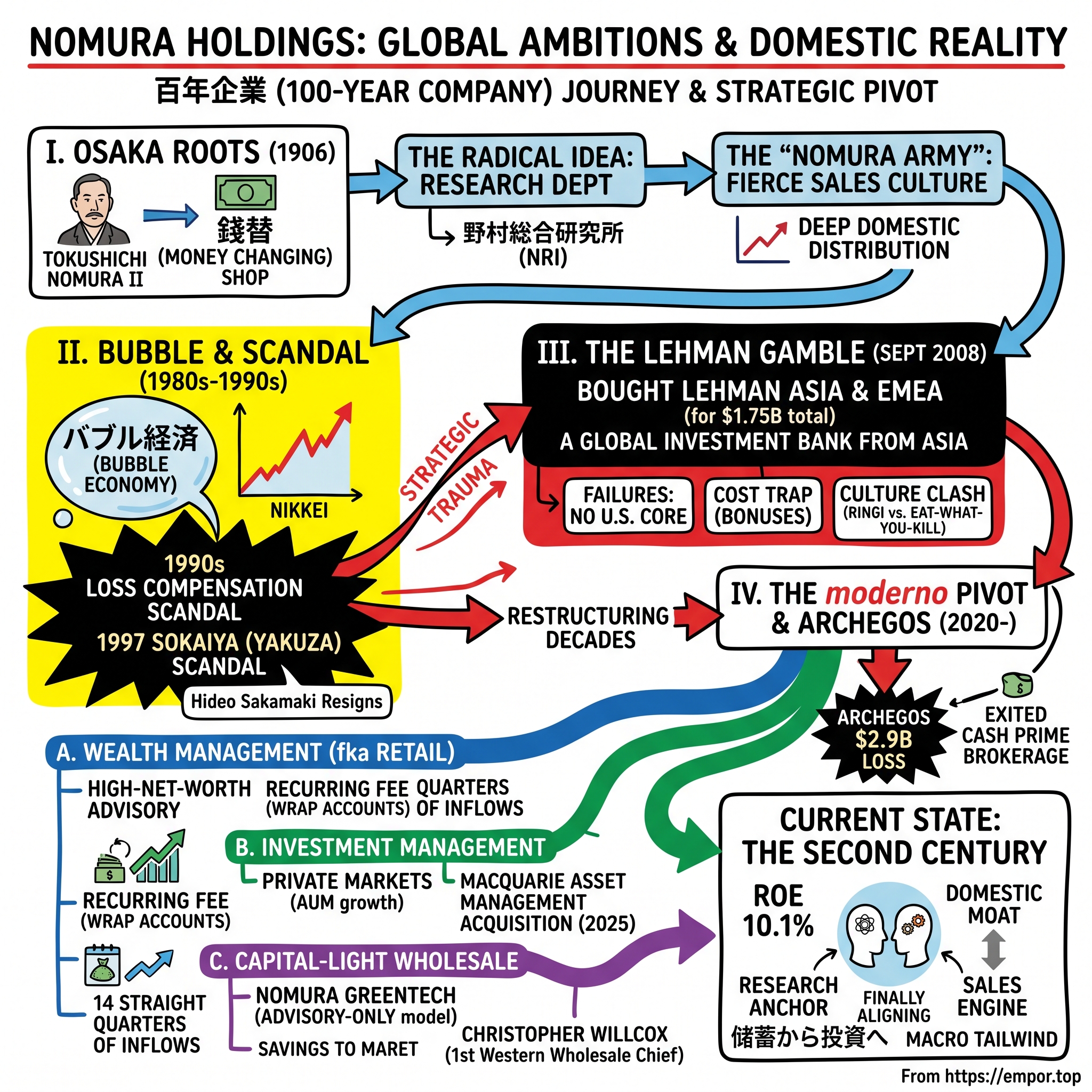

Nomura Holdings: The Global Ambitions and Domestic Reality of Japan's Financial Giant

I. Introduction & Episode Roadmap

In the final days of March 2021, a small circle of executives inside 野村ホールディングス株式会社 Nomura Holdings, Inc. (8604.T) sat staring at a hole in the balance sheet that had opened, almost literally, overnight. The source was not a rogue trader in Tokyo. It was not a bad bet on Japanese government bonds, nor a bad loan to a Japanese conglomerate, nor any of the domestic risks a century-old securities house is actually built to survive. It was a single family office, run out of a Midtown Manhattan skyscraper by a man most of Nomura's own board had never heard of: Bill Hwang, and his fund, Archegos Capital Management.

When the dust settled, Nomura disclosed that its exposure to that one client would cost it roughly $2.9 billion — a $2.3 billion charge booked in the quarter, followed by a further write-down of around $570 million.1 It was enough to push Nomura to its worst quarterly loss since the depths of the 2009 financial crisis, and it made the firm the second-hardest-hit institution on the planet, behind only Credit Suisse, whose $4.8 billion wound would eventually contribute to that bank's outright demise.1 Nomura had first warned the market of a "significant" loss from an unnamed US client on March 29, 2021, and cancelled a bond sale the very same day.2

Here is the paradox this story is really about. Nomura sits atop one of the most enviable positions in all of global finance: privileged, trusted, decades-deep access to Japanese households, who collectively hold the largest and most patient pool of savings in the world. That is a goldmine that should print stable, boring, high-margin money for decades. And yet, with almost clockwork regularity, this Japanese powerhouse has managed to set fire to its abundant domestic profits somewhere out on Wall Street or in the City of London. Why does a firm this well-endowed at home keep getting burned abroad?

That question — the gap between the domestic reality of a fortress franchise and the global ambition that keeps threatening to torch it — is the thread we will pull for the next two hours. To understand it, we have to travel across a full century of ambition, hubris, reinvention, and reckoning.

Here is the roadmap:

- The Osaka roots. How a visionary merchant,

二代目 野村徳七 Tokushichi Nomura II, turned a money-changing stall into a financial empire, and why his single most radical idea was not a trade at all but a research department. - The powerhouse of the bubble. The vertiginous heights of the 1980s

バブル経済 bubble economy, when Nomura was briefly one of the most profitable companies on Earth — and the twin scandals that shattered its reputation at home and rewired its psychology for a generation. - The Lehman gamble. The fateful September 2008 decision to buy the carcass of

リーマン・ブラザーズ Lehman Brotherseverywhere except the United States, why it looked like the deal of the century, and how it became a decade-long cost trap and culture war. - The modern pivot. How Group CEO

奥田健太郎 Kentaro Okudaand his Western-hired wholesale chief, Christopher Willcox, have been quietly executing one of the most radical transformations in the history of Japanese finance: a deliberate retreat away from volatile, capital-hungry trading, and back toward the stable, fee-generating businesses of wealth management, private markets, and capital-light advisory.

The tension running through all of it is a simple one for a long-term investor to hold in mind. Is Nomura, at 100 years old, finally learning to lean into the moat it actually has — the Japanese saver — or is it forever one derivative blowup away from proving it never learned anything at all? The firm's recent numbers make the strongest case in a generation that something has genuinely changed. The firm's own history is the reason to keep asking. To weigh both, we start where Nomura started: not in New York, but in Osaka.

II. Founding Context: Osaka Roots & The Power of Research

Picture Osaka in the first years of the twentieth century. This is Japan's merchant city — brash, commercial, a place where fortunes were made and lost in rice, cotton, and the noisy, semi-respectable business of trading stocks. The Tokyo establishment looked down on Osaka money the way old aristocracy looks down on new. And into this world stepped a young man named Tokushichi Nomura II, the adopted heir to a small money-changing shop, a business that survived on the thin spreads between coins and currencies.

He was, by temperament, a builder and a contrarian. In an era when Japanese stockbroking sat much closer to a gambling den than a profession — speculators shouting bids across smoke-filled rooms, acting on rumor, bravado, and gut — Nomura made a bet that sounds almost banal today and was genuinely heretical then. He bet that information, gathered systematically and analyzed rigorously, would beat instinct over time.

The Radical Idea: Research

So in 1906, long before he had a securities firm to hang the name on, Nomura established a dedicated in-house research department, and reportedly put a former newspaperman in charge of it.5 Think about how strange that was. His competitors were essentially betting shops; the whole industry ran on tips and nerve. Nomura hired people whose entire job was to study balance sheets, track macroeconomic trends, and assess the real underlying health of the companies whose shares everyone else was merely punting on.

This is the seed of everything that follows. Nomura the man grasped a truth that would later make fortunes for people like Benjamin Graham a continent away: in a market dominated by speculators, the participant with the best information is not gambling — he is compounding a structural edge. That conviction gave the house an intellectual prestige its rivals could never buy. And the research tradition ran so deep in the firm's identity that decades later it would help seed a separate analytical institution, 野村総合研究所 Nomura Research Institute, one of Japan's most influential think tanks and IT-consulting houses. Research was not a department at Nomura. It was the origin myth.

The firm we know today was formally born on December 25, 1925, when the securities department of Osaka Nomura Bank was spun out as a standalone company, 野村證券株式会社 Nomura Securities Co., Ltd., beginning life with just 89 employees.45 From day one it carried two distinct pieces of DNA — and the entire hundred-year saga is, in a sense, the story of the collision between them.

The Two Souls of Nomura

The first piece of DNA was that research-driven, analytical self-image: the belief that Nomura was the thinking person's securities house, more sophisticated than the boiler rooms around it.

The second was a sales culture of near-military intensity — and it is impossible to overstate how central this became. Over the postwar decades, Nomura built what came to be known, half in awe and half in fear, as the "Nomura Army": a relentlessly drilled, fiercely loyal force of retail salespeople who fanned out across every corner of Japan. They were famous for their discipline, their long hours, and their sheer refusal to take no for an answer. New recruits were forged in a culture that prized aggression, hierarchy, and total commitment to the firm.

That army did something no competitor could replicate: it embedded Nomura into the financial lives of ordinary Japanese families and provincial business owners, relationship by relationship, generation after generation. In a country organized around 系列 keiretsu corporate groupings and dense webs of local business ties, Nomura's foot soldiers became fixtures — the people who managed a family's savings, advised a regional manufacturer, and stayed in touch across decades. This is the origin of the firm's single most valuable and durable asset: unmatched domestic distribution. If you wanted to place a bond, float an equity, or reach tens of millions of Japanese savers, the road ran through Nomura, because Nomura had already knocked on every door in the country.

Why This Matters a Century Later

Here is where the two souls create tension. The research culture gave Nomura genuine credibility and a claim to being something more elevated than a sales machine. But the sales culture created a bottomless institutional hunger to move product — to keep the army fed, quarter after quarter. In a benign environment, that hunger drove healthy growth. In the wrong environment, as we will see, it curdled into churning, into favoritism, and eventually into outright scandal.

For a long-term investor, the takeaway from the origin story is not nostalgia; it is diagnosis. Nomura's genuine, durable competitive advantage — the thing that has survived every self-inflicted catastrophe since — was built here, at home, in distribution and trust. Every single time the firm has prospered, it has been leaning on Osaka and the saver. And every single time it has nearly destroyed itself, it has been reaching for something glamorous and far away. For the first six decades, that tension stayed mostly productive, as Nomura rose alongside Japan's postwar economic miracle. Then came the 1980s, when the firm would experience both of its faces — triumph and rot — at nearly the same moment.

III. The Powerhouse of the Bubble & The Scandalous Fall

By the late 1980s, Nomura was not merely a brokerage. It was one of the most formidable money-making machines on the face of the earth. Japan's asset-price bubble had inflated the Nikkei to numbers that seemed to defy financial gravity; the grounds of the Imperial Palace in Tokyo were said, only half-jokingly, to be worth more than the entire state of California. And Nomura sat at the dead center of the geyser.

The Peak

The firm underwrote wave after wave of equity and equity-linked securities for corporate Japan, which was raising capital as fast as investors could throw money at it. It churned retail stock trades through the Nomura Army at volumes its Western rivals could only envy. It posted profit margins that rivaled — and at moments exceeded — the mightiest US investment banks. For a brief, intoxicating window, Nomura ranked among the most valuable and profitable companies anywhere, its swollen market capitalization taken by many as proof that Japanese finance was about to inherit the postwar world the way Japanese manufacturing already had.

It is worth pausing on how total that confidence was, because it explains the trauma that followed. Nomura in 1989 was not an underdog dreaming of the big leagues; it was, by some measures, the big league. The idea that this firm might one day be a perennial global also-ran, restructuring its overseas operations again and again, would have seemed absurd. Hubris is always easiest to see in hindsight.

The Crash

It was, of course, a mirage — and when the bubble burst at the turn of the 1990s, it did not deflate gently. The Nikkei collapsed. Land values cratered. Japan slid into what the world would later call the "Lost Decades" — a generation-long grind of stagnation, deflation, and painful balance-sheet repair that would define the country's economy well into the twenty-first century.

For Nomura, the crash did something far more dangerous than shrink its profits. It stripped away the rising tide that had, for years, concealed a great deal of rot beneath the waterline. When the water went out, what it exposed nearly ended the firm's reputation.

The Dual Scandals

The first bomb detonated in 1991. It emerged that Nomura had been quietly practicing 損失補填 loss compensation — secretly reimbursing its largest, most favored institutional clients for their stock-market losses, while the ordinary retail investors whom the Nomura Army had so diligently recruited were left to swallow their own. The revelation was corrosive precisely because it inverted the firm's founding promise. Research, fairness, and sober analysis were the brand. A rigged, two-tier system in which the powerful were quietly made whole and the small saver ate the loss was the reality. Executives resigned, including at the very top of the house, and the affair became a national scandal about the cozy machinery of Japanese finance.

Then, before the memory could fade, came the second blow — arguably even more damaging because it dragged in the underworld. In 1997, Nomura was engulfed in a 総会屋 sokaiya scandal. The sokaiya were a peculiarly Japanese species of corporate racketeer: extortionists who bought a few shares in a company and then threatened to disrupt, humiliate, and drag out its annual shareholder meeting unless they were quietly paid to stay silent. It was corporate blackmail dressed in the clothing of shareholder democracy. Nomura executives had funneled some $560,000 through an illicit account to one such racketeer.6

The consequences were seismic and very public. President Hideo Sakamaki — who had himself been elevated to the top job back in 1991, in the reshuffle after the loss-compensation debacle — resigned in disgrace.6 And this time it was not one or two heads. In the end, fifteen senior executives stepped down in a single, brutal purge.6 The chairman, Masashi Suzuki, called it "the biggest crisis we've had since Nomura was established," and the firm reached for a relatively junior, US-based executive named Junichi Ujiie to take the helm precisely because he was untainted by the Tokyo rot.6 For a firm whose founding identity rested on being the respectable one, being raided and shamed over payments to gangsters was an existential humiliation.

The Strategic Trauma

Strip away the lurid specifics and you find the psychological wound that would reshape Nomura's strategy for the next twenty-five years. Twice in a single decade, the firm's domestic reputation had been gutted, its leadership decapitated, and its regulators enraged. And all of this was happening against the backdrop of a Japanese economy that now looked shrinking, aging, deflationary, and permanently over-scrutinized.

So a fateful idea took root deep in the corporate subconscious: salvation lies abroad. If the home market was a source of stagnation, scandal, and shame, then the path forward was to become a genuinely global investment bank — to diversify away from Japanese regulatory pressure and economic decline by planting flags on Wall Street and in London. Escape became the strategy.

It was an entirely understandable instinct. It was also, as the next fifteen years would prove again and again, the wellspring of nearly every catastrophe still to come. The urge to escape home is precisely what set up the single most consequential gamble in Nomura's century of existence — a gamble that arrived, gift-wrapped in the ruins of a rival, in September 2008.

IV. The Lehman Gamble: Buying the Remains of a Giant

On the morning of Monday, September 15, 2008, Lehman Brothers filed for the largest bankruptcy in American history, and the global financial system went into cardiac arrest. In New York, stunned bankers carried cardboard boxes of belongings out of a dying institution while photographers snapped away. Half a world away, in Tokyo, Nomura's leadership looked at the same wreckage and saw something different. Not a catastrophe. An opportunity — perhaps the opportunity of a lifetime.

The Bold Move

The logic, as CEO Kenichi Watanabe and his chief operating officer Takumi Shibata framed it, was audacious and, on paper, genuinely brilliant. The single hardest thing to build in global finance is a deep, functioning network of elite people and long-standing client relationships spanning continents. It takes decades and enormous sums, and you usually cannot buy it at any price because it is not for sale. Lehman had spent generations assembling exactly that — and now, in the chaos of the bankruptcy, it was being broken up for scraps.

Within days, Nomura moved with a speed that was, frankly, out of character for the consensus-driven firm. It acquired Lehman's franchise across the Asia-Pacific region, reportedly for a figure in the low hundreds of millions of dollars, and then, separately, its investment-banking and equities businesses across Europe and the Middle East — the latter for a famously nominal sum, the corporate equivalent of a token handshake to make the paperwork legal.7 That European and Middle Eastern unit alone employed roughly 2,500 people and its acquisition became legally effective on October 13, 2008.8 Taken together across the regions, Nomura absorbed on the order of 8,000 sophisticated Lehman staff almost overnight.

The Vision

The pitch to the market was intoxicating, and Watanabe delivered it with conviction: Nomura would become "a global investment bank from Asia." In a single stroke, the firm had bought itself an instant worldwide footprint to challenge Goldman Sachs and Morgan Stanley on their own turf. It had inherited the trading desks, the sector specialists, and the client rolodexes of a Wall Street titan for pennies on the dollar. For a firm still carrying the psychological scars of the 1990s and desperate to escape a stagnant home market, this was the dream made flesh: not incremental expansion, but a leap straight to the top table of global finance.

To hold that dream together through the panic, Nomura did the thing firms always do in a bidding war for scarce talent — it guaranteed them. Multi-year, Wall Street-scale compensation packages were promised to the Lehman stars to keep them from bolting to rivals during the most uncertain months in living memory. In the emotional logic of September 2008, this looked like prudence: you had just bought a business whose entire value was its people, so of course you paid to keep the people.

And then, slowly and very expensively, the whole edifice began to reveal its structural flaws.

Why It Failed: A Post-Mortem

The geographic disconnect. This was the flaw hiding in plain sight. Barclays had swooped in and bought Lehman's US operations — the core North American investment-banking and distribution engine — for a sum in the region of $1.75 billion. Nomura got Europe and Asia. But you cannot run a truly global investment bank without a dominant, highly profitable American franchise, because the United States is where the deepest capital markets, the largest fee pools, and the most coveted corporate clients live. A global bank without a strong US core is like an airline with a magnificent route map and no hub. Nomura had, in effect, bought the arms and legs of a global institution while Barclays took the beating heart.

The cost trap. Those generous guaranteed bonuses had been sized, emotionally and financially, for a world that was about to return to boom. Instead, global markets ground into a multi-year stretch of anemic volumes, thin margins, and heavy new regulation. Nomura now found itself carrying a Wall Street-sized cost base into a post-crisis desert — enormous fixed compensation obligations set against trading and banking revenues that stubbornly refused to materialize. Fixed costs are wonderful when revenue is climbing and lethal when it is flat. Nomura learned the lethal version.

The culture clash. This was the deepest wound of all, because it could not be fixed with a spreadsheet. Nomura's consensus-driven, hierarchical, 稟議 ringi-style decision-making — in which proposals circulate patiently for collective sign-off before anything happens — collided head-on with the individualistic, eat-what-you-kill, move-fast ethos of the ex-Lehman bankers. The two cultures never truly fused. Decisions that a nimble American desk expected in hours took weeks to wind through Tokyo. And the guarantees, it turned out, were a slow-acting poison: many of the highest-profile hires collected their guaranteed bonuses and then walked straight out the door the instant those packages vested, decamping to competitors and taking their client relationships with them.7 Nomura was left holding the expensive infrastructure and the inflated cost base, but hemorrhaging exactly the revenue-generating talent it had paid so dearly to retain.

So What It Meant

The Lehman acquisition was the boldest possible expression of Nomura's post-scandal dream of escaping Japan. Instead of vaulting the firm to the global top table, it chained Nomura to a sprawling wholesale business that would bleed capital, management attention, and credibility for more than a decade. Every restructuring to come, every cost program, every awkward retreat, traces back in some way to the fixed-cost machine and cultural mismatch bought in the autumn of 2008.

The dream of leaping to the summit had quietly become a recurring bill. And what came next was not a single, cathartic reckoning but something more grinding: a long war of attrition, waged by Nomura against the consequences of its own ambition.

V. The Restructuring Decades & The Archegos Disaster

If you compressed the 2010s at Nomura into one recurring scene, it would be a management team standing before a room of skeptical analysts, slides glowing behind them, announcing — once again — that this time the global wholesale division would finally be fixed.

A Decade of Bloodletting

The pattern repeated with almost seasonal reliability. A cost program would be unveiled with fanfare. Desks would close, businesses would be exited, geographies would be trimmed. Management would promise that the platform was now right-sized and poised for consistent profitability. And then, a couple of years later, another program would arrive, because the underlying problem — a global wholesale business that was structurally too small in the places that mattered and too expensive everywhere — had never actually been solved. This is the "bloodletting" decade: a slow, repeated draining of ambition, each round leaving the patient a little weaker and the promises a little less credible.

The most consequential of these arrived in April 2019, under then-CEO Koji Nagai. Nomura announced a roughly $1 billion cost-cutting program and, tellingly, moved to shut around 30 of its roughly 156 Japanese retail branches — an admission that even the sacred home franchise had grown bloated and needed pruning.9 But the numbers were less important than the philosophy quietly buried inside them. For the first time, Nomura publicly elevated capital efficiency above global scale. It began pulling back from low-margin fixed-income businesses in Europe. The old dream — matching Goldman Sachs on every product, on every desk, in every financial capital — was being abandoned, not with a dramatic announcement but through the accumulated weight of a decade of disappointment. In its place came a more sober, more adult question: which of these businesses actually earns back its cost of capital, and which are just prestige we can no longer afford?

Enter Okuda

In April 2020, in the teeth of the COVID-19 pandemic, the baton passed to Kentaro Okuda, who became Group CEO. In one sense he was a classic Nomura insider: he had joined the firm in the late 1980s, at the height of the bubble, and built his career in the wholesale and investment-banking businesses. But he was also a company man shaped by years spent in New York, fluent in the language of global markets and — crucially — in the language and expectations of Western institutional investors. He was, in other words, a bridge figure: Japanese to his core, but comfortable being challenged by an American analyst on a conference call.

His mandate was to stabilize the sprawling global platform and finally make the long-promised transformation stick. Almost immediately, the market handed him a test he had no conceivable way of preparing for.

Understanding the Weapon: Total Return Swaps

To grasp what happened with Archegos, you first have to understand a deceptively simple instrument called the total return swap, because the whole disaster lives inside its mechanics.

Normally, if you want exposure to a stock, you buy the stock. Simple. But a total return swap lets a client get all the economic upside and downside of a stock without ever owning it. Here is the trick. The client — say, Bill Hwang's Archegos — goes to a prime broker like Nomura and enters a swap. Under the contract, Nomura goes into the market and buys the actual shares, and Hwang agrees to pay Nomura a fee plus any losses on those shares, in exchange for receiving any gains. Economically, Hwang has the full exposure. Legally, Nomura owns the stock, and Hwang's name never appears on the company's shareholder register.

Two things make this dangerous. First, leverage: the client only has to post a fraction of the position's value as collateral, so a relatively small amount of capital can control a very large economic bet. Second, invisibility: because Hwang ran the same play across several prime brokers simultaneously — a swap here, a swap there — no single bank could see the true, terrifying, aggregate scale of his concentrated wagers on a handful of stocks like ViacomCBS and Discovery. Each broker saw its own slice and assumed it was manageable. None saw the whole monster.

The Liquidating Race

The scheme worked beautifully until it didn't. When ViacomCBS's share price cracked in late March 2021, the swaps flipped violently against Hwang. The prime brokers issued margin calls — demands for more collateral — and Archegos could not meet them. At that instant, every bank holding those swaps faced the same brutal choice: dump the underlying shares fast, before the price fell further, or hold on and hope.

This became a race, and the race exposed everything the Lehman decade had failed to fix. Goldman Sachs and Morgan Stanley — faster, more ruthless, better wired for exactly this kind of moment — moved first and hardest, liquidating the collateral backing their exposures early and getting out before the fire fully spread. Nomura, by contrast, was slower. It was tangled in its own risk committees, culturally inclined toward relationship-preserving hesitation, and simply not built for the split-second, take-the-loss-now reflexes that a fire sale demands. By the time it acted, the assets had collapsed. The firm was left holding the bag, and the bill — disclosed over the following weeks — came to roughly $2.9 billion, dragging Nomura to its worst quarterly loss in more than a decade.1

The episode was a savage indictment. It suggested that after ten years of restructuring rhetoric about discipline and risk, Nomura's US prime-brokerage risk management still contained a blind spot large enough to swallow an entire year of hard-won profits in a single week. The very slowness and consensus-seeking that defined the firm's culture — the same traits that had made the Lehman integration so painful — had now cost it billions in a context where speed was survival.

The Course Correction

And yet, this is precisely the moment where Okuda's credibility began to be built rather than merely asserted — so it deserves careful attention from anyone assessing today's management. He did not simply issue an apology and promise to try harder.

He took a voluntary temporary pay cut. He forced out senior wholesale executives, accepting accountability at the top rather than pinning the failure on a mid-level risk officer. And most importantly, he did something structural: he systematically exited the business that had caused the damage, winding down cash prime brokerage in the United States and Europe rather than vowing to run it more carefully next time. That last decision is the tell. A management team defending its ego doubles down and promises better controls. A management team that has genuinely learned something removes the loaded gun from the house. Okuda chose the second path.

It was the clearest signal yet that Nomura might finally be willing to shrink its way to strength rather than gamble its way to scale. That instinct — deliberate retreat toward defensible ground — became the spine of the entire strategy he would unveil next.

VI. Modern Nomura: Okuda's 2030 Pivot

Every good transformation story needs a villain, and the villain Okuda chose was Nomura's own past self: the volatile, capital-devouring trading house whose fortunes swung wildly with the market and whose periodic disasters kept incinerating the steady earnings thrown off by the domestic franchise. His answer, which the firm branded "Reaching for Sustainable Growth," was a plan to remake Nomura by 2030 into something its founder might actually recognize — a firm that earns durable, recurring fees from managing other people's money, rather than repeatedly betting its own balance sheet and holding its breath.

Rebranding Retail as Wealth Management

The reorganization began, as these things often do, with a rebrand that was much more than cosmetic. In April 2021 — just weeks after the Archegos loss landed — Nomura renamed its long-standing "Retail" division "Wealth Management." That is not a marketing footnote; it is a statement of strategic intent.

The old retail model was transactional at its heart. The Nomura Army generated commissions by getting clients to trade — to buy this fund, switch into that bond, act on the latest idea. That model had two mounting problems. It attracted intense regulatory scrutiny, because "getting clients to trade" and "churning clients for commissions" can look uncomfortably similar. And it was a sitting duck for the zero-commission online brokers who were about to make transactional trading essentially free.

The new model aims deliberately upmarket, toward high-net-worth advisory. Its centerpiece is the discretionary "wrap" account — an arrangement in which the client pays a steady annual fee calculated on the assets under management, and Nomura manages the portfolio, rather than earning a commission every time something is bought or sold. Around that sit estate planning, inheritance structuring, and tax advice tailored to Japan's rapidly aging, asset-rich population, where trillions of yen are poised to pass from one generation to the next. The strategic logic is clean: fee-on-assets revenue is stickier, higher-margin, and far less dependent on whether clients happen to feel like trading this quarter. It converts a business that lived and died on transaction volume into one that compounds quietly on the size of the asset base.

Creating Investment Management

At the same time, in April 2021, Nomura created a new division called "Investment Management" by merging its asset-management arm with its merchant-banking operations. The explicit purpose was to manufacture stable management-fee income at scale — the classic, capital-light economics of an asset manager, who earns a slice of the assets it oversees regardless of market direction.

Bolted onto this was the real growth engine: private markets. Private equity, private debt, real estate, and infrastructure — the "alternative" assets that wealthy clients increasingly demand and that, crucially, carry far richer fees than plain-vanilla stock and bond funds. For a firm trying to move away from balance-sheet risk and toward fee income, alternatives are attractive precisely because clients will pay premium fees for access and expertise, and because the money tends to be locked up for years, making the fee stream unusually durable.

The boldest move to scale this ambition came in April 2025, when Nomura agreed to acquire Macquarie's US and European public asset management business for $1.8 billion in cash — its largest acquisition since Lehman.1213 The deal brought roughly $180 billion of client assets and a Philadelphia-based platform, and it was expected to lift Investment Management's total assets under management toward $770 billion, finally giving Nomura a genuine distribution presence in American retail and institutional funds.13

It is worth sitting with the symbolism here, because it is the whole thesis in miniature. The Lehman deal in 2008 was a leap into volatile, capital-hungry, culturally alien trading. The Macquarie deal in 2025 was a purchase of exactly the opposite: a steady, fee-generating, capital-light asset-management business. Same firm, same instinct to expand in America — but the kind of business being bought had completely inverted. That said, an independent observer should hold one pointed question open: Nomura's record of integrating US-facing acquisitions is, to put it gently, poor. Whether it can absorb an American asset manager and retain its people and clients — where it so conspicuously failed to integrate American traders — is precisely the thing the deal has yet to prove. Buying capital-light economics is easy. Keeping them is the hard part.

Re-engineering Wholesale

The wholesale division — the perennial problem child, the source of both the Lehman trap and the Archegos disaster — received a different kind of intervention: an outsider with no emotional attachment to its past.

In September 2022, Nomura announced that Christopher Willcox, the former CEO of JPMorgan's asset-management business, would take over the Wholesale Division, effective that October, making him the firm's first non-Japanese executive officer.10 Installing a battle-hardened Western executive at the head of the division that had caused so much pain was itself a message — to employees, to regulators, and above all to investors. It signaled that Nomura understood that credibility and risk discipline in cutthroat global markets might require someone who had actually lived and led in that world, rather than another rotation of a domestic lifer.

Willcox's mandate carried a pointed and revealing condition: wholesale would have to become "self-funding." In plain terms, it would need to generate its own growth from its own returns, without siphoning capital away from the profitable domestic wealth business that had quietly subsidized its global ambitions for more than a decade. This is the strategic reversal stated as a budgeting rule. For years the healthy franchise had bankrolled the volatile one. Now the volatile one was being told to pay its own way or shrink.

The Capital-Light Blueprint: Greentech

Rounding out the pivot was a smaller but unusually revealing deal that actually predated the strategy's formal branding — a kind of prototype for the whole philosophy. In late 2019 Nomura agreed to buy Greentech Capital Advisors, a boutique investment bank focused on clean-energy and sustainable-infrastructure dealmaking, completing the acquisition in April 2020 and rebranding it Nomura Greentech.11

The logic was philosophical, not just commercial. In the energy transition, there are two ways to make money. You can lend money — deploy your balance sheet against wind farms and battery projects, taking on credit risk and tying up capital for years. Or you can advise — earn high-margin fees for arranging the deals, structuring the transactions, and connecting the capital, while risking none of your own balance sheet. Nomura chose the second, and Greentech became a small, capital-light advisory engine: fee income, no balance-sheet exposure, high return on the modest capital it consumes. It was, in effect, a miniature working model of the entire 2030 thesis.

The question a neutral investor has to ask is whether all of this — the rebrands, the reorganizations, the acquisitions — is actually showing up where it counts: in the audited economics of the firm. Slogans are cheap. Segment income is not. So let's look at the numbers.

VII. Segment-Level Economics & Capital Allocation

For a firm whose entire modern story has been one long argument about whether it can stop hurting itself, the fiscal year ended March 31, 2026 was, by its own historical standards, a genuine vindication — and, viewed skeptically, also a warning about how much of the good news rests on a strong market.

The Financial Engine

Nomura reported net revenue of ¥2,167.7 billion, up 15%; income before income taxes of ¥539.8 billion, up 14%; and net income attributable to shareholders of ¥362.1 billion — a record, and notably the second consecutive year of record profit.3 Return on equity came in at 10.1%.3

That ROE figure deserves the spotlight more than any headline profit number, because it goes to the heart of the historical indictment. For years, the case against Nomura was not that it couldn't make money in good years — anyone can — but that it couldn't consistently earn a double-digit return on the capital shareholders had entrusted to it. Capital-intensive trading businesses are ROE killers: they soak up huge amounts of balance sheet to generate returns that, averaged across good years and blow-up years, often failed to clear the firm's cost of equity. Clearing 10% two years running is the difference between a turnaround claim and a turnaround fact. It suggests, at minimum, that the mix shift toward capital-light fee income is doing what management said it would.

The Segment Story

Peel back the group headline and the segment composition explains where the durability is genuinely coming from — and where it is not. Of the roughly ¥506.9 billion in combined pre-tax income across Nomura's four operating segments (itself an all-time high), the split is the real story.15

Wealth Management — the cash cow. This is the division the entire strategy was built to elevate, and it delivered pre-tax income of roughly ¥204 billion, up around 23% and a record since the division's creation.15 The engine underneath it is the steady accumulation of client assets, which reached about ¥175.8 trillion, and — more meaningful for the thesis than the raw asset figure — recurring-revenue assets of around ¥30 trillion.1522 That recurring pool is the one that throws off predictable fees whether or not clients trade, and it is the truest measure of the shift away from commission dependence. Most tellingly, Nomura has now booked net inflows of client money for fourteen consecutive quarters.22 Fourteen straight quarters is not a fluke or a single good campaign; it is a sustained behavioral pattern, and it is the strongest piece of evidence that the move from churning commissions to fee-based advice is real rather than rhetorical. On the evidence, this is the low-risk, high-quality earnings core the strategy promised.

Investment Management — the fee generator. Here the picture is more mixed, and honesty requires saying so. Pre-tax income of about ¥88 billion was roughly flat year on year, even as assets under management swelled to around ¥136.9 trillion.15 Flat profit on a rising asset base is a yellow flag: it means the new assets are not yet translating into proportional fee growth, whether because of mix, fee compression, or integration costs. The Macquarie acquisition is precisely the bet that international scale will eventually convert asset growth into faster fee growth. For now, the segment has bought scale but not yet demonstrably monetized it — a "watch this space," not a "mission accomplished."

Wholesale — the volatile giant. The division that gave us both the Lehman trap and Archegos turned in pre-tax income of roughly ¥200 billion, up around 21% and its best result since the unit was established.15 Under Willcox, wholesale has lowered its break-even point and leaned toward capital-light advisory and away from balance-sheet-heavy trading. But this is exactly the number a neutral analyst should hold at arm's length. Wholesale earnings are inherently cyclical; they are flattered by the strong, high-volume, high-volatility markets that have prevailed recently. A single great year does not prove the tail risk has been engineered out of the business — Archegos, after all, arrived in the middle of what was otherwise a strong period. The fair read is that wholesale is now better run and better managed, not that it has been made safe. Those are different claims, and management's credibility rests on not conflating them.

Capital Allocation and Alignment

On capital allocation, management is trying to signal discipline in two directions at once: reinvesting for growth and returning cash to owners. For the record year, Nomura declared a total dividend of ¥51 per share — a ¥27 interim plus a ¥24 year-end — against a payout ratio of roughly 41%.3 A sharp-eyed reader will notice that ¥51 was actually down from ¥57 the prior year, which looks odd in a record year. The explanation is that the prior year's figure had included a ¥10 special commemorative dividend tied to the firm's 100th anniversary, so the underlying, repeatable payout policy is steadier than the year-over-year drop suggests.314 Alongside dividends, Nomura has run systematic share buybacks and pursued bolt-on acquisitions like Macquarie — the familiar balancing act of a company trying to prove it can simultaneously grow and hand money back.

Management alignment is a fair thing to probe given the firm's history of enriching people who then walked out the door. Okuda's compensation for the year rose about 36% to roughly ¥1.6 billion (around $10 million), the large majority of it performance-linked through restricted and performance stock units, and it rose specifically because profits hit a record.16 That is a defensible pay-for-performance structure. Two caveats belong in the ledger, though. First, the absolute level is modest by Wall Street standards, which cuts both ways — it looks restrained, but it also means the retention economics for Nomura's own star bankers remain a live competitive problem in a world where JPMorgan and Goldman pay multiples more. Second, Okuda is a career salaryman-executive, not a founder-owner with a large personal stake; investors should read his alignment as "incentive-aligned," not "skin-in-the-game" in the way a large equity holding would imply. Working alongside him, CFO Hiroyuki Moriuchi, appointed in mid-2025, has become the public face of the firm's capital-discipline message.

Put it together and the credibility scorecard reads honestly like this: a disastrous opening act in Archegos, followed by several consecutive years of roughly doing what was promised — hitting the ROE bar, growing the stable segments, exiting the businesses that caused past disasters. That track record is the real foundation on which everything else in the investment case now rests. It is good. It is not yet proof against the next cycle.

VIII. Playbook: Business & Investing Lessons

Step back from the century-long chronology and Nomura offers a set of lessons that generalize well beyond Japanese finance — a playbook written mostly in the expensive ink of its own mistakes. These are the transferable ideas for founders, operators, and allocators.

Lesson 1: Beware the Cross-Subsidization Discount

For decades, Nomura's superb domestic franchise quietly subsidized its sub-scale global wholesale ambitions, funneling stable Japanese cash flows into a business that repeatedly gave them back to the market in the form of losses. And investors noticed. They did not reward Nomura for the good business and shrug off the bad one; they punished the whole company, applying a persistent discount because they could never trust that a given year's domestic profits would actually survive to reach them rather than being vaporized by an overseas trading disaster.

The transferable insight is uncomfortable: a great business bolted to a structurally weak one does not average out to "pretty good." It frequently trades below the weak business's drag, because the market cannot separate the cash flows it trusts from the ones it fears, so it discounts everything. Whenever you attach a volatile, capital-hungry venture to a stable cash machine, you should assume the market will price the combination for the venture's worst tendencies, not the machine's best ones. Know where your structural moat actually lies, and be ruthless about what you allow to feed off it.

Lesson 2: The Brutal Economics of Sub-Scale Investment Banking

Global wholesale banking is close to a winner-take-all game, and the winning position is anchored in the United States, where the deepest capital markets, the biggest fee pools, and the most valuable clients concentrate. Scale there confers operating leverage, client access, and the ability to absorb a bad quarter that sub-scale players simply lack.

Nomura's Lehman experience is the cautionary tale in its purest form. Buying a global network without the dominant American core was not a clever shortcut to the top table; it was an expensive, high-beta gamble on being able to build the missing piece before the fixed costs ate the returns. The uncomfortable truth the episode illustrates is that in a business with a few dominant winners, being a distant number six or seven can be worse than not competing at all — you carry most of the costs of playing without the scale that makes playing pay. Sometimes the disciplined move is to not fight a war you are structurally positioned to lose.

Lesson 3: Risk Management Is a Strategic Driver, Not a Back-Office Chore

It is tempting, especially in a good year, to think of risk control as bureaucratic overhead — the department that slows things down and says no. Archegos is the definitive rebuttal. A single, unglamorous failure of transparency and speed — the inability to see one client's true aggregate leverage, and the inability to act fast when it unwound — erased billions and undid years of restructuring in a matter of days.

For any leveraged institution, risk management is not a support function; it is the business of protecting equity value, and it belongs in the strategic conversation at the highest level. The mechanism matters: the danger was invisible (spread across brokers) and the response was slow (tangled in committees), and it was the combination that proved lethal. Blind spots plus slow reflexes is the formula for a catastrophe. The lesson is not "have a risk department"; every firm that has blown up had one. The lesson is that the speed and independence of that function is a first-order strategic variable, not an afterthought.

Lesson 4: Position for the Macro Shift You Can Actually See Coming

Japan is in the early innings of a genuinely generational transition captured by the phrase 貯蓄から投資へ — "from savings to investment." Households that parked money in cash for decades of deflation are, prodded by a revamped tax-free investment regime and by the return of real inflation, finally beginning to move it into markets. A firm with Nomura's distribution is the natural, obvious beneficiary of that wave.

But the lesson has a sting in its tail, and it is the part operators tend to forget. Structural tailwinds only reward incumbents who are still standing where the customers are when the wind arrives — and who haven't lost those customers to a cheaper, faster competitor in the meantime. A generational tailwind is not the same as a guaranteed win; it is an opportunity that goes to whoever is best positioned to capture it. Identify the slow, powerful macro shift early, then make sure you still own the distribution when it finally pays off.

The thread connecting all four lessons is discipline over vanity — the hard-won recognition that Nomura's edge was never in out-Goldman-ing Goldman, but in owning the relationship with the Japanese saver. Whether that edge truly qualifies as a moat — durable, defensible, genuinely hard to replicate — is a question we can test directly with the standard strategy frameworks.

IX. Strategic Position: 7 Powers & Porter's 5 Forces Analysis

Let's war-game Nomura's competitive position properly, using two complementary lenses. First, Hamilton Helmer's 7 Powers, which asks not the lazy question "is this company big?" but the sharp one: "what specifically prevents a competitor from competing away these returns?" Then Porter's Five Forces, which is considerably less flattering.

The Powers Nomura Genuinely Has

Scale economies. In Japanese domestic wealth management, Nomura's scale is real and hard to match. A client-asset base on the order of ¥175.8 trillion, spread across a nationwide advisory network, gives it a low unit-cost base and the distribution muscle to roll out new products faster and more cheaply than any smaller rival.15 The point is subtle but decisive: manufacturing an investment product is worthless without the shelf space to sell it, and Nomura owns an unusually large, unusually well-trafficked shelf. A rival with a better fund but a fraction of the distribution simply cannot reach the customers economically.

Switching costs. In the high-net-worth segment specifically, switching costs are real and rising. Wealthy and elderly Japanese clients rarely fire the advisor who holds their multi-generational relationships, understands the intricacies of their estate, and has already structured their inheritance and tax affairs. Unwinding all of that to chase a slightly lower fee elsewhere is disruptive, risky, and simply not worth it for most such clients. This is exactly why Okuda's upmarket pivot deliberately targets this cohort: the stickiness is not a side benefit, it is the entire point. The more complex the client's financial life, the harder they are to poach.

Cornered resource. Nomura's decades-deep access to the boardrooms of "Japan Inc." is extremely difficult to replicate on any reasonable timescale. That accumulated relationship capital gives it a near-structural claim on major domestic M&A, equity, and debt underwriting mandates — the kind of business that flows to the bank the CEO already knows and trusts. A newcomer, however well-capitalized, cannot simply purchase a century of accumulated trust and access.

The Forces Working Against It

Now the counterweight, and it is a heavy one. Porter's Five Forces paints a far more contested picture than the Powers analysis alone would suggest.

Rivalry is intense. In the domestic arena, Nomura faces the mega-bank-backed brokers 三菱UFJモルガン・スタンレー証券株式会社 Mitsubishi UFJ Morgan Stanley Securities Co., Ltd. and SMBC日興証券株式会社 SMBC Nikko Securities Inc., both of which can lean on the vast deposit bases and corporate lending relationships of their megabank parents to win business. It also faces the traditional independent rival 株式会社大和証券グループ本社 Daiwa Securities Group Inc., Japan's other great securities house. None of these players will cede the lucrative high-net-worth and corporate-advisory prizes without a fight, and the bank-backed rivals in particular can bundle securities services with lending in ways a standalone broker cannot.

The threat of new entrants — really, digital disruption — is high and structural. This is the force that should worry a long-term holder most. The low-cost online brokers 株式会社SBI証券 SBI Securities Co., Ltd. and 楽天証券株式会社 Rakuten Securities, Inc. moved to zero commissions on Japanese equity trades starting in September 2023, a first for the industry.21 They dominate the younger demographic, they operate at a fraction of the cost of a branch-and-salesforce model, and they have effectively driven the economics of transactional retail broking toward zero. This is precisely the force that made Nomura's flight upmarket not a strategic luxury but a survival necessity: you cannot win a price war against a competitor whose price is nothing, so you retreat to advice, complexity, and relationships that a discount app cannot easily replicate. Nomura is not beating the disruptors on their turf; it is deliberately abandoning that turf for higher ground.

The bargaining power of suppliers — meaning elite talent — is high, particularly in wholesale. Top global bankers and traders command Wall Street compensation, and that structurally compresses the margins of any investment bank that wants to employ them. This is the very same force that turned the Lehman guarantees toxic more than a decade ago, and it has not disappeared. In the businesses where Nomura most wants to compete globally, the most valuable people can capture much of the economic value for themselves.

The Synthesis

Line the two frameworks up and a clear picture emerges. Nomura's genuine powers — scale, switching costs, cornered resources — are concentrated almost entirely in its domestic wealth and Japanese corporate franchise. And the forces working against it — commoditizing price competition, talent costs — bite hardest in exactly the arenas where it has historically over-reached: globally competitive wholesale, and the mass-retail market now being hollowed out by zero-commission apps.

Read through this lens, Okuda's entire strategy is not merely a preference or a slogan. It is Nomura rationally retreating toward the ground where it holds durable power and away from the ground where it does not. The open question — the one that separates the bull from the bear — is whether that retreat is happening fast enough, and whether the powers it is retreating toward can survive the demographic and digital pressures now bearing down on them. That is the debate we turn to last.

X. Bull vs. Bear Case & Current Risk Radar

So how should a disciplined long-term investor actually track whether this hundred-year transformation is working — separating durable signal from the noise of any given quarter? Cut through everything and three KPIs carry most of the information.

The Three KPIs That Matter

First, Wealth Management recurring-revenue assets and net inflows. This is the single truest gauge of whether the shift from transactional commissions to sticky, fee-on-assets advice is real and sustained. The roughly ¥30 trillion of recurring-revenue assets and the fourteen-consecutive-quarter inflow streak are the specific figures to watch either hold or break.22 If inflows stall or the recurring pool stops growing, the core thesis is in trouble regardless of what any given year's headline profit says.

Second, group ROE. This is the one number that condenses the entire question of whether Nomura is finally earning its cost of capital rather than destroying it. Management cleared 10% two years running and has since raised its own long-term bar — which we will come to. A sustained double-digit ROE is the proof of the pudding; a relapse back toward mid-single digits would signal that the capital-heavy old firm is reasserting itself.

Third, the Wholesale cost-to-income ratio and capital consumption. This measures whether Willcox's discipline is durable or merely borrowed from a friendly market. If wholesale can hold down its costs and its balance-sheet usage even as market conditions normalize, the "self-funding" promise is being kept. If costs balloon the moment revenues wobble, it isn't.

The Bull Case

The bull case is that Nomura is, at bottom, a leveraged play on an irreversible macroeconomic shift in the world's third-largest economy. Japanese household financial assets reached a record ¥2,351 trillion at the end of 2025, and — for the first time in nearly two decades — the share sitting idle in cash and deposits slipped below half, to roughly 48.5%.19 That single statistic is the whole bull thesis in one line: an unimaginably large pool of money is finally, slowly, beginning to move.

The revamped NISA regime — the 少額投資非課税制度 Nippon Individual Savings Account, made permanent from January 2024 with an indefinite tax-free holding period and a lifetime tax-free investment cap of ¥18 million — is engineered by the government precisely to accelerate that migration from cash into markets.18 Early flows into the scheme have run well ahead of the government's original targets, suggesting the behavioral shift is real and not merely policy on paper. If even a modest fraction of that colossal cash pile keeps moving into investments over the coming decade, the firm with the deepest, most trusted distribution network in the country stands to harvest it. Layer on top the alternatives-driven fee growth in Investment Management and a wholesale division that finally pays its own way, and the bull argues the firm's earnings base is now both structurally higher and structurally calmer than at any prior point in its modern history.

Management's own confidence shows in a concrete, falsifiable way: at its investor day, Nomura raised its 2030 targets, lifting the ROE goal to 10–12%+ and the pre-tax income target to over ¥750 billion — up sharply from the roughly ¥500 billion figure it had floated only a year earlier.17 Raising targets after hitting the old ones is, at minimum, a sign of a management team that believes its own strategy is compounding rather than topping out.

The Bear Case and Risk Radar

The bear case — the risk radar — is that none of Nomura's three great historical vulnerabilities have actually been eliminated. They have been managed, mitigated, and talked around. That is not the same as gone.

Digital disintermediation. This is the slow, structural threat, and it is demographic in nature. The zero-commission online brokers own the young. As wealth passes from Japan's elderly savers to their children and grandchildren over the coming decades — one of the largest intergenerational wealth transfers in the world — those heirs may never walk into a Nomura branch or call a Nomura advisor. They already bank and trade on their phones. Nomura's moat is strong among today's wealthy and demonstrably weak among tomorrow's, and the clock runs in only one direction. The upmarket pivot buys time and defends the current book; it does not obviously solve the pipeline problem a generation out.

Macro and interest-rate risk. The Bank of Japan 日本銀行 ended its long era of negative interest rates in March 2024 — its first rate hike in some seventeen years — and has been cautiously edging rates upward since.20 Normalizing rates can help a wealth manager in some respects, by making certain products more attractive and widening some spreads. But rising and volatile rates also cut the other way: they can inject sharp volatility into markets, freeze the debt-underwriting windows that wholesale depends on, and generate valuation losses across the large fixed-income inventories a firm like Nomura carries on its books. A disorderly move in Japanese government bond yields, after decades of ultra-low rates, is a genuine tail risk for the entire domestic financial complex, Nomura very much included.

Execution and tail risk in wholesale. This is where a skeptical long/short investor or an activist would press hardest, and the pressure is fair. Nomura has stood before analysts and promised risk discipline before — and Archegos happened anyway, in the middle of a restructuring that was supposed to have instilled exactly that discipline. The sheer complexity of a global markets business means that the next blowup, if it comes, will almost by definition arrive from a direction no committee is currently watching — just as the last one did. A single derivative or operational failure could, once again, torch a year of patiently rebuilt credibility in a week.

An activist would sharpen the challenge further: is the portfolio still too complex? Does a firm with a fortress domestic wealth business and a chronically hard-to-manage global wholesale arm really benefit shareholders by keeping both under one roof, or is the market still applying a version of the old conglomerate discount? Is management being held genuinely accountable, or does a strong market cycle paper over structural fragility? These are not rhetorical jabs; they are the exact questions that determine whether the recent record results represent a durable re-rating of the business or a well-timed ride on a friendly cycle.

Management's answer to all of it is consistent: it has exited the specific businesses that caused past disasters, installed an outsider to enforce discipline, and shifted the earnings mix toward stable fees. The honest, neutral investor response is that these steps genuinely reduce the odds of another catastrophe without ever driving them to zero — which is the permanent condition of owning a leveraged financial institution. The real case for Nomura from here is not that the risk has been abolished. It is that, for the first time in a long time, the firm may finally be getting paid enough, from stable enough sources, to be worth bearing that irreducible risk.

XI. Epilogue & Outro

A century after 89 employees walked into an Osaka office to open the doors of a new securities firm, Nomura crossed its 100-year milestone as, above all, a survivor — which, in the wreckage-strewn history of global finance, is no small thing at all. Consider the company it has outlasted. Institutions that towered over Nomura on Wall Street in 2008 no longer exist in any form. Nomura is still here: still the dominant force in Japanese finance, still standing on the distribution moat that its founder began building with a research department in 1906 and an army of salespeople in the decades after. Endurance, in this industry, is itself an achievement.

But survival is not the same thing as vindication, and the honest verdict on Nomura in 2026 is that it is a company in the middle of proving something, not at the end of having proved it. The strategy Okuda has pursued amounts to a deliberate, sustained act of self-denial: sacrificing the vanity of global "league table" size in favor of the harder, quieter, less glamorous economics of a capital-light, high-margin, domestically anchored business. For a firm whose entire post-scandal psychology was built around the dream of escaping Japan, the decision to consciously lean back into Japan — into the saver, the estate, the multi-generational relationship — is a genuinely radical reversal. And on the evidence of the last two years of record results and consistent execution, it appears, so far, to be a working one.

The century's ultimate lesson, for founders, operators, and long-term investors alike, is embedded in that reversal. Nomura spent decades and many billions of dollars chasing an advantage it did not actually possess — a dominant global wholesale franchise — while chronically under-investing in the one advantage it did possess: privileged, trusted access to the savings of an entire wealthy nation. The transformation now underway is, in the end, simply the belated recognition of where the moat was all along.

Whether Nomura can hold that hard-won discipline through the seductions of the next bull market and the shocks of the next inevitable crisis is the question its second century will answer. The long-term investor's job is more modest and more concrete: to watch the handful of numbers — recurring-fee assets, group ROE, wholesale discipline — that will reveal in real time whether the change is durable or merely cyclical, and to remember, always, that this is a firm whose single most expensive habit across a hundred years has been forgetting where its real strength lies. The test from here is not whether Nomura can dream bigger. It is whether it can stay disciplined enough to keep winning where it has always actually won.

References

-

Nomura posts full-year net profit drop on $2.9 bln Archegos hit — Reuters, 2021-04-27 ↩↩↩

-

Nomura Flags Potential $2 Billion Loss From US Client, Cancels Bond Sale — Bloomberg, 2021-03-29 ↩

-

Highlights of Nomura Holdings' 4Q and Full-year FY2025/26 Financial Results — Nomura Holdings, 2026-04-24 ↩↩↩↩

-

15 top executives resign in 2nd Nomura scandal — The Baltimore Sun, 1997-04-23 ↩↩↩↩

-

Nomura's fateful Lehman Brothers acquisition of 2008 — Financial Times, 2018-09-13 ↩↩

-

Nomura completes acquisition of Lehman Brothers' equities and investment banking businesses in Europe and the Middle East — Nomura, 2008-10-06 ↩

-

Nomura launches major restructuring of Wholesale Division — Financial Times, 2019-04-04 ↩

-

Nomura Appoints Christopher Willcox as Head of Wholesale Division — Nomura Holdings, 2022-09-21 ↩

-

Nomura Completes Acquisition of Greentech Capital Advisors, Rebranded as Nomura Greentech — Nomura Holdings, 2020-04-01 ↩

-

Nomura Announces Acquisition of Macquarie's U.S. and European Public Asset Management Business — Nomura Holdings, 2025-04-22 ↩

-

Japan's Nomura to buy Macquarie's U.S. and European public asset management business for $1.8 billion — CNBC, 2025-04-22 ↩↩

-

Nomura Holdings FY2024/25 full-year financial results — Nomura Holdings, 2025-04-28 ↩

-

Nomura posts record FY2025/26 profit and 10.1% ROE (SEC Form 6-K summary) — StockTitan, 2026-04-30 ↩↩↩↩↩↩

-

Nomura Holdings CEO's Compensation Raised to $10 Million as Company Achieves Record High Net Profit — Bitget News, 2026-06-22 ↩

-

Nomura: 2030 targets raised — ROE 10-12%+, income before taxes over ¥750bn — TradingView/Quartr, 2026-05-29 ↩

-

Changes to NISA Aim to Encourage More Investment — Nippon.com, 2023-01-05 ↩

-

Household Financial Assets Hit Record High of ¥2,351 Trillion — BigGo Finance (citing BOJ Flow of Funds), 2026-03-18 ↩

-

Negative Interest Rates No More: Bank of Japan Ends Decade of Covering for Kuroda Bazooka's Misfires — Nippon.com, 2024-03-28 ↩

-

Biggest Japan online brokers to debut zero-commission stock trades — Nikkei Asia, 2023-08-31 ↩

-

Highlights of Nomura Holdings' 2Q FY2025/26 Financial Results — Nomura Holdings, 2025-10-29 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube