US did the heavy lifting at ¥57.4 billion, powered by block acquisitions and relentless administrative cost-cutting, with TAL in Australia adding on the order of ¥42 billion off its dominance of institutional group life.1 The analytical point is that this segment is doing exactly what it was bought to do: providing profit growth uncorrelated with, and structurally faster than, the shrinking home market. It is also where the hidden risks live — US corporate credit and commercial real estate backing Protective's annuity books, and Australian regulatory exposure — a concentration we will weigh shortly.

Segment three: Non-Insurance — the unproven frontier

Then there is the newest and smallest slice: non-insurance, at ¥32.3 billion of adjusted profit, around 7% of the group, with management targeting ¥60 billion-plus for FY2025 largely on the full-year consolidation of Benefit One.1 This is the segment carrying the strategic narrative — subscription-like corporate-welfare revenue, digital health, and the promised cross-sell flywheel. It is also the segment where the gap between ambition and evidence is widest. A near-doubling of segment profit is a bold guide; hitting it will be the single cleanest early test of whether the Benefit One thesis is real or rhetorical.

It is worth naming a quiet risk that lurks beneath the tidy segment tables: complexity itself. A domestic mutual insurer was, for all its problems, a simple thing to understand — one country, one product family, one balance sheet. Today's group spans Japanese life, US life-and-annuity, Australian and New Zealand life, a scatter of Asian ventures, asset management across two continents, and a corporate-benefits platform. Each is run by different people under different regulators in different currencies. Diversification of this kind genuinely reduces the risk that any one market sinks the group — but it also raises the risk that management attention is spread thin, that a problem festers unnoticed in a subsidiary, and that the market applies a "conglomerate discount" because outsiders simply cannot see clearly into every corner. An activist would frame the question sharply: is this a focused compounder or an insurance conglomerate acquiring its way into businesses it does not deeply understand? The honest answer is that it is currently both, and which description dominates will be settled by results, not slogans.

Myth versus reality

Two consensus narratives deserve a fact-check. The first myth is that Daiichi is "just a bond proxy" — a place to park money for a dividend and nothing more. The reality is more interesting: roughly a quarter of its profit now comes from overseas insurance operations growing faster than anything in Japan, and its earnings are increasingly a bet on management's capital-allocation skill, not merely on the JGB curve. The second myth runs the opposite way — that Daiichi has transformed into a nimble global wellness-and-services group, as the rebrand implies. The reality is that roughly two-thirds of profit still comes from the traditional Japanese life business, and the non-insurance dream is 7% of the group and unproven. The truth sits between the two slogans: this is a legacy insurer with a genuine, capital-backed transformation underway — neither finished nor fake.

Add it up and you have a portfolio with one mature cash engine finally catching a rate tailwind, one offshore growth engine doing its job, and one small, expensive, unproven bet on the future. Whether that adds up to a durable competitive advantage — or just a well-diversified pool of average businesses — is a question best answered with a framework.

VIII. The Strategic Framework: 7 Powers & Porter's 5 Forces

It is tempting, given the scale and the trust and the century of history, to assume Daiichi Life must have a deep moat. The disciplined answer is more mixed: it has one or two genuinely powerful advantages, several that are eroding, and one it is trying to build with borrowed money. Let us war-game it properly.

Porter's Five Forces

Threat of new entrants: very low. You cannot start a life insurer in a weekend. Regulatory capital requirements are enormous, licensing is slow, and — the deepest barrier of all — no consumer signs a forty-year mortality contract with a brand they have never heard of. Trust compounds over decades and cannot be bought. This is the most durable structural protection the industry has.

Bargaining power of buyers: moderate. An individual shopping for term life has real choice and the internet to compare prices, which pressures margins at the commodity end. But corporate and SME relationships — group contracts, the Benefit One membership base — are far stickier, embedded in payroll and HR systems and renewed almost by inertia.

Bargaining power of suppliers: low. The insurer's raw material is capital, sourced globally, and its distribution is largely proprietary. There is no dominant outside supplier able to squeeze it.

Threat of substitutes: moderate and rising. Robo-advisers, low-cost index funds, and direct wealth platforms increasingly compete for the savings portion of the household wallet — the annuity and investment products. What they cannot substitute is pure mortality and morbidity protection: no ETF pays your family if you die. So the threat is real on the savings side and negligible on the protection side.

Competitive rivalry: high. Nippon Life, Sumitomo, and Meiji Yasuda at home; MetLife, Prudential and others in the bank and digital channels. This is a mature, consolidated, share-of-wallet knife-fight, and it caps pricing power.

Hamilton Helmer's 7 Powers

Switching costs: very high — the real moat. This is where the durable advantage lives. Cancelling a life or medical policy mid-life is genuinely punitive to the customer: you forfeit accumulated surrender value, and you must be re-underwritten at an older age and often a higher price — if you are insurable at all. That asymmetry locks in the in-force book and produces the exceptionally stable, decades-long cash flows that make an insurer investable in the first place.

Scale economies: high. Fixed costs — compliance, IT platforms, actuarial and investment systems — spread across a ¥65 trillion asset base give the giants a unit-cost edge that sub-scale insurers cannot match. It is a real advantage, though one Daiichi shares with its largest rivals rather than owning alone.

Cornered resource: moderate and declining. The ~37,000 career-agent network was, for decades, the cornered resource — irreplaceable, proprietary, impossible to copy quickly. But it is now high-cost and low-productivity in a digital age, an asset slowly curdling into a liability. Management's explicit bet is to substitute a new cornered resource for the old one: Benefit One's 9.5 million-member platform, which no rival Japanese insurer can easily replicate. That substitution is the strategic wager of the decade, and it is unproven.

Network effects: emerging, not established. Benefit One is a genuine multi-sided platform — more corporate clients attract more perk vendors offering deeper discounts, which attract more clients. If the cross-sell works, it becomes a low-cost customer-acquisition flywheel. But "emerging network effect" is a hope with a business model attached, not yet a demonstrated power. And it is worth being clear-eyed about the limits of the analogy: a benefits platform's network effect is real but bounded — it operates within Japan's finite universe of employers, and its members did not join to buy insurance. Grafting an insurance-distribution flywheel onto a discount-perks network is an unproven maneuver, and the burden of proof sits squarely on management.

The composite picture is a company with a strong but undifferentiated moat — the switching costs, scale, and trust that protect every incumbent giant — and a differentiated advantage that is still speculative. That is an unusual profile. It means the downside is well-defended (a big, sticky, trusted insurer does not disappear) while the upside depends almost entirely on execution of the new strategy. For a long-term investor, that asymmetry is the whole shape of the opportunity: the floor is the legacy insurer; the ceiling is whether the transformation is real.

The honest verdict from the framework: Daiichi's moat is switching costs plus scale plus trust — powerful, but shared with its mutual rivals and largely a function of being a big old insurer. Its distinctive advantage — public-market capital and the Benefit One platform — is the part that is unproven. Which is exactly the fault line along which the bull and bear cases split.

IX. The Investment Spine: Bull vs. Bear Case & Activist Stress Test

Every long-term thesis on this company comes down to a single tension: a cheap, cash-generative, rate-sensitive insurer that is also making a large, unproven pivot with shareholders' money. Here is the case on each side, tested rather than asserted.

Why it wins

The rising-rate arbitrage. This is the cleanest, most mechanical part of the bull case, and it does not depend on management being clever. As Japanese rates normalize after a generation at zero, Daiichi is arguably the most direct listed beneficiary among the giants: it is simultaneously selling roughly ¥2 trillion-plus of low-yielding legacy equities and reinvesting into higher-yielding JGBs and credit, widening the domestic investment spread from both ends.10 On the Q2 FY2025 call, management leaned hard on this dynamic and raised its full-year profit outlook — the live version of the same story told in the filings.13

The demutualization dividend. Because it is listed, Daiichi can do what its mutual rivals structurally cannot: return capital aggressively and use ESR headroom to flex buybacks. The 45%-and-rising payout policy and the flexible buyback program are real tools of shareholder value, tethered to adjusted-ROE targets of roughly 12% by FY2026 and 14% by FY2030.[^12][^13] Management has so far hit its headline targets early, which earns it some credibility on execution.

The re-rating optionality. There is a second-order version of the bull case that turns on perception rather than profit. Japanese financials have long traded at depressed multiples, frequently below the book value of their net assets, because the market assumed they would never earn their cost of capital or return surplus to owners. If Daiichi demonstrably breaks that pattern — sustainably out-earning its cost of capital and handing back cash — the reward is not just higher earnings but a higher multiple on those earnings, as the market stops treating it like a capital-destroyer. That double-barreled effect, earnings growth times multiple expansion, is what a re-rating story looks like. It is also the part of the thesis most dependent on things Daiichi cannot fully control: the sustainability of higher Japanese rates and the market's willingness to believe the transformation is durable rather than cyclical.

The wellness flywheel — if it works. Successful integration of Benefit One would convert a low-margin perks business into a digital acquisition funnel for insurance, structurally lowering the cost of selling a policy and finally providing an answer to the sales-lady problem. Note the conditional; it belongs there.

Management credibility, judged by behavior. A neutral assessment has to weigh not just the strategy but the people executing it, and here the record is genuinely mixed-to-favorable. On the positive side of the ledger: the company set a FY2026 adjusted-profit target and beat it two years early; it has consistently unwound cross-shareholdings on or ahead of the disclosed pace; and it has put management pay and even employee compensation on a performance-and-equity footing that matches its rhetoric about capital efficiency. That is a pattern of setting targets and hitting them, which is the single most valuable thing a management team can build. On the skeptical side: the Benefit One price was aggressive for a company that preaches discipline, and the ¥60 billion non-insurance profit projection is exactly the kind of forward promise on which credibility is eventually won or lost. The honest read is that management has earned trust on the parts of the plan that are mechanical — selling equities, buying bonds, returning capital — and has not yet earned it on the part that requires genuine operating execution.

Why it fails — the activist stress test

Now put on the short-seller's hat, because a neutral platform owes the reader the strongest version of the bear case.

The Benefit One hangover. The company paid a rich price for cross-sell synergies that are, historically, the least reliable synergies in finance. If the ¥290 billion bet does not convert members into policyholders at scale, the outcome is not neutral — it is impairment and goodwill write-downs against a segment that was supposed to double its profit. Early hard evidence of conversion is thin. An activist would demand a specific, disclosed cross-sell KPI and treat management's reluctance to publish one as a tell.

The legacy-agent anchor. Winding down or restructuring a politically sensitive, ~37,000-person career-agent network is slow, expensive, and culturally fraught in Japan. The cornered resource of the twentieth century is the fixed-cost overhang of the twenty-first, and it cannot be cut quickly without reputational and human cost.

US credit and real-estate risk. Protective's earnings rest on large blocks of US corporate credit and commercial real estate backing its annuity liabilities. A severe US credit downturn would hit group solvency directly — the price of buying an offshore growth engine is importing offshore tail risk.

The ESR handcuff. The entire capital-return promise is tethered to the group's Economic Solvency Ratio staying comfortably above its target floor (management treats levels above roughly 170% as a green light for flexible returns).16 The Economic Solvency Ratio is, in plain terms, an economic measure of capital against risk — how much cushion the insurer has to absorb a market shock before its solvency is threatened. But ESR is itself market-sensitive: a sharp global equity drawdown or a spike in volatility could compress it and freeze the buybacks precisely when the stock is cheapest — the classic pro-cyclical trap that turns a capital-return story into a disappointment overnight. The very flexibility that management sells as a virtue in good markets becomes a discretion to stop in bad ones.

The interest-rate double edge. The rate story is not a pure positive, and a rigorous bear would press it. Rising rates lift reinvestment yields, yes — but they also reduce the market value of the long bonds already on the books, and a rapid, disorderly rise in Japanese yields could strain the balance sheet even as it improves the long-run earnings picture. The insurer is, in this sense, long duration in a way that helps its income statement and can hurt its solvency simultaneously. The bull case treats normalization as an unalloyed gift; the reality is more of a tightrope, and the pace of the BOJ's exit matters as much as the direction.

The activist's summary would be pointed: this is a company doing many of the right things — cutting cross-holdings, returning capital, aligning pay — but its transformation story rests on an unproven acquisition, its capital return is hostage to markets, and its cheapest, most reliable tailwind (rates) is the one part management can take no credit for. Bull and bear are not arguing about the facts. They are arguing about whether the Benefit One bet pays off and whether rates stay high — two variables, one of which is outside anyone's control.

For a long-term owner, that framing points to what actually deserves watching.

What to actually track

Ignore the quarterly noise and watch three things. First, group adjusted profit and adjusted ROE against the 12%/14% targets — the single cleanest scorecard for whether capital circulation is genuinely lifting returns rather than just reshuffling assets. Second, the pace and price of the domestic-equity divestment and its reinvestment yield — this is the mechanical engine of the whole thesis, and it is measurable. Third, non-insurance segment profit and any disclosed Benefit One cross-sell metric — because that number, more than any speech, will reveal whether the ¥290 billion bet was strategic vision or expensive hope.

X. Epilogue & Lessons for Founders and Investors

Stand back from the balance sheet and the segment tables, and the Daiichi Life story resolves into something larger than one insurer. It is a case study in how a company escapes a structure that no longer fits the world it lives in — and what that escape costs and unlocks.

The corporate structure is the strategy. For 108 years the mutual form was Dai-ichi's greatest asset — the source of its trust, its patience, its alignment with policyholders. Then the environment changed, and the same structure became a cage. The lesson is not that mutuals are bad; they are extraordinarily resilient. It is that legal form and strategic ambition must match, and when they diverge, structure wins until you change it. Demutualization was the single act that made everything since — the acquisitions, the buybacks, the Benefit One raid — even conceivable. Nippon Life is larger and safer; it will also never play this game.

Buy platforms, not trophies. Dai-ichi's offshore record is instructive precisely because it is unglamorous. Protective and TAL were not prestige assets; they were competent local operators bought at sane prices and left to run themselves. The Japanese acquirers who bought trophies at the peak mostly wrote them off. The ones who bought platforms and paid local management to keep compounding built durable earnings. It is a lesson that survives translation into any industry.

Actively arbitrage your own balance sheet — but prove it pays. The most modern idea in this century-old company is the refusal to let capital sit idle. Converting dead cross-shareholdings into JGB yield and digital-wellness optionality is exactly the kind of self-restructuring that separates a compounder from a museum. And yet the neutral investor must hold two thoughts at once: the discipline is real and rare, but its payoff — especially the Benefit One leg — is not yet proven. Management has earned credibility by beating its early targets; it has not yet earned the benefit of the doubt on the biggest bet it has ever made.

There is a final lesson that transcends the balance sheet, and it is about time horizons. Nearly everything that defines Daiichi today was set in motion by decisions whose payoffs arrived years or decades later. Yano's choice of the mutual form in 1902 built a reservoir of trust that funded a century of growth. The demutualization of 2010 did not "work" in any visible way for years; its value only showed up when the company deployed the freedom it bought. The Protective acquisition looked expensive in 2014 and obvious in hindsight. Even Kikuta's capital-circulation program is a bet whose verdict will not be in until the end of the decade. Insurance is the ultimate long-duration business — its liabilities stretch forty years out — and it rewards, punishes, and exposes management on the same timescale. Investors conditioned to quarterly results are, in a sense, watching the wrong clock.

That is where the story sits in mid-2026: a legacy giant that did the hard structural work its peers refused to do, now standing on the outcome of a wager it has not yet won. Whether Daiichi Life becomes a genuine global wellness-and-capital-efficiency compounder or reverts to a well-run bond fund with an insurance license is not yet knowable. What is knowable is that, alone among Japan's insurance titans, it gave itself the freedom to find out — and that the same demutualization which handed it that freedom also handed it the market's judgment, quarter after quarter, on whether it is using it well.

References

-

FY2024 Financial Results Presentation (May 15, 2025) — Dai-ichi Life Holdings, Inc. ↩↩↩↩↩↩↩↩↩↩↩

-

Japan's Dai-ichi Life agrees to buy Protective Life for $5.7 billion — CNBC, 2014-06-04 ↩

-

Dai-ichi Life to Acquire Protective Life — Protective Life Corporation press release, 2014 ↩

-

Dai-ichi Life Buys Benefit One for $2 Billion After Rare Bid War — Bloomberg, 2024-03-12 ↩↩↩

-

Dai-ichi Life succeeds in bid for Benefit One — The Japan Times, 2024-03-12 ↩

-

Dai-ichi Life gets Pasona's nod on Benefit One acquisition — The Japan Times, 2024-02-08 ↩

-

Acquisition of Benefit One Inc. as a wholly owned subsidiary — Dai-ichi Life Holdings, Inc. press release, 2024 ↩

-

Daiichi Life Group Unveils New Trade Names and Corporate Brand — Daiichi Life Group, Inc., 2025 ↩↩

-

Domestic Equity Investment Stance — Dai-ichi Life Holdings, Inc. ↩↩

-

Protective to Acquire ShelterPoint — Protective Life Corporation press release, 2024 ↩

-

Protective Life to Acquire Portfolio Holding, Inc. — Daiichi Life Group, Inc. press release, 2025 ↩

-

Earnings call transcript: Dai-ichi Life raises FY profit outlook amid strong Q2 2025 results — Investing.com, 2025 ↩

-

Dai-ichi Life Holdings (8750) Leadership & Management — Simply Wall St ↩

-

FY2024-Q2 Financial Analyst Meeting Q&A Summary — Dai-ichi Life Holdings, Inc. ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube