Sompo Holdings: The Insurance Giant Unwinding Its Past

I. Introduction & Episode Roadmap

Picture the scene inside Sompo Japan's headquarters in the Shinjuku district of Tokyo in the summer of 2023. For years, the group had marketed itself as a "theme park for security, health and wellbeing" — a slightly saccharine slogan for a company whose real business was collecting premiums and paying claims. Then, on July 28, 2023, 日本経済新聞 Nikkei reported that Sompo Japan had failed to report systemic fraud at its largest used-car repair partner.[^9] Within weeks, the slogan curdled into a punchline. Regulators descended. Executives bowed in televised apologies. And by early 2024, the man who had run the group for nearly a decade was gone.

That collision — between a proud, insular corporate culture and a regulator that had finally lost patience — is the dramatic centre of this story. But to understand why it mattered, and why the company that emerged on the other side looks so different, you have to understand five distinct threads that had been developing in parallel.

First, the oligopolistic roots: how three giant insurers came to control the vast majority of Japan's non-life market, and why that comfortable structure planted the seeds of its own crisis. Second, the audacious $6.3 billion acquisition of Bermuda-based Endurance Specialty in 2016 — a deal critics called wildly overpriced, and which turned out to be the earnings engine that later saved the group. Third, the pivot into "Wellbeing," in which Sompo bet that an aging Japan and a partnership with Palantir could turn nursing homes into a data business. Fourth, the twin governance scandals of 2023–2024. And fifth, the modern reformation: the unwinding of decades-old cross-shareholdings, record capital returns, and a historic organizational split executed on April 1, 2025.

Along the way we will keep asking the two questions that matter to any long-term owner of this business. Why might Sompo win from here? And what could break the case? The company's own answer is confident. Our job is to test it.

II. The Foundation: Yasuda Fire & The Oligopoly of Japanese P&C

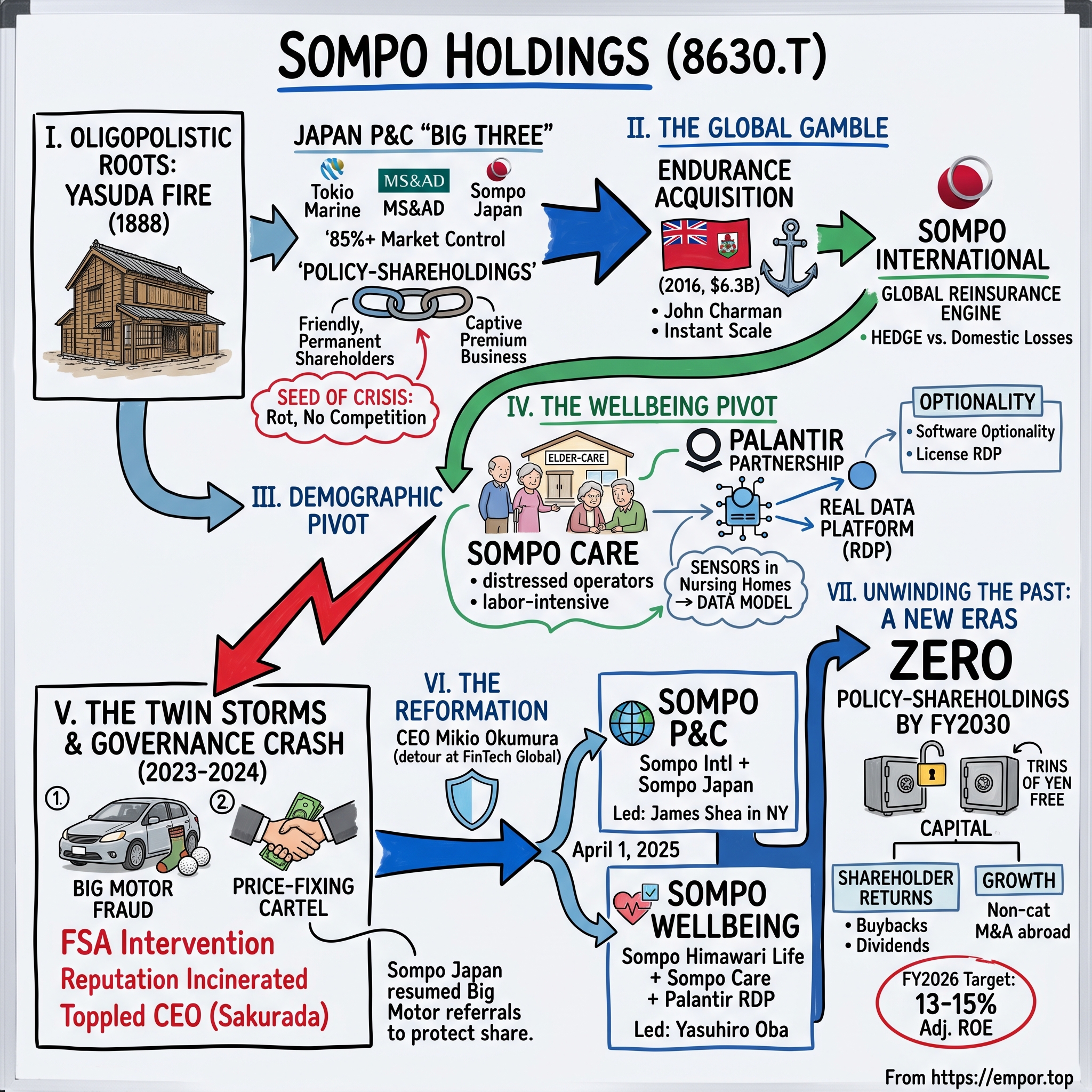

The oldest thread of Sompo's DNA runs back to 1888, when Tokyo Fire Insurance opened its doors — Japan's first fire-insurance company, born in an era when the country was racing to industrialize under the Meiji reforms and its dense wooden cities burned with terrifying regularity. Fire insurance was not a luxury product in Meiji Japan; it was infrastructure for a nation trying to build a modern economy out of flammable materials.

The more important ancestor, though, was 安田火災海上保険 Yasuda Fire & Marine, part of the Yasuda 財閥 zaibatsu — one of the great family financial conglomerates that dominated pre-war Japanese capitalism. When the American occupation broke up the zaibatsu after 1945, the Yasuda insurance business survived and, over the following decades, grew by absorbing rivals. The lineage that eventually became 損害保険ジャパン株式会社 Sompo Japan Insurance Inc. (Sompo Japan) was stitched together from Yasuda Fire & Marine, Nissan Fire & Marine, and others — a slow-motion consolidation typical of a maturing industry with too many players chasing the same premiums.

By the twenty-first century, that consolidation had produced one of the most concentrated insurance markets on earth. Japan's non-life sector settled into a "Big Three": 東京海上ホールディングス株式会社 Tokio Marine Holdings, Inc., MS&ADインシュアランスグループホールディングス株式会社 MS&AD Insurance Group Holdings, Inc., and Sompo. Between them, these three groups controlled well over 85% of the domestic property-and-casualty market. In most industries, that degree of concentration would attract fierce antitrust scrutiny. In Japanese non-life insurance, it was simply the way things were.

And here we reach the mechanism that quietly shaped everything: 政策保有株式 policy-shareholdings, or cross-shareholdings. For generations, Japanese insurers held large equity stakes in their corporate customers — automakers, trading houses, manufacturers, utilities. In return, those corporations steered their fat, high-margin commercial insurance contracts to the insurer that held their shares. It was a mutual embrace. The insurer got a captive book of premium business; the client got a friendly, permanent shareholder who would never side with an activist or vote against management. Money and loyalty flowed in a closed loop, insulated from the vulgar business of competing on price or product.

For decades, this was extraordinarily profitable. But profitability built on relationships rather than merit tends to hide rot. The domestic market underneath it was going nowhere. Japan's population had begun shrinking; its drivers were aging; its auto fleet — the beating heart of P&C premiums — had stopped growing. The core underwriting business was becoming a mature, zero-growth engine, its returns propped up less by skill than by an unspoken agreement among giants not to rock the boat.

A company can coast on that arrangement for a long time. But coasting is not a strategy, and by the mid-2010s Sompo's leadership had concluded that the domestic engine alone could not carry the group's ambitions. The question was where to find growth — and the answer would take them 11,000 kilometres away, to a rock in the Atlantic.

III. The Endurance Gamble: John Charman and the $6.3B Global Reinsurance Bet

The man who decided Sompo needed to leave home was 櫻田謙吾 Kengo Sakurada, the group's chief executive and, for the better part of a decade, the most powerful figure in Japanese non-life insurance. Sakurada was not a caretaker. He was an ambitious, globally-minded executive who chaired the influential business lobby 経済同友会 Keizai Doyukai and spoke openly about the existential threat that demographic decline posed to any purely domestic Japanese business. His diagnosis was blunt: a shrinking country cannot sustain a growing insurer, so the growth has to come from somewhere else.

On October 5, 2016, Sakurada delivered his answer. Sompo announced it would acquire Bermuda-based Endurance Specialty Holdings, a specialty insurer and reinsurer, for $93.00 per share in cash — roughly ¥637.5 billion, or about $6.3 billion in aggregate.5 It was, at the time, one of the largest overseas acquisitions ever made by a Japanese insurer.

The price tag raised eyebrows immediately, and the numbers explain why. The offer represented a premium of approximately 40.3% over Endurance's closing price on October 3, and about 41.6% over its three-month average — and valued the company at roughly 1.36 times its book value.6 For a reinsurer, paying more than 1.3x book is a statement. Reinsurance is a commodity-ish, cyclical business where book value is a meaningful anchor, and plenty of peers traded around or below it. Critics argued Sompo had done what cash-rich Japanese acquirers so often did overseas: overpaid for a trophy to plant a flag, then quietly watched value leak away.

So was it overpaid? On the raw multiple, the sceptics had a point. But the thesis was never really about buying a book of contracts at a fair price. It was about buying two things Sompo could not build organically: instant global underwriting scale, and a management team that actually knew how to run a specialty insurer. Chief among them was Endurance's chairman and chief executive, John Charman — a legendary, combative figure in the London and Bermuda insurance markets, the kind of underwriter whose reputation moved capital. As part of the deal, Charman and his senior team agreed to stay on and keep running the business for at least five years.5

This is where Sompo did something genuinely unusual, and where the story diverges from the graveyard of failed Japanese overseas deals. The classic pattern — the one that has destroyed billions in shareholder value across corporate Japan — is for the Tokyo parent to parachute in domestic lifers to "supervise" the foreign subsidiary, smothering exactly the local expertise it paid a premium to acquire. Sompo declined to run that playbook. It rebranded the operation Sompo International, kept Charman's team empowered and incentivized, and largely let Bermuda be Bermuda. The parent supplied capital and a balance sheet; the subsidiary supplied underwriting judgment.

The proof arrived in the numbers, and in the crises they cushioned. In the years that followed, the Overseas Insurance and Reinsurance business grew into the group's single largest profit centre. By fiscal 2024, the overseas segment delivered adjusted profit of roughly $1.38 billion, up more than $200 million year over year on top-line growth, lower adverse prior-year development, and higher investment income.8 More strategically, that overseas engine repeatedly offset brutal years in the domestic book — the typhoons, floods, and natural-catastrophe losses that periodically savage Japanese P&C earnings. The expensive Bermuda bet became the hedge that kept group earnings standing when the home market buckled.

Whether Sompo overpaid in 2016 is, in hindsight, almost the wrong question. The right one is whether it could have generated a decade of geographic diversification and half its profit base any other way. It almost certainly could not. But an insurer cannot diversify its way out of every problem by buying catastrophe risk abroad — and Sakurada knew it. The next bet would be aimed not at the Atlantic hurricane belt, but at the demographic slow-motion disaster unfolding at home.

IV. The Wellbeing Pivot: Aging Japan, Sompo Care, and the Palantir Partnership

Japan is the oldest society the world has ever seen. More than a quarter of its population is over 65, its birth rate has been below replacement for decades, and its rural towns are quietly emptying. For most industries this is a catastrophe. Sakurada looked at it and saw a market — enormous, non-cyclical, and, crucially, uncorrelated with the typhoons and hurricanes that whipsawed the insurance book. If catastrophe risk was volatile and lumpy, caring for the elderly was the opposite: a vast, steady, structurally growing tide of human need.

So Sompo went shopping for nursing homes. Between roughly 2015 and 2018, it rolled up a series of distressed and undervalued elder-care operators — most notably the care businesses of ワタミ Watami (Watami no Kaigo) and Message — and welded them into SOMPOケア株式会社 Sompo Care Inc. (Sompo Care).11 The result was one of Japan's largest private nursing-care platforms, employing tens of thousands of caregivers across hundreds of facilities and home-care operations. Overnight, an insurance company had become one of the country's biggest employers of frontline care workers.

Here, though, honesty about proportionality matters, and Sompo's own disclosures make the point. As a business line, nursing care is not where the money is. It is a low-margin, labour-intensive operation whose pricing is effectively capped by government long-term-care reimbursement rates — you cannot simply raise prices when the state sets the tariff. The segment has typically contributed only a modest slice of group net income, well under a tenth of the whole, despite its outsized share of headcount. Judged as a profit centre in isolation, Sompo Care is a rounding error attached to a giant workforce. Anyone evaluating this company has to resist the very human temptation to confuse 28,000 employees with 28,000 employees' worth of profit.

So why do it? The answer is that Sompo never intended nursing homes to be the product. It intended them to be the sensor network. And to turn that network into something valuable, it turned to Silicon Valley's most polarizing company.

In 2019, Sompo struck its partnership with Palantir Technologies — the data-integration firm co-founded by Peter Thiel, whose Foundry software specializes in fusing messy, fragmented real-world data into a single operational picture. On November 18, 2019, the two companies announced a 50-50 joint venture; the entity, Palantir Technologies Japan K.K., was established that December, with Sompo agreeing to invest roughly ¥54 billion — about $500 million — directly into Palantir itself.7 For Palantir, still a private company at the time, it was a marquee validation in Asia. For Sompo, it was the technological key to the entire Wellbeing thesis.

The concept they built together is the リアルデータプラットフォーム Real Data Platform (RDP). Strip away the jargon and the idea is intuitive. Sompo's nursing facilities generate a firehose of real-world data — sensor readings, vital signs, care records, staff movements, incident logs. Historically that data sat in silos, useless. Foundry's job is to stitch it into one live model of what is actually happening across the facilities, so that software can help decide who needs attention, how to route a caregiver's shift, when a resident is trending toward a fall or a health crisis. In an industry crippled by chronic labour shortages, squeezing more effective care out of each scarce worker is not a luxury; it is survival.

That is the operational case, and it is real. The more speculative case — the one that excites the equity story — is the software optionality. Japan's nursing-care market is spectacularly fragmented, with tens of thousands of small operators, most of them running on paper and goodwill. If Sompo can package the RDP as workflow software and license it to those operators, it converts a capped, low-margin services business into a high-margin, recurring-revenue software platform sitting on top of proprietary data no competitor can easily replicate. The relationship has continued to deepen — in August 2025, Sompo and Palantir announced a multi-year expansion of their agreement.10

But optionality is not a result, and a neutral observer has to hold the line here. As of today, the RDP's value to third parties remains largely a promise. Selling enterprise software to fifty thousand tiny, tech-averse care operators is a genuinely hard commercial motion, and Sompo has disclosed little in the way of standalone RDP licensing revenue to prove the platform play at scale. The nursing homes are a real beachhead; whether the software business built on top of them ever becomes material is, for now, an open question rather than an achievement. Investors should track it as a bet, not book it as a win.

That tension — between a company that could tell a beautiful strategic story and a company that could execute it cleanly — was about to be tested in the harshest possible way, and not in nursing homes or Bermuda, but in the mundane world of car repairs.

V. The Twin Storms: The Big Motor Insurance Fraud & The Price-Fixing Scandals

Every cosy relationship looks fine until you see what it was hiding. For years, Sompo Japan enjoyed a warm, mutually profitable partnership with ビッグモーター Big Motor, Japan's largest used-car dealer and vehicle-repair chain. Big Motor sent Sompo Japan a torrent of auto-insurance customers; Sompo Japan sent Big Motor a steady flow of repair referrals and, in a telling detail, seconded its own employees into Big Motor's operations to help manage the relationship. Sompo Japan later disclosed that from May 2015 to January 2023 it had a total of eight employees on secondment inside Big Motor's auto-body and paint divisions.3 It was the physical embodiment of the relationship-driven model: not a supplier at arm's length, but a partner with staff inside the building.

Then the details came out, and they were grotesque. Big Motor employees, it emerged, had been systematically and deliberately damaging customers' cars in order to inflate repair bills and the insurance claims attached to them. Investigators and press reports described technicians slashing tyres, scratching paintwork, and — in the detail that seared the scandal into public memory — whacking car bodies with socks stuffed with golf balls to fake hail or impact damage.[^9] This was not a rogue mechanic. It was an organized scheme to defraud insurers and customers, running through the country's biggest repair chain.

Sompo Japan's role turned outrage into a governance crisis. By 2022 the insurer had internal indications that something was badly wrong with Big Motor's claims. And yet — this is the part that damns the culture — after briefly pausing, Sompo Japan chose to resume sending customer referrals to Big Motor.[^9] The commercial logic was as cold as it was corrosive: if Sompo cut ties, Big Motor might retaliate by steering its lucrative auto-insurance business to Tokio Marine or MS&AD. In the zero-sum arithmetic of a three-firm oligopoly, protecting share from your rivals outranked protecting your own customers from fraud. The relationship model had inverted the company's priorities completely.

As if one scandal were not enough, a second broke almost simultaneously — and this one implicated the entire industry. The FSA uncovered widespread collusion among Japan's major non-life insurers, who had been coordinating and effectively fixing the premiums charged to large corporate clients on co-insured policies. Household-name buyers — transport groups, utilities, industrial conglomerates — had been quoted pre-arranged prices by insurers who were supposed to be competing for their business.9 The cross-shareholding culture had a natural endpoint: if everyone owns everyone and nobody really competes, why not just agree on the price? The cartel was the oligopoly's logic taken to its conclusion.

The regulatory hammer fell on January 26, 2024. The FSA issued business-improvement orders to both Sompo Japan and, pointedly, to the holding company Sompo Holdings itself — a signal that this was not a subsidiary's isolated lapse but a failure of group governance.3 The regulator's language was withering, describing a corporate culture that had prioritized business volume and market position over customer protection and legal compliance. The order demanded that the companies clarify management responsibility, overhaul their governance and administration systems, and report back on their progress.3

Management responsibility, in Japanese corporate ritual, means resignations. And so the era ended. Kengo Sakurada — the architect of the Endurance deal and the Wellbeing pivot, the globally-minded reformer who had spent years lecturing corporate Japan about the need to change — stepped down from the group's top post, his legacy fused permanently to a scandal about golf balls in socks. Sompo Japan's president, 白川儀一 Giichi Shirakawa, resigned as well. The strategist who had dragged Sompo onto the global stage was undone by the oldest, most parochial failing in the book: a domestic relationship the company was too comfortable, and too frightened of its rivals, to sever.

Out of that wreckage, Sompo had to find someone who could credibly promise it would never happen again.

VI. The Reformation: Mikio Okumura's Playbook & The 2025 Bifurcation

The man handed that job was 奥村幹夫 Mikio Okumura, who became Group CEO in April 2024, stepping into a role defined by disgrace and a regulator watching his every move. What made Okumura the right choice was less what he had done than where he had not been.

His career had an unusual kink in it. Okumura joined Yasuda Fire & Marine in 1989, on the conventional lifetime-employment track. But in 2006 he did something almost heretical for a Japanese salaryman on the rise: he left, decamping to the world of investment banking at FinTech Global, before returning to the Sompo fold in 2009. That detour matters. It gave him a dose of outside commercial discipline and a view of the company from the perspective of markets and capital, rather than from inside the insurance guild. Executives who have only ever known one employer tend to absorb its blind spots; Okumura had at least stepped outside the building.

Just as important, his hands were clean. Okumura had spent formative years running Sompo Care, driving digitization and efficiency in the nursing business — a world away from the auto-insurance and corporate-underwriting operations where the scandals festered. When he took the top job, he could stand in front of regulators, the press, and the public and credibly say that he had not been in the room where it happened. In a moment when Sompo's most valuable and most depleted asset was trust, a leader untainted by the P&C scandals was not a nice-to-have. It was the whole point.

Okumura's stated reform agenda leaned on the language of accountability and incentive alignment. Executive compensation was tied more explicitly to long-term return metrics, using stock-based structures — including a J-ESOP (Japan-style employee stock ownership plan) trust — intended to bind management's payout to sustained ROE rather than to the market-share instincts that had gotten the company into trouble.12 Whether incentive redesign can actually rewire a decades-old culture is, of course, exactly the sort of claim a sceptic should file under "prove it" — governance charts are easy to redraw, and cartels formed under prior incentive schemes too. The test is behaviour over years, not the org chart.

The most dramatic structural move came on April 1, 2025, when Okumura executed a sweeping reorganization of the entire group. Announced in February 2025, the plan collapsed Sompo's tangle of businesses into two streamlined global segments, with the explicit aim of pushing decision-making down and out of the Tokyo centre that had presided over the scandals.4

The first segment, Sompo P&C, integrated Sompo International's global insurance and reinsurance operations with Sompo Japan's commercial and consumer property-and-casualty business — uniting the Bermuda underwriting engine and the domestic book under one roof. Tellingly, the segment was placed under James Shea, the head of the international business, operating from New York rather than Tokyo.4 Putting a global specialty-insurance executive in charge of the combined P&C franchise, and seating him outside Japan, was itself a statement about where the company thought underwriting discipline actually lived.

The second segment, Sompo Wellbeing, gathered the domestic life-insurance business SOMPOひまわり生命保険株式会社 Sompo Himawari Life Insurance, the Sompo Care nursing operation, and the Palantir-powered digital business into a single unit aimed squarely at the challenges of an aging society — health, retirement security, and elder care. It was placed under 大場康弘 Yasuhiro Oba, previously CEO of Sompo Himawari Life.4

The logic of the split is coherent: separate the volatile, globally-scaled risk business from the steady, domestically-rooted human-services business, give each its own leadership and capital logic, and stop pretending one Tokyo hierarchy can optimally run both a Bermuda reinsurer and a chain of Japanese nursing homes. Whether decentralization genuinely fixes the accountability failures the FSA identified — or simply relocates them — is the open question the next few years will answer. Structure can enable a culture change; it cannot substitute for one.

Reorganizing the business, though, was only half the reformation. The other half was aimed at the balance sheet — and specifically at dismantling the very mechanism that had made the oligopoly possible in the first place.

VII. Unwinding the Past: The Death of Cross-Shareholdings & The Shareholder Return Bonanza

If you want to understand the deepest change at Sompo, don't look at the org chart. Look at what the FSA demanded next, because it struck at the financial machinery underneath the entire scandal. Having exposed the price-fixing cartel, the regulator turned to its root cause and pressed Japan's non-life insurers to eliminate the corporate cross-shareholdings that had greased decades of anti-competitive coziness. The logic was clean: as long as insurers were permanent shareholders in their corporate customers, the incentive to collude rather than compete would never fully die. Kill the shareholdings, and you kill the mechanism.

Sompo's response was to commit to something that would have been unthinkable a decade earlier: reducing its trillions of yen in strategic 政策保有株式 policy-shareholdings to a zero balance by the end of fiscal 2030.2 For a company whose commercial model had been built on these holdings, this was not a tweak. It was the deliberate demolition of the old way of doing business — a promise to sever the financial ligaments connecting it to corporate Japan.

And here is where a regulatory punishment quietly turned into a shareholder windfall. Those cross-holdings represented enormous amounts of capital that had been sitting dormant for decades, earning meagre returns while serving a relationship purpose rather than an economic one. Selling them releases that capital. The question of what to do with the proceeds is the central capital-allocation story of Sompo today, and management has been unusually explicit about the answer.

The first destination is shareholder returns, at a scale the old Sompo never contemplated. Under the FY2024–FY2026 Mid-Term Management Plan, the company has leaned hard into buybacks and dividends — including a ¥260 billion share buyback tied to fiscal 2024 results, alongside a stated commitment to a 50% dividend payout ratio.8 The mechanics are straightforward and powerful: liquidate low-returning legacy equity stakes, and recycle the cash into shrinking the share count and lifting the dividend. For years, the bull case on Japanese insurers was essentially a bet that they would eventually be forced to give this hidden capital back. At Sompo, that forcing function finally arrived, courtesy of a scandal.

The second destination is growth. Management has signalled that a portion of the proceeds will fund M&A — specifically, non-catastrophe P&C acquisitions abroad, intended to diversify the risk book away from the volatile natural-catastrophe exposures that dominate the current earnings mix.2 This is the more debatable use of the money. A company that has just been rewarded by the market for promising capital discipline, and that has a decidedly mixed cultural history, redeploying scandal-freed capital into acquisitions is exactly the kind of move a sharp-eyed investor should watch closely. The Endurance deal proved Sompo can do a transformative acquisition well; it does not prove every future deal will clear that bar.

The financial ambition wrapping all of this is a target of roughly 13–15% adjusted consolidated ROE by fiscal 2026, on a path toward ¥500 billion in adjusted consolidated profit by fiscal 2030.1 The early evidence has been encouraging rather than merely aspirational: for fiscal 2025 (the year ended March 2026), Sompo reported adjusted profit of about ¥535 billion and an adjusted consolidated ROE of roughly 13.4%, having reduced strategic shareholdings by around ¥292 billion in that year alone.1 Hitting the low end of its ROE target a year early, and already booking large annual chunks of shareholding sell-down, is precisely the kind of "did they actually do it" evidence that separates a real transformation from a press release. The demolition, so far, is on schedule.

VIII. Playbook: Business & Investing Lessons

Step back from the specifics, and Sompo's arc offers a set of lessons that travel well beyond Japanese insurance.

The first is the oligopoly curse. Concentrated, comfortable markets are wonderful for margins and terrible for character. When three firms control a market and hold each other's customers as shareholders, the competitive pressure that normally keeps a company honest simply evaporates. Share gets won through relationships and equity stakes rather than better products or sharper pricing, and over time the organization forgets who it is actually supposed to serve. The Big Motor and price-fixing scandals were not random accidents; they were the predictable end-state of a system where customer advocacy had quietly become optional. For investors, the lesson is to be wary of businesses whose profitability rests on cozy structures rather than genuine competitive merit — the returns look stable right up until they don't.

The second is the smart-M&A-integration model, and here Sompo genuinely earned its stripes. The reason the Endurance deal worked where so many Japanese overseas acquisitions failed was a discipline of restraint: buy the talent, then leave it alone. Sompo resisted the deep-seated corporate instinct to control a foreign specialty business from Tokyo, and instead let Bermuda and London operate with real autonomy under leaders who understood those markets. The transferable lesson is that when you pay a premium for human capital and local expertise, the worst thing you can do is smother it with head-office oversight. Cultural humility, not just capital, is what makes cross-border deals pay.

The third is the danger of confusing scale with value. Sompo Care employs tens of thousands of people and touches a vast social need, yet contributes only a sliver of group profit. Headcount and social importance are not the same as economic contribution. The subtler lesson embedded in the Wellbeing pivot is where the real leverage is supposed to come from: not the physical care operation itself, but the software and data layer built on top of it. Physical operations can be a beachhead; the model only becomes powerful if operational data can be turned into a high-margin product. That remains an if, not a fact — which is itself the lesson.

The fourth is the shareholder catalyst, perhaps the most important for anyone investing in entrenched, cash-rich, insider-run companies. Sometimes the thing that finally unlocks decades of trapped value is not a brilliant strategy or a visionary CEO. It is a crisis. Regulatory pressure and public disgrace did what years of polite investor letters never could: they forced Sompo to dismantle its cross-shareholdings and hand capital back to owners. Governance failure, painful as it is, can be the ultimate value-unlock — a reminder that in corporate Japan especially, the catalyst is often external and involuntary.

Those lessons frame the investment question. The next section confronts it directly.

IX. Analysis: Bull vs. Bear, Helmer's 7 Powers & Porter's 5 Forces

To assess whether Sompo can win from here, it helps to run its businesses through two well-worn analytical frameworks — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — and then to state the bull and bear cases plainly.

Helmer's 7 Powers. Three of Helmer's powers are worth examining, because they map onto Sompo's three distinct engines.

The clearest is scale economies, concentrated in Sompo P&C. Global reinsurance is a business where size is a genuine advantage: larger, more diversified books absorb catastrophe volatility better, spread fixed costs of catastrophe modelling and analytics across more premium, and command better access to retrocession and capital. Sompo International operates at a scale that a domestic-only insurer could never reach, and that scale is a real, if not unassailable, source of edge. The caveat is that Sompo is not the largest player globally — it competes with far bigger reinsurers — so its scale advantage is relative, not dominant.

The second is switching costs, most relevant in Sompo Wellbeing. Once a family has moved an elderly relative into a Sompo Care facility, the emotional, logistical, and health-continuity costs of moving them again are steep. Elderly residents do not switch care homes casually. That stickiness is real — but it is worth being honest that it is a modest, low-margin form of lock-in, not a pricing-power engine, because the state largely sets the price.

The third and most speculative is cornered resource, which is the crux of the Palantir bet. In principle, Sompo's exclusive access to Foundry-powered tooling in this domain, combined with a proprietary trove of Japanese senior-care operational data, could constitute a resource competitors cannot replicate. If — and it is a large if — that data-and-software combination becomes a licensable platform, it would be a durable, high-margin advantage. Today it is better described as a potential cornered resource than a proven one.

Porter's Five Forces (domestic P&C). The competitive structure is shifting under the industry's feet. Rivalry among the Big Three remains intense, but its character is changing — from collusive, relationship-driven coexistence toward, at least in theory, genuine underwriting-discipline competition, forced by the death of cross-shareholdings. Threat of new entrants is low, protected by enormous capital-reserve requirements and tight FSA regulation; this is not a market a startup disrupts. Bargaining power of buyers is bifurcated: retail auto and homeowners' customers remain price-takers with little leverage, but large corporate buyers — newly aware they were being quoted rigged prices — have gained both leverage and motivation to shop around. Supplier power and substitutes are relatively muted in insurance, though one could argue that self-insurance and alternative capital (catastrophe bonds, insurance-linked securities) act as a slow-building substitute pressure on the reinsurance side.

The Bull Case — why Sompo wins from here. The bull rests on three concrete mechanisms. First, the unwinding of cross-shareholdings creates a multi-year, highly visible tailwind of buybacks and rising dividends, with an external regulator ensuring management follows through — and the FY2025 results suggest the sell-down and ROE improvement are genuinely materializing, not just promised.1 Second, Sompo P&C under James Shea concentrates real underwriting talent, offering the prospect of a lower, more disciplined consolidated combined ratio. Third, the Palantir RDP offers embedded optionality: if it ever scales as licensed software, it re-rates the low-margin Wellbeing business entirely. Crucially, only the first of these is close to proven; the other two are credible but contingent.

The Bear Case — what could break it. The bear case is equally concrete. Escalating climate change means more frequent and severe catastrophes — typhoons in Japan, hurricanes and wildfires abroad — which strike directly at the P&C earnings engine that now carries the group; a bad catastrophe year can erase the benefit of a good underwriting year. Japan's chronic labour shortage bites hardest exactly where Sompo has placed a large bet: nursing care margins can be crushed by rising wages the company cannot pass through to state-capped prices. And the RDP software thesis may simply never find adoption among tens of thousands of fragmented, tech-resistant care operators, leaving the Wellbeing segment as a worthy but structurally low-return business. Layered over all of it is the hardest risk to underwrite: whether a company that just endured twin governance scandals has truly changed, or merely reorganized.

The Risk Radar. Three risks deserve continuous monitoring. Catastrophe risk is the dominant one — heavy, correlated exposure to global climate volatility and domestic natural disasters. Macro and inflation risk is subtler but real: if medical, repair, and wage inflation outrun the company's ability to raise premiums, underwriting margins erode from below. And execution risk looms over the entire 2025 restructuring — integrating legacy systems and cultures under a newly decentralized model is precisely the kind of transformation that looks clean on a slide and messy in practice.

The KPIs that actually matter. Amid the noise, three metrics tell most of the story. First, adjusted consolidated ROE, the single clearest gauge of whether the capital-efficiency transformation is real — with the FY2026 target of 13–15% as the yardstick, already brushed in FY2025. Second, the combined ratio in the P&C segments, the truest measure of underwriting discipline, where anything sustainably below 95% signals the business is being run on merit rather than relationships. Third, the pace of policy-shareholding divestment toward the zero-by-FY2030 goal, which is both the engine of capital returns and the litmus test of whether the old culture is genuinely dead. Beneath these, the emergence of any real RDP software revenue and the trajectory of Care margins are the leading indicators of whether the Wellbeing story becomes more than a hedge.

X. Epilogue & Future Outlook

So where does this leave Sompo, and the investor trying to make sense of it? Mikio Okumura has staked the company's future on a set of numbers he cannot fully control — a march toward a ¥6 trillion market capitalization and ¥500 billion in adjusted profit by 2030, built on the twin pillars of a globally disciplined risk business and a data-enabled Wellbeing franchise.12 The early evidence is that the financial machinery is working: capital is being returned, shareholdings are being sold, and returns are climbing toward target ahead of schedule. That is not nothing. In a corporate landscape where promises routinely outrun delivery, Sompo has, so far, delivered against the parts of its plan that can be measured.

What cannot yet be measured is the harder thing. The scandals of 2023 and 2024 were not really about used cars or corporate premiums; they were about a culture that had learned to value position over customers and quiet coordination over honest competition. Reorganizing into two segments, redrawing incentive plans, and installing untainted leaders are the visible signs of reform. Whether they add up to a genuinely changed company, or merely a better-organized version of the old one, is the question no annual report can answer and only time can.

Viewed from a distance, Sompo's journey is a compressed portrait of modern Japan's corporate reckoning — the slow, often involuntary abandonment of cross-shareholdings, insular boards, and relationship capitalism in favour of capital efficiency, global competitiveness, and, increasingly, technology. The company that once insured Meiji-era warehouses against fire is now trying to reinvent itself as a decentralized, data-driven, shareholder-friendly global group. It has the balance sheet, the overseas engine, and the external pressure to pull it off. Whether it also has the character is the story still being written.

References

-

Highlights of FY2025 Results — Sompo Holdings, 2026-05-20 ↩↩↩↩

-

Sompo Japan to Cut Cross-Shareholdings to Zero by End-FY2030 — Bloomberg Law ↩↩↩

-

Administrative Action against Sompo Holdings and Sompo Japan (Business Improvement Order) — Sompo Holdings, 2024-01-26 ↩↩↩

-

Sompo Holdings establishes global Property and Casualty (re)insurance, and Wellbeing business segments — Sompo International / Sompo Holdings, 2025-02-14 ↩↩↩

-

Japan's SOMPO to Acquire Endurance for $6.3 Billion — Insurance Journal, 2016-10-05 ↩↩

-

Endurance Specialty Holdings Ltd — Form 8-K (transaction terms) — U.S. Securities and Exchange Commission, 2016 ↩

-

Palantir calls in $500m from Sompo Holdings — Global Venturing, 2019 ↩

-

Highlights of FY2024 Results — Sompo Holdings, 2025-05-20 ↩↩

-

Japan's big insurers commit to complete exit of cross-shareholdings — Reuters, 2024-02-29 ↩

-

Palantir and SOMPO Expand Partnership in Multi-Year Agreement — Business Wire, 2025-08-12 ↩

-

Sompo Care Official Site & Senior Living Overview — Sompo Care Inc. ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube