The Great Corporate Unwinding: How a Price-Fixing Scandal Unlocked the Trillion-Yen Empire of MS&AD

I. Introduction & Episode Roadmap

Picture a mid-level procurement officer at 東急株式会社 Tokyu Corporation, the Tokyo railway-and-department-store conglomerate, sometime in late 2022. He is doing something profoundly boring: comparing insurance quotes for the group's sprawling property portfolio. Four of Japan's largest non-life insurers have submitted bids to share the risk. And as he lines the numbers up in a spreadsheet, he notices something that should be statistically impossible. The premiums are identical. Not close. Not within a rounding error. Identical, down to the last yen.1

That spreadsheet became the loose thread that unraveled a system nearly a century old. What followed was a regulatory earthquake that reached into the boardrooms of every major Japanese insurer, exposed a cozy web of relationships that had quietly taxed corporate Japan for generations, and forced one of the country's great financial institutions to blow up its own architecture.

That institution is MS&ADインシュアランスグループホールディングス株式会社 MS&AD Insurance Group Holdings, Inc. (JPX: 8725.T), Japan's largest non-life insurer by market share and one of the ten largest property-and-casualty groups on Earth. As of July 2026 it carried a market capitalization of roughly ¥6.4 trillion (about $43 billion), writing trillions of yen in premiums a year across 40-plus countries.2 For most of its life it was exactly the kind of company a foreign investor would scroll past: conservative, asset-heavy, opaque, and cheap for reasons that seemed structural rather than temporary.

This is the story of how that changed. Of how a company that spent seventeen years deliberately running two separate insurance subsidiaries — to avoid hurting anyone's feelings — decided in 2025 to finally merge them. On April 1, 2027, 三井住友海上火災保険株式会社 Mitsui Sumitomo Insurance Co., Ltd. (MSI) and あいおいニッセイ同和損害保険株式会社 Aioi Nissay Dowa Insurance Co., Ltd. (ADI) will combine into a single carrier, 三井住友あいおい損害保険株式会社 Mitsui Sumitomo Aioi Insurance Company, Limited, and the parent holding company will take a new name of its own.3

The catalyst was not a visionary CEO or a McKinsey deck. It was a scandal. The collapse of Japan's centuries-old system of 政策保有株式 (policy-holding, or strategic cross-shareholdings) — triggered by that price-fixing investigation — pulled the load-bearing wall out from under the entire industry's business model. And in doing so, it handed MS&AD a once-in-a-generation opportunity to convert a mountain of dead, unproductive equity into cash, buybacks, and a genuinely different kind of company.

The question this story keeps returning to is a skeptical one. Is MS&AD becoming a high-return compounder because management finally got religion on capital efficiency? Or is it simply being marched, at regulatory gunpoint, out of a comfortable arrangement it never would have left voluntarily — and if so, what happens to its profits when the comfort is gone? Let's start where all Japanese corporate stories start: with the industrial families.

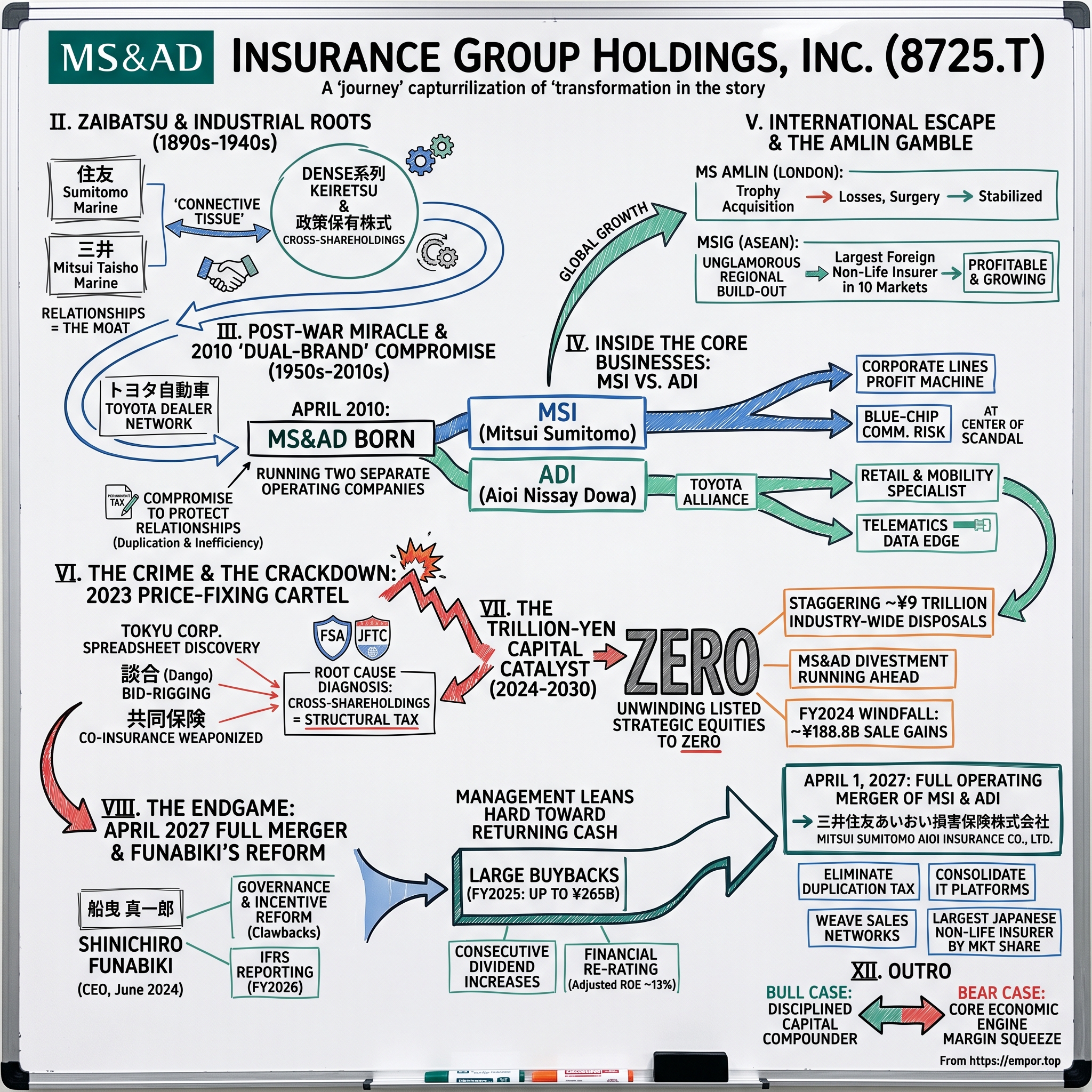

II. The Zaibatsu & Industrial Roots (1890s – 1940s)

To understand why four insurers were quoting identical prices in 2022, you have to go back to a world where competing on price would have been considered almost rude.

In 1893, in the mercantile bustle of Osaka, a marine insurer was founded to serve the shipping and trading interests orbiting the 住友 Sumitomo house — one of the great 財閥 zaibatsu, the family-controlled industrial conglomerates that built modern Japan.4 A quarter-century later, in 1918, a parallel institution named Taisho Marine & Fire Insurance was established in Tokyo, wired into the 三井 Mitsui zaibatsu, the oldest and grandest of them all, with roots in a 17th-century kimono shop and money-lending house.

These were not insurance companies in the way an American or British investor of the era would recognize. They were not competing for the public's business on a shop floor. They were captive utilities — organs of the industrial body they belonged to. The Mitsui trading house needed to insure its cargoes, its warehouses, its factories; Taisho Marine existed to underwrite them. The premiums stayed inside the family. The risk stayed inside the family. And crucially, the insurer held shares in the very companies it insured, while those companies held shares right back.

This is the mechanism that matters for everything that follows, so it's worth slowing down on it. Imagine a village where the blacksmith owns a stake in the farm, and the farmer owns a stake in the smithy, and neither would ever dream of shopping around for a cheaper horseshoe or a better price on wheat — because to do so would be to undercut the value of their own holdings and, worse, to insult a partner. That reciprocal ownership was 政策保有株式, the strategic cross-shareholding. It was not primarily a financial investment. It was a handshake made permanent, a loyalty bond encoded on a share register. Multiply it across thousands of firms and you get the 系列 keiretsu: dense, interlocking networks of ownership and obligation that made Japanese capitalism cohesive, patient — and almost completely closed to outside competition.

Within this world, insurance pricing was barely a market activity at all. Premium rates were heavily regulated and standardized. Where a risk was too large for one insurer, the majors wrote it together through 共同保険 co-insurance contracts, dividing the premium pool among themselves at pre-arranged, identical rates. Sharing large risks is normal and prudent everywhere in global insurance — Lloyd's of London was built on it. But in Japan the practice fused with the cross-shareholding culture into something more troubling: a habit of arriving at the same number, together, as a matter of routine. Nobody thought of it as collusion. It was simply how gentlemen did business.

The war and the postwar American occupation formally dissolved the zaibatsu holding companies. But the relationships did not die; they reorganized into the looser keiretsu groupings, and the cross-shareholdings survived as their connective tissue. Taisho Marine would later become Mitsui Marine & Fire in 1991; Osaka Marine became Sumitomo Marine & Fire. Different names, same DNA. The insurers had learned a lesson that would prove extraordinarily durable and, eventually, extraordinarily expensive: relationships, not prices, were the moat. Hold your client's shares, and you hold your client.

That lesson worked beautifully for decades. Then the ground began to shift beneath it.

III. The Post-War Miracle, Deregulation, and the 2010 "Dual-Brand" Compromise (1950s – 2010)

The engine that reshaped Japanese insurance in the second half of the 20th century was not finance. It was the automobile.

As postwar Japan rebuilt itself into an industrial superpower, the car became the country's defining export and its defining domestic risk. Tens of millions of new drivers meant tens of millions of compulsory auto policies — a vast, recurring, high-frequency stream of premium unlike the lumpy corporate risks of the old marine business. And into that stream stepped a new kind of insurer, aligned not with a bank-centered zaibatsu but with a manufacturer. Chiyoda Fire & Marine grew up heavily backed by トヨタ自動車株式会社 Toyota Motor Corporation, pioneering a model where insurance was sold through the car dealership itself — you bought the Corolla and the policy in the same showroom, from the same salesman. That dealer-distribution channel would become one of the most valuable assets in the entire Japanese industry. Chiyoda later merged with Dai-Tokyo Fire to form Aioi Insurance in 2001, carrying the Toyota relationship with it.

Meanwhile, the walls were coming down. In the late 1990s Japan launched its financial "Big Bang," a sweeping deregulation that dismantled the rigid rate controls and product restrictions that had kept the insurance market frozen in amber. Premiums could now, in theory, be competed. Foreign entrants circled. And a fragmented industry of dozens of mid-sized carriers — each too small to absorb the coming volatility of catastrophe risk and technology spending — began a frantic decade of consolidation.

When the music stopped, three giants stood where a crowd had been. Tokio Marine Holdings emerged as the blue-blood leader. Sompo Holdings assembled itself from another cluster of mergers. And in April 2010, a third colossus was born from the integration of Mitsui Sumitomo Insurance, Aioi Insurance (the Toyota-aligned auto specialist), and Nissay Dowa General Insurance (backed by 日本生命 Nippon Life, the country's largest life insurer): MS&AD.5 Together the "Big Three" would come to control close to 90% of Japan's domestic non-life market — one of the tightest oligopolies in the developed world.

But here MS&AD made a fateful choice, and it is the choice this entire episode circles back to. When Mitsui Sumitomo, Aioi, and Nissay Dowa came together, management did not fully merge the operating companies. Instead, it created a hybrid: the three legacy insurers were combined into two subsidiaries — MSI and, from 2010, Aioi Nissay Dowa (ADI) — which continued to operate as distinct brands under a single holding company.

Why keep them separate? Because the moat was made of relationships, and relationships are jealous. A blue-chip Mitsui or Sumitomo client, insured for generations by Mitsui Sumitomo, might bristle at suddenly being served by a carrier stamped with the Toyota-linked Aioi brand — and vice versa. Management feared culture clash, feared losing captive corporate accounts, feared that forced integration would hand rivals an opening to poach the very cross-shareholding-anchored clients that made the whole thing profitable. So it compromised. It preserved two headquarters, two nationwide agency forces, two IT backbones, two of nearly everything.

This was a rational decision inside the logic of the old system. It was also, viewed from the outside, an enormously expensive one — a permanent duplication tax paid to keep legacy egos and legacy relationships undisturbed. For seventeen years, MS&AD would run what was essentially two companies wearing one holding-company hat, and the market would quietly discount the stock for the inefficiency. The compromise made sense only as long as the relationships it protected were worth more than the money it wasted. The moment that stopped being true, the whole structure would look absurd. Before we get to that reckoning, we need to look inside the two engines themselves.

IV. Inside the Core Businesses: MSI vs. ADI

If you want to understand MS&AD as a business rather than a stock, the essential fact is that it has never really been one company. It has been two very different animals sharing a cage.

Start with the cage itself: the domestic non-life oligopoly. Together, Tokio Marine, Sompo, and MS&AD write the overwhelming majority of Japan's property-and-casualty premiums — roughly 90% of a market worth on the order of ¥9 trillion in annual net premiums.6 This is a mature, slow-growing, but ferociously stable pool of money. In an aging country where auto and fire premiums grind higher only slowly, the game is less about winning share than about pricing risk correctly and keeping costs down. It is, in other words, exactly the kind of market where a duplicated cost base quietly bleeds you.

Now the two animals. 三井住友海上火災保険 Mitsui Sumitomo Insurance (MSI) is the corporate engine — the profit-and-revenue heavyweight of the group. In fiscal 2024 (the year ended March 2025), MSI generated on the order of ¥2,492.6 billion in ordinary income and roughly ¥459.9 billion in net income, according to the group's disclosures.7 MSI is where the blue-chip commercial business lives: the factory fire policies, the marine cargo, the complex liability and specialty risk advisory sold to the largest Japanese enterprises. It is the direct heir to the Mitsui and Sumitomo zaibatsu relationships, and it is precisely these lucrative corporate lines that sat at the center of the price-fixing scandal — a point we will return to with some force.

あいおいニッセイ同和損害保険 Aioi Nissay Dowa Insurance (ADI) is the other animal entirely: the retail and mobility specialist. In fiscal 2024 it produced roughly ¥1,430.4 billion in ordinary income and about ¥108.7 billion in net income.7 Notice the shape of those numbers — a lot of revenue, a much thinner slice of profit. That's the signature of a high-volume, personal-lines business: millions of individual auto and household policies, sold through a vast dealer and agency network, each one small, the margins earned on operational grind rather than on advisory pricing power.

And ADI's crown jewel is its relationship with Toyota. This is not a vague "partnership"; it is deep operational plumbing. Through joint ventures such as Toyota Insurance Management SE in Europe and Toyota Insurance Management Solutions in the United States, ADI plugs directly into the global Toyota dealership network, and increasingly into the cars themselves. Modern Toyotas are rolling sensor arrays, streaming data on speed, braking, cornering, and mileage. ADI uses that connected-car data to build telematics products — insurance that prices your premium on how you actually drive rather than on a crude actuarial guess based on your age and postcode. Its "TOUGH Connecting Car Insurance" is an early expression of this idea.

Why does that matter to an investor? Because telematics is one of the few places where a Japanese non-life insurer has a plausible, hard-to-copy edge. Pricing risk more accurately than a rival is the whole game in insurance, and privileged access to Toyota's fleet data is a genuine informational advantage — the closest thing ADI has to a proprietary resource. The obvious question, which we'll interrogate later, is how durable that edge is when Toyota is a partner and not an owner, and when every automaker on Earth is now sitting on the same kind of data.

Two animals, then: one a corporate-lines profit machine built on relationships, the other a retail-mobility grinder built on a manufacturer alliance. For seventeen years the argument for keeping them caged separately was that their clients were too different to share a brand. To see why that argument collapsed, we have to follow the money out of Japan — and watch MS&AD learn, painfully, what happens when it ventures beyond home.

V. The International Escape: Going Global & The Amlin Gamble (2010s)

Every Japanese growth story eventually runs into the same wall, and it is made of demographics.

Japan is getting older and smaller. Fewer young drivers means fewer new auto policies; a shrinking population and workforce means a domestic premium pool that, however stable, is essentially flat-lining over the long run. For a company the size of MS&AD, "manage a slowly declining home market efficiently" is a survival strategy, not a growth strategy. So, like Tokio Marine and Sompo before and alongside it, MS&AD went shopping abroad. The logic was straightforward and correct: to grow, it had to import risk from faster-growing or higher-margin markets.

The headline expression of that logic came in 2016, when Mitsui Sumitomo completed the acquisition of Amlin plc, a storied London-listed specialty insurer and Lloyd's of London underwriter, for roughly £3.5 billion.8 The deal had been struck at a rich premium — the kind of price you pay when you are a cash-rich buyer with strategic ambition and a weak yen making London assets look tempting. Overnight, MS&AD acquired a marquee position in the Lloyd's market, the world's oldest and most prestigious specialty-insurance ecosystem, and rebranded the unit MS Amlin.

Did they overpay? On the evidence of the following years, the honest answer is: yes, and then some. The MS Amlin era became a case study in how a trophy acquisition can turn into a multi-year headache. Between roughly 2017 and 2022, the unit was battered by a brutal sequence: a run of global natural-catastrophe losses as climate-driven wildfires and hurricanes intensified, COVID-19 business-interruption claims, exposures tied to the Russia-Ukraine war, and painful inflation-driven write-ups of prior-year claims reserves — the "incurred but not reported" liabilities (IBNR) that insurers estimate today and true up later, usually at the worst possible moment. The result was repeated, severe underwriting losses in exactly the business MS&AD had paid a premium to own.

It took years of unglamorous surgery to fix. Management imposed strict underwriting reform — the industry euphemism is "cycle management," meaning the discipline to shrink or exit lines when prices are bad and lean in only when they're good — pruning the risk book back toward profitability. Only relatively recently has MS Amlin been described as stabilized. The episode is a useful antidote to the idea that MS&AD's current management is uniformly brilliant at capital allocation: it bought high, bled for half a decade, and had to rebuild the thing it bought.

But here is the twist that the Amlin headlines obscured. While MS Amlin was soaking up attention and losses in London, MS&AD had quietly assembled something far more valuable in Southeast Asia. Under the MSIG banner, the group built what it describes as the largest foreign non-life insurer with a presence across all ten ASEAN markets — the only insurer with a direct underwriting network spanning the entire region, from Singapore and Thailand to Indonesia, Vietnam, and Myanmar.9 Unlike Amlin, ASEAN offered what Japan could not: young populations, rising incomes, and low insurance penetration climbing off a small base. It was profitable, it was growing, and it was strategically defensible in a way a Lloyd's book never is.

The contrast between the two overseas bets is the real lesson of MS&AD's globalization: the loud, expensive, prestigious acquisition disappointed, while the patient, unglamorous regional build-out became the genuine crown jewel. It's a pattern worth remembering when management next tells you which of its trophies to admire. And it sets up the central irony of this whole story — because for all the drama abroad, the force that would finally reshape MS&AD came not from London or Jakarta, but from a spreadsheet in a Tokyo procurement office.

VI. The Crime and the Crackdown: The 2023 Price-Fixing Cartel

Return now to that Tokyu Corporation employee and his impossible spreadsheet. What he had stumbled onto was not a glitch. It was the visible surface of a practice so ingrained that the people doing it barely registered it as wrongdoing.

When co-insurance bids from the big Japanese insurers — Tokio Marine, Sompo, MSI, and ADI among them — came in identical to the yen, it was because underwriters at the rival firms had, in effect, agreed in advance who would lead, at what price, and how the pie would be split. This was the 共同保険 co-insurance mechanism, honorable in principle, quietly weaponized into 談合 (dango, or bid-rigging). The insurers weren't competing to offer Tokyu the best price on its risk. They were coordinating to preserve the price. Once Tokyu's complaint surfaced in 2023, the scandal metastasized with astonishing speed, as reporters and regulators discovered the same fingerprints across a long list of major corporate accounts.10

金融庁 Japan's Financial Services Agency (FSA) and the 公正取引委員会 Japan Fair Trade Commission (JFTC) launched sweeping, parallel probes. The investigations uncovered systemic, pre-arranged premium-setting across hundreds of corporate contracts, touching household names and critical infrastructure. In December 2023, the FSA issued business improvement orders to the core operating units of all three giants — including MSI and ADI — a stern regulatory rebuke that forced each company to submit and execute detailed remediation plans.11 The following year, in October 2024, the JFTC brought the antitrust hammer down, issuing cease-and-desist orders and surcharge payment orders against the offending insurers.12 Shares in the sector wobbled as the news broke, though — tellingly — they recovered quickly, a sign that investors saw the direct fines as survivable.13

But the fines were never the real story. The lasting damage — and, paradoxically, the lasting opportunity — came from the diagnosis. When the FSA dug into why this collusion had proven so durable and so casual, it kept arriving at the same root cause: the cross-shareholdings.

Here the regulator said out loud what everyone in the industry had always known and never confronted. The insurers held enormous strategic equity stakes in their corporate clients. Those clients, in turn, felt obligated to keep buying insurance from the firms that owned their shares — and to tolerate inflated premiums as the price of the relationship. Why haggle over a fire policy with a partner who is also a loyal, permanent shareholder propping up your stock and your governance? And why would the insurers ever compete hard on price when the business was guaranteed by the share register anyway? The 政策保有株式 that had knitted corporate Japan together for a century was, the FSA concluded, the very thing that made genuine competition impossible. It was, in effect, a structural tax on the Japanese economy — an invisible surcharge on every corporate insurance policy, paid in the currency of loyalty.

That is a remarkable thing for a regulator to say, because it doesn't just condemn a few rogue underwriters. It condemns the entire operating model that MS&AD and its peers had been built on since the days of Taisho Marine. The scandal, in other words, could not be fixed by firing some salesmen and writing better compliance manuals. It could only be fixed by dismantling the thing that caused it. And in early 2024, that is exactly what the regulators demanded — setting in motion the largest voluntary destruction of trapped capital in the history of Japanese finance.

VII. The Trillion-Yen Capital Catalyst: Unwinding to Zero (2024 – 2030)

Every so often a regulatory crackdown does something its authors never quite intended: it makes the target companies far more valuable. The unwinding of Japan's insurance cross-shareholdings is shaping up to be one of the great examples.

Under sustained pressure from the FSA's diagnosis and, running in parallel, the Tokyo Stock Exchange's high-profile campaign to shame chronically undervalued companies into improving capital efficiency, the three insurance giants made an extraordinary commitment. They would sell all of their listed strategic cross-shareholdings — not trim them, not reduce them to a "policy" level, but drive the balance to zero by around March 2030.14 For an industry that had treated these holdings as sacred, untouchable relationship bonds, this was the corporate equivalent of agreeing to demolish the family shrine.

The numbers involved are staggering. Across the industry, the listed equities marked for disposal ran to something on the order of ¥9 trillion in value — a colossal pool of capital that had been sitting inert on insurance balance sheets, generating dividends but doing almost nothing productive, and exposing shareholders to the whims of the Japanese equity market for no good underwriting reason.[^15] For MS&AD specifically, this was a treasure vault whose door had just been forced open. The group moved aggressively, running ahead of schedule; by December 2025 it had divested on the order of ¥600 billion of holdings under its running plan, and in fiscal 2024 alone it booked around ¥188.8 billion in gains on equity sales, a windfall that helped drive group profits to record highs.7

Now, an important note of skepticism, because this is where a promotional narrative would get carried away. Selling an appreciated stock and booking the gain is not, by itself, value creation — the value was always there on the balance sheet; the company is simply converting one asset (shares) into another (cash) and recognizing an accounting gain in the process. A one-time sale gain flatters the income statement without making the underlying insurance business one yen better. So the real test is not whether MS&AD sells the shares — the regulator has guaranteed that — but what it does with the money. That is where the story either becomes genuinely transformational or fizzles into financial theater.

On the evidence so far, management has leaned hard toward returning the cash. The company shifted into an aggressive capital-return posture, adopting a total-payout framework and executing large buybacks — repurchases measured in the hundreds of billions of yen, including a program of up to ¥265 billion authorized for fiscal 2025.15 On the dividend side, it has built a long record of consecutive annual increases and guided its per-share payout steadily upward, toward the ¥170 area for fiscal 2026.15 Reducing the share count while raising the dividend is the textbook way to convert a bloated balance sheet into per-share value, and it is exactly what activists and the TSE had been demanding.

The intended endpoint is a financial re-rating. Management has set adjusted return-on-equity targets that step up materially — an adjusted ROE in the low double digits, roughly 13% including equity-sale gains, and a stated ambition to sustain double-digit returns on core business profits even after the one-off sale gains run dry.7 That last clause is the one that matters. Anyone can post a big ROE while liquidating a decade of appreciated stock. The question that separates a real compounder from a value trap dressing up for a party is whether MS&AD can still earn attractive returns in 2031, when the shares are gone, the gains are booked, and the only thing left to compete on is the actual business of underwriting risk. Which brings us to the man who has staked his tenure on the answer, and to the structural bet he is making to secure it.

VIII. The Endgame: The April 2027 Full Merger & Shinichiro Funabiki's Reform

In June 2024, 船曳 真一郎 Shinichiro Funabiki took over as President and CEO of MS&AD.16 On paper he is the ultimate insider — a career Mitsui Sumitomo man who rose through corporate planning and the executive ranks over three decades, having already served as president of the MSI operating company.17 You might reasonably expect such a figure to be a defender of the old order. Instead, he has positioned himself as the executioner of it.

Funabiki inherited a company at an inflection point, and to his credit he has not treated the scandal as a PR problem to be managed and forgotten. He has treated it as a mandate. His governance reforms lean into the changes the crisis forced, and his own incentive structure signals the shift he wants the whole organization to internalize: compensation split roughly into thirds — fixed pay, performance-linked cash, and restricted stock — with clawback provisions that can reach back and reclaim awards in the event of compliance failures.16 Executive-pay design is easy to over-read, but the direction is unambiguous: tie the leadership's wealth to the share price and to clean conduct, not to preserving cozy relationships. Whether it changes behavior is something only time and the next scandal-free decade can prove.

The intellectual core of Funabiki's reform is a syllogism, and it is worth stating plainly because it explains the merger. If the cross-shareholdings are being driven to zero, then the relationship-based lock on corporate clients disappears. If that lock disappears, then MS&AD's blue-chip customers will — for the first time in living memory — genuinely shop around, forcing the company to win on price, service, and technology rather than on the share register. And if MS&AD has to win on cost and price, then running two duplicative insurance companies side by side — two headquarters, two systems, two agency forces — is no longer a defensible compromise. It is a liability. The seventeen-year truce between MSI and ADI, built to protect relationships that are now being deliberately dissolved, has lost its reason to exist.

So Funabiki did what his predecessors would not. The board approved the full merger of MSI and ADI on March 28, 2025; in September 2025 the group confirmed the new names — the combined carrier will be 三井住友あいおい損害保険株式会社 Mitsui Sumitomo Aioi Insurance Company, Limited, and the holding company itself will be renamed — and the parties subsequently signed the definitive merger contract, with the combination set to take legal effect on April 1, 2027.318 When it does, it will create the largest non-life insurer in Japan by domestic market share, edging past longtime leader Tokio Marine.18

The mechanics of the merger are, in essence, the systematic elimination of the duplication tax. Overlapping IT infrastructure — long a notorious cost sink, run through the group's shared systems arm — will be consolidated onto common platforms. Redundant regional offices will be closed. Two national sales networks will be woven into one. The prize is billions of yen in stripped-out SG&A, and, just as importantly, a single unified balance sheet with the scale to absorb catastrophe volatility and fund the enormous technology investment modern insurance demands. Management insists it will preserve the specialized franchises that matter — dedicated capabilities to keep Toyota's mobility ecosystem and the regional retail networks satisfied — so that integration captures the savings without shattering the moats.

That is the plan. It is coherent, it is overdue, and it is genuinely hard to execute — Japanese IT mergers in particular have a long and grim history of budget overruns and go-live disasters. The bull and bear cases for MS&AD both flow directly from whether Funabiki can pull it off while the ground shifts under him. Before we get there, it's worth stepping back to ask a colder, more structural question: once the relationships are gone, what — if anything — actually protects this business?

IX. Competitive Moat: Hamilton Helmer's 7 Powers & Porter's 5 Forces

Strip away a company's story and you are left with a simpler question: what stops a competitor from taking its customers? For MS&AD, the honest answer in 2026 is that some of its defenses are formidable and permanent, while its single most important historical moat is being deliberately dismantled by its own regulator. Let's war-game it.

Begin with Hamilton Helmer's framework of durable competitive "powers." The clearest one MS&AD holds is scale economies. The merged entity will command an enormous domestic net premium base — on the order of several trillion yen — and in insurance, scale is not vanity; it is survival. A larger balance sheet spreads catastrophe risk across more policies, negotiates reinsurance more cheaply, and — critically — amortizes the crushing fixed cost of technology and regulatory compliance across a bigger revenue line. As climate change makes Japanese typhoons and floods more frequent and severe, and as IT and cyber spending balloons, the biggest players can absorb costs that would break a smaller carrier. The merger's entire logic is to convert MS&AD's latent scale into realized scale by killing the internal duplication that blunted it.

The second, subtler power is a cornered resource: the Toyota relationship and the vehicle-telematics data that flows from it. Access to real-world driving data from one of the world's largest automakers, embedded through the TIM and TIMS joint ventures, is something no rival can simply replicate — you cannot buy your way into Toyota's fleet. In a future of connected and increasingly automated vehicles, whoever prices driving risk most accurately wins the auto line, and MS&AD starts with a privileged data feed. The caveat, and it is real, is that Toyota is a partner, not a captive subsidiary; the alliance could be renegotiated, and every automaker now generates similar data. It is an edge, but a contingent one.

Then there is the power that is actively eroding: switching costs, historically manufactured out of cross-shareholdings. For a century, the reason a Sumitomo-group company didn't switch insurers was that switching meant betraying a shareholder and unwinding a relationship. That artificial switching cost is precisely what the drive to zero cross-shareholdings destroys. By 2030, corporate insurance in Japan is set to become something it has never been: a genuinely contestable, competitively bid market. MS&AD is losing a moat here, not gaining one — and any analysis that pretends otherwise is selling something.

Porter's five forces sharpen the same picture. The threat of new entrants is very low and will stay that way: FSA licensing, punishing capital requirements, and entrenched nationwide agency-distribution networks make the oligopoly nearly impregnable from the outside. But the bargaining power of corporate buyers is rising fast — post-scandal, corporate Japan has learned that it was overpaying, and it is now demanding transparent, competitively tendered pricing. And internal rivalry is set to intensify sharply: with the relationship glue dissolving, MS&AD must now go head-to-head on price and service against Tokio Marine, widely regarded as the industry's margin champion, and against Sompo. The threats of substitutes and supplier power are comparatively muted in this business.

Net it out and the competitive picture is genuinely two-sided. MS&AD is trading a soft, relationship-based moat that regulators are demolishing for a harder, efficiency-and-data-based moat it must now build under fire. Whether that is a good trade is the entire investment debate — and it is a debate about execution, not slogans. Which is exactly why the operating lessons of this saga are worth pausing on before we score the bull and bear cases.

X. The Playbook: Business & Investing Lessons

Great corporate stories are also cautionary tales, and MS&AD offers three lessons that travel far beyond Japanese insurance.

The first is the price of compromise. When MS&AD formed in 2010, keeping MSI and ADI as separate operating companies felt like the wise, humane, conflict-avoiding choice — nobody's client got upset, nobody's culture got steamrolled, nobody's executives lost their fiefdom. But partial integration is often the most expensive option on the menu. For seventeen years the group paid for two of everything — two IT stacks, two headquarters, two agency armies — to avoid a fight it would eventually have to have anyway. The half-merger captured the reputational optics of consolidation while forfeiting most of its economics. When you find yourself running two of something to preserve organizational peace, it is worth asking, honestly, what that peace is costing per year — and whether you are simply deferring an unavoidable reckoning at compounding expense.

The second lesson is darker and more structural: entrenched practices rarely die from within. Everyone inside the Japanese insurance industry knew the cross-shareholdings were unproductive. Everyone knew co-insurance had shaded into collusion. Governance consultants, foreign investors, and the Tokyo Stock Exchange had been pushing for reform for years, mostly in vain. What finally broke the system was not enlightenment but crisis — a scandal severe enough, and public enough, to make the status quo untenable. It took the humiliation of a price-fixing exposé and the blunt force of regulatory orders to dislodge capital that logic alone could never free. For investors, the practical implication is that some of the largest value-unlocks come not from companies that reform voluntarily, but from ones forced to — and that a regulatory shock, so often read as pure risk, can be the very thing that pries open a trapped balance sheet.

The third lesson is about governance as a re-rating tool. Markets do not just price a company's assets; they price their trust that management will deploy those assets well. For decades, MS&AD traded at a discount not because its insurance business was bad but because international investors had no confidence that the capital would ever be returned rather than hoarded in cross-held shares. The reforms now underway — clawback-laden incentive pay, an aggressive payout framework, and a planned move to IFRS accounting from fiscal 2026 that makes the numbers legible to global investors — are aimed squarely at that trust deficit.19 If they work, the re-rating comes not from earning more but from the market believing the earnings will reach shareholders. Governance, in this sense, is not a compliance chore. It is a multiple.

Those lessons are clean in hindsight. The harder task is applying them forward, into a future that is genuinely uncertain. So let's put the case on trial.

XI. Analysis: Bull vs. Bear Case & Key KPIs

Here is where a neutral platform has to resist the gravitational pull of the management deck. MS&AD's own materials tell a triumphant story of transformation. The job of an investor is to ask what would have to be true for that story to hold — and what would break it.

The bull case — the return-on-capital machine. In this telling, MS&AD is early in a multi-year mechanical re-rating. The forced liquidation of cross-shareholdings guarantees a steady stream of capital that management is funneling into buybacks and rising dividends, shrinking the share count and lifting per-share value almost regardless of how the underlying business performs in any given year. Layered on top, the April 2027 merger delivers a large, largely self-help cost reduction — synergies that don't depend on winning new customers, just on stopping the duplication. And underneath both, the genuine growth assets — the ASEAN-leading MSIG franchise and the Toyota telematics data — provide higher-margin expansion that home-market maturity cannot. In the bull case, a sleepy, asset-heavy value trap becomes a disciplined compounder, and the IFRS switch invites global capital to notice.

The bear case — the margin squeeze the bulls are cheering for. The bear points out an awkward irony buried in the bull thesis. The very reform being celebrated — driving cross-shareholdings to zero — is what strips away MS&AD's captive corporate clients and forces its most profitable commercial lines into open competitive bidding for the first time in a century. Those historically lucrative MSI margins were, in part, a product of the cozy system now being dismantled. As corporate Japan learns to shop around, underwriting profitability in the crown-jewel commercial book could compress meaningfully, and there is no guarantee the merger's cost savings outrun that revenue-side erosion. Add the climate overhang — intensifying domestic typhoons and floods that threaten to punch through catastrophe reinsurance limits — plus the execution risk of a giant Japanese IT and organizational merger with a grim industry track record, and the bear sees a company running down a one-time asset (the shares) to mask a slow decline in its core economic engine. The buybacks, in this reading, are not evidence of strength; they are the pleasant sound of the family silver being sold.

The activist's stress test sits right in the middle of that debate. A skeptical long/short investor would press on precisely the point management is quietest about: how much of the record profit and the shiny ROE is sustainable core earning power versus non-recurring equity-sale gains that vanish after 2030? They would scrutinize whether the merger synergies are real and bankable or a round number in a slide. They would ask whether management, having promised capital discipline, maintains it — or drifts back toward another expensive overseas trophy once the Amlin scars fade. And they would note that a company celebrating its escape from a collusion scandal is, structurally, being asked to compete for real for the first time in its existence — an untested muscle.

Which is why, for this company, the noise resolves down to a very small number of things actually worth watching. Three KPIs carry the case:

First, the combined ratio — the sum of claims and expenses as a percentage of premiums, the single cleanest measure of whether an insurer is actually making money on underwriting rather than on its investments. A combined ratio comfortably below 100% (management's ambition sits nearer the mid-90s) is the proof that MS&AD can still write profitable business in a competitive, post-cartel market. If that ratio drifts up as corporate clients start bidding out their coverage, the bear thesis is being confirmed in real time.

Second, the strategic-equity balance — the running total of cross-shareholdings still on the books against the zero-by-2030 target. This is the fuel gauge for the entire capital-return engine. Watching how fast it falls tells you how much buyback-and-dividend firepower remains, and — just as important — how close the company is to the moment when the training wheels come off and it has to generate returns from operations alone.

Third, group adjusted profit excluding equity-sale gains — the number that answers the only question that ultimately matters. Strip out the one-time windfalls from selling shares, and is the core insurance business actually growing its profit? This is the metric that separates a genuine compounder from a company merely liquidating its past in style, and it is the one to hold management to as IFRS reporting arrives and the sale gains eventually run dry.

XII. Outro

MS&AD began as two insurance houses stitched into the industrial families of Mitsui and Sumitomo, built to keep risk and loyalty circulating inside a closed keiretsu world. For more than a century it prospered on relationships rather than prices, held together by cross-shareholdings that doubled as a moat and, it turned out, as the machinery of an industry-wide price-fixing habit. It took a junior employee's spreadsheet, a regulator willing to name the rot, and a CEO willing to demolish his own company's architecture to break the spell.

What emerges on April 1, 2027 — a single unified carrier, a renamed parent, a balance sheet stripped of dead equity and pointed toward shareholders — is a genuinely different animal from the sleepy conglomerate of ancient zaibatsu roots and automotive alliances. Whether it becomes the high-return compounder its management promises, or simply a more efficient competitor in a market that has finally learned to fight on price, is not yet decided. That answer will be written in the combined ratio, in the pace of the equity unwind, and in whether the core business can stand on its own once the windfalls are spent. The scandal forced the door open. What MS&AD walks toward now is up to it.

References

-

Japan penalizes biggest property insurers for price fixing — The Japan Times, 2023-12-26 ↩

-

Tokyo Stock Exchange / JPX Group — Listed Company Directory (8725) ↩

-

Japan's MS&AD rebrands merged non-life business — The Insurer, 2025-09-30 ↩↩

-

MS&AD Integrated Report 2025 — MS&AD Insurance Group Holdings, Inc., 2025 ↩

-

MS&AD, Sompo, Tokio Marine shrug off price-fixing scandal as shares rebound — S&P Global Market Intelligence, 2023-10 ↩

-

MS&AD posts annual profit growth, plans merger and buyback — Life Insurance International, 2025 ↩↩↩↩

-

Mitsui Sumitomo Insurance Completes Acquisition of 'MS Amlin' — Insurance Journal, 2016-02-02 ↩

-

Japan Insurers Sink on Concerns Over Suspected Price Fixing — Insurance Journal, 2023-08-02 ↩

-

Japan penalizes biggest property insurers for price fixing — The Japan Times, 2023-12-26 ↩

-

The JFTC Issued Cease and Desist Orders and Surcharge Payment Orders against Non-Life Insurance Companies — Japan Fair Trade Commission, 2024-10-31 ↩

-

MS&AD, Sompo, Tokio Marine shrug off price-fixing scandal as shares rebound — S&P Global Market Intelligence, 2023-10 ↩

-

Japan's Big Non-Life Insurers Plan to Sell Cross Shareholdings — Insurance Journal, 2025-05-20 ↩

-

Shareholder Return Policy and Dividend Information — MS&AD Insurance Group Holdings, Inc. ↩↩

-

MS&AD — Interview with CEO Shinichiro Funabiki — Sollers Consulting ↩↩

-

Japan's MS&AD to shed cross-held shares in 2 years, says next CEO — Nikkei Asia ↩

-

MS&AD Insurance Group Announces Merger of 2 Non-Life Subsidiaries — Insurance Journal, 2025-03-28 ↩↩

-

MS&AD boosts profit, dividends and shifts to IFRS reporting — TipRanks, 2025 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube